Robust Auction Design with Support Information

Abstract

A seller wants to sell an item to buyers. Buyer valuations are drawn i.i.d. from a distribution unknown to the seller; the seller only knows that the support is included in . To be robust, the seller chooses a DSIC mechanism that optimizes the worst-case performance relative to the first-best benchmark. Our analysis unifies the regret and the ratio objectives.

For these objectives, we derive an optimal mechanism and the corresponding performance in quasi-closed form, as a function of the support information and the number of buyers . Our analysis reveals three regimes of support information and a new class of robust mechanisms. i.) With “low” support information, the optimal mechanism is a second-price auction (SPA) with random reserve, a focal class in earlier literature. ii.) With “high” support information, SPAs are strictly suboptimal, and an optimal mechanism belongs to a class of mechanisms we introduce, which we call pooling auctions (POOL); whenever the highest value is above a threshold, the mechanism still allocates to the highest bidder, but otherwise the mechanism allocates to a uniformly random buyer, i.e., pools low types. iii.) With “moderate” support information, a randomization between SPA and POOL is optimal.

We also characterize optimal mechanisms within nested central subclasses of mechanisms: standard mechanisms that only allocate to the highest bidder, SPA with random reserve, and SPA with no reserve. We show strict separations in terms of performance across classes, implying that deviating from standard mechanisms is necessary for robustness.

Keywords: robust mechanism design, minimax regret, maximin ratio, support information, prior-independent, standard mechanisms, second-price auctions, pooling.

1 Introduction

The question of how to optimally sell an item underlies much of modern marketplaces, from online advertising and e-commerce to art auctions. Selling mechanisms are widely used in practice, and in turn they are studied in economics, computer science, and operations research under optimal mechanism design, starting from the pioneering work of (Myerson, 1981). The literature often assumes that the seller knows the environment perfectly, but (i) this knowledge is often either not available or reliable, and (ii) the optimal mechanism prescribed by the theory is often too complicated or fine-tuned to the details of the environment, to be used in practice. There is therefore a need to develop mechanisms that depend less on market details, and this need is often referred to as the “Wilson doctrine” (Wilson, 1987).

The emerging literature on robust mechanism design, in turn, aims to design mechanisms that perform “well” in the worst case against “any” environment. This line of work often leads to interesting insights but, taken literally, they can lead to mechanisms that are too conservative. In practice, while we do not have complete knowledge about the environment, we often do have partial knowledge, and how to incorporate additional side information into the robust framework is essential to bring the robust theory closer to practice. In this paper, we make progress in this direction by analyzing the role of support information of bidder valuations, as captured by lower bounds and upper bounds on bidder valuations.

The motivation of the knowledge of such bounds is that we operate in a world with minimal or no data. The bounds need not be learned from data but rather are derived from asking experts, using domain knowledge, or common sense. Examples include launching a new product, or auctioning rarely traded goods such as fine art, collectibles, and jewelry. In these contexts, the support information is a natural form of partial knowledge because it is easier and more intuitive to come up with a reasonable range of values than to guess something like the shape of the valuation distribution (either parametric or nonparametric like regularity or monotone hazard rate) or distributional parameters like the mean or the optimal monopoly price.

More formally, consider a seller who wants to sell an item to bidders. The bidders’ valuations are unknown to the seller and are assumed to be drawn from a joint distribution . The seller does not know , and knows only a lower bound and an upper bound on the support of , and that the valuations belong to the class of i.i.d. distributions. Similarly, the bidders also do not know . Therefore, we focus on mechanisms that are dominant strategy incentive compatible (DSIC). Under such a mechanism, every bidder optimally reports her true value regardless of other bidders’ valuations and strategies.

We will quantify the performance of mechanisms by the gap between the benchmark oracle revenue and the mechanism revenue. The benchmark revenue is the ideal expected revenue the seller could have collected with knowledge of the buyers’ valuations, while the mechanism revenue is the expected revenue garnered by the actual mechanism. Our framework will be general and apply to two classical notions of gaps considered in the literature: (i) the regret (absolute gap) is the difference between these two revenues, and (ii) the approximation ratio (relative gap) is the ratio of these two revenues. The seller selects a mechanism that performs well (minimizes regret or maximizes approximation ratio) in the worst case against all admissible distributions.

The interval associated with the admissible distribution class captures the amount of uncertainty of the decision maker. We will parameterize this uncertainty through , which we call the relative support information, and which is a unitless quantity ranging from 0 to 1. When (either because or ), we have minimal relative support information while when we have maximal support information as the endpoints are close.

For the special case of pricing, i.e., when there is one bidder, the problem is well understood. It was analyzed concurrently in Bergemann and Schlag (2008) for the regret objective and in Eren and Maglaras (2010) for the approximation ratio objective. The one-bidder case is simpler because it is sufficient for the seller to optimize over randomized pricing. In the multiple-bidders case, however, the space of feasible mechanisms is much richer and more unstructured, making the seller’s problem challenging: only the case , which corresponds to minimal relative support information, has been studied. Anunrojwong et al. (2022) shows that a second-price auction with appropriately randomized reserve price is an optimal minimax regret mechanism. It is also possible to show that with minimal relative support information, no mechanism can guarantee positive worst-case approximation ratio. The understanding of the interplay of support information and robust auctions is very limited outside of these special cases, leading to the following question: how does support information affect the structure of optimal robust auctions and achievable performance?

This is the departure point of our work. We study optimal performance and associated mechanisms across the relative support information spectrum and establish richness in the structure of the resulting robust mechanisms with three distinct information regimes corresponding to three mechanism types. In particular, our work subsumes and unifies the three studies mentioned above, characterizing an optimal mechanism and the associated performance for an arbitrary number of bidders and any support information , for both the regret and ratio objectives. See Table 1 for a high level summary of known results and the results we develop in this paper.

| Problem | Information | Objective | |

| Type | level | Regret | Ratio |

| pricing () | all | Bergemann and Schlag (2008) | Eren and Maglaras (2010) |

| auctions () | Anunrojwong et al. (2022) | 0 | |

| auctions () | all | —This work— | |

1.1 Summary of Main Contributions

We develop a unified framework for regret and approximation ratio through a single quantity, the minimax -regret, where -regret is the difference between times the benchmark revenue and the mechanism revenue, and is a constant. The reduction itself is through an epigraph formulation and is fairly standard. Our main contribution, however, is the full characterization of a minimax optimal mechanism and its associated performance for -regret for any value of , any number of buyers and any support information . Since we are primarily interested in the effect of the support , we initially assume that the valuations are i.i.d. distributions given the canonical nature of this setting. Our family of optimality results across this spectrum brings to the foreground a very rich structure of optimal mechanisms, and establishes how relative support information critically impacts the structure of optimal mechanisms.

Novel mechanism class.

A natural candidate for an optimal mechanism is a second-price auction with appropriate random reserve. This was shown to be optimal with zero relative support information, i.e., for . Suppose for a moment that relative support information is high (i.e., ) and we are restricted to the class of SPAs. Setting any nontrivial reserve is risky because when the highest buyer’s value is below the reserve the seller does not allocate and gets zero revenue. At the same time, the benefits of a reserve price are limited since the highest and lowest values are close. On the other hand, the seller can guarantee a revenue of with no reserve, which is close to the maximal revenue achievable of . Hence, it should be intuitive that when relative support information is high, a SPA with no reserve is optimal among the class of SPAs. (A formal result is presented in Section 4.2.) A natural question is then whether there are mechanisms that can outperform a SPA with no reserve from a robust perspective, and what their structures are.

We define a new mechanism class, with the aim of softening the trade-offs associated with reserve pricing in second-price auctions. These mechanisms, that we dub “pooling auctions,” have an associated threshold. When the highest bid is above the threshold, the mechanism allocates to the highest bidder, as in a SPA when the highest bid is above the reserve price. However, when the highest bid is below the threshold, rather than not allocating as a SPA would do, the seller allocates uniformly at random to any of the bidders. In particular, the lowest bidder may get the item. In other words, this auction pools the low types. Slightly more formally, we can define the following parameterized mechanism classes:

-

•

, second-price auction with reserve , always allocates to the highest-value agent if the highest value is above , otherwise the mechanism does not allocate.

-

•

, the “pooling auction” with threshold , always allocates to the highest-value agent if the highest value is above , otherwise the mechanism allocates to each one of the agents uniformly at random with probability .

In a pooling auction, we can still use the threshold to differentiate between bidders with different values and potentially extract more revenue, without risking the zero payoff that comes from not allocating the item. Of course, this has implications for payments. We illustrate this interplay in Figure 1, where we depict, for the case of two agents, the allocation rule and revenue at each valuation vector for three mechanisms: SPA (no reserve), , and . The payment rule, and thus pointwise revenue, is determined via Myerson’s envelope formula to guarantee incentive compatibility.

We can see intuitively that pooling low types indeed softens the tradeoff associated with reserve pricing. By increasing the allocation for the low types, we increase the payment accrued from lower-value bidders but, at the same time, we decrease the payment accrued from higher-value bidders to guarantee incentive compatibility (so higher-value bidders do not pretend to be lower-value ones). When the relative support information is high (i.e., ), the lower-value and higher-value bidders are not too different, and this softer tradeoff has the potential to lead to more robust mechanisms.

Characterization of an optimal mechanism.

Our main theorem fully characterizes a minimax optimal mechanism for any relative support information level, for the -regret (and hence for the minimax regret and maximin ratio). We present an abridged version of our main result here. The full version is available in Theorem 2.

Theorem 1 (Main Theorem, Succinct).

Fix and . Then, there exists constants , depending only on and , such that the problem admits an optimal minimax -regret mechanism , depending on , as follows.

-

•

(Low Relative Support Information) For , there is a probability distribution of reserves such that with .

-

•

(High Relative Support Information) For , there is a probability distribution of thresholds such that with .

-

•

(Moderate Relative Support Information) For , then there is , such that is a randomization over SPAs and POOLs in the following sense. There is a probability distribution on such that when we draw a sample , if , the mechanism is , otherwise the mechanism is .

Our main theorem shows there always exists an optimal mechanism that is a convex combination of different mechanisms in the families and . Therefore, an optimal mechanism can be implemented in terms of a random instance of one of these “base” mechanisms. Furthermore, three fundamental relative support information regimes emerge. In the high (resp. low) support information regime, POOL (resp. SPA) is optimal. The moderate information regime is an interpolation between the two extreme regimes.

The resulting optimal mechanism inherits qualitative features from the base mechanisms SPA and POOL, and so their properties depend critically on the relative support information. We note that SPA is a standard mechanism, meaning that it never allocates to non-highest bidders, but POOL is not. Therefore, the optimal mechanism we have identified is standard if and only if . Secondly, POOL always allocates, meaning it allocates with probability one, whereas SPA does not (because it does not allocate below the reserve). Therefore, the optimal mechanism always allocates if and only if .

While the result above applies for any , we note that for the maximin ratio problem, the value of is endogenous, and it is not clear a priori in which information regime one falls. Quite interestingly, we can prove that the optimal maximin ratio mechanism is never in the SPA regime and thus some amount of pooling is always necessary in this case (see Section 3.1 and Proposition B-1).

Methodology and closed-form characterization.

We characterize the optimal mechanism and worst-case distribution in closed form via a saddle-point argument. In particular, if we assume that a saddle point exists and the optimal mechanism has the form outlined in the previous paragraph, we derive necessary conditions for Nature’s worst-case distribution (cf. Section 3.3) as well as the distributions of random reserve and threshold (Proposition C-5), under a few fairly mild technical conditions. We then prove that the resulting mechanism is optimal without any additional assumptions. Our methodology provides a unified treatment across all support information levels, and objectives (regret and approximation ratio) in one framework. We also characterize Nature’s worst-case distribution as part of our analysis, which takes the following form: for , the worst-case distribution is an isorevenue distribution (i.e., zero virtual value), whereas for , the worst-case distribution has a constant positive virtual value in the interior of the support.111For a distribution with CDF and density , the virtual value at is defined by .

Quantifying the value of scale information and competition.

Using the machinery we develop, we can exactly compute the minimax regret and maximin ratio for any support information and number of buyers . Approximation ratio values are shown in Table 2.

| 0.01 | 0.05 | 0.10 | 0.20 | 0.25 | 0.30 | 0.50 | 0.75 | 0.99 | ||

| 0.0979 | 0.1784 | 0.2503 | 0.3028 | 0.3832 | 0.4191 | 0.4537 | 0.5906 | 0.7766 | 0.9900 | |

| 0.1086 | 0.2158 | 0.3228 | 0.4038 | 0.5197 | 0.5660 | 0.6077 | 0.7463 | 0.8841 | 0.9957 | |

| 0.1148 | 0.2406 | 0.3673 | 0.4529 | 0.5668 | 0.6110 | 0.6504 | 0.7779 | 0.9001 | 0.9963 | |

| 0.1194 | 0.2582 | 0.3884 | 0.4743 | 0.5869 | 0.6302 | 0.6684 | 0.7909 | 0.9066 | 0.9966 | |

| 0.1310 | 0.2836 | 0.4175 | 0.5035 | 0.6139 | 0.6556 | 0.6922 | 0.8080 | 0.9150 | 0.9969 |

This table provides quantitative evidence that even a small amount of knowledge can lead to nontrivial guarantees on revenue. For example, Table 2 shows that, even when we only know that values can vary over a full order of magnitude (), we can guarantee of the first best with only buyers. When the knowledge of the scale is more precise, say, if we know the value up to a factor of two (), we get 74.63% with 2 buyers. With more agents, the guarantees improve (around 5% and 3% more, respectively, for an additional buyer).

Quantifying the power of mechanism features.

We have identified an optimal mechanism that is a convex combination of base mechanisms in the SPA and POOL classes. The distinguishing feature of this mechanism is that it is non-standard, i.e., it allocates to non-highest bidders. We show that this feature is necessary for optimality by characterizing the minimax optimal mechanism and performance within the class of all standard mechanisms and showing that the optimal mechanism strictly improves over optimal standard mechanisms. More broadly, we quantify the value of different features in the mechanism class by computing the worst-case -regret (and thus, regret and ratio) for different nested mechanism subclasses of all DSIC mechanisms: all DSIC mechanisms (), all standard mechanisms (), SPA with random reserve (), SPA with deterministic reserve (), and SPA with no reserve (). These results are also of independent interest, as they characterize the worst-case performance of commonly used mechanisms. We present in Table 3 the maximin ratio across mechanism classes and levels of relative support information, and observe that introducing some features (such as non-standardness) can lead to significant performance improvements.

| 0.10 | 0.20 | 0.25 | 0.30 | 0.50 | 0.75 | 0.99 | |

| all mechanisms | 0.4743 | 0.5869 | 0.6302 | 0.6684 | 0.7909 | 0.9066 | 0.9966 |

| standard mechanisms | 0.4137 | 0.5236 | 0.5684 | 0.6092 | 0.7471 | 0.8853 | 0.9958 |

| SPA with random reserve | 0.3918 | 0.5045 | 0.5517 | 0.5951 | 0.7424 | 0.8849 | 0.9958 |

| SPA with no reserve | 0.3586 | 0.4933 | 0.5457 | 0.5923 | 0.7424 | 0.8849 | 0.9958 |

1.2 Related Work

Auction Design and Mechanism Design

Vickrey (1961), Myerson (1981) and Riley and Samuelson (1981) pioneered a long line of work on the design of auctions and other economic mechanisms with strategic agents. In particular, Myerson (1981) shows that if agent valuation distributions are known, i.i.d. and regular, then the optimal (expected-revenue-maximizing) mechanism is a second-price auction with reserve. This is the classical paradigm of Bayesian mechanism design. However, in practice, we most often do not know the environment precisely, motivating the design of auctions that are robust to various environments.

Robust Mechanism Design

We refer the reader to a recent survey Carroll (2019) for robustness in mechanism design and contracting. In particular, by requiring that the mechanism performs well in a wide range of environments, we often gain structural insights: the resulting robustly optimal mechanism is often (but not always) “simple” and “detail-free” because, in some sense, it extracts the salient features of the mechanism that are common across a range of environments.

We will highlight the work on robustness to distributions throughout the rest of this subsection because they are most related to our work, but we want to note that there are other forms of robustness as well, e.g., robustness to higher-order beliefs (Bergemann and Morris, 2005, 2013), robustness to collusion and renegotiation (Che and Kim, 2006, 2009; Carroll and Segal, 2019), and robustness to strategic behavior that is weaker than dominant strategy (Chung and Ely, 2007; Babaioff et al., 2009).

Structures of Robust Mechanisms

The closest line of work to ours is how to robustly sell an item with non-Bayesian uncertainty on valuation distributions. The one-agent case reduces to a pricing problem; Bergemann and Schlag (2008) and Eren and Maglaras (2010) provide exact characterization for minimax regret and maximin ratio pricing, respectively. Koçyiğit et al. (2020b, 2022) analyze minimax regret against any number of agents whose valuation distributions are arbitrarily correlated with a known upper bound on the support. They show that their problem reduces to the one-agent case because Nature can choose the worst-case distribution to only have one effective bidder. Anunrojwong et al. (2022) shows that the second-price auction is robustly optimal for any number of agents when only the upper bound of the valuations are known, for a wide range of distribution classes with positive dependence (including i.i.d.). Anunrojwong et al. (2022) only assumes that the upper bound is known, whereas our work assumes that both the lower bound and the upper bound are known. This allows us to capture the entire spectrum of support information. We note that departure from the case requires to explore the space of DSIC mechanisms beyond second price auctions. As soon as one departs from SPAs, the space of mechanisms is much larger and it is not clear what should be a good candidate class a priori. We identify new focal mechanisms and show that qualitatively different forms of optimal mechanisms emerge: SPA, POOL, and a convex combination of the two, depending on the amount of information . We also unify both the regret and the ratio objectives in a single framework.

Optimal Mechanisms with Partial Information

Our work is also related to the design of robustly optimal pricing and mechanisms with partial information about the distribution. Some works assume access to samples drawn from the i.i.d. distribution (Cole and Roughgarden, 2014; Dhangwatnotai et al., 2015; Allouah et al., 2022; Feng et al., 2021; Fu et al., 2021) while others assume that summary statistics of distributions are known (Azar et al., 2013; Suzdaltsev, 2020a, b; Bachrach and Talgam-Cohen, 2022).

SPA as a focal robust mechanism in previous works

Previous works that study robust mechanism design tend to identify second-price auctions (SPA) as optimal. Anunrojwong et al. (2022) show that SPA minimizes worst-case regret for an auction with bidders and minimal support information for a wide range of distribution classes. Bachrach and Talgam-Cohen (2022) show that SPA maximizes worst-case revenue for an auction with two i.i.d. bidders when only the mean and the upper bound of the support are known. Koçyiğit et al. (2020a) and Zhang (2022a) show that separate SPAs minimize worst-case regret for an auction with multiple goods and multiple bidders when only the upper bounds are known. Zhang (2022b) shows that if the seller knows only the marginal distribution of each bidder but not the joint distribution, then SPA maximizes worst-case revenue over all DSIC mechanisms in the case of two bidders and over all standard DSIC mechanisms in the case of bidders. Che (2022) assumes only the upper bound and the mean are known but considers a different notion of robustness and shows that SPA is optimal among a class of mechanisms he calls competitive. Allouah and Besbes (2018) shows that SPA (without reserve) achieves exactly the optimal worst-case fraction of the second best benchmark revenue when there are two bidders and the distribution has monotone hazard rate.

The upshot of this discussion is that SPA has been the focal candidate for a robust mechanism. One of the main contributions of this paper is to show why SPA fails to be optimal when we have sufficient relative support information and propose a new building block for robust mechanism design, the pooling auction mechanism (POOL). Other than the fact that the optimal mechanism in our setting is composed of these new mechanisms, this new class of mechanisms may also be of independent interest and can be useful in other robust mechanism design problems as well.

Pooling in Auctions

While the specific form of the pooling auction POOL that we propose is new, the more general notion of pooling in auctions has appeared in the literature, starting from the pioneering work on revenue-maximizing auctions of Myerson (1981). When is not regular, it is shown the distribution must be “ironed” such that the all bidders in the same ironing interval have the same allocation, that is, their types are pooled. The main difference is that in Myerson (1981), there is a known focal distribution to iron, whereas there is no single distribution in our problem, and the pooling emerges naturally from the worst-case analysis over all feasible distributions. The distribution of pooling thresholds depends only on and not on any specific distribution.222This is why we name our auctions POOL rather than IRON to distinguish it from standard Myerson ironing. In fact, we can see from the main theorem (Theorem 2 and 5) that the worst case distributions are all regular.333Zero virtual value distributions in the low and moderate information regimes, and constant positive virtual value distributions in the high information regime. Therefore, even if we only consider the worst case over all regular distributions, the robustly optimal mechanism will still pool, whereas if we know the true distribution to be any specific regular distribution, the Bayesian optimal mechanism will not pool by Myerson. The robust auction framework therefore gives qualitatively different prescriptions.

Beyond Myerson (1981), there are also some recent works featuring the pooling element. For example, motivated by conflation in digital advertising, Bergemann et al. (2022) shows that the optimal information disclosure in auctions is to reveal low types and pool high types. The setting is different from ours in that in their setting, the distribution is known and bidders are Bayesian and the goal is to optimize the information structure. Their mechanism pools high values, whereas our pooling auctions pools low values. Feldman et al. (2022) proposes lookahead auctions with pooling and prove revenue guarantees in the Bayesian setting. Pooling also arises in the design of optimal mechanisms for financially constrained buyers even in the presence of standard regularity conditions on valuations (Laffont and Robert, 1996; Pai and Vohra, 2014).

Mechanism Design and Approximation

There is a long line of literature that proves approximation ratio guarantees for mechanisms (Hartline and Roughgarden, 2009; Hartline and Roughgarden, 2014; Feng et al., 2021; Allouah and Besbes, 2018; Hartline et al., 2020; Hartline and Johnsen, 2021). See Roughgarden and Talgam-Cohen (2019); Hartline (2020) for surveys.

2 Problem Formulation

The seller wants to sell an indivisible object to one of buyers. The buyers have valuations drawn from a joint cumulative distribution . The seller does not know , and only knows a lower bound and an upper bound of the valuation of each buyer. That is, the seller only knows that the support of the buyers’ valuations belongs to . As discussed in the introduction, the seller chooses a mechanism to minimize the worst-case “gap” (either absolute or relative) between the mechanism revenue and benchmark revenue; we will formalize this later in this section.

Seller’s Problem.

We model our problem as a game between the seller and Nature, in which the seller first selects a selling mechanism from a given class and then Nature may counter such a mechanism with any distribution from a given class . Buyers’ valuations are then drawn from the distribution chosen by Nature and they participate in the seller’s mechanism.

We will now consider the choice of the mechanism class . A selling mechanism is characterized by an allocation rule and a payment rule , where and . Given buyers’ valuations , gives the probability that the item is allocated to buyer , and his expected payment to the seller. In our main result, we will consider the class of all dominant strategy incentive compatible (DSIC) direct mechanisms. A mechanism is DSIC if and only if it is optimal for every buyer to report her true valuation (IR) and participate in the mechanism (IC), regardless of the realization of valuations of the other buyers, and the seller can allocate at most one item (AC). More formally, we require that the mechanism satisfies the following constraints:

| (IR) | ||||

| (IC) | ||||

| (AC) |

Note that we allow the seller’s mechanism to be randomized. We can now define the class of all DSIC mechanisms

| (1) |

Seller’s Objective.

Informally, the seller seeks to minimize the “gap” between the expected revenue relative to the benchmark associated with the revenues that could be collected when the valuations of the buyers are known .444The benchmark we use, maximum revenue with known valuations, is called the first-best benchmark. Another plausible benchmark we can use is the second-best benchmark, maximum revenue with known distributions. Both benchmarks are extensively used in the economics, operations, and computer science literatures; examples of papers using the first-best benchmark include (Bergemann and Schlag, 2008; Caldentey et al., 2017; Guo and Shmaya, 2019; Kleinberg and Yuan, 2013). The first-best benchmark is also reminiscent of the offline optimum benchmark, which is extensively used in the analysis of algorithms (Borodin and El-Yaniv, 2005). We consider two notions of gaps. First is the absolute gap, or regret, defined by

| (2) |

Second is the relative gap or approximation ratio, defined by

| (3) |

After the seller chooses a mechanism , Nature then chooses a distribution from a given class of distributions such that the valuation of the agents are drawn from . The seller aims to select the mechanism to either minimize the worst-case regret or maximize the worst-case approximation ratio. Our goal, therefore, is to characterize the minimax regret and maximin ratio for different classes of mechanisms and classes of distributions :

| (4) | ||||

| (5) |

For , define the -regret

To unify the minimax regret and maximin ratio objectives, we will focus on the minimax -regret defined by

| (6) |

The following proposition, whose proof is given in Appendix A, formalizes that the values of problems (4) and (5) can be obtained from a characterization of the problem in (6).

Proposition 1.

and is the largest constant such that .

Admissible distributions.

Lastly, we consider the choice of the class of admissible distributions . This class can be seen as capturing the “power” of Nature: the larger the class, the more powerful/adversarial Nature becomes. To simplify exposition, we will assume for most of the paper that is a class of independently and identically distributed (i.i.d.) distributions , defined formally as follows.

Definition 1.

The class consists of all distributions such that there exists a distribution with support on , referred to as the marginal, such that for every .

Saddle point approach.

For each and considered in this work, we establish the optimality of a mechanism and characterize the associated performance via a saddle point approach.

Definition 2.

is a saddle point of defined in (6) if and only if

Note that if is a saddle point then . Therefore, is the minimax -regret (the optimal performance), is an optimal mechanism, and is a corresponding worst-case distribution. Therefore, it is sufficient to exhibit a saddle point and verify the inequalities in Definition 2 to obtain an optimal mechanism and its associated performance.

3 Optimal mechanisms over the class of all DSIC mechanisms

In this section, we characterize the optimal mechanism over the class of all DSIC mechanisms for the minimax -regret problem against i.i.d. distributions for any , support information , and number of bidders . Our main theorem presents an optimal mechanism for each uncertainty regime. We will then use the main theorem to gain insights into the structure and performance of the optimal mechanism.

As discussed in the introduction, we consider the mechanism classes SPA and POOL, which are defined formally as follows.

Definition 3 (second-price and pooling auctions).

A second-price auction with reserve , denoted , is defined by the allocation rule given by, for each ,

A pooling auction with threshold , denoted , is defined by the allocation rule given by, for each ,

The payment rules of both and are determined up to a constant from Myerson’s envelope formula and for every , such that the resulting mechanism is dominant strategy incentive compatible.

Theorem 1 in the introduction is stated in a succinct way to highlight the structural features of our optimal mechanism. It is a corollary of the following Theorem 2 which fully characterizes the saddle point (the optimal mechanism and the worst-case distribution) and the corresponding optimal performance of the minimax -regret problem all in closed form.

Theorem 2 (Main Theorem, Full Saddle Characterization).

Fix and . Define as a unique solution to

and if , define and if , define to be the unique solution to

-

•

Suppose , and let . Define to be with

and

Then the pair is a saddle point and the minimax -regret is given by

-

•

Suppose , and let . Define as with

and

Then the pair is a saddle point and the minimax -regret is given by

where .

-

•

Suppose . Let be the unique solution to

Define the mechanism to be based on a unified threshold distribution such that if we draw a sample , if the mechanism is , otherwise the mechanism is , where the CDF of is given by

Furthermore, define

Then the pair is a saddle point and the minimax -regret is given by

We will present some of the ideas associated with the proof of Theorem 2 in Section 3.3, and we give the full proof in Appendix C. We now use our closed form characterization to gain insights into the structure and performance of the optimal mechanism.

3.1 Structure of Optimal DSIC Mechanisms

3.1.1 Minimax Regret Objective

The case of minimax regret is obtained by setting in Theorem 2. In Figure 2, we depict optimal mechanisms for different choices of and .

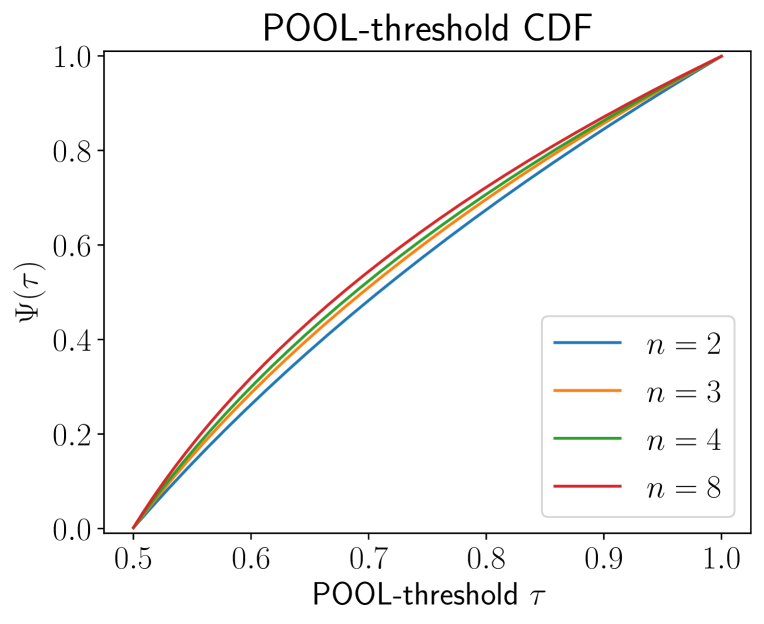

In Figure 2a, we depict the CDF of the optimal SPA-reserve distribution as a function of ; in Figure 2b, we plot the optimal POOL-threshold distribution as a function of .

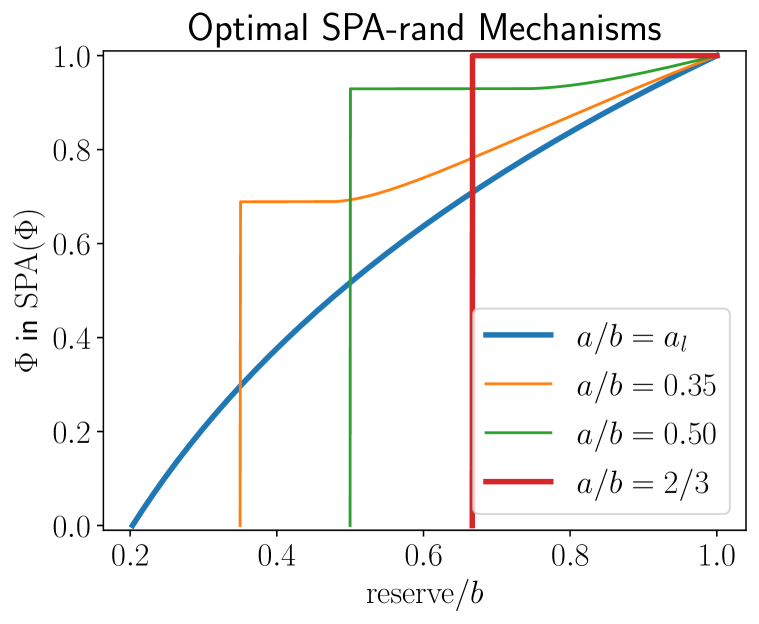

Theorem 2 states that in the moderate support information regime (), the optimal mechanism is a randomization over SPAs with random reserves (thresholds) in and POOLs with random thresholds in . We collectively call both types of thresholds “unified thresholds” such that the mechanism is characterized by the CDF of the random unified threshold . Figure 3(a) shows the example of such a mechanism (the CDF ) for , which is between and . The unified threshold distribution can be decomposed into a measure over SPA-reserves on with weight and a measure over POOL-thresholds on with weight for some as in Theorem 2. The SPA and POOL parts are shown with solid and dashed lines, respectively. The two parts meet at boundary with CDF value , the total measure of .

Lastly, we observe that as varies from to , the optimal mechanism transitions smoothly from low (SPA) to high (POOL) support information regimes. Figure 3 shows the continuous interpolation as . As gets closer to , the SPA part shrinks and the POOL part expands, and vice versa.

3.1.2 Maximin Ratio Objective

Unlike the minimax regret case where is set exogenously, here is obtained from bisection search to find the value of such that the minimax -regret is zero (cf. Proposition 1) and is a function of , i.e., the maximin ratio given that we computed earlier. As a result, the regime is determined endogeously. For each , we then compare with and to determine the regime. We can prove that the pure SPA regime is never possible for the maximin ratio objective; we formalize and prove this in Proposition B-1. For reasonable values of ,555For for , for , and for we are in the pure POOL regime. the optimal mechanisms are in the regime of pure pooling auctions. For a POOL-threshold , we define the normalized threshold as . As , we have , so this normalization allows us to compare the shape of threshold distributions on the same scale. For and , we plot the normalized POOL-threshold CDFs in Figure 4. We see that for low , the distribution puts more weight on lower thresholds, and vice versa.

3.2 Remark on the case

An important corollary of Theorem 2 is the pricing case (one-bidder / no-competition). Applying the result with directly recovers the minimax regret result of Bergemann and Schlag (2008) and the maximin ratio result of Eren and Maglaras (2010) as special cases.666More precisely, Eren and Maglaras (2010) derives the maximin ratio against the second-best benchmark in the discrete price setting, whereas our result is against the first-best benchmark in the continuous setting. However, their numerical value for the ratio approaches ours as the grid resolution becomes finer. We can also show that for the case, the maximin ratio for two benchmarks are the same. Eren and Maglaras (2010) also does not explicitly derive the optimal mechanism, whereas we do. We give the proof of this corollary in Appendix D.6.

Corollary 1 (Pricing).

Suppose . For , the minimax -regret is , achieved with the price distribution CDF for and 0 otherwise. For , the minimax -regret is achieved with the price distribution CDF for .

In particular, the minimax regret is if and if . For , the maximin ratio is , achieved by the price distribution for .

We remark that in the one-bidder case, and , so there are only two regimes (low and moderate support information), and this is reflected in the corollary statement. Moreover, with only one bidder, POOL becomes a degenerate mechanism that always allocates. This is why in the regime (moderate information), the optimal mechanism, which is a mixture of SPA and POOL, always allocates with positive probability. This can be seen in the pricing CDF , which has a point mass of positive size at .

3.3 Outline of the Proof of the Main Theorem

The key idea of proof of our main theorem (Theorem 2) is to explicitly exhibit a saddle point of the zero-sum game between seller and Nature, as discussed at the end of Section 2, that is, to find and such that for all and . We proceed in two steps. First, we assume that the mechanism is a randomization over SPA and POOL. Then, under certain regularity assumptions, through necessary conditions, we can pin down the weights of each component and of the mechanism, and thus the mechanism itself. We can also pin down the worst-case distribution . Second, we formally verify, with no additional assumptions, that the pair we derived is indeed a saddle point.

We now outline the first step in more detail. In the full proof, it will be more convenient mathematically to consider the class of mechanisms, parameterized by two functions , where if the valuation vector is with highest , then the highest bidder is allocated with probability and the other bidders are allocated with probability each. Every convex combination over SPA and POOL mechanisms with random thresholds can be expressed in terms of (see Propositions C-2). Therefore, the formalism will allow us to treat all three regimes in a unified manner. However, for concreteness, in the main text below we will focus on the high support information regime and work directly with the threshold distribution for illustration; the proof of the moderate support information is more challenging but follows a similar outline.

Assume that is i.i.d. with marginal . We can compute the -regret of and show that it has two representations using an ad-hoc integration by part result that handles distributions that are not necessarily smooth (cf. Proposition C-3). Suppose that is arbitrary, while has a density in the interior with point masses and at and , then

| (Regret-) |

Note that (Regret-) depends on only through and is linear in . This representation is useful for the seller’s saddle , because we do not make any assumption on the seller’s choice . By the first-order conditions, under the worst-case distribution , the coefficient of each is zero wherever is interior. Otherwise, the seller could decrease his regret by changing the distribution of reserves. Therefore,

This pins down Nature’s candidate distribution as , a distribution with constant virtual value .

Alternatively, let be arbitrary but assume that is differentiable, then can be written as

| (Regret-) |

Note that (Regret-) depends on only through and is “separable” (different terms do not interact). This representation is useful for Nature’s saddle , because we do not make any assumption on Nature’s choice and we can optimize the integrand pointwise as an expression in , i.e., we can equivalently solve for each . Taking derivatives with respect to , the first-order condition on gives

because, at the saddle, this first derivative must be zero. Substituting gives

| (ODE-) |

or

Because is zero at , integrating from to gives

Performing the integration, we can rewrite as

This expression makes it clear that , so is well-behaved and does not have a point mass at , and that is increasing in . For to be feasible as a CDF, the only additional condition we need is , which gives the following equation that determines :

By definition of , we see by inspection that this equation has an explicit solution

We need for Nature’s saddle to hold: this is why we need in the pure POOL regime.

Now that we have identified a candidate saddle-point, we need to formally verify its optimality. Seller’s saddle (optimize over with fixed ) is a standard Bayesian mechanism design problem and the optimality of follows because every mechanism that always allocates is optimal since has positive, constant virtual value. For Nature’s saddle (optimize over with fixed ), we need to check that maximizes the regret given the mechanism . It is sufficient to show that globally maximizes the integrand , as a function of , pointwise. The expression is polynomial in with two nonzero degree terms and . Two conditions are sufficient to guarantee global optimality: (i) the first-order optimality condition (FOC), (ii) nonnegativity of the coefficient of . To see why this is true, consider the expression as a function of . The first derivative of this expression is , and the sign of is the same as the sign of . From (i), FOC is equivalent to , so if we have from (ii), then we also have . We can immediately see that is unimodal with a peak at (increasing in for and decreasing in for ), justifying our claim.

We conclude by checking that the coefficient of is nonnegative:

Substituting the expression for from (ODE-) reduces the above inequality to

which is trivially true. We therefore have established a saddle point of the problem in the high relative support information case.

4 Minimax -Regret across Mechanism Classes

Our main theorem (Theorem 2) gives a complete characterization of the optimal robust performance when Nature’s distribution is i.i.d. () and the seller can choose any DSIC mechanism (). It turns out that the optimal mechanism is generally a randomization over SPA and POOL mechanisms. This optimal mechanism has interesting features, and we would like to quantify how much each feature contributes to the performance. That is, without that feature, how much (robust) performance, if any, we will lose. Equivalently, our results quantify the “cost of simplicity” or the performance loss if the seller is restricted to simpler classes of mechanisms. We formalize this problem by solving minimax -regret problems, , when the mechanism classes are successively smaller, omitting one feature at a time. The subclasses under consideration are shown in Figure 5.

First, our optimal mechanism is not standard because POOL might allocate to a bidder who is not the highest. To isolate the role of the pooling feature, we study the class of standard mechanisms that only allocate to the maximum bidder. Second, we study the need to deviate from SPAs in standard mechanisms, and hence study SPAs with randomized reserves. Lastly, we quantify the power of randomness and the power of using a reserve by computing minimax regret under the class of SPA with a deterministic reserve and the class of SPA with no reserve. Interestingly, we show that there are strict separations in terms of maximin ratio between , , , and (but not between and ). In other words, pooling and deviations from SPAs are critical for robust performance, and so is the randomization of reserve prices.

4.1 Minimax -Regret Over Standard Mechanisms

A mechanism is said to be standard if it never allocates to an agent that does not have the highest value. Formally, it satisfies the following constraint:

| (STD) |

We can now define the class of all standard mechanisms.

Definition 4.

The class of all standard mechanisms is given by

| (7) |

It is clear that any second-price auction (SPA) with random reserve is standard, and intuitively, SPAs seem like “natural” and “typical” elements of this class, but as it turns out, other standard mechanisms lead to higher performance than SPAs when relative support information is high. We now introduce the following mechanism class.

Definition 5 (Generous SPA).

A generous SPA with reserve distribution , denoted , is defined by the allocation rule given by, for each ,

and zero otherwise, breaking ties uniformly at random. The payment rule is determined uniquely from Myerson’s formula such that the resulting mechanism is dominant strategy incentive compatible.

We call this mechanism generous SPA because it behaves like SPA, except in the case when all other non-highest agents have the lowest possible value , then it always allocates (“generously”). We now state the main theorem of this section.

Theorem 3 (Optimal Standard Mechanism).

Fix and , and let . Define as in Theorem 2. Then, the problem admits an optimal minimax -regret standard mechanism , depending on as follows.

-

•

(Low Relative Support Information) For , is the same as in Theorem 2.

-

•

(High Relative Support Information) For , there is a probability distribution such that .

Note that by Theorem 2, if , then SPA with random reserve is optimal in , and it is also standard, so it is immediate that it is also optimal in the class . Similar to Theorem 1, Theorem 3 highlights the structural features of our optimal mechanism and is a corollary of Theorem 6 in the Appendix which fully characterizes the saddle point in closed form.

The proof of Theorem 3 follows a similar outline to that of Theorem 2, although the calculations are nontrivial. In particular, we need to derive the expressions of conditional distributions of order statistics for arbitrary , taking into account potential ties, which complicate the calculations.777The existing results on conditional distributions of order statistics assume that has a density, see e.g. David and Nagaraja (2003). These results do not apply because we do not make any assumptions on . In fact, the worst case has point masses. In contrast, the regret of any mechanism (whose class contains all other mechanisms in this paper) depends only on the marginal distributions of the first- and second-order statistics, which are simpler (cf. Proposition C-3). However, the hardest part is coming up with the right structural class GenSPA that contains the optimal mechanism (within the subclass of standard mechanisms) and is tractable, because our techniques based on solving differential equations can pin down the candidate mechanism only once we fix the mechanism up to a one-dimensional functional parameter. We discuss key technical challenges and give the full proof in Appendix E.1.

4.2 Minimax -Regret over SPA with random and deterministic reserve

We can characterize the minimax -regret mechanism and its corresponding worst-case distribution and performance in the following theorem.

Theorem 4 (Optimal SPA with Random Reserve).

Fix and . Define as in Theorem 2 and . Then, the problem admits a minimax -regret , depending on , as follows.

-

•

(Low Relative Support Information) For , is the same as in Theorem 2.

-

•

(High Relative Support Information) For , is a point mass only at , i.e., is a SPA with no reserve.

-

•

(Moderate Relative Support Information) For , there is such that has a point mass at and a density on .

The second bullet point of Theorem 4 formalizes the intuition highlighted in the introduction that in the high scale information regime ( is close enough to 1), the optimal SPA with random reserve sets no reserve at all. Similar to Theorem 1, Theorem 4 highlights the structural features of our optimal mechanism and is a corollary of Theorem 7 in Appendix E.2 which fully characterizes the saddle point in closed form. The proof of the moderate information regime of Theorem 4 is the most challenging. It is different from previous saddle problems because in this case, the increasing condition on the reserve price distribution is binding; if we optimize pointwise, the resulting distribution is not increasing, which is infeasible. We characterize an optimal distribution of reserves using a Lagrangian approach that involves introducing a Lagrange multiplier for the monotonicity constraint and then designing a primal-dual pair that satisfies complementary slackness and Lagrangian optimality. We discuss key technical challenges and give the full proof in Appendix E.2.

Lastly, we characterize the optimal SPA with deterministic reserve and SPA with no reserve . Proposition E-9 in the Appendix gives the the minimax -regret for with a fixed deterministic reserve . In particular, it subsumes the problem of choosing the regret-minimizing reserve as well as computing worst-case regret of SPA without reserve ().

4.3 Performance Separation Between Mechanism Classes

Table 3 in the introduction shows the maximin ratio as a function of of all mechanism classes we consider for . Figure 6 graphically depicts the same information for . This metric captures the performance of the optimal mechanism. We can see that while and have the same maximin ratios (so a fixed reserve does not improve over no reserve), there are strict separations between , , , and .

The gap between and shows that no SPA is optimal within the class of standard mechanisms, even though the gap is quantitatively small. In contrast, the gap between and is significant. This means that in robust settings, it is important to sometimes allocate to non-highest bidders. We can see from the plots with and that the non-standard gap becomes bigger and dominates all other gaps as gets large, so this becomes more important with more bidders.

Echoing discussions in the introduction, our work shows that there are interesting mechanism classes in DSIC mechanisms beyond SPA in the sense that they are robustly optimal in natural settings. Interestingly, SPA is not optimal even within the class of standard mechanisms; GenSPA is. It is an open question whether GenSPA will also be useful in other settings as well.

We can also use analytical results derived in this section to gain insights into the structure of optimal mechanisms within subclasses. We further discuss this in Appendix F.1.

5 Extensions and Conclusion

In this paper, we give an explicit characterization of a robustly optimal mechanism to sell an item to buyers knowing only a lower bound and an upper bound of the support of values, where the seller’s performance is evaluated in the worst case. Our general framework is broadly applicable to an arbitrary number of buyers and several mechanism classes and captures both regret and ratio objectives.

Furthermore, we note that it is possible to extend the framework to other classes of distributions. It is possible to show that the minimax -regret we have obtained for the case of i.i.d. distributions (and the corresponding optimal mechanism) does not change if Nature optimizes over broader classes of distributions capturing positive dependence: exchangeable and affiliated values, a common class considered with knowledge of the distributions (Milgrom and Weber, 1982); and mixtures of i.i.d. distributions, another common class. The results also do not change if Nature optimizes over the smaller class of i.i.d. regular distributions.

There are many avenues for future work. This present paper is a step in the more general agenda of robust mechanism design with partial information, and it would be interesting to investigate how other forms of side information (such as moments, samples, and shapes of distributions) impact the structure and performance of optimal or near-optimal mechanisms, and the value of such information. Another direction is to consider other benchmarks, especially the second-best benchmark rather than the first-best benchmark considered in this paper.

References

- Allouah and Besbes [2018] Amine Allouah and Omar Besbes. Prior-independent optimal auctions. In Proceedings of the 2018 ACM Conference on Economics and Computation, EC ’18, New York, NY, USA, 2018. Association for Computing Machinery.

- Allouah et al. [2022] Amine Allouah, Achraf Bahamou, and Omar Besbes. Pricing with samples. Operations Research, 70(2):1088–1104, 2022.

- Anunrojwong et al. [2022] Jerry Anunrojwong, Santiago R. Balseiro, and Omar Besbes. On the robustness of second-price auctions in prior-independent mechanism design. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 151–152. ACM, 2022.

- Azar et al. [2013] Pablo Azar, Constantinos Daskalakis, Silvio Micali, and S. Matthew Weinberg. Optimal and efficient parametric auctions. Proceedings of the 24th annual ACM-SIAM symposium on Discrete algorithms, 2013.

- Babaioff et al. [2009] Moshe Babaioff, Ron Lavi, and Elan Pavlov. Single-value combinatorial auctions and algorithmic implementation in undominated strategies. Journal of the ACM, 2009.

- Bachrach and Talgam-Cohen [2022] Nir Bachrach and Inbal Talgam-Cohen. Distributional robustness: From pricing to auctions. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 182–183. ACM, 2022.

- Bergemann and Morris [2005] Dirk Bergemann and Stephen Morris. Robust mechanism design. Econometrica, 2005.

- Bergemann and Morris [2013] Dirk Bergemann and Stephen Morris. An introduction to robust mechanism design. Foundations and Trends in Microeconomics, 2013.

- Bergemann and Schlag [2008] Dirk Bergemann and Karl H. Schlag. Pricing without priors. Journal of the European Economic Association, 2008.

- Bergemann et al. [2022] Dirk Bergemann, Tibor Heumann, Stephen Morris, Constantine Sorokin, and Eyal Winter. Optimal information disclosure in classic auctions. American Economic Review: Insights, 2022.

- Bertsimas et al. [2011] Dimitris Bertsimas, David B. Brown, and Constantine Caramanis. Theory and applications of robust optimization. SIAM Review, 2011.

- Borodin and El-Yaniv [2005] Allan Borodin and Ran El-Yaniv. Online Computation and Competitive Analysis. Cambridge University Press, 2005.

- Caldentey et al. [2017] René Caldentey, Ying Liu, and Ilan Lobel. Intertemporal pricing under minimax regret. Operations Research, 2017.

- Carroll [2019] Gabriel Carroll. Robustness in mechanism design and contracting. Annual Review of Economics, 2019.

- Carroll and Segal [2019] Gabriel Carroll and Ilya Segal. Robustly optimal auctions with unknown resale opportunities. The Review of Economic Studies, 2019.

- Che [2022] Ethan Che. Robustly optimal auction design under mean constraints. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 153–181. ACM, 2022.

- Che and Kim [2006] Yeon-Koo Che and Jinwoo Kim. Robustly collusion-proof implementation. Econometrica, 2006.

- Che and Kim [2009] Yeon-Koo Che and Jinwoo Kim. Optimal collusion-proof auctions. Journal of Economic Theory, 2009.

- Chung and Ely [2007] Kim-Sau Chung and J. C. Ely. Foundations of dominant-strategy mechanism. The Review of Economic Studies, 2007.

- Cole and Roughgarden [2014] Richard Cole and Tim Roughgarden. The sample complexity of revenue maximization. Proceedings of the 46th Annual ACM Symposium on Theory of Computing, 2014.

- David and Nagaraja [2003] Herbert A. David and Haikady N. Nagaraja. Order Statistics 3rd ed. Wiley-Interscience, 2003. ISBN 978-0471389262.

- Dhangwatnotai et al. [2015] Peerapong Dhangwatnotai, Tim Roughgarden, and Qiqi Yan. Revenue maximization with a single sample. Games and Economic Behavior, 2015.

- Eren and Maglaras [2010] Serkan S Eren and Costis Maglaras. Monopoly pricing with limited demand information. Journal of revenue and pricing management, 9(1-2):23–48, 2010.

- Feldman et al. [2022] Michal Feldman, Nick Gravin, Zhihao Gavin Tang, and Almog Wald. Lookahead auctions with pooling. Proceedings of the International Symposium on Algorithmic Game Theory (SAGT), 2022.

- Feng et al. [2021] Yiding Feng, Jason D Hartline, and Yingkai Li. Revelation gap for pricing from samples. Proceedings of the 53rd Annual ACM SIGACT Symposium on Theory of Computing, 2021.

- Fu et al. [2021] Hu Fu, Nima Haghpanah, Jason Hartline, and Robert Kleinberg. Full surplus extraction from samples. Journal of Economic Theory, 2021.

- Guo and Shmaya [2019] Yingni Guo and Eran Shmaya. Robust monopoly regulation. Technical report, 2019.

- Hartline [2020] Jason Hartline. Mechanism Design and Approximation. 2020.

- Hartline and Johnsen [2021] Jason Hartline and Aleck Johnsen. Lower bounds for prior independent algorithms. Technical report, 2021.

- Hartline and Roughgarden [2014] Jason Hartline and Tim Roughgarden. Optimal platform design. Technical report, 2014.

- Hartline et al. [2020] Jason Hartline, Aleck Johnsen, and Yingkai Li. Benchmark design and prior-independent optimization. Proceedings of the 2020 IEEE 61st Annual Symposium on Foundations of Computer Science (FOCS), 2020.

- Hartline and Roughgarden [2009] Jason D. Hartline and Tim Roughgarden. Simple versus optimal mechanisms. Proceedings of the 11th ACM Conference on Economics and Computation, 2009.

- Kleinberg and Yuan [2013] Robert Kleinberg and Yang Yuan. On the ratio of revenue to welfare in single-parameter mechanism design. In Proceedings of the 14th ACM Conference on Economics and Computation, pages 589–602. ACM, 2013.

- Koçyiğit et al. [2020a] Çagil Koçyiğit, Daniel Kuhn, and Napat Rujeerapaiboon. Regret minimization and separation in multi-bidder multi-item auctions. Technical report, 2020a.

- Koçyiğit et al. [2022] Çagil Koçyiğit, Napat Rujeerapaiboon, and Daniel Kuhn. Robust multidimensional pricing: separation without regret. Mathematical Programming, 196(1):841–874, 2022.

- Koçyiğit et al. [2020b] Çağıl Koçyiğit, Garud Iyengar, Daniel Kuhn, and Wolfram Wiesemann. Distributionally robust mechanism design. Management Science, 2020b.

- Laffont and Robert [1996] Jean-Jacques Laffont and Jacques Robert. Optimal auction with financially constrained buyers. Economics Letters, 52(2):181–186, 1996.

- Milgrom and Weber [1982] Paul R. Milgrom and Robert J. Weber. A theory of auctions and competitive bidding. Econometrica, 1982.

- Monteiro and Svaiter [2010] Paulo Klinger Monteiro and Benar Fux Svaiter. Optimal auction with a general distribution: Virtual valuation without densities. Journal of Mathematical Economics, 2010.

- Myerson [1981] Roger B. Myerson. Optimal auction design. Mathematics of Operations Research, 1981.

- Pai and Vohra [2014] Mallesh M Pai and Rakesh Vohra. Optimal auctions with financially constrained buyers. Journal of Economic Theory, 150:383–425, 2014.

- Rahimian and Mehrotra [2019] Hamed Rahimian and Sanjay Mehrotra. Distributionally robust optimization: A review. Technical report, 2019.

- Riley and Samuelson [1981] John G. Riley and William F. Samuelson. Optimal auctions. American Economic Review, 1981.

- Roughgarden and Talgam-Cohen [2019] Tim Roughgarden and Inbal Talgam-Cohen. Approximately optimal mechanism design. Annual Review of Economics, 11(1):355–381, 2019.

- Suzdaltsev [2020a] Alex Suzdaltsev. An optimal distributionally robust auction. Technical report, 2020a.

- Suzdaltsev [2020b] Alex Suzdaltsev. Distributionally robust pricing in independent private value auctions. Technical report, 2020b.

- Vickrey [1961] William Vickrey. Counterspeculation, auctions, and competitive sealed tenders. The Journal of Finance, 1961.

- Wilson [1987] Robert Wilson. Game-theoretic analyses of trading processes in advanced in economic theory. In Truman Fassett Bewley, editor, Advances in Economic Theory Fifth World Congress, chapter 2, pages 33–70. Cambridge University Press, 1987.

- Zhang [2022a] Wanchang Zhang. Auctioning multiple goods without priors. Technical report, 2022a.

- Zhang [2022b] Wanchang Zhang. Correlation-robust optimal auctions. Technical report, 2022b.

Electronic Companion:

Robust Auction Design with Support Information

Jerry Anunrojwong111Columbia University, Graduate School of Business. Email: janunrojwong25@gsb.columbia.edu,

Santiago R. Balseiro222Columbia University, Graduate School of Business. Email: srb2155@columbia.edu., and Omar Besbes333Columbia University, Graduate School of Business. Email: ob2105@columbia.edu..

Appendix

Appendix A Proofs for Section 2

Proof of Proposition 1.

The definition of says that it is a solution to

or

or

That is, the maximin ratio is the highest value of such that there exists that . Equivalently,

Appendix B Proofs for Section 3

Proposition B-1.

The optimal maximin ratio mechanism is never in the pure SPA regime.

Proof of Proposition B-1.

Suppose for the sake of contradiction that the SPA regime is possible. By Theorem 2, the -regret

is zero, while the corresponding satisfies

Substituting the expression of gives

| (B-1) |

Let be the left hand side of (B-1). We will derive a contradiction by showing that for all . We will prove this by viewing as a free variable. Let

Note that

Also, by integration by part,

Therefore, both integrals in can be written in terms of . We want to show that

This is equivalent to

Note that , so the above manipulation is valid, and both sides of the inequality are positive. Let

It is clear from the integral definition of that . We now compute, by L’Hopital’s rule,

Therefore, To prove that it is sufficient to prove that is strictly increasing in , i.e., . This is very convenient because does not involve an integral. We compute

Then is equivalent to

Let , algebraic simplification gives that the left hand side is

It is clear that . We also have

We conclude that the optimal maximin ratio mechanism is never in the SPA regime.∎

Appendix C Full Proof of Theorem 2

C.1 ) Mechanisms As A Unified Direct Mechanism Representation

Our main theorem shows that the optimal mechanism is a convex combination over the base mechanisms . To prove the necessary saddle inequalities, we need to be able to compute the expected regret of any such mechanism against some distribution. It is more mathematically convenient to “flatten” the randomness over thresholds and give an almost equivalent “direct” representation that gives the allocation rule and payment rule for any valuation vector as follows.

Definition 6 ( mechanisms).

Let be given functions. A mechanism is defined by the allocation rule given by, for each ,

and the payment rule is determined uniquely from Myerson’s formula such that the resulting mechanism is dominant strategy incentive compatible.

In other words, the mechanism allocates to the highest bidder(s) and to the non-highest bidder(s). If there are highest bidders, select one of them to be the “winner” with uniformly at random.

The mechanism representation has the advantage that all mechanisms in the three different support information regimes (SPA, POOL, and a convex combination between SPA and POOL) can all be represented in this form, so we can have a unified treatment for all of them.

More formally, we can prove the following proposition, that mechanisms and convex combination of are almost equivalent representations of the same mechanism class in the sense that one can be converted to another.

Proposition C-2.

We have the following correspondence between the mechanisms arising in our main theorem (Theorem 5) and convex combinations of SPAs and POOLs.

-

(1)

A mechanism is a mechanism with increasing in , , and for all if and only if it is , has measure 1, and .

-

(2)

A mechanism is a mechanism with increasing in , , and for all if and only if is , has measure 1, and .

-

(3)

A mechanism is a mechanism with increasing in for , , for for some constant , for if and only if it is a randomization over , with supported on and with supported on . Furthermore, their cumulative probabilities are given by for and for .

We choose to highlight in the main text because the base mechanisms SPA and POOL are intuitive and interpretable. However, the representation is more mathematically convenient because it directly gives the allocation probabilities and payments for each valuation vector which are ingredients for the expected regret calculation, and also because it allows the three cases to be treated in a unified manner.

Theorem 5 (Main Theorem in ).

Fix and . Define as a unique solution to

and if , define and if , define to be a unique solution to

Then we have for any and , where and (which is i.i.d. with marginal ) is defined depending on the value of as follows.

-

•

Suppose , and let . We define as a mechanism with , where

and

-

•

Suppose , and let . We define as a mechanism with

and

-

•

For , we define as a mechanism with

and

and

where is the unique solution to

The rest of this Appendix will be devoted to proving the above reformulated main theorem (Theorem 5). We need to verify Nature’s saddle (fixing the mechanism , the best distribution is ) and Seller’s saddle (fixing the distribution , the best mechanism is the mechanism). (The above Theorem 5 only states the optimal mechanism and worst-case distribution that together form a saddle pair. We will separately verify the expressions of the minimax -regret that we also state in Theorem 2 later in Proposition D-6.)

The Seller’s Saddle is a Bayesian mechanism design problem, and we can check optimality through the conditions of Monteiro and Svaiter [2010]. (In particular, we see that the mechanism and the distribution have the same support, and the distribution has constant nonnegative virtual value on the support.) Therefore, for the rest of this proof we will focus on Nature’s saddle.

C.2 Conditions for Nature’s Saddle

To prove the necessary saddle inequalities, we need an expression for the expected regret of a mechanism under a given distribution , given in the following proposition.

Proposition C-3 (Expected Regret of a mechanism).

Let be the expected regret of a mechanism and valuation distribution .

If we assume that and are continuous everywhere and differentiable everywhere except a finite number of points, and is arbitrary, then the expected regret is

| (Regret-) |

where and are the first and second order statistics (highest and second-highest) among agents whose valuations are drawn from .

If we further assume that is i.i.d. with marginal , then

| (Regret-) |

If, instead, we let and be arbitrary but we assume that is i.i.d. with marginal such that has a density on (so it potentially has point masses only at and of size and respectively), then we have the (Regret-) expression

| (Regret-) |

The above expression is valid for if we take the expression to be zero for .

We prove Proposition C-3 in Appendix D.2. The precise expression for the regret is not qualitatively as important as the crucial fact that the regret can be written as an integral over a polynomial function of only, as seen in (Regret-). Therefore, in Nature’s saddle, if we fix and optimize over , we can optimize over each pointwise, subject only to monotonicity constraints. If we can find a global minimum of the polynomial that also satisfies the monotonicity constraints, then we will automatically achieve pointwise optimality. As argued in the main text, the expression as a function of has a global maximum at if the following two conditions hold: (i) first-order condition , (ii) . We therefore have the following proposition.

Proposition C-4.

Suppose that is a mechanism and is an increasing function that satisfies the following conditions:

| (FOC) | |||

| (SOC) |

Then for any .

We label the condition corresponding to as (SOC) because it is equivalent to the second-order condition on the . To see this, we compute , where the last equality holds because of FOC . Therefore, SOC is equivalent to . Nevertheless, we want to emphasize that we do not say that first-order and second-order conditions together imply global optimality in general. This is not true; it is only true in this case due to the special structure of the integrand, which we analyze directly.

C.3 Verification of First and Second Order Conditions for Nature’s Saddle

The last step of the proof is to verify the (FOC) and (SOC) conditions for the pair given in Theorem 5. To do this, we first show that the satisfies a certain ordinary differential equation (ODE).

Proposition C-5.

Define in the regime, in the regime, and be defined as stated in Theorem 5 in the the regime. Also define as in Theorem 5 in the regime, and in other regimes. Let be given as in Theorem 5. Then satisfies , for and for , and is an increasing continuous function that satisfies the ODE

| (ODE--1) | |||||

| (ODE--2) |

Furthermore, in the regime, the system of equations defining actually has a unique solution, and if we view and as a function of , then we have and as , while and as .

Proposition C-5 gives a unifying description of the mechanism across three support information regimes and makes it clear that the intermediate regime interpolates between the SPA regime and the POOL regime.

Checking (FOC)

We first consider the case , where (ODE--1) applies. We only need to check this case in the low information () and moderate information () regimes, because this case becomes vacuous () in the high information () regime. In both of these regimes, . Therefore, the (FOC) equation is

where the last equality holds by (ODE--1).

Now we consider the case where (ODE--1) applies. We only need to check this case in the high information () and moderate information () regimes, because this case becomes vacuous () in the low information () regime. In both regimes, . ( for the moderate information regime, and for the high information regime.) therefore, the (FOC) is

where the second-to-last equality holds by (ODE--1).

Checking (SOC).

The following applies whether we are in the regime , , or .

In the case , we have and , so (SOC) reduces to , which is true by definition of in the interior.

In the case , we have and , so (SOC) reduces to .

Appendix D Technical Results Supporting the Proof of the Main Theorem (Theorem 2 and 5) From Appendix C

D.1 Technical lemmas

Throughout this section, we will use the following technical lemmas.

Lemma D-1.

Let be a constant, then for any positive integer and we have the identity

Proof of Lemma D-1.

We first check the equality of the first and the second expressions. Note that both expressions are zero when . It is then sufficient to check that the derivatives of the two expressions agree. The derivative of the second expression is

which is the derivative of the first expression.

Now we check the third expression. We have the Taylor Series

Substituting gives

We see that the first terms of cancel out, and we get the third expression. ∎

Lemma D-2.

D.2 Mechanisms As A Unified Direct Mechanism Representation (Appendix C.1)

Proof of Proposition C-2.

Note that the representation of is and , and the representation of is and . All three cases follow from computing the convex combination of these.

(1) is straightforward. For (2), the representation of is

We can then see that , and . Conversely, given this , we can let giving a valid .

For (3), the mechanism is

We therefore have a formula that transforms to . From these formula, we immediately see that ; we let this be . We also see that is increasing in , while is decreasing in , because and are increasing functions.

Conversely, assume that has these properties. We will show that we can invert these formulas and find the corresponding . From , setting gives , so , and . From , we get , and from , we get . ∎

D.3 Conditions for Nature’s Saddle (Appendix C.2)

Proof of Proposition C-3.

We first derive the (Regret-) expression, assuming that and are continuous everywhere and differentiable everywhere except a finite number of points.

From Myerson’s lemma,

the allocation rule gives

so the pointwise regret is

We will now prove the following technical lemma.

Lemma D-3.

If is a differentiable function, then

Proof of Lemma D-3.

Therefore, by Lemma D-3,

Now we compute the second term.

Lastly, we compute the third term

Therefore, the regret is

Rearranging this gives the (Regret-) expression.

Now we derive the (Regret-) expression, assuming that and are arbitrary but is i.i.d. with marginal with a density in the interior. We start with the expected pointwise regret expression

The third term is still the same

We will write the point mass of at as for convenience. Now for the first term, we know that the probability that is

The probability that is

For , has a density given by

Now,

and

For , has a density given by

and CDF given by

We then have

and

Therefore,

or

By integration by part, the first term of the third line is times

where . Substituting this in gives

D.4 Verification of Conditions for Nature’s Saddle (Appendix C.3)

Proof of Proposition C-5.

We first consider the regime where the ODE is (ODE--1). By multiplying both sides of (ODE--1) by , we observe that (ODE--1) is equivalent to

For the case , we set and integrate the above equation from to arbitrary to get the as stated in the theorem statement.

For the case , we set and integrate the above equation from to arbitrary to get the as stated in the theorem statement.

In both cases, we can use Lemma D-1 to write in the valid region as

which immediately implies that is an increasing continuous function in .

In the case, the valid region starts at and the expression immediately implies that , and

which equals 1 because satisfies the same defining equation as , so we can set , and the expression is decreasing in , so the equation setting the above to 1 has a unique solution in (equivalently, in ) if and only if as , the expression is , which is equivalent to that we had just assumed.

In the case, the valid region is from to . The expression implies . The defining equation for in this regime implies that

so . (We still need to prove that the two equations defining has a unique solution; we will defer this to the end of the proof.)

Now we consider the regime where the ODE is (ODE--2). By multiplying both sides by , we observe that (ODE--2) is equivalent to

In the case , this equation applies for all , so we integrate this equation from to arbitrary and note that is 0 when (because of the factor), so we get

which is equivalent to the as stated in the theorem statement. By Lemma D-2, we can write as

The expression immediately implies that is an increasing continuous function of and . We also have

by the defining equation of , and by inspecting the defining equations for and we see that as claimed. The defining equation of is

The expression is decreasing in and it is as , and as because the harmonic series is divergent, so the equation has a unique solution .

In the case , this equation applies for . By requiring that , integrating the equation from arbitrary to gives

Just as before, Lemma D-2 implies that the right hand side is decreasing and continuous in , so is increasing and continuous in . We also have

by the defining equations for , so . We therefore see that the value of at from both the and the regions are equal, so is continuous at as well.

Finally, we will prove that the equations defining in the regime have a unique solution.

Eliminating from the two equations gives

or

Let denote the right hand side viewed as a function of , namely,

We claim that is a decreasing function. That is, we want to show that . We compute

Note that

We then have

Therefore, we have if and only if

We can prove this inequality as follows. Both sides are zero for , so it is sufficient to show that the derivative of the LHS is the derivative of the RHS. This is true because the derivative of the LHS is and the derivative of the RHS is

Therefore, we have proved that is decreasing in .

Therefore, to show that the equation has a unique solution , it is sufficient to show that , or

The first inequality

is true by the definition of and . The second inequality is equivalent to

which is true by the definition of and .

We also conclude from the above that as we have , while as , we have .