Label Smoothing is Robustification

against Model Misspecification

Abstract

Label smoothing (LS) adopts smoothed targets in classification tasks. For example, in binary classification, instead of the one-hot target used in conventional logistic regression (LR), LR with LS (LSLR) uses the smoothed target with a smoothing level , which causes squeezing of values of the logit. Apart from the common regularization-based interpretation of LS that leads to an inconsistent probability estimator, we regard LSLR as modifying the loss function and consistent estimator for probability estimation. In order to study the significance of each of these two modifications by LSLR, we introduce a modified LSLR (MLSLR) that uses the same loss function as LSLR and the same consistent estimator as LR, while not squeezing the logits. For the loss function modification, we theoretically show that MLSLR with a larger smoothing level has lower efficiency with correctly-specified models, while it exhibits higher robustness against model misspecification than LR. Also, for the modification of the probability estimator, an experimental comparison between LSLR and MLSLR showed that this modification and squeezing of the logits in LSLR have negative effects on the probability estimation and classification performance. The understanding of the properties of LS provided by these comparisons allows us to propose MLSLR as an improvement over LSLR.

Index Terms:

Label smoothing, logistic regression, asymptotic statistics, robust statistics, smoothed KL-divergenceI Introduction

Label smoothing (LS) adopts smoothed targets in classification problems. Conventional logistic regression (LR) uses a one-hot vector as a target (Section II-B), while LR with LS (LSLR) [1] uses a smoothed target vector that replaces the component 1 in the one-hot vector with a smaller value and 0 with a larger value (Section II-C). Previous studies have provided, mostly through experimental considerations, several heuristic findings on behaviors of LSLR, for example,

-

A1.

It prevents the largest logit from becoming much larger than all others (squeezes the logits) and encourages the model to be less confident [1].

-

A2.

It generally improves adversarial robustness against a variety of attacks [2].

-

A3.

It can often significantly improve the generalization of a (multi-class) neural network [3].

Motivated by these supportive findings, LS has recently been actively adopted, together with a neural network model, in various modern applications such as speech recognition [4], machine translation [5, 6], image classification [7, 8], and visual tracking [9]. However, in spite of the above-mentioned findings on LS and its wide use, the underlying mechanism of LS has not been fully explored yet. In this paper we study it and provide further understanding on LS, including verification of the significance of squeezing of the logits stated in A1 and supportive arguments on A2 and A3, which is the first of two contributions of this paper.

Although most previous studies have interpreted LSLR as entropy-regularized LR that squeezes the logits (Section II-D), we propose in this paper an alternative interpretation of LSLR in which LSLR performs probability estimation using a different loss function and consistent estimator than LR (Section II-E). We then study the significance of each of these two modifications, via introducing a novel method, modified LSLR (MLSLR), that uses the same loss function as LSLR and the same consistent probability estimator as LR, which results in no squeezing of the logits (Section II-F).

For the modification of the loss function, we give theoretical comparisons between LR and MLSLR: Compared with LR, MLSLR with a larger smoothing level has lower efficiency with correctly-specified models (Section III-B) but higher robustness against model misspecification (Section III-C). As far as the authors’ knowledge, this paper is the first to report the low efficiency as a disadvantage of LS, and the robustness is a basis for the adversarial robustness A2 of LS. Also, the trade-off between the low efficiency and the high robustness explains the better practical performance A3.

Moreover, for the modification of the consistent probability estimator, we prove that an estimator of LSLR can have output with an unnecessarily large range like , implying that it is inappropriate as a probability estimator. We also experimentally compare LSLR and MLSLR using a neural network model, and the result shows that LSLR performed worse than MLSLR (Section IV). This experimental result implies that modifying the consistent probability estimator and squeezing the logits are not effective in improving the probability estimation and classification performance of LR, but rather have a negative impact, as opposed to the previous understanding A1. In other words, MLSLR based on a consistent probability estimator with an appropriate range would be recommended over LSLR, in typical usages with a large-size model such as a deep neural network model. Collaterally, we propose to practically use MLSLR as the second of two contributions of this paper.

II Preliminaries

II-A Problem Formulation, Notation, and Terminology

In this section, we discuss interpretations of LS. We first formulate probability estimation and classification tasks, along with preparing required notations and terminologies.

Suppose that one has the data from the joint distribution of the explanatory random variable and target random variable , where is the number of different values that take and . A classification task is defined in this paper as a task to obtain a good classifier such that the task risk , defined as the expectation value with respect to the pair of a user-specified task loss function , is made small. The task of minimizing misclassification rate corresponds to using the zero-one loss as the task loss, where values 1 if a condition is true and 0 otherwise.

Classification methods that we discuss in this paper rely on the framework of so-called empirical (surrogate) risk minimization (ERM). Let be a learner class, where denotes the set of values the learners in may output. A classifier is constructed as with a labeling and a learner that minimizes the empirical surrogate risk (which is an empirical counterpart of the surrogate risk ) for a surrogate loss function that is continuous in its first argument. ERM can be interpreted as estimation of the conditional probability distribution (CPD) function , where is the probability simplex in , and the labeling is designed according to that interpretation.

Note that our notations show possibly-multivariate objects in bold and often omit the -dependence for the brevity.

II-B LR: Conventional Logistic Regression

For the learner class , LR solves

| (1) |

where is the one-hot encoding function, whose -th component is for . The obtained functions are also called the logits.

As satisfies , a mean of the targets can be seen as an empirical estimate of the CPD function . The KL-divergence, defined for probability mass functions as

| (2) |

has the consistency property

| (3) |

This property shows that LR applies the logit model

| (4) |

as a consistent estimator (see also Corollary 1), in estimation of the true CPD function through minimization of an empirical estimate of the mean KL-divergence , where denotes the expectation value regarding the random variable .

II-C LSLR: Logistic Regression with Label Smoothing

For the smoothing function

| (5) |

with a smoothing level that is conventionally in , LSLR applies the smoothed target instead of the one-hot encoded target of LR. Namely, LSLR considers the learning process

| (6) |

II-D Regularization View: LSLR is Entropy Regularized LR

Since the smoothed target satisfies , a mean of the smoothed targets can be seen as an empirical estimate of the smoothed CPD function . On the basis of this consideration, along with an implicit supposition that LSLR adopts the logit model for estimation of the true CPD function , and the equation

| (7) | ||||

with the all-1 -dimensional vector , most previous studies regard LSLR as LR with the entropy regularization term which penalizes the deviation of from the uniform CPD function ; See [1, 3, 2, 10]. As a result, the learned logit model is expected not to take an extreme probability estimate like , or equivalently, the logits by LSLR will be squeezed; See Theorem 1, B6. Many previous studies claim that this squeezing helps avoid over-fitting of the model, as in the finding A1.

II-E Our Loss View: LSLR modifies Loss Function and Consistent Probability Estimator from LR

We here introduce an alternative view of LS that LSLR adopts a loss function and consistent estimator different from those of LR for probability estimation (the loss view). First, we define the smoothed KL (SKL)-divergence

| (8) |

for . The SKL-divergence satisfies the consistency property

| (9) |

for or and in a certain range (see Theorem 1, B3). Then, we view that LSLR (6) adopts not the logit model but what we call the roughened logit (R-logit) model, which is defined with an unconventional link function as

| (10) | ||||

as an estimator (as ) of the true CPD function through minimizing an empirical estimate of the mean SKL-divergence . As one can see from the fact that appearing in the loss (8) and in the model (10) cancel out each other, this estimator, not the logit model, is consistent to the true CPD for LSLR.111One may see that LSLR estimates the smoothed CPD function with the logit model . However, since this view changing properties of the data makes it difficult to compare with the original LR, our paper will not discuss this view further.

Note that the logit model is not the only probability estimator; For example, another well-known probability estimator is the probit model in probit regression. Our loss view uniformly determines which parts we treat as a probability estimator and which parts we treat as a loss function for a probability estimation method, according to the consistency of the probability estimator to the true CPD function, for fair comparisons to be performed in this paper.

We here list basic properties of the SKL-divergence and R-logit model , which are the KL-divergence and logit model when :

Theorem 1.

For any ,

-

B1.

for and can range or for or , and these intervals cover .

-

B2.

for any and .

-

B3.

, and if and only if , for any and . Also, for any .

-

B4.

is convex in for any : , for any and .

-

B5.

for .

-

B6.

, , or for , any , or .

-

B7.

, , , and , for any , , and .

For ,

-

B8.

, , , and , for any , , and .

The constraint in B5 and B6 is for removing the degree of freedom of translation of the minimizers; Consider that, for example, if minimizes , then also minimizes that SKL-divergence for any . The consistency property (9) holds for as stated in B3, and one can perform LSLR and MLSLR (formulated in the next section) even with . However, we have found no advantage of choosing for , and there is no advantage at all especially when because LSLRs or MLSLRs with and behave equivalently as suggested by B8, so we restrict our subsequent discussion to to simplify the statement of the paper; See appendices for supplemental discussions on the case with .

II-F MLSLR: Modified LSLR

As we described in the previous section, LS of LSLR modifies a loss function and a consistent estimator for probability estimation, from the KL-divergence and logit model of LR to the SKL-divergence and R-logit model, respectively. A direct comparison between LR and LSLR does not distinguish effects of these two modifications on behaviors of LS. We therefore propose a novel method which we call the modified LSLR (MLSLR),

| (11) |

that adopts as the loss function the same SKL-divergence as LSLR, along with the same logit model as LR for estimating the CPD function . MLSLR allows us to study significance of the modification of the loss function via its comparison with LR, as well as significance of the modification of the estimator via its comparison with LSLR. It should be noted that the latter comparison will also clarify the importance of squeezing the logits in LSLR, as MLSLR does not squeeze the logits (see Theorem 1, B5).

II-G LSQLR: MLSLR with

We find it useful to consider the limit of MLSLR in understanding properties of MLSLR and LSLR.

Theorem 2.

For any and , as , where is the Euclidean norm in .

This theorem indicates especially that MLSLR with a limiting smoothing level approaches least squares logistic regression (LSQLR)

| (12) |

LSQLR adopts the logit model as a consistent estimator (as ) of the true CPD function via minimizing an empirical version of the mean squared distance (plus -independent quantity ), where . Then, one can regard MLSLR with as interpolating between LR () and LSQLR ().

In contrast, even if considering the consequence of Theorem 2 into account, LSLR with

| (13) |

remains the -dependence, and this method is not practical since diverges almost everywhere. Due to this trouble, we do not study LSLR using very close to 1.

II-H Summary on Our Comparing Methods

LR applies the KL-divergence loss and logit model (see Section II-B and (1)), LSLR applies the SKL-divergence loss and R-logit model (see Sections II-C and II-E, and (6)), and MLSLR including LSQLR applies the SKL-divergence loss and logit model (see Sections II-F and II-G, and (11) and (12)). This paper formulated these methods according to the framework of ERM, and these methods do not have an explicit term for regularization in our formulations (so we do not use the terminology ‘regularization’ except when discussing statements of existing studies). We will compare these methods that use different loss functions and consistent probability estimators, under settings regarding the underlying data distribution and data characteristics, and the model size or representation ability of the probability estimators, according to classical analysis for ERM methods.

One may be concerned about the remaining one of the four combinations of the KL- or SKL-divergence loss and the logit or R-logit model. The following problem corresponds to the combination of the KL-divergence loss and the R-logit model:

| (14) |

However, an element of the R-logit model can take a negative value, so the KL-divergence for this model will be ill-defined and the optimization will fail. This method is therefore not promising and will not be considered in this study.

III Statistical Analysis: LR versus MLSLR

III-A Setting, Notation, and Basic Properties

In the theoretical analysis presented in this section, for the sake of interpretability of the comparison results, we consider the simple case of binary classification () for the task of minimizing misclassification rate (). See Appendix B for analysis under more general settings including multi-class cases and cost-sensitive tasks.

We write the distribution of as , relabel to , and abbreviate the conditional probability as . Then, for the real-valued learner class , the surrogate loss functions for LR, LSLR, MLSLR, and LSQLR are respectively given by with

| (15) | ||||

where itself is also called a surrogate loss (subscript LR, LS, MLS, or LSQ of an object indicates that it is for LR, LSLR, MLSLR, or LSQLR).222The learner model is written as a real-valued function in Section III, which is a simplification in the binary case, from the formulations (1), (6), (11), and (12) of the four methods that adopted an -valued function, by letting be the model. The loss function is also known as Savage loss [11]. Also, a labeling function is fixed to the sign function, (if ), (if ), considering the task and surrogate losses.

First, we summarize results showing that LR, MLSLR, and LSQLR can consistently perform probability estimation via the logit model, while LSLR can via the R-logit model:

Corollary 1.

Assume , and let . Then, regardless of the distribution of , a.s. for LR, MLSLR, and LSQLR, and , a.s. for LSLR.

Also, it can be found that surrogate loss is properly designed for the task loss under the labeling function .

Corollary 2.

Assume , and let . Then, regardless of the distribution of , for LR, LSLR, MLSLR, and LSQLR.

This result can be proved from the fact that the loss is classification calibrated; Refer to [12]. Also, this result can be generalized to the multi-class cases () and cost-sensitive tasks () [13].

These properties form an important basis for analysis of the performance in probability estimation and classification tasks with an empirical surrogate risk minimizer, which are the subjects below. These results indicate that the methods have no difference in the limit of the performances, and suggest that we should discuss their estimation performance (error) and the adequacy of the models in more specific settings.

III-B Lower Efficiency with Correctly-Specified Models

III-B1 Theories on Asymptotic Behaviors

In order to make a detailed comparison, we focus in this section on a specific case where the data are distributed in association with a certain linear model and methods adopt a linear learner class (the correctly-specified model). Namely, assuming that the true conditional positive probability is for any , we study the estimation result of the true parameter by LR, MLSLR, and LSQLR that use the same logit model with the learner class as a probability estimator. Since LSLR adopts a consistent probability estimator (the R-logit model) different from the others, it will not give a consistent parameter estimate of under the above-mentioned setting. Thus, it is difficult to perform fair comparisons of LSLR with the other methods, and so we here consider only LR and MLSLR including LSQLR. The only difference between these compared methods lies in their loss functions.

With the correctly-specified model, one can show consistency, asymptotic normality, and asymptotic mean squared error (AMSE) of an empirical parameter estimate defined by

| (16) |

on the basis of well-established theories for generalized linear models (see [14, Section 3] for LR) or M-estimators (see [15] or [16, Chapter 6] for MLSLR and LSQLR).

Theorem 3.

Theorem 4.

Assume C1–C3 in Theorem 3, , and

-

C4.

for LR, or for MLSLR and LSQLR.

Then, for defined by (16), converges in distribution to a -dimensional normal distribution with mean and covariance matrix with

| (17) | ||||

where and are respectively the nabla and Hessian operator with respect to the model parameter, and where and for LR, MLSLR, and LSQLR are

| (18) |

In the large-sample limit , the AMSE of becomes

| (19) |

Therefore, the ratio (which is called asymptotic relative efficiency, ARE) serves as an indicator of the estimation performance of a method corresponding to the matrix ; The smaller the ARE is, the lower the asymptotic efficiency of the method is (a larger-size sample is needed to achieve the same level of estimation performance as LR). Note that it can be theoretically found that LR gives asymptotically the most efficient estimate by considering the Cramér-Rao bound since LR is a maximum likelihood method.

| MLSLR | LSQLR | ||||

|---|---|---|---|---|---|

| .9815 | .9627 | .9496 | .9421 | .9396 | |

| .9043 | .8531 | .8239 | .8085 | .8036 | |

| .7815 | .7112 | .6749 | .6566 | .6510 | |

| .9604 | .9286 | .9085 | .8972 | .8937 | |

| .8844 | .8282 | .7969 | .7805 | .7754 | |

| .7760 | .7051 | .6688 | .6504 | .6447 | |

| .8915 | .8279 | .7916 | .7725 | .7665 | |

| .8281 | .7605 | .7248 | .7065 | .7009 | |

| .7605 | .6885 | .6518 | .6334 | .6277 | |

Table I shows AREs of MLSLR and LSQLR in the example where the data with a 2-dimensional covariate follow the distribution , in which the probability density at is given as a product of

| (20) |

with , , where is a point mass distribution at . It indicates that the asymptotic efficiency of MLSLR tends to decrease, as the smoothing level increases to 1.

III-B2 Simulation Experiment

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

We are also interested in estimation performance of MLSLR and LSQLR in a finite-sample situation as well as the large-sample limit. The numerical experiment in this section was performed to see it.333Our program codes for experiments in Sections III-B2, III-C2, and IV and Appendix D are in https://github.com/yamasakiryoya/LSIS.

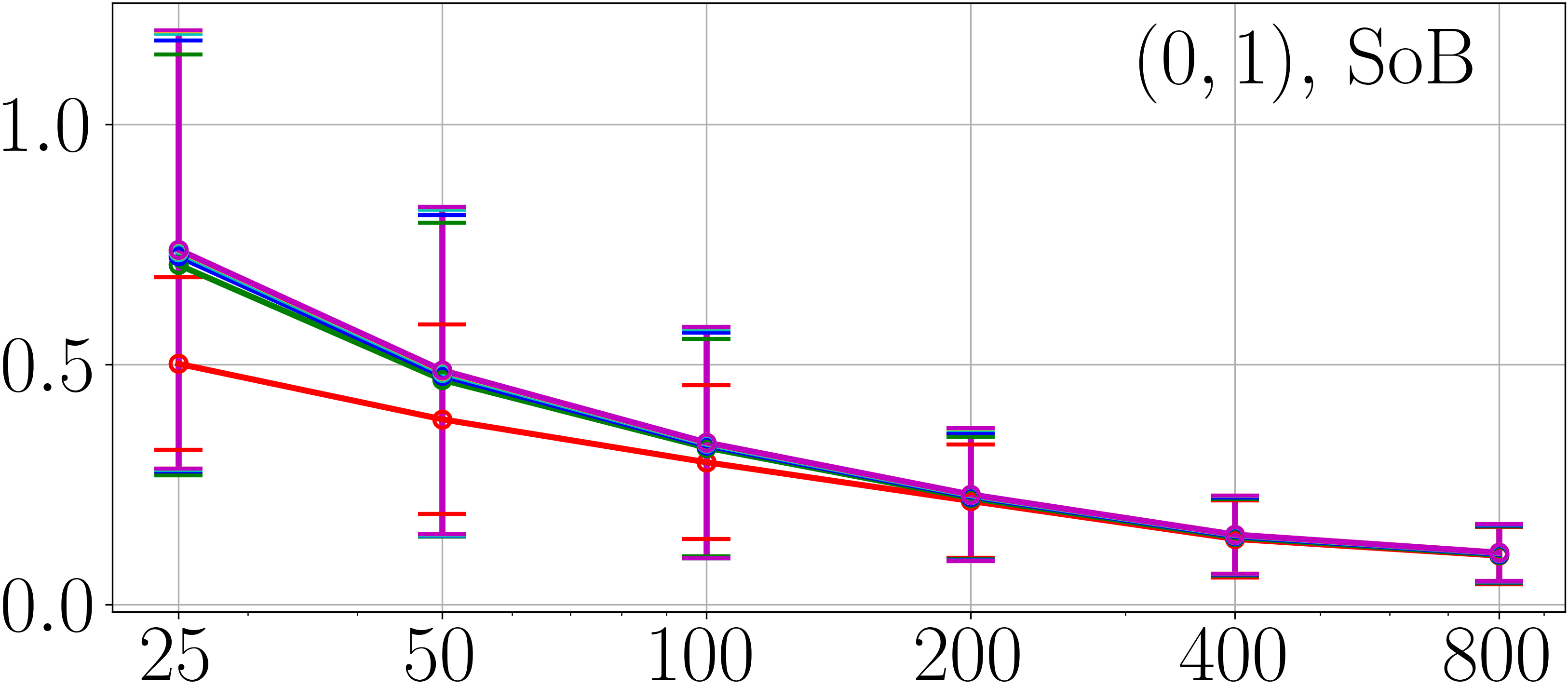

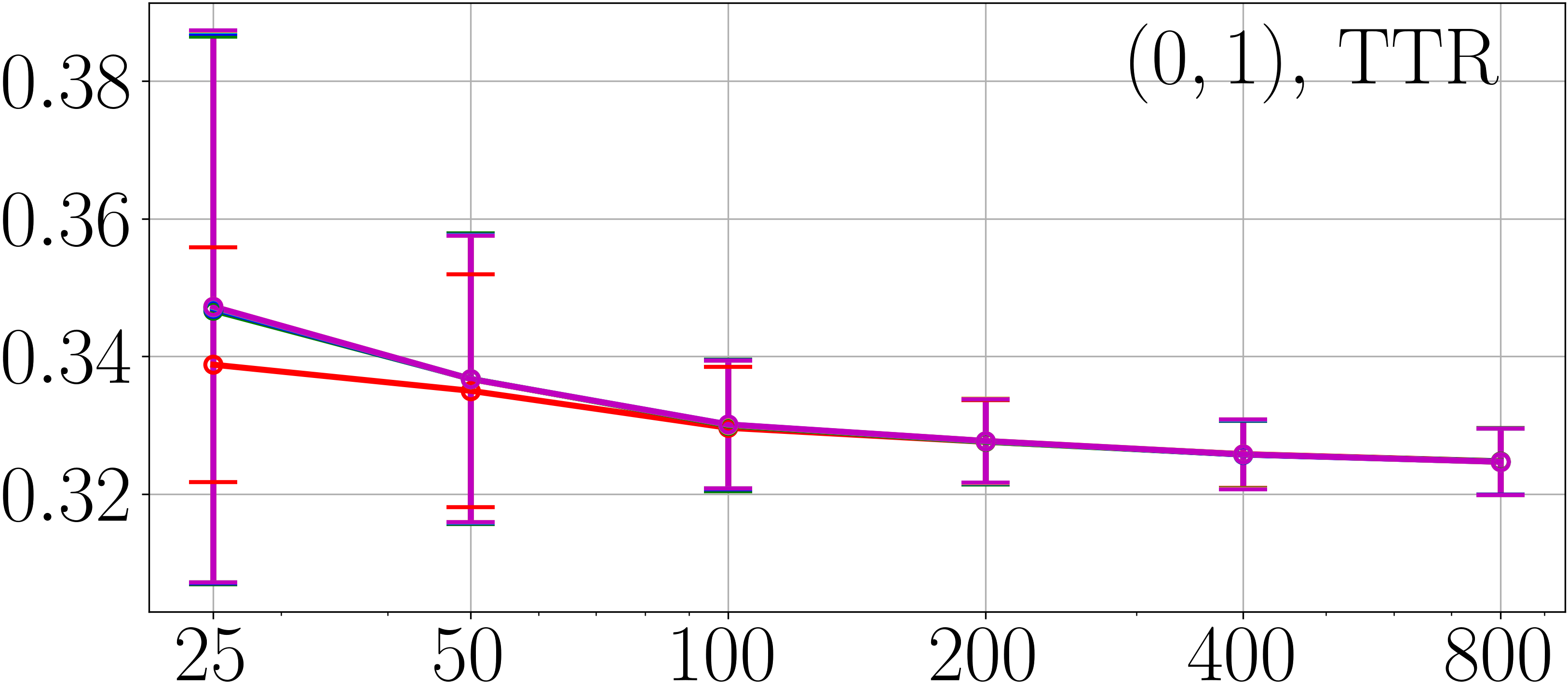

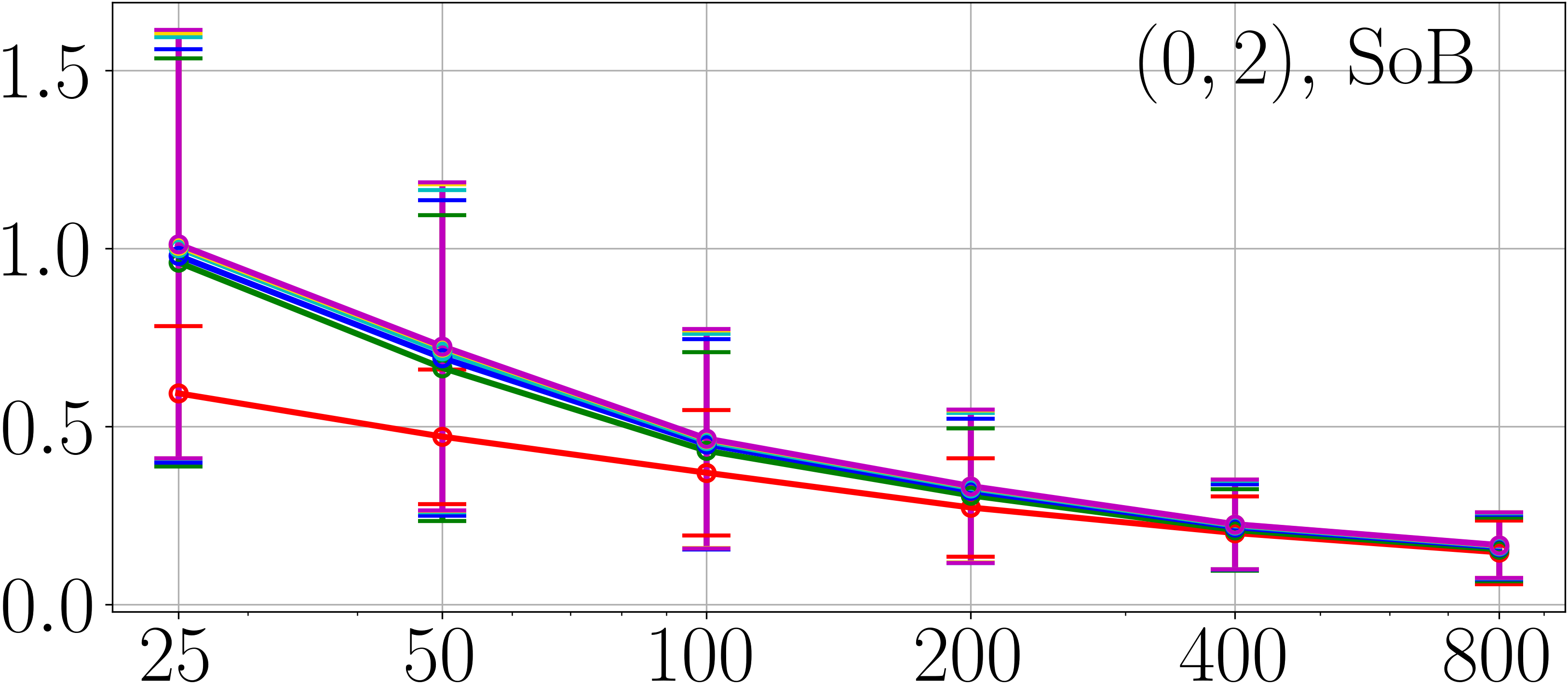

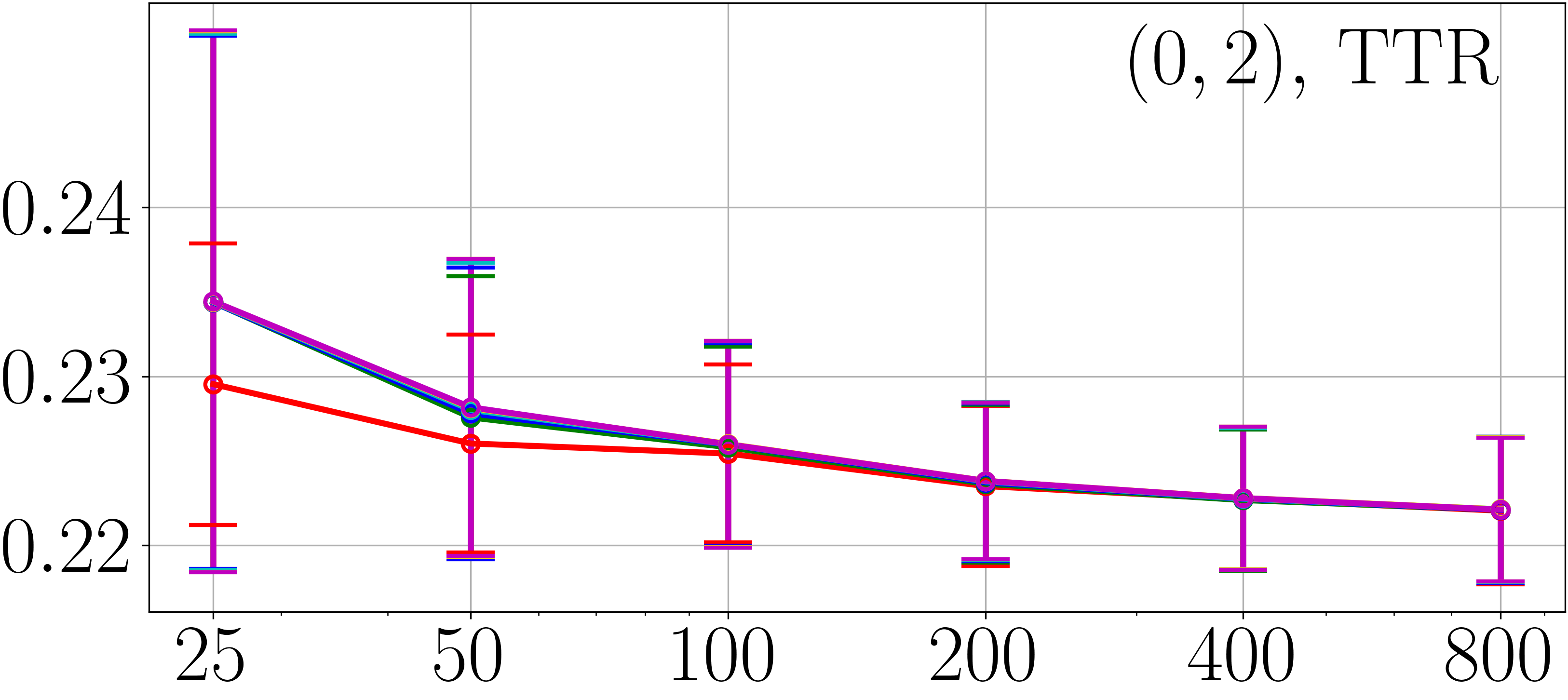

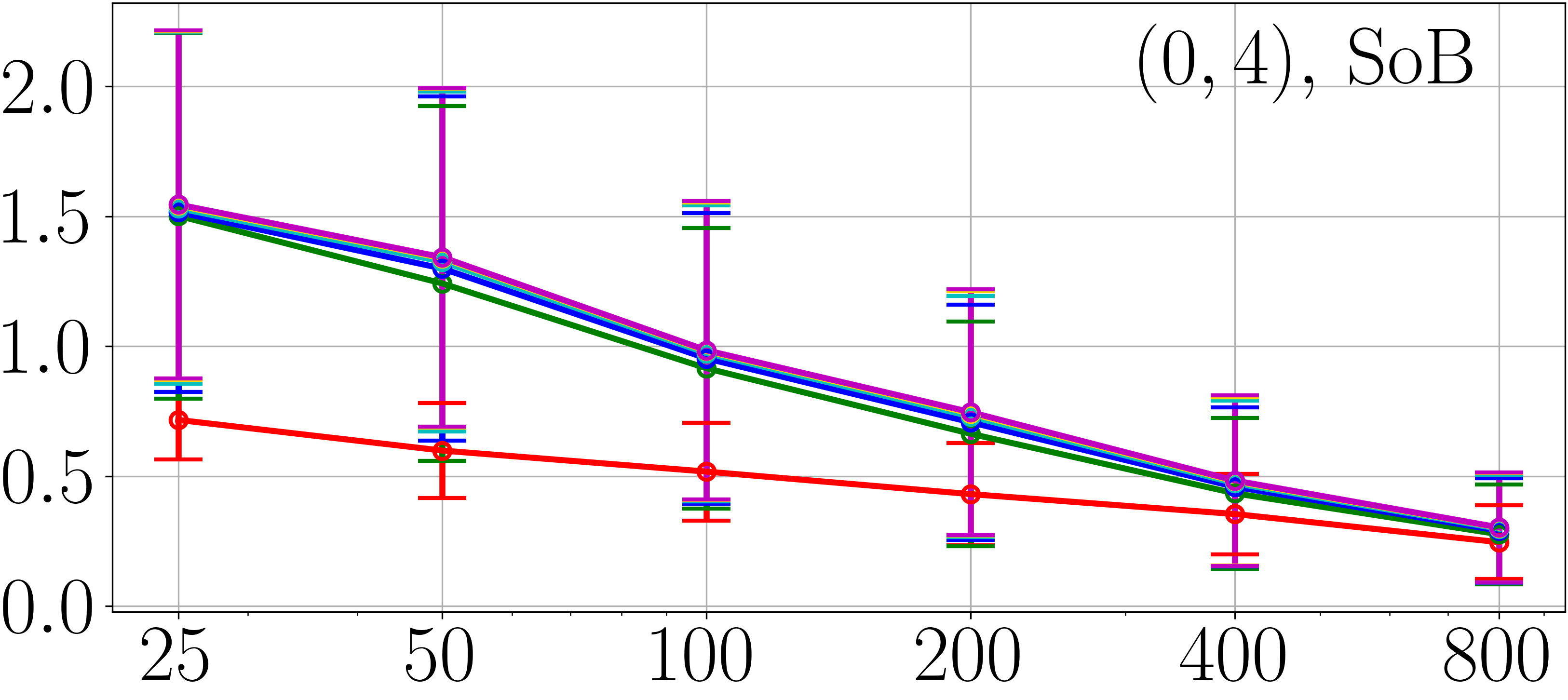

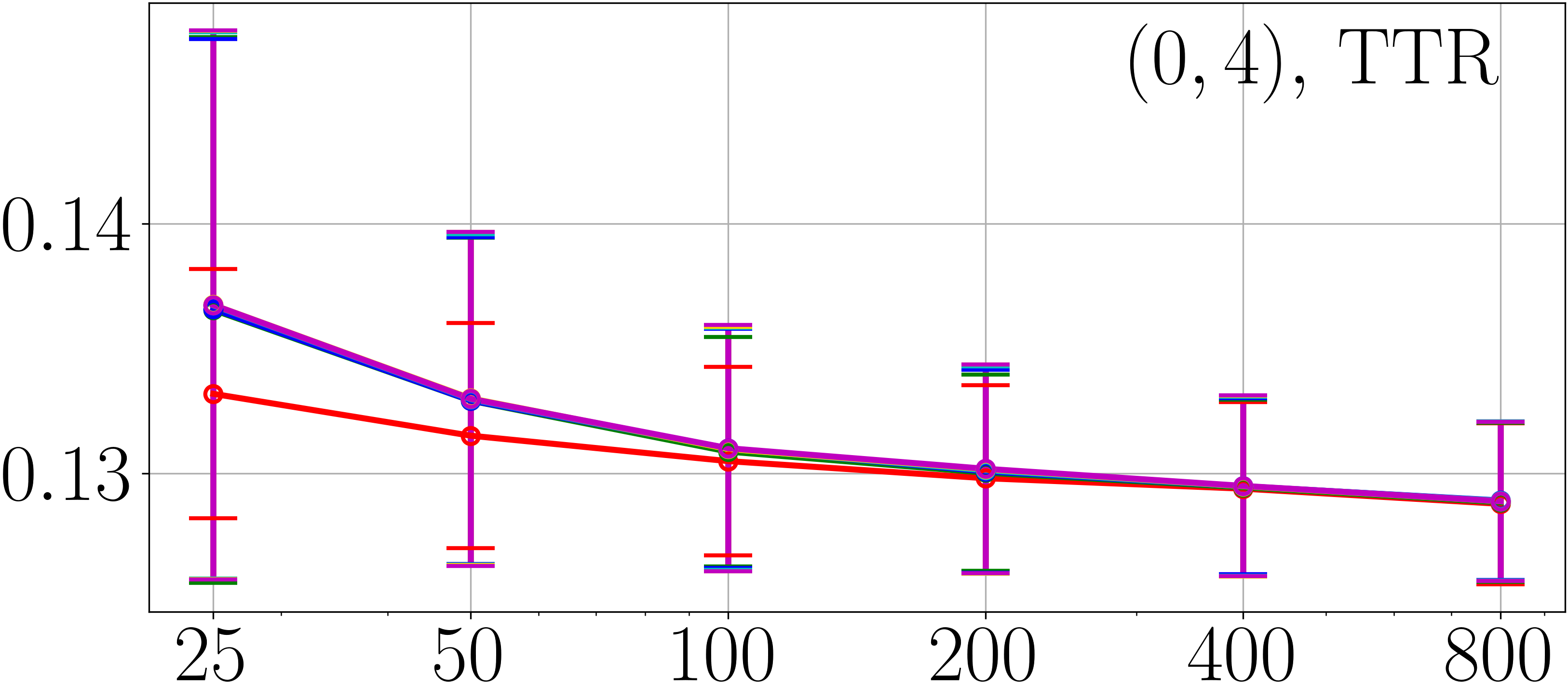

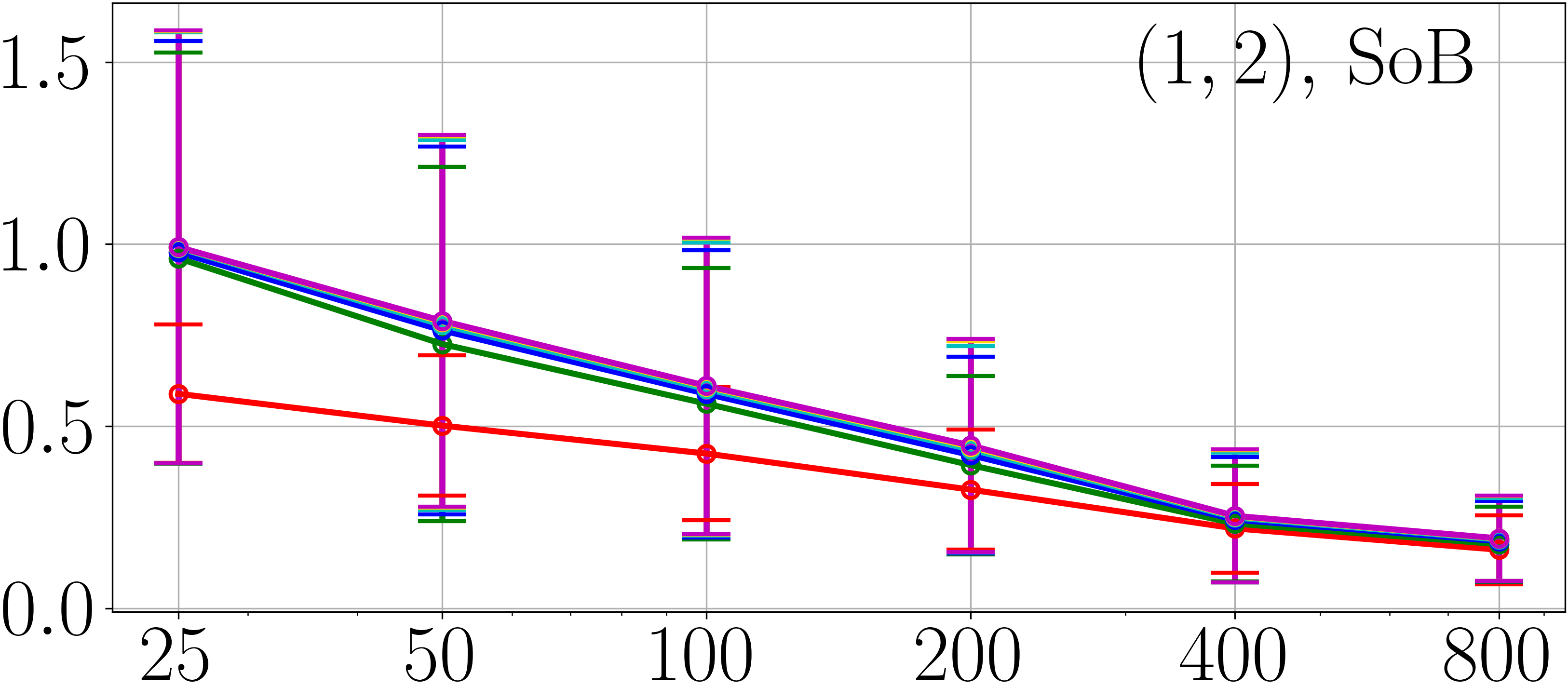

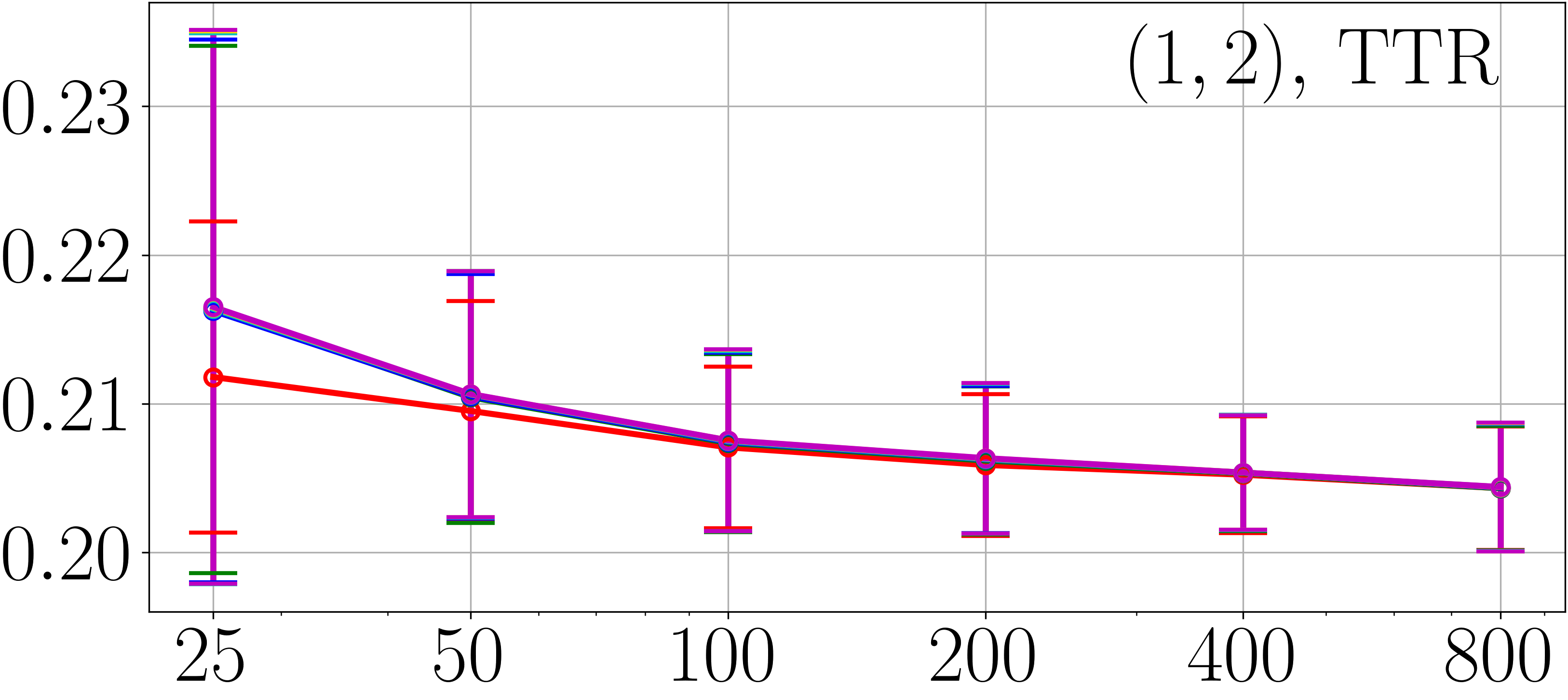

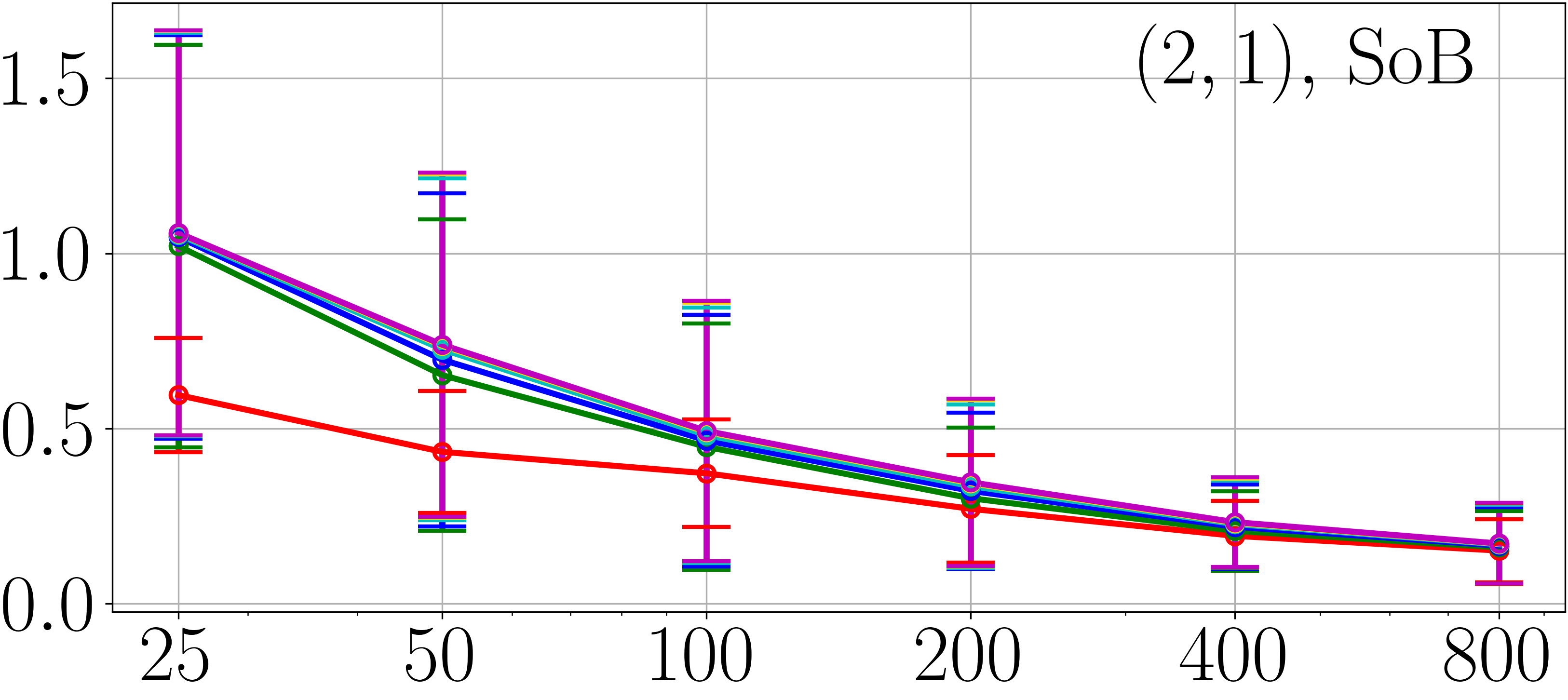

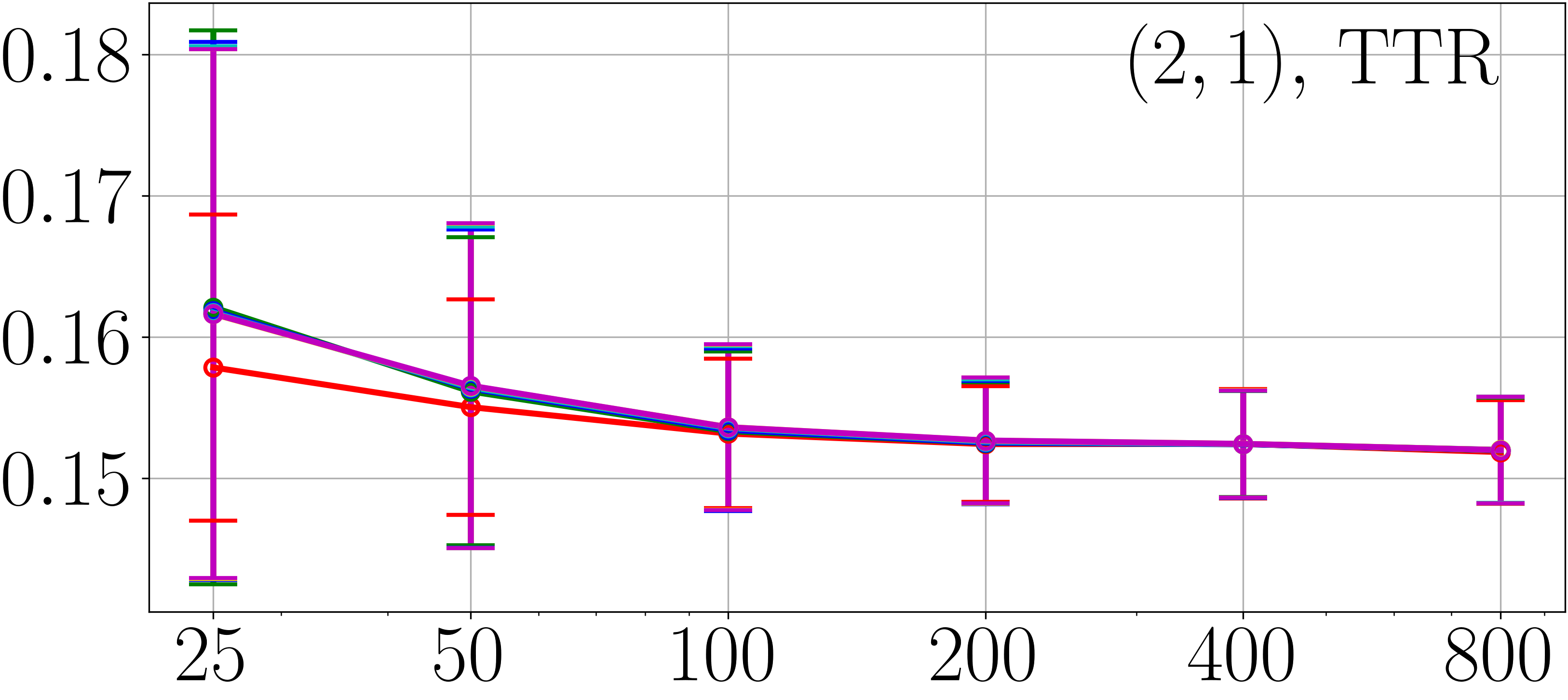

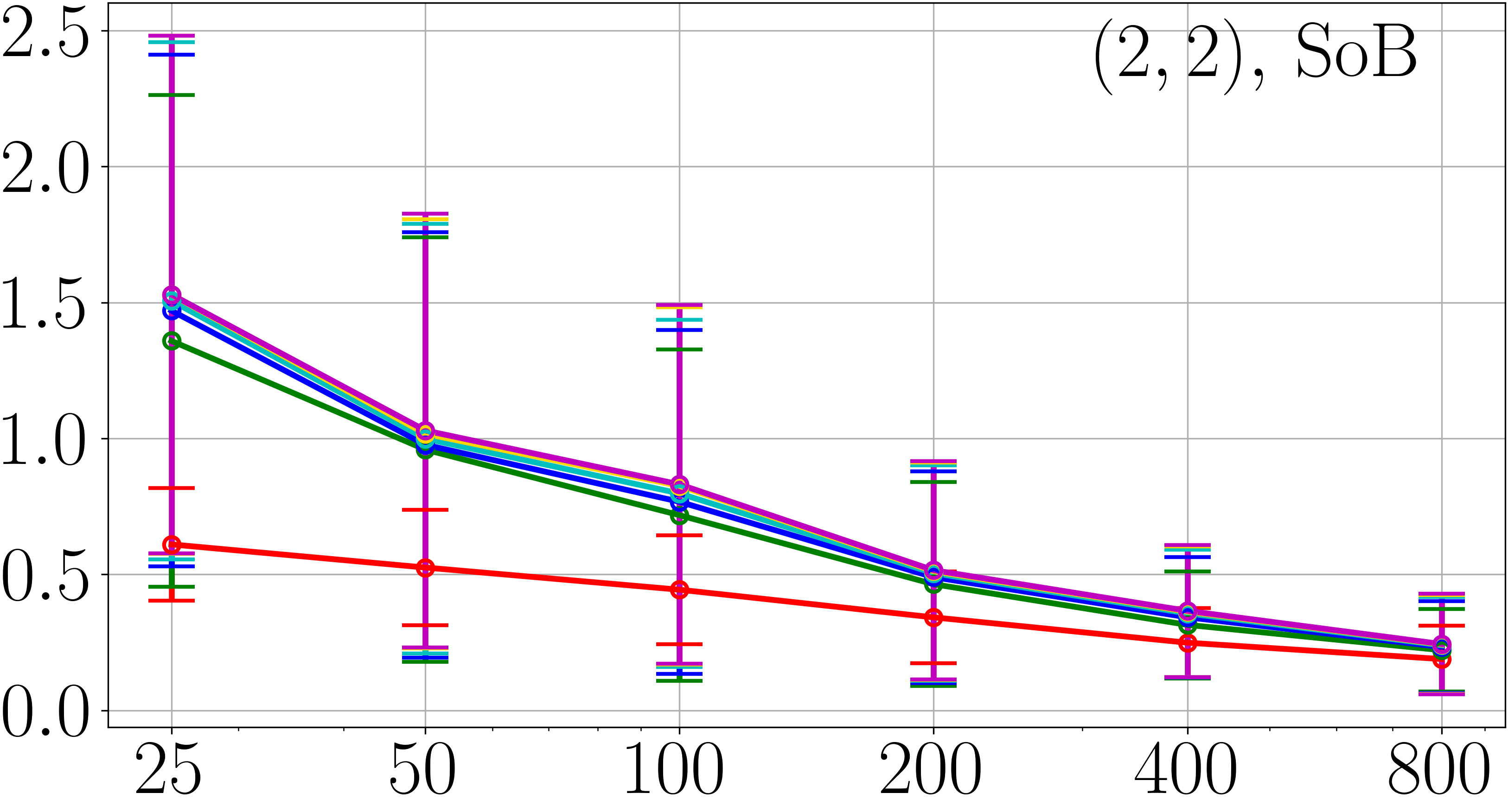

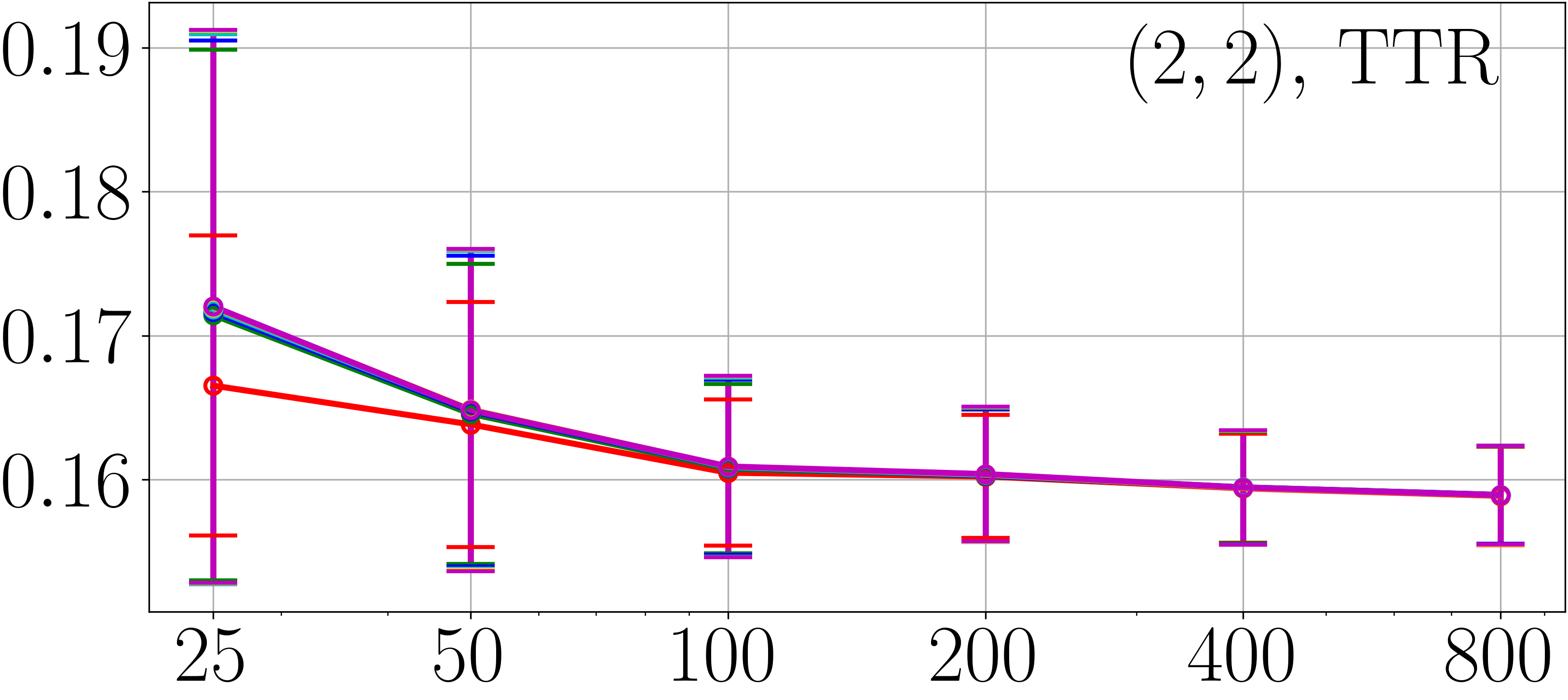

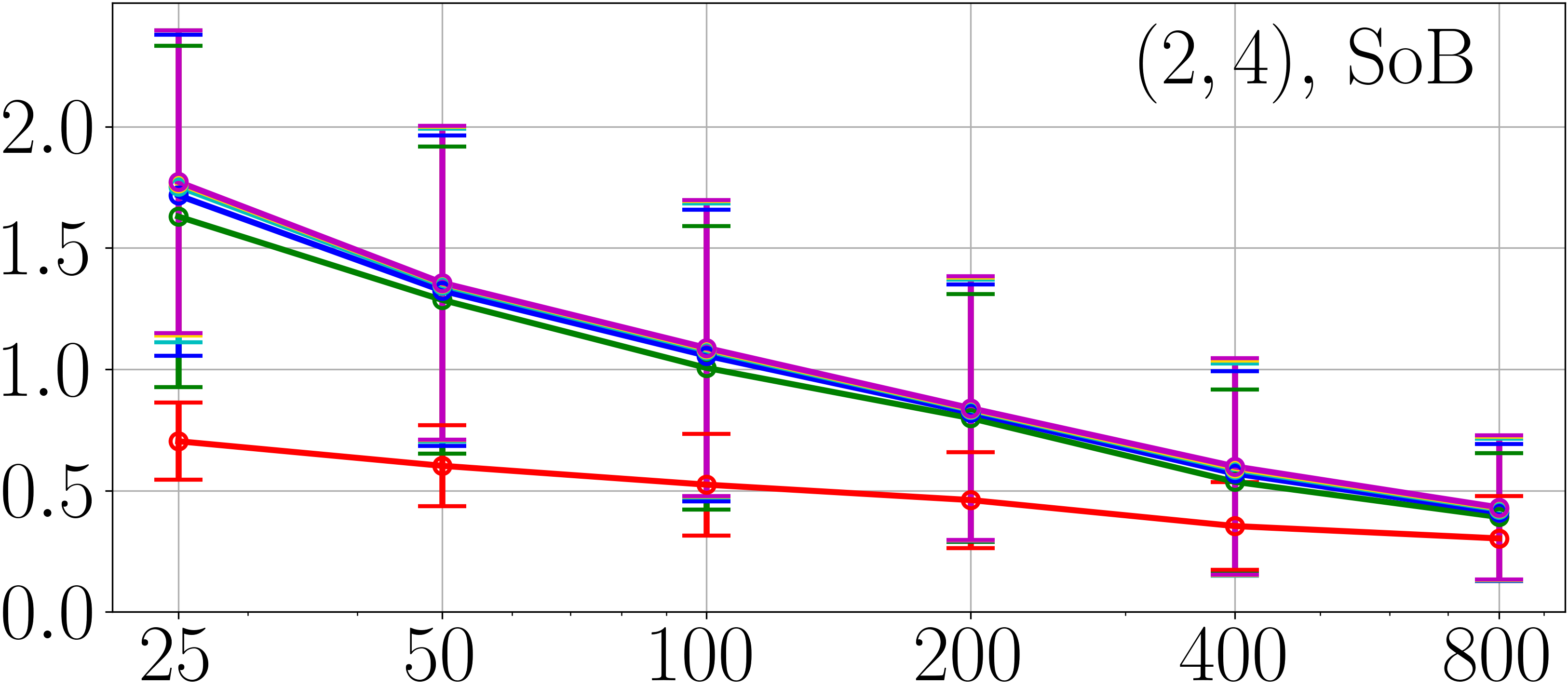

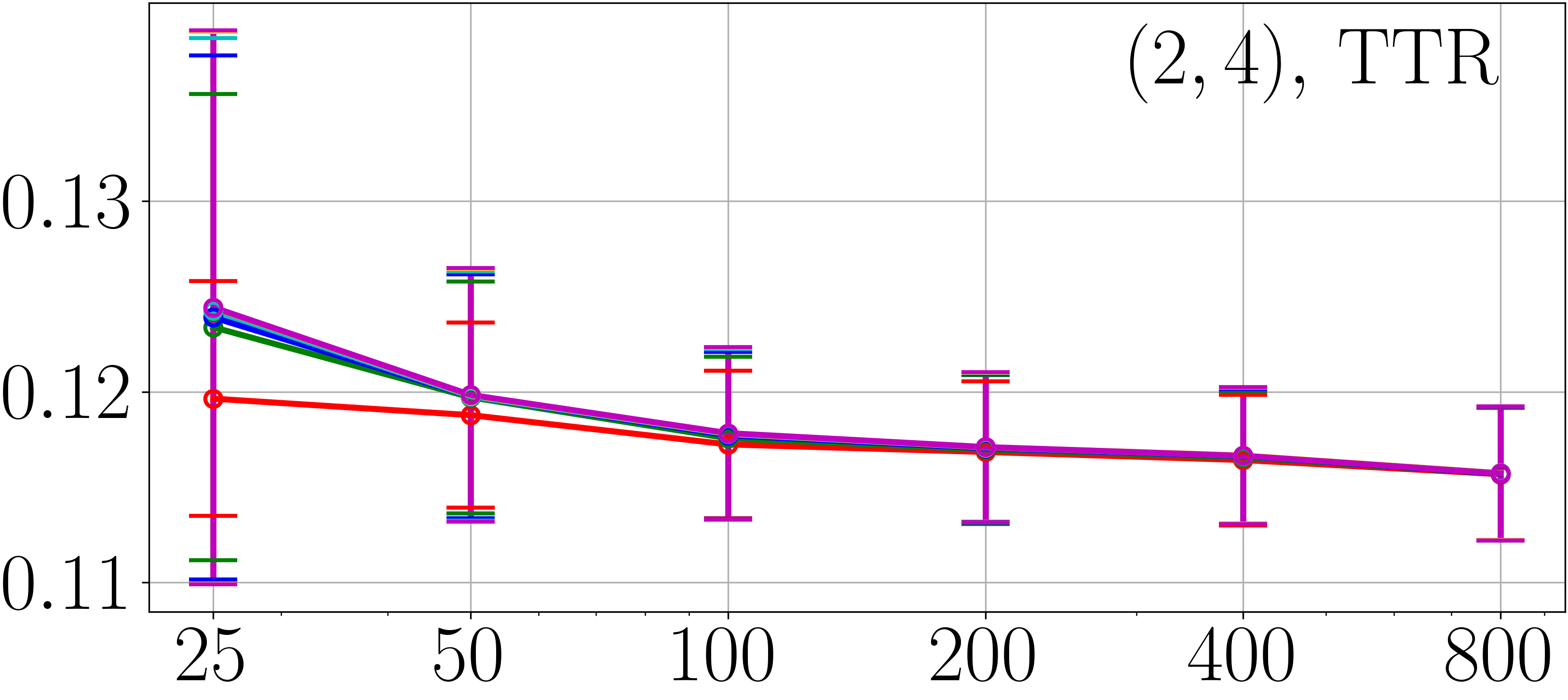

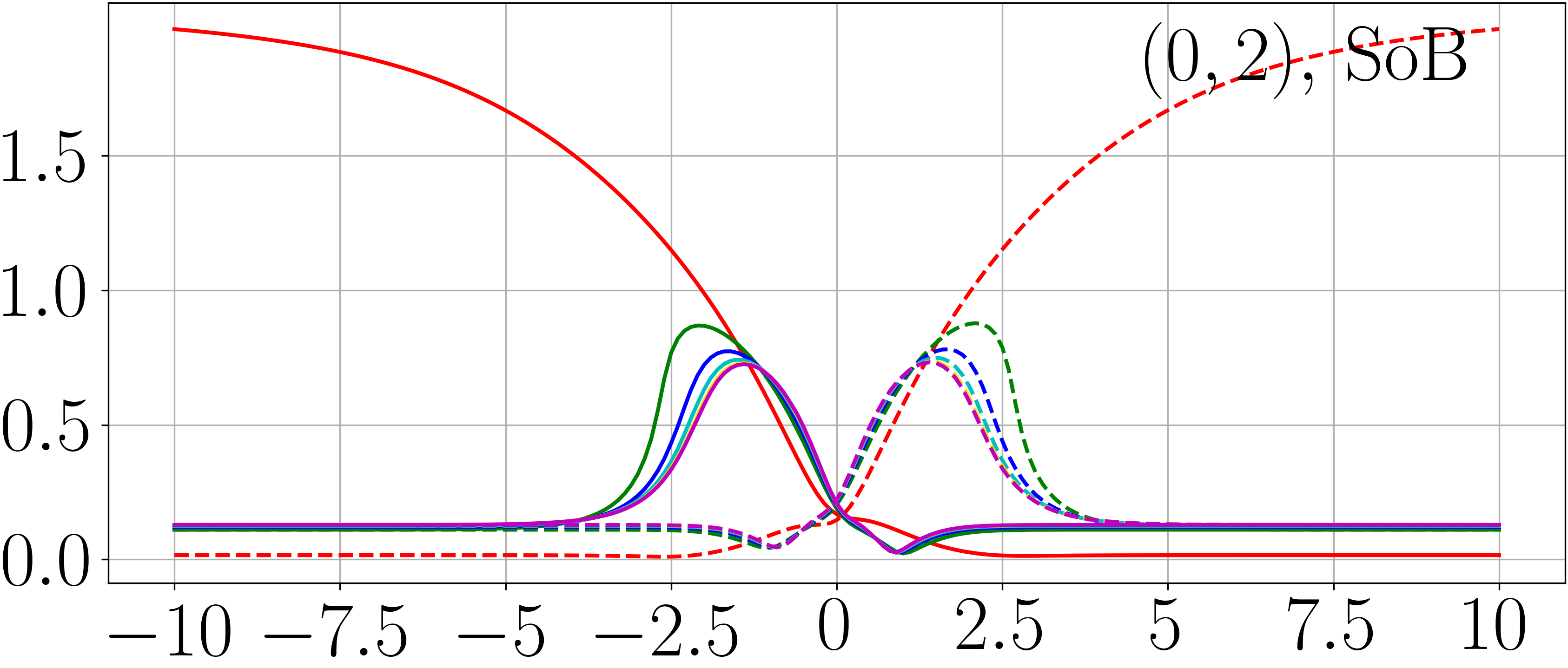

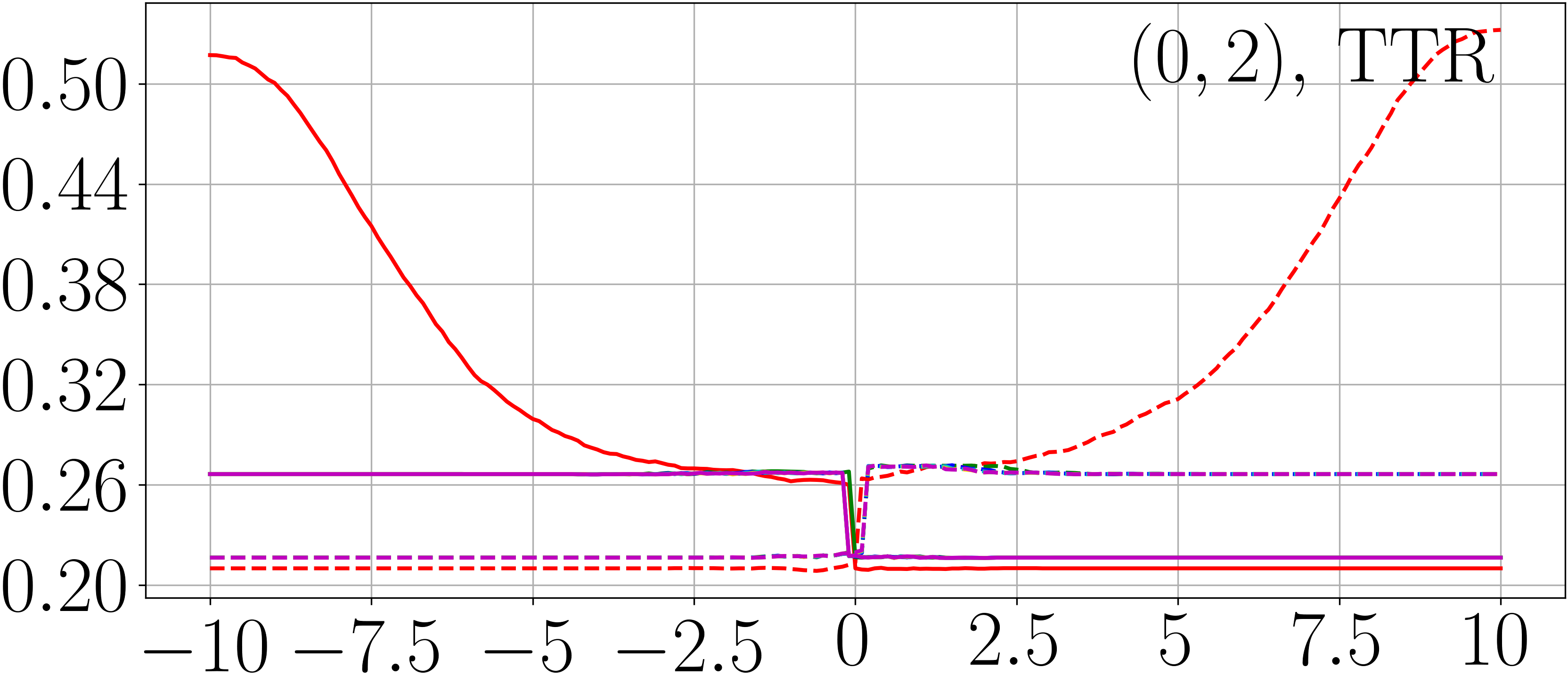

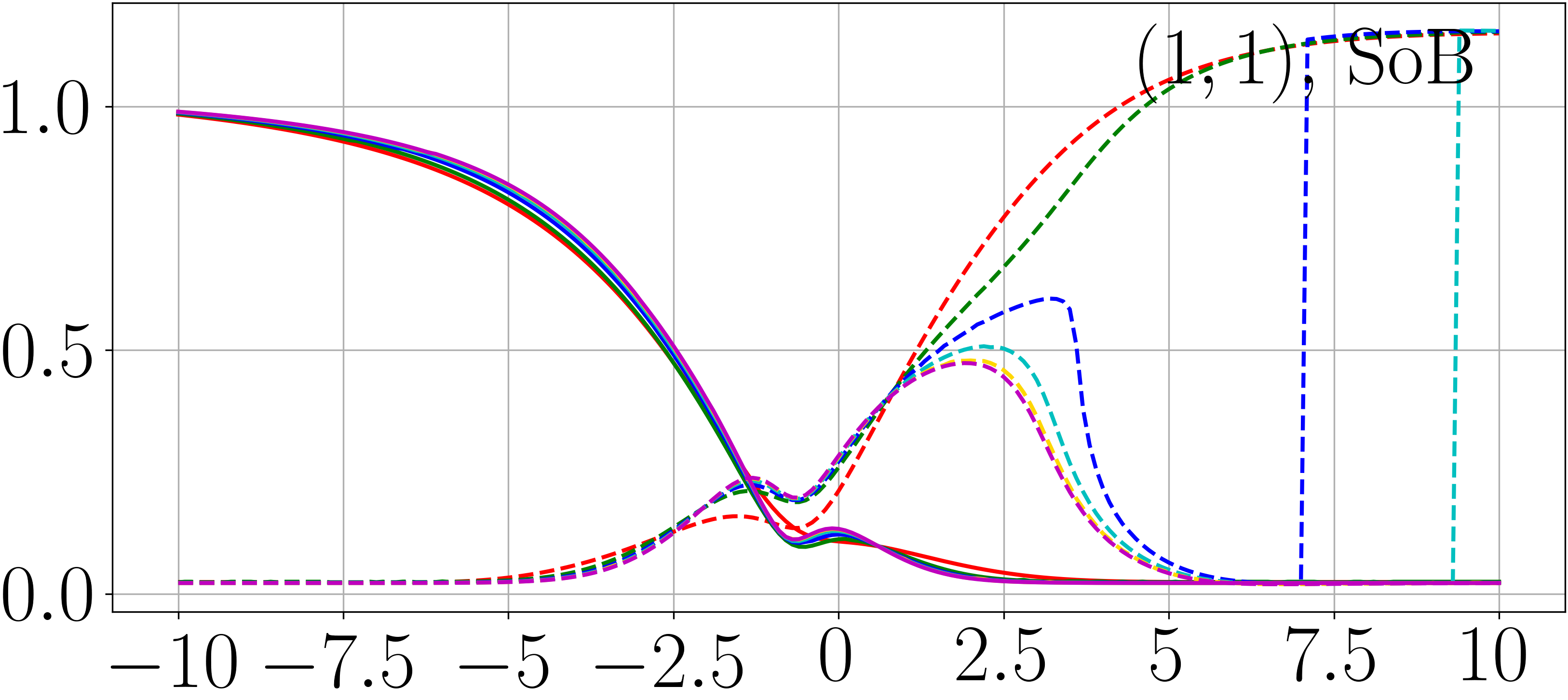

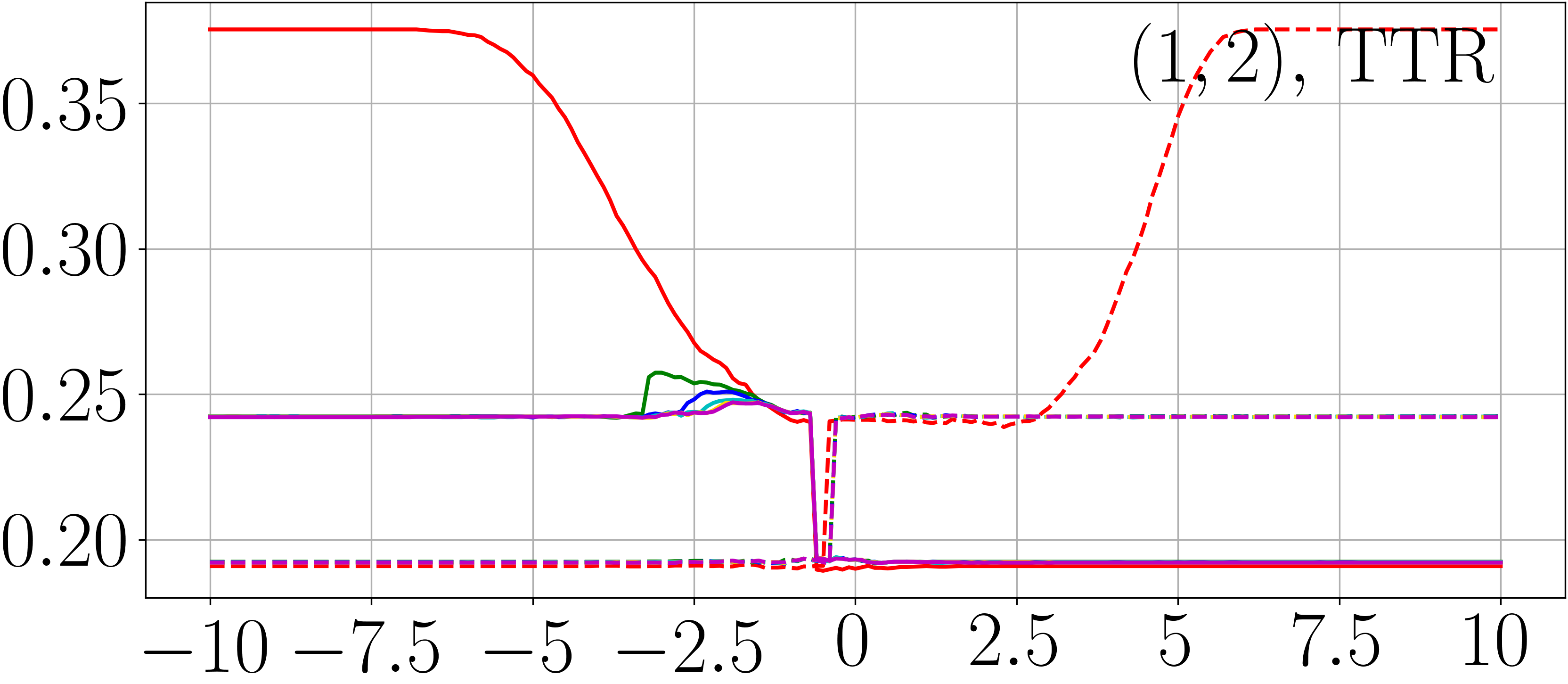

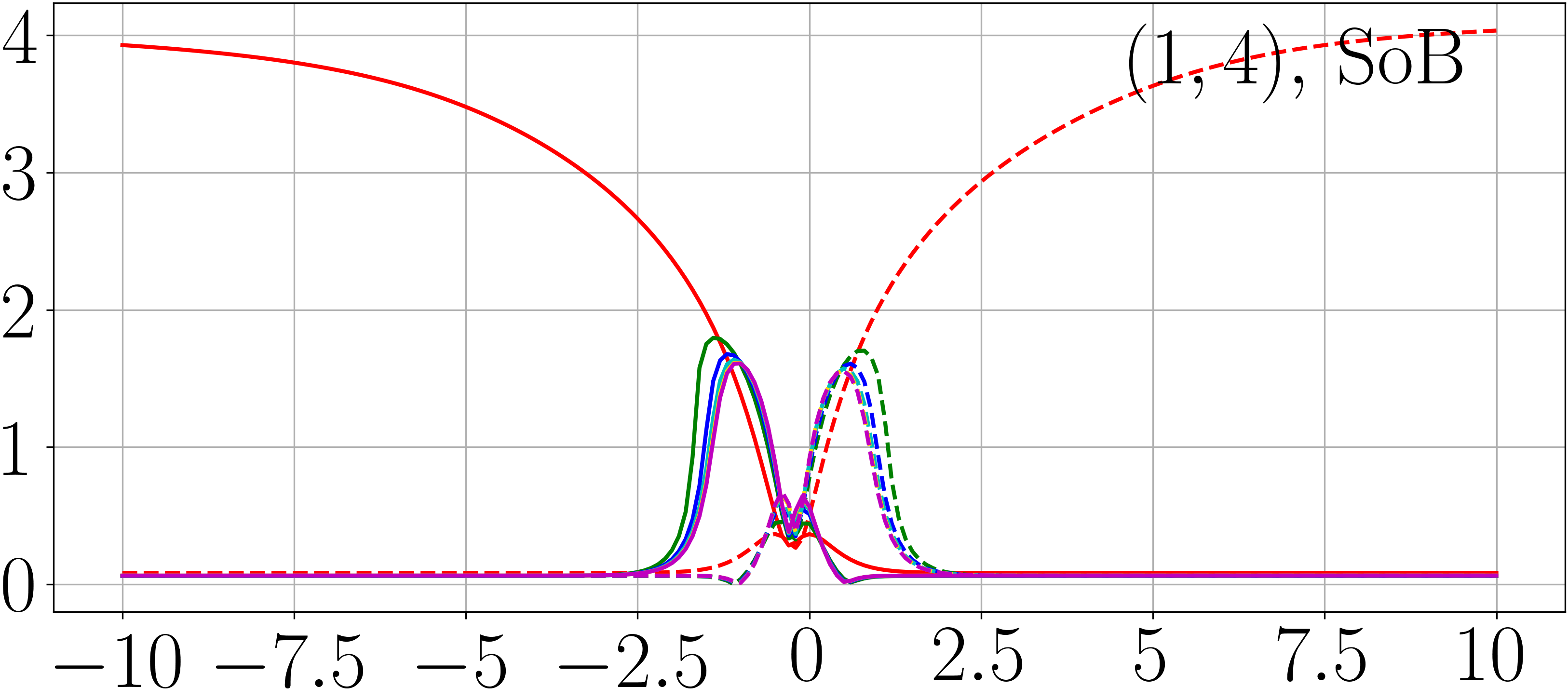

We consider the task with the zero-one task loss . With the correctly-specified model (20), we calculated with a training sample of size and evaluated the size of bias (SoB) and test task risk (TTR) (i.e., misclassification rate) with a test sample of size , for LR, MLSLR with , and LSQLR. Note that it makes no sense to compare the test surrogate risk (TSR) for different surrogate losses. We trained the model parameter using (batch-version) Adam with learning rate that is multiplied by every 50 epochs from 0.01 for 150 epochs, from the initial point for LR or together with multi-start strategy with 30 initial points scattered from for MLSLR and LSQLR. Figure 2 shows some of the results on the mean and standard deviation (STD) of the errors over 100 randomized trials.

Consequently, similarly to the ARE results in Table I, it was also experimentally confirmed that parameter estimation performance with the correctly-specified model decreased along with increase of the smoothing level even when the sample size is small (see mean of SoB in Figure 2). Along with this behavior, TTR for MLSLR and LSQLR also deteriorated.

III-C Robustness against Model Misspecification

III-C1 Similarity to Existing Robust LRs

Use of a loss function that leads to low efficiency with correctly-specified models may be motivated by expectation for robustness against model misspecification, as also suggested by [17]: One may want to make the estimation result stable even when the data distribution deviates from the specified model. Various studies have confirmed that LR lacks robustness against model misspecification [18], and then proposed robust LRs via the idea of -transformation (see below) of the loss function [19, 15, 20]; See also the monograph [21, Chapter 7.2].

[19] proposed to use a -transformed loss

| (21) |

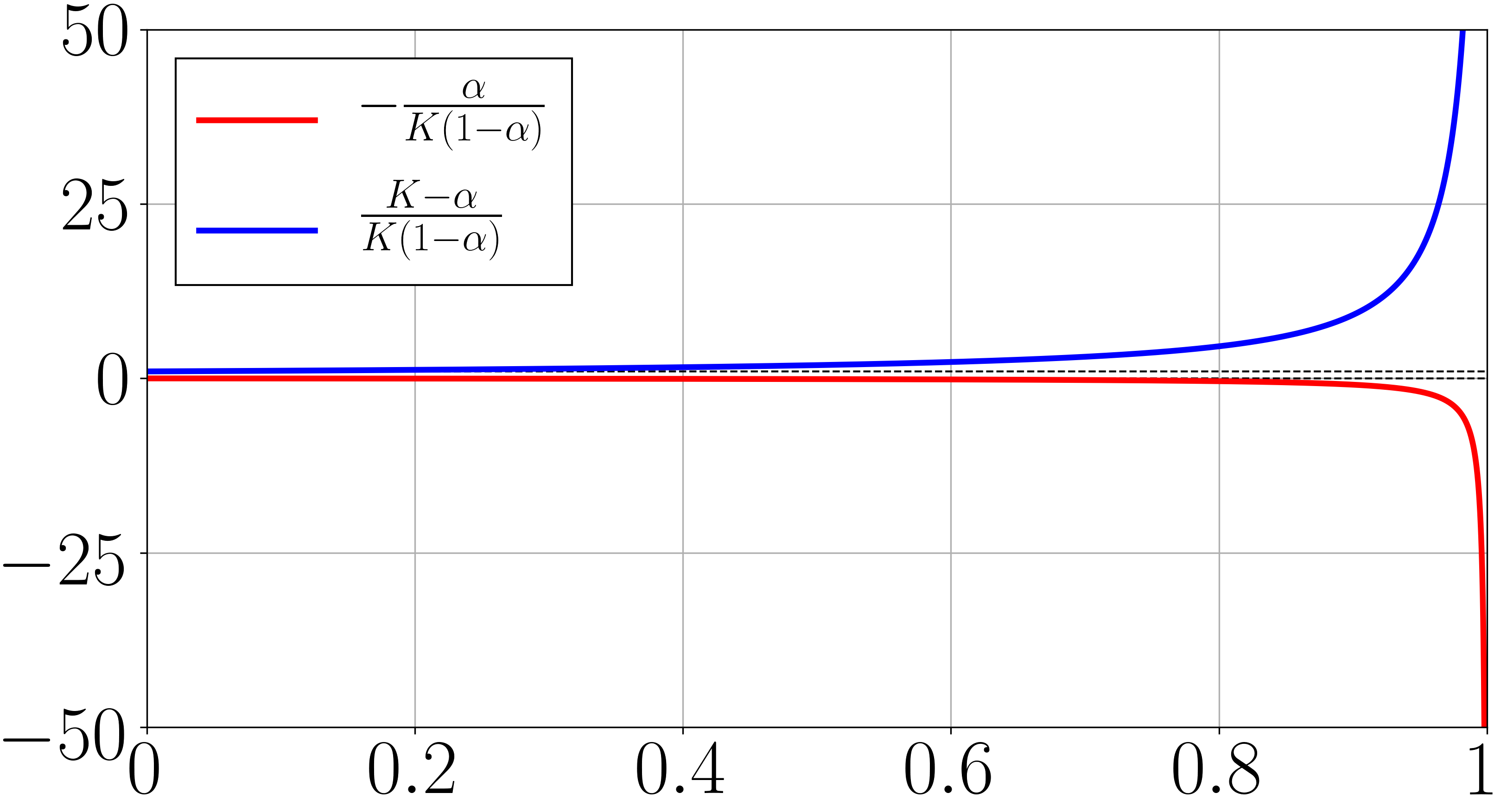

where is a function with sublinear growth (e.g., (if ), (if ) with some constant , inspired by a Huber-type loss). However, his robust estimator based on is not consistent even with correctly-specified models, and it has been pointed out that it is not sufficiently robust against outliers [22]. Thus, seeking a robust LR with consistency (having a guarantee like Corollary 1), [15]444They originally defined their estimator by the loss function (22) where (if ), (if ) with some constant , and where . The form (23)–(24) in the body is that our study derived so that it follows the unified formulation through the -transformation (21). found the following -transformation:

| (23) |

that is non-decreasing in and bounded, where

| (24) | ||||

Also, [20] used, besides a data-weighting scheme similar to [23], (if ), (if ) instead of in the formulation (22), yielding an increasing and bounded -transformation .

|

|

|

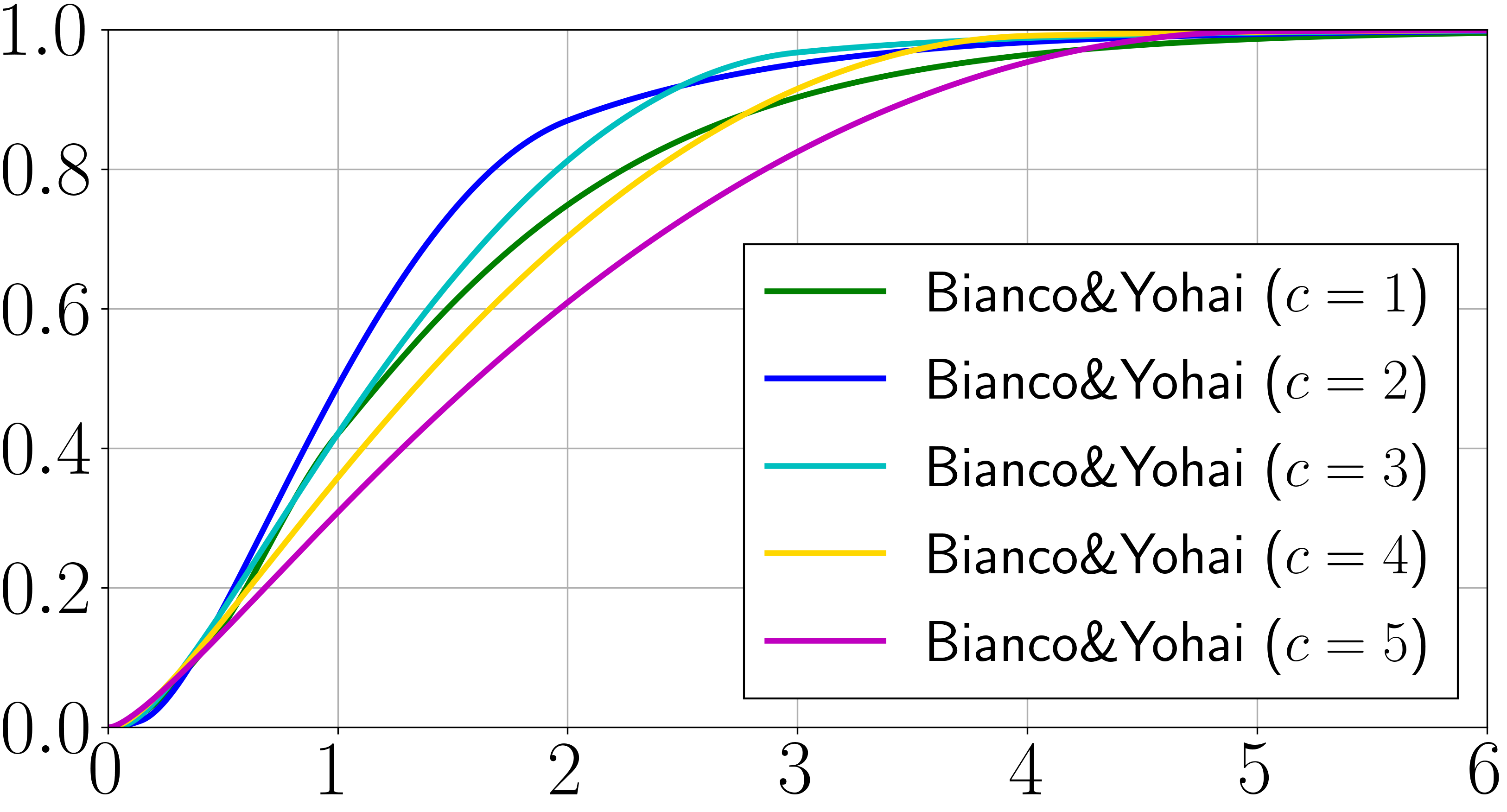

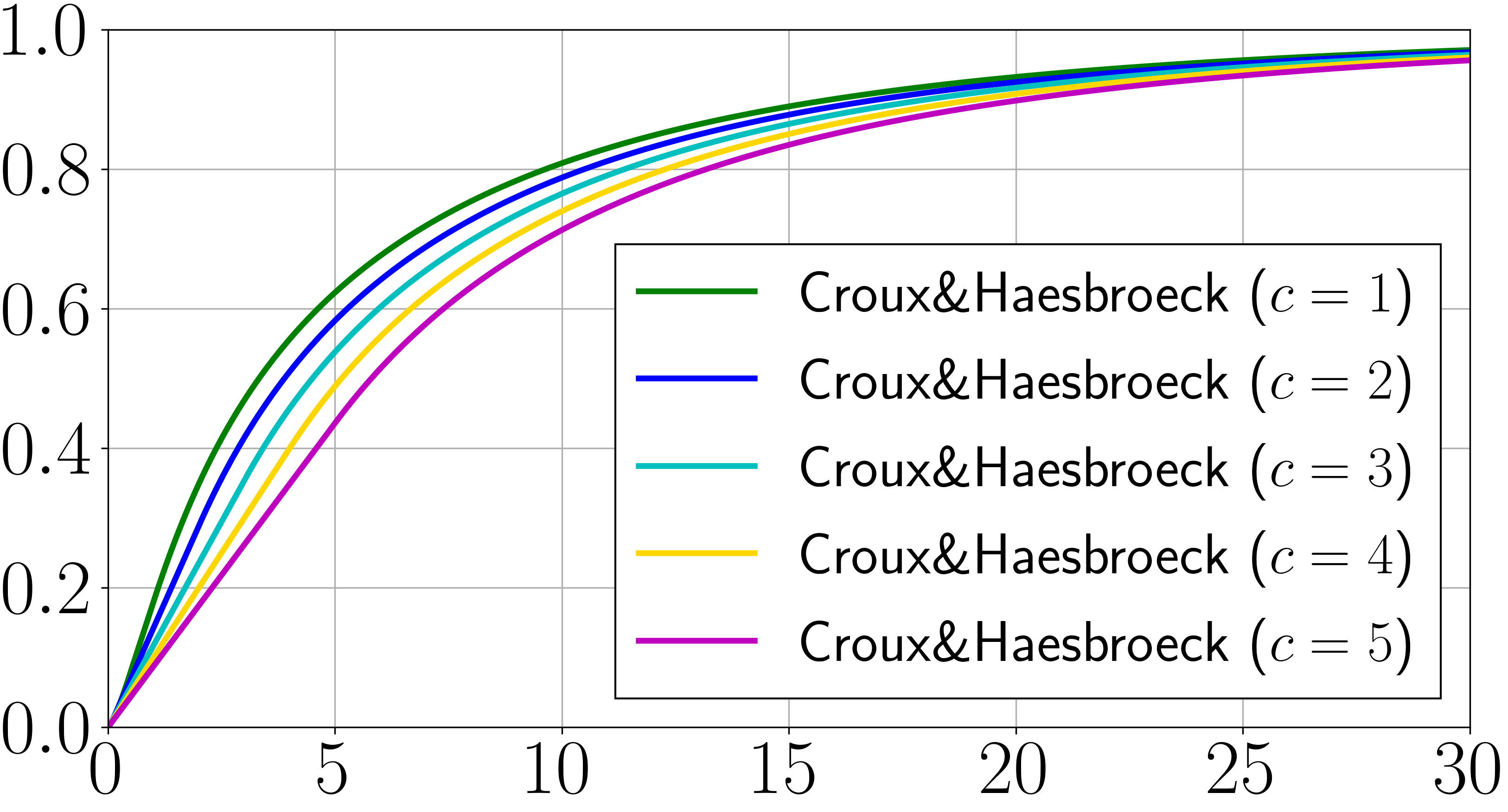

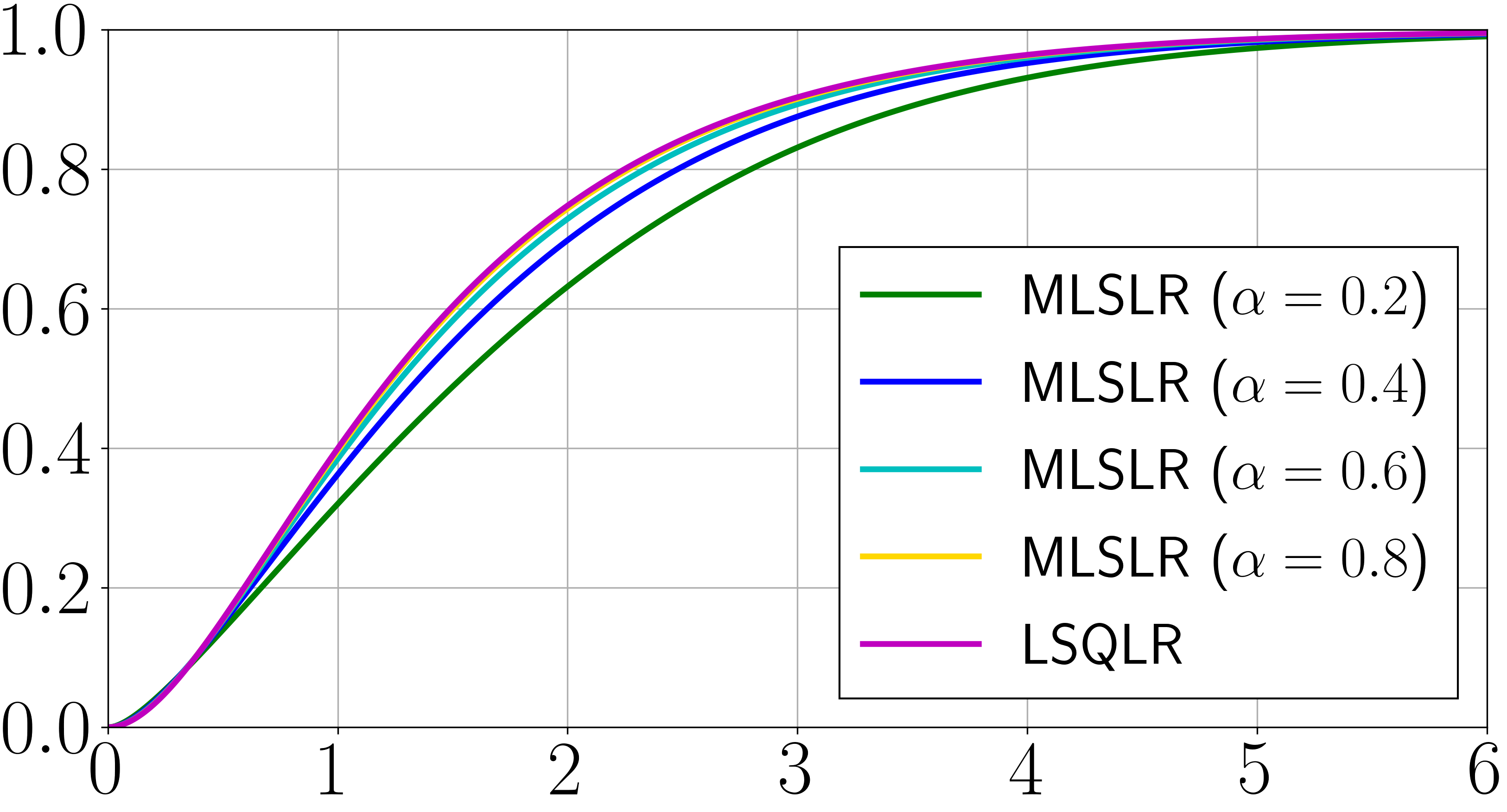

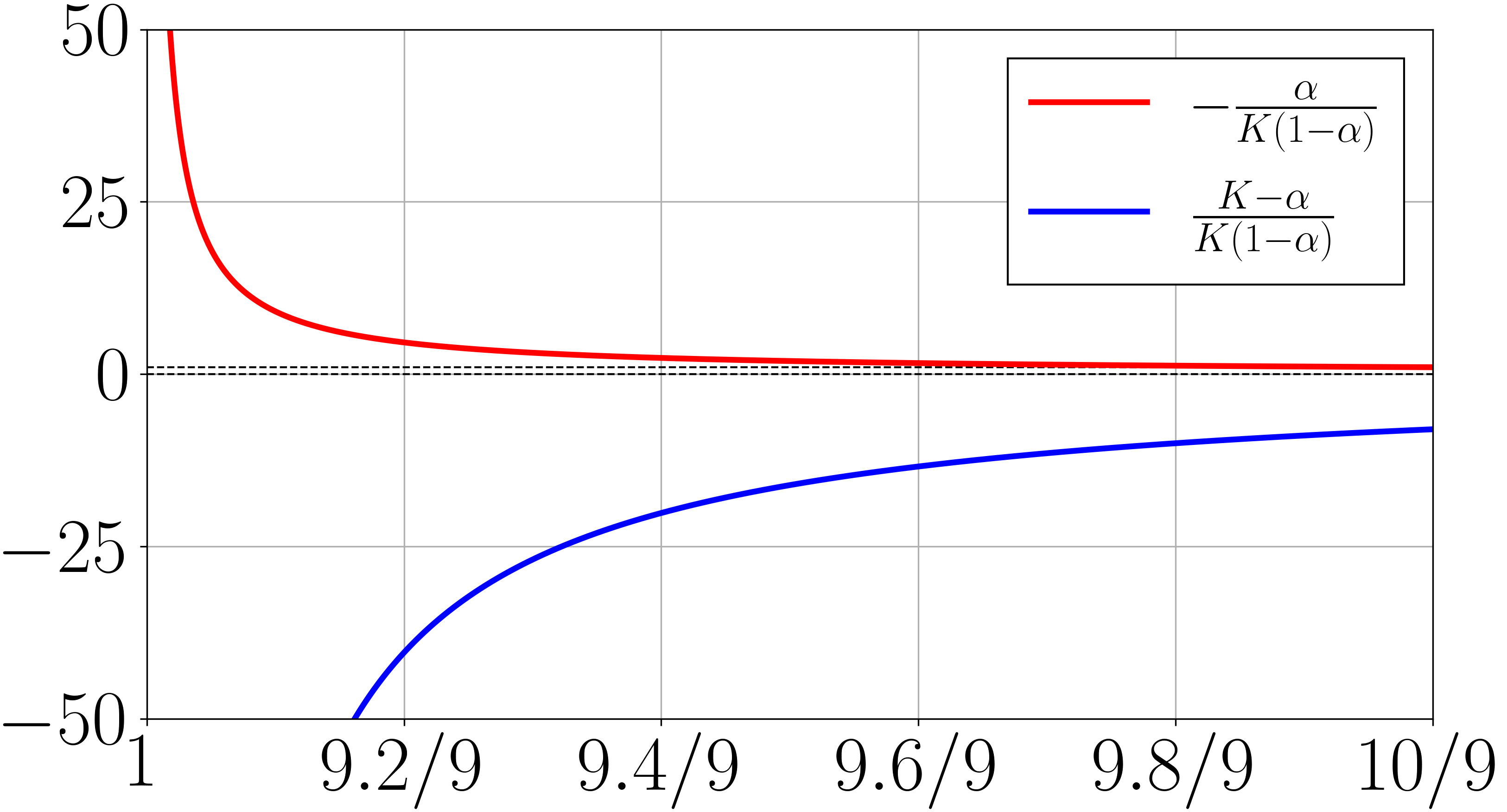

Our observation here is that MLSLR and LSQLR can be regarded as instances of -transformation-based robust LR, with

| (25) | ||||

Both of these transformations are increasing (in ) and bounded. This property and Figure 3 show close similarity of MLSLR, LSQLR, and the existing robust LRs by [15, 20], which will suggest the robustness of MLSLR and LSQLR.

III-C2 Simulation Experiment

In robust statistics, it is common to study the performance of an estimator under (point-mass) data contaminations, which cause model misspecification. The discussion in this section follows that approach.

We introduce the -valued functional , defined on the space of probability distribution functions of random variables , that represents the procedure of the surrogate risk minimization:

| (26) |

where the expectation is taken with respect to . Now, we are interested in behaviors of the estimate for the contaminated distribution

| (27) |

where is a nominal distribution of such that implying , and is a small ratio.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

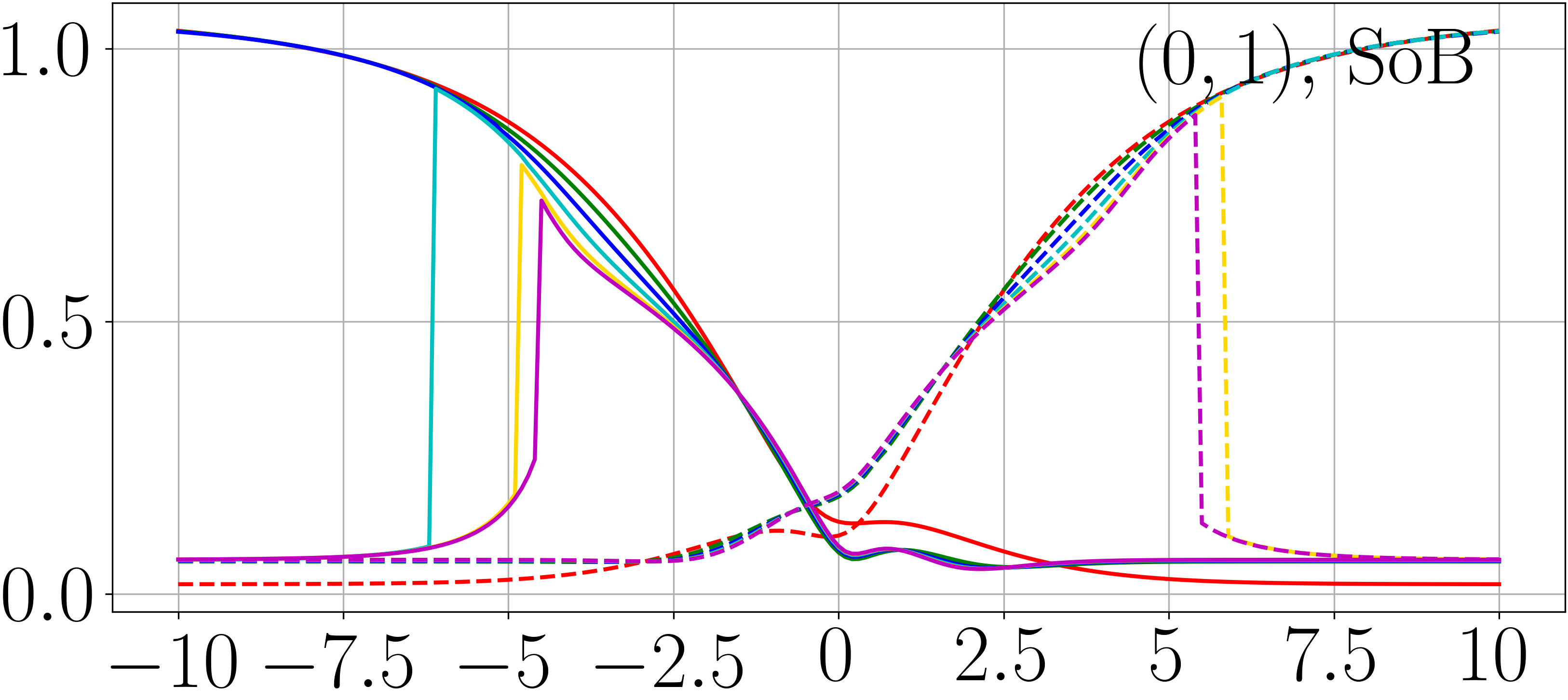

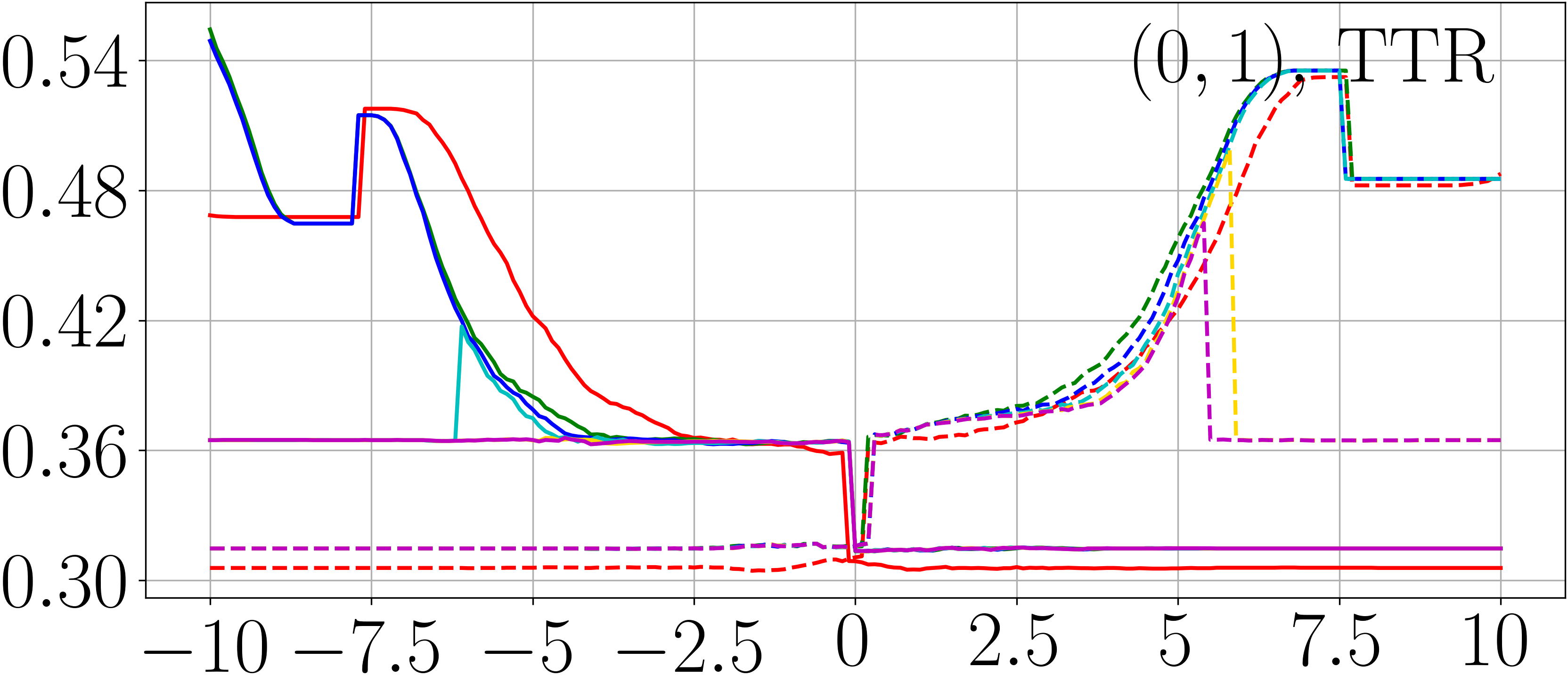

Although theoretical discussion to guarantee the robustness of an estimator often adopts the notion of ‘breakdown point’ (), it has been known that it does not bring about meaningful results in the context of binary classification; For example, [24, Theorem 1]555[24, Theorem 2] discussed an unconventional version of breakdown point () too, under the linear learner class . However, such breakdown is different from the situation in which the largest logit takes a quite large value, which is regarded as a trouble in studies on LS. Also, it does not provide suggestions for cases where flexible models such as a neural network model are used, because it can occur depending heavily on the linearity of the learner. This paper thus adopts only the conventional version of the breakdown point. states that the breakdown (in the above-mentioned sense) in the finite-sample situation will not happen even for LR, which is in conflict with the observed instability of LR as confirmed by [18]. Due to such difficulty in theoretical discussion, we study the robustness by resorting to a simulation experiment here. The focuses of this experiment are to see if MLSLR and LSQLR actually make LR robust and how the choice of smoothing level affects the robustness of those methods.

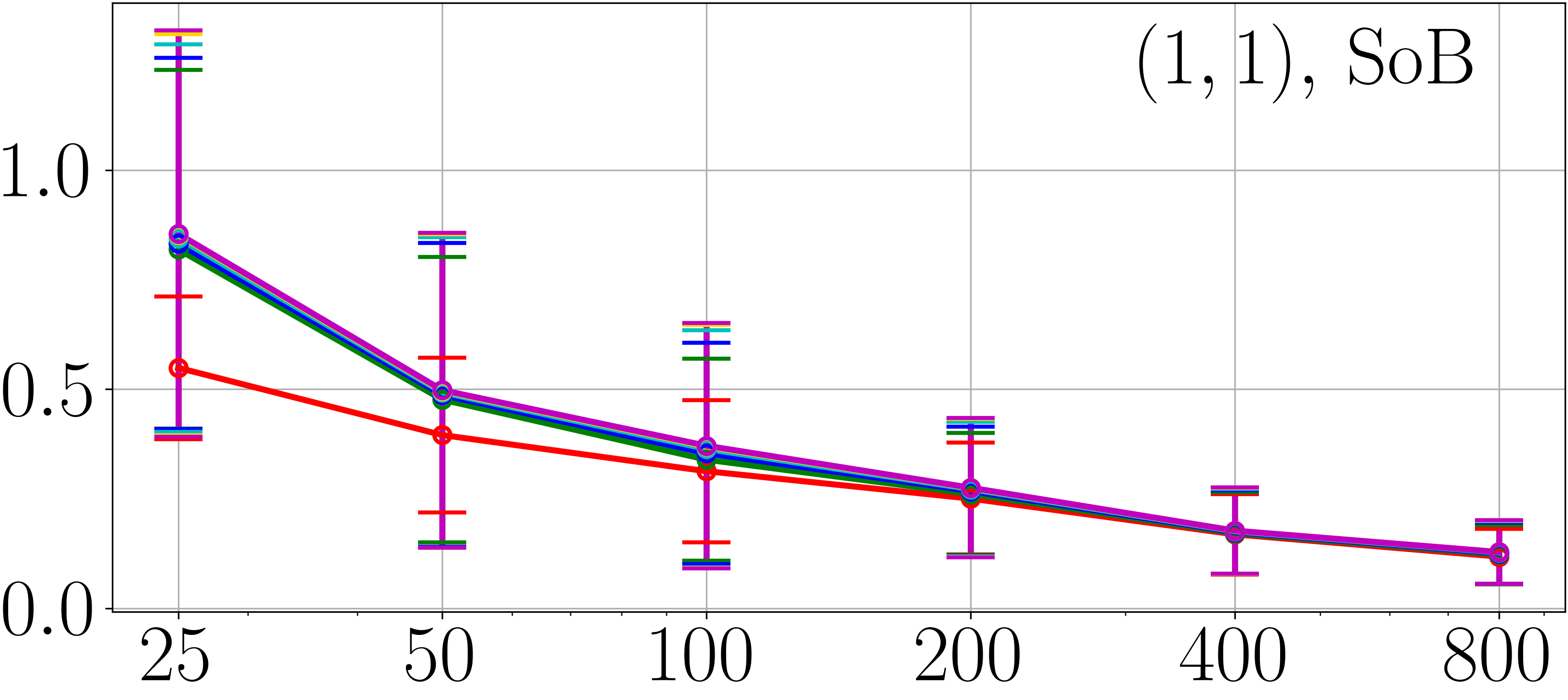

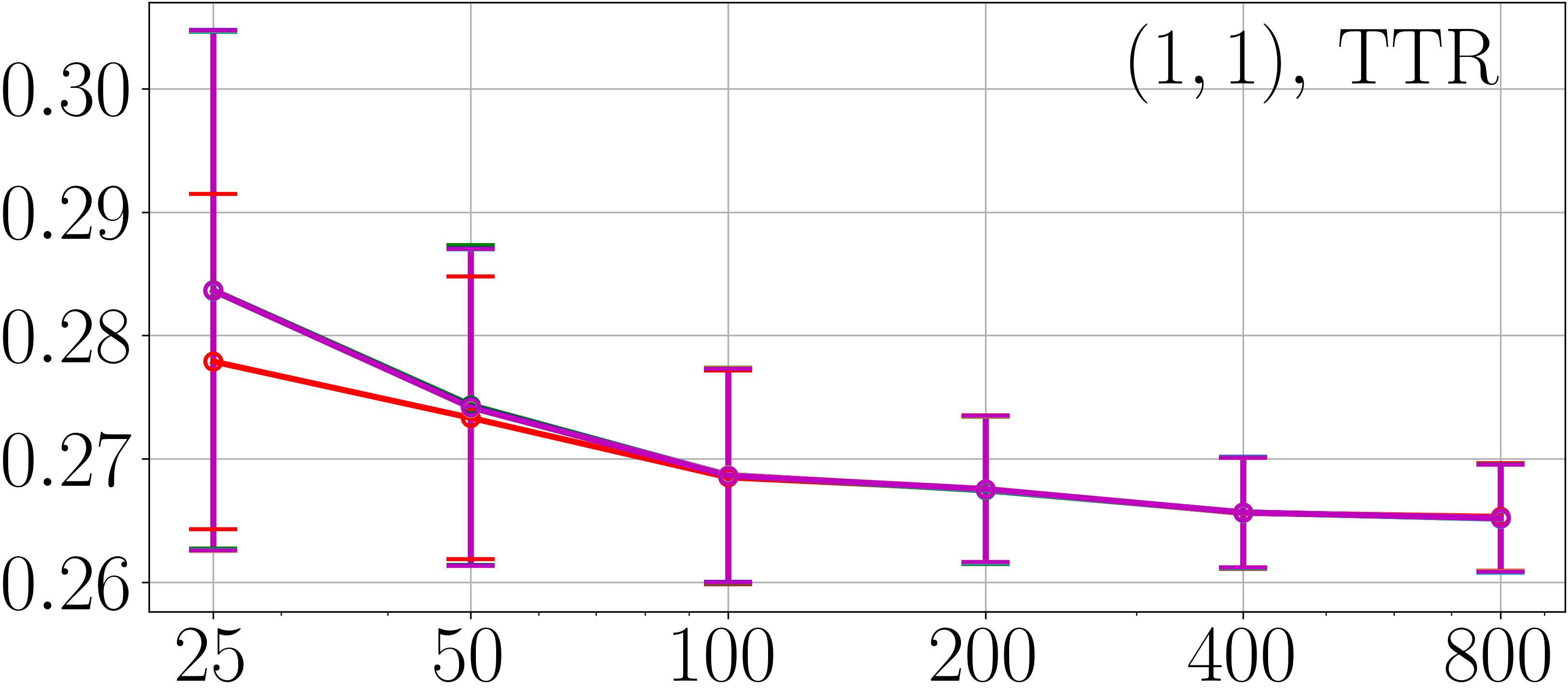

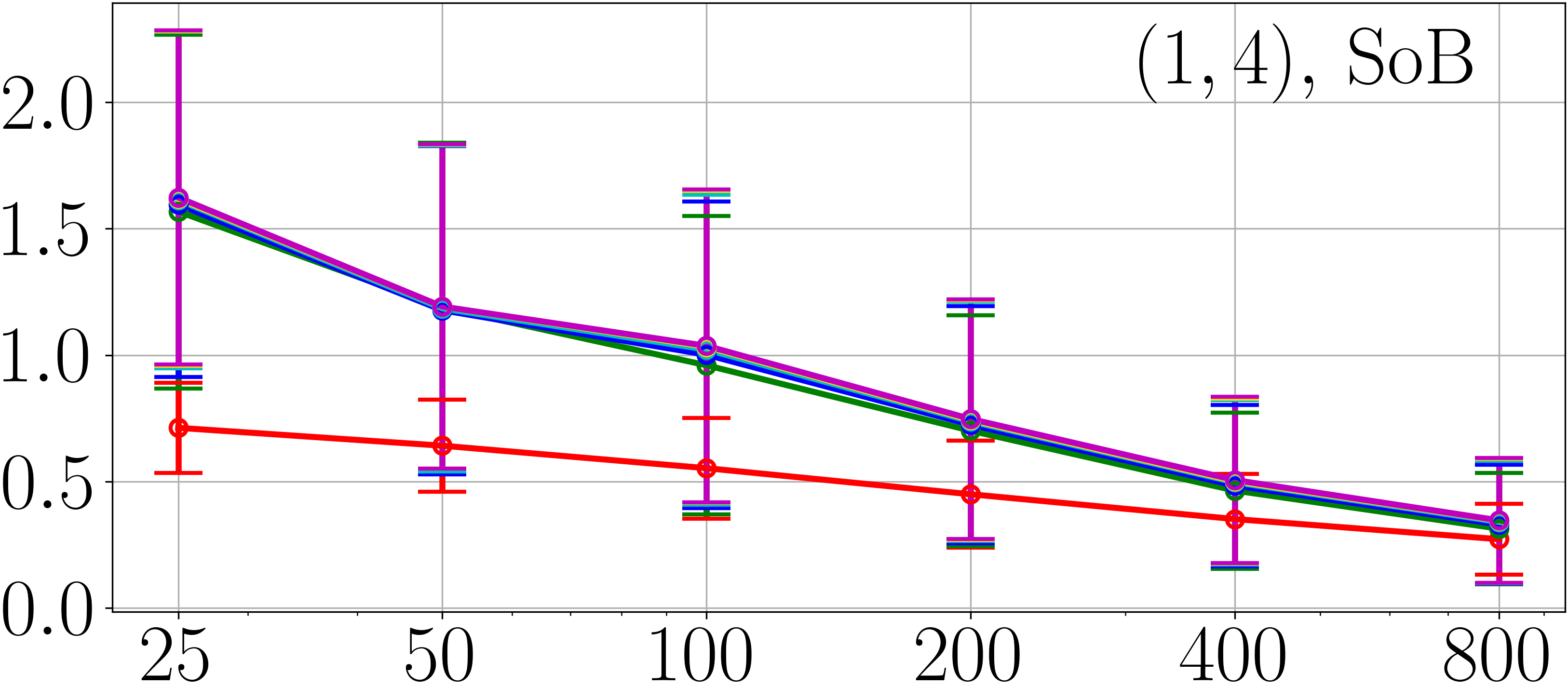

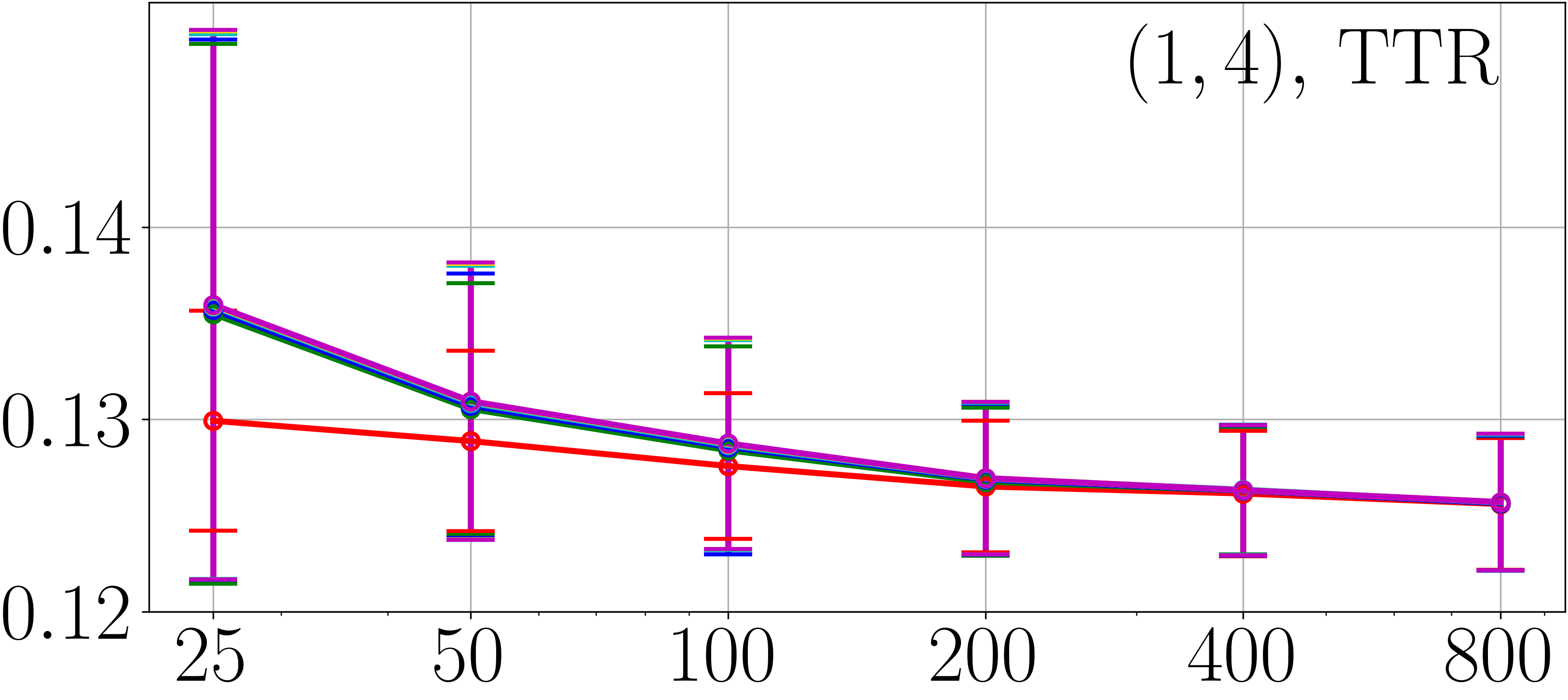

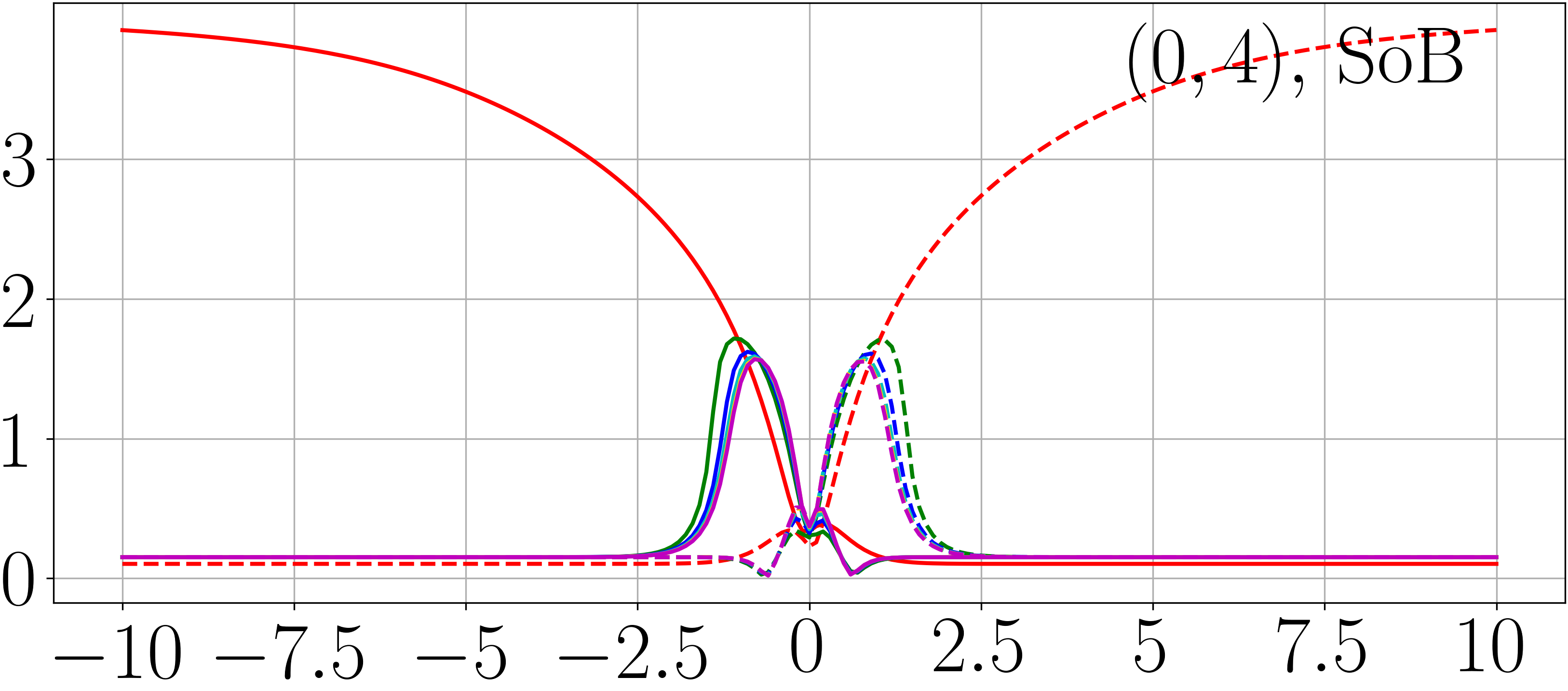

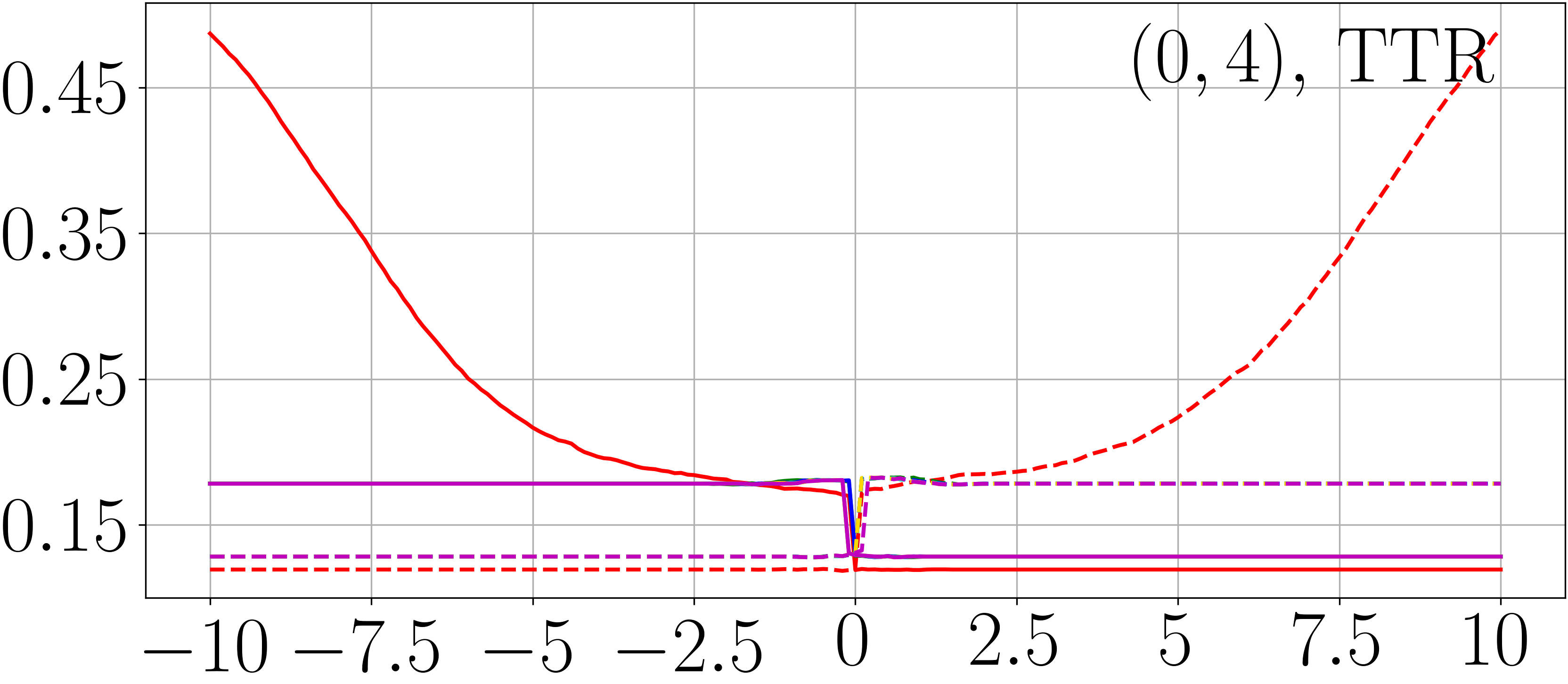

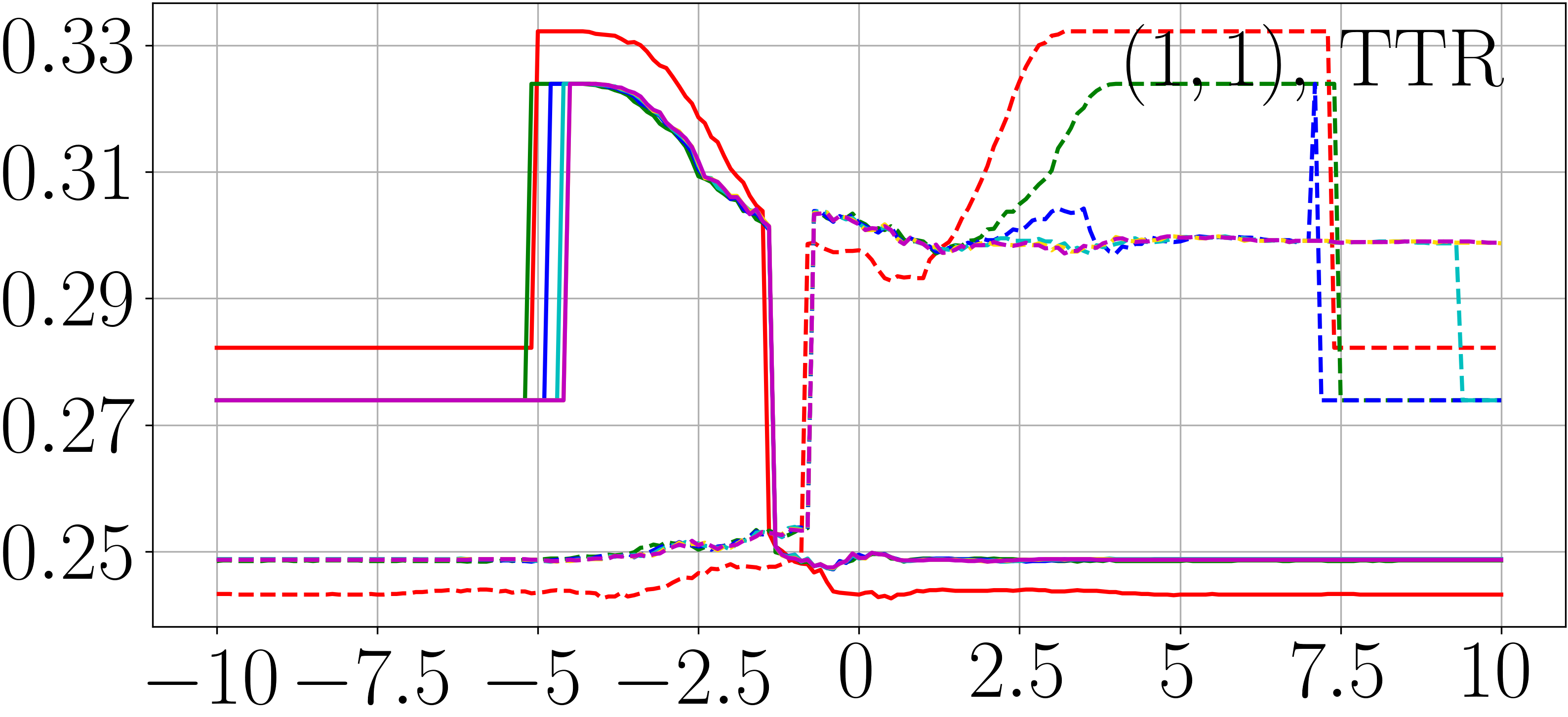

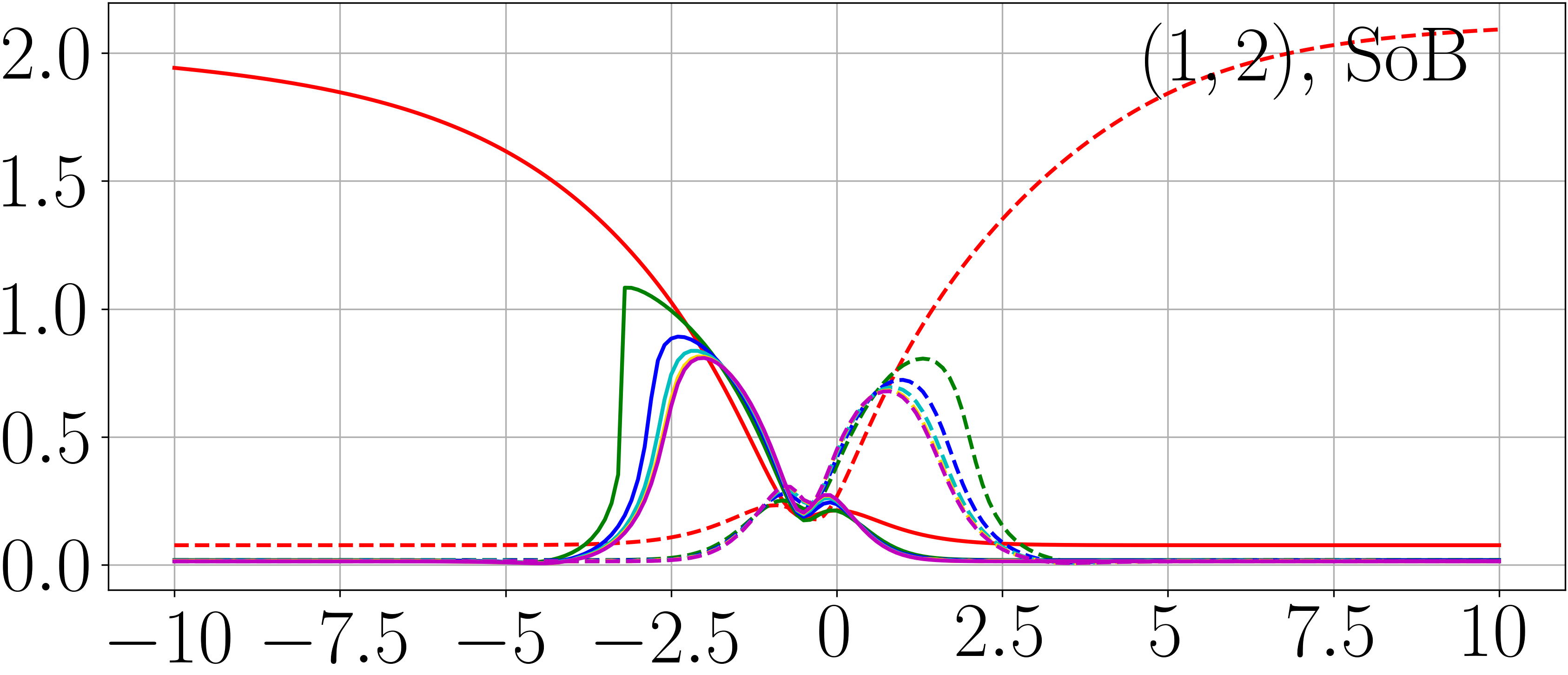

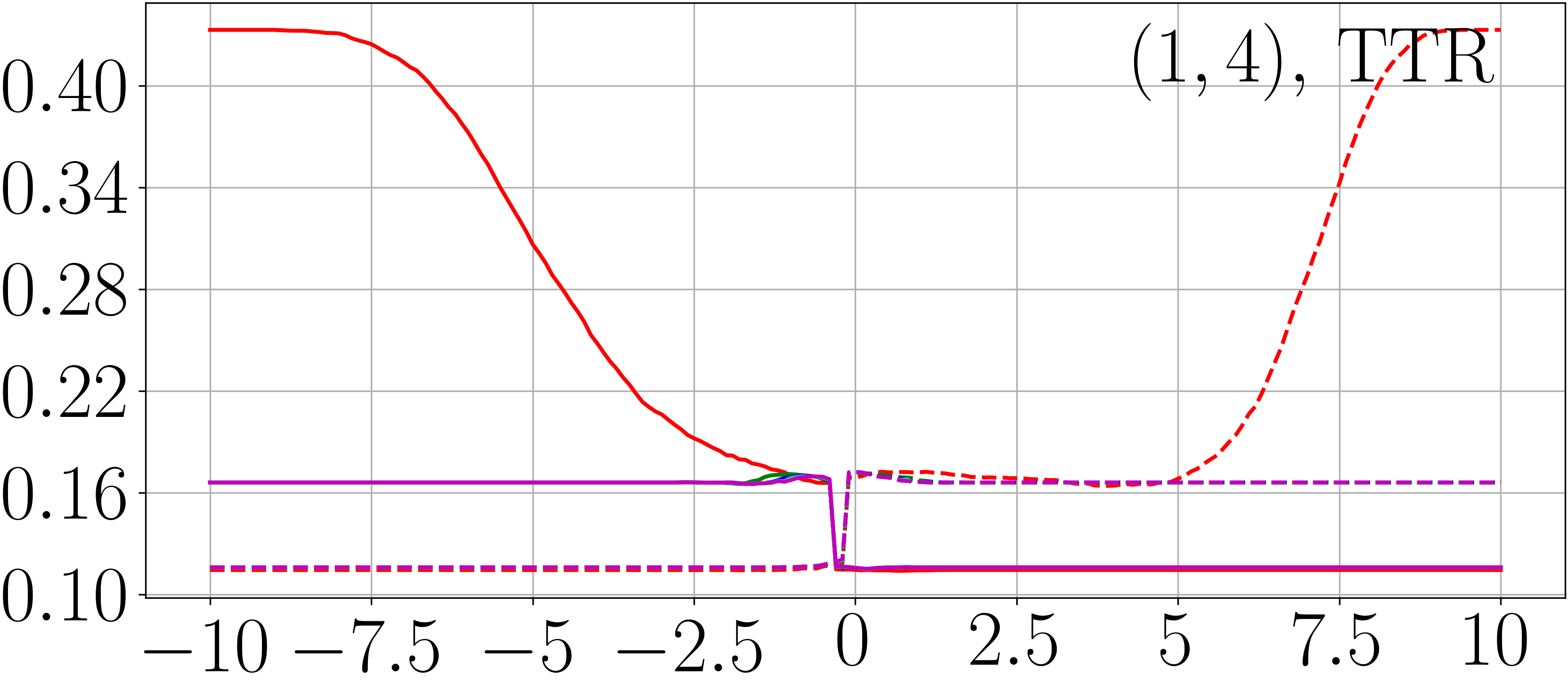

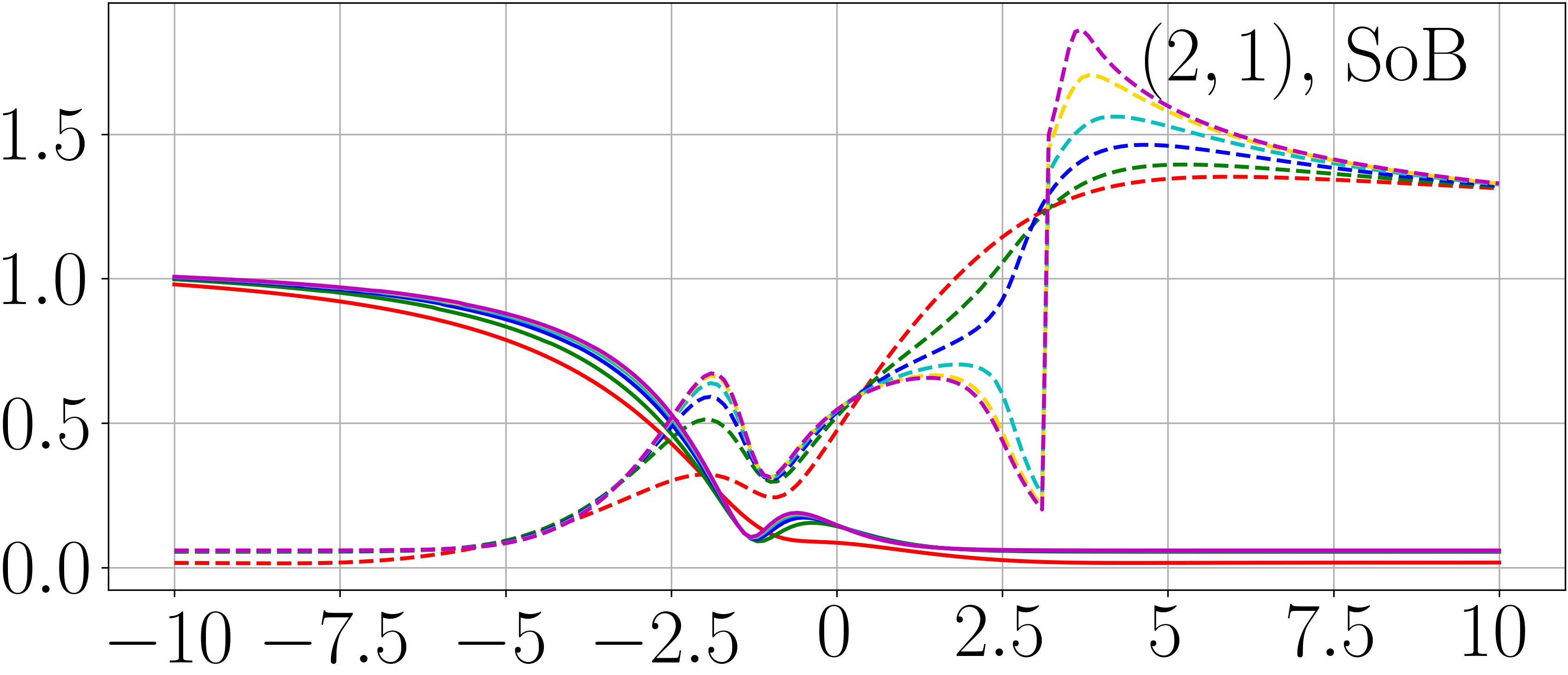

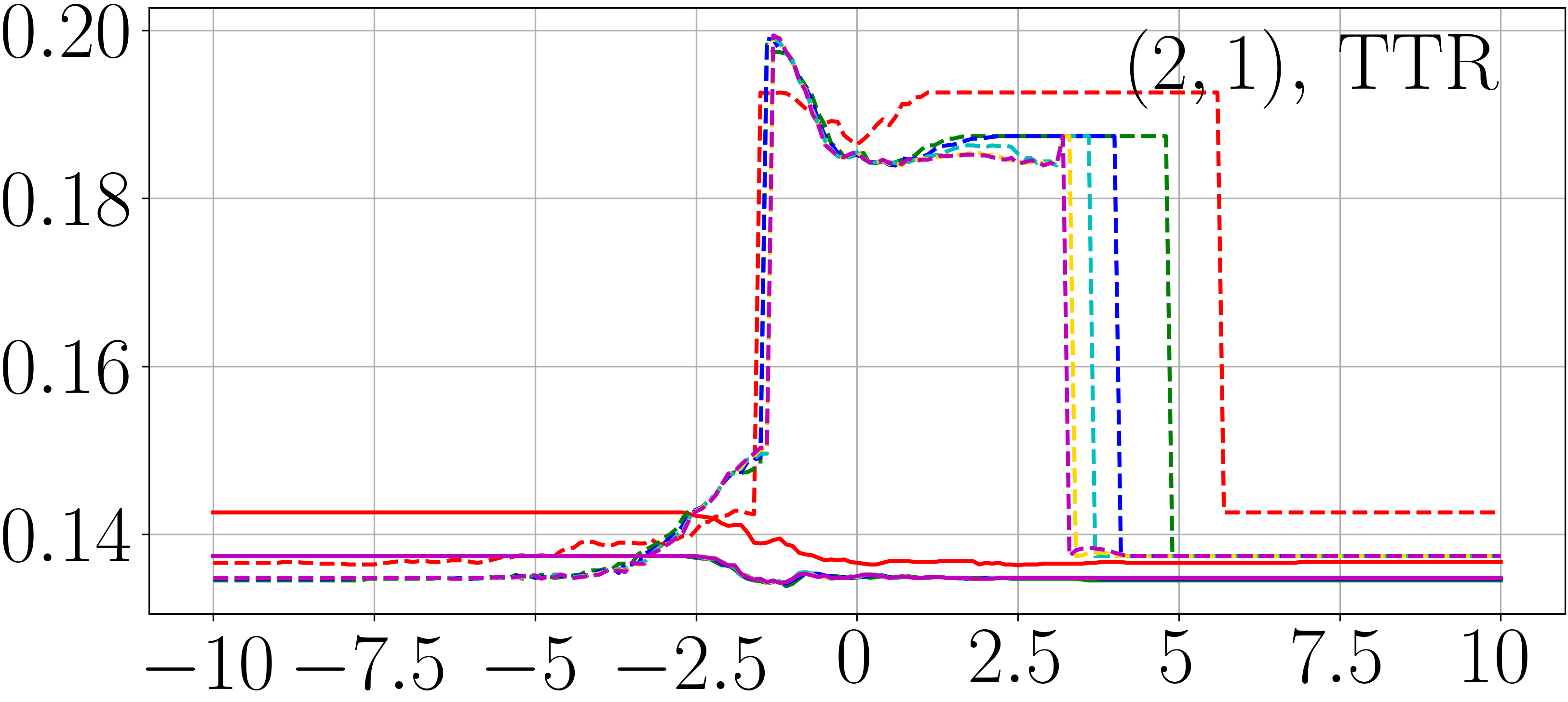

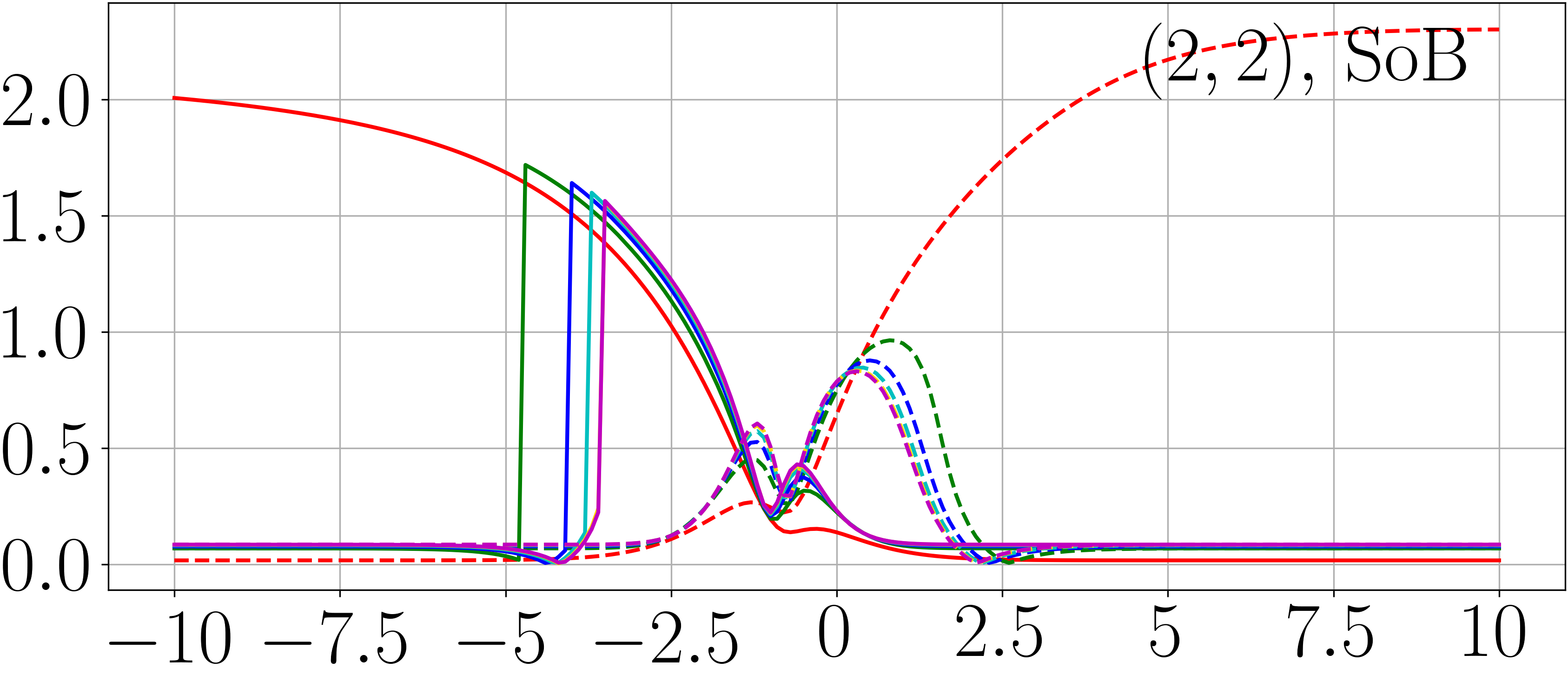

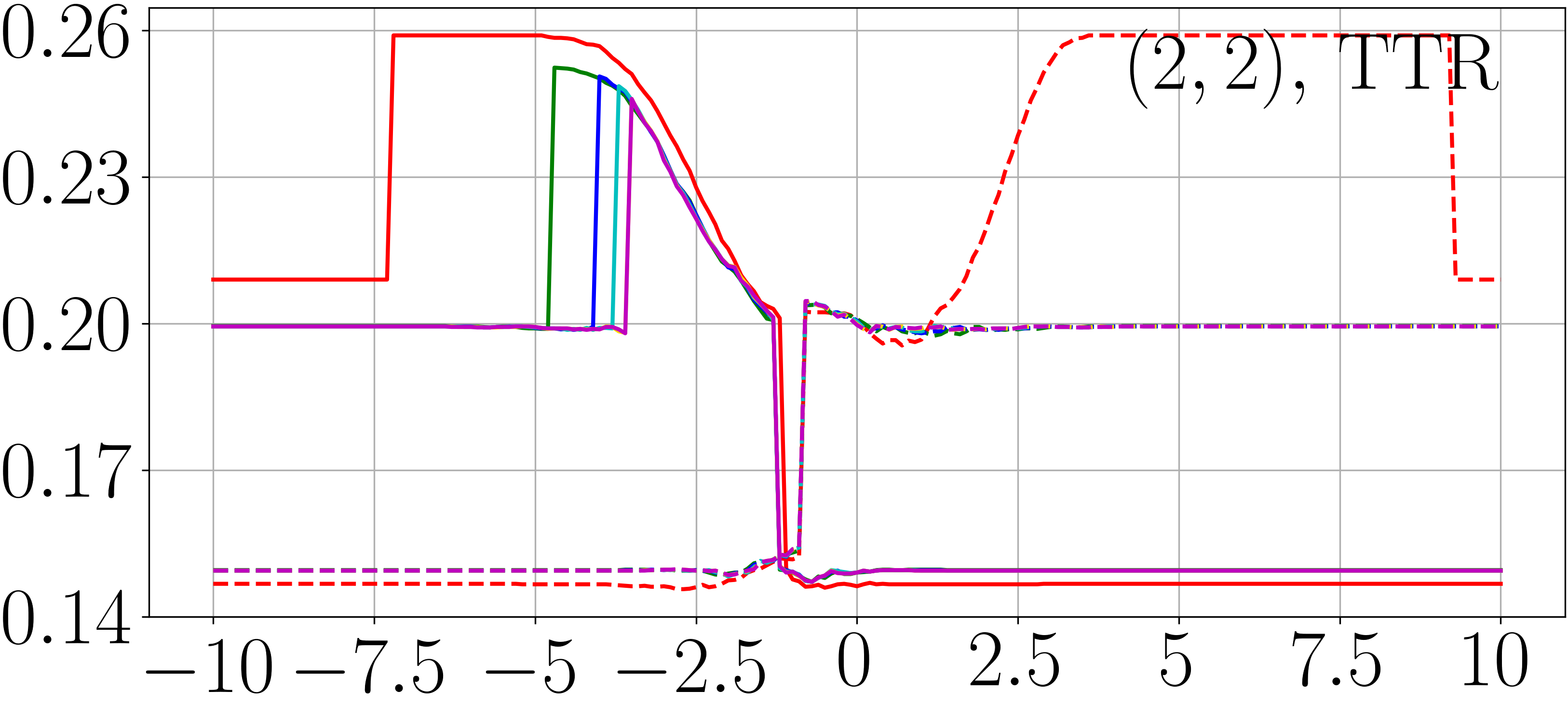

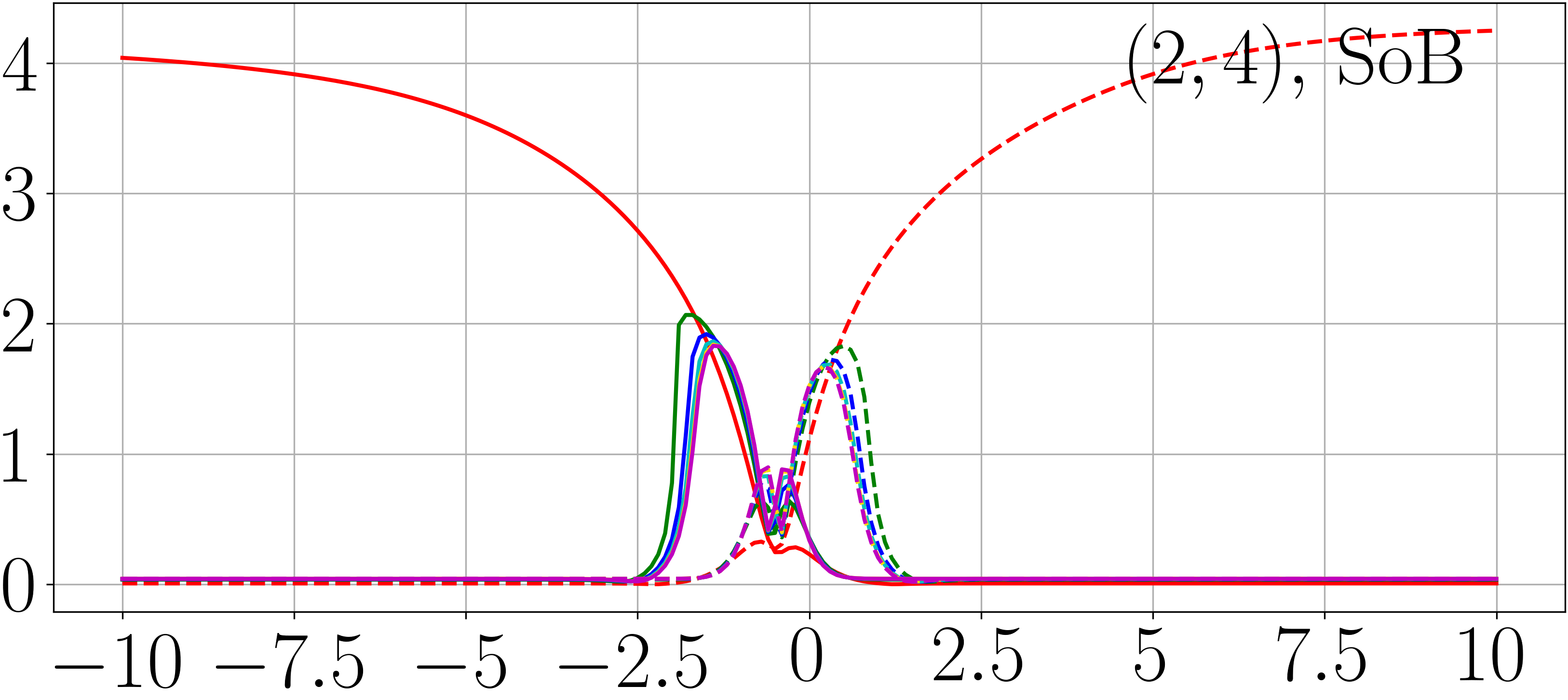

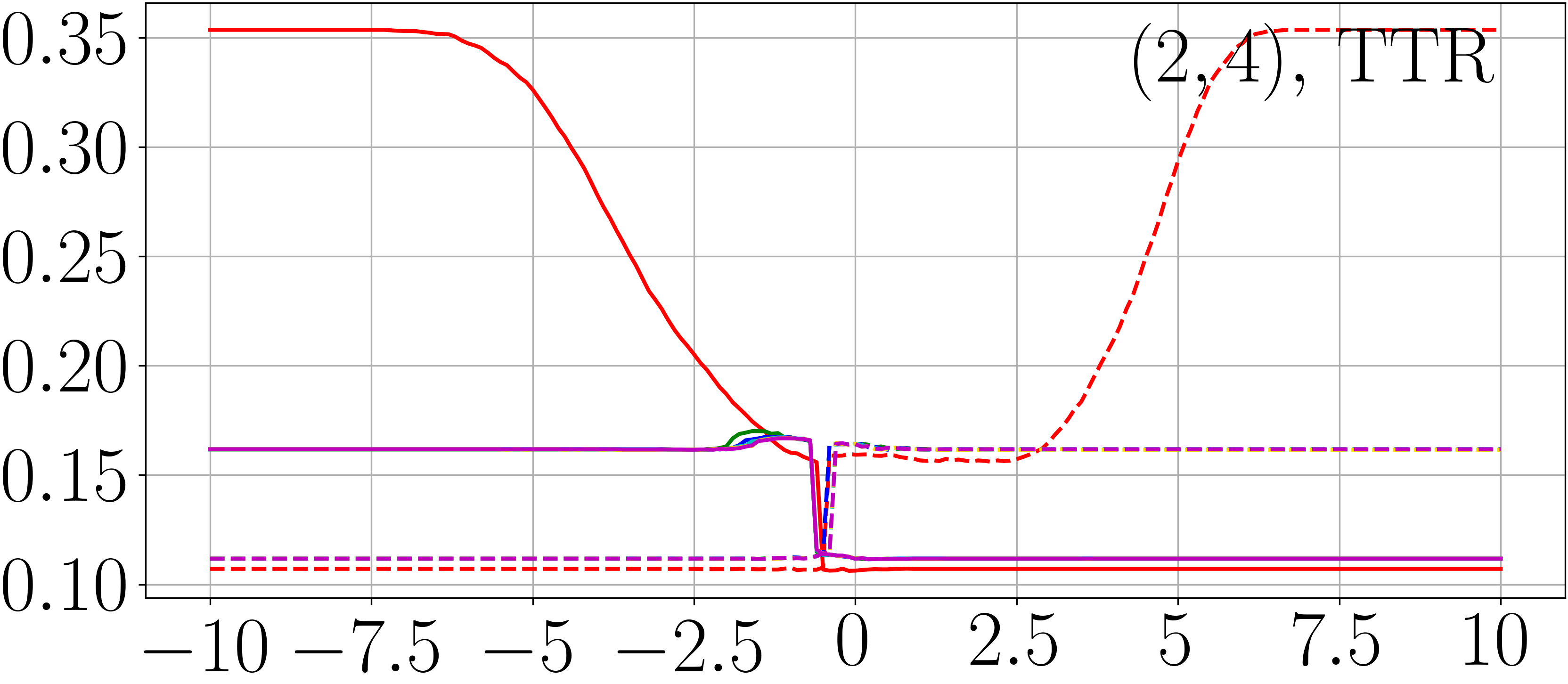

We consider the setting with the task with the zero-one task loss , the nominal distribution given by (20), and the point-mass contamination of , (), and . We could not find a closed-form representation of , so we estimated it with a sample from of sufficiently large size such that the resulting variance gets negligibly small (denote it ). We calculated with a training sample of size and evaluated SoB and TTR with a sample of size (both samples follow the distribution (27)), for LR, MLSLR with , and LSQLR (by 1 trial). We trained the model parameter in the same way as one in Section III-B2. Figure 4 shows some of the results.

Using a larger smoothing level tended to improve SoB and TTR for many ’s that are so anomalous for (20) that gets quite small (in the setting with larger ). This result indicates that LS greatly robustified LR with larger . Also, the improvement of TTR was larger than that of the experiment in Section III-B2, which clarifies that LS is promising for better classification performance.

IV Experiment: LSLR versus MLSLR

In this section, so as to study the significance of LSLR using a consistent probability estimator different from LR and MLSLR, we perform an experimental comparison between LSLR and MLSLR that respectively apply probability estimators based on the R-logit model and the logit model, while using intrinsically the same (surrogate) loss functions based on the SKL-divergence for probability estimation. Several previous works claim that squeezing of the logits in LSLR (see Theorem 1, B6) works as regularization and is an advantage of LS. Recalling the contrasting property that the logits of MLSLR can output quite large values (see Theorem 1, B5), if this claim were correct, LSLR would perform better than MLSLR. The experiment will test whether a regularization mechanism based on logit-squeezing actually works.

Once LSLR and MLSLR select a (common) model class (e.g., the network architecture), optima of their surrogate risk will be different. In order to reduce such a difference stemmed from the lack of representation ability of the model and focus on their estimation performance, we perform an experiment with a large-size learner model, unlike those experiments in Sections III-B2 and III-C2.

Following the experiments by [3] with the CIFAR-10 dataset, we trained LR, LSLR and MLSLR with , and LSQLR based on ResNet-18 architecture (while we did not use the weight-decay [25] in the implementation of [3]) with the training sample of size , and evaluated TSR and TTR (where ) with . We trained each model for 150 epochs using the Nesterov’s accelerated SGD similar to [3], and adopted a model at the point in time when each test risk achieved its minimum among those evaluated at the end of each epoch. The results for 20 trials are summarized in Table II (mean and STD of TTR for LR and LSQLR were and ). Note that it is meaningless to compare TSRs for different ’s, and we compare TSRs or TTRs of LSLR and MLSLR with the same or TTRs with the different ’s.

| LSLR (upper) and MLSLR (lower) | ||||

|---|---|---|---|---|

| TSR | ||||

| TTR | ||||

| LSLR | |||||

|---|---|---|---|---|---|

| training | OPDER | ||||

| OPER | |||||

| MSoR | |||||

| test | OPDER | ||||

| OPER | |||||

| MSoR | |||||

|

|

The R-logit model , a consistent probability estimator of LSLR, has an unnecessarily larger range than that of the CPD function , (see Theorem 1, B1 and Figure 5). This fact can be interpreted as learning a probability estimator from an unnecessarily larger hypothesis space, and we consider that it may prevent proper learning and degrade prediction performance of LSLR, in contrast to the positive statement by existing studies for the logit-squeezing. To evaluate the degree to which the R-logit model deviates from the probability simplex, we calculated the following three criteria: Table III shows outlier probability distribution estimate rate (OPDER)

| (28) |

outlier probability estimate rate (OPER)

| (29) |

and mean size of residual (MSoR)

| (30) |

evaluated for training and test (with instead of ) sets at an epoch with the minimum TSR, where .

Comparing TSRs or TTRs of LSLR and MLSLR with the same (see Table II), it can be seen that the modification of the consistent probability estimator or squeezing of the logits does not help to improve the probability estimation and classification performance. Rather, MLSLR had stable and better performance in many cases. Table III indicates that the R-logit model of the LSLR often, and greatly for larger , deviates from the probability simplex, as Theorem 1, B1 and Figure 5 also suggest. This result is coherent with the fact that the TTR of LSLR is much worse than that of MLSLR for large , and supports our hypothesis about the trouble of LSLR. These observations and considerations are novel findings and recommend MLSLR over LSLR when one uses a large-size learner model.

Besides, the best method with respect to the TTR was MLSLR with an intermediate smoothing level . Although this result is apart from the preset purpose of the experiment in this section, it is also notable and can be understood from the trade-off between efficiency and robustness discussed in Sections III-B and III-C: Even a large-size neural network model () cannot completely represent the optimal solution (), and due to such deviations (model misspecification), robustification by LS would have contributed to improve the probability estimation and classification performance.

V Conclusion and Future Prospect

This paper has proposed the loss view, that LS adopts a loss function different from that of LR, in contrast to the regularization view, that LS is a sort of regularization techniques, adopted in most existing studies. This loss view will also provide theoretical generalization analysis of LSLR; See Appendix E. Also, we introduced MLSLR, for fair comparison with LR, that adopts the same logit model as a consistent probability estimator. Previous studies have stated

- A4.

-

A5.

LS is competitive with loss-correction techniques under label noise [27].

-

A6.

LS can help to speed up the convergence of SGD by reducing the variance [28].

but they regarded the inconsistent logit model as a probability estimator of LSLR, which does not result in a fair comparison with LR. Thus, it may be still meaningful to re-consider these statements in the introduced alternative view, coupled with the fact that MLSLR provided better probability estimation and classification performance than LSLR when they depend on a large-size neural network model.

In Sections III-B and III-C, we showed that MLSLR and LSQLR are less efficient but more robust than LR: This tendency becomes more pronounced as the smoothing level is increased. As demonstrated in Section IV, the selection of the smoothing level controls the trade-off between efficiency and robustness and is practically important for better classification performance. For example, [29] studied and proposed covariate-dependent adaptation of the smoothing level: it decides the smoothing level locally according to an estimated maximum conditional probability and estimated marginal distribution of the covariate. Also, [30] adopted target-dependent adaptation of the smoothing level, so called non-uniform LS. The trade-off that we have discovered may lead to a more sensible selection of the smoothing level.

Since the SKL divergence, on which LS is based, is a divergence that provides a robust statistical procedure, it may also be associated with another class of robustifying divergence, such as density power divergence [31, 32, 33]. Also, although entropy regularization techniques [34, 35] actively used in reinforcement learning would be more difficult to express its corresponding loss function or divergence in a closed form and theoretically analyze them, it might be able to interpret them and other similar logit-squeezing [36, 37] as robustification in the same way as LSLR. These related topics are the subject of future work, and these methods have potential to be improved like MLSLR against LSLR.

Appendix A Proof of Theorems 1 and 2

First, we present a proof of Theorem 1.

Proof of Theorem 1.

The method of Lagrange multiplier,

| (31) | ||||

shows that the optimal solution is determined to as far as . This result and prove B3.

On the basis of the calculus of the second derivatives of in , that is, for s.t. ,

| (32) | ||||

one has that, for ,

| (33) |

which clarifies the statement B4.

Next, we prove Theorem 2.

Proof of Theorem 2.

Taylor expansion for with a small absolute value shows

| (34) | ||||

when . ∎

Appendix B Generalized Version of Corollaries 1 and 2

This section describes the generalized version of Corollaries 1 and 2 for the multi-class settings (), cost-sensitive tasks (), and .

For an -valued learner, the surrogate loss function for LR, LSLR, MLSLR, and LSQLR can be represented as

| (35) | ||||

Then, one has the following results:

Proposition 1.

Assume , and let . Then, regardless of the distribution of , a.s. for LR, MLSLR, and LSQLR, and a.s. for LSLR.

Proposition 2.

Assume , and let . Then, regardless of the distribution of , satisfies for LR, MLSLR, and LSQLR, and satisfies for LSLR.

Theorem 1, B3 shows Proposition 1, and Proposition 2 is trivial from Proposition 1, considering the form of the task risk, . Also, one has to pay attention to the labeling function of LSLR with even for the task with the zero-one task loss .

Corollary 3.

Under the assumption of Proposition 2, for LR, LSLR with with , MLSLR with , and LSQLR, and for LSLR with with .

Appendix C Proof of Theorems 3 and 4

[14] shows Theorems 3 and 4 for the loss . Also, the surrogate losses , and are bounded, and Theorems 3 and 4 for these losses can be proved in a way similar to that for [15, Theorems 2.3 and 2.4], which is based on [16, Chapter 6]; Refer to these studies for the proof of Theorems 3 and 4. Additionally, we note that these theorems can be extended to the case (which is for ): As Theorem 1, B8, , and suggest, MLSLRs with and provide the same result.

Appendix D Discussion on LSLR and MLSLR with

In the binary setting , Theorem 1, B8 suggests that LSLRs or MLSLRs with and give the same probability estimation and classification performance. On the other hand, in a multi-class setting , an analogy for LSLRs or MLSLRs with and may not exactly hold; See Theorem 1, B7. It would be more difficult to understand the results for than to understand the results for in a multi-class setting in our way of interpreting the LS technique with respect to LR, because the difference from LR () gets bigger (just like that the mathematical approximation becomes less accurate for a more distant point). Therefore, we here report only considerations based on the experimental observations.

We took CIFAR-10 experiments similar to those in Section IV for . We tried LSLR and MLSLR for under the task with the zero-one task loss , where we used the labeling function described in Corollary 3. The results are shown in Tables IV and V.

As Figure 5 and Table V show, the R-logit model of the LSLR often and largely deviates from the probability simplex, and LSLR gave worse TSR and TTR than MLSLR with the same . When , the smaller is, the larger the deviation tended, which negatively affected the probability estimation and classification performance of LSLR. Also, all TTRs of MLSLR with were worse than TTR of MLSLR with , the best result of MLSLR with . In the CIFAR-10 experiments (), we could not find advantage of choosing .

Appendix E Discussion on Generalization Analysis

Several previous studies have provided experimental investigations of the generalization performance of LSLR, but there has not been theoretical analysis. This may be attributed to the fact that many studies view the LS technique as regularization added to LR. The loss view gives generalization analysis of LSLR collaterally. Although it does not present a meaningful comparison between LR and LSLR, we here give discussions on generalization analysis in probability estimation and classification tasks for LSLR from the loss view to compensate for the absence of theory, and mention challenges in this direction.

According to [12, Theorem 4], one can obtain a generalization bound for LSLR (and LR) that uses a classification calibrated, Lipschitz continuous and convex loss function in a simple setting of Section III-A. This bound is governed by a covexified variational transformation of the loss (called -transform in [12]), and the tightest possible upper bound uniform over all probability distributions. By viewing the LS technique as modification of the surrogate loss, a lot of theories by existing research can be directly applied to analyze the properties of LSLR in other various settings; See [12, Theorem 5] under low-noise assumption (which assumes that is unlikely to be close to ), [38, Chapter 10] for a norm-regularized version using a kernel-based learner, and [13] for multi-class cost-sensitive tasks. However, it also should be noted that such results grounded on learning theories are often loose bounding-based evaluation and contain quantities such like or -transform that cannot be known in advance or may vary for methods using different surrogate losses, making it difficult to make clear comparisons between methods using different losses.

Acknowledgment

This work was supported by Grant-in-Aid for JSPS Fellows, Number 20J23367.

References

- [1] C. Szegedy, V. Vanhoucke, S. Ioffe, J. Shlens, and Z. Wojna, “Rethinking the inception architecture for computer vision,” in Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, 2016, pp. 2818–2826.

- [2] M. Goibert and E. Dohmatob, “Adversarial robustness via adversarial label-smoothing,” arXiv preprint arXiv:1906.11567, 2019.

- [3] R. Müller, S. Kornblith, and G. E. Hinton, “When does label smoothing help?” in Advances in Neural Information Processing Systems, 2019, pp. 4694–4703.

- [4] J. Chorowski and N. Jaitly, “Towards better decoding and language model integration in sequence to sequence models,” arXiv preprint arXiv:1612.02695, 2016.

- [5] A. Vaswani, N. Shazeer, N. Parmar, J. Uszkoreit, L. Jones, A. N. Gomez, Ł. Kaiser, and I. Polosukhin, “Attention is all you need,” in Advances in Neural Information Processing Systems, 2017, pp. 5998–6008.

- [6] Y. Gao, W. Wang, C. Herold, Z. Yang, and H. Ney, “Towards a better understanding of label smoothing in neural machine translation,” in Proceedings of the Conference of the Asia-Pacific Chapter of the Association for Computational Linguistics and the International Joint Conference on Natural Language Processing, 2020, pp. 212–223.

- [7] B. Zoph, V. Vasudevan, J. Shlens, and Q. V. Le, “Learning transferable architectures for scalable image recognition,” in Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, 2018, pp. 8697–8710.

- [8] Y. Huang, Y. Cheng, A. Bapna, O. Firat, D. Chen, M. Chen, H. Lee, J. Ngiam, Q. V. Le, Y. Wu, and Z. Chen, “Gpipe: Efficient training of giant neural networks using pipeline parallelism,” in Advances in Neural Information Processing Systems, 2019, pp. 103–112.

- [9] Y. Han, P. Zhang, W. Huang, Y. Zha, G. D. Cooper, and Y. Zhang, “Robust visual tracking based on adversarial unlabeled instance generation with label smoothing loss regularization,” Pattern Recognition, vol. 97, p. 107027, 2020.

- [10] C. Meister, E. Salesky, and R. Cotterell, “Generalized entropy regularization or: There’s nothing special about label smoothing,” arXiv preprint arXiv:2005.00820v2, 2020.

- [11] H. Masnadi-Shirazi and N. Vasconcelos, “On the design of loss functions for classification: theory, robustness to outliers, and savageboost,” in Advances in Neural Information Processing Systems, 2008.

- [12] P. L. Bartlett, M. I. Jordan, and J. D. McAuliffe, “Convexity, classification, and risk bounds,” Journal of the American Statistical Association, vol. 101, no. 473, pp. 138–156, 2006.

- [13] B. A. Pires, C. Szepesvari, and M. Ghavamzadeh, “Cost-sensitive multiclass classification risk bounds,” in Proceedings of the International Conference on Machine Learning, 2013, pp. 1391–1399.

- [14] L. Fahrmeir and H. Kaufmann, “Consistency and asymptotic normality of the maximum likelihood estimator in generalized linear models,” Annals of Statistics, vol. 13, no. 1, pp. 342–368, 1985.

- [15] A. M. Bianco and V. J. Yohai, “Robust estimation in the logistic regression model,” in Robust Statistics, Data Analysis, and Computer Intensive Methods, 1996, pp. 17–34.

- [16] P. J. Huber, Robust Statistics, 2nd ed. John Wiley & Sons, 2009.

- [17] H. Zhang, Y. Yu, J. Jiao, E. Xing, L. El Ghaoui, and M. Jordan, “Theoretically principled trade-off between robustness and accuracy,” in Proceedings of the International Conference on Machine Learning, 2019, pp. 7472–7482.

- [18] D. Pregibon, “Logistic regression diagnostics,” Annals of Statistics, vol. 9, no. 4, pp. 705–724, 1981.

- [19] ——, “Resistant fits for some commonly used logistic models with medical applications,” Biometrics, vol. 38, no. 2, pp. 485–498, 1982.

- [20] C. Croux and G. Haesbroeck, “Implementing the bianco and yohai estimator for logistic regression,” Computational Statistics & Data Analysis, vol. 44, no. 1-2, pp. 273–295, 2003.

- [21] R. A. Maronna, R. D. Martin, V. J. Yohai, and M. Salibián-Barrera, Robust Statistics: Theory and Methods (with R), 2nd ed. John Wiley & Sons, 2019.

- [22] J. B. Copas, “Binary regression models for contaminated data,” Journal of the Royal Statistical Society: Series B (Methodological), vol. 50, no. 2, pp. 225–253, 1988.

- [23] R. J. Carroll and S. Pederson, “On robustness in the logistic regression model,” Journal of the Royal Statistical Society: Series B (Methodological), vol. 55, no. 3, pp. 693–706, 1993.

- [24] C. Croux, C. Flandre, and G. Haesbroeck, “The breakdown behavior of the maximum likelihood estimator in the logistic regression model,” Statistics & Probability Letters, vol. 60, no. 4, pp. 377–386, 2002.

- [25] A. Krogh and J. A. Hertz, “A simple weight decay can improve generalization,” in Advances in Neural Information Processing Systems, 1992, pp. 950–957.

- [26] L. Yuan, F. E. Tay, G. Li, T. Wang, and J. Feng, “Revisiting knowledge distillation via label smoothing regularization,” in Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, 2020, pp. 3903–3911.

- [27] M. Lukasik, S. Bhojanapalli, A. Menon, and S. Kumar, “Does label smoothing mitigate label noise?” in Proceedings of the International Conference on Machine Learning, 2020, pp. 6448–6458.

- [28] Y. Xu, Y. Xu, Q. Qian, H. Li, and R. Jin, “Towards understanding label smoothing,” arXiv preprint arXiv:2006.11653v2, 2020.

- [29] W. Li, G. Dasarathy, and V. Berisha, “Regularization via structural label smoothing,” in Proceedings of the International Conference on Artificial Intelligence and Statistics, 2020, pp. 1453–1463.

- [30] A. Galdran, J. Dolz, H. Chakor, H. Lombaert, and I. B. Ayed, “Cost-sensitive regularization for diabetic retinopathy grading from eye fundus images,” in Proceedings of the International Conference on Medical Image Computing and Computer-Assisted Intervention, 2020, pp. 665–674.

- [31] A. Basu, I. R. Harris, N. L. Hjort, and M. Jones, “Robust and efficient estimation by minimising a density power divergence,” Biometrika, vol. 85, no. 3, pp. 549–559, 1998.

- [32] H. Fujisawa and S. Eguchi, “Robust parameter estimation with a small bias against heavy contamination,” Journal of Multivariate Analysis, vol. 99, no. 9, pp. 2053–2081, 2008.

- [33] A. Cichocki and S. Amari, “Families of alpha-beta-and gamma-divergences: Flexible and robust measures of similarities,” Entropy, vol. 12, no. 6, pp. 1532–1568, 2010.

- [34] T. Miyato, S. Maeda, M. Koyama, K. Nakae, and S. Ishii, “Distributional smoothing with virtual adversarial training,” in Proceedings of the International Conference on Learning Representation, 2016, arXiv preprint arXiv:1507.00677v9.

- [35] G. Pereyra, G. Tucker, J. Chorowski, Ł. Kaiser, and G. Hinton, “Regularizing neural networks by penalizing confident output distributions,” arXiv preprint arXiv:1701.06548, 2017.

- [36] H. Kannan, A. Kurakin, and I. Goodfellow, “Adversarial logit pairing,” arXiv preprint arXiv:1803.06373, 2018.

- [37] L. Engstrom, A. Ilyas, and A. Athalye, “Evaluating and understanding the robustness of adversarial logit pairing,” arXiv preprint arXiv:1807.10272v2, 2018.

- [38] F. Cucker and D. X. Zhou, Learning Theory: An Approximation Theory Viewpoint. Cambridge University Press, 2007.

![[Uncaptioned image]](/html/2305.08501/assets/image/yamasaki.png) |

Ryoya Yamasaki received the B.E. and M.Inf. degrees from Kyoto University, Kyoto, Japan, in 2018 and 2020, respectively. He is currently working toward the D.Inf. degree of Graduate School of Informatics, Kyoto University, Kyoto, Japan. His research interests are in areas of statistics and machine learning. |

![[Uncaptioned image]](/html/2305.08501/assets/image/Tanaka.png) |

Toshiyuki Tanaka received the B.E., M.E., and D.E. degrees from the University of Tokyo, Tokyo, Japan, in 1988, 1990, and 1993, respectively. He is currently a professor of Graduate School of Informatics, Kyoto University, Kyoto, Japan. His research interests are in areas of information, coding, and communications theory, and statistical learning. |