Conditional mean embeddings and optimal feature selection via positive

definite kernels

Palle E.T. Jorgensen

(Palle E.T. Jorgensen) Department of Mathematics, The University of

Iowa, Iowa City, IA 52242-1419, U.S.A.

palle-jorgensen@uiowa.edu, Myung-Sin Song

(Myung-Sin Song) Department of Mathematics and Statistics, Southern

Illinois University Edwardsville, Edwardsville, IL 62026, USA

msong@siue.edu and James Tian

(James F. Tian) Mathematical Reviews, 416 4th Street Ann Arbor, MI

48103-4816, U.S.A.

jft@ams.org

Abstract.

Motivated by applications, we consider here new operator theoretic

approaches to Conditional mean embeddings (CME). Our present results

combine a spectral analysis-based optimization scheme with the use

of kernels, stochastic processes, and constructive learning algorithms.

For initially given non-linear data, we consider optimization-based

feature selections. This entails the use of convex sets of positive

definite (p.d.) kernels in a construction of optimal feature selection

via regression algorithms from learning models. Thus, with initial

inputs of training data (for a suitable learning algorithm,) each

choice of p.d. kernel in turn yields a variety of Hilbert spaces

and realizations of features. A novel idea here is that we shall allow

an optimization over selected sets of kernels from a convex set

of positive definite kernels . Hence our “optimal”

choices of feature representations will depend on a secondary optimization

over p.d. kernels within a specified convex set .

Recently the mathematical tools for what is often called Conditional

mean embeddings (CME) have played a role in multiple and new applications

[KSS20, LZW21, GLB+12, PM21, RCOR20, LSTSS16, LZWK21].

One reason for this is that they (the CMEs) stand at the crossroads

of stochastic processes and constructive learning algorithms. Our

present focus will be a new use of CMEs in an analysis of optimization-based

selections of positive definite (p.d.) kernels (and their associated

reproducing kernel Hilbert spaces RKHS), and their use in a construction

of optimal feature selection via regression algorithms for particular

learning models; see [MGP21, ZL21, LRI21]. Our present

use of positive definite kernels , defined on ,

serves two purposes: First, every positive definite kernel is

a covariance kernel for a centered Gaussian process indexed by ,

so in particular there are associated probability spaces realized

in a generalized path space, with sigma-algebra, and probability measures

. Secondly, every choice of a p.d. kernel yields

factorizations via Hilbert space, and so each choice of opens

up a variety choices of Hilbert spaces allowing in turn realization

of features as they are reflected in initial inputs of training data

(for a suitable learning algorithm.) In earlier approaches to such

generalized regression analyses, the p.d. kernel for the model

is given at the outset. By contrast, a novel idea in our present approach

to selection of features is that we shall allow an optimization over

suitably selected sets of kernels in a convex set of positive

definite kernels . Hence our “optimal”

choices of feature representations will depend on a secondary optimization

over kernels within a specified convex set . Below, we begin

with a summary of the mathematical notions which will enter our analysis,

starting with the tools we need from Conditional mean embeddings (CME).

Our present approach to feature selection is motivated in part by

machine learning and data mining. Such uses are typically dictated

by “big data,” and the need for

dimension reduction. This refers to the process of transforming the

data from the high-dimensional space into a space of fewer dimensions,

such as to avoid loss of “essential”

information [NSW11, SZ09, SY06]. The linear case

of data transformation encompasses principal component analysis (PCA),

while by contrast, the nonlinear theories make use of kernel theory,

our present focus. In our approach we aim for adaptive selections

of nonlinear mappings serving to maximize the variance in the data,

hence the design of optimal kernels for the task at hand. Such approaches

are especially useful for dealing with clustering, and with the need

for selection of partitions of the total data-set into some natural

connected components. For kernel learning, we refer to [LS21, CnBCFR21, XWCT21, ZC21].

2. Overview

In the discussion below, we shall make use of some facts from the

analysis and geometry which arise naturally from the use of positive

definite kernels , selection of features via factorization, and

the use of reproducing kernel Hilbert spaces for

regression and optimization. While this list of topics is well covered

in the literature, the references [JT22, JT21a, JT20, JT19b, JT19a]

are especially relevant for what we need.

In summary, the purpose of our paper is illustrated with the following

framework. Problem: Selection of optimal positive definite (p.d.)

kernels for use in feature analysis, adapted to large training

data:

Question 2.1.

(i)

What is the best in ?

Here, is a fixed measure on and

is p.d.

(ii)

What is the best when and are fixed? How to

adjust to optimize ?

The following diagram shows a workflow for learning training data

via choices of p.d. kernels, which returns an optimal feature.

The “best” kernel is the one that picks out the best features

for a given pair :

extends to a unique bounded linear functional on ,

and so by Riesz,

for some . Setting , then

That is, .

∎

Lemma 2.7.

If is an integral operator acting on

, where is -finite,

then it is positive definite if and only if

(2.12)

Remark 2.8.

It is easy to check (2.12) for ,

, .

Then (2.12) is equivalent to

Lemma 2.9.

If is an ONB (or a frame) in ,

then

and

Moreover,

Given all admissible pairs , let

and be as above. There are two selfadjoint operators

(possibly unbounded):

(2.13)

(2.14)

In particular,

(2.15)

which holds in general.

Lemma 2.10.

Let , then

Proof.

One checks that

and so

∎

3. Optimal feature selections

In the remaining of the paper, we formulate three versions of the

general optimization problem as presented in outline in 2,

i.e., the problem optimization over suitable choices of convex sets

of kernels . In brief outline, the three variants are as follows:

(i) In 3, the optimalization entails just the -norm2

applied to the optimal from 2.2. (ii) In

4, a different measure of “optimal”

is used, with solution formula as in 4.2. Finally, (iii)

in 5, our optimization is obtained, and it makes use of

the CME approach.

Hence 3 presents some cases of non-existence of optimizers.

This in turn serves to motivate our affirmative optimization results

in Sections 4 & 5, especially 4.4,

4.5, and 5.7.

Our assumptions below remain as mentioned above. In particular, a

fixed function is specified (representing “training

data.”). Also given is a positive sigma-finite measure

. We assume . Our analysis

of feature selection is based on both regression starting with a p.d.

kernel , as well as a variation for choices of p.d. kernels .

Each yields a selection of admissible features. But a “good”

choice of yields corresponding optimal feature functions ,

thus representing more distinct features, reflected in feature functions

with large -norm2,

i.e., large variance. Optimal choices of typically represent

more successful discrimination by features resulting from input of

a particular training data, the function . More precisely,

the -norm2 refers to the features

entailed by a choice of . By contrast, the training data represented

by is fixed.

where is the spectral measure of the

operator , i.e.,

(3.4)

Proof.

Let . Note that

is a bounded operator. We have

∎

Remark 3.2.

Note that, if ,

then the function is

monotone relative to the order of kernels: .

In that case, we need only optimize with respect to the spectral measure

of the kernel , with fixed.

Below we fix a positive measure as per 2.3. When an

ONB is fixed in the corresponding we then arrive at

a convex set of Mercer kernels , see (3.5):

is specified as in (3.5) below. So, these p.d.

kernels , and the corresponding RKHSs, are determined by the spectral

data (3.8). As a consequence, we see that the optimal feature

vector may be found via a solution to this convex optimization problem

for in . Further note that the spectral data used in

the case (of Mercer kernels) is a special case of the general structure

presented in 3.1 above. Indeed, the reader can verify that

the optimization algorithm presented below for the case of Mercer

kernels generalizes to more general cases of convex sets of p.d. kernels

as per 3.1 above.

Theorem 3.4.

Fix , and let .

Let be an ONB in ,

and consider the Mercer kernel

The condition in (3.9) follows from an application of the

Cauchy-Schwarz inequality.

The fact that the solution to (3.9)

in fact represents the solution to the optimization (3.8)

follows from the observation that the one term in the inner

product is fixed, so the max in (3.8) is attained when quality

holds in the corresponding Cauchy-Schwarz Inequality. Further note

that, for every fixed value of the index , (3.9) is simply

a quadratic equation (see also 3.1), and the optimal spectral

distribution is explicit. The form

of the optimal p.d. kernel then follows by substitution of

into (3.5).

∎

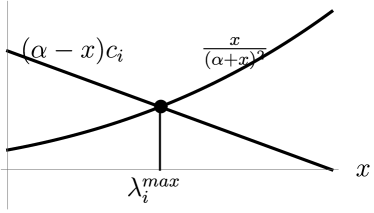

Corollary 3.5.

Consider the finite-dimensional case, i.e., is atomic, where

,

with an ONB in .

Then the optimization problem

Figure 3.2. The solution determined

by the intersection of two curves.

4. Optimization in an ambient Hilbert space

The setting below is as in the previous sections: input is specified

by two parts, first a fixed measure , and secondly, an input

of functions from , with the variety

of functions representing training data in the model. We then examine

optimal choices for p.d. kernels with view to optimization of

-features for the corresponding kernel-learning, see 2

above. The choices of optimal kernels are made precise in Theorems

3.4, and in 4.4 below. In both cases, an ONB in

is chosen, and we study the corresponding convex sets

of Mercer kernels as specified in (3.5). Here, then

each is determined by a spectral distribution .

The corresponding optimization quantity is from (2.2), and

it has a penalty term weighted with an assigned

parameter , see (2.1). We then arrive at an optimal

feature vector for every , and we consider its -variance,

measured with the use of the norm-squared. Two

such variance measures are considered, (3.7) and (4.8).

For the first one, we note a singularity blowup for values of

close to . In the second case, the dependence on takes

a different form; we show that then the -variance (see (4.8))

is monotone, in a sense made precise in 4.4, and 4.5

(spectral a priori error-bounds).

Finally, in 5, we present a solution to the feature optimization

with the use of a conditional-mean embedding, CME. The latter refers

to (i) a choice of probability space, (ii) a family of p.d. kernels

, and corresponding conditional mean embeddings into the RKHSs

.

Below we first recall some basic facts from operator theory. Let

be a closed, densely defined linear operator between Hilbert spaces.

On , define the inner product

(4.1)

where is a positive constant.

Define

by

Then the projection from onto

is

(4.2)

Remark 4.1.

Recall that in our general setup for regression optimization, we have

arranged that training data may be represented via an operator

in Hilbert space. Note that, if , then the block matrix

in (4.2) represents the projection from the direct sum

onto the graph of the operator , see e.g., [JT21b, Corollary 1.55].

Corollary 4.2.

Let

be as above. Then, for all , we have

(4.3)

Proof.

Note that

and the projection of onto

is

which is equal to , for a unique

in . This gives (4.3).

∎

Now, return to optimal feature selections. Fix , and consider

kernels , see 2.4. Let ,

by

The inner product on

is as in (4.1), with parameter .

Fix , then we get a unique ,

such that is the projection of

onto . That is,

Let and be as in 4.4,

and assume is bounded. Let ,

.

(i)

The following hold:

(4.9)

(ii)

Equivalently, the approximation error satisfies

(4.10)

(iii)

By increasing , approximates

in arbitrarily well.

Proof.

Notice that the function in

(4.5) is strictly increasing in , so that (4.9)

follows from (4.8). The other assertions are immediate.

∎

Remark 4.6.

The difference between the two feature selection methods in Sections

3 and 4 is as follows.

Fix a measure , and consider ,

i.e., all admissible kernels. Let be the associated

RKHS. In both cases, for a given ,

the best feature vector in is the same

is the projection of in

onto the graph of . Thus, (4.12) is the norm squared

of the projected vector and the corresponding optimization makes use

of Hilbert space geometry.

5. Applications to CME

A key feature in what is called conditional mean embedding

(CME) concern an analysis of systems of random variable, and conditional

distributions, which take values in suitable choices of reproducing

kernel Hilbert space, typically infinite-dimensional RKHSs. Hence

conditional expectations, and relative transition operators, will

entail choices of p.d. kernels, typical one for each random variable

under consideration. The implementation of kernel embedding of distributions

(also called the kernel mean or mean map) yields nonparametric

outcomes in which a probability distribution is represented as an

element of a reproducing kernel Hilbert space (RKHS). In diverse applications,

the use of CMEs has served as useful tools in for example, problems

of sequentially optimizing conditional expectations for objective

functions. In such settings, typically both the conditional distribution

and the objective function, while fixed, are assumed to be unknown.

The assumption is that input is fixed in the form of a pair

(generalized training data) and as described. The interpretation

for feature selection is that variation of choices of p.d. kernels

amounts to a more versatile feature selection. A possible condition

on a “good” kernel is that

it will yield optimal selection of feature function , i.e.,

representing an output of more distinct features. Often a feature

functions with large -norm2

comes from a choice of that yields a more successful discrimination

by features that reflects input of training data via . More

precisely, the -norm2 refers

to the features selected with optimal choices of .

The setting for CME is as follows:

Let be random variables on a probability space ,

taking values in sets , respectively, and has joint measure

for all .

Denote by the corresponding marginal measures,

and let be the conditional measure defined as

for all and .

Assume further that are given p.d. kernels on , with

RKHSs , , respectively.

Lemma 5.1.

For every , set

(5.1)

Then, for all , it holds that

(5.2)

The map is called the kernel mean embedding

(KME) of the conditional expectation .

Remark 5.2.

Note that the integral on the RHS in formula (5.1) is an

extension of (2.8) from 2.5 above. Moreover, the

proof of the lemma follows the ideas in 2.

Lemma 5.3.

As in 5.1, consider for , as

per the definition (5.1) in 5.1. Then

(i)

if and only if

(5.3)

where

(ii)

if and

only if

In that case, setting ,

then

for all .

Proof.

Consider the filter of finite measurable partitions

of the measurable space , i.e.,

for some , with ,

if , and , then

(5.4)

with

(5.5)

Since is assumed measurable, the right-hand side of (5.5)

has a limit, as we pass to the limit of the filter of all measurable

partitions , see (5.4), and the

limit is well defined and finite if and only if (5.3) holds.

This follows from the following computation:

But since we have “” in the identity (5.5) for all

finite partitions, it follows that (5.3) holds if and only

if the integral on the right-hand side in (5.1) is convergent

with its values in .

The second part of the lemma is immediate.

∎

Remark 5.4.

The setting of the lemma is a fixed a p.d. kernel and a measure

space . We have defined on

and assumed measurable w.r.t. the corresponding product sigma algebra.

The key idea behind the justification of the RKHS

valued integral in (5.1) is a rigorous justification

of a limit of an approximation by finite sums in ,

and the limit with respect to the RKHS norm in .

This is doable as per our discussion, but the limit will be indexed

by a filter of partitions of the measure space .

And the limit is with respect to refinement within the filter of partitions,

where refinement defined by recursive subdivision, i.e., subdivisions

of one partition are creating a finer partition. Note that the reasoning

involves the same kind of limit which is used in the justification

of general Ito isometries, and Ito integrals for Gaussian processes.

Question 5.5.

Assume .

What is the best approximation to choice of CME from an -valued

RKHS?

One option in the literature is to approximate from .

More generally, one may start from an -valued

p.d. kernel ,

i.e.,

(5.6)

, ,

and .

Let be the Hilbert completion of the set

with respect to the inner product

(5.7)

Then is an RKHS with the following reproducing

property:

For all , and ,

we have

(5.8)

Remark 5.6.

In the special case ,

we have ,

where is the scalar valued p.d. kernel of ,

and denotes the identity operator on .

Theorem 5.7.

Assume is compatible with the marginal distribution

of , then we have

(5.9)

(5.10)

Then, we may apply the methods from 3 to the problem:

(5.11)

Proof.

Illustrating the versatility of Hilbert space operators, the reader

will be able to fill in the argument for this formula (5.10),

and its implications, following the general framework presented in

sections 2 and 3 above.

∎

6. A new convex set of p.d. kernels

Let be the set of all Borel

measures on , and

be the subset of probability measures. For all ,

let

(6.1)

denote the Fourier transform.

Consider the following convex set of stationary kernels

(6.2)

Lemma 6.1.

Fix , and let

be the corresponding RKHS. Then, for all ,

(6.3)

(6.4)

Proof.

Assume , then

Conversely, suppose .

Then, for all , we have

It follows that by density and

Riesz’s theorem.

∎

Fix , and let be the RKHS.

Let denote the Lebesgue measure on . Suppose

is dense in . Then, the operator

(6.5)

is densely defined and closable, and its adjoint is given by

(6.6)

where .

Corollary 6.2.

For all , we have

(6.7)

Proof.

This follows from 6.1 by setting , and

is the -Fourier transform of .

∎

Example 6.3.

Consider the following two p.d. kernels on :

(6.8)

Note that

Moreover, for , if ,

then

In other words, the RKHS is the RKHS from the Green’s function for

, or in , .

Given , the convolution

may be extended to measures or distributions.

Given , where ,

and is a finite positive Borel measure on , the

reproducing property of below may be verified

using Fourier-inversion:

Proof.

Indeed, we have

∎

Theorem 6.6.

Fix , and let be the RKHS.

Let

be as in (6.5), where denotes the Lebesgue measure

on . Let be the solution in 2.2,

i.e.,

(6.11)

where is fixed. Then, by

the -Fourier transform, we have

(6.12)

Moreover, the optimal selections from 3.1 and 4.3,

respectively, admit the following explicit spectral representations:

(6.13)

(6.14)

Proof.

By the definition of from (6.6), it follows

that ,

and so .

It follows from this, that

and on the other hand,

∎

Example 6.7.

Let and be the p.d. kernels from (6.8).

The formulas in (6.13)-(6.14) take explicit forms,

summarized in 1.

Table 1. The p.d. kernels and .

References

[CnBCFR21]

Juan Cerviño, Juan Andrés Bazerque, Miguel Calvo-Fullana, and Alejandro

Ribeiro, Multi-task reinforcement learning in reproducing kernel

Hilbert spaces via cross-learning, IEEE Trans. Signal Process. 69

(2021), 5947–5962. MR 4341244

[GLB+12]

Steffen Grünewälder, Guy Lever, Luca Baldassarre, Sam Patterson, Arthur

Gretton, and Massimilano Pontil, Conditional mean embeddings as

regressors, Proceedings of the 29th International Coference on International

Conference on Machine Learning (Madison, WI, USA), ICML’12, Omnipress, 2012,

pp. 1803–1810.

[JST21]

Palle E. T. Jorgensen, Myung-Sin Song, and James Tian, Positive definite

kernels, algorithms, frames, and approximations, 2021.

[JT19a]

Palle Jorgensen and Feng Tian, Decomposition of Gaussian processes, and

factorization of positive definite kernels, Opuscula Math. 39

(2019), no. 4, 497–541. MR 3964760

[JT19b]

by same author, Realizations and factorizations of positive definite kernels,

J. Theoret. Probab. 32 (2019), no. 4, 1925–1942. MR 4020693

[JT20]

Palle Jorgensen and James Tian, Sampling with positive definite kernels

and an associated dichotomy, Adv. Theor. Math. Phys. 24 (2020),

no. 1, 125–154. MR 4106884

[JT21a]

by same author, Reproducing kernels: harmonic analysis and some of their

applications, Appl. Comput. Harmon. Anal. 52 (2021), 279–302.

MR 4218424

[JT22]

by same author, Reproducing kernels and choices of associated feature spaces, in

the form of -spaces, J. Math. Anal. Appl. 505 (2022), no. 2,

Paper No. 125535, 31. MR 4295177

[KSS20]

Ilja Klebanov, Ingmar Schuster, and T. J. Sullivan, A rigorous theory of

conditional mean embeddings, SIAM J. Math. Data Sci. 2 (2020),

no. 3, 583–606. MR 4121886

[LMY16]

Yeon Ju Lee, Charles A. Micchelli, and Jungho Yoon, On multivariate

discrete least squares, J. Approx. Theory 211 (2016), 78–84.

MR 3547633

[LRI21]

David K. Lim, Naim U. Rashid, and Joseph G. Ibrahim, Model-based feature

selection and clustering of RNA-seq data for unsupervised subtype

discovery, Ann. Appl. Stat. 15 (2021), no. 1, 481–508.

MR 4255285

[LS21]

Chi-Ken Lu and Patrick Shafto, Conditional Deep Gaussian Processes:

Multi-Fidelity Kernel Learning, Entropy 23 (2021), no. 11,

Paper No. 1545. MR 4349381

[LSTSS16]

Guy Lever, John Shawe-Taylor, Ronnie Stafford, and Csaba Szepesvári,

Compressed conditional mean embeddings for model-based reinforcement

learning, AAAI, 2016, pp. 1779–1787.

[LZW21]

Tingyu Lai, Zhongzhan Zhang, and Yafei Wang, A kernel-based measure for

conditional mean dependence, Comput. Statist. Data Anal. 160

(2021), Paper No. 107246, 22. MR 4242933

[LZWK21]

Tingyu Lai, Zhongzhan Zhang, Yafei Wang, and Linglong Kong, Testing

independence of functional variables by angle covariance, J. Multivariate

Anal. 182 (2021), Paper No. 104711, 15. MR 4187269

[MGP21]

Erfan Mehmanchi, Andrés Gómez, and Oleg A. Prokopyev, Solving a

class of feature selection problems via fractional 0-1 programming, Ann.

Oper. Res. 303 (2021), no. 1-2, 265–295. MR 4288278

[MPWZ16]

Charles A. Micchelli, Massimiliano Pontil, Qiang Wu, and Ding-Xuan Zhou,

Error bounds for learning the kernel, Anal. Appl. (Singap.)

14 (2016), no. 6, 849–868. MR 3564937

[NSW11]

P. Niyogi, S. Smale, and S. Weinberger, A topological view of

unsupervised learning from noisy data, SIAM J. Comput. 40 (2011),

no. 3, 646–663. MR 2810909

[PM21]

Junhyung Park and Krikamol Muandet, A measure-theoretic approach to

kernel conditional mean embeddings, 2021.

[RCOR20]

Sayak Ray Chowdhury, Rafael Oliveira, and Fabio Ramos, Active learning of

conditional mean embeddings via bayesian optimisation, Proceedings of the

36th Conference on Uncertainty in Artificial Intelligence (UAI) (Jonas Peters

and David Sontag, eds.), Proceedings of Machine Learning Research, vol. 124,

PMLR, 03–06 Aug 2020, pp. 1119–1128.

[SY06]

Steve Smale and Yuan Yao, Online learning algorithms, Found. Comput.

Math. 6 (2006), no. 2, 145–170. MR 2228737

[SZ09]

Steve Smale and Ding-Xuan Zhou, Geometry on probability spaces, Constr.

Approx. 30 (2009), no. 3, 311–323. MR 2558684

[XWCT21]

Ping Xu, Yue Wang, Xiang Chen, and Zhi Tian, COKE:

communication-censored decentralized kernel learning, J. Mach. Learn. Res.

22 (2021), Paper No. 196, 35. MR 4329775

[ZC21]

Yikun Zhang and Yen-Chi Chen, Kernel smoothing, mean shift, and their

learning theory with directional data, J. Mach. Learn. Res. 22

(2021), Paper No. 154, 92. MR 4318510

[ZL21]

Puning Zhao and Lifeng Lai, Minimax rate optimal adaptive nearest

neighbor classification and regression, IEEE Trans. Inform. Theory

67 (2021), no. 5, 3155–3182. MR 4282408