Fast robust location and scatter estimation: a depth-based method

Abstract

The minimum covariance determinant (MCD) estimator is ubiquitous in multivariate analysis, the critical step of which is to select a subset of a given size with the lowest sample covariance determinant. The concentration step (C-step) is a common tool for subset-seeking; however, it becomes computationally demanding for high-dimensional data. To alleviate the challenge, we propose a depth-based algorithm, termed as FDB, which replaces the optimal subset with the trimmed region induced by statistical depth. We show that the depth-based region is consistent with the MCD-based subset under a specific class of depth notions, for instance, the projection depth. With the two suggested depths, the FDB estimator is not only computationally more efficient but also reaches the same level of robustness as the MCD estimator. Extensive simulation studies are conducted to assess the empirical performance of our estimators. We also validate the computational efficiency and robustness of our estimators under several typical tasks such as principal component analysis, linear discriminant analysis, image denoise and outlier detection on real-life datasets. A R package FDB and potential extensions are available in the Supplementary Materials.

Keywords: Computationally efficient; High-dimensional data; Outliers; Robustness; Statistical depth.

1 Introduction

The Minimum Covariance Determinant (MCD) estimator (Rousseeuw, 1984) is among the first affine equivariant and highly robust estimators of multivariate location and scatter. Specifically, for a collection of multivariate data, MCD seeks a subset of samples that leads to a sample covariance matrix with the minimum determinant out of all the candidate sets of a specific size. The location and scatter estimators are then defined as the average and a scaled covariance matrix of these samples, respectively. Butler et al. (1993) and Cator and Lopuhaä (2012) established the consistency and asymptotic normality of the MCD estimator.

MCD has been applied in various fields such as quality control, medicine, finance, image analysis, and chemistry (Hubert et al., 2008, 2018). Estimating the covariance matrix is the cornerstone of many multivariate statistical methods, so MCD has also been used to develop robust and computationally efficient multivariate techniques, such as principal component analysis (Croux and Haesbroeck, 2000; Hubert et al., 2005b), factor analysis (Pison et al., 2003), classification (Hubert and Van Driessen, 2004), clustering (Hardin and Rocke, 2004), multivariate regression (Rousseeuw et al., 2004b), and others (Hubert et al., 2008). To cater to its broad applications, extensive effort has been made to improve the computational efficiency of the approximation algorithm. For example, Rousseeuw and Driessen (1999) propose the first computationally efficient algorithm, termed FASTMCD; (Hubert et al., 2012) suggest an improved version of FASTMCD, termed DetMCD; De Ketelaere et al. (2020) accelerates DetMCD by refinement of the calculation steps and parallel computation. Furthermore, Boudt et al. (2020) generalizes the MCD to high-dimensional cases as the minimum regularized covariance determinant (MRCD). Other variants include the orthogonalized Gnanadesikan-Kettenring (Maronna and Zamar, 2002), the minimum (regularized) weighted covariance determinant (Roelant et al., 2009; Kalina and Tichavskỳ, 2021), and kernel MRCD for non-elliptical data (Schreurs et al., 2021).

Practically, the MCD-type algorithms are limited by two factors. First, the computational complexity of the concentration step (C-step), which is critical for such algorithms, is , and this severely limits the scalability of the algorithm for massive high-dimensional data. Second, the approximation to the true MCD subset becomes less accurate due to the curse of dimensionality. We note that the asymptotic trimmed region induced by a class of statistical depth shares the same form with the asymptotic MCD subset when the data are elliptically symmetric distributed (Butler et al., 1993; Zuo and Serfling, 2000b). This motivates us to investigate the possibility of finding the MCD subset directly by utilizing statistical depth. Statistical depth was first considered for ranking multivariate data from the center outward (Mahalanobis, 1936; Tukey, 1975; Oja, 1983; Liu, 1990; Zuo and Serfling, 2000a; Vardi and Zhang, 2000). Usually, a statistical depth is an increasing function of the centrality of observations, taking values in .

Motivated by the connection mentioned above, we propose a fast depth-based algorithm, denoted as FDB, which approximates the MCD subset with a depth-induced trimmed region. Specifically, we investigate FDB based on two representative depth notions, projection depth and depth, and denote the estimators as, and , respectively. Four main advantages of the proposed algorithm are worth mentioning: 1) Asymptotically, leads to a trimmed region equivalent to the MCD subset for elliptically symmetric distributions. 2) Both and achieve the same level of robustness as the MCD estimator. 3) Empirically, FDB reveals comparable or even better performance than the MCD estimator regarding estimation accuracy. 4) Furthermore, the computational efficiency is dramatically improved by using FDB, especially for high-dimensional cases.

The rest of the paper is organized as follows. Section 2 reviews the MCD estimator and some related theoretical properties. Section 3 introduces the idea of FDB estimators and demonstrates the theoretical equivalence between the MCD subsets and the depth-trimmed regions. Section 4 investigates the invariance, robustness, and computational complexity of the proposed FDB estimators. In Section 5, we conduct extensive simulation studies to assess the performance of the FDB algorithm and compare it with the existing ones regarding estimation accuracy and computational efficiency. Section 6 applies the proposed methods to several real applications through typical multivariate analysis tasks, including principal component analysis, linear discriminant analysis, image denoise, and outlier detection. We end the paper with some discussion in Section 7. Proofs of the theoretical results and additional simulation results are provided in the Supplementary Material.

2 MCD Estimators

In this section, we review the theoretical property of the MCD estimator as well as three widely utilized approximation algorithms. Let be a random variable from an elliptically symmetric distribution, denoted as , whose density is of the form

where is a symmetric positive definite matrix, and the function is assumed to be non-increasing so that is unimodal.

Considering random samples independently generated from the above distribution, MCD aims to solve the following optimization problem

| (1) |

where is an index set of observations (with , where means the largest integer smaller than or equal to ), and is the collection of all such sets. Observations with corresponding indices constitute the final MCD subset, termed ,. Define as the difference between sets and . The convergence property of is revisited in Lemma 1, with the proof provided in Section S1.1 of the Supplementary Material.

Lemma 1

Assume that the random samples . Then for , we have

for any sequence as , where with .

Given an data matrix , with its estimated center and scatter matrix , we denote with the Mahalanobis distance of . The C-step described in Algorithm 1 is crucial for MCD-type algorithms.

Input: initial subset or the estimates (), subset size .

Output: or ()

Rousseeuw and Driessen (1999) proposed the first computationally feasible algorithm, termed FASTMCD, for approximating the MCD subset. Specifically, they randomly constructed several initial subsets and applied two C-steps for each subset, yielding the ten subsets with the lowest determinant. Then, they took C-step iteratively for these ten subsets until the determinant sequence converged and eventually chose the MCD subset as the one leading to the smallest determinant. Given this, the computational efficiency of FASTMCD is thus roughly proportional to the number of the initial subsets. Hubert et al. (2012) proposed an alternative algorithm DetMCD, which replaces random initial subsets (of which there could be many) in FASTMCD with six well-designed deterministic estimators of , and also involves the C-step in a similar way. Denote the estimates as the location and scatter matrix estimates of the -subset for which the determinant of the sample covariance matrix is as small as possible. Further, an additional reweighted step is employed in both algorithms to improve the efficiency of the estimators. To be more specific, the estimators are renewed as trimmed estimates for location and scatter,

| (2) |

where when and 0 otherwise, is the -quantile of the distribution and .

3 A Depth-based Alternative

The idea behind the premier step of MCD-type algorithms is to construct outlier-free subsets as the initial values for the C-step. This motivates us to approach such a purpose using statistical depth, a popular tool for robust multivariate data analysis. More importantly, we find the equivalence between the eventual MCD subset and the depth-trimmed region, which avoids the implementation of the iterative C-steps and hence improves the computational efficiency dramatically.

In general, a statistical depth notion is a function , for and from some class of -variate probability distributions, that provides a center-outward order for a collection of data. Taking into account the robustness as well as the computational efficiency, to be discussed later, we specifically consider the following two depth notions for the proposed method.

Projection depth (Zuo and Serfling, 2000a):

where is the distribution of , denotes the median of a univariate random variable , and its median absolute deviation from the median. Practically, one may choose a finite number of random directions to approximate the projection depth values.

Consider random samples independently generated from the elliptically symmetric (ES) distribution. For a given depth function and for , we call

and the sample version is

the corresponding -trimmed region with .

Lemma 2 (Zuo and Serfling (2000b))

Assume that the random samples , . Then for the projection depth, the depth trimmed region (subset) satisfies

for any sequence as .

Other depth notions could also lead to the same conclusion except for the projection depth. We omit those notions since they are either not robust enough or computationally demanding. Also note that the result does not necessarily hold for the depth, although indeed provides satisfactory results in the simulation. Combining Lemmas 1 and 2, it is straightforward that the two subsets are asymptotic equivalent. We state this result formally in the following theorem.

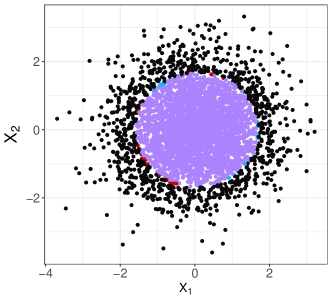

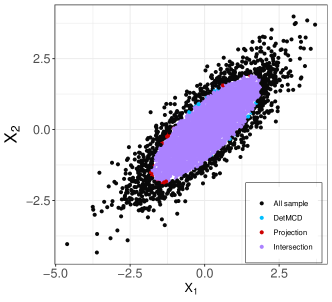

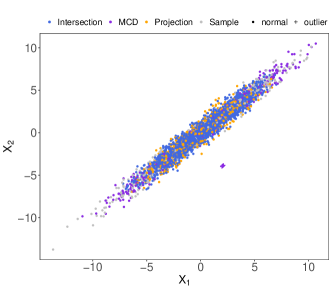

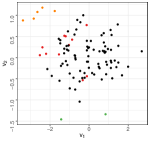

Proof of Theorem 1 is provided in Section S1.2 of the Supplementary Material. Motivated by the above result, we propose to approximate the eventual MCD subset with the depth-trimmed region and avoid the iterative implementation of the C-step. We provide two toy examples in Figure 1 to illustrate such a coincidence. Specifically, we generate data from bivariate normal distributions with unit variance and correlation coefficients 0 and 0.5 for Figure 1 and 1, respectively. We consider and . In both cases, the two subsets match quite well, such that the proportions of the common elements are no less than 97%, which well supports the high effectiveness of the proposed method.

For data of low dimensions, both MCD subsets and depth-based trimmed regions can be computed efficiently, and the result matches well, as shown in Figure 1. However, for high-dimensional data, the MCD algorithms are severely challenged by the cubically increased computational complexity, and hence the approximation will be less efficient. To alleviate this challenge, we consider replacing the MCD subsets with the trimmed regions induced by some computationally efficient depth notions. By doing so, we may not only reduce the computational time significantly but also attain comparable or better robust estimation for both the location and scatter matrix, especially in high-dimensional cases. In what follows, we introduce the FDB algorithm.

Input: , subset size , selected depth notion.

Output: , .

Algorithm 2 considers the case of , which is the condition to guarantee the invertibility of estimated matrix (Rousseeuw and Van Zomeren, 1990). All algorithms for the original MCD require that the dimension be lower than to obtain an invertible covariance matrix. It is recommended that in practice (Rousseeuw and Driessen, 1999).

According to Lemmas 1 and 2, for data from an elliptically symmetric distribution, MCD and FDB algorithms both approximate the optimal subset, though from different perspectives. MCD approaches the solution by combining well selected (or random) initial subset and the iterative implementation of the C-step, which could be computationally demanding for high dimensional data. In contrast, FDB relies on ordering the data from the center outward, and hence its computational complexity is mainly determined by the cost of assigning depth values to each sample.

The idea of incorporating depth (outlyingness) to construct MCD estimators has been considered in the literature. For example, the Stahel–Donoho outlyingness (Donoho, 1982), equivalent to the projection depth, is applied to determine an -subset consisting of the points with the lowest outlyingness, and the corresponding sample mean and covariance matrix are used as one initial value for the C-step (Hubert et al., 2005a; Schreurs et al., 2021). Debruyne and Hubert (2009) studied the influence function and asymptotic relative efficiency of the estimators obtained directly based on such a subset (without the reweighted step). For the first time, we establish the equivalence of the two subsets, which indicates that the depth-based subset is a reasonable approximation to the optimal subset rather than just one option of the initial value for the C-step.

4 Properties of FDB

This section focuses on the properties of the FDB estimators. Specifically, We discuss three types of properties, that are of main interest for such methods (Maronna and Zamar, 2002; Hubert et al., 2012), invariance, robustness and computational complexity. We show that the proposed estimators are quite satisfactory in these aspects.

4.1 Invariant Properties

Affine equivariance makes the analysis independent of any affine transformation of the data. For any nonsingular matrix and vector , the estimators and are affine equivariant if they satisfy

where . The projection depth has been shown affine equivariant (Zuo and Serfling, 2000a; Zuo, 2006), that is the depth value does not vary through affine transformation for any sample, and hence the indexes of samples forming the trimmed region remain the same. Consequently, is obviously affine equivariant. For , a similar property holds for rigid transformation (Mosler and Mozharovskyi, 2022), which is a bit more restrictive than the affine transformation. For high dimensional situations, the affine equivariance may be less important under nonstandard data contamination such as componentwise outliers (Alqallaf et al., 2009).

Permutation invariance provides an effective way to guaranteeing the robustness of analysis to the perturbation of observations. An estimator is said to be permutation invariant if for any permutation matrix . Permutation invariance holds for both projection depth and depth since they do not involve any random subsets, and hence the depth values remain the same through permutation and so will the -subset.

4.2 Robustness

Robustness is the property of main interest when outlier contamination of the data is suspected. As aforementioned, the MCD estimator is highly robust that it achieves the highest possible asymptotic breakdown point, about 1/2, with . The robustness of FDB is determined by the property of the employed depth notion. According to Zuo (2006) and Lopuhaa and Rousseeuw (1991), the breakdown points of the trimmed regions induced by the projection depth and depth are both 1/2, with . That is, and both have a breakdown point as high as that of the MCD estimator. Another indicator is the influence function, which captures the local robustness of estimators. Zuo (2006) and Niinimaa and Oja (1995) showed the influence functions of depth regions induced by projection depth and depth are both bounded. Therefore, and are highly robust locally as well as globally.

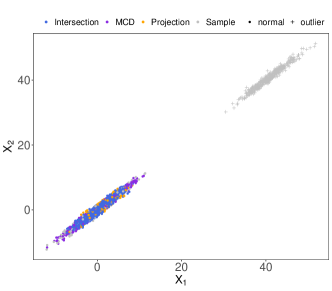

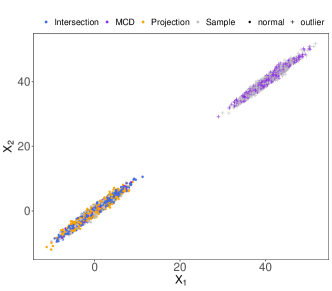

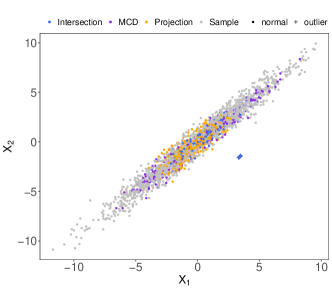

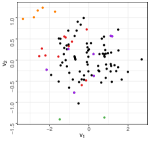

The robustness discussed above is from the theoretical aspect. Practically, both FDB and MCD approximate the theoretically optimal subsets, and their empirical performances do not necessarily match the theoretical results under all the scenarios. This means that the subset selected by the two methods under finite samples may still contain outliers. To show this point, we provide an example in Figure 2, where we generate samples from a 40-dimensional normal distribution with standard normal marginal distributions and a correlation coefficient of 0.5. We consider two levels of contamination, 10% and 40%, and two types of outliers, point and cluster (see for details in Section 5.1), respectively. For the first column with 10% outliers, we set ; for the second column with 40% outliers, . performs perfectly for the first three cases and fails for the last scenario; in contrast, DetMCD is only satisfactory for the first case but fails for the rest. This indicates that for high-dimensional data, provides more reliable approximations to the optimal subset.

4.3 Computational complexity

The computational complexity for finding the -subset by MCDs is . Specifically, for each C-step, it requires computing the covariance matrix and Mahalanobis distances, with complexities and respectively, and depends on the number of initial estimates and the times of C-step iteration. For FASTMCD, the number of initial estimates defaults to 500; for DetMCD, it defaults to 6; and for RT-DetMCD, it is further reduced to 2. However, these efforts only reduced the value of but the order term still remains the same.

In contrast, the computational complexity of for finding the subset is with as the number of projection directions. According to our numerical experiments, The performance of is quite stable when the number of random directions is set around ; see Figure S2 of the Supplement. Hence, leads to a significant improvement over the MCD estimators. We remark that it is possible to further reduce the number of projection directions according to some elaborate generative algorithms (Dyckerhoff et al., 2021). However, these algorithms may instead lengthen the total computational time due to the tedious procedure for searching “better” directions, and hence we stick to selecting the directions randomly. For the case of ultra-high dimensional data, we suggest an adaptive rule, . As for , the computational complexity is , which scales linearly with the dimension of data.

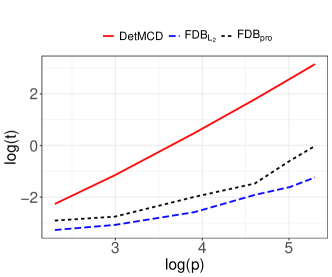

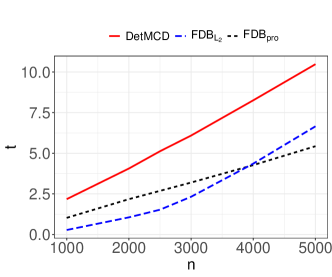

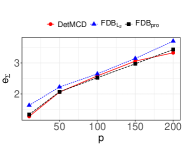

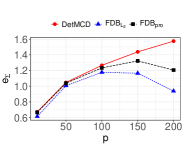

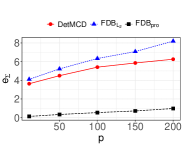

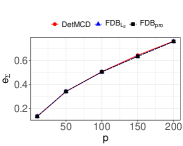

To show the improvement, we provide some numerical results for computation time in Figure 3. Notably, the speed of DetMCD is also influenced by the way of constructing the initial estimates. Specifically, (Rousseeuw and Croux, 1993) is applied to construct initial estimates for DetMCD, which is computationally demanding. To improve speed, Hubert et al. (2012) suggested substituting with the -scale of Yohai and Zamar (1988) when . We follow this suggestion by using the estimator for DetMCD in Figure 3(a), and the -estimator in Figure 3(b), respectively. For , we let . All experiments are run using R-package ddalpha for DetMCD on an Intel(R) Xeon(R) with 3.10GHz and 192 GB memory processor.

FDBs show significant improvement over DetMCD under all the settings. Specifically, in Figure 3(a), the line of DetMCD is steeper than those of the other two methods, which matches well with different orders of dimension in their theoretical computational complexities aforementioned. In Figure 3(b), both DetMCD and reveal linear trends with the increasing sample size, while shows a quadratic trend, though its computation time is the least when .

5 Simulations

We conduct extensive simulations with data from symmetric distributions to assess the performance of our proposed algorithms, and , and make a comparison with DetMCD (Hubert et al., 2012). Besides, we also provide some exploration for the scenarios of asymmetric distributions in Section S3.1 of the Supplement. To evaluate the estimation results, we use the following five measures (the smaller the better).

-

•

An error measure of the location estimator, given by , where denotes the true sample mean.

-

•

An error measure of the scatter estimator, defined as the logarithm of the condition number of ,

-

•

The mean squared error (MSE) of ,

-

•

The Kullback Leibler (KL) divergence between and , , which is identical the KL divergence between the two Gaussian distributions with the same mean.

-

•

The computation time (in seconds) of the whole procedure, including the optimal subset pursuit and the reweighted step.

5.1 Estimation performance

In this subsection, we generate the bulk of non-outlying samples as , where are from and is a matrix with unit diagonal elements and off-diagonal elements equal to 0.75. The number of outliers is and denotes the level of contamination. Four contamination types are considered: point, random, cluster, and radial outliers. Point outliers are obtained by generating , where is a unit vector generated orthogonal to . Random outliers are obtained by generating , where with a random vector from . Cluster outliers are obtained by generating , where is a constant. Radial outliers are obtained by generating . Except for the random outliers, the other three types have been considered by Hubert et al. (2012).

Different contamination levels are considered, namely , and . Let be when or , and when for each method under investigation. The number of directions for projection depth is set as as suggested in Section 4.3. For each method, we compute the reweighted location vectors and the reweighted scatter matrices . The corresponding estimators for the data set are obtained as and , which are compared to the true values using the aforementioned measures. In this part, the true covariance matrix of is .

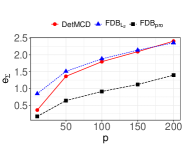

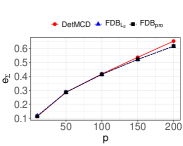

We first provide a full picture for the performance of each method by conducting simulation studies under a broad range of settings. To be more specific, we generated data sets consisting of different types of contamination under a broad range of and , and computed the average with the three methods. The results are illustrated in Figures 4 and 5. Other measures, , MSE, and KL divergence, all reveal similar patterns as and hence are omitted. As shown in Figure 4, and outperform DetMCD across all values of for both random and cluster outliers under either low or high contamination levels. For the case of point contamination, still holds the upper hand, with slightly worse than DetMCD, especially for small values.

Figure 5 shows that is among the best estimators for all the settings. However, in general, DetMCD’s performance deviates more seriously with the increase of dimension , suggesting that it is less suitable for high-dimensional data. Overall, provides the best performance among the three options, that both and DetMCD produce large under point contamination since their induced subsets may contain outliers, which is consistent with the results in Figure 2. Between and DetMCD, the later is better for point contamination while the former is better (or even the best) for cluster contamination.

Next, we provide more detailed numerical outputs for typical simulation settings under study. Following Hubert et al. (2012), we consider three options, A: and , B: and , and C: and , representing low, moderate and high dimensions, respectively. Other settings remain the same as those in Figure 4 except that is fixed at for point, random, and cluster outliers. We report the average measures over 1000 runs in Tables 1, 2 and 3, corresponding to 0% (clean data), 10% and 40% contamination, respectively.

| MSE | KL | t | ||||

|---|---|---|---|---|---|---|

| A | DetMCD | 0.158 (0.050) | 0.238 (0.051) | 0.008 (0.003) | 0.119 (0.046) | 0.022 |

| 0.157 (0.051) | 0.245 (0.054) | 0.008 (0.003) | 0.122 (0.049) | 0.003 | ||

| 0.157 (0.050) | 0.232 (0.049) | 0.007 (0.003) | 0.112 (0.044) | 0.011 | ||

| B | DetMCD | 0.344 (0.040) | 0.615 (0.029) | 0.003 (0.000) | 2.771 (0.179) | 0.388 |

| 0.329 (0.038) | 0.571 (0.025) | 0.003 (0.000) | 2.404 (0.135) | 0.014 | ||

| 0.331 (0.038) | 0.573 (0.025) | 0.003 (0.000) | 2.435 (0.137) | 0.039 | ||

| C | DetMCD | 0.355 (0.016) | 0.656 (0.011) | 6e-4 (0.000) | 14.202 (0.249) | 3.876 |

| 0.331 (0.016) | 0.596 (0.008) | 5e-4 (0.000) | 11.796 (0.166) | 1.043 | ||

| 0.334 (0.016) | 0.598 (0.008) | 5e-4 (0.000) | 11.876 (0.177) | 1.109 | ||

| Point | Random | Cluster | Radial | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Det | Det | Det | Det | ||||||||||

| A | 0.166 | 1.188 | 0.165 | 0.164 | 0.166 | 0.164 | 0.163 | 0.163 | 0.163 | 0.165 | 0.171 | 0.163 | |

| (0.054) | (0.071) | (0.054) | (0.054) | (0.056) | (0.054) | (0.053) | (0.053) | (0.053) | (0.051) | (0.053) | (0.051) | ||

| 0.236 | 1.333 | 0.236 | 0.228 | 0.236 | 0.230 | 0.228 | 0.227 | 0.229 | 0.233 | 0.251 | 0.233 | ||

| (0.052) | (0.070) | (0.052) | (0.045) | (0.047) | (0.046) | (0.045) | (0.045) | (0.045) | (0.049) | (0.054) | (0.048) | ||

| MSE | 0.008 | 5.526 | 0.008 | 0.008 | 0.008 | 0.008 | 0.007 | 0.007 | 0.007 | 0.008 | 0.009 | 0.008 | |

| (0.003) | (0.268) | (0.003) | (0.003) | (0.003) | (0.003) | (0.03) | (0.003) | (0.003) | (0.003) | (0.003) | (0.003) | ||

| KL | 0.107 | 9.375 | 0.112 | 0.101 | 0.112 | 0.105 | 0.101 | 0.101 | 0.102 | 0.103 | 0.117 | 0.104 | |

| (0.041) | (0.314) | (0.043) | (0.038) | (0.042) | (0.039) | (0.038) | (0.038) | (0.038) | (0.038) | (0.046) | (0.037) | ||

| B | 2.403 | 3.456 | 0.339 | 0.347 | 0.339 | 0.340 | 0.349 | 0.340 | 0.341 | 0.347 | 0.337 | 0.338 | |

| (1.597) | (0.67) | (0.037) | (0.040) | (0.038) | (0.039) | (0.037) | (0.036) | (0.038) | (0.039) | (0.037) | (0.037) | ||

| 1.787 | 2.420 | 0.591 | 0.622 | 0.595 | 0.596 | 0.616 | 0.588 | 0.592 | 0.616 | 0.593 | 0.594 | ||

| (0.911) | (0.028) | (0.026) | (0.031) | (0.026) | (0.027) | (0.026) | (0.025) | (0.024) | (0.027) | (0.026) | (0.026) | ||

| MSE | 4.049 | 5.912 | 0.003 | 0.003 | 0.003 | 0.003 | 0.003 | 0.003 | 0.003 | 0.003 | 0.003 | 0.003 | |

| (3.145) | (0.147) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

| KL | 64.051 | 95.728 | 2.591 | 2.789 | 2.591 | 2.597 | 2.781 | 2.558 | 2.591 | 2.801 | 2.574 | 2.587 | |

| (47.593) | (1.304) | (0.131) | (0.172) | (0.141) | (0.138) | (0.168) | (0.144) | (0.140) | (0.162) | (0.147) | (0.142) | ||

| C | 7.824 | 8.056 | 0.348 | 0.355 | 0.340 | 0.341 | 0.359 | 0.344 | 0.346 | 0.362 | 0.345 | 0.347 | |

| (2.507) | (0.082) | (0.018) | (0.015) | (0.015) | (0.015) | (0.017) | (0.016) | (0.017) | (0.018) | (0.018) | (0.018) | ||

| 2.965 | 3.151 | 0.618 | 0.654 | 0.617 | 0.618 | 0.654 | 0.617 | 0.618 | 0.653 | 0.613 | 0.616 | ||

| (0.773) | (0.012) | (0.009) | (0.010) | (0.009) | (0.009) | (0.010) | (0.008) | (0.008) | (0.012) | (0.010) | (0.009) | ||

| MSE | 6.488 | 6.366 | 6e-04 | 6e-04 | 6e-04 | 6e-04 | 6e-04 | 6e-04 | 6e-04 | e-04 | e-04 | e-04 | |

| (2.185) | (0.103) | (8e-06) | (7e-06) | (7e-06) | (7e-06) | (8e-06) | (8e-06) | (8e-06) | (8e-06) | (8e-06) | (8e-06) | ||

| KL | 495.2 | 513.9 | 12.61 | 14.08 | 12.648 | 12.92 | 14.02 | 12.57 | 12.65 | 14.06 | 12.58 | 12.65 | |

| (161.4) | (4.320) | (0.174) | (0.167) | (0.151) | (0.150) | (0.195) | (0.141) | (0.142) | 0.174 | 0.156 | 0.142 | ||

| Point | Random | Cluster | Radial | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Det | Det | Det | Det | ||||||||||

| A | 7.226 | 6.946 | 6.335 | 0.193 | 0.280 | 0.191 | 0.604 | 0.179 | 0.240 | 0.216 | 0.233 | 0.215 | |

| (0.982) | (0.354) | (0.376) | (0.066) | (0.100) | (0.066) | (0.215) | (0.061) | (0.106) | (0.072) | (0.071) | (0.072) | ||

| 2.989 | 2.981 | 2.563 | 0.279 | 0.623 | 0.278 | 0.421 | 0.263 | 0.284 | 0.299 | 0.447 | 0.291 | ||

| (0.290) | (0.208) | (0.184) | (0.062) | (0.126) | (0.062) | (0.386) | (0.058) | (0.170) | (0.058) | (0.081) | (0.053) | ||

| MSE | 31.34 | 33.45 | 36.43 | 0.011 | 0.474 | 0.011 | 1.037 | 0.009 | 0.071 | 0.041 | 0.120 | 0.045 | |

| (3.592) | (2.941) | (2.329) | (0.006) | (0.360) | (0.005) | (2.017) | (0.004) | (0.111) | (0.019) | (0.054) | (0.020) | ||

| KL | 29.66 | 29.46 | 29.91 | 0.142 | 2.363 | 0.141 | 1.673 | 0.130 | 0.349 | 0.365 | 0.963 | 0.400 | |

| (0.918) | (0.894) | (0.795) | (0.060) | (1.453) | (0.058) | (3.523) | (0.053) | (0.483) | (0.142) | (0.324) | (0.152) | ||

| B | 22.98 | 25.30 | 25.10 | 0.408 | 0.408 | 0.407 | 4.796 | 0.411 | 0.409 | 0.412 | 0.413 | 0.410 | |

| (0.079) | (0.041) | (1.138) | (0.047) | (0.048) | (0.048) | (0.371) | (0.045) | (0.045) | (0.044) | (0.046) | (0.045) | ||

| 4.373 | 6.161 | 6.003 | 0.732 | 0.729 | 0.724 | 2.000 | 0.718 | 0.720 | 0.737 | 0.739 | 0.726 | ||

| (0.112) | (0.151) | (0.470) | (0.033) | (0.036) | (0.035) | (0.093) | ( 0.031) | (0.032) | (0.037) | (0.036) | (0.033) | ||

| MSE | 24.51 | 15.98 | 16.55 | 0.004 | 0.004 | 0.004 | 0.875 | 0.004 | 0.004 | 0.004 | 0.004 | 0.004 | |

| (0.568) | (0.366) | (3.196) | (0.000) | (0.000) | (0.000) | (0.074) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | ||

| KL | 242.1 | 229.1 | 231.1 | 3.868 | 3.815 | 3.796 | 36.654 | 3.731 | 3.747 | 3.877 | 3.890 | 3.799 | |

| (2.489) | (2.716) | (5.105) | (0.217) | (0.217) | (0.216) | (2.466) | (0.201) | (0.210) | (0.218) | (0.236) | (0.204) | ||

| C | 51.43 | 56.56 | 55.64 | 0.420 | 0.409 | 0.413 | 6.345 | 0.418 | 0.417 | 0.421 | 0.410 | 0.415 | |

| (0.016) | (0.012) | (3.242) | (0.020) | (0.020) | (0.021) | (0.161) | (0.019) | (0.020) | (0.021) | (0.020) | (0.021) | ||

| 5.061 | 6.996 | 6.756 | 0.769 | 0.745 | 0.753 | 2.317 | 0.757 | 0.758 | 0.769 | 0.747 | 0.760 | ||

| (0.039) | (0.027) | (0.674) | (0.012) | (0.011) | (0.011) | (0.009) | (0.012) | (0.011) | (0.011) | (0.009) | (0.011) | ||

| MSE | 24.57 | 16.01 | 17.33 | 9e-04 | 8e-04 | 4e-04 | 0.155 | 8e-04 | 8e-04 | 9e-04 | 8e-04 | 8e-04 | |

| (0.085) | (0.055) | (4.426) | (1e-05) | (1e-05) | (1e-05) | (0.004) | (1e-05) | (1e-05) | (1e-05) | (9e-06) | (1e-05) | ||

| KL | 1204 | 1151 | 1140 | 19.20 | 18.09 | 18.45 | 88.81 | 18.63 | 18.66 | 19.14 | 18.12 | 18.70 | |

| (2.094) | (2.722) | (31.32) | (0.238) | (0.199) | (0.224) | (0.975) | (0.233) | (0.237) | (0.240) | (0.198) | (0.222) | ||

For clean data (Table 1), the three estimators are comparable for low-dimensional cases; FDBs achieve slightly smaller values for , and KL when the data dimension is moderate or high. More importantly, the running time of DetMCD is reduced in all settings, with the relative computational efficiency, defined as , ranging between 2 and 10 for , and between 3 and 27 for . Such a comparison of computation time holds similarly when contamination presents, and hence is omitted in the remaining tables.

When the amount of contamination is 10% (Table 2), the performances of three methods are all satisfying under settings with random, cluster or radial contamination, and the comparison is similar to that for clean data. For point contamination, performs the worse for each of the three settings, that it generates the largest values for the four measures of estimation accuracy; DetMCD gets problematic for moderate and high dimensional data (settings B and C), which indicates its deficiency for such cases; in contrast, remains robust under all three settings and provides values of measures quite close to corresponding ones for the clean data in Table 1.

When the amount of contamination increases to 40% (Table 3), the three methods all work well and are comparable under settings with random or radial contamination. However, none of them is satisfactory when the contamination presents as point outliers, and this weak performance was also observed for both DetMCD and FASTMCD under similar settings in Hubert et al. (2012). For cluster contamination, DetMCD leads to larger estimation errors in each cell, especially when the dimension of data is moderate or high; however, both and instead remains very stable across all three settings. Additional results for and are provided in Tables S1–S4 of the Supplementary Material, from which we may draw similar conclusions for the comparison of the three methods.

5.2 Robustness assessment

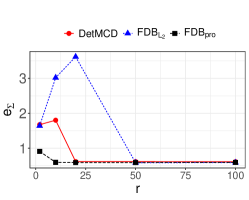

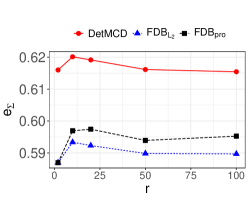

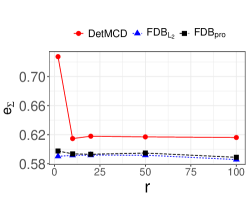

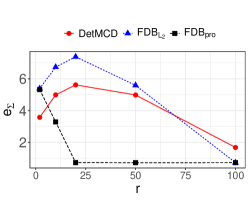

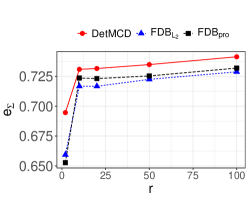

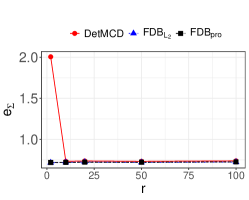

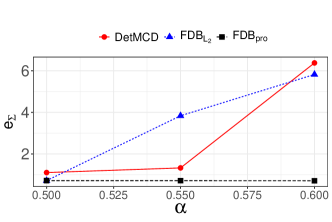

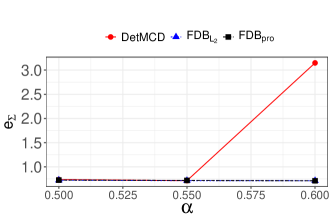

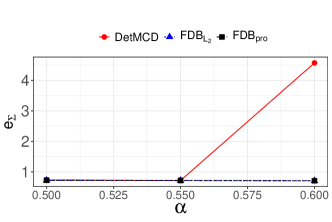

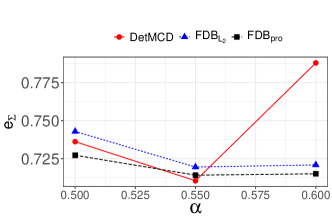

In addition, we assess the tolerance of each method to the core-set size . Specifically, we generate data from Setting B with 40% contamination, which is high enough for most practical implementations, and we set for point, random and cluster outliers. Meanwhile, we consider ranging from 0.5 to 0.6, which is the highest value that possibly produces a clean subset. The average from 1000 replications are reported in Figure 6. remain robust for different values of under all the investigated settings; is satisfactory for random, cluster and radial contamination, while its estimation error grows substantially with for point contamination; DetMCD generates table estimation when and but becomes deficient when raises up to 0.6 in each plot of Figure 6. The other three measures show similar patterns as illustrated in Figure S1 of the Supplementary Material. In conclusion, reaches the strongest tolerance to the core-set size, when the proportion of outliers in the data is very high.

To sum it up, FDBs improves the computational efficiency significantly, which is the main motivation of this work, and generally achieves the highest computational efficiency. Besides, we surprisingly find that shows superiority in terms of both estimation accuracy and robustness, especially in high-dimensional cases. One may safely substitute DetMCD with for practical implementation.

6 Real data examples

In this section, we apply the FDB methods to four real datasets of various dimensions and sizes. The resultant robust multivariate location and scatter estimates are evaluated via some typical tasks in multivariate analysis such as outlier detection, linear discriminant analysis (LDA), principal component analysis (PCA), and image denoise. The same three methods from Section 5 are utilized. The computations are performed in R (R Core Team 2021) on a laptop with a 10-core and 32GB memory processor.

6.1 Robust PCA for forged bank notes data

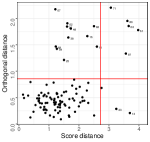

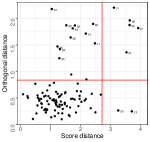

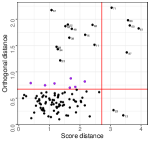

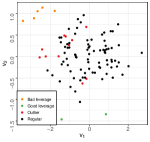

The first dataset is the forged Swiss bank notes data (Milo, 1990), which is also used in Hubert et al. (2012). The data are of size and dimension , denoted as . Since this dataset includes outliers and highly correlated variables (Rousseeuw et al., 2004a; Willems et al., 2009), we employ the proposed algorithms and DetMCD to get robust estimation first and conduct robust PCA based on these estimates. The classical PCA obtained by sample location and scatter is also demonstrated for comparison. We use the first two principal components , which explain over of the total variance. The projections of data on the -dimensional PCA subspace, , are shown in Fig. 7(e)–7(h).

The score distance (SD) and orthogonal distance (OD) represent the robust distance of samples in the two-dimensional PCA subspace and the orthogonal distance of samples to the PCA subspace, respectively. For each sample , we have , where and are the first two eigenvalues of , and , where . Figure 7(a)–7(d) illustrate diagnostic plots. By two cutoff values in each diagnostic plot, we categorize samples into four types and assign different colors to them in Fig. 7(e)–7(h). Regular samples gather in the bottom-left region of diagnostic plots with both score distances and orthogonal distances relatively small, which form the main body of the data cloud. Good leverage samples are close to the PCA subspace but far from the regular samples, e.g., the samples and in the bottom-right region of Fig. 7(a)–7(c), and the green points in Fig. 7(e)–Fig. 7(g). Orthogonal outliers are far from the PCA subspace but not distinguishable by only observing their projections. With larger orthogonal distances but smaller score distances, they locate on the top-left region of diagonal plots, e.g., samples , and in Fig. 7(a)–7(c), and red points in Fig. 7(e)–Fig. 7(g). For bad leverage samples, both score and orthogonal distances are large. They lie on the top-right region of diagonal plots and are represented as orange points in projection plots. In general, the three robust methods lead to comparable analysis results and all significantly improve the performance of the classical PCA, which agrees with Theorem 1. However, DetMCD may identify some regular points as outliers according to its specific cutoff value for the orthogonal distance; see the purple points in the third column of Figure 7.

6.2 Outlier detection for phoneme data

In the second example, we detect outliers for a phoneme dataset, which comes from a speech recognition database TIMIT and has been discussed in Hastie et al. (2009). The data includes speech frames, of which are “ao” and of which are “iy”. Each data frame has been transformed to be a log-periodogram of length . First, we reduce the dimensions by smoothing splines. For each sample, we replace the original variables with -dimensional variables , where is the basis matrix of natural cubic splines. We use basis functions with knots uniformly placed over . To this end, we are dealing with data of and .

| Method | DetMCD | Sample | ||

|---|---|---|---|---|

| Number | ||||

| AUC | ||||

| Time |

We take “ao” and “iy” to be regular cases and outliers, respectively, and perform outlier detection. To be more specific, we calculate the robust Mahalanobis distances based on FDBs and DetMCD, and classical Mahalanobis distances based on Sample. Then, we treat cases with the top largest distances as outliers, and the remaining ones as regular cases. Table 4 records the number of “iy” that are flagged as outliers, the area under the ROC curve (AUC), and the average computational time (second) of replicates for these methods. Again, the proposed methods and DetMCD perform similarly and they all outperform Sample with higher AUCs. In addition, the proposed methods reveal advantages in computation time.

6.3 Denoise for MNIST data

The Modified National Institute of Standards and Technology (MNIST) database is widely used for training various image processing systems. It contains a large set of handwritten images representing the digits zero through nine. Each digit is stored as a gray-scale image with a size . Training data and testing data of are randomly selected from MNIST. Noises are generated and added to of the images in the training set and all images in the testing set. Our task is to denoise the testing images, which has been considered in Schreurs et al. (2021).

The detailed process is similar to the robust PCA in Section 6.1. First, we apply , , DetMCD, and Sample to training images and obtain the estimated location and scatter. with , denoted as , is also used for better comparison. Here all methods have comparable computational time. Then, we calculate the eigenvectors of the robust estimated scatter. Next, we project the testing data to the subspace spanned by the first eigenvectors and then transform the projected data, i.e., scores, back to the original space. We denote the reconstructed data as . Fig. 8 illustrates obtained by various methods with . DetMCD is removed since it returns an error of high condition numbers and hence is not applicable to this example. We can see that the denoised images for the proposed methods are more clear than those for the Sample, which verifies the influence of adding noise on evaluating scatter and the efficiency of the proposed methods. As in Schreurs et al. (2021), we also calculate the mean absolute error between the original and denoised images. Table 5 shows that the MAE for Sample is obviously larger than those for proposed methods.

| Sample |

|---|

6.4 Outlier detection for Musk data

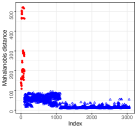

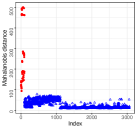

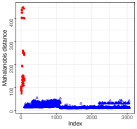

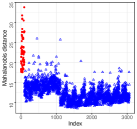

Musk data is commonly used in high-dimensional classification and outlier detection problems (Aggarwal and Sathe, 2015; Porwal and Mukund, 2017). The original data, which can be found in UCI includes samples, divide into musk and non-musk classes. Each sample has features characterizing the molecule structure. Here we use a preprocessed musk dataset of , which consists of non-musk samples as inliers and musk sample as outliers. Our task is to detect the outliers with the proposed methods, DetMCD and Sample. As shown in Fig. 9, our proposed methods and DetMCD can exactly pick out outliers, which are represented as red points, whereas Sample would take many regular samples as outliers. Furthermore, the computational time of , , and DetMCD are , , and seconds, respectively. The proposed methods are computationally more efficient than DetMCD.

7 Discussion

MCD-type methods suffer from high computational complexity due to the iteratively used C-step. To tackle the issue, we directly approximate the MCD subset with the trimmed subset induced by statistical depth. Two depth notions, the projection depth and the depth, are recommended due to high computational efficiency and robustness. In addition, we establish the equivalence between the desired MCD subset and the trimmed subset induced by the projection depth. Bypassing the iteration of the C-step, we manage to reduce the computational complexity from to and with and , respectively. Moreover, the proposed estimators also reach the same level of robustness as the MCD estimator. We conduct extensive simulation studies and show that our estimators are comparable with MCD-type estimators for low-dimensional data and significantly outperform MCD-type estimators for high-dimensional cases.

The real data examples provide strong evidence that FDB is a valuable complement to the toolset of robust multivariate analysis, including but not limited to PCA, LDA, image denoise and outlier detection. The FDB algorithm may benefit other applications that directly or indirectly rely on robust covariance matrix estimation, such as robust linear regression (Coakley and Hettmansperger, 1993), regression with continuous and categorical regressors (Hubert and Rousseeuw, 1997), MCD-regression (Rousseeuw et al., 2004b), multivariate least trimmed squares estimation (Agulló et al., 2008), and robust errors-in-variables regression (Fekri and Ruiz-Gazen, 2004).

The present study primarily focuses on data from elliptical symmetric distributions with enough samples, which may be violated in practical scenarios (Schreurs et al., 2021). In Section S3.1 of the Supplementary Material, we evaluate the effectiveness of our estimators when dealing with skewed distributions. In addition, we did preliminary work to extend the proposed algorithm to the scenario of “small , large ” and evaluate our idea with a real-world dataset in Section S3.2 of the Supplementary Material. Our preliminary exploration shows promising results for both cases. Further investigation is needed to address more general scenarios. One possible solution is to adapt depth notions applicable to more general distributions to obtain the -subset and then apply the kernel trick to map the subset to a feature space, where outlier detection can be conducted. The computational time is significantly reduced for high-dimensional scenarios (); however, the estimation accuracy still desires further improvement. Rather than a shrinkage estimator, it is also of interest to extend the MCD framework by considering a low-rank and sparse estimator to alleviate the curse of dimensionality.

Supplementary materials

-

•

We provide an R-package named FDB and R codes of the FDB algorithm proposed in this paper.

-

•

The file of supplement involves proofs of theoretical results, additional simulation results as well as preliminary explorations of potential extensions.

Acknowledgement

We are very grateful to three anonymous referees, an associate editor, and the Editor for their valuable comments that have greatly improved the manuscript. The first two authors contribute equally to the paper.

References

- Aggarwal and Sathe (2015) Aggarwal, C. C. and Sathe, S. (2015), “Theoretical foundations and algorithms for outlier ensembles,” ACM SIGKDD Explorations Newsletter, 17, 24–47.

- Agulló et al. (2008) Agulló, J., Croux, C., and Van Aelst, S. (2008), “The multivariate least-trimmed squares estimator,” Journal of Multivariate Analysis, 99, 311–338.

- Alqallaf et al. (2009) Alqallaf, F., Van Aelst, S., Yohai, V. J., and Zamar, R. H. (2009), “Propagation of outliers in multivariate data,” The Annals of Statistics, 311–331.

- Boudt et al. (2020) Boudt, K., Rousseeuw, P. J., Vanduffel, S., and Verdonck, T. (2020), “The minimum regularized covariance determinant estimator,” Statistics and Computing, 30, 113–128.

- Butler et al. (1993) Butler, R., Davies, P., and Jhun, M. (1993), “Asymptotics for the minimum covariance determinant estimator,” The Annals of Statistics, 21, 1385–1400.

- Cator and Lopuhaä (2012) Cator, E. A. and Lopuhaä, H. P. (2012), “Central limit theorem and influence function for the MCD estimators at general multivariate distributions,” Bernoulli, 18, 520–551.

- Coakley and Hettmansperger (1993) Coakley, C. W. and Hettmansperger, T. P. (1993), “A bounded influence, high breakdown, efficient regression estimator,” Journal of the American Statistical Association, 88, 872–880.

- Croux and Haesbroeck (2000) Croux, C. and Haesbroeck, G. (2000), “Principal component analysis based on robust estimators of the covariance or correlation matrix: influence functions and efficiencies,” Biometrika, 87, 603–618.

- De Ketelaere et al. (2020) De Ketelaere, B., Hubert, M., Raymaekers, J., Rousseeuw, P. J., and Vranckx, I. (2020), “Real-time outlier detection for large datasets by RT-DetMCD,” Chemometrics and Intelligent Laboratory Systems, 199, 103957.

- Debruyne and Hubert (2009) Debruyne, M. and Hubert, M. (2009), “The influence function of the Stahel–Donoho covariance estimator of smallest outlyingness,” Statistics & probability letters, 79, 275–282.

- Donoho (1982) Donoho, D. L. (1982), “Breakdown Properties of Multivariate Location Estimators,” Ph. D. Qualifying Paper, Harvard University.

- Dyckerhoff et al. (2021) Dyckerhoff, R., Mozharovskyi, P., and Nagy, S. (2021), “Approximate computation of projection depths,” Computational Statistics & Data Analysis, 157, 107166.

- Fekri and Ruiz-Gazen (2004) Fekri, M. and Ruiz-Gazen, A. (2004), “Robust weighted orthogonal regression in the errors-in-variables model,” Journal of Multivariate Analysis, 88, 89–108.

- Hardin and Rocke (2004) Hardin, J. and Rocke, D. M. (2004), “Outlier detection in the multiple cluster setting using the minimum covariance determinant estimator,” Computational Statistics & Data Analysis, 44, 625–638.

- Hastie et al. (2009) Hastie, T., Tibshirani, R., and Friedman, J. (2009), The Elements of Statistical Learning: Data Mining, Inference, and Prediction, Springer Science & Business Media.

- Hubert et al. (2018) Hubert, M., Debruyne, M., and Rousseeuw, P. J. (2018), “Minimum covariance determinant and extensions,” Wiley Interdisciplinary Reviews: Computational Statistics, 10, e1421.

- Hubert and Rousseeuw (1997) Hubert, M. and Rousseeuw, P. J. (1997), “Robust regression with both continuous and binary regressors,” Journal of Statistical Planning and Inference, 57, 153–163.

- Hubert et al. (2005a) Hubert, M., Rousseeuw, P. J., and Branden, K. V. (2005a), “ROBPCA: A New Approach to Robust Principal Component Analysis,” Technometrics, 47, 64 – 79.

- Hubert et al. (2008) Hubert, M., Rousseeuw, P. J., and Van Aelst, S. (2008), “High-breakdown robust multivariate methods,” Statistical Science, 23, 92–119.

- Hubert et al. (2005b) Hubert, M., Rousseeuw, P. J., and Vanden Branden, K. (2005b), “ROBPCA: a new approach to robust principal component analysis,” Technometrics, 47, 64–79.

- Hubert et al. (2012) Hubert, M., Rousseeuw, P. J., and Verdonck, T. (2012), “A deterministic algorithm for robust location and scatter,” Journal of Computational and Graphical Statistics, 21, 618–637.

- Hubert and Van Driessen (2004) Hubert, M. and Van Driessen, K. (2004), “Fast and robust discriminant analysis,” Computational Statistics & Data Analysis, 45, 301–320.

- Kalina and Tichavskỳ (2021) Kalina, J. and Tichavskỳ, J. (2021), “The minimum weighted covariance determinant estimator for high-dimensional data,” Advances in Data Analysis and Classification, 1–23.

- Liu (1990) Liu, R. Y. (1990), “On a notion of data depth based on random simplices,” The Annals of Statistics, 18, 405–414.

- Lopuhaa and Rousseeuw (1991) Lopuhaa, H. P. and Rousseeuw, P. J. (1991), “Breakdown points of affine equivariant estimators of multivariate location and covariance matrices,” The Annals of Statistics, 229–248.

- Mahalanobis (1936) Mahalanobis, P. C. (1936), “On the generalized distance in statistics,” National Institute of Science of India, 12, 49–55.

- Maronna and Zamar (2002) Maronna, R. A. and Zamar, R. H. (2002), “Robust estimates of location and dispersion for high-dimensional datasets,” Technometrics, 44, 307–317.

- Milo (1990) Milo, W. (1990), “Multivariate statistics: a practical approach,” Journal of the Royal Statistical Society: Series A, 153, 112–113.

- Mosler and Mozharovskyi (2022) Mosler, K. and Mozharovskyi, P. (2022), “Choosing among notions of multivariate depth statistics,” Statistical Science, 37, 348–368.

- Niinimaa and Oja (1995) Niinimaa, A. and Oja, H. (1995), “On the influence functions of certain bivariate medians,” Journal of the Royal Statistical Society: Series B (Methodological), 57, 565–574.

- Oja (1983) Oja, H. (1983), “Descriptive statistics for multivariate distributions,” Statistics & Probability Letters, 1, 327–332.

- Pison et al. (2003) Pison, G., Rousseeuw, P. J., Filzmoser, P., and Croux, C. (2003), “Robust factor analysis,” Journal of Multivariate Analysis, 84, 145–172.

- Porwal and Mukund (2017) Porwal, U. and Mukund, S. (2017), “Outlier detection by consistent data selection method,” arXiv preprint arXiv:1712.04129.

- Roelant et al. (2009) Roelant, E., Van Aelst, S., and Willems, G. (2009), “The minimum weighted covariance determinant estimator,” Metrika, 70, 177–204.

- Rousseeuw et al. (2004a) Rousseeuw, P., Van Aelst, S., Driessen, K., and Agullo, J. (2004a), “Robust multivariate regression,” Technometrics, 46, 293–305.

- Rousseeuw (1984) Rousseeuw, P. J. (1984), “Least median of squares regression,” Journal of the American Statistical Association, 79, 871–880.

- Rousseeuw and Croux (1993) Rousseeuw, P. J. and Croux, C. (1993), “Alternatives to the median absolute deviation,” Journal of the American Statistical Association, 88, 1273–1283.

- Rousseeuw and Driessen (1999) Rousseeuw, P. J. and Driessen, K. V. (1999), “A fast algorithm for the minimum covariance determinant estimator,” Technometrics, 41, 212–223.

- Rousseeuw et al. (2004b) Rousseeuw, P. J., Van Aelst, S., Van Driessen, K., and Gulló, J. A. (2004b), “Robust multivariate regression,” Technometrics, 46, 293–305.

- Rousseeuw and Van Zomeren (1990) Rousseeuw, P. J. and Van Zomeren, B. C. (1990), “Unmasking multivariate outliers and leverage points,” Journal of the American Statistical Association, 85, 633–639.

- Schreurs et al. (2021) Schreurs, J., Vranckx, I., Ketelaere, B. D., Hubert, M., Suykens, J. A. K., and Rousseeuw, P. J. (2021), “Outlier detection in non-elliptical data by kernel MRCD,” Statistics and Computing, 31, 1–18.

- Tukey (1975) Tukey, J. W. (1975), “Mathematics and the picturing of data,” in Proceedings of the International Congress of Mathematicians, Vancouver, 1975, vol. 2, pp. 523–531.

- Vardi and Zhang (2000) Vardi, Y. and Zhang, C.-H. (2000), “The multivariate L1-median and associated data depth,” Proceedings of the National Academy of Sciences, 97, 1423–1426.

- Willems et al. (2009) Willems, G., Joe, H., and Zamar, R. (2009), “Diagnosing multivariate outliers detected by robust estimators,” Journal of Computational and Graphical Statistics, 18, 73–91.

- Yohai and Zamar (1988) Yohai, V. J. and Zamar, R. H. (1988), “High breakdown-point estimates of regression by means of the minimization of an efficient scale,” Journal of the American Statistical Association, 83, 406–413.

- Zuo (2006) Zuo, Y. (2006), “Multidimensional trimming based on projection depth,” The Annals of Statistics, 34, 2211–2251.

- Zuo and Serfling (2000a) Zuo, Y. and Serfling, R. (2000a), “General notions of statistical depth function,” The Annals of Statistics, 28, 461–482.

- Zuo and Serfling (2000b) — (2000b), “Structural properties and convergence results for contours of sample statistical depth functions,” The Annals of Statistics, 28, 483–499.