Product Disintegrations: Some Examples

1 Introduction and general setup

The main objective of this brief work is to provide a collection of examples involving the concept of a product disintegration, which we introduce here and in a forthcoming paper that addresses the theory and establishes a convergence result (restated here, for convenience, as Theorem 1, without a proof). Therefore, the present text can be seen as an appendix to the main paper. The concept of a product disintegration generalizes exchangeability, a well-known concept in Probability and Statistics (Aldous 1985, Draper et al. 1993, Dawid 2013, Konstantopoulos and Yuan 2019), which we recall next.

A sequence of random variables with values in a Borel space is said to be exchangeable iff for every integer and every permutation of it holds that the random vectors and are equal in distribution. An important characterization of exchangeability is de Finetti’s Theorem, which says that a necessary and sufficient condition for a sequence of random variables to be exchangeable is that it is conditionally independent and identically distributed. In view of de Finetti’s Theorem, we propose to replace the random product measure that characterizes exchangeable sequences—whose factors are all the same—by an arbitrary random product measure, as follows: with as above, we shall say that a sequence of random probability measures on is a product disintegration of iff, with probability one, the equality

| (1) |

holds for each and each family of measurable subsets of . If is a stationary sequence, then we say that is a stationary product disintegration. In other words, product disintegration allows one to have conditional independence in terms of a hidden process consisting of a sequence of random probabilities.

Remark 1.

Any sequence of -valued random variables admits a canonical product disintegration, obtained by taking for all integer .

Before proceeding, let us fix some notation: in all that follows, is a compact metrizable space, is the set of continuous real valued maps defined on , and denotes the set of Borel probability measures on . For and , we write . The next result claims that, given a sequence , , of random elements with values in , and a continuous function (sometimes called an observable in the context of Ergodic Theory), a Strong Law of Large Numbers for the process , , holds if and only if the hidden process used in the product disintegration satisfies an associated Strong Law of Large Numbers itself.

Theorem 1.

Let be a sequence of -valued random variables. Assume is a product disintegration of , and let be a continuous function from to . Then it holds that

| (2) |

In particular, the limit exists almost surely if and only if the limit exists almost surely, in which case one has almost surely.

2 Examples

In what follows, given a probability space , a random probability measure on is a Borel measurable mapping . Throughout this section, its value at a point is denoted by and interchangeably.

2.1 Product disintegrations per se

Example 1 (Product disintegrations are not (necessarily) unique).

Let be a sequence of independent and identically distributed random variables, uniformly distributed in the unit interval , and let, for , be the random probability measure on defined via , where for simplicity we write , , instead of . Assume further that is a product disintegration of a given sequence of Bernoulli random variables. Without much effort, it is possible to prove that and, in particular, it holds that, conditionally on , each is a Bernoulli random variable with parameter . That is, for each we have Now define by , so that is the canonical product disintegration of . Clearly and are different since is equal either to or whereas this is not true of . Indeed, for , we have , whereas

Example 2 (Random Walk as a two-stage experiment with random jump probabilities).

In the same setting as Example 1, let , . Clearly is an independent and identically distributed sequence of standard Rademacher random variables, i.e., for each it holds that . Indeed, for any , we have where the last equality follows from the assumption that the ’s are independent. Moreover, since the left-hand side in this equality is either or . Now let and for . By the above derivation, is the symmetric random walk on . Therefore, although — unconditionally — at each step the process jumps up or down with equal probabilities, we have that conditionally on it evolves according to the following rule: at step , sample a Uniform random variable independent of anything that has happened before (and of anything that will happen in the future), and go up with probability , or down with probability .

Example 3.

Let be an exchangeable sequence of Bernoulli) random variables. In particular, satisfies

for some random variable taking values in the unit interval. Then, defining the random measures via for all , it is clear that is a stationary product disintegration of — again using the fact that . In particular, in this scenario, an unconditional Strong Law of Large Numbers does not hold for , unless when is a constant. See also Theorem 2.2 in Taylor and Hu (1987), which provides a characterization of the Strong Law for the class of integrable, exchangeable sequences. This example illustrates the fact that the existence of a product disintegration is not sufficient for the Law of Large Numbers to hold (indeed, by Remark 1, any sequence of random variables admits a product disintegration).

Example 4 (Concentration inequalities).

One important consequence of the notion of a product disintegration is that it allows us to easily translate certain concentration inequalities (such as the Chernoff bound, Hoeffding’s inequality, Bernstein’s inequality, etc) from the independent case to a more general setting. Recall that the classical Hoeffding inequality says that, if is a sequence of independent random variables with values in , then one has the bound for all , where .

Theorem 2 (Hoeffding-type inequality).

Let be a sequence of random variables with values in the unit interval , and let be a product disintegration of . Then, for any , it holds that

where .

Proof.

By applying the classical Hoeffding inequality to the probability measures , we have

Taking the expectation on both sides of the above inequality, and dividing by , yields the stated result. ∎

Notice that if is the canonical product disintegration of , then the above theorem is not very useful: indeed in this case we have , so the left-hand side in the inequality is zero. The above theorem also tells us that, for ,

so the rate at which as is governed by the rate at which as . To illustrate, let us consider two extreme scenarios, one in which for all (so that is exchangeable) and one in which the ’s are all mutually independent: in the first case, we have that , and thus the rate at which as depends only on the distribution of the random variable . On the other hand, if the ’s are independent, then we have that , and in this case the summands are independent random variables with values in the unit interval. Therefore, we can apply the classical Hoeffding inequality to these random variables to obtain the upper bound for (in fact, we already know that the upper bound holds, since independence of the ’s entails independence of the ’s).

Example 5.

Let where is a positive integer and . Given a sequence of -valued random variables, we shall write . Suppose is a product disintegration of . Equation (1) then yields, for all measurable sets , with and , the equality

An identity as above appears naturally in statistical applications, for instance when one observes samples of size , , , from distinct “populations” — we refer the reader to Petersen and Müller (2016) and references therein for details.

2.2 Convergence

Example 6 (Regime switching models).

Let and put with . The measures and are to be interpreted as distinct “regimes” (for example, expansion and contraction, in which case one would likely assume ). Let be a row stochastic matrix with stationary distribution . Let be a Markov chain with state space , initial distribution and transition probabilities . Notice that for all .

Assume is a sequence of -valued random variables and that is a product disintegration of . Then we have, for , that . We also have, for ,

| (3) | ||||

This shows that in general it may be difficult to compute the finite-dimensional distributions of the process — although this process inherits stationarity from . Also, an easy check tells us that generally speaking is not a Markov chain.

Nevertheless, assuming is irreducible and positive recurrent (i.e., ), we have by the ergodic theorem for Markov chains, that

| (4) |

for any bounded . Now let and consider the particular case where . Equation 4 becomes

| (5) |

Therefore, using Theorem 1 and then (5), we have that

holds almost surely. In particular this is true with ; thus, even though the ‘ups and downs’ of are governed by a law which can be rather complicated (as one suspects by inspecting equation (3)), we can still estimate the overall (unconditional) probability of, say, the expansion regime by computing the proportion of ups in a sample :

Example 7.

Suppose is a submartingale, with for all . By the Martingale Convergence Theorem, there exists a random variable such that almost surely (thus, we can assume without loss of generality that ). Furthermore, let and, for , let denote the random probability measure on defined via , and . We have a.s. Assume further that is a product disintegration of a sequence of random variables with values in . Using Theorem 1 we have

which means, the proportion of 1’s in approaches with probability one.

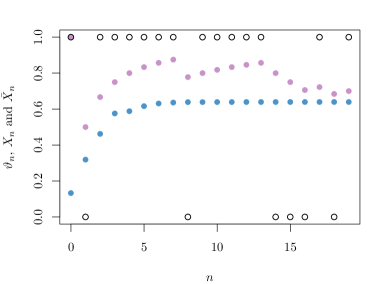

To illustrate, let be a sequence of independent and identically distributed Uniform random variables. Let and, for , define . Figure 1 displays, in blue, a simulated sample path of the submartingale up to . The ’s represent the successive outcomes of the coin throws (where the probability of ‘heads’ in the th throw is ). In purple are displayed the sample path of the means , where is the partial sum . In this model, even if we only observe the outcomes of the coin throws, we can still estimate the value of : all we need to do is to compute the proportion of heads in , with large.

The following lemma gives us a characterization of product disintegrations. It allows us to work with a requirement seemingly weaker than the almost sure validity of eq. (1) uniformly for all integer and Borel sets ; in practice, this lemma is merely a “rearrangement of quantifiers”. It will be used in the next example, the result itself as well as the reasoning used in its proof.

Lemma 3.

Let be a sequence of random variables taking values in a compact metric space , and let be a sequence of random probability measures on . Then is a product disintegration of if and only if for each and each -tuple of measurable subsets of , the equality (1) holds almost surely.

Proof.

The ‘only if’ part of the statement is trivial. For the ‘if’ part, let denote the product -field on . By Lemma 1.2 in Kallenberg (2002), coincides with the Borel -field corresponding to the product topology on , and therefore is a Borel space. By Theorem 6.3 in Kallenberg (2002), there exists an event with such that is a probability measure on for each .

Now let be a countable collection of sets of the form which generates . By assumption, for each there is an event with such that holds for . Thus, for , with , the probability measures and agree on a -system which generates , and therefore they agree on . This establishes the stated result. ∎

We now present an example where product disintegrations can be applied to a problem in finance.

Example 8 (Stochastic Volatility models).

This example demonstrates that a certain class of stochastic volatility models can be accommodated into our framework of product disintegrations. Stochastic volatility models are widely used in the financial econometrics literature, as they provide a parsimonious approach for describing the volatility dynamics of a financial asset’s return — see Shephard and Andersen (2009) and Davis and Mikosch (2009) and references therein for an overview. A basic specification of the model444Which can be relaxed by putting in place of , and allowing to evolve according to more flexible dynamics. is as follows: let and be centered iid sequences, independent from one another, and define and via the stochastic difference equations

where and are real constants and where follows some prescribed distribution. The random variable is interpreted as the return (log-price variation) on a given financial asset at date , and the ’s are latent (i.e, unobservable) random variables that conduct the volatility of the process . Usually this process is modelled with Gaussian innovations, that is, with and normally distributed for all . In this case the random variables are supported on the whole real line, so we need to consider other distributions for and if we want to ensure that the ’s are compactly supported.

Our objective is to show how Theorem 1 can be used to estimate certain functionals of the latent volatility process in terms of the observed return process . To begin with, notice that if and if is defined via the series , then (and ) is strictly stationary and ergodic, in which case we have that

| (6) |

almost surely, for any -integrable , where we write . Also, notice that, by construction, we have for all , all measurable and all ,

| (7) |

Where is yielded by the substitution principle, follows from the fact that and are independent (as only depends on ), and is just a matter of repeating the previous steps. A reasoning similar to the one used in the proof of Lemma 3 then tells us that is a product measure on for almost all . Also, notice that in particular we have that for all . In fact, let be defined via , for and measurable , where we write in place of for convenience. Since the ’s are identically distributed, we have in particular that for all . The preceding derivations now allow us to conclude that

| (8) |

We are now in place to introduce a product disintegration of , by defining for measurable , and . To see that is indeed a product disintegration of , first notice that is -measurable for every and every -tuple of measurable subsets of . Moreover, defining via , we obtain, by equations (7) and (8),

whence , and then Lemma 3 tells us that is — voilà — a product disintegration of .

Now, since is continuous and one-to-one, we have that is a homeomorphism from onto its range whenever is compact (in particular, is compact, hence measurable, in ). Also, as for all , we have that is well defined. Suppose now that is a given continuous function. We have

and, as is ergodic, it holds that where we know that the expectation is well defined, as with the expected value given by . We can now apply Theorem 1 to see that

The conclusion is that, for suitable of the form , we can estimate by the data as long as is large enough, even if we cannot observe . Of course, this follows from ergodicity of , but it is interesting anyway to arrive at this result from an alternate perspective; moreover, one can use Hoeffding type inequalities as in Example 4 to easily derive a rate of convergence for sample means of based on the rate of convergence of sample means of .

References

- Aldous (1985) D. J. Aldous. Exchangeability and related topics. In Lecture Notes in Mathematics, pages 1–198. Springer Berlin Heidelberg, 1985. URL https://doi.org/10.1007/bfb0099421.

- Davis and Mikosch (2009) R. A. Davis and T. Mikosch. Probabilistic properties of stochastic volatility models. In Handbook of financial time series, pages 255–267. Springer, 2009.

- Dawid (2013) A. P. Dawid. Exchangeability and its ramifications. In Bayesian Theory and Applications. Oxford University Press, 01 2013. URL 10.1093/acprof:oso/9780199695607.003.0002.

- Draper et al. (1993) D. Draper, J. S. Hodges, C. L. Mallows, and D. Pregibon. Exchangeability and data analysis. Journal of the Royal Statistical Society: Series A (Statistics in Society), 156(1):9–28, 1993. URL https://doi.org/10.2307/2982858.

- Kallenberg (2002) O. Kallenberg. Foundations of modern probability. Springer-Verlag, New York, 2002. URL http://dx.doi.org/10.1007/b98838.

- Konstantopoulos and Yuan (2019) T. Konstantopoulos and L. Yuan. On the extendibility of finitely exchangeable probability measures. Trans. Amer. Math. Soc., 371:7067–7092, 2019. URL https://doi.org/10.1090/tran/7701.

- Petersen and Müller (2016) A. Petersen and H.-G. Müller. Functional data analysis for density functions by transformation to a Hilbert space. The Annals of Statistics, 44(1):183 – 218, 2016. URL https://doi.org/10.1214/15-AOS1363.

- Shephard and Andersen (2009) N. Shephard and T. G. Andersen. Stochastic volatility: origins and overview. In Handbook of financial time series, pages 233–254. Springer, 2009.

- Taylor and Hu (1987) R. L. Taylor and T.-C. Hu. On laws of large numbers for exchangeable random variables. Stochastic Analysis and Applications, 5(3):323–334, 1987. URL https://doi.org/10.1080/07362998708809120.

3 Acknowledgements

The author Luísa Borsato was supported by grants 2018/21067-0 and 2019/08349-9, São Paulo Research Foundation (FAPESP).