Robustness of Bayesian ordinal response model against outliers via divergence approach

Abstract

Ordinal response model is a popular and commonly used regression for ordered categorical data in a wide range of fields such as medicine and social sciences. However, it is empirically known that the existence of “outliers”, combinations of the ordered categorical response and covariates that are heterogeneous compared to other pairs, makes the inference with the ordinal response model unreliable. In this article, we prove that the posterior distribution in the ordinal response model does not satisfy the posterior robustness with any link functions, i.e., the posterior cannot ignore the influence of large outliers. Furthermore, to achieve robust Bayesian inference in the ordinal response model, this article defines general posteriors in the ordinal response model with two robust divergences (the density-power and -divergences) based on the framework of the general posterior inference. We also provide an algorithm for generating posterior samples from the proposed posteriors. The robustness of the proposed methods against outliers is clarified from the posterior robustness and the index of robustness based on the Fisher-Rao metric. Through numerical experiments on artificial data and two real datasets, we show that the proposed methods perform better than the ordinary bayesian methods with and without outliers in the data for various link functions.

Keywords: Density-power divergence; -divergence; General bayesian inference; Link function; Ordered category; Robust inference

Mathematics Subject Classification: Primary 62F35; Secondary 62F15

1 Introduction

Ordered categorical data appear frequently in a wide range of fields such as medicine, sociology, psychology, political sciences, economics, marketing, and so on, and studies on their analysis methods have been quite active even today (Franses and Paap,, 2001; Rossi and Allenby,, 2003; Agresti,, 2010; Madahian et al.,, 2015; Agresti and Kateri,, 2017; Satake et al.,, 2018; Liu and Zhang,, 2018; Baetschmann et al.,, 2020). Ordered categorical data are, for example, the progression of a certain disease expressed as stage 1, 2, 3, or 4, or opinions on a certain policy expressed as opposition, neutrality, or approval. Additionally, when continuous data are summarized into categorical data, such as ages 0-20, 21-40, 41-60, 61-80, and 80 or more, the categorical data are ordered categorical data. For this reason, ordered categorical data are often considered to be discretized values of latent continuous variables. For more details on ordered categorical data, its traditional analysis methods, and related studies, we refer the reader to Agresti, (2010), which is a very excellent book.

The ordinal response model has been gaining popularity in regression for the ordered categorical data thanks to its interpretability and flexibility since it was proposed by a pioneering work Walker and Duncan, (1967) in this field. The ordinal response model is also being developed as a package in R (R Core Team,, 2022), one of the most popular programming languages today, and the ease that the analysis can be performed regardless of the maximum likelihood or Bayesian methods is another reason why the ordinal response model is often used. For details on the R packages for the ordinal response model, see Christensen, (2018). The ordinal response model is one of the frameworks of generalized linear models, and is called the ordinal regression model, or the cumulative link model since it connects the cumulative probability of belonging to a certain category to the covariates with the “link” function (McCullagh,, 1980). The link functions most commonly used the probit, logit, log-log, and complementary log-log (clog-log) links, which are the distribution function of the standard normal, logistic, right-skewed Gumbel, and left-skewed log-Weibull distributions, respectively. The formulation of the ordinal response model is described in Section 2. The inference methods in the ordinal response model are generally the maximum likelihood method (McCullagh,, 1980; Harrell,, 2001) and the Bayesian method with latent variables (Albert and Chib,, 1993; Nandram and Chen,, 1996), but these methods are known to be strongly affected by outliers in the data. An “outlier” in the ordinal response model is defined as a combination of ordered categorical data and its covariates that is heterogeneous relative to other pairs (Riani et al.,, 2011). This may be taken to mean that the combination of ordered categorical data and its covariates is inconsistent. Outliers can be caused by various reasons, such as typos in the values and misrecognition of units. One of the other common examples of outliers appearing is that in social surveys such as questionnaires, respondents sometimes submit incoherent answers due to their lack of interest in the issue.

There are various ways to check whether an inference method is robust against outliers in data, and inference in the frequentist framework may often use the influence function mentioned in Hampel, (1974). Simply put, the influence function is an index to check the “influence” of the data on an inference method, and its value must be at least bounded to be robust against outliers. This is because if the values diverge for certain data, the inference results will be almost entirely dependent on that data, ignoring other data. The influence function is desired to satisfy not only boundedness but also redescendence. While boundedness means that the influence from outliers is limited but a certain amount of influence still remains, redescendence means that the influence of large outliers on the inference can be ignored (Maronna et al.,, 2019). Hence, many robust inference methods based on the Huber-loss and robust divergences (Hampel et al.,, 1986; Basu et al.,, 1998; Jones et al.,, 2001; Fujisawa and Eguchi,, 2008; Huber and Ronchetti,, 2009; Ghosh and Basu,, 2013; Maronna et al.,, 2019; Castilla et al.,, 2021) have been studied so that the influence function satisfies boundedness and redescendence. However, most of them are focused on continuous, binary, or counted data.

In some studies on robust inference methods in the ordinal response model, Croux et al., (2013) and Iannario et al., (2017) proposed the weighted maximum likelihood methods using the Student, 0/1, and Huber weights so that the influence function is bounded. Scalera et al., (2021) derived a class of link functions for bounded influence functions in the maximum likelihood method in the ordinal response model, and Momozaki and Nakagawa, (2022) proved that the maximum likelihood method in the ordinal response model can no longer satisfy the redescendence of the influence function. Their contributions show that the maximum likelihood method in the ordinal response model does not allow robust and flexible analysis (the conditions derived by Scalera et al., (2021) are not satisfied by commonly used link functions such as the probit and logit links), and that more robust inference in the maximum likelihood method is no longer achievable. Unfortunately, Czado and Santner, (1992) showed that misspecification of the link function in binary regression causes a substantial bias in the parameter inferences, and it is confirmed that the same thing happens in the ordinal response model (Momozaki and Nakagawa,, 2022), so the inability to select the link function is very serious problem.

One way to solve these problems is to develop inference methods using robust divergences such as the density-power and -divergences (Basu et al.,, 1998; Jones et al.,, 2001; Fujisawa and Eguchi,, 2008), which have contributed to the development of robust inference methods in the framework of linear regression and others. Pyne et al., (2022) and Momozaki and Nakagawa, (2022) proposed the inference methods in the ordinal response model using the density-power and -divergences. Momozaki and Nakagawa, (2022) further derived conditions for the link function to satisfy both boundedness and redescendence of the influence functions in those inference methods. Since these conditions are satisfied by commonly used link functions such as the probit, logit, log-log, and clog-log link functions, their contributions allow analysts to perform robust and flexible analysis. Thus, in the framework of the frequentist approach, there is a certain amount of research on robust inference methods in the ordinal response model, although the number of such methods is limited. However, to the best of our knowledge, there are no studies on robust Bayesian inference methods in the ordinal response model, although there have been many studies on robust Bayesian inference on continuous, binary, or counted data.

In the Bayesian framework, there are methods to check whether the Bayesian inference method is robust against outliers in the data, such as the Bayesian version of the influence function mentioned in Ghosh and Basu, (2016) and Nakagawa and Hashimoto, (2020), or the index using the Fisher-Rao metric proposed in Kurtek and Bharath, (2015). Another method is to prove that the posterior robustness (Desgagné,, 2015), which is the property that the influence of outliers on the posterior distribution of parameters in a statistical model is negligible even if there are large outliers in the data, holds. There are also many studies on the Bayesian inference methods using the Huber-loss and robust divergences, for example, Kawakami and Hashimoto, (2023) proposed the linear model using the Huber-loss, Ghosh and Basu, (2016) proposed the inference method of mean parameter using the density-power divergence, Nakagawa and Hashimoto, (2020) proposed the inference method of mean and variance parameters using the -divergence, and Hashimoto and Sugasawa, (2020) proposed the inference method in the linear model using the -divergence. Jewson et al., (2018) provides a comprehensive review in Bayesian inferences with the robust divergences. Another robust Bayesian inference methods are those using distributions with the extremely heavy tail, for example, the log-Pareto truncated normal distribution proposed by Gagnon et al., (2020) and the extremely heavily-tailed distribution proposed by Hamura et al., (2022).

In this article, we prove that the posterior distribution of parameters based on the log-likelihood in the ordinal response model does not satisfy the posterior robustness with any link functions. Furthermore, to achieve robust Bayesian inference in the ordinal response model, we define general (synthetic) posteriors of the parameters based on the framework of the general (synthetic) posterior inference (Bissiri et al.,, 2016; Jewson et al.,, 2018; Bhattacharya et al.,, 2019; Miller and Dunson,, 2019; Nakagawa and Hashimoto,, 2020; Hashimoto and Sugasawa,, 2020), by replacing the log-likelihood function with two robust divergences, the density-power and -divergences. The robustness of these proposed methods against outliers is clarified from the posterior robustness and the index of robustness proposed by Kurtek and Bharath, (2015). Although sampling from the proposed posteriors is apparently intractable, we solve this problem by using the Bayesian bootstrap (Rubin,, 1981; Newton and Raftery,, 1994; Newton et al.,, 2021). Numerical experiments using several artificial data with varying outlier ratios show that the proposed methods achieve better estimation accuracy than conventional one, regardless of the presence or absence of outliers. Two real data applications are also used to demonstrate the usefulness of the proposed methods.

This article is organized as follows. Section 2 introduces the ordinal response model and the posterior distribution based on the log-likelihood. Section 3 defines Bayesian ordinal response models using the density-power and -divergences, and formulates the posteriors in those models. We also describe the sampling method from the proposed posteriors using the WLB method. Section 4 proves that posterior based on the log-likelihood in the ordinal response model does not satisfy the posterior robustness, and that the proposed posteriors in our robust Bayesian ordinal response models satisfies the posterior robustness. Section 5 confirms that the proposed Bayesian ordinal response models with the robust divergences are robust against outliers by numerical experiments using the index of robustness proposed by Kurtek and Bharath, (2015) and by applying them to artificial data and some real data. Section 6 provides the conclusion and some remarks.

2 Bayesian ordinal response model and its problems

In this section, we discuss the ordinal response model, several Bayesian inference methods in this model, and problems with those methods in the presence of outliers in data.

The probability mass function for an -th unit () in the ordinal response model can be expressed as

by considering the following latent variable model for ordered categorical data as the response variable.

| (1) |

for , where is called the (continuous) latent variable, (), the covariates , the coefficients , (known) and has the density function , the cutpoints , and the parameters for inference with . We refer to as the link function. For the identification, in the there is no error scale and the latent model has no the intercept term. Note that the observed data is , where and , and the latent variable is unobserved. The likelihood function in the ordinal response model is

| (2) |

Let be a prior distribution for the parameters . Then the (standard) posterior distribution of is given by

| (3) |

where denotes the set of observed data.

The posterior samplings of from equation (3) are generally intractable. Albert and Chib, (1993) addressed this problem in the probit and robit ( is the distribution function of the Student’s distribution) links by using the data augmentation method with latent variables . In the case of the probit link, assume the flat prior for (), the full conditional posterior of , (), and () are the multivariate normal, the uniform, and the truncated normal distributions, respectively, so the posterior samplings from these distributions are tractable. Note that Albert and Chib, (1993)’s method is known to reduce the effective sample size due to the high autocorrelation of Gibbs samplings of the cutpoints parameter . For the details to address this problem, see Nandram and Chen, (1996) and Sha and Dechi, (2019). Other methods for the posterior sampling of include the Hamiltonian Monte Carlo method (Duane et al.,, 1987; Neal,, 2003; Neal et al.,, 2011) and its extension the no-U-turn sampler (Hoffman et al.,, 2014), and in the R programming language, the brm and stan_polr functions in the brms (Bürkner,, 2017) and rstanarm (Goodrich et al.,, 2020) packages, respectively, using the probabilistic programming language Stan (Carpenter et al.,, 2017) are available for implementing them.

These Bayesian inferences in the ordinal response model are very useful for the analysis of ordered categorical data by virtue of their ease of implementation. However, when there are outliers in the data, i.e., when there are heterogeneous pairs of ordered categorical data and covariates compared to other pairs, a serious problem arises in the inference with the standard posterior (3) in the ordinal response model. We will illustrate this through a simple example.

Example 1.

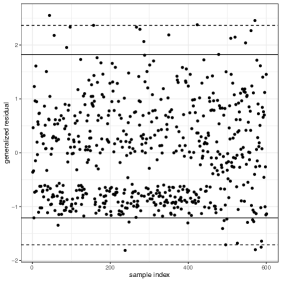

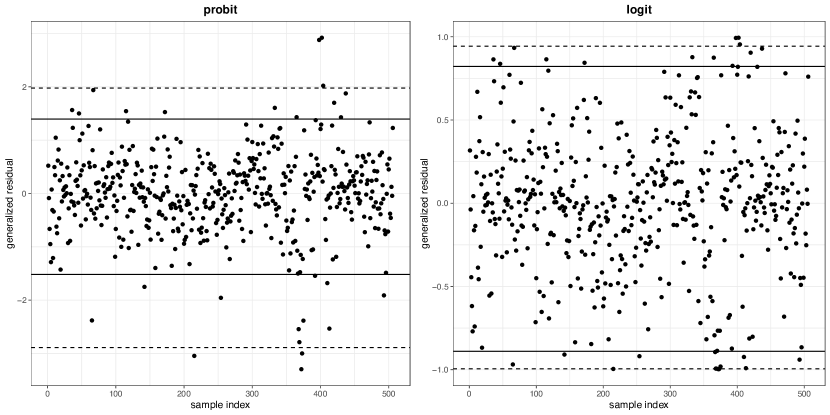

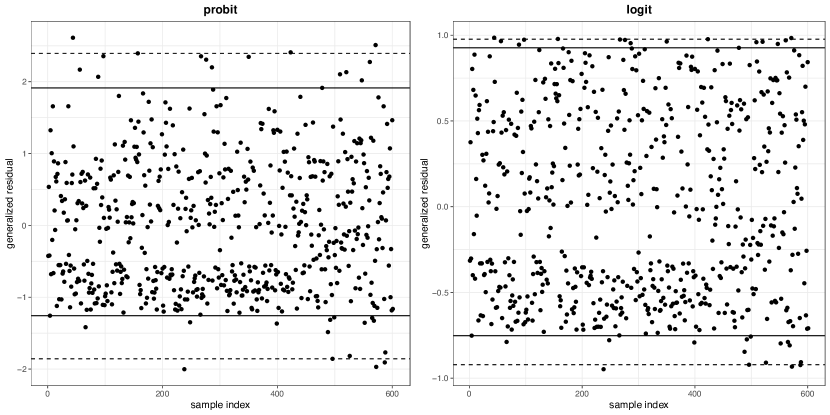

We consider the Affairs data (Fair,, 1978). The data contains 601 observations on three continuous, two binary, two ordered categorical, and two multinomial categorical variables. The ordered categorical response variable is the self rating of marriage, and we standardized three continuous valued covariates, transform one ordered categorical covariate by the Likert sigma method, and create dummy variables from the multinomial categorical covariates. Figure 1 shows the generalized residuals obtained by the Bayesian inference using the standard posterior (3) with the probit link for the Affairs data. The generalized residuals (Franses and Paap,, 2001) are calculated by

where () and () are the posterior means for the standard posterior. The solid and dashed lines in the figure show the 95% and 99% intervals of the generalized residuals, respectively. The large values of may indicate the presence of outlying observations (Franses and Paap,, 2001).

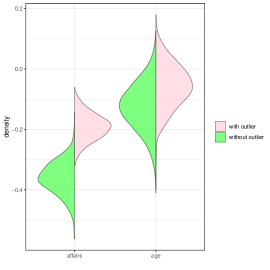

Figure 2 shows the standard posteriors for the coefficients of the “affairs” and “age” covariates using the original Affairs data and the modified data in which the absolute values of larger than the 95% interval are removed from the original data. The posteriors using the original and modified data are different, i.e., the posterior inference with the standard posterior is affected by outliers and does not satisfy the posterior robustness (Desgagné,, 2015). We prove that this phenomenon occurs in the posterior inference using the standard posterior (3) with arbitrary distribution function belonging to the parametric model (Theorem 1 in Section 4.1).

3 Robust bayesian ordinal response models via robust divergences

As described in Section 2, the Bayesian inference using the standard posterior (3) is strongly affected by outliers. To achieve robust Bayesian inference in the ordinal response model, we define general (synthetic) posteriors of the parameters based on the framework of the general (synthetic) posterior inference (Bissiri et al.,, 2016; Jewson et al.,, 2018; Bhattacharya et al.,, 2019; Miller and Dunson,, 2019; Nakagawa and Hashimoto,, 2020; Hashimoto and Sugasawa,, 2020), by replacing the log-likelihood function with two robust divergences, the density-power (Basu et al.,, 1998) and -divergences (Jones et al.,, 2001; Fujisawa and Eguchi,, 2008). Section 3.1 defines a general posterior in the ordinal response model with the density-power divergence in the form of Ghosh and Basu, (2016). Sections 3.2 and 3.3 define synthetic and general posteriors in the ordinal response model with Hashimoto and Sugasawa, (2020)’s and Nakagawa and Hashimoto, (2020)’s forms of the -divergence, respectively. Section 3.4 describes the method of the posterior computation based on our general posteriors.

3.1 Case: density-power divergence

Here, we use the following form of the density-power divergence in Ghosh and Basu, (2016).

where

and is a tuning parameter that controls the robustness. Note that when , reduces to the log-likelihood function, and in the second term, the summation is used instead of the integral since is the discrete variable.

Then, using the density-power divergence , we define the following general posterior in the ordinal response model, which will be referred to as the density-power posterior hereafter.

| (4) |

where . Note that since the density-power posterior is equivalent to the standard posterior (3) when , the density-power posterior may be regarded as a natural extension of the standard posterior (3).

We briefly confirm the proposed density-power posterior (4) is robust against outliers. Suppose that the observation is outlier compared to the other data, i.e., is large enough. Then, since takes a small value, the density-power divergence for the unit is expressed as

Thus, the density-power posterior (4) is expressed as

Namely, the density-power posterior (4) can be expressed by removing the outlier , and as a result, the influence of the outlier can be ignored in the posterior inference.

3.2 Case: -divergence of the form in Hashimoto and Sugasawa, (2020)

Here, we use the following form of -divergence in Hashimoto and Sugasawa, (2020).

where

and is a tuning parameter that controls the robustness. Note that when , reduces to the log-likelihood function, and in , the summation is used instead of the integral since is the discrete variable.

Then, using the -divergence , we define the following synthetic posterior in the ordinal response model, which will be referred to as the -synthetic posterior hereafter.

| (5) |

where . Note that since the -synthetic posterior is equivalent to the standard posterior (3) when , the -synthetic posterior may be regarded as a natural extension of the standard posterior.

We briefly confirm the proposed -synthetic posterior (5) is robust against outliers. Suppose that the observation is outlier compared to the other data, i.e., is large enough. Then, in terms of the similar manner of the previous subsection, since takes a small value, the -divergence for the unit is expressed as

Thus, the -synthetic posterior (5) is expressed as

Namely, the -synthetic posterior (5) can be expressed by removing the outlier , and as a result, the influence of the outlier can be ignored in the posterior inference.

3.3 Case: -divergence of the form in Nakagawa and Hashimoto, (2020)

Here, we use the following form of -divergence in Nakagawa and Hashimoto, (2020).

where

and is a tuning parameter that controls the robustness. Note that when , reduces to the log-likelihood function.

Then, using the -divergence , we define the following general posterior in the ordinal response model apart from (5), which will be referred to as the -general posterior hereafter.

| (6) |

where and . Note that since the -general posterior is equivalent to the standard posterior (3) when , the -general posterior (6) may also be regarded as a natural extension of the standard posterior.

We briefly confirm the proposed -general posterior (6) is robust against outliers. Suppose that the observation is outlier compared to the other data, i.e., is large enough. Then, in terms of the similar manner of the previous subsection, since takes a small value, , and thus the -general posterior (6) is expressed as

Namely, the -general posterior (6) can also be expressed by removing the outlier , and as a result, the infuluence of the outlier can be ignored in the posterior inference.

Remark.

In the framework of the general posterior inference, the general Bayesian posterior is defined by

where is the learning rate and is the loss function defined additively for the observations , i.e., . Since the -synthetic posterior is not define by an additive loss function, we use the term “synthetic”. There have been many studies on how to choose the learning rate , also known as the calibration weight or loss scale (Grünwald and van Ommen,, 2017; Holmes and Walker,, 2017; Lyddon et al.,, 2019; Syring and Martin,, 2019; Wu and Martin,, 2023). In this article, we set according to Section 2.3.2 of Jewson et al., (2018).

3.4 Posterior draws from proposed robust posteriors

Consider how to draw the posterior samples from our proposed robust posteriors (4), (5), and (6). Since these posteriors do not have simple forms, the posterior sampling of is intractable. To solve this problem, we use the weighted likelihood bootstrap (WLB) method. WLB is an approximate sampling method proposed by Newton and Raftery, (1994), whereby the posterior sampling from the posterior is obtained from the minimal solution of the weighted objective function.

The weighted objective functions in our proposed robust posteriors (4), (5) and (6) are

| (7) |

| (8) |

and

| (9) |

where , respectively. Note that although the solution of the minimization problem in the weighted objective function is an approximate posterior sampling, Lyddon et al., (2018) and Newton et al., (2021) show that its approximation error is negligible when is sufficiently large.

This sampling method does not depend on the previous posterior samples of and to draw the current posterior sample of the parameters and . This means that the autocorrelation in each of and in this algorithm may be very small. This is particularly useful in the sense that it solves the problem of autocorrelation among the posterior samples of , which is a bottleneck in Albert and Chib, (1993)’s method.

Remark.

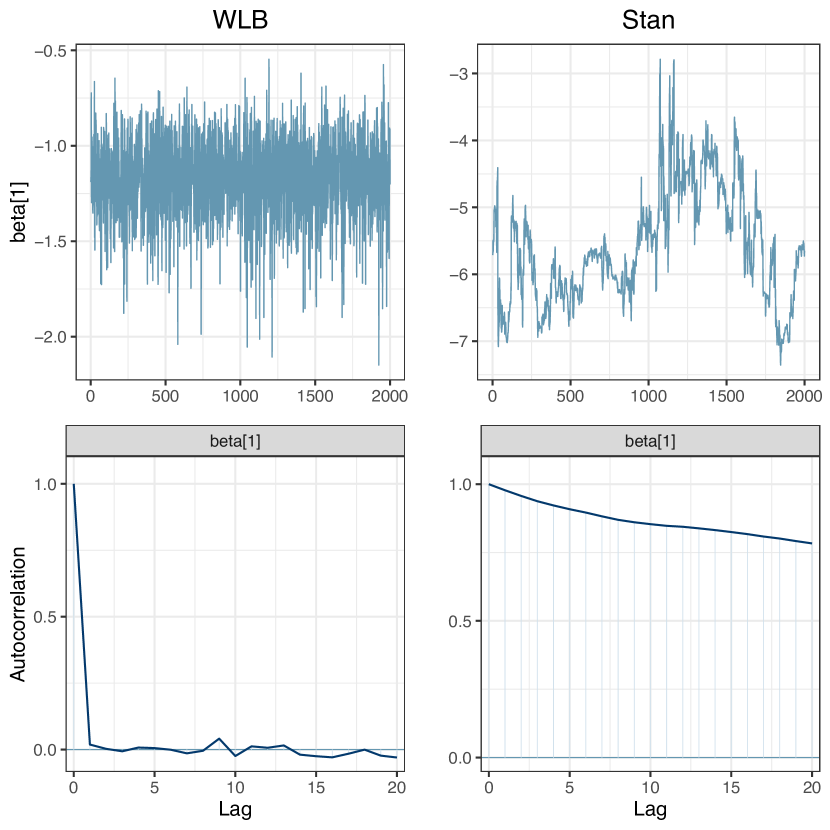

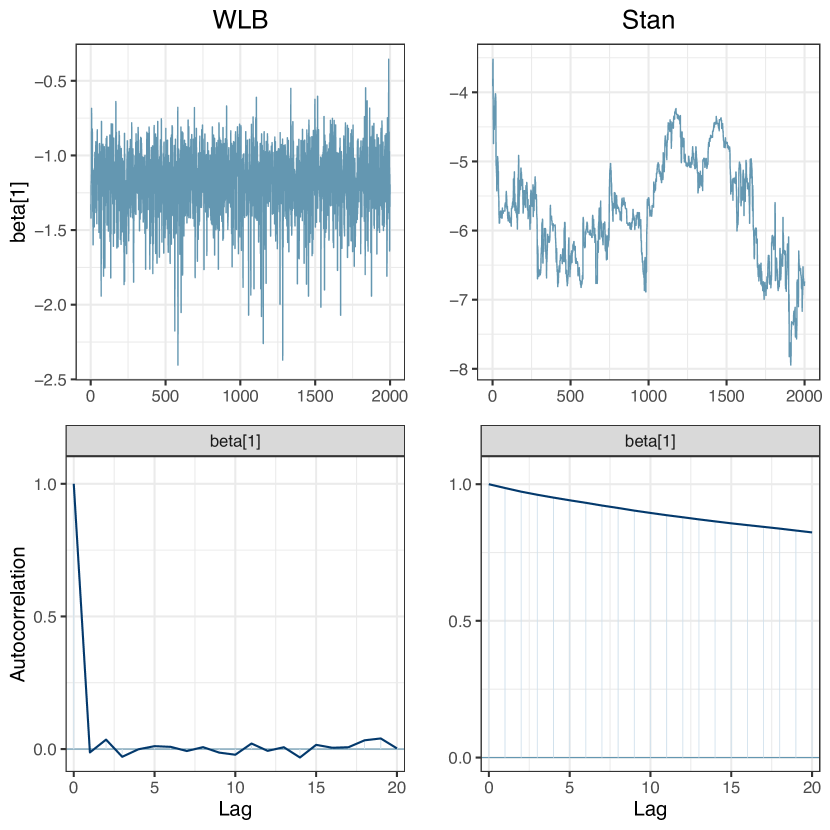

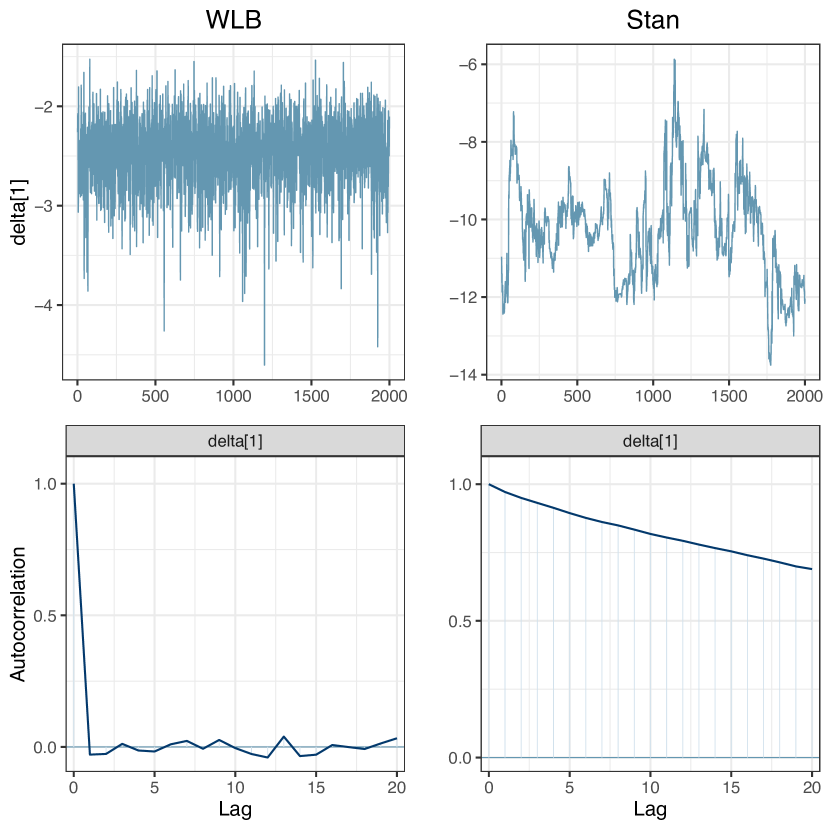

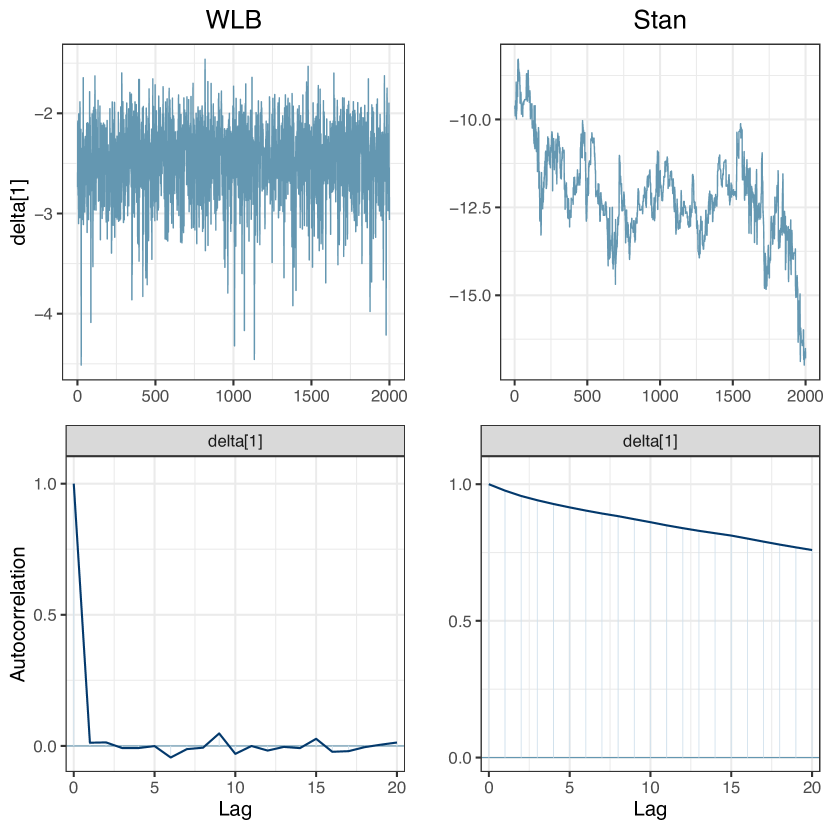

Sampling from the posterior distributions (4), (5), and (6) can be implemented using the probabilistic programming language Stan in addition to the method using the WLB. However, it uses the Hamiltonian Monte Carlo method, which is one of the MCMC methods, and depending on the structure of the data, the computational performance may be poor in terms of the number of effective samplings. In particular, the performance tends to deteriorate as the number of dimensions increases. We will illustrate this through a simple example. Suppose that an ordered categorical data is generated from (1) with and , where is generated from with the identity matrix , is generated from , , and . Note that this is the ordinal probit model, that is, the link function in the ordinal response model is the probit link. We obtain the 2000 posterior draws with the WLB. In the method with the Stan, 500 of the 2500 posterior draws are discarded as burn-in and the rest are used.

Figures 3 and 4 show trace plots and autocorrelations for the draws of and from the density-power and -general posteriors (4), (6) with the WLB and Stan. As can be seen from these figures, in the case of the WLB, solving the minimization problem of weighted objective function, independent posterior draws can be obtained, hence the mixing is quite well and the autocorrelation is negligible. Contrarily, the Stan algorithm causes poor mixing and quite high autocorrelation. More unfortunately, as p grows, the posterior draws with the Stan are sampled far away from the true values of the parameters (, in this simulation). Even increasing the length of MCMC sequences does not resolve this problem at all, and in our experience, such a situation is more likely to occur when is larger than 15. In this simulation, we used 0.5 as the value of the tuning parameter, but other values did not change the results of the mixing and autocorrelations. The results for the -synthetic posterior (5) are not different from those for the -general posterior (6), so we omit the details.

4 Posterior robustness of standard and proposed posteriors

The previous section defined the general (synthetic) posteriors (4), (5), (6) in the ordinal response model using the density-power and -divergences, and developed the robust Bayesian ordinal response model. In this section, we prove that our three robust posteriors (4), (5), (6) are robust against outliers in terms of the posterior robustness (Desgagné,, 2015), including the standard posterior (3). Before proving the posterior robustness, we redefine the notation for outliers with the similar manner of Desgagné and Gagnon, (2019).

The set of indices for observations, , is divided into two mutually disjoint subsets, and , and let denote the set of indices that are not outliers and denote the set of outlier indices. Note that and is the empty set. Let denote the -th observation and be the set of the observed data. The set of the non-outlying observations is defined by . Then the (non-)outliers for the observed values are defined as

where , which describes the direction of outlier, and . If is sufficiently large, the value of for is extremely large, either positively or negatively due to , i.e., the observation is outlier. Note that a large value of means a large absolute value of generalized residuals (see Example 1).

4.1 Case: standard posterior

For the standard posterior (3) in the ordinal response model, the following theorem on the posterior robustness holds.

Theorem 1.

Assume that the probability density function of the distribution is proper. Then,

holds.

Theorem 1 implies that the standard posterior in the ordinal response model cannot satisfy the posterior robustness, i.e., the posterior inference without removing the influence of outliers is not possible with the conventional Bayesian ordinal response model. In the inferences of the location and scale parameters, and the linear regression, it is several well-known results that the posterior robustness can be satisfied by using the heavy-tailed distributions (O’Hagan and Pericchi,, 2012). For example, Gagnon et al., (2020) and Hamura et al., (2022) prove that the standard posterior in the linear regression satisfies the posterior robustness by using the extremely heavy tail distribution whose order of the tail is same as (e.g., the log-Pareto tailed normal and extremely heavily-tailed distributions). Interestingly, however, the standard posterior in the ordinal response model requires the distribution of to have the tail of order smaller than , so the standard posterior (3) cannot satisfy the posterior robustness even if the extremely heavy tail distribution is used, which can achieve the posterior robustness in the linear regression. It is also important to note that the standard posterior (3) with the distribution that satisfies the regularly varying (O’Hagan and Pericchi,, 2012), such as the Student’s -distribution and the Cauchy distribution, cannot satisfy the posterior robustness.

4.2 Case: general (synthetic) posteriors

For the proposed general (synthetic) posteriors (4), (5), (6) in the ordinal response model, the following theorems on the posterior robustness hold.

Theorem 2.

Assume that is proper. Then the density-power posterior (4) satisfies the posterior robustness, i.e.,

where are the density-power posterior that is conditioned by the full dataset , and are the density-power posterior that is conditioned by the dataset without the outliers .

Theorem 3.

Assume that is proper. Then the -synthetic posterior (5) satisfies the posterior robustness, i.e.,

where are the synthetic -posterior that is conditioned by the full dataset , and are the synthetic -posterior that is conditioned by the dataset without the outliers .

Theorem 4.

Assume that is proper. Then the -general posterior (6) satisfies the posterior robustness, i.e.,

where are the general -posterior that is conditioned by the full dataset , and are the general -posterior that is conditioned by the dataset without the outliers .

While the standard posterior (3) in the conventional Bayesian ordinal response model could not satisfy the posterior robustness, the general (synthetic) posteriors (4), (5), (6) in our state-of-the-art robust Bayesian ordinal response model can satisfy the posterior robustness for any distribution function . Namely, the Bayesian inference with these general (synthetic) posteriors gives a choice of the link function to those analyzing data that may (or may not) contain outliers, and provides robust and flexible results against outliers.

5 Numerical experiments

5.1 Bayesian robustness property

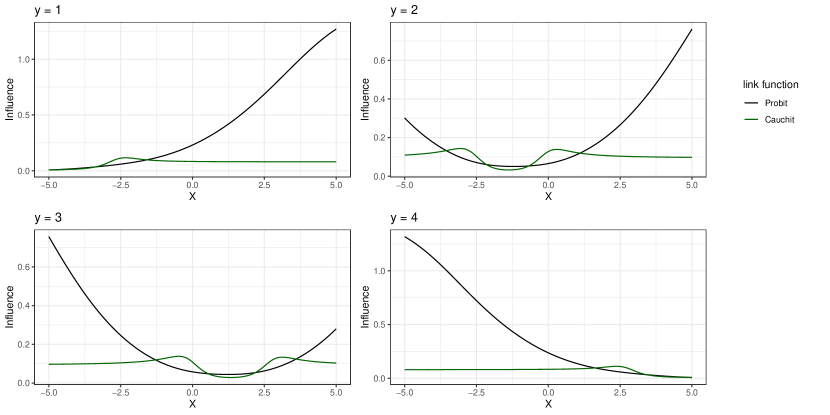

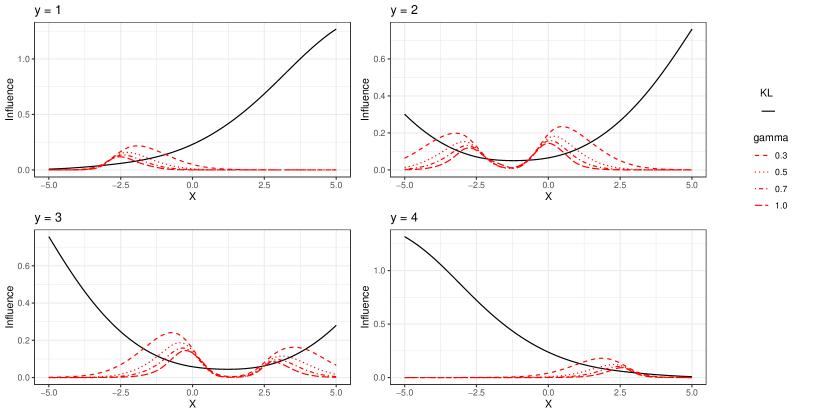

This section demonstrates that our proposed robust Bayesian ordinal response model is robust against outliers through a numerical experiment using the robustness index proposed by Kurtek and Bharath, (2015). The robustness index represents the influence of each individual data on the inference, i.e., the value of the index should be small for heterogeneous individual data.

In this numerical experiment, we employ the following simple ordinal response model as the data generation process.

where , , is a value that ticks from to 5 in increments of 0.05, and . As comparison methods with our proposed robust Bayesian ordinal response model, we use the conventional Bayesian ordinal response model with the probit and cauchit (the distribution function of the Cauchy distribution) links as the link function. In our proposed robust Bayesian ordinal response model, the probit link is used as the link function, and both the density-power and -divergences set the tuning parameter of the robust divergences to 0.3, 0.5, 0.7, and 1.0. To run the conventional Bayesian ordinal response model, we use the function stan_polr of the rstanarm package in the R programming language. For all Bayesian inferences performed in this numerical experiment, 2500 samples are taken, of which 500 are burn-in.

Figure 5 shows the values of robustness index of Kurtek and Bharath, (2015) when using the conventional Bayesian ordinal response model with the probit (black line) and cauchit (green line) links. It can be seen that the values of the index is considerably large for heterogeneous individual data in the conventional Bayesian ordinal response model with the probit link. Here, the heterogeneous data means, for example, (upper left panel of Figure 5), where may be negative in the latent variable model used in this numerical experiment, so that the data where and is positive may be said to be heterogeneous. In contrast to the case with the probit link, the values of the robustness index in the conventional Bayesian ordinal response model with the cauchit link are small even for heterogeneous individual data, but the value is not zero. This means that the conventional Bayesian ordinal response model with the cauchit link can suppress the influence of heterogeneous data to some extent, but cannot eliminate it completely.

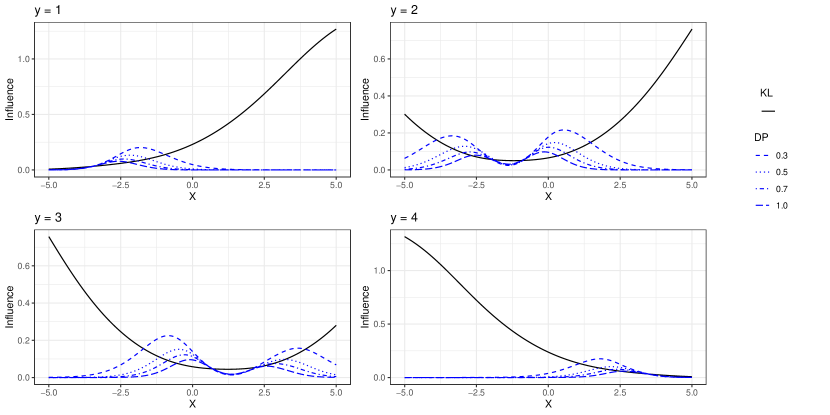

Figures 6 and 7 show the values of the robustness index when using the density-power posterior (4) and -general posterior (6) in our proposed robust Bayesian ordinal response model, respectively. The black line represents the values of the index when using the conventional Bayesian ordinal response model with the probit link (posterior with the Kullback-Leibler loss). The results using the -synthetic posterior (5) show almost the same behavior as those using the -general posterior (6), so the output is omitted in this numerical experiment. As can be seen from these results, the values of the index in our proposed robust Bayesian ordinal response model with the robust divergences approaches zero for heterogeneous data. Namely, our method not only suppresses the influence of heterogeneous data, but also completely eliminates it, indicating that our method can achieve a more robust inference than the conventional Bayesian ordinal response model.

5.2 Simulation studies

This section evaluates the performance of our proposed robust Bayesian ordinal response model through this numerical experiments. In order to compare with the conventional Bayesian ordinal response model, we perform some simulation studies referring to Section 5 of Scalera et al., (2021). We employ the following ordinal response model as the data generation process.

where with outlier ratio , , and and are mutually independent. The random variable is distributed as the standard normal, logistic, and Gumbel, and in this numerical experiment, we use the link function corresponding to the error distribution, for example, if has the standard normal distribution, then we use the probit link. This is because it is well known that the misspecification of the link function can cause a substantial bias in the inference. The development of a doubly robust Bayesian ordinal response model for both outliers and the link misspecification is a future work. We set the values of the regression coefficients and cutoffs as follows according to the error distribution.

-

•

When is distributed as the standard normal:

-

•

When is distributed as the standard logistic:

-

•

When is distributed as the Gumbel:

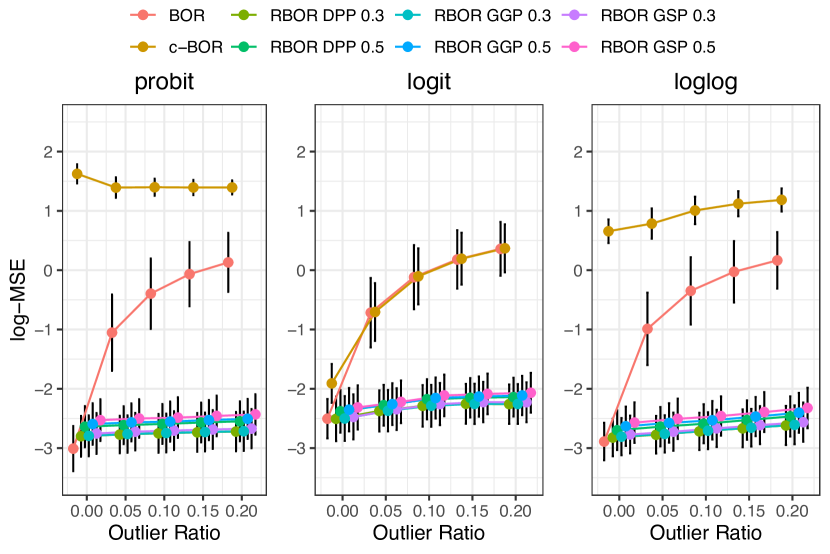

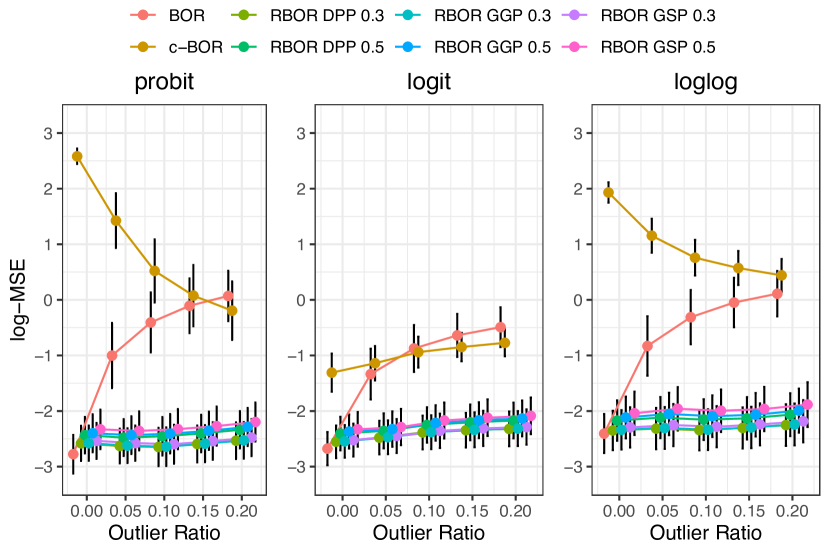

With the above settings, we apply our proposed Bayesian ordinal robust model with the density-power posterior (RBOR DPP), -synthetic posterior (GSP), and -general posterior (GGP) to these data and generate 2000 posterior samples using the WLB method. The tuning parameters ( and ) for the density-power and -divergences are set to 0.3 and 0.5. For comparison, we apply the non-robust Bayesian ordinal response model with the standard posterior (BOR) and generate 2500 posterior samples using the function stan_polr of the rstanarm package in the R, 500 of which are burn-in. The Bayesian inference with the standard posterior distribution using the cauchit link (c-BOR), which is the distribution function of the Cauchy distribution, is also included in the comparison with our methods. This is because indeed, as mentioned earlier, the cauchit link does not satisfy the posterior robustness, and the misspecification of the link function can cause a substantial bias in the parameter estimation, but from the numerical experiment using the robustness index in Section 5.1, the Bayesian inference using the cauchit link seems to give more robust inference results against outliers than using the probit link. For the point estimates of , we use their posterior means and evaluate their performance in terms of mean squared error (MSE) defined by with the number of parameters. We also use coverage probabilities (CP) defined by to evaluate credible intervals (CI) of . The 200 observations are generated by the above data generation processes and these values are computed for each of the 100 replicates of the artificial dataset and averaged.

Figure 8 plots the logarithm of MSE (log-MSE) values with estimated Monte Carlo error bars of each method for each outlier ratio. In the absence of outliers, our proposed robust methods (RBOR DPP, GSP, and GGP) perform as well as the conventional BOR methods. When the outlier ratio increases, the performance of BOR deteriorates, while the performance of our proposed robust methods remains almost the same. The c-BOR method using the cauchit link is found to have bounded values of the robustness index of Kurtek and Bharath, (2015) as shown in Figure 5 of Section 5.1, but the parameter estimation is adversely affected due to the misspecification of the link function. Tables 1 and 2 present the results for the CP of the 95% credible intervals regarding the interval estimation for the coefficient parameters and the cutoff parameters . These results show that our proposed robust methods perform as well as the conventional BOR method even in the interval estimation when there are no outliers. As the outlier ratio increases, the CPs of our robust methods remain around the nominal level, while those of the BOR method become smaller than the nominal level. The c-BOR method with the cauchit link has quite low CPs due to the misspecification of the link function, as in the case of log-MSE.

| BOR | c-BOR | RBOR DDP | RBOR GSP | RBOR GGP | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| link | 0.3 | 0.5 | 0.3 | 0.5 | 0.3 | 0.5 | |||||

| 0% | 93.7 | 29.3 | 91.7 | 94.0 | 92.0 | 92.7 | 92.0 | 93.3 | |||

| 5% | 48.3 | 31.2 | 93.3 | 94.2 | 93.5 | 93.5 | 93.5 | 93.7 | |||

| probit | 10% | 33.3 | 31.1 | 92.2 | 93.0 | 92.1 | 92.4 | ||||

| 15% | 25.5 | 31.5 | 92.8 | 93.0 | 92.7 | 92.3 | |||||

| 20% | 20.7 | 31.5 | 93.0 | 93.1 | 92.9 | 92.4 | |||||

| 0% | |||||||||||

| 5% | |||||||||||

| logit | 10% | ||||||||||

| 15% | |||||||||||

| 20% | |||||||||||

| 0% | |||||||||||

| 5% | |||||||||||

| loglog | 10% | ||||||||||

| 15% | |||||||||||

| 20% | |||||||||||

| BOR | c-BOR | RBOR DDP | RBOR GSP | RBOR GGP | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| link | 0.3 | 0.5 | 0.3 | 0.5 | 0.3 | 0.5 | |||||

| 0% | |||||||||||

| 5% | |||||||||||

| probit | 10% | ||||||||||

| 15% | |||||||||||

| 20% | |||||||||||

| 0% | |||||||||||

| 5% | |||||||||||

| logit | 10% | ||||||||||

| 15% | |||||||||||

| 20% | |||||||||||

| 0% | |||||||||||

| 5% | |||||||||||

| loglog | 10% | ||||||||||

| 15% | |||||||||||

| 20% | |||||||||||

Remark (Selection of tuning parameters, and ).

Robust divergences such as the density-power and -divergences have one tuning parameter to control the robustness against outliers (e.g., and ). If the value of the tuning parameter is smaller than required, the inference result may still be affected by outliers, and conversely, if it is unnecessarily large, the inference may lose the statistical efficiency (Basu et al.,, 1998). Therefore, it is necessary to select the optimal tuning parameter, but there are few studies discussing the tuning parameter selection method in the Bayesian inference with the robust divergence. One method is to use the asymptotic relative efficiency, as in the frequentist framework. Ghosh and Basu, (2016) discuss the case where there is only one parameter to be estimated, and Nakagawa and Hashimoto, (2021) generalizes the method. Nakagawa and Hashimoto, (2021) further state that it is difficult to ensure both the robustness and statistical efficiency when the data are heavily contaminated. Warwick and Jones, (2005) and Basak et al., (2021) propose frequentist methods to chose the optimal value of the tuning parameter using the asymptotic mean squared errors. Although it may be considered natural to use the model evidence or marginal likelihood as a method to find the optimal tuning parameter in the Bayesian framework, Yonekura and Sugasawa, (2023) show that such a method is not useful for unnormalized statistical models such as our proposed model. Recently, Yonekura and Sugasawa, (2023) proposed a sequential Monte Carlo method (Del Moral et al.,, 2006) for simultaneously sampling from the posterior distribution and selecting the tuning parameter in unnormalized statistical models using the Hyvärinen score (Hyvärinen and Dayan,, 2005). They avoid the pilot plot (estimate) problem used in the methods of Warwick and Jones, (2005) and Basak et al., (2021) and ensure the stable inference and statistical efficiency. Applying the method of Yonekura and Sugasawa, (2023) to the Bayesian ordinal response model requires the development of another computational algorithm based on the sequential Monte Carlo method, and will be the subject of future research.

5.3 Real data analysis

This section compares analysis results of our proposed robust Bayesian ordinal response models with those of the non-robust Bayesian ordinal response model through two real datasets: Boston housing data (Harrison and Rubinfeld,, 1978) and Affairs data (Fair,, 1978). The Boston housing data is often used to evaluate the robust inference methods with continuous data as the response variable (Hashimoto and Sugasawa,, 2020; Hamura et al.,, 2022; Kawakami and Hashimoto,, 2023). Here, the corrected median value of owner-occupied homes in USD 1000’s is transformed into the ordered categorical data with five categories (), and used it as the response variable. The Boston housing data has 506 observations and 14 variables, including one binary and 13 continuous variables. The Affairs data has 601 observations and nine variables, including three continuous, two binary, two ordered categorical, and two multinomial categorical variables. The self-rating of marriage, one of the ordered categorical data, is set as the response variable. In the two real data, the continuous data are standardized to have a mean of zero and variance of one, the ordered categorical data in the covariates is numerically transformed using the Likert sigma method, and the multinomial categorical data are transformed using the dummy variables. In analyzing the two sets of real data, we use the commonly used symmetric link functions, the probit and logit links. Figures 9 and 10 show the generalized residuals (Franses and Paap,, 2001) plots with two link functions for two real datasets. The 95% and 99% intervals of the generalized residuals are indicated in these figures as the solid and dashed lines, respectively. As can be seen from these figures, since some of the data are well outside the solid line of the 95% interval, the Boston housing data and the Affairs data may contain outliers.

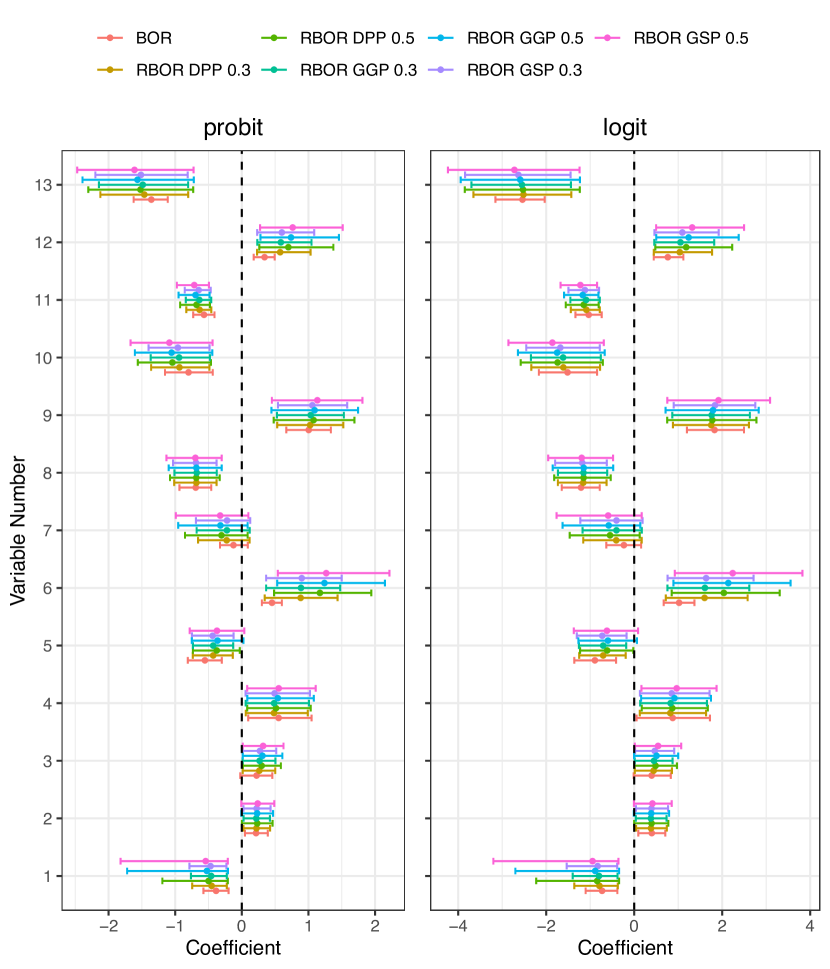

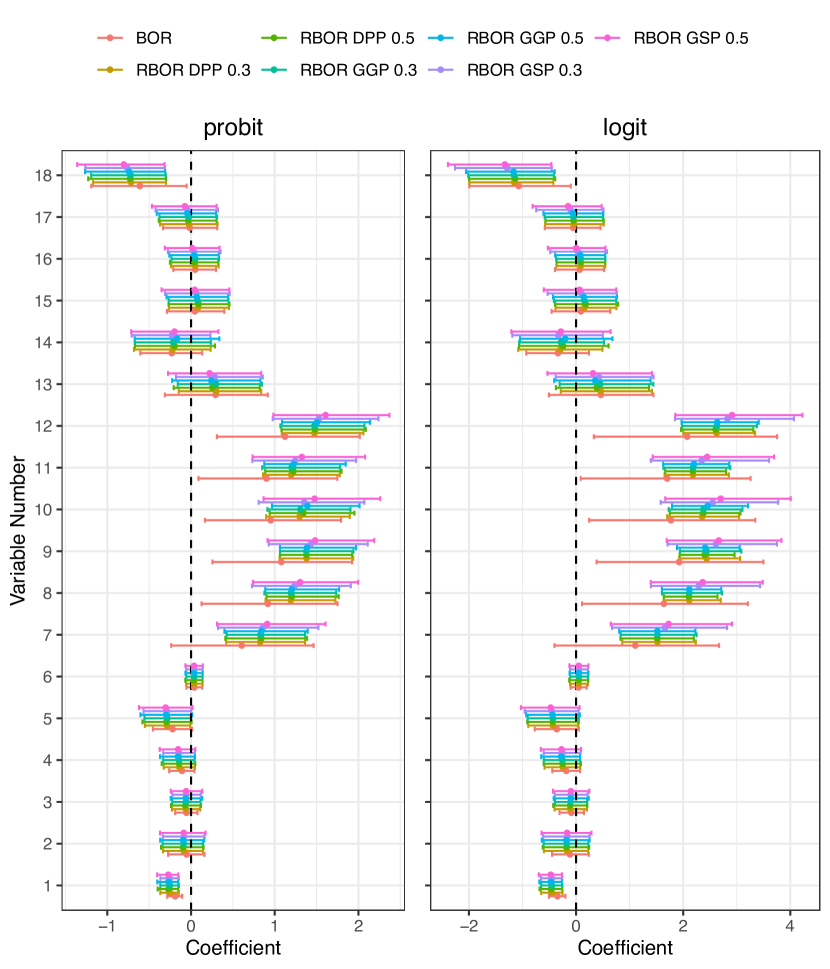

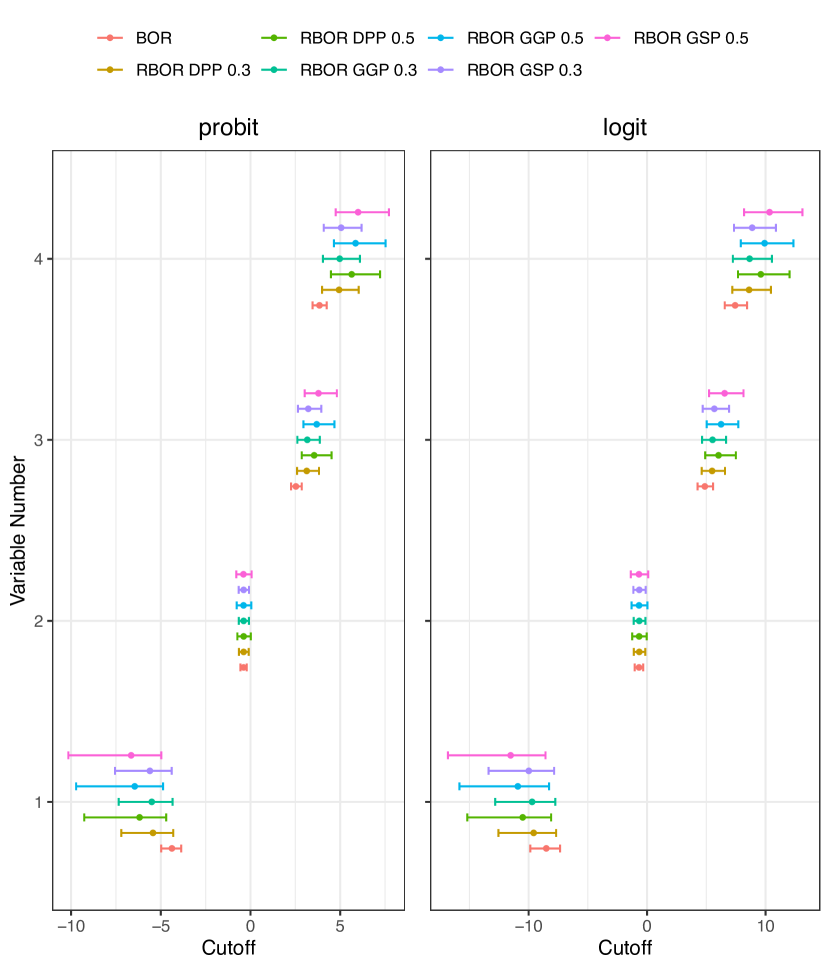

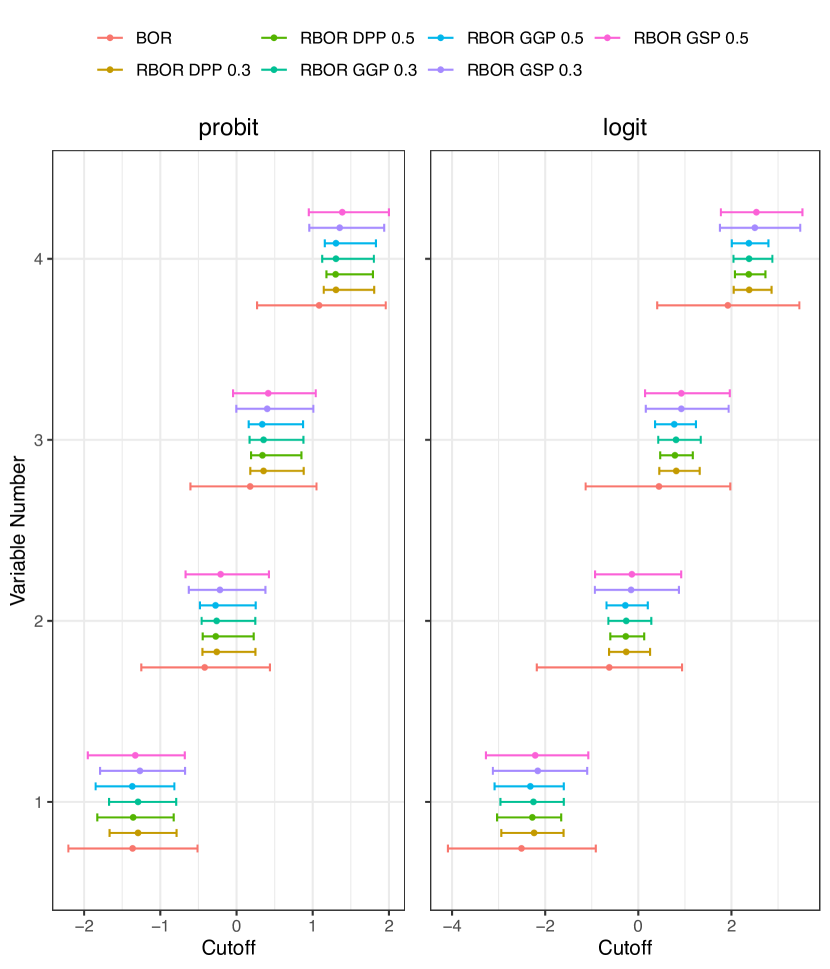

We apply our proposed Bayesian ordinal robust model with the density-power posterior (RBOR DPP), -synthetic posterior (GSP), and -general posterior (GGP) to these data and generate 2000 posterior samples using the WLB method. The tuning parameters ( and ) for the density-power and -divergences are set to 0.3 and 0.5. For comparison, we apply the non-robust Bayesian ordinal response model with the standard posterior (BOR) and generate 2500 posterior samples using the function stan_polr of the rstanarm package in the R, 500 of which are burn-in. The posterior medians and 95% credible intervals are calculated using the 2000 posterior samples obtained for all methods. Figures 11 and 12 show the 95% credible intervals and posterior medians of the coefficient and cutoff parameters applying the proposed robust Bayesian ordinal response model and the non-robust Bayesian ordinal response model with the probit and logit link to the Boston housing data and the Affairs data. From these figures, we can see that the proposed robust method, RBOR, and the non-robust method, BOR, show different results in the inference of some parameters. Particularly, in Figure 11, for variable number 3 in the Boston housing data and variable number 7 in the Affairs data, the credible intervals in the BOR includes 0, but not in the RBOR. Additionally, for variables number 2 and 5 in the Boston housing data, the credible intervals in the BOR do not include 0, but some of the RBORs do. Since the positions of the credible intervals and the posterior medians of the parameters are different in many cases between the BOR and RBOR, both the Boston housing data and the Affairs data may contain outliers.

6 Conclusion and remarks

This article addressed the problem induced by outliers on the ordinal response model, which is a regression on an ordered categorical data as the response variable, in the Bayesian framework. Through the application of the Affairs data (Fair,, 1978) (Example 1 in Section 2), we confirmed that the posterior distribution in the conventional Bayesian ordinal response model based on the likelihood (3) does not satisfy the posterior robustness, i.e., the posterior distribution differs between cases with and without large outliers. Furthermore, we proved that the standard posterior cannot satisfy the posterior robustness with the distribution function (link function) of any distribution that belongs to the parametric distribution (Theorem 1 in Section 4.1). Meanwhile, the robustness against outliers on the ordinal response model in the framework of the frequentist has been addressed by Scalera et al., (2021) and Momozaki and Nakagawa, (2022). Scalera et al., (2021) derives conditions for the link function such that the influence function satisfies the boundedness, and shows that the Student’s and Cauchy distributions satisfy the conditions. Momozaki and Nakagawa, (2022) proved that the influence function cannot satisfy the redescendence, i.e., it cannot completely eliminate the influence of large outliers in the ordinal response model with arbitrary link function. Thus, the redescendence of the influence function in the frequentist framework and the posterior robustness in the Bayesian framework may be related.

In order to achieve robust Bayesian inference in the ordinal response model, we proposed state-of-the-art robust Bayesian ordinal response models with two robust divergences, the density-power and -divergences, based on the general (synthetic) posterior inference. We also proved that our proposed posteriors satisfy the posterior robustness (Theorems 2, 3, and 4 in Section 4). Furthermore, we proposed an algorithm for generating posterior samples from our proposed posteriors using the weighted likelihood bootstrap (WLB) method. As described in the remark in Section 3.4, it is possible to generate the posterior samples using the probabilistic programming language Stan based on the Hamiltonian Monte Carlo method instead of the WLB method. However, we recommend the use of the algorithm based on the WLB method because the algorithm based on the WLB method generates independent samples and thus can ignore the mixing problem in the posterior samples, and the algorithm based on the Stan does not work well when the dimension of parameters is large. Using the index of robustness based on the Fisher-Rao metric proposed in Kurtek and Bharath, (2015), we also showed that our proposed robust methods are robust against outliers, i.e., can ignore the influence of large outliers (Section 5.1). Furthermore, using several artificial data with varying outlier ratios, we demonstrated that our proposed methods perform as well as the conventional method when there are no outliers, and that as the outlier ratio increases, the conventional method performs worse, while our proposed methods still perform well (Section 5.2). In applications using two real datasets, the Boston housing and Affairs data, that seem to include outliers from the values of the generalized residuals, our proposed methods and the conventional method yield different analysis results in terms of significant variables (Section 5.3).

The posteriors in our proposed robust Bayesian ordinal response model satisfy the posterior robustness even with the commonly used link functions such as the probit, logit, and complementary loglog links. This fact is a significant contribution to the analysts using the ordinal response model as it provides them with robust and flexible analysis methods for data with outliers. As confirmed in the numerical experiments in Section 5.2, the misspecification of the link function causes a substantial bias in the inference. It would be very important for analysts to be able to choose a link function that suits their field of study. Furthermore, our study will provide a basis for developing an inference method that is robust to both the misspecification of the link function and outliers. This is also our future work.

Finally, the choice of prior distribution is an important topic in the Bayesian inference. When there is no prior information on the parameters in a model, we may consider an objective prior distribution. Giummolè et al., (2019) and Leisen et al., (2020) derived objective prior distributions based on scoring rules. Nakagawa and Hashimoto, (2021) derived the reference prior and the moment matching prior in the inference with the -divergence. The derivation of the objective prior in our proposed robust Bayesian ordinal response model is a subject for future work.

The R code implementing the proposed robust Bayesian method for the ordinal response model is available at GitHub repository (https://github.com/t-momozaki/RBORM).

Acknowledgement

This work was JSPS Grant-in-Aid for Early-Career Scientists Grant Number JP19K14597, JSPS Grant-in-Aid for Scientific Research (C) Number JP20K03756, JSPS Grant-in-Aid for Scientific Research (B) Number 21H00699, and JSPS Grant-in-Aid for Early-Career Scientists Grant Number JP23K13019.

Appendix

A.1 Proof of the theorems in Section 4

A.1.1 Proof of Theorem 1

Consider

where and .

Since from the Lagrange’s theorem for such that ,

where is independent variable of the parameter , and

Therefore, for the posterior robustness to hold, it must be

which requires that is a regularly varying function (O’Hagan and Pericchi,, 2012). However, for to be a regularly varying function, its tail order must be smaller than , and such a distribution does not exist. Namely, no matter what distribution is used, the posterior robustness does not hold for the standard posterior in the ordinal response model.

∎

A.1.2 Proof of Theorem 2

Consider

where and .

Since , then

where is the number of outliers and

Next, consider

Since is bounded, where is the distribution function,

is also clearly bounded. Hence since under the proper prior , from Lebesgue’s dominated convergence theorem,

and then

so the posterior robustness holds.

∎

A.1.3 Proof of Theorem 3

Consider

where and .

Since , then

and

Next, consider

Since is bounded, where is the distribution function,

is also clearly bounded. Hence since under the proper prior , from Lebesgue’s dominated convergence theorem,

and then the posterior robustness

holds.

∎

A.1.4 Proof of Theorem 4

Consider

where and .

Since , then

and

Next, consider

Since is bounded, where is the distribution function,

is also clearly bounded. Hence since under the proper prior , from Lebesgue’s dominated convergence theorem,

and then the posterior robustness

holds.

∎

References

- Agresti, (2010) Agresti, A. (2010). Analysis of Ordinal Categorical Data. John Wiley & Sons.

- Agresti and Kateri, (2017) Agresti, A. and Kateri, M. (2017). Ordinal probability effect measures for group comparisons in multinomial cumulative link models. Biometrics, 73(1), 214–219.

- Albert and Chib, (1993) Albert, J. H. and Chib, S. (1993). Bayesian analysis of binary and polychotomous response data. Journal of the American statistical Association, 88(422), 669–679.

- Baetschmann et al., (2020) Baetschmann, G., Ballantyne, A., Staub, K. E., and Winkelmann, R. (2020). feologit: A new command for fitting fixed-effects ordered logit models. The Stata Journal, 20(2), 253–275.

- Basak et al., (2021) Basak, S., Basu, A., and Jones, M. (2021). On the ‘optimal’ density power divergence tuning parameter. Journal of Applied Statistics, 48(3), 536–556.

- Basu et al., (1998) Basu, A., Harris, I. R., Hjort, N. L., and Jones, M. (1998). Robust and efficient estimation by minimising a density power divergence. Biometrika, 85(3), 549–559.

- Bhattacharya et al., (2019) Bhattacharya, A., Pati, D., and Yang, Y. (2019). Bayesian fractional posteriors. The Annals of Statistics, 47(1), 39–66.

- Bissiri et al., (2016) Bissiri, P. G., Holmes, C. C., and Walker, S. G. (2016). A general framework for updating belief distributions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(5), 1103–1130.

- Bürkner, (2017) Bürkner, P.-C. (2017). brms: An R package for Bayesian multilevel models using Stan. Journal of statistical software, 80, 1–28.

- Carpenter et al., (2017) Carpenter, B., Gelman, A., Hoffman, M. D., Lee, D., Goodrich, B., Betancourt, M., Brubaker, M., Guo, J., Li, P., and Riddell, A. (2017). Stan: A probabilistic programming language. Journal of Statistical Software, 76(1).

- Castilla et al., (2021) Castilla, E., Jaenada, M., and Pardo, L. (2021). Estimation and testing on independent not identically distributed observations based on Rényi’s pseudodistances. arXiv preprint arXiv:2102.12282, .

- Christensen, (2018) Christensen, R. H. B. (2018). Cumulative link models for ordinal regression with the r package ordinal. Submitted in J. Stat. Software, 35.

- Croux et al., (2013) Croux, C., Haesbroeck, G., and Ruwet, C. (2013). Robust estimation for ordinal regression. Journal of Statistical Planning and Inference, 143(9), 1486–1499.

- Czado and Santner, (1992) Czado, C. and Santner, T. J. (1992). The effect of link misspecification on binary regression inference. Journal of Statistical Planning and Inference, 33(2), 213–231.

- Del Moral et al., (2006) Del Moral, P., Doucet, A., and Jasra, A. (2006). Sequential monte carlo samplers. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68(3), 411–436.

- Desgagné, (2015) Desgagné, A. (2015). Robustness to outliers in location–scale parameter model using log-regularly varying distributions. The Annals of Statistics, 43(4), 1568–1595.

- Desgagné and Gagnon, (2019) Desgagné, A. and Gagnon, P. (2019). Bayesian robustness to outliers in linear regression and ratio estimation. Brazilian Journal of Probability and Statistics, 33(2), 205–221.

- Duane et al., (1987) Duane, S., Kennedy, A. D., Pendleton, B. J., and Roweth, D. (1987). Hybrid monte carlo. Physics letters B, 195(2), 216–222.

- Fair, (1978) Fair, R. C. (1978). A theory of extramarital affairs. Journal of Political Economy, 86(1), 45–61.

- Franses and Paap, (2001) Franses, P. H. and Paap, R. (2001). Quantitative Models in Marketing Research. Cambridge University Press.

- Fujisawa and Eguchi, (2008) Fujisawa, H. and Eguchi, S. (2008). Robust parameter estimation with a small bias against heavy contamination. Journal of Multivariate Analysis, 99(9), 2053–2081.

- Gagnon et al., (2020) Gagnon, P., Desgagné, A., and Bédard, M. (2020). A new Bayesian approach to robustness against outliers in linear regression. Bayesian Analysis, 15(2), 389–414.

- Ghosh and Basu, (2013) Ghosh, A. and Basu, A. (2013). Robust estimation for independent non-homogeneous observations using density power divergence with applications to linear regression. Electronic Journal of statistics, 7, 2420–2456.

- Ghosh and Basu, (2016) Ghosh, A. and Basu, A. (2016). Robust Bayes estimation using the density power divergence. Annals of the Institute of Statistical Mathematics, 68(2), 413–437.

- Giummolè et al., (2019) Giummolè, F., Mameli, V., Ruli, E., and Ventura, L. (2019). Objective Bayesian inference with proper scoring rules. Test, 28(3), 728–755.

- Goodrich et al., (2020) Goodrich, B., Gabry, J., Ali, I., and Brilleman, S. (2020). rstanarm: Bayesian applied regression modeling via Stan. R package version 2.21.1.

- Grünwald and van Ommen, (2017) Grünwald, P. and van Ommen, T. (2017). Inconsistency of Bayesian inference for misspecified linear models, and a proposal for repairing it. Bayesian Analysis, 12(4), 1069–1103.

- Hampel, (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. Journal of the American Statistical Association, 69(346), 383–393.

- Hampel et al., (1986) Hampel, F. R., Ronchetti, E. M., Rousseeuw, P. J., and Stahel, W. A. (1986). Robust statistics. Wiley Online Library.

- Hamura et al., (2022) Hamura, Y., Irie, K., and Sugasawa, S. (2022). Log-regularly varying scale mixture of normals for robust regression. Computational Statistics & Data Analysis, 173, 107517.

- Harrell, (2001) Harrell, F. E. (2001). Regression modeling strategies: with applications to linear models, logistic regression, and survival analysis. Springer.

- Harrison and Rubinfeld, (1978) Harrison, J. D. and Rubinfeld, D. L. (1978). Hedonic housing prices and the demand for clean air. Journal of Environmental Economics and Management, 5(1), 81–102.

- Hashimoto and Sugasawa, (2020) Hashimoto, S. and Sugasawa, S. (2020). Robust Bayesian regression with synthetic posterior distributions. Entropy, 22(6), 661.

- Hoffman et al., (2014) Hoffman, M. D., Gelman, A., et al. (2014). The no-u-turn sampler: adaptively setting path lengths in hamiltonian monte carlo. Journal of Machine Learning Research, 15(1), 1593–1623.

- Holmes and Walker, (2017) Holmes, C. C. and Walker, S. G. (2017). Assigning a value to a power likelihood in a general Bayesian model. Biometrika, 104(2), 497–503.

- Huber and Ronchetti, (2009) Huber, J. and Ronchetti, E. M. (2009). Robust Statistics, Second Edition. Wiley.

- Hyvärinen and Dayan, (2005) Hyvärinen, A. and Dayan, P. (2005). Estimation of non-normalized statistical models by score matching. Journal of Machine Learning Research, 6(4).

- Iannario et al., (2017) Iannario, M., Monti, A. C., Piccolo, D., and Ronchetti, E. (2017). Robust inference for ordinal response models. Electronic Journal of Statistics, 11(2), 3407–3445.

- Jewson et al., (2018) Jewson, J., Smith, J. Q., and Holmes, C. (2018). Principles of Bayesian inference using general divergence criteria. Entropy, 20, 442.

- Jones et al., (2001) Jones, M., Hjort, N. L., Harris, I. R., and Basu, A. (2001). A comparison of related density-based minimum divergence estimators. Biometrika, 88(3), 865–873.

- Kawakami and Hashimoto, (2023) Kawakami, J. and Hashimoto, S. (2023). Approximate Gibbs sampler for Bayesian Huberized lasso. Journal of Statistical Computation and Simulation, 93(1), 128–162.

- Kurtek and Bharath, (2015) Kurtek, S. and Bharath, K. (2015). Bayesian sensitivity analysis with the Fisher–Rao metric. Biometrika, 102(3), 601–616.

- Leisen et al., (2020) Leisen, F., Villa, C., and Walker, S. G. (2020). On a class of objective priors from scoring rules (with discussion). Bayesian Analysis, 15(4), 1345–1423.

- Liu and Zhang, (2018) Liu, D. and Zhang, H. (2018). Residuals and diagnostics for ordinal regression models: a surrogate approach. Journal of the American Statistical Association, 113(522), 845–854.

- Lyddon et al., (2018) Lyddon, S., Walker, S., and Holmes, C. C. (2018). Nonparametric learning from Bayesian models with randomized objective functions. Advances in Neural Information Processing Systems, 31.

- Lyddon et al., (2019) Lyddon, S. P., Holmes, C., and Walker, S. (2019). General Bayesian updating and the loss-likelihood bootstrap. Biometrika, 106(2), 465–478.

- Madahian et al., (2015) Madahian, B., Roy, S., Bowman, D., Deng, L. Y., and Homayouni, R. (2015). A Bayesian approach for inducing sparsity in generalized linear models with multi-category response. BMC Bioinformatics, 16(13), 1–10.

- Maronna et al., (2019) Maronna, R. A., Martin, R. D., Yohai, V. J., and Salibián-Barrera, M. (2019). Robust statistics: theory and methods (with R). John Wiley & Sons.

- McCullagh, (1980) McCullagh, P. (1980). Regression models for ordinal data. Journal of the Royal Statistical Society: Series B (Methodological), 42(2), 109–127.

- Miller and Dunson, (2019) Miller, J. W. and Dunson, D. B. (2019). Robust Bayesian inference via coarsening. Journal of the American Statistical Association, 114(527), 1113–1125.

- Momozaki and Nakagawa, (2022) Momozaki, T. and Nakagawa, T. (2022). Robustness against outliers in ordinal response model via divergence approach. arXiv preprint arXiv:2209.11965, .

- Nakagawa and Hashimoto, (2020) Nakagawa, T. and Hashimoto, S. (2020). Robust Bayesian inference via -divergence. Communications in Statistics-Theory and Methods, 49(2), 343–360.

- Nakagawa and Hashimoto, (2021) Nakagawa, T. and Hashimoto, S. (2021). On default priors for robust Bayesian estimation with divergences. Entropy, 23(1), 29.

- Nandram and Chen, (1996) Nandram, B. and Chen, M.-H. (1996). Reparameterizing the generalized linear model to accelerate gibbs sampler convergence. Journal of Statistical Computation and simulation, 54(1-3), 129–144.

- Neal, (2003) Neal, R. M. (2003). Slice sampling. The Annals of Statistics, 31(3), 705–767.

- Neal et al., (2011) Neal, R. M. et al. (2011). MCMC using Hamiltonian dynamics. Handbook of markov chain monte carlo, 2(11), 2.

- Newton et al., (2021) Newton, M. A., Polson, N. G., and Xu, J. (2021). Weighted Bayesian bootstrap for scalable posterior distributions. Canadian Journal of Statistics, 49(2), 421–437.

- Newton and Raftery, (1994) Newton, M. A. and Raftery, A. E. (1994). Approximate Bayesian inference with the weighted likelihood bootstrap. Journal of the Royal Statistical Society: Series B (Methodological), 56(1), 3–26.

- O’Hagan and Pericchi, (2012) O’Hagan, A. and Pericchi, L. (2012). Bayesian heavy-tailed models and conflict resolution: A review. Brazilian Journal of Probability and Statistics, 26(4), 372–401.

- Pyne et al., (2022) Pyne, A., Roy, S., Ghosh, A., and Basu, A. (2022). Robust and efficient estimation in ordinal response models using the density power divergence. arXiv preprint arXiv:2208.14011, .

- R Core Team, (2022) R Core Team (2022). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Riani et al., (2011) Riani, M., Torti, F., and Zani, S. (2011). Outliers and robustness for ordinal data. Modern Analysis of Customer Surveys: with applications using R, , 155–169.

- Rossi and Allenby, (2003) Rossi, P. E. and Allenby, G. M. (2003). Bayesian statistics and marketing. Marketing Science, 22(3), 304–328.

- Rubin, (1981) Rubin, D. B. (1981). The bayesian bootstrap. The Annals of Statistics, 9(1), 130–134.

- Satake et al., (2018) Satake, E., Majima, K., Aoki, S. C., and Kamitani, Y. (2018). Sparse ordinal logistic regression and its application to brain decoding. Frontiers in Neuroinformatics, 12(51), 1–10.

- Scalera et al., (2021) Scalera, V., Iannario, M., and Monti, A. C. (2021). Robust link functions. Statistics, 55(4), 963–977.

- Sha and Dechi, (2019) Sha, N. and Dechi, B. O. (2019). A Bayes inference for ordinal response with latent variable approach. Stats, 2(2), 321–331.

- Syring and Martin, (2019) Syring, N. and Martin, R. (2019). Calibrating general posterior credible regions. Biometrika, 106(2), 479–486.

- Walker and Duncan, (1967) Walker, S. H. and Duncan, D. B. (1967). Estimation of the probability of an event as a function of several independent variables. Biometrika, 54(1-2), 167–179.

- Warwick and Jones, (2005) Warwick, J. and Jones, M. (2005). Choosing a robustness tuning parameter. Journal of Statistical Computation and Simulation, 75(7), 581–588.

- Wu and Martin, (2023) Wu, P.-S. and Martin, R. (2023). A comparison of learning rate selection methods in generalized Bayesian inference. Bayesian Analysis, 18(1), 105–132.

- Yonekura and Sugasawa, (2023) Yonekura, S. and Sugasawa, S. (2023). Adaptation of the tuning parameter in general Bayesian inference with robust divergence. Statistics and Computing, 33(2), 39.