Jinyang Jiang, Jiaqiao Hu, and Yijie Peng

Quantile-Based Deep Reinforcement Learning

Quantile-Based Deep Reinforcement Learning using Two-Timescale Policy Gradient Algorithms

Jinyang Jiang

\AFFDepartment of Management Science and Information Systems,

Guanghua School of Management, Peking University, Beijing 100871, CHINA, \EMAILjinyang.jiang@stu.pku.edu.cn

\AUTHORJiaqiao Hu

\AFFDepartment of Applied Mathematics and Statistics,

State University of New York at Stony Brook, Stony Brook, NY 11794, U.S.A., \EMAILjqhu@ams.stonybrook.edu

\AUTHORYijie Peng

\AFFDepartment of Management Science and Information Systems,

Guanghua School of Management, Peking University, Beijing 100871, CHINA, \EMAILpengyijie@pku.edu.cn

Classical reinforcement learning (RL) aims to optimize the expected cumulative reward. In this work, we consider the RL setting where the goal is to optimize the quantile of the cumulative reward. We parameterize the policy controlling actions by neural networks, and propose a novel policy gradient algorithm called Quantile-Based Policy Optimization (QPO) and its variant Quantile-Based Proximal Policy Optimization (QPPO) for solving deep RL problems with quantile objectives. QPO uses two coupled iterations running at different timescales for simultaneously updating quantiles and policy parameters, whereas QPPO is an off-policy version of QPO that allows multiple updates of parameters during one simulation episode, leading to improved algorithm efficiency. Our numerical results indicate that the proposed algorithms outperform the existing baseline algorithms under the quantile criterion.

Deep Reinforcement Learning; Quantile Optimization; Stochastic Approximation; Asymptotic Analysis

1 INTRODUCTION

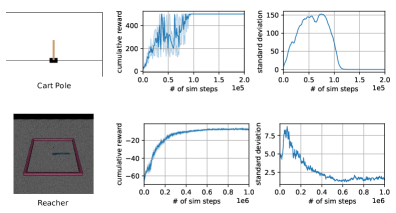

Deep reinforcement learning (RL) has recently made significant successes in games (Mnih et al. 2015, Silver et al. 2016), robotic control (Levine et al. 2016), recommendation (Zheng et al. 2018) and many other fields. RL formulates a complex sequential decision-making task as a Markov Decision Process (MDP) and attempts to learn an optimal policy by interacting with the environment via sampling rewards and state transitions. In the classical RL framework, the goal is to optimize the expectation/mean of the cumulative reward. Under such a criterion, the optimal policy of the MDP satisfies the well-known Bellman equation, which forms the basis for many popular RL algorithms. In application domains such as robotic control and board games, where RL achieves great successes, the reward functions and the underlying system dynamics are often deterministic, and random transitions are merely introduced artificially to characterize complex physical environments. For these settings, optimizing the expected reward turns out to be a desirable goal because a well-trained policy would typically result in the underlying dynamics being acted in a nearly deterministic fashion, leading to a cumulative reward that contains little or no variation; see Figure.1 for an illustration.

The output of a business system, however, is usually the random outcome of group human behaviors, which could be extremely difficult to predict. For instance, in inventory management, customer demands, arrival times, and order lead times are intrinsically random, so even under the (mean-based) optimal ordering policy, the inventory cost may still be subject to large uncertainty. In such cases, it is important to question whether the mean is an appropriate objective for optimization because mean only measures the average performance of a random system but not its extreme or “tail” behavior. The tail performance may actually reflect a catastrophic outcome for a system. For example, the joint defaults of subprime mortgages led to the 2008 financial crisis, and in the post-crisis era, the Basel accord requires major financial institutes to maintain a minimal capital level for sustaining the loss under extreme market circumstances. A quantile, on the other hand, can be used to capture the tail behavior of a random system, and thus could be a more useful alternative in applications involving risk minimization or the prevention of damages/losses caused by the occurrence of extreme events. For example, managers in service industry may try to optimize the quantile level of system reliability that guarantees the service for of the customers (DeCandia et al. 2007); physicians may want to make a treatment decision that maximizes the percentile of health improvement rate (Beyerlein 2014). In finance, quantiles are also known as value-at-risk (VaR) and can be directly translated into the minimal capital requirement.

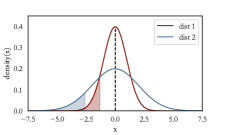

In this paper, we consider the setting where the goal is to optimize the quantiles of the cumulative rewards. As a simple illustration of the difference between mean and quantile, Figure.2 shows the return distributions of two portfolios. It can be clearly observed that although both distributions have the same mean, the -quantile of distribution 1 is significantly larger than that of distribution 2, meaning that portfolio 2 would require more capital to avoid irreversible loss or bankruptcy at the confidence level. The difference between these two criteria in the RL setting is also highlighted in Figure.2: quantile optimization improves the tail performance while mean optimization improves the average value.

For some distributions, e.g. the Cauchy distribution, the mean does not even exist and hence cannot be used as a meaningful performance measure. In contrast, quantiles are always well-defined.

Unfortunately, quantile measures are known to be extremely difficult to optimize (Rockafellar 2020), and solving MDPs with quantile objectives is even more challenging because unlike in the mean case, a quantile of the cumulative reward cannot be decomposed into the sum of quantiles of rewards at different decision epochs, making it impossible to apply conventional RL methods rooted in the Bellman equation. This issue does not occur under nested risk measures (Ruszczyński 2010, Jiang and Powell 2018) or other measures that allow for a recursive structure decomposition. For MDPs under the conditional value-at-risk (CVaR) criterion, some recent work (Chow and Pavone 2013, Chow and Ghavamzadeh 2014) considers the use of state-space augmentation techniques. However, none of these techniques can be suitably applied to the quantile setting. More recently, Li et al. (2022) also propose a dynamic programming algorithm for quantile-based MDP, but their work requires explicit specification of the model parameters and does not fit into the RL context considered in this paper.

We parameterize the policy controlling actions by neural networks. When the parameterization is smooth but entails a large number of parameters, it is natural to adopt a gradient descent-based technique for solving the nonlinear optimization problem required in policy training. However, the difficulty is that, in contrast to the gradient of a mean, which can be estimated without bias using a single sample/simulation trajectory, the quantile gradient relies on the true quantile value and hence does not allow for an unbiased estimation. To address this issue, we propose two novel policy gradient algorithms. The first algorithm, called Quantile-Based Policy Optimization (QPO), uses two coupled stochastic approximation (SA) iterations running at different timescales for simultaneously computing quantiles and policy parameters, allowing quantile estimation and parameter optimization to be conducted in a coherent manner. Each update of policy parameters in QPO requires a single sample trajectory (episode) of the system. For MDPs with complicated system dynamics and/or long planning horizons, updating parameters once at the end of an episode may not be practical if observing/simulating the entire trajectory is computationally demanding. The second algorithm draws ideas from the state-of-art mean-based RL techniques, in particular, the Proximal Policy Optimization (PPO) approach of Schulman et al. (2017), yielding an off-policy variant of QPO we call Quantile-Based Proximal Policy Optimization (QPPO) that allows multiple updates of policy parameters during one simulation episode. This, in effect, leads to improved efficiency in data utilization and significantly enhanced algorithm convergence behavior. Our empirical study on several business applications indicates that the proposed algorithms are promising and outperform some of the existing algorithms under the quantile criterion.

We summarize our main contributions as follows.

-

•

We derive a quantile-based policy gradient estimator, propose a two-timescale policy gradient algorithm, QPO, for quantile optimization in the deep RL setting, and establish the strong convergence and rates of convergence of the algorithm.

-

•

We introduce an enhanced version of QPO that allows multiple updates of policy parameters during a single episode, show its convergence, and provide new error bounds to characterize its performance.

-

•

We carry out simulation studies to empirically investigate and compare the performance of our new algorithms with existing baseline techniques on realistic business applications, including financial investment and inventory management problems.

To the best of our knowledge, our work is the first to develop quantile-based deep RL algorithms capable of training policies parameterized by large-scale neural networks. Preliminary versions of the two algorithms, QPO and QPPO, have been presented in the conference paper Jiang et al. (2022) but without convergence analysis. In this work, in addition to providing complete convergence proofs, we perform detailed analysis to characterize the performance of the algorithms in terms of convergence rates/error bounds and conduct more comprehensive numerical experiments to illustrate the algorithms on realistic applications.

The rest of the paper is organized as follows. In Section 2, we review the related work on gradient estimation and deep RL. In Section 3, we describe the MDP problem and present our quantile-based RL optimization model. Section 4 contains a detailed description of the proposed QPO algorithm, accompanied by its theoretical convergence and rate results. In Section 5, we introduce an accelerated variant of QPO and further provide error bounds on its performance. Simulation studies are carried out in Section 6, and we conclude the paper and discuss future directions in Section 7. The proofs of all theoretical results are given in the online appendix.

2 RELATED WORK

2.1 Mean-based RL

In mean-based RL, there are two major categories of methods. The first category is value-based methods, which learn the value/Q-function and rely on the Bellman equation to select the action with the best value. Pioneer work in deep RL includes Deep Q-learning (DQN) and its variants (Mnih et al. 2015, Hessel et al. 2018). The second category of methods are based on policy optimization, where the policies are parameterized in various ways, e.g., through basis functions or neural networks, and optimized by stochastic gradient descent. REINFORCE is an early policy gradient algorithm (Williams 1992). Trust Region Policy Optimization (TRPO) introduces importance sampling techniques into RL to increase data utilization efficiency (Schulman et al. 2015). PPO further improves upon TRPO through optimizing a clipped surrogate objective and has currently become a commonly used baseline algorithm (Schulman et al. 2017). There are also algorithms that combine the advantages of these two types of methods such as Deep Deterministic Policy Gradient (DDPG) and Soft Actor-Critic (SAC) (Lillicrap et al. 2016, Haarnoja et al. 2018).

Recently, mean-based RL has been studied actively in the domain of operations research and management science. On the application side, there is a growing literature applying RL techniques to problems in fields such as market making (Baldacci et al. 2022), business management (Moon et al. 2022), consumer targeting (Wang et al. 2022b), network optimization (Qu et al. 2022), and collusion avoidance (Abada and Lambin 2020). In terms of theory, Sinclair et al. (2022) improve the training cost of value-based online RL algorithms through adaptive discretization of problem space; Wang et al. (2022a) derive confidence bounds for off-policy evaluation by leveraging methodologies from distributionally robust optimization; other recent advancements on important concepts in RL can be found in, e.g., Cen et al. (2022), Bhandari et al. (2021).

2.2 Gradient Estimation of Risk Measures

In classical gradient estimation problems, the focus has been on mean-based performance measures (Fu 2006), whereas gradient estimation of risk measures such as quantiles and CVaRs is considered to be more difficult and is an area of active research. A number techniques have been developed over the past two decades, including infinite perturbation analysis (Hong 2009, Jiang and Fu 2015), kernel estimation (Liu and Hong 2009, Hong and Liu 2009), and measure-valued differentiation (Heidergott and Volk-Makarewicz 2016). Recently, Glynn et al. (2021) also consider the use of the generalized likelihood ratio method for estimating the gradient of a general class of distortion risk measures. Unfortunately, applying these methods in an MDP environment would require the analytic expressions for the transition and reward functions, which are typically not available in a RL setting. A well-known black-box gradient estimation approach is Simultaneous Perturbation Stochastic Approximation (SPSA) (Spall 1992). However, tuning parameters such as perturbation- and step-sizes in optimization requires care and it could be hard to apply SPSA to high-dimensional optimization problems in deep RL when policies are parameterized by neural networks.

2.3 Risk-sensitive RL

Risk measures have been introduced into RL either in the forms of objectives or constraints, which are referred as risk-sensitivity RL in the literature. With risk measures as the objective functions, well-trained agents can be expected to perform more robustly under extreme events. For example, an expected exponential utility approach is taken by Borkar (2001); Petrik and Subramanian (2012) and Tamar et al. (2014) study CVaR-based objectives; Prashanth and Ghavamzadeh (2013) aim to optimize several variance-related risk measures using SPSA and a smooth function approach; Prashanth et al. (2016) apply SPSA to optimize an objective function in the cumulative prospect theory. For a comprehensive discussion on policy optimization under various risk measures, we refer the reader to Prashanth et al. (2022).

There are also studies that incorporate a risk measure as the constraint to an RL problem. For example, a Lagrangian approach has been used in Bertsekas (1997) to solve RL problems subject to certain risk measure constraints; dynamic and time-consistent risk constraints are considered in Chow and Pavone (2013); Borkar and Jain (2014) use CVaR as the constraint; Chow et al. (2017) also develop policy gradient and actor-critic algorithms under VaR and CVaR constraints.

3 Problem Formulation & Preliminaries

3.1 Markov Decision Process

An MDP can be defined as a 5-tuple , where and are the state and action spaces, is the transition probability, is the reward function, and is the reward discount factor. We consider the class of stationary, randomized, Markovian policies parameterized by a vector , where each represents a probability distribution over for every . Denote the state and action encountered at time by and , where , , and is the decision horizon. Then the trajectory generated by following a policy can be defined as , where is the initial state and . The accumulated total reward can thus be written as , which is being viewed as a function of a random trajectory and follows a distribution denoted by .

3.2 Mean-based Criterion for RL

In the classical RL setting, the objective is to determine the optimal choice of that maximizes the expected cumulative reward, i.e.,

| (1) |

where is the parameter space.

An important class of techniques for solving (1) is the policy gradient algorithms, where the likelihood-ratio method is frequently used to derive unbiased gradient estimators that do not rely on knowledge of the transition probabilities. Specifically, the gradient of the objective function in (1) can be reformulated as

| (2) |

where the interchange of the gradient and integral in the second equality can be justified by the dominated convergence theorem (L’Ecuyer et al. 1992). This yields an unbiased estimator for estimating . In addition, by noticing that for , , the gradient estimator can be further reduced to , where is the reward-to-go when starting from state and action .

3.3 Quantile-Based Criterion for RL

For a given probability level , the -quantile for distribution is defined as

We assume that is continuously differentiable on , i.e., , so that the -quantile can be written as the inverse of the distribution function, i.e., . Our goal is to maximize the -quantile of the distribution on a compact convex set , i.e.,

| (3) |

As in a typical policy gradient algorithm, we consider solving (3) by a stochastic gradient ascent method that makes use of the gradient information. To this end, note that by the definition of , we have . Thus, an analytical expression for its gradient can be readily obtained by taking gradients at both sides of the equation (see, e.g., Fu et al. 2009),

| (4) |

The simplest way to use this relationship would be to construct two separate estimators for the numerator and denominator of (4). However, there are two major difficulties:

-

The right-hand-side of (4) contains the -quantile itself, which is unknown and changes value as the underlying parameter vector changes;

-

The density function of the cumulative reward usually does not have an analytical form.

4 Quantile-Based Policy Optimization

Following our discussion in Section 3.3, we propose a viable approach for approximating the quantile gradient (4) and present a new on-policy policy gradient algorithm, QPO, for solving (3). We then establish the strong convergence of the algorithm and characterize its rates of convergence.

4.1 On-Policy RL Algorithm for Optimizing Quantiles

Hu et al. (2022) recently propose a three-timescale SA algorithm for stochastic optimization problems with quantile objectives. However, it is difficult to apply their algorithm in our setting because the density estimation in the denominator of (4) relies on the analytical forms of the transition probability and reward function that are typically not available in an RL context. In addition, tuning and finding the best set of algorithm parameters in a three-timescale SA method could be elusive. Algorithms with less hyperparameters consume smaller amounts of trial-and-error tuning data and effort, and hence are easier and more efficient to implement on large scale RL problems that require expensive simulation models for performance evaluation.

The QPO algorithm we propose is a two-timescale approach that does not require estimating the density . In particular, a simple but important observation is that the density in the denominator of (4) is always non-negative so that the quantile gradient shares the same direction as . This allows us to estimate the best ascent direction in searching for the optimum by constructing an estimator for and then replacing by an estimate of .

The quantile estimates can be computed using the following recursive procedure proposed in Hu et al. (2022):

| (5) |

where is the step-size, is the trajectory simulated by following the current policy parameterized by , and is an estimate of at step . When is fixed, it can be seen that (5) is essentially an SA iteration for solving the root-finding problem and hence converges to under mild conditions on .

On the other hand, we note that a similar likelihood ratio technique as in (2) can be applied to derive the gradient , yielding

Consequently, an unbiased estimator for is given by

The estimator, when combined with the quantile estimate obtained in (5), can be effectively integrated into the following gradient ascent method for solving (3):

| (6) |

where is the gradient search step-size and represents a projection operations that bring an iterate back to the parameter space whenever it becomes infeasible. This leads to our proposed QPO algorithm whose detailed steps are presented in Algorithm 1 below.

4.2 Strong Convergence of QPO

Let be a probability space. We define as the filtration generated by our algorithm for . For a given vector , let be the norm of ; for a matrix , let be the Frobenius norm of . Here we introduce some assumptions before the analysis.

For any , .

is Lipschitz continuous with respect to both and , i.e., there exists a constant such that for any , .

The step-size sequences and satisfy

(a) , , ; (b) , , ; (c) .

The log gradient of the neural network output with respect to is bounded, i.e., for any state-action pair and parameter , .

Assumption 4.2 requires that the objective function is smooth enough, which is commonly assumed in continuous optimization. Assumptions 4.2 and 4.2 are standard in stochastic approximation analysis.

Since in Assumption 4.2 (c), recursion (5) is updated on a faster timescale than recursion (6). Let

and we expect them to track two coupled ODEs:

| (7) |

where is a projection function satisfying

where is the vector with the smallest norm needed to keep in , and is the normal cone to at . When , projects the gradient onto .

Intuitively, can be viewed as static for analyzing the dynamic of the process . Suppose that for some constant , the unique global asymptotically stable equilibrium of the ODE

| (8) |

is . Recursion (6) can be viewed as tracking the ODE

| (9) |

If is the unique global asymptotically stable equilibrium of this ODE, then the global convergence of QPO to can be proved; otherwise, the sequence generated by recursion (6) converges to some limit set of the ODE, which consists of local maxima. For simplicity, we prove the unique global asymptotically stable equilibriums for ODEs (8) and (9) under certain conditions, the details of which can be found in Appendix 8.1.

Lemma 4.1

is the unique global asymptotically stable equilibrium of ODE (8) for all .

Lemma 4.2

If is strictly convex on , then is the unique global asymptotically stable equilibrium of ODE (9).

To prove that recursions (5) and (6) track coupled ODE (7), we apply the convergence theorem of the two-timescale stochastic approximation as below:

Theorem 4.3

(Borkar 1997) Consider two coupled recursions:

where is a projection function, and are Lipschitz continuous, and satisfy Assumption 4.2, and are random variable sequences satisfying

If ODE (8) has a unique global asymptotically stable equilibrium for each , then the coupled recursions converge to the unique global asymptotically stable equilibrium of the ODE a.s. provided that the sequence is bounded.

Next we show that the sequence is almost surely bounded under our assumptions. Then the conditions in Theorem 4.3 can be verified in Theorem 4.5.

Lemma 4.4

4.3 Rate of Convergence

We first establish a central limit theorem for the two-timescale SA algorithm, the proof of which can be found in Appendix 8.2. We consider specific step-sizes of the forms and for , where and and introduce an assumption on the Hessian of the distribution function. All conclusions in this section on the convergence rates of the algorithm are based on assuming that QPO converges to that lies in the interior of .

The smallest eigenvalue of is greater than 0. To derive the joint weak convergence rate of the sequences and , we apply a central limit theorem for two-timescale stochastic approximation in Mokkadem and Pelletier (2006). Let be the block coefficient matrix in the first order Taylor polynomial of at , i.e.,

where

and by the first order necessary condition for optimality.

In addition to the above asymptotic normality result, we further characterize the finite-time performance of the algorithm in terms of its mean-squared errors. We make the following assumptions:

Let be a set containing all . There exist , such that for and .

Let and be its largest eigenvalue. , such that for all .

We first derive the order of the mean squared errors for recursion (5).

Next, we establish the convergence rate of recursion (6).

5 Acceleration Technique

In this section, we propose an acceleration technique for the vanilla QPO to improve the data utilization efficiency and prove its convergence. We begin by introducing in Section 5.1 a variant of QPO that allows the quantile estimation and parameter update to be carried out based on truncated trajectories. This is then used in conjunction with an importance sampling technique in Section 5.2 to arrive at an off-policy procedure that reuses simulation samples and performs multiple policy updates during a single episode. A clipped surrogate objective approach is subsequently considered in Section 5.3 to further reduce the variance of the estimates in order to achieve better learning capacity and stability.

5.1 Parameter Update with Truncated Trajectory

For the state-of-art mean-based RL algorithms such as the one in Schulman et al. (2017), the parameters can be updated multiple times during one episode, whereas the quantile-based RL algorithm (6) only updates the parameters once in an episode, which is inefficient in utilizing the simulated data. To alleviate the issue, we use truncated subsequences rather than the entire trajectory to update policy parameters.

Denote the trajectory generated at the -th simulation episode with length as and the corresponding accumulated reward as , which follows the distribution . Assume that the MDP has a finite time horizon , and our objective (3) can be rewritten as:

| (11) |

We keep track of not only the quantile estimate of but also the quantile estimates of distributions with being a truncation parameter. In the -th iteration, we randomly select an integer from with equal probabilities and then run a simulation of length to obtain . The parameters are updated as follows:

| (12) | ||||

| (13) |

where the trajectories are generated independently for each iteration . Note that in recursion (13), we use to compute descent direction , which is a biased estimate of .

Next, we establish the convergence of this algorithm in a similar manner as that of Algorithm 1. We assume for all and show that recursions (12) and (13) track the following coupled ODEs:

| (14) | ||||

where and . Here we introduce some additional assumptions before the analysis.

For any and , .

For all , is Lipschitz continuous with respect to both and , i.e., there exists a constant such that for any , .

Suppose that for , is the unique global asymptotically stable equilibrium of the ODE

| (15) |

Then recursion (13) tracks the ODE

| (16) |

Let and assume that is the unique global asymptotically stable equilibrium of this ODE, so that we can establish the global convergence of the coupled recursions to . Note that if we fix to a constant , then is decoupled, and we immediately have the following lemmas:

Lemma 5.1

To apply the convergence theorem for two-timescale SAs, we next show in Lemmas 5.2 and 5.3 below that the sequence is almost surely bounded and the simulation error accumulated over the iterations remains bounded.

Lemma 5.2

Denote , where and is randomly chosen from with equal probabilities.

Theorem 5.4

Finally, we show that the error introduced by truncation is asymptotically negligible as under different reward settings. We consider uniformly bounded and Gaussian rewards, as well as the more general sub-Gaussian case. In each case, we provide an explicit bound on the error caused by trajectory truncation. Proofs of all three cases can be found in Appendix 9.

Theorem 5.5

If the reward function is bounded, i.e., there exists a constant , for any , then .

The reward setting in Theorem 5.5 is the most common situation in classical RL problems. For video games and robotic control, rewards are often chosen to be finite, such as the position of an agent, or the time it takes to finish a task.

Theorem 5.6

If the reward is normally distributed, i.e., there exist constants , for any , , where , , then , where and is the -quantile of the standard normal distribution.

In financial portfolio management, the rewards (returns) of assets are often assumed to be Gaussian.

Theorem 5.7

If the reward is a sub-Gaussian random variable, i.e., there exist constants , for any , , where the mean of is finite, i.e., , then .

Sub-Gaussian family of distributions includes Gaussian, Bernoulli, bounded distributions, and Beta or Dirichlet distributions under certain conditions (Marchal and Arbel 2017). Moreover, the sub-Gaussianity is preserved by linear operations, which enables us to construct more complex distributions belonging to the family.

5.2 Off-Policy RL Algorithm for Optimizing Quantiles

By applying the importance sampling method, we can use a fixed policy to interact with the environment, and then recursions (12) and (13) can be transformed into

| (17) | ||||

| (18) |

where trajectories are generated independently following and the importance sampling ratio is defined as

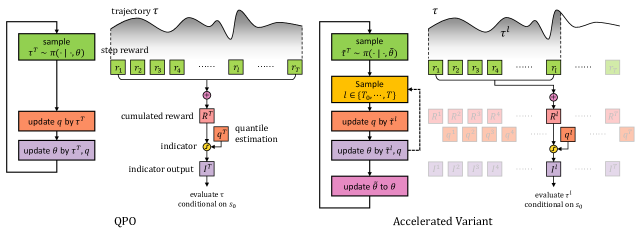

Recursions (17) and (18) are equivalent to recursions (12) and (13) in a probability sense (Glynn and Iglehart 1989). And the convergence results in Section 3.1 hold for recursions (17) and (18). The differences in logical structure and data flow between vanilla QPO and the accelerated variant are shown in Figure.3.

We consider modified versions of (17) and (18) that improve data utilization efficiency by allowing multiple updates on in one episode for quantile-based RL. Let be the policy parameter obtained just prior to the -th episode. In the -th episode, the latest policy is used to interact with the environment and generate a trajectory . Then the policy parameter is updated multiple times based on subsequences of generated in one simulation episode. For , we randomly select from with equal probabilities in the -th iteration. Then we use the subsequence of trajectory to perform the following recursions:

| (19) | ||||

| (20) |

where . Since subsequences of in recursions (19) and (20) share common random variables, the stochastic gradient estimates at different iterations of recursions (19) and (20) become correlated. The convergence result of SA with correlated noise are rather technical and can be referred to Chapter 6 in Kushner and Yin (2003).

5.3 Clipped Surrogate Objective

In Section 5.2, the on-policy QPO is transformed to an off-policy algorithm by employing the importance sampling method. However, the importance ratio term may inflate the variance significantly. This issue has been considered in mean-based RL algorithms. In TRPO (Schulman et al. 2015), an optimization problem with a surrogate objective of (1) is proposed by applying the importance sampling method, i.e.,

where is the advantage function of the -th decision calculated by some variant of the “reward-to-go” and the KL divergence constraint is used to enforce the distribution under to stay close to so that the variance of the importance ratio does not become excessively large. To simplify the computation, Schulman et al. (2015) use a penalty rather than a hard constraint, whereas PPO introduced by Schulman et al. (2017) is based on an optimization problem with a clipped surrogate objective that is much easier to handle, i.e.,

where the clip function is denoted as , and and are the lower and upper truncation bounds.

Note that given and , recursion (20) optimizes the surrogate objective

| (21) |

Therefore, to constrain the difference between and , we adapt the technique used in PPO to our quantile-based algorithm. Specifically, we introduce a clip operation to the ratio term in surrogate problem (21). To further reduce the variance, we employ a baseline network , that does not depend on and is updated by minimizing the mean-squared error (MSE) of the difference from . Then, the clipped surrogate objective can be written as

| (22) | ||||

By applying the technique developed in Section 5.2 to optimization problem (22), we propose a quantile-based off-policy deep RL algorithm, named QPPO. The pseudo code of QPPO is presented in Algorithm 2.

6 Numerical Experiments

In this section, we conduct simulation experiments on different RL tasks to demonstrate the effectiveness of proposed algorithms. We first compare our QPO and QPPO with baseline RL algorithms REINFORCE and PPO, as well as the SPSA-based algorithm, in a simple example for illustration. In the more complicated financial investment and inventory management examples, we focus on comparing QPPO with one of the state-of-art mean-based algorithms, PPO, to demonstrate the behavioral patterns of agents under different criteria and the high learning efficiency of QPPO. Exogenous parameters of simulation environments and hyperparameters of algorithms used in all three examples can be found in Appendix 10.

The selection of affects the convergence speed of the algorithms, since the quantile estimation is the reference for the agent to evaluate the action. To simplify parameter tuning, we relax the divergence conditions in Assumption 4.2 and let and decay exponentially at rates and , respectively. Then we employ an Adam optimizer for the quantile estimation recursion and use a small number of simulation episodes to provide an initial point for the quantile estimation.

6.1 Toy Example: Zero Mean

In a simulation environment with time steps and alternative choices, the reward of an agent at the -th step is given by , where the state is a vector obtained by randomly reshuffling the entries of , and is the action chosen by the agent. The agent observes the current state and chooses the coordinate index of the state vector which determines the support of the uniform distribution of the reward. It is obvious that the cumulative reward follows a distribution with zero mean. Therefore, optimizing the expected cumulative reward is ineffective, whereas the quantile performance can be optimized by choosing .

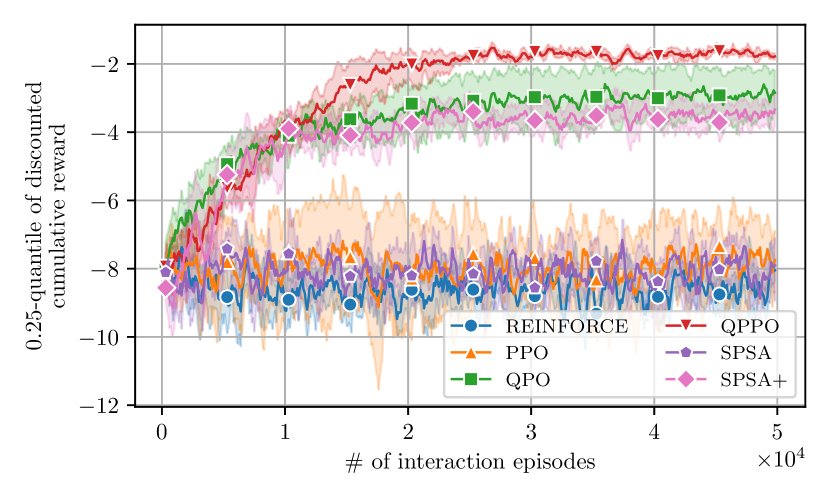

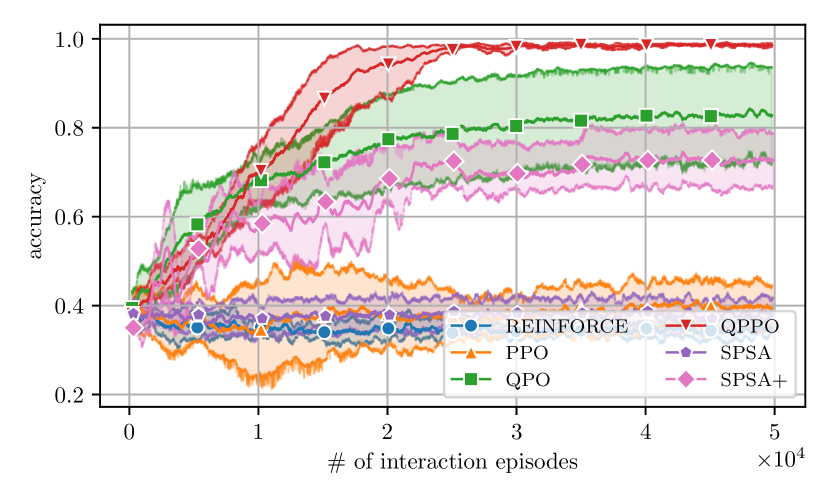

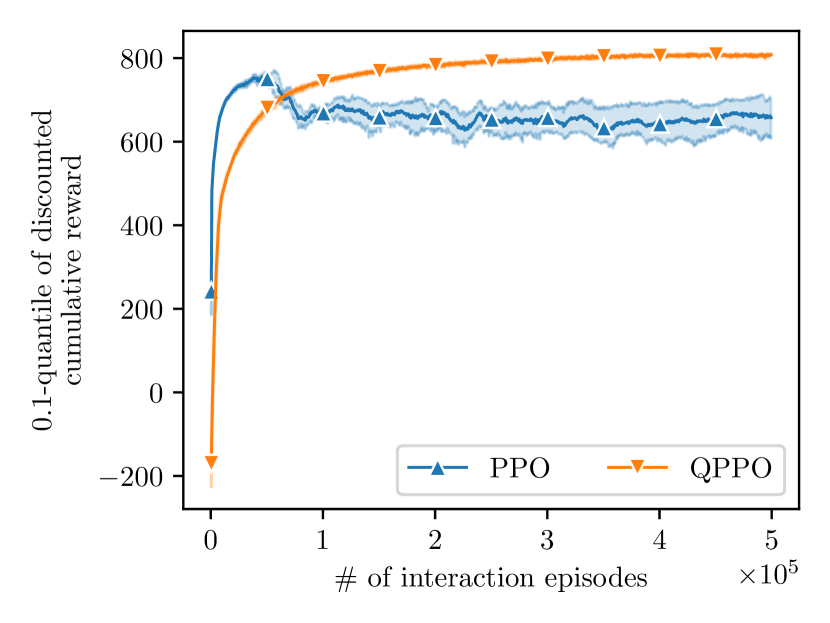

We first test REINFORCE, PPO, QPO, QPPO and SPSA on a simple setting in which the state vector takes values in . The policy and baseline are represented by multi-layer perceptrons. The agent makes decisions in time steps. The learning curves are presented in Figure 4. The quantile performance is estimated by rewards in the past episodes. The accuracy curves report the probabilities of the agent selecting the minimum alternative. The shaded areas represent the confidence intervals, and the curves are appropriately smoothed for better visibility. SPSA uses a batch of 10 samples for empirical estimation of quantile. All algorithms have the same learning rate for efficiency comparison. Due to the low efficiency of SPSA, we also use a learning rate 50 times larger than that of other algorithms in SPSA to confirm the validity of SPSA in this simple example. We can see that QPO and QPPO significantly improve the agent’s -quantile performance, while REINFORCE and PPO do not learn anything. The quantile performance of SPSA improves slowly, but the learning curve of SPSA is almost flat. In independently replicated macro experiments, QPPO outperforms others in terms of both stability and efficiency due to the improvement in data utilization.

Next, we further test the performance of quantile-based algorithms in a harder setting where the state vector takes values in . We increase the size of the neural networks. The results are shown in Figure 5, with the same plotting settings as in Figure 4.

SPSA represents SPSA with a learning rate 100 times larger than others. The advantage of QPPO over QPO and SPSA is even more obvious in the hard scenario. The results also indicate that the ability of SPSA-based algorithm is limited as the policy and environment become more complex. Due to the low data efficiency of QPO and SPSA, and the difficulty in tuning SPSA, we will no longer test these two algorithms in subsequent more complicated experiments.

6.2 Financial Investment

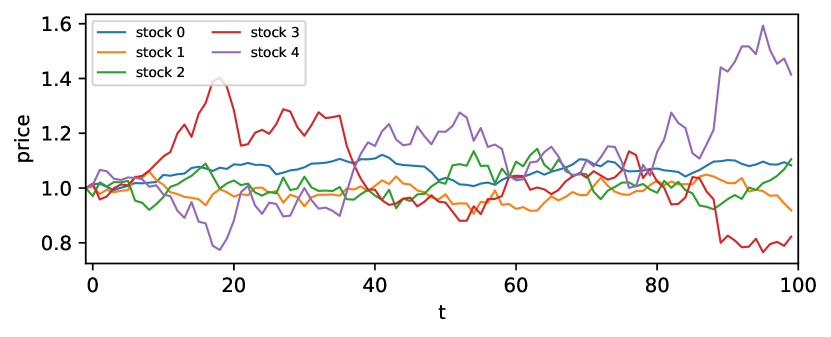

We consider a portfolio management problem with simulated prices and time steps, where high returns are associated with high risks. The price vector of the alternative assets follows a multivariate geometric Brownian motion:

| (23) |

where and are the drift and volatility, and is a Wiener process, which is widely used in finance to model stock prices, e.g., in the Black–Scholes model (Black and Scholes 1973). We generate the price paths by Monte Carlo simulation, following the Euler-Maruyama discretization (Kloeden et al. 1992) of the stochastic process (23), i.e., for , which leads to

| (24) |

where is the time interval for adjusting positions, and denotes the Hadamard product.

The agent initially holds a portfolio with a vector of random positions on assets and a fixed total value and can control the proportion of the value invested into each asset. In addition, the market has friction, i.e., there is a transaction fee of proportion every time the agent buys. Therefore, for , the new position of the -th asset is given by

where and represent and , respectively. At every time step , the agent first makes investment decisions , and calculates the total value of the portfolio under current prices and that under new prices simulated by recursion (24). The agent is rewarded by the differences of two total values, i.e., . The observation state contains the current vector of asset positions , prices and some statistics of profit margin , where , over a certain window width.

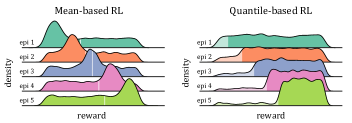

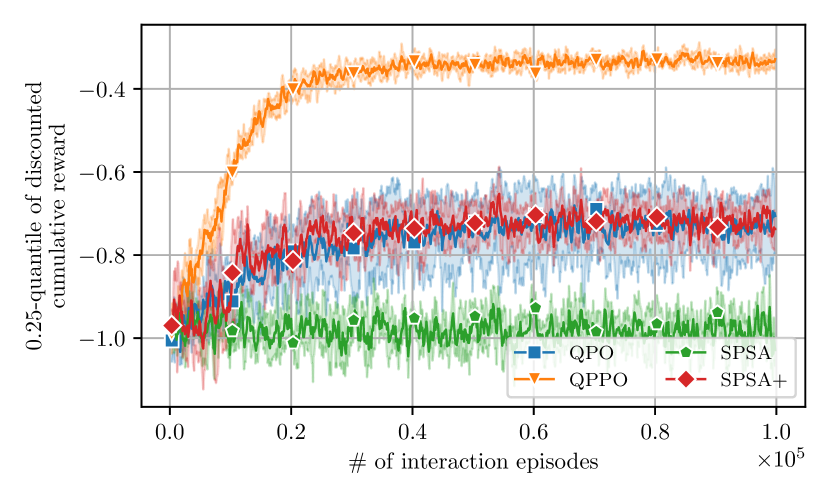

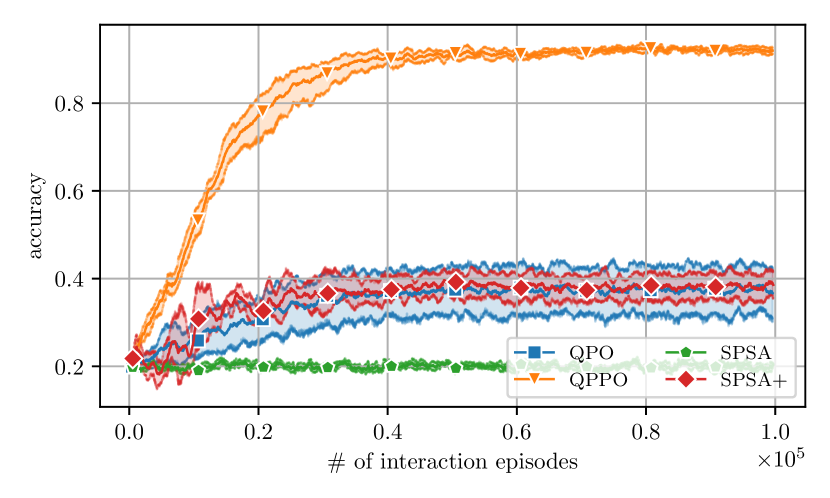

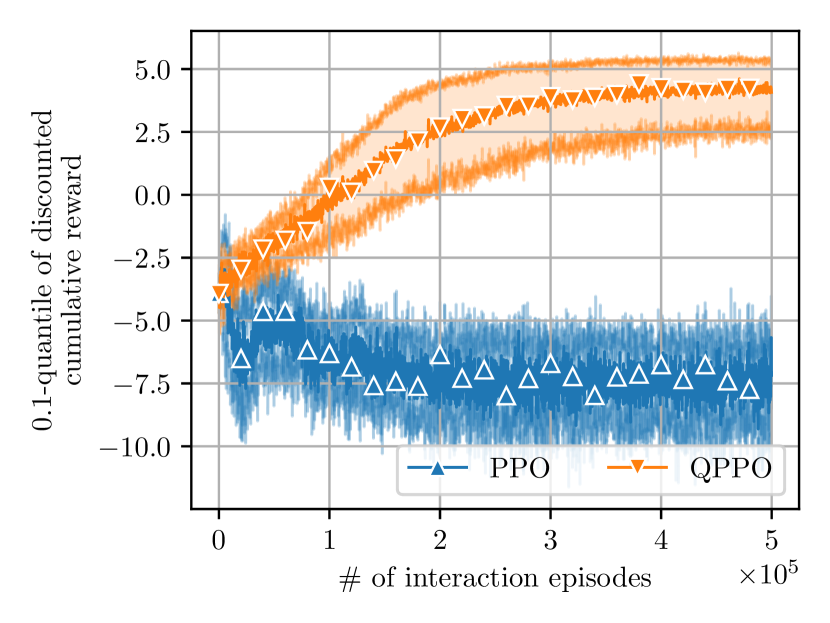

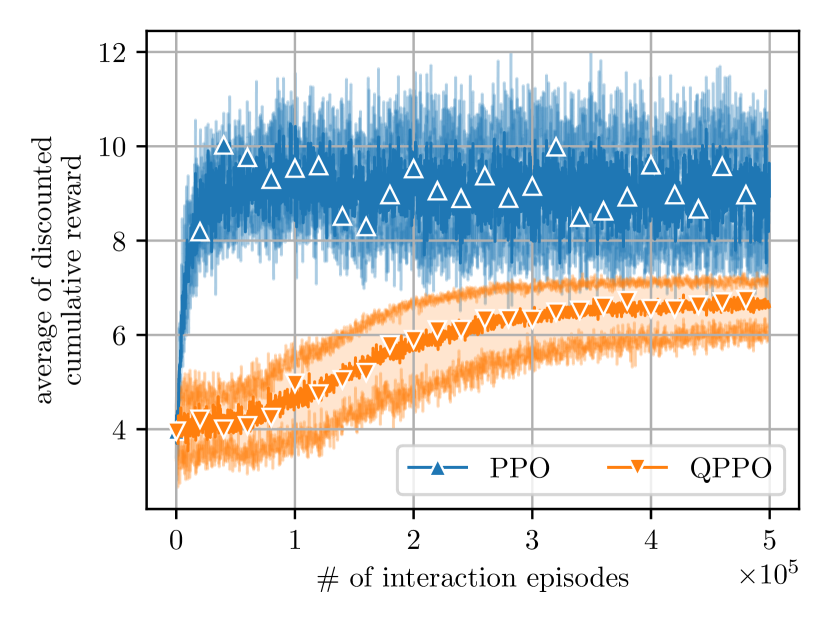

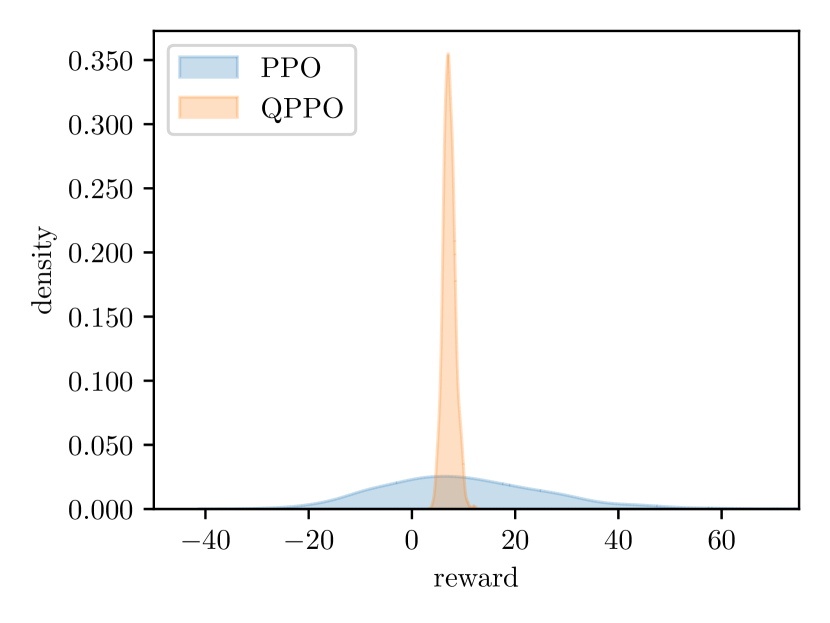

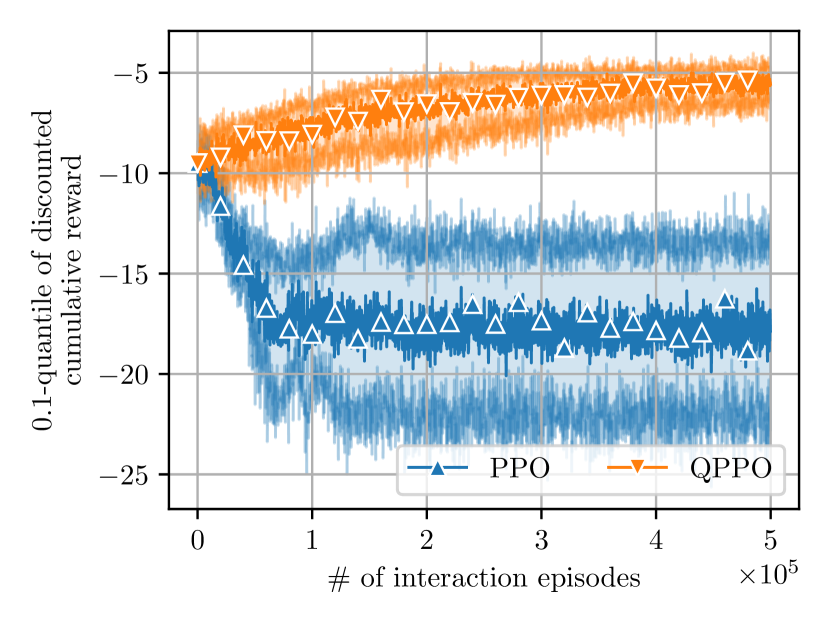

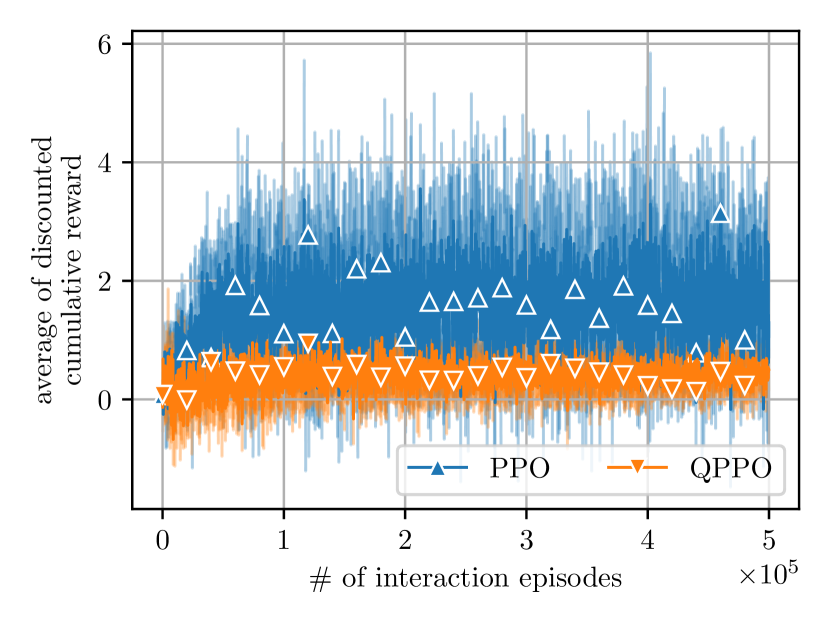

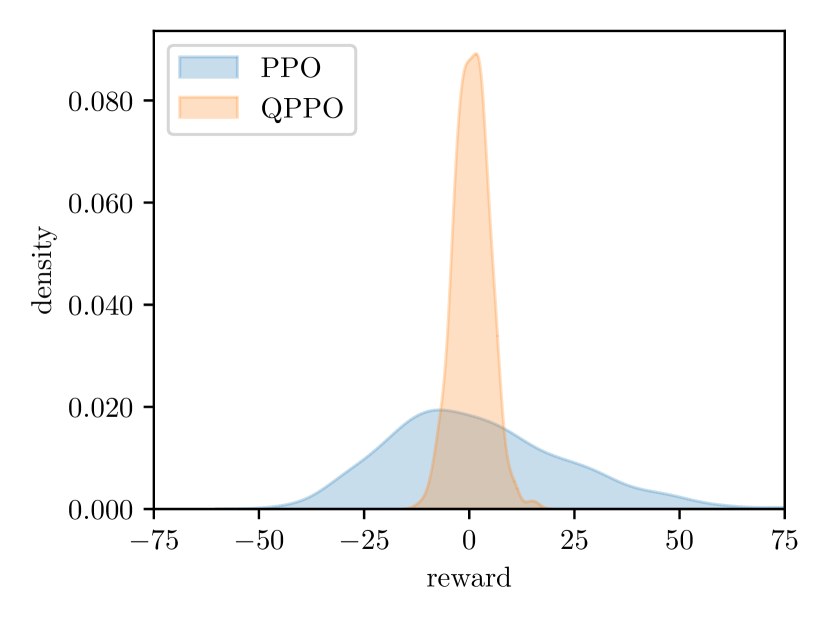

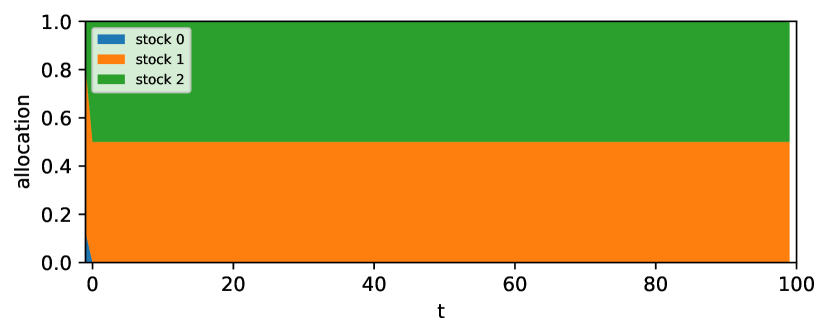

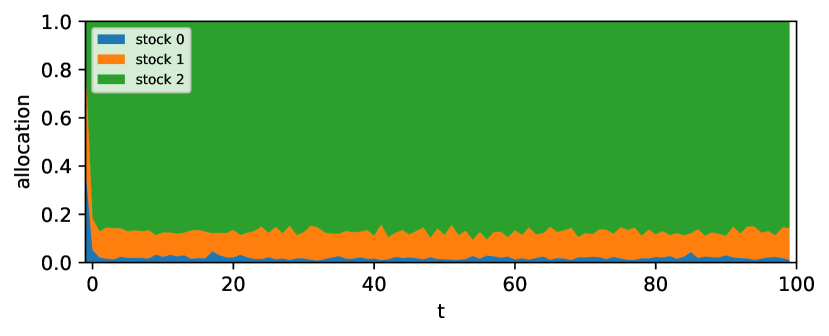

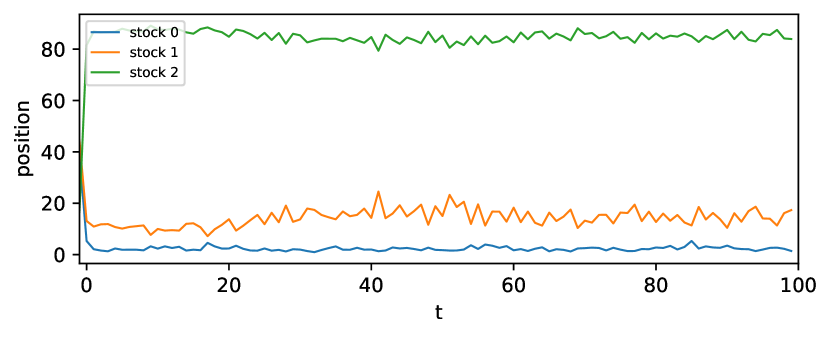

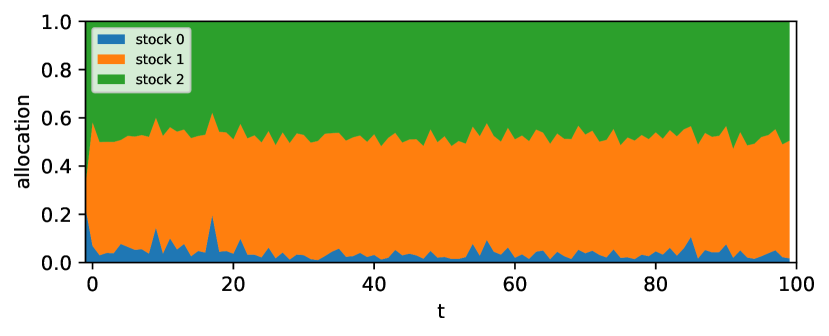

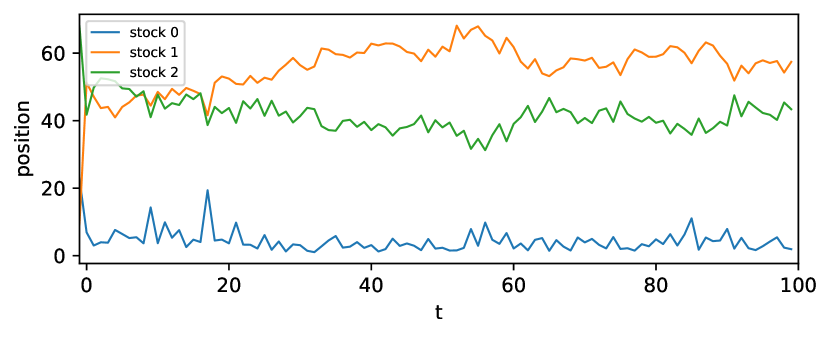

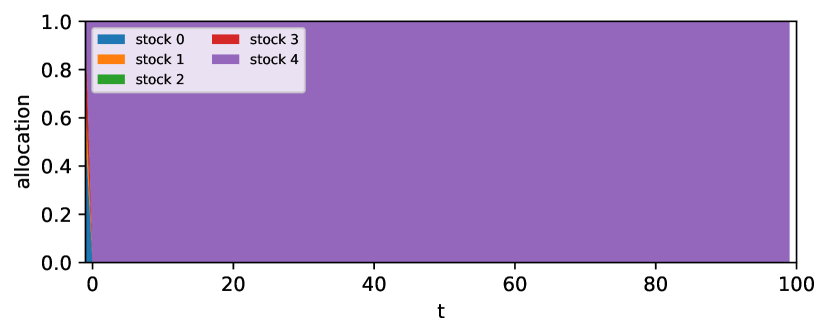

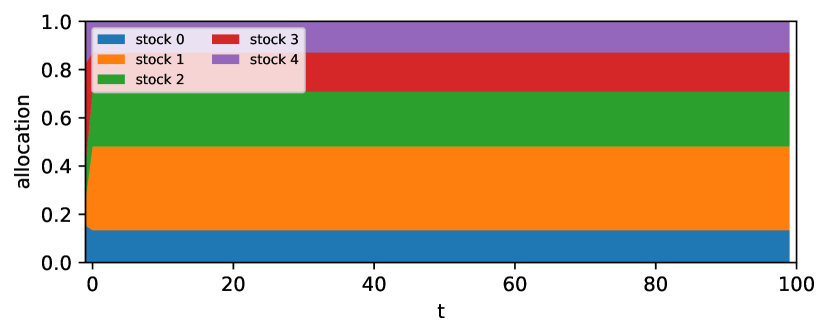

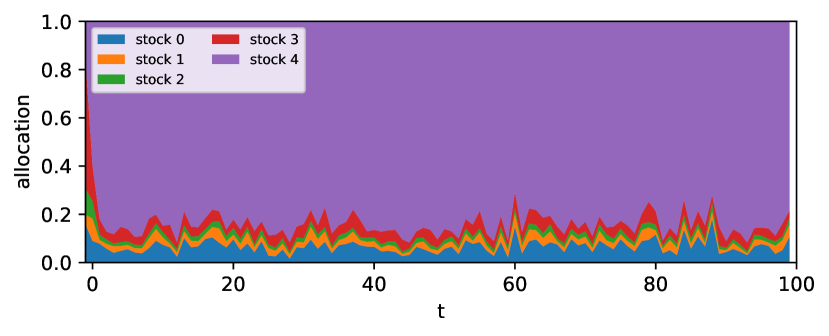

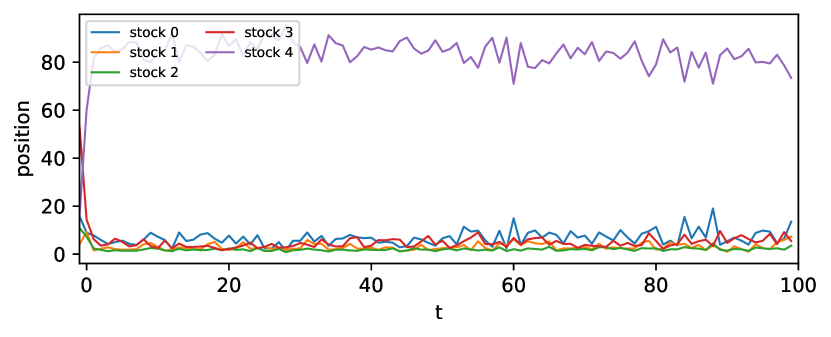

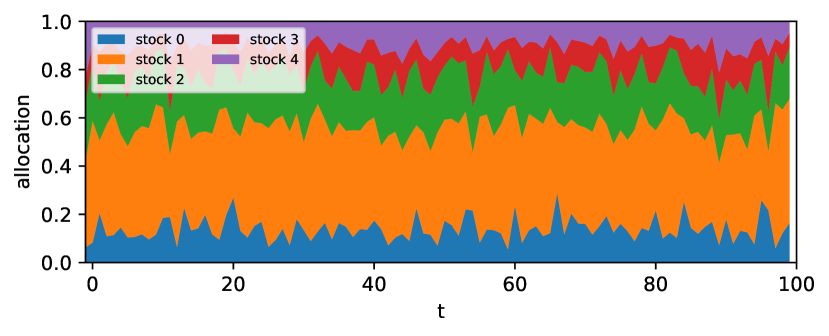

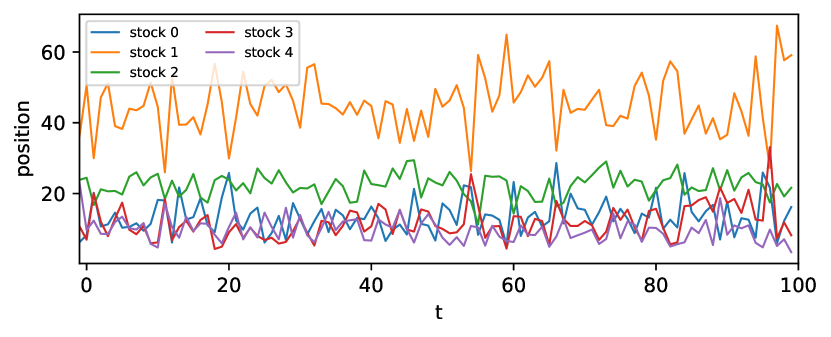

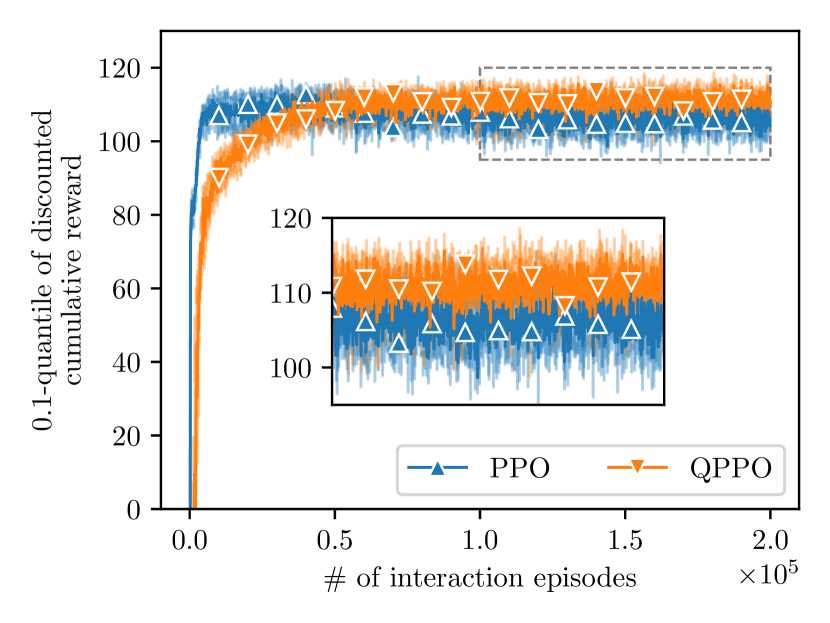

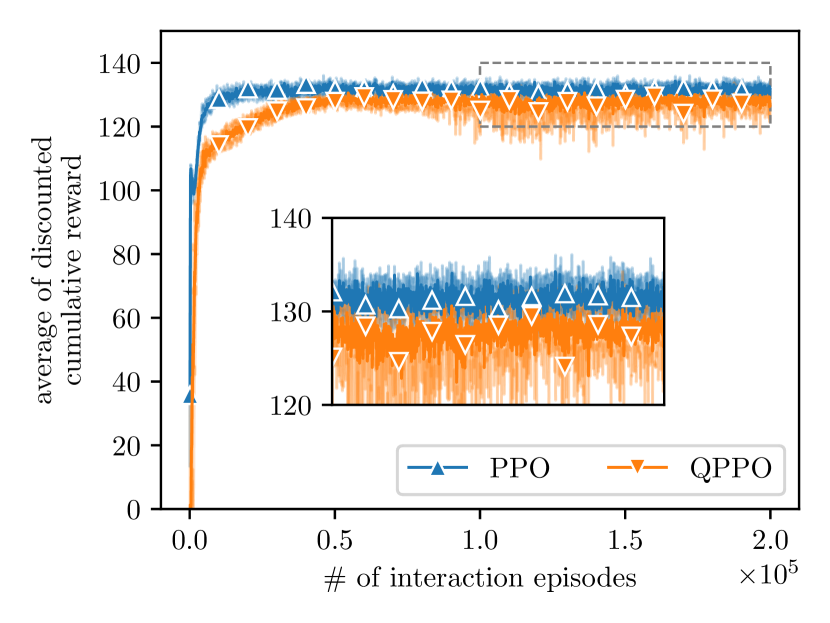

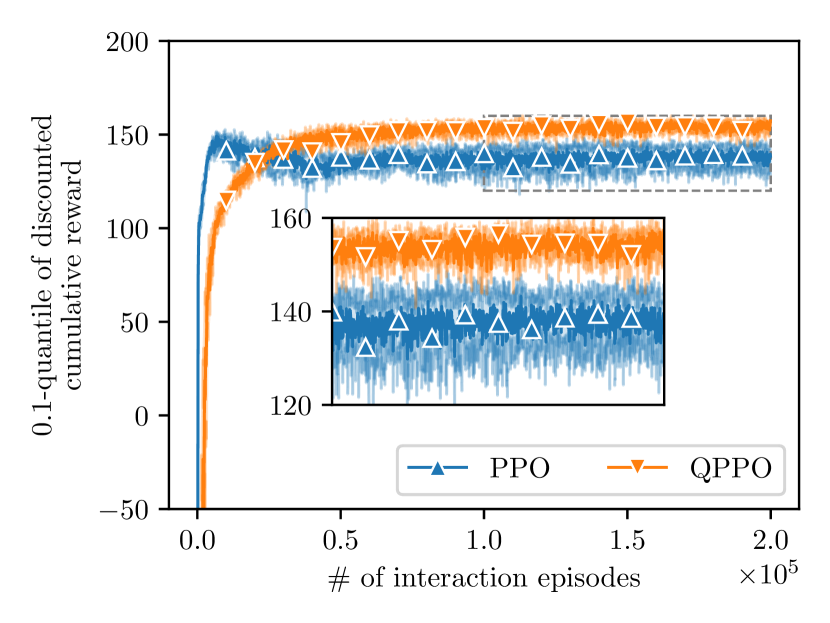

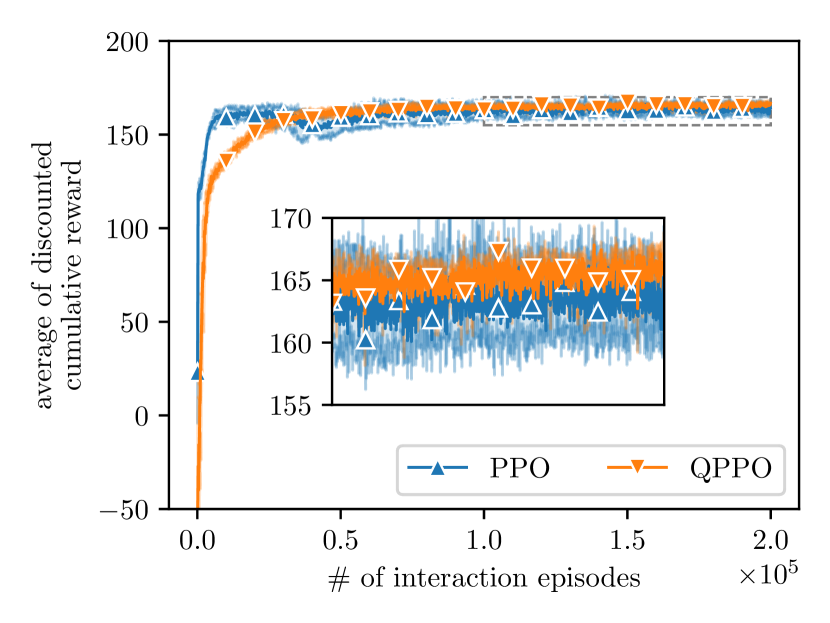

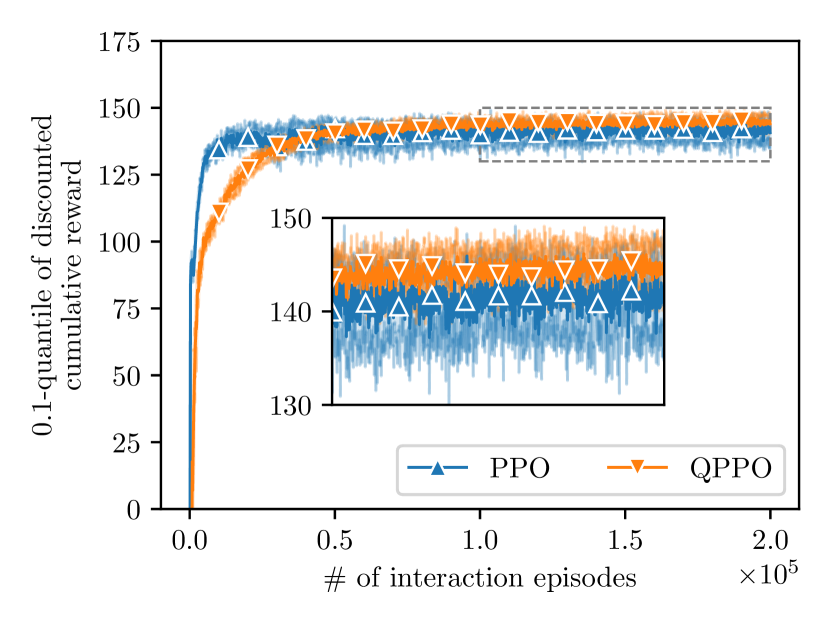

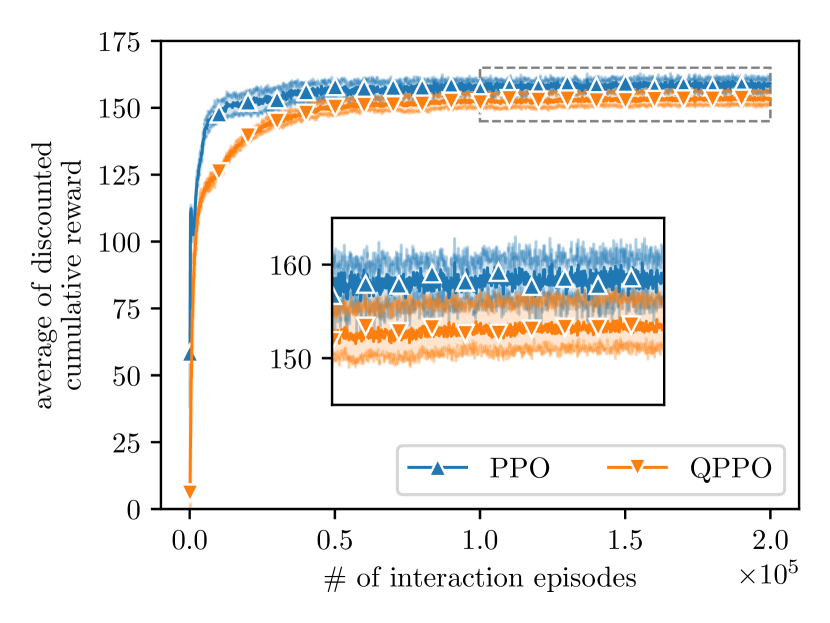

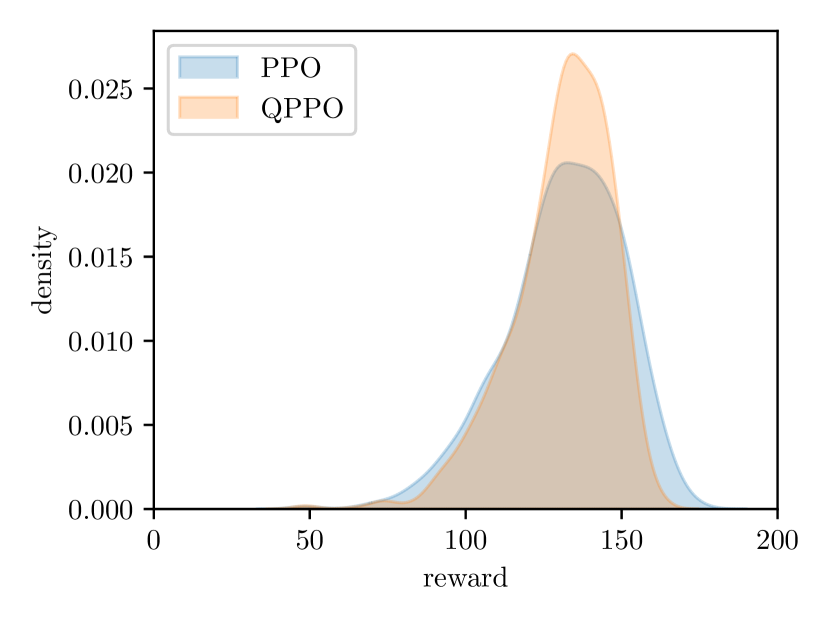

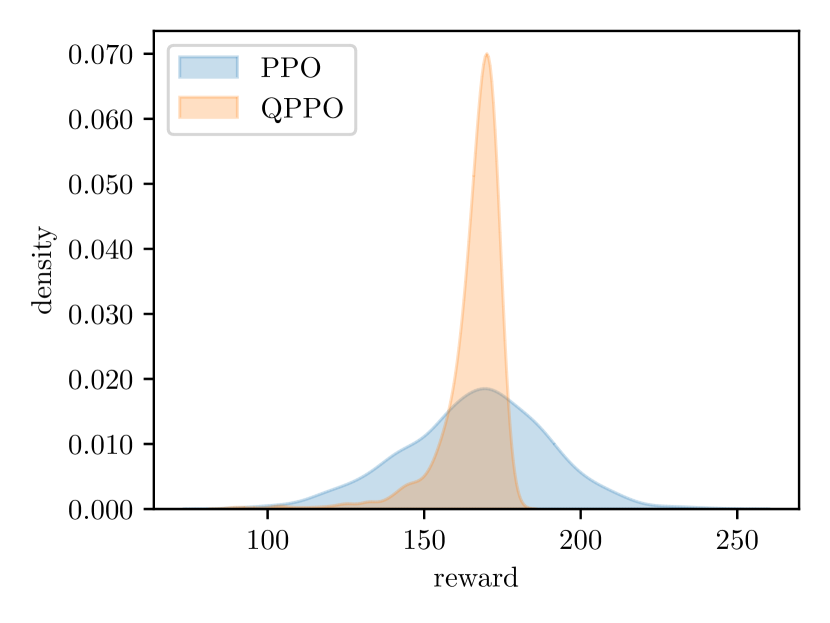

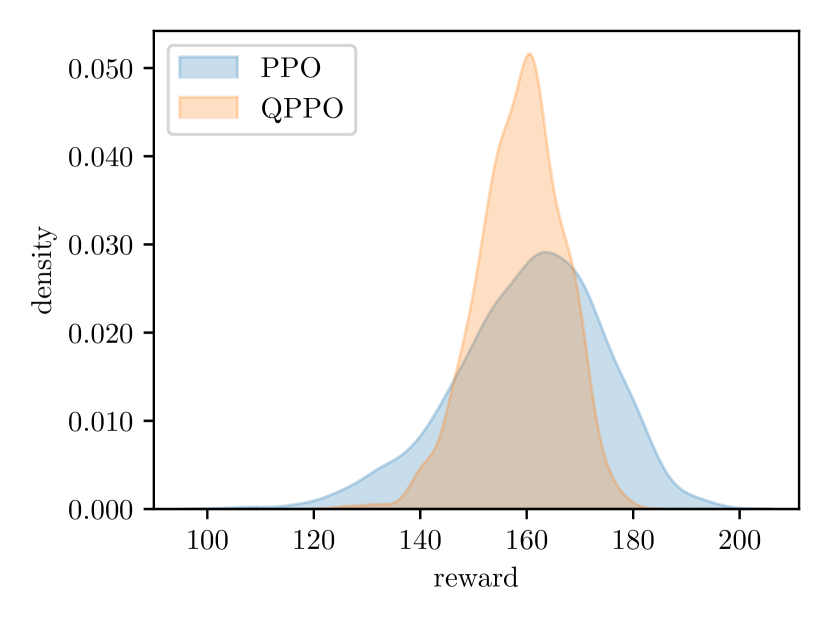

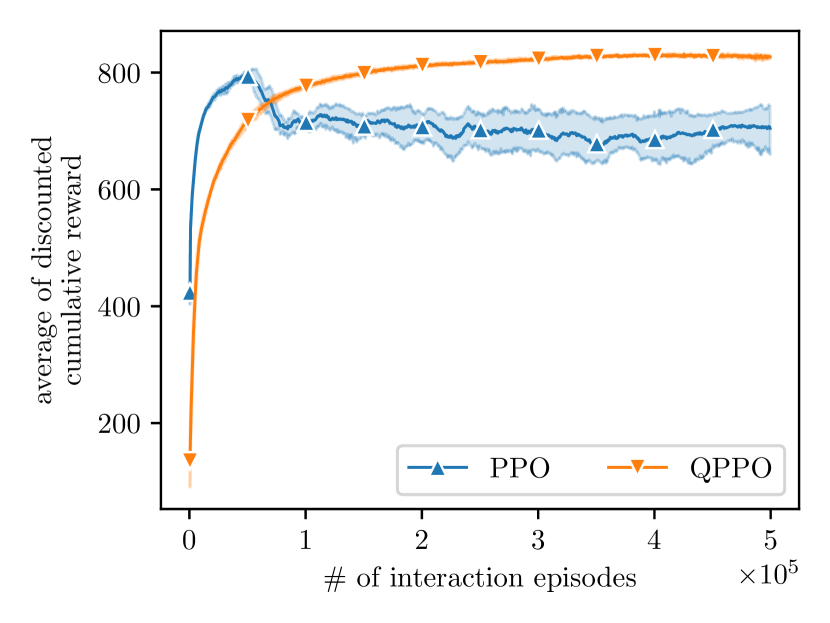

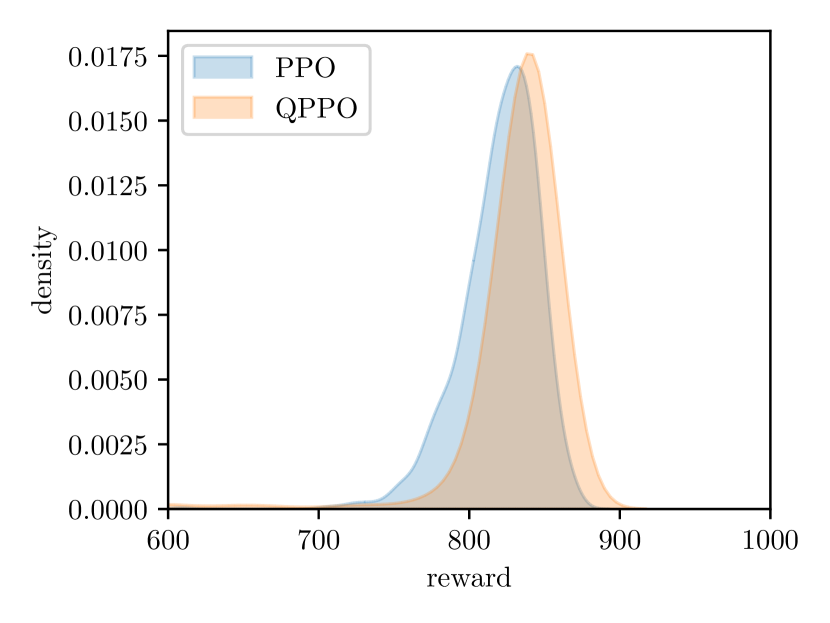

We conducted experiments in two investment portfolio management scenarios distinguished by whether the portfolio risk can be perfectly hedged or not. The volatility for each asset increases with the growth of the drift. In the perfectly hedgeable scenario, alternative assets include a low-risk asset and a pair of high-risk ones that can be fully hedged. In the imperfectly hedgeable scenario, alternative assets include a low-risk asset, a pair of medium-risk ones, and a pair of high-risk ones, but the risk cannot be fully hedged. The policy and baseline are represented by neural networks consisting of three fully connected layers. The agent invests into or assets in time steps and the observed statistics are estimated over past steps. The learning curves of PPO and QPPO calculated by independent experiments are presented in Figures 6(a, b) and 7(a, b), where (a) shows the -quantile learning curve and (b) shows the average learning curve. The quantile and average performances are estimated by rewards in the past episodes. The shaded areas represent the confidence intervals. We then test the agents after training for replications and plot the kernel density estimation (KDE) in Figures 6(c) and 7(c). Although PPO leads to a slight advantage in average rewards, the advantage of QPPO in terms of 0.1-quantile is significant. Particularly, note that the 0.1-quantile learning curves of PPO even decrease with more training episodes. The advantage of QPPO appears to be more significant in the imperfectly hedgeable scenario which is more challenging in risk management. Moreover, the KDE of rewards obtained by QPPO is much more concentrated relative to that obtained by PPO, which means that the extreme outcomes would appear much less often by using QPPO.

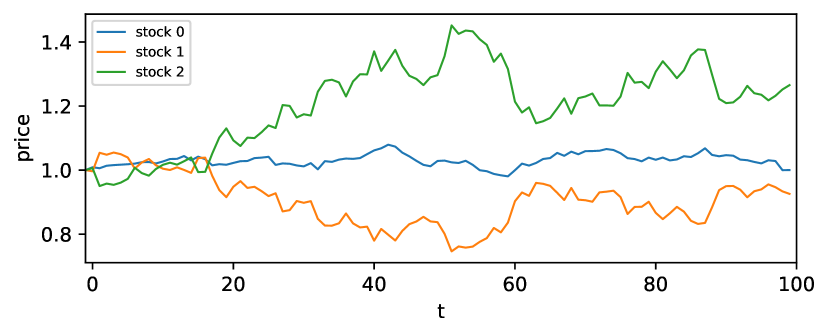

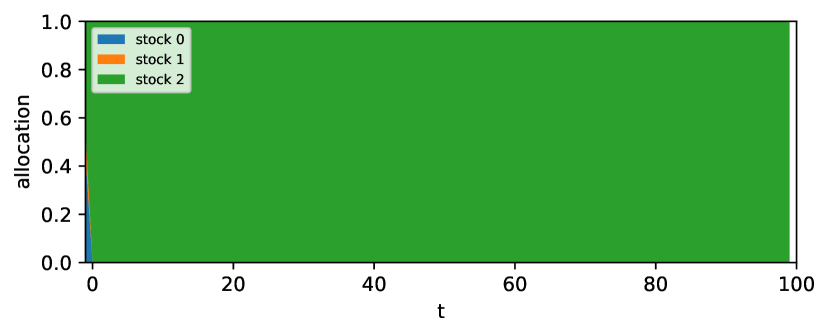

To further investigate the policies of the two agents, we fine tune their networks and visualize their behavior in Figures 8 and 9. Note that the profit margin follows a multivariate Gaussian distribution , so the quantile can be calculated directly by a linear combination of the real mean and variance. Therefore, we can solve the best asset allocation under both criteria by Markowitz model (Fabozzi et al. 2008) ignoring the compound interest and transaction fee in reinvestment. As shown in Figures 8 and 9, both algorithms reproduce the results of Markowitz model. With the help of deep RL, we are able to solve optimal quantile-based asset allocation problem after taking market frictions into consideration. In both scenarios, the agent trained by PPO invests all cash into the asset with the highest expected return, whereas the agent trained by QPPO invests in assets with negative correlations to hedge against risks. The slight difference between the position determined by the Markowitz model and that determined by QPPO is because of the fact that transaction fee is ignored by the the Markowitz model while it is taken into account by QPPO, and the position determined by the Markowitz model only solves a static quantile optimization while the position determined by the QPPO algorithm is the outcome of an optimal policy for an MDP under the quantile criterion.

6.3 Inventory Management

Solving multi-echelon inventory management by deep RL has attracted attention in operation management recently (Gijsbrechts et al. 2022). The existing literature considers optimizing the ordering policy under the criterion of expected inventory profit. We focus on an inventory management problem with lost sales in a multi-echelon supply chain system, which is more difficult than the backlogging case because the optimal decision depends on the entire inventory pipeline.

We consider an -echelon supply chain during periods and index echelons by integers from to , where the first and last echelons are the customer and manufacturer, respectively, and the rest represents the intermediate echelons. We use , and to denote the goods shipped by echelon , the lost sales and on-hand inventory of echelon at the end of period . The quantity ordered by echelon from echelon is denoted as , with being the customer’s demand. In each period , the agent can control the ordering quantities of intermediate echelons. For , the shipped quantities and lost sales of the intermediate echelons are given by

where denotes the lead time for shipping goods in echelon . Then the on-hand inventory is updated by

Note that the manufacturer always has unlimited resources, i.e., . The profit of each echelon is calculated below:

where , and are the unit price, unit holding cost and unit penalty for lost sales of echelon . The observation state consists of the inventories, lost sales, shipped and ordering quantities in past periods, and the rewards of the agent are the total supply chain profits, i.e., .

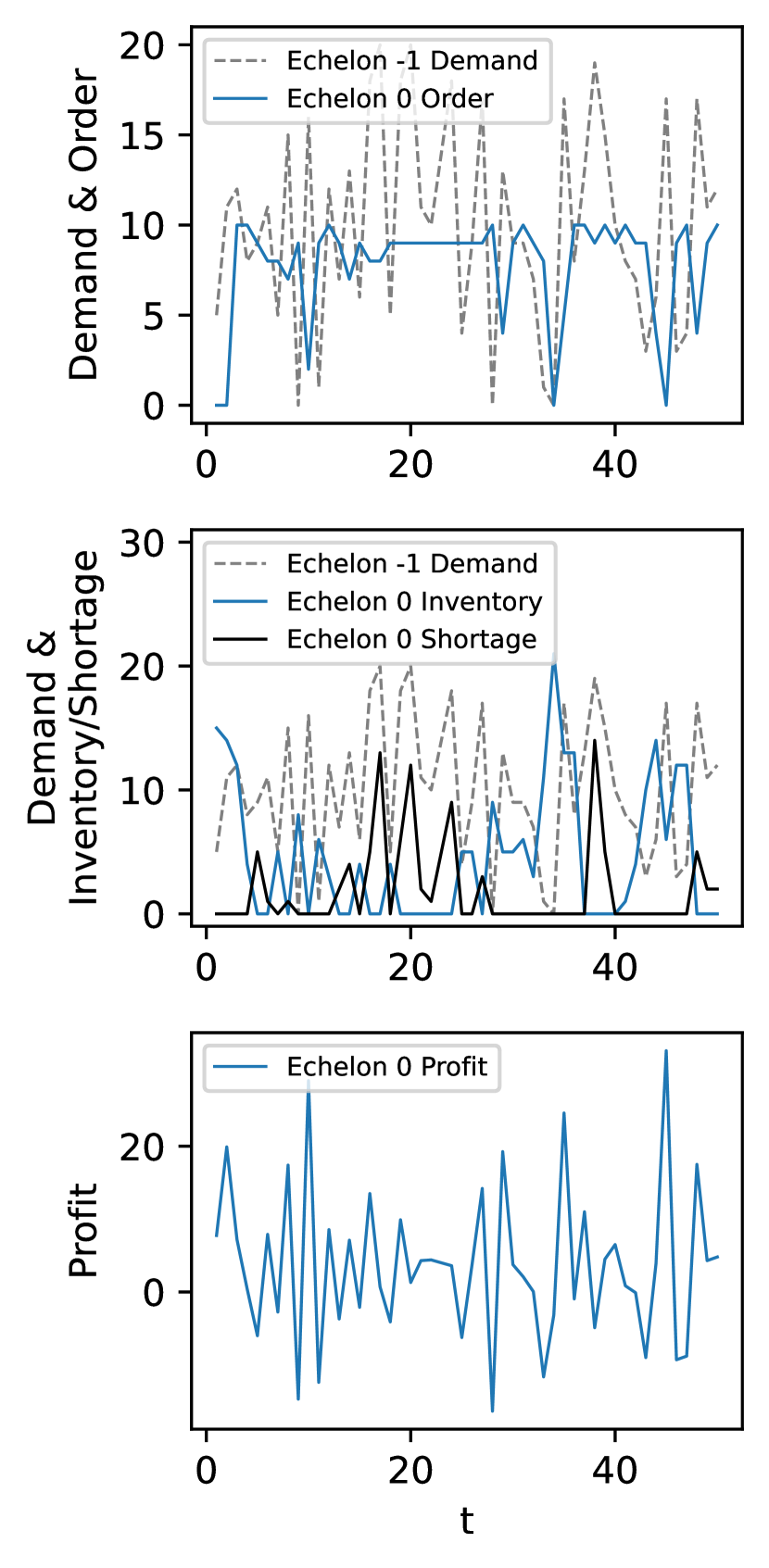

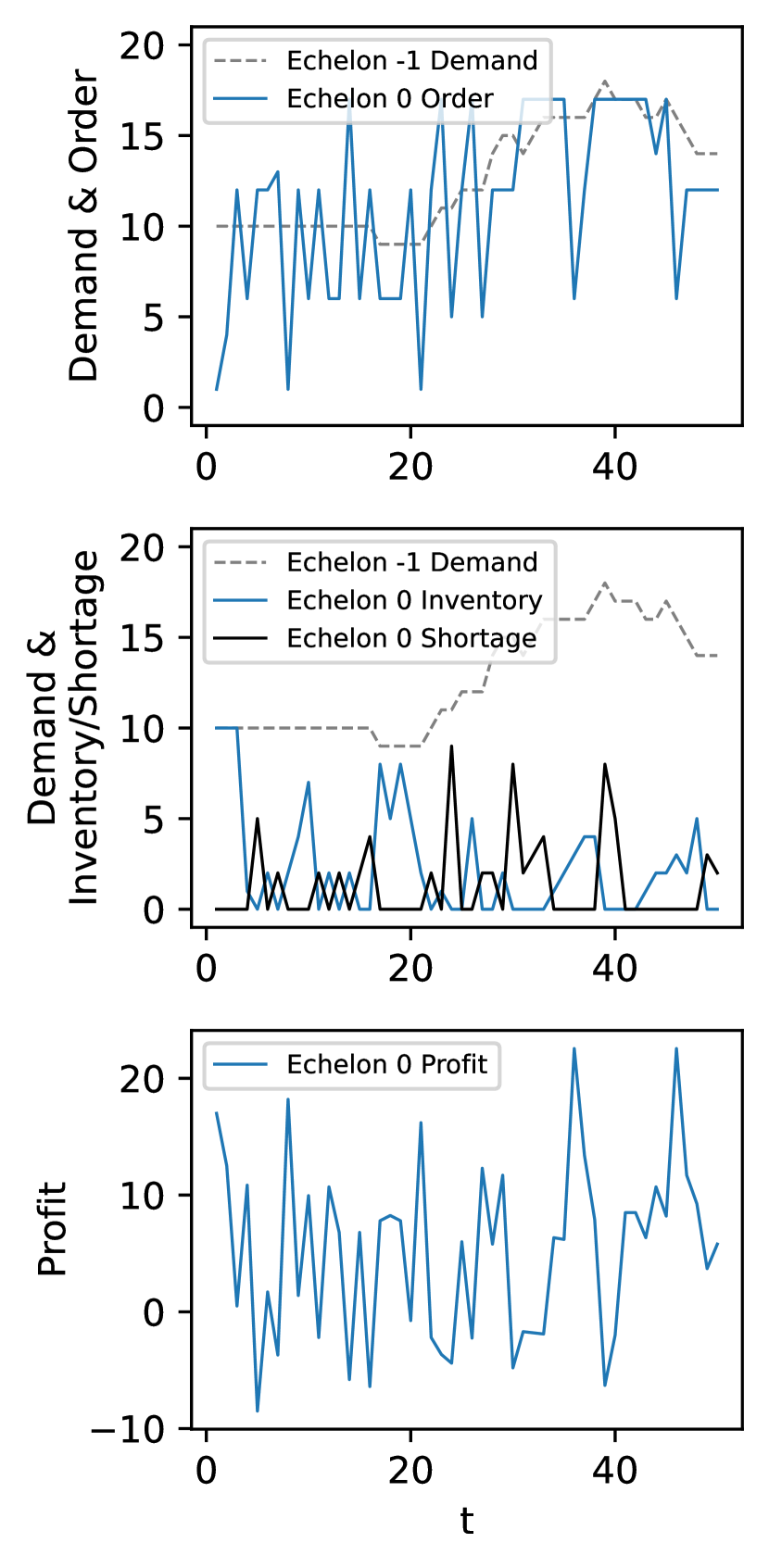

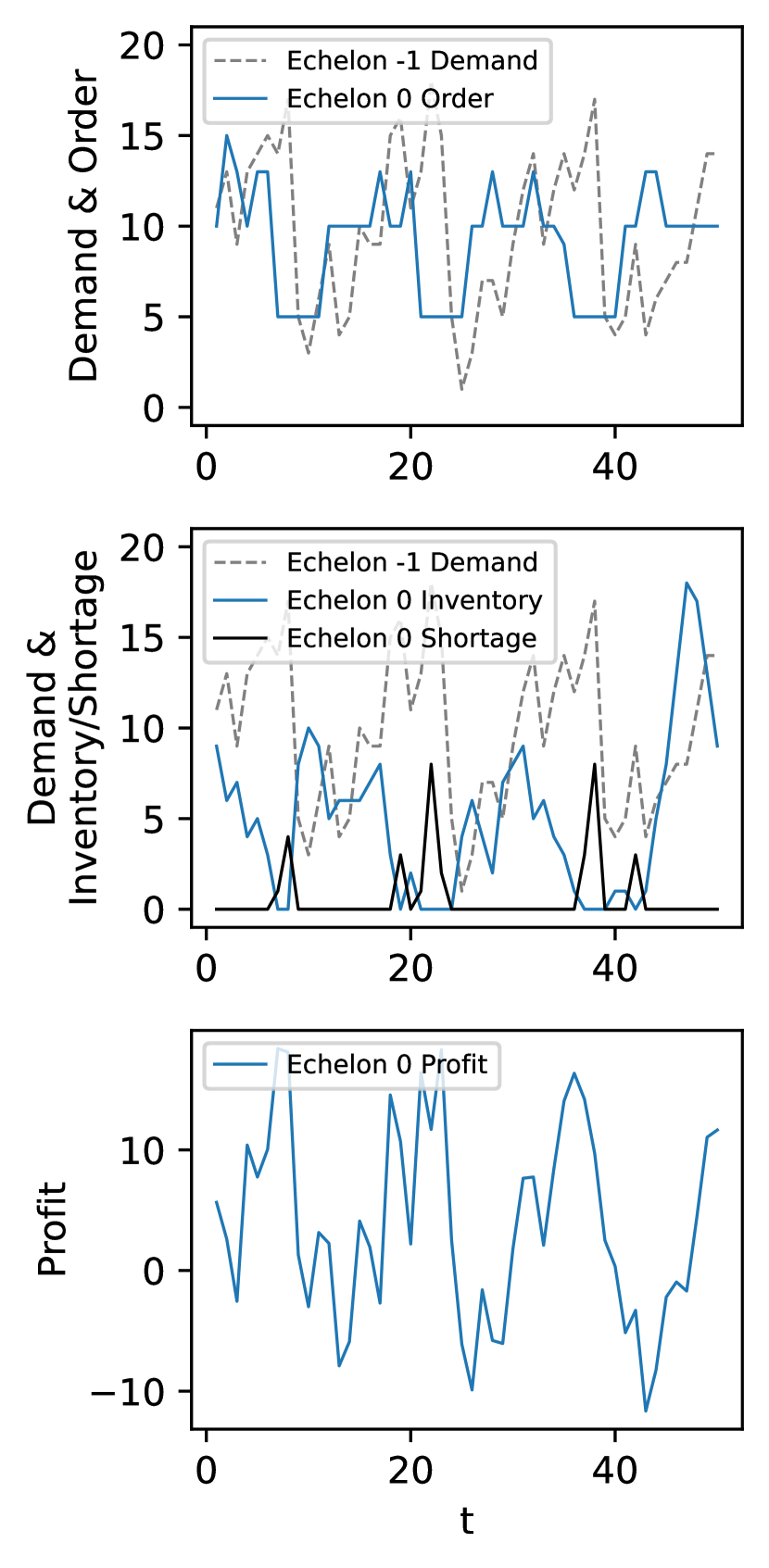

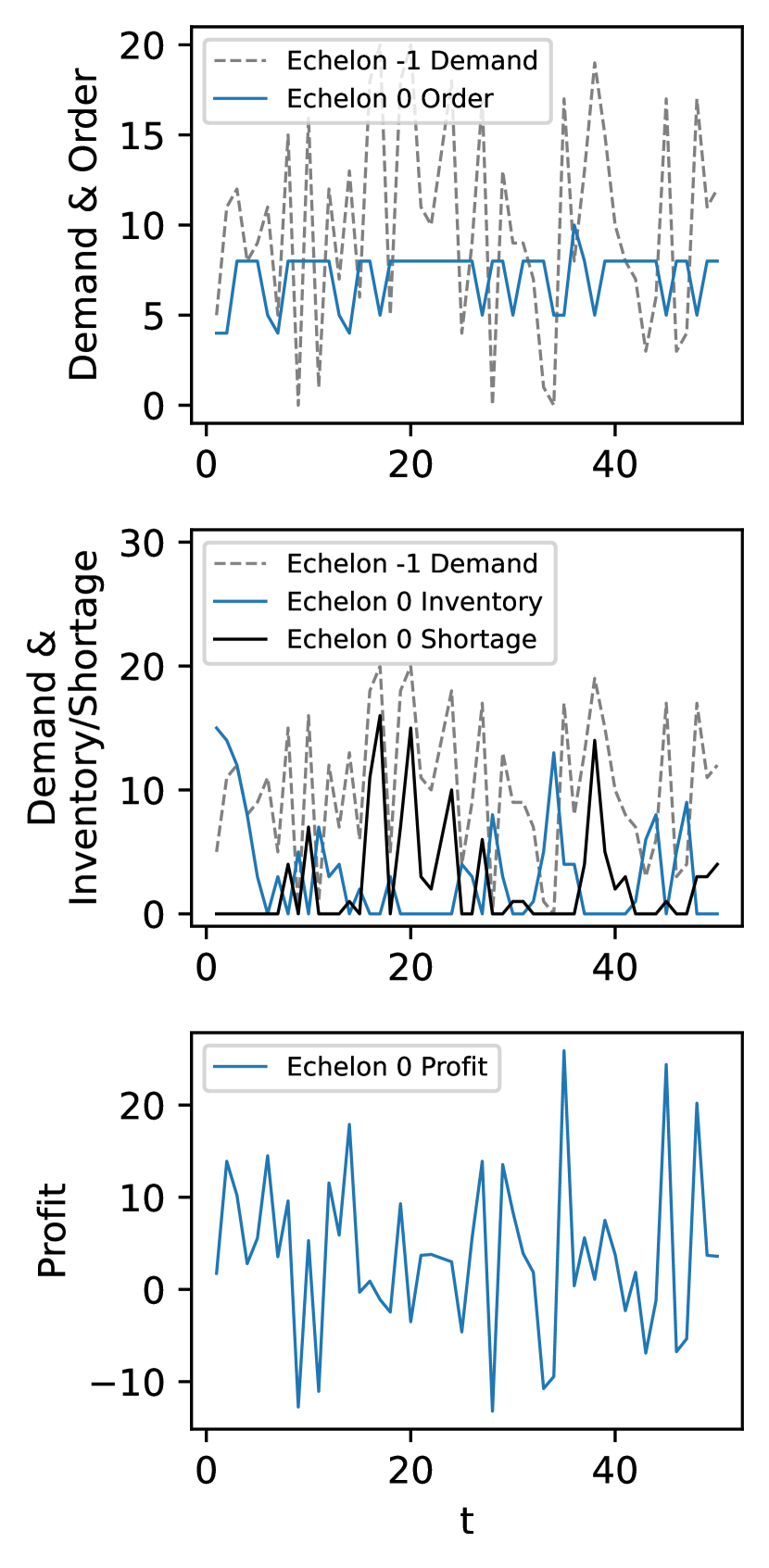

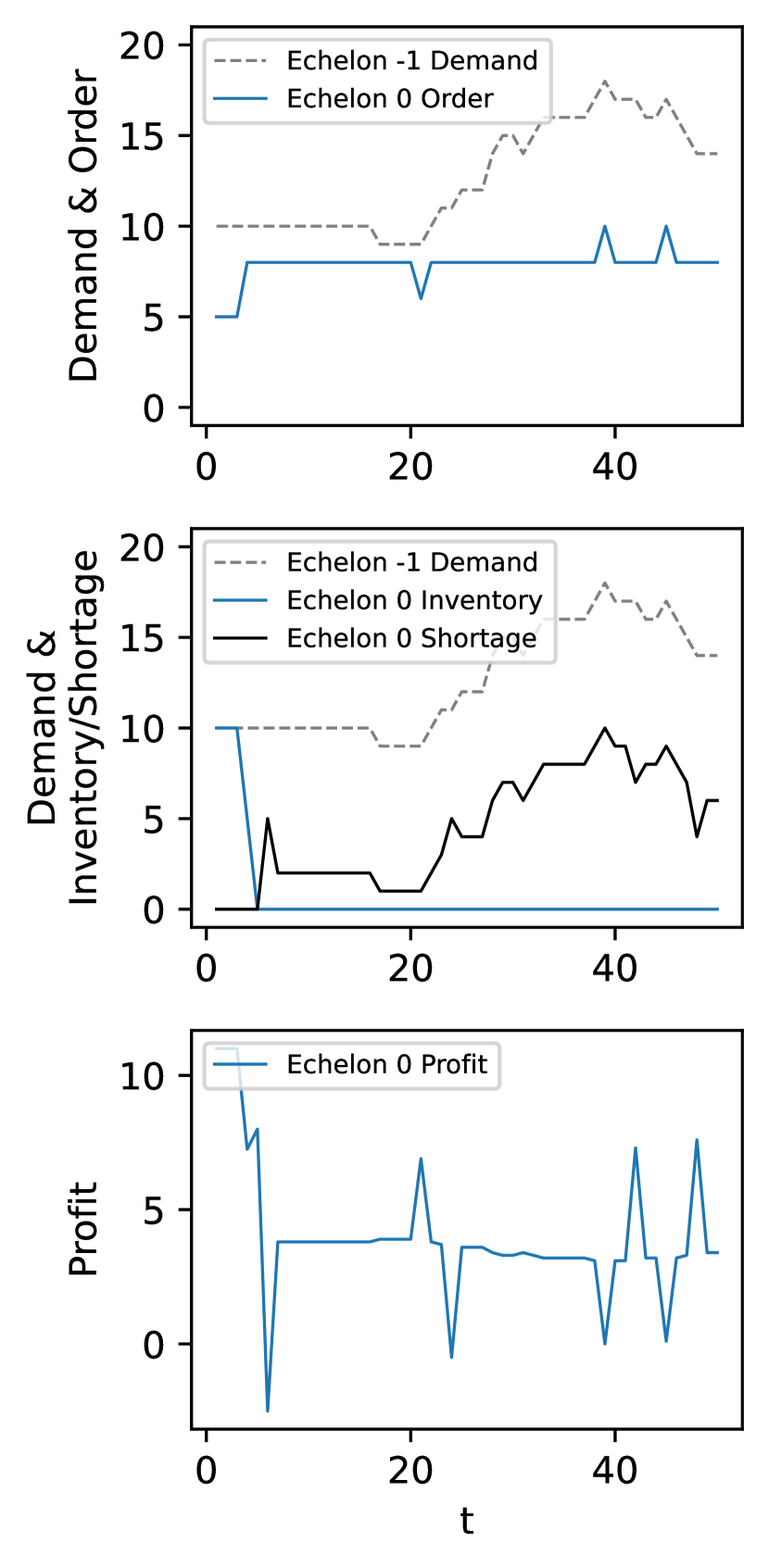

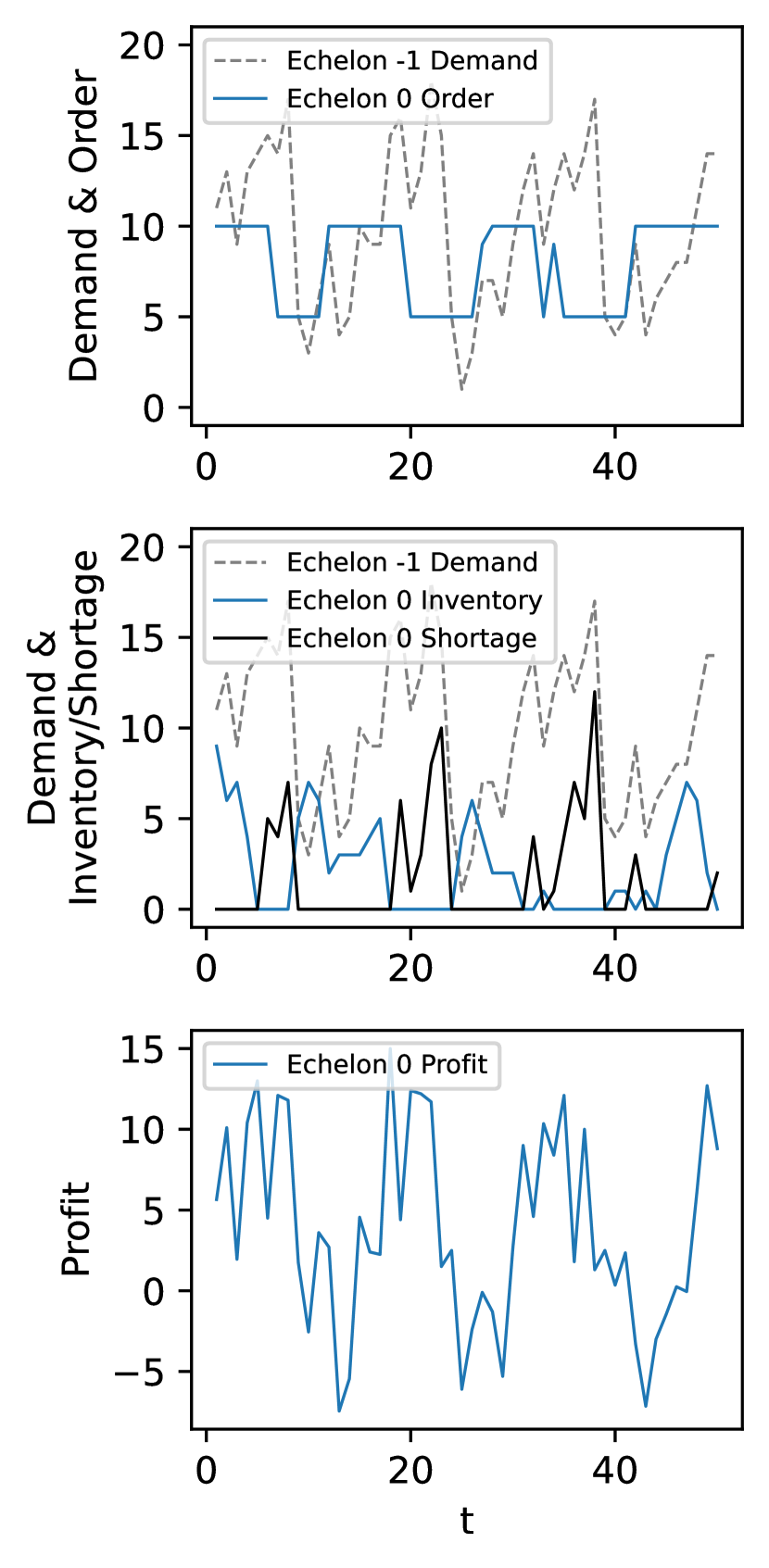

We first apply PPO and QPPO to three single-echelon inventory management problems, where customer demands are generated from a uniform distribution, Merton jump diffusion model (Merton 1976), and a periodic stochastic model with a saw-wave trend, respectively. The policy and baseline are represented by neural networks consisting of a temporal convolutional layer and a fully connected layer. The agent makes reordering decisions in time steps and can look back at information within the past steps. The learning curves of PPO and QPPO are presented in Figure 10. The quantile and average performances are estimated by rewards in the past episodes. The shaded areas represent the confidence intervals.

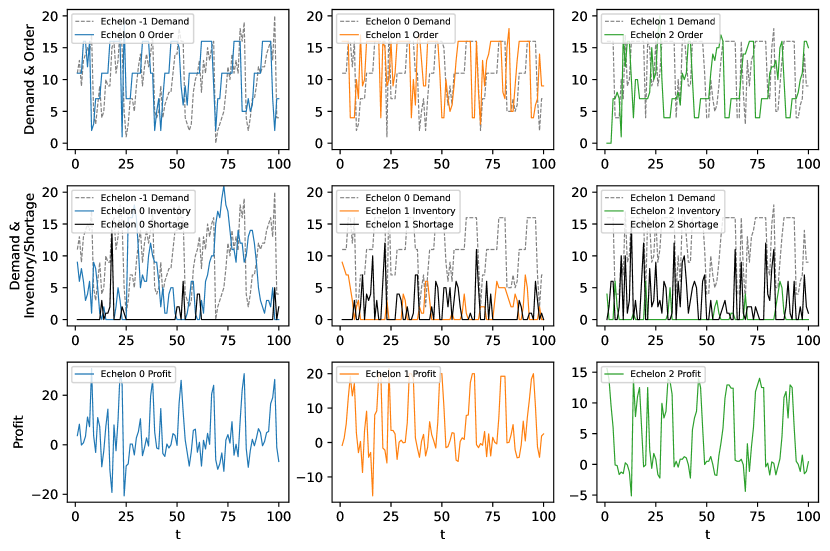

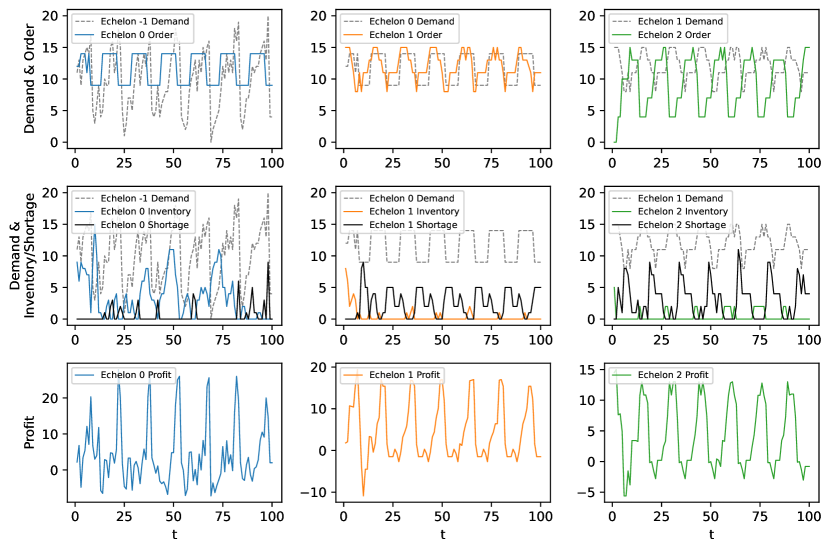

The steep initial climb in the learning curve indicates that QPPO has a comparable learning ability as the state-of-the-art mean-based algorithm, PPO. Meanwhile, QPPO achieves higher -quantile performance at the end of the training. We test the agents for replications after training and present the results in Figure 11 and Table 1. In all single-echelon examples, QPPO achieves much superior -quantile performance with only a slight loss in mean compared to PPO, and its KDE is much more concentrated than PPO. The agents’ policies after training can be visualized in Figures 12 and 13. The oscillation of the profits obtained by QPPO is narrower than that of PPO. Although the performances of PPO and QPPO in simple single-echelon problems occasionally lead to similar statistics, agents’ policies are significantly different. The reordering decisions of PPO change dramatically as customer’s demand changes, which are difficult to implement in practice. The decisions of QPPO are relatively stable, with limited amplitude and frequency of changes.

| Demand | -quantile | Average | ||

|---|---|---|---|---|

| PPO | QPPO | PPO | QPPO | |

| Uniform | ||||

| Merton | ||||

| Periodical | ||||

We further conduct experiments in a multi-echelon inventory management problem in which customer demands are generated by using a periodical stochastic model with a saw-wave trend. The policy and baseline are represented by neural networks consisting of two temporal convolutional layers and three parallel fully connected blocks to control each echelon. The agent makes reordering decisions in time steps and can look back at information within the past steps. The learning curves obtained through independent experiments and testing KDE plotted based on by replications are shown in Figure 14 with the plotting settings the same as the single-echelon case. The policies generated by both algorithms are shown in Figure 15. Although the ordering behavior of both agents show periodical patterns, QPPO’s reordering quantities are almost the same in each period with smaller amplitude, whereas PPO leads to dramatic inventory adjustment more frequently. We note that the performance of PPO degrades in the later stage. In addition, QPPO outperforms PPO under both criteria in this example, which suggests that it may be more desirable to solve multi-echelon supply chain inventory management problems from a quantile optimization perspective.

7 Conclusions

In this paper, we have proposed the QPO algorithm for RL with a quantile criterion under a policy optimization framework. We have shown that QPO converges to the global optimum under certain conditions and derived its rates of convergence. Then, we have introduced an off-policy version QPPO, which significantly improves the learning efficiency of agents. Convergence and new error bounds are established to provide insights into the theoretical performance of QPPO with new computational architecture. Numerical experiments show that our proposed algorithms are effective for policy optimization under the quantile criterion. In finance, QPPO can learn how to hedge against risk based on the rewards obtained in the process of investment. In inventory management, QPPO can learn to control the tail risk and lead to more stable reordering decisions. In the future work, the criterion can be extended to the distortion risk measures that are more general than quantiles (Glynn et al. 2021). The codes that support this study can be found in https://github.com/JinyangJiangAI/Quantile-based-Policy-Optimization.

This work was supported in part by the National Natural Science Foundation of China (NSFC) under Grants 72250065, 72022001, and 71901003.

References

- Abada and Lambin (2020) Abada I, Lambin X (2020) Artificial intelligence: Can seemingly collusive outcomes be avoided? Management Science .

- Baldacci et al. (2022) Baldacci B, Manziuk I, Mastrolia T, Rosenbaum M (2022) Market making and incentives design in the presence of a dark pool: A stackelberg actor–critic approach. Operations Research .

- Bertsekas (1997) Bertsekas DP (1997) Nonlinear programming. Journal of the Operational Research Society 48(3):334–334.

- Beyerlein (2014) Beyerlein A (2014) Quantile regression—opportunities and challenges from a user’s perspective. American Journal of Epidemiology 180(3):330–331.

- Bhandari et al. (2021) Bhandari J, Russo D, Singal R (2021) A finite time analysis of temporal difference learning with linear function approximation. Operations Research 69(3):950–973.

- Black and Scholes (1973) Black F, Scholes M (1973) The pricing of options and corporate liabilities. Journal of political economy 81(3):637–654.

- Borkar and Jain (2014) Borkar V, Jain R (2014) Risk-constrained markov decision processes. IEEE Transactions on Automatic Control 59(9):2574–2579.

- Borkar (1997) Borkar VS (1997) Stochastic approximation with two time scales. Systems & Control Letters 29(5):291–294.

- Borkar (2001) Borkar VS (2001) A sensitivity formula for risk-sensitive cost and the actor–critic algorithm. Systems & Control Letters 44(5):339–346.

- Cen et al. (2022) Cen S, Cheng C, Chen Y, Wei Y, Chi Y (2022) Fast global convergence of natural policy gradient methods with entropy regularization. Operations Research 70(4):2563–2578.

- Chow and Ghavamzadeh (2014) Chow Y, Ghavamzadeh M (2014) Algorithms for cvar optimization in mdps. Advances in Neural Information Processing Systems 27.

- Chow et al. (2017) Chow Y, Ghavamzadeh M, Janson L, Pavone M (2017) Risk-constrained reinforcement learning with percentile risk criteria. The Journal of Machine Learning Research 18(1):6070–6120.

- Chow and Pavone (2013) Chow YL, Pavone M (2013) Stochastic optimal control with dynamic, time-consistent risk constraints. 2013 American Control Conference, 390–395 (IEEE).

- DeCandia et al. (2007) DeCandia G, Hastorun D, Jampani M, Kakulapati G, Lakshman A, Pilchin A, Sivasubramanian S, Vosshall P, Vogels W (2007) Dynamo: Amazon’s highly available key-value store. ACM SIGOPS Operating Systems Review 41(6):205–220.

- Durrett (2019) Durrett R (2019) Probability: Theory and Examples, volume 49 (Cambridge university press).

- Fabozzi et al. (2008) Fabozzi FJ, Markowitz HM, Gupta F (2008) Portfolio selection. Handbook of finance 2.

- Fu (2006) Fu MC (2006) Gradient estimation. Handbooks in Operations Research and Management Science 13:575–616.

- Fu et al. (2009) Fu MC, Hong LJ, Hu JQ (2009) Conditional monte carlo estimation of quantile sensitivities. Management Science 55(12):2019–2027.

- Gijsbrechts et al. (2022) Gijsbrechts J, Boute RN, Van Mieghem JA, Zhang DJ (2022) Can deep reinforcement learning improve inventory management? performance on lost sales, dual-sourcing, and multi-echelon problems. Manufacturing & Service Operations Management 24(3):1349–1368.

- Glasserman (2004) Glasserman P (2004) Monte Carlo methods in financial engineering, volume 53 (Springer).

- Glynn and Iglehart (1989) Glynn PW, Iglehart DL (1989) Importance sampling for stochastic simulations. Management Science 35(11):1367–1392.

- Glynn et al. (2021) Glynn PW, Peng Y, Fu MC, Hu JQ (2021) Computing sensitivities for distortion risk measures. INFORMS Journal on Computing 33(4):1520–1532.

- Haarnoja et al. (2018) Haarnoja T, Zhou A, Abbeel P, Levine S (2018) Soft actor-critic: Off-policy maximum entropy deep reinforcement learning with a stochastic actor. International Conference on Machine Learning, 1861–1870 (PMLR).

- Heidergott and Volk-Makarewicz (2016) Heidergott B, Volk-Makarewicz W (2016) A measure-valued differentiation approach to sensitivities of quantiles. Mathematics of Operations Research 41(1):293–317.

- Hessel et al. (2018) Hessel M, Modayil J, Van Hasselt H, Schaul T, Ostrovski G, Dabney W, Horgan D, Piot B, Azar M, Silver D (2018) Rainbow: Combining improvements in deep reinforcement learning. Thirty-Second AAAI Conference on Artificial Intelligence.

- Hong (2009) Hong LJ (2009) Estimating quantile sensitivities. Operations Research 57(1):118–130.

- Hong and Liu (2009) Hong LJ, Liu G (2009) Simulating sensitivities of conditional value at risk. Management Science 55(2):281–293.

- Hu et al. (2022) Hu J, Peng Y, Zhang G, Zhang Q (2022) A stochastic approximation method for simulation-based quantile optimization. INFORMS Journal on Computing 34(6):2889–2907.

- Jiang and Powell (2018) Jiang DR, Powell WB (2018) Risk-averse approximate dynamic programming with quantile-based risk measures. Mathematics of Operations Research 43(2):554–579.

- Jiang and Fu (2015) Jiang G, Fu MC (2015) On estimating quantile sensitivities via infinitesimal perturbation analysis. Operations Research 63(2):435–441.

- Jiang et al. (2022) Jiang J, Hu J, Peng Y (2022) Quantile-based policy optimization for reinforcement learning. 2022 Winter Simulation Conference (WSC), 2712–2723 (IEEE).

- Kloeden et al. (1992) Kloeden PE, Platen E, Kloeden PE, Platen E (1992) Stochastic differential equations (Springer).

- Kushner and Yin (2003) Kushner H, Yin GG (2003) Stochastic Approximation and Recursive Algorithms and Applications, volume 35 (Springer Science & Business Media).

- Levine et al. (2016) Levine S, Finn C, Darrell T, Abbeel P (2016) End-to-end training of deep visuomotor policies. The Journal of Machine Learning Research 17(1):1334–1373.

- Li et al. (2022) Li X, Zhong H, Brandeau ML (2022) Quantile markov decision processes. Operations Research 70(3):1428–1447.

- Liapounoff (2016) Liapounoff AM (2016) Probleme General de la Stabilite du Mouvement.(AM-17), Volume 17 (Princeton University Press).

- Lillicrap et al. (2016) Lillicrap TP, Hunt JJ, Pritzel A, Heess N, Erez T, Tassa Y, Silver D, Wierstra D (2016) Continuous control with deep reinforcement learning. 4th International Conference on Learning Representations, ICLR 2016, San Juan, Puerto Rico, May 2-4, 2016, Conference Track Proceedings.

- Liu and Hong (2009) Liu G, Hong LJ (2009) Kernel estimation of quantile sensitivities. Naval Research Logistics (NRL) 56(6):511–525.

- L’Ecuyer et al. (1992) L’Ecuyer P, Giroux N, Glynn PW (1992) Experimental results for gradient estimation and optimization of a markov chain in steady-state. Simulation and Optimization, 14–23 (Springer).

- Marchal and Arbel (2017) Marchal O, Arbel J (2017) On the sub-gaussianity of the beta and dirichlet distributions. Electronic Communications in Probability 22:1–14.

- Merton (1976) Merton RC (1976) Option pricing when underlying stock returns are discontinuous. Journal of financial economics 3(1-2):125–144.

- Mnih et al. (2015) Mnih V, Kavukcuoglu K, Silver D, Rusu AA, Veness J, Bellemare MG, Graves A, Riedmiller M, Fidjeland AK, Ostrovski G, et al. (2015) Human-level control through deep reinforcement learning. Nature 518(7540):529–533.

- Mokkadem and Pelletier (2006) Mokkadem A, Pelletier M (2006) Convergence rate and averaging of nonlinear two-time-scale stochastic approximation algorithms. The Annals of Applied Probability 16(3):1671–1702.

- Moon et al. (2022) Moon K, Bergemann P, Brown D, Chen A, Chu J, Eisen EA, Fischer GM, Loyalka P, Rho S, Cohen J (2022) Manufacturing productivity with worker turnover. Management Science .

- Petrik and Subramanian (2012) Petrik M, Subramanian D (2012) An approximate solution method for large risk-averse markov decision processes. Proceedings of the Twenty-Eighth Conference on Uncertainty in Artificial Intelligence, 805–814.

- Prashanth et al. (2022) Prashanth L, Fu MC, et al. (2022) Risk-sensitive reinforcement learning via policy gradient search. Foundations and Trends® in Machine Learning 15(5):537–693.

- Prashanth and Ghavamzadeh (2013) Prashanth L, Ghavamzadeh M (2013) Actor-critic algorithms for risk-sensitive mdps. Advances in Neural Information Processing Systems 26.

- Prashanth et al. (2016) Prashanth L, Jie C, Fu M, Marcus S, Szepesvári C (2016) Cumulative prospect theory meets reinforcement learning: Prediction and control. International Conference on Machine Learning, 1406–1415 (PMLR).

- Qu et al. (2022) Qu G, Wierman A, Li N (2022) Scalable reinforcement learning for multiagent networked systems. Operations Research .

- Rockafellar (2020) Rockafellar RT (2020) Risk and utility in the duality framework of convex analysis. Jonathan M. Borwein Commemorative Conference, 21–42 (Springer).

- Rugh (1996) Rugh WJ (1996) Linear System Theory (Prentice-Hall, Inc.).

- Ruszczyński (2010) Ruszczyński A (2010) Risk-averse dynamic programming for markov decision processes. Mathematical Programming 125(2):235–261.

- Schulman et al. (2015) Schulman J, Levine S, Abbeel P, Jordan M, Moritz P (2015) Trust region policy optimization. International Conference on Machine Learning, 1889–1897 (PMLR).

- Schulman et al. (2017) Schulman J, Wolski F, Dhariwal P, Radford A, Klimov O (2017) Proximal policy optimization algorithms. arXiv preprint arXiv:1707.06347 .

- Silver et al. (2016) Silver D, Huang A, Maddison CJ, Guez A, Sifre L, Van Den Driessche G, Schrittwieser J, Antonoglou I, Panneershelvam V, Lanctot M, et al. (2016) Mastering the game of go with deep neural networks and tree search. Nature 529(7587):484–489.

- Sinclair et al. (2022) Sinclair SR, Banerjee S, Yu CL (2022) Adaptive discretization in online reinforcement learning. Operations Research .

- Spall (1992) Spall JC (1992) Multivariate stochastic approximation using a simultaneous perturbation gradient approximation. IEEE Transactions on Automatic Control 37(3):332–341.

- Tamar et al. (2014) Tamar A, Glassner Y, Mannor S (2014) Policy gradients beyond expectations: Conditional value-at-risk. arXiv preprint arXiv:1404.3862 .

- Vershynin (2018) Vershynin R (2018) High-Dimensional Probability: An Introduction with Applications in Data Science, volume 47 (Cambridge university press).

- Wang et al. (2022a) Wang J, Gao R, Zha H (2022a) Reliable off-policy evaluation for reinforcement learning. Operations Research .

- Wang et al. (2022b) Wang W, Li B, Luo X, Wang X (2022b) Deep reinforcement learning for sequential targeting. Management Science .

- Williams (1992) Williams RJ (1992) Simple statistical gradient-following algorithms for connectionist reinforcement learning. Machine Learning 8(3):229–256.

- Zheng et al. (2018) Zheng G, Zhang F, Zheng Z, Xiang Y, Yuan NJ, Xie X, Li Z (2018) Drn: A deep reinforcement learning framework for news recommendation. Proceedings of the 2018 World Wide Web Conference, 167–176.

8 Supplements for Section 4

8.1 Proofs in “Strong Convergence of QPO”

Proof 8.1

Proof 8.2

Proof of Lemma 4.2. If , then and ; if , then must lie in , so . By convexity of on , is the unique equilibrium point. Take as the Lyapunov function, and the derivative is . Since is strictly convex, for any , which implies . Since , we have . Thus, is global asymptotically stable. \Halmos

Proof 8.3

Proof of Lemma 4.4. Recursion (5) can be rewritten as

| (25) |

where . Let . We then verify that is a -bounded martingale sequence. With Assumption 4.2(b) and boundedness of , we have

By noticing , we have

for all . Thus, . From the martingale convergence theorem (Durrett 2019), we have w.p.1. Then for any , there exists a constant such that for any , we have

| (26) |

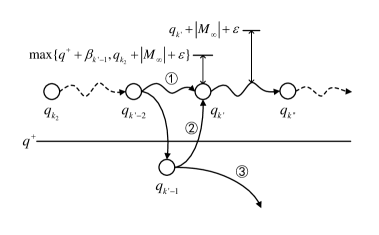

Denote and . Since Assumption 4.2 holds and is compact, we have and . From Assumption 4.2(b), there exists such that for any , . We then establish an upper bound of . If the tail sequence is bounded by , the boundedness of holds. Otherwise, let be the first time that rises above (i.e. and ), and denote a segment above of as . We discuss all three possible situations as shown in Figure.16. On path 1, stays above ; on path 2, drops below first and then rises above ; and on path 3, once drops below , it never rises above .

For the situations corresponding to path 1 and path 2, the definition of -quantile implies for . Then with equality (25) and inequality (26), we have for . In addition, if the situation corresponds to path 1, then by the previous result; and if it corresponds to path 2, there holds by recursion (5). By the definition of , we have a bound for both cases: . Thus, we have for all . Analogously, we have for . For the situation corresponding to path 3, the tail sequence is naturally bounded. In summary, the conclusion has been proved. \Halmos

Proof 8.4

Proof of Theorem 4.5. With and Assumption 4.2, we have and are Lipschitz continuous. It has been verified in Lemma 4.4 that . Denote , where with . Since is Lipschitz continuous on the compact set and is bounded as shown in Lemma 4.4, is bounded. By Assumption 4.2, we have

By noticing , Assumption 4.2(a), and a similar argument in Lemma 3, we can prove is a -bounded martingale sequence, which implies that is bounded w.p.1.

With Assumption 4.2 and the conclusions in Lemmas 4.1 and 4.4, all conditions in Theorem 4.3 are satisfied. Therefore, it is almost sure that recursions (5) and (6) converge to the unique global asymptotically stable equilibrium of ODE (9), which is the optimal solution of problem (3) by the conclusion of Lemma 4.2. \Halmos

8.2 Proofs in “Rate of Convergence”

Proof 8.5

Proof of Theorem 4.6. Since , we can omit the projection operator in the recursion (6). The convergence of to has already been proved in Theorem 4.5. With Assumption 4.3 and , the largest eigenvalues of and are less than 0. Since and are unbiased estimations of and , a.s. And we can find that

which must be a positive matrix. By noticing and are uniformly bounded, we immediately have the boundedness of all their finite moments. Therefore, all conditions in the central limit theorem of two-timescale stochastic approximation are satisfied, and the joint weak convergence rate of are as given in equation (10). \Halmos

Proof 8.6

Proof of Theorem 4.7. In Theorem 4.5, we have checked that is bounded. Denote . By noticing Assumption 4.2 and compactness of , is Lipschitz continuous on and denote its Lipschitz constant as . Then we have

where the second inequality comes from the definition of the projection function . Define and rewrite the recursion (5) as

By taking square on both sides, we have

With the definition of quantile and the intermediate value theorem, we can obtain

where lies in the interval between and . By taking expectation with respect to and applying the Cauchy Schwarz inequality, we further obtain

where . By assuming without lossing generality and repeatedly applying the inequality above, we have

| (27) |

We then bound the order of the second term on the right hand side of inequality (27). For any ,

where and is a sufficiently large constant, and the last inequality holds because is monotonically increasing when . Let

Then by noticing that is monotonically decreasing and , we have

| (28) |

where the equality comes from integration by parts. The order of the first term on the right hand side of inequality (28) is

| (29) |

For large enough, there exist constant such that and . Then for large enough ,

which goes to zero as . Combining this with inequality (28) and (29), we have

| (30) |

Therefore, the second term on the right hand side of inequality (27) is in the order of . Note that and

so the first term on the right hand side of inequality (27) decays exponentially so that it can be absorbed into the second term. Finally, we can conclude that , which completes the proof.\Halmos

Proof 8.7

Proof of Theorem 4.8. Rewrite the recursion (6) as

| (31) |

where is the vector with the shortest norm needed to project onto . Let . From the equality (31) and Assumption 4.2, we have

By noticing the strict convexity of , we have , which implies from Assumption 4.3 and the equality (4). Then, we can obtain

where lies between and ; the second equality comes from the Taylor expansion of around . Using the Rayleigh-Ritz inequality (Rugh 1996) and Assumption 4.3, we have

Note that . And by Theorem 4.7, we have . Taking expectation on both sides and applying the Cauchy Schwarz inequality, we have

| (32) |

Now we derive a bound for . Assume the interior of is not empty, so that is a constant such that , where represents a round neighborhood of with radius . Let . By the definition of the projection function , the occurrence of implies . Thus, we have

Using the Markov’s inequality, we further have

| (33) |

Next, we apply inequality (33) to inequality (32) and obtain:

where . Let . From the inequality above, we have

| (34) |

By an analogous analysis in Theorem 4.7, the second term on the right hand side of inequality (34) can be proved to be in the order of . Similarly, the first term decays exponentially so that it can be absorbed into the second term. Therefore, the conclusions of the theorem holds. \Halmos

9 Supplements for Section 5

Proof 9.2

Proof 9.3

Proof of Lemma 5.3. can be rewritten as , where

| (35) | ||||

| (36) |

Similar to the proof of Theorem 4.5, since and are bounded and , is an -bounded martingale sequence and bounded w.p.1. Considering that , we can conclude that is also an -bounded martingale sequence and almost surely bounded. Further, the sequence is bounded w.p.1. \Halmos

Proof 9.4

Proof of Theorem 5.4. With and Assumption 5.1, and are Lipschitz continuous. Let , for . It can be verified by Assumption 4.2(b) and the martingale convergence theorem that is a -bounded martingale sequence and bounded w.p.1. With Assumption 4.2 and the conclusions in Lemmas 5.1, 5.2 and 5.3, all conditions in Theorem 4.3 are satisfied. Therefore, it is almost sure that recursions (12) and (13) converge to the unique global asymptotically stable equilibrium of ODE (16), which is the optimal solution of problem (11) by the conclusion of Lemma 5.1. \Halmos

Proof 9.5

Proof 9.6

Proof 9.7

Proof of Theorem 5.7. Without loss of generality, we first consider centralized reward , where , such that . From the general Hoeffding’s inequality (Vershynin 2018), for any , and its subsequence , , we have

where is an absolute constant independent of other parameters, and . The norm is finite if and only if is sub-Gaussian, which implies is finite.

Let , where , . Thus, and are the -quantiles of and respectively. For , such that , denote the double truncated random variable of with interval as and the -quantile of as , where has a density given by

The boundedness of implies .

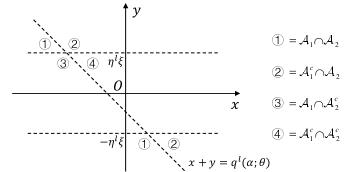

By -continuity of reward distribution function, there exists a unique , i.e., . Let and . The image space of and is divided as shown in Figure.17. Hence, by the definition of , we have

By noticing

where , we have Therefore, we can obtain . Using the Lagrange’s mean value theorem, we have

where . Since is continuous, then has a lower bound on . Let be the uniform lower bound of on a sufficiently large neighborhood of that contains , where and . And we can obtain

| (38) |

where . Since both terms in the third line of the inequality (38) are monotonic, the minimizer satisfies the first order condition . By plug-in, we further have

| (39) |

where , . For rewards without zero mean, similar to the proof of Theorem 5.6, there will be an additional term that can be absorbed by in the inequality (39). Finally, in the same manner as in the proof Theorem 5.5, we have

as . \Halmos

10 Supplements for Section 6

10.1 Experiment Settings in “Zero Mean”

Except for the last four parameters in Table 2, all parameters are shared by all algorithms. Note that the learning rate for SPSA is the same as the other algorithms, whereas the learning rate for SPSA+ is 50 and 100 times that of the other algorithms for the simple and hard examples, respectively.

| Hyperparameter | Simple example | Hard example |

|---|---|---|

| Network width | - | -- |

| Reward discount factor | ||

| Learning rate | ||

| Learning rate decay factor | ||

| Learning rate decay interval | episodes | episodes |

| Clip parameter (PPO & QPPO) | ||

| Update interval (PPO & QPPO) | steps | steps |

| Quantile learning rate (QPO & QPPO) | ||

| Truncated trajectory length (QPPO only) |

10.2 Experiment Settings in “Financial Investment”

In both examples, the initial prices of all assets are set to . The initial value allocation is randomly generated. And the transaction fee is of the trading value. The policy and baseline networks consist of three fully connected layer with a width of 64.

| Asset | Drift | Volatility | ||

| 1 | 2 | 3 | ||

| 1 | 0.01 | 0.01 | 0 | 0 |

| 2 | 0.08 | 0 | 0.08 | -0.08 |

| 3 | 0.16 | 0 | -0.08 | 0.08 |

| Asset | Drift | Volatility | ||||

| 1 | 2 | 3 | 4 | 5 | ||

| 1 | 0.01 | 0.01 | 0 | 0 | 0 | 0 |

| 2 | 0.02 | 0 | 0.04 | -0.055 | 0 | 0 |

| 3 | 0.03 | 0 | -0.055 | 0.09 | 0 | 0 |

| 4 | 0.04 | 0 | 0 | 0 | 0.16 | -0.19 |

| 5 | 0.05 | 0 | 0 | 0 | -0.19 | 0.25 |

| Hyperparameter | Value |

|---|---|

| Reward discount factor | |

| Learning rate | |

| Learning rate decay factor | |

| Learning rate decay interval | episodes |

| Clip parameter | |

| Update interval | steps |

| Quantile learning rate (QPPO only) | |

| Truncated trajectory length (QPPO only) |

10.3 Experiment Settings in “Inventory Management”

In the uniform case, the customers’ demand is uniformly sampled from . In the Merton case, the customers’ demand is generated by a discretized version of Merton jump diffusion model in Glasserman (2004), i.e.,

where and are independently generated from , is independently generated from , , , , , and . In the periodical case, the customers’ demand is generated by

where is uniformly sampled from , , and .

| Echelon | Lead time | Price | Holding cost | Penalty of lost sale | Initial inventory |

| 1 | 3 | 2 | 0.15 | 0.10 | 10 |

| 2 | / | 1.5 | / | / |

| Echelon | Lead time | Price | Holding cost | Penalty of lost sale | Initial inventory |

| 1 | 2 | 2 | 0.2 | 0.125 | 10 |

| 2 | 3 | 1.5 | 0.15 | 0.1 | 10 |

| 3 | 5 | 1 | 0.1 | 0.075 | 10 |

| 4 | / | 0.5 | / | / |

In the single-echelon example, the policy and baseline networks consist of a temporal convolutional layer with a kernel size of 3 and 64 output channels, and an output fully connected layer. In the multi-echelon example, the policy and baseline networks include a convolutional block composed of a temporal convolutional layer with a kernel size of 3 and 32 output channels, and another one with 64 output channels, and three parallel output fully connected layers.

| Hyperparameter | Sinle-echelon example | Multi-echelon example |

|---|---|---|

| Reward discount factor | ||

| Learning rate | ||

| Learning rate decay factor | ||

| Learning rate decay interval | episodes | episodes |

| Clip parameter | ||

| Update interval | steps | steps |

| Quantile learning rate (QPPO only) | ||

| Truncated trajectory length (QPPO only) |