On the impact of noise on quennching for a nonlocal diffusion model driven by a mixture of Brownian and fractional Brownian motions

Abstract.

In this paper, we study a stochastic parabolic problem involving a nonlocal diffusion operator associated with nonlocal Robin-type boundary conditions. The stochastic dynamics under consideration are driven by a mixture of a classical Brownian and a fractional Brownian motions with Hurst index We first establish local in existence result of the considered model and then explore conditions under which the resulting SPDE exhibits finite-time quenching. Using the probability distribution of perpetual integral functional of Brownian motion as well as tail estimates of fractional Brownian motion we provide analytic estimates for certain statistics of interest, such as quenching times and the corresponding quenching probabilities. The existence of global in time solutions is also investigated and as a consequence a lower estimate of the quenching time is also derived. Our analytical results demonstrate the non-trivial impact of the considered noise on the dynamics of the system. Next, a connection of a special case of the examined model is drawn in the context of MEMS technology. Finally, a numerical investigation of the considered model for a fractional Laplacian diffusion and Dirichlet-type boundary conditions is delivered.

Key words: Nonlocal diffusion, Brownian motion, fractional Brownian motion, exponential functionals, quenching, global existence, SPDEs, MEMS.

Mathematics Subject Classification: Primary: 60G22, 60G65, 60H15, 35R60; Secondary: 65M06, 35A01, 60J60.

1. Introduction

In this paper we consider the following nonlocal stochastic semilinear parabolic problem

| (1.1) | |||

| (1.2) | |||

| (1.3) |

where is an integral (nonlocal) operator of the fractional Laplacian type and is the corresponding nonlocal Neumann-type operator whose forms are specified in Section 2. Also, is a stochastic process which is a mixture of the Wiener process and the fractional Brownian motion with a Hurst index of and is a nonlinear function such that as whereas for large enough. A possible function with this behavior can be for . The choice of this asymptotic behaviour for in the limit as is so that the model, in its deterministic form induces quenching behaviour whereas for sufficiently large non vanishing solutions can be maintained.

System (1.1) – (1.3) is a rather general model that may be used to study the effects of spatio-temporal nonlocality and noise on quenching in nonlinear problems. The motivation for the introduction of the integral (nonlocal) diffusion operator and the noise terms is so that we may study the combined effects of nonlocal spatio-temporal processes on the quenching behaviour of nonlinear stochastic PDEs; the considered nonlocal diffusion term modelling spatial nonlocal effects and the noise term as a mixture of the Wiener process and the fractional Brownian motion, modelling the combined effects of stochasticity and temporal nonlocal effects. Furthermore, the choice of the noise term is so that in the limit where quenching happens , the noise term will not dominate over the dynamics of the model and sweep them away under the effects of noise. On the other hand, before quenching is about to happen, i.e., when is not close to , the effects of the noise term may be such as to drive the system away from the quenching regime (note that has a symmetric distribution around ).

In Section 7 we provide a detailed example, where such a model can arise from a concrete system of the MEMS type, and consider the general results provided in the context of the failure of MEMS systems. The determinisitc version of (1.1) – (1.3) for the case of local diffusion and for reaction terms of the form is related with applications in MEMS systems and it has been extensively studied, see [24, 27, 40, 44] and the refences therein. Nonlocal versions of those deterministic MEMS models also investigated in [17, 32, 33, 34, 43, 52, 53, 54, 61]. Whilst, hyperbolic type deterministic MEMS models with both local and nonlocal nonlinearities have been considered in [28, 31, 35, 41, 41]. The aforementioned works mainly focused on the impact of the parameter and the initial data on the mathematical phenomenon of quenching, that is when so the nonlinear term becomes singular. Such a singular behaviour is closely related to the mechanical phenomenon of touching down, cf. [44, 60, 61], which potentially might lead to the collapse of MEMS systems. The dynamics of stochastic systems analogous to (1.1) – (1.3), with either local or nonlocal diffusion, but with blow-up nonlinear terms has been explored in [2, 12, 13, 14, 15, 16, 45]. There the impact of the noise, in the case of a Wiener process, a fractional Brownian motion and a mixture of them, on the phenomenon of blow-up is investigated. To this end estimates of the blow-up probability and the blow-up time are provided. The dynamics of other analogous nonlocal stochastic PDE models has been investigated in [4, 47, 38, 66, 67]. However, a stochastic model with a MEMS nonlinearity and local diffusion was only first considered in [39]. The author in [39] considered a multiplicative noise of the form for a Lipschitz function, and proved the finite-time quenching of the solution moments for large parameter values and big enough initial data. Later on in [18, 19] the authors explored the dynamics of stochastic MEMS models with multiplicative noise of the form and for Hurst index The relatively simple form of the multiplicative noise term allowed for the path-wise analysis of quenching and hence estimates of quenching probability and quenching time were obtained. This is to be contrasted with weaker notions of quenching, which was discussed in [39].

The aim of the present paper is twofold; first we examine the conditions under which quenching occurs for the stochastic problem (1.1) – (1.3). Secondly, we obtain analytic estimates of the quenching probability as well as of the quenching time, which is a stopping time of (1.1) – (1.3). To the best of our knowledge, this is the first time that those two tasks are considered in the context of nonlocal diffusion SPDEs. Such considerations have their own theoretical importance in the context of singular SPDEs. Also, based on the potential connection of model (1.1) – (1.3) to apllications of MEMS devices, see section 7, and provided the significance of those devices in biomedical applications, such as drug delivery and diagnostics [8, 58, 64], our analysis might offer valuable insights into their operational characteristics in the presence of a mixture noise.

The layout of the paper is as follows: in the next section we provide all the theoretical framework for the investigation of (1.1) – (1.3). In Section 3, we introduce a relevant to (1.1) – (1.3) random PDE (RPDE) problem and define the different kind of solutions for those related problems, which are proven to be equivalent. Next we establish the local in time existence and uniqueness of those two problems. Section 4 deals with the derivation of upper estimates for the quenching probability and the quenching time. To this end we make use of some known tail estimates for the fractional Brownian. In section 5 we derive lower estimates for the quenching probability by means of the probability distribution of perpetual integral functionals of Brownian motion as well as using tail estimates of the fractional Brownian motion. Next, in section 6 we explore conditions under which model (1.1) – (1.3) has global in time solutions. This study leads also to the derivation of lower bounds for the quenching time. We investigate the connection of our nonlocal model with some applications in MEMS industry in section 7. A complementary numerical analysis of (1.1) – (1.3) for the fractional Laplacian operator and for Dircihlet boundary conditions is conducted in section 8, since our analytical approach is not easily applicable in that case. Then a discussion section, where our main results are highlighted, and an Appendix section, where the proof of an important auxiliary result is given, follow.

2. Preliminaries

2.1. The nonlocal operators and

By we denote the nonlocal operator

| (2.1) |

where is measurable kernel satisfying

for some that is the density of a symmetric Lévy measure. Moreover, is the nonlocal analogue of the Neumann operator, defined by

| (2.2) |

In the special case where the operator is translation invariant and the generator of a symmetric Lévy process. This is the case we will focus on for this work. For the choice , for the corresponding operator reduces to the fractional Laplacian, . The usual choice of the constant is with being the Euler function. For this choice the operator converges (in the appropriate sense) to the standard Laplacian operator in the limit as .

2.1.1. Variational formulation and relevant function spaces

Consider the bilinear forms

and

As shown in [26], the bilinear form is related to the nonlocal Robin problem

| (2.3) | |||

| (2.4) |

The connection between the two comes in terms of the variational formulation of (2.3)-(2.4)

| (2.5) |

where

and

This space can be turned into a Hilbert space when equipped with the norm

Concerning the Robin coefficient we will assume that and that is essentially bounded and non-trivial (as in [26]). The above weak formulation follows from the nonlocal Gauss-Green formula

and the density of in (for such that is compact and Lipschitz; see in [26, Theorem 2.11]).

2.1.2. The nonlocal Robin boundary value problem

In [26, Theorem 4.21] it is shown that the Robin eigenfunctions of , are a countable set satisfying

| (2.6) | |||

| (2.7) |

with such that forms an orthonormal basis of , and

We now state the following result which will be used in this paper (for the proof see Appendix in section 10)

2.1.3. The semigroup generated by

The operator with the corresponding nonlocal boundary conditions can be shown to generate a strongly continuous semigroup on an appropriate space. There are two possible approaches to the choice of the required space.

In the first approach (see e.g. [9] for the case of the fractional Laplacian) we may modify the boundary condition (1.2) to

| (2.9) |

and then we define an extension of a function to a function in such a way so that the external boundary condition is automatically satisfied. Note that the modified boundary condition carries no information as to what happens for but this is of little importance if we are only interested in considering as an object since . For the case of the Robin boundary condition studied here the corresponding extension can be defined as

| (2.10) |

where and let be the corresponding extension operator defined by . It can easily be seen (see e.g. in [9, Lemma 3.15] for the case of the fractional Laplacian) the satisfies the exterior boundary condition on , for any . Moreover, is well defined for (note again that ). We can then define the bilinear form

which is well defined on

To this bilinear form we can associate an operator defined as in terms of the weak formulation of the problem (2.3) with the (modified) Robin boundary condition (2.9) as follows: Consider any , such that its Robin extension as defined by (2.10) satisfies the weak formulation of (2.3) with boundary condition (2.9) for some function : Then we define the operator in terms of

The above definition indicates that the appropriate domain for this operator will be

It can be shown (see in [9, Theorem 3.18] for the fractional Laplacian) that the form is closed, symmetric and densely defined on , hence the corresponding operator is a self adjoint operator generating a strongly continuous semigroup on which moreover is positivity preserving and can be extended to a contraction semigroup on for all , and is strongly continuous for .

In the second approach (see [26]) we do not consider directly the idea of a Robin extension but rather consider the problem on the whole of and making sure that the exterior condition holds in terms of the weak formulation (2.5). It can then be shown (see in [26, Theorem 2.25] ) that the bilinear form is a regular Dirichlet form on where is any of the measures

where is bounded and open and is an arbitrary fixed number. The need for the weight is so that the asymptotic behaviour of the function is controlled, since now we consider the function as a function on the whole of and not just on as above. Here again, by the properties of Dirichlet forms the operator generates an operator semigroup on , which is strongly continuous and can be extended to a contraction semigroup on for all (by the Beurling-Deny conditions).

For the needs of this work we may consider either of the above semigroups which will be invariably denoted by acting on (which may be either or ).

Moreover, we note that here we are interested in the family of operators . This family of operators generates a evolution family as follows:

Define the functions

| (2.11) | |||

| (2.12) |

We may then define the evolution family by its action

on any . Using this evolution family we may express the solution of the nonhomogeneous system

in terms of

where we use the simplified notation .

2.2. The noise term

The noise term is of mixed form and it is defined as follows:

| (2.13) |

for some positive functions where and stand for the one-dimensional, real-valued Brownian and fractional Brownian motions, defined on a stochastic basis with filtration and Hurst index .

2.2.1. Fractional Brownian motion and its properties

Recall that the fractional Brownian motion is a Gaussian process with the properties

-

(i)

a.s. ,

-

(ii)

-

(iii)

,

The above properties uniquely characterize the fractional Brownian motion in terms of its characteristic function

where the matrix and denotes the standard inner product in . For the choice we recover the standard Brownian motion. The fractional Brownian motion is a self similar process (in the sense that for any the processes and have the same distribution) and has stationary increments, which are uncorrelated for , positively correlated for and negatively correlated for . In this work we will focus on positively corellated regime in which the process displays long-range dependence, which corresponds to an aggregation behaviour useful for describing clustering phenomena in various applications ranging from physical phenomena to economics (see e.g. [57, 29]). Note that for fractional Brownian motions with it holds that . On the other hand, for the standard Brownian motion .

2.2.2. Stochastic integration with respect to fractional Brownian motion for

The fractional Brownian motion is not a semimartingale for . For the process though, it is interesting to note that when it is equivalent in law to Brownian motion.

Eventhough the fractional Brownian motion is not a semimartingale a theory for stochastic integration can be developed in parallel to the corresponding theory for the Wiener process. The development of stochastic integration differs between the cases where and ; here we will focus in the latter case. We assume throughout the rest of the paper that . Moreover, there are different notions available for stochastic integration over the fBM, depending on the type of integrand in consideration. Various notions of stochastic integration over fBM include the pathwise integration, or the Maliavin calculus approach involving the Skorokhod integral. Different notions of stochastic integration result to integrals with different properties so we need to specify the particular concept of stochastic integration used to define the corresponding SPDE since the begining. In this paper we will use the pathwise approach.

The pathwise stochastic integral can be defined for a process with -Hölder continuous trajectories, for in the sense of Young integration as the limit of the Riemann-Stieltjes sums. Let us consider the sequence of partitions such that for . The pathwise stochastic integral is defined as

| (2.14) |

The pathwise approach follows a simple transformation rule for pointwise transformations of stochastic integrals in terms of smooth functions . In particular (see [51, Lemma 2.7.3 page 182]) if then

| (2.15) |

Throughout this work, we will use the Banach space , which consists of all measurable functions for which the norm is defined, i.e.,

where is the usual norm in , cf. [50, 51, 68]. The requirement that for some ensures that the stochastic integral with respect to in (2.14) exists as a generalized Stieltjes integral in the sense of [68]; see also [56, Proposition 1].

As far as the mixed process is concerned, the stochastic integral with respect to will be considered in the above pathwise sense, whereas the stochastic integral with respect to will be considered in the Itô sense, i.e. in the Riemann-Stieltjes sum (2.14) we must set and moreover, the convergence of the Riemann sum in (2.14) must be considered in the sense. This leads to a modification to the Itô formula (2.15) to

| (2.16) |

Note that the last term arises because of the interpretation of the limit for the Itô integral for in the sense.

The Itô lemma can be generalized for composition of a smooth function with more complicated processes of the form , for or linear combinations of such processes. The following Itô’s lemma will be used (see [51, Theorem 2.7.3 page 184] ): Let be a function and let , be Itô processes driven by the mixed process . Then,

| (2.17) | |||||

In the above formula the rules , and will be used for the calculation of the quadratic covariation processes . For example, if , then since all other covariation processes vanish except for . This is because we consider the case for the fractional Brownian motion.

2.2.3. The Malliavin derivative

We close this section by defining the Malliavin derivative that will be used in section 4.

To define this we will consider as the space of continuous functions vanishing at , equipped with the supremum norm, and set the unique probability measure on such that the canonical process is the fBM with Hurst exponent .

We define the square integrable Volterra kernel for by

| (2.18) |

where

and stands for the usual beta function, c.f. section 5.1.3 in [55] for more details. Note that in this case and are dependent since can be represented as

We then express the auto-covariance function of the fBM in terms of

Let be the space of step functions on and let be the closure of this space with respect to the scalar product . We define the mapping on and its extension to an isometry between and the Gaussian space spanned by , denoted by .

We can now define the Malliavin derivative with respect to fBM. Consider any smooth cylindrical random function of the form where , and . The Malliavin derivative is the random variable in defined by

which can be interpreted as the generalization of the directional derivative along the possible paths of the fBM. The derivative operator is a closable operator from into for any . It can be used to define generalizations of Sobolev spaces. The most commonly used of this spaces is which is the closure of the space of cylidrical smooth random variables with respect to the norm

In the present setting the Malliavin derivative will be intepreted as a stochastic process (see [55] Section 1.2.1 and Chapter 5).

3. Local solutions

We start by providing a precise definition of the notion of quenching time that was alluded to in the introduction.

Definition 3.1.

Definition 3.2 (Weak solutions).

The mild solutions for the above equations can be defined in terms of the evolution family generated by the family of operators

Definition 3.3 (Mild solutions).

Note that in Definition 3.3 (ii) we may rewrite the mild solution in terms of the evolution family generated by the family of operators where represents the unit operator. This will lead to the equivalent mild form

| (3.5) |

The following proposition allows us to reduce the SPDE problem (1.1)–(1.3) to the RPDE problem (3.1)–(3.3).

Proposition 3.4.

Proof.

To show that we simply need to apply Itô’s formula (2.17) to the process , for being a weak solution of (1.1)–(1.3). Using Definition 3.3 we note that we may express

for , with

In order to clarify the exposition we use the following scheme in the notation: We denote the terms depending on the Wiener process by , the terms depending on the fractional Brownian motion by and by the process that can be expressed as a Riemann integral over . Clearly, (a) by independence there is no quadratic covariation between the processes and , (b) by the fact that there is no quadratic covariation between the processes and - even for , and (c) by the standard rules of stochastic calculus there is no quadratic covariation between the processes and . The only contributions in quadratic coveriation will be from the processes (including ). Hence, only the second derivatives and will contribute to the Itô formula.

A straightforward application of (2.17) taking into account the above comments yields that

| (3.6) |

Moreover, since , we see that

Note that since is a weak solution of the SPDE,

| (3.7) |

it holds that

hence, in the contribution of the first order terms in the Itô formula, the stochastic integral over is eliminated to yield

Noting that and , we see that (using again (3.7))

Substituting the above in (3) and using once more (3.7) to express the first and second term as and respectively we obtain that

Expressing the above in terms of yields

which proves that is a weak solution of the RPDE problem (3.1)–(3.3).

To prove the converse, we follow a similar route, starting from a satisfying Definition 3.3 and considering the process using Itô’s formula for the process where

and . The details are left to the reader. ∎

Following the same reasoning as in [16, Theorem 2.2] we can derive the equivalence between weak and mild solutions for the random problem (3.1)–(3.3). Therefore the proof is omitted.

Proposition 3.5 (Equivalence of weak and mild solutions).

Proposition 3.6 (Existence of local weak solutions).

Proof.

By Proposition 3.4 it suffices to show the existence of a weak local in time solution for the related RPDE problem (3.1)–(3.3).

The proof is broken up in three steps.

1. We introduce the mild form for (3.1)–(3.3)

| (3.8) |

recalling that is the evolution family generated by the operators while are defined by (2.11) and (2.12) respectively.

By Proposition 3.5 we have that the weak form and the mild form are equivalent. Hence, showing existence for the mild form guerantees existence for the weak form as well.

2. To prove existence we need to handle the singular behaviour of at . To this end we consider the approximating sequence defined by . Assuming the is decreasing in a neighbourhood of we see that are bounded below by and moreover for each the functions are locally Lipschitz. To ease notation we will denote by the bound of and the Lipschitz constant for in .

We note that for any , as long as . Moreover, if then (equiv. ).

Using the approximation we define the random fields as the mild solutions for the approximate problems

| (3.9) |

and define the stopping times , where

We will show that problem (3.9) admits a unique solution in for small enough, for every , so that the stopping times are well defined. This is due to the local Lipschitz property of and is shown in step 3 below.

Note that if . Indeed, if then hence by uniqueness of the solution of (3.9) we have that as long as both are above , that is as long as . This means that up to time neither nor are below , hence will go below at a time . Therefore the sequence defined above is an increasing and bounded (by ) sequence of stopping times.

Since up to , it holds that then in where is the solution of (3.5). We will then construct the solution of (3.5) via

The solution can be continued up to , and is the local solution of (3.9).

3. We now prove the existence of a local in time mild solution for (3.9) in for small enough. We will use a fixed point scheme for the operator defined by

| (3.10) |

on the Banach space where the norm is defined by , where is a suitable time (to be determined).

We will show that the operator leaves invariant and is a contraction on the subset for a suitable hence guaranteeing the existence of a unique non negative solution.

We first consider the invariance property for . Consider any and take . We have that

where and Note that since for then by a continuity argument we have

We will choose and so that

and thus is invariant under the operator

We now consider the contraction property for We start by noting that

| (3.11) | |||||

where we first used the fact that and then the contractivity of the evolution family . To proceed further we must make use of the local Lipschitz properties of the nonlinearity . Let be locally Lipschitz, satisfying the property

for some . Then as long as we may estimate

Using the above estimate we may further estimate (3.11) by

Hence we conclude that

Choosing so that

| (3.12) |

it can be seen that is a contraction. ∎

4. Upper bounds for quenching time and quenching probability

The current section is focused on the derivation of upper bounds for the quenching time as well as the quenching probability for problem (1.1)–(1.3). Along this section we consider the following growth condition for the nonlinearity

| (4.1) |

for some positive constant

4.1. An upper bound for the quenching time

Define:

| (4.2) |

Consider now the following eigenvalue problem

| (4.3) | |||

| (4.4) |

then it is known, see Appendix, that for the first eigenpair we have whilst the corresponding eigenfunction could be taken also positive.

Theorem 1.

Proof.

By choosing as a test function into the weak formulation ((ii)) the principal eigenfunction to (4.3)-(4.4) normalized as

| (4.6) |

then

| (4.7) | |||||

4.2. A tail estimate leading to an upper bound of quenching time

In the current subesction, our main purpose is to provide a tail estimate for the upper bound defined by (4.5), making use of a tail probability estimate for exponential estimates of fBM given in [20, Theorem 3.1]. To this end we consider that the stochastic process is defined as follows

| (4.8) |

where the Volterra kernel is given by (2.18).

Henceforth, for simplicity, we drop the superscript from the notation of the kernel

Theorem 4.1.

Proof.

Consider the stochastic process

then thanks to (4.8) we have the representation

| (4.10) |

Now from [20, Theorem 3.1] it folows that for any and it holds

| (4.11) |

where and is such that

| (4.12) |

and stands for the Malliavin derivative of

So in order to obtain the desired tail estimate we are working towards finding an upper bound of such that (4.12) holds.

We first note, using the representation (4.10), that for

and thus

| (4.13) |

Next we are working towards the derivation of a bound of the second integral of the right-hand side of (4.13). Indeed, via Fubini’s theorem and following the same calculations like in [16, page 15] we have

| (4.14) |

where

Since

then using [55, relation (5.7) ] for we deduce

Next by virtue of (4.14) and following the same calculations as in [16, page 16] yields

| (4.15) | |||||

Then (4.13) infers

| (4.16) |

Since by (4.5)

| (4.17) | |||||

then the desired result follows by virtue of (4.11) and (4.16) for ∎

Theorem 4.2.

-

(1)

Assume that

(4.18) where is the Volterra kernel given by (2.18) and is a Brownian motion defined in the same probability space, and adapted to the same filtration as the Brownian motion Then

(4.19) -

(2)

Assume that and are independent then

(4.20)

Proof.

-

(1)

Making use first of Hölder’s and then Chebichev’s inequalities then (4.5) yields

(4.21) Note that in order to pass from the second to the third inequality above we have used the inequality for the choice

Indeed, since for any it holds that

by the monotonicity and the subadditivity of the probability measure we pass from the second to the third inequality. Moroever, note that in the last inequality has been used that

Furthemore thanks to (4.18) and by virtue of [46, Theorem 4.12] we have

Using now (4.15) we deduce

(4.22) Therefore (4.21) in conjunction with (4.22) implies estimate (4.19).

-

(2)

In this case using again Chebichev’s inequality reads

(4.23) where the third equality is an immediate consequence of the independence of and whilst the last inequality follows from the same calculations employed in the previous case.

∎

5. Lower bounds for quenching probability

Along this section we also assume that the nonlinearity satisfies the growth condition (4.1).

5.1. General case

Theorem 5.1.

Proof.

Note that (4.17), and under the assumption (4.1), yields that

for

Next for the estimate of the probability we will make use of [21, Theorem 3.1].

Indeed, using representation (4.10) we infer

where the last inequality is an immediate consequence of [46, Theorem 4.12].

Consequeently, using (4.15) as well as (5.1) we derive

| (5.6) | |||||

taking also into account condition (5.2). In (5.6) and henceforth by the notation we mean that function is asymptotically bounded above by as

Note that (4.16) implies that Furthermore, (4.16) in conjunction to (5.1) and (5.2) infers

| (5.7) | |||||

for some new constant and fixed function Choosing now then

and thus via (5.6) we have

Now the conclusion is derived by an immediate application of [21, Theorem 3.1] and the fact that is an upper bound of the quenching (stopping) time for the solution of problem (1.1) – (1.3). ∎

By the proof of Theorem 5.1 we easily derive the following:

5.2. An interesting special case

In the current subscetion we are working towards the derivation of more explicit lower bound for the quenching probability To this end we focus on the case and suppose that and are independent with for any and is a positive constant. Under those conditions for It is known, see [7, Theorem 1.7], that in that specific case the stochastic process is equivalent in law to a Brownian motion and so is equivalent In addition, is a martingale and therefore a time-changed Brownian motion, in particular c.f. [2, 18].

Theorem 5.4.

Consider and assume that and are independent with for any where is a positive constant. In addition to growth condition (4.1) suppose also that functions and are positive continuous on and that there exists positive constant such that

| (5.8) |

and that

| (5.9) |

- (1)

- (2)

Proof.

Under the change of variable we derive

Using now (5.9) and the fact that is a inreasing function, so that is we get Combining that with (5.8) then (5.10) infers

| (5.11) | |||||

Next, we introduce the change of variables and thus via the scaling property of Brownian motion (5.11) entails

| (5.12) | |||||

where and

Next we distinguish the following cases:

- (1)

-

(2)

Assume that and so Then, by virtue of the law of the iterated logarithm for the Brownian motion cf. [3, Theorem 2.3] and [37, Theorem 9.23], that is

(5.15) and (5.16) we deduce that for any sequence

with and thus

The latter, due to (5.11), infers

(5.17) and hence

(5.18) Now since then as well and thus the solution to problem (1.1) – (1.3) quenches in finite time almost surely.

∎

Remark 5.5.

Note that conditions (5.8) is satisfied, whilst (5.9) is not needed anymore, for constant functions and and thus Theorem 5.4 is valid in that special case. Indeed, for and following the same steps as in the proof of the first part of Theorem 5.4 we obtain that the solution of problem (1.1) – (1.3) quenches in finite time with positive probability

6. Global existence–Lower bound of quenching time

In this section we consider the following growth condition for the nonlinearity

| (6.1) |

Then thanks to (3.5) any mild solution of problem (3.1)–(3.3) satisfies the integral inequality

| (6.2) |

Notably, the weak and mild solutions are equivalent for problem (3.1)–(3.3), see Proposition 3.5, therefore in the current subection we will use the concept of a mild solution to derive lower bounds for the quenching (stopping) time for and To this end, in the sequel we follow the same approach as in [19] (see also [13]) to derive such a lower bound.

Consider the stochastic process

| (6.3) |

where is defined by (4.2) and

| (6.4) |

due to the initial condition. Its stopping time is defined by

| (6.5) |

Our first result towards the derivation of this lower bound is the following:

Theorem 6.1.

Proof.

Note that By differentiating (6.3), we obtain

and thus

Set

| (6.7) |

for where is any nonnegative function such that and

| (6.8) | |||

In the following we denote for simplicity and without any confussion.

An immediate consequence of (6.7) is The latter in conjunction with (6.8) gives

| (6.9) | |||||

Next, using once more (6.8) and applying the semigroup property [59, Definition 2.3, page 106] into the last inequality of (6.9) reads

| (6.10) | |||||

Accordingly,

| (6.11) |

Next, we consider the iteration scheme

Due to (6.11), If we assume that for some and for every and then since

The latter implies by induction that is a decreasing sequence of nonnegative functions. Therefore, the limit

exists for every and all

Consequently, using the version of the monotone convergence theorem for decreasing functions reads

and hence coincides with the unique mild solution of the following random problem

which is given as the following integral representation

Furthermore, by virtue of (6.2), (6.3), (6.10) then the comparison principle, cf. [5], yields

| (6.12) |

Now, (6.6) is an immediate consequence of (6.12) using also that ∎

Remark 6.2.

Next using Theorem 6.1,we provide a condition under which problem (1.1)- (1.3) has a global in time solution alsmost surely.

Corollary 6.3.

Proof.

In the sequel we derive a sufficient condition for condition (6.13) to be satisfied. Such a condition is provided in terms of the principal eigenpair of the eigenvalue problem (4.3)–(4.4) normalized such that (4.6) holds.

We consider initial data such that

| (6.15) |

for some constant to be specified in the sequel. Remarkably, by virtue of Jentsch’s Theorem (see [62, Theorem V.6.6]), we obtain for any .

Set , then (6.15) yields

| (6.16) | |||||

where the lower bound in (6.16) is independent of the spatial variable

Since the function is uniformly bounded in then (6.4) thanks to (6.16) reads

and thus condition (6.13) is satisfied provided that

or equivalently

| (6.17) |

for

Therefore we deduce the following global existence result.

Theorem 6.4.

Proof.

Remark 6.5.

Remark 6.6.

Notably the random variables and , defined by (4.5) and (6.5) respectively, provide lower and upper bounds for the quenching time of the solution to (1.1)- (1.3). Indeed, consider now intial data for some constant Then, and are expressed in terms of the same exponential function of the stochastic process Indeed, under that choice for the initial data, we have:

and

Then, due to (6.5) and (4.5), we deduce that

and

which implies that provided that

The latter relation is readily seen to be always true since and

7. Applications: MEMS models

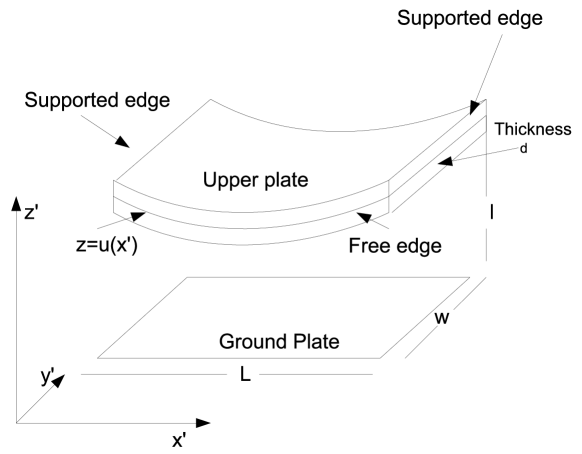

Deterministic versions of model (1.1) – (1.3) with local diffusion have been introduced the last decade to describe the operation of certain types of micro-electromechanical systems (MEMS), cf [24, 40, 44, 60]. MEMS devices are precision devices which integrate mechanical processes with electrical circuits. Their size ranges from millimetres down to microns, and involve precision mechanical components which can be constructed using semiconductor manufacturing technologies [44, 60, 65]. MEMS devices are commonly employed in biomedical engineering applications, including the design of micro-scale drug delivery devices and the development of micropumps for microfluidic diagnostic tools, among others [8, 58, 64].

The key part of such an electrostatically actuated MEMS device usually consists of an elastic plate (or membrane) suspended above a rigid ground one. Regularly the elastic plate is held fixed at two ends while the other two edges remain free to move (see Figure 1).

A potential difference is applied between the elastic membrane and the rigid ground plate, leading to a deflection of the membrane towards the plate. Considering the width of the intermediate gap, i.e the gap between the membrane and the bottom plate, to be small compared to the device length , then the deformation of the elastic membrane after proper scaling, is given by the dimensionless equation

| (7.1) |

see [44, 60, 61], where the laplacian term describes to the spread of the deformation, whilst the term arises as a consequence of the electrostatic features of the MEMS device. Here, the term describes the varying dielectric properties of the membrane and for some elastic materials can be taken to be constant; for simplicity, henceforth we assume that Furthermore, the parameter appearing in (7.1) equals to and is the tuning parameter of the device. Note that stands for the tension of the elastic membrane, is the characteristic width of the gap between the membrane and the fixed ground plate (electrode), whilst is the permittivity of free space. For extending further the stable operation of the MEMS device then a capacitance connected in series with MEMS is introduced to the underlying electrical circuit. Then we are led, via the application of Kirchoff’s laws, into versions of model (7.1) involving nonlocal reaction terms, cf. [44, 60, 61].

MEMS engineers are commonly interested in identifying the conditions under which the elastic membrane can touch the rigid plate, a mechanical phenomenon usually referred to as touching down and one that can potentially lead to the destruction of the device. Touching down can be described via model (7.1), and its nonlocal variations. It actually corresponds to the case when the deformation reaches the value such a situation is known as quenching (or extinction) in the mathematical literature.

Experimental observations (see [65]) show a significant uncertainty regarding the values of and In that case, incorporating this uncertainty into the tunning parameter we can obtain some a stochastic model with a multiplicative white noise involving [18, 39]. In case of a MEMS device with a long-range dependence uncertainty for and it seems reasonable to consider a stochastic model with multiplicative fractional noise with Hurst index cf. [19].

A more complex configuration of the MEMS device described in Figure1 incorporates the case where two edges of the membrane are attached to a pair of torsional and translational springs, modeling a flexible, non-ideal support, see [17, 65]. In that case homogeneous Robin boundary conditions should be assigned to equation (7.1), cf. [17, 19].

Now consider the case we would also like to model nonlocal effects of the elastic membrane, maybe due to material discontinuities. In that case the spread of the membrane’s deflection should be modeled, into equation (7.1), by a nonlocal diffusion operator of the form (2.1), with a possibly time-dependent diffusion coefficient, incorporating the natural treatment of balance laws on and off material discontinuities, cf. [11, 22]. To integrate any possible material anomalies on the boundary a nonlocal Robin boundary condition of the form (1.2) should be assigned to the underlying nonlocal equation. A rather simple choice is to take whilst the nonlocal operator given by (2.2), should have kernel of the form Finally, in order to include elastic membranes could generate long-range and short-range voltage and tension fluctuations (occuring as clustering) we could embody a noise of the form (2.13).

For such a model with extended Robin conditions the analysis and the analytical results and estimates of sections 3-6 give an insight about the quenching behaviour of the model. For the case of the extended Dirichlet conditions, where no similar analytical results are available, we present a preliminary numerical treatment of the problen in the following section 8.

8. Numerical solution

In the current section we deliver a numerical study of the following problem

| (8.1) | |||

| (8.2) | |||

| (8.3) |

for the one-dimensional case The considered time-dependent noise is a combination of standard and fractional Brownian motions. This case corresponds to a simpler version of the more general problem studied in the previous sections and it is closely related to the MEMS application described in the preceding section. In relation to problem (1.1)-(1.3), here we consider, , , , and extended Dirichlet boundary conditions.

The considered noise term is of a multiplicative form, that is for . In particular we take the noise being of the form for some positive constants that is a mixture of the standard and fractional Brownian motion.

Here we focus in the case of homogeneous Dirichlet conditions in the complement of the interval Note that homogeneous Dirichlet boundary condition in corresponds in having for and this case is not actually covered by the analysis in the previous sections.

The consideration of extended Dirichlet boundary conditions is important, since those conditions are quite relevant to the MEMS application (see for example [24, 44, 60]) considered in the previous section. On the other hand, since as for the case of the standard Laplacian operator the analytical methods for estimating the quenching probability are more delicate (see [18, 19]) an initial numerical study of the Dirichlet problem is a valuable contribution. So we attempt a numerical study of the conisdered stochastic nonlocal model in that case. We intend to derive an initial estimation of the dynamics of our nonlocal stochastic problem under the infuence of extended Dirichlet boundary conditions.

8.1. Finite Differences approximation

In order to approximate numerically the problem (8.1)-(8.3) we proceed with a finite difference semi–implicit Euler in time scheme, cf. [23, 49].

We set a discretization in , , with , for the number of time steps and we also introduce the grid points in , , for and .

Then, initially we apply a finite differences approximation for the fractional Laplacian term in (8.1). We follow the finite differences approximation approach given in [23].

Following this approach we obtain , for an matrix having the form:

| (8.9) |

where here we set , for and for . Also the parameter and in our simulations we take . For more details about the derivation of the scheme and the choices of the various parameters we refer to [23].

We then apply a semi-implicit Euler method in time. We denote by the finite difference approximation of , i.e. , and by since due to Dirichlet boundary conditions .

By a standard discretization in time we obtain

or

where we denote by the vector . Also where are i.i.d. random variables for i.i.d. standard Brownian motions . Similarly we sample the fractional Brownian motion by considering i.i.d. fractional Brownian motions . The latter are sampled by the circulant embedding method with a standard routine (e.g. see [49], Chapter 6).

8.2. Simulations

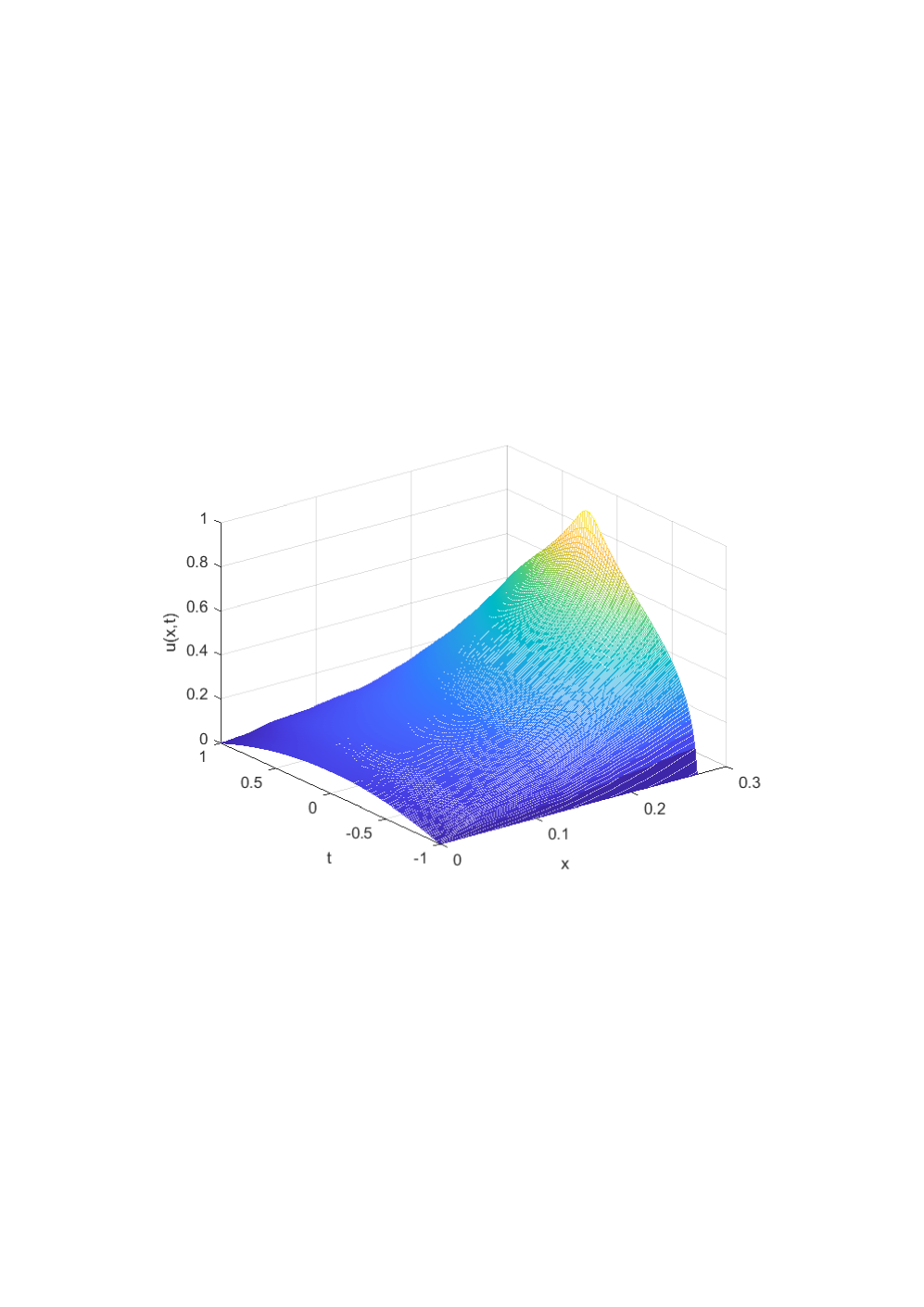

Initially, we present a realization of the numerical solution of problem (8.1)-(8.3) in Figure 2(a) for , , initial condition for and extended homogeneous Dirichlet boundary conditions. We also consider the nonlocal diffusion exponent and take Hurst index . By this performed realization the occurrence of quenching is evident.

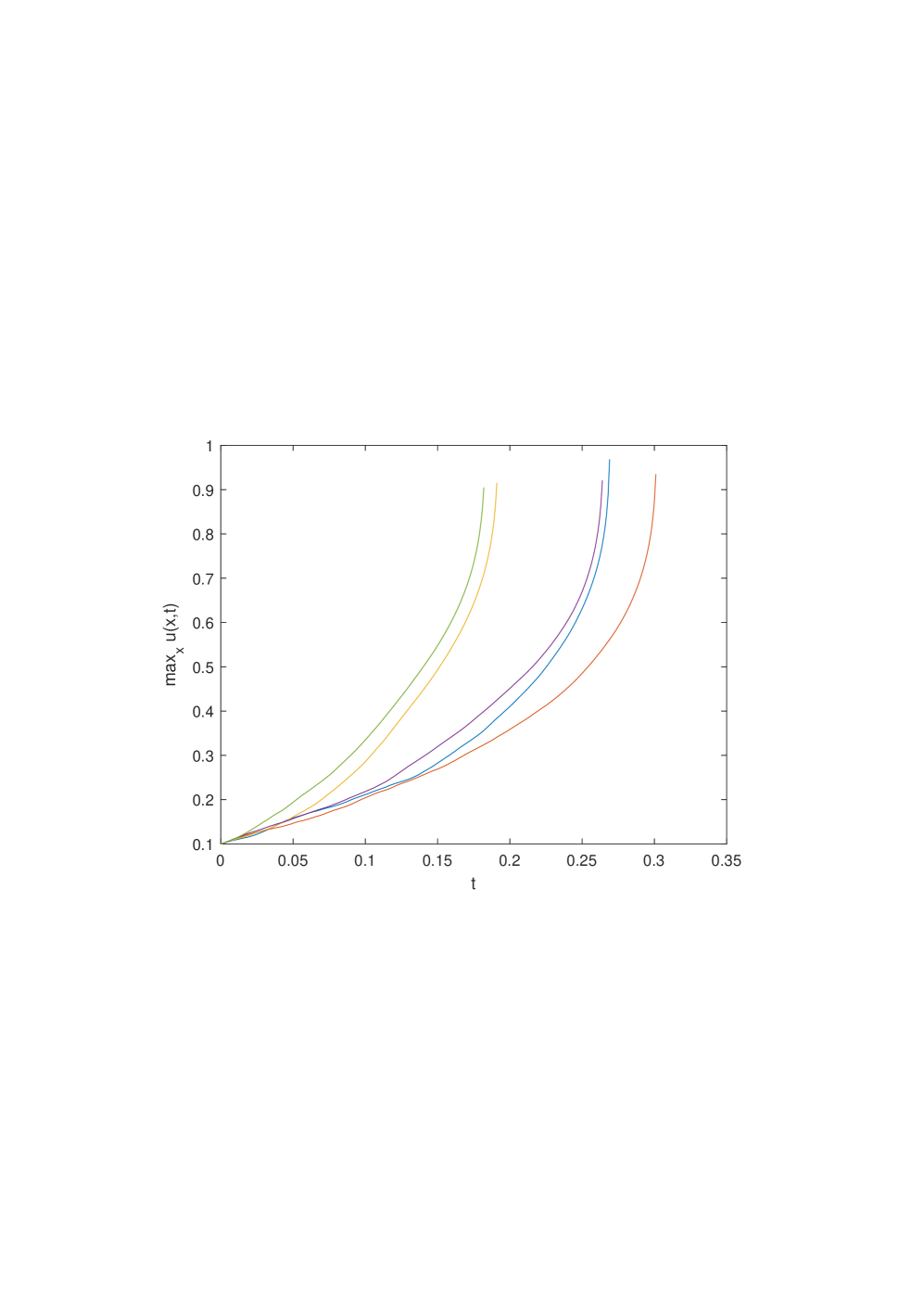

For a different set of five realizations but for the same parameters in Figure 2(b) the maximum of the solution at each time step is plotted and again a similar quenching behaviour is observed.

An interesting aspect worth investigating is the derivation of estimates of the quenching probability in a specific time interval for some

We know, see [40, 44], that for the coresponding deterministic problem with the Laplacian operator, that is (8.1)-(8.3) with and and imposed Dirichlet boundary conditions, then the solution will eventually quench in some finite time for large enough values of the parameter or big enough initial data.

From the application point of view, an estimate of the probability that with respect to various values of the parameter would be desirable. In Table the results of such a numerical experiment are presented. In particular, implementing realizations, in the first column we print out the values of the parameter considered. The second column contains the number of times that the solution quenched before the specified simulation time over the number of realizations which provides the estimation of the quencing probability. Additionally, in the last two columns the mean and the variance of the quenching time respectively are given. The quenching time numerically is approximated as for the maximum time step for which the condition holds for a predefined small number . In the simulations of this section is taken to be the machine tolerance i.e. . The rest of the parameters were taken to be the same as in the previous simulations but with , , , .

Table (T1)

Realizations of the numerical solution of problem (8.1)-(8.3)

for in the time interval

| Quenching Probability | |||

|---|---|---|---|

| 0.01 | 0 | - | - |

| 0.2 | 0.1802 | 0.8285 | 0.0124 |

| 0.4 | 0.5141 | 0.6953 | 0.0200 |

| 0.6 | 0.8021 | 0.5482 | 0.0182 |

| 0.8 | 0.9542 | 0.4145 | 0.0091 |

| 1 | 0.9953 | 0.3188 | 0.0026 |

| 1.2 | 0.9997 | 0.2583 | 6.5095e-04 |

| 1.4 | 1.0000 | 0.2192 | 2.2777e-04 |

From the results presented in Table we deduce that we have a behaviour of the problem resembling the deterministic case. Increasing results in a corresponding increase of the quenching events while the estimated quenching time decreases. Finally for large enough value of the parameter we have quenching with estimated probability one while for very small we have no quenching events in the interval .

Next we proceed with an investigation of the effect of the regularizing term on the quenching behaviour. We solve numerically the problem ((8.1)-(8.3)) using the same set of parameters as for the experiments in Table but with the source term having now the form , with . The results are demonstrated in Table

Table (T2)

Realizations of the numerical solution of problem (8.1)-(8.3) with the addition of the regularizing term .

for and , in the time interval

| Quenching Probability | |||

|---|---|---|---|

| 0.01 | 0 | - | - |

| 0.2 | 0.1470 | 0.8388 | 0.0112 |

| 0.4 | 0.4614 | 0.7154 | 0.0198 |

| 0.6 | 0.7473 | 0.5729 | 0.0192 |

| 0.8 | 0.9274 | 0.4386 | 0.0113 |

| 1 | 0.9907 | 0.3350 | 0.0038 |

| 1.2 | 0.9998 | 0.2683 | 8.5834e-04 |

| 1.4 | 1.0000 | 0.2259 | 2.9059e-04 |

Indeed comparing these results with those of Table we observe that the probability of quenching decreases due to the addition of the regularizing term. Also the mean value of the quenching time is larger with slightly smaller variation. This is a result combatible with those obtained analyticaly for the extended Robin conditions case.

In the next set of experiments in Table , and in the rest of this section, we drop the regularizing term i.e. we set and focus on the effect of the fractional Brownian noise on the quenching behaviour of the problem. Namely for a fixed value of and of we vary the coefficient expressing the intensity of the fractional Brownian term. The rest of the parameters are kept the same as in the previous simulations.

Table (T3)

Realizations of the numerical solution of problem (8.1)-(8.3) in the case of varying fractional Brownian noise intensity for in the time interval

| Quenching Probability | |||

|---|---|---|---|

| 0.05 | 0.5191 | 0.7179 | 0.0177 |

| 0.1 | 0.5205 | 0.6961 | 0.0196 |

| 0.5 | 0.5341 | 0.5244 | 0.0285 |

| 1 | 0.5575 | 0.4453 | 0.0321 |

| 1.5 | 0.5702 | 0.3989 | 0.0344 |

| 2 | 0.5799 | 0.3718 | 0.0354 |

We observe that by increasing the coefficient we have a tendency to obtain more quenching events and consequently a decreased average quenching time . Such a result should be expected due to the long-range dependence is exhibited by the fractional Brownian motion for

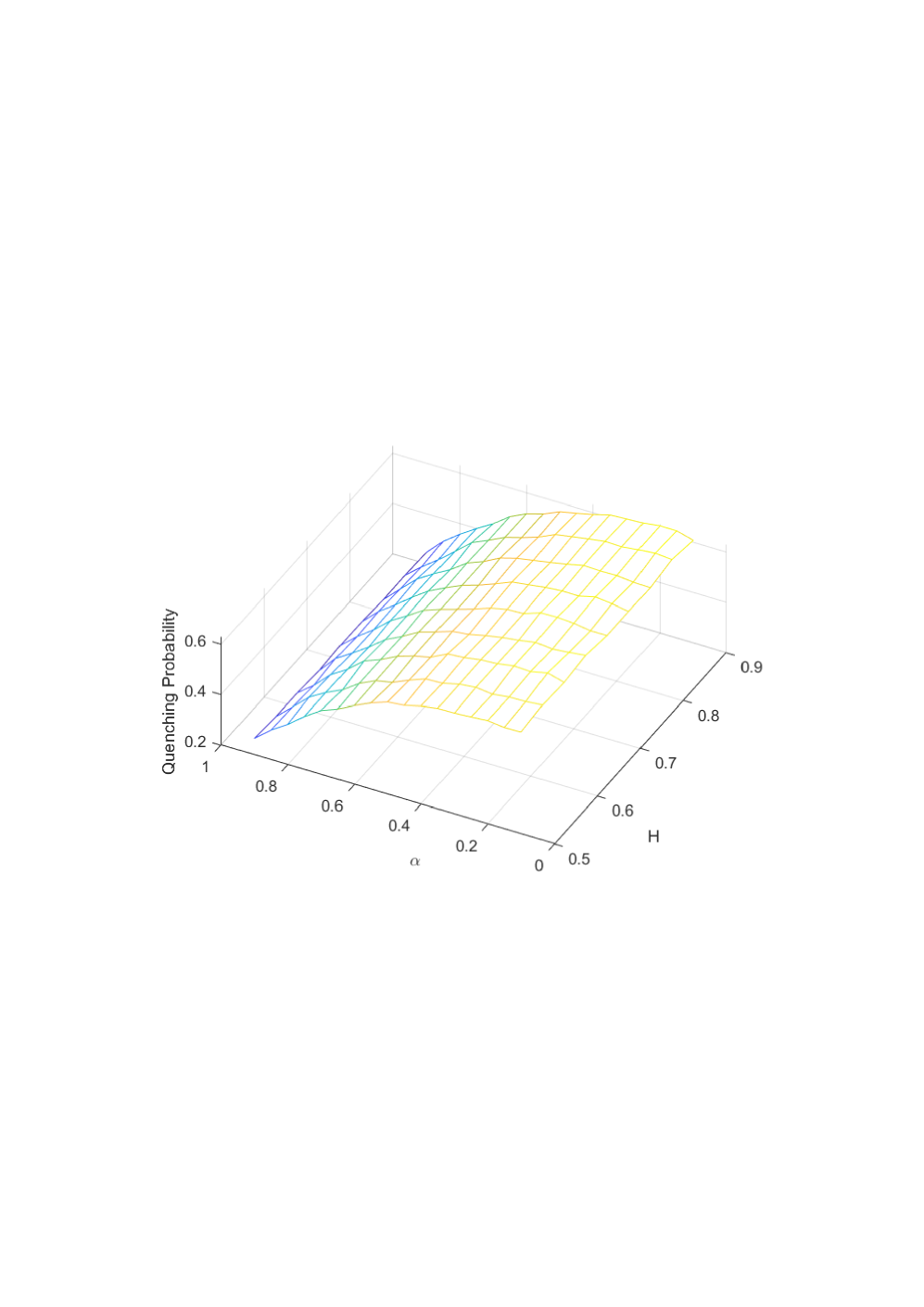

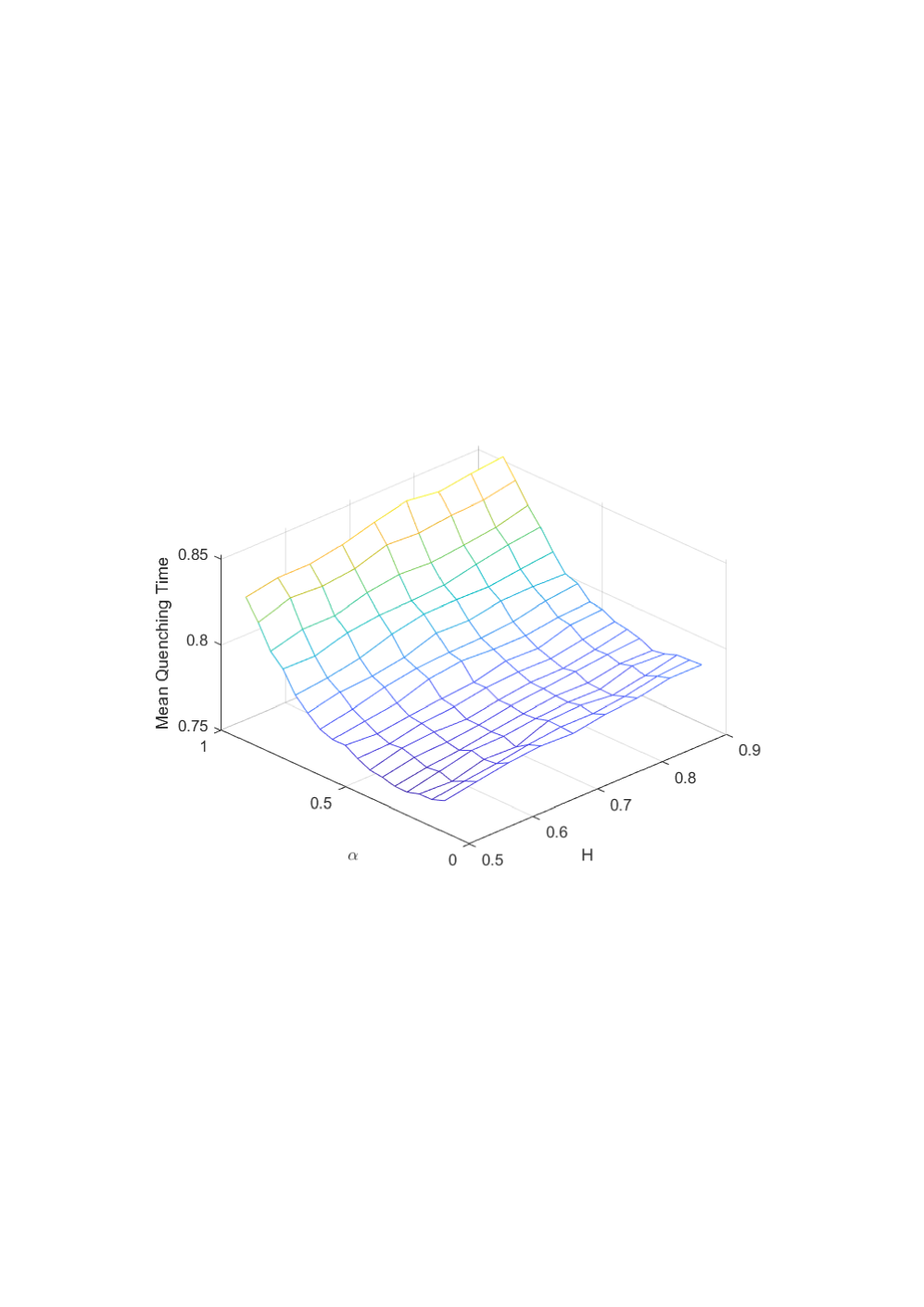

Moreover in the next set of graphs, see Figure 3, we investigate the effect of the Hurst index and the order of the fractional Laplacian operator upon the quenching probability and the quenching time. We set and and a partition in these intervals with step , while for the rest of the parameters we have , and . The number of realisations for each choise of where , , , , and again .

Figure 3(a) shows that the quenching probability decreases as the Hurst index increases from to while there is no significant variation of the probability with respect to the order of the fractional Laplacian In Figure 3(b) we observe that the mean quenching time increases as both the Hurst index and the order of the fractional Laplacian increase.

9. Discussion

In the current work, we investigated the behaviour of certain stochastic partial differential equations, including nonlocal diffusion operators assigned to nonlocal Robin conditions. The dynamics were driven by a mixture of a Wiener process and fractional Brownian motion with Hurst index The considered model can describe the operation of MEMS devices embeded to materials with discontinuities. This model can exibit the phenomenon of finite time quenching, which is closely related to the mechanical phenomenon of touching down in MEMS devices. Similar models, related also to MEMS systems, driven by either single Brownian or fractional Brownian motions have been investigated in [18, 19, 39]. However, to the best of our knowledge, this is the first time in the literature that the quenching behaviour of such nonlocal model with mixed noises is investigated.

Our theoretical analysis enabled us to provide upper bounds for the quenching probability and for the quenching time. To this end, we employed estimates of perpetual integral functionals of Brownian motion as wells as recently obtained tale estimates of fractional Brownian motion. Moreover, we were able to estimate the probability of global existence, and as a by-product we also derived lower estimates of the quenching time. The produced analytical results exhibit the strong impact of the noise to the long time dynamics of the model. In particular, as alluded to in Theorem 5.4, the form of the nonlinear term in problem (1.1) – (1.3) forces the solution towards quenching almost surely. This is in stark contrast with the dynamics of the corresponding deterministic local diffusion system, cf. [40, 44]. A key auxiliary result for our analytical approach is the positivity of the principal Robin eigenpair of the considered nonlocal operator. It is worth emphasizing, that since such a result was not available in the literature we had to prove it, see Appendix.

A complementary numerical study of the underlying nonlocal model has been employed for the case of fractional Laplacian and for homogeneous extended Dirichlet boundary conditions. The presented numerical experiments shed light to the impact of the mixed noise to the dynamics of the model. More interestingly, the numerical simulations illuminate how the dispersal coefficient affects the quenching behaviour of the underlying model, an effect cannot be observed by means of an analytical approach.

10. Appendix

Proof of Proposition 2.1.

The proof (that follows the strategy of [25]) can be broken into the following steps:

1. We first now that by the Green-Gauss formula, for any it follows that

as long as satisfies the nonlocal Robin-type boundary conditions.

Hence, for any satisfying Robin-type boundary conditions

| (10.1) |

2. We now take any , such that . Since the set of Robin eigenfunctions for forms an orthonormal basis (see Theorem 4.21 in [26]) we expect an expansion for of the form , with , and the expansion converging in and .

Moreover, for any two eigenfunctions , , we have (using (10.1)) that

| (10.2) |

where we also used the orthonormality of in .

Using arguments related to the Lax-Milgram lemma, we can consider the bilinear form as forming an inner product on the fractional Sobolev space , which will subsequently be denoted by to indicate the resemblance with the standard Sobolev space used for the local problem. To this end, motivated by (10.2), we note that the set forms a basis for Indeed, (10.2) shows that is orthonormal with respect to this new inner product. To show that this is a basis for it suffices to show that for all implies that . To see this we simply have to use (10.1), to observe that

and by the fact that is an orthonormal basis for , we see that as required.

Hence, is an orthonormal basis for the Hilbert space , endowed with the inner product . This implies that for any , the series , for converges in . We easily see that . By the observation the , so that also admits an expansion , in , and upon direct comparison with the corresponding expansion for in , we see that the two expansions coincide.

3. We are now ready to show the variational formula (2.8).

Consider any , such that . By the results of step 2, it admits an expansion of the form , with and . We now calculate using this expansion and the bilinearity of :

where we used the fact that and .

Hence, for any such that it holds that . Choosing, , the first Robin eigenfunction we see that . Hence, (2.8) is proven.

4. We now show that for any such that the following are equivalent:

| (10.3) | |||

| (10.4) |

and

| (10.5) |

Clearly (10.3)–(10.4) implies (10.5) by a simple application of the Green-Gauss formula. It thus remains to prove the reverse implication.

Suppose that (10.5) holds for some such that . By step 2, admits an expansion of the form with , and . Moreover, by the bilinearity of , and the above expansion we have that (essentially as in step 3) that

| (10.6) |

Note that

| (10.7) |

which upon rearrangement yields,

| (10.8) |

and in return (recalling the fact that ) yields

| (10.9) |

Combining that with the expansion for we see that the only contribution on comes from projections of on the solutions of the Robin eigenvalue problem, for .

There is no guarantee for uniqueness (up to constant multiplications) for the solution of problem , subject to Robin boundary conditions. However, using results from the Fredholm theory (for the inverse of ) we know that has finite multiplicity, hence there exists solutions of problem , subject to Robin boundary conditions, .

Taking into account that for all and the finite multiplicity of the first eigenfunction we conclude that , with , , with Robin boundary conditions. Then,

and with a similar calculation . Hence, (10.5) implies (10.3) and the proof of this step is complete.

Step 5. We now show that if is an eigenfunction of (with Robin boundary conditions and ) with eigenvalue , then so it is .

To show that note that since is an eigenfunction of we have by (2.8) that

| (10.10) |

We recall the elementary inequality which we apply for , to see that , hence,

| (10.11) |

where we also used (10.10).

But since also implies that , once more by (10.10) and (10.11) we see that

| (10.12) |

which by the results of step 4 yields that is also an eigenfunction.

We note that by the same argument, and since , by a convexity argument the same holds for , and subsequently for .

Step 6. By the results of step 5 we have that in , which in turn implies that in , with . With the comment above, same applies for . By the strong maximum principle (see Theorem 1.1, or Theorem 1.2 in [36]) this implies that either is strictly positive or identically zero. Exactly the same applies for . Since having and identically zero will lead to the trivial solution, we conclude that hence .

∎

References

- [1] M. Abramowitz and I.A. Stegun, Handbook of mathematical functions with formulas, graphs, and mathematical tables, volume 55. Dover Publications, New York, 1972. 9th Edition.

- [2] A. Alvarez, J. Alfredo Lopez -Mimbela and N. Privault, Blowup estimates for a family of semilinear SPDES with time-dependent coefficients, Differ. Equ. Appl., 7 (2) (2015), 201–219.

- [3] M.A. Arcones, On the law of the iterated logarithm for Gaussian processes, J. Theor. Probab. 8, (1995), 877–903.

- [4] S. A. Asogwa, J. B. Mijena & E. Nane, Blow-up results for space-time fractional stochastic partial differential equations, Potential Analysis 53, 2020, 357–386.

- [5] B. Barrios & . Medina, Strong maximum principles for fractional elliptic and parabolic problems with mixed boundary conditions, Proc. Roy. SSoc. Edinburgh 150, 2020, 475–495.

- [6] A.N. Borodin, & P. Salminen, Handbook of Brownian motion—facts and formulae. Second edition. Probability and its Applications. Birkhäuser Verlag, Basel, 2002.

- [7] P. Cheridito, Mixed fractional Brownian motion, Bernoulli 7 (2001), 913–934.

- [8] C.Chirkov & A.Grumezescu, Microelectromechanical systems (MEMS) for biomedical applications, Micromachines 13 (2022), 164.

- [9] B. Claus & M. Warma, Realization of the fractional Laplacian with nonlocal exterior conditions via forms method, J. Evol. Equ. 20 (2020), 1597–1631.

- [10] G. Da Prato & J. Zabczyk, Stochastic Equations in Infinite Dimensions, Cambridge University Press, Cambridge, 2nd Edition, 2014.

- [11] M. D’Elia, Q. Du, M. Gunzburger & R. Lehoucq, Nonlocal convection-diffusion problems on bounded domains and finite-range jump processes, Comput. Methods Appl. Math. 17 (4) (2017), 707–722.

- [12] M.Dozzi, E.T. Kolkovska and J.A.Lopez-Mimbela, Global and non-global solutions of a fractional reaction-diffusion equation perturbed by a fractional noise, Stoch. Anal. Applications, 38(6), 959–978, 2020.

- [13] M. Dozzi & J. A. López-Mimbela, Finite-time blowup and existence of global positive solutions of a semi-linear SPDE, Stoch. Proc. Applications 120, (2010), 767–776.

- [14] M. Dozzi, E.T. Kolkovska, & J. A. López-Mimbela, Finite-time blowup and existence of global positive solutions of a semi-linear stochastic partial differential equation with fractional noise, Modern stochastics and applications, 9–108, Springer Optim. Appl., 90, Springer, Cham, 2014.

- [15] M. Dozzi, E.T. Kolkovska, & J. A. López-Mimbela, Global and non-global solutions of a fractional reaction-diffusion equation perturbed by a fractional noise, Stoch. Anal. Applications 38 (6) 2020, 959–978

- [16] M. Dozzi, E.T. Kolkovska, J. A. López-Mimbela, R. Touibi, Large time behaviour of semilinear stochastic partial differential equations perturbed by a mixture of Brownian and fractional Brownian motions, Stochastics doi:10.1080/17442508.2023.2167518

- [17] O. Drosinou, N.I. Kavallaris and C.V. Nikolopoulos, A study of a nonlocal problem with Robin boundary conditions arising from technology, Math. Methods Appl. Sci. 44 (13), (2021), 10084–10120.

- [18] O. Drosinou, N.I. Kavallaris and C.V. Nikolopoulos, Impacts of noise on the quenching of some models arising in MEMS technology, Euro. Jnl of Applied Mathematics doi:10.1017/S0956792522000262.

- [19] O. Drosinou, C.V. Nikolopoulos, A. Matzavinos N.I. Kavallaris and, A stochastic parabolic model of MEMS driven by fractional Brownian motion, J. Math. Biol. 86, 73 (2023), https://doi.org/10.1007/s00285-023-01897-6.

- [20] N. T. Dung, Tail estimates for exponential functionals and applications to SDEs Stoch. Proc. Appl. 128(12), (2018), 4154–4170.

- [21] N. T. Dung, The probability of finite-time blowup of a semi-linear SPDE with fractional noise Stat. Probab. Letters 149, (2019), 86–92.

- [22] Q. Du, Nonlocal modeling, analysis, and computation CBMS-NSF Regional Conference Series in Applied Mathematics, 94. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 2019.

- [23] S. Duo, H. W. van Wyk & Y. Zhang, A novel and accurate finite difference method for the fractional Laplacian and the fractional Poisson problem, Journal of Computational Physics 355, (2018), 233–252.

- [24] P. Esposito, N. Ghoussoub & Y. Guo, Mathematical analysis of partial differential equations modeling electrostatic MEMS, Courant Lecture Notes in Mathematics, 20. Courant Institute of Mathematical Sciences, New York, American Mathematical Society, Providence, RI, 2010.

- [25] L. C. Evans, Partial Differential Equations, Second Edition, American Mathematical Society, 2010.

- [26] G. Foghem, and M. Kassmann, A general framework for nonlocal Neumann problems, arXiv preprint arXiv:2204.06793 (2022).

- [27] G. Flores, G. Mercado, J. A. Pelesko & N. Smyth, Analysis of the dynamics and touchdown in a model of electrostatic MEMS, SIAM J. Appl. Math., 67 (2006/07), 434–446.

- [28] G. Flores, Dynamics of a damped wave equation arising from MEMS, SIAM J. Appl. Math., 74 (2014), 1025–1035.

- [29] N. E. Frangos, S. D. Vrontos & A. N. Yannacopoulos, Ruin probability at a given time for a model with liabilities of the fractional Brownian motion type: A partial differential equation approach., Scandinavian Actuarial Journal 2005, 4 (2005): 285–308.

- [30] N. Ghoussoub & Y. Guo, On the partial differential equations of electrostatic MEMS devices II: dynamic case, Nonlinear Diff. Eqns. Appl. 15 (2008) 115–145.

- [31] Y. Guo, Dynamical solutions of singular wave equations modeling electrostatic MEMS, SIAM J. Appl. Dyn. Syst., 9 (2010), 1135–1163.

- [32] J.-S. Guo, B. Hu & C.-J. Wang, A nonlocal quenching problem arising in micro-electro mechanical systems, Quarterly Appl. Math., 67 (2009), 725–734.

- [33] J.-S. Guo and N.I. Kavallaris, On a nonlocal parabolic problem arising in electrostatic MEMS control, Discrete Contin. Dyn. Syst., 32(5) (2012), 1723–1746.

- [34] J.-S. Guo, N.I. Kavallaris, C.-J. Wang & C.-Y. Yu , The bifurcation diagram of a micro-electro mechanical system with Robin boundary condition, Hiroshima Mathematical Journal (to appear).

- [35] H. Gimperlein, R.He & A. A. Lacey, Quenching for a semi-linear wave equation for micro-electro-mechanical systems, Proc. R. Soc. A. 478 2022049020220490 http://doi.org/10.1098/rspa.2022.0490

- [36] S. Jarohs & T. Weth, On the strong maximum principle for nonlocal operators, Mathematische Zeitschrift 293 (2019), 81–111.

- [37] I. Karatzas & S. Shreve, Brownian motion and stochastic calculus, Vol. 113 of Graduate Texts in Mathematics, Springer-Verlag, New York, 2nd edition, 1991.

- [38] N. I. Kavallaris, Explosive solutions of a stochastic nonlocal reaction-diffusion equation arising in shear band formation, Math. Methods Appl. Sci. 38(16) (2015), 3564–3574.

- [39] N. I. Kavallaris, Quenching solutions of a stochastic parabolic problem arising in electrostatic MEMS control, Math. Methods Appl. Sci. 41 (3) (2018), 1074–1082.

- [40] N.I. Kavallaris, T. Miyasita and T. Suzuki, Touchdown and related problems in electrostatic MEMS device equation, Nonlinear Diff. Eqns. Appl., 15 (2008), 363–385.

- [41] N. I. Kavallaris, A. A. Lacey, C. V. Nikolopoulos and D. E. Tzanetis, A hyperbolic non-local problem modelling MEMS technology, Rocky Mountain J. Math., 41 (2011), 505–534.

- [42] N. I. Kavallaris, A. A. Lacey, C. V. Nikolopoulos and D. E. Tzanetis, On the quenching behaviour of a semilinear wave equation modelling MEMS technology, Discrete Contin. Dyn. Syst., 35 (2015), 1009–1037.

- [43] N.I. Kavallaris, A.A. Lacey and C.V. Nikolopoulos, On the quenching of a nonlocal parabolic problem arising in electrostatic MEMS control, Nonlinear Analysis, 138 (2016), 189–206.

- [44] N.I. Kavallaris & T. Suzuki, Non-Local Partial Differential Equations for Engineering and Biology: Mathematical Modeling and Analysis, Mathematics for Industry Vol. 31 Springer Nature 2018.

- [45] N.I. Kavallaris & Y. Yan, Finite-time blow-up of a non-local stochastic parabolic problem, Stoch. Proc. Applications, 130(9), (2020), 5605–5635 doi.org/10.1016/j.spa.2020.04.002.

- [46] F.C. Klebaner, Introduction to Stochastic Calculus with Applications, 2nd edition, Imperial College Press, London, 2005.

- [47] L. Li, Z. Chen & T. Caraballo, Dynamics of a stochastic fractional nonlocal reaction–diffusion model driven by additive noise, Discrete and Continuous Dynamical Systems - S. doi: 10.3934/dcdss.2022179.

- [48] J. López-Mimbela & Pérez, Global and nonglobal solutions of a system of nonautonomous semilinear equations with ultracontractive Lévy generators, J. Math.Anal.Appl. 423 (2015) 720–733.

- [49] G.J. Lord , C.E. Powell & T. Shardlow An Introduction to Computational Stochastic PDEs, Cambridge University Press: Cambridge, UK, 2014.

- [50] B. Maslowski & D. Nualart, Evolution equations driven by a fractional Brownian motion, J. Funct. Anal. 202 (2003), 277–305.

- [51] Y. Mishura, Stochastic calculus for fractional Brownian motion and related processes, Springer Lecture Notes in Mathematics, 1929, Springer, Berlin (2008).

- [52] T. Miyasita, On a nonlocal biharmonic MEMS equation with the Navier boundary condition, Sci. Math. Jpn. 80(2) (2017), 189–208.

- [53] T. Miyasita, Convergence of solutions of a nonlocal biharmonic MEMS equation with the fringing field, J. Math. Anal. Appl. 454(1) (2017), 265–284.

- [54] T. Miyasita, Global existence of radial solutions of a hyperbolic MEMS equation with nonlocal term, Differ. Equ. Appl. 7 (2) (2015), 169–186.

- [55] D. Nualart, The Malliavin Calculus and Related Topics, Springer Verlag, Berlin, 2006.

- [56] D. Nualart & P. Vuillermot, Variational solutions for partial differential equations driven by a fractional noise, J. Funct. Anal. 232 (2006), 390–454.

- [57] D. Nualart, Fractional Brownian motion: stochastic calculus and applications. In International Congress of Mathematicians (Vol. 3, pp. 1541-1562). Eur. Math. Soc., 2006.

- [58] E. Nuxoll, BioMEMS in drug delivery, Adv. Drug Deliv. Rev. 65 (2013), 1611–1625.

- [59] A. Pazy ,Semigroups of linear operators and applications to partial differential equations Applied Mathematical Sciences, 44 Springer-Verlag, New York, 1983.

- [60] J.A. Pelesko & D.H. Bernstein, Modeling MEMS and NEMS, Chapman Hall and CRC Press, 2002.

- [61] J.A. Pelesko & A.A. Triolo, Nonlocal problems in MEMS device control, J. Eng. Math. 41 (2001) 345–366.

- [62] H. Schaefer, Banach lattices and positive operators, Springer 1974.

- [63] M. Yor, Exponential Functionals of Brownian Motion and Related Processes, Springer 2001.

- [64] P. Yager, T. Edwards, E. Fu et al., Microfluidic diagnostic technologies for global public health, Nature 442 (2006), 412–418.

- [65] M. Younis, MEMS Linear and Nonlinear Statics and Dynamics, Springer, New York, 2011.

- [66] J. Xu & T. Caraballo, Dynamics of stochastic nonlocal partial differential equations, Eur. Phys. J. Plus 136, 849, (2021). https://doi.org/10.1140/epjp/s13360-021-01818-w.

- [67] J. Xu & T. Caraballo, Dynamics of stochastic nonlocal reaction-diffusion equations driven by multiplicative noise, Analysis and Applications https://doi.org/10.1142/S0219530522500075.

- [68] M. Zähle, Integration with respect to fractal functions and stochastic calculus II Math. Nachr. 225, (2001), 145–183.