Does Principal Component Analysis Preserve the Sparsity in Sparse Weak Factor Models?

Abstract

This paper studies the principal component (PC) method-based estimation of weak factor models with sparse loadings. We uncover an intrinsic near-sparsity preservation property for the PC estimators of loadings, which comes from the approximately upper triangular (block) structure of the rotation matrix. It implies an asymmetric relationship among factors: the rotated loadings for a stronger factor can be contaminated by those from a weaker one, but the loadings for a weaker factor is almost free of the impact of those from a stronger one. More importantly, the finding implies that there is no need to use complicated penalties to sparsify the loading estimators. Instead, we adopt a simple screening method to recover the sparsity and construct estimators for various factor strengths. In addition, for sparse weak factor models, we provide a singular value thresholding-based approach to determine the number of factors and establish uniform convergence rates for PC estimators, which complement Bai and Ng (2023). The accuracy and efficiency of the proposed estimators are investigated via Monte Carlo simulations. The application to the FRED-QD dataset reveals the underlying factor strengths and loading sparsity as well as their dynamic features.

JEL Classification: C12, C53, C55

Key Words: Factor number, Factor strength, Principal component, Rotation matrix, Sparse factor loadings, Sparsity preservation, Weak factors

1 Introduction

Factor models have been widely used in economics and finance. Until very recently, a large body of literature on factor models has built on the assumption that all factors are strong or pervasive in the sense that each factor can influence almost all cross-sectional units. Under this assumption, Bai and Ng (2002) and Bai (2003) establish the asymptotics of principal component (PC) estimators with units observed with periods. It is well known that the space spanned by the factors can be estimated consistently by the PC method with rate , and both the estimated factors and factor loadings are consistent up to some rotation matrices.

However, many empirical findings support the existence of weak factors with sparse factor loadings. For instance, both Stock and Watson (2002) and Ludvigson and Ng (2009) find that the extracted PC factors from a large set of standardized macroeconomic variables can only fit a few variables’ time series observations well, suggesting a sparsity structure in factor loadings. More recently, Kristensen (2017), Freyaldenhoven (2022a), and Uematsu and Yamagata (2023a, b) revisit the same dataset in Stock and Waston (2002) and further confirm the findings on loadings. In addition, Uematsu and Yamagata (2023a) find sparse factor loadings in the FRED-MD dataset (McCracken and Ng, 2016) and in firm security excess returns of the S&P 500 index. Another motivation for sparse factor loadings comes from the literature on hierarchical or group factor models, where the local factors have nonzero factor loadings only for some specific cross-sectional groups. For example, shocks due to oil supply may only affect industrial production sectors, but not the industry of service. In empirical asset pricing, it is expected that portfolios formulated by size or value factor are influenced by such factors, but portfolios formulated by the momentum factor may not be. For more examples of local/group factors, see Ando and Bai (2017) and Choi et al. (2021).

Due to the aforementioned reasons, weak factor models have gained immense popularity and attracted the attention of many researchers. For instance, Onatski (2012) shows that the PC estimate is inconsistent when the true factor loadings are weak enough such that has a positive definite (p.d.) limit as approaches infinity. More recently, Uematsu and Yamagata (2023a, b) propose a sparse orthogonal factor regression (SOFAR) estimator that uses regularization to achieve sparsity, and also provide a new inferential procedure to determine whether each component of the factor loadings is zero or not and prove that it controls false discovery rate (FDR) under a pre-assigned level; Freyaldenhoven (2022a) proposes a new class of estimators to determine the number of relevant factors in the presence of local factors, and Guo et al. (2022) investigate information criteria with a new penalty to determine the number of factors, which can be adaptive to the degree of factor pervasiveness and favor more parsimonious models; Bai and Ng (2023) investigate the large sample properties of static PC estimators for approximate factor models with general weak factor loadings and show that the PC estimators are still consistent and asymptotically normal; for factor-based forecasting with large sets of variables, Chao et al. (2022), Chao and Swanson (2022), and Giglio et al. (2022b) use pre-screening methods to select valid predictors when factor pervasiveness does not hold.

In this paper, we delve into the study of weak factor models with sparse factor loadings.111There is another type of weak factor models that involve nonzero but small factor loadings, i.e., loadings shrinking towards zero as sample size increases. However, for economic and financial applications, sparsity-induced weak factor models are more relevant and the estimators with sparsity tend to have meaningful interpretation. As such, this paper focuses on weak factor models with sparse loadings. A factor is called “sparsely weak” when it only affects a small subset of cross-sectional units. This is the same as the “sparsity-induced” weak factor in Uematsu and Yamagata (2023a, b). Instead of taking SOFAR of Uematsu and Yamagata (2023a), we follow Bai and Ng (2023) to consider the PC estimation since it is much simpler and free of tuning parameters. To recover the sparsity in factor loadings, we adopt a simple screening on the PC estimator of factor loadings. Our computation burden is almost negligible compared to the procedures with regularization in Uematsu and Yamagata (2023a, b).

Under the sparsity assumption on factor loadings, we show that PC estimators of factors, factor loadings, and the common components are still consistent, and further establish their asymptotic distributions and uniform convergence rates. In addition to the usual large sample properties of PC estimators, we find that the rotation matrix in PC estimation has a special structure that leads to nearly sparse PC estimates for factor loadings. Based on this finding, we further sparsify the loading estimator exactly by screening the estimated PC loadings. Then with the sparsified loading estimator, we can straightforwardly estimate distinct factor strengths consistently. Finally, we propose using singular value thresholding (SVT) to determine the number of factors in sparse weak factor models.

In summary, this paper studies the properties of PC estimates for weak factor models with sparse loadings and proposes a PC-based screening method to sparsify the estimator for factor loadings. It has the following additional contributions to the existing literature on weak factor models. First, under our sparsity assumption on factor loadings with mixed sparsity degrees, we establish the large sample properties of PC estimates for factors, factor loadings, and common components, respectively. In particular, we provide the uniform convergence rates for PC estimates, which complement Bai and Ng (2023). Second, we show that the PC estimators for loadings are still sparse, meaning the sparsity structure in factor loadings is nearly invariant to the rotation matrix induced by the PC method. To the best of our knowledge, our paper is the first to reveal this intrinsic sparsity preservation feature of the PC estimator. This result is also in sharp contrast to the common sense that the sparsity of factor loadings cannot be reserved due to the matrix rotation in PC estimation; see Bailey et al. (2021, BKP hereafter) and Freyaldenhoven (2022b). We show that the invariance of sparsity to rotation comes from the particular structure of the rotation matrix , which is an (approximately) upper triangular matrix. Third, given the invariance of sparsity of factor loadings to PC rotation, we can easily recover the sparsity of factor loadings by applying proper screening to the PC estimates of factor loadings. In some scenarios, it is important and necessary to recover the sparsity structure of factor loadings when the estimated factor loadings are used as “generated regressors”. For example, ignoring the sparsity structure of factor loadings will lead to an inconsistent estimator of risk premia in the empirical asset pricing model of Giglio and Xiu (2021) and Giglio et al. (2022a). Fourth, based on the sparse loading estimators, we provide straightforward estimators for all factor strengths and establish their consistency. This result improves BKP (2021) where only the strength of the strongest factor is identified and estimated. Lastly, we make a contribution to the determination of the number of factors in weak factor models. Research on selecting the number of factors in weak factor models is still very limited. We investigate the SVT approach and establish its consistency in determining the factor number.

It is worth mentioning that our work is also related to the large literature on sparsity pursuit in factor models. The sparse principal component analysis (SPCA) pursues a sparse structure in the estimation of factor loadings to achieve a good interpretation for extracted PC factors. In order to obtain PCs with sparse factor loadings, different penalties or threshold techniques to the fitted loadings are usually adopted. For example, Rapach and Zhou (2021) estimate sparse PCs for 120 monthly macroeconomic variables from the FRED-MD database by combining the -norm restriction in factor loadings with the PC objective function; Pelger and Xiong (2022) construct sparse proximate factors by using the largest, say, eigenvalues, and show a weaker form of correlation consistency. They do not focus on whether the factor model being weak or not but investigate its sparse approximation, while our approach can be cast as a generalized version of Pelger and Xiong (2022) in terms of selecting adaptively to factor strengths. Freyaldenhoven (2022b) explores possible rotations of estimated loadings to recover sparsity. Based on consistently estimated factor loadings , Freyaldenhoven (2022b) suggests minimizing the -norm of rotated loadings (: , subject to the rotation matrix being nonsingular, and implements solving the problem with a more feasible -norm. His basic idea is to search among different rotations of the estimated loadings to achieve sparsity. If the true factor loadings are indeed sparse, this approach may identify the sparsity pattern. For other rotation-based methods of nearly-sparse factor loadings, see Despois and Doz (2022).

We would also like to compare our paper with the recent one by Bai and Ng (2023). Both of the two papers show the asymptotic properties of factors, loadings and common components in weak factor models with possibly heterogeneous factor strengths.222Bai and Ng (2023) obtain the average errors in estimating the common components in the squared Frobenius norm only under homogeneous factor strength, while we generalize the results under heterogeneous strengths. In fact, to derive these theoretical results we are inspired by the novel proof in Bai and Ng (2023), e.g., by making use of several asymptotically equivalent rotation matrices. In spite of the overlapped targets, there are certain fundamental differences. The setup of Bai and Ng (2023) is more general allowing that the entries of are non-zero but small, whereas ours only admits sparsity induced weak factor models. Besides, our requirement of the minimal factor strength for estimation consistency, while still reasonable, is more stringent than Bai and Ng’s. We impose the stronger conditions in order to show that the rotation matrix is upper triangular. The upper triangularity reveals the sparsity preservation properties by PC estimators, which is our ultimate interest and yet not pursued by Bai and Ng (2023). Moreover, convergence rates of PC estimators may also be improved due to the upper triangularity. We also establish uniform convergence rates of these estimators, propose additional estimators for factor strengths and number of factors and prove their consistency in our setup. These questions are not formally addressed in Bai and Ng (2023), and yet may be of independent interest.

The rest of this paper is organized as follows. We formally introduce weak factor models with sparse factor loadings and the PC estimation in Section 2. In Section 3, we study the asymptotics of PC estimators for factors, factor loadings and the common components under the weak factor scheme, including consistency, asymptotic distributions, and uniform convergence rates. Based on the finding on the rotation matrix in Section 3, we propose a screening method to sparsify the estimated factor loadings and provide consistent estimators for factor strengths in Section 4. Section 5 discusses the determination of the number of factors for weak factor models. The Monte Carlo simulation and empirical application are reported in Section 6 and 7, respectively. Section 8 concludes. All technical proofs are relegated in the Appendix.

NOTATIONS. For a set , let be its cardinality. Let and for two real numbers and . For two sequences and , denotes is bounded and denotes that both and are bounded. For two random sequences and denotes is stochastically bounded and if and For a square matrix , and are the smallest and largest eigenvalue of , respectively. For a matrix let be its Frobenius norm and be its spectral norm. For a vector , its -norm is , where is the usual indicator function. Throughout, we use the running indices and for the observations, indices , for the cross-sectional units, and and for the factors.

2 The Weak Factor Models with Sparse Loadings

2.1 The model setup

To fix ideas, let us consider a static factor model with the following representation

| (2.1) |

, where is the observed data for the th individual at time , is a vector of latent factors, is the corresponding vector of factor loadings, and is the idiosyncratic error with possible weak dependence across or/and over . Or we may write the factor model in a matrix form as

| (2.2) |

where and are both matrices with and , respectively, , and . Also for later reference, denote the th column of by and the th column of by , . Throughout the paper, we let be the vector of true factors and be the true loadings, with and being the corresponding matrices.

In a standard factor model, it is typically assumed that all factors are strong in the sense that the matrix is a full rank matrix for a sufficiently large and it has a positive definite (p.d.) limit. In contrast, we allow that there are both strong and weak factors. A factor is (sparsely) weak when it is not persuasive in the sense that the proportion of its non-zero factor loadings diminishes at a certain rate. The number (in magnitude) of individuals effectively affected by the th factor is of order , and the strength of this factor can be represented by the degree parameter (BKP, 2021) such that

| (2.3) |

Obviously, a strong factor has degree . As BKP (2021) point out, for a factor with an extremely weak signal with , it is not identified without priori restrictions and not relevant in most financial and macroeconomic applications. Moreover, Freyaldenhoven (2022a) discusses the reasons why only factors affecting proportionally more than of individuals are relevant in arbitrage pricing theory (APT) and aggregate fluctuations in macroeconomics. Hence we restrict the factor strength so that for with some .333The factors with the strength parameter bigger than are named as “semi-strong” factors in BKP (2021). It may be also worth mentioning that the strength degree defined in (2.3) is -dependent (we suppress here) and thus may vary with samples.444In this paper, we aim at estimating consistently, but not inferring on it.

Our setup allows that some or even all of factors in are weak in terms of potential sparsity of . In such a model with latent factors, a standard normalization which one might want to impose is as in Uematsu and Yamagata (2023a) and Freyaldenhoven (2022a). However, this identification restriction is no longer innocuous as it is not compatible with sparsity of in general. In other words, a weak factor model (with a particular sparsity structure of ) is not invariant to an arbitrary rotation transformation. This insight is also shared by Bai and Ng (2023, Section 5.2) in terms of an overidentification restriction on , implying that the aforementioned methods would incur a problem when the restriction fails to hold in general, as verified in our Monte Carlo simulations. Since our proposed methods hinge on the particular structure of the underlying sparsity, we leave unspecified ex ante for coherence (except for its being p.d.). It is also worth mentioning that the major findings for the weak factor model in this paper can be readily applied to deal with a rank-deficient model, as a rank-deficient model is equivalent to a weak factor model up to a rotation transformation; see Giglio et al. (2022a).

2.2 PC estimation

To begin with, we assume that the true number of factors is known, and leave the determination of in Section 5. The estimation of factors and their loadings is via the method of PC in minimizing

subject to the usual identification restriction that and being diagonal.555Since it is known that the PC estimator is identified up to a full rank rotation, the identification restriction is only employed to pin down for the purpose of estimation, and should not be understood as a restriction imposed on the underlying true factors in the weak factor model. The estimated factors, denoted by , is times the eigenvectors corresponding to the largest eigenvalues of the matrix in decreasing order. Then , and . Also, let be the diagonal matrix consisting of the largest eigenvalues of in decreasing order. We also define the common component estimator as the estimator for

Without loss of generality, we assume that the degrees of factor strength are arranged such that . Given the possibility that two factors may have the same degree of strength, e.g., there may be two strong factors or two weak ones with an equal strength, we can distribute ’s into groups so that

with , and when every factor’s strength is unique. For ease of notation, let us also define the cardinality of by for Clearly, . In addition, let be the same strength shared in group , i.e., for It is obvious that

3 Large Sample Properties for PC Estimators

3.1 Main assumptions and a key result on the eigenvalue matrix

We first define a scale matrix as follows,

which will be frequently used in this paper. To study the large sample properties of PC estimators, we make the following assumptions on the weak factor models.

Assumption 1. for and as for some p.d. matrix .

Assumption 2. For the factor loadings,

(i) for all ’s and some constants and ;

(ii) For the th factor, the number of non-zero factor loading is for with for

(iii) as for some p.d. matrix .

Assumption 3. There exists a positive constant , such that for all and ,

(i) and for all and

(ii) , for all , and ;

(iii) with for all with some . In addition, for , and

(iv) For every , ;

(v) for ;

(vi) Define and . and ;

(vii) ;

(viii) The eigenvalues of are distinct.

Assumption 4.

Assumptions 1-2 are standard in the literature on panel factor models. Assumption 1 imposes a moment condition on the true factors and requires the existence of a p.d. probability limit of . Assumption 2 imposes a boundedness condition on the norm of factor loading vectors, and specifies the sparse structure in factor loadings. The deterministic factor loadings can be relaxed to be stochastic with some moment conditions. Assumption 3 provides some conditions on factors, factor loadings, and errors. 3(i)-(iii) impose moment conditions on errors and allow for weak cross-sectional/serial dependence as Bai (2003). Note that Assumption 3(iii) is weaker than Bai (2003) and thus generalizes the counterpart under a strong factor model. Assumption 3(vi) is used by Su and Wang (2017), and it is not redundant since we do not assume and are independent. Assumption 4 is also adopted by Bai and Ng (2002, 2023) and Moon and Weidner (2017). It surely holds for independently identically distributed (iid) data with uniformly bounded th moments, and may also hold for weakly dependent data across and

We first present one of the key interesting results for weak factor models via PC: the eigenvalue matrix preserves the magnitude of factor strength, as stated in Proposition 3.1 below.

Proposition 3.1

Under Assumptions 1-4, we have for

Remark 1. Unlike in a strong factor model, the diagonal elements of matrix vanish at various rates determined by their corresponding factor strengths. It raises more challenges to our asymptotic theory later involving frequently, whereas in a strong factor model all these terms are .

3.2 Consistency and asymptotic distributions

In this subsection, we establish the consistency and asymptotic distributions for PC estimators. To reveal the asymptotic properties of our estimators, it is necessary to introduce several rotation matrices as below. We have suppressed the dependence on sample sizes for these matrices to ease burden of notations. Define

We will show the asymptotic equivalence of the matrices and for which also generalizes Lemma 3 of Bai and Ng (2023). These rotation matrices and the equivalence results will play an indispensable role in establishing the convergence rates and the asymptotic distributions of our PC estimators. Before doing so, we would like to first introduce an interesting finding related to the matrix defined above. One more additional condition is needed.

Assumption 5. .

It is worth mentioning that Bai and Ng (2023) impose a weaker condition for consistency. They do not impose until in proving distributional theory. However, we impose Assumption 5 at an early stage in this paper to obtain our main result stated in Proposition 3.2, which is fundamental in sparsity recovery results in Section 4. Besides, a sharper result may be obtained for consistency rate, e.g., Proposition 3.4, by making use of Proposition 3.2 valid under Assumption 5. Also note that under as assumed by Freyaldenhoven (2022a), Assumption 5 is trivial.

Proposition 3.2

Under Assumptions 1-5, the matrix is a full rank matrix in probability and

Remark 2. Proposition 3.2 implies a very important property of serving as the rotation matrix: is (block) upper triangular asymptotically. Such a property is very helpful in working with the sparsity-induced weak factor models.

Next, we state the convergence rate of in the following proposition.

Proposition 3.3

Under Assumptions 1-5,

Remark 3. The associated convergence rate for Proposition 3.3 from Bai and Ng (2023, Proposition 6.i) is , which is a bit better than ours. The reason is that they use a slightly different rotation matrix from ours , as indicated by the comment below their Proposition 6. The reason behind our choice of the rotation matrix is that it is more closely related to playing a major role in our later analysis.

The convergence rate for factor loading estimate is provided in the next proposition.

Proposition 3.4

Under Assumptions 1-5,

Remark 4. Note that our rate in Proposition 3.4 is better than what is stated in Bai and Ng (2023, Proposition 6.ii). The reason is that we utilize the upper triangularity of rotation in our proof, which helps sharpen the bound for estimation errors.

Before proceeding, we present here the equivalence results of and for Define

Lemma 3.5

Under Assumptions 1-5,

Recall that and Lemma 3.5 thus implies that This equivalence immediately implies the consistent estimation of the common component Lemma 3.5 generalizes Lemma 1 of Bai and Ng (2019) for strong factor models, and Lemma 3 of Bai and Ng (2023) for weak factor models with a single strength.

Proposition 3.6

Under Assumptions 1-5,

Remark 5. It is noted in Proposition 3.6 that the convergence rate of in general depends on weak factor strengths, or precisely, the discrepancy of strengths between the strongest and weakest factors. It is only when all factor strengths are the same that the convergence rate is maximal and coincides with that under strong factor models. Also note that this result agrees with Bai and Ng (2023, Proposition 3) in considering homogeneous factor strength.

Now we turn to the asymptotic distributions of PC estimators. We impose the following assumption for establishing the central limit theorem (CLT), which is adaptive to weak factor models.

Assumption 6. The following hold for each and as

(i) where

(ii) where

One more regularity condition is imposed on sample size () and the weakest factor strength to guarantee the distributional theory, which is also used by Bai and Ng (2023, Assumption C’(iv)).

Assumption 7. .

Theorem 3.7

Under Assumptions 1-7,

where

Remark 6. (i) As shown in the proof of Theorem 3.7, the matrix is (block) diagonal. In particular, if no two factors have the same strength, i.e., for then is an exactly diagonal matrix so that (ii) Theorem 3.7 also reveals that the th factor is asymptotically normally distributed with convergence rate of

Assumption 8. .

Theorem 3.8

Under Assumptions 1-8,

Remark 7. Theorem 3.8 reveals that the asymptotic distribution of is the same under both strong and weak factors and invariant to factor strengths.

With Theorems 3.7 and 3.8, we come to the limiting distribution of To this end, recall from Section 2.2, and define the matrix .

Theorem 3.9

Under Assumptions 1-8,

where and

Remark 8. Theorem 3.9 thus implies that As for the asymptotic covariance matrix for ( Bai and Ng (2023) have proposed consistent estimators assuming cross-section (serial) independence for Under weakly serial dependence, Bai (2003) proposes a consistent Newey-West HAC estimator for the asymptotic covariance of For estimating the asymptotic covariance of under weakly cross-section (CS) independence, Bai and Ng (2006) propose a consistent CS-HAC estimator under covariance stationarity with for all ’s. One could follow the aforementioned approaches to formulate consistent estimators of the asymptotic covariance matrices for and which would lead to a consistent variance estimator for . For hypothesis testing, with for instance, there is no need to know factor strengths, as the feasible estimator for the variance of automatically accommodates factor strengths, and is thus adequate for such a purpose.666See the discussion under Proposition 4 of Bai and Ng (2023) for the case with a homogeneous factor strength, and one can easily show that the argument also works under heterogeneous factor strength.

3.3 Uniform convergence rates

In this section, we will establish uniform convergence rate results for , and over or (and) These results can be exploited in recovering model sparsity in Section 4, in the potential application of factor-augmented forecast regression, and are perhaps also of independent interest.

Given that dependence is allowed across both and , we first define a strong mixing condition, generalized over and similar to Ma et al. (2021). Suppose that there is some labeling of the cross-sectional units whose generic index we denote by such that the CS dependence decays with distance Then we will define a mixing rate applied for the random field where For let

where denotes a sigma-field. Then the -mixing coefficient of is defined as

where

The definition of generalizes the usual one in the time series context. In particular, when is applied to to a (single or vector of) time series, it coincides with the usual one defined by, e.g., Fan et al. (2011). (ii) For the purpose of estimation, we do not need to know the true labeling Ma et al. (2021) show that their inference is valid as long as the number of mis-assigned indices is In conducting inference, our approach is effective with the true labeling completely unknown, and thus further relaxes the assumption by Ma et al. (2021).

We now specify the additional assumptions for the uniform results.

Assumption 9. (i) and are both stationary and ergodic;

(ii) There exists and such that

(iii) There exists satisfying and , such that and for

(iv) where

From the previous section, we see that the PC estimators and are both consistent up to a certain rotation matrix. So to better state the uniform convergence result, we define the rotated factor and factor loading by and respectively.

Theorem 3.10

Under Assumptions 1-9,

(i) for

(ii) for

(iii)

Remark 9. In Theorem 3.10, result (i) implies that the estimation errors for factor loadings are uniformly dominated by . This result is very useful to explore loading sparsity and factor strength in the next section. For each factor, result (ii) provides the uniform convergence rate which depends on the factor strength. Result (iii) establishes the uniform convergence rate for the common component estimators and the rate is determined by the smallest factor strength and a parameter which controls the probability tail bound of factors.

4 Revelation of the Sparsity in Loadings with PC Estimators

It is well known that latent factor models are subject to a rotational indeterminacy. This identification issue is unwanted to reveal the loading sparsity structure. Specifically, our results in Section 2 indicates that loadings are identified only up to the rotation , and it is believed that a rotation in general plays a deterrent role in revealing sparsity. As a result, interpretation of estimated factors becomes intimidating, as it is usually drawn in a manner by relating to observables which an individual factor loads on primarily. For example, Ludvigson and Ng (2009) write,

“Moreover, we caution that any labeling of the factors is imperfect, because each is influenced to some degree by all the variables in our large dataset and the orthogonalization means that no one of them will correspond exactly to a precise economic concept like output or unemployment, which are naturally correlated.”

However, we show that even in the presence of the rotation brought in by PC, the sparsity in factor loadings can still be preserved. This justifies the ad hoc manner of interpretation of PC factors with only a small set of variables or individuals in many empirical applications; see Pelger and Xiong (2022).

4.1 Preservation of sparsity degree by the PC rotation

The success of sparsity preservation by PC largely hinges on the property of the particular rotation matrix . Proposition 3.2 implies that is a non-strictly (block) upper triangular matrix with full rank in probability.777A (lower, upper) triangular matrix is strictly (lower, upper) triangular if its diagonal elements are zero, see Abadir and Magnus (2005, page 17). In particular,

The particular formation of matrix gives rise to sparsity recovery as grows. To illustrate, consider a simple two-factor model with factor strengths and . Now

| (4.1) |

According to Proposition 3.4, the PC estimated factor loading matrix converges to a rotation of the true loading matrix, i.e., , which can be written as

Given the approximately upper triangular structure of in (4.1), we have

| (4.3) |

So the rotated loadings for factor 1 preserve its sparsity degree. Given that , the sparsity degree of factor 2 is contaminated by . Nevertheless, the contamination is non-essential due to diminishing . So, for with , if we adopt a slightly adaptive measure for sparsity degree for a generic vector as , then it follows that

| (4.4) |

The statement in (4.3) will also certainly hold if the -norm is replaced with the norm . This result suggests that the PC rotation will preserve sparsity degree, up to negligible terms, so that the factor strengths remain unchanged.

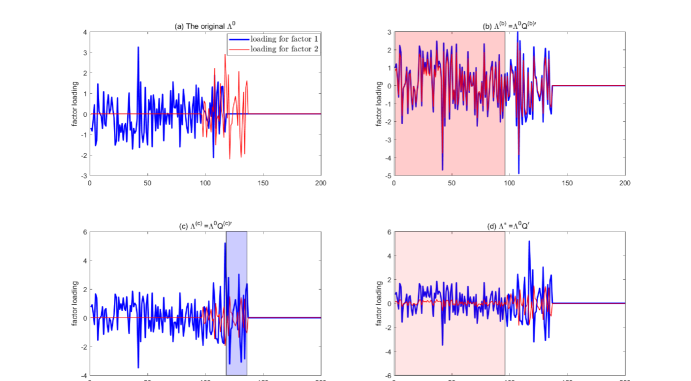

To have a better understanding of how the PC rotation acts upon the sparse loading , we continue to illustrate with the two-factor model as above via a simulation. The data generating process is set the same as in Section 6 where . Define the non-null set with regard to ’s, for , as

Part (a) of Figure 1 shows underlying in which , and . The rotation matrix is calculated as Panel (b) illustrates a common concern that rotated by an arbitrary nonsingular matrix, say , would become less sparse. To make an example, we randomly generate each element of as so that . It is obvious in part (b) that is “inflated” considerably (by the shaded area) such that the two factors turn out to have the same strength. Part (c) displays the rotation effect by a stylized exactly upper triangular matrix . here is set the same as except , i.e., . Clearly, the upper triangular resolves inflation to . On the other hand, we see in part (c) that is somewhat inflated due to the loading on (by the shaded area) from factor 2. Nevertheless, the distortion is much less severe and negligible relative to factor 1’s pervasiveness, since factor 2 is relatively weak. Finally, part (d) displays rotated by the real in the simulation. The absolute value of is indeed very small as expected in a finite sample (), though it is not exactly 0. By virtue of this feature, the inflated part of (by the shaded area) is uniformly small and vanishing at a certain rate, which will be screened off together with estimation errors to reveal sparsity. We formalize the idea in the next subsection.

4.2 Sparsity recovery with PC estimators

Our previous analysis in subsection 4.1 provides a positive identification result for rotated by . In practice, is not observable, and the available is the PC estimator . In this subsection, we will present how the recovery of sparsity, not just its degree, is achieved by working with . Undoubtedly we need to take into account of the estimation error consisting of . Theorem 3.10 (i) lends us a hand stating that the estimation errors are also uniformly vanishing, and thus justifies the sparsity recovery via screening the PC estimator .

We shall show that the set characterizing sparsity for factor can be recovered well approximately with regulated PC estimators. When the absolute value of is small, we can set the factor loading as 0. So we choose the non-zero factor loadings with a threshold value :888With the limiting distribution for PC loadings estimators in Theorem 3.8, we can also follow Uematsu and Yamagata (2023b) to select the nonzero factor loadings based on multiple testing approach. We leave this as future research.

Similarly define the estimated non-zero set for the th factor loading by To evaluate the sparsity recovery accuracy of , we denote the symmetric difference between the true non-zero set and its estimator by

We present the main results on sparsity recovery of factor loadings in the following Proposition.

Proposition 4.1

Under Assumptions 1-9, for , we have:

(i) if is unique in , then

(ii) if is not unique in , then

Remark 10. The approximation of sparsity for the th factor is characterized by bounding the symmetric difference between and () well relative to its factor strength. In particular, the th factor’s sparsity, measured in , is recovered consistently relatively to its pervasiveness when is unique; when is not unique, the difference is still well bounded relatively—a condition implying consistency of the factor strength estimator in Section 4.3.

Remark 11. (i) In the sparsity recovery of factor loadings, plays the key role of screening off noises due to rotation and estimation errors that are negligible in size. We show that the noises are uniformly, where i.e., the minimum discrepancy between distinct factor strengths. So we set to dominate the noise. (ii) Alternatively, We can consider an alternative threshold value with a tuning parameter . The optimal value of can be determined by some adaptive methods such as cross validation. Given that each (time) series will be demeaned and standardized to have unit variance, as recommended by Bai and Ng (2002), we focus on the simple threshold . In both simulations and the empirical application, our tuning parameter-free threshold value works reasonably well. (iii) The choice of a threshold value simply by the relevant dominant rate is also adopted in Fan et al. (2015) to construct a screening statistic.

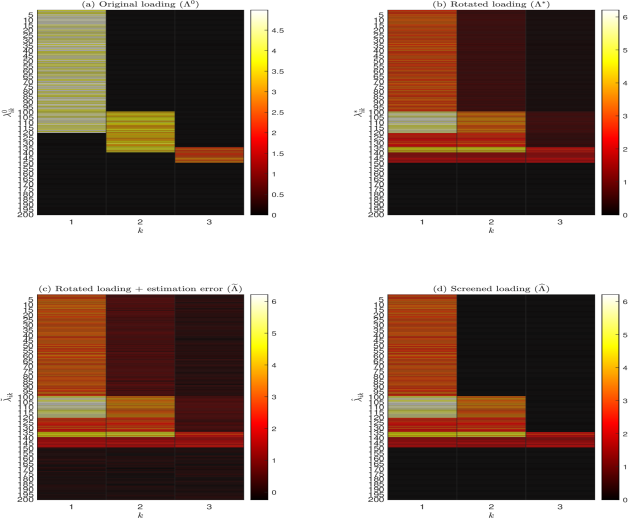

Figure 2 shows the intuition behind Proposition 4.1 using a three-factor model.999For illustration, parts (a)-(d) in Figure 2 are based on stylized manifestation but not simulation. By the path from part (a) to (b) and then to (c), we see that the distortion to model sparsity by rotation and estimation errors is either (i) dominated in absolute values relative to our screening threshold , or (ii) negligible in size relative to factor pervasiveness. Consequently, sparsity is well approximated by regulation in part (d).

Note that Uematsu and Yamagata’s (2023a) SOFAR estimator recovers sparsity alternatively by regularization. Interestingly, if we contrast the estimate of factor loadings by PC (their Figures 7 and 2) with that by SOFAR (their Figures 9 and 11) in their empirical results, we immediately realize that PC and SOFAR estimates are almost identical, except for many small noises introduced by PC. This observation suggests the validity of combining PC estimate with proper screening to recover sparsity, which in fact underlines the method used in our paper.

4.3 Estimating factor strengths

BKP (2021) consider the pervasiveness of the unobserved macroeconomic shocks by using the estimated factor strength. They can only identify and estimate the strength of the strongest factor, and the results are thus limited. We can consistently estimate factor strengths for all weak factors with various strengths, which helps understand pervasiveness of factors completely. We hope that our proposed estimator of factor strength is of independent interest.

We can understand how influential each factor is by studying to its strength. Recall that is such that Now for define

where as before. Our estimator for is simply

To consistently estimate all factor strengths, one additional restriction is needed. Define

Assumption 10. , , for some constant .

The above assumption implies that is the sparsest representation, up to a constant, among all observationally equivalent loading matrices. is of most interest as it provides the most concise interpretation of latent factors. Assumption 10 excludes, for instance, two factors with highly correlated loadings.

Theorem 4.2

Under Assumptions 1-10, for

Remark 12. Theorem 4.2 shows that our proposed estimator can consistently estimate strengths for all factors, not just for the strongest one as in BKP (2021). The intuition behind this consistency result is similar to that behind Proposition 4.1. Again, the key is to realize that the rotated loading matrix is able to preserve strength as up to the given threshold , and also that the errors induced by estimation are also uniformly dominated by .

5 The Determination of the Number of Factors

The determination of the number of factors has been of long-standing interest in the literature of factor models. Various selection criteria have been proposed, e.g., Bai and Ng (2002), Onatski (2010), Ahn and Horenstein (2013), and Wei and Chen (2020). As for consistent selection in weak factor models, Uematsu and Yamagata (2023a) show that the edge distribution (ED) estimator by Onatski (2010) is consistent, and Onatski (2015) proposes selecting the number of factors based on the approximations to the squared error of the least squares estimator of the common component under both strong and weak factors asymptotics. Freyaldenhoven (2022a) devises a statistic in combining both eigenvalues and eigenvectors of the covariance matrix, to enhance its discriminatory power in distinguishing factors stronger than a certain threshold, assuming that and grows proportionally. Guo et al. (2022) exploit a data-driven adaptive penalty of factor strength for information criteria, to select weak factors and meanwhile avoid overfitting.

In this paper, we propose determining the number of factors based on SVT, as discussed by Bai and Ng (2019) and Freyaldenhoven (2022a). The procedure is very simple and works in the same spirit as Bai and Ng (2002). To determine the number of factors in , we use the following estimator of ,

where is a consistent estimator of , is a constant independent of and , is a large bounded positive integer such that , and is the th diagonal element of being an diagonal matrix consisting of the largest eigenvalues of in decreasing order. As for in practice, we compute it similar to Bai and Ng (2002) as , where the superscript signifies the allowance of factors in the estimation.

Remark 13. To implement, we choose the value of via twice K-fold cross validation as proposed by Wei and Chen (2020). Specifically, for a given and the consequent estimator of , in step one we run a “leave one of folds out” (across columns of ) estimation by PC to obtain estimated loadings for all units, which are then sparsified by . In step two we further run a “leave one of folds out” (across rows of ) estimation based on the fold left over from step one, to obtain estimated factors. Lastly, we evaluate the performance of estimation by out-of-sample mean squared errors averaged over all possible folds, and choose the to minimize the average. One can refer to Wei and Chen (2020) for implementation details. In practice, we choose and find the results are very robust against various values of and .

Theorem 5.1

Under Assumptions 1-7,

Remark 14. Proving Theorem 5.1, detailed in the Appendix, is to check two conditions to hold in probability: (i) and (ii) Condition (i) is actually implied by Proposition 3.1. We prove condition (ii) by contradiction, and this relies on a sharper bound obtained under imposed by Assumption 4. This assumption is also needed for Bai and Ng (2002) in determining the number of factors via information criteria even in strong factor models.

Remark 15. The ED estimator proposed by Onatski (2010) is based on the fact that all the “systematic” eigenvalues diverge to infinity, whereas any finite number of the largest “idiosyncratic” eigenvalues cluster around a single point. Onatski (2010) determines the number of factors by separating the diverging eigenvalues with a wedge , and proves the consistency of the ED estimator only requiring that . However, the ED estimator hinges on the idiosyncratic terms being guassian, or independent cross-sectionally or over time in case of nonguassian, and is thus restrictive in applications with macroeconomics and finance. As for choosing , Onatski (2010) approximates the upper bound of eigenvalue differences by an OLS estimate which is then doubled to formulate . His final estimator of is obtained via iterations given . In contrast, our estimator of is more straightforward to use.

6 Monte Carlo Simulations

In this section, we study the finite sample performance of our proposed estimators for sparsity-induced weak factor models. It includes comparison of simple PC estimators with Lasso type estimators, estimation of number of factors, as well as factor strength.

6.1 The data generating process

We consider the following data generating process (DGP):

The simulated factors are correlated with each other with various degrees. We let be mutually uncorrelated for . To specify the factor loadings for each we first randomly select of and specify them as iid , and then set the rest of as zero.

For the vector we specify the (marginal) distribution of as the student- to allow for heavy tail. The cross sectional dependence across is admitted through the covariance matrix as follows. as a block-diagonal matrix with blocks located along the main diagonal. Each is assumed to be initially. We then randomly choose blocks among them and make them non-diagonal by setting . The design of cross sectional dependence follows Fan et al. (2015) except that the dependence is stronger here.

We have tried simulations with the number of factors and For we set while for we set . The number of simulations is 2000.

6.2 Simulation results

We first compare different methods to determine the number of factors with ours (WZ). The alternative selection rules range from the by Bai and Ng (2002, BN), Guo et al. (2022, GCT), Freyaldenhoven (2022b, FR), ED by Onatski (2010), and Ahn and Horenstein (2013, AH). is set to be 8 if needed. The root mean square error (RMSE) and bias of the estimated number of factors by each method are reported in Tables 1 and 2. It is obvious that GCT, FR and AH are all subject to overestimation of in the presence of weak factors. ED and BN are not very bad but they are outperformed by our proposed method, since they tend to over- and under-estimate , respectively. The ED estimator is not as effective as found previously in weak factor models, e.g., by Uematsu and Yamagata (2023a), implying that the ED performance may be sensitive to the choice of the wedge parameter , as remarked in Section 5. Our proposed estimator of factor numbers is outstanding against all alternatives at all sample sizes.

| RMSE | Bias | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| WZ | BN | GCT | FR | ED | AH | WZ | BN | GCT | FR | ED | AH | |||

| 100 | 100 | 0.273 | 0.673 | 0.939 | 1.962 | 0.400 | 1.998 | -0.059 | -0.443 | -0.882 | -1.943 | 0.030 | -1.998 | |

| 200 | 0.132 | 0.446 | 0.866 | 1.964 | 0.425 | 1.999 | -0.011 | -0.190 | -0.748 | -1.945 | 0.090 | -1.999 | ||

| 400 | 0.084 | 0.314 | 0.783 | 1.978 | 0.964 | 1.998 | -0.006 | -0.095 | -0.611 | -1.968 | 0.330 | -1.997 | ||

| 200 | 100 | 0.102 | 0.600 | 0.916 | 1.973 | 0.284 | 2.000 | -0.002 | -0.355 | -0.839 | -1.955 | 0.059 | -2.000 | |

| 200 | 0.055 | 0.241 | 0.739 | 1.952 | 0.354 | 2.000 | -0.001 | -0.056 | -0.543 | -1.909 | 0.075 | -2.000 | ||

| 400 | 0.000 | 0.120 | 0.445 | 1.952 | 0.448 | 1.999 | 0.000 | -0.010 | -0.180 | -1.909 | 0.091 | -1.998 | ||

| 400 | 100 | 0.081 | 0.687 | 0.932 | 1.946 | 0.244 | 2.000 | 0.004 | -0.468 | -0.870 | -1.895 | 0.058 | -2.000 | |

| 200 | 0.000 | 0.180 | 0.610 | 1.767 | 0.248 | 2.000 | 0.000 | -0.032 | -0.370 | -1.562 | 0.057 | -2.000 | ||

| 400 | 0.000 | 0.039 | 0.209 | 1.584 | 0.297 | 1.997 | 0.000 | 0.001 | -0.011 | -1.255 | 0.061 | -1.995 | ||

| RMSE | Bias | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| WZ | BN | GCT | FR | ED | AH | WZ | BN | GCT | FR | ED | AH | |||

| 100 | 100 | 0.273 | 0.742 | 2.708 | 3.975 | 0.455 | 4.000 | -0.060 | -0.499 | -2.654 | -3.962 | -0.032 | -4.000 | |

| 200 | 0.122 | 0.443 | 2.408 | 3.970 | 0.362 | 4.000 | -0.014 | -0.190 | -2.321 | -3.950 | 0.059 | -4.000 | ||

| 400 | 0.081 | 0.305 | 2.114 | 3.981 | 0.803 | 4.000 | -0.006 | -0.089 | -2.011 | -3.970 | 0.230 | -4.000 | ||

| 200 | 100 | 0.120 | 0.590 | 2.465 | 3.960 | 0.278 | 4.000 | -0.001 | -0.333 | -2.387 | -3.925 | 0.052 | -4.000 | |

| 200 | 0.059 | 0.228 | 1.843 | 3.909 | 0.254 | 4.000 | -0.001 | -0.046 | -1.749 | -3.822 | 0.049 | -4.000 | ||

| 400 | 0.032 | 0.095 | 1.371 | 3.911 | 0.257 | 3.998 | -0.001 | -0.007 | -1.289 | -3.826 | 0.041 | -3.996 | ||

| 400 | 100 | 0.087 | 0.640 | 2.299 | 3.800 | 0.239 | 4.000 | 0.006 | -0.404 | -2.220 | -3.610 | 0.052 | -4.000 | |

| 200 | 0.039 | 0.166 | 1.548 | 3.256 | 0.235 | 4.000 | 0.002 | -0.025 | -1.462 | -2.650 | 0.051 | -4.000 | ||

| 400 | 0.022 | 0.045 | 1.051 | 2.889 | 0.249 | 3.996 | 0.001 | 0.001 | -1.033 | -2.085 | 0.054 | -3.992 | ||

To study the finite sample performance of PC estimators under weak factor models, we compare PC regression with the sparse orthogonal factor regression (SOFAR) proposed by Uematsu and Yamagata (2023a, b), assuming the true number of factors to be known. Based on Lasso penalization on factor loadings for sparsity, Uematsu and Yamagata develop the Adaptive (Ada) SOFAR estimator. They later improve the SOFAR estimator by introducing the Debiased (Deb) SOFAR estimator to recover its asymptotic normality. Furthermore, they address the multiple testing problem of loading sparsity and construct the Resparsifed (Res) SOFAR estimator to fulfill FDR control. Note that the various SOFAR estimators proposed by Uematsu and Yamagata result from penalized regression which targets sparsity explicitly. Thus it seems natural to suggest that one should be better off using their approaches to deal with weak factor models than using PC. However, as we have mentioned before, the simple PC estimators enjoy a nice property of automatic sparsity recognition, so that PC could even outperform the complicated SOFAR.

To measure the performance of factor and loading estimators, we follow Doz et al. (2012) to use the trace statistics:101010Uematsu and Yamagata (2023a) evaluate performance of estimators by the norm losses: and . Such norm losses are more relevant when the factors and loadings are identified up to column-wise sign indeterminacy, rather than just rotation indeterminacy, and additional restrictions are required, as we explain right below. We instead employ the trace statistics whose validity does not rely on such restrictions, and they demonstrate how effectively estimators of factors (loadings) span the same space as latent factors (loadings).

We also report the root mean squared errors in estimating the common component (RMSEC). All results are included in Tables 3 and 4. The Res estimator is under the FDR rate .111111We have calculated the Res estimator when , and the results are very close to reported here. It is interesting to see that the PC estimators of factors and common components are almost always better than any of SOFAR type estimators. Although the Resparsifed SOFAR estimator for outperforms PC under bigger sample sizes, the margin is small. Recall that the SOFAR estimator are constructed under the restriction on the true DGP that being diagonal and (or ), which implies that the rotation matrix will be asymptotically . However, the restriction is violated under our DGP with correlated underlying factors, which might account for the worse performance of SOFAR. In an additional experiment whose results are not reported here, we modify our DGP with factors being indeed independent, and find that the SOFAR estimators are much closer to or even outperforms the PC estimator in estimating factors evaluated by , though their are still bigger in general. Hence regression by PC seems a better choice given its robustness and easy implementation.121212The estimators obtained via rotation suggested by Freyaldenhoven (2022b) render exactly the same results as PC in Tables 3 and 4, as the trace statistics and estimators for common components are rotation-invariant.

| PC | Ada | Deb | Res | PC | Ada | Deb | Res | PC | Ada | Deb | Res | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 0.924 | 0.898 | 0.909 | 0.909 | 0.718 | 0.622 | 0.709 | 0.713 | 0.973 | 1.020 | 1.005 | 1.005 | ||

| 200 | 0.936 | 0.918 | 0.924 | 0.924 | 0.786 | 0.720 | 0.783 | 0.788 | 0.953 | 0.988 | 0.967 | 0.967 | |||

| 400 | 0.943 | 0.935 | 0.938 | 0.938 | 0.830 | 0.806 | 0.833 | 0.837 | 0.948 | 0.970 | 0.958 | 0.957 | |||

| 200 | 100 | 0.955 | 0.934 | 0.942 | 0.942 | 0.745 | 0.647 | 0.765 | 0.786 | 0.886 | 0.941 | 0.894 | 0.893 | ||

| 200 | 0.964 | 0.953 | 0.957 | 0.957 | 0.811 | 0.752 | 0.826 | 0.841 | 0.881 | 0.910 | 0.879 | 0.879 | |||

| 400 | 0.969 | 0.964 | 0.966 | 0.966 | 0.852 | 0.838 | 0.861 | 0.871 | 0.872 | 0.892 | 0.877 | 0.877 | |||

| 400 | 100 | 0.969 | 0.951 | 0.956 | 0.956 | 0.750 | 0.660 | 0.767 | 0.803 | 0.813 | 0.866 | 0.820 | 0.818 | ||

| 200 | 0.976 | 0.966 | 0.970 | 0.970 | 0.816 | 0.764 | 0.828 | 0.853 | 0.806 | 0.844 | 0.812 | 0.812 | |||

| 400 | 0.980 | 0.975 | 0.977 | 0.977 | 0.858 | 0.846 | 0.864 | 0.879 | 0.802 | 0.822 | 0.805 | 0.804 | |||

| PC | Ada | Deb | Res | PC | Ada | Deb | Res | PC | Ada | Deb | Res | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 0.946 | 0.919 | 0.922 | 0.922 | 0.774 | 0.685 | 0.769 | 0.766 | 1.612 | 1.653 | 1.620 | 1.622 | ||

| 200 | 0.953 | 0.938 | 0.941 | 0.941 | 0.820 | 0.761 | 0.818 | 0.817 | 1.599 | 1.633 | 1.610 | 1.611 | |||

| 400 | 0.956 | 0.948 | 0.950 | 0.950 | 0.844 | 0.814 | 0.845 | 0.845 | 1.594 | 1.615 | 1.603 | 1.603 | |||

| 200 | 100 | 0.969 | 0.947 | 0.949 | 0.949 | 0.794 | 0.699 | 0.796 | 0.800 | 1.500 | 1.574 | 1.527 | 1.529 | ||

| 200 | 0.973 | 0.960 | 0.963 | 0.963 | 0.837 | 0.777 | 0.839 | 0.843 | 1.496 | 1.541 | 1.513 | 1.514 | |||

| 400 | 0.976 | 0.969 | 0.971 | 0.971 | 0.860 | 0.829 | 0.862 | 0.864 | 1.497 | 1.516 | 1.500 | 1.501 | |||

| 400 | 100 | 0.980 | 0.961 | 0.963 | 0.963 | 0.798 | 0.704 | 0.804 | 0.816 | 1.438 | 1.497 | 1.444 | 1.446 | ||

| 200 | 0.983 | 0.972 | 0.974 | 0.974 | 0.841 | 0.780 | 0.844 | 0.852 | 1.430 | 1.467 | 1.434 | 1.435 | |||

| 400 | 0.985 | 0.979 | 0.980 | 0.980 | 0.866 | 0.833 | 0.867 | 0.872 | 1.425 | 1.447 | 1.428 | 1.429 | |||

We further investigate the estimated factor strength by various methods in Tables 5 and 6. All estimates become less accurate as the true strength degree decreases, as expected. It is admitted that our proposed strength estimate (PC+Screening) suffers more of overestimation with fairly weak factors, e.g., those with . Otherwise, our estimate is comparable to, and sometimes even better than, those from SOFAR which is designed deliberately for sparsity recovery, especially for strength . The message here again delivers the usefulness of our factor strength estimator, which works reasonably well while avoids involving heavy computation as in SOFAR. Moreover, we find that SOFAR tends to underestimate the number of factors in our simulation, and hence the relative advantage of our estimate is conservative as we assume is known here.

| RMSE | Bias | |||||||

|---|---|---|---|---|---|---|---|---|

| Panel A: PC+Screening | ||||||||

| 100 | 100 | 0.014 | 0.047 | 0.138 | 0.000 | 0.006 | 0.100 | |

| 200 | 0.014 | 0.048 | 0.169 | 0.002 | 0.003 | 0.073 | ||

| 400 | 0.014 | 0.049 | 0.208 | 0.003 | 0.007 | 0.048 | ||

| 200 | 100 | 0.010 | 0.048 | 0.126 | 0.002 | 0.028 | 0.111 | |

| 200 | 0.009 | 0.045 | 0.138 | 0.002 | 0.023 | 0.091 | ||

| 400 | 0.009 | 0.045 | 0.166 | 0.004 | 0.026 | 0.075 | ||

| 400 | 100 | 0.007 | 0.053 | 0.114 | 0.002 | 0.044 | 0.101 | |

| 200 | 0.006 | 0.048 | 0.103 | 0.002 | 0.040 | 0.079 | ||

| 400 | 0.006 | 0.052 | 0.115 | 0.003 | 0.042 | 0.065 | ||

| Panel B: SOFAR_Debiased | ||||||||

| 100 | 100 | 0.017 | 0.094 | 0.085 | 0.004 | -0.060 | -0.019 | |

| 200 | 0.023 | 0.065 | 0.106 | 0.019 | 0.028 | 0.067 | ||

| 400 | 0.030 | 0.103 | 0.162 | 0.028 | 0.096 | 0.146 | ||

| 200 | 100 | 0.012 | 0.095 | 0.059 | 0.000 | -0.071 | -0.021 | |

| 200 | 0.017 | 0.052 | 0.084 | 0.014 | 0.025 | 0.062 | ||

| 400 | 0.025 | 0.095 | 0.148 | 0.024 | 0.091 | 0.138 | ||

| 400 | 100 | 0.010 | 0.102 | 0.050 | -0.004 | -0.085 | -0.033 | |

| 200 | 0.013 | 0.043 | 0.054 | 0.011 | 0.023 | 0.036 | ||

| 400 | 0.020 | 0.088 | 0.114 | 0.019 | 0.086 | 0.105 | ||

| Panel C: SOFAR_Resparsified | ||||||||

| 100 | 100 | 0.024 | 0.067 | 0.095 | 0.020 | 0.044 | 0.064 | |

| 200 | 0.030 | 0.103 | 0.130 | 0.028 | 0.095 | 0.106 | ||

| 400 | 0.036 | 0.137 | 0.179 | 0.035 | 0.135 | 0.164 | ||

| 200 | 100 | 0.017 | 0.062 | 0.096 | 0.015 | 0.057 | 0.085 | |

| 200 | 0.025 | 0.099 | 0.129 | 0.024 | 0.098 | 0.121 | ||

| 400 | 0.031 | 0.130 | 0.162 | 0.031 | 0.129 | 0.157 | ||

| 400 | 100 | 0.013 | 0.057 | 0.090 | 0.012 | 0.054 | 0.081 | |

| 200 | 0.021 | 0.093 | 0.104 | 0.020 | 0.092 | 0.098 | ||

| 400 | 0.027 | 0.123 | 0.140 | 0.026 | 0.123 | 0.136 | ||

| RMSE | Bias | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Panel A: PC+Screening | ||||||||||||

| 100 | 100 | 0.036 | 0.045 | 0.041 | 0.076 | 0.156 | -0.034 | -0.035 | 0.020 | 0.050 | 0.111 | |

| 200 | 0.034 | 0.043 | 0.043 | 0.076 | 0.187 | -0.033 | -0.034 | 0.021 | 0.047 | 0.081 | ||

| 400 | 0.033 | 0.040 | 0.043 | 0.078 | 0.223 | -0.032 | -0.030 | 0.023 | 0.045 | 0.058 | ||

| 200 | 100 | 0.031 | 0.032 | 0.047 | 0.083 | 0.139 | -0.030 | -0.023 | 0.035 | 0.065 | 0.115 | |

| 200 | 0.030 | 0.030 | 0.047 | 0.076 | 0.159 | -0.029 | -0.021 | 0.035 | 0.052 | 0.095 | ||

| 400 | 0.029 | 0.027 | 0.049 | 0.076 | 0.172 | -0.028 | -0.018 | 0.037 | 0.053 | 0.079 | ||

| 400 | 100 | 0.027 | 0.020 | 0.053 | 0.089 | 0.117 | -0.027 | -0.009 | 0.045 | 0.077 | 0.101 | |

| 200 | 0.026 | 0.018 | 0.052 | 0.084 | 0.107 | -0.026 | -0.008 | 0.042 | 0.070 | 0.065 | ||

| 400 | 0.025 | 0.015 | 0.053 | 0.082 | 0.124 | -0.025 | -0.006 | 0.044 | 0.067 | 0.051 | ||

| Panel B: SOFAR_Debiased | ||||||||||||

| 100 | 100 | 0.029 | 0.056 | 0.045 | 0.055 | 0.062 | -0.027 | -0.045 | -0.009 | 0.003 | 0.021 | |

| 200 | 0.020 | 0.024 | 0.061 | 0.089 | 0.106 | -0.019 | 0.000 | 0.050 | 0.077 | 0.088 | ||

| 400 | 0.015 | 0.037 | 0.097 | 0.142 | 0.157 | -0.013 | 0.033 | 0.093 | 0.136 | 0.144 | ||

| 200 | 100 | 0.027 | 0.055 | 0.041 | 0.046 | 0.046 | -0.026 | -0.047 | -0.013 | -0.016 | 0.018 | |

| 200 | 0.019 | 0.020 | 0.059 | 0.070 | 0.089 | -0.018 | 0.002 | 0.048 | 0.058 | 0.076 | ||

| 400 | 0.013 | 0.037 | 0.097 | 0.127 | 0.136 | -0.013 | 0.035 | 0.094 | 0.123 | 0.127 | ||

| 400 | 100 | 0.027 | 0.053 | 0.039 | 0.045 | 0.031 | -0.026 | -0.048 | -0.023 | -0.031 | -0.002 | |

| 200 | 0.018 | 0.017 | 0.051 | 0.051 | 0.061 | -0.017 | 0.002 | 0.041 | 0.040 | 0.046 | ||

| 400 | 0.012 | 0.039 | 0.095 | 0.107 | 0.103 | -0.012 | 0.037 | 0.092 | 0.103 | 0.095 | ||

| Panel C: SOFAR_Resparsified | ||||||||||||

| 100 | 100 | 0.024 | 0.021 | 0.053 | 0.092 | 0.100 | -0.023 | 0.003 | 0.043 | 0.080 | 0.084 | |

| 200 | 0.017 | 0.036 | 0.087 | 0.136 | 0.135 | -0.016 | 0.033 | 0.082 | 0.130 | 0.122 | ||

| 400 | 0.012 | 0.056 | 0.121 | 0.181 | 0.179 | -0.011 | 0.055 | 0.119 | 0.178 | 0.168 | ||

| 200 | 100 | 0.022 | 0.018 | 0.048 | 0.081 | 0.098 | -0.022 | 0.010 | 0.040 | 0.074 | 0.092 | |

| 200 | 0.016 | 0.039 | 0.076 | 0.116 | 0.115 | -0.015 | 0.038 | 0.071 | 0.111 | 0.110 | ||

| 400 | 0.011 | 0.058 | 0.111 | 0.163 | 0.153 | -0.011 | 0.058 | 0.108 | 0.160 | 0.148 | ||

| 400 | 100 | 0.021 | 0.019 | 0.041 | 0.068 | 0.087 | -0.021 | 0.016 | 0.034 | 0.063 | 0.085 | |

| 200 | 0.015 | 0.042 | 0.066 | 0.095 | 0.098 | -0.014 | 0.041 | 0.062 | 0.092 | 0.095 | ||

| 400 | 0.010 | 0.060 | 0.097 | 0.139 | 0.123 | -0.010 | 0.059 | 0.095 | 0.137 | 0.121 | ||

7 Empirical Application

We apply our approach to explore potential weak factors on macroeconomic indicators. We use data from the FRED-QD as a quarterly database for macroeconomic research (McCracken and Ng, 2021). The original data set consists of 248 quarterly frequency series dating back to 1959:Q2. By disregarding series with missing observations, we end up with series. The series are classified into 13 groups: NIPA; Industrial Production; Employment and Unemployment; Housing; Inventories, Orders, and Sales; Prices; Earnings and Productivity; Interest Rates; Money and Credit; Household Balance Sheets; Exchange Rates; Stock Markets; and Non-Household Balance Sheets.131313The original FRED-QD data have one additional group named “Other”, containing only two series. However, both series are dropped due to missing observations, leaving us 13 groups in use.

For each of the series used in our sample, after having made the decision that the series should be managed in levels or log-levels, the transformation codes are first and second differences based on whether the series is , ), or tested and suggested by McCracken and Ng (2021). Due to the transformation, two initial observations are dropped so each series starts from 1959: actually. We also normalize each series to have zero mean and unit variance.

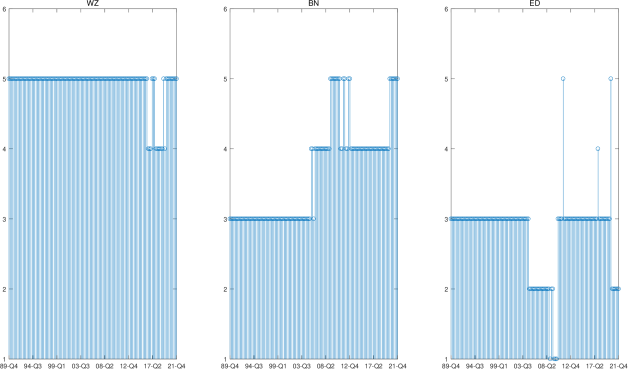

We depict the numbers of weak factors estimated by WZ, BN () and ED in Figure 3. The estimation is implemented under a rolling window scheme with length fixed at 120. The time on the x-axis denotes the right end point of the window interval. By WZ, the large panel is with five factors in most of the time considered here. There are a few windows taking four factors, in which BN also reports the same number. On the other hand, BN results in only three factors for the first half of rolling windows. For the second half, BN finds five factors in only a few window intervals. Onatski (2010) suggests that the ED method is expected to detect present weak factors. However, the result does not seem to agree with this: ED outputs three factors most of time, and the number may drop to two or even one at times. There are only three times when ED reports estimated factor numbers bigger than three.

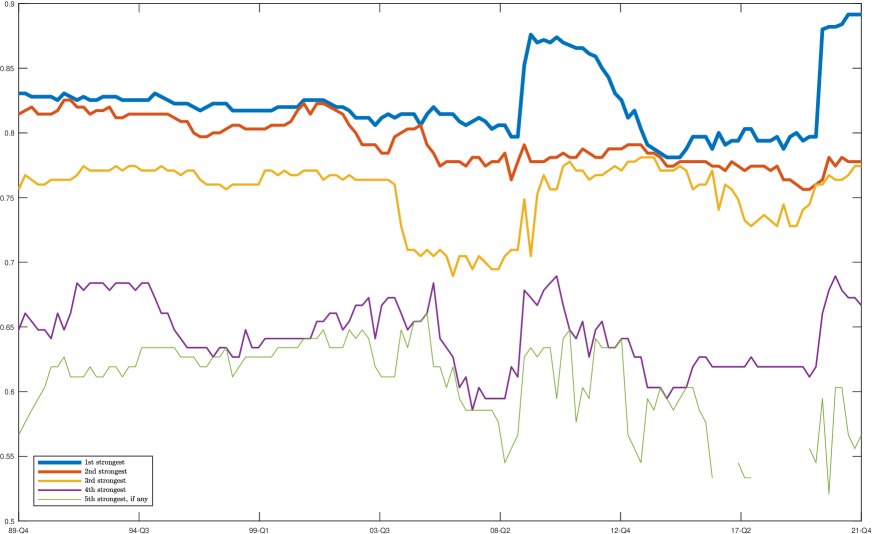

To have an idea of estimated factor strength and its dynamic, for each of our identified weak factors we further draw its associated factor strength over rolling windows in Figure 4 in a fashion similar to that in Figure 3. For most of window intervals ending from : to :, we have five weak factors. Figure 4 demonstrates a clear sparsity structure of latent factors. The first two strongest factors seem to have very close strength around 0.8 most of the time, although may spike to being close to 0.9 a few times. ranges from 0.7 to 0.8. fluctuates between 0.6 to 0.7, and interestingly it seems to spike simultaneously with , while reach bottom simultaneously with . is around 0.6 and moves close to up to 2014. However, drops even to 0 (a reduced factor) during the last 6 years.

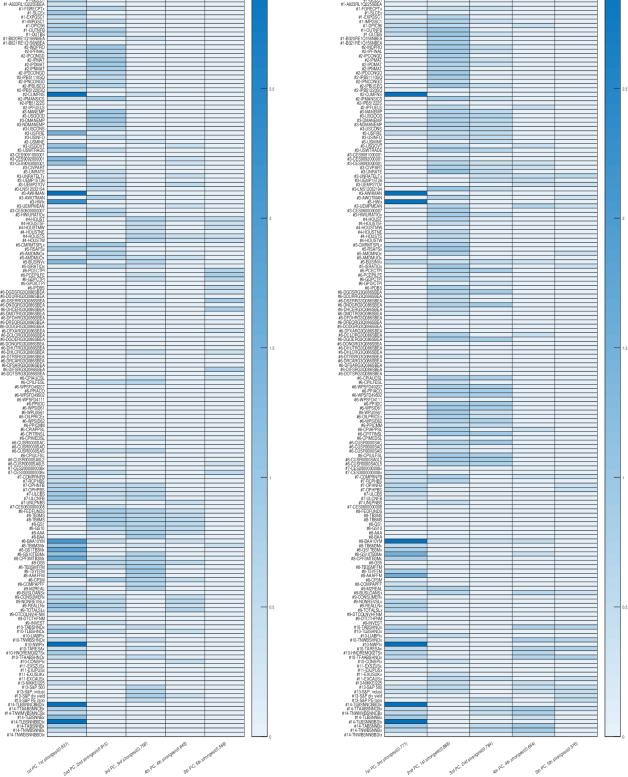

We are also interested in factor pervasiveness in the cross sectional dimension, that is, what are those specific series exposed to each weak factor and the relative influence each factor exerts over space. We can infer the degree of influence roughly by looking at the sparsity of over , given the implication by Proposition 4.1. We represent distribution of via a heat map of Figure 5. We consider two subperiods of roughly the same length: 1959:-1989: and 1989:-2021:. For each subperiod, we detect 5 weak factors. Each row () represents a series and we add its associated group number () in front of its name. Each column () represents a principle component extracted as a latent factor, and we also signify its rank by factor strength. In particular, the estimated factor strengths are 0.831, 0.815, 0.756, 0.648, and 0.566 for 1959:-1989:, and 0.888, 0.784, 0.771, 0.654, 0.576 for 1989:-2021:, as put in the parenthesis. The darkness of each cell indicates the absolute value of . Given that mostly across and , we right censor at 3 to obtain a sharper visualization of the heat map.

Some interesting results are the following. While the top two factor strengths are close during the first subperiod, they move farther away from each other during the second subperiod. The rest of three factor strengths are fairly stable over the two subperiods. The 1st PC extracted as a factor is not necessarily the strongest one: it ranks the 3rd by the number of influenced series on the second subperiod. The 2nd PC ranks 2nd in strength in the first subperiod, yet rises to the 1st in strength in the second subperiod, as it is loaded by many new series most of which belong to group 6 (Prices). Meanwhile, the 3rd PC also gains additional influence, mostly from groups 1, 2 and 3 (NIPA; Industrial Production; Employment and Unemployment), giving rise to its incremental strength and rank enhancement, although it loses influence on a few series belonging to groups 8 (Interest Rates) and 10 (Household Balance Sheets). It may be also worth noticing that while some series are not influenced by any weak factors in subperiod 1, e.g., many of those from group 6, they start to load on some factors in subperiod 2.

8 Conclusion

This paper proposes a novel approach to deal with weak latent factor models with sparse factor loadings. It reveals an interesting and fundamental fact that the PC estimators can preserve the sparsity in estimated factor loadings for sparsity-induced weak factor models. This fact facilitates the derivation of asymptotic properties of PC estimators, enables us to recover the sparsity of loadings, and estimate the strengths of each factor. In addition, the determination of the number of factors in weak factor models is also investigated. The numerical studies confirm that our proposed approach works reasonably well in finite sample, and an empirical application to FRED-QD data set shows that our method is useful to detect factor strengths, loading sparsity and their dynamics.

Our estimators of weak factor models belong to unsupervised PCA. Conceptually, one could think of applying supervised PCA (e.g., Huang et al., 2022) to weak factor models and obtain more efficient results for estimation and inference. We agree that supervision would further improve the performance of our proposed estimators by better exploiting information available, and yet also raise up additional complexity. So we leave it to future research.

References

-

Abadir, K. and Magnus, J. (2005) Matrix Algebra. Cambridge University Press.

-

Ahn, S.C. and Horenstein, A.R. (2013) Eigenvalue ratio test for the number of factors. Econometrica, 81(3), 1203–1227.

-

Ando, T. and Bai, J. (2017) Clustering Huge Number of Financial Time Series: A Panel Data Approach With High-Dimensional Predictors and Factor Structures. Journal of the American Statistical Association, 112(519), 1182–1198.

-

Bai, J. (2003) Inferential theory for factor models of large dimensions. Econometrica, 71(1), 135–171.

-

Bai, J. and Ng, S. (2002) Determining the number of factors in approximate factor models. Econometrica, 70(1), 191–221.

-

Bai, J., and Ng, S. (2006). Confidence intervals for diffusion index forecasts and inference for factor-augmented regressions. Econometrica, 74(4), 1133-1150.

-

Bai, J. and Ng, S. (2019) Rank regularized estimation of approximate factor models. Journal of Econometrics, 212(1), 78–96.

-

Bai, J. and Ng, S. (2023) Approximate factor models with weaker loadings. Forthcoming at Journal of Econometrics.

-

Bailey, N., Kapetanios, G., and Pesaran, M.H. (2021) Measurement of factor strength: Theory and practice. Journal of Applied Econometrics, 36(5), 587–613.

-

Chao J.C., Liu, Y., and Swanson, N.R. (2022) Consistent factor estimation and forecasting in factor-augmented VAR models. Working Paper, Maryland University.

-

Chao J.C. and Swanson, N.R. (2022) Selecting the relevant variables for factor estimation in FAVAR models. Working Paper, Maryland University.

-

Choi, I., Lin, R., and Shin, Y. (2023) Canonical correlation-based model selection for the multilevel factors. Journal of Econometrics, 233(1), 22-44.

-

Doz, C., Giannone, D., and Reichlin, L. (2012) A quasi-maximum likelihood approach for large, approximate dynamic factor models. The Review of Economics and Statistics, 94(4), 1014–1024.

-

Despois, T. and Doz, C. (2022). Identifying and interpreting the factors in factor models via sparsity: Different approaches. Forthcoming at Journal of Applied Econometrics.

-

Fan, J., Liao, Y., and Mincheva, M. (2011) High-dimensional covariance matrix estimation in approximate factor models. Annals of Statistics, 39(6), 3320–3356.

-

Fan, J., Liao, Y., and Yao, J. (2015) Power enhancement in high-dimensional cross sectional tests. Econometrica, 83(4), 1497–1541.

-

Freyaldenhoven, S. (2022a) Factor models with local factors determining the number of relevant factors. Journal of Econometrics, 229(1), 80–102.

-

Freyaldenhoven, S. (2022b) Identification through sparsity in factor models: The -rotation criterion. Working Paper, Federal Reserve Bank of Philadelphia.

-

Giglio, S. and Xiu, D. (2021) Asset pricing with omitted factors. Journal of Political Economy, 129(7), 1947–1990.

-

Giglio, S., Xiu, D., and Zhang, D. (2022a) Test assets and weak factors. Working Paper, NBER.

-

Giglio, S., Xiu, D., and Zhang, D. (2022b) Prediction when factors are weak. Working Paper, NBER.

-

Guo, X., Chen, Y., and Tang, C. Y. (2023) Information criteria for latent factor models: A study on factor pervasiveness and adaptivity. Journal of Econometrics, 233(1), 237-250.

-

Huang, D., Jiang, F., Li, K., Tong, G., and Zhou, G. (2022) Scaled PCA: A new approach to dimension reduction. Management Science, 68(3), 1678–1695.

-

Kristensen, J.T. (2017) Diffusion indexes with sparse loadings. Journal of Business & Economic Statistics 35(3), 434–451

-

Ludvigson, S.C. and Ng, S. (2009) Macro factors in bond risk premia. The Review of Financial Studies, 22(12), 5027-5067.

-

Ma, S., Linton, O., and Gao, J. (2021) Estimation and inference in semiparametric quantile factor models. Journal of Econometrics, 222(1), 295–323.

-

McCracken, M., and Ng, S. (2016). FRED-MD: A Monthly database for macroeconomic research. Journal of Business and Economic Statistics, 34(4), 574–589.

-

McCracken, M., and Ng, S. (2021). FRED-QD: A quarterly database for macroeconomic research. Federal Reserve Bank of St. Louis Review, 103(1), 1–44.

-

Merlevede, F., Peligrad, M., and Rio, E., (2011) A Bernstein type inequality and moderate deviations for weakly dependent sequences. Probability Theory and Related Fields, 151, 435–474

-

Moon, H.R. and Weidner, M. (2017) Dynamic linear panel regression models with interactive fixed effects. Econometric Theory, 33(1), 158–195.

-

Onatski, A. (2010) Determining the number of factors from empirical distribution of eigenvalues. The Review of Economics and Statistics, 92(4), 1004–1016.

-

Onatski, A. (2012) Asymptotics of the principal components estimator of large factor models with weakly influential factors. Journal of Econometrics, 168(2), 244–258.

-

Onatski, A. (2015) Asymptotic analysis of the squared estimation error in misspecified factor models. Journal of Econometrics, 186(2), 388–406.

-

Pelger, M. and Xiong, R. (2022) Interpretable Sparse Proximate Factors for Large Dimensions. Journal of Business and Economic Statistic, 40(4), 1642–1664.

-

Rapach, D. and Zhou, G. (2021) Sparse macro factors. Working paper, Washington University in St. Louis.

-

Stock, J.H. and Watson, M.W. (2002) Macroeconomic forecasting using diffusion indexes. Journal of Business & Economic Statistics, 20(2), 147–162.

-

Su, L. and Wang, X. (2017) On time-varying factor models: Estimation and testing. Journal of Econometrics, 198(1), 84–101.

-

Uematsu, Y. and Yamagata, T. (2023a) Estimation of sparsity-induced weak factor models. Journal of Business & Economic Statistics, 41(1), 126–139.

-

Uematsu, Y. and Yamagata, T. (2023b) Inference in sparsity-induced weak factor models. Journal of Business & Economic Statistics, 41(1), 213–227.

-

Wei, J., and Chen, H. (2020) Determining the number of factors in approximate factor models by twice K-fold cross validation. Economics Letters, 191, 109149.

APPENDIX

(Online)

The appendix provides formal proofs of main results in Sections 3-5 as well as auxiliary lemmas. We will use the fact that over several places in our proofs.

Appendix A Proofs of the main results in Section 3

To start with, we present several useful lemmas which will be used frequently in the proofs of main results. Their proofs can be found in Section D.

Lemma A.1

Under Assumptions 1-5, is a full rank (block) lower triangular matrix, and

Lemma A.2

Under Assumptions 1-5,

Lemma A.3

Under Assumptions 1-5,

Lemma A.4

Under Assumptions 1-5, the matrix is of full rank in probability.

Next we provide the proofs for the main results on PC estimator.

Proof of Proposition 3.1. Given we get

Multiplying both sides by ,

Note that the Frobenius norm of the second and third terms on the RHS is as

This implies that

For the fourth term,

Hence, the eigenvalues of are equal to the eigenvalues of in probability. Given that the eigenvalues of matrix and those of are identical, the eigenvalue of are determined in probability by

By Assumptions 1-2, and are both converging to p.d. matrices. It follows that the th eigenvalue of

Thus,

Proof of Proposition 3.2. For the so defined recall that we have already shown in proving Lemma A.4 that (a) is of full rank in probability, and (b) . Also recall that , ,141414Recall that iff . and . Hence for to hold with the asymptotic properties (a) and (b) just mentioned above, the matrix must be such that

This clearly demonstrates that matrix is a (block) lower triangular matrix in probability. Specifically, for such that it must be that Moreover, since is also of full rank of asymptotically as proved in Lemma A.4, we also have that . Therefore, is a non-strictly (block) lower triangular matrix. Noticing that we are done.

Proof of Proposition 3.3. Note that

This implies

Note that Also, Together with Lemma A.2 and Proposition 3.1, it leads to that

Proof of Proposition 3.4. First, note that

Then let

Note

By Assumption 2, By Lemma A.1, So,

Next for so

Given that by Proposition 3.3, we have

Lastly for

Given Assumption 5 Also, it’s easy to see So it follows that

| (A.1) |

Meanwhile, as implied by Assumption 3 (vii), and as proved in Lemma A.4,

So we have

Proof of Lemma 3.5. First, note that from we have That is,

Thus, multiplying on both sides of the above equation leads to

which gives rise to

It is easy to show that The same result also holds for Meanwhile,

So it follows that

| (A.2) |

implying that

Second, notice that (A.2) also implies that

Third, recall by definition, Therefore, we have

So it is followed by

where We further note that It is followed by

The results above imply that Again, recall the definitions that and , together with proved previously, we come to that

Fourth, notice immediately that , and we post-multiply on both sides of the equation, making use of , to get that

Lastly, to deal with , we again start by definition

Now, if we pre-multiply on both sides, we get

where

and the third equality is by Theorem 3.4, Lemma A.1 and Assumption 3 (v). It follows that

Putting things together, we have shown (i) (ii) (iii) (iv) In all, we conclude that

Proof of Proposition 3.6. Now we have

The second last equality is due to Propositions 3.3, 3.4, and Lemma 3.5. The last equality is due to Assumption 5.

Proof of Theorem 3.7. Let us start from the definition, Then by plugging we get That is, . So

We first consider the first term on the RHS of the above equation.

For we have a further decomposition as

For we first have by Assumption 3 (vi). Also recall that Hence,

For , by Lemma A.3,

For ,

Turning to given that and it follows that Therefore,

as by the assumption of and

We next show that by showing for First,

where we have used and again. Second,

by Assumption 7. Third,

So we have come to that

| (A.3) |

As for the term given Assumption 8, we come to that .

Here it may be interesting to investigate the matrix . Note that Also recall that is a (block) upper triangular matrix (in probability) such that

and for It then follows that Hence,

So obviously, is an asymptotically (block) diagonal matrix with full rank.

Finally, we conclude that

Proof of Theorem 3.8. Recall that As for the second term,

The first term on the RHS is

where is first equality is by Lemma A.1 and the second equality is by Assumption 2 and 3(iii). So we have

Together with Assumption 8, we come to that Given Assumption 6(ii) and the proved result that we conclude that

Proof of Theorem 3.9. By definition of , we have the following decomposition:

For define and then

Notice that So,

Consider

Note that Also note that

where the last equality is due to and which has been proved as in (A.3) when proving 3.7. So it follows that

For

Given that we have shown (a) (b) and (c)

it then follows that

Lastly, under the weak dependence assumption over both and and are asymptotically independent. Therefore, by a similar argument in proving Theorem 3 of Bai (2003), we come to that

where and

Proof of Theorem 3.10. (1) We first prove the uniform convergence rate of . Recall

As for the second term,

For

Assumption 9 implies that for and thus by Lemma A.3 of Fan et al. (2011), there exists a such that

Now let us define and then

For is a full rank (block) lower triangular matrix by Lemma A.1. Then it follows that for the vector for Similarly, we have

and for by Assumption 3 (iii). Hence,

Next for

Given Assumption 9, there exists a such that

by Lemma B.1 of Fan et al. (2011). Hence,

Third, for

Now given that and

| (A.4) |

by Lemma A.3 of Fan et al. (2011), we come to

Putting things together, and by the previously proved result it follows that, for

given implied by Assumption 8.

(2) We next prove the uniform convergence rate of . From the linear expansion of

Our purpose is to show that and in the following. To this end, we first study

As for the term by Lemma A.2 of Fan et al. (2011), it satisfies the exponential tail condition given our Assumption 9, as well as the strong mixing condition with parameter . Hence we can apply Theorem 1 of Merlevede et al. (2011) to show

Meanwhile, by Assumption 3 (vi). Therefore

Meanwhile, given that and (A.4), we come to that