Robust Regulation of Firms’ Access to Consumer Data111I am deeply grateful from comments and suggestions provided by Piotr Dworczak, Yingni Guo, Alessandro Pavan and Harry Pei. All errors remain my own.

Abstract

I study how to regulate firms’ access to consumer data when the latter is used for price discrimination and the regulator faces non-Bayesian uncertainty about the correlation structure between data and willingness to pay, and hence about the way the monopolist will segment the market. I characterize all policies that are worst-case optimal when the regulator maximizes consumer surplus: the regulator allows the monopolist to access data if and only if the monopolist cannot use the database to identify a small group of consumers.

1 Introduction

Data markets allow firms to access information about consumers like never before. These data can be valuable for multiple reasons, a particular one is that it can be informative about a consumer’s willingness to pay, potentially leading to price discrimination and consequently affecting welfare and consumer surplus. Therefore, growing access to consumer data imposes new challenges for regulation.

In response to these challenges, recent consumer data privacy laws, such as the the General Data Protection Regulation (GDPR) in Europe, aim to facilitate efficient data sharing by granting consumers control over their data. While giving consumers control over sharing represents an important step towards protecting their privacy and possibly increasing their welfare333See Ali et al. (2022) and Pram (2021)., there are cases where it might be too complicated for consumers to comprehend how their data will be used or who will ultimately get it444The New York Times recently uncovered a partnership deal where Facebook granted access to consumer data to firms such as Spotify and Apple. This type of partnerships suggests how complicated it can be for consumers to fully understand where and how their data will ultimately be used. See more details at https://www.nytimes.com/2018/12/18/technology/facebook-privacy.html., as well as situations where firms may potentially access consumers’ information without their consent. For instance, data leaks or breaches555T-mobile recently reported a data breach that may have exposed 37 million customers. The data included customers’ names, billing addresses, emails and phone numbers. See more details at https://www.nytimes.com/2021/08/18/business/tmobile-data-breach.html. can expose consumer data to firms and data brokers, beyond consumers’ control. Then, a broader scope of regulation can be desirable to address these gaps.

Motivated by the search for additional regulatory interventions that protect consumers’ welfare, this paper examines an environment where a monopolist can access consumer data beyond consumers’ control or understanding. The data is correlated with consumers’ willingness to pay and the monopolist uses this additional information to offer different prices to different segments of the aggregate market.

I am particularly interested in the following questions: if a regulator maximizes consumer surplus and she can implement policies that restrict access to any type data, what class of data should she permit firms to access? Furthermore, identifying the correlation between data and willingness to pay relies on knowledge and information that the seller probably has, but the regulator might lack; therefore, what policies are optimal for the regulator when she is unsure of this correlation?

More formally, I analyze a model where a monopolist (he) sells a good to a unit mass of consumers. The monopolist can access a database that specifies for each consumer certain characteristics, and he knows the correlation between the characteristics and willingness to pay. Therefore, he uses the database to segment the market and carry out third-degree price discrimination. A regulator (she) cares about consumer surplus and has the power to ban the monopolist from accessing any database. She knows the marginal distribution over willingness to pay (aggregate market) and over characteristics, but she faces non-Bayesian uncertainty about the joint distribution between the two. To resolve this uncertainty she evaluates each database under the worst-case consumer surplus over all feasible joint distributions, and she allows the monopolist to access a database if the database is worst-case optimal.

My main result, Theorem 1, characterizes the set of worst-case optimal databases. A database is worst-case optimal if and only if the monopolist cannot use the database to identify a small group of consumers. In this context, consumers are considered part of the same group if they share a characteristic disclosed by the database, and the group is classified as small if the proportion of consumers belonging to the group is below a threshold determined by the distribution over willingness to pay or aggregate market.

Theorem 1 provides an economic explanation for why consumer privacy laws may find it necessary to prohibit access to data that reveals the race, ethnicity or sexual orientation of consumers, as small groups can be identified. Similarly, Theorem 1 suggests that a regulator should forbid access to data that is too granular (Corollary 1), e.g., it is easier for the monopolist to identify a small group of consumers if he has access to a database that lists the actual income of each consumer, instead of a database that pools or aggregates information by just showing the income bracket to which each consumer belongs.

Nonetheless, the regulator can also guarantee her worst-case optimal payoff by simply implementing a policy that prohibits access to data. If the monopolist cannot access consumer data, he will not be able to identify any small group of consumers and therefore the condition imposed by Theorem 1 is satisfied. However, as Börgers (2017), I refine the set of worst-case optimal policies by showing that no access to data is dominated by a database that does not identify a small group of consumers. Corollary 2 shows that if the monopolist has access to any database that does not identify a small group of consumers, then, under any feasible joint distribution between the consumers’ characteristics and willingness to pay—after the monopolist uses the database to offer different prices to different segments of the market—consumer surplus is weakly greater than when the monopolist has no access to data. Furthermore, Theorem 2 shows that under sufficient and necessary conditions on the aggregate market there exists some worst-case optimal database and feasible joint distribution under which consumer surplus is strictly greater.

2 Related Literature

This paper contributes to the literature on data markets recently surveyed by Bergemann and Bonatti (2019). Within this literature, I am particularly motivated by the insights from Bergemann et al. (2015).

Bergemann et al. (2015) characterize all combinations of consumer surplus, producer surplus and welfare that can emerge from third-degree price discrimination. This characterization shows that market outcomes can be quite heterogeneous when the monopolist has additional information about the market beyond the prior distribution. This paper then asks: if a regulator prioritizes consumer surplus, what additional information about the market should she permit the monopolist to access?

Ali et al. (2022), Pram (2021) and Vaidya (2023) also analyze the regulation of data markets. They explore what is the effect of giving consumers control over their data. Distinct from their work, I am interested in situations where the monopolist has access to data beyond consumers’ control or understanding. Furthermore, I study regulation using a non-Bayesian approach.

Methodologically, this paper is related to Lin and Liu (2022). They analyze a persuasion setting where the sender can credibly deviate to any disclosure policy that leaves the distribution over messages unchanged. In my setting, given the distribution over characteristics imposed by a database, the monopolist can credibly pick any market segmentation if it keeps such distribution unchanged. Nonetheless, the question and results of Lin and Liu (2022) are quite different. They are interested in whether a sender can persuade a receiver by using credible disclosure policies. They find that in many settings no informative disclosure policy is credible.

Another relevant strand of literature is mechanism and information design with worst-case and worst-regret objectives. Carroll (2017) explores correlation as a source of uncertainty in a screening mechanism with multidimensional types where the principal knows the marginal distribution, but is unsure of the joint. Guo and Shmaya (2019) study a regulator that has non-Bayesian uncertainty about the demand function and cost function faced by a monopolist. Finally, suppose the regulator applies the robust solution concept proposed by Dworczak and Pavan (2022). That is, she applies any conjecture she might have about the correlation between data and willingness to pay over the set of worst-case optimal databases. Theorem 2 implies that, no matter the conjecture, she “prefers” a worst-case optimal policy that grants access to data, as long as the database does not identify a small group of consumers, over one that bans access to data.

3 Model

A monopolist (he) sells a good to a unit mass of consumers, each of whom demands one unit. The monopolist faces constant marginal costs of production that I normalize to zero. The consumers privately observe their willingness to pay (valuation) for the good, which can take possible values, , with ; without loss of generality assume

A market is a distribution over the valuations, with the set of all markets being

where is the proportion of consumers who have valuation . I say that the price is optimal for market if the expected revenue from price satisfies

Throughout the analysis I fix and denote by the market faced by the monopolist. Denote by the highest price among all optimal prices for market , that is

I will refer to as the uniform monopoly price and I will assume that is strictly below the highest possible valuation, e.g., 666As it will be shown later (Lemma 3), the regulator disallows the monopolist to access a database if and only if there is some feasible market segmentation under which the database leads to a consumer surplus strictly below . If , then, and there is no way a database can lead to a consumer surplus strictly below . Therefore, the regulator allows the monopolist to access any type of data. To avoid this trivial case, assume . . Given this uniform monopoly price, the corresponding consumer surplus is given by

3.1 Data

A database specifies for each consumer a unique label from a finite set . I denote a database by , where is the proportion of consumers with label and . In other words, is the distribution over labels among consumers. To simplify the notation, throughout the analysis, I drop the dependence of many objects on , although the set of labels is not fixed. In particular, two different databases, and , may correspond to different sets of labels, and . The set of all possible databases is

includes all possible distributions with finite and full support. In particular, when , we have the only distribution in whose support is a singleton. I will denote this element by and it will represent the case when the monopolist does not obtain any data about consumers777See that is equivalent to a database revealing the same characteristic for all consumers. Thus, the monopolist does not get any valuable information about consumers and is therefore equivalent to no access to data..

Fix any , let be the set of labels specified by and be the joint distribution of valuations and labels, where is the proportion of consumers with valuation and label . This joint distribution, together with , leads to a segmentation of the aggregate market . Formally, a segmentation is a collection of conditional distributions , such that for all , and

where is the proportion of consumers with valuation conditional of having label . We can think of each as a sub-market (segment), each corresponding to a different label. Furthermore, all this sub-markets are a division of the aggregate market since

I will refer to as segment .

Example 1.

Suppose that and the market is . For this market the uniform monopoly price is equal to , and leads to a consumer surplus equivalent to . Assume that there is a database that specifies for each consumer their gender, thus , where stands for woman and for men. Furthermore, assume and that is such that we obtain the following market segmentation:

| Segment | ||||

|---|---|---|---|---|

| 0 | ||||

| 1 |

3.2 Value of Data

Given segmentation , an optimal pricing rule is a mapping , where is the price the monopolist sets for consumers in segment , and belongs to

Suppose that the monopolist can access , knows and he can set different prices at each segment . Then, with database , he will be able to match each consumer to their unique label and charge each of them a price specified by some optimal pricing rule. Note that since is not necessarily a singleton there can be multiple optimal pricing rules. For instance, if we get an optimal pricing rule where the monopolist breaks ties against consumers. I denote the consumer surplus obtained from such pricing rule by

3.3 Regulation

A regulator (she) cares about consumer surplus and she can ban the monopolist from accessing . I assume the regulator knows the aggregate market and the distribution over labels . However, she is unsure about the true joint distribution between valuations and labels. Thus, the regulator faces non-Bayesian uncertainty about the correlation structure between data and valuations; she evaluates by its worst-case consumer surplus over all possible joint distributions. Let be the set of all joint distributions that have marginals equal to and , respectively:

Then, is evaluated by

Note that the regulator not only considers the worst possible joint distribution for consumer surplus, but also an adversarial monopolist that picks the worst optimal pricing rule for consumers.

After evaluating by its worst-case consumer surplus, the regulator allows the monopolist to access if is a worst-case optimal database, where is a worst-case optimal database if it belongs to

4 Results

I start by presenting the main result of this paper:

Theorem 1 (Characterization of worst-case optimal databases).

is a worst-case optimal database if and only if for every label , the proportion of consumers that have label , , is strictly above , where

and .

Then, the regulator grants the monopolist access to if and only if the monopolist cannot use to identify a small group of consumers. In this context, consumers are part of the same group if they share the same label, and the group is considered small if the proportion of consumers belonging to the group is weakly lower than .

Furthermore, Theorem 1 implies that a database cannot be too granular in order to be worst-case optimal. Particularly, if we think of as a measure of the level of data granularity or the level of detail in a database, where a higher means higher granularity, then a regulator prefers not too much granularity. How much is too much granularity?

Corollary 1 (Granularity).

If , then there exists an such that , and therefore cannot be a worst-case optimal database.

Proof.

Follows from Theorem 1. ∎

I now proceed to show the three lemmas that imply Theorem 1.

Lemma 1.

For any database let

be the set of feasible market segmentations. Then, without loss of generality, the regulator can evaluate by its worst-case consumer surplus over the set of feasible market segmentations. That is,

Proof.

Pick any . Denote by the segmentation we get from , clearly . Equivalently, for any we can construct a joint distribution, , that leads to and . Furthermore, since consumer surplus is pinned down by , we can compute the worst-case consumer surplus over rather than over . ∎

Lemma 2.

The maximum worst-case consumer surplus is equal to , the consumer surplus obtained when the monopolist charges the uniform monopoly price . More precisely,

Proof.

For any database , for all is always a feasible segmentation. In other words, no correlation between consumers’ labels and willingness to pay is always possible. In that case, charging the uniform monopoly price in every segment is optimal, and therefore consumer surplus is equal to . Thus, is an upper bound on the worst-case consumer surplus. On the other hand, under —which recall represents no data—the only feasible consumer surplus is . ∎

A direct consequence of Lemma 2 is that the regulator will not grant the monopolist access to any database that leads to a worst-case consumer surplus strictly below . Lemma 3 shows the sufficient and necessary conditions under which we get such strict inequality.

Lemma 3.

A database leads to a worst-case consumer surplus strictly below if and only if there exists a label such that .

Proof.

See Appendix A. ∎

I provide some intuition for the if part of Lemma 3 using Example 1. Recall that in this example , , , and it is easy to check that . Suppose we have a database with two labels, , such that and , hence .

I construct a such that and . Note that this will lead to a consumer surplus strictly below . Why? A positive share of consumers that get the good pay 3 and the rest of them pay 2, while with the uniform monopoly price everyone pays 2.

An intuitive first approach to get is to let , which is feasible since is sufficiently small. However, feasibility also implies that and , thus and consumer surplus is actually strictly larger than . Hence, perfect correlation between having a high valuation and label does not work.

The idea then is to set such that a price of 3 is optimal and we can not further decrease and still get that a price of 3 is optimal. This achieved by what Bergemann et al. (2015) call an extreme market or a market where charging any price in the support of is optimal, which in this case is , and . Then we have and for sure . Why for sure ? Suppose that , then 1 is an optimal price in segment and is an optimal price in segment . On the other hand, 2 is an optimal price in segment , but is not optimal in segment . Therefore, 1 leads to strictly higher profits over 2 for the aggregate market , a contradiction. Finally, note that this is feasible as long as or equivalently as long as .

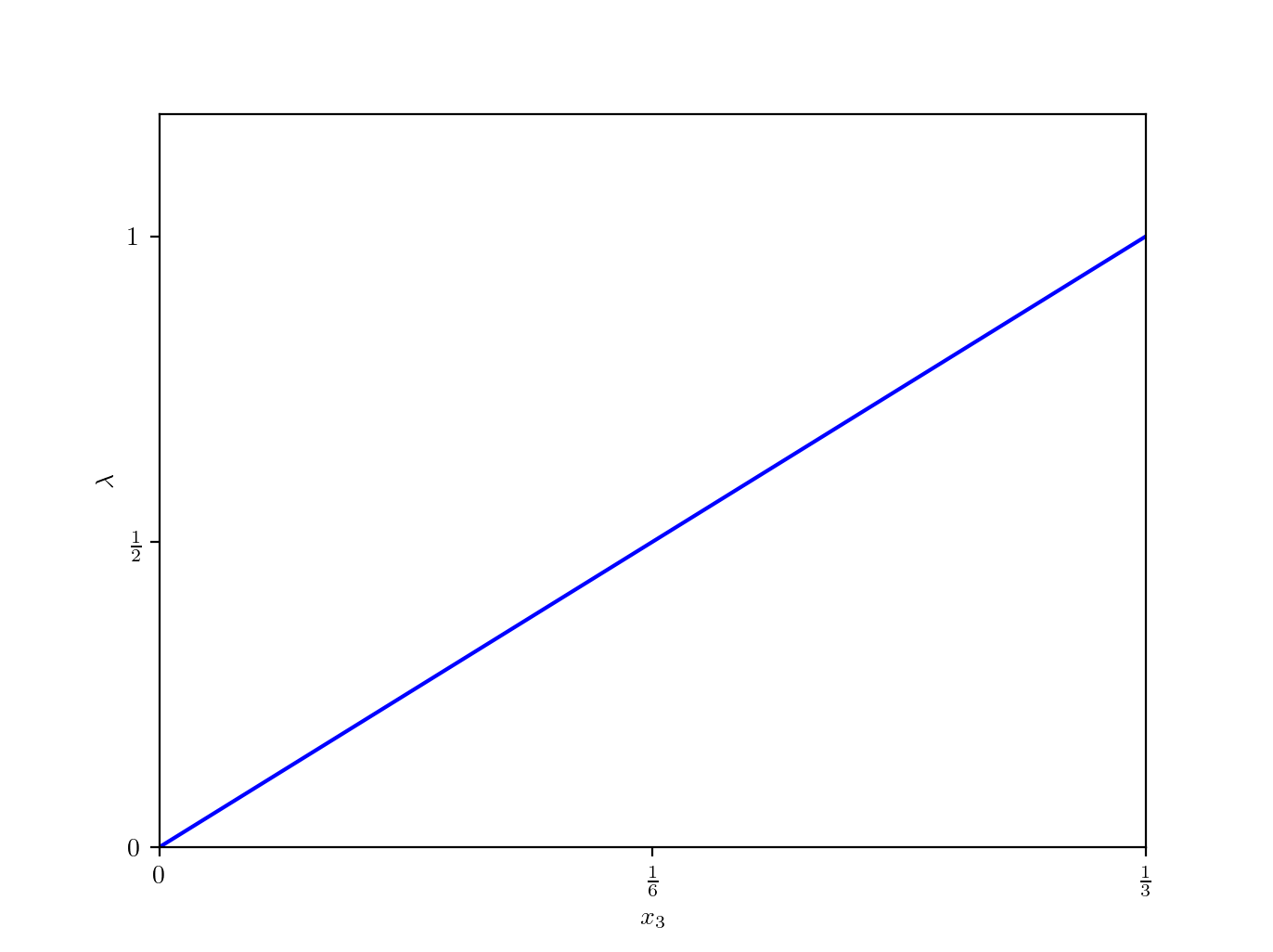

Figure 1 shows how varies when we perturb Example 1. Particularly, , moves between 0 and and . The figure shows that can be arbitrarily small and this occurs when decreases.

Nonetheless, note that satisfies all conditions of Theorem 1 and thus . Then, the regulator can guarantee her worst-case optimal payoff by implementing a policy that prohibits access to data—recall represents the case when the monopolist has no access to data. Therefore: Why the regulator should implement a policy that allows the monopolist to access a database as long as he cannot use the database to identify a small group of consumers, if she can simply ban all access to data and get her worst-case optimal payoff?

Similar to Börgers (2017) I refine the set of worst-case optimal databases, , by showing that under sufficient and necessary conditions on the aggregate market, there exists some that dominates .

Definition 1 (Domination).

Database dominates , if for all and for some , .

Corollary 2.

If , then for all .

Theorem 2.

Suppose , there exists an that dominates if and only if

Additionally, if it is also the case that

where , then any dominates .

Proof.

See Appendix B. ∎

To get some intuition for Theorem 2 see that, first of all, we need , otherwise is empty. Next, the condition imposed on is equivalent to

where is the index assigned to the uniform monopoly price . This condition is likely to be satisfied whenever decreases or when the share of consumers that have a valuation strictly lower than the uniform monopoly price goes up. This implies that for some worst-case optimal database we can construct a feasible market segmentation where one of its segments pools a high share of consumers with a valuation strictly below with an small enough share of consumers with a valuation weakly higher than such that the price is strictly below . Furthermore, since the database is worst-case optimal, for the other segments the price must be weakly lower than . Thus, consumer surplus is strictly higher than .

For instance, the aggregate market in Example 1 satisfies all conditions of Theorem 2. See that in this market the share of consumers with valuation 1 is high—if we increase such share by any positive number, 2 is no longer the uniform monopoly price—and therefore for any worst-case optimal database is “easy” to construct a feasible market segmentation where in one of the segments a price of 1 is optimal and in the other segments a price of 2 is optimal.

5 Conclusion

In this paper I analyzed how to regulate firms’ access to consumer data when the latter is used for third-degree price discrimination and the regulator faces non-Bayesian uncertainty about the correlation structure between data and willingness to pay, and hence about the way the monopolist will segment the market. The main result shows that preventing the monopolist from using consumer data is desirable if and only if the monopolist can use the database to identify a small group of consumers.

The main finding of my analysis has potential implications for consumer data privacy laws. For instance, such laws may deem it necessary to prohibit firms from acquiring data about consumers’ ethnicity, race, or sexual orientation, as small group of consumers can be identified. Additionally, privacy laws could consider imposing restrictions in the level of data granularity that firms can access. For example, by requiring data brokers to pool or aggregate information.

Appendix A Proof of Lemma 3

Proof.

If part: Suppose there is an such that . I construct a such that and for all . This then implies that . Let be any element that belongs to

Given , let be any element that belongs to

| (1) |

As it will be useful later, note that for all the following inequality holds:

| (2) |

To see why, towards a contradiction suppose not, then

where the strict inequality follows from the fact that is the highest optimal price and therefore for all . Now I construct using the following steps:

-

1.

Define as

where, throughout the proof, any sum that goes from index to is defined as zero. Let be the minimum index such that and satisfies

If or for all the above equality is not satisfied, set . Define as

If or stop and set for all . Otherwise, set for all and proceed to step 2.

-

2.

Let

for all . Denote by the minimum index such that

If for all the above equality is not satisfied, set . Define as

If or stop and set for all . Otherwise, set for all and proceed to step 3.

-

3.

Let

for all . Denote by the minimum index such that

If for all the above equality is not satisfied, set . Define as

If or stop and set for all . Otherwise, set for all and proceed to step 4.

Since there are finitely many indices between 1 and the above process is guaranteed to stop at some index . Furthermore, we already defined for all , so it only remains to define for . For that purpose let be given by

Then, set for all , and for all pick such that

Note that for all and

The above shows that . We now prove that . By construction, for all we have that

Moreover, if the above weak inequality is actually an equality. Then, the profits from are weakly higher over any strictly lower valuation and therefore . Now, I construct for all . Define

and for all let

Note that and for all . Then, for to belong in is enough to verify that for all , which is equivalent to checking that . By construction, this is true for all and . Therefore, we only have to check that it is also true for and . First we check is true for . Let be the smallest index such that

and if for all the above equality is not satisfied, set . See that

where the first inequality follows from the fact that and by Equation 1 :

and the second inequality follows from Equation 2, which implies that

I now show that for all . First note that

where the inequality follows once more from and Equation 1. Recall that and . Then, there must exist such that for all . This proves that . It only remains to show that . Towards a contradiction, suppose that and . This implies that

Furthermore, it can not be the case that , otherwise and would not be an optimal price for segment . Then , and since this implies that

which further implies that

but then combining both inequalities we get that

which implies implies is not an optimal price for aggregate market , a contradiction.

Only if part: Suppose that , then there must exist a and an such that . Let with . Then, for all the following inequality holds:

Furthermore, since it must be that for all . Using this and multiplying both sides of the above inequality by we get that

Since this is true for all , it immediately follows that

Moreover, given the above is true for some , it is also immediate that

∎

Appendix B Proof of Theorem 2

Proof.

If part: Suppose that

where and are defined as in the proof of Lemma 3 (Appendix A). Is easy to check that the above inequality implies that

Then, there exists an such that for some we have that

Let for all and for all set such that . Note that

Which implies that for segment , leads to strictly higher income relative to . We still have to check that . First, assume that . Denote by and for all let

This implies that . Furthermore, it can not be the case that for some we have that . Otherwise, by the only if part of the proof of Lemma 3 it will follow that . Then, and . Hence, .

If we have that , then for at least one we can reduce and get that , where is sufficiently small such that . This shows that dominates . Moreover, if also satisfies that

we get that

and for any there must be an such that

Only if part: Suppose that dominates . Then, there exists a such that . This implies that there must be an and a such that

Furthermore, since , we also get that

Manipulating the above inequality we get that

Recall also that , hence

which implies that

∎

References

- (1)

- Ali et al. (2022) Ali, S Nageeb, Greg Lewis, and Shoshana Vasserman, “Voluntary Disclosure and Personalized Pricing,” The Review of Economic Studies, 07 2022, 90 (2), 538–571.

- Bergemann and Bonatti (2019) Bergemann, Dirk and Alessandro Bonatti, “Markets for information: An introduction,” Annual Review of Economics, 2019, 11, 85–107.

- Bergemann et al. (2015) , Benjamin Brooks, and Stephen Morris, “The limits of price discrimination,” American Economic Review, 2015, 105 (3), 921–957.

- Börgers (2017) Börgers, Tilman, “(No) Foundations of dominant-strategy mechanisms: a comment on Chung and Ely (2007),” Review of Economic Design, 2017, 21 (2), 73–82.

- Carroll (2017) Carroll, Gabriel, “Robustness and separation in multidimensional screening,” Econometrica, 2017, 85 (2), 453–488.

- Dworczak and Pavan (2022) Dworczak, Piotr and Alessandro Pavan, “Preparing for the worst but hoping for the best: Robust (Bayesian) persuasion,” Econometrica, 2022, 90 (5), 2017–2051.

- Guo and Shmaya (2019) Guo, Yingni and Eran Shmaya, “Robust monopoly regulation,” arXiv preprint arXiv:1910.04260, 2019.

- Lin and Liu (2022) Lin, Xiao and Ce Liu, “Credible persuasion,” arXiv preprint arXiv:2205.03495, 2022.

- Pram (2021) Pram, Kym, “Disclosure, welfare and adverse selection,” Journal of Economic Theory, 2021, 197, 105327.

- Vaidya (2023) Vaidya, Udayian, “Regulating Disclosure: The Value of Discretion,” Working Paper, 2023.