Estimating the impact of supply chain network contagion on financial stability

Abstract

Realistic credit risk assessment, the estimation of losses from counterparty’s failure, is central for the financial stability. Credit risk models focus on the financial conditions of borrowers and only marginally consider other risks from the real economy, supply chains in particular. Recent pandemics, geopolitical instabilities, and natural disasters demonstrated that supply chain shocks do contribute to large financial losses. Based on a unique nation-wide micro-dataset, containing practically all supply chain relations of all Hungarian firms, together with their bank loans, we estimate how firm-failures affect the supply chain network, leading to potentially additional firm defaults and additional financial losses. Within a multi-layer network framework we define a financial systemic risk index (FSRI) for every firm, quantifying these expected financial losses caused by its own- and all the secondary defaulting loans caused by supply chain network (SCN) shock propagation. We find a small fraction of firms carrying substantial financial systemic risk, affecting up to of the banking system’s overall equity. These losses are predominantly caused by SCN contagion. For every bank we calculate the expected loss (EL), value at risk (VaR) and expected shortfall (ES), with and without accounting for SCN contagion. We find that SCN contagion amplifies the EL, VaR, and ES by a factor of , , and , respectively. These findings indicate that for a more complete picture of financial stability and realistic credit risk assessment, SCN contagion needs to be considered. This newly quantified contagion channel is of potential relevance for regulators’ future systemic risk assessments.

keywords:

supply chain networks , financial networks , contagion , stress testing , systemic risk , multi-layer networks1 Introduction

Credit risk (CR) assessment is central for banks to operate in an economically sustainable way. CR materialises when a counterparty is unable or unwilling to fulfil its contractual debt obligations. In 1988 the Basel Committee on Banking Supervision (BCBS) published the first Basel Accord (BCBS, ()) providing a set of minimum capital requirements that must be met by banks to guard against CR. These requirements have been refined also in the following accords Basel II (2004) (BCBS, ()) and Basel III (2010) (BCBS, ()), reflecting the importance of CR for financial stability. The regulatory path has been evolving towards a system where capital requirements are explicitly linked to the risk of activities undertaken by banks. This means that as perceived default risks increase, so do the risk-weights and the bank’s capital buffer. Therefore, for being able to properly determine adequate capital buffers and adjust their interest rates, it is essential for banks to have an in-depth knowledge of all sources of CR.

Recent crises like the COVID-19 pandemic, the conflict in Ukraine, and several natural disasters have impressively shown that the propagation of shocks along supply chain networks (SCNs) lead to large financial losses of firms, and as a consequence, also to their creditors. It was shown that shock propagation along supply chains can be dramatic, for example in the case of Hurricane “Katrina” (Hallegatte, 2008), the Japanese earthquake of 2011 (Carvalho et al., 2020; Inoue and Todo, 2019), natural disasters in the US(Barrot and Sauvagnat, 2016), the UK lockdowns during the COVID-19 crises (Pichler et al., 2022b), disruptions of natural gas supply (Pichler et al., 2022a), or failures of systemically important firms (Diem et al., 2022a). The COVID-19 crises led to substantial shock propagation effects along SCNs and affected almost every sector, including the especially vulnerable small and medium enterprises (SMEs) (Bartik et al., 2020). Banks only did not suffer extensive losses from non-performing loans during the pandemic by the virtue of enormous liquidity support measures, furlough schemes, and other measures imposed by governments and central banks (Milstein and Wessel, 2021; ECB, 2020). In the future, an accelerating climate crisis is likely to increase the frequency and magnitude of natural disasters, which will make the propagation of shocks along supply chains an even larger concern (Willner et al., 2018; Battiston et al., 2021).

To date, shock propagation through firm-level SCNs has not yet reached its ways into quantitative financial risk assessment of banks, or stress testing methodologies used by regulators; it has only recently been scarcely featured by research. Traditionally, credit risk models focus on the financial conditions of the borrowers, using their financial statements as the most relevant inputs. A rating assessment of borrowers usually involves variables derived from balance sheets, income statements, and cash flow statements. For example, according to the BCBS, the leverage ratio (total assets divided by total equity) has the strongest explanatory power, especially when combined with revenue, see BCBS, (). Credit rating models that are applied on these variables, are primarily based on classical statistical methods, such as logistic regression Cox (1958)111By now, machine learning and deep learning based credit risk models outperform classical ones in terms of accuracy (Shi et al., 2022). They can handle large alternative data sets, such as text- or graph data Hamilton (2020) including the extraction of relevant information from these. These approaches could be used to include SCN data. As discussed in the European Banking Authority report on big data and advanced analytics EBA (2020), there is an evident tendency in employing big data and advanced analytics (BDAA) into many aspects of the banking business, such as fraud detection or client interactions. There is also growing interest in the area of financial risk management. On the other side, there are still many concerns like the “biasness” or the fact that (BDAA) methods still largely remain “black boxes”. That is why regulators so far have been cautious of approving their usage for risk management.. Credit risk management evaluates information about suppliers and buyers in given markets or under specific economic conditions in, predominantly, qualitative ways (Gorgijevska and Gorgieva-Trajkovska, 2019; Moretto et al., 2019). The subjective analysis of clients’ supply chain exposures can complement existing quantitative credit ratings, but is limited to first-tier supplier-buyer relations and, hence, can not capture the complex structures of SCNs that transmit disruptions far beyond the first tier (Carvalho et al., 2020).

Research on network-based financial systemic risk (Boss et al., 2004; Battiston et al., 2012; Thurner and Poledna, 2013; Poledna et al., 2015, 2021; Diem et al., 2020; Feinstein et al., 2017; Gai and Kapadia, 2010; Thurner, 2022; Poledna et al., 2018), and macro prudential stress testing (Farmer et al., 2022; Cont and Schaanning, 2017; Glasserman and Young, 2016; Gauthier et al., 2012; Cont et al., 2010; Elsinger et al., 2006), primarily focuses on the nature of the propagation of shocks in financial networks, but does not include contagion effects along the SCNs, the back bone of the real economy. Further examples of this stream of literature include Buncic and Melecky (2013), Acharya et al. (2014), Levy-Carciente et al. (2015), Arnold et al. (2012), Borio et al. (2014), Vazquez et al. (2012). As pointed out in Battiston and Martinez-Jaramillo (2018), the literature connecting the real economy with the financial system is strongly under-researched. Herring and Schuermann (2022) and Potter and Schuermann (2020) emphasise that the framework of current stress testing should be broadened to include non-financial threats to financial stability, such as economic or climate shocks. Similarly, Farmer et al. (2021) highlights the need for so-called system-wide stress testing to account for relations between economic and financial systems. An earlier attempt of agent based approaches to linking the real economy to the financial system is found in Klimek et al. (2015). Several regulating bodies and institutions such as the BCBS BCBS, (), BCBS, (), BCBS, (), the Federal Reserve (FED) (Brunetti et al., 2021), and the European Central Bank (ECB) (ECB/ESRB, 2022) pointed out the significance of climate-related risk to financial stability and identified supply chains as one of the relevant risk transmission channels.

Due to a lack of granular data, so far it has been impossible to quantify exposures of financial systems to contagion in SCNs on the firm-level. On the industry level contributions in this direction were provided by Guth et al. (2020) where aggregated supply chain networks in the form of IO tables were used to assess the impact of supply chain disruptions in the context of the COVID-19 crises on the Austrian banking system. However, the use of aggregated industry-level production network data can cause substantial mis-estimations of production losses (Diem et al., 2023), showing the need for firm-level modelling approaches of supply chain shock propagation. Recently, the spreading of liquidity shortages on the production network (Huremovic et al., 2020; Demir et al., 2022) was explored, which can also generate feedback effects for the financial sector (Silva et al., 2018). The first works considering explicit interactions between the firm-level production network and the financial sector using granular network data for both systems are (Huremovic et al., 2020; Borsos and Mero, 2020), however, the framework is limited to shocks that originate in the financial sector.

Here we present a data-driven computational framework for estimating how the initial failure of firms spreads along the supply chain network (SCN) within a country, leading to potentially additional firm defaults. These spread to the financial system through additional firm-loan write-offs and equity losses for banks. Based on a nation-wide micro-dataset, containing all supply chain links of all Hungarian firms in combination with comprehensive credit registry data containing all commercial loans that firms obtained from banks, we are in the unique position to address the following two research questions. First, to what extent does systemic risk in the real economy — created by cascades of production failures in national SCNs — affect financial stability? And second, how is the credit risk exposure of banks — measured by expected loss, value at risk, and expected shortfall — amplified by contagion in these SCNs, or, equivalently, how much is credit risk underestimated by ignoring supply chain contagion? To answer these questions, we take two perspectives, a system-wide and one that is bank-specific. For the former, we introduce for every firm a financial systemic risk index (FSRI). FSRI quantifies the financial losses of the banking system, caused directly by the firm’s failure and indirectly from the resulting propagation of shocks in the supply chain network. For the latter, we then stress the system with different initial shock scenarios (each shock is an iid draw from firms’ probability of defaults) and estimate additional risks for every single bank by generating loss distributions that take SCN contagion into account. In particular, we compute the expected loss (EL), the value at risk (VaR), and the expected shortfall (ES) for all banks with and without SCN contagion. In this way we extend the economic systemic risk index (ESRI) (Diem et al., 2022a) — that quantifies the supply-network-wide production (output) losses caused by the initial failure of a single firm or group of firms — to account for financial losses and potential contagion effects to the financial system.

2 Model and Methods

To describe how the propagation of production disruptions along supply chains spreads to banks, we use the supply chain network (SCN) of firms given by the matrix, . Its elements, , are the sales volumes of firm to firm , or equivalently, purchases of firm from in monetary units (Euros per year). The second network layer is the interbank network, , containing banks, where a link, , represents a liability of bank towards bank . Note that could also represent any other direct exposure, such as studied in Poledna et al. (2015). Every bank is endowed with an equity, . The two network layers are connected through the firm-bank loan matrix, , where is the outstanding amount of the liability firm has towards bank . In this paper we focus on contagion from the supply chain, , to the interbank network, . We omit potential cascading effects inside 222Interbank financial contagion channels could be straight forwardly included as an extension of the model presented in this work.. This model is calibrated with actual data derived from Hungarian VAT and balance sheet data for the year 2019 for , , , and . For details, see Section 3.

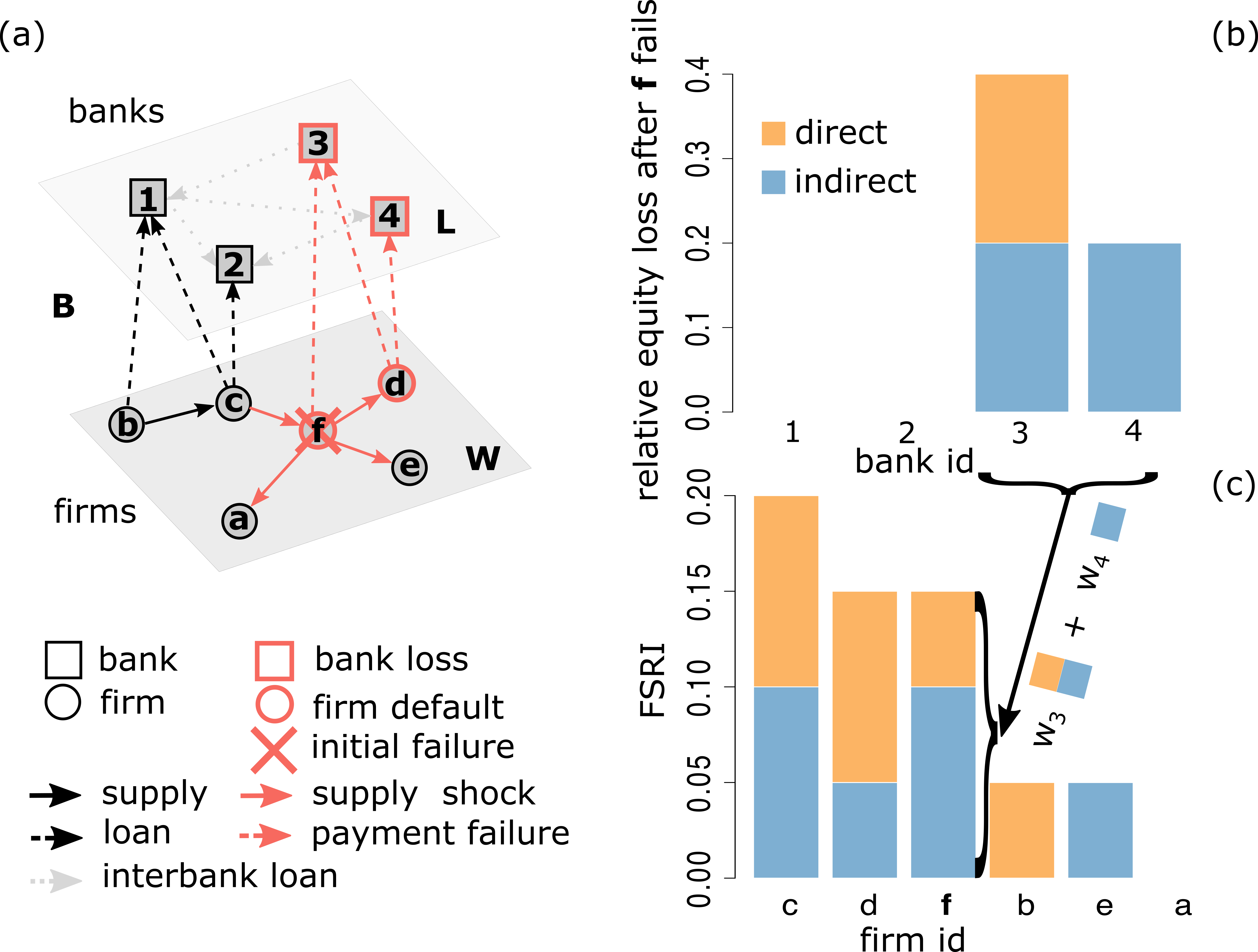

Schematically we describe the two-layer network in Fig.1(a). The bottom layer represents the SCN, , consisting of firms (circles). Arrows between them indicate supplier-buyer relations (from supplier to buyer), e.g. is a supplier of and are the sales from to in Euros per year. The upper layer represents a financial network consisting of banks (squares). Layers are connected by firm-bank loans, (dashed arrows), e.g. firm has a loan from bank , with being the outstanding amount. All firm loans are assumed to be of size and all interlayer links are, (light gray; no contagion between banks is possible). The capital or equity, of all banks is set to 5.

Contagion spreading from the SCN layer, , to the individual banks occurs in three steps:

-

1.

quantify the propagation of production disruptions in the SCN after a firm’s initial failure;

-

2.

update equity and liquidity buffers of firms in response to potentially reduced production levels and check if they became insolvent and default on their loans;

-

3.

update the banks’ equity buffers by writing off the loans of the initially failed (and defaulted) firms, and the firms that defaulted due to supply chain network contagion.

In this multi-layer network micro-simulation model, the actual data for , , , and is considered to be the realisation of an “undisrupted” economy, where firms normally buy and sell in the SCN. The data contains firms’ income statements, balance sheets and the outstanding principles of banks’ commercial loan portfolios of the respective year. Given this initial state of the economy, we can next simulate the effects on this economy when it is hit by an initial shock that affects the production capacities of firms and propagates through the supply chain network. This will now lead to counterfactual realisations of income statements and balance sheets of the firms. From these we infer which firms would have defaulted on their loans if the initial shock had happened. Banks write off the respective loans and suffer hypothetical losses, given the initial firm shock. We next describe the three steps of the model in more detail.

Step 1

To simulate how a specific firm failure spreads through the SCN, , we use the firm-level shock propagation mechanism of Diem et al. (2022a), described in A. There, a Generalized Leontief Production Function (GLPF) is specifically calibrated for every firm, , to determine how much it can still produce if one of its suppliers, , fails to deliver its products. We refer to this as a supply shock or downstream shock propagation (from supplier to buyer). If a customer, , of firm stops buying it faces a demand shock or upstream shock propagation (from buyer to supplier). The undisturbed production state of the SCN at time, , is represented by the production-level vector, . Initially, each firm, , produces of its original production level, i.e. for every . At time, , an initial event occurs that disrupts the production of at least one firm in the SCN. This can be for example the (temporary) failure of a single firm, or a simultaneous production stop of many firms due to a COVID-19 lockdown or a natural disaster. The vector denotes the severity of the initial shock by specifying the remaining production level for every firm after the initial event occurred. For instance, means that firm can still produce of its pre-shock production level. We set the production level of every firm, , to () 333Note that initial shocks could affect firms at different time points, i.e. happens before if . Here we always assume that and omit the time index in the notation. The model can be easily adjusted to feature different time points of disruption events. In the presented model the time intervals between two elements of the sequence correspond to the same time unit, e.g., a calendar day or a calendar week.. The initial shock, , triggers an upstream and downstream shock propagation cascade along the supply chain links of firms. The propagation continues until every firm stops to adjust its production levels, i.e. , and the system converges to a new stationary state at time . This state is represented by the final remaining production levels, , after the initial event. For example, means that firm lost of its original production level. We assume that production levels remain at this new state for a certain amount of time before firms can recover by finding new suppliers and buyers. Here, we do not model this rewiring of the network since a realistic rewiring dynamics needs substantially more assumptions and data that would go beyond the scope of this work. Therefore, the model outputs represent the short term effects before firms can adjust their production and sales structure.

In the example of Fig.1(a) the initial shock scenario assumes the failure of firm (red X), e.g. due to an exogenous event such as a fire. Initially, we have corresponding to a production level of all 6 firms , , , , , and , respectively. Next, the initial shock at time is introduced with the vector, , where the 6th element indicates the drop of ’s production level to . The shock now spreads (red arrows) upstream to ’s supplier and downstream to its buyers , , and . To keep the example short, we assume here that the production of , , and does not depend on the inputs of , but can not produce without them, i.e. suffers a production disruption. Consequently, after convergence at, , the final production level vector is .

Step 2

The now reduced production levels, , cause a drop in firms’ revenues and material costs that affects their profits. This change is relative to the pre-shock profits recorded in the income statement. Reduced profits may turn into large losses and potentially will affect the equity and liquidity of firms, and eventually, the ability to repay their bank loans (if they have any). To find out whether a company can withstand the financial losses from a given production disruption we use the information from its income statement and balance sheet, a stylized version of which is depicted in Table 1.

| Assets | Liabilities |

|---|---|

| Short term assets | Short term liab. |

| Inventory | Other liabilities |

| Fixed assets | Equity |

| Other assets | Profit |

| Other equity | |

| Total Assets | Total Liabilities |

| Operational profit |

| + Revenues |

| Material costs |

| Non-operational profit () |

| + Other income |

| Other costs |

| Net Profit |

For every firm, , we infer for a given year its revenue, , its material costs, , its non-operational profit, , consisting of other income (e.g., income from financial assets, sales of land, etc.), and other costs (e.g. HR costs, depreciation, rent, and other costs that can not be adjusted within a short period of time), from its income statement data. From the balance sheet data we read off firm ’s equity, , its short-term assets, (including cash, short-term claims, and securities), and its short-term liabilities, (including short-term loans to suppliers, etc.).

We next determine how a production reduction of firm, , translates into a reduction of its revenues, , and its material costs, , affecting the profit, . We assume that the non-operational profit stays the same, and that the revenue is reduced to . Note, that for simplicity we neglect potential inventories of inputs and finished goods. We further assume that firms can reduce their material costs proportionally to the production level, i.e. material costs after the cascade are . This assumes that firms only have to buy exactly the amount they need for production and neglects the fact that supply contracts might be long-term. This assumption might be overly optimistic. Since, the net profit is the sum of revenue, negative costs, and non-operational profit, , the new profit at the reduced production level is and the change in profit is

| (1) |

The change in profits affects a firm’s equity and its liquid assets (via the cash flow statement). The equity, , of firm includes the equity from the previous year and the net profit of the current year, . Note, that can also be negative. After accounting for the change in profits the new equity is . According to The Insolvency Code (Act, 1991) (Section 27 (2f)) firm becomes insolvent if . The cash position of the firm at the balance sheet reporting date depends on the profits, , made during this period444The explicit link between profits and cash is the cash flow statement. The indirect method for calculating the cash flow during the year starts with the profit and adds or subtracts transactions that are not cash effective and eventually yields the change in cash position. Examples for non cash effective transactions are adding back depreciation, adding a reduction of accounts receivable, deducting an increase in inventory levels, or deducting the purchase price of a new machine.. A reduction of profits will cause a decrease of the firm’s cash position. If cash turns negative the firm becomes illiquid, can no longer pay bills or repay loans, and may become bankrupt according to the Insolvency Code (Act, 1991) (Section 27 (2a)). We define the variable to measure a liquidity default more broadly as the sum of short-term assets (that could be sold fast) minus the sum of short-term liabilities (that are due soon), i.e. . After the shock, firm has a liquidity of and if it is negative we assume that it declares bankruptcy, defaults on its loan and banks write off all loans extended to . Due to the cash flow calculation procedure and the assumption that the other transactions happen in the same way as in the case where the shock did not occur, the change in liquidity is . This assumption presumably leads to an over-estimation of the liquidity loss as firms in distress would possibly defer investments into new machinery that are cash flow negative or could try to receive additional loans from banks (cash flow positive) to avoid becoming illiquid. We abstain from modelling this behaviour in detail as it involves a number of additional assumptions that can not be backed with the available data.

In summary, we derived two insolvency conditions for firms that depend on the size of the firm’s production reductions, , and its financial strength (liquidity, , and equity buffers, ). We assume that insolvency of a firm leads to its bankruptcy, which reflects the unlikeliness of loans to be repaid. The unlikeliness to pay indicator is one of the conditions under which a bank classifies its client as defaulted, see, e.g., Article 178(1-3) of Regulation (EU) No 575/2013 (RegulationEU, 2013). To conclude step 2, for all firms we define a binary default indicator

| (2) |

It indicates, which firms defaulted () as a result of an initial shock, , and the ensuing supply chain contagion after the cascade stops at time . means is still going concern (not defaulted). To see the role of the equity- and liquidity default conditions in Eq. (2) individually, we define the equity default indicator vector, , that only considers the condition , and the liquidity default indicator vector, that only checks the condition . Note, that the union of the two vectors gives . In the following we define all equations in terms of , however, all definitions can be rewritten in terms of and to analyse the effects of liquidity or equity defaults individually.

Step 3

Loans of defaulted firms are classified as non-performing loans (NPL). We assume that borrowers are not subject to any forbearance solutions (as would be standard procedure, see BCBS, ()), and they cause write-offs or provisions for banks that reduce the banks’ equity buffers. Impairment allowances for non-performing loans (or loan loss provisions) implied by current accounting practice are described in the International Financial Reporting Standards (IFSR 9) (IASB, 2014) or in Guidance on credit risk and accounting for expected credit losses (BCBS, ()). For simplicity, we assume a loss given default of 100%, i.e., the entire exposure, , bank has towards firm at the time of default is written off. We distinguish between direct and indirect losses of banks’ equity. Direct losses are caused when a debtor, , immediately defaults in response to the initial disruption, i.e., and . Accordingly, we define the direct default indicator via binary -dimensional vector . Indirect bank losses are caused when a firm defaults, , but not due to its initial production disruption, i.e. , but because of the additional production losses stemming from the propagation of the initial disruption. These equity losses of banks would not occur if supply chain network contagion is not present. The indirect default indicator is defined as the binary -dimensional vector

| (3) |

Then, holds555Note, that to obtain we don’t need to perform contagion at all, meaning that Step 1 can be omitted, and in Step 2 we put . is obtained accordingly from Eq. (2).. The fraction of lost equity, , of bank, , — after the initial shock, , has propagated through the supply chain network —, is calculated as

| (4) |

where is calculated for every bank . Since, the elements of are given in monetary units, we divide the loans, , by the respective bank’s equity, . The fraction of the lost equity from direct defaults is and from the supply chain contagion induced defaults . The equity losses suffered by the entire banking sector from initial shock, , is

| (5) |

To illustrate steps and in Fig.1(a) the red circles indicate that firms and defaulted, i.e . We consider that firms , , , and were able to withstand the shock, caused by the initial disruption of . Red dotted arrows indicate payment failures of defaulted firms and , red squares show that banks and suffered losses. Bank suffered losses from two non-performing loans, (directly) and (indirectly). Bank suffered losses only indirectly from . For this scenario, and , . Recall, in this example all banks have the same initial amount of equity of , and all loans have the same outstanding amounts of . Relative losses of banks after the initial failure of firm are depicted in Fig.1(b), where every bar is associated to one bank. Banks and didn’t experience any losses, explaining why . Bank lost of equity directly (orange brick) and of its equity indirectly (blue brick), i.e. . Similarly, we get and .

Estimating the effects of individual-firm failures on overall bank equity. To address our first research question, to what extent a firm’s systemic risk in the real economy affects financial stability, we estimate the impact on the banking system (sum of all the banks’ equities) caused by a full production disruption of a single firm, , by computing the resulting supply chain contagion and loan defaults. For the initial failure of firm we define single-firm shock vector

| (6) |

The value indicates the production level of firm under the initial shock scenario, (failure of firm ).666 The super script S indicates that the shock vector, , represents the failure of a single firm . The set , collects the possible shock scenarios, corresponding to a failure of a single firm. Note that we use the indices to indicate firms in the SCN and for banks. For every initial single firm failure, , we perform steps and receive the fraction of lost equity, , for every bank . Based on the equity losses, , we compute the financial systemic risk index (FSRI) of firm , as

| (7) |

can be interpreted as the equity-weighted sum of losses suffered by individual banks in the network. It is the fraction of overall bank equity that is lost after the initial failure of a single firm propagates through the supply chain network, , causing firm insolvencies and loan write offs. It can be used to rank the companies operating in the production network by their systemic relevance to financial stability. Note the difference to simply computing the DebtRank of companies in the credit network without their role in the supply chains, as was done in Poledna et al. (2018); Landaberry et al. (2021).

Fig.1, panel (c) shows for our example SCN how FSRIf of firm is computed as the weighted average of the direct and indirect losses shown in panel (b). The weights are given by the relative equity size of every bank, i.e. , since we assume that all banks in our example have the same equity. We see that , meaning that of the overall bank equity is at risk should firm fail. Similarly, if we simulate the initial failure of the other firms in the example SCN, we expect system-wide losses of , , , and for the shock vectors , , , , and , respectively.

To highlight the effect from supply chain contagion, we distinguish between the direct and indirect components of FSRI

| (8) |

For every firm the direct component is proportional to the loans of that firm; the indirect FSRI is equal to the weighted sum of loans of firms that defaulted because of the operational failure of the firm .

If in Eqs. (4) and (7) is substituted by or by , we get the FSRI triggered by equity or liquidity defaults,

| (9) |

| (10) |

respectively.

Estimating individual bank losses from supply chain contagion. To answer the second research question about how much the risk of individual banks is amplified by supply chain contagion, we need to investigate the exposure of banks to losses transmitted by the supply chain network under more general initial shock scenarios. Typical measures used by banks to assess the riskiness of portfolios are expected loss (EL), value at risk (VaR) and expected shortfall (ES) (McNeil et al., 2015). These measures are calculated from a loss distribution (McNeil et al., 2015). Here we estimate the loss distribution for each bank with a Monte Carlos simulation that generates initial shock scenarios — representing the simultaneous failure of multiple firms — to the supply chain network. In this way we generate different stress scenarios for the economy and simulate the corresponding losses for each bank.

Specifically, we simulate initial shocks, , where multiple firms suffer a full production disruption. The value indicates the production level of firm under the initial shock scenario, . We use the index to distinguish the 10,000 scenarios. Every shock scenario vector, , is created by drawing from a -dimensional multivariate Bernoulli random variable, where the success probabilities correspond to the -dimensional vector of default probabilities (PDs) of firms, i.e.

where is the default probability of firm . We set the initial production level of firm to in case of a success and to , otherwise. The PDs are estimated by the Central Bank of Hungary, for details see B. Note that due to data limitations we draw the defaults of firms independently, i.e. we neglect systematic or correlated events like a large crises affecting specific industry sectors. We denote the set of initial shock vectors by 777The super script M indicates that the shock vector, , represents the simultaneous failure of multiple firms..

As before, contagion leads to direct and indirect losses for banks. For each bank , we compute the two loss distributions consisting of its contagion-adjusted equity losses, and its direct equity losses , corresponding to the 10,000 shock scenarios, . Similarly, is used to obtain the loss distribution for the entire banking system. For a given shock vector , the losses and are obtained by performing

-

1.

Step 1 for and yielding the production losses of firms, ;

-

2.

Step 2 yielding the vector of defaulted firms, ;

- 3.

The procedure is repeated for every .

For the VaR and ES we choose the threshold. To compare these risk measures for the direct and the contagion-adjusted loss distributions, we use the risk amplification factor, for bank , where stands for EL, VaR, or ES. We define it as

| (11) |

where is the value calculated from the direct- and from the contagion-adjusted loss distribution of bank . We denote the averages over all banks by , , and .

3 Data

We calibrate the model to a unique real-world firm-level data set composed of 4 distinct micro-data sets that are available within the Central Bank of Hungary. These are the

-

1.

VAT based supplier-buyer relationships between practically all firms in Hungary;

-

2.

balance sheets and income statements of firms;

-

3.

loans of banks to firms;

-

4.

CET1 equity of banks.

The first dataset is used to reconstruct the supply-chain network, . It is based on the 2019 value added tax (VAT) reports, reflecting any purchase between two firms exceeding 100,000 HUF tax content (approximately Euros) made in Hungary. The resulting network consists of anonymized Hungarian companies. The link weights correspond to the monetary value of transactions (price times quantity). We filter the links such that they contain only relationships that are stable. We include links that did occur in at least 2 transactions in two different quarters of the year 2019. of links are stable in this sense and they cover of the traded volume in the network. For a more detailed description of the data set based of the year 2017, see (Borsos and Stancsics, 2020; Diem et al., 2022a).

The second dataset consists of the financial statements of every firm in the supply chain network. The variables obtained from the balance sheets and income statements, see Table 1, are used to calculate the equity and liquidity buffers of firms, as well as their profits. For every firm, we have an estimate of its default probability obtained from a model developed at the Central Bank of Hungary, see Burger et al. (2022) and B for more details.

The third dataset, the credit registry, is needed to determine the firm-bank loans, . It consists of the overall exposures of firms in the supply chain network, , to banks in Hungary. The remaining companies do not have reported bank loans in Hungary. We remove small-scale banks for which we do not have Common Equity Tier 1 (CET1) values (contained in the fourth data set) available, arriving at banks that cover of the loan volume of the original dataset with banks. Hence, is a matrix of size with non-zero inputs (multi-layer links), with and . firms have loans from one of the banks.

Based on this information the model is fully data-driven, meaning that there are no free parameters. The only modelling choices concern the, set-up of the SCN shock propagation (taken from Diem et al. (2022a, 2023)), assumptions of how production shocks affect the financial health of a firm, i.e. that revenues and material costs can be reduced proportionally to production losses, the choice that a decrease of in equity or liquidity cause bankruptcy, and the assumption that LGD is equal to , see more in Discussion 5.

4 Results

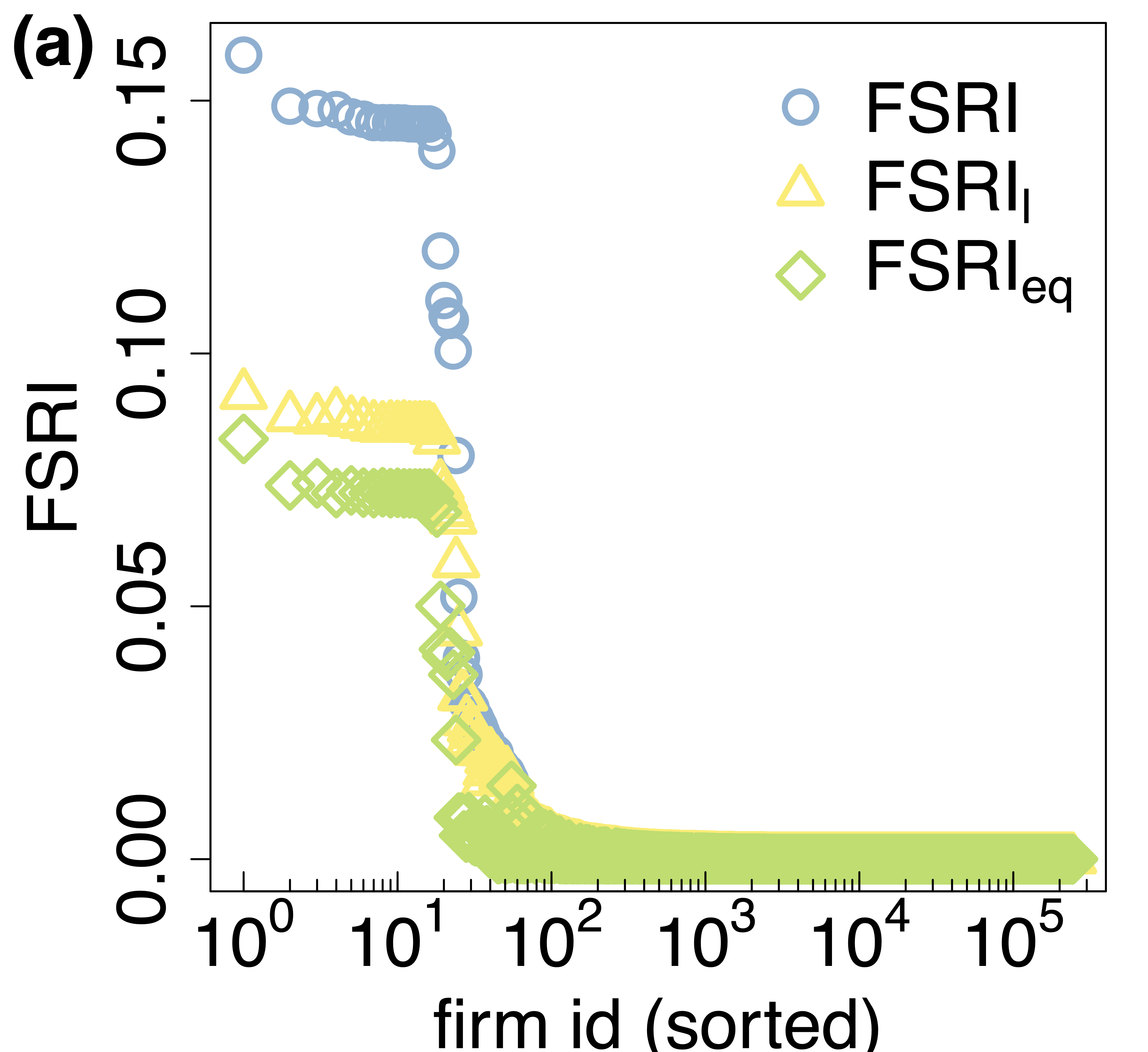

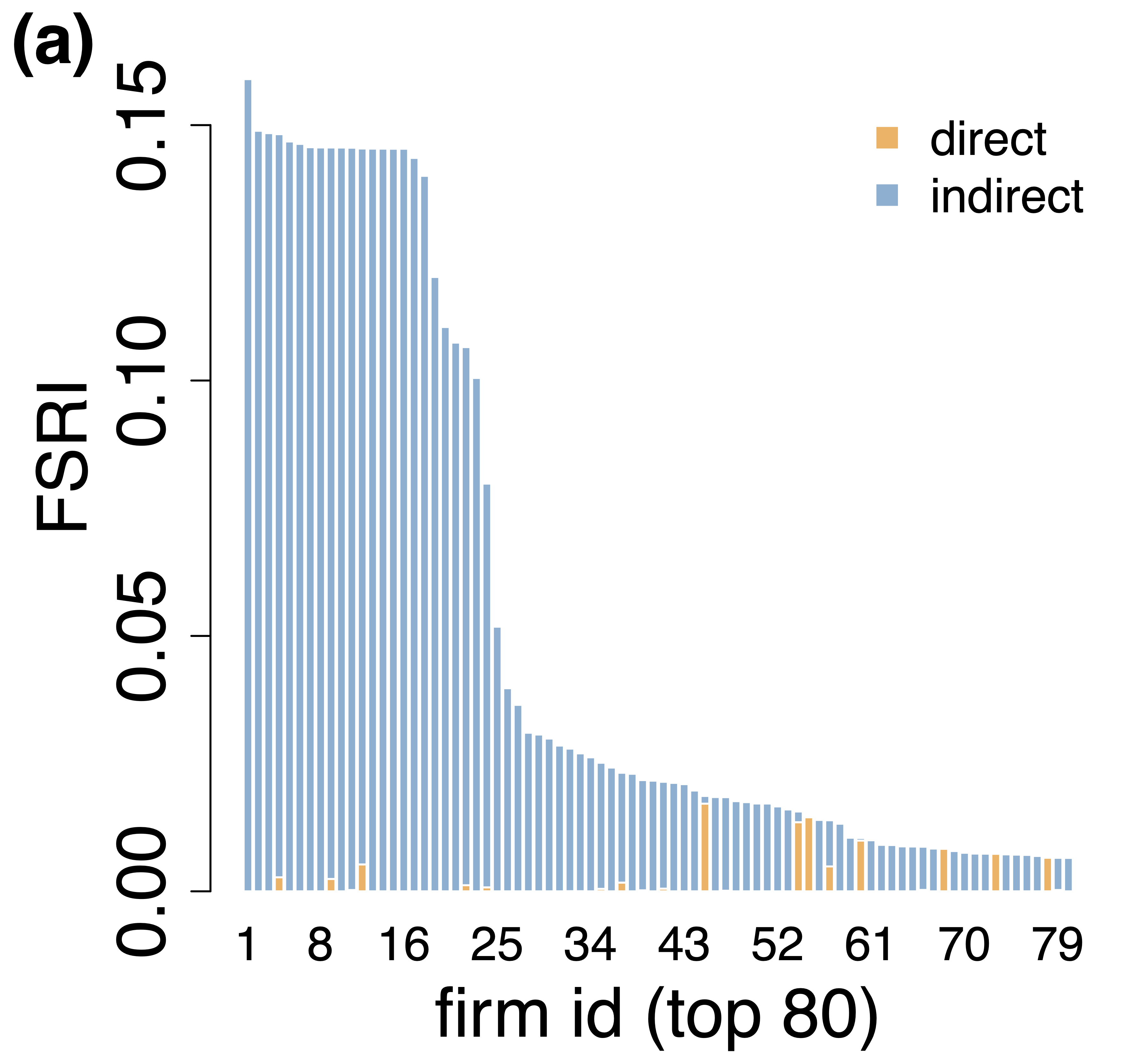

We compute the financial systemic risk index (FSRI) (7) for each of the companies contained in the Hungarian supply chain network. The rank-sorted distribution of the FSRI values (blue circles) is shown in Fig.2(a) in log-linear scale, where the -axis denotes firm ranks and the -axis their respective FSRI values. The firm with the highest financial systemic risk is to the very left and the lowest systemic risk firms to the very right. The riskiest firm has an FSRI value of slightly above , meaning that its failure and the ensuing supply chain disruption cascade would lead to loan write offs equivalent to approximately of the overall CET1 capital of the Hungarian banks in the sample (see Fig.5(a) for how banks are affected individually). A group of firms form a plateau with very similar FSRI values slightly below . This high-risk plateau is followed by a sharp drop in FSRI values of more firms with values above and firms with values between and . In total, firms have FSRI values higher than . To a large extent the relatively high risk of these firms is driven by the substantial supply chain cascades they trigger (indirect losses). The firms in the high FSRI plateau cause similar supply chain cascades, i.e., they affect mostly the same firms in response to their failure and hence also their financial impacts on the firms in the network is similar, finally causing similar losses to banks’ equity levels. This pattern of similar supply chain cascades can be explained by the observed plateau firms, forming a tightly knit network (systemic core of the economy) of highly risky supply relations (Diem et al., 2022a). These companies predominantly belong to the energy, communication, and transportation sectors, a few belong to waste collection and manufacture of basic chemicals. These sectors have been identified as essential to many other industries in the survey conducted by (Pichler et al., 2022b), which is used as input to the supply chain shock propagation algorithm, see A.

Next we distinguish between the bank capital losses that originate from insolvencies due to a lack of liquidity or a lack of equity. The financial systemic risk index, (9), solely based on firm insolvencies caused by their equity turning negative after supply-chain shock propagation is shown by green diamonds. Similarly, the financial systemic risk index, (10), solely based on firm insolvencies caused by their liquidity turning negative after supply-chain shock propagation is shown by yellow triangles. As expected, and are consistently smaller than FSRI, since the insolvency criterion for FSRI encompasses both, equity and liquidity based insolvencies. Remarkably, the high-risk plateaus of and show similar heights, of and , respectively. This indicates that as a result of the largest supply-chain disruption cascades most firms only suffer from either their equity or their liquidity turning negative; only a few firms suffer from both at the same time. In the profile distribution there are firms with risk over , additional firms in the interval , and in total firms with risk higher than . Similarly, in the profile distribution there are firms with risk over , additional firms in the interval , and a total of firms exceeding the risk of .

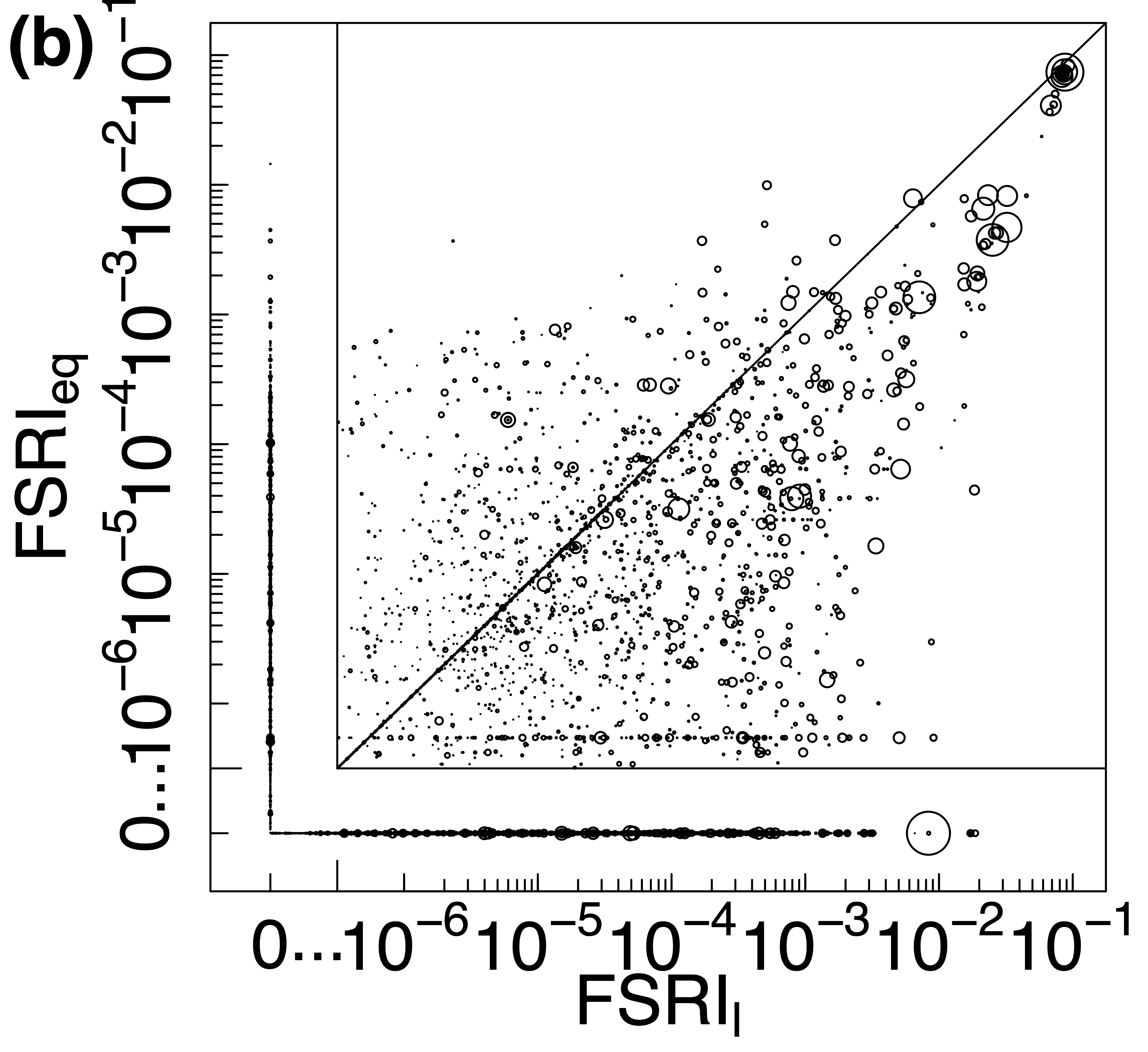

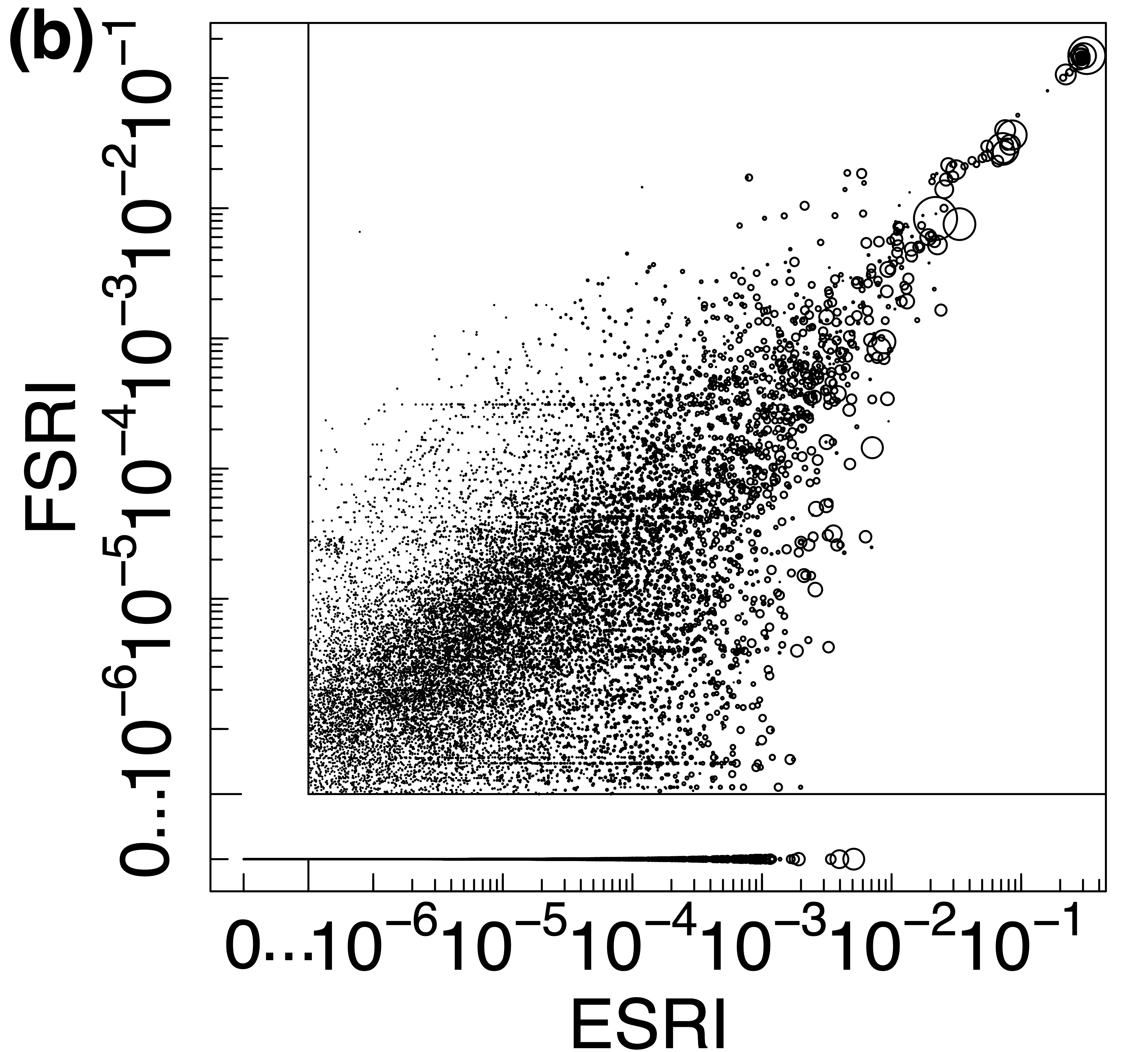

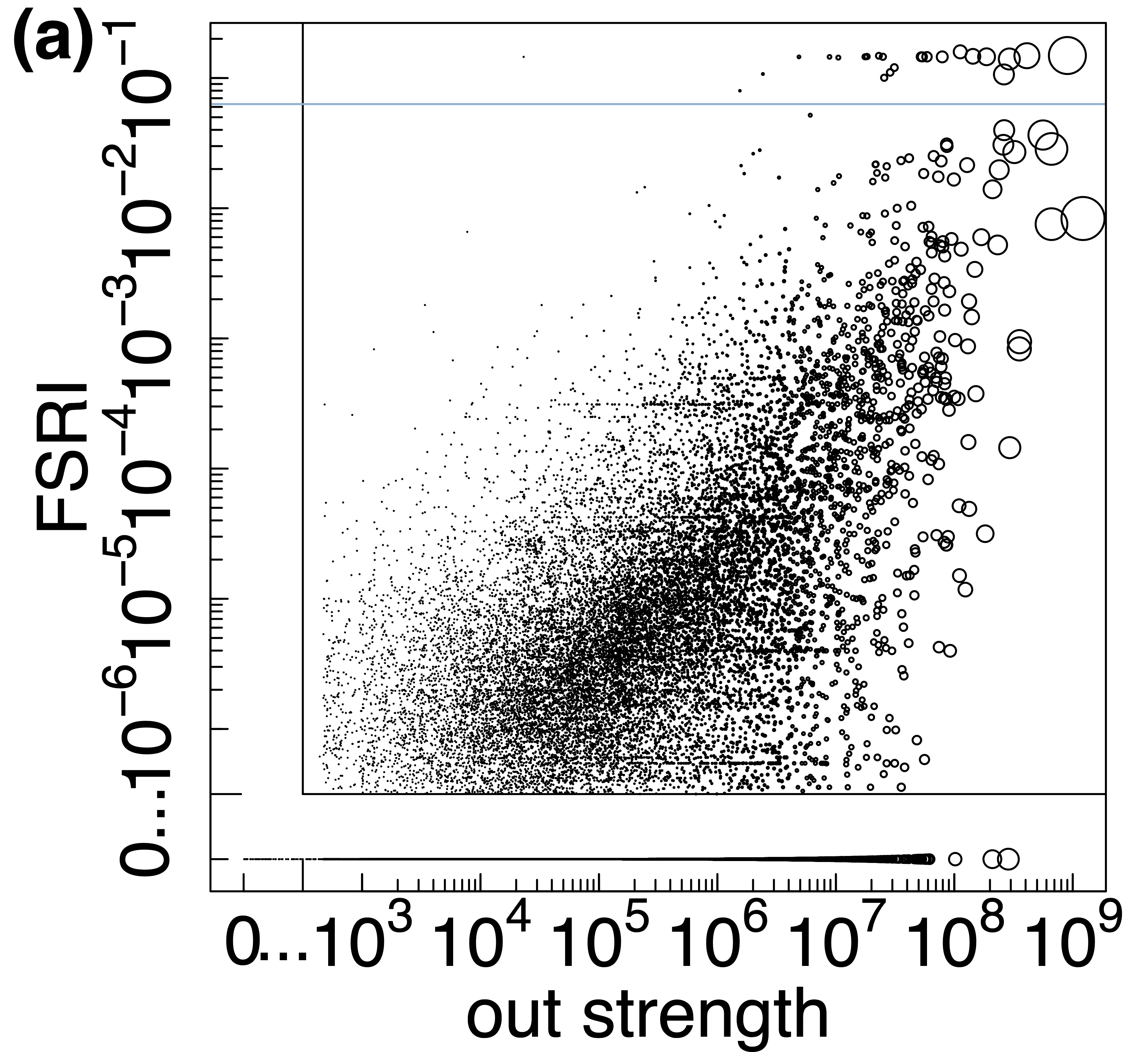

To investigate the relation between liquidity- and equity based insolvencies more closely, we provide a scatter plot in log-log scale in Fig.2(b). Since, many firms only cause either liquidity or equity based insolvencies, we plot two additional segments that would not be visible on the log-log scale. The first one shows the values if and the second segment shows the values if . Bubble size is proportional to the out-strength (sales to other firms) of the respective firm (see A). Firms in the FSRI plateau cause both, large amounts of equity- and liquidity based losses (top right, close to the diagonal). One observes that these are caused by large (large bubbles) and small firms (small bubbles). For small values and seem uncorrelated. There are firms with non-zero FSRI values, for and for . The low number of positive FSRI values can be explained by two factors. First, even though economic systemic risk (ESRI) — measuring the fraction of the production that is lost in the supply chain network after the failure of a firm — values decay as power law (see Diem et al. (2022b) Fig. S4), only a few firms cause large supply-chain cascades that can affect the financial conditions of other firms severely enough to cause a default. Second, in the data set of firms have loans, i.e., only firms out of have loans in one of the banks. Hence, indirect losses to banks are only caused when supply chain contagion leads to default of at least of these firms.

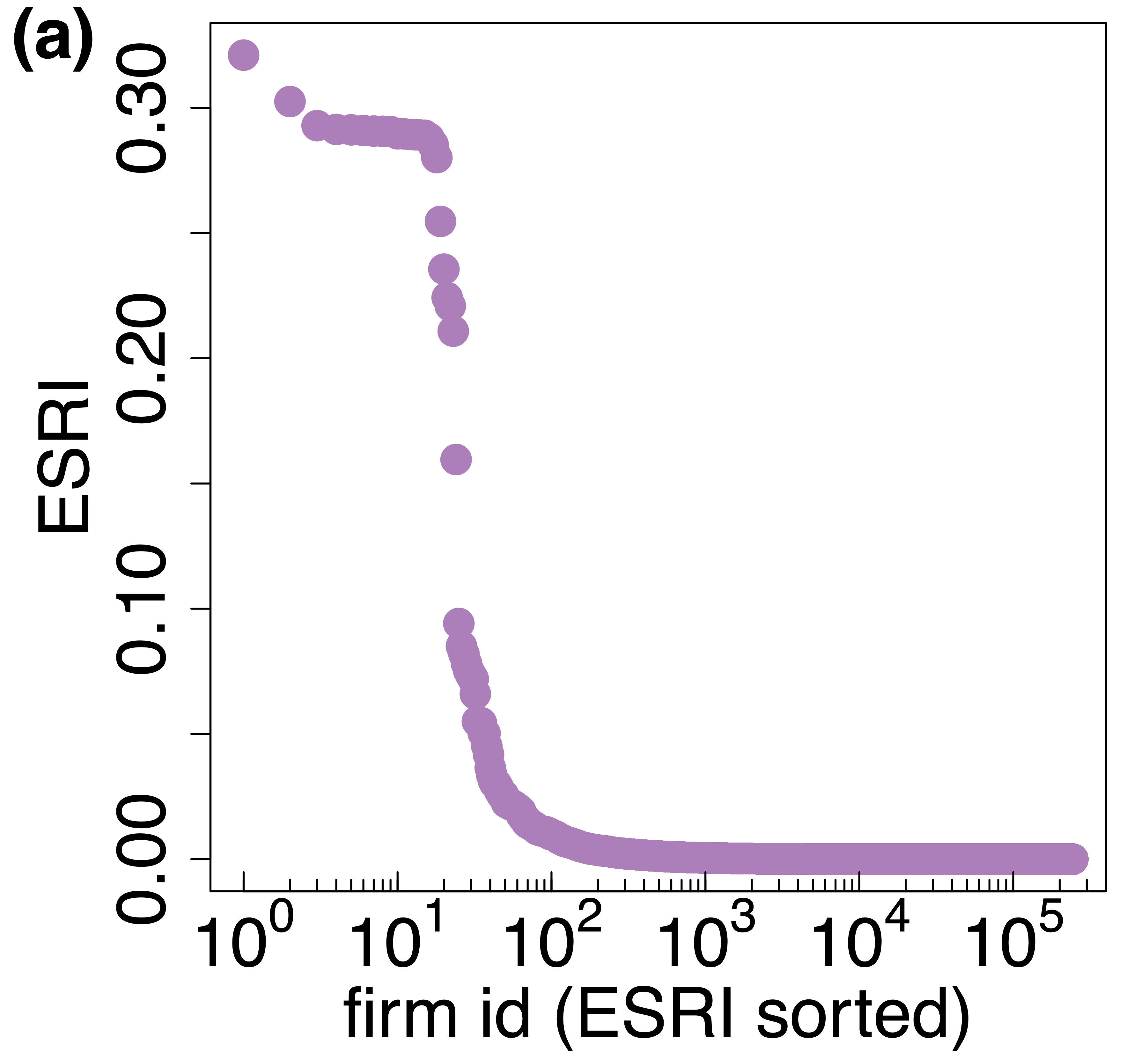

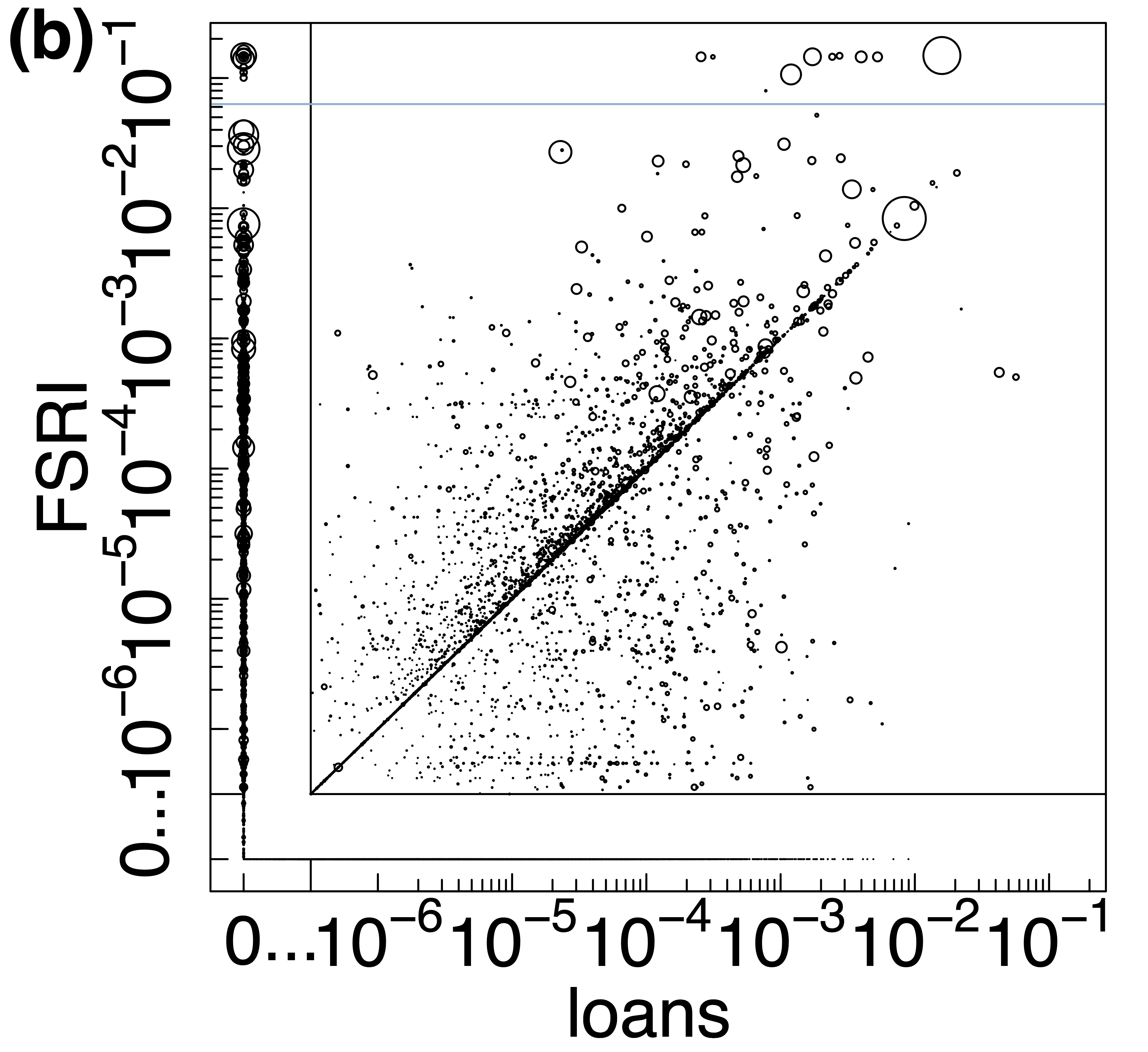

In Fig.3 we study the relation between FSRI and ESRI. The later quantifies the size of the supply-chain disruption cascade (in the real economy) in terms of the fraction of the production network’s total output that is affected in case of a firm’s failure; for details on ESRI and its calculation see A, Eq. (15) and Diem et al. (2022a). Figure 3(a) shows the characteristic shape (high-risk plateau, steep (power-law) drop, and many small-risk firms) of the ESRI distribution (purple dots) as observed in (Diem et al., 2022a). These features obviously carry over to the FSRI values (blue circles) as shown in Fig.2(a). The most systemically risky companies lead to production losses between 10% and 32% in case of their failure. These firms coincide with the high-risk firms in the FSRI plateau. This is visible in the log-log (plus zero section) scatter plot in Fig.3(b) with ESRI on the x-axis and FSRI on the y-axis. Bubble size is again proportional to out strength. We see that for the highest values of ESRI and FSRI are strongly correlated. The overall correlation coefficient of non-zero values is about on the log-log scale. There are many firms with an FSRI equal to , but relatively large ESRI values up to around . The likely reason is that firms’ supply-chain cascades, even though large, do not affect the financial conditions of other firms severely enough to cause their default or cause defaults to firms without loans. Again, many firms do not have bank loans; see Section 3).

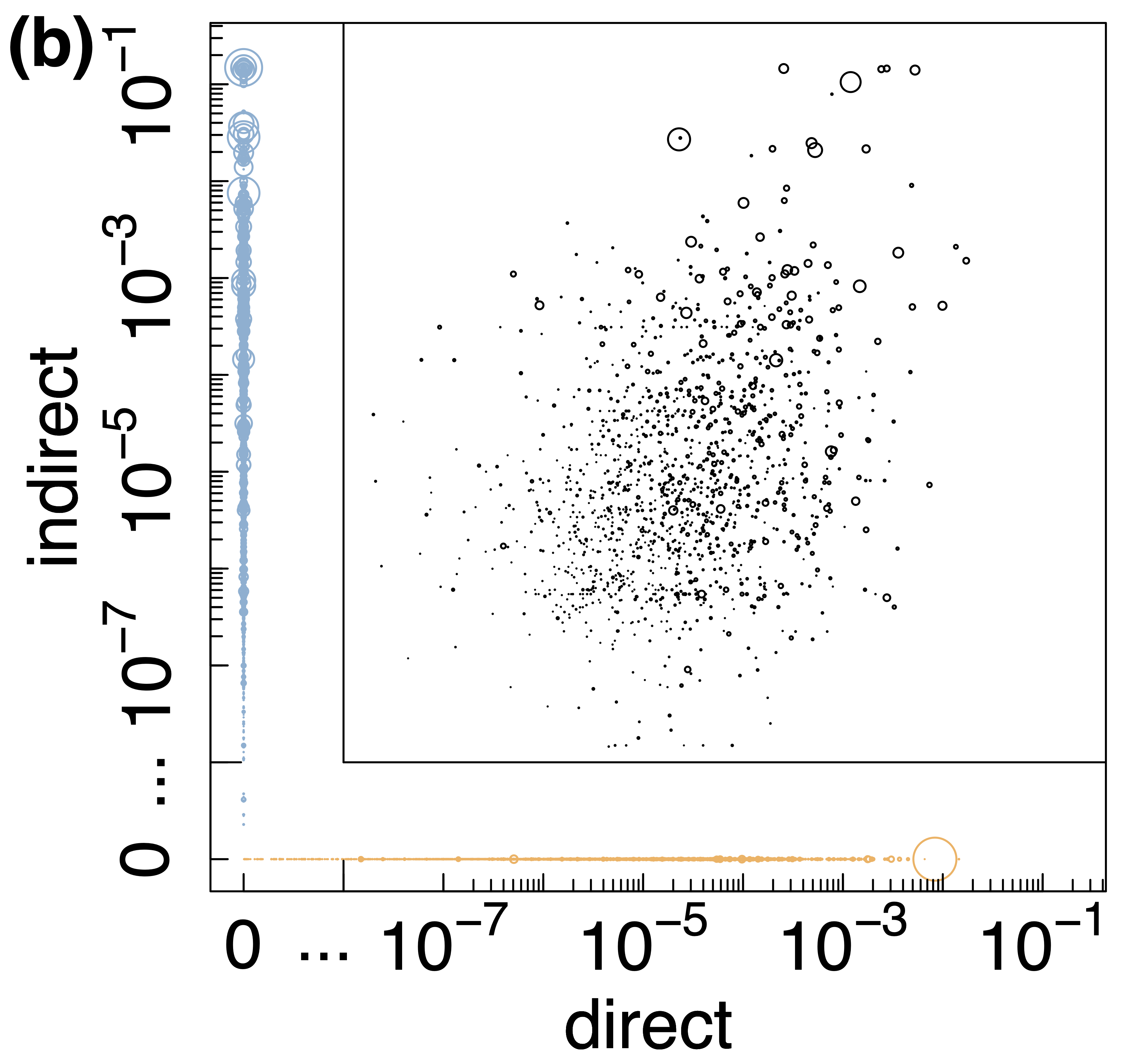

We next investigate the relation between losses caused directly by firms defaulting on their own loans and indirect loan defaults caused by secondary supply chain disruptions. Figure 4(a), disaggregates the FSRI values into direct and indirect losses for those 80 firms that cause the largest bank equity losses. The direct share (orange bar) of firm (see Eq. (8)) is simply the size of its defaulted loans divided by overall banks’ equities. Naturally most loans are very small with respect to total bank equity. The indirect share (blue bar) defined in Eq. (8) is proportional to loans that default after triggered a supply-chain cascade. The overwhelmingly blue color in the bar-plot indicates that the highest losses to overall bank equity are caused by supply chain shock propagation and not by the size of the firms’ own loans, see also Fig.8. A direct loss can be caused only by firms that have loans. If a firm without a loan initially fails and defaults it won’t cause a direct loss. For instance, out of the firms in Fig.4(a) have loans and default. The two sets intersect for firms, whereas the remaining firms with loans do not default because of their strong equity and liquidity buffers, i.e., they cause only indirect losses.

In Fig.4(b) we show the relation of direct versus indirect losses with a log-log (plus a zero section) scatter plot. In more detail, companies have only positive direct effects, i.e . firms (blue circles) have only positive indirect effects, i.e. . The remaining firms (black circles) have non-zero direct as well as indirect effects, i.e. . Most of the biggest companies, with respect to out strength (bubble size) cause zero direct losses (blue circles). Nevertheless, in Fig.4(a) we see some firms with big loans causing small indirect effect. In particular, firms , , or (showing the highest orange bars) have loans size around of total banks’ equities each, and belong to the top based on their revenue and sale sizes.

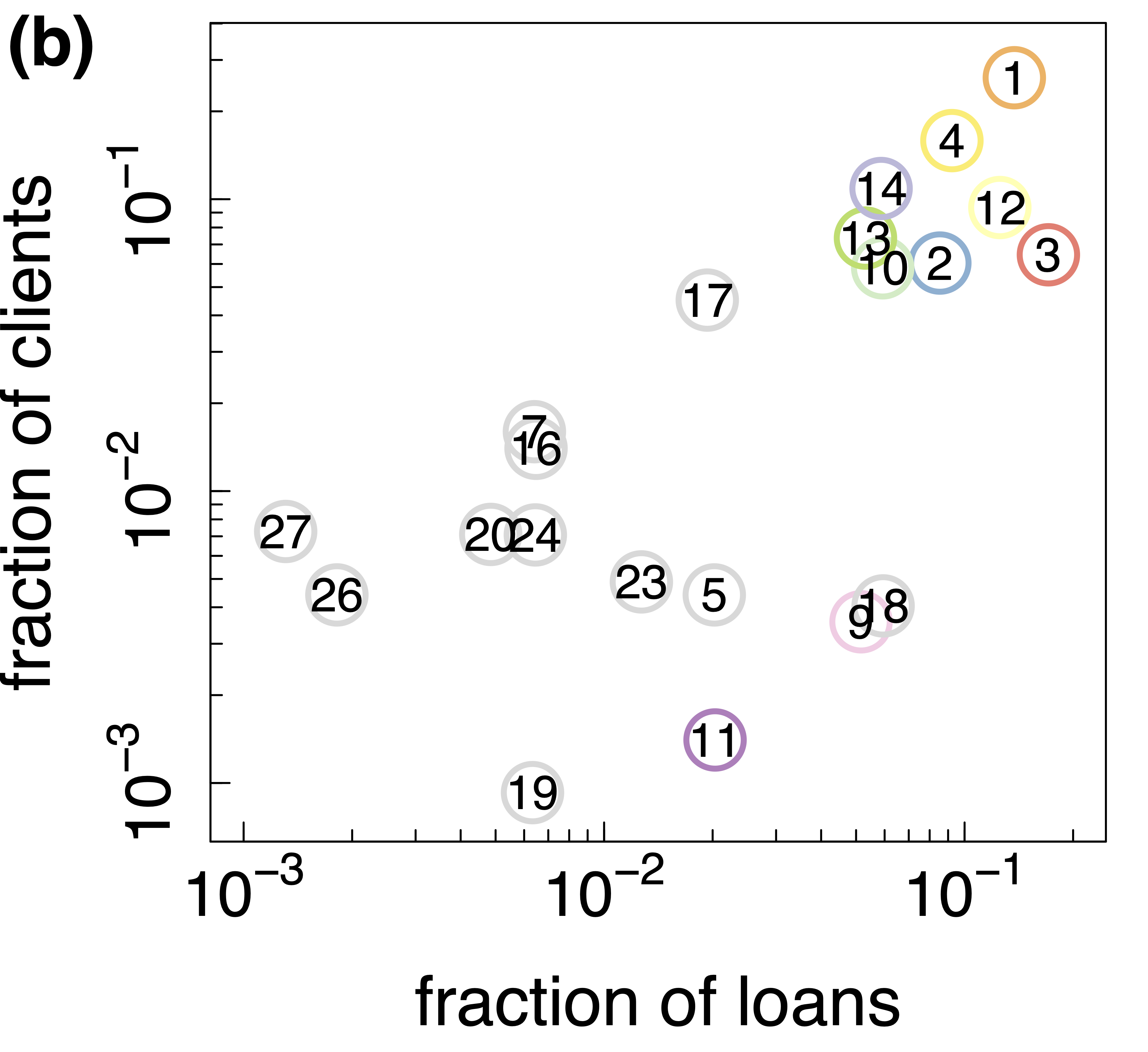

Having discussed the impact on a system-wide bank capital level, we now turn to how banks are affected individually after initial failures of the riskiest firms. We disaggregate the FSRI profile to the bank-level in Fig.5(a). The bar-plot shows the contributions from Eq. (7), the losses of banks are shown with different colors, the relative compound losses of the remaining banks in grey. Again, since the failure of the top FSRI firms trigger highly similar supply chain cascades, they trigger highly similar financial losses. This is reflected by the fact that banks are affected in a very similar ways by these 17 initial firm-failures. However, in general not always the same banks are affected. Different banks have different business models and different client structures. Some banks have large corporate loan portfolios relative to their equity, others have a stronger focus on retail- and mortgage lending. Further, banks can have a strong focus on certain industry sectors such as agriculture. Therefore, some firms cause supply chain cascades that affect specific banks disproportionately. The log-log scatter plot in Fig.5(b) shows the fractions of loans (-axis) against the fractions of clients (-axis) of banks in the financial layer (we skip 6 banks with fractions below ). Bank 3 has the biggest amount of loans; bank 1 has the biggest proportion of clients. The bar-plot reveals that losses are suffered mainly by the banks 1, 2, 3, 4, 9, 10, 11, 12, 13, 14, covering of the entire equity in the financial layer. Those banks hold of the clients that have of loans in those banks. Banks 3, 1, 4, 12, 13 cover of total equity, hold of clients having of loaned money in the system.

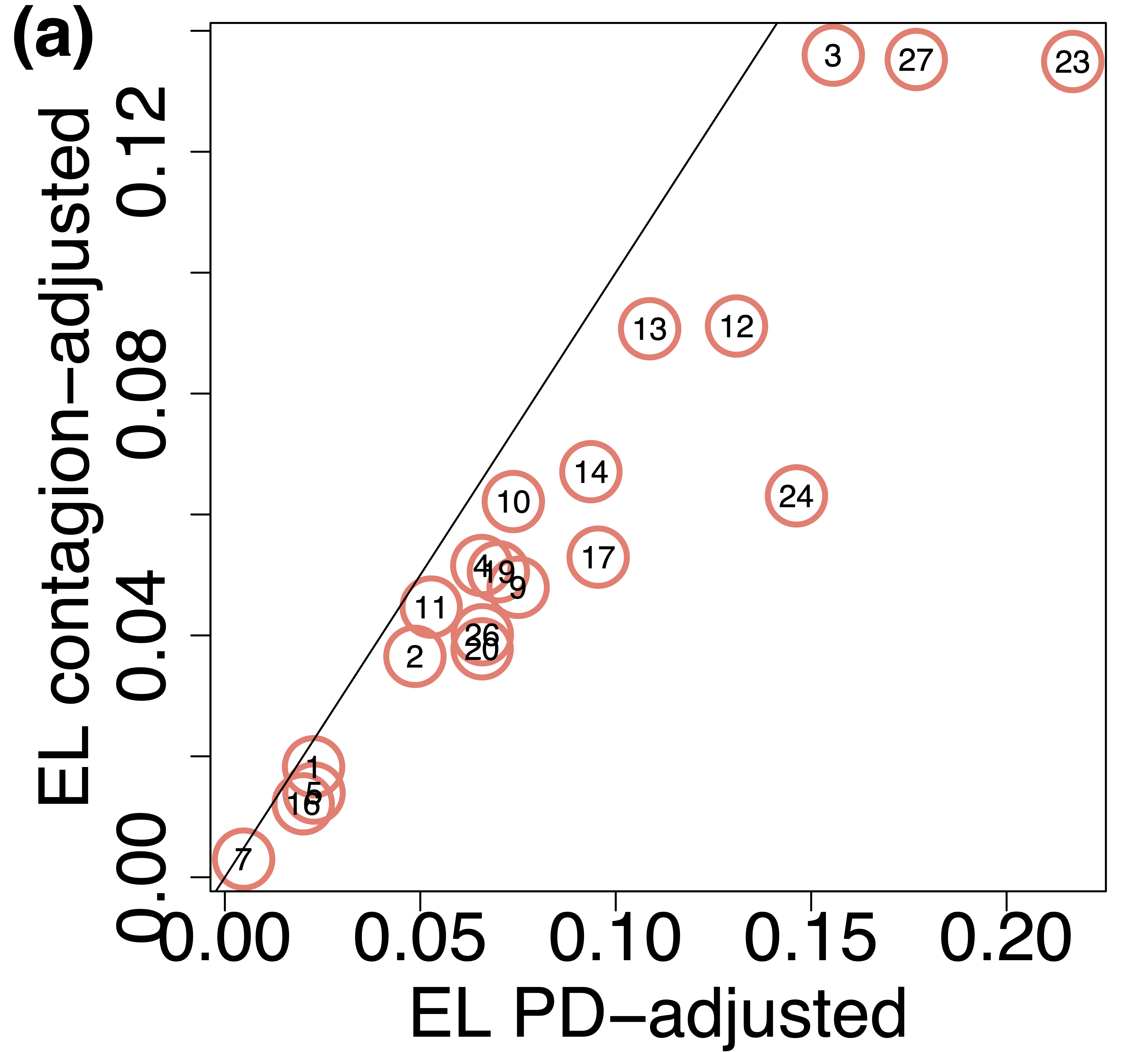

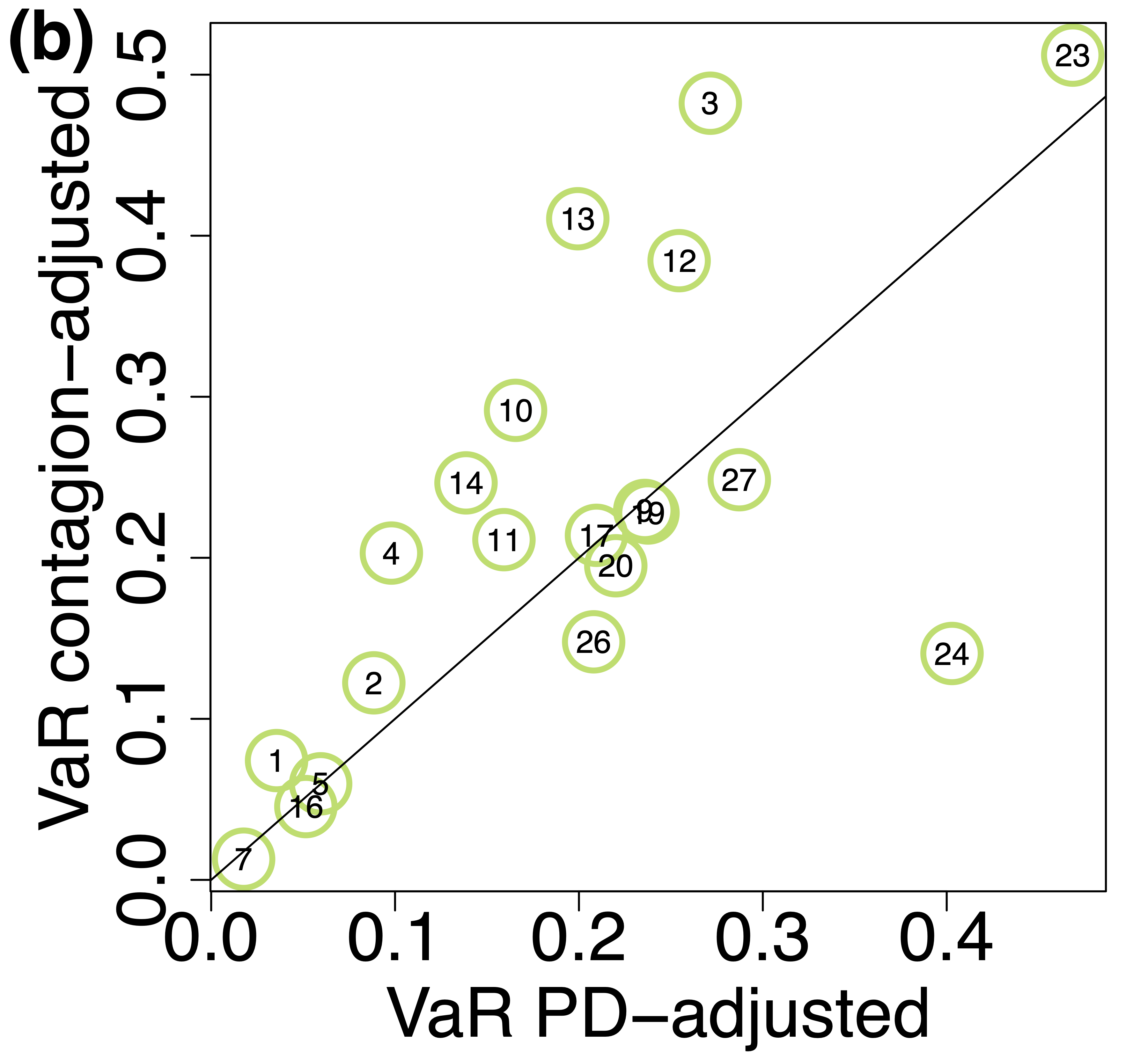

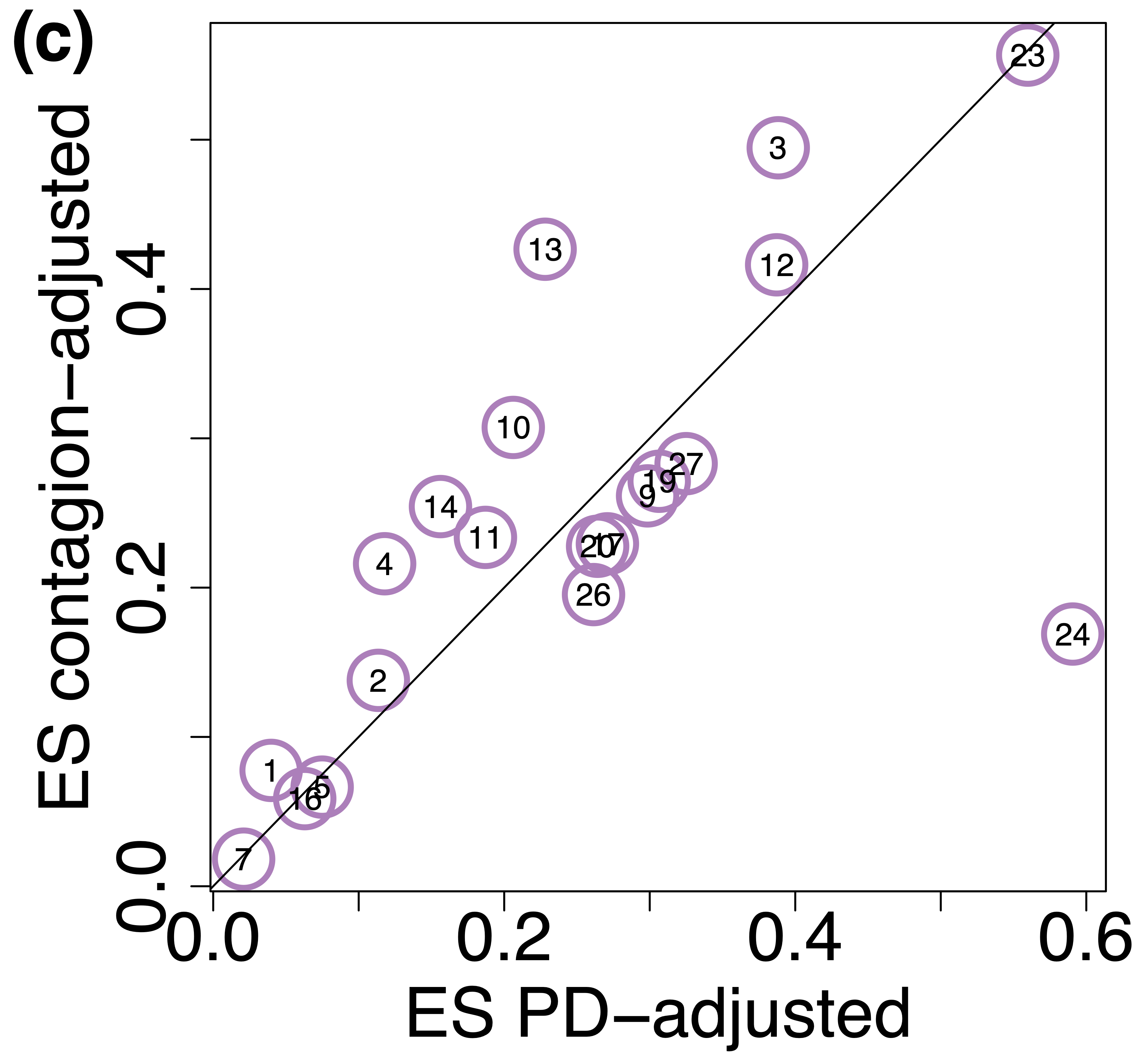

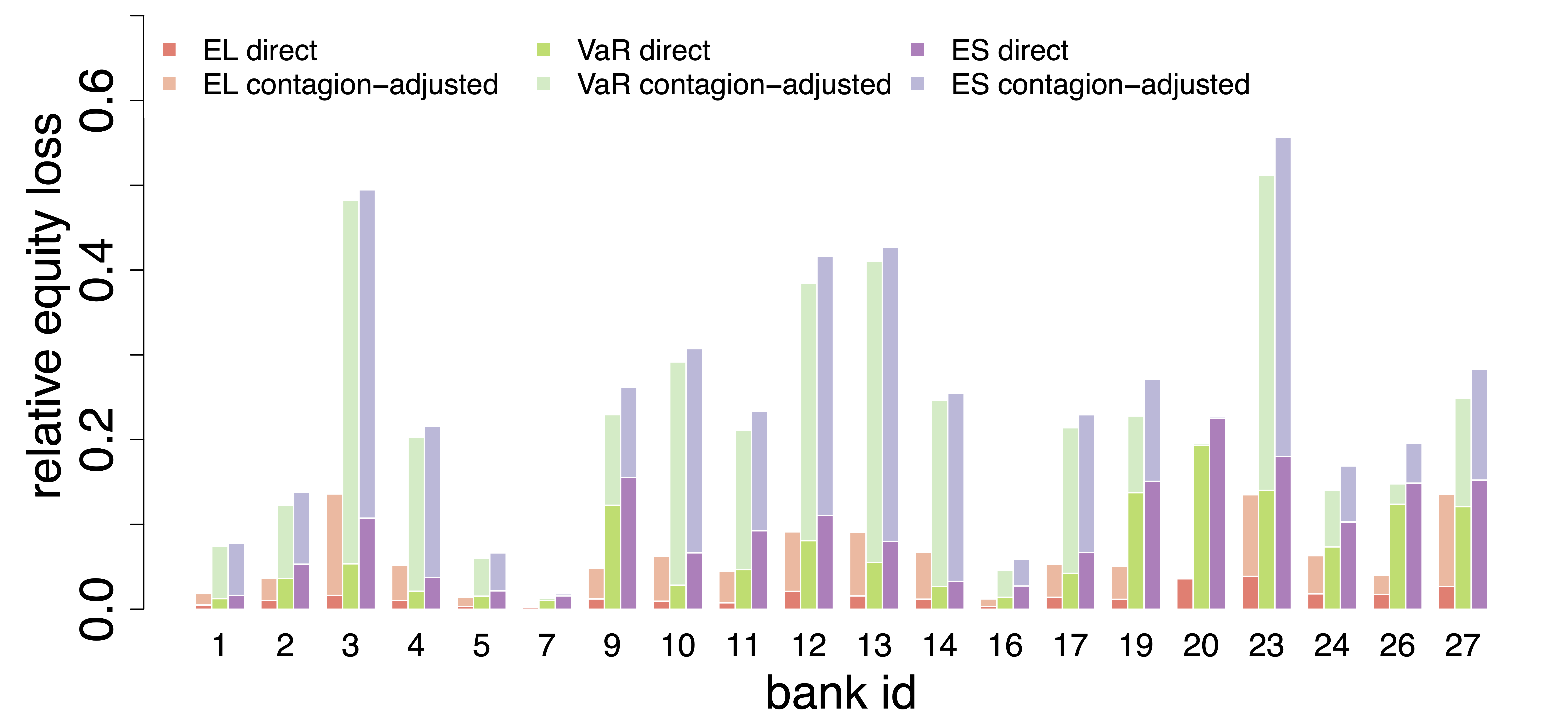

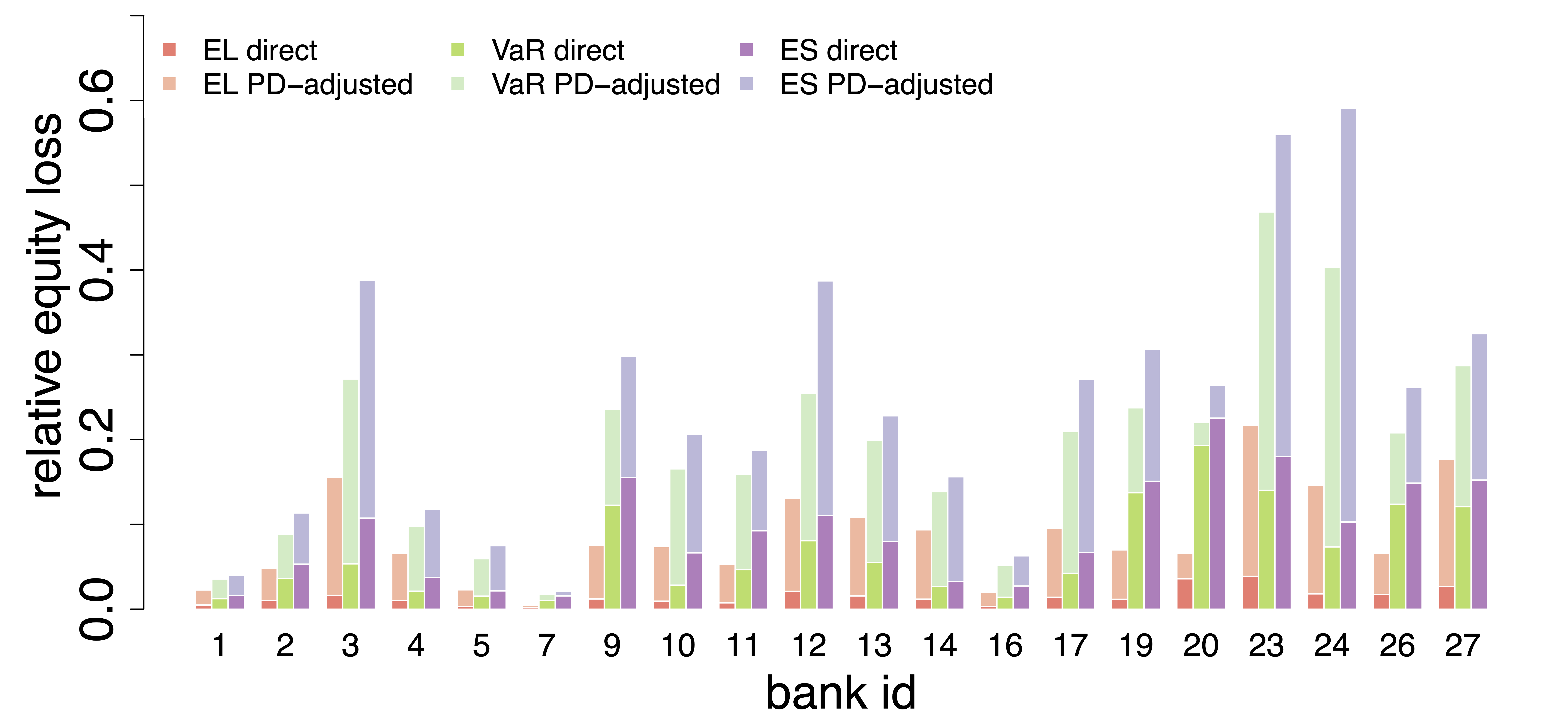

We next focus on how the credit risk exposure of individual banks is amplified in the presence of supply chain contagion. We measure the amplification by calculating the EL, VaR, and ES for the simulated losses of each banks’ commercial loan portfolio, once without supply chain contagion (direct losses only) and with supply chain contagion. We calculate the direct losses, , and the supply chain contagion adjusted ones, with a Monte Carlo simulation for 10,000 initial shock scenarios, , as described in Section 2, step 3. EL is the mean of the losses, VaR0.95 is the 95% quantile of losses, and the ES0.95 is the average over the 500 largest losses. Figure 6 shows the EL (red), VaR (green), and the ES (purple) for every bank from the direct (dark shade) and contagion-adjusted (light shade) loss distributions. Indices of banks are the same as in Fig.5. We skip banks 6, 8, 15, 18, 21, 22, and 25 that have less than clients. The y-axis shows the value of the respective risk measures. Note that the bars are not stacked (dark bars are always plotted in front of light bars) meaning that the height of the light shaded bars is the overall value of the risk measure with supply chain contagion. The height of the light bars minus the height of the dark bars gives the additional risk from contagion (marginal systemic risk). The plot shows that EL, VaR, and ES are substantially lower when the supply chain is not taken into account. The average risk amplification factor across the 20 banks are found to be , , and . Note that the overall levels of commercial credit risk strongly differ across banks — again potential reasons being differences in business models, etc. as outlined before. Amplification factors also differ across banks.

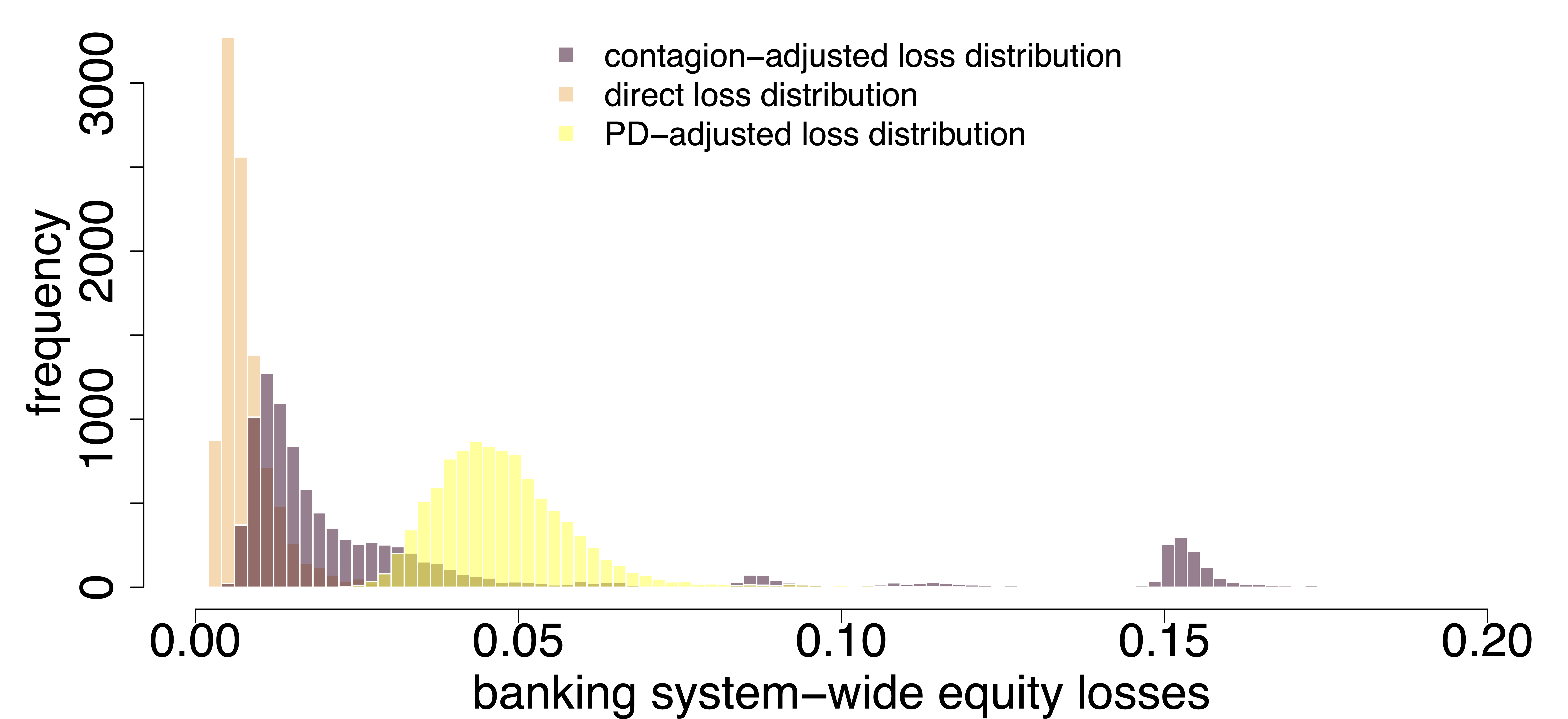

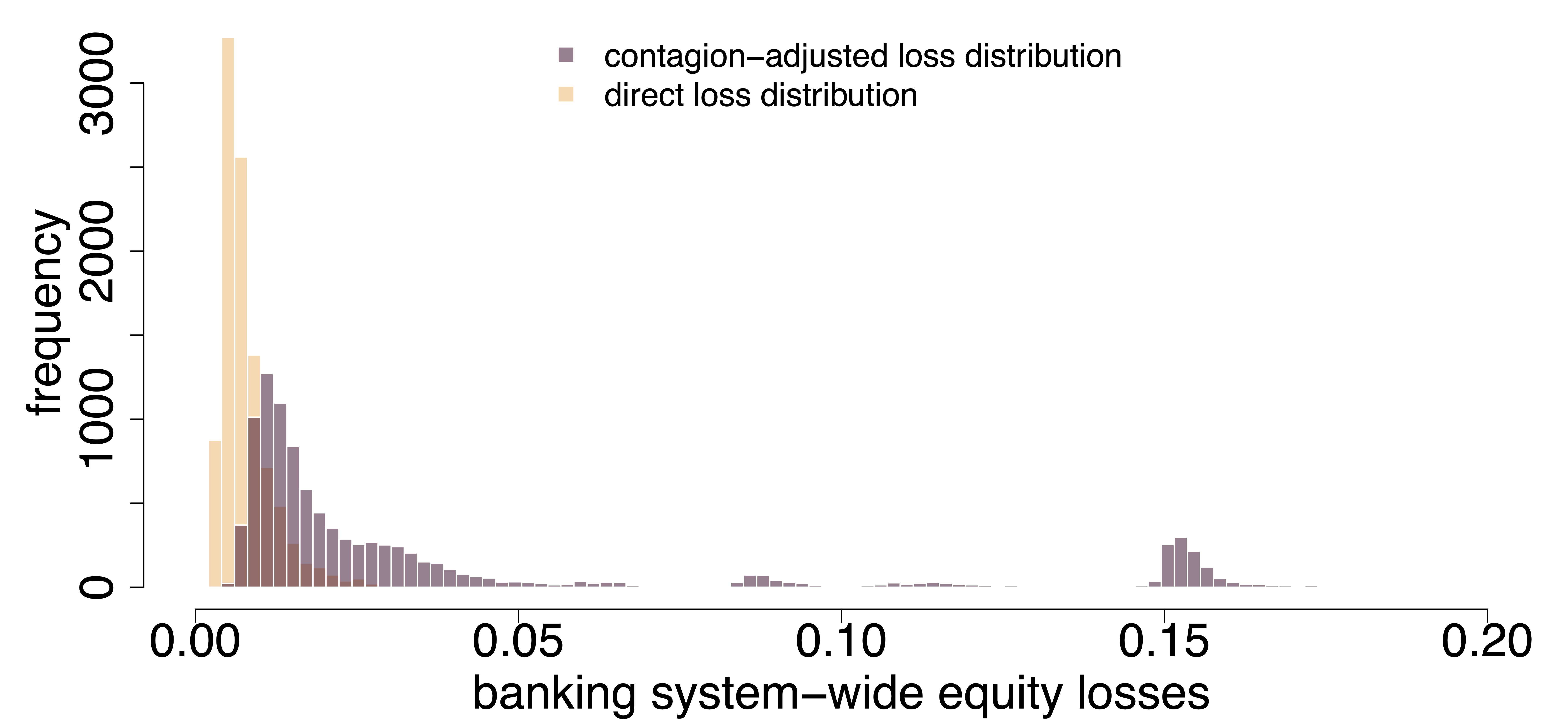

Finally, in Fig.7 we present the system-wide histogram of direct losses, (orange) and the contagion-adjusted ones, (brown), summed over all banks; see Eq. (5). The -axis denotes the fraction of equity that is lost due to an initial shock scenario, , the y-axis shows the frequency the respective loss. One clearly sees that the two distributions differ substantially. The direct loss distribution is concentrated at low values and has only scenarios where a maximum of around is reached. The contagion-adjusted loss distribution is bimodal with most weight centered around . It slowly decays with a fat tail and has a second concentration point around of system wide equity losses. In between there are a few scenarios yielding losses of around and . This pattern is driven by the shape of the FSRI distribution; see Fig. 2. The most risky firms cause system-wide losses of around of equity. If one of these firms fails in an initial shock scenario, , they trigger a supply chain cascade leading to losses of around . Similarly, there are a few high systemic risk firms causing losses of around and of equity, explaining the respective parts in the loss distributions. The risk respective amplification factors for EL, VaR, and ES are , , and , respectively.

5 Discussion

A thorough assessment of credit risk is central to a sustainable banking sector. Classical credit rating models hitherto do not include information about supply chain networks (SCNs) on the firm level, their structures, and default dynamics in a systematic way. Here we introduced a fully data-driven model (containing a minimum number of free parameters) that allows us to quantitatively estimate how SCN contagion translates to capital losses in the banking sector and to what extent it affects financial stability. The model is a 1:1 agent-based representation of (almost)every single firm and bank in the national economy of Hungary in 2019, containing more than 240,000 firms, 27 banks, including their balance sheets and income statements, along with more than million supply links and bank-firm loans. A unique feature of this model is that the 1:1 representation of the real economy is linked to financial system through credit exposures. It allows us to study how risks spread from the real economy (production layer) to the financial layer. We follow the philosophy that parameters in ABMs should not be freely assumed but fully are determined and fixed by the data. This is the reason why we refrain from including additional features to the model that we can not calibrate with available data, such as details of the rewiring dynamics. For estimating the production functions of the companies and a simple substitutability dynamics we follow Diem et al. (2022a, 2023). As, at this stage, we do not employ rewiring dynamics the model is not yet predictive or generative. It has been conceived in the spirit of stress testing. It is designed to estimate and monitor the likely costs of hypothetical external shocks, assuming that there are no interventions of governments or central banks. It is not designed for medium- and long term predictions but rather for short time scales below the typical times that are needed to restructure the SCN.

Within this framework our results show that the failure of very few individual firms (those that can cause large cascades of supply chain contagion), can lead to system-wide bank equity losses in the banking sector of around . These losses can be mostly attributed to supply chain contagion induced defaults of firms (indirect losses); the loan write-offs caused by the initially failing firms (direct losses) only play a minor role. Half of the financial system’s losses, approximately , caused by an initial failure of one of the riskiest firms, can be linked to firms defaulting only due to their insufficient liquidity buffers. This implies that increasing liquidity provision to firms that do not face negative equity levels can alleviate already large parts of loan defaults. However, a substantial amount of bank capital losses (approximately ) would still be caused by firms with larger losses than equity in response to supply chain disruptions.

Our results also indicate, that those firms causing the largest losses do have no, or relatively small, loans from Hungarian banks (they could either borrow from the capital market or from banks abroad), while firms with the largest loans cause small indirect supply-contagion-induced financial losses. This implies that firms with the largest bank-loans might not be the most relevant for monitoring financial stability, but those that can cause substantial indirect defaults. This type of firms would be clearly missed when not taking supply chain contagion into account. It is indicated that regulators could benefit from building up capabilities to monitor supply chain generated and amplified systemic risks. Governments and regulators could collect this type of data as done today already in about a dozen of countries (Bacilieri et al., 2022).

Analysis of system-wide bank equity losses shows that the bulk of the indirect losses caused by the systemically riskiest firms are suffered by 10 banks. These make up for around of the entire equity, of loans, but have a substantial number, , of corporate clients. This indicates that a relatively large number of clients can potentially expose banks to direct and indirect losses, i.e., systemic risk.

Within our framework we performed a stylized stress test by sampling initial shocks based on randomly failing about of firms (based on their estimated default probabilities) and simulating the spread of the production network contagion to the financial layer. This way we create 10,000 initial shock scenarios and obtain two loss distributions for each bank, one with and the other without SCN contagion. The results suggest a substantial amplification of financial risks, when SCN contagion is taken into account. On average, expected losses of banks are amplified by a factor of , value at risk - by a factor of , and expected shortfall - by a factor of . Amplification factors differ across banks. Nevertheless, if events trigger supply-chain contagion, then direct losses of bank equity are negligible in comparison to the indirect losses caused by SCN contagion. This implies that shock propagation in SCNs can potentially lead to substantially fatter tails in banks’ loan defaults, suggesting that capital ratios should factor in these risks.

The observed amplification of credit risk measures by unambiguously demonstrates that supply chain contagion is an extremely important factor for a realistic credit risk assessment in a world with increasing numbers of supply chain disruptions. It also is a message that current practice could systematically and grossly underestimates capital requirements and sustainable interest rates when large exogenous shocks trigger SCN contagion. The present study strongly indicates that supply chain contagion poses unexpectedly large systemic risks to financial stability. In practice the default probability estimates (performed by banks) implicitly also account for defaults due to SCN contagion occurring in normal times. This is because the data (past default events in the loan portfolios) contains defaults that originated from SCN contagion, e.g., the failure of a major customer or supplier). On the one hand, our results hint at the fact that SCN contagion actually is a substantial driver of credit risk. On the other hand most data points to correspond to times where no major SCN contagion has occurred or it has been cushioned by government interventions, such as during the COVID-19 pandemic. Therefore, credit risk might be underestimated. Mis-estimations of correlations in housing loans played a major role in causing the financial crises 2007/2008. Ignoring that supply chain networks have the potential to cause substantial default correlations can lead to unexpected financial losses due to neglecting economic mechanisms leading to correlated defaults — this time of firms.

The presented study has a number of obvious limitations. Foremost, our results depend on a range of assumptions that are relevant for the micro-simulation model. These include the supply-chain contagion mechanism itself, how production disruptions due to supply-chain contagion translate into financial losses for firms, and how the insolvency of firms translates into capital losses for banks. We take a pragmatic approach for firm behaviour. In the proposed setting we assume that revenues and material costs are reduced proportional to the production loss that a firm suffers after the SCN contagion. In this way all firms are treated equally without any consideration of their industry affiliation, or nuances in their business models. Given the present data it is not feasible to account for varying transmission mechanisms according to business models. However, future improvements could take into account the industry sector of firms and other not yet utilized items of their income statements and balance sheets. A second assumption is the condition under which firms default. We use firm’s equity and short term liquidity (cash, short term claims and securities subtracted by short term liabilities) as buffers against income losses. If the losses exceed one of the buffers we use this as an indicator of default. Our current buffer calculation neglects that firms could, e.g., ask for additional liquidity from banks, or tap additional equity from their owners and, hence, avert a default. A further assumption is the value of the loss given default (LGD). We assume it to be at of the outstanding principal. This means that we do not take into account the possibility of instalment postponement, restructuring of firms in case of any problems or use of collateral by banks. However, for the short term view this is not unrealistic as collection and resolution processes can last years. Further, the production loss of a firm, its bankruptcy and default, and losses of banks happen immediately, without a detailed concept of time being modelled. In this manner our results suggest upper limit of possible losses. Finally, the data even though unique in coverage has shortcomings. The supply-chain network is not entirely complete; small firms and import-export links are missing. We only included the largest banks due to data availability, which, however, should affect results only to a limited extent since the majority of bank-firm loans and loan volume are covered.

Data driven 1:1 models along the lines presented here can be used as a base to assess governmental recovery policies, such as loan guarantees for firms, revenue loss subsidies that have been implemented, for example during the COVID-19 pandemic. Applying it to specific shock scenarios such as pandemic restrictions or devaluations of assets due to the climate change, would be natural future extensions. Model assumptions would have to be calibrated to the specific initial shock scenario. Maybe the most important step to make the model more practicable, also as a predictive tool, is to include price information that is so-far missing. Further, the contagion between banks needs to be modelled as well as the financing for firms’ production activities. Also more detailed behavioural mechanisms for firms and banks should be included in future work.

In a wider context, the demonstrated risk amplification mechanism through the coupling of the financial network to the SCN can be seen as a concrete example that “networks of networks” are generally expected to show a significant risk-increase in comparison as defaults on simple networks Gao et al. (2011).

References

- Act (1991) Hungarian Insolvency Code (Act xlix of 1991 on Bankruptcy Proceedings and Liquidation Proceedings) 1991;.

- Acharya et al. (2014) Acharya V, Engle R, Pierret D. Testing macroprudential stress tests: The risk of regulatory risk weights. Journal of Monetary Economics 2014;65:36–53. URL: https://www.sciencedirect.com/science/article/pii/S0304393214000725. doi:https://doi.org/10.1016/j.jmoneco.2014.04.014; carnegie-Rochester-NYU Conference Series on Public Policy “A Century of Money, Banking, and Financial Instability” held at the Tepper School of Business, Carnegie Mellon University on November 15-16, 2013.

- Arnold et al. (2012) Arnold B, Borio C, Ellis L, Moshirian F. Systemic risk, macroprudential policy frameworks, monitoring financial systems and the evolution of capital adequacy. Journal of Banking & Finance 2012;36(12):3125–32. URL: https://www.sciencedirect.com/science/article/pii/S0378426612002038. doi:https://doi.org/10.1016/j.jbankfin.2012.07.023; systemic risk, Basel III, global financial stability and regulation.

- Bacilieri et al. (2022) Bacilieri A, Borsos A, Reisch , Astudillo-Estevez P, Lafond F. Firm-level production networks: what do we (really) know? Technical Report; work in progress; 2022.

- Banai et al. (2016) Banai Á, Körmendi G, Lang P, Vágó N. A magyar kis-és középvállalati szektor hitelkockázatának modellezése, mnb-tanulmányok 123. 2016.

- Barrot and Sauvagnat (2016) Barrot JN, Sauvagnat J. Input Specificity and the Propagation of Idiosyncratic Shocks in Production Networks. The Quarterly Journal of Economics 2016;131(3):1543–92. URL: https://doi.org/10.1093/qje/qjw018. doi:10.1093/qje/qjw018. arXiv:https://academic.oup.com/qje/article-pdf/131/3/1543/30636709/qjw018.pdf.

- Bartik et al. (2020) Bartik AW, Bertrand M, Cullen Z, Glaeser EL, Luca M, Stanton C. The impact of covid-19 on small business outcomes and expectations. Proceedings of the National Academy of Sciences 2020;117(30):17656--66. URL: https://www.pnas.org/doi/abs/10.1073/pnas.2006991117. doi:10.1073/pnas.2006991117.

- Basel Committee on Banking Supervision (1988) Basel Committee on Banking Supervision . Basel I: International convergence of capital measurement and capital standards. 1988.

- Basel Committee on Banking Supervision (2001) Basel Committee on Banking Supervision . The Internal Ratings-Based Approach. 2001.

- Basel Committee on Banking Supervision (2004) Basel Committee on Banking Supervision . Basel II: International convergence of capital measurement and capital standards. 2004.

- Basel Committee on Banking Supervision (2011) Basel Committee on Banking Supervision . Basel III: A global regulatory framework for more resilient banks and banking systems revised version June 2011. 2011.

- Basel Committee on Banking Supervision (2015) Basel Committee on Banking Supervision . Guidance on credit risk and accounting for expected credit losses. 2015.

- Basel Committee on Banking Supervision (2017) Basel Committee on Banking Supervision . Guidance to banks on non-performing loans. 2017.

- Basel Committee on Banking Supervision (2021a) Basel Committee on Banking Supervision . Climate-related financial risks – measurement methodologies. 2021a.

- Basel Committee on Banking Supervision (2021b) Basel Committee on Banking Supervision . Climate-related risk drivers and their transmission channels. 2021b.

- Basel Committee on Banking Supervision (2022) Basel Committee on Banking Supervision . Principles for the effective management and supervision of climate-related financial risks. 2022.

- Battiston et al. (2021) Battiston S, Dafermos Y, Monasterolo I. Climate risks and financial stability. Journal of Financial Stability 2021;54:100867. URL: https://www.sciencedirect.com/science/article/pii/S1572308921000267. doi:https://doi.org/10.1016/j.jfs.2021.100867.

- Battiston and Martinez-Jaramillo (2018) Battiston S, Martinez-Jaramillo S. Financial networks and stress testing: Challenges and new research avenues for systemic risk analysis and financial stability implications. Journal of Financial Stability 2018;35:6--16. URL: https://www.sciencedirect.com/science/article/pii/S157230891830192X. doi:https://doi.org/10.1016/j.jfs.2018.03.010; network models, stress testing and other tools for financial stability monitoring and macroprudential policy design and implementation.

- Battiston et al. (2012) Battiston S, Puliga M, Kaushik R, Tasca P, Caldarelli G. DebtRank: Too Central to Fail? Financial Networks, the FED and Systemic Risk. Scientific Reports 2012;2(1):541. URL: https://doi.org/10.1038/srep00541. doi:10.1038/srep00541.

- Borio et al. (2014) Borio C, Drehmann M, Tsatsaronis K. Stress-testing macro stress testing: Does it live up to expectations? Journal of Financial Stability 2014;12:3--15. URL: https://www.sciencedirect.com/science/article/pii/S1572308913000454. doi:https://doi.org/10.1016/j.jfs.2013.06.001; reforming finance.

- Borsos and Mero (2020) Borsos A, Mero B. Shock propagation in the banking system with real economy feedback. Technical Report; MNB Working Papers; 2020.

- Borsos and Stancsics (2020) Borsos A, Stancsics M. Unfolding the hidden structure of the Hungarian multi-layer firm network. Technical Report; MNB Occasional Papers; 2020.

- Boss et al. (2004) Boss M, Elsinger H, Summer M, Thurner S. Network topology of the interbank market. Quantitative Finance 2004;4(6):677--84. URL: https://www.tandfonline.com/doi/abs/10.1080/14697680400020325. doi:10.1080/14697680400020325. arXiv:https://www.tandfonline.com/doi/pdf/10.1080/14697680400020325.

- Brunetti et al. (2021) Brunetti C, Dennis B, Gates D, Hancock D, Ignell D, Kiser EK, Kotta G, Kovner A, Rosen RJ, Tabor NK. Climate change and financial stability. FEDS Notes Washington: Board of Governors of the Federal Reserve System 2021;URL: https://doi.org/10.17016/2380-7172.2893.

- Buncic and Melecky (2013) Buncic D, Melecky M. Macroprudential stress testing of credit risk: A practical approach for policy makers. Journal of Financial Stability 2013;9(3):347--70. URL: https://www.sciencedirect.com/science/article/pii/S1572308912000666. doi:https://doi.org/10.1016/j.jfs.2012.11.003; central banking 2.0.

- Burger et al. (2022) Burger C, et al. Defaulting Alone: The Geography of Sme Owner Numbers and Credit Risk in Hungary. Technical Report; Magyar Nemzeti Bank (Central Bank of Hungary); 2022.

- Carvalho et al. (2020) Carvalho VM, Nirei M, Saito YU, Tahbaz-Salehi A. Supply Chain Disruptions: Evidence from the Great East Japan Earthquake. The Quarterly Journal of Economics 2020;136(2):1255--321. URL: https://doi.org/10.1093/qje/qjaa044. doi:10.1093/qje/qjaa044. arXiv:https://academic.oup.com/qje/article-pdf/136/2/1255/36725306/qjaa044.pdf.

- Cont et al. (2010) Cont R, Moussa A, Santos E. Network Structure and Systemic Risk in Banking Systems. SSRN 2010;doi:10.2139/ssrn.1733528.

- Cont and Schaanning (2017) Cont R, Schaanning E. Fire sales, indirect contagion and systemic stress testing. SSRN 2017;doi:http://dx.doi.org/10.2139/ssrn.2541114.

- Cox (1958) Cox DR. The regression analysis of binary sequences. Journal of the Royal Statistical Society: Series B (Methodological) 1958;20(2):215--32. doi:https://doi.org/10.1111/j.2517-6161.1958.tb00292.x.

- Demir et al. (2022) Demir B, Javorcik B, Michalski TK, Ors E. Financial Constraints and Propagation of Shocks in Production Networks. The Review of Economics and Statistics 2022;:1--46URL: https://doi.org/10.1162/rest_a_01162. doi:10.1162/rest_a_01162. arXiv:https://direct.mit.edu/rest/article-pdf/doi/10.1162/rest_a_01162/1983885/rest_a_01162.pdf.

- Diem et al. (2022a) Diem C, Borsos A, Reisch T, Kertész J, Thurner S. Quantifying firm-level economic systemic risk from nation-wide supply networks. Scientific Reports 2022a;12(1):7719. URL: https://doi.org/10.1038/s41598-022-11522-z. doi:10.1038/s41598-022-11522-z.

- Diem et al. (2022b) Diem C, Borsos A, Reisch T, Kertész J, Thurner S. Supplementary Information Quantifying firm-level economic systemic risk from nation-wide supply networks. Scientific Reports 2022b;12(1):7719. URL: https://doi.org/10.1038/s41598-022-11522-z. doi:10.1038/s41598-022-11522-z.

- Diem et al. (2023) Diem C, Borsos A, Reisch T, Kertész J, Thurner S. Estimating the loss of economic predictability from aggregating firm-level production networks. arXiv preprint arXiv:230211451 2023;.

- Diem et al. (2020) Diem C, Pichler A, Thurner S. What is the minimal systemic risk in financial exposure networks? Journal of Economic Dynamics and Control 2020;116:103900. URL: https://www.sciencedirect.com/science/article/pii/S0165188920300683. doi:https://doi.org/10.1016/j.jedc.2020.103900.

- EBA (2020) EBA . EBA report on big data and advanced analytics. European Banking Authority, 2020.

- ECB (2020) ECB . Our response to the coronavirus pandemic. 2020. URL: https://www.ecb.europa.eu/home/search/coronavirus/html/index.en.html.

- ECB/ESRB (2022) ECB/ESRB . The macroprudential challenge of climate change. ESRB and ECB report 2022;.

- Elsinger et al. (2006) Elsinger H, Lehar A, Summer M. Risk Assessment for Banking Systems. Management Science 2006;52(9):1301--14. doi:10.1287/mnsc.1060.0531.

- Farmer et al. (2022) Farmer JD, Kleinnijenhuis AM, Schuermann T, Wetzer T. Handbook of financial stress testing. Cambridge University Press, 2022.

- Farmer et al. (2021) Farmer JD, Kleinnijenhuis AM, Wetzer T. Stress testing the financial macrocosm. Forthcoming in Handbook of Financial Stress Testing (CUP, 2022) 2021;doi:http://dx.doi.org/10.2139/ssrn.3913749.

- Feinstein et al. (2017) Feinstein Z, Rudloff B, Weber S. Measures of systemic risk. SIAM Journal on Financial Mathematics 2017;8(1):672--708. URL: https://doi.org/10.1137/16M1066087. doi:10.1137/16M1066087.

- Gai and Kapadia (2010) Gai P, Kapadia S. Contagion in financial networks. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences 2010;466(2120):2401--23. doi:10.1098/rspa.2009.0410.

- Gao et al. (2011) Gao J, Buldyrev SV, Havlin S, Stanley HE. Robustness of a network of networks. Phys Rev Lett 2011;107:195701. URL: https://link.aps.org/doi/10.1103/PhysRevLett.107.195701. doi:10.1103/PhysRevLett.107.195701.

- Gauthier et al. (2012) Gauthier C, Lehar A, Souissi M. Macroprudential capital requirements and systemic risk. Journal of Financial Intermediation 2012;21(4):594--618. doi:10.1016/j.jfi.2012.01.005.

- Glasserman and Young (2016) Glasserman P, Young HP. Contagion in financial networks. Journal of Economic Literature 2016;54(3):779--831. URL: https://www.aeaweb.org/articles?id=10.1257/jel.20151228. doi:10.1257/jel.20151228.

- Gorgijevska and Gorgieva-Trajkovska (2019) Gorgijevska A, Gorgieva-Trajkovska O. Qualitative and quantitative analysis of creditworthiness of the companies. Journal of Economics 2019;URL: https://js.ugd.edu.mk/index.php/JE/article/view/2736.

- Guth et al. (2020) Guth M, Lipp C, Puhr C, Schneider M, et al. Modeling the COVID-19 effects on the Austrian economy and banking system. Technical Report; 2020.

- Hallegatte (2008) Hallegatte S. An adaptive regional input-output model and its application to the assessment of the economic cost of Katrina. Risk Analysis: An International Journal 2008;28(3):779--99. doi:https://doi.org/10.1111/j.1539-6924.2008.01046.x.

- Hamilton (2020) Hamilton WL. Graph representation learning. Synthesis Lectures on Artifical Intelligence and Machine Learning 2020;14(3):1--159.

- Herring and Schuermann (2022) Herring RJ, Schuermann T. Objectives and challenges of stress testing. Handbook of Financial Stress Testing 2022;:9.

- Huremovic et al. (2020) Huremovic K, Jiménez G, Moral-Benito E, Vega-Redondo F, Peydró JL, et al. Production and Financial Networks in Interplay: Crisis Evidence from Supplier-Customer and Credit Registers 2020;.

- IASB (2014) IASB . International Accounting Standards (IFRS 9, Financial Instruments) 2014;.

- Inoue and Todo (2019) Inoue H, Todo Y. Firm-level propagation of shocks through supply-chain networks. Nature Sustainability 2019;2(9):841--7. URL: https://doi.org/10.1038/s41893-019-0351-x. doi:10.1038/s41893-019-0351-x.

- Klimek et al. (2015) Klimek P, Poledna S, Doyne Farmer J, Thurner S. To bail-out or to bail-in? Answers from an agent-based model. Journal of Economic Dynamics and Control 2015;50:144--54. URL: https://www.sciencedirect.com/science/article/pii/S0165188914002097. doi:https://doi.org/10.1016/j.jedc.2014.08.020; Crises and Complexity.

- Landaberry et al. (2021) Landaberry V, Caccioli F, Rodriguez-Martinez A, Baron A, Martinez-Jaramillo S, Lluberas R. The contribution of the intra-firm exposures network to systemic risk. Latin American Journal of Central Banking 2021;2(2):100032. URL: https://www.sciencedirect.com/science/article/pii/S2666143821000120. doi:https://doi.org/10.1016/j.latcb.2021.100032.

- Levy-Carciente et al. (2015) Levy-Carciente S, Kenett DY, Avakian A, Stanley HE, Havlin S. Dynamical macroprudential stress testing using network theory. Journal of Banking & Finance 2015;59:164--81. URL: https://www.sciencedirect.com/science/article/pii/S0378426615001454. doi:https://doi.org/10.1016/j.jbankfin.2015.05.008.

- McNeil et al. (2015) McNeil AJ, Frey R, Embrechts P. Quantitative Risk Ranagement: Concepts, Techniques and Tools. Princeton University Press, 2015.

- Milstein and Wessel (2021) Milstein E, Wessel D. What did the Fed do in response to the COVID-19 crisis. Brookings Institution 2021;17. URL: https://www.brookings.edu/research/fed-response-to-covid19/.

- Moretto et al. (2019) Moretto A, Grassi L, Caniato F, Giorgino M, Ronchi S. Supply chain finance: From traditional to supply chain credit rating. Journal of Purchasing and Supply Management 2019;25(2):197--217. URL: https://www.sciencedirect.com/science/article/pii/S1478409218301833. doi:https://doi.org/10.1016/j.pursup.2018.06.004; supply Chain Finance: Historical Foundations, Current Research, Future Developments.

- Pichler et al. (2022a) Pichler A, Hurt J, Reisch T, Stangl J, Thurher S. Austria without russian natural gas? Expected economic impacts of a drastic gas supply shock and mitigation strategies. CSH Policy Brief 2022a;.

- Pichler et al. (2022b) Pichler A, Pangallo M, del Rio-Chanona RM, Lafond F, Farmer JD. Forecasting the propagation of pandemic shocks with a dynamic input-output model. Journal of Economic Dynamics and Control 2022b;144:104527. URL: https://www.sciencedirect.com/science/article/pii/S0165188922002317. doi:https://doi.org/10.1016/j.jedc.2022.104527.

- Poledna et al. (2018) Poledna S, Hinteregger A, Thurner S. Identifying Systemically Important Companies by Using the Credit Network of an Entire Nation. Entropy 2018;20(10). URL: https://www.mdpi.com/1099-4300/20/10/792. doi:10.3390/e20100792.

- Poledna et al. (2021) Poledna S, Martínez-Jaramillo S, Caccioli F, Thurner S. Quantification of systemic risk from overlapping portfolios in the financial system. Journal of Financial Stability 2021;52:100808. URL: https://www.sciencedirect.com/science/article/pii/S1572308920301108. doi:https://doi.org/10.1016/j.jfs.2020.100808; network models and stress testing for financial stability: the conference.

- Poledna et al. (2015) Poledna S, Molina-Borboa JL, Martínez-Jaramillo S, van der Leij M, Thurner S. The multi-layer network nature of systemic risk and its implications for the costs of financial crises. Journal of Financial Stability 2015;20:70--81. doi:10.1016/j.jfs.2015.08.001.

- Potter and Schuermann (2020) Potter S, Schuermann T. Stressing the Fed Stress Tests Against COVID-19. 2020. URL: https://europepmc.org/article/PPR/PPR242634. doi:10.2139/ssrn.3635187.

- RegulationEU (2013) RegulationEU . Regulation (EU) no 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012 2013;.

- Shi et al. (2022) Shi S, Tse R, Luo W, D’Addona S, Pau G. Machine learning-driven credit risk: a systemic review. Neural Computing and Applications 2022;:1--13.

- Silva et al. (2018) Silva TC, da Silva Alexandre M, Tabak BM. Bank lending and systemic risk: A financial-real sector network approach with feedback. Journal of Financial Stability 2018;38:98--118. URL: https://www.sciencedirect.com/science/article/pii/S1572308916302121. doi:https://doi.org/10.1016/j.jfs.2017.08.006.

- Thurner (2022) Thurner S. A Complex Systems Perspective on Macroprudential Regulation, in: J. D. Farmer et al. (eds.), Handbook of Financial Stress Testing. Cambridge University Press 2022;5:593–634. URL: https://www.cambridge.org/core/books/abs/handbook-of-financial-stress-testing/complex-systems-perspective-on-macroprudential-regulation/4317CB6A85321EBCA52F4DBC64E58330.

- Thurner and Poledna (2013) Thurner S, Poledna S. DebtRank-transparency: Controlling systemic risk in financial networks. Scientific Reports 2013;3:1888. doi:10.1038/srep01888.

- Vazquez et al. (2012) Vazquez F, Tabak BM, Souto M. A macro stress test model of credit risk for the Brazilian banking sector. Journal of Financial Stability 2012;8(2):69--83. URL: https://www.sciencedirect.com/science/article/pii/S1572308911000362. doi:https://doi.org/10.1016/j.jfs.2011.05.002.

- Willner et al. (2018) Willner SN, Otto C, Levermann A. Global economic response to river floods. Nature Climate Change 2018;8(7):594--8. URL: https://doi.org/10.1038/s41558-018-0173-2. doi:10.1038/s41558-018-0173-2.

Appendix A Economic Systemic Risk Index

We use the supply-chain network, , ( matrix, ), where is the trade volume between buyer, , and supplier, . Therefore, total purchase volume of firm , the in-strength, is , and total amount of sales, the out-strength, is .

Every firm, , is equipped with a generalized Leontief production function, defined as

| (12) |

is the set of essential inputs and is the set of non-essential inputs of firm . The parameters are technologically determined coefficients, is the production level possible without non-essential inputs and is chosen to interpolate between the full production level (with all inputs) and . All parameters are determined by , and . Note, that labour, and capital, , are not explicitly modelled, due to the short-term perspective of our model. The initial labour shock is modelled as the remaining production level, . We simulate how the initial supply and demand reductions spread downstream to the direct and indirect buyers and upstream to the direct and indirect suppliers of the initially affected firm, by recursively updating the production levels of all firms in the network. We update for each firm the production output at , given production levels of its suppliers, , at time as

The production output of firm at , given the production level of its customers, , at time is computed as

| (14) |

For details and the full algorithm we employ see the methods section in Diem et al. (2022a).

The algorithm can be used to asses a systemic importance of every firm in the SCN. By defaulting a firm, i.e., using a scenario , and running the supply chain contagion model, we end up with remaining production levels at time of firms in the network represented by a vector, . The economic systemic risk index (ESRI) of a firm is now defined as

| (15) |

The losses in response to more general shock scenarios, , are modelled with the same shock propagation dynamics as is demonstrated in Diem et al. (2023) for COVID-19 shock scenarios.

Appendix B Central bank methodology to PD-estimation for all Hungarian firms liable to corporate tax