Optimal Battery Charge Scheduling For Revenue Stacking Under Operational Constraints Via Energy Arbitrage

Abstract

As the share of variable renewable energy sources increases in the electricity mix, new solutions are needed to build a flexible and reliable grid. Energy arbitrage with battery storage systems supports renewable energy integration into the grid by shifting demand and increasing the overall utilization of power production systems. In this paper, we propose a mixed integer linear programming model for energy arbitrage on the day-ahead market, that takes into account operational and availability constraints of asset owners willing to get an additional revenue stream from their storage asset. This approach optimally schedules the charge and discharge operations associated with the most profitable trading strategy, and achieves between 80% and 90% of the maximum obtainable profits considering one-year time horizons using the prices of electricity in multiple European countries including Germany, France, Italy, Denmark, and Spain.

I Introduction

In IEA’s pathway to net-zero CO2 emissions by 2050 [1], electricity accounts for 50% of energy use in 2050, with 70% produced by wind and solar photovoltaic. As reliance on variable energy sources (VES) increases, important investments in grid-scale storage solutions are required to balance their variable and non-dispatchable aspects, and to increase grid flexibility, capacity, and reliability [2]. While Pumped-storage hydroelectricity (PHS) represents 90% of the world’s storage [3], battery system storage (BSS) are expected to see the largest market growth and can play a similar role [4]. BSS have many use cases, from replacing backup emergency power units in hospitals to frequency response systems. Some of the applications of BSS are listed in [5], including energy arbitrage, which helps accommodate changes in demand and production by charging BSS during low-cost periods and discharging them during consumption peaks when prices are high. This assists the integration of renewable energy and allows higher utilization of VES by shifting demand to align with important production periods. The profitability of energy arbitrage depends on factors such as battery cost and price differences between low and high-demand periods. Intraday price variability represents an opportunity for asset owners to stack additional revenue streams obtained from arbitrage to their existing ones, providing additional incentives for operating and investing in grid-scale BSS. Furthermore, Energy arbitrage increases the return on investment (ROI) of BSS. Paper [6] shows other positive societal impacts, such as increasing the return to renewable production and reducing CO2 emissions. Energy arbitrage with BSS requires a charging/ discharging schedule. This schedule needs to consider battery characteristics, such as the charging curve, maximum cycles per day, and discharging rate. Many papers have dealt with this problem using model predictive control based on linear programming (LP) or mixed-integer linear programming (MILP) optimizations [7, 8, 9, 10, 11]. However, those approaches often assume constant charging rates and no battery degradation.

In this paper, we propose an approach to generate optimal charging schedules for arbitrage on the Day Ahead Market (DAM) under availability constraints that considers variable charging rates and battery degradation. Our contributions are:

-

•

A battery model with variable charging rates, discharge efficiency decrease, and capacity fading, that can be parametrized by the user.

-

•

A MILP formulation of the profit maximization task via energy arbitrage on the DAM.

-

•

A Python library that outputs daily optimal schedules from user inputs using built-in price forecasting, and allows running the algorithm on historical prices.

-

•

A quantitative comparison of the performances of our predictive optimization model relying on price forecasts with a baseline that outputs optimal schedules a posteriori, for different key hyperparameters and different European countries.

-

•

A discussion of the impact of capacity fading, discharge efficiency decrease, and charging rates on profits.

Our battery model and optimization framework are introduced in Section II. The main results: the comparison of our output schedules to the optimal a posteriori schedule, the performances of our algorithm on datasets considering a one-year time horizon in multiple European countries, and the discussion of the impact of prediction accuracy and battery degradation on the obtained profits are presented in Section III. In Section IV we conclude and discuss future work.

II Methodology

II-A Desired algorithm output

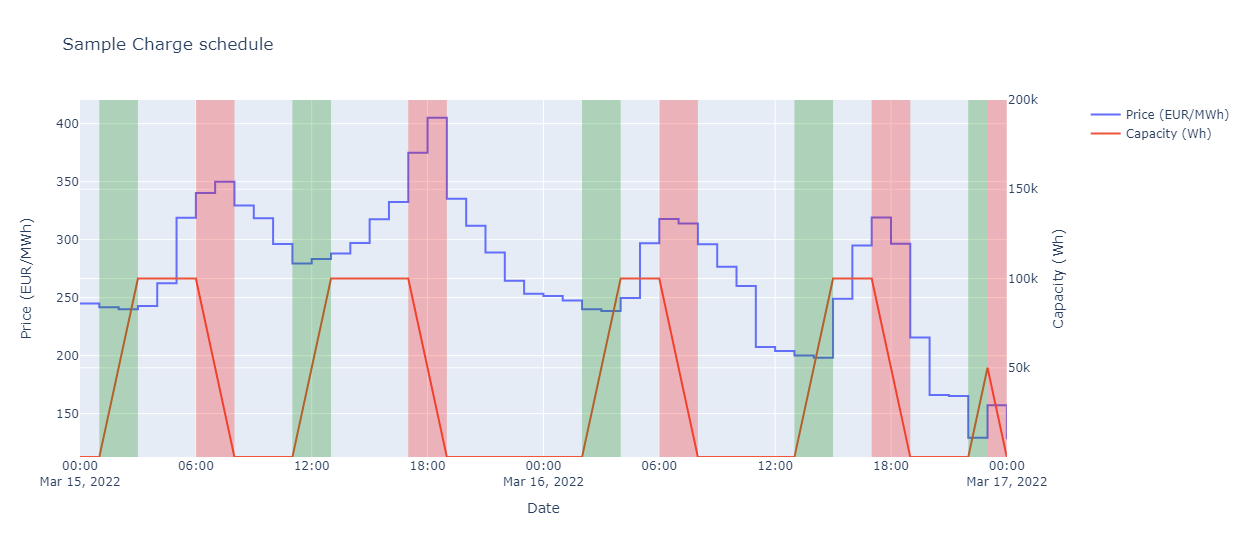

In a DAM, the prices for the next day are determined through an auction process that typically closes before midday. The auction sets prices simultaneously for all 24 hours of the next day, allowing for the acquisition of buy-sell pairs without leaving any open positions. This means that our algorithm has to generate the schedule for the day before market closure on day . In Fig. 1, a sample schedule is shown. We denote by the change in energy stored in the battery between hour and hour on day . Our scheduling problem is, thus, formulated as an optimization task that outputs a sequence of length 24 (one set point per hour):

II-B Price prediction

The exact prices for electricity on the day are not known until after the day-ahead auction has closed. Thus, there is a need to rely on price predictions to be able to get our schedule before the market closure. In the present approach, the mean hourly prices over the last preceding day are used as a prediction of the electricity prices for the day . We, then, generate the schedule for the day before market closure on day . , the forecast of the electricity price at hour denoted by is given by .

II-C Grid costs

There are variable and fixed costs and associated with buying and selling electricity from and to the grid that depends on the day and the hour . The value of is expressed in EUR/MWh and is to be multiplied by the total amount of energy exchanged with the grid. The value of is expressed in EUR and is paid for every hour when energy has been exchanged with the grid.

II-D Battery model

We introduce a battery model that simulates a battery of a given energy capacity . The state of charge at hour , is computed as stated below, where denotes the initial energy stored in the battery at hour :

II-E Variable charging rates

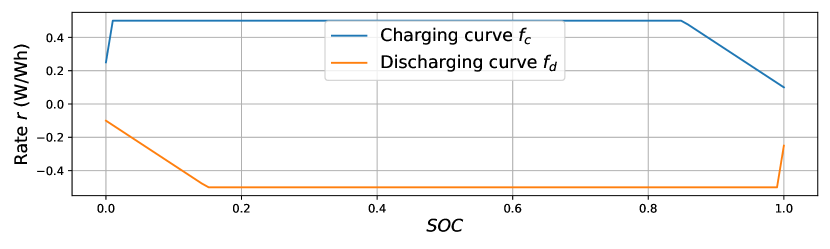

The state of charge SOC of the battery can be computed as a function of the charging rate , expressed in W/Wh, which varies during the charge:

The charging and discharging curves give the charging and discharging rates as a function of the SOC. Fig. 2 shows sample charging and discharging curves for a lithium-ion battery. The charging and discharging curves and can be used to derive the maximum (positive) hourly SOC change and the minimum (negative) hourly SOC change between hour and hour :

The constraint on the change in energy stored in the battery between hour and hour , then, becomes:

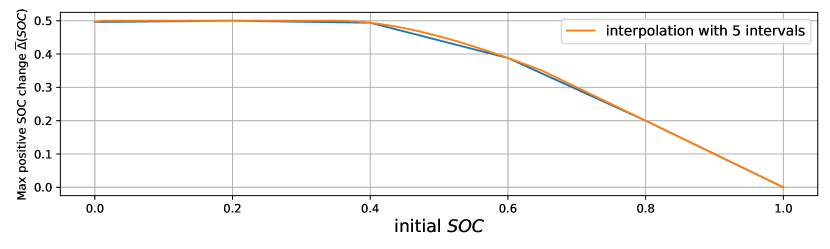

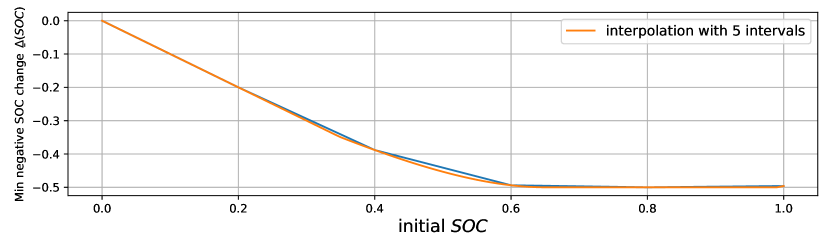

As those functions are not linear, we use convex combination formulations to obtain piecewise linear approximations. We discretize the interval into intervals of length . This adds the following set of constraints ():

| (1) | |||

| (2) | |||

| (3) | |||

| (4) | |||

| (5) | |||

| (6) |

Constraints (1) are used to set the values of the convex combination weights and , (2) guarante the convex requirement (sum to 1), (3) ensure that one interval is selected for each point, and (4) and (5) set the maximum and minimum energy change for each hour. On Fig. 3 values of and for different initial SOC values are shown. The blue lines correspond to the true functions, while the orange ones correspond to a piecewise linear approximation using 5 intervals (6 cut-points).

II-F Availability constraints

Energy arbitrage can represent an additional revenue stream for asset owners using their batteries for another main purpose (e.g. backup energy source) [12]. In this case, the battery has to be charged enough at some key points in time, or, on the contrary, needs to be able to store energy excess, for example, from renewable electricity production systems. We define the parameters and , which sets the upper and lower bounds for the state of charge at hour . This adds the following simple bounds:

II-G Battery degradation

We characterize and model the evolution of the state of health of the battery by decreasing the initial capacity and by decreasing the charge efficiency factor .

II-G1 Capacity fading

During the life of the battery, its capacity decreases with the number of cycles [13]. This is referred to as capacity fading. We model capacity fading by decreasing its initial capacity with a daily frequency, linearly with the number of cycles. The battery is characterized by its cycle life . The battery capacity reaches 80% of its initial capacity after cycles. The MILP parameter corresponding to the capacity on day , denoted by , is computed as below, where denotes the total amount of energy exchanged during day :

II-G2 Charge efficiency decrease

The charge efficiency decreases with the number of cycles. We update it similarly to the capacity:

II-H Objective function

Our goal is to maximize forecasted profits. If the battery is charging at hour , the forecasted (negative) profit is the forecasted cost of the electricity bought added to the variable and fixed grid costs:

If the battery is discharging at hour , the forecasted profit is the revenue from the electricity sold taking into account the discharge efficiency , net of the variable and grid costs:

So as to have a linear objective function, we keep track of the chosen actions at each hour . We introduce the binary variables that indicate if the amount of energy stored in the battery changes during hour . We divide into positive and negative parts and we obtain the objective function in a linear form:

with added constraints:

III Results and Discussion

III-A Data and experiment setup

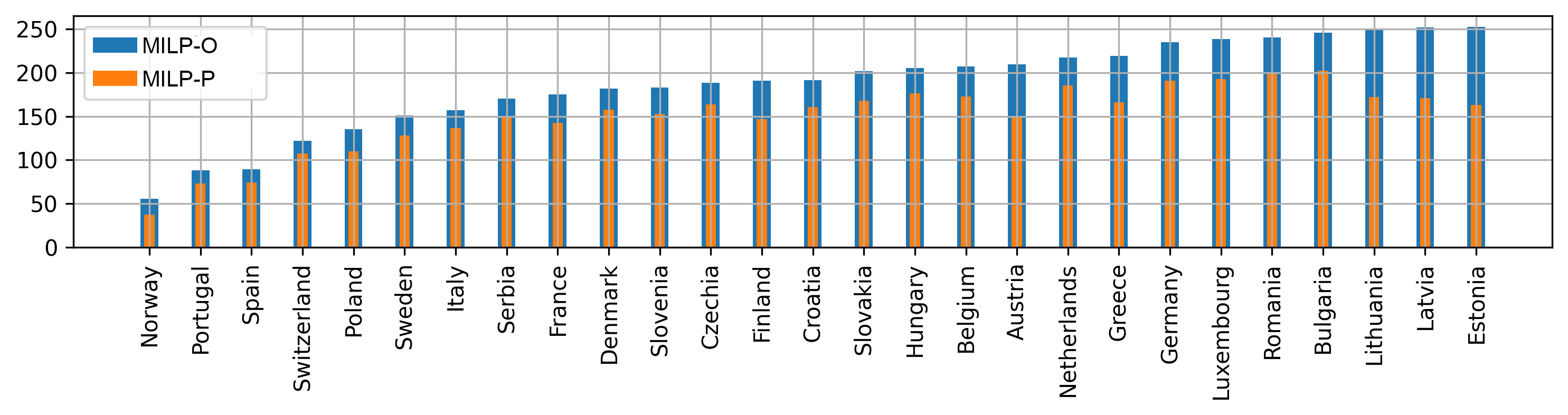

We test our algorithm using the electricity prices for the year 2022 from the European Wholesale Electricity Price Dataset [14], which contains average hourly wholesale day-ahead electricity prices for European countries. We use a battery with a 1 MWh initial capacity (), and with charging and discharging curves as shown on Fig.2. We also set , , and assume no fixed grid costs. The variable grid costs are set to 5 EUR/MWh for every day and every hour of the run, i.e. . We set the maximum and minimum state of charge to 0 and 1 respectively for every hour of every day of the time-horizon, except midnight, i.e. . We use our method to calculate daily schedules for each day of the year 2022. Each schedule starts at 00:00 (midnight) and ends at 24:00. We set for every day so that the battery is always empty at the end of the day. We use the Amplpy library to directly integrate the AMPL [15] model into our Python library. We update the battery parameters (e.g. , ) after every call to the MILP solver (i.e. after each daily schedule is generated). We compare our algorithm described above (denoted by MILP-P) with MILP-O, where MILP-O denotes the algorithm that uses the true prices instead of price forecasts and provides us with the optimal schedule.

III-B Results

Table I shows the results of MILP-O and MILP-P with different window sizes on the German electricity prices. The optimization for the entire year 2022 took under minutes for the whole year with the Gurobi solver on a Huawei Matebook with an AMD Ryzen 5 4600H and 16.0 GB RAM.

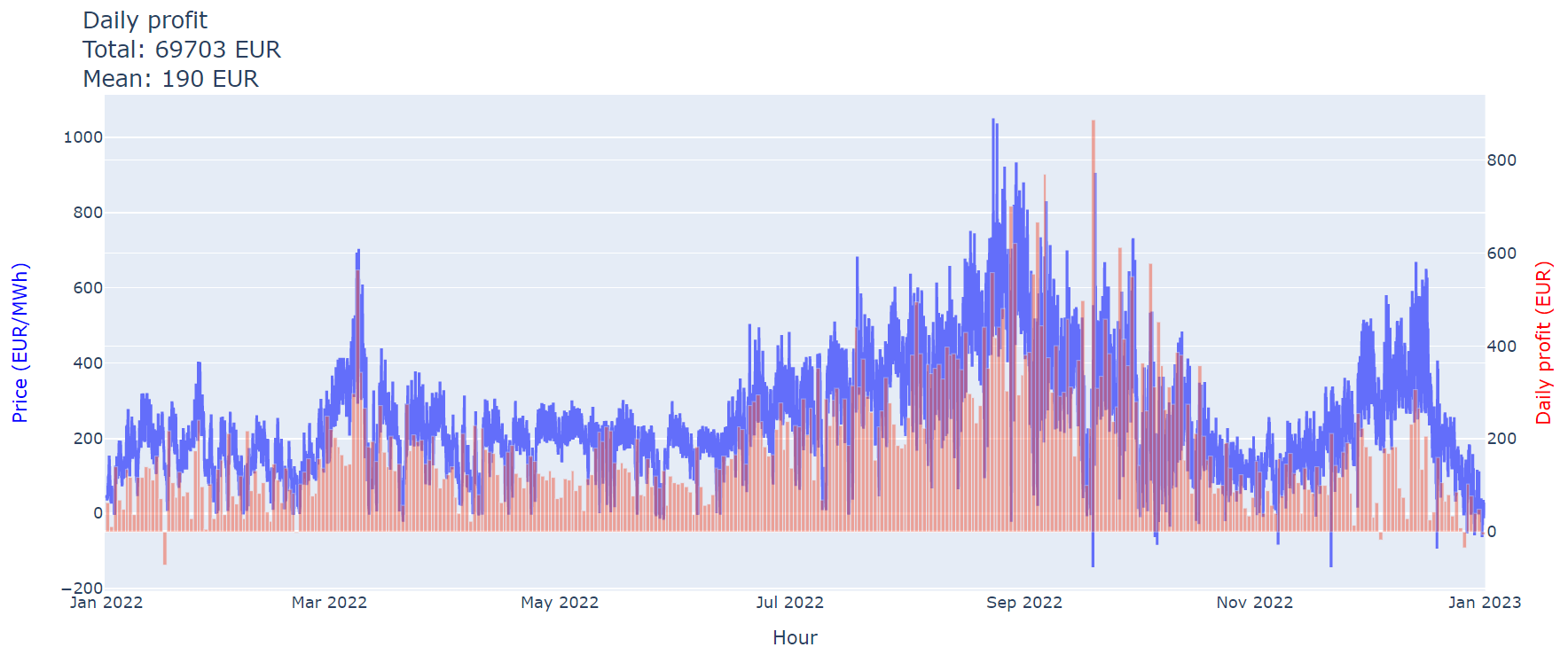

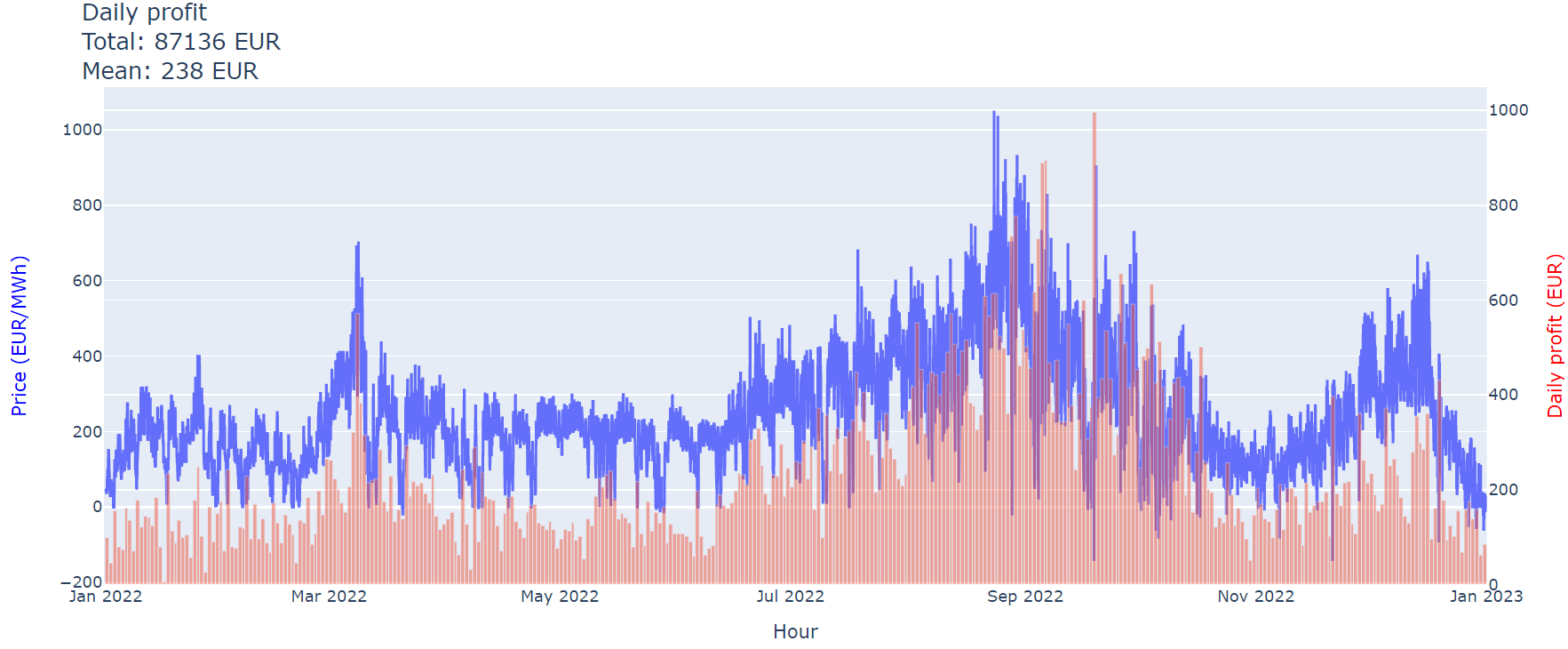

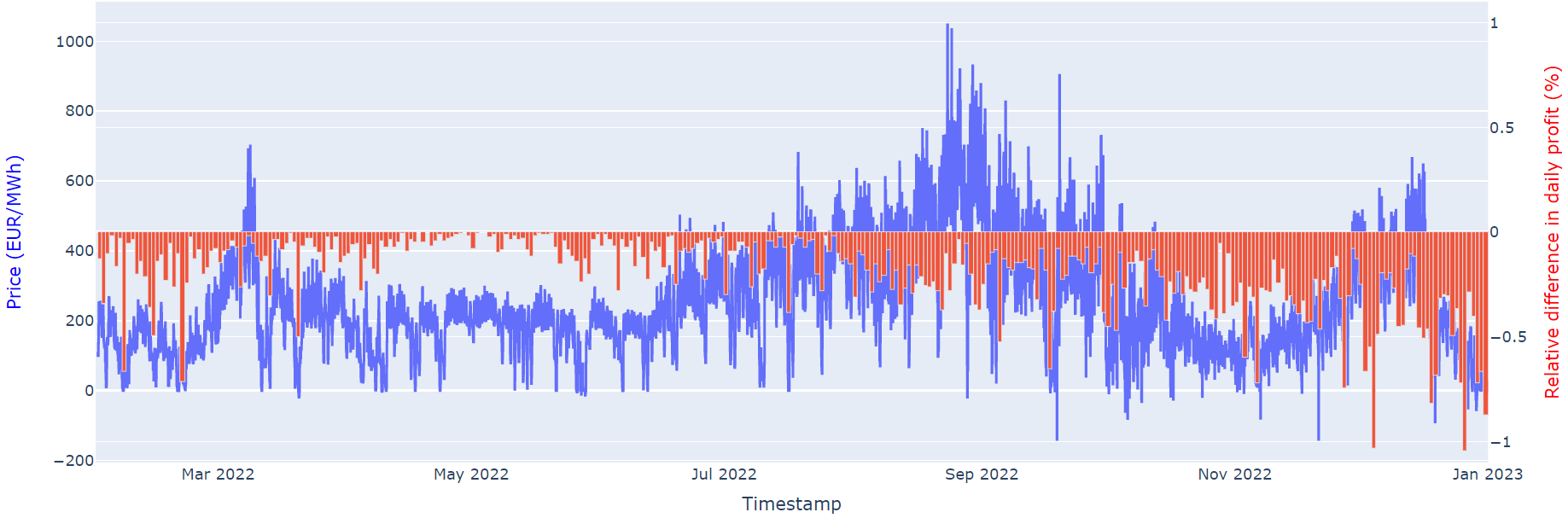

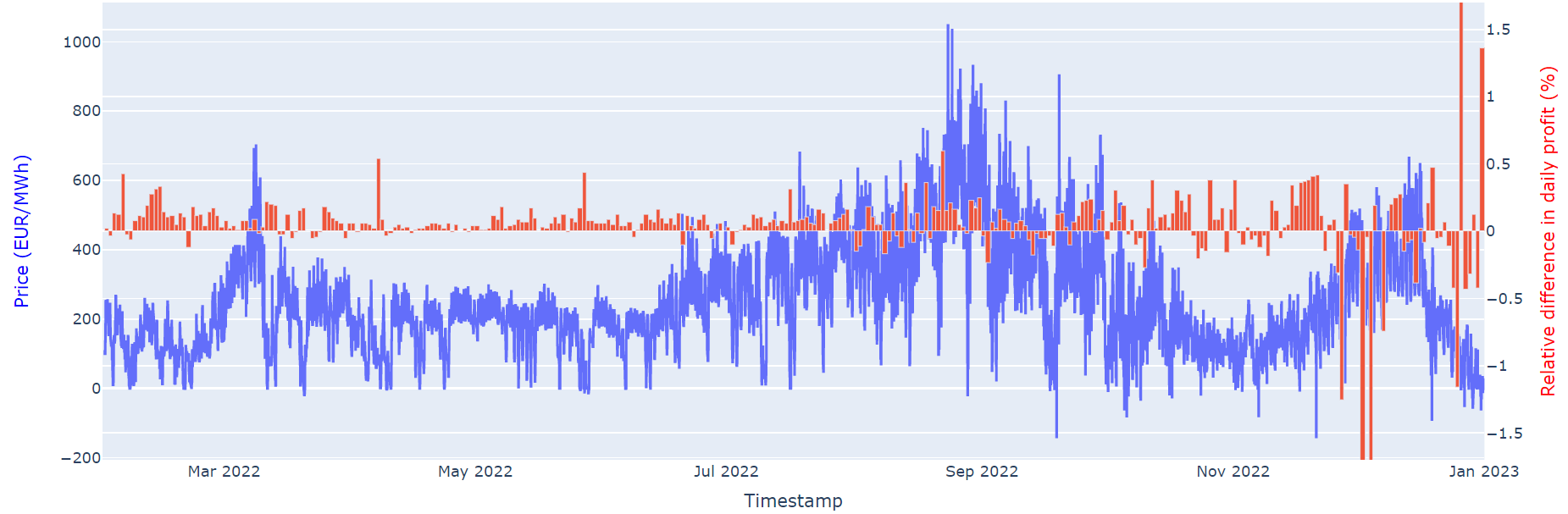

The average daily profit increases with the number of days used for the computation of the price forecast , until , for which the relative difference in profit between MILP-P and MILP-O is -19.39%. The number of charging-discharging cycles decreases as increases, while the profit increases, meaning that the algorithm is better at tracking electricity price spreads when the forecast is based on a reasonably longer historical period. On the contrary, when is small, the schedule shows battery operations that are based on variations observed in the last days, but that do not accurately describe the usual intraday price variations. In this context, the model is overfitting on the last-day price variations. The extreme case is with , where the model builds the schedule on the prices of the previous day, which likely showed variations that are not appearing in the current day’s prices. This also increases the number of days with negative profits. We see that the mean absolute error (MAE) is not a good indicator of how good the price prediction is for the optimization task, as a low MAE is not correlated with higher profits. When is too large, e.g. , the obtained profit decrease, as the price variation forecast becomes less specific to the current day. We show in Fig.5 the daily profit distribution using MILP-O and MILP-P with . There are two main drivers of the daily profits: the daily mean electricity prices, and their intraday variations. The prices were the highest in early September, but the largest daily profits were obtained during days when the prices were lower and the intraday variations larger. Fig. 6 shows the relative difference in profit between the two algorithms. We show the performance of both algorithms on the Danish, French, Spanish, and Italian electricity prices in Table II and the profits obtained with MILP-P and MILP-O on the prices for the year 2022 in other European countries in Fig. 4. The smallest relative difference in profit is obtained for Italy and Denmark, where the intraday price variations vary less from one day to another.

| Algorithm | Avgerage | Relative Difference in | #Cycles | #Days of | prediction MAE | |

| Daily Profit | profit with MILP-O | negative profits | ||||

| MILP-P | 42 | 190.68 | -20.13% | 692.69 | 6 | 94.61 |

| MILP-P | 28 | 192.43 | -19.39% | 689.62 | 4 | 87.54 |

| MILP-P | 21 | 191.98 | -19.58% | 687.53 | 4 | 82.51 |

| MILP-P | 14 | 191.89 | -19.62% | 688.92 | 4 | 77.27 |

| MILP-P | 7 | 189.97 | -20.42% | 696.36 | 7 | 68.39 |

| MILP-P | 2 | 172.04 | -27.94% | 728.06 | 10 | 65.74 |

| MILP-P | 1 | 157.55 | -34.00% | 762.78 | 19 | 62.82 |

| MILP-O | / | 238.7 | / | 763.9 | 0 | 0 |

| Algorithm | Country | Avgerage | Relative Difference in | MAE prediction | |

| Daily Profit | profit with MILP-O | ||||

| MILP-P | Austria | 28 | 150.44 | -28.18% | 81.12 |

| MILP-P | Germany | 28 | 192.43 | -19.39% | 87.53 |

| MILP-P | France | 28 | 142.61 | -18.48% | 82.20 |

| MILP-P | Spain | 28 | 74.34 | -16.82% | 34.71 |

| MILP-P | Denmark | 28 | 157.87 | -13.16% | 90.75 |

| MILP-P | Italy | 28 | 136.70 | -12.81% | 68.25 |

III-C Impact of charging and discharging rates

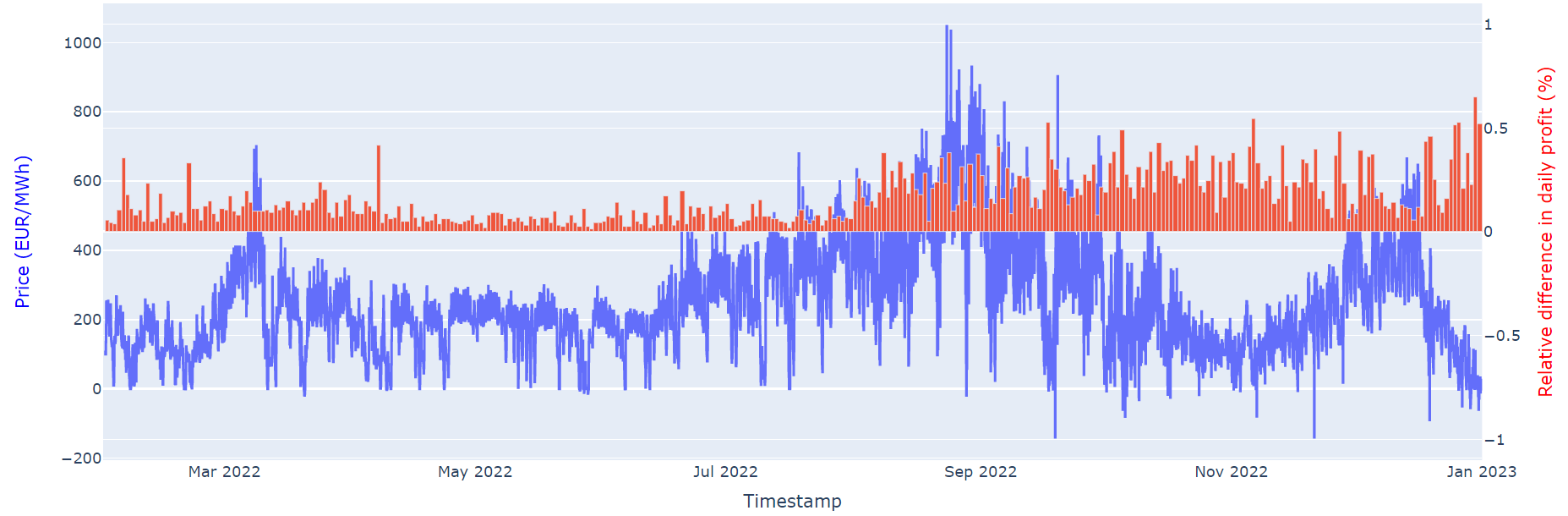

Higher charging and discharging rates increase the amount of electricity that can be bought and sold at every hour of the day. While smaller rates cause the buying and selling prices to be averaged out over multiple hours, high charging rates allow buying and selling more electricity at the local maximum and minimum prices. Fig.7 shows the relative difference in daily profit of MILP-P obtained with a battery with a W/Wh peak charging rate and with a W/Wh peak charging rate. The relative difference in daily profit is constant and greater than in the period when the price variability is low. In December 2022, there are days when the battery with high rates yields much lower profit than the one that has low rates. Over the entire year 2022, the difference in profit is EUR (+5.86% with the high-rate battery). When the rates are high, wrong price predictions yield higher losses, since a larger volume of electricity is traded at the wrong times. This is what happens in December 2022, when the price variations are harder to predict. When the prices are known, higher rates constantly generate more profits (+17.69% over the entire year), as shown on Fig.7. Also note that assuming constant rates equal to the peak rate, as opposed to variable rates (as displayed in Fig.2), leads to an overestimation of the profits by 3.6%.

III-D Impact of battery degradation and grid costs

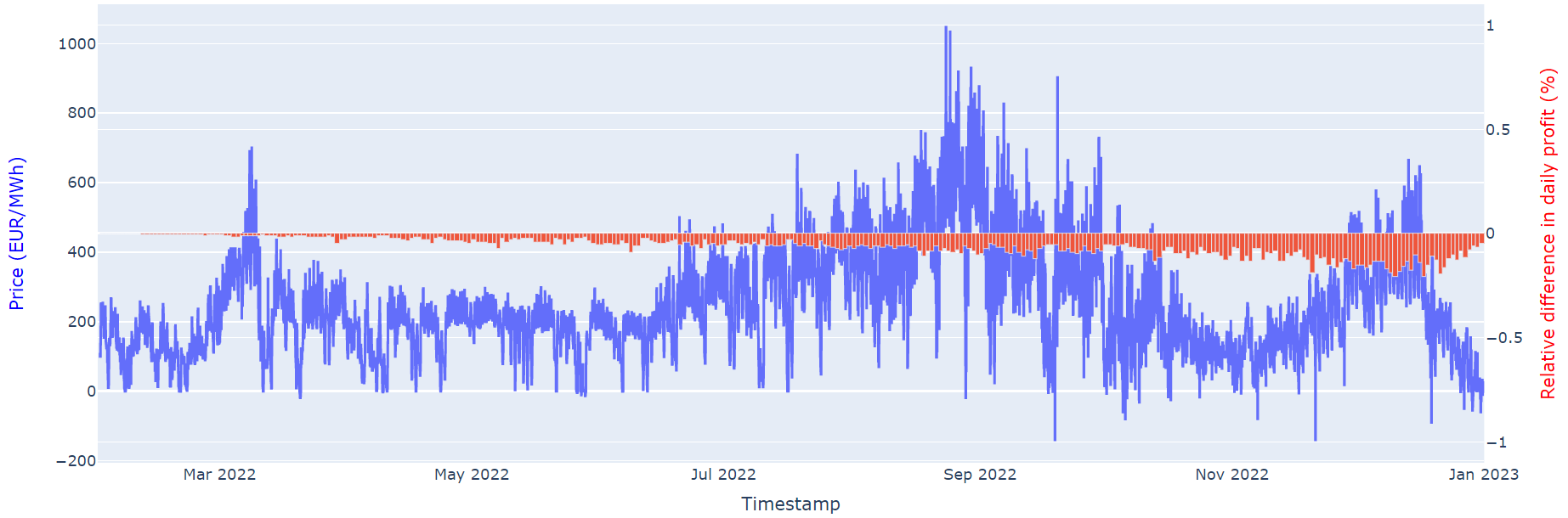

We show the relative profit delta due to capacity fading and efficiency decrease using MILP-O in Fig.8. As the number of cycles increases, the efficiency and capacity decrease. Capacity fading reduces the amount of energy that can be stored in the battery, and a smaller efficiency decreases the amount of energy that can be taken back from the battery. We report a relative difference in profit of 6.67 % over the entire run.

IV Conclusion and Future Work

We introduced a battery model, and a Mixed Integer Linear Programming formulation of the profit maximization task of energy arbitrage on the day-ahead market. Our battery model takes into account the capacity fading effect, the decrease in discharge efficiency, and uses variable charging and discharging rates. We developed a library111The code used to run the simulations is available at https://github.com/albanpuech/Energy-trading-with-battery to generate daily charging schedules by solving the optimization problem using forecasted prices. Its ability to take into account availability constraints, variable and fixed grid costs, custom charging curves, and battery degradation in the optimization step makes it particularly suitable for industrial use cases. It achieved 80% of the maximum obtainable profits on a one-year-long simulation on the 2022 German electricity prices. We report similar or better results for France (81%) or Italy, and Denmark (87% for both). This represents an average daily profit of 190 EUR on the German DAM222battery of 1MWh capacity, 0.5W/Wh peak charging rate, and variable grid costs of 5 EUR/MWh. We also discussed the impact of the battery degradation on the daily profits and the profit changes when using higher charging and discharging rates. We reported a relatively small profit increase (5.86%) when doubling the peak charging rate from 0.5W/Wh to 1 W/Wh. In the future, we plan on improving the forecasting models. This will likely be done by using machine learning forecasting models and by formulating a loss function that better translates the relevance of the prediction for the optimization task.

References

- [1] Iea. Net zero by 2050 – analysis, May 2021.

- [2] Claudia Pavarini. Battery storage is (almost) ready to play the flexibility game – analysis, Nov 2018.

- [3] Mike McWilliams. 6.08 - pumped storage hydropower. In Trevor M. Letcher, editor, Comprehensive Renewable Energy (Second Edition), pages 147–175. Elsevier, Oxford, second edition, 2022.

- [4] Max Schoenfisch and Amrita Dasgupta. Grid-scale storage – analysis, Sep 2022.

- [5] Vinayak Sharma, Andres Cortes, and Umit Cali. Use of forecasting in energy storage applications: A review. IEEE Access, 9:114690–114704, 2021.

- [6] Omer Karaduman. Economics of grid-scale energy storage. Job market paper, 2020.

- [7] Dheepak Krishnamurthy, Canan Uckun, Zhi Zhou, Prakash R. Thimmapuram, and Audun Botterud. Energy storage arbitrage under day-ahead and real-time price uncertainty. IEEE Transactions on Power Systems, 33:84–93, 2018.

- [8] Md Umar Hashmi, Arpan Mukhopadhyay, Ana Bušić, and Jocelyne Elias. Optimal control of storage under time varying electricity prices. In 2017 IEEE International Conference on Smart Grid Communications (SmartGridComm), pages 134–140, 2017.

- [9] Peter M. van de Ven, Nidhi Hegde, Laurent Massoulié, and Theodoros Salonidis. Optimal control of end-user energy storage. IEEE Transactions on Smart Grid, 4(2):789–797, 2013.

- [10] Yixing Xu and Chanan Singh. Adequacy and economy analysis of distribution systems integrated with electric energy storage and renewable energy resources. IEEE Transactions on Power Systems, 27(4):2332–2341, 2012.

- [11] Alessandro Di Giorgio, Francesco Liberati, Andrea Lanna, Antonio Pietrabissa, and Francesco Delli Priscoli. Model predictive control of energy storage systems for power tracking and shaving in distribution grids. IEEE Transactions on Sustainable Energy, 8(2):496–504, 2017.

- [12] Paul Brogan, Robert Best, D.J. Morrow, Robin Duncan, and Marek Kubik. Stacking battery energy storage revenues with enhanced service provision. IET Smart Grid, 3, 08 2020.

- [13] Rutooj Deshpande, Mark Verbrugge, Yang-Tse Cheng, John Wang, and Ping Liu. Battery cycle life prediction with coupled chemical degradation and fatigue mechanics. Journal of the Electrochemical Society, 159:A1730–A1738, 08 2012.

- [14] Ember Climate. European wholesale electricity price data, Jan 2023.

- [15] Robert Fourer, David M. Gay, and Brian W. Kernighan. A modeling language for mathematical programming. Management Science, 36(5):519–554, 1990.