Delegating to Multiple Agents

Abstract.

We consider a multi-agent delegation mechanism without money. In our model, given a set of agents, each agent has a fixed number of solutions which is exogenous to the mechanism, and privately sends a signal, e.g., a subset of solutions, to the principal. Then, the principal selects a final solution based on the agents’ signals. In stark contrast to single-agent setting by Kleinberg and Kleinberg (EC’18) with an approximate Bayesian mechanism, we show that there exists efficient approximate prior-independent mechanisms with both information and performance gain, thanks to the competitive tension between the agents. Interestingly, however, the amount of such a compelling power significantly varies with respect to the information available to the agents, and the degree of correlation between the principal’s and the agent’s utility. Technically, we conduct a comprehensive study on the multi-agent delegation problem and derive several results on the approximation factors of Bayesian/prior-independent mechanisms in complete/incomplete information settings. As a special case of independent interest, we obtain comparative statics regarding the number of agents which implies the dominance of the multi-agent setting () over the single-agent setting () in terms of the principal’s utility. We further extend our problem by considering an examination cost of the mechanism and derive some analogous results in the complete information setting.

1. Introduction

In many real-world situations, a decision-maker (called ”principal”) is encountered with a difficult task that cannot be solved by herself.111Throughout the paper we use feminine pronouns to denote the principal and masculine pronouns to denote the agents. To cope with it, she delegates the process of finding a solution to several agents who have the ability to solve the task, and then examines agents’ proposed solutions to take the best one. An interesting tension arises when the utility of the agents are not aligned with that of the principal. Since the agents are self-interested to maximize their own payoff, they may not propose the solutions for sake of the principal.

As a concrete example, consider a research proposal selection process by a grant agency. In this problem, a principal (e.g., the grant agency) introduces a topic for proposals and asks each agent (e.g., a principal investigator) to send a private proposal, or a set of proposals, based on a set of his research directions (possibly coming from some distribution) related to the topic introduced by the principal. Each proposal has some valuation for the agent and some valuation for the principal which can be different (e.g., a proposal may be more aligned with a research direction by the agent but less aligned with the principal’s interests). The goal of the principal is to maximize own valuation of the finally selected proposal while the goal of each agent is to maximize his utility which is his valuation for a proposal selected by the principal and zero otherwise.

In this example, the principal faces a problem of mechanism design without money to incentivize the agents to behave more in favor of her. In practice, the setting here can be an incomplete information game in the sense that though an agent knows the topic introduced by the principal and general research topics of the other agents (i.e., distributions of possible proposals), he may not know the exact topics that other agents consider for their proposals. In addition, the principal may have an examination cost (e.g., travel cost for time-consuming site visits) for each proposal which should be accounted for in the proposal selection process as well. A fundamental question in this example is how should the principal design a mechanism to maximize her own utility function.

Initiated by Holmstrom (1980), there exists a rich line of literature studying the theory of delegation without monetary transfer. The restriction that the principal cannot commit to a contingent monetary transfer in the mechanism imparts a restrictive structure on feasible mechanisms in which the mechanism simply commits to a set of acceptable solutions, and only decide whether or not to accept the proposed solutions. Holmstrom (1980) study the optimality of these simple mechanisms and the characterizations of the regimes for these mechanisms to be optimal. Subsequent works including Alonso and Matouschek (2008) and Armstrong and Vickers (2010) develop the theory of delegation in this context and broaden its scope in fruitful direction.

Recently, with a lens of computer science, Kleinberg and Kleinberg (2018) study a problem of designing approximate mechanisms in the delegated search problem.222They study two types of model, one of which is similar to delegated choice without search cost by (Armstrong and Vickers, 2010), and the other is that with search (sampling) cost. Our model can be framed as either of a delegated search problem with exogenous solutions, or delegated choice problem which delegates the choice between given alternatives. They consider a simple mechanism so-called a single-proposal mechanism, which consists of single-round interaction between the principal and the agent. Remarkably, it achieves a -approximation compared to an ideal scenario in which the principal can directly select the best solution among the entire set of agents’ solutions. Their analysis is based on a novel observation regarding a connection between the dynamics of the single-proposal mechanism and the dynamics of threshold-based algorithms in prophet inequalities (see Samuel-Cahn (1984), Krengel and Sucheston (1987), Hajiaghayi et al. (2007), Alaei et al. (2012), Abolhassani et al. (2017), Correa et al. (2017) for more reference to prophet inequalities).

As we discussed in the above example, there exists a variety of real-world situations, spanning economical applications to modern intelligent systems, such that the principal needs to delegate the task to multiple agents with misaligned payoff. Surprisingly, however, the problem of delegating to multiple agents in the framework of mechanism design without money has received less attention in the community. The recent work by Gan et al. (2022), preceded by Alonso et al. (2014), study the optimal delegation mechanism with two agents in the context of mechanism design without money, but their model is significantly different from ours, and also is restricted to small number of agents with specific utility functions.333We provide the detailed discussion in Section 3.

In this context, we introduce the multi-agent delegation problem, and conduct a comprehensive study on the approximation factors of various mechanisms without monetary transfer. Technically, we aim to design a multi-agent delegation mechanism that improves upon the guarantees of a single-agent mechanism by Kleinberg and Kleinberg (2018). Surprisingly, different from the single-agent mechanism which assumes the prior knowledge on the agent’s distribution to derive a constant approximation factor, i.e., Bayesian mechanism (BM), we show that we can construct an efficient mechanism even without those prior knowledge, i.e., by prior-independent mechanism (PIM), which is mainly due to the competitive tension arise from the multi-agent extension. Notably, however, we further observe that the amount of such a compelling power from competition differs with respect to the information available to the agents, and the degree of correlation between the principal’s and the agent’s utility. Overall, we comprehensively analyze the approximation factors of BM and PIM in both the complete and incomplete information settings (in terms of the agents’ information). We note that our main technical results lie on the analysis of approximation factors of PIM. To highlight a few of the main results,

-

(1)

In the complete information setting, we show that there exists a PIM such that the principal’s expected utility is bounded below by the first-best solution (in the principal’s view) of the second-best agent. We further quantify this approximation factor by analyzing the upper and lower bound of the principal’s expected utility in various regimes. This tends to asymptotically optimal in certain regimes, i.e., the gains from multi-agent delegation is significant. En route to this analysis, we present several technical results regarding the order statistics of i.i.d. random variables, which might be of independent interest.

-

(2)

In the incomplete information setting, we show that under symmetric agents with uniform distribution and the assumption of independent utility, we can construct a PIM in which there exists a -approximate Bayes Nash equilibrium such that the principal’s expected utility becomes exactly optimal, where converges to as the number of agents increases. We numerically verify that this guarantee is almost tight. Using a similar technique, we analyze that there exists a Bayes correlated equilibrium with a multiplicative approximation factor of .

-

(3)

We further show that the assumptions of symmetric agents and independent utility are necessary. More formally, without these assumptions, we can construct a problem instance such that there exists a Bayesian Nash equilibrium in which the agents propose their worst solutions for the principal, which may induce arbitrarily bad principal’s utility.

To select the best solution among the solutions from multiple agents, however, the principal suffers a cost of examining the candidates. In this context, we extend our problem setup and further study a trade-off between such an examination cost and an efficiency of mechanisms, and provide an analogous result in the complete information setting.

The remainder of the paper is organized as follows. In Section 2, we summarize overall results and the techniques therein. Section 3 provides detailed discussions on the related work. Section 4 introduces the formal problem setup. In Section 5 and 6, we provide the results in the complete and incomplete information setting, respectively. Finally in Section 7, we introduce the examination cost and some results in this extension.

2. Overview of results

Before presenting the summary of our results, we briefly discuss our problem setup and some preliminaries. We refer to Section 4 for a more formal problem setup. In multi-agent delegation problem, there exists a principal who wants to find a solution for a task by designing a mechanism that delegates the task to agents. Each agent observes solutions by sampling from his own distributions, where both the number of solutions and the distributions are exogenous to the mechanism. These exogenous parameters can be interpreted as the intrinsic level of effort and skill of the agent. Afterward, each agent proposes a subset of observed solutions (signal) to the principal. Eventually, the mechanism selects a single solution, winner, from the proposed ones. If the solution is selected as the winner, the principal receives the utility of . If is proposed by agent , he gets the utility of while other agents realize the utility of zero. Given the mechanism, each agent determines a (possibly mixed) strategy to maximize own utility, which maps the observed solutions and information regarding others’ solutions to the signal, and plays an action based on the strategy. Importantly, we impose no restriction on the utility function and , i.e., they might be misaligned, which brings an interesting trade-off in designing the mechanism.

We introduce technical notations to summarize our results. Denote by the agent ’s observed solutions for .444We use to denote for throughout the paper. Define for and . Sort for in decreasing order, and denote by . We denote by the first-best solution of agent . Again, sort for in decreasing order, and obtain . Let the owner of be the -th best agent. We often overwrite by . Our benchmark of the mechanism is , i.e., the case when the principal can select the best one by directly accessing all the observed solutions. Let be an interim allocation function which specifies the outcome under the mechanism and some strategies , given a realization of the solutions. Then, given some strategies of the agents, we say that mechanism is -approximate if

We denote by and the multiplicative and additive approximation factors, respectively. We say that has multiplicative price of anarchy () of if it is -approximate under any Nash equilibrium of agents’ strategies, and it has multiplicative price of stability () of if there exists a Nash equilibrium such that is -approximate. We similarly define and to denote the price of anarchy/stability for -approximation, i.e., additive approximation factor.555See Definition 4.4 and 4.5 for more details.

2.1. Contributions and techniques

We here summarize our key results and the major techniques therein. Basically, we analyze two types of mechanisms: (1) Bayesian mechanism (BM) with knowledge of the prior distributions, and (2) prior-independent mechanism (PIM) which does not know the distributions in advance. We further consider complete and incomplete information settings. In the complete information setting, each agent knows the others’ observed solutions while in the incomplete information setting, he only knows the distributions from which the others sample, but not the realized solutions.

We begin by showing that any mechanism can be reduced to a multi-agent single-proposal mechanism (MSPM, Definition 4.7) in Theorem 4.11. Essentially, this theorem implies that we can narrow down our scope of interest to the space of the MSPMs. We note that the MSPM can be either BM or PIM depending on whether the mechanism uses the knowledge on the distributions or not. All the positive results we present below will be built upon MSPMs.

General result in the complete information setting

We start with the general result on MSPM.

Informal Statement of Theorem 5.1.

In the complete information setting, for any , there exists a MSPM with of

Intuitively, the first-best agent needs to guarantee that he will be selected by the principal while maximizing his own utility. This motivates him to propose a solution that yields the principal’s utility at least that of the first-best solution of the second-best agent. The proof is built upon such simple intuition, however, it is still tricky to characterize arbitrary (possibly mixed) Nash equilibrium of the agents, and the formal proof can be found in Appendix F.2. This result implies that the additive approximation factor is characterized by the difference between and , i.e., the difference of first-best solution between the first-best and second-best agents. On top of it, the principal can also smartly define the threshold using the prior information, and further improve the quality of the candidates, although it may decrease the probability of the acceptance.

BM in the complete information setting

From the general result, we obtain the following result on BM which recovers the single-agent guarantee in Kleinberg and Kleinberg (2018).

Informal Statement of Theorem 5.3 and 5.5.

In the complete information setting, there exists a BM with of . In addition, this multiplicative approximation factor is tight, i.e., there exists a problem instance that no BM can achieve .

| Information | Bound | General | Symmetric -decaying |

| Complete | Lower | ( Thm 5.5) | open |

| Upper | (Thm 5.3) | (Thm 5.8) | |

| Incomplete | Lower | (Cor 6.2) | open |

| Upper | (Cor 6.2) | (Cor 6.2) |

The upper bound follows from the reduction from multi-agent setting to single-agent setting, where we in fact obtain stronger comparative statics such that the multi-agent delegation is always superior to the single-agent delegation. We discuss a more detailed comparison between the single-agent and multi-agent settings in Appendix E. The lower bound is obtained by introducing a concept of super-agent equipped with the standard worst-case instance in prophet inequalities. This worst-case instance implies that there is no merit in delegating the task to multiple agents with highly asymmetric levels of skill.

We then naturally consider a symmetric case (see Definition 5.6) when the agents are equipped with the same parameters, i.e., they have similar levels of skill and effort. In this case, for a certain class of distributions, we show that the multiplicative approximation factor can be subconstant for BM, i.e., converges to as (the num. of agents) or (the num. of solutions per agent) increases.

Informal Statement of Theorem 5.8.

In the complete information setting, consider the symmetric agents with where is a distribution supported on and the cumulative distribution function (c.d.f.) of satisfies for some . Then, there exist a BM with of . Hence, the principal’s expected utility converges to as or increases.

To obtain the subconstant bound above, we use threshold-based eligible sets that are tighter than the ones used in the prophet inequalities. We present the summary of results for BM in Table 1.

PIM in the complete information setting

For PIM, we observe that Theorem 5.1 yields an additive approximation factor of by setting (see Corollary 5.9). This indeed requires no prior knowledge as it accepts any solution. On the other hand, we argue that this guarantee can be arbitrarily bad if we do not restrict our problem instances to symmetric agents.

Informal Statement of Theorem 5.10.

In the complete information setting, suppose that principal’s utility function lies in for some . Then for any , there exists a problem instance such that no PIM can achieve .

The proof is based on a construction worst-case instance with a super-agent similar to the lower bound under the general setting in BM.

We thus consider the symmetric agents and derive the following result.

Informal Statement of Theorem 5.11.

In the complete information setting, consider symmetric agents with the principal’s utility function lies in for some . Then, there exists a PIM with of .

Note that for all , and decreases to as increases. This constant approximation is a big improvement over the arbitrarily bad approximation in the general setting.

Next, we improve the approximation factors of PIM to be subconstant with respect to some canonical family of distributions. At the heart of this analysis, we come up with several new results (see Lemma 5.12, 5.14, 5.16, and 5.17) in order statistics666Given i.i.d. samples, -th order statistics refer to the -th smallest value among the i.i.d. samples., which might be of independent interest. Detailed discussions are presented in Section 5.2.

Informal Statement of Theorem 5.15 and 5.18.

In the complete information setting, consider symmetric agents such that where is a distribution with a probability distribution function (p.d.f.) of . Let be the distribution of for any . Denote by the variance of a distribution. Then, the following holds.

-

(1)

If has MHR (see Section 5.2 for definition), then there exists a PIM with of . In case of , we have .

-

(2)

If is nondecreasing on , then there exists a PIM with of . In case of , we have .

Incomplete information setting

In the incomplete information setting, we first discuss that the results on the BM, Theorem 5.3 and 5.5 and Theorem 5.8, still carry over in the incomplete information setting. In addition, without the assumption of symmetric agents, we still have an arbitrarily bad lower bound in the approximation ratio for any PIM, i.e., Theorem 5.10 still holds. This justifies our assumption of symmetric agents in the incomplete information setting as well. Interestingly, however, assuming the symmetric agents is not sufficient to derive a positive result.

Informal Statement of Theorem 6.4.

In the incomplete information setting, under symmetric agents with , there is a problem instance where no PIM has .

Note that by making arbitrarily large give , RHS can be arbitrarily close to . The proof is based on a construction of strongly negatively correlated utility between the principal and the agents, preceded by some algebraic manipulations. Interestingly in this problem instance, each agent’s utility decreases by playing for sake of the principal. Hence, each agent settles with a solution that gives the agent largest ex-post utility (and thus smallest principal’s utility), even though it yields a small probability to be selected. We present the result for uniform distribution for simplicity, but we in fact provide a more general result.

| Information | Bound | General | Symmetric (Sym) | Sym MHR | Sym Inc | Sym Ind | |||||

| Complete | Lower |

|

Open | Open | Open | Remark 2.2 | |||||

| Upper | Cor 5.9 |

|

|

|

Remark 2.2 | ||||||

| Incomplete | Lower |

|

|

Remark 2.1 | Remark 2.1 | Open | |||||

| Upper | Remark 2.3 | Remark 2.1 | Remark 2.1 | Remark 2.1 |

|

In this context, we additionally consider an independent utility assumption in which the agents’ and principal’s utilities are independent of each other (see Definition 6.5 for more details). Then we show that there exists a good approximate Bayes Nash equilibrium (BNE) (see Definition 6.6 for more details) such that the principal’s expected utility becomes exactly optimal.

Informal Statement of Theorem 6.7.

In the incomplete information setting, consider symmetric agents and independent utility assumption such that . Then, there is an optimal PIM with -approximate BNE where . Note that becomes as grows.

Different from the complete information setting, deriving and analyzing BNE is far more challenging, especially for our problem setup. One reason is that the feasible action of an agent depends on the realization of his solution. In addition, computing the expected payoff of an agent’s strategy requires us to compute the expectation over every possible realization of the others’ solutions. Despite these difficulties, we obtain the above result, of which the proof heavily relies on the FKG inequality (Lemma F.9) and some properties on the joint density function of two order statistics, preceded by some algebraic manipulations. Using a similar but more involved technique, in Appendix C, we show that there exists a PIM such that under some Bayes correlated equilibrium, it achieves a multiplicative approximation factor of (as increases). We present the summary of results on PIM in Table 2. We remark on some points regarding the table as follows.

Remark 2.1.

We do not study the upper bound for symmetric agents in the incomplete information setting because the lower bound in this setting can be arbitrarily bad for certain problem instances. In addition, we do not consider Sym MHR and Sym INC in the incomplete information setting since the lower bound in the symmetric setting already implies a pessimistic result.

Remark 2.2.

Since the complete information setting inherently admits positive results only with the symmetry assumption, we do not consider the symmetric agents and independent utility scenario in the complete information setting.

Remark 2.3.

The upper bound for the general incomplete information setting is not studied, as one can easily obtain a mechanism with an approximation ratio of , e.g., a mechanism that selects a solution to maximize the agent’s utility.

Examination cost

Finally, we study an extension to consider the examination cost of the mechanism. The examination cost of a mechanism is defined by the number of candidates that the mechanism has to access to choose the winner. We refer to Definition 7.2 for more details. In this extension, we obtain the following result of a similar flavor to Theorem 5.1.

Informal Statement of Theorem 7.5.

Define . For any , there exists a mechanism with examination cost such that is at most,

This depicts the trade-off between the examination cost and the approximation ratio. Indeed, PoA increases as decreases, and plugging carries over to the bound in Theorem 5.1.

3. Related work

Initiated by Holmstrom (1980), a rich line of literature has studied the delegation mechanism without monetary transfer. Holmstrom (1980) considers a setting in which a single agent is delegated to solve an optimization problem over a compact interval, and characterizes conditions under which an optimal solution of the principal exists. Alonso and Matouschek (2008) fulfill the results by providing a general characterization of the solution. Armstrong and Vickers (2010) study a discrete model in which an agent samples a set of solutions from a distribution and optimizes over the sampled set, which is the most similar problem setup to ours.

While most literature in the theory of delegation aims at characterizing regimes in which the optimal mechanism exists or the structure of it, Kleinberg and Kleinberg (2018) study the loss of efficiency from delegating the task into an agent with misaligned payoff. They consider two models, one of which is similar to delegated project choice of Armstrong and Vickers (2010). In this model, the agent samples a fixed number of solutions from a distribution and proposes some of the solutions to the principal in a strategic manner. Surprisingly, they show that a simple mechanism enjoys a -approximation ratio compared to the ideal scenario in which the principal can directly choose the optimal solution, based on a connection to the prophet inequalities.

Several works have been devoted to the delegation mechanism without money in the presence of multiple agents. One of the most relevant problem setting would be legislative game with asymmetric information by Gilligan and Krehbiel (1989), Krishna (2001), Martimort and Semenov (2008) and Fuchs et al. (2022). They consider a model in which two self-interested agents with information advantage observe a state of nature and independently send a private signal to the principal. The principal aims to extract truthful information on the state of nature to maximize own utility that depends on it. Recent works by Alonso et al. (2014) and Gan et al. (2022) extend these settings by considering multiple actions for the principal. Importantly however, all of their models are significantly different from our model. In our model, the information asymmetry between the principal and the agents arises from ”moral hazard” versus ”adverse selection” of the previous works, as per Ulbricht (2016).777Notably, Ulbricht (2016) study both effect of moral hazard and adverse selection in the delegation mechanism but with a monetary transfer. Likewise, there exists a fruitful line of literature dealing with contract-based delegation, e.g., Krishna and Morgan (2008) and Lewis (2012), but we will not discuss in detail on the delegation mechanism with money. In moral hazard, the principal cannot directly observe all the alternatives, but can only access a subset of them based on the signals, whereas in adverse selection, a state of nature is revealed only to the agent but affects the principal’s utility as well.

Finally, there is an increasing attention in the Computer Science community regarding an algorithm design with a delegated decision. Bechtel and Dughmi (2020) considers a stochastic probing problem when the principal delegates the role of probing to a self-interested agent. They quantify the loss of delegation similar to Kleinberg and Kleinberg (2018) by revealing a connection between delegated stochastic probing and generalized prophet inequalities. Bechtel et al. (2022) generalizes the second model of Kleinberg and Kleinberg (2018), namely Weitzman’s box problem which deals with a costly sampling of the agent, by considering a combinatorial constraint.

4. Problem setup

Multi-agent delegation. Consider a principal who designs a delegation mechanism and a set of agents who perform the task and decide solutions. Let be a set of potential solutions. Each agent is equipped with a number of solutions , and each solution for is sampled from a probability distribution supported on . We assume that for to avoid trivial regime. Each distribution may refer to the potential quality of the th solution of agent , and the number of solutions can be interpreted as the agent’s willingness-to-pay in terms of his effort, both of which are exogenous to the mechanism. We denote by the agent ’s -th solution for , and the agent ’s multi-set of all solutions. We further use to denote the multi-set of all the solutions sampled by the agents. After agent observes his own solutions , he sends a signal to the principal, and then the principal finally adopts one of the solutions based on the agents’ signals.

For notational consistency, let solution denote an outcome observed by an agent, candidates to denote the set of solutions that the mechanism can access given the agents’ signals, winner to denote the final solution adopted by the principal. We further say our problem to be single-agent problem if , and multi-agent problem if .

Mechanism

A mechanism is specified by a set of signals of which the -th coordinate corresponds to the signal from agent , a set of possible random bits of the mechanism, and an allocation function which denotes the winner selected by the principal given the signals by agents and the random bits. If the mechanism is deterministic, we overwrite the domain of the allocation as . We mostly deal with a deterministic mechanism but introduce a general definition for completeness. For some given random bits , we denote by the mechanism in which its random bits are fixed to be . Note that we use a generalized notion of signal to denote any possible interaction from the agents to the principal. For example, agent may simply propose a subset of his observed solutions as candidates, or he may exploit a mixed strategy of proposing solutions randomly. Throughout the paper, we use to denote a family of all finite multi-set over .

Agent’s strategy

Each agent selects a certain signal based on a strategy . More formally, given a multi-set of the solutions , agent sends a signal to the principal. Importantly, agent determines the strategy based on the information regarding the others’ solutions as well as his own solutions. We elaborate more in the subsequent paragraph. The principal has a utility function and each agent for has a utility function . If solution is selected as the winner and belongs to agent , then the principal and agent realize utilities of and respectively. The other agents realize their utility to be zero. Note that we restrict the winner to be within so that the principal cannot commit to a solution beyond the observed set of solutions. We further assume that includes a null outcome . If the principal selects as the winner, this represents that no solution is adopted by the principal and the realized utility is zero, i.e., for .

Information structure

In terms of the principal’s information for agents’ distributions of solutions, we consider the following two types of mechanism.

Definition 4.1 (Bayesian and prior-independent mechanism).

We say that mechanism is prior-independent mechanism (PIM), if it does not have any information on the distributions from which the solutions are drawn. If it priorly knows the distribution from which the quantity over the solutions are drawn for each agent, we denote by Bayesian mechanism (BM).

Importantly, as noticed in the definition, PIM has significant informational gain over BM. It does not require any process of acquiring information on the distribution of solutions. Indeed, in practice, it is difficult or even impossible to estimate the distribution of each agent in advance. Even if it’s possible, it usually entails a costly procedure to acquire such information, and thus PIM is more broadly applicable.

Regarding the principal’s information on the agents’ solutions, we consider an information asymmetry arises from moral hazard such that the principal has no information on the realized set of solutions since she delegates the search (choice) to the self-interested agents. Instead, she can only access a subset of solutions based on the signals provided by the agents.

To model the agent’s information structure, we basically assume that the agents know the principal’s utility function. Furthermore, we consider two cases of complete information and incomplete information based on the agent’s information with respect to the others. In the complete information setting, all the observed solutions are revealed to each other, thereby each agent determines his own strategy after observing all the solutions. In the incomplete information setting, only the distributions of the solutions are publicly available to the agents but not the exact observed solutions, and thus each agent determines his own strategy based on the given knowledge of the others’ distributions.

Allocation function and overall mechanism

We first define an interim allocation function which represents the winner adopted by the mechanism given the observed set of solutions.

Definition 4.2 (Interim allocation function).

is an (interim) allocation function given mechanism and strategy . That is, given , the mechanism selects as the winner when each agent plays . In case of randomized mechanism, we use to denote the allocation function given the random bits , and to denote the set of possible winners .

Overall, the mechanism proceeds as follows: (1) the principal commits to a mechanism , (2) each agent observes solutions , (3) each agent strategically sends a private signal , and (4) the principal selects the winner (or ).

4.1. Further preliminaries

We here present further notations that will be broadly used throughout the paper.

Definition 4.3 (Nash equilibrium).

Given a mechanism , a set of strategies is called a Nash equilibrium, if yields

| (1) |

for agent ’s any other strategy given the others’ strategy . We call each an equilibrium strategy of agent . We often abuse equilibria or equilibrium to denote Nash equilibrium. Whenever the mechanism is randomized, we take expectation over the utility in (1).

For sake of exposition, we define and for each and . Furthermore, we denote by the -th highest solution in in terms of so that and define the agent ’s utility for the solution that corresponds to . We often overwrite by the first-best solution of agent , and the agent who has by -th best agent. Note that and for each and are random variables such that and are correlated with respect to .

We measure the principal’s utility by comparing it to a strong benchmark Opt given a realized set of solutions , defined formally as follows.

We often abuse . Note that Opt denotes the principal’s utility when she can access all the solutions sampled by the agents, and select the best solution by herself.

In terms of the approximation ratio of the mechanism, we consider both the additive and multiplicative approximation factors, defined as follows.

Definition 4.4.

Mechanism and corresponding strategies are -approximate if

Note that the expectation in LHS is taken over the randomness in as well as that in solutions.

Since we deal with the approximation factor of the mechanism in its equilibrium, we further define the notion of the price of anarchy and the price of stability as follows.

Definition 4.5 (Price of anarchy/stability).

Mechanism has multiplicative price of anarchy () of if it is -approximate under any equilibrium. It has multiplicative price of stability () of if there exists an equilibrium such that is -approximate. We similarly define and to denote the price of anarchy/stability for the additive approximation factor .

For self-containedness, we present the mechanism introduced by Kleinberg and Kleinberg (2018).

Definition 4.6 (Single-proposal mechanism).

In a single-proposal mechanism (SPM) under the single-agent setting, an eligible set is announced by the principal, the agent proposes a solution , and the principal accepts it if , and rejects it otherwise.

In our multi-agent setup, we mainly investigate a variant of the SPM defined as follows.

Definition 4.7 (Multi-agent single-proposal mechanism).

In a multi-agent single-proposal mechanism (MSPM), a tie-breaking rule and an eligible set are announced by the principal for each agent . Each agent proposes up to one solution, and the principal filters a candidate from agent if it is not contained in . After filtering, the principal selects the winner by choosing the candidate that maximizes her utility, given the tie-breaking rule . We say that MSPM has a homogeneous eligible set if for .888We provide further examples of reasonable mechanisms in Appendix B.

Remark 4.8.

Importantly, in terms of the principal’s information, MSPM can be both BM and PIM depending on the eligible set . If we specify to admit any solution from , then it is PIM as we do not need any kind of prior knowledge on the solution. However, if we want to specify to accept only a certain type of solution as in SPM by Kleinberg and Kleinberg (2018), then we essentially need the prior information regarding the distribution of the solution. This is indeed true because if we commit to an eligible set that possibly rejects some solutions without knowing the distribution of the solutions, then it is obvious that we can construct a worst-case problem instance in which the mechanism essentially cannot accept any solution, resulting in an arbitrarily bad approximation factor. We refer to Claim F.2 in Appendix F.6 for a formal discussion.

Finally, we pose a (minor) assumption that if an agent is indifferent between two solutions, he selects a solution that induces a higher utility for the principal.

Assumption 4.9 (Pareto-optimal play).

If an agent has two solutions and such that , and at least one of these inequalities are strict, then the agent does not play strategy .

Remark 4.10.

This assumption is reasonable since there exists no merit in playing such a dominated strategy . Moreover in practice, the agents may also want to behave in favor of the principal as much as possible unless they need to sacrifice their own utilities, for any future interactions.

Before presenting our main results, we begin with the following observation that any mechanism can be reduced to MSPM with the proper choice of parameters.

Theorem 4.11.

In the multi-agent setting, for any mechanism with an arbitrary equilibrium , there exists a MSPM such that for any equilibrium , for any and any , we have for any observed solutions .

The proof is provided in Appendix F.1. Thanks to the theorem, it suffices to narrow down our scope of interest to the set of MSPMs. Correspondingly, we focus on analyzing the approximation factor of MSPM in both the complete and incomplete information settings.

5. Complete information

In the complete information setting, we first present a generic result regarding MSPM with arbitrary threshold-based eligible sets.

Theorem 5.1.

Given any , let be an eligible set with threshold such that , and be an arbitrary deterministic tie-breaking rule. Then, the MSPM with and a homogeneous eligible set has of at most

We present the proof in Appendix F.2. To interpret the bound above, suppose that we set . Then it implies that the principal can obtain the utility of first-best solution of the second-best agent. In addition, by properly defining the eligible set, i.e., in this case, she can further improve the potential quality of the candidates, although it might possibly decrease the probability that each agent samples eligible solutions. Intuitively, the existence of the other agents make each agent more competitive in sending signals, thus motivating them to submit more qualified solution.

Remark 5.2.

The role of deterministic tie-breaking rule is essential. Indeed if the principal exploits a randomized tie-breaking rule, it may reduce the power of competition in certain cases since the agents may settle with a bad solution in terms of the principal, as it still gives the agents higher utility with some small but still positive probability due to the randomized tie-breaking rule.

As per Remark 4.8, the mechanism presented in Theorem 5.1 can be either BM or PIM. In what follows, we obtain guarantees for BM and PIM independently by quantifying the approximation factor in Theorem 5.1.

5.1. Bayesian mechanism

For BM, we first show that we can exactly recover the guarantees under the single-agent setting provided in Kleinberg and Kleinberg (2018) by setting proper eligible sets.

Theorem 5.3.

There exists a BM with .

The proof can be found in Appendix F.3. To obtain the result above, we reduce the multi-agent delegation problem to a single-agent one and then use the results by Kleinberg and Kleinberg (2018) regarding the upper bound on the multiplicative approximation factor.

Remark 5.4.

In the proof of Theorem 5.3, we in fact derive a stronger result such that there always is a multi-agent mechanism which yields higher (or equal) principal’s utility compared to any mechanism in the corresponding single-agent setting. We complement this result in Appendix E by proving that for any single-agent problem instance, we can construct a multi-agent instance with higher (or equal) principal’s utility.

The tightness of the bound in Theorem 5.3 is also obtained as follows.

Theorem 5.5.

For any , there exists a problem instance such that no BM achieves .

To construct a matching lower bound, we introduce a super-agent of superior solutions. The super-agent always induce solutions each of which is dominant over any solution by other agents. The principal thus always select one of the super-agent’s solution, which in turn reduces the multi-agent setting to the single-agent setting. Then we borrow the standard worst-case problem instance of the prophet inequalities to construct a matching lower bound. The formal proof is provided in Appendix F.4. In words, if the principal faces a superior agent who overwhelms all the other agents, there is no merit in delegating to multiple agents, other than the superior one.

This naturally bring us to consider a symmetric assumption defined as follows.

Definition 5.6 (Symmetric agents).

If for , and for we say that the agents are symmetric.

This assumption implies that the agents have a similar level of effort and skill, and importantly, all the agents can possibly become the owner of the winner.

Example 5.7.

In the example of research proposal selection process we presented in Section 1, the grant agency (principal) may announce a shortlist of the investigators (agents) with a similar level of research abilities, e.g., by comparing their publication records. Indeed, the grant agency will not include an investigator who is expected to be not qualified than the others in the shortlist.

The symmetry assumption effectively sparks a fire in the competitive tension between the agents due to their similar level of quality. Formally, in the following theorem, we obtain an upper bound on the additive approximation factor of a Bayesian mechanism under the symmetric agents. We refer to Appendix F.5 for the proof.

Theorem 5.8.

Consider symmetric agents such that where is supported on and its c.d.f. satisfies for any for some . Then, there exists a BM with , where converges to as increases.

In order to obtain the above result, we introduce a tighter threshold compared to the ones studied in the canonical prophet inequalities algorithm. Combined with the guarantee of MSPM in Theorem 5.1, followed by some elementary calculations, we derive the subconstant bound above, where the principal attains the optimal utility as and increase. This is in stark contrast to the general setting under which the principal can obtain only a constant factor of the optimal utility.

5.2. Prior-independent mechanism

Now we turn our attention to the class of PIM. 999Standard approach to analyze prior-independent mechanism would be to use Bulow-Klemperer-style result by Bulow and Klemperer (1994), but this does not apply for our case. We discuss more in details in Appendix D. By plugging in Theorem 5.1, we directly obtain the following corollary, where we omit the proof as it is trivial to derive.

Corollary 5.9.

There exists a PIM with of at most .

This corollary mainly implies that even without the eligible set, the multi-agent setting brings some advantages for the principal, which is mainly due to the competitive tension between the agents. As the readers may have noticed, this additive approximation factor is equivalent to the expected difference between the -th (highest) order statistics and -th order statistics of the random variables , which is again the highest order statistics of each agent.

Although there exists a vast amount of papers studying order statistics of similar flavor in the literature, the expected gap , i.e., the expected difference of the highest order statistics between the first-best and second-best agents, has not been studied before to the extent of our knowledge. In this context, we provide some analysis under which the additive factor is nicely bounded, using some characterizations on the order statistics.

Before presenting our positive results, we present the following negative result, which dictates that one should consider a reasonable assumption on the distribution to obtain positive results.

Theorem 5.10.

Suppose that both the principal’s utility functions are supported on for some . For any , there exists a problem instance such that .

We provide the proof in Appendix F.6. Similar to the case of BM, we consider the symmetric agents. In this case, we can derive the following upper bound on the additive approximation factor regardless of the underlying distributions. We present the proof in Appendix F.7.

Theorem 5.11.

Under the symmetric agents, suppose that the principal’s utility functions are supported on . Then there exists a PIM with of , where for all , and it decreases to as increases.

We also note that this upper bound is tight for , i.e., we can construct a problem instance with exactly having . Note that this approximation ratio is a big improvement over the general setting under which the additive approximation factor can be arbitrarily bad.

Moreover, if we consider a specific scenario where the principal’s utility is endowed with a certain class of distributions, we show that the approximation factor can become arbitrarily small as the number of solutions per agent () increases. At the heart of this result, we prove several new properties on the order statistics, which might be of independent interest. First, we show that the expected difference between any top -th and -th order statistics is a nonincreasing function on for any distributions with monotone hazard rates (MHR). Note that a distribution with p.d.f. and c.d.f. has a monotone hazard rate if is nondecreasing on . Using a similar technique, we also show that the expected difference between any -th and -th lowest order statistics is also a nonincreasing function on , for any distribution with monotone reverse hazard rate, where a distribution has MRHR if is nonincreasing on .

In case of the difference between the first and the second order statistics, or the -th and the -th order statistics under the distribution with MHR, Li (2005) shows that they indeed are nonincreasing on with applications to the expected rent of the (reverse) auction. To the best of our knowledge, we first provide a generalized and strengthened result of theirs. Our proof builds upon the techniques by Watt (2021) which proves the convexity of -th order statistics with respect to . We present the precise statement below, and its proof is provided in Appendix F.8.

Lemma 5.12.

Let be i.i.d. random variables equipped with a continuous distribution . Let be corresponding order statistics. Define , i.e., the difference between the -th largest and -th largest order statistics, and . Then, for any , the following holds.

-

(1)

If has MHR, then is a nonincreasing function on .

-

(2)

If has MRHR, then is a nonincreasing function on .

Remark 5.13.

The fact that these quantities are nonincreasing on is fairly intuitive at first glance since as more samples are drawn their order statistics will lie more compactly within a fixed interval, however, this is not true in hindsight for certain cases. For example, in case of Bernoulli distribution with , it is straightforward to check that . Hence, is equivalent to , which holds only for .

Next, we prove that any -th order statistics of i.i.d. random variables with MHR distribution has MHR distribution, which also has not been studied before to the extent of our knowledge. We defer the proof in Appendix F.9.

Lemma 5.14.

Let be i.i.d. random variables equipped with a MHR distribution, then its -th order statistics has MHR distribution for any .

Using the two lemmas described above, we prove that under MHR distribution, PIM can achieve subconstant additive approximation factor as follows. We present the proof in Appendix F.10.

Theorem 5.15.

Under symmetric agents with such that has MHR, there exists a PIM with where is the distribution of and denotes the variance of the distribution. In case of , the approximation factor becomes approximately .

We note that for uniform distribution, the subconstant approximation factor above guarantees the negative dependency on the number of solutions . Thus, it improves largely upon the constant factor approximation of Theorem 5.11, and the constant factor approximation ratio of for the Bayesian mechanism in Kleinberg and Kleinberg (2018).

Furthermore, if we consider a more restrictive class of problem instances, we prove that one can obtain both negative dependencies on and , i.e., the PoA converges to whenever or increases. Similar to the MHR distribution case, our proof heavily relies on the following lemmas.

Lemma 5.16.

Define variables the same as Lemma 5.12. Then, for any , the following holds.

-

(1)

If is nondecreasing on , then .

-

(2)

If is nonincreasing on , then .

Lemma 5.17.

Let be i.i.d. random variables with p.d.f. . Then, the following holds.

-

(1)

If is nondecreasing, then the p.d.f. of the largest order statistics is nondecreasing on .

-

(2)

If is nonincreasing, then the p.d.f. of the smallest order statistics is nonincreasing on .

We highlight that Lemma 5.16 implies that the expected difference between two consecutive order statistics is strictly decreasing over with the factor of . Using the above lemmas, we obtain the following theorem, where the proof is presented in Appendix F.13.

Theorem 5.18.

Under symmetric agents with such that has nondecreasing p.d.f. , there exists a PIM with . In case of , the approximation factor becomes approximately .

This strictly improves upon the approximation factor of Theorem 5.15, since the approximation factor has positive effects on both and . This highlights that delegating to multiple agents indeed brings significant advantages over the single-agent case, under which the best one may hope for is to construct constant factor approximation ratio even with Bayesian mechanism. Notably, the approximation factor decreases to zero as or increases, i.e., the principal’s utility converges to . It remains a major open problem to see whether the guarantees above are tight or not.

6. Incomplete information

Recall that in the incomplete information setting, each agent decides his own action at the interim stage of the Bayesian game, i.e., when he observes his own solutions. More formally, agent ’s strategy is a function from the observed solutions to a signal, which is typically a subset of solutions. We denote by the agent’s action given the observed solution . Given and others’ strategies , agent ’s strategy induces the following expected utility.

where denotes the p.d.f. of observing . Namely, each agent accounts for the probability that certain solutions are observed by the other agents, confirms their corresponding strategies, and computes his own utility based on them. This process is captured by the integral in the last equation. Note that the expectation inside the integral accounts for the random bits of the mechanism, which does not appear in deterministic mechanisms.

Then, given the others’ strategies , agent ’s expected utility of playing can be written as

Finally, a Bayesian Nash equilibrium can be defined as follows.

Definition 6.1 (Bayesian Nash Equilibrium).

Under the incomplete information setting, given a mechanism , a set of strategies is defined to be a Bayesian Nash equilibrium (BNE), if for any , satisfies the following for any other strategy of agent .

Our main objective is to construct a mechanism that induces a large principal’s expected utility under its BNE. In the case of incomplete information, the analysis of the approximation ratio becomes more involved as all the computations of the expected payoff of some strategies entail probabilistic arguments regarding the realization of the others’ solutions. Moreover, since the feasible strategy depends on the realization of the solutions for each agent, its analysis significantly differs from the standard Bayesian games such as the first-price auction or the all-pay auction. Due to this fact, even under the symmetric agents, the standard technique of computing symmetric BNE in the first-price auction, e.g., which involves the use of the Envelope theorem (Milgrom and Segal, 2002), does not apply to our setting. Despite these analytical challenges, we succeed in obtaining several positive results in terms of the PIM.

Before presenting our main result on PIM, we first study the class of the Bayesian mechanism. In the case of BM, it is straightforward to see that all the results in the complete information setting hold in the incomplete information setting as well.

We skip the proofs as exactly the same arguments of the corresponding proofs in the complete information setting directly carry over to the incomplete information setting.

In the case of PIM, similar to the complete information setting, we can directly argue that the additive approximation factor can be arbitrarily bad. We omit the proof as it is exactly the same as the proof of Theorem 5.10.

Corollary 6.3.

Theorem 5.10 still holds for the incomplete information setting.

This again naturally leads us to focus on the symmetric agents. Interestingly however, in the following theorem, we show that even under the symmetric agents, for any PIM, there exists a problem instance such that proposing a solution that minimizes the principal’s utility constructs a BNE, and thus we can construct a problem instance such that the approximation factor can be arbitrarily bad. We defer the proof in Appendix F.14.

Theorem 6.4.

Under the symmetric agents, there exists no PIM such that . For the uniform distribution , there exists no PIM such that , i.e., the additive approximation factor of any PIM can be arbitrarily bad as increases given .

Compared to the subconstant approximation ratio of Theorem 5.15 and 5.18 in the complete information setting, Theorem 6.4 implies rather pessimistic consequence such that its worst-case guarantees may become arbitrarily bad, alike to the efficiency of prior-independent mechanism in the single-agent setting. Thus, the gain from multi-agent delegation becomes highly restrictive.

This negative result mainly arises from the fact that each agent has a utility function which is negatively correlated with the principal’s utility, and they have limited information regarding each other’s solutions. This induces the agents to propose more in a selfish manner, compared to the complete information setting.

This phenomenon resembles the bid shading effect in the BNEs of the first-price auction, in which the bidders tend to bid less than their valuations in equilibriums. Due to the lack of information on the other’s strategy, each agent may tend to submit a candidate which brings more ex-post utility even though it has a smaller chance of being selected. Similarly from the first-price auction, this is mainly to prevent the case in which he submits more in favor of the principal when the others’ solutions were revealed to be less competitive in terms of being selected. Combined with this effect and the fact that the agent’s utility is strongly negatively correlated with the principal’s utility, each agent tends to submit a solution that minimizes the principal’s utility.

In this context, one natural question is whether we can recover a better approximation ratio in more restricted problem instances. To this end, we consider the following assumption.

Definition 6.5 (Independent utility).

A problem instance satisfies independence if is a product measure over and , i.e., , such that each of and are associated with the distributions and respectively, and is independent for .

Note that with independent utility assumption, we can overcome the bad problem instance presented in the proof of Theorem 6.4, as the principal and the agents do not longer have negatively correlated utility, but are rather not correlated at all. Although we only obtain a positive result under the independent utility assumption due to the analytical tractability, we hope that one may extend our analysis into the case where the principal and the agents have positively correlated utility (or mild amount of negative correlation), and we leave it as a major open problem.

Due to the intrinsic difficulties in analyzing BNE, we consider a more general solution concept of approximate equilibrium defined as follows.

Definition 6.6 (Approximate BNE).

Given a mechanism , a set of strategies is -approximate BNE if for any , satisfies the following for any other strategy of agent .

Our definition of PoS and PoA naturally carries over to the approximate equilibrium. We eventually present our main result in the incomplete information setting. Our main result in the incomplete information setting is as follows.

Theorem 6.7.

Under the symmetric agents and independent utility with , there exists a PIM such that there exists -approximate BNE that results in the optimal utility, i.e., , where . Note that converges to as increases.

The proof can be found in Appendix F.15. Remarkably, this implies that the principal can recover the optimal utility if the agents agree to sacrifice only a constant portion of their utility. This is indeed possible due to the independence assumption and the fact that the agent does not have the exact information on the others’ solutions.

Our proof is based on analyzing the probability of the event that the principal’s and the agent’s utility is somehow aligned, i.e., an agent maximizes his expected utility by proposing his best solution in terms of principal. We show that this probability is lower bounded by ,101010In Appendix A, we numerically verify that our lower bound is almost tight. which converges to as increases. The proof heavily relies on the FKG inequality (Lemma F.9) and some properties on the joint density function of two order statistics.

Remark 6.8.

In appendix C, we also prove that using a similar but more involved technique, we can derive that there exists a PIM such that under some Bayes correlated equilibrium, it achieves -approximation, i.e., constant approximation ratio for sufficiently large .

Remark 6.9.

Note that in some cases it might be complicated or even computationally intractable for each agent to compute a best-response given the others’ strategies since he needs to account for every possible realization of the solutions for the others. In this context, it would be reasonable for the agents to follow the mechanism’s recommendation to propose a solution that maximizes the principal’s utility, even though it may slightly decrease their utility up to some constant factors.

7. Examination cost

Since we allow multiple agents to propose a solution, on one hand, it helps the principal find a better solution because she can compare more solutions as observed in Section 5 and 6. On the other hand, since the principal needs to select which ones to choose among the multiple candidates, it entails an additional burden to evaluate the candidates, compared to the single-agent setting.

Example 7.1.

Suppose that a project manager delegates the task of finding a solution for a project to multiple teams. Each team proposes a candidate and then the manager needs to find the best candidate by sequentially examining the candidates. This procedure can be costly for the manager and even cannot be parallelized since the manager may want to examine the candidates by herself.

To effectively study the trade-off between such a burden in evaluating the candidates and the principal’s utility, we introduce the following notion of the examination cost of a mechanism.

Definition 7.2 (Examination).

Given a set of solutions and corresponding strategies , suppose that mechanism can eventually choose a winner among a subset . The mechanism cannot directly access the subset , and does not have information on their values, but only knows from whom each candidate in is proposed. In order to select the winner, the mechanism should examine the solution by accessing each candidate in , and this incurs an examination cost of . We call this procedure an examination process.

It is important to note that the principal may randomize the examination process. We further denote that a mechanism has (examination) budget , if its total cost of examination does not exceed for any realized set of solutions and any corresponding strategies.

We aim to study the trade-off between the examination budget and the approximation factor of a mechanism. Unlike the previous results in which the MSPM can examine all the candidates proposed by the agents and commit to the best one, if the examination budget is finite, the principal should selectively examine them. In this context, we present the following variant of MSPM.

Definition 7.3 (Randomized single-proposal mechanism).

In a randomized single-proposal mechanism (RSPM) with budget , a tie-breaking rule , an eligible set are announced by the principal for each agent . Each agent proposes up to one solution, and the principal selects candidates uniformly at random and adopts the one of them to maximize her utility.

Note that RSPM with budget always examine at most candidates. As it can be observed in the definition of the RSPM, once a candidate is submitted by agent , there is no chance of getting accepted by the mechanism. This implies that there is no incentive for the agent to submit a candidate beyond the eligible set. In this context, we impose the following mild assumption.

Assumption 7.4 (Rationality).

Given a RSPM with arbitrary tie-breaking rule and eligible sets , each agent for does not play strategy if .

In Section 5 and 6, we assume that the principal can examine all candidates (at most ) and takes the best one as the winner, i.e., the principal has a sufficient budget . To study the nontrivial effect of examination cost, we assume that the budget is not sufficient to examine all the candidates, i.e., . We analyze RPSM in the complete information setting by generalizing Theorem 5.1 in Section 5 to the limited budget case.

Theorem 7.5.

Given any , let be an eligible set with threshold such that and be an arbitrary deterministic tie-breaking rule. Let . Given , RSPM with and a homogeneous eligible set has of at most

Its proof structure follows that of Theorem 5.1, but is more involved due to the randomness in the mechanism. Formal proof is deferred to Appendix F.16. This result depicts the trade-off between the budget and the the efficiency of a mechanism. Indeed, the upper bound on PoA presented above decreases as increases, and by plugging we can exactly recover the guarantee provided in Theorem 5.1. This is fairly intuitive as if the principal can evaluate more candidates, then she can commit to more efficient solutions. Similar to Remark 4.8, RSPM can be either BM or PIM depending on the choice of the eligible sets. For PIM, we can directly obtain the following result.

Corollary 7.6.

There exists a PIM having budget with of .

Importantly, quantifying the additive approximation factor in Corollary 7.6 is intrinsically more challenging than the previous result without the examination cost, since we need to deal with the expected difference of two order statistics which are not consecutive. One straightforward approach would be to simply sum up the bound for two consecutive ones, but we found this bound to be cumbersome and couldn’t find any take-away. Analyzing or simplifying this gap for arbitrary budget and deriving analogous results as in Section 5 remains a major open problem.

Although RSPM has the benefit of its simplicity, however, it is not a clever choice as it examines the candidates in uniformly at random. A better approach might be to exploit the prior information on the distributions regarding the quality of candidates, which might be an interesting topic.

8. Conclusion

In this paper, we present a thorough study on efficient delegation mechanisms against multiple agents, spanning the analysis of Bayesian/prior-independent mechanisms in complete/incomplete information settings We mainly reveal that the competitive tension arising from the multiple agents enables us to obtain efficient prior-independent mechanisms, in stark contrast to the Bayesian single-agent mechanism by Kleinberg and Kleinberg (2018). Furthermore, the gain from competition largely depends on the information available to the agents and the correlation between the agent’s and the principal’s utility, e.g., it significantly degrades in the incomplete information setting with strongly negatively correlated utility. Closing the gap between the approximation factors in various regimes and analyzing exact Bayes Nash equilibriums along with its efficiency in the incomplete information setting remains as major open problems. In perspective of model, exploring the impact of examination costs more in details, endogenizing agents’ costs to search/choose solutions, and studying the strategic tension arise from a repeated interaction would be interesting directions as well.

Acknowledgements.

The work is partially supported by DARPA QuICC, NSF AF:Small #2218678, and NSF AF:Small # 2114269.References

- (1)

- Abolhassani et al. (2017) Melika Abolhassani, Soheil Ehsani, Hossein Esfandiari, MohammadTaghi Hajiaghayi, Robert Kleinberg, and Brendan Lucier. 2017. Beating 1-1/e for ordered prophets. In Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing. 61–71.

- Alaei et al. (2012) Saeed Alaei, MohammadTaghi Hajiaghayi, and Vahid Liaghat. 2012. Online prophet-inequality matching with applications to ad allocation. In Proceedings of the 13th ACM Conference on Electronic Commerce. 18–35.

- Alon and Spencer (2016) Noga Alon and Joel H Spencer. 2016. The probabilistic method. John Wiley & Sons.

- Alonso et al. (2014) Ricardo Alonso, Isabelle Brocas, and Juan D Carrillo. 2014. Resource allocation in the brain. Review of Economic Studies 81, 2 (2014), 501–534.

- Alonso and Matouschek (2008) Ricardo Alonso and Niko Matouschek. 2008. Optimal delegation. The Review of Economic Studies 75, 1 (2008), 259–293.

- Armstrong and Vickers (2010) Mark Armstrong and John Vickers. 2010. A model of delegated project choice. Econometrica 78, 1 (2010), 213–244.

- Barlow and Proschan (1975) Richard E Barlow and Frank Proschan. 1975. Statistical theory of reliability and life testing: probability models. Technical Report. Florida State Univ Tallahassee.

- Bechtel and Dughmi (2020) Curtis Bechtel and Shaddin Dughmi. 2020. Delegated stochastic probing. arXiv preprint arXiv:2010.14718 (2020).

- Bechtel et al. (2022) Curtis Bechtel, Shaddin Dughmi, and Neel Patel. 2022. Delegated Pandora’s box. arXiv preprint arXiv:2202.10382 (2022).

- Bergemann and Morris (2016) Dirk Bergemann and Stephen Morris. 2016. Bayes correlated equilibrium and the comparison of information structures in games. Theoretical Economics 11, 2 (2016), 487–522.

- Bulow and Klemperer (1994) Jeremy I Bulow and Paul D Klemperer. 1994. Auctions vs. negotiations.

- Cerone and Dragomir (2005) Pietro Cerone and Sever S Dragomir. 2005. Bounds for the Gini mean difference via the Sonin identity. Computers & Mathematics with Applications 50, 3-4 (2005), 599–609.

- Correa et al. (2017) José Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. 2017. Posted price mechanisms for a random stream of customers. In Proceedings of the 2017 ACM Conference on Economics and Computation. 169–186.

- David (1997) HA David. 1997. Augmented order statistics and the biasing effect of outliers. Statistics & probability letters 36, 2 (1997), 199–204.

- Elder (2016) Sam Elder. 2016. Bayesian adaptive data analysis guarantees from subgaussianity. arXiv preprint arXiv:1611.00065 (2016).

- Fuchs et al. (2022) William Fuchs, Satoshi Fukuda, and Mahyar Sefidgaran. 2022. Who to Listen to?: A Model of Endogenous Delegation. (2022).

- Gan et al. (2022) Tan Gan, Ju Hu, and Xi Weng. 2022. Optimal contingent delegation. Journal of Economic Theory (2022), 105597.

- Gilligan and Krehbiel (1989) Thomas W Gilligan and Keith Krehbiel. 1989. Asymmetric information and legislative rules with a heterogeneous committee. American journal of political science (1989), 459–490.

- Hajiaghayi et al. (2007) Mohammad Taghi Hajiaghayi, Robert Kleinberg, and Tuomas Sandholm. 2007. Automated online mechanism design and prophet inequalities. In AAAI, Vol. 7. 58–65.

- Holmstrom (1980) Bengt Holmstrom. 1980. On the theory of delegation. Technical Report. Discussion Paper.

- Kleinberg and Kleinberg (2018) Jon Kleinberg and Robert Kleinberg. 2018. Delegated search approximates efficient search. In Proceedings of the 2018 ACM Conference on Economics and Computation. 287–302.

- Krengel and Sucheston (1987) Ulrich Krengel and Louis Sucheston. 1987. Prophet compared to gambler: an inequality for transforms of processes. The Annals of Probability 15, 4 (1987), 1593–1599.

- Krishna (2001) Vijay Krishna. 2001. Asymmetric information and legislative rules: Some amendments. American Political science review 95, 2 (2001), 435–452.

- Krishna and Morgan (2008) Vijay Krishna and John Morgan. 2008. Contracting for information under imperfect commitment. The RAND Journal of Economics 39, 4 (2008), 905–925.

- Lewis (2012) Tracy R Lewis. 2012. A theory of delegated search for the best alternative. The RAND Journal of Economics 43, 3 (2012), 391–416.

- Li (2005) Xiaohu Li. 2005. A note on expected rent in auction theory. Operations Research Letters 33, 5 (2005), 531–534.

- Lopez and Marengo (2011) Manuel Lopez and James Marengo. 2011. An upper bound for the expected difference between order statistics. Mathematics Magazine 84, 5 (2011), 365–369.

- Martimort and Semenov (2008) David Martimort and Aggey Semenov. 2008. The informational effects of competition and collusion in legislative politics. Journal of Public Economics 92, 7 (2008), 1541–1563.

- Milgrom and Segal (2002) Paul Milgrom and Ilya Segal. 2002. Envelope theorems for arbitrary choice sets. Econometrica 70, 2 (2002), 583–601.

- Samuel-Cahn (1984) Ester Samuel-Cahn. 1984. Comparison of threshold stop rules and maximum for independent nonnegative random variables. the Annals of Probability (1984), 1213–1216.

- Ulbricht (2016) Robert Ulbricht. 2016. Optimal delegated search with adverse selection and moral hazard. Theoretical Economics 11, 1 (2016), 253–278.

- Watt (2021) Mitchell Watt. 2021. Concavity and Convexity of Order Statistics in Sample Size. arXiv preprint arXiv:2111.04702 (2021).

Appendix A Numerical Experiments on the Tightness of Theorem 6.7

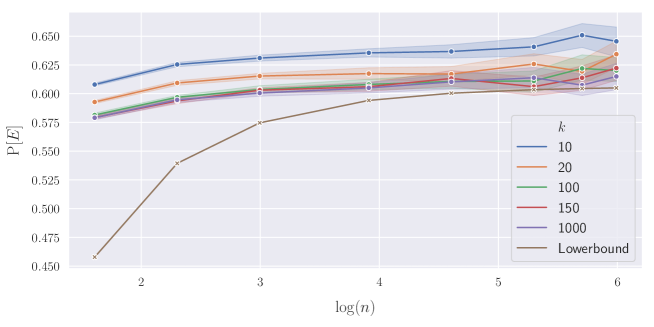

We here numerically verify that the lower bound on obtained in the proof of Theorem 6.7, i.e., , is almost tight. Figure 1 represents with respect to the value of for some choices of . To obtain the true value of probability of the event , we simulate the principal and agents and compute the frequency of the event that each agent’s utility is aligned, i.e., proposing a solution that maximizes the principal’s utility also maximizes the agent’s utility, for every agent. To present some details in the experiment, we consider and . For each pair of and , we run times to compute the probability that the event happens. We repeat this procedure times to obtain the variance for each setting, which is plotted as the shade in the figure. The main take-away here is that the lower bound and the average value of the quantity is indeed becoming tight as increases. As a side note, one can observe that as increases the precision error appears in each experiment (shade) becomes wider. This is because large introduces more randomness in each experiment which requires more samples to stabilize its average, and thus we believe it not to be a meaningful phenomenon.

Appendix B Further discussion on feasible mechanisms

Another reasonable choice of mechanism will be to require each agent submitting certain number, say two, of solutions, i.e., multi-proposal mechanism. Under this mechanism, each agent might select a pair of aggressive solution with large ex-post utility but smaller chance to be selected, and conservative solution with small ex-post utility but larger probability of winning, in order to balance these features of two solutions. More abstractly, one may consider a mechanism that requires each agent to signal some statistics of the observed solutions, e.g., sample average or the number of eligible solutions, upon the solutions themselves. As astute readers may have noticed, in the complete information setting, however, the revelation principle style of result allows us to reduce any mechanism to single-proposal mechanism, so such generalization does not help. This is formalized in Theorem 4.11. Note that this reduction does not preclude any randomized mechanism.

Appendix C Bayes Correlated equilibrium

In this section, we discuss that the mechanism presented in Theorem 6.7 also has an efficient Bayes correlated equilibrium. To be more specific, we are interested in the notion of Bayes correlated equilibrium (Bergemann and Morris, 2016). Suppose that there exists a mediator who is able to access the realization of all the solutions observed by the agents. Given the realization of all the solutions observed by the agents, the mediator recommends a strategy for each agent . It is important to note that the mediator recommends the strategy based on observing all the agents’ solutions. Given the recommended strategy and observed solution , agent plays a strategy . The procedure of recommending strategies is specified as a part of the mechanism , and we denote by the interim allocation function, i.e., the selected winner, of the mechanism given and

Then, given and , agent ’s expected utility of playing is

and agent ’s total expected utility of playing is

We now define a Bayes correlated equilibrium as follows.

Definition C.1 (Bayes correlated equilibrium).

We say that induces a Bayes correlated equilibrium (BCE) if for any ,

for any other strategy , i.e., there exists no incentive to deviate from the mediator’s recommendation.

Compared to BNE, due to the existence of the additional signals provided by the mediator who can observe all the solutions, both the principal and agents may enjoy the increased utility. In the following theorem, we prove that there exists a PIM such that it achieves asymptotically constant multiplicative approximation factor for some BCEs. We provide the proof in Appendix F.17

Theorem C.2.

Consider a symmetric and independent setting such that the distributions of the both principal’s and agent’s utility follow . Then, there exists an -approximate PIM and corresponding BCE.

Appendix D Bulow-Klemperer-style result for prior-independent mechanism

In constructing efficient PIM, one standard way would be to construct PIM from BM by applying the Bulow-Klemperer-style result by Bulow and Klemperer (1994), which considers a fictitious BM with agents to find a good upper bound on the efficiency of PIM with agents. More precisely, they first show the existence of PIM (auction in their case) which always allocates the item to some bidders and then prove that such PIM is optimal among the mechanism that always allocates the item. Then, for any Bayesian mechanism with an arbitrary reserve price, one can consider a fictitious auction with agents such that it runs with the first agents, and if it does not allocate the item, then it allocates the item to -th agent. Given the observations above, one can conclude that the PIM with agents defined above outperforms arbitrary BM with agents, and thus we can derive the approximation factor of PIM based on BM. This technique, however, does not work in our case as we cannot easily argue that MSPM that admits all the solutions induces the optimal utility for any mechanism that always adopts the winner. This is because we can consider a PIM that always admits all the solutions for some agents, but enforce some nontrivial (which does not always accept any solution) eligible sets for other agents. Indeed, this mechanism may outperform MSPM that admits all solutions, since it may motivate the other agents with nontrivial eligible sets to propose more in favor of the principal, while maintaining the mechanism to always delegate to some agents.

Appendix E Comparing multi-agent and single-agent delegation

To give a brief intuition in how one can reasonably compares the multi-agent and single-agent setting in terms of the principal, we start with an example.

Example E.1.