[subfigure]position=bottom

Debiased Inference for Dynamic Nonlinear Models with Two-way Fixed Effects

Abstract

Panel data models often use fixed effects to account for unobserved heterogeneities. These fixed effects are typically incidental parameters and their estimators converge slowly relative to the square root of the sample size. In the maximum likelihood context, this induces an asymptotic bias of the likelihood function. Test statistics derived from the asymptotically biased likelihood, therefore, no longer follow their standard limiting distributions. This causes severe distortions in test sizes. We consider a generic class of dynamic nonlinear models with two-way fixed effects and propose an analytical bias correction method for the likelihood function. We formally show that the likelihood ratio, the Lagrange-multiplier, and the Wald test statistics derived from the corrected likelihood follow their standard asymptotic distributions. A bias-corrected estimator of the structural parameters can also be derived from the corrected likelihood function. We evaluate the performance of our bias correction procedure through simulations and an empirical example.

Keywords: analytical bias correction, dynamic panel models,

incidental parameter problem, two-way fixed effects

JEL Classification C23

1 Introduction

Panel data, also known as longitudinal data, is common in empirical studies where observations are collected from individuals over a span of time periods. These data sets often contain unobserved heterogeneities specific to individuals or time periods which can be correlated with the covariates in a regression context. To account for such unobserved heterogeneities, a standard technique is to use two-way fixed effects, where individual and time effects are included for every individual and every time period .

Unlike linear models, however, the usual technique of within transformation is generally not applicable to nonlinear maximum likelihood models, and the estimation of the fixed effects is often inevitable. Such an estimation induces the incidental parameter problem (IPP) of Neyman and Scott (1948) in the sense that the estimators of the fixed effects contaminate the likelihood function. See Lancaster (2000) and Fernández-Val and Weidner (2018) for recent reviews. Under a large asymptotics, the estimators of individual and time effects converge at a rate of, respectively, and . These slow rates of convergence cause the asymptotic distribution of the likelihood function, evaluated at the estimated effects, to have a non-zero center and exhibit bias. Consequently, many likelihood-based test statistics inherit such a bias and no longer follow their standard asymptotic distributions, leading to incorrect test sizes. In particular, the likelihood-ratio (LR), the Lagrangian-multiplier (LM), and the Wald test statistics are no longer -distributed under the null (about the true value of the structural parameter, ). It is worth noting that such an asymptotic bias would become negligible under as , if the model included only the individual effects; or under as , if the model only included the time effects. However, when the model includes both effects, there is no such relative rate under which the bias becomes negligible, and certain procedures have to be employed to correct the bias. In this paper, we consider a generic class of dynamic nonlinear models with two-way fixed effects and develop a bias-corrected likelihood free of the asymptotic bias under where and grow proportionally. Our bias-corrected likelihood essentially approximates an IPP-free infeasible likelihood in the sense of profiled likelihoods (see, e.g., Pace and Salvan (2006)). We formally prove that the LR, the LM, and the Wald test statistics are all asymptotically under the null when they are derived from our corrected likelihood.

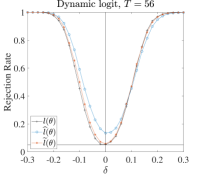

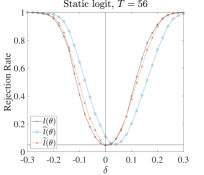

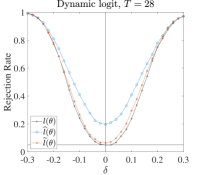

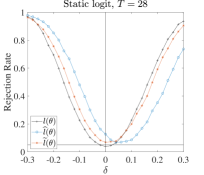

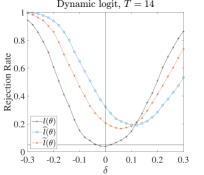

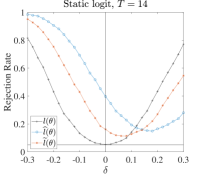

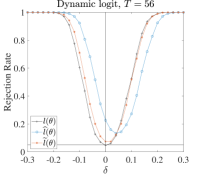

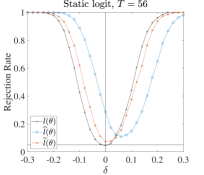

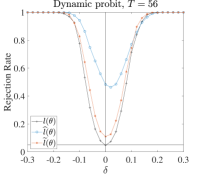

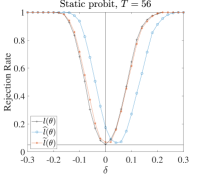

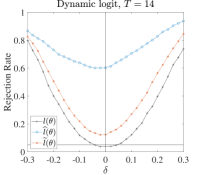

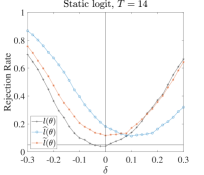

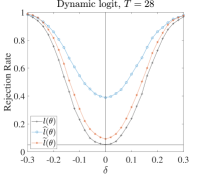

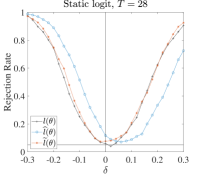

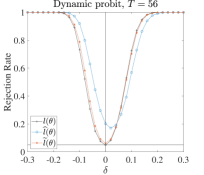

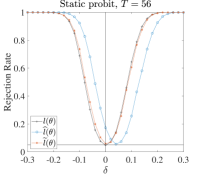

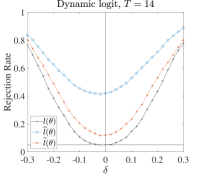

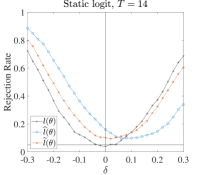

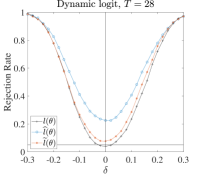

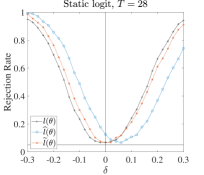

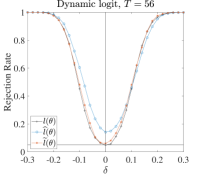

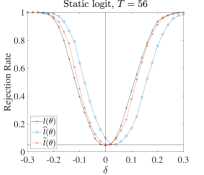

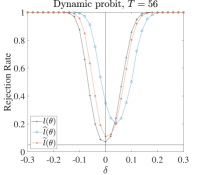

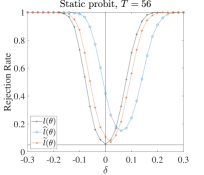

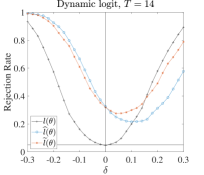

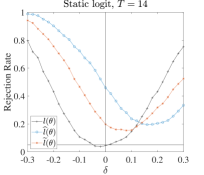

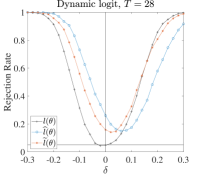

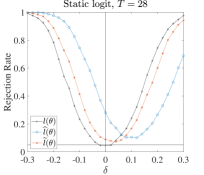

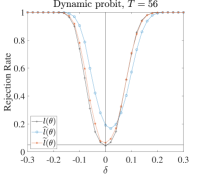

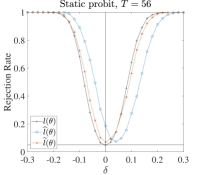

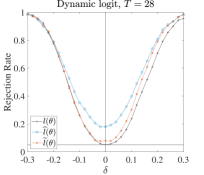

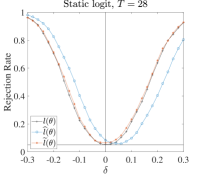

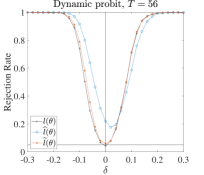

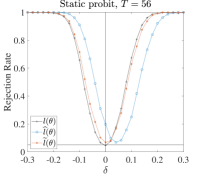

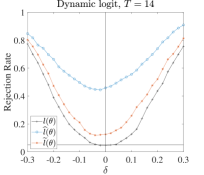

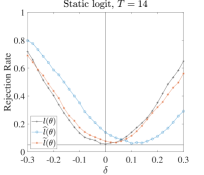

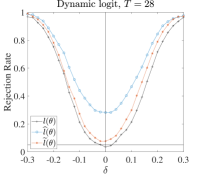

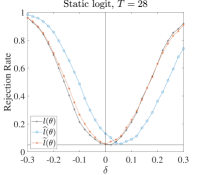

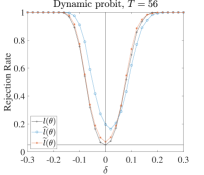

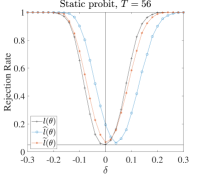

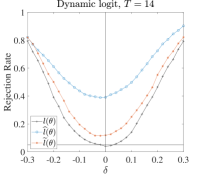

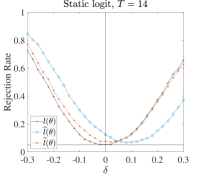

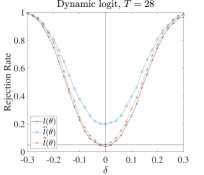

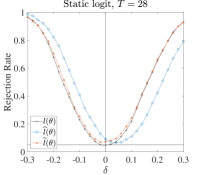

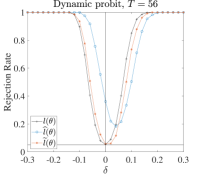

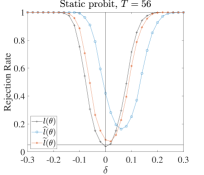

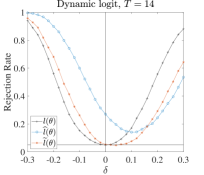

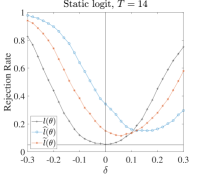

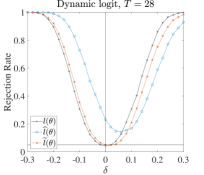

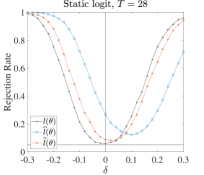

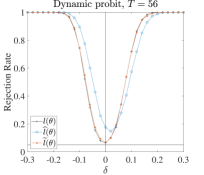

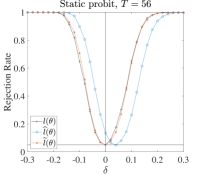

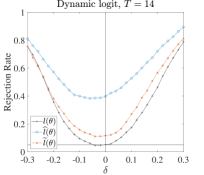

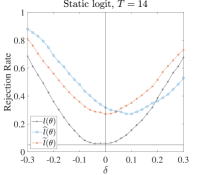

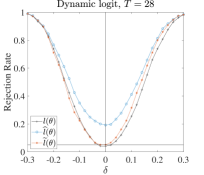

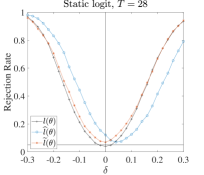

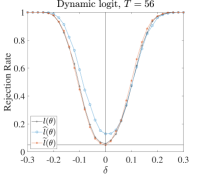

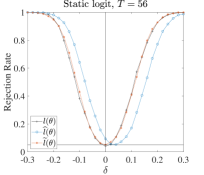

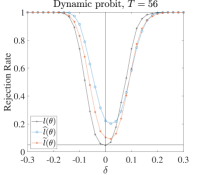

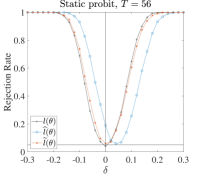

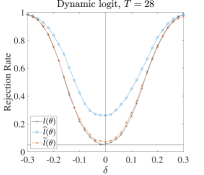

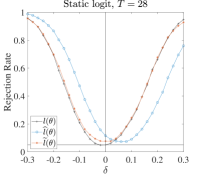

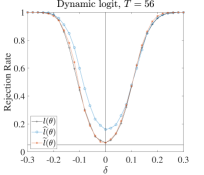

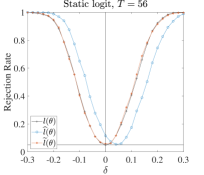

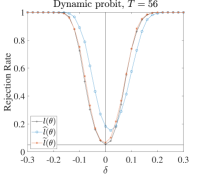

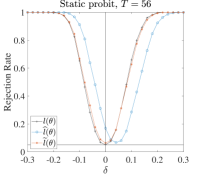

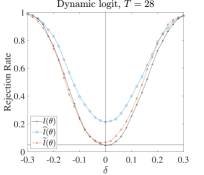

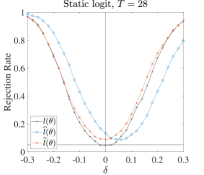

Figure 1 illustrates the consequences of the IPP in test statistics for logit models. The figure displays the simulated rejection rates of the LR test, with a significance level of 5%, under a range of null hypotheses about . The rejection rates are calculated using different likelihood functions: i) an infeasible likelihood that is free of the IPP, ii) the original (contaminated) likelihood that is affected by the IPP, and iii) the bias-corrected likelihood that we develop. The precise definition of these likelihood functions will become clear as we proceed. The plotted curves show that the LR test using the original likelihood severely over-rejects the true null hypothesis at , with rejection rates approaching for both the dynamic and static logit models. This is the IPP in the context of hypothesis testing, and it arises due to the inclusion of the estimated two-way effects in the original likelihood. The LM and Wald tests using the original likelihood also suffer from the IPP. On the other hand, the LR test using the infeasible likelihood delivers rejection rates very close to the nominal level of at for both the dynamic and static models. Our bias-corrected likelihood produces a rejection rate close to the nominal level of at . The performance is comparable to the infeasible likelihood.

Notes: The plotted curves are the rejection rates of the LR tests based on an infeasible likelihood , the original likelihood , as well as our corrected likelihood function . They are all profiled likelihood functions whose exact definitions will become clear as we proceed. The dynamic model is and the static model is , where is the indicator function, with , and is standard logistic. and are generated in the same way as . Other details are given in Section 4. The true value of structural parameter for the dynamic model and for the static. The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Several papers in the literature on the IPP in the presence of two-way fixed effects are closely related to our method. For example, Fernández-Val and Weidner (2016) propose a bias correction method for the maximum likelihood estimator (MLE) of a generic class of nonlinear dynamic model with two-way additive effects. See also Chen et al. (2021) for a similar approach for interactive effects. Both approaches of Fernández-Val and Weidner (2016) and Chen et al. (2021) are “parameter-based” in the sense that they develop formulas for the asymptotic bias of the MLE. However, bias corrections of the MLE do not generally lead to bias corrections of the likelihood or its related objects. For instance, the LR test statistic generally does not follow a -distribution under the null, even when evaluated at the bias-corrected MLE. This paper differs from Fernández-Val and Weidner (2016) and Chen et al. (2021) in that our approach is “likelihood-based” as the correction applies to the likelihood function itself. This benefits objects in the entire likelihood hierarchy. In this paper, the objects of interest are the LR, the LM, and the Wald test statistics.

In addition to this, we accommodate a wider class of models where the two-way effects enter the model in general, and potentially non-additive, ways. A particular class is the recent heterogeneous slope coefficient model. In such a model, the slope coefficients may depend on both and , due to unobserved heterogeneities in both dimensions. For instance, the slope coefficient may be given by (see, e.g., Keane and Neal (2020)) or (see, e.g., Lu and Su (2023) and Hahn et al. (2023)). The heterogeneous slope coefficient model is useful in many empirical works as it allows for richer forms of heterogeneities compared to the traditional “heterogeneous intercept” model. However, such models are generally subject to the incidental parameter problem as well, and bias correction procedures are not yet well-discussed.

Our procedure is similar to Jochmans and Otsu (2019), who also develop a likelihood-based bias correction method. In fact, Jochmans and Otsu (2019) already show using simulations that the LR, the LM, and the Wald test all benefit from their corrected likelihood with reduced size distortions. However, Jochmans and Otsu (2019) only consider models with strictly exogenous regressors, whereas we allow for predetermined regressors as well. Beyond this point, we also provide formal proofs for the asymptotic properties of the corrected likelihood and of the derived LR, the LM, and the Wald statistics under relatively mild regularity conditions. Amongst other things, we formally establish that the profiled score inherits the bias correction of the likelihood. This seems to be missing in the current relevant literature but can be important for the general understanding of the behaviors of the bias-corrected likelihood and its derived objects.

Other works for models with two-way fixed effects include Hahn and Moon (2006), Bai (2009), Bai (2013), Moon and Weidner (2015), Charbonneau (2017), and Hong et al. (2022). For models with individual effects only, the literature is extensive. For instance, Rasch (1961), Andersen (1970), Chamberlain (1980), Arellano and Bond (1991), and Lancaster (2002) provide solutions that eliminate the IPP under fixed for rather narrow classes of models. Several bias correction methods are also available. They do not eliminate the IPP bias but provide asymptotically unbiased MLE under jointly where . They include Hahn and Kuersteiner (2002), Hahn and Newey (2004), and Hahn and Kuersteiner (2011) which are parameter-based; and Dhaene and Jochmans (2015b), Arellano and Hahn (2016), Dhaene and Sun (2021), and Schumann (2022) which are likelihood-based. In addition, Sartori (2003), Arellano and Bonhomme (2009), and De Bin et al. (2015) achieve bias corrections through integrated likelihoods; Bellio et al. (2023) through parametric bootstrap; while Galvao and Kato (2016) focus on quantile regressions. See also Kosmidis (2014) for discussing bias corrections in a generic context.

The rest of this paper is organized as follows. Section 2 presents a detailed discussion on IPP under a generically specified nonlinear model with both individual and time effects. Section 3 gives the main results, the corrected likelihood function, and related asymptotic theory. Section 4 presents some simulation results on the performance of the bias correction and Section 5 presents an empirical example. Finally, Section 6 leaves some concluding remarks. All proofs are in the appendix. Items with a letter-prefixed reference are also in the appendix.

2 Bias in Two-way Fixed-effect Models

In this section, we present a detailed discussion of the IPP for two-way models. We briefly explain the class of two-way models we focus on; the IPP in our context; and the intuition of the bias correction procedure.

2.1 Fixed-effect Models

Throughout the paper, denotes the log-likelihood (“likelihood” hereafter) of conditional on where are, respectively, the structural parameter, the individual, and time effects. are their true values. The covariate may contain lagged values of . We omit the covariate for simplicity whenever possible. We use and to denote, respectively, the partial and total derivative of some with respect to (w.r.t.) the variable and evaluated at some . For instance, is the partial derivative with respect to argument and evaluated at some values . Higher-order derivatives are written in a similar manner. We consider with fixed and finite dimensions while and entering the density in an arbitrary but known form. Our procedure applies to nonseparable panel models where the two-way effects enter the model arbitrarily (see, e.g., Chernozhukov et al. (2013)). We use the following examples to motivate our settings.

Example 1 (nonlinear model with two-way effects)

We consider a probit model with observation-level likelihood function

where is the standard normal c.d.f. and is the linear index. can take various forms such as

| (2.1) | ||||

| (2.2) | ||||

| (2.3) | ||||

| (2.4) |

for some additional covariates . The specification in (2.1) represents the simplest additive-effect model. Identification can be achieved by adding the condition, e.g., . Equations (2.2) to (2.4) are essentially heterogeneous slope models. (2.2) is used by, e.g., Keane and Neal (2020). The structural effect is accompanied by so that the overall effect is both time- and individual-heterogeneous. Identifications of the effects can be achieved by imposing, e.g., . (2.3) is seen in, e.g., Lu and Su (2023) and Hahn et al. (2023). The fixed effects are allowed to interact with the common parameter. Identification can be achieved by imposing, e.g., . Specification (2.4) is a general heterogeneous slope model. The parameters are identified as long as vary across and do not overlap with .

Example 2 (nonlinear multiple-index model)

Consider

with

where is the Poisson distribution with mean , are the structural parameters, and are covariates. may be estimated by the zero-inflated Poisson model. The exact likelihood of is omitted here because it is irrelevant for the discussion. However, it shall be clear that there are two linear indices and ; and the effects and enter different ones. Our procedure applies to this class of models as well. In particular, we allow the fixed effects to be included in different linear indices. The approaches of Fernández-Val and Weidner (2016) and Jochmans and Otsu (2019) may not be employed (again, not without modifications) because the fixed effects are no longer additive and the model contains the predetermined regressor .

2.2 Incidental Parameter Problem

Next, we explain the bias in the asymptotic distribution of the likelihood and illustrate the consequence of such a bias to various test statistics. We consider as for some . Let for and , with . For a given , denote

| (2.5) | ||||

where represents the expectation given the true parameter values, strictly exogenous covariates, and the initial conditions of predetermined covariates.111The estimation of may require the use of Lagrangian with certain identification conditions depending on the way the fixed effects enter the model. In addition, let

Here is the original (profiled) likelihood and the infeasible (but IPP-free) likelihood. can be Taylor-expanded as

for some remainder term , where the incidental parameter scores

Since and are correlated, in general. Analogously, . This causes indicating the asymptotic distribution of has a nonzero center hence is biased.

Intuitively, is asymptotically biased because it depends on and suffers from the contamination of the slow convergence rates of (relative to ). The profiled score, in turn, inherits this bias so that either. Consequently, the asymptotic distribution of is nonzero centered. This causes the standard maximum likelihood asymptotic theory to break down. In Example A.1, we use an example of a two-way panel autoregressive model to illustrate the bias.

Many derived test statistics no longer follow their theoretical asymptotic distribution under the null, as a consequence of being nonzero-centered. Consider a generic null hypothesis where is an vector-valued function with the Jacobian of a full row rank. Denote subject to , and . Under , the LR test statistic is

where

with . For to be asymptotically , it is required that is asymptotically normal with mean zero. This is, however, not true due to the IPP in the likelihood. As a result, is not asymptotically and the standard LR test delivers an excessive Type-I error under . Similarly, the LM test statistic

depends on as well and suffers from the same problem. The Wald test statistic

is not asymptotically either because is nonzero-centered due to the incorrect centering of .

2.3 Correcting the Likelihood

Our proposal is to bias-correct the likelihood itself as this benefits the three tests all together. Existing “parameter-based” bias corrections approaches, such as Fernández-Val and Weidner (2016) and Chen et al. (2021), aim at delivering a bias corrected MLE (hence ). These procedures are useful in salvaging the Wald test but not the LR and the LM test. This is simply because , even evaluated at a bias-corrected MLE, is still asymptotically biased. Approaches targeting the bias correction of , such as Li et al. (2003) and Dhaene and Jochmans (2015a), is insufficient for the LR test, because does not deliver an asymptotically unbiased upon differentiation.

In particular, we propose an analytical bias correction procedure that applies directly on to eliminate the bias at the order . Under regularity conditions given in Section 3, we derive bias correction terms, and , analytically and show that

where and depend on . These two terms correct the bias caused by the inclusion of the individual and the time effects, respectively. We construct and by replacing with , and obtain the corrected likelihood

| (2.6) |

The corrected likelihood is free of the IPP in that . We show that, under our regularity conditions, inherits the bias correction in that . This implies an asymptotically unbiased so that test statistics derived from follow their standard asymptotic distribution under the null. Our procedure yields a bias-corrected estimator of as well, denoted by . We show that is asymptotically normal with zero mean in Lemma D.2.

While parameter-based approaches are able to deliver a bias-corrected Wald test, it is worth noting that there is still benefit in considering, for instance, the LR. A crucial prerequisite for the Wald test statistic to be asymptotically is the consistent and efficient estimation of the asymptotic variance. This is not always an easy task with, e.g., many panel time-series models where bandwidth selections are necessary for the estimation of the asymptotic variance; and models whose variance estimator is numerically unstable. In addition, the Wald test is highly sensitive to the formulation of while the LR test is not. Our procedure can be invoked for a bias-corrected LR test when the bias-corrected Wald test is hard to obtain. In fact in calibrating our empirical results, we sometimes find the estimated variance numerically unstable while the LR test statistics behave as expected.

3 Asymptotic Theory

In this section, we present the corrected likelihood function for a general nonlinear model with two-way fixed effects and show that it converges in probability to the infeasible likelihood at a rate faster than . Consequently, the LR, the LM, and the Wald test statistics constructed using this corrected likelihood follow the standard -distribution under a null hypothesis concerning . Let be the compact parameter space of which includes in its interior and has a finite and fixed dimension. We assume the identification of the fixed effects. We use to denote the -norm of a matrix , defined as where is the th element of . In addition, denote the -norm .

Our results are established in three steps. Below in Proposition 1, we give the formula and state the (uniform) rate of convergence for the corrected likelihood . Subsequently in Proposition 2, we state that the profiled score inherits the same rate of convergence from the corrected likelihood, as we have claimed in Section 2. This is crucial for the test statistics to follow their standard asymptotic distribution. Finally in Theorem 1, we formally show that the three classical test statistics all follow -distribution asymptotically when constructed from . For the sake of focus, the asymptotic properties of the corrected estimator is given in Lemma D.2.

The following conditions are imposed to establish the corrected likelihood.

Assumption 1

-

(i) Asymptotic sequence: with for some .

-

(ii) Ergodicity and mixing: let . is ergodic for each and is independent across . Denote and to be the -algebras generated by, respectively, and . is -mixing across with mixing coefficient

as with for some given below in Assumption 1.

-

(iii) Smoothness and boundedness: denote to be a compact -dimensional neighborhood around that contains in its interior. The observation-level likelihood is at least three-time differentiable almost surely (a.s.) w.r.t. for every . There exists a -independent measurable function with for some such that

a.s., where and (with understood as not taking the derivative at all).

-

(iv) Invertible Hessian: , where , is negative definite.

-

(v) Diagonally dominant incidental parameter Hessian:

Assumption 1 states a large- asymptotic framework and is standard in the literature. Assumption 1 requires the data to be ergodic, independent across , and -mixing across . The mixing coefficient is assumed to converge to , as , at a certain rate. This is to ensure that certain autocovariances in our proof are summable. This is also a standard assumption and is seen in, e.g., Fernández-Val and Weidner (2016) and Hahn and Kuersteiner (2011). Note that stationarity is not needed and is violated in two-way models. Assumption 1 enforces that the likelihood function and its derivatives are uniformly bounded so that the differentiation and expectation operators can be interchanged and the uniform law of large numbers applies. While the expansion of the original likelihood only depends on up to the second derivatives, we require the third derivatives to be bounded so that the remainder term of the expansion is also uniformly bounded. This makes our result uniform over . Assumption 1 imposes that the incidental parameter Hessian is invertible and has negative diagonal elements so that our expansion is well-defined. Assumption 1 states that the incidental parameter Hessian is diagonally dominant and is used as a sufficient condition to show (in Lemma B.3)

| (3.1) |

where is but with off-diagonal elements set to . This enables us to establish the corrected likelihood with two simple additive bias correction terms and . When the fixed effects are themselves additive but the sum enters the likelihood in general ways222That is, the linear index takes the form where . Examples are Equations (2.2) and (2.3)., Assumption 1 further reduces to Assumption ′ ‣ 3 below.

Assumption 1′

There exist positive constants and such that for all and ,

The proof of (3.1) under Assumption ′ ‣ 3 is given in the Appendix E. It is worth mentioning that Assumptions 1 and ′ ‣ 3 are essentially sufficient conditions and, when they do not hold, (3.1) can be shown under an alternative but high-level condition. We present the relevant discussion about this in Appendix F.

Proposition 1 (corrected likelihood)

Under Assumption 1, we have, uniformly over :

-

(i)

The original likelihood admits

(3.2) where

and is a matrix of ones.

-

(ii)

The corrected likelihood is

and satisfies

(3.3) where

in which , , , and are , , , and but with replaced by ; and is a truncation matrix with the th element being if and otherwise, for some such that .

Proposition 1 gives the analytical formula for the corrected likelihood and states that ; i.e., is not subject to the IPP. is a cuf-off value imposing that the lag time involved in the autocovariance of the score is no greater than . This technique is commonly used for estimating autocovariances. To select an appropriate value for , we suggest to conduct sensitivity tests across several fixed , following Fernández-Val and Weidner (2016). In addition, for models with strictly exogenous regressors, can be replaced by an identity matrix; i.e., the th element may be set to as soon as .

The formulas of and depend on the expected values of the incidental parameter scores and . These scores are zero at . Therefore, and (respectively in and ) converge to zero and may be dropped when evaluated at or at any consistent estimator of .

For the computation, may be constructed without profiling if and are not of interests. For instance, to obtain or the LR test statistic, can be considered instead, where is the same as but with replaced by a general . This is essentially replacing with and it is valid because is equivalent to . Such a “short-cut” does not require nested optimizations and shall reduce the computational stress considerably.

In the proof of (3.2) of Proposition 1, we utilize two Taylor expansions, with respect to the fixed effects, of and of . The Taylor expansion of () is employed to obtain a representation of . This technique is commonly found in literature (see, e.g., Cox and Snell (1968)). We then use this representation to substitute in the Taylor expansion of . This delivers (3.2) after some additional simplification steps (which mainly depend on Assumption 1). To prove (3.3), we demonstrate that and uniformly over as . Here the convergence relation for involves replacing by the truncation matrix . The validity of such a replacement is guaranteed by Assumption 1.

Next, we establish that converges to at a rate faster than , just like (3.3). Additional assumptions as below are imposed.

Assumption 2

-

(i) Smoothness and boundedness: the log-density is four-time differentiable with respect to every and with partial derivatives

a.s. where given in Assumptions 1 and for and being the th element of .

-

(ii) Invertible Hessian: is negative definite.

Assumption 2 requires the derivatives of the likelihood being uniformly bounded. Assumption 2 ensures that the Hessian of the profiled likelihood is invertible.

Proposition 2 states that the profiled score inherits the same rate of convergence from . In particular, we show from (3.4) that enjoys a limiting normal distribution with mean zero (seeing ). In other words, and are asymptotic equivalent. This is crucial to showing the asymptotic properties of the test statistics and estimators under the maximum likelihood context.

Proposition 2 is not trivial, as this result often appears as a high-level assumption in other works, e.g., Condition 3 of Arellano and Hahn (2016) and Assumption 4.5 of Schumann (2022). We, instead, establish this result using the Landau-Kolmogorov inequality.

Finally, the asymptotic distributions of the test statistics (constructed using ) can be established from Proposition 2. We consider a generic nonlinear null hypothesis where is an vector-valued function independent of the data for some . As in Section 2, we denote to be the Jacobian of . We impose the following assumption.

Assumption 3

-

(i) Identification: for every with , .

-

(ii) Constraint: is continuously differentiable and .

Assumption 3 requires the identification of the true parameter and is standard in the maximum likelihood literature. Assumption 3 is imposed to guarantee that there are no redundant restrictions in . Recall . Let .

In contrast to their -based counterparts, the Wald, the LM, and the LR test statistics given in Theorem 1 are all asymptotically under . Here involved in and may be replaced by for the ease of computations. The validity of this replacement is guaranteed by Slutsky’s theorem, seeing . During the proof we first show the trinity that , , and are asymptotically equivalent to whose formula is given in the proof. is subsequently shown to follow an asymptotic -distribution under using Proposition 2.

4 Simulations

In this section, we present some simulation studies. We consider a panel data set with and . The number of replications is set to . We simulate a logit model with the data generating process (DGP)

| (4.1) | ||||

| (4.2) |

and those without , where is the indicator function; is standard logit; ; ; ; and

for (4.1) and (4.2) respectively. We set . For (4.1), we set , and with and . are generated in the same way as . This setting is similar to Fernández-Val and Weidner (2016). For (4.2), we consider a simpler setting with as as we have experienced some numerical instability with the earlier setting. We present results for the LR test about with the test statistics defined in Theorem 1 and null hypotheses at where (i.e., ranges from to with a step of ). During our experiments, we obtain test statistics using the infeasible likelihood , the original (uncorrected) likelihood , and our corrected likelihood functions . We then calculate and plot the rejection rates at a nominal level of over the replications. Note that for the particular hypotheses tested, the rejection rate at is the empirical size and those at are the empirical powers.

Here is the corrected likelihood defined in Proposition 1 but with and set to . These expectations generally cannot be calculated in real applications. As mentioned next to Proposition 1, however, dropping these two expectations is valid when the corrected likelihood is evaluated at consistent estimators of (including itself). When evaluated at other values of , these two terms should, in principle, be kept. However, for the purpose of our paper, dropping these terms only affects the statistical power of the tests; and most importantly, the effect quickly diminishes as the sample size grows, which we will see in the simulation results below.

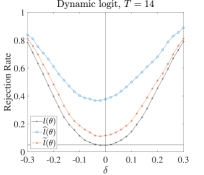

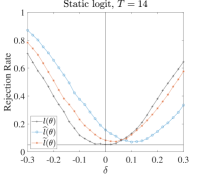

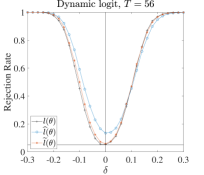

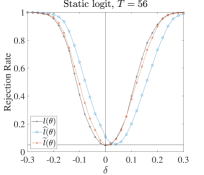

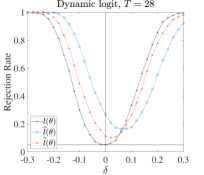

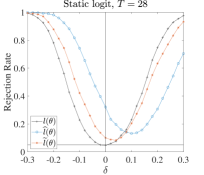

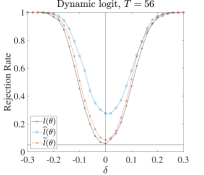

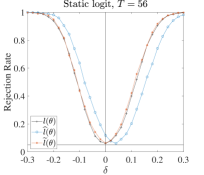

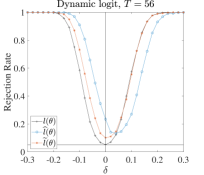

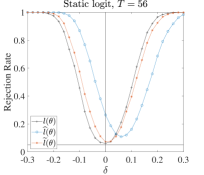

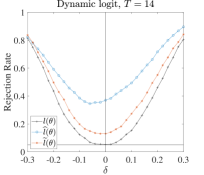

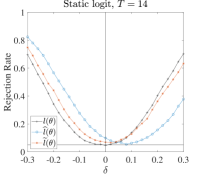

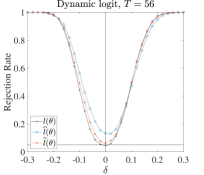

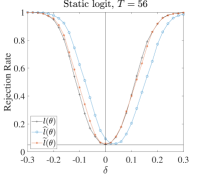

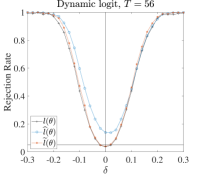

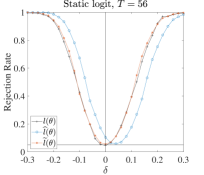

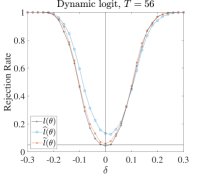

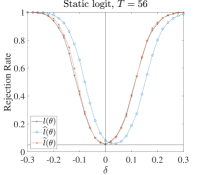

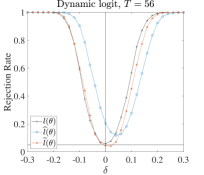

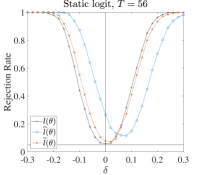

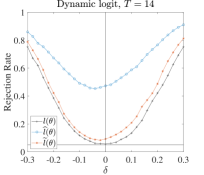

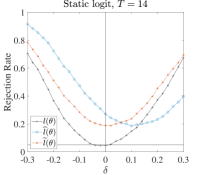

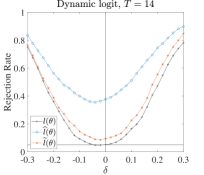

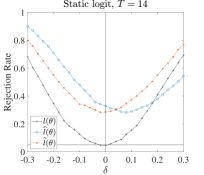

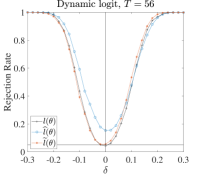

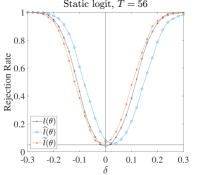

Figure 2 presents the simulation results for the LR tests on (4.1). The horizontal line is at and the vertical at . For dynamic models with , the LR test using severely over-rejects the true at with a size of roughly whereas that using is significantly improved, having a size of roughly . It is expected that the size using is still away from for . When is small, and , which are dropped in are not yet close to . However, as soon as , already delivers a size reasonably close to whereas still gives a size of roughly . As increases to , the size of the LR test using is effectively and the power is very close to that using whereas the LR test based on still over-rejects with a size at above . Similar patterns are observed for static models or for (4.2) presented in Figure G.1.

We put more results in Appendix G for other models/specifications and for the LM and The Wald test. The patterns are generally similar except that the results for probit models are slightly worse than its logit counterpart for certain tests. The results on bias corrections of the estimator is also put in Appendix G.

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static , where the true value for the dynamic model and for the static model respectively, is standard-logistically distributed, with , and . and are generated in the same way as . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, is standard-logistically distributed, , and . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

5 Empirical Illustration: Single Mother Labor Force Participation

In this section we apply our likelihood-based bias correction method to examining the determinants of the labor force participation (LFP) decision of single mothers. In particular, we look at the impact of the number of children on the decision of the mother to engage in paid employment.

An extensive literature in labor economics has studied the labor supply decisions of married women (Killingsworth and Heckman, 1986; Angrist and Evans, 1998; Blau and Kahn, 2007; Eckstein and Lifshitz, 2011). These studies have uncovered the impacts of a variety of economic variables, including female market wage and husband income (Mincer, 1962), education (Heath and Jayachandran, 2016), childcare costs (Connelly, 1992), the cost of home technology (Greenwood et al., 2016), and culture norms (Fernandez, 2013). Among these variables, the number of children consistently emerges as one of the most important determinants of female labor supply (Nakamura and Nakamura, 1992). This is unsurprising since women continue to bear a disproportionate share of child-rearing responsibilities (Aguero and Marks, 2008).

In contrast to the substantial body of research on the labor supply behavior of married women, the labor supply decisions of single mothers have received relatively limited attention, with only a few exceptions (Kimmel, 1998; Blundell et al., 2016). Single mothers, however, face distinctive challenges when it comes to balancing work and child-rearing responsibilities due to the absence of a second earner in the household. Moreover, their employment decisions may have a more pronounced impact on their children’s well-being compared to the decisions of married women and should thus be of great importance to economists and policymakers.

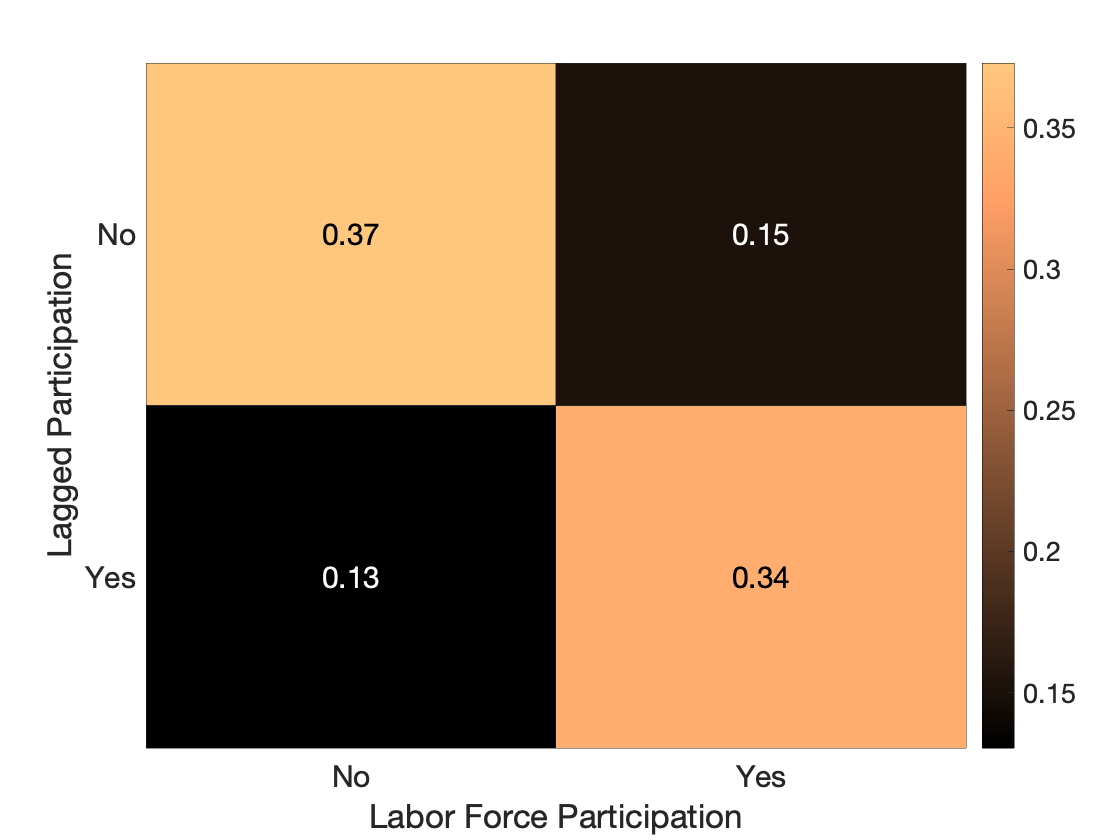

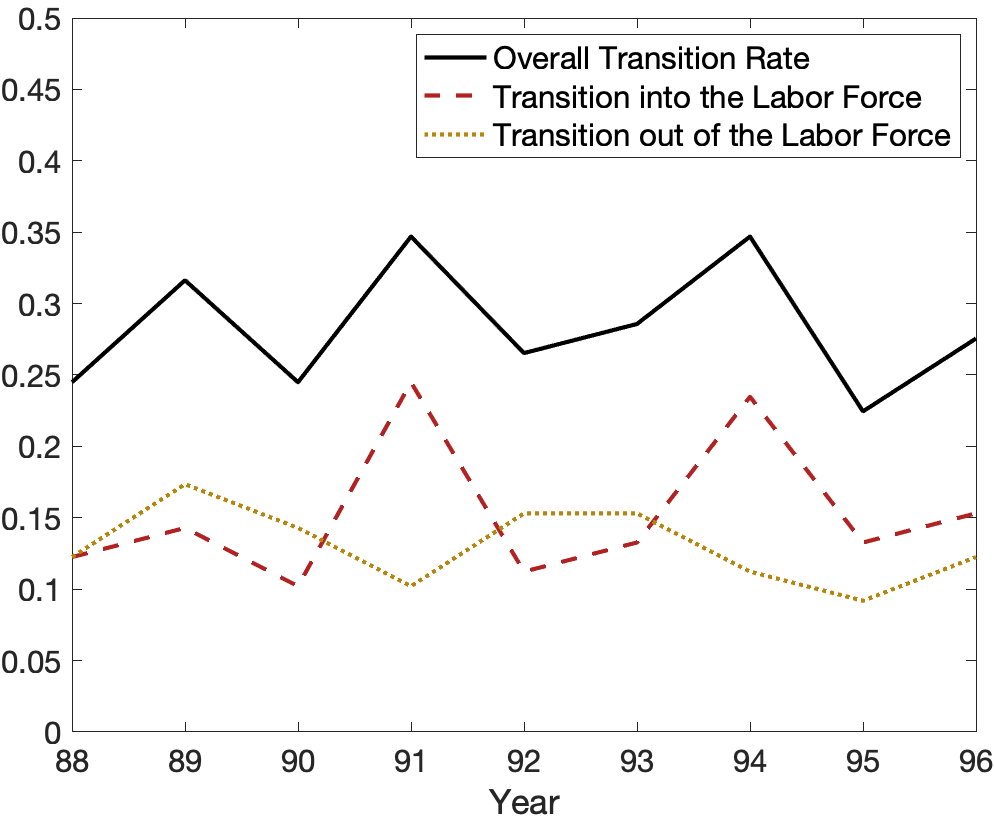

To study the labor supply decisions of single mothers, we compile a data set using waves of the Panel Study of Income Dynamics (PSID), which span the years of 1987 to 1996. The data set consists exclusively of single mothers, whom we define as unmarried female household heads with at least one child. Our dependent variable is labor force participation status, which we define as whether the individual has worked nonzero hours during the interview year. Our set of explanatory variables includes the number of children, which is our main treatment variable of interest, alongside age dummies. Following Dhaene and Jochmans (2015b), we restrict our sample to individuals between the age of 18 and 60 whose LFP status changed at least once during the sample period. The final sample consists of individuals whose labor supply status are continuously observed over a period of years from 1988 to 1996. See the Appendix H for more details. On average, 28 percent of these individuals switched in and out of the labor force in each year (Figure H.1H.2). Table H.2 gives the summary statistics.

Let indicate the labor force participation status of individual in time . Let denote her number of children, and let be the set of age dummies. We estimate the following two probit regressions:

| (5.1) | ||||

| (5.2) |

where is an indicator function, and . In model (5.1), we focus on estimating the average treatment effect of the number of children on mother’s labor supply while controlling for unobserved heterogeneity through the inclusion of two-way fixed effects in the intercept. In model (5.2), we focus on estimating the heterogeneity in the elasticity of labor supply with respect to the number of children. This is accomplished by incorporating two-way fixed effects into the slope coefficient.333We only include and on the slope coefficient because our method currently works for scalar fixed effects.

Given the “small N, small T” characteristics of our sample, direct estimation of (5.1) and (5.2) could lead to severe incidental parameter problems. Therefore, we apply our bias correction procedure to the estimation. Table 5 presents our results on Model (5.1). Let . The first two columns of the table shows the MLE () and the bias-corrected estimate (), along with standard errors computed from the Hessian matrix of their respective uncorrected and corrected profile likelihood. Looking at , we find a large and positive correlation between past and current labor force participation, indicating the existence of substantial costs for single mothers to transit in and out of the labor force. We also find that the number of children positively influences a mother’s labor supply. The presence of an additional child increases a mother’s LFP zscore by 0.239, which, on average, translates into a 9 percent higher likelihood of working.444The marginal effect is computed on an individual who has median fixed effects, is young (age ), was not working last period (lagged participation ), and has a median number of children (# Children ). The coefficients associated with age groups are not statistically significant. Since we follow the same group of individuals over time, the effect of age is largely absorbed into . Comparing with , we see that the MLE under-estimates the importance of state dependence while slightly over-estimating the impact of the number of children. Bias correction leads to a 40 percent greater estimate of the former and a 6 percent lower estimate of the latter. Columns of Table 5 report the Wald, the LM and the LR test statistics for the null hypothesis of , obtained using respectively the uncorrected and the corrected likelihood. The three tests unanimously reject and . For all parameters, bias correction results in larger statistics across all three tests. The magnitude of adjustment is particularly pronounced for lagged participation, where the test statistics more than double when computed using the corrected likelihood.

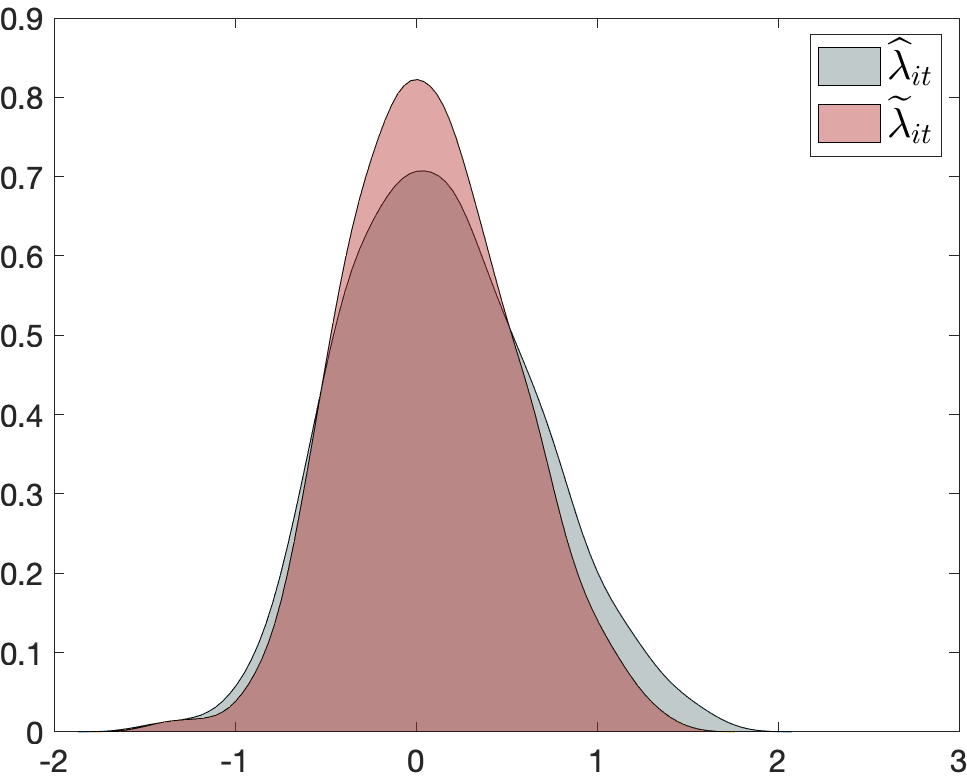

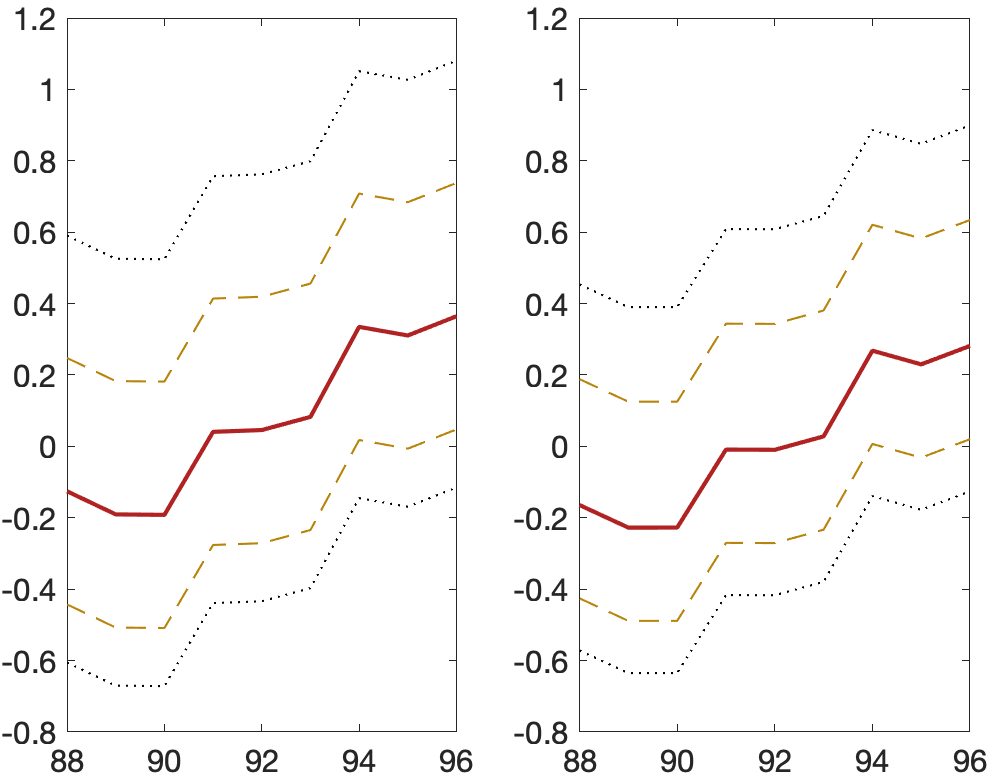

Table H.2 reports the estimation results on Model (5.2). Although not directly comparable with those of Model (5.1), these estimates reveal substantial variability in how the number of children affects a mother’s LFP. Let and let be its bias-corrected counterpart. In Figure 4a, we plot the distributions of and . Table H.2 reports their summary statistics. Notably, bias correction leads to a less skewed and less varied distribution, but significant heterogeneity remains after correction. In Figure 4b, we illustrate the evolution of the estimated effects over time. Looking at , we see that in 1987, for more than half of the population, having more children is associated with a lower likelihood of labor force participation. Over time, however, there is a clear trend of increasingly positive labor supply response to having a larger number of children.

Why are single mothers on average more likely to work when they have more children? And why does this effect vary among different people over time? To delve deeper into this topic, we investigate the relationship between a mother’s labor force participation and the number of children within specific age groups. Following the approach of Dhaene and Jochmans (2015b), we categorize children into three groups: those aged 0 to 2, 3 to 5, and 6 to 17. This enables us to independently assess the impact of having more infants, preschool-age children, and school-age children on the labor supply of mothers. We proceed by re-estimating Model (5.1), with the number of children in each group as a key variable of interest.

Table 5 reports our estimation results. Looking at , we find that the effects of having more infants or preschool children are statistically insignificant. The Wald, LM, and LR tests all fail to reject the null hypothesis of their coefficients being zero. On the other hand, the effect of having more school-age children is positive and highly statistically significant according to all three tests. This suggests that the overall positive impact of having more children on a mother’s labor supply that we observe in Model (5.1) may be primarily driven by the number of school-age children. This isn’t surprising, considering that single mothers, unlike their married counterparts who may share financial responsibilities with their spouses, often need to work to support their children’s education. These findings could also help explain the increasing trend that we observe in Model (5.2) in the heterogeneous effects of the number of children over time. Since we follow the same group of women, as their children grew up and entered school in the later years of our sample, more of them would have to enter the labor force to support their children.

Additionally, we conduct two further tests to explore specific hypotheses: (1) whether the number of infants and preschool children have the same impact on a mother’s LFP, and (2) whether the effect of the number of children on a mother’s LFP is the same regardless of children’s ages. The final two rows of Table 5 provide the test results. Both hypotheses are rejected by all three tests at the 5 percent level. This is a curious result for hypothesis (1) since neither nor is significant on their own. In both cases, all three test statistics become larger after bias-correction. All in all, the evidence suggests that the number of children at different stages of childhood will have different impact on their mother’s labor supply.

In summary, our analysis demonstrates the applicability of our likelihood-based bias correction method to analyze data with small and small . We find that on average, an increase in the number of children corresponds to a higher likelihood of a single mother’s employment. However, these relationships exhibit heterogeneity across individuals and over time, with the impact primarily driven by the presence of school-age children, whom single mothers often need to support through education. Other findings including the importance of state dependence are consistent with literature.

[c]

Estimation results: Model (5.1)

| Lagged Participation | ||||||||

|---|---|---|---|---|---|---|---|---|

| # Children | ||||||||

| Age 30-44 | ||||||||

| Age 45-60 | ||||||||

-

•

Notes: Standard errors in parentheses. The Wald, the LM and the LR statistics have limiting chi-squared distributions under , with critical values given by .

[c]

Estimation results: Model (5.1) with the number of children by age groups

| Wald | Wald | LM | LM | LR | LR | |||

|---|---|---|---|---|---|---|---|---|

| Lagged participation () | ||||||||

| # Children 0-2 () | ||||||||

| # Children 3-5 () | ||||||||

| # Children 6-17 () | ||||||||

| Age 30-44 () | ||||||||

| Age 45-60 () | ||||||||

-

•

Notes: Standard errors in parentheses. The Wald, the LM and the LR statistics have limiting chi-squared distributions under , with critical values given by for the first 7 hypothesis tests and by for the last hypothesis test.

6 Conclusion

Nonlinear models with two-way fixed effects are subject to the incidental parameter problem, resulting in many test statistics failing to follow their standard asymptotic distribution under the null hypothesis. As a consequence, the sizes of these tests may depart severely from the nominal level. The purpose of this paper is to introduce an approach to bias-correct the likelihood function. The approach yields a corrected likelihood function that serves as an alternative to the original (uncorrected) likelihood for constructing hypothesis testing procedures. In particular, we prove that the three commonly used hypothesis testing procedures, the likelihood-ratio, the Lagrange-multiplier, and the Wald test, all have test statistics that follow the correct asymptotic distributions when derived from the corrected likelihood. This is not the case when they are derived from the original likelihood which is subject to the incidental parameter problem. Simulation studies and empirical analysis are further carried out to demonstrate the performance of our bias correction procedures.

The proposed approach is more general than many existing procedures. Specifically, our corrected likelihood applies to dynamic nonlinear models with two-way fixed effects and is able to revert the asymptotic distributions of test statistics from many testing procedures, whereas existing approaches mostly focus on static models or on bias-correcting the estimators, which do not benefit all testing procedures.

Acknowledgement

We would like to express our gratitude to valuable comments and suggestions from Geert Dhaene, Whitney Newey, Jun Yu, participants of various conferences and seminars. We would also like to thank our research assistant Yuchi Liu for helping us with the empirical work. This work is supported by the National Natural Science Foundation of China under Grant Number 72203032.

Appendix

AppendixAppendix

A Panel Autoregressive Model with Two-way Effects

Example A.1

Consider an autoregressive

| (A.1) |

where and are i.i.d. . The initial value is . We assume the variance of known so that the observation-level likelihood of is

where are parameters for the individual and fixed effect, respectively; and is the structural parameter. We impose for the identification and consider for simplicity. Let . We have the MLEs

and it can be shown that, seeing (where the expectation is conditional on the initial value ),

Let the original and the infeasible likelihood be, respectively,

is subject to the IPP. In particular,

| (A.2) |

and it converges to a nonzero constant as with . Given the cross-sectional independence, the first term on the right-hand side of (A.2),

converges to a nonzero constant, assuming the autocovariances of summable. The second term of (A.2) does so as well from the standard asymptotic theory for MLEs. Since converges to a nonzero constant, contains a bias in its asymptotic distribution.

The IPP of affects its score. We have

| (A.3) |

The first two term of (A.3) converges to a nonzero constant using the same arguments above; whereas the last term converges to zero. Therefore, converges to a nonzero constant, inducing a bias in the asymptotic distribution of .

B Proof of Proposition 1

B.1 Lemmas

We first introduce some Lemmas that are used during the proof. The lemma below is based on Proposition 2.5 of Fan and Yao (2003). It shows that the covariance of two measurable functions on alpha-mixing data is summable.

Lemma B.1 (summable covariances under alpha mixing)

Proof. Applying Proposition 2.5 of Fan and Yao (2003) with and using the fact that is alpha mixing with the same mixing coefficient, we obtain

Equation (B.1) follows directly from here by observing as in Assumption 1 and Equation (B.2) follows by observing that is a summable series in .

The next lemma states the rates of convergence of several likelihood derivatives.

Lemma B.2 (order of derivatives)

Proof. Under standard maximum likelihood asymptotic theory and Assumption 1, the last three can be shown trivially. The uniform property is a result of the assumption that the likelihood derivatives are uniformly bounded. Therefore, we focus on here. The key of showing this result is Lemma B.1. We start by observing that can be partitioned into

where and all blocks are discussed below. All statements below are uniformly over .

: Under cross-sectional independence, is a diagonal matrix with elements

| (B.3) |

By Assumption 1, the first term on the right-hand side of (B.3) is

uniformly over Observing , the second term on the right-hand side of (B.3) can be rewritten as

where, by invoking Lemma B.1, we have uniformly over so that

The above leads to for all so that

: Since the data are serially correlated, is not a diagonal matrix. Instead, is a matrix with the th element being and the sum of absolute values of elements on the th row being

| (B.4) |

The first term on the right-hand side of (B.4) rewrites,

where because of the cross-sectional independence and

because uniformly over by Lemma B.1. The second term on the right-hand side of (B.4) rewrites,

because . These lead to for all so that

: Next, is an matrix with th element being

| (B.5) |

Here, the first term on the right-hand side of (B.5) contains

by cross-sectional independence and by the definition of score. The second term on the right-hand side of (B.5) contains

where, by Lemma B.1, and, by the definition of score, . These lead to for all so that

Since we have now identified the order of each block of , it follows directly that

where

The conclusion follows from here by seeing with .

The next lemma states that the matrix of the off-diagonal elements of is of a smaller order than that of the diagonal elements, in terms of the -norm denoted by which is defined as for a matrix having the th element with and . Using this lemma, the off-diagonal elements can be dropped during the proof.

Lemma B.3 (order of inverse Hessian)

Proof. For simplicity, we omit the argument during the proof. We begin by noticing

where and . Here, and are diagonal matrices so that

by the definition of . Similarly, is an matrix of elements with so that

Denoting , we have

by a block inversion of where

By Assumption 1,

Define

Then, and Noting that by the above, we set where and obtain that

Analogously, Thus,

Using the above and properties of , it follows that

and

Thus, by the definition of , we have , leading to the conclusion.

B.2 Proof for expansion of likelihood (Equation 3.2)

The proof is based on the combination of asymptotic expansions of the likelihood and the score. In particular, since , a Taylor expansion of around would give

leading to

| (B.6) |

This expansion is similar to, e.g., Cox and Snell (1968) and is rather standard. Here the terms are uniform over because the third derivative of the likelihood is uniformly bounded and has a finite asymptotic variance (under the standard maximum likelihood asymptotic theory). Next, Taylor-expanding around gives

| (B.7) |

where the remainder term is actually but we write to be consistent to what is presented in Proposition 1. In addition, by a similar argument as above, the remainder is also uniform here. Next, plugging (B.6) into (B.7),

where . Noting that the second term on the right-hand side is a quadratic form in and that , we calculate expectations term by term to obtain

where denotes the trace of a matrix .

The above is an early version of Proposition 1 and it can be simplified. In particular, by Lemmas B.3 and B.2, we have

and

so that

with . Using this, we arrive at

| (B.8) |

where the remainder is uniform over . The numerators can be further simplified. In particular, seeing ,

Using this, the second term on the right-hand side of (B.8) becomes . Similarly seeing ,

where the last equality is because of the cross-sectional independence (so that the second term on its left-hand side is ). Using this, the third term on the right hand-side of (B.8) becomes . Equation (3.2) follows from here.

B.3 Proof for corrected likelihood (Equation 3.3)

Given the construction of , the proof of Equation 3.3 boils down to showing and under . First, uniformly over the denominator of each ratio involves the incidental parameter Hessian evaluated at which is consistent for its infeasible counterpart evaluated at Then according to the continuous mapping theorem for convergence in probability, we only need to show that the numerators are also consistent uniformly over

For , we show

uniformly over . Recall . Omitting the arguments and for simplicity,

| (B.9) |

It shall be easy to see that the first term on the right-hand side of (B.9) is . In addition, by invoking Lemma B.1, we also find that the second and third terms on the right-hand side of (B.9) are as ; and, as , the last term on the right-hand side of (B.9),

for some positive constant and defined in Assumption 1 with . The above leads to .

For , an invocation of the dominated convergence theorem gives

which leads to directly.

C Proof of Proposition 2

C.1 Lemmas

The following Lemma establishes the order of and is needed for the proof of Proposition 2.

Proof. The proof is similar to the proof of Proposition 1. First, since the dimension of is fixed, showing this lemma is equivalent to showing

| (C.1) |

where and denotes, respectively the th and th element of . Let

Showing Equation (C.1) boils down to showing .

To prove this, we consider the mean-value expansion

where , which is immediate; , which is the same as in Lemma B.2; and with being a point on the segment connecting and . Calculating the expectation,

First, using (B.6) and noticing , we have

where , which is the covariance matrix of and since . Now, it shall be clear that has a similar structure as . Therefore, it can be verified, using the same technique as in Lemma B.2, that . Using the same strategy in the proof of Proposition 1, we can immediately conclude that

leading to

| (C.2) |

Second,

where and denote the minimum and maximum eigenvalues of the symmetric matrix . Using and , we immediately have

| (C.3) |

C.2 Proof of Proposition 2

Under our assumption of boundedness, the differentiation and expectation can be interchanged. Therefore, denoting ,

Next, invoking the Landau-Kolmogorov inequality, we have

for some positive constant . Here by (3.3) of Proposition 1; and

where the final order is because of Lemma C.1 together with the fact that and which can be verified by a similar argument as the proof of (3.3) of Proposition 1. The conclusion follows naturally from here.

D Proof of Theorem 1

D.1 Lemmas

The following Lemma states that uniformly. This result is used during the proofs of Lemma D.2 and Theorem 1. Note, this lemma follows from Proposition 2 quite easily and does not depend on Assumption 3 at all.

Proof. Using Proposition 1, we have

where and . Here, by similar arguments as in the proof of (3.3) in Proposition 1, and uniformly over and respectively. Therefore, by the law of large numbers,

leading to

| (D.1) |

where the last equality can be shown by a uniform linear approximation near . Now,

Using Proposition 2 and seeing that the remainder term of (D.1) is uniform in , the proof concludes here.

The following lemma establishes the consistency and asymptotic normality of .

Lemma D.2 (asymptotic properties of )

Proof. We first show the consistency of . The key point here is that converges uniformly to since does and the correction terms and are uniformly bounded. In particular, uniformly in , so that

for every . Also, since is the unique maximizer of , for small. Combining these three,

| (D.2) |

with probability approaching . Notice that is continuous in since is so. Next, denote

for given . Here, since is compact and is open, is compact. This, together with the continuity of , indicates that there exists a such that . On the other hand, is the global maximizer of over by assumption, we may conclude that

For every small enough , we have with probability approaching by (D.2), so that

with probability approaching . Now, since is the maximizer of over , this implies , and thus

as .

For the asymptotic normality, standard technique applies. Consider a mean value expansion of around , i.e.,

where is a point on the segment connecting and . By Lemma D.1, we can immediately see

| (D.3) |

where the last equality is because of with invertible . From here, the conclusion follows that

with the asymptotic covariance matrix

where

provided that the cross-section is independent. The proof concludes here.

The next lemma presents the limiting random variable of . This result is used to establish the asymptotic distributions of and which are written in terms of .

Lemma D.3 (Asymptotic representation about )

Proof. We consider the constrained maximization problem

where is the Lagrangian multiplier. The constrained maximization problem has the first-order conditions

| (D.4) | ||||

| (D.5) |

Because is an asymptotically normal estimator under the null hypothesis, following from a similar proof as in Lemma D.2. Moreover, as implied by (D.4) seeing and is of full row rank. Now, We mean-value expand around to obtain

| (D.6) |

where is a point on the segment connecting and ; and the last equality is because of . Seeing and , A combination of (D.4) and (D.6) yields

| (D.7) |

Similarly for Equation (D.5),

| (D.8) |

where the last equality is because of . Now, Equations (D.7) and (D.8) represent the system of linear equations

| (D.9) |

which has the solution

Invoking Lemma D.1,

| (D.10) |

The conclusion follows by subtracting (D.3) in Lemma D.2 from (D.10).

D.2 Proof of Theorem 1

Since , , and are constructed in the context of maximum likelihood, we make use of the information matrix equality here; i.e., let in Lemma D.2 reduce to . Our proof strategy is to first show

where

Then we show . We take the consistency of given, since the proof is analogous to that of under .

We start from showing . In particular, a mean value expansion of around gives

where is between and . Since and , we immediately have

where the last equality is by invoking Lemma D.3 seeing that is consistent for . Similarly for , we have

where is between and (not necessarily the same as for ). It follows from the same argument that

For , a mean-value expansion of gives

where is between and . By Lemma D.3, seeing that is consistent for and that by definition, we have

Next, for , we have so that the delta method gives

We therefore conclude that . The degree of freedom is because the dimension of is in fact .

E Proof for Lemma B.3 under Assumption ′ ‣ 3

In this section, we provide the proof for Lemma B.3 under Assumption ′ ‣ 3. We consider models with linear index where . This specification covers many commonly used models such as

We equivalently consider the Lagrangian likelihood

where are Lagrange multipliers, and is some constant from the identification condition. Define and then where

Lemma E.1

Proof. By definition, and It then follows from Woodbury identity that

Define and

Then, where is the matrix with elements Therefore,

Assumption ′ ‣ 3 states that and which implies that

for large enough and Because from the symmetries present in the models under consideration, we conclude that

Analogously,

Lemma E.2

Proof. Following from Lemma S.1 in Fernández-Val and Weidner (2016), it suffices to show (E.1) for some Then (E.1) holds for all We choose so that Lemma E.1 applies for large enough and Notice that

and by the block matrix inversion

with

Furthermore, Let The Woodbury identity states that

and hence

By Assumption ′ ‣ 3, and This shows that

Analogously, and Define

Then, and Noting that by Lemma E.1, we obtain that

where Analogously, Thus,

It follows that

analogously, , and

This shows the desired result.

Proof of Lemma B.3 under Assumption ′ ‣ 3. Given that since

where refers to the Moore-Penrose pseudo-inverse. We then have and thus

F Further discussion on incidental parameter Hessian

Assumption 1′′

There exist positive constants and such that for all and ,suppose

Assumption ′′ ‣ F can be used to show Lemma B.3. The proof itself is straightforward and, hence, omitted. In addition, we would like to emphasize that i) we numerically verify in Appendix F.1 that all models involved in the simulation satisfy Assumption ′′ ‣ F at least for some ; and that ii) none of Assumptions 1, ′ ‣ 3, and ′′ ‣ F are crucial, in the sense that, without them, the corrected likelihood has a slightly more complicated expression which we give in Appendix F.2.

F.1 Numerical examination

In this appendix, we present a brief numerical examination of Assumption 1 for the models involved in our simulation. We suppress the dependency on whenever possible in this appendix for simplicity. The purpose is to investigate if and are, respectively, - and -invariant, where

We use exactly the same simulation designs as in Section 4 except the following. For each model, we consider two sequences of : i), with (with the increment being ); and ii), with . (We have tried but have decided to abandon because we would run into an insufficient memory problem.) Under i), we generate a data set and calculate for each ; and under ii), we do the same to obtain for each . Note that, for each (and ), (and ) is calculated on a single simulated data set. In addition, the expectations involved in and are calculated using analytical formulas. For instance, a probit model with the observation-level likelihood

has the expected likelihood

where and is the linear index as in Example 1. can easily be calculated analytically and the derivatives can be calculated from .

To investigate the -invariance of , we then calculate the first difference and regress on (a vector of of length where is the cardinality of ). Finally, we seek to verify if the coefficient for is statistically insignificant. The intuition is the following. If or, equivalently, is -invariant, then first-differencing will remove all the -invariant components in it so that the mean would be . We repeat this experiment for with . The -invariance of is verified in the same way. Table F.1 presents the results of this experiments. In short, we find that in all designs, the means of and are all very close to zero and the -tests with or all accept the null hypothesis. From this point, we conclude that Assumption 1 seems satisfied on the models involved in our simulation.

[c]

Estimated means and associated -value of and

| Probit | Logit | ||||||||||||

| Dynamic | Static | Dynamic | Static | ||||||||||

| Est. | Sig. | Est. | Sig. | Est. | Sig. | Est. | Sig. | ||||||

-

•

Notes: The estimated means for with , , , and ; and for with , , , and . Est. is the estimated mean and Sig. is the -value of a -test of or . The model is with for dynamic model and for static model, where is given in the table. The true value is for the dynamic model and for the static model, is standard-normally distributed for the probit model and standard-logistically distributed for the logit model. , and with and . and are generated in the same way as .

F.2 Corrected likelihood without Assumptions 1, ′ ‣ 3, and ′′ ‣ F

Below we provide an alternative form of Proposition 1 without Assumption ′′ ‣ F. As argued above, the corrected likelihood would have a slightly more complicated form where the bias correction term is expressed as a matrix trace instead of two additive terms .

Proposition F.1 (alternative corrected likelihood)

-

(i)

The likelihood admits

(F.1) with, as in Lemma B.2,

where denotes a matrix with th element being for and .

-

(ii)

The corrected likelihood satisfies

(F.2) where

where is but with replaced with and is a column vector of .

Proof. It shall be clear from the proof of Proposition 1 that Equation (F.1) is an intermediate result of (3.2) in Proposition 1. Therefore, we omit the proof of (F.1) and focus on Equation (F.2) here.

In fact, the proof of Equation (F.2) is rather straightforward. Observing under our setting, we only need to show . For and , by the same argument as in the proof of (3.2) in Proposition 1,

From here, repeating the same technique in the proof of (3.3) in Proposition 1,

For , repeating the same argument as in the proof of Lemma B.2,

It is also immediate from here that .

G Extra simulation results

G.1 Extra results for the LR test

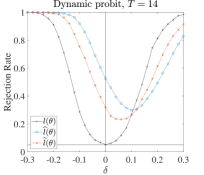

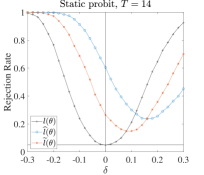

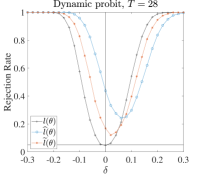

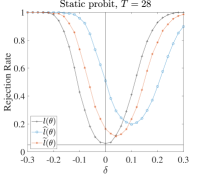

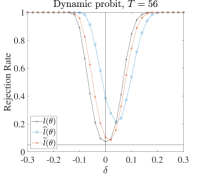

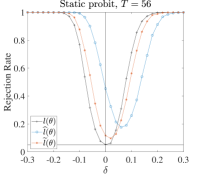

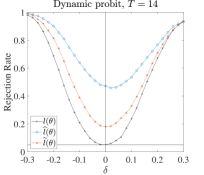

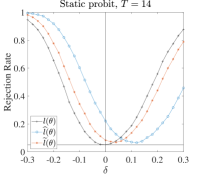

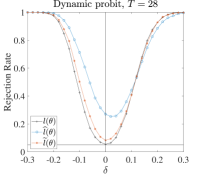

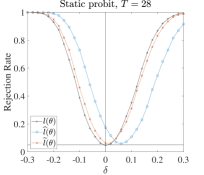

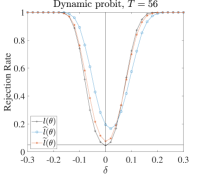

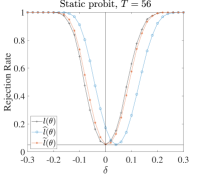

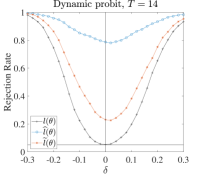

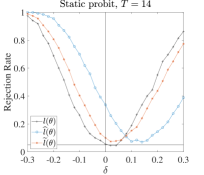

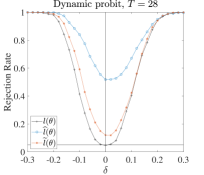

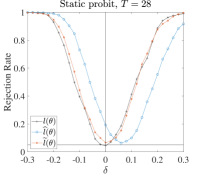

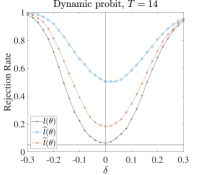

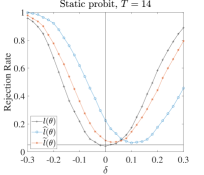

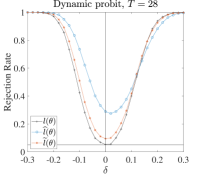

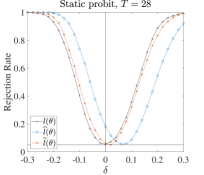

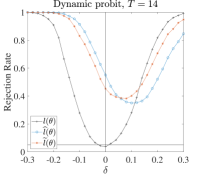

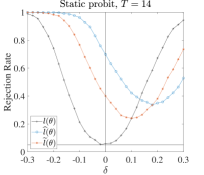

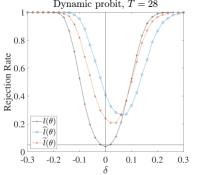

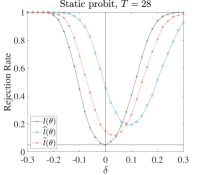

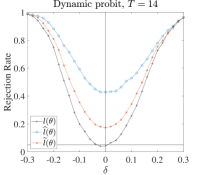

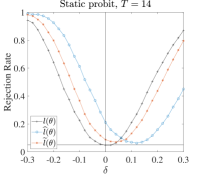

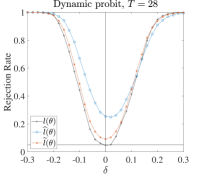

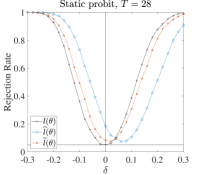

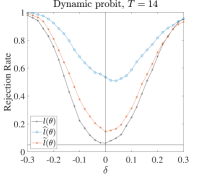

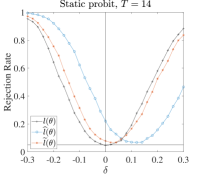

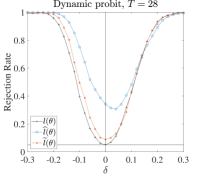

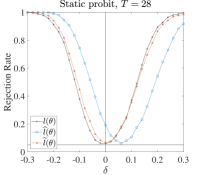

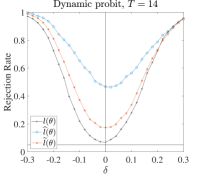

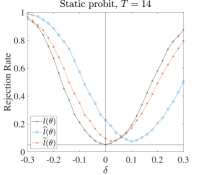

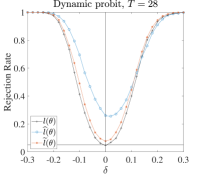

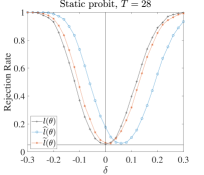

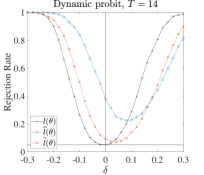

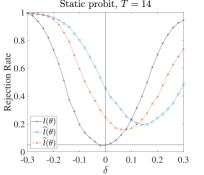

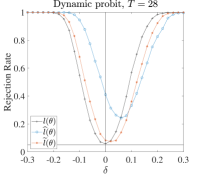

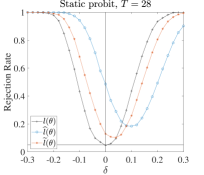

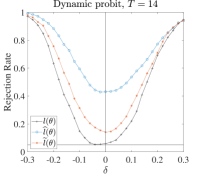

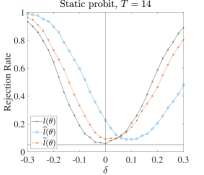

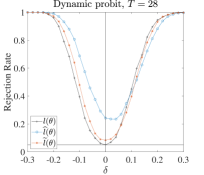

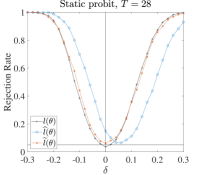

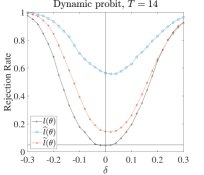

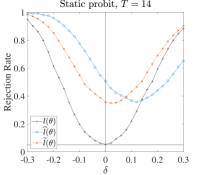

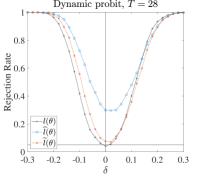

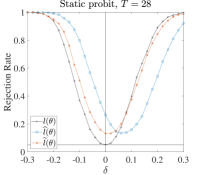

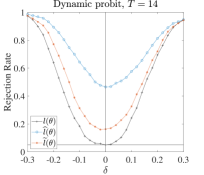

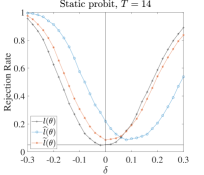

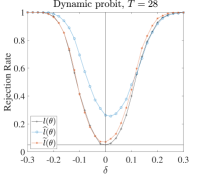

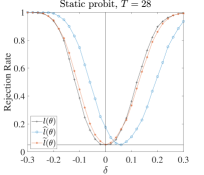

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, , , and . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, , with , and . and are generated in the same way as . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model,, , and with and . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, , , and with and . is generated in the same way as . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LR tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . is generated in the same way as . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

G.2 Extra results for the LM test

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, , , and . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, is standard-logistically distributed, , and . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static , where the true value for the dynamic model and for the static model respectively, , with , and . and are generated in the same way as . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static , where the true value for the dynamic model and for the static model respectively, is standard-logistically distributed, with , and . and are generated in the same way as . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, , , and with and . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, , , and with and . is generated in the same way as . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the LM tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . is generated in the same way as . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

G.3 Extra results for the Wald test

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, , , and . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, is standard-logistically distributed, , and . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static , where the true value for the dynamic model and for the static model respectively, , with , and . and are generated in the same way as . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. The dynamic model is with and the static , where the true value for the dynamic model and for the static model respectively, is standard-logistically distributed, with , and . and are generated in the same way as . . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model,, , and with and . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model,, , and with and . is generated in the same way as . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

Notes: The plotted curves are the rejection rates of the Wald tests based on (+), (o), and (*) calculated over replications. . The model is for the dynamic model with and for the static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . is generated in the same way as . The null is at where, as depicted on the horizontal axis, . The vertical line is at the true value and the horizontal at the significance level .

G.4 Bias correction on estimators

[c]

Bias-corrected probit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. and are the uncorrected estimators of and respectively; and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The model is for dynamic model with and for static model where the true value for the dynamic model and for the static model, is standard-normally distributed, , and with and .

[c]

Bias-corrected logit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. and are the uncorrected estimators of and respectively; and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The model is for dynamic model with and for static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and .

[c]

Bias-corrected probit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. and are the uncorrected estimators of and respectively; and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The model is for dynamic model with and for static model where the true value for the dynamic model and for the static model, is standard-normally distributed, , and with and . is generated in the same way as .

[c]

Bias-corrected logit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. and are the uncorrected estimators of and respectively; and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The model is for dynamic model with and for static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . is generated in the same way as .

[c]

Bias-corrected probit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. and are the uncorrected estimators of and respectively; and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The model is for dynamic model with and for static model where the true value for the dynamic model and for the static model, is standard-normally distributed, , and with and . and are generated in the same way as .

[c]

Bias-corrected logit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. and are the uncorrected estimators of and respectively; and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The model is for dynamic model with and for static model where the true value for the dynamic model and for the static model, is standard-logistically distributed, , and with and . and are generated in the same way as .

[c]

Bias-corrected probit estimates with ,

| Mean | Bias | RMSE | Mean | Bias | RMSE | Mean | Bias | RMSE | ||||

| Dynamic model | ||||||||||||

| Static model | ||||||||||||

-

•

Notes: The number of replications is . Mean is the monte-carlo mean of the estimates. Bias is the percentage bias of the estimates relatively to the true value. RMSE is the root mean squared error. , , and are the uncorrected estimators of , , and respectively; , , and are the bias-corrected estimators using (without and ) and setting the truncation parameter at (for dynamic model only). . The dynamic model is with and the static model , where the true value for the dynamic model and for the static model respectively, , , and .

[c]

Bias-corrected logit estimates with ,