On the properties of Gaussian Copula Mixture Models ††thanks: Citation: Ke Wan, Alain Kornhauser, On the properties of Gaussian Copula Mixture Models

Abstract

This paper investigates Gaussian copula mixture models (GCMM), which are an extension of Gaussian mixture models (GMM) that incorporate copula concepts. The paper presents the mathematical definition of GCMM and explores the properties of its likelihood function. Additionally, the paper proposes extended Expectation Maximum algorithms to estimate parameters for the mixture of copulas. The marginal distributions corresponding to each component are estimated separately using non parametric statistical methods. In the experiment, GCMM demonstrates improved goodness-of-fitting compared to GMM when using the same number of clusters. Furthermore, GCMM has the ability to leverage un-synchronized data across dimensions for more comprehensive data analysis.

Keywords Gaussian Mixture, Copula, Model Clustering, Gaussian Processes, Machine Learning, Other Algorithms and Architectures, Kernels

1 Introduction

Gaussian Mixture models have been employed in various areas of research (Yang 1998 [13] and Pekka 2006 [8]). In the present study, we extend Gaussian Mixture Models into Gaussian Copula Mixture Models to address the following two concerns:

-

•

Heavy-tailed data require increasing numbers of clusters to fit with GMMs. To control number of clusters, heavy tails on marginal distributions should not lead to significantly greater clusters given the same underlying dependence structure.

-

•

GMMs are usually applied to a synchronized data matrix of dimension and number of observations . In many problems, there are numerous unsynchronized data each dimension, the number of which is denoted as for the -th dimension. Such data should be utilized to update the joint distribution shared by the different dimensions.

To address the concerns, we introduced copulas into mixture models and new Expectation Maximum type algorithms are developed to estimate their parameters.

2 Related Studies

Gaussian mixture models have been used widely in various applications and the Expectation Maximum algorithm has been utilized for estimating their parameters. The convergence properties of such Expectation Maximum algorithms have been discussed in Lei (1996 [12]). However, each component of a GMM is a multivariate gaussian distribution that cannot effectively capture heavy tails and the number of components become sensitive w.r.t heavy tails. The introduction of more flexible components may help to further reduce number of components when working with heavy-tailed data.

On the other hand, copulas have been used in research for model dependence. The definition of a copula in the two dimensional case is given as below:

Let be a conditional bivariate distribution function with continuous margins and , and let be some conditioning set. There then exists a unique conditional copula such that (Sklar (1959) [9]):

| (1) |

The definitions above can easily be generalized to higher dimensions. The advantages of the copula method include the following:

-

•

Heavy-tailed joint distributions can be modeled;

-

•

Marginal distributions and their dependence structure can be studied separately;

-

•

Copulas can be calibrated to data sets that are sparse and unevenly distributed.

Upper tail dependence can be studied using copulas (Nelson 2006 [7]) and copulas can be estimated using a two-step maximum likelihood method the properties of which are discussed in White (1994 [10]). In the two dimensional case, Archimedean copulas such as BB1 are more flexible than Gaussian in capturing heavy tails while the estimation of higher dimensional Archimedean copulas may not be as fully studied as in the two dimensional case (Marius 2012 [6]). Factor models have been introduced to control model complexity as well (DongHwan 2011 [4]). Within this context, a mixture of Gaussian copulas presents an effective alternative method for improving model performance if one wants to study complex dependence structures based on simple copulas.

Finally, Gaussian Copula Mixture Models are developed to meet both needs. Gaussian Copula Mixture Models can be viewed as extension of Gaussian Mixture Models ([8]] and [13]), which aim to address the following two concerns:

-

•

Heavy-tailed data require increasing numbers of clusters to fit GMMs. To capture the control number of clusters, heavy tails on marginal distributions may lead to greater number of clusters in GMM. However, if the heavy-tailed data appear independently on each dimension, we should not use increasing number of clusters to describe them; in another word, multidimensional cluster should be introduced in copula space instead of the original data space and heavy tailed marginal distributions should be modeled separately. These intuition leads to GCMM, in which marginal distributions can be updated using non-parametric methods, and mixture models are used to model the dependent structure. Such a model potentially leads to fewer number of clusters.

-

•

GMMs are usually applied to a synchronized panel data matrix of dimension and number of observations . In many problems, there are numerous unsynchronized data on each dimension, the number of which is denoted as for the -th dimension. Such data should be utilized to update the joint distribution shared by the different dimensions. For a concrete example, if we have 500 observations on variable A and 400 observations on variable B, with 300 by 2 observations which are synchronized data between A and B, GMM will utilize the 300 by 2 observations to update the mixture model while GCMM can utilize 300 by 2 observations points to update the mixture copula structure. But GCMM will further utilize the unsynchronized 200 observations for A and 100 observations for B to update their marginal distributions respectively, which further contributes to the estimation of the copula mixture during iteration.

Ke [14] proposed implicit Gaussian mixture models in 2010 and summarized its theoretical properties in the PHD dissertation as in 2014 [15]. Gaussian copula mixture models are extension to GMM and expectation maximum method was used to generate estimates for the joint distribution of travel time on nearby highways. This paper extends the PHD dissertation and discussed the theoretical properties of the Gaussian copula mixture models and proposed ways to employed usage of un-synchronized data in the EM algorithm. Such theoretical study provided foundations for all relevant applications on different data set.

Independently there is a similar term called Gaussian Mixture Copula Models which was introduced by Tewari 2011 [16], where EM method and gradient descent method was proposed to estimate the distributions. However, the theoretical properties of the log likelihood is not fully explored and how marginal data can be explored in the estimation process can be further studied. Rajan 2016 [17] used Gaussian mixture copulas, to model complex dependencies beyond those captured by meta–Gaussian distributions, for clustering. Bilgrawu 2016 [18] presented and discussed an improved implementation in R of both classes of GMCMs along with various alternative optimization routines to the EM algorithm. Kasa 2020 [19] real high-dimensional gene-expression and clinical data sets showed that HD-GMCM outperforms state-of-the-art model-based clustering methods, by virtue of modeling non-Gaussian data and being robust to outliers through the use of Gaussian mixture copula. Sheikholeslami 2021 [20] uses Gaussian mixture copulas to approximate the joint probability density function of a given set of input-output pairs for estimating the variance-based sensitivity indices.

On Bayesian stats side, Feldman 2022 [21] developed a novel Bayesian mixture copula for joint and non-parametric modeling of multivariate count, continuous, ordinal, and unordered categorical variables. In Zou 2022 [22], a high-dimensional Vine-Gaussian mixture Copula model is combined with Bayesian CNN-BiLSTM model to evaluate uncertainties of model output.

3 Mathematical Definitions

A Gaussian copula mixture model (GCMM) consists of a weighted sum of a finite number of joint distributions, each of which contains a Gaussian copula. It is a generalization of the usual a Gaussian mixture model (GMM). When the marginal distributions are restricted to be Gaussian, the model reduces to a GMM. To begin, the multivariate Gaussian copula is defined by the following probability function:

| (2) |

whose density is given by

| (3) |

where

-

•

is the one dimensional cumulative distribution function for a standard normal distribution with density ;

-

•

is the copula parameter matrix;

-

•

is the number of dimension.

Then, with the Gaussianlization of original data on each dimension, a GCMM for the joint distribution of a random vector can be defined as follows:

| (4) |

where

-

•

is the marginal observation.

-

•

is the vector of the transferred data.

-

•

is the d-th dimension of the transferred data.

-

•

is the density of the marginal distribution.

-

•

is the weight to the -th copula.

Its density is given by

| (5) |

The density above is defined conditioned on the cumulative probability values and Gaussianized random variables which are both determined by the marginal distributions. The marginal distribution on each dimension for each component can be estimated via nonparametric methods such as kernel smoothing (Bowman 1998 [1]).

4 Basic Properties of GCMM

A GCMM is defined based on the separation of the mixture of copulas and marginal distributions, which may potentially lead to different behavior from GMM. To understand the properties of GCMM, its likelihood function is studied so that appropriate estimation algorithms can be designed. The major properties of GCMM are discussed below:

-

•

A GCMM has a bounded likelihood function value on bounded domains and tractable derivatives conditioned on the estimated marginal probability functions. The likelihood function is given below:

(6) We provide the following theorem to demonstrate the features of such a likelihood function and the proof is given in the appendix.

Theorem 1

Under suitable conditions, the likelihood function is bounded above in bounded region; non-decreasing and negative semi-definite w.r.t density ; may contain both local minimum and local maximum w.r.t transformed variables .

-

•

The value of its likelihood function is nondecreasing during iterations of Expectation-Maximum algorithms that are applied with GCMM and the algorithms converge globally to local maximums under mild conditions(Wu 1983 [11]). The design and properties of these Expectation-Maximum algorithms are discussed in the next section.

-

•

Model selection can be conducted through Akaike information criteria (Fan 2009 [5]) and cluster methods such as k-means or hierarchy clustering can be used to set the initial parameters of each component.

5 Expectation Maximum Algorithms for GCMM

5.1 The Base Case Algorithm

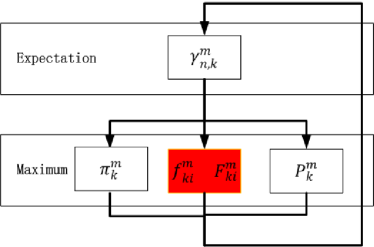

The algorithm updates the mixture of copulas and the marginal distributions separately. Essentially when estimating GMMs, the weights & correlation matrixes of components and the sufficient statistics (mean and standard deviation ) of the marginal normal distributions are updated (Dempster 1977 [3]) based on the posterior probability . In GCMMs, the sufficient statistics of marginal normal distributions are replaced with non-parametric estimators to the marginal pdf and cdf to improve flexility, see the red boxes in Figure 1.

The major challenge of algorithm design lies in how the marginal distributions should be updated considering the posterior probability. An updating formula is developed and given by the following theorem:

Theorem 2

In the GCMM base case, the updating of the marginal distributions follows the following formula with necessary normalizations:

Based on the theorem, the algorithm is further developed below:

-

•

Expectation Step:

(7) (8) -

•

Maximum Step:

(9) (10) (11) -th copula, -th dimension

The issue here is that heavy tail phenomenons may be categorized into two classes: the heavy tails in the marginal distribution and the heavy tails in the dependence structure. GCMM separates the estimation for them and control the number of clusters purely based on the complexity of heavy tails in dependence structure (the latter). In this manner, the number of clusters could be further reduced and the mixture of copulas are robust towards heavy tails on the marginal distributions (the former).

5.2 With Unsynchronized Data

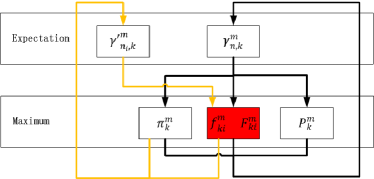

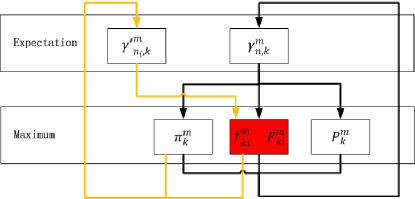

GCMMs with unsynchronized data are developed based on the rationale that unsynchronized data in each dimension can be used to update the marginal distribution, given the estimation of marginal distribution is separated from the mixture of copulas. An additional posterior probability is introduced to represent the probability of -th unsynchronized data on the -th dimension belonging to the -th component. An additional loop is then inserted into the Expectation Maximum algorithm for GCMM base case which further updates based on new information, see the orange loop in Figure 2.

The major challenge of algorithm design lies in how the marginal distributions should be further updated given unsynchronized data and the existing nonparametric estimator. An updating formula is developed and given by the following theorem:

Theorem 3

In the GCMM with unsynchronized data, the updating formula of marginal distribution follows by the following formula with necessary normalizations:

Based on the theorem, the algorithm is further developed below (similar parts as the base case are ignored to save space):

-

•

In Expectation step:

-

–

update for synchronized data;

-

–

update for un-synchronized data using the following Bayes formula:

(12)

-

–

-

•

In each iteration, update the marginal cdfs according to and . k-th copula, i-th dimension:

(13)

The philosophical issue here is whether synchronized data truly represent the joint distribution adequately and whether the unsynchronized data may add to our understanding of it. To bring unsynchronized data into the whole Expectation Maximum algorithm enlarges the information set of the probability space () so that deeper elaboration of the data is possible (Cinlar 2011 [2]). This is a significant improvement from GMM beyond the flexibility applied to the marginal distribution.

6 Experiment

6.1 Simulation Test

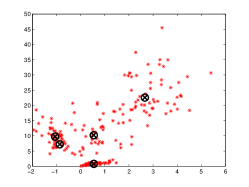

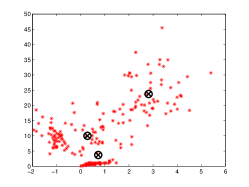

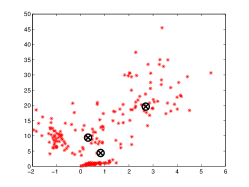

In this section, two-dimensional data are simulated based on a three-copula GCMM and the distribution of the data is given in Figure 3. Then the two Expectation Maximum algorithms are utilized to estimate the model and Akaike information critera is used to select the number of clusters. It is found that GMM needs five clusters to explain the data well while GCMM needs three. We further aggregate the data in the three dimensions to see the fitting for their sum: additional data are simulated with the estimated GMM and GCMM and their sum is compared with that for the calibration data. Two sample KS test demonstrates that the simulated data based on GCMM captures the distribution of the calibration data set.

-

•

GCMM achieves better fitting with fewer clusters.

Figure 3: Clusters for GMM v.s. Clusters for GCMM -

•

The p-values of two sample KS test for the sum of two random variables are compared in Table 1, which suggests that the GCMM fits the distribution of sum better than the GMM given the same number of clusters.

Table 1: p-values of two-sample KS test compared with the simulated distribution GMM Base Case Extra-Data 0.0002 0.1304 0.1003

6.2 Test on Empirical Data

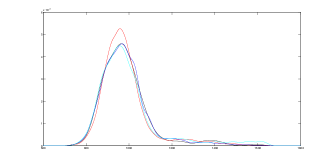

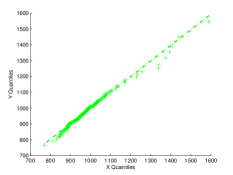

A real data set from the transportation system using the travel time of individual drivers in New Jersey which is captured from GPS devices is employed for model testing. On each transportation link (a road segment) there are many travel time observations, and by matching the departure time of the current link and the arrival time of the immediate downstream link, such data can be synchronized to construct the vector for running GMM. However, not all data on each link can be synchronized because the arrival times of drivers are random and sparse in time. The ultimate goal is to aggregate such link level data for estimating the distribution of the travel time over a path consisting of a few consecutive links. The same procedure is used as the simulation test in the previous section except the calibration data set is real. The results are summarized below, to save space the three-dimensional clusters are omitted:

-

•

The comparison to the empirical path travel time distribution is shown in Table 2 for a three segment path. Akaike information criteria indicates both the GMM and the GCMM needs three clusters to describe the data well and p-values of the KS tests for GCMM are noticeably larger.

Table 2: p-values of two-sample KS test compared with the empirical distribution GMM Base Case Extra-Data 0.0518 0.9646 0.1157 -

•

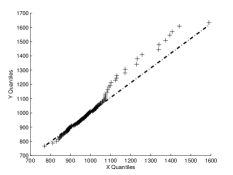

Estimated distributions are compared in Figure 4, GCMM with unsynchronized data captures heavier tails as there are some higher values in the unsynchronized data. The heavier tail is caused by differences in marginal distributions due to new information in the synchronized data, but not by material changes of the mixture of copulas.

Figure 4: Comparison of pdf (Red: GMM; Blue: GCMM base case; Cyan: GCMM with unsynchronized data; Black: Empirical); Green QQplot Empirical(x) v.s. GCMM base case(y); Black QQplot Empirical(x) v.s. GCMM with unsynchronized data(y)

7 Conclusion

In this paper, Gaussian copula mixture models (GCMMs) are developed to estimate the joint distribution of a group of random variables and further estimate the distribution of their sum. The Expectation Maximum algorithm is extended to estimate the GCMM models. Overall, GCMMs first add more flexibility to fit heavy tails on marginal distributions while remaining relatively robust against it; GCMMs further incorporate unsynchronized data into estimation, both of which improve the approximation to the complex dependence structures given limited number of components. In the future, the empirical properties of this new category of models on specific data sets can be studied further.

8 Proofs

8.1 Proof to Theorem 1

Proof Consider maximizing the following function

| (14) |

with the constraints:

, , and

If it is changed into a minimization problem by multiplying the objective by -1, the full Lagrange objective function will be:

with

, , ,

and

, , and

Then

Where

where And

,

By taking , there should be the following relationship:

| (15) |

| (16) |

| (17) |

The objective may be minimized in the inner area, that is: (1) and the solution is denoted as ; (2) and , the solution is denoted as ; (3) and , the solution is denoted as .

For , the following analysis is conducted:

where and as defined in the previous section

Notice here is diagonalizable since is the covariance matrix of two normally distributed random vectors. is then positive and semi-definite. Define

Since is positive, will determine the properties of the function with respect to .

if , and

if , and

Then

| (18) |

| (19) |

| (20) |

Then can be solved using the equations above. Furthermore, extreme values of the are considered as follows:

If then the data point is classified as Type 1 for k-th copula. The objective is always minimized on the boundary. That is: (1) and , the solution is denoted as ; (2) and the solution is denoted as .

If , then the data point is classified as Type 2 for k-th copula. The objective may be minimized in the inner area. That is: (1) and , the solution is denoted as ; (2) and , the solution is denoted as ; (3) and , the solution is denoted as .

In all cases, the value of the likelihood function is bounded above by a value determined by these finite extreme values in and . Q.E.D.

8.2 Proof to Theorem 2

Denote as the observed synchronized data vector, are the complete data. Recall in the Expectation step we calculate the posterior probability for -th data vector belong to -th cluster such that the incomplete data likelihood function below is expressed explicitly.

In the Maximum step we calculate to obtain new parameters based on such .

In this process, the poster distribution is

So the natural estimator for the marginal distribution for the -th dimension of the -th component is its histogram conditioned on the current weights:

Further normalization is used to maintain the properties of a cdf and other univariate non-parametric estimator can be used. Q.E.D

8.3 Proof to Theorem 3

Denote as the observed synchronized data vector, as -th observed unsynchronized data on the i-th dimension and as the complete data Recall in the Expectation step of the likelihood function is to calculate the posterior probability for -th data vector belong to -th cluster such that the incomplete data likelihood function below is expressed explicitly.

Moreover, we also calculate the posterior probability for (the -th unsynchronized observation on the i-th dimension) to belong to -th cluster based on .

In the Maximum step we calculate to obtain new parameters based on such and .

The poster distribution is

The poster distribution is

So the natural estimator for the marginal distribution for the -th dimension of the -th component is its histogram conditioned on the current weights for all data on that dimension.

Further normalization is used to maintain the properties of a cdf and other univariate non-parametric estimators can be used. Q.E.D

9 Acknowledgement

10 Reference

[1] Bowman, A., Hall, P. & Prvan, T. (1998), ‘Bandwidth selection for the smoothing of distribution functions’, Biometrika 85(4), 799.

[2] Erhan Cinlar, Probability and stochastics, volume 261. Springer, 2011.

[3] Arthur P Dempster, Nan M Laird, Donald B Rubin, et al. Maximum likelihood from incomplete data via the em algorithm. Journal of the Royal statistical Society, 39(1):1-38, 1977

[4] Dong Hwan Oh and Andrew J. Patton, Modelling Dependence in High Dimensions with Factor Copulas, Duke University 31 May 2011

[5] Jianqing Fan, Richard Samworth and Yichao Wu Ultrahigh dimensional feature selection: beyond the linear model, 2009, Journal of Machine Learning Research 2013-2038.

[6] Marius Hofert, Martin Machler, Alexander J. McNeil: Estimators for Archimedean copulas in high dimensions 2012-11-05, arXiv:1207.1708v2 [stat.CO] 2 Nov 2012

[7] R.B. Nelsen. An Introduction to Copulas. Springer Science+ Business Media, Inc., 2006.

[8] Pekka Paalanen , Joni-Kristian Kamarainen, Jarmo Ilonen , Heikki Kelvininen, Feature representation and discrimination based on Gaussian mixture model probability densities practices and algorithms,Pattern Recognition, Volume 39, Issue 7, July 2006, Pages 1346-1358

[9] M Sklar. Fonctions de r’epartition ‘a n dimensions et leurs marges. Universit’e Paris 8, 1959.

[10] H. White. Estimation, Inference and Specification Analysis. Cambridge University Press, 1994

[11] CF Jeff Wu. On the convergence properties of the em algorithm. The Annals of statistics, pages 95-103, 1983.

[12] Lei Xu and Michael I Jordan. On convergence properties of the em algorithm for Gaussian mixtures. Neural computation, 8(1):129-151, 1996.

[13] Ming-Hsuan Yang, Narendra Ahuja: Gaussian mixture model for human skin color and its applications in image and video databases Proc. SPIE 3656, Storage and Retrieval for Image and Video Databases VII, 458 (December 17, 1998); doi:10.1117/12.333865

[14] Ke Wan and Alain Kornhauser: Turn-by-turn routing decision based on copula travel time estimation with observable floating car data, TRB 2010

[15] Ke Wan: Estimation of travel time distribution and travel time derivatives, 2014

[16] Tewari, Ashutosh and Giering, Michael J and Raghunathan, Arvind: Parametric characterization of multimodal distributions with non-gaussian modes, 2011 IEEE 11th international conference on data mining workshops, 2011

[17] Rajan, Vaibhav and Bhattacharya, Sakyajit: Dependency Clustering of Mixed Data with Gaussian Mixture Copulas, IJCAI, 2016

[18] Bilgrau, Anders Ellern and Eriksen, Poul Svante and Rasmussen, Jakob Gulddahl and Johnsen, Hans Erik and Dybkær, Karen and Bøgsted, Martin: GMCM: Unsupervised clustering and meta-analysis using gaussian mixture copula models, Journal of Statistical Software, 2016

[19] Kasa, Siva Rajesh and Bhattacharya, Sakyajit and Rajan, Vaibhav: Gaussian mixture copulas for high-dimensional clustering and dependency-based subtyping, Bioinformatics, 2020

[20] Sheikholeslami, Razi and Gharari, Shervan and Papalexiou, Simon Michael and Clark, Martyn P: VISCOUS: A Variance-Based Sensitivity Analysis Using Copulas for Efficient Identification of Dominant Hydrological Processes, Water Resources Research, 2021

[21] Feldman, Joseph and Kowal, Daniel R: Nonparametric Copula Models for Mixed Data with Informative Missingness, arXiv preprint arXiv:2210.14988, 2022

[22] Zou, Mingzhe and Holjevac, Ninoslav and Đaković, Josip and Kuzle, Igor and Langella, Roberto and Di Giorgio, Vincenzo and Djokic, Sasa Z: Bayesian CNN-BiLSTM and Vine-GMCM Based Probabilistic Forecasting of Hour-Ahead Wind Farm Power Outputs, IEEE Transactions on Sustainable Energy, 2022