ChihYun Chuang and TingFang Lee

11institutetext: AMIS, Taipei, Taiwan

11email: chihyun@maicoin.com,

22institutetext: College of Pharmacy, University of Rhode Island, Rhode Island, USA

22email: tingfanglee@uri.edu

A Practical and Economical Bayesian Approach to Gas Price Prediction

Abstract

On the Ethereum network, it is challenging to determine a gas price that ensures a transaction will be included in a block within a user’s required timeline without overpaying. One way of addressing this problem is through the use of gas price oracles that utilize historical block data to recommend gas prices. However, when transaction volumes increase rapidly, these oracles often underestimate or overestimate the price. In this paper, we demonstrate how Gaussian process models can predict the distribution of the minimum price in an upcoming block when transaction volumes are increasing. This is effective because these processes account for time correlations between blocks. We performed an empirical analysis using the Gaussian process model on historical block data and compared the performance with GasStation-Express and Geth gas price oracles. The results suggest that when transactions volumes fluctuate greatly, the Gaussian process model offers a better estimation. Further, we demonstrated that GasStation-Express and Geth can be improved upon by using a smaller training sample size which is properly pre-processed. Based on the results of empirical analysis, we recommended a gas price oracle made up of a hybrid model consisting of both the Gaussian process and GasStation-Express. This oracle provides efficiency, accuracy, and better cost.

keywords:

Ethereum, Gas Price Oracle, Blockchain, Gaussian Process, Bayesian1 Introduction

On the Ethereum blockchains[1], Gas refers to the fuel required to conduct a transaction or execute a smart contract[2]. Since each block on the chain has an upper bound on the amount of gas that can be included in it111The average block gas limit was around 12,500,000 units of gas at the day of Mar 4, 2021., miners maximize profit by prioritizing transactions offering higher gas prices. As with all markets exhibiting supply and demand dynamics, it is advantageous for users to be able to predict and offer the minimum gas price that ensures their transactions will be included in a block within a pre-determined timeline.

Developing such a gas price oracle is complicated by the high variability in transaction volume. Under these conditions, some existing gas price oracles either underestimate the prices needed such that these transactions have to wait a long time to be included, or overestimate the price, which results in users overpaying for the transaction.

To date, one of the primary methods for gas price prediction is to analyze the pricing structure of pending transactions in large mempools [3]. This method is resource intensive as it requires accessing large quantities of mempools to obtain enough pending transaction data for analysis. Further, it can only accurately predict the gas prices under the assumption that the data from mempools is correct, something that is difficult for users to verify. Another method is to utilize recent transactions that were included by miners to recommend a price. Some algorithms based on this concept have been used to develop gas price oracles including Geth, EthGasStation, GasStation-Express (abrev. GS-Express) and the work of Sam M. Werner et al. [4, 5, 6, 7, 8].

One such gas price oracle, GS-Express, proposed using the set of minimum gas prices in the most recent blocks. The model suggests that the probability of the th percentile of the set is greater than the minimum gas price of the transactions in the next block is . In other words, the th percentile of the set has probability to be included in the next block. An additional oracle, Geth, uses the set of minimum gas prices in the most recent blocks and takes the th percentile of the set as a recommended gas price. These models provide an efficient way to recommend gas prices when the quantity of pending transactions are relatively few. However, when there is a surge of pending transactions, these models will underestimate the prices.

In this paper, we will focus on a novel predictive model that uses recent successful mining blocks to estimate the lowest price a user should offer to obtain a specified probability level that the transaction will be processed. The proposed methodology uses Gaussian process (abrev. GP) models to predict the distribution of the minimum price in the upcoming block. Stochastic processes, including GP, are often used to study numerous stock market micro-structure related questions, including price discovery, competition among related markets, strategic behavior of market participants, and modeling of real time market dynamics. These processes present potentially efficient estimators and predictors for volatility, time-varying correlation structures, trading volume, bid-ask spreads, depth, trading costs, and liquidity risks. The market forces acting within Ethereum markets are very similar to these, making GP an appropriate method to capture the dynamics of Ethereum gas prices. Another attractive feature of stochastic processes is the covariance functions, which allows the model to estimate the time correlation between blocks; that is, it can capture the stronger correlation between closer blocks. Our method provides stable price prediction even when there is a surge in transaction volume. Over the long-term, the gas prices recommended by the model are more economical and practical222The average time consumed of the GP model is seconds to predict a new price. compared with existing methods.

Our contributions include the following: 1) We introduce a novel application of Gaussian process to evaluate pricing models and then use it to study the advantages and disadvantages of GS-Express, Geth, and GP. Our findings indicate that GS-Express and Geth over/under-estimated the price when the transaction volume fluctuates greatly, while GP maintained reasonable accuracy. Additionally, GP possesses time efficiencies in model training and prediction. 2) A sensitivity analysis was conducted to study the impact of the training data sizes on the performance of the GS-Express model. This showed reducing the training data size to 50 or 30 can effectively improve prediction. However, this requires a reliable data pre-processing procedure. 3) We propose a practical and economical gas price oracle in Algorithm 1 which retains the advantages of both GP and GS-Express and avoids the disadvantages of each. Our method is superior in achieving the targeted short-term and long-term success rates among the considered blocks compared with existing methods. Remarkably, except for (see Table 7 and 8), the average cost of our method is still less than the others.

The outline of this paper is as follows. In section 2, we introduce the operation of transactions in the Ethereum network and Gaussian processes. In section 3, we establish our methodology, including data pre-processing and modeling. In Section 4 we present the results for GP predictive models and compare with GS-Express and Geth models . Finally in Section 5, we propose a gas price oracle that is a hybrid of GP and GS-Express and utilizes the advantages of each.

2 Background

In this section, we provide a brief overview of transactions in the Ethereum network and Gaussian processes.

2.1 Ethereum & Gas

Like other permission-less blockchains and cryptocurrencies, Ethereum obtains consensus using a form of cryptographic zero-knowledge proof called “Proof-of-work“. In such protocols, a character called “miner”, groups transactions into a block and appends it to the end of blockchains. This work is resource consumptive, and thus, operations using Ethereum require a fee, which is received by miner in exchange for performing the work. Based on the gas price, miners determine which transactions should be included in a block.

A transaction fee is calculated in Gas, using a unit called weiETH or GweiETH, where ETH is the currency in Ethereum. The cost of execution is equal to:

Here

-

•

The gas cost is bounded by the lower bound and the upper bound gas limit, which represents the maximum amount of gas a user is willing to use for an operation. The precise amount of gas cost depends on the complexity of performing “smart contracts”, which define a set of rules using a Turing-complete programming language. After the transaction is completed, all unused gas is returned to the user’s account. If the gas limit is less than the gas cost, then the transaction is viewed as invalid and will be rejected; the gas spent to perform calculations will not be returned to the account.

-

•

The gas price is also determined by the user and represents the price per unit of gas the user is offering to pay. Since a miner’s reward is largely determined by the gas price, a higher gas price results in a greater probability of transactions being selected by miners and grouped into blocks.

2.2 Gaussian Process

A Gaussian process is a stochastic process that provides a powerful tool for probabilistic inference on distributions over functions. It offers a flexible non-parametric Bayesian framework for estimating latent functions from data. Briefly speaking, Gaussian Process makes prediction with uncertainty. For instance, it will predict that a stock price of the next minute is $100, with a standard deviation of $30. Knowing the prediction uncertainty is important for pricing strategies. The rest of this section will follow [9] to describe the GP regression.

Definition 2.1.

A Gaussian process is a collection of random variables, any finite number of which have a joint Gaussian distribution.

A GP is specified by its mean function and covariance function which determine the functions’ smoothness and variability. Given input vectors and , we define mean function and the covariance function of a real process as

and will write the Gaussian process as

Given a training dataset where denotes the input vector and denotes the target variable. One can consider the Gaussian noise model

The squared exponential with hyperparameter ,

is considered the most widely used covariance function. This covariance function is also appropriate in our model, since recent gas prices have stronger correlation.

The joint distribution of the observed target values and the function value at a new input is

| (1) |

where , the notation denotes matrix transportation, is the covariance matrix, , and . Therefore, the posterior predictive distribution is

| (2) |

The accuracy of the GP regression model depends on how well the covariance function is selected. In particular, estimating the hyperparameter of the covariance function is critical to prediction performance. The Laplace approximation framework is often utilized to approximate the predictive posterior distribution and is constructed from the second order Taylor expansion of around the maximum of the posterior. It has been shown to provide more precise estimates in much shorter time [10].

3 Methodology

In this section, we explain the steps of data pre-processing. Then, processed data will be fitted into the GP regression model, Geth, and GS-Express. The method to evaluate the performance of each model is introduced in 3.3.

3.1 Pre-processing

In order to maintain statistical significance, we removed blocks with a number of transactions less than . Further, some blocks have uncommonly low cost transactions. For instance, there are three zero fee transactions in block . Such transactions are rare and yet create noise in the models. Therefore, we excluded these transactions by removing all transactions in which the fees were lower than the 2.5 percentile among all gas prices. The processing steps are as follows:

-

1.

Take blocks with more than six transactions.

-

2.

Calculate the 2.5 percentile of each block, called .

-

3.

Remove the transactions in which the fees are lower than .

-

4.

Obtain the minimum gas price in each block, called .

3.2 The Model

Take consecutive blocks, , and let the training dataset where The goal is using the GP regression model to predict in .

We consider the Gaussian noise model The squared exponential covariance function is used to estimate the covariance matrix in the joint distribution (1). The posterior predictive distribution (2) is used to predict the mean, , and the standard deviation, , of the minimum gas price in the -th block; that is,

More specifically, the above estimation means that the probability of that is greater than the minimum gas price, , of -th block is 50%. We then define that is of -th block. Similarly, is of -th block. ( is 333More precisely, it should be ; is ).

3.3 Model Evaluation

In this section, we will introduce a model comparison criteria, inverse probability weight (IPW), to compare models performance in terms of accuracy and efficiency. Our procedure to compare the GP regression model, GS-Express, and Geth contains the following steps:

-

I.

Given consecutive blocks and , we use the GP regression model, GS-Express, and Geth to predict . We then compare the predicted with actual . If , the transaction is viewed as successfully included in block . Define

-

II.

Iterating the model fitting obtains , and so on. Define the success rate among blocks as

Here is the number of observations of training data.

Note that the function is an increasing function for . We use to observe the short term () and long term () success rate while using training data with observations. It is notable that

given an ideal gas price oracle. Therefore, in the long run, the success rate of all three methods, GP model, GS-Express, and Geth, using should be approximately (i.e. is a consistent estimator of ). That is,

When is not large, can reflect the predictive performance of each method in the short-term. An inefficient gas price oracle can result in a pending transaction, e.g. 50 minutes. Although users can resign444Use the same nonce and increase the gas price. the pending transactions from the Ethereum network, a new price is still required from the oracle. Therefore, a gas price oracle needs to perform reasonably in a short period of time.

The ultimate goal is to predict the lowest prices such that the transactions can be included in a block. Higher prices can, of course, result in higher success rates. Therefore, we introduce a measurement, inverse probability weight, which can reflect better pricing strategy.

In words, a small IPW represents low cost with high success rate; on the other hand, high cost with low success rate gives large IPW. We will use this measurement to evaluate model performance in the next section.

4 Empirical Analysis

We use a laptop with CPU:Intel® Xeon® Processor E3-1505M v5 2.80 GHz and 32gb ram to perform all analysis. Mathematica 12 was utilized for Gaussian process regression model fitting with squared exponential covariance function specified. SageMath was used GS-Express and Geth to operate the model fitting and prediction. All used data can be found in [11].

4.1 Observations

The historical block data, block 11753792 to 11823790555Jan-29-2021 to Feb-09-2021, were used in the analysis. There were 1450 blocks that have no transaction and 4 blocks have less than 7 transactions. We first removed these blocks and followed steps 2, 3, and 4 in Section 3.1 to process the remaining blocks. After pre-processing each block, we have 68,545 blocks. We denote those blocks by , e.g. the block number of is 11753792, and is 11753994. Taking 200 consecutive blocks as training data, we fit the GP model and GS-Express to the training data. Geth uses only 100 training data. Each model will be used to predict the minimum gas price of the next block. In other words, we fit each of the three models into 1st to 200th blocks, we then predict , , , and of the minimum gas price of 201st block. Next, we fit the models into 2nd to 201st blocks, we then predict , , , and of the minimum gas price of 202nd block, and so on. The obtained values will be used to compare with the true minimum gas price. Following I. and II. in Section 3.3, we will demonstrate the success rate of each model, and compare the performance.

Ideally, the success rate would be approximately when using to compare with the true minimal price. We find that the long term success rate , Table 1, of GS-Express and Geth on are around 0.5 and GP is 0.36. GS-Express and Geth underestimated the prices on , , and and GP suggested relatively accurate prices on , , and . The average cost,

of each method is also reported in Table 1.

| Success Rate | Average cost (Gwei) | |||||||

|---|---|---|---|---|---|---|---|---|

| Method | ||||||||

| GP | 0.358 | 0.744 | 0.862 | 0.972 | 128.6 | 168.3 | 187.4 | 225.3 |

| GS-Express | 0.502 | 0.696 | 0.784 | 0.914 | 141.6 | 168.0 | 178.2 | 197.1 |

| Geth | 0.500 | 0.712 | 0.798 | 0.922 | 143.1 | 164.7 | 174.1 | 193.3 |

| Inverse Probability Weight | ||||

|---|---|---|---|---|

| Method | ||||

| GP | 359.22 | 226.22 | 217.40 | 231.79 |

| GS-Express | 282.07 | 241.38 | 227.30 | 215.65 |

| Geth | 286.20 | 231.32 | 218.17 | 209.65 |

Note: The average cost is .

We also calculated the minimum short term success rate

and reported the minimum success in Table 2. The success rate of consecutive blocks are considered to be fast, average, and slow, respectively, when grouped by miners. From Table 1 and 2, we observe that GP performs better when using , , and in a long term and also maintain better success rate in short terms .

| GP | GS-Express | Geth | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 25 | 0 | 0.12 | 0.24 | 0.36 | 0 | 0 | 0 | 0.12 | 0 | 0 | 0 | 0.24 |

| 50 | 0.04 | 0.20 | 0.32 | 0.54 | 0.02 | 0.06 | 0.06 | 0.18 | 0.04 | 0.06 | 0.08 | 0.40 |

| 100 | 0.09 | 0.33 | 0.42 | 0.71 | 0.07 | 0.12 | 0.16 | 0.32 | 0.10 | 0.19 | 0.23 | 0.50 |

We now focus on the success rate of of each method. GP gave 0.744 success rate while GS-Express and Geth had 0.696 and 0.712. We derived an such that from GP provided a comparable level of success rate, but lower cost than GS-Express and Geth, see Table 3. Therefore, in the long term, GP has the advantage in cost and success rate. However, GS-Express can have better performance when using less training data.

| Short term success rate | Long term | ||

|---|---|---|---|

| 0.12 | Success rate | 0.712 | |

| 0.18 | Average cost | 164.16 Gwei | |

| 0.30 | IPW | 230.56 | |

4.2 More Observations

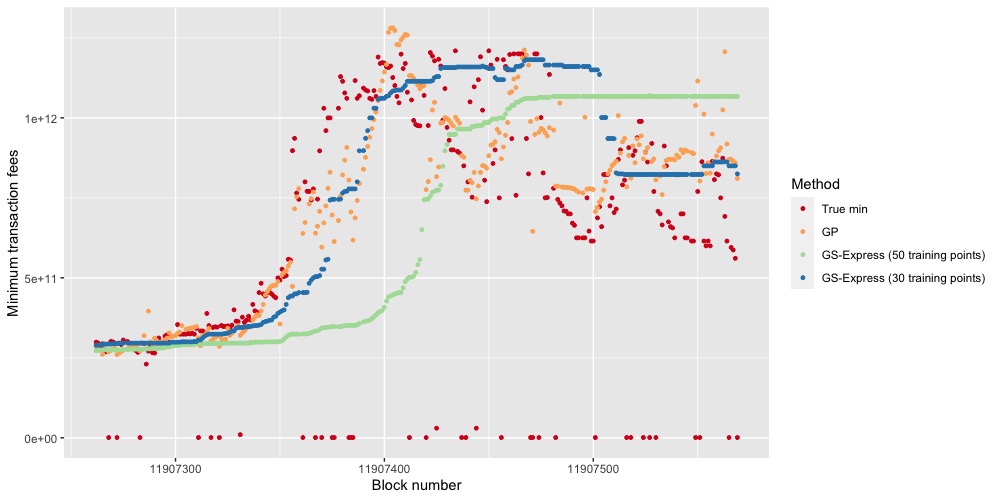

The gas prices showed large fluctuations during block 11903793 to 11917694666Feb-22-2021 to Feb-24-2021. We also provided analogous results for these blocks transaction data. According to the previous observations, we reduced the training data points for GS-Express to 50 or 30. After pre-processing these recent block data, we have 13627 blocks denoted by , e.g. the block number of is 11903793, and is 11903999. The long term success rate of GP and and of GS-Express, and the average costs are reported in Table 4. The minimum short term success rates () of each model can be found in Table 5. The results are consistent with the observations in Section 4.1.

| Success Rate | Average cost (Gwei) | |||||||

|---|---|---|---|---|---|---|---|---|

| Method | ||||||||

| GP | 0.375 | 0.79 | 0.911 | 0.982 | 248.5 | 314.5 | 346.3 | 409.4 |

| GS-Express (30) | 0.516 | 0.70 | 0.786 | 0.882 | 270.9 | 297.0 | 312.4 | 331.8 |

| GS-Express (50) | 0.506 | 0.70 | 0.786 | 0.893 | 270.2 | 301.1 | 317.5 | 341.0 |

| Inverse Probability Weight | ||||

|---|---|---|---|---|

| Method | ||||

| GP | 662.67 | 398.10 | 380.13 | 416.60 |

| GS-Express (30) | 525.00 | 424.29 | 397.46 | 376.19 |

| GS-Express (50) | 533.99 | 430.14 | 403.94 | 381.86 |

| GP | GS-Express(30) | GS-Express(50) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 25 | 0 | 0.08 | 0.24 | 0.32 | 0 | 0 | 0 | 0.28 | 0 | 0 | 0 | 0.16 |

| 50 | 0.04 | 0.24 | 0.38 | 0.52 | 0.08 | 0.10 | 0.14 | 0.42 | 0.06 | 0.08 | 0.10 | 0.28 |

| 100 | 0.09 | 0.30 | 0.42 | 0.63 | 0.12 | 0.16 | 0.21 | 0.52 | 0.12 | 0.12 | 0.16 | 0.39 |

Similarly, we find that the prediction from GP gave a comparable level of success rate with the other methods, but lower cost, see Table 6.

| Short term success rate | Long term | ||

|---|---|---|---|

| 0.08 | Success rate | 0.701 | |

| 0.20 | Average cost | 298.85 Gwei | |

| 0.26 | IPW | 426.32 | |

5 Discussion

The goal of our study is to develop a gas price oracle which ensures that transactions will be included in a block within a user required timeline without overpaying. The proposed the GP regression provided an efficient prediction of gas prices, especially when the transaction volumes increase rapidly.

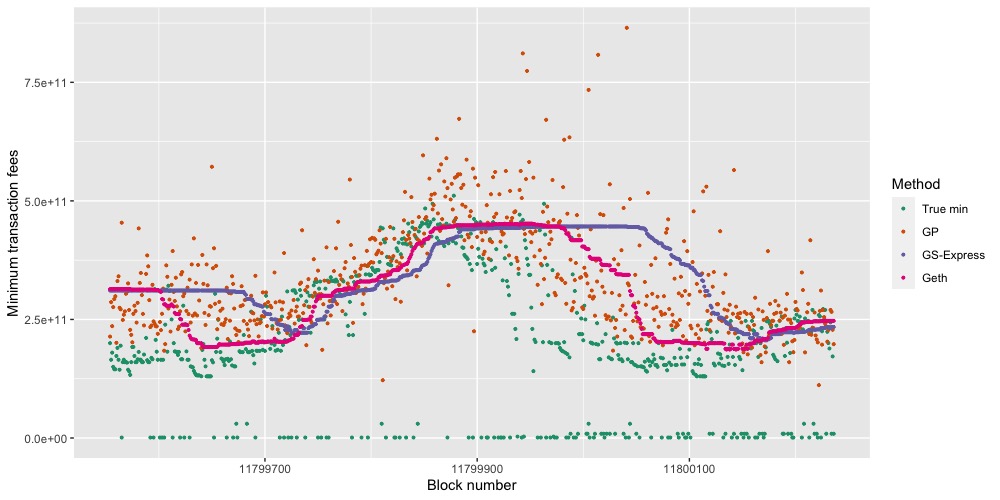

When using various amounts of data, e.g., 200, 100, 50, or 30, the GS-Express model performed poorly from block to and to . Figure 2(b) compared the prediction of from each method to the true minimum gas price in each block. When gas prices increased, GS-Express often underestimated the price and resulted in a pending transaction until the price stabilized or dropped. Furthermore, GS-Express overestimated the price when the price just dropped from a peak, which results in the user overpaying.

When the pending transaction volume remains stable, GS-Express performs better if we reduce the training data observations (from 200 down to 50 or 30). Reducing the training data can be a risk due to abnormal transactions such as zero fee transactions which may create more noise for the models. Pre-processing the data can effectively reduce the impact of these abnormal data points. Therefore, our observations from the empirical analysis are as follows:

-

1.

GP maintains a better success rate with little overpayment when transaction volumes are increasing rapidly.

-

2.

The prediction of Geth and GS-Express can be improved by reducing training data when the transaction volume fluctuate greatly. However, abnormal transactions can interfere with the models. Therefore, pre-processing data is an important step.

-

3.

Long term success rates of all 3 methods are comparable. However, Geth and GS-Express often underestimate the gas price when gas price rise rapidly.

In addition to using GP only, we propose the following gas price oracle, Algorithm 1, which consists of GP and GS-Express and depends on the change of instant success rates. Instant success rate can be used to monitor the bias of the GP and GS-Express estimators. When the gas prices are stable, GS-Express with a small training sample size performs well. When gas prices increases rapidly, the success rate is smaller than the expected value , and users can switch to GP to maintain the expected . If is higher than , the value should be adjusted to a lower level. This oracle offers efficiency, success rate, and better cost.

Input: the desired success rate , (resp. ) the size of training data of GS-Express(resp. GP), and an allowed error .

Output: a prediction of the block with the number .

-

i.

Take blocks with more than six transactions.

-

ii.

Calculate the 2.5 percentile of each block, called

-

iii.

Remove the transactions in which the fees are lower than .

-

iv.

Construct a set of the minimum gas price in each block.

-

a.

the case : The output is .

-

b.

the case : The output is .

-

c.

the case : Use intermediate value theorem to find such that . If such does not exist, one takes . Then the output is .

| Success Rate | Average cost (Gwei) | |||||||

|---|---|---|---|---|---|---|---|---|

| Method | ||||||||

| Our method | 0.52 | 0.73 | 0.81 | 0.92 | 143.0 | 158.4 | 168.1 | 189.7 |

| GS-Express | 0.50 | 0.70 | 0.78 | 0.91 | 141.6 | 168.0 | 178.2 | 197.1 |

| Geth | 0.50 | 0.71 | 0.80 | 0.92 | 143.1 | 164.7 | 174.1 | 193.3 |

| Inverse Probability Weight | ||||

|---|---|---|---|---|

| Method | ||||

| Our method | 275.00 | 216.99 | 207.53 | 206.20 |

| GS-Express | 283.20 | 240.00 | 228.46 | 216.59 |

| Geth | 286.20 | 231.97 | 217.63 | 210.11 |

| Success Rate | Average cost (Gwei) | |||||||

|---|---|---|---|---|---|---|---|---|

| Method | ||||||||

| Our method | 0.52 | 0.75 | 0.842 | 0.92 | 272.7 | 303.6 | 323.5 | 352.3 |

| GS-Express | 0.52 | 0.70 | 0.79 | 0.90 | 264.8 | 316.2 | 335.2 | 367.8 |

| Geth | 0.50 | 0.70 | 0.78 | 0.91 | 268.8 | 309.4 | 324.5 | 358.7 |

| Inverse Probability Weight | ||||

|---|---|---|---|---|

| Method | ||||

| Our method | 524.42 | 404.80 | 384.20 | 382.93 |

| GS-Express | 509.23 | 451.71 | 424.30 | 408.67 |

| Geth | 537.60 | 442.00 | 416.03 | 394.18 |

Note: The average cost is .

To evaluate the proposed gas price oracle, we use the gas prices in block 11799554 to 11800236 and 11903999 to 11917694. The gas prices in block 11799554 to 11800236 changed gradually and in 11903999 to 11917694 changed rapidly. We take , , and in our oracle. Our gas price oracle has smaller inverse probability weighting under most circumstances. The results suggested that our oracle has lower costs with higher long term success rates while also preserving the desired short term success rates, see Table 7 and 8.

Potential future work includes practicing the proposed gas price prediction procedure in real-time and verifying the efficiency and accuracy of this procedure. This will also enhance the study of short term success rate and real waiting times. Additionally, different covariance functions of the GP regression models should also be studied closely to determine which covariance function would be the best suited for predicting gas prices.

| block 11753792 to 11823790 | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Our method | GS-Express | Geth | |||||||

| 25 | 50 | 100 | 25 | 50 | 100 | 25 | 50 | 100 | |

| 0.04 | 0.08 | 0.18 | 0 | 0.02 | 0.07 | 0 | 0.04 | 0.10 | |

| 0.12 | 0.22 | 0.34 | 0 | 0.06 | 0.12 | 0 | 0.06 | 0.19 | |

| 0.20 | 0.38 | 0.50 | 0 | 0.06 | 0.16 | 0 | 0.08 | 0.23 | |

| 0.68 | 0.72 | 0.81 | 0.12 | 0.18 | 0.32 | 0.28 | 0.40 | 0.50 | |

| block 11903793 to 11917694 | |||||||||

| Our method | GS-Express | Geth | |||||||

| 25 | 50 | 100 | 25 | 50 | 100 | 25 | 50 | 100 | |

| 0 | 0.08 | 0.17 | 0 | 0.04 | 0.06 | 0 | 0.04 | 0.08 | |

| 0.12 | 0.28 | 0.35 | 0 | 0.04 | 0.10 | 0 | 0.06 | 0.12 | |

| 0.32 | 0.46 | 0.50 | 0 | 0.06 | 0.12 | 0 | 0.08 | 0.12 | |

| 0.52 | 0.64 | 0.73 | 0 | 0.08 | 0.13 | 0.08 | 0.14 | 0.22 | |

Acknowledgment

We would like to thank all of the AMIS data management teams, and participants who contributed to this project. We also thank Yu-Te Lin and Gavino Puggioni for their useful comments and feedbacks in earlier drafts and all the reviewers’ helpful comments and suggestions.

References

- [1] Ethereum.org. https://ethereum.org/en/, last accessed: February 17, 2021

- [2] Wood, G.: Ethereum: A secure decentralised generalised transaction ledger petersburg version 41c1837. Ethereum Yellow Paper (02 2021)

- [3] Gas platform. https://www.blocknative.com/gas, last accessed: February 17, 2021

- [4] Github. official go implementation of the ethereum protocol. https://github.com/ethereum/go-ethereum/, last accessed: February 17, 2021

- [5] Ethgasstation. https://ethgasstation.info, last accessed: February 17, 2021

- [6] Github. gasstation-express. https://github.com/ethgasstation/gasstation-express-oracle, last accessed: February 17, 2021

- [7] Antonio Pierro, G., Rocha, H., Tonelli, R., Ducasse, S.: Are the gas prices oracle reliable? a case study using the ethgasstation. In: 2020 IEEE International Workshop on Blockchain Oriented Software Engineering (IWBOSE). pp. 1–8 (2020)

- [8] Werner, S., Pritz, P., Perez, D.: Step on the Gas? A Better Approach for Recommending the Ethereum Gas Price, pp. 161–177 (10 2020)

- [9] Rasmussen, C., Williams, C.: Gaussian Processes for Machine Learning (01 2005)

- [10] Rue, H., Martino, S., Chopin, N.: Approximate bayesian inference for latent gaussian models by using integrated nested laplace approximations. Journal of the Royal Statistical Society Series B 71, 319–392 (04 2009)

- [11] Bayesian gas price oracle. https://github.com/bayesian-gas-price-oracle/A-Practical-and-Economical-Bayesian-Approach-to-Gas-Price-Prediction, last accessed: March 9, 2021