Augmented balancing weights as linear regression††thanks: We would like to thank David Arbour, Eli Ben-Michael, Andreas Buja, Alex D’Amour, Skip Hirshberg, Guido Imbens, Apoorva Lal, Mark van der Laan, Whitney Newey, Rahul Singh, Jann Spiess, and Qingyuan Zhao for useful discussion and comments. A.F. and D.B-S. were supported in part by the Institute of Education Sciences, U.S. Department of Education, through Grant R305D200010. The opinions expressed are those of the authors and do not represent the views of the Institute or the U.S. Department of Education. O.D. was supported by NIH grant 579679 and by the FWO grant 1222522N. E.L.O. was supported by ONR grant N000142112820 and by the Simons Institute for Theoretical Computer Science.

Abstract

We provide a novel characterization of augmented balancing weights, also known as automatic debiased machine learning (AutoDML). These popular doubly robust or double machine learning estimators combine outcome modeling with balancing weights — weights that achieve covariate balance directly in lieu of estimating and inverting the propensity score. When the outcome and weighting models are both linear in some (possibly infinite) basis, we show that the augmented estimator is equivalent to a single linear model with coefficients that combine the coefficients from the original outcome model coefficients and coefficients from an unpenalized ordinary least squares (OLS) fit on the same data; in many real-world applications the augmented estimator collapses to the OLS estimate alone. We then extend these results to specific choices of outcome and weighting models. We first show that the augmented estimator that uses (kernel) ridge regression for both outcome and weighting models is equivalent to a single, undersmoothed (kernel) ridge regression. This holds numerically in finite samples and lays the groundwork for a novel analysis of undersmoothing and asymptotic rates of convergence. When the weighting model is instead lasso-penalized regression, we give closed-form expressions for special cases and demonstrate a “double selection” property. Our framework opens the black box on this increasingly popular class of estimators, bridges the gap between existing results on the semiparametric efficiency of undersmoothed and doubly robust estimators, and provides new insights into the performance of augmented balancing weights.

1 Introduction

Combining outcome modeling and weighting, as in augmented inverse propensity score weighting (AIPW) and other doubly robust (DR) or double machine learning (DML) estimators, is a core strategy for estimating causal effects using observational data. A growing body of literature finds weights by solving a “balancing weights” optimization problem to estimate weights directly, rather than by first estimating the propensity score and then inverting. The DR versions of these estimators are referred to by a number of terms, including augmented balancing weights (Athey et al., 2018; Hirshberg and Wager, 2021), automatic debiased machine learning (AutoDML; Chernozhukov et al., 2022d), and generalized regression estimators (GREG; Deville and Särndal, 1992); see Ben-Michael et al. (2021b) for a review. This strategy applies to a wide range of linear estimands via the Riesz representation theorem (e.g., Hirshberg and Wager, 2021; Chernozhukov et al., 2022e).

In this paper, we consider augmented balancing weights in which the estimators for both the outcome model and the balancing weights are based on penalized linear regressions in some possibly infinite basis; in addition to all high-dimensional linear models, this broad class includes popular nonparametric models such as kernel regression and certain forms of random forests and neural networks. We generalize existing results by proving that any linear balancing weights estimator is numerically equivalent to applying unregularized ordinary least squares (OLS) coefficient estimates to a re-weighted — rather than observed — target covariate profile.

We use this characterization to show that, somewhat surprisingly, augmenting any regularized linear outcome regression (the “base learner”) with linear balancing weights is numerically equivalent to a single linear outcome regression applied to the target covariate profile. The resulting coefficients are an affine (and often convex) combination of the base learner model coefficients and unregularized OLS coefficients; the hyperparameter for the balancing weights estimator directly controls the regularization path defining the affine combination. We specialize these results to ridge and lasso regularization and show that augmenting an outcome model with balancing weights often corresponds to a form of undersmoothing. We then show that our numerical results on undersmoothing for (kernel) ridge-augmented balancing weights offer a new perspective on the optimal asymptotic regularization schedule for undersmoothed ridge regression. Finally, we demonstrate the implications of these results on several causal inference benchmark data sets. For the canonical LaLonde (1986) study, we show that applying several off-the-shelf augmented balancing weights and AutoDML estimators can be numerically equivalent to estimating the effect with unregularized OLS alone, even if the outcome regression base learner is heavily regularized.

Our results provide important insights into the nexus of causal inference and machine learning. First, these results open the black box on the growing number of methods based on augmented balancing weights and AutoDML — methods that can sometimes be difficult to taxonomize or understand. We show that, under linearity, these estimators all share an underlying and very simple structure. Our results highlight that estimation choices for augmented balancing weights can lead to potentially unexpected behavior. Most notably, the choice of (kernel) ridge regression for both outcome and weighting models collapses to a single (kernel) ridge regression estimator. This is a generalization of the argument in Robins et al. (2007) that “OLS is doubly robust” to a much broader class of penalized parametric and non-parametric regression models. At a high level, as causal inference moves towards incorporating machine learning and automation, our work highlights how the traditional lines between weighting and regression-based approaches are becoming increasingly blurred.

Second, our results connect two approaches to “automate” semiparametric causal inference. AutoDML and related methods exploit the fact that we can estimate a Riesz representer without a closed form expression for a wide class of functionals. The estimated Riesz representer then augments a base learner by bias correcting a plug-in estimator of the functional. Older approaches, such as undersmoothing (Goldstein and Messer, 1992; Newey et al., 1998), twicing kernels (Newey et al., 2004), and sieve estimation (Newey, 1994; Shen, 1997), also avoid estimation of the Riesz representer, tuning the base learner regression fit such that an additional bias correction is not required. Achieving this optimal tuning in practice has long been a hurdle for the implementation of these methods. Subject to certain conditions, both approaches can yield estimators that are asymptotically efficient. We show that if all required tuning parameters are defined in terms of an -norm constraint, then these two approaches can be numerically identical even in finite samples. This is a surprising result that may have implications for optimal undersmoothing tuning parameter selection.

In Section 2 we introduce the problem setup, identification assumptions, and common estimation methods; we also review balancing weights and previous results linking balancing weights to outcome regression models. In Section 3 we present our new results, and in Sections 4 and 5 we cache out the implications for and balancing weights specifically. Section 6 gives a numeric illustration. Section 7 gives some implications of our results for the asymptotics of kernel ridge regression. Section 8 discusses the connection with the semiparametrics literature and offers some other directions for future research. The appendix includes extensive additional technical discussion and extensions.

1.1 Related work

Balancing weights and AutoDML.

With deep roots in survey calibration methods and the generalized regression estimator (GREG; see Deville and Särndal, 1992; Lumley et al., 2011; Gao et al., 2022), a large and growing causal inference literature uses balancing weights estimation in place of traditional inverse propensity score weighting (IPW). Ben-Michael et al. (2021b) provide a recent review; we discuss specific examples at length in Section 2.3 below. This approach typically tries to achieve minimax finite-sample balance of features of the covariate distributions in the different treatment groups. Of particular interest here are augmented balancing weights estimators that combine balancing weights with outcome regression; see, for example, Athey et al. (2018); Hirshberg and Wager (2021); Ben-Michael et al. (2021c).

A parallel literature in econometrics instead focuses on so-called automatic estimation of the Riesz representer, of which IPW are a special case, where “automatic” refers to the fact that we can estimate the Riesz representer without obtaining a closed form expression. The corresponding augmented estimation framework is known as Automatic Debiased Machine Learning, or AutoDML; see, among others, Chernozhukov et al. (2022a), Chernozhukov et al. (2022b), Chernozhukov et al. (2022d), and Chernozhukov et al. (2022e). This approach has also been applied in a range of settings, including to corrupted data (Agarwal and Singh, 2021), to dynamic treatment regimes (Chernozhukov et al., 2022c), and to address noncompliance (Singh et al., 2022). As we discuss in Appendix C.3, the AutoDML approach nearly always employs cross-fitting and is typically motivated by asymptotic properties rather than achieving balance in finite samples.

Numerical equivalences for balancing weights.

Many seminal papers highlight connections between weighting approaches, such as balancing weights and IPW, and outcome modeling; see Bruns-Smith and Feller (2022) for discussion. Most relevant are a series of papers that show numerical equivalences between linear regression and (exact) balancing weights, especially Robins et al. (2007); Kline (2011); Chattopadhyay and Zubizarreta (2021), and between kernel ridge regression and forms of kernel weighting (Kallus, 2020; Hirshberg et al., 2019). We discuss these equivalences at length in Appendix A. Finally, as we discuss in Appendix D, there are close connections between balancing weights and Empirical Likelihood (Hellerstein and Imbens, 1999; Newey and Smith, 2004).

2 Problem setup and background

2.1 Setup and motivation

Our paper proves new numeric equivalences for existing estimation procedures, and as such the results hold absent any causal assumptions or statistical model. However, a primary motivation for this work is the task of estimating unobserved counterfactual means in causal inference. We briefly review this setting here and use it as a running example throughout, emphasizing that this is purely for interpretation. We begin with the canonical case of estimating a counterfactual mean under conditional ignorability, and then turn to the more general setup of estimating linear functionals via the Riesz representer.

2.1.1 Warmup: counterfactual means

Let be random variables defined on with joint probability distribution . To begin, consider the example of a binary treatment, and covariates . Define potential or counterfactual outcomes and under assignment to treatment and control, respectively. Under SUTVA (Rubin, 1980), we observe outcomes . To estimate the average treatment effect, , we first estimate the means of the partially observed potential outcomes, and .

Let be the outcome model, be the propensity score, and be the inverse propensity score weights (IPW). Under the additional assumptions of conditional ignorability, , and overlap, , we have that is identified by , a (linear) functional of the observed data distribution. A symmetric argument holds for .

There are three broad strategies for estimating . First, the identifying functional above suggests estimating the outcome model, among those units with , and plugging this into the regression functional, . Second, the equality suggests estimating the inverse propensity score weights, , and plugging these into the weighting functional. Finally, we can combine these two via the doubly robust functional (Robins et al., 1994):

This functional has the attractive property of being equal to even if either one of or is replaced with an arbitrary function of and , hence the term “doubly robust.” See Chernozhukov et al. (2018); Kennedy (2022) for recent overviews of the active literature in causal inference and machine learning focused on estimating versions of this functional.

2.1.2 General linear functionals via the Riesz representer

The setup above used causal assumptions to identify the mean potential outcome as a linear functional of the observed data distribution . A recent literature (e.g., Hirshberg and Wager, 2021; Chernozhukov et al., 2022d) emphasizes that we can generalize this approach to estimate a wide range of linear functionals of the data. In particular, we now let be an arbitrary set and let be a random variable with support . Our goal is to estimate a linear functional of the form:

| (1) |

where is a real-valued, mean-squared continuous linear functional of .

Following Chernozhukov et al. (2022d, e), we can generalize the weighting functional to this general class of estimands via the Riesz representer, which is a function such that, for all square-integrable functions :

| (2) |

To make this more concrete, consider the following three examples.

Example 1 (Counterfactual mean).

Let and Under SUTVA and conditional ignorability, this estimand is equal to . The Riesz representer is the IPW, .

Example 2 (Average derivative).

Let and Under an appropriate generalization of SUTVA and conditional ignorability, this estimand corresponds to the average derivative effect of a continuous treatment. Under regularity conditions the Riesz representer is given by where is the conditional density of given .

Example 3 (Distribution shift).

Consider an example without , following the machine learning literature on covariate shift. Let denote the source distribution of the observed data, and let over denote the target distribution. The estimand is then . In a causal inference setting, this can recover the Average Treatment Effect on the Treated (ATT) under SUTVA and conditional ignorability; i.e., let be the distribution of covariates and outcomes for units assigned to control and be the distribution of the covariates for units assigned to treatment. The Riesz representer is the density ratio, .

As in the counterfactual mean example, we can identify this more general target functional via the outcome model functional in (1), via the Riesz representer functional in (2) with , or via the doubly robust functional

| (3) |

Estimators of this DR functional are augmented in the sense that they augment the “plug-in,” “outcome regression,” or “base learner” estimator with appropriately weighted residuals; or, equivalently, that augment the weighting estimator with an appropriate outcome regression. This is the class of estimators to which our results apply.

2.2 Balancing weights: Background and general form

The balancing weights framework, also known as automatic estimation of the Riesz representer, estimates the Riesz representer directly — rather than estimating it via an analytic functional form, e.g., by estimating the propensity score and inverting it (Ben-Michael et al., 2021b; Chernozhukov et al., 2022d). This approach does not require a known analytic form (Chernozhukov et al., 2022e), is often much more stable (Zubizarreta, 2015), and offers improved control of finite sample covariate imbalance (Zhao, 2019).

Weighting for balance.

A central property of the Riesz representer is that the corresponding weights, , are the unique weights that satisfy the population balance property property in Equation 2 for all square-integrable functions . To see why this rather abstract equality is known as a balance property, consider the case of a missing mean in Example 3: weighting the source population observations with the Riesz representer balances the covariate distributions in the source and target populations by making the source population distribution perfectly match the target population distribution.

We can use this property to characterize as the unique solution to the optimization problem:

| (4) |

where the objective is called the “imbalance.” However, this does not lead to a practical estimator: due to the flexibility of , the inner supremum can behave erratically for .

We make this problem more tractable by imposing simplifying assumptions on the nature of confounding. In particular, for our target estimand we only need to satisfy the condition in Equation 2 for the special case of . If we are willing to assume that lies in a model class , then it suffices to balance functions in that class, and we can replace the objective in (4) with the imbalance over :

| (5) |

Typically, the balancing weights approach also introduces a regularization hyperparameter to ensure a unique minimum and to introduce a bias-variance trade-off. The resulting balancing weights are the unique solution to the following strictly-convex optimization problem (see Appendix D for alternative variants):

| (6) |

If the true conditional expectation , then the imbalance , will be small and thus is an approximately unbiased estimate of . For a more formal statement, see, for example, Hirshberg and Wager (2021).

Direct estimation of the Riesz representer.

Chernozhukov et al. (2022d) consider an alternative motivation for balancing weights: estimating the Riesz representer directly by finding weights that directly minimize the mean-squared error for ,

| (7) |

With the introduction of a hyperparameter (see (8) below), this problem is equivalent to the optimization problem in Equation (6).

2.3 Linear balancing weights

2.3.1 Population balance

In this paper, we consider the special case where the outcome models are linear in some basis expansion of and . This is an extremely broad class that encompasses linear and polynomial models of arbitrary functions of and and with dimension possibly larger than the sample size, as well as non-parametric models such as reproducing kernel Hilbert spaces (RKHSs; Gretton et al., 2012), the Highly-Adaptive Lasso (Benkeser and Van Der Laan, 2016), the neural tangent kernel space of infinite-width neural networks (Jacot et al., 2018), and “honest” random forests (Agarwal et al., 2022). However, this class excludes models for that are fundamentally non-linear in their parameters, like general neural networks or generalized linear models passed through a non-linear link function. We extend our results to arbitrary nonlinear balancing weights in Appendix D.

Define the feature map and let denote the mapping for the th feature. Let where can be any norm on . The general setup constrains ; we set without loss of generality, which simplifies exposition below. Let be the dual norm of ; that is, Many common vector norms have familiar, closed-form, dual norms, e.g., the dual norm of the -norm is the -norm; and the dual norm of the -norm is the -norm.

Under linearity, the imbalance over all has a simple closed form. For any , where is short-hand for the vector with th entry . We can then write the imbalance in terms of the transformed feature space ; following the balancing weights literature, we refer to this quantity as the target features. Applying the linear functional from (1) to the features , we have the following closed form:

For instance, for the missing counterfactual mean in Example 1, . The imbalance is then the difference between the re-weighted features from the whole population, , and the target features with , .

2.3.2 Finite sample balance

Because our results concern numeric equivalences, we will focus on the finite sample version of the linear balancing weights problem. Let be i.i.d. samples from the distribution of the observed data, and denote . Let denote the target features. We will write for sample averages; define and . For exposition, we assume that and that has rank . We emphasize that this is not necessary for our results — one can replace with an infinite-dimensional Hilbert space and relax the rank restriction. See Appendix B for a formal presentation of the high-dimensional setting.

In what follows we write for the vector , to highlight the fact that we will estimate directly rather than as an explicit function of or . Using the derivation above, we can directly calculate the finite sample imbalance as:

Now we can write the balancing weights optimization problem in (6) equivalently as either:

| Penalized form: | |||

| Constrained form: | |||

Furthermore, we can write the equivalent problem in (7) as:

| Automatic form: | (8) |

where we use the terminology “automatic” from Chernozhukov et al. (2022d). For any parameter and corresponding constrained problem solution , there exists a parameter such that , where is the solution to the automatic form. As a result, for any norm , the penalized and constrained forms will always produce weights that are linear in (Ben-Michael et al., 2021b). Without loss of generality, we therefore use to denote the regularization parameter for the balancing weights problem, regardless of the specific form. We now illustrate several common choices for this problem; in Appendix D we discuss popular forms of balancing that constrain the weights to be non-negative.

Example 4 (Exact balancing weights).

The most common balancing weights estimation problem finds the minimum weights that exactly balance each element of . In the constrained form, exact balancing solves

| (9) | |||

Example 5 ( balancing).

The balancing weights problem is usually expressed via its penalized form:

| (10) |

The automatic form is a ridge-penalized regression for the Riesz representer.

Example 6 ( balancing).

The constrained form of the balancing weights problem is

| (11) | |||

The automatic form is a lasso-penalized regression for the Riesz representer, sometimes known as the Minimum Distance Lasso (Chernozhukov et al., 2022d).

Example 7 (Kernel balancing).

As a brief preview of the balancing problem in the infinite-dimensional setting, we provide an example where is a reproducing kernel Hilbert space on with norm and kernel . Then for any , the representer . Using infinite-dimensional matrix notation, we denote and as above. The penalized balancing weights problem for is:

| (12) |

See Appendix B for details and references.

Remark 1 (Intercept).

An important constraint in practice is to normalize the weights, . This corresponds to replacing and with their centered forms, and , in the dual form of the balancing weights problem. This is also equivalent to adding a column of s to . Appropriately accounting for this normalization, however, unnecessarily complicates the notation. Therefore, without loss of generality, we will assume that the features are centered throughout, that is, .

Remark 2 (Equivalence with kernel ridge regression).

For the special case of balancing (e.g., Examples 4, 5, and 7), the balancing weights problem is numerically equivalent to directly estimating the conditional expectation via (kernel) ridge regression and applying the estimated coefficients to . Moreover, the solution to the balancing weights problem has a closed form that is always linear in ; we provide further details in Appendix A. For exact balance with , the balancing weights problem is equivalent to fitting unregularized OLS; see, for example, Robins et al. (2007), Kline (2011), and Chattopadhyay et al. (2020).

3 Novel equivalence results for (augmented) balancing weights and outcome regression models

Our first main result demonstrates that any linear balancing weights estimator is equivalent to applying OLS to the re-weighted features. Our second result provides a novel analysis of augmented balancing weights, demonstrating that augmenting any linear balancing weights estimator with a linear outcome regression estimator is equivalent to a plug-in estimator of a new linear model with coefficients that are a weighted combination of estimated OLS coefficients and the coefficients of the original linear outcome model.

3.1 Weighting alone

Our first result is that estimating with any linear balancing weights is equivalent to fitting OLS for the regression of on and then applying those coefficients to the re-weighted target feature profile. The key idea for this result begins with the simple unregularized regression prediction for , .

Proposition 3.1.

Let , , be any linear balancing weights, with corresponding weighted features . Let be the OLS coefficients of the regression of on . Then:

where is the mean feature shift implied by the balancing weights and where superscript indicates possible dependence on a hyperparameter. We have assumed without loss of generality that , but we sometimes use notation to demonstrate the role of mean feature shift in various expressions.

Note that here we have written the OLS coefficients using the pseudo-inverse . For clarity in the main text, we focus on the full rank setting, where ; we provide a proof for the general setting in Section B.3. In Appendix D, we extend Proposition 3.1 to non-linear balancing weights, including those wiht a non-negativity constraint.

We can interpret this result via a contrast with standard regularization. Regularized regression models navigate a bias-variance trade-off by regularizing estimated coefficients relative to , leading to . The balancing weights approach instead keeps fixed and regularizes the target feature distribution by penalizing the implied feature shift, .

We emphasize that this a new and quite general result. As we discuss in Appendix A, it has been shown previously that for exact balancing weights, . However, Proposition 3.1 holds for any weights of the form with arbitrary . In Sections 4 and 5, we consider the particular form of for and balancing, respectively.

3.2 Augmented balancing weights

We can immediately extend this to augmented balancing weights, which regularize both the coefficients and the feature shift. Let be the coefficients of any regularized linear model for the relationship between and , where the superscript indicates dependence on a hyperparameter (e.g., estimated by regularized least squares). We consider augmenting with using the doubly robust functional representation in Equation (3). The augmented estimator is:

| (13) |

If the weighting model and outcome model have different bases, our result applies to a shared basis by either combining the dictionaries as in Chernozhukov et al. (2022d) or by applying an appropriate projection as in Hirshberg and Wager (2021). Many recently proposed estimators have this form; see e.g., Athey et al. (2018); Ben-Michael et al. (2021b).

We apply Proposition 3.1 to the first term of the right-hand side of (13) to yield the following result. As this result is purely numerical, it applies to arbitrary vectors , but substantively we think of as the estimated coefficients from an outcome model.

Proposition 3.2.

For any , and any linear balancing weights estimator with estimated coefficients , and with and , the resulting augmented estimator

where the th element of is:

where is the observed mean feature shift for feature ; and is the feature shift for feature implied by the balancing weights model. Finally, when the covariance matrix is diagonal, , with .

This is our central numerical result for augmented balancing weights: when both the outcome and weighting models are linear, the augmented estimator is equivalent to a linear model applied to the target features , with coefficients that are element-wise affine combinations of the base learner coefficients, , and the coefficients from an OLS regression of on . (The coefficients are additionally convex combinations of and when the covariance matrix is diagonal.) In Sections 4 and 5 below, we analyze some of the properties of the augmented estimator for and balancing weights problems respectively.

The regularization parameter for the balancing weights problem, , parameterizes the path between and . As the balancing weights problem prioritizes minimizing balance over controlling variance, and for all . (Recall that we assume for all . Thus, and . So is equivalent to .) In this case, , and the weights fully “de-bias” the original outcome model by recovering unregularized regression, . In Section 6, we will see that when chosen by cross-validation, often equals exactly in applied problems. In these settings, even when is a sophisticated regularized estimator, e.g., based on an elastic net regression, the final augmented point estimate is nonetheless numerically equivalent to the simple OLS plug-in estimate. Conversely, as , the balancing weights problem prioritizes controlling variance, leading to uniform weights and . In this case, , the weighting model does very little, and .

Remark 3 (Sample splitting).

Sample splitting is a common technique in the AutoDML literature especially, in which we only apply the outcome and weighting models to data points not used for estimation; see, for example, Newey and Robins (2018); Chernozhukov et al. (2022d). Since Proposition 3.2 holds for arbitrary vectors and , the results still hold under cross-fitting. See Appendix C for an extended discussion.

Remark 4 (Infinite dimensional setting).

While we emphasize the linear, low-dimensional setting where is invertible, Proposition 3.2 holds far more broadly. The result remains true when the function class is a subset of any Hilbert space. This includes the high dimensional setting where and the infinite dimensional setting. See Appendix B for a formal statement.

Finally, we briefly review two edge cases, before turning to new results for and balancing.

OLS outcome model.

Consider the special case of fitting an unregularized linear regression outcome model, i.e., . Then Proposition 3.2 reproduces the result, originally due to Robins et al. (2007), that “OLS is doubly robust” (see also Kline, 2011). This is because for arbitrary linear weights . Thus, OLS augmented by linear balancing weights collapses to OLS alone. Equivalently, we can view OLS alone as an augmented estimator that combines a linear regression outcome model with linear balancing weights.

Exact balancing weights.

A similar result holds for unregularized balancing weights, i.e., exact balancing weights. Let be the solution to a balancing weights problem in Section 2.3 with hyperparameter , and let be arbitrary coefficients. Then from the balance condition, , for all , and we have that . Thus, the augmented exact balancing weights estimator also collapses to the OLS regression estimator. Equivalently, the augmented exact balancing weights estimator collapses to the unaugmented exact balancing weights estimator. Zhao and Percival (2017) use a very similar result to argue that entropy balancing, a form of exact balancing weights, is doubly robust.

Because many common augmented balancing weights estimators collapse to OLS alone when the hyperparameter tuning procedure (e.g., cross-validation) selects , we often observe this collapsing behavior even if the balancing weights model is a generic regularized regression model. Indeed, this idea often underpins the theoretical justification of plug-in estimators based on sieve/series methods (Newey, 1994), which are implemented via standard OLS or maximum likelihood.

4 Augmented Balancing Weights

In this section, we study balancing weights estimators, which are commonly used in the context of kernel balancing (Gretton et al., 2012; Hirshberg et al., 2019; Kallus, 2020; Ben-Michael et al., 2021a) and for panel data methods (Abadie et al., 2010; Ben-Michael et al., 2021c). We first show that the regularization path from Proposition 3.2 follows typical ridge regression shrinkage, with a smooth decay. Moreover, augmenting with balancing weights is equivalent to boosting with ridge regression, and always overfits relative to the unaugmented outcome model alone. We then show that when the outcome model used to augment balancing weights is itself a ridge regression (which we refer to as “double ridge”), the augmented estimator is itself equivalent to a single, generalized ridge regression, albeit undersmoothed relative to the base learner. These results extend immediately to the RKHS setting of “double kernel ridge” estimation, combining kernel balancing weights and kernel ridge regression. In Section 7, we show the implications of these numeric results for undersmoothing in the statistical sense.

While the following results hold for arbitrary covariance matrices, in the main text we simplify the presentation by assuming that is diagonal; that is, , with . We show that this is without loss of generality for balancing in Appendix E.

4.1 General linear outcome model

Following Remark 2 above, balancing weights, including kernel balancing weights, have a closed form that is always linear in . Our next result applies this closed form to Proposition 3.2 to derive the regularization path that results from augmenting an arbitrary linear outcome model with balancing weights. Although this is an immediate consequence of Proposition 3.2, the resulting form of the augmented estimator has unique structure that warrants a new result.

Proposition 4.1.

Let be (penalized) linear balancing weights with regularization parameter and . Then Therefore, the augmented balancing weights estimator with outcome model has the form

where the coefficient of is given by

| (14) | ||||

In this case, the are exactly equal to the standard regularization path of ridge regression. To see this, recall that ridge regression with penalty shrinks the coefficients as follows:

| (15) |

This is identical to the expression in (14) but with set to : Ridge regression shrinks towards with regularization path , while augmenting shrinks towards with the same regularization path.

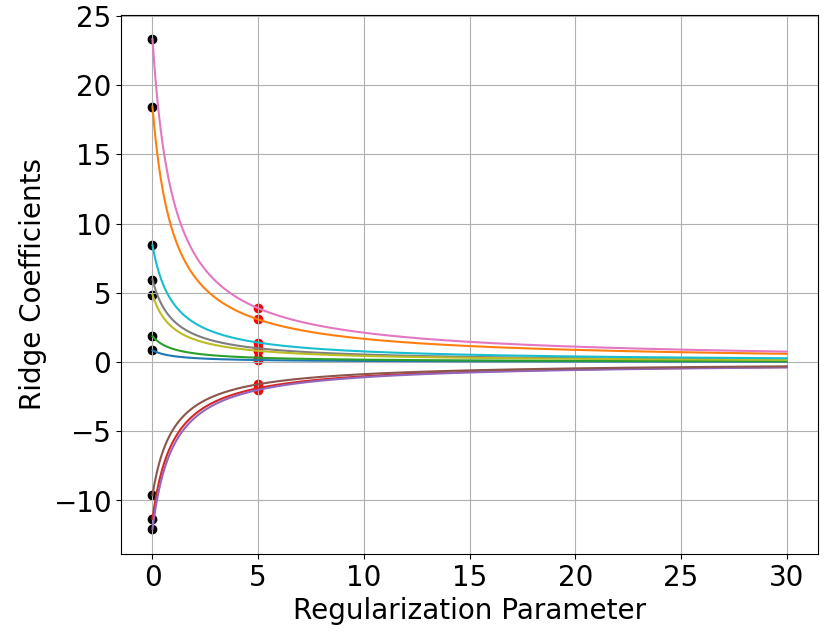

As an illustration, the right panel of Figure 1 shows (on the y-axis) for ten covariates, with increasing from (on the x-axis). The dots on the left pick out ; when , then and . The limit on the right shows . The smooth regularization path is characteristic of ridge regression shrinkage.

We can also view as the output of a single iteration of a ridge boosting procedure, fit using and alone. See Bühlmann and Yu (2003) and Park et al. (2009) for detailed discussion; Newey et al. (2004) makes a similar connection in the context of twicing kernels.

Proposition 4.2.

Let be the residuals from the base learner. Let be the coefficients from the ridge regression of on with hyperparameter . Then, and

So for a fixed , the augmented balancing estimator is equivalent to estimating a new outcome model that overfits relative to (in the sense of having smaller in-sample training error), and then applying that model to .

Surprisingly — and in contrast to the general result in Proposition 3.2 — the augmented coefficients are the same for every target covariate profile . To see this, note that Proposition 4.1 shows that balancing weights are always linear in . Therefore, the corresponding regularization path does not depend on the target profile ; it depends only on and the source distribution variances . This property is closely related to universal adaptability in the computer science literature on multi-group fairness (Kim et al., 2022b). The particular may nonetheless impact the choice of in hyperparameter selection, e.g., via cross-validating imbalance, which in turn influences the degree of overfitting; see Section 7.

4.2 Ridge regression outcome model

Proposition 4.1 holds for arbitrary linear outcome models ; we now state the corresponding result for a “double ridge” estimator, where the base learner outcome model is itself fit via ridge regression. The key takeaway is that the implied augmented coefficients are undersmoothed relative to the base learner ridge coefficients.

For this section, we will consider the following generalized ridge regression, sometimes known as “adaptive” ridge regression (Grandvalet, 1998). Let be a diagonal matrix with th diagonal entry . Then the generalized ridge coefficients are:

Standard ridge regression is the special case where the all take the same value and so . As above, the generalized ridge coefficients can be rewritten as shrinking the OLS coefficients:

| (16) |

We now demonstrate that the augmented balancing weights estimator with base learner is equivalent to a plug-in estimator using generalized ridge with smaller hyperparameters, , where is a diagonal matrix with th diagonal entry .

Proposition 4.3.

Let denote the coefficients of a generalized ridge regression of on with hyperparameters , and let denote balancing weights with hyperparameter defined in Section 2.3. Define the diagonal matrix with th diagonal entry:

Then:

Furthermore, are standard ridge regression coefficients (i.e., is a constant for all ) when and for all .

The same result holds for kernel ridge regression; see Section B.4.

In this setting, augmenting with balancing weights is equivalent to undersmoothing the original outcome model fit. In particular, we can use the expansion in Equation 16 to see the undersmoothing in explicitly:

where the first term is the shrinkage from the original generalized ridge model alone, and the second term is due to augmenting with balancing weights. Importantly, the second term is in and therefore partially reverses the shrinkage of the original estimate. In Section 7, we connect this to undersmoothing in the statistical sense.

5 Augmented balancing weights

In this section, we study balancing weights estimators, which are widely used in the balancing weights literature (Zubizarreta, 2015; Athey et al., 2018) and in the AutoDML literature (Chernozhukov et al., 2022d). In the main text, we consider the special case where the covariance matrix is diagonal; that is, , with . Unlike with balancing, this is no longer without loss of generality. We discuss this general case in Section E.3.

For diagonal covariance, we first show that balancing has a closed form: it is equivalent to applying a soft-thresholding operator to the feature shift from to . We then write the resulting augmented estimator as applying coefficients to and show that is a sparse, element-wise convex combination of the base learner coefficients and OLS coefficients. When the outcome model is also fit via the lasso, we use the resulting representation to demonstrate a familiar “double selection” phenomenon (Belloni et al., 2014), where inherits the non-zero coefficients of both the base learner and the weighting model. This is a form of undersmoothing in the “norm,” in the sense that always has at least as many non-zero coefficients as the base learner, .

5.1 Weighting alone

We first define the soft-thresholding operator and show that the balancing problem has a closed form solution.

Definition (Soft-thresholding operator).

For , define the soft-thresholding operator,

Proposition 5.1 ( Balancing).

If is diagonal, the solution to the optimization problem (11) is:

where , where we include (equal to by assumption) to emphasize the dependence on feature shift, and with corresponding reweighted features, .

For intuition, compare the (un-augmented) balancing weights estimator to the lasso coefficients (Hastie et al., 2009):

where we simplify here to emphasize the connections between the methods. Whereas lasso performs soft-thresholding on the OLS coefficients (regularizing the outcome regression), balancing performs soft-thresholding on the implied feature shift to the target features.

5.2 General linear outcome model

We can then plug the closed-form solution for the weights into Proposition 3.2.

Proposition 5.2.

Let be defined as above. Then the augmented balancing weights estimator with outcome model fit has the form,

where the coefficient of equals:

where .

The augmented coefficients are an element-wise convex combination of and . For features where the mean feature shift is small (relative to ), is equivalent to the base learner coefficient . The remaining coefficients are interpolated linearly toward the coefficients.

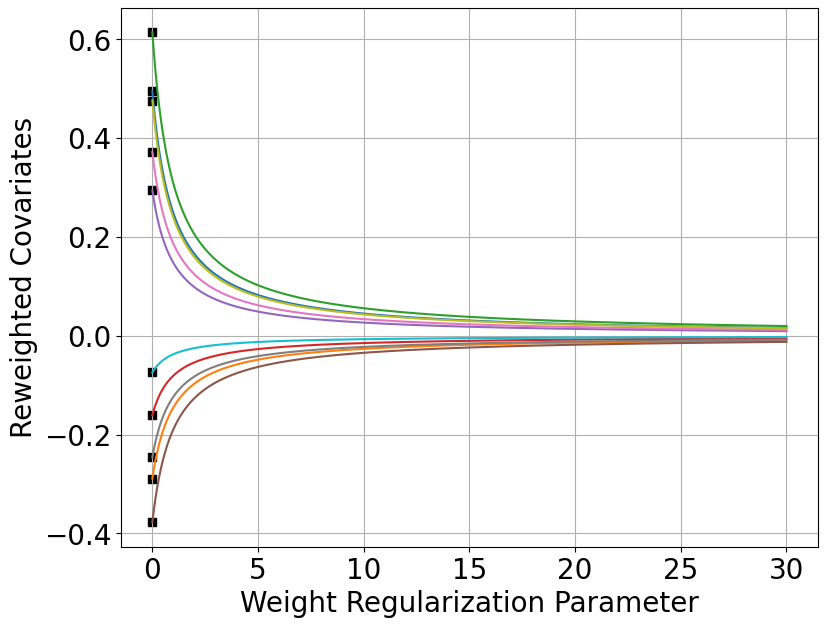

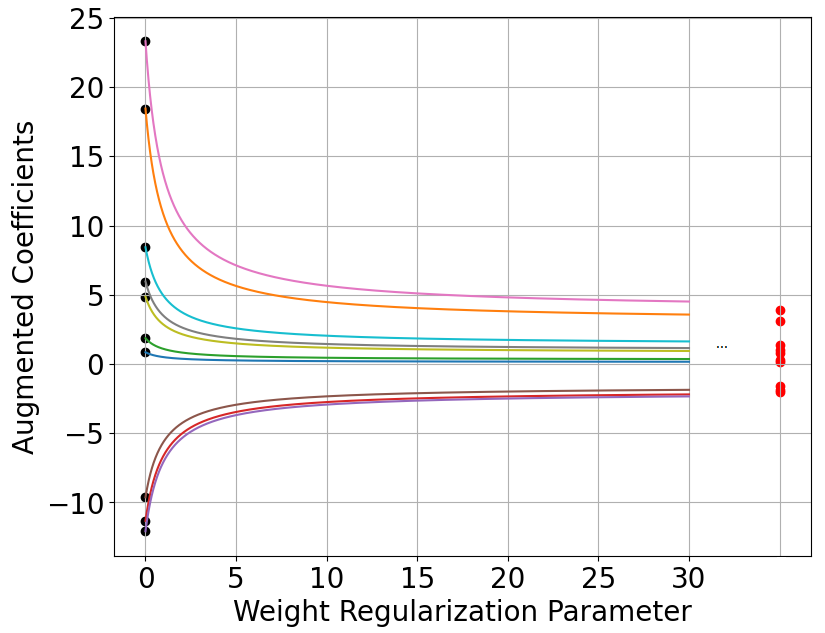

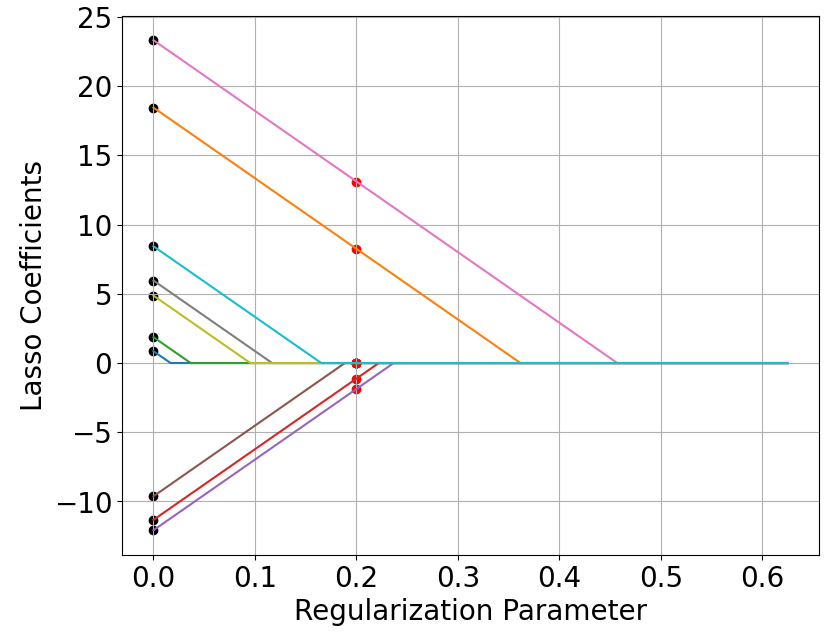

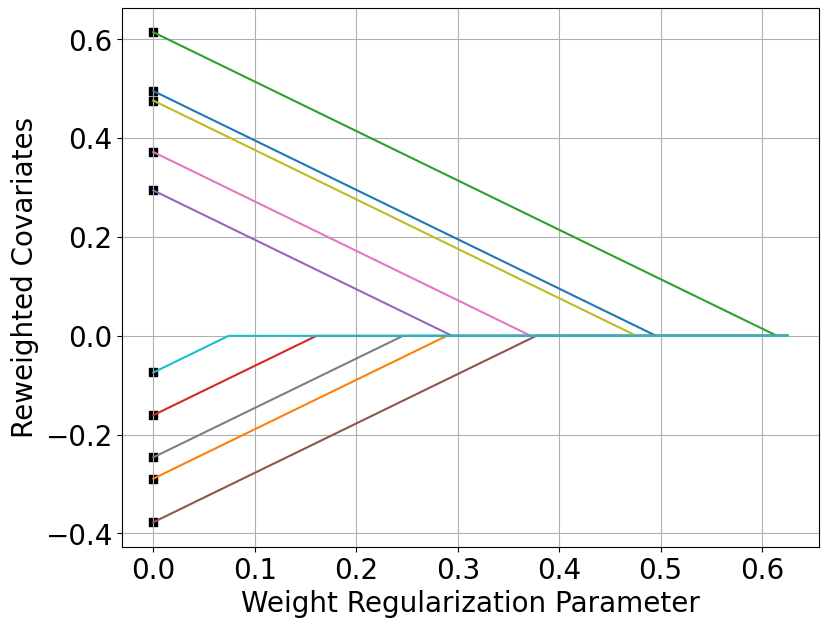

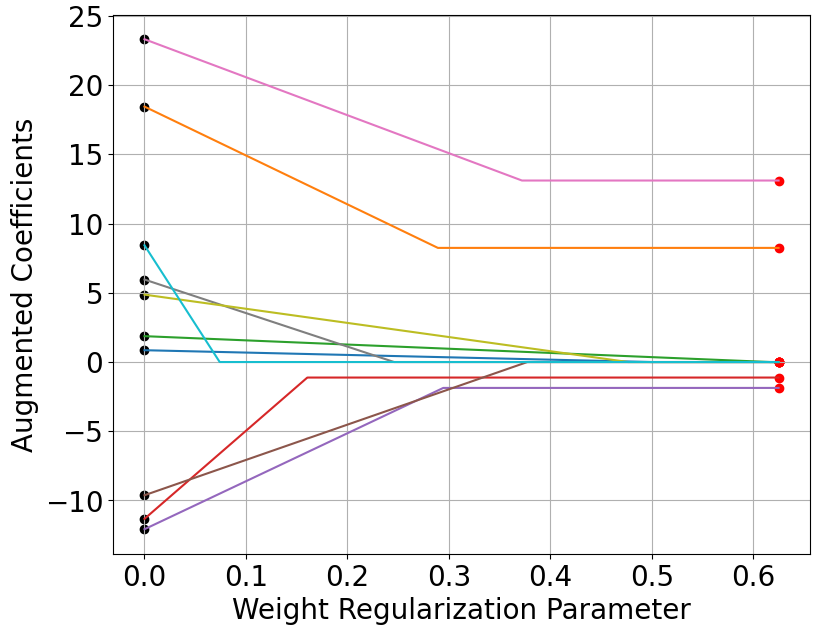

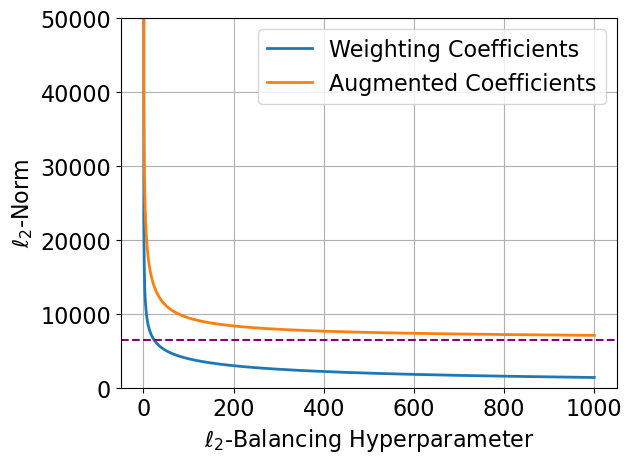

Figure 2 summarizes these results and their implications for the augmented estimator. As with Figure 1, we generate simple simulated data with . In the left panel, we plot the coefficients from lasso regression of on as a function of the lasso regularization parameter. The regularization path begins with the black dots, which represent the OLS coefficients. Each lasso coefficient (represented by a colored line) then shrinks linearly to exactly zero, due to the soft-thresholding operator. The middle panel plots the reweighted covariates using balancing weights between and solved in the constrained form. The black dots represent , corresponding to exact balance. Then as the weight regularization parameter increases, the reweighted covariates shrink linearly to exactly zero, just as in lasso. The right panel plots coefficients for the augmented estimator that combines a baseline outcome model fit with balancing weights. The lines correspond to as defined in Proposition 5.2. The regularization path begins at the black dots, where , and eventually converges to , showing the usual soft-thresholding behavior. The order at which the coefficients go to zero reflects the size of , because the regularization path depends on the weight coefficients from the middle panel. Thus, the augmented estimator shrinks toward but via a soft-thresholding operator applied to the feature shift, .

5.3 Lasso outcome model

In the case where is itself fit via lasso, as studied in Chernozhukov et al. (2022d), then we recover a familiar double selection phenomenon (Belloni et al., 2014).

Proposition 5.3 (Double Selection).

Let denote the coefficients of lasso regression of on with regularization parameter . Denote the indices of the non-zero coefficients as . Let be balancing weights with parameter as in Proposition 5.1. Let denote the non-zero entries of the reweighted covariates . Assume that is dense. Then the indices of the non-zero entries of the augmented coefficients are

The lasso coefficients have a sparsity pattern generated by soft-thresholding the OLS coefficients. The augmented estimator then shrinks from OLS toward by soft-thresholding the implied feature shift to the target features. As a result, wherever the lasso coefficients are non-zero or the weight coefficients are non-zero, the final augmented coefficients are also non-zero. The “included coefficients” for the final estimator are then the union of the coefficients included in either individual model. Therefore, augmenting a lasso outcome model with balancing also exhibits a form of undersmoothing in the “norm”, , in the sense that there are always at least as many non-zero coefficients as for the unaugmented lasso outcome model. However, this will not correspond to undersmoothing the base learner in the traditional sense, because in general there will not exist a lasso hyperparameter that will produce sparsity pattern .

6 Numerical illustrations

We now illustrate these findings through several real-data examples. Following Chernozhukov et al. (2022d), we focus on the canonical LaLonde (1986) data set evaluating a job training program in the National Supported Work (NSW) Demonstration. The primary outcome of interest is annual earnings in 1978 dollars.

For these illustrations, we focus on estimating the Average Treatment Effect on the Treated (ATT), . We recover the missing conditional mean using the setup from Example 3, where the source and target populations are the control and treated units respectively. Thus and correspond to the feature expansion applied to the covariates in the control group and treated group respectively. We consider two different features expansions of the original covariates: (1) a “short” set of 11 covariates used in Dehejia and Wahba (1999);111These are: age, years of education, Black indicator, Hispanic indicator, married indicator, 1974 earnings, 1975 earnings, age squared, years of education squared, 1974 earnings squared, and 1975 earnings squared. and (2) an expanded, “long” set of 171 interacted features used in Farrell (2015).

For the “short” feature set, we show that off-the-shelf augmented balancing weight estimators indeed collapse to simple OLS: for both ridge-augmented balancing and lasso-augmented balancing, choosing the optimal hyperparameters via cross-validation leads to estimators that are equivalent to OLS. For the expanded feature set, these estimators no longer collapse to OLS. Instead, we show how these estimators undersmooth in practice. For the special case of double ridge, we show that this is equivalent to undersmoothing the hyperparameter in a single ridge regression. We assess the sensitivity of these numerical results to cross-fitting in Section F.2. See Appendix F for dataset summaries and corroborating results from the Infant Health Development Program (IHDP).

6.1 Low-dimensional setting

We begin by applying lasso-augmented balancing weights (“double lasso”) to the short version of the LaLonde (1986) data set with 11 features. The key takeaway is that the resulting estimate collapses to a simple OLS regression, even though the base learner lasso outcome model is heavily regularized. This finding repeats in a variety of low-dimensional settings. Additional results in Section F.3 show the same pattern on Lalonde with balancing weights, as well as in a re-analysis of the “low-dimensional” IHDP data set with both and augmented balancing weights.

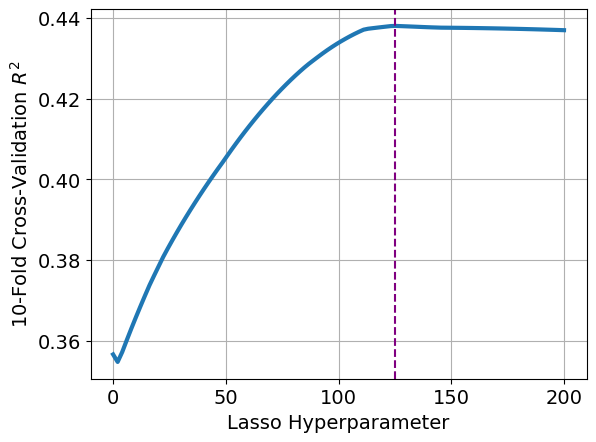

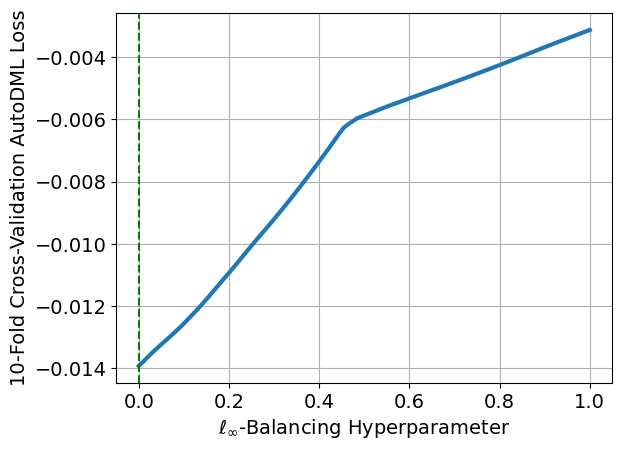

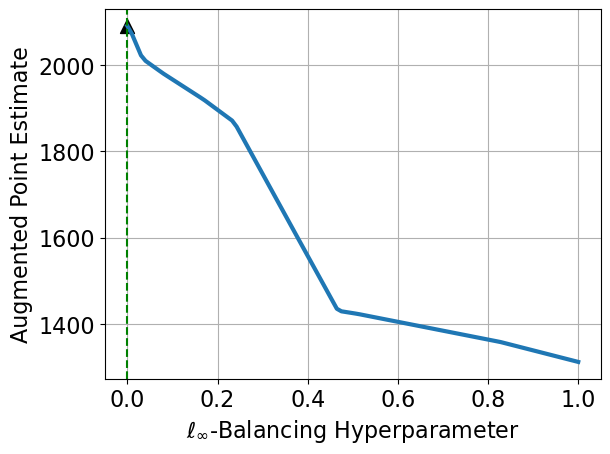

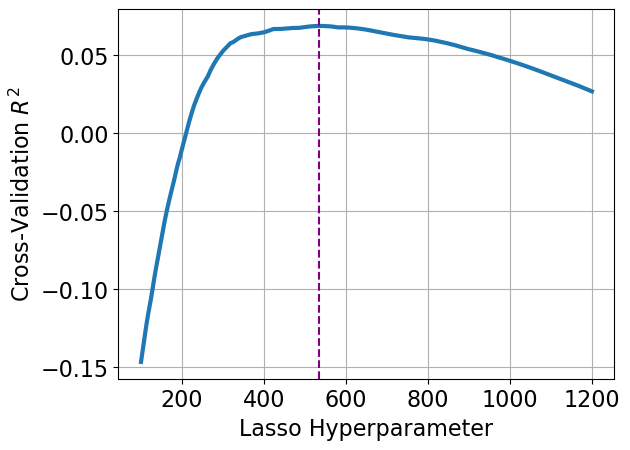

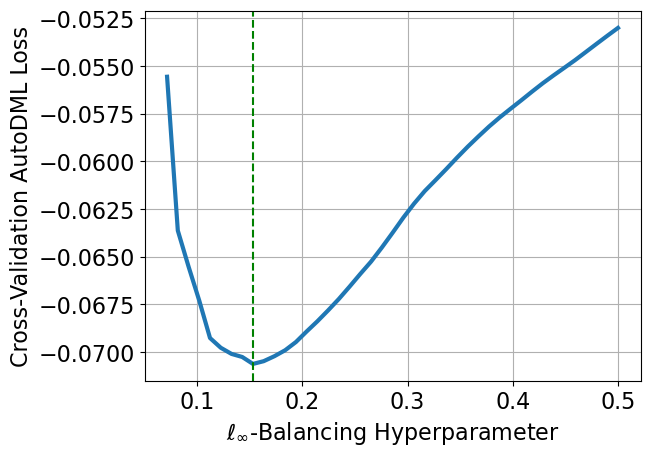

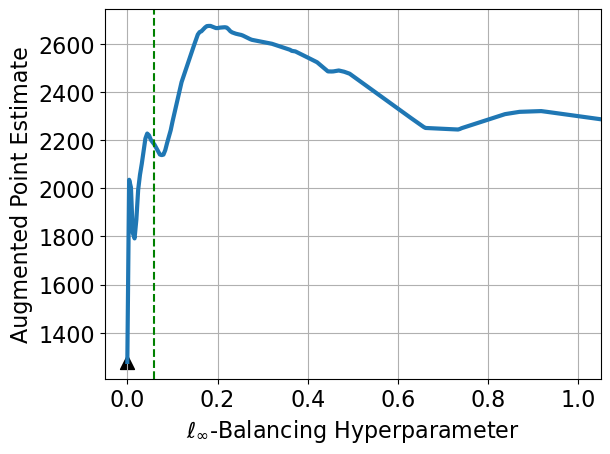

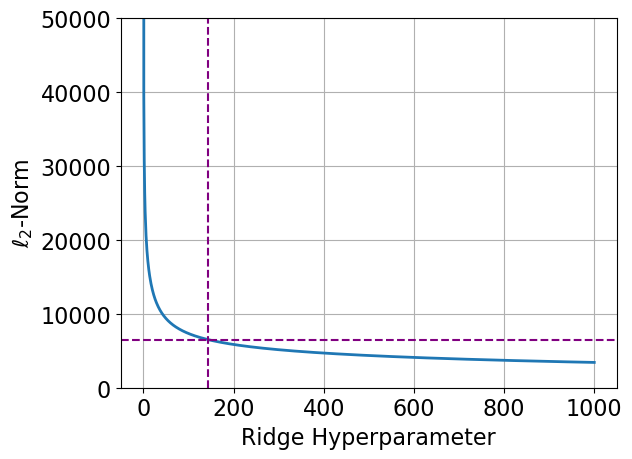

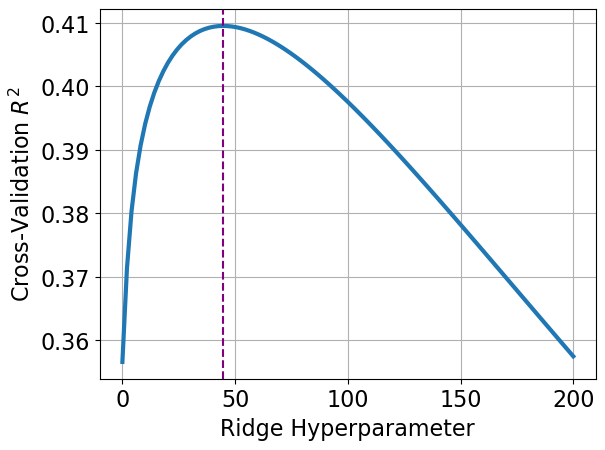

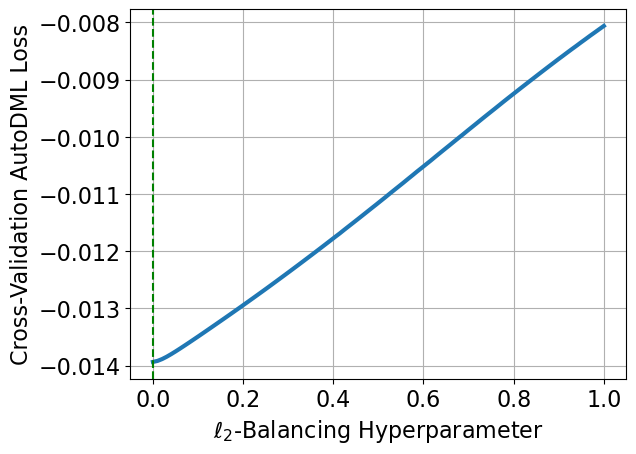

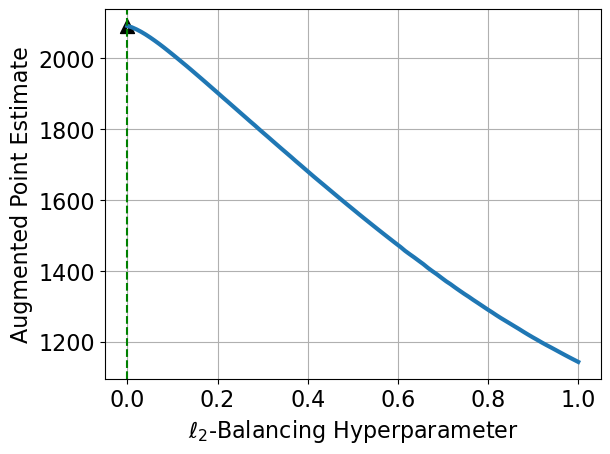

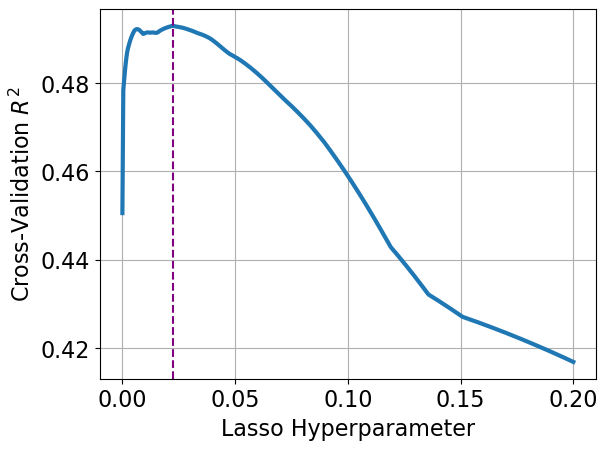

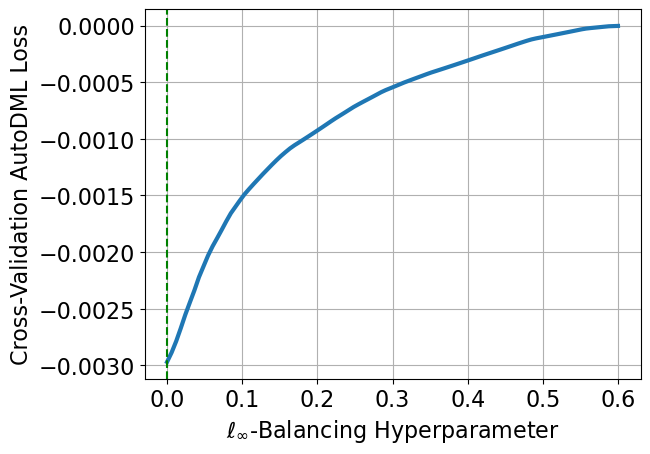

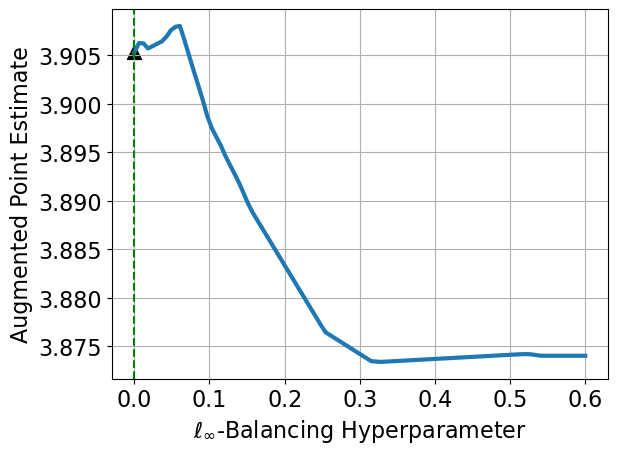

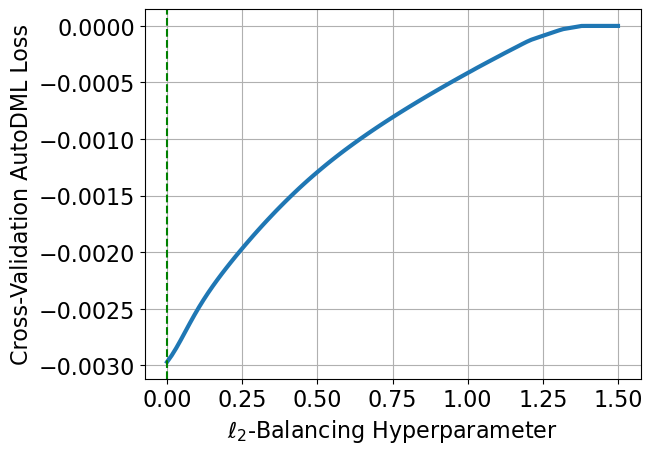

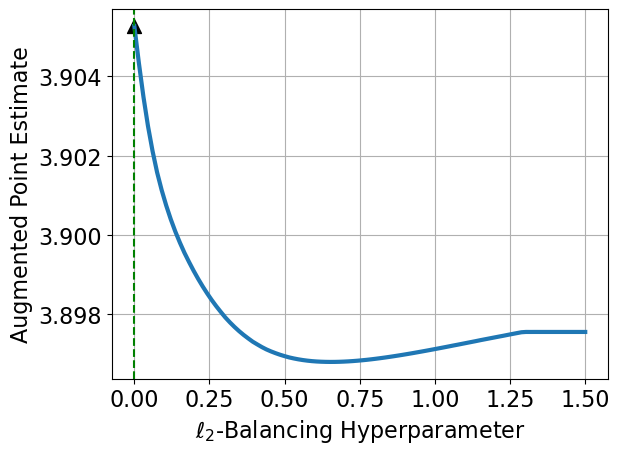

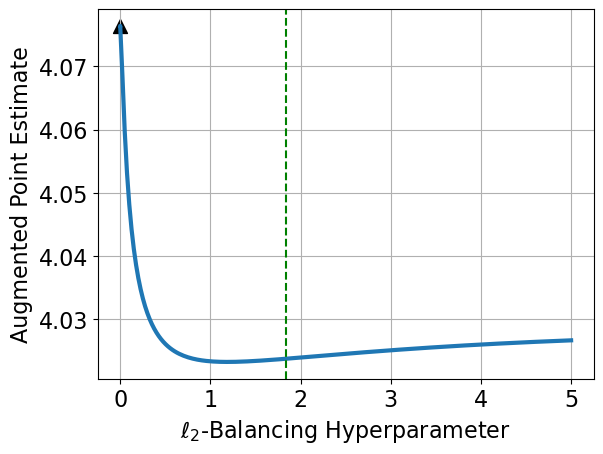

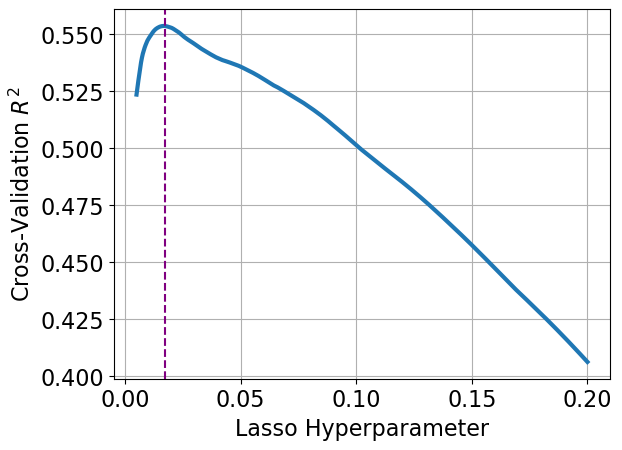

Figures 3(a) and 3(b) show the cross-validation curves for the outcome and weighting models, respectively. For the outcome model, ten-fold cross-validation chooses a non-zero value for the lasso hyperparameter (purple dotted line) resulting in a sparse model. For the weighting model, however, cross-validation on the automatic form loss function (8) selects the hyperparameter , which is equivalent to exact balance.

Figure 3(c) shows the point estimate as a function of the weighting hyperparamter , holding the outcome model hyperparameter fixed; the black triangle represents the OLS plug-in point estimate. For context, the corresponding experimental estimate is $1,794 (see Dehejia and Wahba, 1999). Because cross-validation chooses , the weights achieve exact balance, and . In short, because the bias-variance trade-off for the weights prefers exact balance, the entire estimator collapses to the simple OLS plug-in estimate, even though our base learner is a highly regularized sparse model.

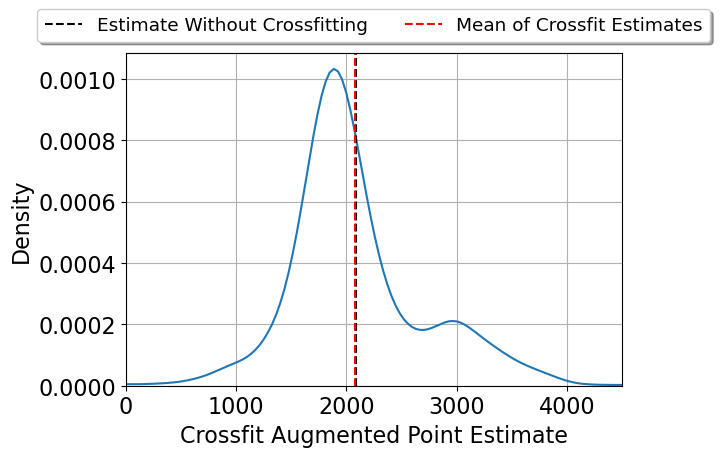

Some augmented balancing weights procedures, including Chernozhukov et al. (2018), additionally implement sample splitting and cross-fitting. We repeat the numerical experiments in the low-dimensional setting with 5-fold cross-fitting and find that on average (over draws of folds) the estimate is essentially identical to the OLS plug-in estimate, but the distribution is skewed and displays substantial variation. See Section F.2 for a summary of the results.

6.2 High-dimensional setting

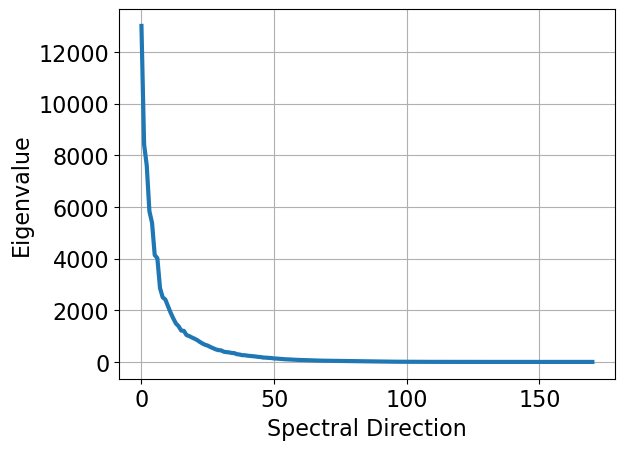

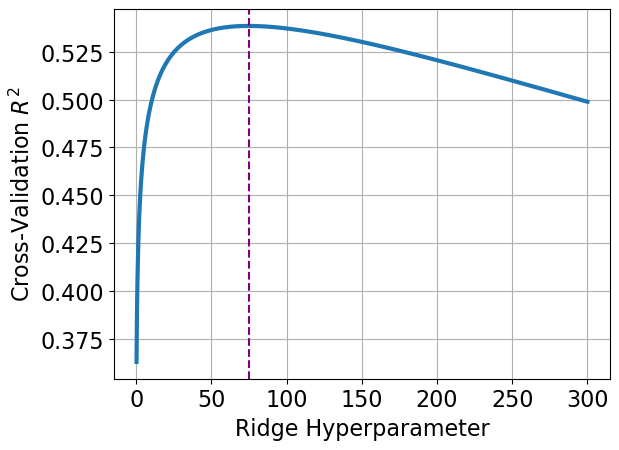

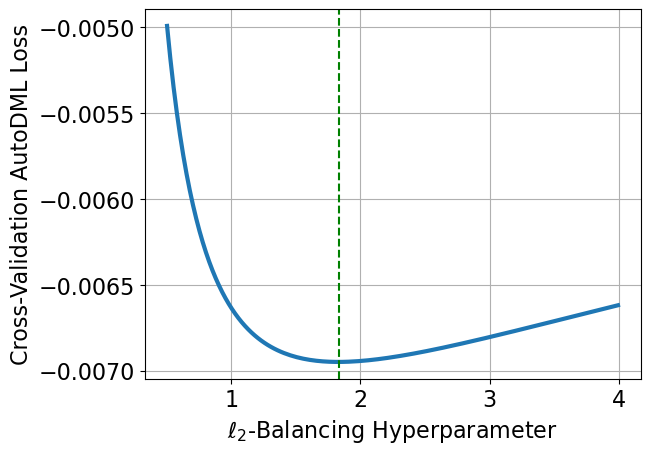

We next consider the expanded set of 171 features for LaLonde (1986) used in Farrell (2015). To simplify exposition, we first run a pre-processing step for this expanded feature set using the eigenvectors of to decorrelate the features; as we discuss above, this is without loss of generality for balancing but not for balancing.

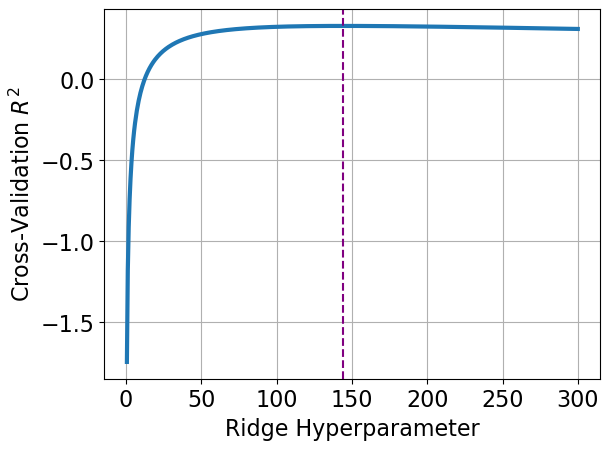

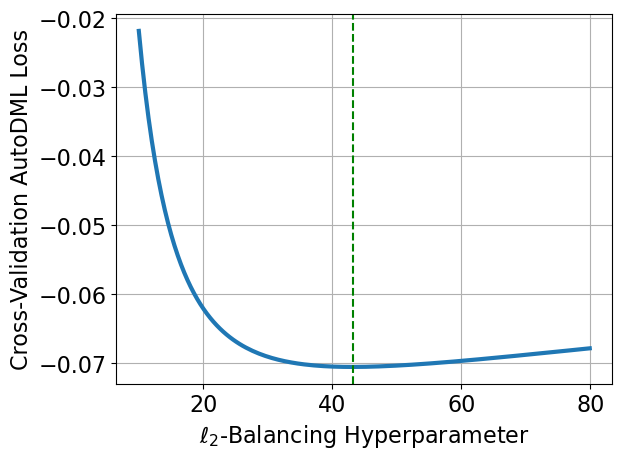

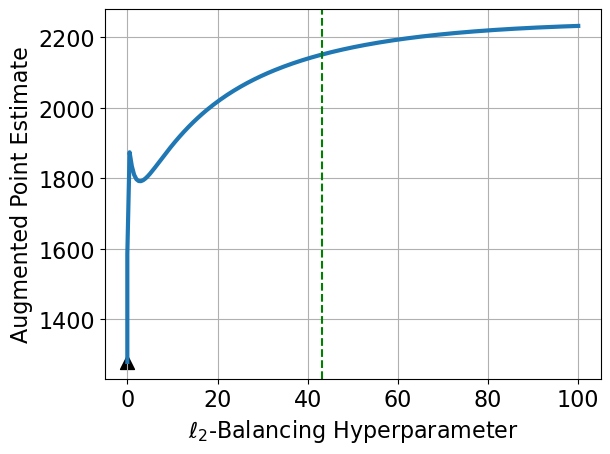

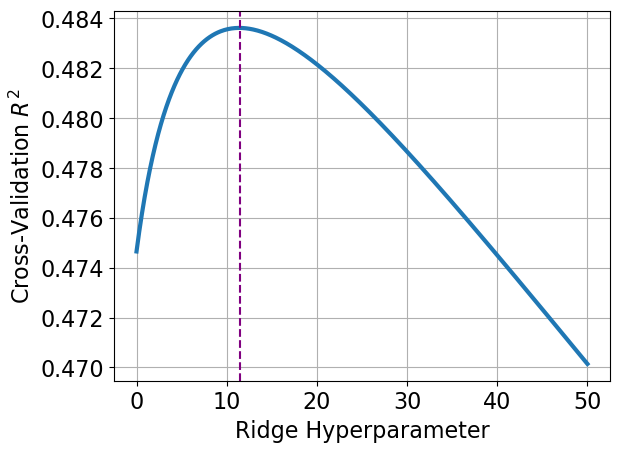

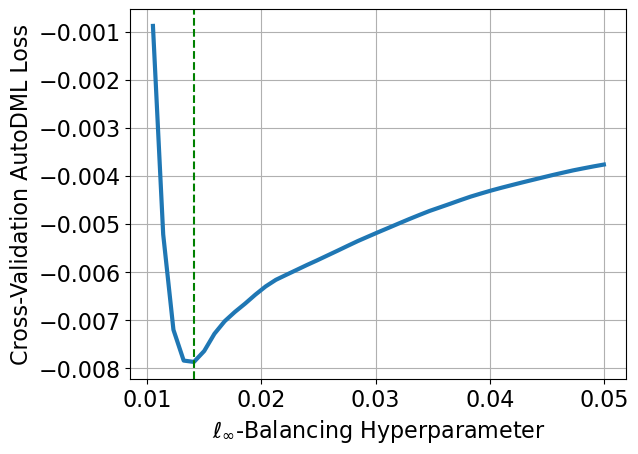

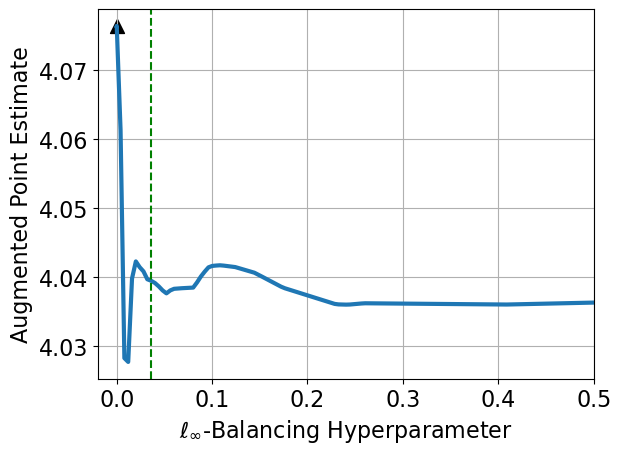

Figure 4 shows estimates for ridge-augmented balancing (top row) and lasso-augmented balancing (bottom row). The left two panels of each row show the cross-validation curves for the outcome regression and balancing weights, respectively. Unlike in the low-dimensional setting, the CV-optimal hyperparameter is non-zero for all of these models. As a result, the final augmented estimates shown on the right — where the dotted green lines and blue lines intersect in Figure 4(c) and Figure 4(f) — are not equivalent to OLS.

6.2.1 Undersmoothing for double ridge

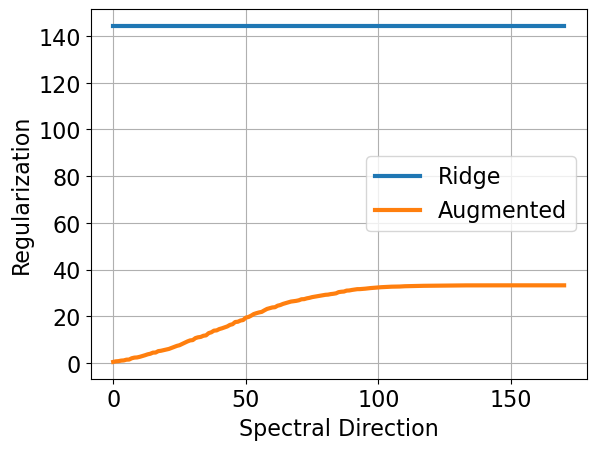

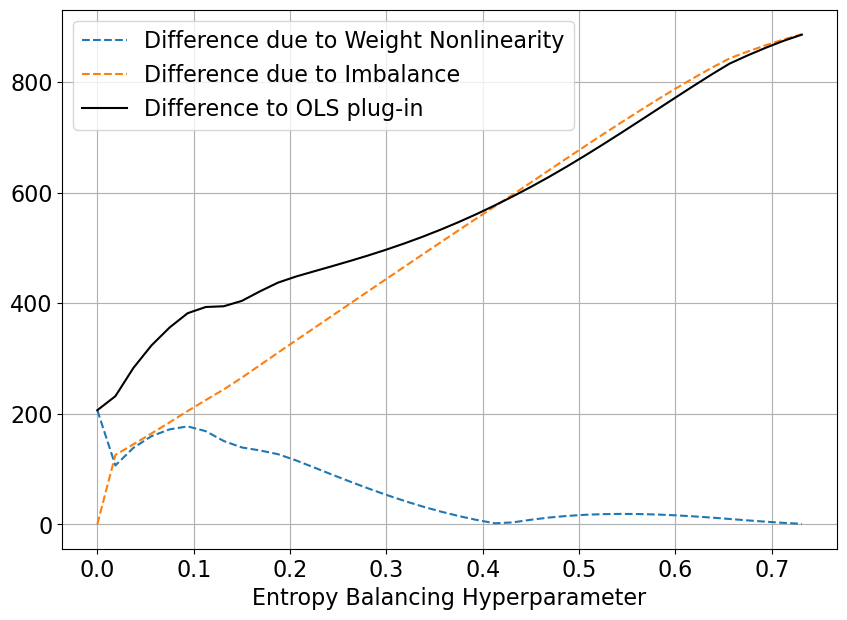

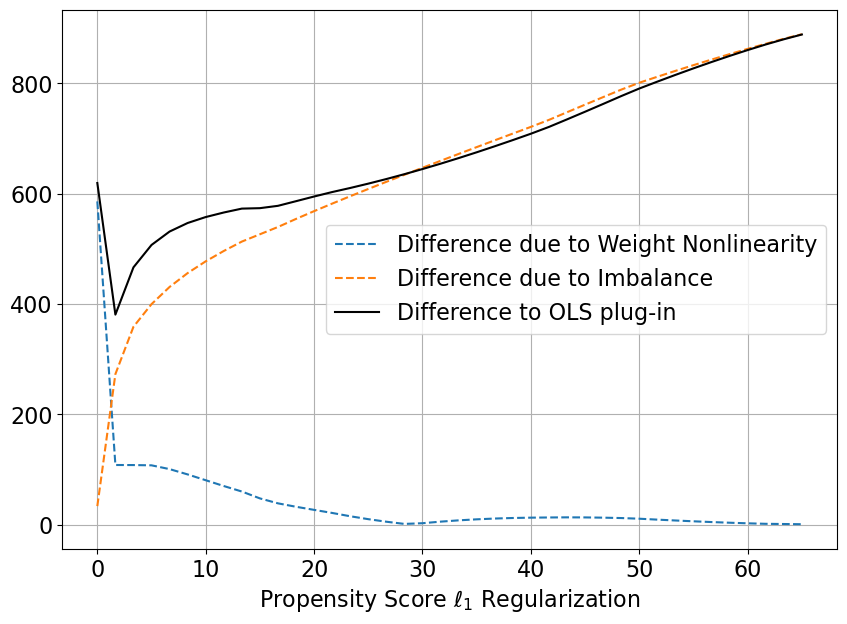

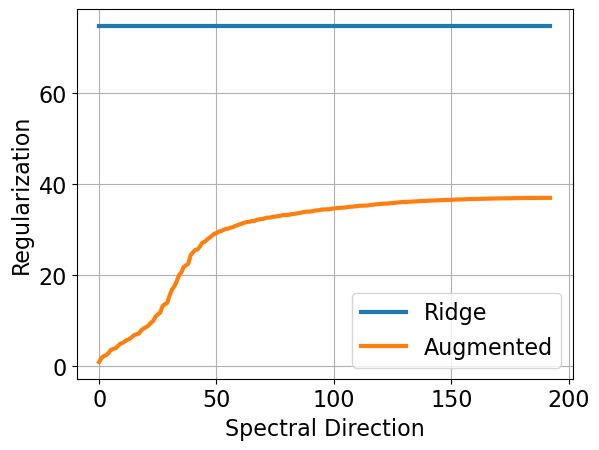

For the special case of double ridge, we now illustrate our result from Proposition 4.3 that balancing weights produce a new outcome model that is undersmoothed relative to the original ridge regression model. Recall that when the base learner is a generalized ridge model with parameters , then the augmented estimator is equivalent to plugging in a generalized ridge models with parameters . In this example, the are all equal to the same value (chosen via cross-validation), indicated by the purple dotted line in Figure 4(a). We compute the corresponding for chosen by cross-validation, indicated by the green dotted line in Figure 4(b).

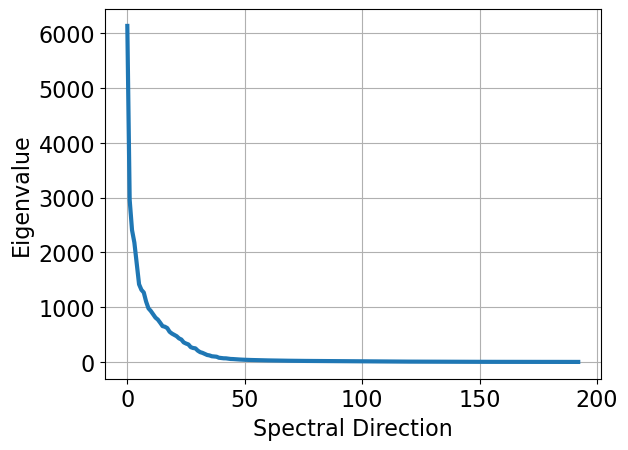

Figure 5(a) plots the and , with on the -axis sorted in the order of the eigenvalues of from largest to smallest. Figure 5(b) plots the corresponding eigenvalues. For standard ridge regression, the key idea is to push the eigenvalues of away from zero so that the resulting matrix is invertible and well-conditioned. Thus, the original ridge regression applies the same amount of regularization across the spectrum, as shown by the blue line in Figure 5(a). By contrast, the implied outcome model from the augmented procedure uses far less regularization and is substantially undersmoothed. Importantly, the augmented estimator undersmooths more where the eigenvalues of are large and undersmooths less where the eigenvalues of are close to zero. The augmented estimator therefore avoids bias by only regularizing the spectral directions that are the most significant sources of variation — and even these to a much smaller degree than is optimal for MSE predictions.

6.2.2 Undersmoothing in norm

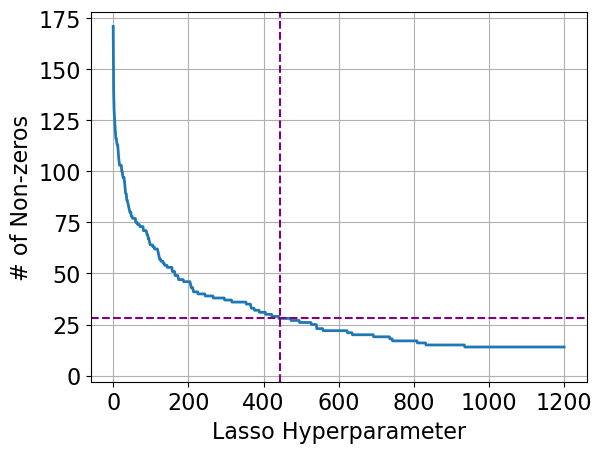

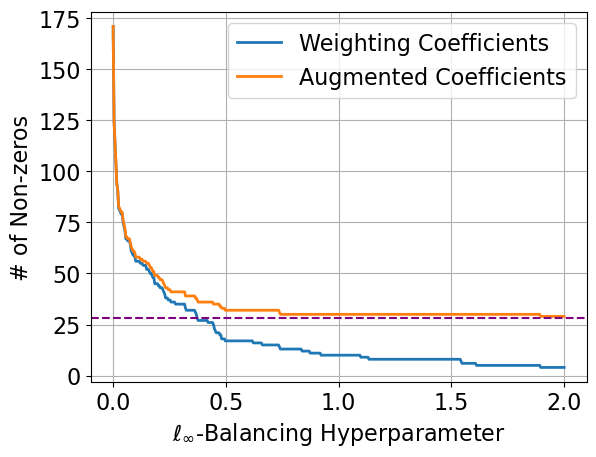

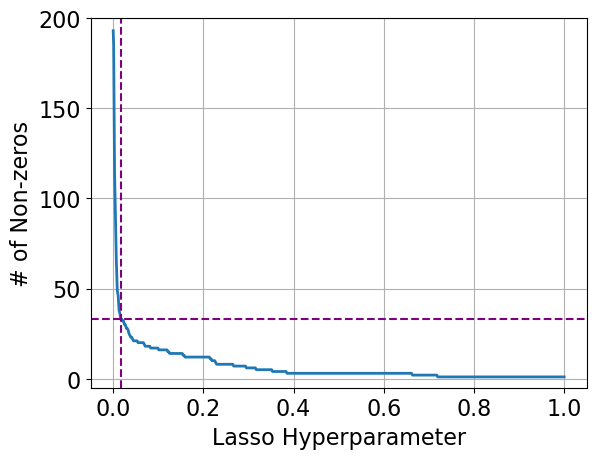

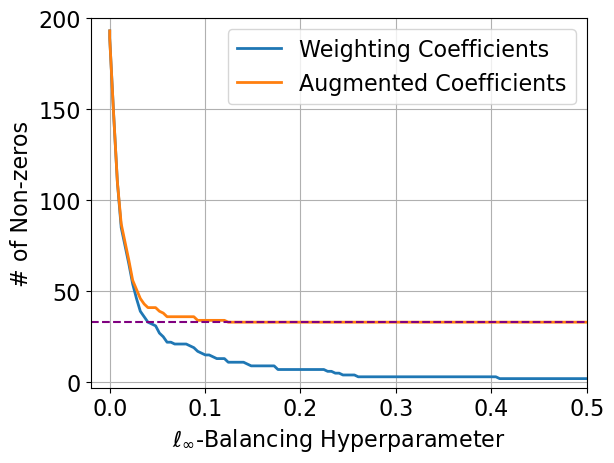

For the special case with diagonal covariates, both double ridge and double lasso undersmooth in a particular norm of , relative to the unaugmented outcome model, as shown in Figure 6. In particular, Figures 6(a) and 6(c) show the norm and the number of included covariates (the “norm”) for the ridge and lasso outcome regression models, respectively, as a function of the outcome hyperparameter . The purple dotted lines show the values of chosen via cross validation, and the corresponding values of the and norms. Figures 6(b) and 6(d) show the corresponding norm for the unaugmented and balancing weights estimators, “double ridge” and “double lasso,” respectively. For both, the norms for the augmented estimators are always at least as large as the norms for the outcome model alone. While the patterns are qualitatively the same, the behavior for balancing does not correspond to traditional undersmoothing, since the union of non-zero coefficients of the outcome and weighting models cannot generally be recovered by changing the hyperparameter of the lasso outcome model.

7 Undersmoothing and asymptotic results for kernel ridge regression

Our numeric results above suggests a way to understand augmented balancing weights through the lens of undersmoothing — and vice versa. In particular, we show above that ridge-augmented balancing is numerically equivalent to a single, undersmoothed (generalized) ridge regression outcome model, and that this equivalence holds for kernel ridge regression. We now show that these numerical results extend to undersmoothing in the statistical sense as well.

7.1 Regularization bias, double robustness, and undersmoothing

Using off-the-shelf penalized regression leads to non-negligible regularization bias for our target estimand: choosing the hyperparameter that minimizes the predictive MSE does not drive the bias to zero sufficiently fast asymptotically. Undersmoothing — choosing a smaller regularization parameter than is prediction optimal — is an alternative to the doubly robust approach of using an augmentation term as a bias correction (Goldstein and Messer, 1992; Newey et al., 1998). A main difficulty lies in finding the optimal hyperparameter.

A series of recent papers have explored both approaches in the context of kernel ridge regression. From the doubly robust perspective, Wong and Chan (2018) and Singh (2021) show that forms of “double kernel ridge” are semiparametrically efficient. From the undersmoothing perspective, Hirshberg et al. (2019) and Mou et al. (2023) demonstrate that a single, unaugmented kernel ridge regression estimator can also achieve efficiency with careful selection of the regularization schedule.

Our Proposition 4.3 demonstrates that the augmented balancing weights estimator in the RKHS setting with “double kernel ridge regression” is numerically equivalent to a single-stage undersmoothed kernel ridge estimator. To relate the existing statistical analyses, we will begin with the RKHS framework in Caponnetto and De Vito (2007) and derive the implied undersmoothed kernel ridge hyperparameter of the corresponding augmented estimator from Singh (2021). We find that the implied hyperparameter can go to zero either faster or slower than the standard rate of studied in the undersmoothing literature, depending on the effective dimension and smoothness of the outcome model in the RKHS.

7.2 The statistical setting

To move from numerical results to statistical results, we must place some constraints on the data generating process. Our setup for the RKHS follows Singh (2021). First, assume that the space is Polish. Let be an RKHS on with corresponding kernel satisfying standard regularity conditions (Singh, 2021, Assumption 5.2) and let , denote the eigenvalues and eigenfunctions respectively of its kernel integral operator under . Next, assume that the eigenvalues satisfy the decay condition for some and a constant . The parameter encodes information on the effective dimension of . For a bounded kernel, (Fischer and Steinwart, 2020): the case where corresponds to a finite-dimensional RKHS; for the case with , the must decay at a polynomial rate.

We then assume that for some , the outcome function belongs to the set:

| (17) |

where encodes additional smoothness of the conditional expectation. If , then by the spectral decomposition of the RKHS, Equation 17 is equivalent to requiring ; choosing larger values of corresponds to being a smoother element of , with a “saturation effect” kicking in for (Bauer et al., 2007). Varying (the effective dimension of the RKHS) and (the additional smoothness of the outcome function) changes the optimal rates for regression, with larger values of both corresponding to faster rates of convergence.

Finally, we assume that the Riesz representer, , of our linear functional estimand also belongs to . Under these conditions, Singh (2021) demonstrates that an augmented estimator combining kernel balancing weights and a kernel ridge regression base learner is asymptotically normal. Furthermore, it follows that the asymptotic variance achieves the semiparametric efficiency bound. Now we will demonstrate a setting where this estimator is equivalent to a single undersmoothed kernel ridge regression.

7.3 Implied undersmoothing for kernel ridge regression

Under the conditions outlined above, assume that we observe iid samples of from . Define to be the kernel matrix with -th entry . Let denote the eigenvalues of and assume that , a constant for all .222In the finite-dimensional case, we can immediately extend Proposition 7.1 to varying — the resulting regularization parameter would vary for each dimension, but each with identical asymptotic rate as a function of . This extension is more complicated in the infinite-dimensional case. We leave a thorough investigation to future work. The kernel ridge regression outcome model with parameter has coefficients:

Applying Proposition 4.3, the augmented estimator with hyperparameter is equivalent to a plug-in estimate with a new kernel ridge model:

with hyperparameter

Following Caponnetto and De Vito (2007), Theorems 5.1 and 5.2 of Singh (2021) use hyperparameter schedules for and , which depend on the effective dimension and smoothness :

For two functions of , and , let denote that and . We can compute the implied augmented hyperparameter (for large ) using the following proposition.

Proposition 7.1.

Let be any monotonically decreasing function of and let . Then:

To see the connection between double kernel ridge regression and undersmoothing, first consider the standard ridge regression case, which corresponds to the finite-dimensional setting with . Here, we choose hyperparameter to control the prediction error for both the outcome and weighting models. The augmented estimator is then equivalent to a single ridge regression with hyperparameter . Hence, this will always undersmooth relative to the MSE-optimal hyperparameter for a single ridge regression.

This rate matches the one typically used in undersmoothed kernel ridge regression analyses. For example, both Hirshberg et al. (2019) and Mou et al. (2023) demonstrate that, in a similar statistical setting, plug-in estimators of linear functionals using kernel ridge regression with a hyperparameter schedule of can be semiparametrically efficient.

The optimal undersmoothing analysis from Hirshberg et al. (2019) and Mou et al. (2023) also extends to the infinite-dimensional setting (). By contrast, we find that the undersmoothed hyperparameter implied by the augmented procedure can take on a range of asymptotic rates, both faster and slower than , in this infinite-dimensional setting. The implied augmented hyperparameter is of order and the MSE-optimal hyperparameter schedules for the base learner, , can be faster or slower than depending on the effective dimension and smoothness of the RKHS.

For example, when , the optimal rate for is ; the implied hyperparameter is then order for and . Whether or not this smooths more than therefore depends on the relationship between the effective dimension and the smoothness . In particular, the implied hyperparameter goes to zero at a slower rate than whenever . In this sense, Proposition 7.1 generalizes the standard undersmoothing arguments, which typically shift the regularization schedule from to . It is unclear whether the rates we find here are the only undersmoothed rates that will yield efficiency for fixed and ; we leave a thorough investigation to future work.

The results thus far are inherently theoretical, as they depend on unknown properties of the underlying RKHS and outcome function. Thus, we view this more as an aid to understanding rather than giving practical guidance. However, one simple heuristic suggested by Proposition 7.1 is to choose by standard cross-validation and then use a single-stage kernel ridge regression estimator with hyperparameter (as long as the cross-validated is smaller than ). This assumes that the cross-validated is rate-optimal and we leave an empirical investigation of practical performance to future work. Finally, we note that these results are unique to balancing and, especially, do not appear to hold for balancing weights.

8 Discussion

We have shown that augmenting a plug-in regression estimator with linear balancing weights results in a new plug-in estimator with coefficients that are shrunk towards — in some cases all the way to — the estimates from OLS fit on the same observations. We generalize this equivalence for different choices of outcome and weighting regressions, and connect this to undersmoothing for the special case of kernel ridge regression. We then illustrate these results on a canonical data set, highlighting the role of modeling choices and hyperparameter tuning. In the Appendix also explore many extensions, including to nonlinear weights and to high-dimensional features.

There are many promising avenues for future research. The fundamental connection between doubly robust estimation undersmoothing opens up several theory directions. While we focus on the special case of kernel ridge regression in Section 7, we anticipate that these connections will hold more broadly. Similarly, while our focus in this paper has been on interpreting balancing weights as a form of linear regression, the converse is also valid: we could instead focus on how many outcome regression-based plug-in estimators are, in fact, a form of balancing weights; see Lin and Han (2022) for connections between outcome modeling and density ratio estimation.

We also anticipate that our numeric results will lead to better guidance for deploying augmented balancing weights in practice. The most immediate question is hyperparameter tuning, for which recommendations vary (e.g., Kallus, 2020; Wang and Zubizarreta, 2020; Chernozhukov et al., 2022d). We expect that the connection to theoretically optimal results for undersmoothing (e.g., Mou et al., 2023) can help guide hyperparameter choice in the settings where we have shown augmented estimators to be equivalent to undersmoothed outcome regression. More broadly, we can consider special cases, such as multivariate Gaussians, for which we can reason about trade-offs for different choices.

We conjecture that these results may provide new insights into the estimation of causal effects in the proximal causal inference framework (Tchetgen Tchetgen et al., 2020). This framework uses proxy variables to identify causal effects in the presence of unmeasured confounding. Estimation has been complicated by the fact that, in the absence of strong parametic assumptions, estimators of proximal causal effects are solutions to ill-posed Fredholm integral equations. Ghassami et al. (2022) and Kallus et al. (2021) recently proposed tractable nonparametric estimators in this setting. They use an “adversarial” version of double kernel ridge regression — allowing the weighting and outcome models to have different bases — to estimate the solution to the required Fredholm integral equations. Our results apply immediately to standard augmented estimators with different bases for the outcome and weighting models, either via a union basis (Chernozhukov et al., 2022d) or by applying an appropriate projection as in Hirshberg and Wager (2021), and extending these results to proximal causal effect estimators might help in constructing new proximal balancing weights, matching, or regression estimators with attractive asymptotic properties.

Finally, many common panel data estimators are forms of augmented balancing weight estimation (Abadie et al., 2010; Ben-Michael et al., 2021c; Arkhangelsky et al., 2021). We plan to use the numeric results here, especially the results for simplex-constrained weights in Appendix D.2, to better understand connections between methods and to inform inference.

References

- Abadie et al. (2010) A. Abadie, A. Diamond, and J. Hainmueller. Synthetic control methods for comparative case studies: Estimating the effect of california’s tobacco control program. Journal of the American statistical Association, 105(490):493–505, 2010.

- Agarwal and Singh (2021) A. Agarwal and R. Singh. Causal inference with corrupted data: Measurement error, missing values, discretization, and differential privacy. arXiv preprint arXiv:2107.02780, 2021.

- Agarwal et al. (2022) A. Agarwal, Y. S. Tan, O. Ronen, C. Singh, and B. Yu. Hierarchical shrinkage: Improving the accuracy and interpretability of tree-based models. In K. Chaudhuri, S. Jegelka, L. Song, C. Szepesvari, G. Niu, and S. Sabato, editors, Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pages 111–135. PMLR, 17–23 Jul 2022. URL https://proceedings.mlr.press/v162/agarwal22b.html.

- Arkhangelsky et al. (2021) D. Arkhangelsky, S. Athey, D. A. Hirshberg, G. W. Imbens, and S. Wager. Synthetic difference-in-differences. American Economic Review, 111(12):4088–4118, 2021.

- Athey et al. (2018) S. Athey, G. W. Imbens, and S. Wager. Approximate residual balancing: debiased inference of average treatment effects in high dimensions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(4):597–623, 2018.

- Bartlett et al. (2020) P. L. Bartlett, P. M. Long, G. Lugosi, and A. Tsigler. Benign overfitting in linear regression. Proceedings of the National Academy of Sciences, 117(48):30063–30070, 2020.

- Bauer et al. (2007) F. Bauer, S. Pereverzev, and L. Rosasco. On regularization algorithms in learning theory. Journal of complexity, 23(1):52–72, 2007.

- Belloni et al. (2014) A. Belloni, V. Chernozhukov, and C. Hansen. Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies, 81(2):608–650, 2014.

- Ben-Michael et al. (2021a) E. Ben-Michael, A. Feller, and E. Hartman. Multilevel calibration weighting for survey data. arXiv preprint arXiv:2102.09052, 2021a.

- Ben-Michael et al. (2021b) E. Ben-Michael, A. Feller, D. A. Hirshberg, and J. R. Zubizarreta. The balancing act in causal inference. arXiv preprint arXiv:2110.14831, 2021b.

- Ben-Michael et al. (2021c) E. Ben-Michael, A. Feller, and J. Rothstein. The augmented synthetic control method. Journal of the American Statistical Association, 116(536):1789–1803, 2021c.

- Benkeser and Van Der Laan (2016) D. Benkeser and M. Van Der Laan. The highly adaptive lasso estimator. In 2016 IEEE international conference on data science and advanced analytics (DSAA), pages 689–696. IEEE, 2016.

- Bruns-Smith and Feller (2022) D. A. Bruns-Smith and A. Feller. Outcome assumptions and duality theory for balancing weights. In International Conference on Artificial Intelligence and Statistics, pages 11037–11055. PMLR, 2022.

- Bühlmann and Yu (2003) P. Bühlmann and B. Yu. Boosting with the l 2 loss: regression and classification. Journal of the American Statistical Association, 98(462):324–339, 2003.

- Caponnetto and De Vito (2007) A. Caponnetto and E. De Vito. Optimal rates for the regularized least-squares algorithm. Foundations of Computational Mathematics, 7:331–368, 2007.

- Chattopadhyay and Zubizarreta (2021) A. Chattopadhyay and J. R. Zubizarreta. On the implied weights of linear regression for causal inference. arXiv preprint arXiv:2104.06581, 2021.

- Chattopadhyay et al. (2020) A. Chattopadhyay, C. H. Hase, and J. R. Zubizarreta. Balancing vs modeling approaches to weighting in practice. Statistics in Medicine, 39(24):3227–3254, 2020.

- Chernozhukov et al. (2018) V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 01 2018.

- Chernozhukov et al. (2022a) V. Chernozhukov, J. C. Escanciano, H. Ichimura, W. K. Newey, and J. M. Robins. Locally robust semiparametric estimation. Econometrica, 90(4):1501–1535, 2022a.

- Chernozhukov et al. (2022b) V. Chernozhukov, W. Newey, V. M. Quintas-Martinez, and V. Syrgkanis. Riesznet and forestriesz: Automatic debiased machine learning with neural nets and random forests. In International Conference on Machine Learning, pages 3901–3914. PMLR, 2022b.

- Chernozhukov et al. (2022c) V. Chernozhukov, W. Newey, R. Singh, and V. Syrgkanis. Automatic debiased machine learning for dynamic treatment effects and general nested functionals. arXiv preprint arXiv:2203.13887, 2022c.

- Chernozhukov et al. (2022d) V. Chernozhukov, W. K. Newey, and R. Singh. Automatic debiased machine learning of causal and structural effects. Econometrica, 90(3):967–1027, 2022d.

- Chernozhukov et al. (2022e) V. Chernozhukov, W. K. Newey, and R. Singh. Debiased machine learning of global and local parameters using regularized riesz representers. The Econometrics Journal, 2022e.

- Dehejia and Wahba (1999) R. H. Dehejia and S. Wahba. Causal effects in nonexperimental studies: Reevaluating the evaluation of training programs. Journal of the American statistical Association, 94(448):1053–1062, 1999.

- Deville and Särndal (1992) J.-C. Deville and C.-E. Särndal. Calibration estimators in survey sampling. Journal of the American statistical Association, 87(418):376–382, 1992.

- Duchi et al. (2021) J. C. Duchi, P. W. Glynn, and H. Namkoong. Statistics of robust optimization: A generalized empirical likelihood approach. Mathematics of Operations Research, 46(3):946–969, 2021.

- Farrell (2015) M. H. Farrell. Robust inference on average treatment effects with possibly more covariates than observations. Journal of Econometrics, 189(1):1–23, 2015.

- Fischer and Steinwart (2020) S. Fischer and I. Steinwart. Sobolev norm learning rates for regularized least-squares algorithms. The Journal of Machine Learning Research, 21(1):8464–8501, 2020.

- Fuller (2002) W. A. Fuller. Regression estimation for survey samples. Survey Methodology, 28(1):5–24, 2002.

- Gao et al. (2022) C. Gao, S. Yang, and J. K. Kim. Soft calibration for selection bias problems under mixed-effects models. arXiv preprint arXiv:2206.01084, 2022.

- Ghassami et al. (2022) A. Ghassami, A. Ying, I. Shpitser, and E. T. Tchetgen. Minimax kernel machine learning for a class of doubly robust functionals with application to proximal causal inference. In International Conference on Artificial Intelligence and Statistics, pages 7210–7239. PMLR, 2022.

- Goldstein and Messer (1992) L. Goldstein and K. Messer. Optimal plug-in estimators for nonparametric functional estimation. The annals of statistics, pages 1306–1328, 1992.

- Graham et al. (2012) B. S. Graham, C. C. de Xavier Pinto, and D. Egel. Inverse probability tilting for moment condition models with missing data. The Review of Economic Studies, 79(3):1053–1079, 2012.

- Grandvalet (1998) Y. Grandvalet. Least absolute shrinkage is equivalent to quadratic penalization. In International Conference on Artificial Neural Networks, pages 201–206. Springer, 1998.

- Gretton et al. (2012) A. Gretton, K. M. Borgwardt, M. J. Rasch, B. Schölkopf, and A. Smola. A kernel two-sample test. The Journal of Machine Learning Research, 13(1):723–773, 2012.

- Hainmueller (2012) J. Hainmueller. Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political analysis, 20(1):25–46, 2012.

- Harshaw et al. (2019) C. Harshaw, F. Sävje, D. Spielman, and P. Zhang. Balancing covariates in randomized experiments with the gram–schmidt walk design. arXiv preprint arXiv:1911.03071, 2019.

- Hastie et al. (2009) T. Hastie, R. Tibshirani, J. H. Friedman, and J. H. Friedman. The elements of statistical learning: data mining, inference, and prediction, volume 2. Springer, 2009.

- Hazlett (2020) C. Hazlett. Kernel balancing. Statistica Sinica, 30(3):1155–1189, 2020.

- Hellerstein and Imbens (1999) J. K. Hellerstein and G. W. Imbens. Imposing moment restrictions from auxiliary data by weighting. Review of Economics and Statistics, 81(1):1–14, 1999.

- Hill (2011) J. L. Hill. Bayesian nonparametric modeling for causal inference. Journal of Computational and Graphical Statistics, 20(1):217–240, 2011.

- Hirano et al. (2003) K. Hirano, G. W. Imbens, and G. Ridder. Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71(4):1161–1189, 2003.

- Hirshberg and Wager (2021) D. A. Hirshberg and S. Wager. Augmented minimax linear estimation. The Annals of Statistics, 49(6):3206–3227, 2021.

- Hirshberg et al. (2019) D. A. Hirshberg, A. Maleki, and J. R. Zubizarreta. Minimax linear estimation of the retargeted mean. arXiv preprint arXiv:1901.10296, 2019.

- Imai and Ratkovic (2014) K. Imai and M. Ratkovic. Covariate balancing propensity score. Journal of the Royal Statistical Society: Series B: Statistical Methodology, pages 243–263, 2014.

- Jacot et al. (2018) A. Jacot, F. Gabriel, and C. Hongler. Neural tangent kernel: Convergence and generalization in neural networks. Advances in neural information processing systems, 31, 2018.

- Kallus (2020) N. Kallus. Generalized optimal matching methods for causal inference. J. Mach. Learn. Res., 21:62–1, 2020.

- Kallus et al. (2021) N. Kallus, X. Mao, and M. Uehara. Causal inference under unmeasured confounding with negative controls: A minimax learning approach. arXiv preprint arXiv:2103.14029, 2021.

- Kennedy (2022) E. H. Kennedy. Semiparametric doubly robust targeted double machine learning: a review. arXiv preprint arXiv:2203.06469, 2022.

- Kim et al. (2022a) K. Kim, B. A. Niknam, and J. R. Zubizarreta. Scalable kernel balancing weights in a nationwide observational study of hospital profit status and heart attack outcomes. 2022a.

- Kim et al. (2022b) M. P. Kim, C. Kern, S. Goldwasser, F. Kreuter, and O. Reingold. Universal adaptability: Target-independent inference that competes with propensity scoring. Proceedings of the National Academy of Sciences, 119(4):e2108097119, 2022b.

- Kline (2011) P. Kline. Oaxaca-blinder as a reweighting estimator. American Economic Review, 101(3):532–37, 2011.

- LaLonde (1986) R. J. LaLonde. Evaluating the econometric evaluations of training programs with experimental data. The American economic review, pages 604–620, 1986.

- Lin et al. (2022) R. R. Lin, H. Z. Zhang, and J. Zhang. On reproducing kernel banach spaces: Generic definitions and unified framework of constructions. Acta Mathematica Sinica, English Series, 38(8):1459–1483, 2022.

- Lin and Han (2022) Z. Lin and F. Han. On regression-adjusted imputation estimators of the average treatment effect. arXiv preprint arXiv:2212.05424, 2022.

- Lumley et al. (2011) T. Lumley, P. A. Shaw, and J. Y. Dai. Connections between survey calibration estimators and semiparametric models for incomplete data. International Statistical Review, 79(2):200–220, 2011.

- Menon and Ong (2016) A. Menon and C. S. Ong. Linking losses for density ratio and class-probability estimation. In International Conference on Machine Learning, pages 304–313. PMLR, 2016.

- Mou et al. (2023) W. Mou, P. Ding, M. J. Wainwright, and P. L. Bartlett. Kernel-based off-policy estimation without overlap: Instance optimality beyond semiparametric efficiency, 2023. URL https://arxiv.org/abs/2301.06240.

- Newey (1994) W. K. Newey. The asymptotic variance of semiparametric estimators. Econometrica: Journal of the Econometric Society, pages 1349–1382, 1994.

- Newey and Robins (2018) W. K. Newey and J. R. Robins. Cross-fitting and fast remainder rates for semiparametric estimation. arXiv preprint arXiv:1801.09138, 2018.

- Newey and Smith (2004) W. K. Newey and R. J. Smith. Higher order properties of gmm and generalized empirical likelihood estimators. Econometrica, 72(1):219–255, 2004.

- Newey et al. (1998) W. K. Newey, F. Hsieh, and J. Robins. Undersmoothing and bias corrected functional estimation. 1998.

- Newey et al. (2004) W. K. Newey, F. Hsieh, and J. M. Robins. Twicing kernels and a small bias property of semiparametric estimators. Econometrica, 72(3):947–962, 2004.

- Park et al. (2009) B. Park, Y. Lee, and S. Ha. boosting in kernel regression. Bernoulli, 15(3):599–613, 2009.

- Qin and Zhang (2007) J. Qin and B. Zhang. Empirical-likelihood-based inference in missing response problems and its application in observational studies. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(1):101–122, 2007.

- Robins et al. (2007) J. Robins, M. Sued, Q. Lei-Gomez, and A. Rotnitzky. Comment: Performance of double-robust estimators when” inverse probability” weights are highly variable. Statistical Science, 22(4):544–559, 2007.

- Robins et al. (1994) J. M. Robins, A. Rotnitzky, and L. P. Zhao. Estimation of regression coefficients when some regressors are not always observed. Journal of the American statistical Association, 89(427):846–866, 1994.

- Rubin (1980) D. B. Rubin. Randomization analysis of experimental data: The fisher randomization test comment. Journal of the American statistical association, 75(371):591–593, 1980.

- Rubinstein et al. (2021) M. Rubinstein, A. Haviland, and D. Choi. Balancing weights for region-level analysis: the effect of medicaid expansion on the uninsurance rate among states that did not expand medicaid. arXiv preprint arXiv:2105.02381, 2021.

- Shen et al. (2022) D. Shen, P. Ding, J. Sekhon, and B. Yu. A tale of two panel data regressions. arXiv preprint arXiv:2207.14481, 2022.

- Shen (1997) X. Shen. On methods of sieves and penalization. The Annals of Statistics, 25(6):2555–2591, 1997.

- Singh (2021) R. Singh. Debiased kernel methods. arXiv preprint arXiv:2102.11076, 2021.

- Singh et al. (2022) R. Singh, L. Sun, et al. Double robustness for complier parameters and a semiparametric test for complier characteristics. Technical report, 2022.

- Speckman (1979) P. Speckman. Minimax estimates of linear functionals in a hilbert space. Unpublished Manuscript, 1979.

- Tan (2020) Z. Tan. Regularized calibrated estimation of propensity scores with model misspecification and high-dimensional data. Biometrika, 107(1):137–158, 2020.

- Tchetgen Tchetgen et al. (2020) E. J. T. Tchetgen Tchetgen, A. Ying, Y. Cui, X. Shi, and W. Miao. An introduction to proximal causal learning. arXiv preprint arXiv:2009.10982, 2020.

- Wang and Zubizarreta (2020) Y. Wang and J. R. Zubizarreta. Minimal dispersion approximately balancing weights: asymptotic properties and practical considerations. Biometrika, 107(1):93–105, 2020.

- Wong and Chan (2018) R. K. Wong and K. C. G. Chan. Kernel-based covariate functional balancing for observational studies. Biometrika, 105(1):199–213, 2018.

- Zhao (2019) Q. Zhao. Covariate balancing propensity score by tailored loss functions. The Annals of Statistics, 47(2):965–993, 2019.

- Zhao and Percival (2017) Q. Zhao and D. Percival. Entropy balancing is doubly robust. Journal of Causal Inference, 5(1), 2017.

- Zubizarreta (2015) J. R. Zubizarreta. Stable weights that balance covariates for estimation with incomplete outcome data. Journal of the American Statistical Association, 110(511):910–922, 2015.