Independent additive weighted bias distributions and associated goodness-of-fit tests

Abstract

We use a Stein identity to define a new class of parametric distributions which we call “independent additive weighted bias distributions.” We investigate related -type discrepancy measures, empirical versions of which not only encompass traditional ODE-based procedures but also offer novel methods for conducting goodness-of-fit tests in composite hypothesis testing problems. We determine critical values for these new procedures using a parametric bootstrap approach and evaluate their power through Monte Carlo simulations. As an illustration, we apply these procedures to examine the compatibility of two real data sets with a compound Poisson Gamma distribution.

Keywords: Stein identity; independent additive bias; goodness-of-fit; composite hypothesis testing; compound Poisson

1 Introduction

Characterisations of distributions play a crucial role both in probability theory and in statistics. A famous example in probability theory is Stein’s method, where characterisations of distributions depending on so-called Stein operators are successfully applied to distributional approximation in the sense of integral probability metrics. In statistics, characterisations of distributions are widely used to propose goodness-of-fit and symmetry tests. The idea of exploiting characterisations for testing procedures can be traced back to [21] and became widely popular in the nineties of the last century. As noted in [23], goodness-of-fit tests based on characterisations are usually powerful procedures, “[…] because they reflect some intrinsic and hidden properties of probability distributions connected with the given characterisation, and therefore can be more efficient or more robust than others.” For a historical survey on the topic see [23]. The objective of this paper is to combine the characterisations of distributions utilised in Stein’s method with their applications in goodness-of-fit testing.

Let denote the distribution of some random variable . The very first step in any application of Stein’s method for consists in identifying a linear operator and a wide class of functions such that if and only if for all . This is called a Stein characterisation, and the operator is then called a Stein operator. The study of these operators and of their applications towards distributional approximation has attracted considerable attention, see the surveys [28, 20] or the monographs [24, 29] for an overview. Specific Stein characterisations have, in recent years, also been exploited in computational statistics (see [1] and the many references within for an overview); in particularly the corresponding identities have already successfully been exploited in the context of goodness-of-fit tests (see e.g. [6, 5]). In this paper we propose to define an entire class of families of distributions directly through their Stein operators, then exploit this characterisation for the purpose of goodness-of-fit tests.

The paper is structured as follows. In Section 2 we define the class of families of distributions and give specific examples of parametric families contained satisfying the definition. In Section 3 we consider a weighted -type discrepancy measure by considering the spectral version of the Stein characterisation. Section 4 consists of studying empirical counterparts to the discrepancy measures. We apply these for proposing new goodness-of-fit testing procedures to test composite hypotheses. In Section 5 we provide simulation results and apply in Section 6 the tests to two data sets related to insurance cases and rainfall.

2 A new class of families of distributions

Definition 1 (Independent Additive Weighted Bias distributions).

A random variable (or its distribution ) is of independent additive weighted bias-type if there exist functions and a probability distribution on such that, for independent of ,

| (1) |

for all absolutely continuous test functions with polynomial growth. We write when (i) satisfies (1) for the prescribed functions and and (ii) is characterised by this identity, in the sense that if satisfies (1) over the same class of functions then .

In the framework of Stein’s method, an random variable is characterised by an integral Stein operator of the form . This form of operator finds its origins in the so-called size bias distributions, as follows.

Example 1 (Additive size bias: is constant).

A positive random variable with mean is said to satisfy an additive size-bias condition if for some and independent of . Such random variables obviously satisfy a version of (1) with the prescribed parameters; they form a subclass of the family of infinitely divisible distributions, see [2]. See see e.g. [3] for an overview. The following examples are classical:

-

1.

a Poisson random variable with probability mass function on for some . Then with almost surely.

-

2.

a gamma random variable with density on for some . Then with .

-

3.

a (generalized) Dickman random variable with log-characteristic function for some . Then where .

In each case it is easy to show that these identities are characterising, e.g. by using the test functions which then leads to an ODE on the characteristic function. We will return to this in Lemma 1.

Many families of distributions are of IAWD-type, including the binomial, negative binomial, and hypergeometric distributions. In particular compound distributions are also of IAWD-type.

Example 2 (Compound Poisson: ).

We say is a compound Poisson random variable if with for some independent of a sequence of iid random variables with distribution a probability measure on . Then (see [2]) its distribution is characterised by with .

Example 3 (Compound geometric: ).

We say is a compound geometric random variable if with for some independent of a sequence of iid random variables with distribution a probability measure on . Then (see [9]) with and .

Random variables of IAWD-type have certain properties directly inherited from the identity (1). For instance,

-

1.

Additive size bias (Example 1): if , then , and .

-

2.

Compound Poisson (Example 2): if with then , and .

More generally, relations between low order moments of and are particularly easy to obtain through well chosen functions (typically and ). Note moreover how identity (1) also leads to recurrence relations on the moments of in terms of the moments of , through

which is true for all such that . Throughout this paper we will focus exclusively on examples satisfying for and for ; for such simple functions the relations are easy to obtain explicitly on a case-by-case basis. This will be of use in Section 4.1 for the purpose of obtaining moment estimators for the parameters of compound distributions.

Remark 1.

Our definition of the IAWD family contains an implicit assumption on the functions and on the distribution to ensure that identity (1) is characterising. Such will be the case in all examples we consider.

3 A new discrepancy measure

Fix some functions , some distribution on and let . Suppose that (and in particular is thus characterised by its Stein identity). The subscript serves to emphasise that the distribution of is the target distribution in our procedure. The independent and additive structure of the biasing term in (1) encourages us to consider exponential functions in the identity; depending on whether is real or complex, the Stein identity evaluated on these test functions then leads to relations between Laplace and/or Fourier transforms of and .

In this paper we focus on the spectral (Fourier) version: replacing by in (1) leads to

and, for some well chosen weighting function,

| (2) |

as a measure of discrepancy between and . We obtain the following result (see the appendix for details).

Proposition 1.

Let be any positive, integrable and differentiable weight function. Let for some and . We write and introduce the functions , and Then

| (3) | ||||

where, in (3), the indexed random variables denote iid copies of .

Remark 2.

Many choices of weighting function lead to explicit and manageable expressions for the , . For instance, taking one easily sees that for all values of and all . This is obviously not the only choice.

The following holds (see the supplementary material for a proof).

Lemma 1.

Let . Let be a weighting function which is strictly positive and integrable on , and let be as in (2). Then for any real random variable, with equality if and only if .

We now detail some examples.

Example 4 (Additive size bias ).

It follows from (1) (applied with ) that if has finite mean, then necessarily is the mean of the law of and is the characteristic function of . Identity (3) becomes

We further detail several examples which will be studied in the simulations (computations are left to the reader).

-

1.

If is Poisson distributed with mean then , so that and using as in Remark 2 we get (with slight abuse of notation)

(4) -

2.

If is Dickman distributed with mean then for which so . Using we get

(5) -

3.

If is gamma distributed with parameters then , for which so . Using we get

(6)

Example 5 (Compound Poisson ).

After recalling that , (3) becomes

Note that here . We further detail several examples which will be studied in the simulations (computations are left to the reader).

-

1.

Compound Poisson Exponential: here so . Using we get

(7) -

2.

Compound Poisson Gamma: here so . Using we get , but and do not admit a simple expression in terms of elementary functions. These functions can nevertheless be evaluated numerically.

Another natural choice of test functions to consider in (1) is hereby leading to and, for some well chosen weighting function, as an alternative measure of discrepancy between and . Easy computations lead to the following.

Proposition 2.

Let be any positive, integrable and differentiable weight function. Let for some and . We write and introduce the functions and Then

| (8) | ||||

where, in (8), the indexed random variables denote iid copies of .

4 Goodness-of-fit tests for IAWD distributions

4.1 The test statistics

The goodness-of-fit testing problem for a family of distributions , where is an open parameter space, , is as follows. Let be positive independent identically distributed (iid) random variables and denote the distribution of by . We want to test the null hypothesis

| (9) |

against general alternatives. In light of preceding arguments for any distribution of IAWD-type for some and , we propose, for suitable weight functions , the weighted -type (or Cramér-von Mises-type) test statistic

where for , with , and needing to be estimated from the data . Direct computations similar to those performed for Proposition 1 show that

| (10) | ||||

with and , , are as prescribed in equation (3), but this time requiring some estimation of the underlying parameters. A test based on rejects for large values of the statistic.

Remark 4.

For arbitrary let be the empirical version of the discrepancy measure in (10) in dependence of the underlying model parameters . A way to estimate the unknown parameters is to calculate

These estimators fall into the class of minimum distance estimators and the implementation will usually need numerical routines, for a similar approach see [7]. We focus in the following on the goodness-of-fit testing problem and hence leave the investigation of these new estimators open for further research.

Example 6 (Additive size-bias, continued).

Recall that ; since the nonparametric estimate of the mean is the test statistic is of the form

| (11) |

with , as given in (1) but with some parameters possibly needing to be estimated. For instance, if is Poisson or Dickman then, using the same weights as in Example 4, the test statistic is given by (11) with , given without any parameter estimation in (4) (Poisson case) or (5) (Dickman case). The same story holds if is gamma, here the functions are given from (6) but the parameter needs to be estimated from the data; in our simulations we use the moment estimator .

Example 7 (Compound Poisson, continued).

Exactly the same extension for the compound Poisson case as in the previous example holds, here with

where (i) for the compound Poisson exponential the for as given in (7) with needing to be estimated whereas (ii) for the compound Poisson gamma the for are not available explicitly but can be computed numerically, this time with parameters and needing to be estimated. In both cases we use the moment estimators, given in the compound Poisson exponential case by and, in the compound Poisson gamma case, by

| (12) |

with , , and . These moment estimators are obtained by solving the system of equations obtained by applying identity (1) to , in the Poisson exponential case, and to , as well as in the Poisson gamma case.

4.2 Limit null distribution

A convenient setting for asymptotics will be the separable Hilbert space of (equivalence classes of) measurable functions satisfying the integrability condition . Here, , , is the complex absolute value and denotes the complex conjugate of . We add for the notation of the mean an index whenever this might lead to confusion. The scalar product and the norm in will be denoted by

respectively. In this section we assume to be iid. copies of and , as well as and , where is a vector containing some (or all) elements of the unknown parameter . See Theorem 3 of the supplementary material for the limit null distribution of for the case of a known parameter . Denote by a consistent estimator of . Write for and assume that

-

(A1)

is twice differentiable w.r.t. , and the derivatives are bounded in some neighbourhood of ,

-

(A2)

allows an asymptotic expansion

where is a function satisfying and for all .

-

(A3)

All expectations exist.

We introduce the stochastic process

and denote in the following the gradient operator w.r.t. by and by the transpose of a vector. The proof of the subsequent theorem is found in the supplementary material file.

Theorem 1 (limit null distribution, parameters unknown).

Under assumptions (A1)-(A3) we have

where is a centred Gaussian element of with covariance kernel

Example 8 (Example 4 continued).

Recall that and . Since the function does not depend on we drop the variable in the definition for this example to gain readability. In every case denotes the characteristic function of . For the three considered cases we have

-

1.

If is Poisson distributed with parameter then and so that The moment and maximum likelihood estimator is given by and hence (A2) is satisfied with . Direct calculation show

-

2.

If is Dickman distributed with parameter . Then has characteristic function so that and , A suitable estimator for is , hence (A2) is satisfied with . The covariance kernel in Theorem 1 then reduces to

since . Note that , and .

-

3.

The case is detailed in Example 9 in the supplementary material.

The following result is a direct consequence of a Taylor expansion (see the auxiliary processes in Lemma 2 in the supplementary material) and Fatou’s lemma.

Theorem 2.

Under the stated assumptions, we have as

Note that if and only if by Lemma 1. This implies that the test statistic is consistent against any alternative distribution satisfying the assumptions.

4.3 Parametric bootstrap procedure

In this subsection assume that we have a test statistic for testing (9) against general alternatives, that we have a sequence of vectors of parameters with and and that we have shown under a triangular array of row-wise iid random variables with distribution that as , where is a centred Gaussian element in with known covariance kernel depending on . The distribution of is then known to have the equivalent representation , where are independent, standard normally distributed random variables, and are a decreasing series of non-zero eigenvalues of the integral operator

Clearly, the covariance kernel depends on the underlying limiting parameter vector and hence so does the operator . Computing the eigenvalues of the integral operator requires solving the homogeneous Fredholm integral equation of the second kind

| (13) |

Due to the high complexity of the covariance kernel, it seems hopeless to find explicit solutions of (13) and hence formulae for the eigenvalues. Furthermore, since the true parameter is unknown in practice, the limiting null distribution cannot be used to derive critical values of the test. Let be a consistent estimator of , hence assume that as . A solution to this problem is provided by a parametric bootstrap procedure as suggested in [16] and which is stated as follows:

-

(1)

Compute .

-

(2)

Conditionally on simulate bootstrap samples , iid from , and compute , .

-

(3)

Derive an empirical quantile of of .

-

(4)

Reject the hypothesis (9) at level if .

Note that for every computation of parameter estimation has to be done separately for each . Following the notation and methodology of [16] we prove that this bootstrap test has asymptotic level as . Denote the distribution function of under by and write for the distribution of . Note that is continuous and strictly increasing on . By the assumptions at the beginning of this section, we have that holds for every as , so by continuity of we have

Combining this with the consistency of the estimators , we have

Hence, with denoting the empirical distribution function of , we have by an identical construction as in (3.10) of [16]

from which as follows. This implies that if is a random sample from , we have

ensuring an asymptotic level test.

5 Simulations

We now present the results of Monte Carlo simulation studies related to the tests discussed in the previous section. Because these are the most novel tests, we focus on the examples of testing the fit to the gamma distribution, the generalised Dickman distribution, and the compound Poisson gamma law. Other examples are illustrated in the supplementary material. In each case the distributional parameters are unknown and have to be estimated. As a consequence a parametric bootstrap procedure is needed to perform the tests. For the first two families of distributions, we implemented the procedure stated in Subsection 4.3 and for the last family the warp-speed method of [12] due to heavy numerical computation times. We refer to Section B of the supplementary material for further simulation results on testing for the Poisson and the compound Poisson exponential distributions.

All the simulations are performed using the statistical computing environment R, see [27]. For the first three cases, we consider the sample size and the nominal level of significance is set either to or to depending on the comparable simulation studies in the literature. Every entry in Tables 4 - 7 in the supplementary material are based on 10 000 repetitions with a bootstrap sample of . For the compound Poisson gamma law, we fix the simulation parameters to , , and perform 1 000 repetitions. To ensure easy readability the tables containing the simulation results and the description of the alternative distributions have been moved to the supplementary materials file.

5.1 Testing the fit to the gamma family of distributions

The problem of testing the fit of data to the gamma distribution with unknown parameters is considered in the literature, see [4, 17] and the references therein. Note that most of the considered procedures are implemented in the R-package gofgamma, see [8]. As described in Example 6, we compute the test statistic (11) with functions given in (6) with scale parameter replaced with its moment estimator.

Firstly, we see that the type I error is correctly controlled by the bootstrap procedure, although it results in conservative procedures. A comparison of the empirical powers in Table 5 from the supplementary material to the results given in Table 2 of [4] shows that for the SP(2) distribution the newly proposed procedure outperform the existing procedures. On many other cases there are choices of the tuning parameter for which the tests are close to the best performing competitors. Clearly some alternatives as the W(1.5) law are not identified at all.

5.2 Testing the fit to the family of generalized Dickman distributions

The Dickman (or alternatively Dickman-Goncharov) distribution is a distribution appearing as a limiting distributions connected to the analysis of the asymptotic behaviour of the number of positive integers in an interval, where the largest prime factor is smaller than a functional of the length of the interval. For a historic overview and further applications see [22]. The problem of testing the fit of data to a generalized Dickman distribution (which follows the definition in [2]) has not yet been considered in the literature and hence our test statistic presented in Example 6 (obtained from (11) with functions given in (5)) is the only test for this family of distributions. Note that the classical procedures based on the empirical distribution function can’t be computed, since there exists no closed form formula for the distribution function of this law. As estimators of the unknown parameter we chose the moment estimator. Since the support of the Dickman distribution is we choose the notation for the alternative families of distributions given in Section 5.1. Random number generation for the generalized Dickman law was performed using the Algorithm 3.1 of [10] implemented in the R package SubTS, see [14].

The power estimates given in Table 6 in the supplementary materials show that the type I error is controlled for the significance level under the hypothesis and the alternative distributions are well identified.

5.3 Testing the fit to the family of compound Poisson gamma distributions

In this subsection we want to test the fit of data to the compound Poisson gamma distribution, see Example 2 where is the two parameter gamma distribution , . This family of distributions was used to model aggregated insurance claims [15, 26], weighted networks in finance [11]. As estimators of the three unknown parameters we used the method of moments estimators (12) and denote them by respectively.

As already commented upon in example 5, for compound Poisson gamma distributions the test statistic from (3) suffers the drawback that the coefficients , do not admit an explicit form and therefore need to be computed numerically. On the other hand, from (8) with weight function on for a tuning parameter admits explicit coefficients, leading to

where

and denotes the upper incomplete gamma function. As already commented upon in Remark 3, this is precisely the test statistic proposed by [13, Section 3.2] (note that there is a typographical error in the stated formula in display (35)) for the particular case of CPG distributions.

We consider the alternative distributions from Subsection 5.1 described in Subsection B.2 of the supplementary material and add a mixed compound Poisson gamma model by simulating MCP for , , , , and . Since the simulation was numerically involved we restricted the study to the tuning parameter . The results are shown in Table 1. We see that both methods tend to be conservative although for the CP law they both tend to overestimate slightly the nominal level of . This effect might be explained by the low amount of Monte Carlo repetitions. In most cases the Laplace transform method outperforms the test based on using the weight function with tuning parameter , although for Weibull and some mixtures of compound Poisson gamma distributions the power is better in the reverse order. These findings are not surprising, since there is no universally best goodness-of-fit test, see [18].

| Dist./Test | ||

| CP | 6 | 8 |

| CP | 3 | 4 |

| CP | 1 | 5 |

| CP | 2 | 4 |

| 5 | 19 | |

| 5 | 7 | |

| 4 | 8 | |

| IG | 15 | 61 |

| IG | 13 | 54 |

| LN(0.5) | 8 | 22 |

| LN(0.8) | 15 | 49 |

| W(3, 2) | 6 | 1 |

| W(2, 5) | 7 | 3 |

| MCP | 7 | 18 |

| MCP | 11 | 10 |

| MCP | 14 | 9 |

| MCP | 22 | 10 |

| MCP | 4 | 3 |

| MCP | 10 | 8 |

| MCP | 30 | 53 |

| MCP | 46 | 84 |

| MCP | 31 | 44 |

| MCP | 60 | 100 |

6 Real data application

Since the presented method is very general we focus our data examples on the compound Poisson Gamma family of distributions from Example 5. The two most found applications of this law found in the literature are for insurance and rainfall data.

6.1 Insurance data

In our first example we analyse the data set of insurance claims of motorcycle drivers collected in 1999 by the Swedish insurance company Wasa. This data set contains information about motorcycle policies over the time period from 1994 to 1998 containing quantitative and categorical variables like ’owner age’, ’gender’, ’vehicle age’, ’bonus class’, ’number of claims’ and ’claim cost’. The data is available on the companion website of the monograph [25]. This data set has been analysed in Section 4 in [15], where assumptions are made for the quantitative variables ’number of claims’ and ’claim cost’ to be distributed following a Poisson and gamma law, respectively. In the following paragraphs, we aim at studying the validity of the assumptions by the methods proposed in the previous sections. Since ’owner age’ and ’bonus class’ are arguably good parameters to describe the experience of a driver we choose appropriate subsets of the data set. In a first step we analyse the validity of the assumption that the number of claims follow a Poisson law by the test statistic given in item 1 of Example 6 and applying the parametric bootstrap procedure of Subsection 4.3 with 500 bootstrap samples. In Table 2 we provide bootstrap p-values by relative frequency of simulated that are smaller than . It is seen that in most cases the assumption of an underlying Poisson distribution cannot be rejected at a significance level of . Nevertheless there are combinations, where the assumption of Poissonity is clearly rejected, as is the case of Bonusclass 1 and Ownerage . A closer look into this class shows that the data set has values of which 21 are greater than zero, 19 of which take the value 1 and 2 take the value 2. The rest of the data are zero. All the other p-values smaller than 0.05 exhibit a similar or even smaller amount of cases, where the test rejects the hypothesis. This shows that in such sparse data sets the assumption of Poissonity should not be taken for granted.

| Bonusclass | ||||||||

|---|---|---|---|---|---|---|---|---|

| Ownerage | ||||||||

| 1 | 0.182 | 0.030 | 0.000 | 0.004 | 0.424 | 0.486 | 0.004 | 0.328 |

| 2 | 0.538 | 0.146 | 0.548 | 0.460 | 0.522 | 0.424 | 0.454 | 0.306 |

| 3 | 0.368 | 0.484 | 0.506 | 0.438 | 0.578 | 0.510 | 0.002 | 0.546 |

| 4 | 0* | 0.214 | 0.610 | 0.574 | 0.556 | 0.474 | 0.572 | 0.356 |

| 5 | 0* | 0.064 | 0.068 | 0.004 | 0* | 0.416 | 0.352 | 0* |

| 6 | 0* | 0.432 | 0.518 | 0.406 | 0.548 | 0.442 | 0.332 | 0.534 |

| 7 | 0* | 0.580 | 0.028 | 0.068 | 0.472 | 0.002 | 0.000 | 0.484 |

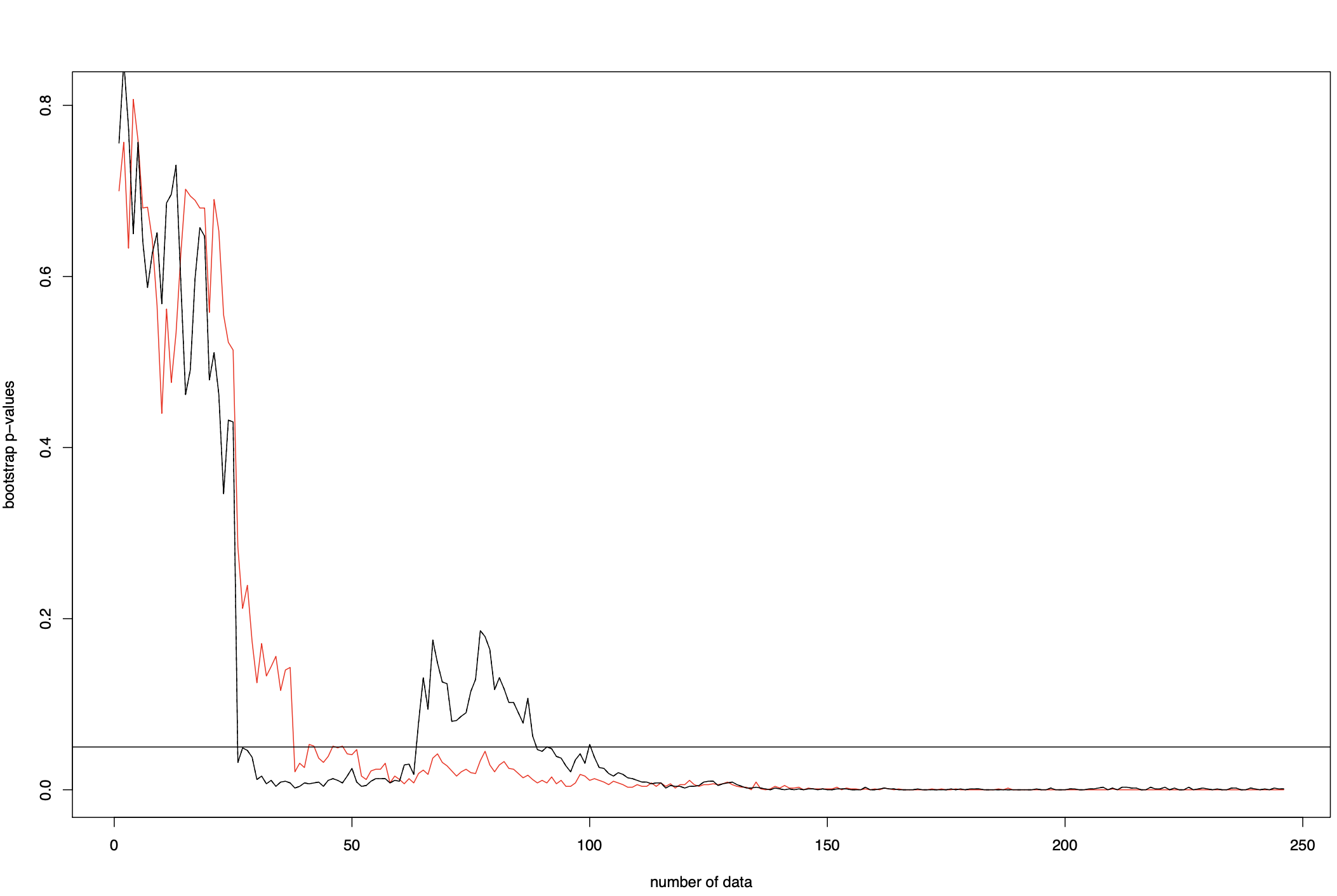

In a second step we consider the subset of data in which exactly one claim occured, which happened in cases. In Figure 1 we plotted the bootstrap p-value (bootstrap sample size 1000) for subsets of this data where the first 5 to 250 values have been considered. A line for a significance level of 5% has been added to show the rejection of the assumption that claims are distributed following a gamma distribution already for small sample sizes of less than 30. Taking all data into account, both procedures return a bootstrap p-value of 0 so the hypothesis is rejected as was to be expected.

As a last step, we look at the comparably more involved case, where we limit the data to only observations of the aggregated claim cost without the knowledge of how many claims have been reported. This setting falls into the class of compound Poisson gamma distributions. Since heavy numerical integration routines have been used, we limit our study to the cases reported in Table 3. The asterisk ’*’ stands for cases where we could not compute a p-value due to numerical problems. Interestingly the flexibility of the model seems to compensate the drawbacks reported in the first two tests. Nevertheless we also have to reject the hypothesis for the groups involving the owner ages at a 5% level.

| BonusclassOwnerage | ||||

|---|---|---|---|---|

| 1 | 0.23 | 0.03 | 0.38 | 0.33 |

| 2 | * | 0.05 | 0.33 | * |

| 3 | * | * | 0.35 | * |

| 4 | * | * | 0.09 | * |

6.2 Rainfall data

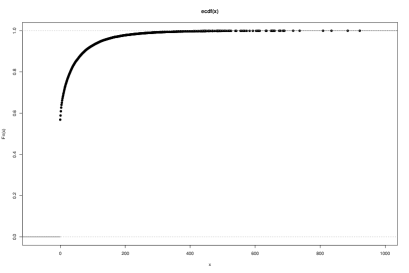

As a second example we consider rainfall data from the European Climate Assessment & Dataset (ECA&D, see www.ecad.eu), see [19]. We consider data taken from the station ID 13, where the data is gathered at Innsbruck University in Austria. The collected precipitation amount is given (in 0.1 mm) on a daily basis, covering the time span from 1st of January 1877 to 31st of July 2022. The data set consists of 53168 entries, after removing 4 NA entries. At 30234 days no rainfall was recorded. A plot of the empirical distribution function is found in Figure 2.

Since such large data sets are numerically not tractable, we restrict ourselves to the first and last year of recording, namely from 1st of January 1877 to 31st of December 1877 and 1st of August 2021 to 31st of July 2022. The values of the estimators are and , respectively. The tests calculate a bootstrap p-value of 0.38 and 0.54 (bootstrap sample size 100). Hence, we cannot reject the null hypothesis that the data stems from a compound Poisson gamma distribution at any level.

References

- [1] A. Anastasiou, A. Barp, F.-X. Briol, B. Ebner, R. E. Gaunt, F. Ghaderinezhad, J. Gorham, A. Gretton, C. Ley, Q. Liu, L. Mackey, C. J. Oates, G. Reinert, and Y. Swan. Stein’s method meets statistics: A review of some recent developments. Statistical Science, 38:120–139, 2021.

- [2] B. Arras and C. Houdré. On Stein’s Method for Infinitely Divisible Laws with Finite First Moment. Springer, 2019.

- [3] R. Arratia, L. Goldstein, and F. Kochman. Size bias for one and all. Probability Surveys, 16:1–61, 2019.

- [4] S. Betsch and B. Ebner. A new characterization of the gamma distribution and associated goodness-of-fit tests. Metrika, 82(7):779–806, 2019.

- [5] S. Betsch and B. Ebner. Testing normality via a distributional fixed point property in the Stein characterization. TEST, 29(1):105–138, 2020.

- [6] S. Betsch and B. Ebner. Fixed point characterizations of continuous univariate probability distributions and their applications. Ann. Inst. Statist. Math., 73:31–59, 2021.

- [7] S. Betsch, B. Ebner, and B. Klar. Minimum -distance estimators for non-normalized parametric models. Can. J. Stat., 49(2):514–548, 2021.

- [8] L. Butsch, B. Ebner, and S. Betsch. gofgamma: Goodness-of-Fit Tests for the Gamma Distribution, 2020. R package version 1.0.

- [9] F. Daly. Upper bounds for Stein-type operators. Electron. J. Probab., 13:566–587, 2008.

- [10] A. Dassios, Y. Qu, and J. W. Lim. Exact simulation of generalised vervaat perpetuities. Journal of Applied Probability, 56(1):57–75, 2019.

- [11] A. Gandy and L. A. M. Veraart. Compound poisson models for weighted networks with applications in finance. Mathematics and Financial Economics, 15(1):131–153, 2021.

- [12] R. Giacomini, D. N. Politis, and H. White. A warp-speed method for conducting monte carlo experiments involving bootstrap estimators. Econometric Theory, 29(3):567–589, 2013.

- [13] P.-O. Goffard, S. R. Jammalamadaka, and S. G. Meintanis. Goodness-of-fit procedures for compound distributions with an application to insurance. Journal of Statistical Theory and Practice, 16(3):52, 2022.

- [14] M. Grabchak and L. Can. SubTS: Positive Tempered Stable Distributions and Related Subordinators, 2023. R package version 1.0.

- [15] D. Hainaut, J. Trufin, and M. Denuit. Response versus gradient boosting trees, GLMs and neural networks under Tweedie loss and log-link. Scandinavian Actuarial Journal, pages 1–26, 2022.

- [16] N. Henze. Empirical-distribution-function goodness-of-fit tests for discrete models. The Canadian Journal of Statistics / La Revue Canadienne de Statistique, 24(1):81–93, 1996.

- [17] N. Henze, S. G. Meintanis, and B. Ebner. Goodness-of-fit tests for the gamma distribution based on the empirical Laplace transform. Commun. Stat. Theory Methods, 41(9):1543–1556, 2012.

- [18] A. Janssen. Global power functions of goodness of fit tests. Annals of Statistics, pages 239–253, 2000.

- [19] A. M. G. Klein Tank, J. B. Wijngaard, G. P. Können, R. Böhm, G. Demarée, A. Gocheva, M. Mileta, S. Pashiardis, L. Hejkrlik, C. Kern-Hansen, R. Heino, P. Bessemoulin, G. Müller-Westermeier, M. Tzanakou, S. Szalai, T. Pálsdóttir, D. Fitzgerald, S. Rubin, M. Capaldo, M. Maugeri, A. Leitass, A. Bukantis, R. Aberfeld, A. F. V. van Engelen, E. Forland, M. Mietus, F. Coelho, C. Mares, V. Razuvaev, E. Nieplova, T. Cegnar, J. Antonio López, B. Dahlström, A. Moberg, W. Kirchhofer, A. Ceylan, O. Pachaliuk, L. V. Alexander, and P. Petrovic. Daily dataset of 20th-century surface air temperature and precipitation series for the european climate assessment. International Journal of Climatology, 22(12):1441–1453, 2002.

- [20] C. Ley and Y. Swan. Parametric Stein operators and variance bounds. Braz. J. Probab. Stat., 30(2):171–195, 2016.

- [21] Y. V. Linnik. Linear forms and statistical criteria i, ii. Selected Translations in Mathematical Statistics and Probability, 3:1–40 , 41–90. Originally published 1953 in the Ukrainian Mathematical Journal, Vol. 5, pp. 207–243, 247–290 (in Russian), 1962.

- [22] S. A. Molchanov and V. A. Panov. The Dickman–Goncharov distribution. Russian Mathematical Surveys, 75(6):1089, 2020.

- [23] Y. Y. Nikitin. Tests based on characterizations, and their efficiencies: A survey. Acta et Commentationes Universitatis Tartuensis de Mathematica, 21:3–24, 2017.

- [24] I. Nourdin and G. Peccati. Normal Approximations with Malliavin Calculus: from Stein’s Method to Universality, volume 192. Cambridge University Press, 2012.

- [25] E. Ohlsson and B. Johansson. Non-Life Insurance Pricing with Generalized Linear Models. EAA Lecture NotesSpringerLink. Springer Berlin Heidelberg, Berlin, Heidelberg, 2010.

- [26] O. A. Quijano Xacur and J. Garrido. Generalised linear models for aggregate claims: to Tweedie or not? Eur. Actuar. J., 5(1):181–202, 2015.

- [27] R Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria, 2020.

- [28] N. Ross. Fundamentals of Stein’s method. Probab. Surv., 8:210–293, 2011.

- [29] Q.-M. Shao. Stein’s method, self-normalized limit theory and applications. In International Congress of Mathematicians (ICM), pages 2325–2350, 2010.

Acknowledgement

We thank Julien Trufin for providing us with the database used in Section 6.

Appendix A Proofs and additional results

Proof of Lemma 1.

Positivity and necessity are trivial. For sufficiency, let us suppose that . Then for (almost) all . Using the inverse Fourier formula and Fubini’s theorem, it follows that for any continuous integrable

with the Fourier transform of . Hence satisfies the same Stein identity (1) as . ∎

Theorem 3 (Limit null distribution, parameters known).

Proof of Theorem 3.

It is direct to see that

with . Some trivial rearrangements then give

with all expressions as defined in the statement of the Theorem. Now note that so that and so that , whence the claim. ∎

Proof of Proposition 1.

Let . Straightforward but tedious computations (we used Mathematica and symmetry arguments to simplify the expressions) lead to

Clearly,

The conclusion follows. ∎

Before formulating the proof of Theorem 1, we introduce the auxiliary processes

as well as

and prove the following Lemma.

Lemma 2.

Under the standing assumptions, we have

Proof of Lemma 2.

Denoting by the Jacobian matrix w.r.t. , we have with a multivariate Taylor expansion of order 2 and by the Cauchy-Schwarz inequality

where lies between and , is the upper bound of w.r.t. (which exists by (A1)), and denotes the Frobenius norm. By the sub-multiplicative structure of the latter we have by the Cauchy-Schwarz inequality

and an application of the strong law of large numbers shows with (A2) and (A3) the claim. The second statement follows by the law of large numbers in Hilbert spaces and (A2). ∎

Proof of Theorem 1.

By Lemma 2, we see that the asymptotic distribution of is determined by and the latter is a sum of iid random variables, hence the central limit theorem in Hilbert-spaces can be applied. The statement is then a direct consequence of the continuous mapping theorem. Writing

the covariance structure of the limit process is given by and straightforward calculations. ∎

In the following we detail the covariance kernel for the gamma distribution with unknown parameters.

Example 9.

Example 1: Example 8 continued. If is gamma distributed with parameter vector . Then with characteristic function , . Then

Note that

The moment estimators are and . Some calculations show that

Some more calculations show

where

Writing

and

Furthermore, we write

where

With these notations the covariance kernel in Theorem 1 is given after cumbersome long calculations by

Appendix B Simulation results

In this section we provide the simulation results for the Monte Carlo simulations involving the parametric bootstrap procedures of Section 5. Note that we chose the weight functions and , .

B.1 Testing Poissonity

In this subsection we focus on testing the fit of discrete data to the Poisson family (Example 4, item 1) by applying the test statistics given in Example 6 for different tuning parameters . Note that this problem has been studied in the literature, see [GH:2000] for a review and Section 5 of [BEN:2022] for new methods and recent references.

We simulate 38 representatives of families of distributions. In order to show that all the considered testing procedures maintain the nominal level of 10%, we consider the Po distribution with . As alternatives we consider the discrete uniform distribution on the values with , the binomial distribution Bin with and , the negative binomial distribution , with and , Poisson mixtures of the form for and , a 0.9/0.1 mixture of Po(3) and point mass in 0 denoted by , the discrete Weibull distribution with and . For pseudo random number generation of and the package extraDistr, see [W:2019], was used. Note that a major part of these alternatives is found in the simulation study presented in [GH:2000], Table 1 and 2, for comparison to other test statistics.

| Dist. / | 0.25 | 0.5 | 1 | 3 | 5 | 0.25 | 0.5 | 1 | 3 | 5 | ||

| Po(1) | 10 | 9 | 9 | 9 | 9 | 9 | 9 | 9 | 9 | 9 | ||

| Po(5) | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 10 | 10 | 9 | ||

| Po(10) | 10 | 10 | 10 | 10 | 10 | 9 | 10 | 10 | 9 | 10 | ||

| Po(30) | 10 | 11 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | ||

| 99 | 100 | 100 | 100 | 100 | 99 | 99 | 100 | 100 | 100 | |||

| 74 | 91 | 92 | 87 | 87 | 67 | 75 | 86 | 92 | 91 | |||

| 63 | 82 | 82 | 73 | 72 | 46 | 72 | 82 | 84 | 80 | |||

| 81 | 89 | 84 | 69 | 67 | 76 | 86 | 89 | 85 | 79 | |||

| 92 | 93 | 87 | 66 | 62 | 91 | 93 | 93 | 88 | 80 | |||

| 100 | 99 | 92 | 56 | 50 | 100 | 100 | 99 | 91 | 77 | |||

| Bin(2,5) | 98 | 98 | 95 | 80 | 77 | 98 | 98 | 98 | 96 | 92 | ||

| Bin(4,0.25) | 32 | 28 | 21 | 16 | 14 | 32 | 33 | 30 | 23 | 19 | ||

| Bin(10,0.1) | 11 | 10 | 9 | 10 | 9 | 11 | 11 | 11 | 10 | 10 | ||

| Bin(10,0.5) | 89 | 69 | 35 | 17 | 15 | 91 | 82 | 65 | 34 | 24 | ||

| Bin(20,0.25) | 26 | 17 | 12 | 11 | 11 | 28 | 23 | 16 | 12 | 11 | ||

| Bin(50,0.1) | 11 | 10 | 10 | 10 | 10 | 11 | 11 | 10 | 10 | 10 | ||

| 90 | 87 | 78 | 62 | 58 | 90 | 89 | 87 | 79 | 71 | |||

| 60 | 55 | 41 | 29 | 26 | 60 | 59 | 53 | 42 | 36 | |||

| 41 | 37 | 27 | 17 | 18 | 41 | 39 | 35 | 27 | 22 | |||

| 16 | 15 | 12 | 10 | 11 | 16 | 16 | 14 | 12 | 11 | |||

| 90 | 74 | 37 | 14 | 13 | 89 | 82 | 66 | 31 | 19 | |||

| 53 | 35 | 17 | 10 | 10 | 54 | 42 | 31 | 16 | 12 | |||

| 35 | 23 | 13 | 10 | 10 | 35 | 28 | 20 | 13 | 11 | |||

| 14 | 12 | 10 | 9 | 9 | 15 | 13 | 12 | 10 | 10 | |||

| 100 | 100 | 95 | 63 | 55 | 100 | 100 | 99 | 94 | 83 | |||

| 79 | 67 | 38 | 17 | 15 | 80 | 75 | 63 | 36 | 24 | |||

| 29 | 20 | 14 | 10 | 10 | 29 | 24 | 19 | 13 | 11 | |||

| 91 | 82 | 54 | 22 | 20 | 92 | 88 | 79 | 52 | 34 | |||

| 20 | 15 | 11 | 10 | 10 | 20 | 18 | 15 | 11 | 11 | |||

| 11 | 10 | 9 | 10 | 10 | 11 | 10 | 11 | 9 | 9 | |||

| 43 | 37 | 26 | 17 | 16 | 42 | 41 | 36 | 26 | 22 | |||

| 90 | 87 | 79 | 61 | 58 | 90 | 89 | 87 | 78 | 71 | |||

| 39 | 38 | 34 | 30 | 28 | 39 | 39 | 39 | 35 | 32 | |||

| 100 | 100 | 99 | 86 | 81 | 100 | 100 | 100 | 99 | 96 | |||

| 59 | 58 | 53 | 50 | 49 | 59 | 58 | 58 | 54 | 54 | |||

| 14 | 15 | 16 | 16 | 18 | 13 | 13 | 14 | 15 | 17 | |||

| 43 | 37 | 27 | 19 | 18 | 44 | 43 | 38 | 29 | 24 | |||

| 14 | 14 | 16 | 16 | 15 | 14 | 14 | 14 | 14 | 16 | |||

B.2 Testing for gamma distribution

As alternative families of distributions we consider the following distributions with scale parameter fixed to 1 (which can be done w.l.o.g. due to invariance properties of the considered estimators): The Weibull distribution , the inverse Gaussian law , the lognormal law , the power distribution , the shifted-Pareto distribution , the Gompertz law and the linear increasing failure rate law . For details on the densities of these probability laws, see [17]. We chose these families, and a significance level of 0.05 for easy comparison to the existing simulation studies in [4].

| Dist. / | 1 | 3 | 5 | 10 | 1 | 3 | 5 | 10 | ||

| 4 | 4 | 5 | 4 | 4 | 4 | 4 | 4 | |||

| 3 | 4 | 4 | 5 | 4 | 4 | 4 | 4 | |||

| 2 | 3 | 4 | 4 | 3 | 4 | 4 | 4 | |||

| 1 | 1 | 2 | 3 | 1 | 2 | 2 | 3 | |||

| 0 | 1 | 2 | 2 | 1 | 2 | 2 | 2 | |||

| W | 22 | 31 | 32 | 32 | 30 | 33 | 33 | 33 | ||

| W | 1 | 3 | 3 | 4 | 3 | 3 | 3 | 3 | ||

| W | 1 | 8 | 14 | 18 | 5 | 12 | 15 | 17 | ||

| IG(0.5) | 32 | 66 | 73 | 74 | 57 | 70 | 73 | 73 | ||

| IG(1.5) | 5 | 28 | 38 | 43 | 18 | 34 | 38 | 43 | ||

| IG(3) | 1 | 11 | 19 | 26 | 7 | 15 | 19 | 24 | ||

| LN(0.5) | 1 | 9 | 17 | 24 | 5 | 13 | 17 | 22 | ||

| LN(0.8) | 8 | 33 | 42 | 48 | 22 | 39 | 44 | 47 | ||

| LN(1.5) | 53 | 75 | 75 | 77 | 69 | 76 | 77 | 77 | ||

| PW(1) | 64 | 91 | 91 | 86 | 90 | 90 | 88 | 86 | ||

| PW(2) | 52 | 62 | 53 | 51 | 64 | 52 | 50 | 50 | ||

| PW(4) | 20 | 12 | 12 | 16 | 12 | 10 | 12 | 15 | ||

| SP(1) | 79 | 88 | 89 | 89 | 86 | 89 | 89 | 89 | ||

| SP(2) | 38 | 57 | 60 | 60 | 52 | 60 | 60 | 60 | ||

| Go(2) | 9 | 36 | 42 | 46 | 33 | 40 | 42 | 44 | ||

| Go(4) | 15 | 58 | 65 | 70 | 51 | 64 | 66 | 68 | ||

| LF(2) | 3 | 8 | 9 | 12 | 7 | 9 | 10 | 11 | ||

| LF(4) | 3 | 11 | 13 | 16 | 9 | 12 | 14 | 15 | ||

B.3 Testing for the generalized Dickman distribution

We borrow the alternatives from Subsection B.2 and show the results in Table 6. Here we fix the nominal level to .

| Dist. / | 0.25 | 0.5 | 1 | 3 | 5 | 0.25 | 0.5 | 1 | 3 | 5 | ||

| 8 | 9 | 10 | 9 | 10 | 9 | 9 | 9 | 10 | 10 | |||

| 8 | 9 | 9 | 9 | 9 | 10 | 10 | 10 | 10 | 10 | |||

| 9 | 9 | 10 | 10 | 10 | 9 | 10 | 10 | 10 | 10 | |||

| 8 | 10 | 9 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |||

| 9 | 10 | 10 | 9 | 11 | 10 | 10 | 9 | 10 | 10 | |||

| 45 | 53 | 64 | 69 | 70 | 65 | 69 | 70 | 70 | 69 | |||

| 14 | 31 | 38 | 36 | 33 | 39 | 37 | 35 | 32 | 33 | |||

| 15 | 47 | 61 | 63 | 62 | 64 | 64 | 63 | 61 | 61 | |||

| 9 | 27 | 57 | 90 | 94 | 66 | 82 | 90 | 94 | 94 | |||

| 10 | 27 | 60 | 98 | 99 | 71 | 91 | 98 | 100 | 100 | |||

| W(0.5) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | ||

| W(1.5) | 6 | 10 | 13 | 18 | 21 | 15 | 17 | 20 | 21 | 21 | ||

| W(3) | 66 | 99 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | ||

| IG(0.5) | 78 | 83 | 92 | 97 | 97 | 93 | 96 | 97 | 97 | 96 | ||

| IG(1.5) | 21 | 37 | 52 | 63 | 57 | 56 | 62 | 63 | 55 | 50 | ||

| IG(3) | 15 | 45 | 68 | 81 | 76 | 72 | 78 | 80 | 75 | 70 | ||

| LN(0.5) | 14 | 43 | 68 | 85 | 84 | 74 | 82 | 84 | 80 | 78 | ||

| LN(0.8) | 37 | 40 | 56 | 85 | 87 | 57 | 72 | 82 | 87 | 86 | ||

| LN(1.5) | 99 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | ||

| PW(1) | 93 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | ||

| PW(2) | 21 | 60 | 86 | 96 | 97 | 92 | 96 | 96 | 97 | 97 | ||

| PW(4) | 5 | 9 | 17 | 28 | 31 | 20 | 25 | 29 | 31 | 32 | ||

| SP(1) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | ||

| SP(2) | 84 | 86 | 92 | 97 | 97 | 93 | 96 | 97 | 98 | 97 | ||

| Go(2) | 7 | 11 | 17 | 35 | 39 | 20 | 27 | 35 | 39 | 40 | ||

| Go(4) | 9 | 15 | 25 | 36 | 28 | 28 | 36 | 35 | 27 | 24 | ||

| LF(2) | 7 | 26 | 50 | 76 | 80 | 59 | 69 | 76 | 80 | 82 | ||

| LF(4) | 27 | 79 | 96 | 99 | 100 | 98 | 99 | 99 | 100 | 100 | ||

B.4 Testing the fit to the family of compound Poisson exponential distributions

The compound Poisson Exponential distribution is denoted by CP, where is the parameter of the Poisson distribution and the parameter of the exponential law, see Example 5 item 1. We borrow the alternatives from Subsection B.2 and add a mixed compound Poisson exponential model by simulating MCP for and , , and . Here we fixed the nominal level to . We show the results in Table 7. Note that the procedure is conservative in view of the type-I error and shows acceptable performance against most of the alternatives, although also practically blind against some alternatives. Note that the sample size is not large, so for bigger data sets the power performance will increase. It would be interesting to compare the power performance to the methods of [13] and [BG:2023].

| Dist. / | 1 | 3 | 5 | 10 | |

| CP(1,Exp(1)) | 2 | 2 | 3 | 3 | |

| CP(2,Exp(2)) | 3 | 4 | 4 | 3 | |

| CP(3,Exp(2)) | 2 | 3 | 3 | 3 | |

| CP(4,Exp(2)) | 2 | 3 | 3 | 4 | |

| 5 | 7 | 5 | 4 | ||

| 7 | 10 | 10 | 9 | ||

| 5 | 9 | 10 | 10 | ||

| 2 | 3 | 4 | 6 | ||

| 1 | 2 | 2 | 3 | ||

| IG(0.5) | 19 | 35 | 40 | 42 | |

| IG(1.5) | 34 | 40 | 40 | 37 | |

| IG(3) | 31 | 31 | 31 | 30 | |

| LN(0.5) | 32 | 33 | 32 | 31 | |

| LN(0.8) | 25 | 42 | 45 | 46 | |

| LN(1.5) | 1 | 2 | 3 | 6 | |

| PW(1) | 80 | 78 | 77 | 74 | |

| PW(2) | 32 | 29 | 26 | 24 | |

| PW(4) | 5 | 4 | 3 | 3 | |

| SP(1) | 0 | 0 | 1 | 2 | |

| SP(2) | 9 | 22 | 29 | 35 | |

| Go(2) | 17 | 16 | 15 | 14 | |

| Go(4) | 34 | 39 | 38 | 37 | |

| W | 10 | 12 | 12 | 12 | |

| W | 2 | 3 | 3 | 3 | |

| MCP(1,1,1,6;0.25) | 11 | 12 | 13 | 10 | |

| MCP(1,1,2,6;0.25) | 30 | 34 | 34 | 30 | |

| MCP(1,1,3,6;0.25) | 36 | 40 | 38 | 39 | |

| MCP(1,1,4,6;0.25) | 29 | 37 | 37 | 39 | |

| MCP(1,1,1,5;0.5) | 3 | 2 | 5 | 4 | |

| MCP(1,1,2,5;0.5) | 5 | 11 | 11 | 10 | |

| MCP(1,1,3,5;0.5) | 08 | 15 | 16 | 15 | |

| MCP(1,1,4,5;0.5) | 10 | 15 | 17 | 18 | |

| MCP(1,1,5,5;0.75) | 2 | 5 | 7 | 6 | |

| MCP(1,1,10,5;0.75) | 7 | 8 | 10 | 10 | |

| MCP(1,1,20,5;0.75) | 13 | 29 | 31 | 31 | |

| MCP(1,1,50,5;0.75) | 09 | 29 | 57 | 81 |