2023

1]Columbia University, USA 2]University of Virginia, USA 3]Rice University, USA 4]SIAT, Chinese Academy of Sciences, China 5]New York University (Shanghai), China 6]Northwestern University, USA 7]IDEA Research, International Digital Economy Academy, China

Dynamic Datasets and Market Environments for Financial Reinforcement Learning

Abstract

The financial market is a particularly challenging playground for deep reinforcement learning due to its unique feature of dynamic datasets. Building high-quality market environments for training financial reinforcement learning (FinRL) agents is difficult due to major factors such as the low signal-to-noise ratio of financial data, survivorship bias of historical data, and model overfitting. In this paper, we present FinRL-Meta, a data-centric and openly accessible library that processes dynamic datasets from real-world markets into gym-style market environments and has been actively maintained by the AI4Finance community. First, following a DataOps paradigm, we provide hundreds of market environments through an automatic data curation pipeline. Second, we provide homegrown examples and reproduce popular research papers as stepping stones for users to design new trading strategies. We also deploy the library on cloud platforms so that users can visualize their own results and assess the relative performance via community-wise competitions. Third, we provide dozens of Jupyter/Python demos organized into a curriculum and a documentation website to serve the rapidly growing community. The open-source codes for the data curation pipeline are available at https://github.com/AI4Finance-Foundation/FinRL-Meta

keywords:

Financial reinforcement learning, FinRL, dynamic dataset, market environment, AI4Finance, open finance1 Introduction

Financial reinforcement learning (FinRL) liu2021finrl ; hambly2021recent is a promising interdisciplinary field of finance and reinforcement learning, driven by the spirit of “trade with an (technology) edge”111Find a (technology) edge and position to win.. In the past decade, deep reinforcement learning (DRL) sutton2018reinforcement , as a disruptive technology, has delivered a superhuman performance in Atari games DQN , Go silver2016alphaGo1 ; silver2017alphaGo2 , StarCraft II vinyals2019grandmaster , the recent eye-catching ChatGPT ouyang2022training , and GPT-4 GPT4 . The financial market is a particularly challenging playground for DRL due to the unique feature of dynamic dataset, a sharp contrast to the static ImageNet dataset deng2009imagenet .

The static ImageNet dataset deng2009imagenet initiated the field of deep learning. Researchers designed and applied many deep neural network models to real-world visual applications. However, these applications deal with “static” datasets, such as MNIST, CIFAR-10, Yale Face Database, which are quite different from the financial market, where the data is dynamic in nature. The market trend, development of companies, and economic situation of countries are refreshing over time. To handle time-sensitive financial data, models have to learn up-to-date information and adapt to real-time market situations.

Existing works lussange2021modelling ; liu2021finrl ; pricope2021deep have already applied various DRL algorithms in financial applications, including investigating market fragility raberto2001agent , designing profitable strategies liu2018practical ; yang2020deep ; zhang2020deep , and assessing portfolio risk lussange2021modelling ; bao2019multiagent . Exemplar financial trading tasks include

-

•

Fundamentals analysis: e.g., value investing, growth investing

-

•

Technical analysis: commodity trading advisor (CTA), momentum, trend following, etc.

-

•

Macro strategies: e.g., bonds, gold, crude oil, forex.

-

•

Quantitative strategies: statistical arbitrage, merge/event arbitrage, etc.

-

•

High-frequency trading: many different sub-strategies inside.

Some recent works lussange2021modelling ; amrouni2021abides ; market_simulator have shown that DRL can deliver better trading performance than classical strategies and conventional machine learning methods do on these tasks regarding cumulative return and Sharpe ratio. However, these works are difficult to reproduce. Several recent efforts have been dedicated to facilitating reproducibility. The FinRL library liu2020finrl ; liu2021finrl provided an open-source framework for financial reinforcement learning. Unfortunately, it only focused on the reproducibility of backtesting performance by providing several market environments. A conference version of FinRL-Meta liu2022finrlmeta provided a financial dataset and benchmark, but it did not provide a dynamic dataset, sentiment data, and market simulator.

However, building near-real market environments for financial reinforcement learning (FinRL) is difficult due to major factors such as low signal-to-noise ratio (SNR) of financial data, partial observation, reward delay, survivorship bias of historical data, and model overfitting. Such a simulation-to-reality gap DulacArnold2020AnEI ; dulac2019challenges degrades the performance of DRL strategies in real markets. A good backtest performance does not necessarily reflect the actual trading performance since the financial dataset could be susceptible to flaws like missing data, noise, and anomalies.

Data-centric AI whang2023data ; zha2023data ; zha2023data2 is a new trend that appeals to shift the focus from model to data. It focuses on the systematic engineering of data in building AI systems, which can lead to better model behaviors in the real world zha2023data . When training DRL agents, if the data is susceptible to flaws, even if our model/strategy can have a good backtest performance, it will be hard to tell whether the model can actually perform well in the real deployment or is just a result of overfitting the dataset. Therefore, building a standard workflow to ensure data quality is imperative to foster reliable market environments and benchmarks and motivate the research and industrialization of FinRL.

In this paper, we present FinRL-Meta, a data-centric and openly accessible library that has been actively maintained by the AI4Finance community, with a particular focus on data quality. The aim of FinRL-Meta is to create an infrastructure to enable real-time paper trading and facilitate the real-world adoption of FinRL technology. This contributes to the broader RL or ML research community since it allows researchers to test DRL agents in real and dynamic environments.

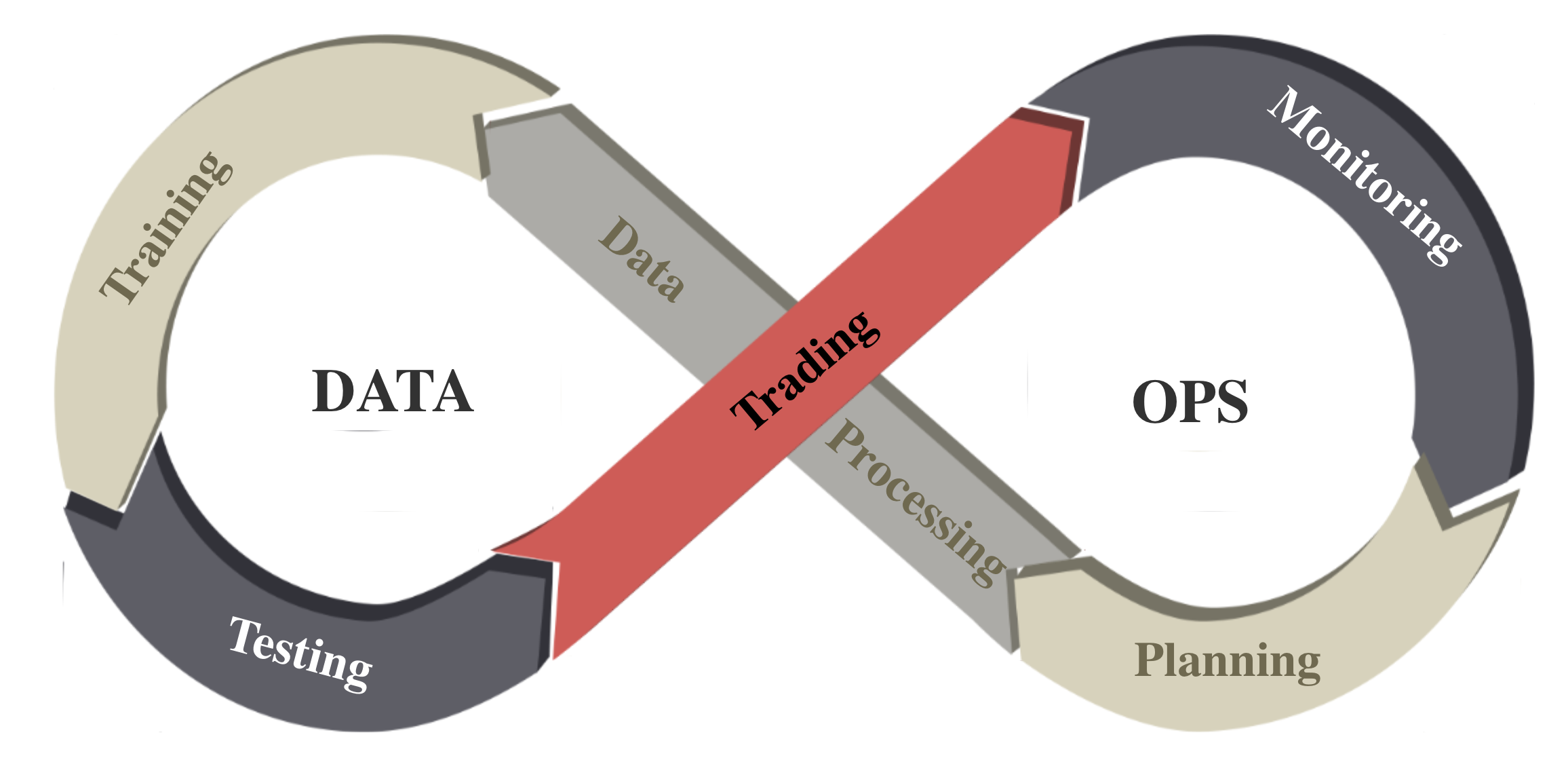

To handle highly unstructured financial big data, we follow the DataOps paradigm and implement an automatic data curation pipeline in Fig. 1 (left). The DataOps paradigm atwal2019practical ; ereth2018dataops refers to a set of practices, processes, and technologies that combines automated data engineering and agile development ereth2018dataops . It helps reduce the cycle time of data engineering and improve data quality. Following the DataOps paradigm, we design an RLOps pipeline tailored for FinRL to continuously produce DRL benchmarks on dynamic market datasets. The RLOps pipeline consists of the following steps:

-

•

The first step is task planning, such as stock trading, portfolio allocation, and cryptocurrency trading.

-

•

Then, we do data processing, including data accessing and cleaning, and feature engineering.

-

•

Next step is where RL takes part in. In particular, the training-testing-trading process, detailed in Fig. 4.

-

•

The final step is performance monitoring.

Fig. 1 (right) shows the overview of FinRL-Meta. First, following the DataOps paradigm atwal2019practical ; ereth2018dataops , we provide hundreds of market environments through an automatic data curation pipeline that collects dynamic datasets from real-world markets and processes them into standard gym-style market environments. Second, we reproduce popular papers as benchmarks, including high-frequency stock trading, cryptocurrency trading and stock portfolio allocation, serving as stepping stones for users to design new strategies. With the help of the data curation pipeline, we hold our benchmarks on cloud platforms so that users can visualize their own results and assess the relative performance via community-wise competitions. Third, we provide dozens of Jupyter/Python demos as educational materials, organized in a curriculum for community newcomers with different levels of proficiency and learning goals. At the same time, we maintain a documentation website to serve the rapidly growing community.

The remainder of this paper is organized as follows. Section 2 describes related works. Section 3 presents an overview of FinRL and the FinRL-Meta framework. Section 4 describes the automatic data curation pipeline of FinRL-Meta. In Section 5, we present several homegrown examples using FinRL-Meta. Finally, we conclude this paper and discuss future works in Section 6.

2 Related Works

We review the technology landscape and existing works on financial big data, data-centric AI, DataOps practices, data-driven RL, and FinRL applications.

2.1 Handling Financial Big Data

Financial big data: Financial big data refers to the vast amount of data that is available in the financial industry from various sources. By analyzing this data, traders can make informed decisions about investments. Like all big data, financial big data also shares the four key properties, known as the 4V’s222The Four V’s of Big Data: https://opensistemas.com/en/the-four-vs-of-big-data/: volume, variety, velocity, and veracity.

-

•

1) Volume. Financial big data has a large scale. Now, the market can support high-frequency trading at the level of microseconds. With high-frequency trading, billions of shares can be traded within a day, generating an enormous amount of data that records these transactions.

-

•

2) Velocity. As the market refreshes at the microsecond level, the velocity of data transmission and processing is very important. Companies are continually seeking ways to speed up data transmission and processing to minimize delays and errors. This includes utilizing closer physical proximity to data vendors, improving cable materials, and developing more efficient algorithms.

-

•

3) Variety. There are structured and unstructured data in finance. A data vendor may provide structured data for users to access, usually the volume-price data. Besides that, there are a huge amount of alternative data from news, social media, and financial reports that are considered during the process of generating indicators.

-

•

4) Veracity. Data quality and availability are extremely important. However, big data’s larger scale also brings a latent risk of lack of veracity. Due to its close relationship with money and assets, data quality is particularly sensitive in the finance industry.

Data-centric AI: With the 4V’s properties, the quality of financial data plays a critical role in enabling strong FinRL models in real deployments. In the past, FinRL research was conducted in a model-centric way, with an emphasis on improving model designs using predetermined datasets. However, solely depending on static datasets does not necessarily result in satisfactory model performance in real-world scenarios, especially when the dataset is flawed mazumder2022dataperf . Furthermore, neglecting the importance of data quality can trigger data cascades sambasivan2021everyone , leading to reduced accuracy in real deployments.

Recently, the attention of researchers and practitioners has gradually shifted toward data-centric AI whang2023data ; zha2023data ; zha2023data2 , with a stronger emphasis on improving data quality by the systematic engineering of data. The benefits of data-centric AI have been validated by both researchers and practitioners zha2023data ; polyzotis2021can . In order to drive tangible advancements in FinRL research and deployment, we have made our library data-centric by building upon dynamic datasets and implementing an automated data curation pipeline for quality control.

DataOps practices: From another perspective, a standardized development cycle is necessary for effectively handling highly unstructured financial big data. DataOps ereth2018dataops ; atwal2019practical applies the ideas of lean development and DevOps to the data science field. DataOps practices have been developed in companies and organizations to improve the quality and efficiency of data analytics atwal2019practical . These implementations consolidate various data sources, and unify and automate the pipeline of data analytics, including data accessing, cleaning, analysis, and visualization.

The DataOps paradigm ereth2018dataops , or more accurately the methodology, is a way of organizing people, processes and technology to deliver reliable and high-quality data efficiently to all its users. The practice of DataOps focuses on enabling collaboration across the organization to drive agility, speed of delivery and new data initiatives. By leveraging the power of automation, DataOps aims to address the challenges associated with inefficiencies in access, preparation, integration and availability of data.

Many researchers studied FinRL applications liu2018practical ; yang2020deep ; zhang2020deep ; ardon2021towards ; amrouni2021abides ; coletta2021towards by building their own market environments. Despite the above-mentioned open-source libraries that provide some valuable settings, there are no established benchmarks yet. On the other hand, the data accessing, cleaning and feature/factor extraction processes are usually limited to data sources like Yahoo Finance and Wharton Research Data Services (WRDS).

However, the DataOps methodology has not been applied to FinRL research. Most researchers access data, clean data, and extract technical indicators (features) in a case-by-case manner, which involves heavy manual work and may not guarantee high data quality.

2.2 Data-Driven Reinforcement Learning

Data-driven RL: If a policy is learned from a collected dataset, it is promising that we can get the data-driven strategy333Note that “data-driven” and “data-centric” are two distinct concepts. The former refers to utilizing data to guide policy training, whereas the latter means placing data quality in the central role in FinRL development. The endeavors of “data-driven” and “data-centric” approaches complement each other in their efforts to enhance overall policy performance.. Based on the datasets, RL will be a powerful method to perform data-driven strategies without any interaction with the environment or human intervention. RL will greatly reduce human labor and therefore improves automation.

Offline RL levine2020offline : Offline RL is a typical data-driven formulation of reinforcement learning problems. In offline RL, agents learn behaviors from a fixed dataset, without the process of exploration in the environment. It has great potential in tasks where collecting real-time data is inconvenient, either too expensive or risky(e.g., robotic tasks, autonomous driving), or the amount of data is limited (e.g., stock market, clinical surgery).

Curriculum learning: Curriculum learning is a technique that trains the model using multiple stages from simple to complex. With fine-tuning for specific tasks, curriculum learning could have faster convergence and find better minima. jpmorgan2023asset proposed to use two stages of training for the portfolio management task, first using a neural network to fit the mean-variance optimization, then fine-tuning the model with online reinforcement learning. Well-known products like AlphaGo and ChatGPT both use similar techniques.

RL from human feedback (RLHF): The idea of RLHF was first introduced by OpenAI and DeepMind in 2017 christiano2017deep . RLHF allows human feedback as part of the agent’s reward function, making it a better alignment of model performance and human expectations. One of the main reasons that ChatGPT outperforms other large language models is its appropriate usage of RLHF.

Next, we review popular projects:

-

•

OpenAI gym brockman2016openai Environments are crucial for training DRL agents sutton2018reinforcement . OpenAI gym provides standardized environments for a collection of benchmark problems that expose a common interface, which is widely supported by many libraries stable-baselines ; liang2018rllib ; elegantrl . Three trading environments, TradingEnv, ForexEnv, and StocksEnv, are included to support stock and FOREX markets. However, it has not been updated for years.

-

•

Game of Go. AlphaGo silver2016alphaGo1 and AlphaGo Zero silver2017alphaGo2 are programs for games of Go. AlphaGo combines Monte Carlo simulation with value and policy networks, and becomes the first computer program that defeats world champions in Go game. AlphaGo Zero is the updated version, it learns by reinforcement learning by playing against itself, without extra human data or knowledge. These programs also provide suggestions for financial reinforcement learning, e.g., how to train the policy network by supervised learning and self-play.

-

•

D4RL fu2020d4rl introduces the idea of datasets for deep data-driven reinforcement learning (D4RL). It provides benchmarks in offline RL. However, D4RL does not provide financial environments.

-

•

FinRL liu2020finrl ; liu2021finrl is an open-source library that builds a full pipeline for financial reinforcement learning. It contains three market environments, i.e., stock trading, portfolio allocation, and crypto trading, and two data sources, i.e., Yahoo Finance and WRDS. However, those market environments of FinRL cannot meet the community’s growing demands.

-

•

NeoRL qin2021neorl collected offline RL environments for four areas, CityLearn vazquez2019cityLearn , FinRL liu2020finrl ; liu2021finrl , Industrial Benchmark hein2017benchmark , and MuJoCo todorov2012mujoco , where each area contains several gym-style environments. Regarding financial aspects, it directly imports market environments from FinRL.

-

•

ChatGPT ouyang2022training and GPT-4 GPT4 are large language models for dialogues, which can be used as the data source and feature/factor calculation for data-driven financial reinforcement learning. However, it is not as professional as we think; therefore, how to train as an intelligent advisor is an important problem. We can follow several steps using dialogue, including guides, listing examples, admitting mistakes, etc.

As a new rising technology, RL is a promising tool for complicated financial tasks. Recently, many Wall Street companies have shown great interest in this rising technology. However, RL’s instability makes it hard to put into practice in the industry. AlphaGo and ChatGPT’s success in data-feed multi-stage learning could be a great approach to adopting RL into their workflow. Hedge funds first feed their private data into supervised learning (imitation learning) models for training, and then use reinforcement learning to fine-tune the model based on interaction with the market environments to achieve super-human performance.

2.3 Financial Reinforcement Learning (FinRL)

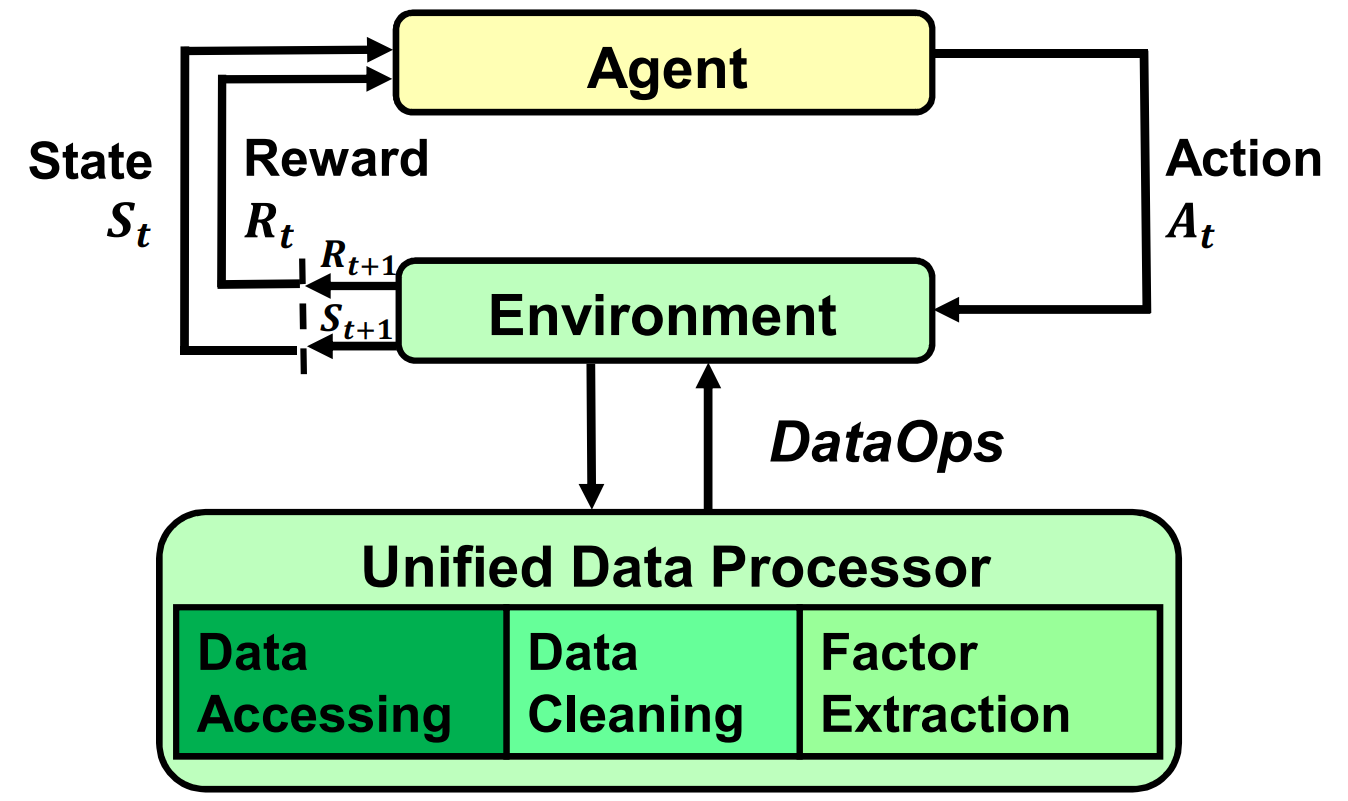

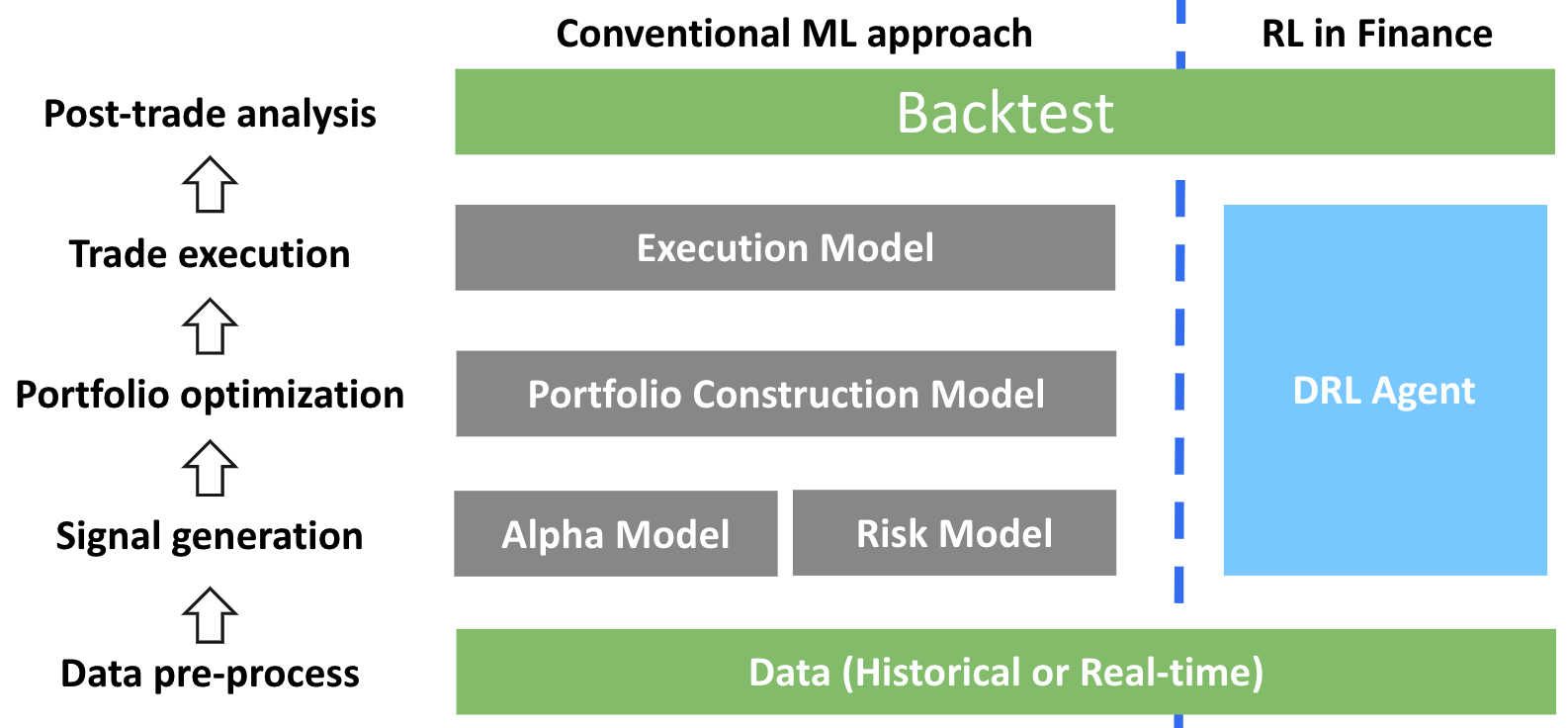

RLOps paradigm in finance. Algorithmic trading Treleaven2013AlgorithmicTR ; Nuti2011AlgorithmicT has been widely adopted in financial investments. The lifecycle of a conventional machine learning strategy may include five general stages, as shown in Fig. 2 (left), namely data pre-processing, modeling and trading signal generation, portfolio optimization, trade execution, and post-trade analysis. Recently, deep reinforcement learning (DRL) silver2016alphaGo1 ; silver2017alphaGo2 ; sutton2018reinforcement has been recognized as a powerful approach for quantitative finance, since it has the potential to overcome some important limitations of supervised learning, such as the difficulty in label specification and the gap between modeling, positioning, and order execution.

We would like to extend the principle of MLOps alla2021mlops 444MLOps is an ML engineering culture and practice that aims at unifying ML system development (Dev) and ML system operation (Ops). to the RLOps in finance paradigm that implements and automates the continuous training (CT), continuous integration (CI), and continuous delivery (CD) for trading strategies. Such a paradigm will have vast profit potential from a broadened horizon and fast speed, which is critical for wider DRL adoption in real-world financial tasks. The RLOps in finance paradigm, as shown in Fig. 2 (right), integrates middle stages (i.e., modeling and trading signal generation, portfolio optimization, and trade execution) into a DRL agent. Such a paradigm aims to help quantitative traders develop an end-to-end trading strategy with a high degree of automation, which removes the latency between stages and results in a compact software stack. The major benefit is that it can explore the vast potential profits behind the large-scale financial data, exceeding the capacity of human traders; thus, the trading horizon is lifted into a potentially new dimension. Also, it allows traders to continuously update trading strategies, which equips traders with an edge in a highly volatile market. However, the large-scale financial data and fast iteration of trading strategies bring imperative challenges in terms of computing power.

FinRL applications: Along with the RLOps paradigm, different FinRL applications can be constructed and deployed. Electronic trading is popular in many countries and is used in stock exchanges, electronic order books, over-the-counter markets, foreign exchange, etc. Electronic trading enhances liquidity since traders can easily buy or sell assets. We describe several FinRL applications inspired by a complete survey hambly2021recent , including optimal execution, portfolio optimization, option pricing and hedging, market making, smart order routing, and robo-advising.

-

•

1) Optimal execution is the problem of maximizing the return from buying or selling a given amount of an asset within a given time period. A classical framework is the Almgren–Chriss model, which relies heavily on the assumptions of the dynamics and the permanent and temporary price impact. There are several popular criteria to evaluate the performance of execution strategies, e.g., the profit and loss, implementation shortfall, and the Sharp ratio.

-

•

2) Portfolio optimization aims to maximize some objective function by selecting and trading the best portfolio of assets. One typical model is mean-variance portfolio optimization, which aims to maximize the return for a given risk measured by variance.

-

•

3) Option pricing and hedging are important in finance. The Black-Scholes model is a typical mathematical model which aims to get the price of a European option given several constraints: stock price, expiration time, and the payoff at expiry.

-

•

4) Market making aims to earn the bid-ask spread by providing liquidity to the market by placing buy/sell limit orders in the limit order books.

-

•

5) Robo-advising or automated investment managing provides online financial advice with minimal human intervention. ChatGPT ouyang2022training and GPT-4 GPT4 may be promising advisors if we guide them step by step.

3 FinRL Tasks and FinRL-Meta Framework

| Key components | Attributes |

|---|---|

| State | Balance ; Shares |

| \cdashline2-3[0.8pt/2pt] | Opening/high/low/close price |

| \cdashline2-3[0.8pt/2pt] | Trading volume |

| \cdashline2-3[0.8pt/2pt] | Fundamental indicators; Technical indicators |

| \cdashline2-3[0.8pt/2pt] | Social data; Sentiment data |

| \cdashline2-3[0.8pt/2pt] | Alpha and beta signals; Smart beta indexes, etc. |

| Action | Buy/Sell/Hold |

| \cdashline2-3[0.8pt/2pt] | Short/Long |

| \cdashline2-3[0.8pt/2pt] | Portfolio weights |

| Reward | Change of portfolio value |

| \cdashline2-3[0.8pt/2pt] | Portfolio log-return |

| \cdashline2-3[0.8pt/2pt] | Sharpe ratio |

| Environments | Dow-, S&P-, NASDAQ- |

| \cdashline2-3[0.8pt/2pt] | Cryptocurrencies |

| \cdashline2-3[0.8pt/2pt] | Foreign currency and exchange |

| \cdashline2-3[0.8pt/2pt] | Futures; Options; ETFs; Forex |

| \cdashline2-3[0.8pt/2pt] | CN securities; US securities |

| \cdashline2-3[0.8pt/2pt] | Paper trading; Live Trading |

We introduce the Markov Decision Process (MDP) as a mathematical model of FinRL tasks, summarize FinRL challenges, and then provide an overview of the proposed FinRL-Meta framework.

3.1 Modeling Financial Reinforcement Learning (FinRL)

FinRL tasks in general take the form of sequential decision-making problems, which can be mathematically formulated as a Markov Decision Process (MDP) with five-tuple as follows

-

•

State space consists of all possible states;

-

•

Action space consists of all available actions;

-

•

Reward function assigns a real-valued reward to a transition ;

-

•

Transition probability models the dynamics of a system (a.k.a., environment);

-

•

Factor discounts a future reward back to its present value.

MDP is a well-formed mathematical model for sequential decision-making tasks in that a decision-maker can partially or fully influence the outcome. State and action define the input and output for decision-making tasks, and reward function allows a model to learn by goal-seeking optimization. Transition probability allows the target problem to be stochastic, which is usually closer to reality. The discount factor makes the model consider the future reward when making decisions.

We summarize the state spaces, action spaces, and reward functions of FinRL applications in Table 1. States usually demonstrate the condition of market and the assets, such as the balance, shares of stocks, OHLCV data, technical indicators, sentiment data, etc. Actions are the operations allowed in the market, including buy/sell/hold certain shares of the stock, short or long, change of portfolio weights on stocks, etc. The reward functions indicate what kind of objective we want the agent to achieve, for example, a change of portfolio value (a larger positive change leads to a larger positive reward, vice versa) for maximizing excess return, Sharpe ratio for balancing return and risk, etc.

Objective function: Many financial tasks can be written in the form of optimization problems. When using RL, the objective function is to find a policy that maximizes the discounted cumulative return .

Example I. For the stock trading task liu2018practical on constituent stocks of the Dow Jones Industrial Average (DJIA) index, we specify the “state-action-reward” as follows:

-

•

State , where scalar is the remaining balance in the account, is the prices of stocks, is a feature vector and each stock has technical indicators, and denotes the share holdings, where is the set of non-negative real numbers.

-

•

Action denotes the trading operations on the 30 stocks, i.e., . When an entry , it means a buy-in of shares on the -th stock, negative action for selling, and zero action keeps unchanged.

-

•

Reward function : Reward is an incentive signal to encourage the trading agent to execute action at state . In the stock trading task liu2018practical , the reward function is set to be the change of total asset values, i.e., , where and are the total asset values at state and , respectively, i.e., .

Example II. Another task is portfolio optimization, also on the 30 constituent stocks of the Dow Johnes Industrial Average (DJIA) index. The "state-action-reward" are specified as follows:

-

•

State , where is the current prices of stocks, is a feature vector and each stock has technical indicators, is the portfolio weight allocated on last time, and is the total asset value at time .

-

•

Action denotes the new weights assigned to each of the 30 stocks. Note there are always . Each means allocating amount of total asset on the -th stock. After is applied, in the state will record the new , and will be recalculated.

-

•

Reward function : Similar to the stock trading task, the reward of portfolio optimization task is also set to be the change of total asset values.

3.2 FinRL Challenges

Training and testing environments based on historical data may not simulate real markets accurately due to the simulation-to-reality gap DulacArnold2020AnEI ; dulac2019challenges , and thus a trained agent cannot be directly deployed in real-world markets. We summarize the main FinRL challenges as follows:

-

•

Low signal-to-noise ratio (SNR): Data from different sources may contain large noise wilkman2020feasibility such as random noise, outliers, etc. It is challenging to identify alpha signals or build smart beta indices using noisy datasets.

-

•

Survivorship bias of historical market data: Survivorship bias is caused by a tendency to focus on existing stocks and funds without consideration of those that are delisted brown1992survivorship . It could lead to an overestimation of stocks and funds, which will mislead the agent.

-

•

Model overfitting: Existing research mainly report backtesting results. It is highly possible that authors are tempted to tune hyper-parameters and retrain the agent multiple times 555There is information leakage. to obtain better backtesting results, resulting in model overfitting gort2022deep ; de2018advances . This might lead to big trouble during real-time trading.

-

•

Delay: Financial markets have delays due to data transmission, reward feedback, and actuation. The true reward may be based on the users’ interaction with the markets, which may take several days. As the delay increases, the performance of deep reinforcement learning decreases.

-

•

Partial observation: The full observability assumption of financial markets can be extended to partial observation (the underlying states cannot be directly observed), i.e., partially observable Markov Decision Process (POMDP). A POMDP model utilizes a Hidden Markov Model (HMM) mamon2007hidden to model a time series that is caused by a sequence of unobservable states. Considering the noisy financial data, it is natural to assume that a trading agent cannot directly observe market states. Studies suggested that the POMDP model can be solved by using recurrent neural networks, e.g., an off-policy Recurrent Deterministic Policy Gradient (RDPG) algorithm liu2020adaptive , and a long short-term memory (LSTM) network that encodes partial observations into a state of a reinforcement learning algorithm rundo2019deep .

-

•

Multi-objective reward function: When we optimize one metric, some other metrics may need to be constrained or improved. Therefore, a trade-off between these metrics may be required. In addition, the reward formulation involves the weights of metrics, i.e., the weights should be fine-tuned manually.

-

•

Low interpretability: In deep reinforcement learning, neural networks are used to fit the Q-value functions and policies. However, neural networks are black-box; therefore, deep reinforcement learning is of low interpretability.

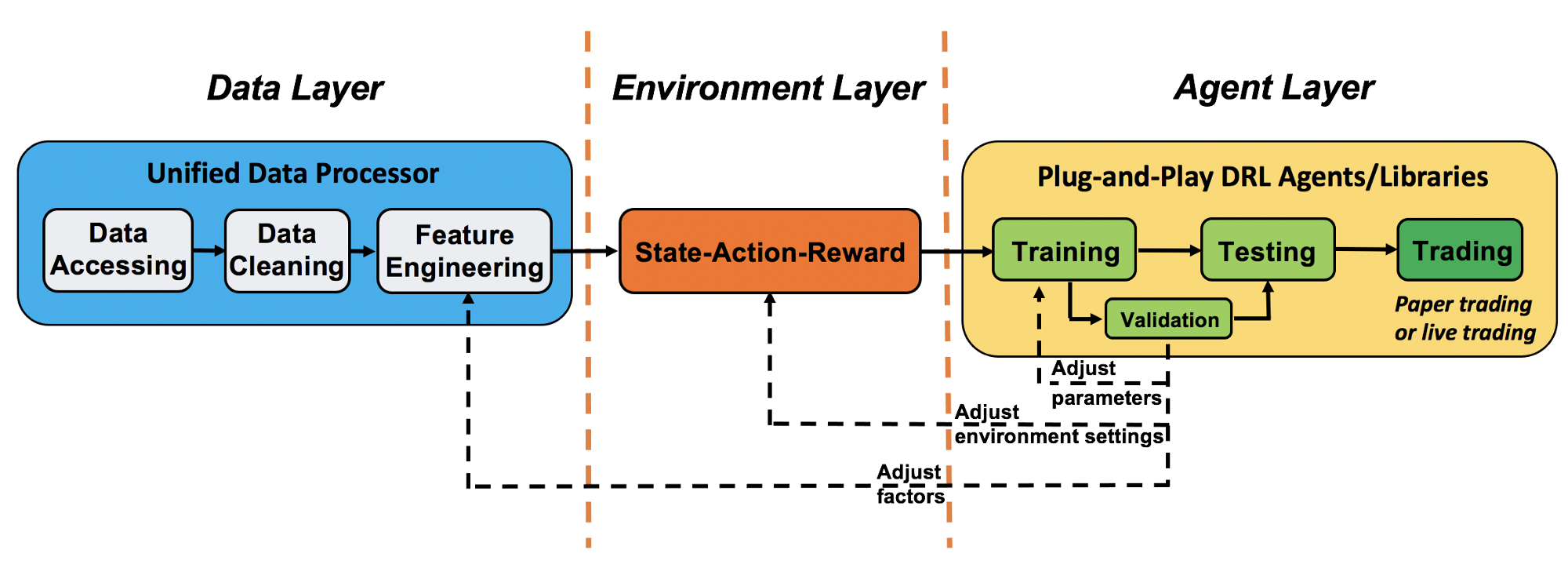

3.3 Overview of FinRL-Meta Framework

Following the DataOps paradigm in Fig. 1 and the standard process of data-centric AI zha2023data , FinRL-Meta builds a universe of market environments for data-driven financial reinforcement learning. FinRL-Meta follows the de facto standard of OpenAI Gym brockman2016openai and the lean principle of software development. We have an automatic pipeline using the dynamic dataset with the following steps: 1). task planning, 2). data processing, 3). training-testing-trading pipeline, 4). performance monitoring.

3.3.1 Layer Structure and Extensibility

We adopt a layered structure that consists of three layers, data layer, environment layer, and agent layer, as shown in Fig. 3. Layers interact through end-to-end interfaces, achieving high extensibility. For updates and substitutes inside a layer, this structure minimizes the impact on the whole system. Moreover, the layer structure allows easy extension of user-defined functions and fast updating of algorithms with high performance.

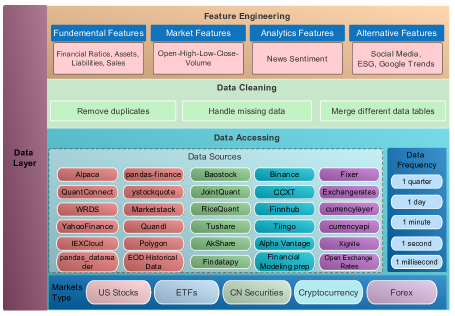

Data Layer: we follow the DataOps paradigm for data curation to reduce the cycle time of data engineering and improve data quality. First, in the data processing step, we provide APIs to collect time series price data and sentiment data from different platforms with a unified interface. Second, the data cleaning step will clean up the raw data, which is usually unstructured and contain different kinds of errors. Third, we will add technical indicators to the data to provide more information on the market in the feature engineering step.

Environment Layer: The well-processed data from the data layer will be made into a gym-style market environment in the environment layer. According to the chosen task, state-action-reward will be set. FinRL-Meta also provides the option of multiprocessing training via vector environment to accelerate the training process.

Agent Layer: we allow a user to plug in a DRL agent and play with a market environment from the environment layer. Currently, three libraries are supported, including Stable-baseline 3, RLlib, and ElegantRL. We call this plug-and-play mode, which will be introduced in detail later.

3.3.2 Dynamic Datasets and Training-Testing-Trading Pipeline

For dynamic financial data, it is crucial to keep the model learning the latest information from the market. However, it will be very time-consuming to process data and train the model frequently. Thus, FinRL-Meta brings forward the concept of the dynamic dataset.

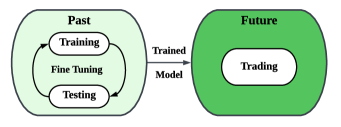

The dynamic dataset is a standardized workflow of downloading and processing data following the need for a “training-testing-trading” pipeline periodically. This makes the time of training controllable.

As shown in Fig. 4, we deploy a training-testing-trading pipeline. The DRL approach follows a standard end-to-end pipeline. The DRL agent is first trained in a training environment and then fined-tuned (adjusting hyperparameters) in a validation environment. Then the validated agent is tested on historical datasets (backtesting). Finally, the tested agent will be deployed in paper trading or live trading markets. Our construction of a dynamic dataset fits the training-testing-trading pipeline well, providing a potential standard workflow of financial reinforcement learning.

3.3.3 Plug-and-play Mode for DRL Algorithms

A DRL agent can be directly plugged in the above training-testing-trading pipeline. The following DRL libraries are supported:

-

•

ElegantRL elegantrl : Lightweight, efficient and stable algorithms using PyTorch.

-

•

Stable-Baselines3 stable-baselines : Improved DRL algorithms based on OpenAI Baselines.

-

•

RLlib liang2018rllib : An open-source DRL library that offers high scalability and unified APIs.

Take the stock trading task described in Section 3.1 as an example. We first download and preprocess the historical data of the 30 constituent stocks of the DJIA index. Then, we construct an environment with the state-action-reward specified in Section 4. Given this environment, we choose an algorithm from one of the above three DRL libraries, plug it in with default parameters, and train a trading agent. Users could compare the performances of different algorithms from the same library or different libraries.

4 Automatic Data Curation Pipeline for Market Environments

Financial big data is usually unstructured, which makes data curation necessary. Following the principles of data-centric AI whang2023data ; zha2023data ; zha2023data2 , we construct an automatic data curation pipeline to process and engineer data. Specifically, we process four types of data de2018advances , including fundamental data (e.g., earning reports), market data (e.g., OHLCV data), analytics (e.g., news sentiment), and alternative data (e.g., social media data, ESG data). In addition, we incorporate NLP features for financial sentiment analysis. We build market environments using these features, by following OpenAI gym-style APIs brockman2016openai .

4.1 Data Layer for Processing and Engineering Highly Unstructured Financial Big Data

Following the training data development pipeline in data-centric AI zha2023data , we develop a data layer using DataOps practices ereth2018dataops , shown in Fig. 5. We establish a standard pipeline for financial data engineering, which processes data from different sources into a unified market environment. The pipeline involves a data accessing module to collect data, as well as data cleaning and feature engineering modules to prepare data and transform it into a form that is appropriate for FinRL model training.

| Data Source | Type | Max Frequency | Raw Data | Preprocessed Data |

|---|---|---|---|---|

| Alpaca | US Stocks, ETFs | 1 min | OHLCV | Prices, indicators |

| Baostock | CN Securities | 5 min | OHLCV | Prices, indicators |

| Binance | Cryptocurrency | 1 s | OHLCV | Prices, indicators |

| CCXT | Cryptocurrency | 1 min | OHLCV | Prices, indicators |

| IEXCloud | NMS US securities | 1 day | OHLCV | Prices, indicators |

| JoinQuant | CN Securities | 1 min | OHLCV | Prices, indicators |

| QuantConnect | US Securities | 1 s | OHLCV | Prices, indicators |

| RiceQuant | CN Securities | 1 ms | OHLCV | Prices, indicators |

| Tushare | CN Securities | 1 min | OHLCV | Prices, indicators |

| WRDS | US Securities | 1 ms | Intraday Trades | Prices, indicators |

| YahooFinance | US Securities | 1 min | OHLCV | Prices, indicators |

| AkShare | CN Securities | 1 day | OHLCV | Prices, indicators |

| findatapy | CN Securities | 1 day | OHLCV | Prices, indicators |

| pandas_datareader | US Securities | 1 day | OHLCV | Prices, indicators |

| pandas-finance | US Securities | 1 day | OHLCV | Prices, indicators |

| ystockquote | US Securities | 1 day | OHLCV | Prices, indicators |

| Marketstack | 50+ countries | 1 day | OHLCV | Prices, indicators |

| finnhub | US Stocks, currencies, crypto | 1 day | OHLCV | Prices, indicators |

| Financial Modeling prep | US stocks, currencies, crypto | 1 min | OHLCV | Prices, indicators |

| EOD Historical Data | US stocks, and ETFs | 1 day | OHLCV | Prices, indicators |

| Alpha Vantage | Stock, ETF, forex, crypto, technical indicators | 1 min | OHLCV | Prices, indicators |

| Tiingo | Stocks, crypto | 1 day | OHLCV | Prices, indicators |

| Quandl | 250+ sources | 1 day | OHLCV | Prices, indicators |

| Polygon | US Securities | 1 day | OHLCV | Prices, indicators |

| fixer | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| Exchangerates | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| Fixer | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| currencylayer | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| currencyapi | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| Open Exchange Rates | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| XE | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

| Xignite | Exchange rate | 1 day | Exchange rate | Exchange rate, indicators |

4.1.1 Data Accessing

Users can connect data APIs of different market platforms in Table 2 via our common interfaces. Users can access data agilely by specifying the start date, end date, stock list, time interval, and other parameters. FinRL-Meta has supported more than data sources, covering stocks, cryptocurrencies, ETFs, forex, etc.

4.1.2 Data Cleaning

Raw data retrieved from different data sources are usually of various formats and with erroneous or missing data to different extents. It makes data cleaning highly time-consuming. With a data processor, we automate the data-cleaning process. In addition, we use stock ticker names and data frequency as unique identifiers to merge all types of data into a unified data table.

4.1.3 Feature Engineering

Feature engineering is an important step in training data development zha2023data . Deep learning-based feature engineering has great potential to automate the design of technical indicators xiao2020feature ; nargesian2017Feature . FinRL-Meta aggregates effective features to help improve model predictive performance. FinRL-Meta currently supports five types of features:

-

•

Market features: Open-high-low-close price and volume data are the typical market data we can directly get from querying the data API. They have various data frequencies, such as daily prices from YahooFinance, and TAQ (Millisecond Trade and Quote) from WRDS. In addition, we automate the calculation of technical indicators based on OHLCV data by connecting the Stockstats666Github repo: https://github.com/jealous/stockstats or TA-lib library777Github repo: https://github.com/mrjbq7/ta-lib in our data processor, such as Moving Average Convergence Divergence (MACD), Average Directional Index (ADX), Commodity Channel Index (CCI), etc.

-

•

Fundamental features: Fundamental features are processed based on the earnings data in SEC filings queried from WRDS. The data frequency is low, typically quarterly, e.g., four data points in a year. To avoid information leakage, we use a two-month lag beyond the standard quarter end date, e.g., Apple released its earnings report on 2022/07/28 for the third quarter (2022/06/25) of the year 2022. Thus for the quarter between 04/01 and 06/30, our trade date is adjusted to 09/01 (same method for the other three quarters). We also provide functions in our data processor for calculating financial ratios based on earnings data such as earnings per share (EPS), return on asset (ROA), price to earnings (P/E) ratio, net profit margin, quick ratio, etc.

-

•

Analytics features: We provide news sentiment for analytics features. First, we get the news headline and content from WRDS xinyi_2019 . Next, we use NLTK.Vader888Github repo: https://github.com/nltk/nltk to calculate sentiment based on the sentiment compound score of a span of text by normalizing the emotion intensity (positive, negative, neutral) of each word. For the time alignment with market data, we use the exact enter time, i.e., when the news enters the database and becomes available, to match the trade time. For example, if the trade time is every ten minutes, we collect the previous ten minutes’ news based on the enter time; if no news is detected, then we fill the sentiment with 0.

-

•

Alternative features: Alternative features are useful but hard to obtain from different data sources de2018advances , such as ESG data, social media data, Google trend searches, etc. ESG (Environmental, social, governance) data are widely used to measure the sustainability and societal impacts of investment. The ESG data we provide is from the Microsoft Academic Graph database, which is an open-resource database with records of scholarly publications. We have functions in our data processor to extract AI publication and patent data, such as paper citations, publication counts, patent counts, etc. We believe these features reflect companies’ research and development capacity for AI technologies fang2019practical ; chen2020quantifying . It is a good reflection of ESG research commitment.

-

•

Natural language processing (NLP) features: We employ NLP methods to extract patterns from many sources such as Twitter, Weibo, Google Trends, and Sina finance. NLP xing2018natural greatly improves the efficiency of data processing, and reduces the labor of reading texts, websites, videos, and so on. NLP in finance can provide meaningful insights, e.g., sentiment analysis and question-answering like ChatGPT ouyang2022training , and GPT-4 GPT4 when making decisions. NLP features are extracted from a large amount of raw data, and reflect the states, predictions, and emotions of traders, governments, financial institutions, etc. We list several NLP features here: number of comments, number of replies, number of praise/dispraise, and number of optimism/pessimism.

Apart from the above default features, users can quickly add customized features using open-source libraries or add user-defined features. New features can be added in two ways: 1) Write a user-defined feature extraction function. The returned features are added to a feature array. 2) Store the features in a file, and put it in a default folder. Then, an agent can read these features from the file.

4.2 Financial Sentiment Analysis

In addition to the features collected directly from the market data, we also perform sentiment analysis on other data sources, and the output sentiment score serves as another feature. FinRL-Meta investigates the potential extension of sentiment analysis to the financial market context and assesses its impact on automated trading. In addition to market data such as price and volume, NLP features can provide complementary information. The use of market data alone is inadequate in capturing unexpected market events, news, and company announcements, leading to a diminished capacity of trading strategies to respond to unpredictable stock price fluctuations. The incorporation of NLP features, specifically news, social media, company announcement, and trends sentiments, can help investors analyze market trends and facilitate the examination of the interplay between textual data and stock prices.

Previous studies have extensively investigated the use of NLP techniques and sentiment analysis in stock price prediction and automated trading strategies. In a review study, xing2018natural summarized the NLFF (Natural Language Processing for Financial Forecasting) methodologies and their applications in related work. They organized and categorized these techniques into two primary groups: 1) Lexicon-based, which utilizes pre-trained financial sentiment orientation dictionaries loughran2011liability to label word segments with sentiment scores; and 2) Automatic Labeling, which employs label propagation frameworks to automatically construct lexicons for the financial domain using seed words hamilton2016inducing ; tai2013automatic . The lexicon-based approach has the advantage of analyzing texts at the word or sentence level by labeling groups of seed word segments with positive, negative, or neutral sentiments and assigning polarity scores to individual words to represent sentiment strengths.

Our observation of financial news revealed that the majority of sentiments are expressed through a small group of signaling words related to trading actions, such as ‘rise’ and ‘drop’. To address this characteristic, we recognized the need for word-level adjustments of sentiment weights for each word segment. As a result, we decided to use the lexicon-based approach in our study. However, we acknowledge that this approach has two major drawbacks: 1) words can have multiple meanings and sentiment strengths in different contexts, and 2) the meaning and sense of a word that is common in one domain, such as e-commerce, may not be common in finance. To overcome these challenges, we explore a specialized framework of lexicon-based sentiment analysis.

In FinRL-Meta, we propose a lexicon-based sentiment analysis framework that is specifically designed for NLP features. To achieve this, we created a customized sentiment dictionary tailored to the characteristics of the financial sector. Our aim is to improve the accuracy of sentiment classification beyond what has been achieved by previous NLP sentiment models by optimizing and extending the existing sentiment analysis framework while adapting it to the textual features of financial news.

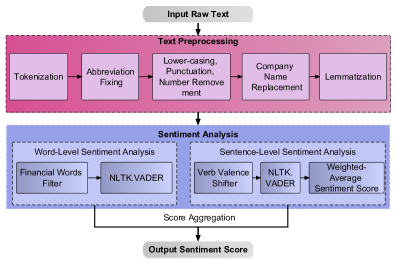

4.2.1 Lexicon-based Sentiment Analysis Framework

Fig. 6 illustrates the structure of our lexicon-based sentiment analysis framework, which comprises two main stages: text preprocessing and multi-level sentiment analysis. The text pre-processing stage involves five specific procedures aimed at transforming unstructured news text into cleaned, structured text vectors suitable for sentiment analysis.

-

•

1) In the tokenization stage, the raw texts are tokenized to split them into sentence and word segments, which are then respectively parsed into word-level and sentence-level sentiment analysis functions.

-

•

2) Abbreviation Fixing is performed to restore abbreviations containing valuable sentiment signaling words to their complete expressions, enabling the sentiment analysis algorithm to capture all sentiment signaling words.

-

•

3) Lower-casing, Punctuation, and Number Removement are conducted to normalize word segments into their lower-cased format and remove unnecessary punctuation and numbers that contain no sentiment values.

-

•

4) Company Name Replacement is carried out to remove company names that contain sentiment-sensitive terms, and replace them with a term containing no sentiment sensitivity, such as “Company Target” or “Company Random”.

-

•

5) Lemmatization is employed to group together the inflected forms of a word so they can be analyzed as a single item, identified by the word’s lemma. Unlike stemming which reduces all terms to their word stem, lemmatization restores each word to its lemma form based on its part of speech tagging. For instance, the word “developed” is tagged as VERB and restored to the lemma “develop”. The word “development” is tagged as NOUN and restored to “development”. Since different inflected forms of a word demonstrate distinctive sentiment polarities, the lemmatization method is used instead of stemming.

The sentiment analysis stage of text data involves transforming word and sentence vectors obtained during text preprocessing into corresponding sentiment scores, which are then aggregated to obtain the overall sentiment score. This stage employs distinct methodologies for word and sentence vectors.

-

•

1) For the word vectors, to filter out irrelevant word segments and concentrate on finance-specific sentiment signaling words, we utilized the LoughranMcDonald MasterDictionary xing2018natural with over 80,000 core financial terms as the base financial corpus. We then computed word-level sentiment scores using the VADER (Valence Aware Dictionary for Sentiment Reasoning) model in NLTK hutto2014vader .

-

•

2) For sentence vectors, we customized and adjusted the intensities of signaling words based on sentence logic and semantics using the Adverb Valence Shifter mechanism in the VADER package hutto2014vader . To incorporate sentiment-strengthening or weakening terms like “hardly” and “significantly”, we also implemented the Verb Valence Shifter mechanism which identified the verb and noun words as the sentence separator for each input sentence. After adjusting the internal sentiment weights of each sentence, we devised rules to assign weights to different sentences and aggregate the sentence vectors to obtain sentence-level sentiment scores.

4.2.2 Financial Sentiment Dictionary Construction

The sentiment dictionary is the foundation for lexicon-based sentiment analysis, containing information about the emotions or polarity expressed by words, phrases, or concepts. As noted in the previous section, one of the major obstacles associated with the lexical annotation approach is that the sentiment intensity and polarity of a given word often vary across different domains. For example, in e-commerce, the term “bull” usually refers to an animal species, while in the finance domain, it signifies an inclination for a specific market, security, or industry to rise.

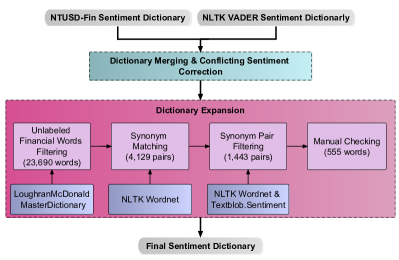

We create a financial sentiment dictionary by customizing and expanding two existing sentiment dictionaries, as shown in Fig. 7. The construction process involved two stages: dictionary merge and dictionary expansion. During the first stage, we merged the NTUSD-Fin Sentiment Dictionary with the built-in dictionary of the NLTK VADER package. The NTUSD-Fin dictionary chen2018ntusd is a sentiment dictionary specifically designed for finance, comprising labels for 8,331 words, 112 hashtags, and 115 emojis, and providing multiple scoring techniques, such as frequency, CFIDF, chi-squared value, market sentiment score, and word vector for tokens. The VADER sentiment dictionary hutto2014vader , created based on social media texts, includes 7,502 labeled words. Throughout the merging process, we detected and manually fixed 479 contradictions in the semantic polarities of words between the two dictionaries.

We also observe that certain financial terms with sentiment values were not accurately captured by the merged sentiment corpus, such as “bullish”, “bearish”, “outperform”, “outgrowth”, “high”, and “rise”. Consequently, in the second stage of the construction process, the dictionary was expanded to label more financial words with sentiment polarity and intensities through a synonym-matching mechanism. This process involved four main steps.

-

•

1) Unlabeled Financial Words Filtering: the LoughranMcDonald MasterDictionary xing2018natural , which contains over 80,000 core financial words, was utilized as the base financial corpus to filter out relevant financial words without attached sentiment polarities, resulting in 23,690 words being filtered out.

-

•

2) Synonym Matching: to assign sentiment polarity and intensity scores to the unlabeled words, the NLTK Wordnet was used to match each word with its labeled synonym. The WordNet miller1998wordnet is an extensive lexical database of English words that groups nouns, verbs, adjectives, and adverbs into sets of cognitive synonyms called “synsets”, each expressing a distinct concept. In this step, the 23,690 unlabeled words were matched with their synonym lists recommended by the WordNet Synset database, and word-synonym pairs with labeled synonyms were selected. This resulted in 4,129 word-synonym pairs being filtered out.

-

•

3) Synonym Pair Filtering: an algorithm was developed to further filter out words with the highest sentiment values from the remaining 4,129 word-synonym pairs. This algorithm utilized the TextBlob loria2018textblob subjectivity indicator and synonym path similarity indicator to identify the most sentiment-rich word-synonym pairs. The algorithm iterated through all words, checking their related synonyms and selecting the synonym with the highest similarity score in the SentiWordNet synonym network. After computing the subjectivity of each word, those with a subjectivity value of less than 0.2 were excluded. This step resulted in 1,443 word-synonym pairs being filtered out.

-

•

4) Manual Checking: each word-synonym-sentiment pair was manually checked, along with its actual usage in the real news context. If the path similarity between the word and its synonym was less than 0.5, its matched sentiment score was adjusted based on its meaning in the context. After this manual checking step, 555 words were selected as the final extended semantic dictionary.

To evaluate sentiment analysis accuracy involving both sentiment polarities and strengths, we conduct an experiment based on the news headlines corpus used in SemEval-2007 dataset strapparava2007semeval , which includes 1000 news headlines manually annotated with sentiment scores on six emotion categories: Anger, Disgust, Fear, Joy, Sadness, and Surprise. The sentiment scores range from -100 (highly negative) to 100 (highly positive), with 0 indicating neutral valence. Of the 1000 headlines, 468 have a positive valence, 526 have a negative valence, and 6 have a neutral valence. For this experiment, only headlines with clear positive emotions (sentiment valence of 50 to 100) and negative emotions (sentiment valence of -100 to -50) were selected, resulting in a dataset of 410 headlines, consisting of 155 positive and 255 negative headlines.

The evaluation results of the experiment are presented in Table 3. Two metrics were used to assess the accuracy of the sentiment analysis approaches Polarity Accuracy, which measures the proportion of predicted polarity (negative, neutral, and positive) that matches the labeled polarity, and Valence Correlation, which measures the correlation between predicted valence scores (ranging from -1 to 1) and labeled valence scores (ranging from -100 to 100), indicating the accuracy of the prediction of news sentiment intensities. As shown in the table, our sentiment analysis approach outperforms the baseline approach in terms of both Polarity Accuracy and Valence Correlation.

| Approach | Polarity Accuracy | Valence Correlation |

|---|---|---|

| NLTK VADER (Baseline) | 0.60 | 0.66 |

| With Verb Valence Shifter | 0.62 | 0.67 |

| With Financial sentiment dictionary (Our Approach) | 0.74 | 0.70 |

4.3 Environment Layer for Dynamic Market Environments

FinRL-Meta follows the OpenAI gym-style brockman2016openai to create market environments using the cleaned data from the data layer. It provides hundreds of environments with a common interface. Users can build their environments using FinRL-Meta’s interfaces, share their results and compare a strategy’s trading performance. Following the gym-style brockman2016openai , each environment has three functions as follows:

-

•

reset() function resets the environment back to the initial state

-

•

step() function takes an action from the agent and updates state from to .

-

•

reward() function computes the reward value transforming from to by action .

Detailed descriptions can be found in yang2020deep gort2022deep .

We plan to add more environments for users’ convenience. For example, we are actively building market simulators using limit-order-book data (refer to Appx. 5.2.6), where we simulate the market from the playback of historical limit-order-book-level data and an order matching mechanism. We foresee the flexibility and potential of using a Hidden Markov Model (HMM) mamon2007hidden or a generative adversarial net (GAN) goodfellow2014generative to generate market scenarios coletta2021towards .

Incorporating trading constraints to model market frictions: To better simulate real-world markets, we incorporate common market frictions (e.g., transaction costs and investor risk aversion) and portfolio restrictions (e.g., non-negative balance).

-

•

Flexible account settings: Users can choose whether to allow buying on margin or short-selling.

-

•

Transaction cost: We incorporate the transaction cost to reflect market friction, e.g., of each buy or sell trade.

-

•

Risk-control for market crash: In FinRL liu2020finrl ; liu2021finrl , a turbulence index kritzman2010skulls is used to control risk during market crash situations. However, calculating the turbulence index is time-consuming. It may take minutes, which is not suitable for paper trading and live trading. We replace the financial turbulence index with the volatility index (VIX) whaley2009understanding that can be accessed immediately.

Multiprocessing training via vectorized environments: We utilize GPUs for multiprocessing training, namely, the vectorized environments technique of Isaac Gym makoviychuk2021isaac , which significantly accelerates the training process. In each CUDA core, a trading agent interacts with a market environment to produce transitions in the form of state, action, reward, next state. Then, all the transitions are stored in a replay buffer and later are used to update a learner. By adopting this technique in our market simulator, we successfully achieve the multiprocessing simulation of hundreds of market environments to improve the performance of DRL trading agents on large datasets.

5 Homegrown Examples and Tutorials

We provide several homegrown examples and a dozen of tutorials, which serve as stepping stones for newcomers. We reproduce popular papers as benchmarks for follow-up research.

5.1 Performance Metrics and Baseline Methods

We provide the following metrics to measure the trading performance:

-

•

Cumulative return , where is the final portfolio value, and is the original capital.

-

•

Annualized return , where is the number of trading days.

-

•

Annualized volatility , where is the annualized return in year , is the average annualized return, and is the number of years.

-

•

Sharpe ratio Sharpe , where , is the risk-free rate, and .

-

•

Max. drawdown: The maximal percentage loss in portfolio value.

The following baseline trading strategies are provided for comparison:

-

•

Passive trading strategy malkiel2003passive is a well-known long-term strategy. The investors just buy and hold selected stocks or indexes without further activities.

-

•

Mean-variance and min-variance strategy ang2012mean are two widely used strategies that look for a balance between risks and profits. They select a diversified portfolio in order to achieve higher profits at a lower risk.

-

•

Equally weighted strategy is a portfolio allocation strategy that gives equal weights to different assets, avoiding allocating overly high weights on particular stocks.

5.2 Homegrown Examples

For educational purposes, we provide Jupyter/Python as tutorials999https://github.com/AI4Finance-Foundation/FinRL-Tutorials to help newcomers get familiar with the whole pipeline.

In Section 2.3, we have described the RLOps paradigm. Here we will demonstrate how to use RLOps in practice by reproducing several prior papers. We have reproduced experiments in several papers as benchmarks. Users can study our codes for research purposes or use them as stepping stones for deploying trading strategies in live markets. In this subsection, we describe several home-grown examples in detail, in a sequence of simple to advanced. Users could choose the one to learn and run based on their proficiency.

5.2.1 Stock Trading Task

The stock trading task is one of the most classical problems in FinRL-Meta. The goal is to train a DRL agent to decide the time, ticker, and amount to buy and sell on the stock market.

First, users can use the APIs provided by FinRL-Meta to fetch historical OHLCV (open, high, low, close prices, and volume) data of the stocks from data platforms like Yahoo Finance. After data cleaning and feature engineering, which checks the error and missing data, and then technical indicators are added.

Second, FinRL-Meta will split the processed data into training and testing, and construct a gym-style market environment for each, with the state-action-reward specified in Section 3.1. Then, we are able to choose algorithms from any one of the DRL libraries and train the agents of these algorithms in the market environment.

Lastly, after we obtain the trained agents, we backtest the agents on the environment with testing data. During backtesting, the performance of the agents will be compared with the performance of several baselines, such as DJIA index, mean-variance, and equally weighted.

In FinRL-Meta’s demo, after fetching from Yahoo! Finance, we use the data from 01/01/2011 to 07/01/2021 for training and the data from 07/01/2021 to 11/01/2022 for trading. The technical indicators in the state space include the following, Moving Average Convergence Divergence (MACD), Relative Strength Index (RSI), Commodity Channel Index (CCI), Average Directional Index (ADX), etc. All these data will be sealed in a gym-style environment.

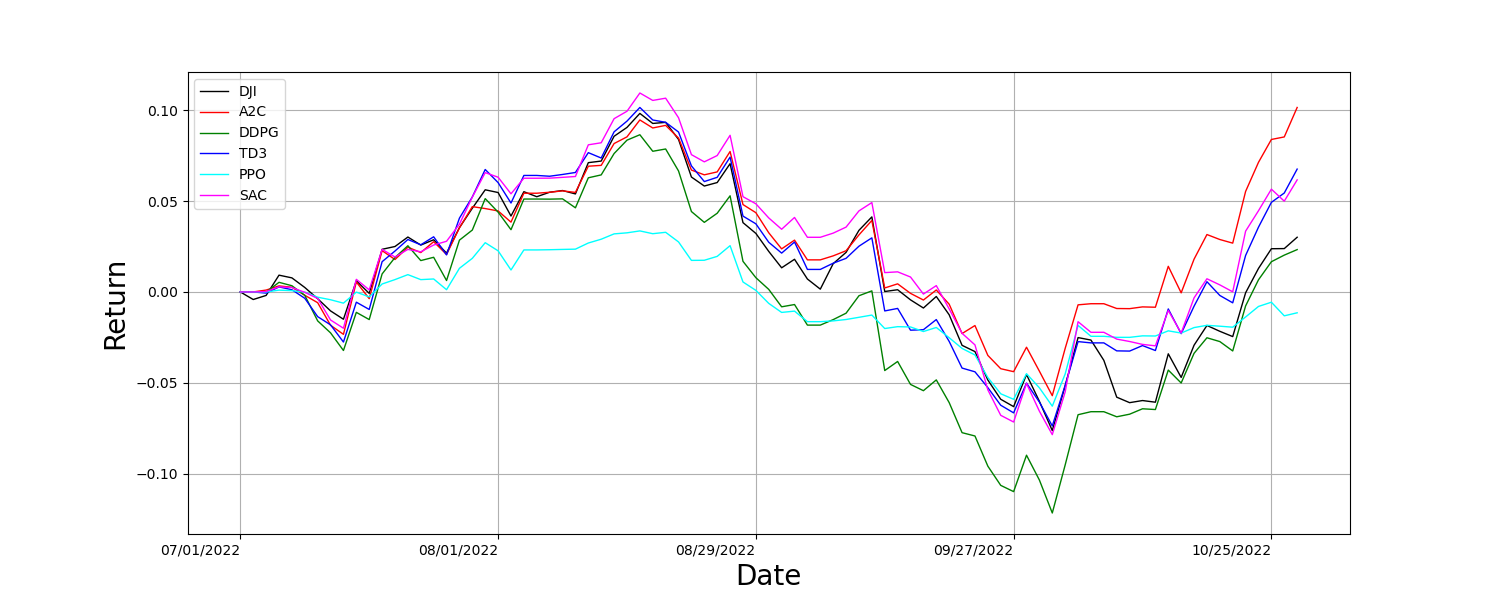

During the training phase, we utilized dynamic datasets with a rolling window of 22 trading days and trained five different deep reinforcement learning (DRL) algorithms (A2C, DDPG, TD3, PPO, and SAC) in the environment. Fig. 9 displays the comparison of their performances with the baseline DJIA index after backtesting all the agents. The best agent was found to be A2C, achieving a return of 0.102 compared to DJI’s return of 0.030. This demo provides a detailed walkthrough of how DRL operates in the stock trading task and serves as a benchmark for subsequent works in the field of financial reinforcement learning liu2018practical . This benchmark is beneficial for getting into the field of financial reinforcement learning.

5.2.2 Trading in Real Time

Practical tasks like stock trading and cryptocurrency trading suffer from the false positive issue due to overfitting, where an agent might perform well on testing data but not on real-world markets. Since backtesting has problems of information leakage and overfitting, its results is not persuasive to show the quality of trained models. Thus, we propose to deploy DRL agent on paper trading.

Fig. 10 shows our “training-testing-trading” pipeline. In a window, there are days’ data for training and days’ data for testing. At the end of a window, we perform paper trading for day. Note that we always retrain the agent using days of training and testing data together. Then, we roll the window forward by day ahead and perform the above steps for a new window. Paper trading is always carried out for day. Therefore, windows correspond to trading days.

Alg. 1 summarizes the pipeline of paper trading. For trading days from to , we keep doing the following three steps:

-

•

Step 1). Download and process -day data, from day to day . Then build the data into a gym-style environment and train the agent. Then download and process S-day data, from day to day . Then build the data into a gym-style environment and validate how the agent performs. According to the agent’s performance on the validation environment, adjust hyper-parameters.

-

•

Step 2). Build the training and testing data, totally days from day to day (note that there are data points for each day’s minute-level data), into a gym-style environment. Update hyper-parameters to the values chosen from Step 1). Then retrain the agent on these -day environments.

-

•

Step 3). Deploy the trained agent to the paper trading market and trade from 9:30 am to 4:00 pm.

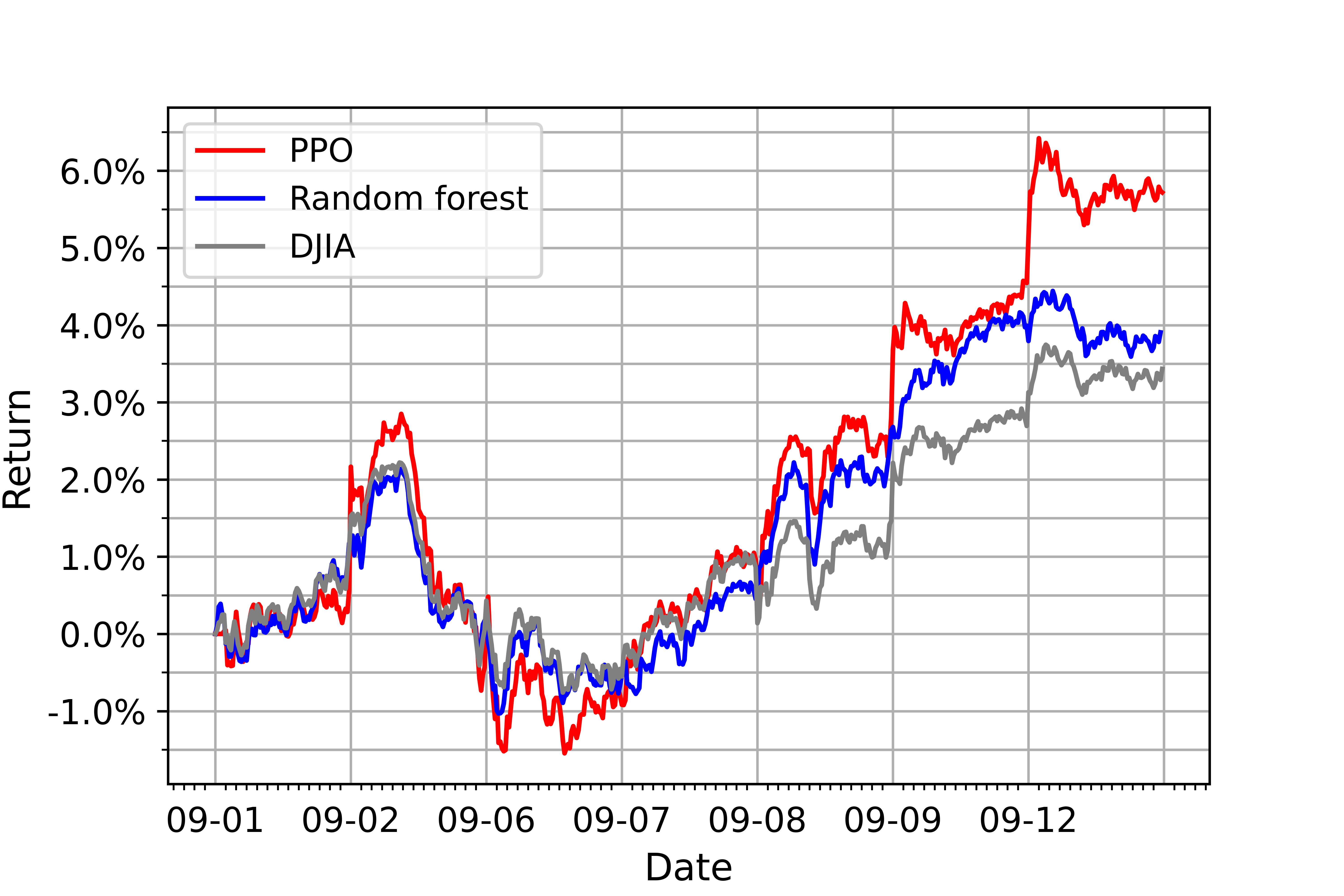

For the experiment, we select Dow Jones 30 stocks as our trading stocks and use minute-level historical market data from to . The data are downloaded from Alpaca101010Web page of Alpaca: https://alpaca.markets/. Then, we use the paper trading APIs provided by Alpaca to do paper trading from to . The cumulative return of our PPO method and conventional random forest method is shown in Fig. 11.

5.2.3 Ensemble Strategy

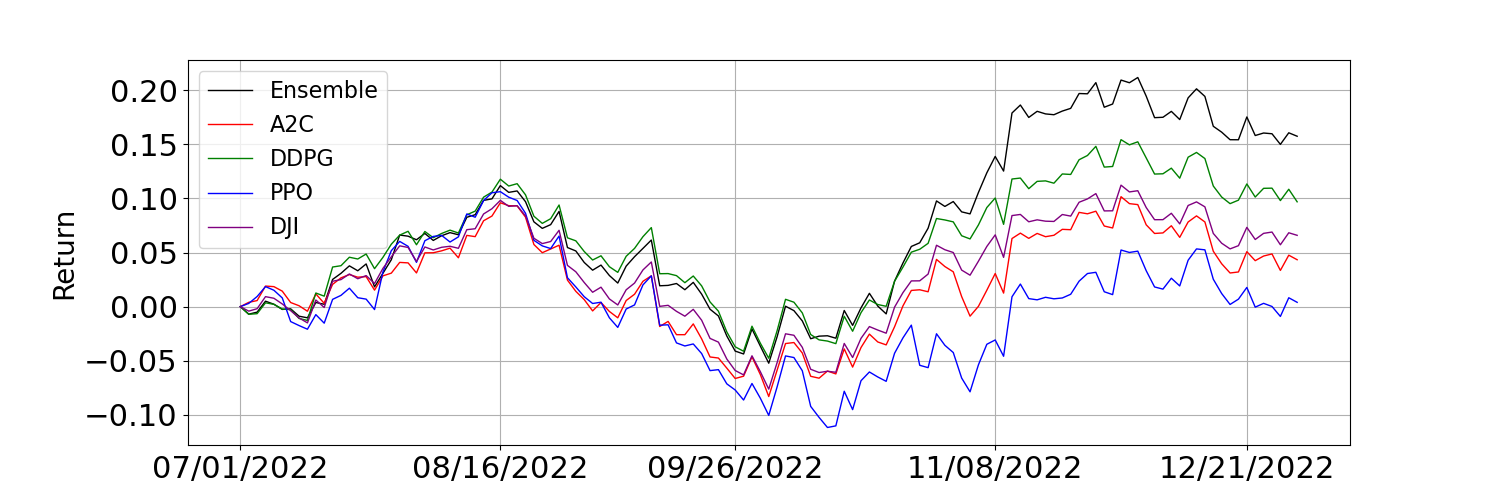

Based on the stock trading task, the ensemble method yang2020deep combines different agents to obtain an adaptive one, which inherits the best features of agents and performs remarkably well in practice. We consider three component algorithms, Proximal Policy Optimization (PPO), Advantage Actor-Critic (A2C), and Deep Deterministic Policy Gradient (DDPG), which have different strengths and weaknesses. Using a rolling window, an ensemble agent automatically selects the best model for each test period. Again on the 30 constituent stocks of the DJIA index, we use data from 01/01/2010 to 07/01/2022 for training and data from 07/01/2022 to 01/01/2023 for validation and testing through a quarterly rolling window.

From Fig. 12, we observe that the ensemble agent outperforms other agents. In the experiment, the return of the ensemble strategy is , while DJI is . The ensemble agent has the highest return, which means it performs the best in profits. This benchmark demonstrates that the ensemble strategy is effective in constructing a more reliable agent based on several components of DRL agents.

5.2.4 Podracer on Cloud

We reproduce cloud solutions of population-based training, e.g., generational evolution (finrl_podracer_2021, ) and tournament-based evolution (liu2021podracer, ). FinRL-Podracer can easily scale out to GPUs, which features high scalability, elasticity and accessibility by following the cloud-native principle. If GPUs are abundant, users can take advantage of this benchmark to work on high-frequency trading tasks. On an NVIDIA SuperPOD cloud, we conducted extensive experiments on stock trading and found that it substantially outperforms competitors, such as OpenAI and RLlib finrl_podracer_2021 . Detailed instructions are provided on our website.

Benchmarks on cloud: We provide demos on a cloud platform, Weights & Biases 111111Website: https://wandb.ai/site, to demonstrate the training process. We define the hyperparameter sweep, training function, and initialize an agent to train and tune hyperparameters. On the cloud platform Weights & Biases, users are able to visualize their results and assess the relative performance via community-wise competitions.

5.2.5 Curriculum Learning for Generalizable Agents

Based on FinRL-Meta (a universe of market environments, say ), one is able to construct an environment by sampling data from multiple market datasets, similar to XLand team2021open . In this way, one can apply the curriculum learning method team2021open to train a generally capable agent for several financial tasks.

5.2.6 Market Simulator

Gym market environments: We build all of our environments following OpenAI-gym style brockman2016openai . The first reason is that this makes it convenient for plugging in any of the three DRL libraries (Stable Baseline3, RLlib, and ElegantRL). Another reason is that it is user-friendly. Newcomers can learn our environments fast and then build their own task-specific environments efficiently.

Synthetic data generation: We create a market simulator market_simulator to simulate the markets from the playback of historical limit-order-book-level data and the order matching mechanism. Currently, the simulator is at the minute level (i.e., one time step = one minute), which is changeable. The state is a stack of market indicators and market snapshots from the last few time steps. The action is to place an order. We support market orders and limit orders. We also provide several wrappers to accept typically discrete or continuous actions. Rewards can be configured by the participants with the aim of generating policies that optimize pre-specified indicators. In our simulator, we take into account the following factors: 1) temporary market impact; 2) order delay. We do not consider the following factors in our simulator: 1) permanent market impact of limit orders; 2) non-resiliency limit order book.

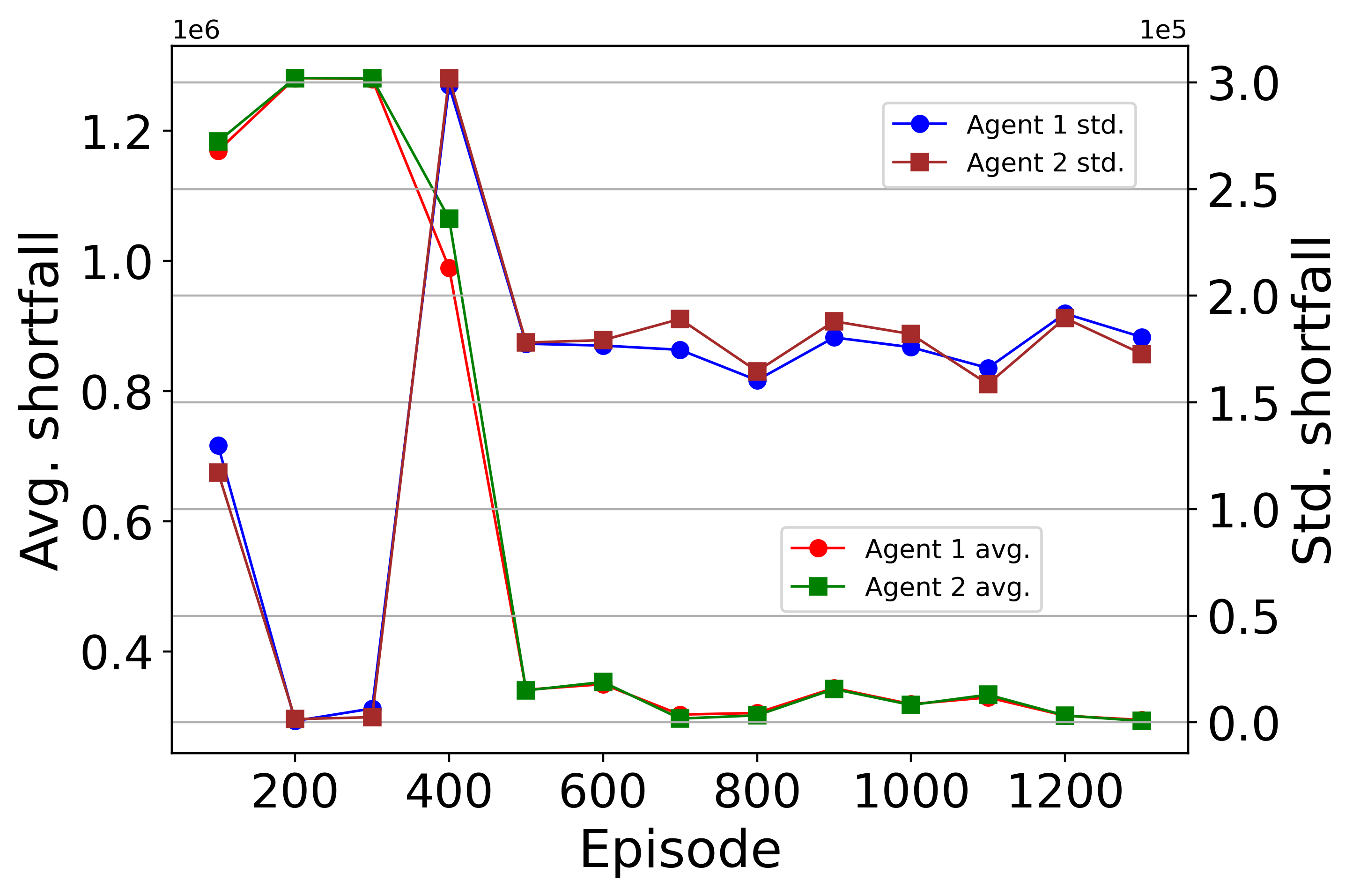

Liquidation analysis and trade execution: By reproducing bao2019multiagent , we build a simulated environment of stock prices according to the Almgren and Chriss model. Then we implement the multi-agent DRL algorithms for both competing and cooperative liquidation strategies. This benchmark demonstrates the trade execution task using deep reinforcement learning algorithms. When trading, traders want to minimize the expected trading cost, which is also called implementation shortfall. In Fig. 13, there are two agents, and we observe that the implementation shortfalls decrease during the training process.

5.3 More FinRL Demos and Tutorials

-

•

Portfolio allocation liu2020finrl : We train a DRL agent to perform a portfolio optimization task on a set of stocks.

-

•

Cryptocurrency trading liu2020finrl : We provide a demo liu2020finrl on popular cryptocurrencies.

-

•

Paper trading demo: We provide a demo for paper trading. Users could combine their own strategies or trained agents in paper trading.

-

•

China A-share demo: We provide a demo based on the China A-share market data using Tushare.

-

•

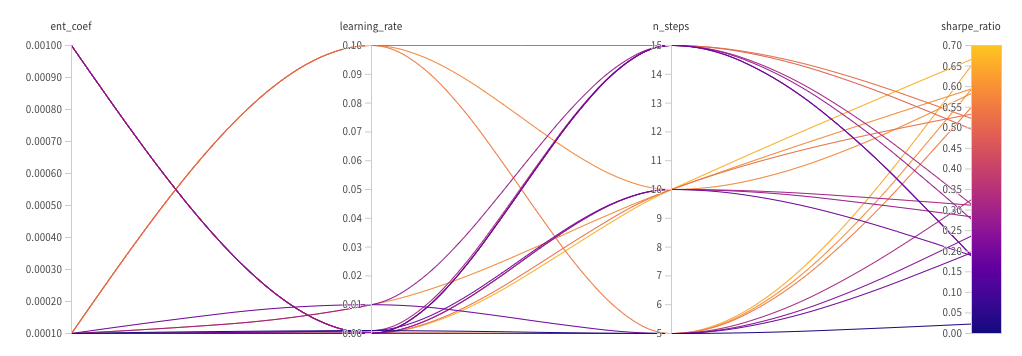

Hyperparameter tuning: The default hyperparamters may not be the best for our tasks. Reinforcement learning algorithms are sensitive to hyperparamters; therefore, hyperparamter tuning is an important issue. Hyperparamters are tuned based on an objective. We provide several demos for hyperparameter tuning using Optuna akiba2019optuna and Ray Tune liaw2018tune . Fig. 14 shows an example of hyperparameter tuning in the portfolio allocation task using A2C, which aims to maximize the Sharpe ratio.

-

•

Robo-advising: Robo-advising by integrating ChatGPT ouyang2022training and GPT-4 GPT4 will be much more powerful than before. Users are encouraged to develop robo-advisor apps by building upon the demos that we have created using ChatGPT ouyang2022training and GPT-4 GPT4 . By engaging in conversation with ChatGPT using a chain of thought prompt, we may be able to obtain good trading advice. Additionally, we have demonstrated that properly guiding ChatGPT can generate new financial factors, which speeds up the process of creating them manually.

6 Conclusion and Future Works

Following the data-centric AI principles and the DataOps paradigm, in this paper, we developed FinRL-Meta, a data-centric library that provides openly accessible dynamic financial datasets and reproducible benchmarks. FinRL-Meta implements an automated data-curation pipeline tailored for the financial market, which processes data from different sources and integrates them into a unified market environment. FinRL-Meta adheres to the standard OpenAI gym-style APIs, making it readily accessible to experts in both reinforcement learning and finance. In addition, we have developed a wide range of homegrown examples and tutorials to facilitate the usage of the library. FinRL-Meta will serve as a source of inspiration for both researchers and practitioners who are interested in FinRL.

For future work, FinRL-Meta aims to build a universe of financial market environments, like the XLand environment team2021open . To improve the performance for large-scale markets, we are exploiting GPU-based massive parallel simulation such as Isaac Gym makoviychuk2021isaac and deploying it into projects such as RL for market simulator. Moreover, it will be interesting to explore the evolutionary perspectives gupta2021embodied ; scholl2021market ; finrl_podracer_2021 ; liu2021podracer to simulate the markets. We believe that FinRL-Meta will provide insights into complex market phenomena and offer guidance for financial regulations.

6.1 Explainability

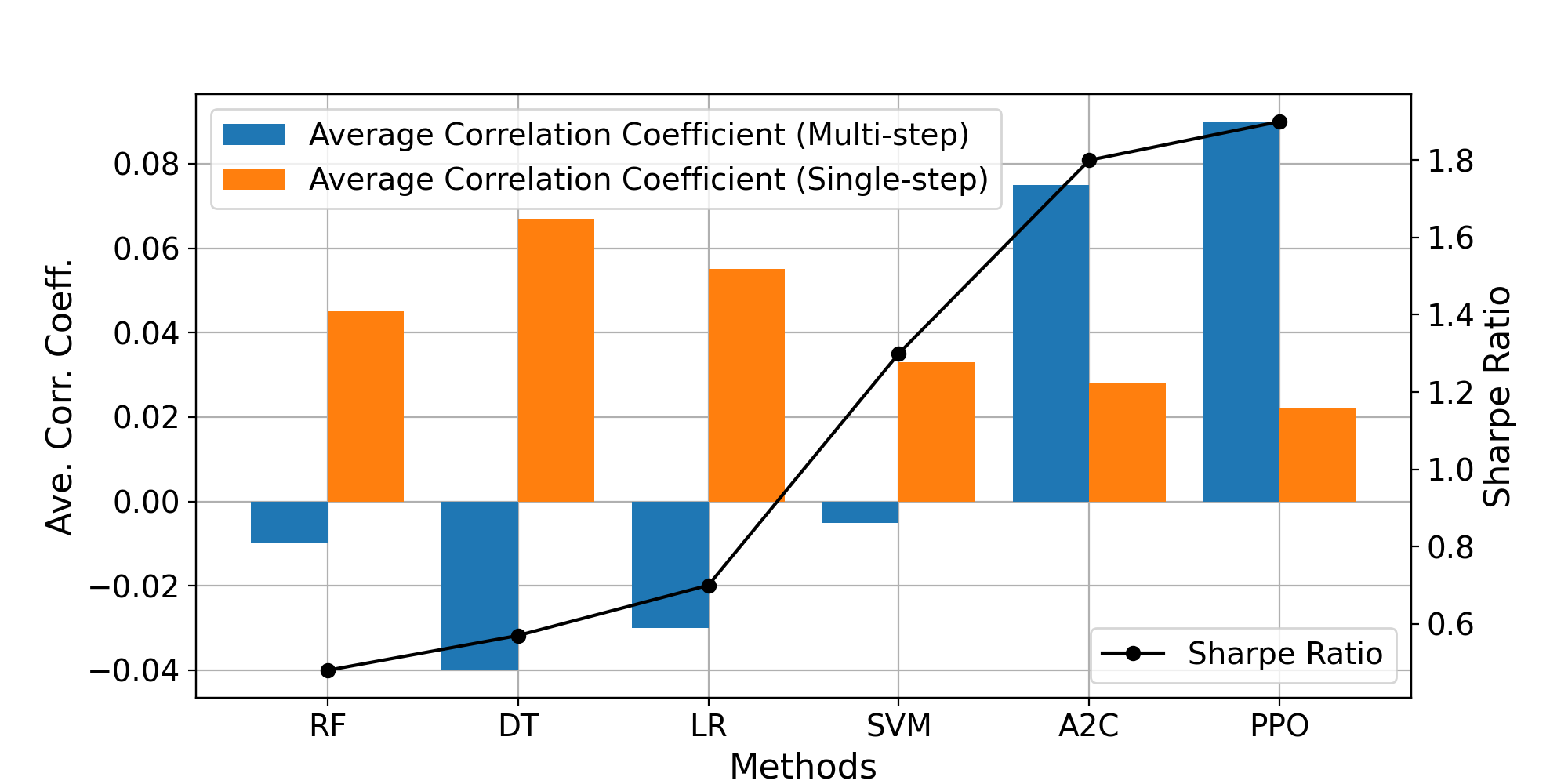

We reproduce guan2021explainable that compares the performance of DRL algorithms with machine learning (ML) methods on the multi-step prediction in the portfolio allocation task. We use four technical indicators MACD, RSI, CCI, and ADX as features. Random Forest (RF), Decision Tree Regression (DT), Linear Regression (LR), and Support Vector Machine (SVM) are the ML algorithms in comparison. We use data from Dow Jones 30 constituent stocks to construct the environment. We use data from 04/01/2009 to 03/31/2020 as the training set and data from 04/01/2020 to 05/31/2022 for backtesting. In Fig. 15, the results show that DRL methods have a higher Sharpe ratio than ML methods. Also, DRL methods’ average correlation coefficients are significantly higher than that of ML methods (multi-step).

We reproduce guan2021explainable that compares the performance of DRL algorithms with machine learning (ML) methods on the multi-step prediction in the portfolio allocation task. We use four technical indicators MACD, RSI, CCI, and ADX as features. Random Forest (RF), Decision Tree Regression (DT), Linear Regression (LR), and Support Vector Machine (SVM) are the ML algorithms in comparison. We use data from Dow Jones 30 constituent stocks to construct the environment. We use data from 04/01/2009 to 03/31/2020 as the training set and data from 04/01/2020 to 05/31/2022 for backtesting.

6.2 Data Privacy, Strategy Privacy and Federated Learning Technology

As our open-source community is continuously developing new features to ensure that FinRL-Meta provides a better user experience, one of the main targets for our next step is to enhance financial data privacy as well as strategy privacy for users. We discuss the potential of integrating the federated learning technology into our open-source FinRL-Meta, in order to achieve data privacy and strategy privacy for our users, say collaboratively training.

Federated learning is a method for training machine learning models from distributed datasets that remains private to data owners. It allows a central machine learning model to overcome the isolated data island, i.e., to learn from data sets distributed on multiple devices that do not reveal or share the data with a central server. We understand that in certain scenarios, our users face the problem that they only have a small amount of financial data and are not unable to train a robust model, but they are also hesitant to train their models with others due to privacy reasons. To the best of our knowledge, we would like to name a few representative examples on the use of federated learning to help financial applications. Byrd et al. byrd2020differentially present a privacy-preserving federated learning protocol on a real-world credit card fraud dataset for the development of federated learning systems. The researchers in WeBank liu2021fate created FATE, an industrial-grade project that supports enterprises and institutions to build machine learning models collaboratively at large-scale in a distributed manner. FATE has been adopted in real-world applications in finance, health and recommender systems. We also want to mention one research work kairouz2021advances which points out the open problems in federated learning. We believe that, as a newly introduced method, federated learning has a lot of undiscovered and exciting applications that we can develop. We would like to encourage our community members to explore the potential of federated learning technologies for the benefit of financial applications.

6.3 FinRL-Meta and DAO, DeFi, NFT, Web3

Over the past decades, we have witnessed capital growth exceeding economic growth globally. However, the door to personal capital growth is not open to all. In a way, one needs to start rich to get richer. The situation is even worsened by the competition with computers. Today in major stock markets, at least of the trades are automated by algorithms.