Recurrent neural network based parameter estimation of Hawkes model on high-frequency financial data

Abstract

This study examines the use of a recurrent neural network for estimating the parameters of a Hawkes model based on high-frequency financial data, and subsequently, for computing volatility. Neural networks have shown promising results in various fields, and interest in finance is also growing. Our approach demonstrates significantly faster computational performance compared to traditional maximum likelihood estimation methods while yielding comparable accuracy in both simulation and empirical studies. Furthermore, we demonstrate the application of this method for real-time volatility measurement, enabling the continuous estimation of financial volatility as new price data keeps coming from the market.

1 Introduction

We propose a real-time estimation and volatility measurement scheme. Specifically, we continuously estimate the financial model parameters and volatility in real-time as new price process become available during the market operation. Our method uses a recurrent neural network to estimate the parameters of a Hawkes model based on high-frequency financial data, and these estimates are subsequently used to compute volatility. This approach exhibits significantly faster computational performance compared to the traditional maximum likelihood estimation (MLE) method.

The Hawkes process introduced by Hawkes (1971) is a type of point process used to model the occurrence of events over time. It is frequently utilized in finance to model the arrival of trades or other financial events in the market; here, we use it to describe the fluctuations in the price in the tick structure. As a two dimensional Hawkes process with symmetric kernel in our study, it is characterized by two key features: self-excitation and mutual-excitation (Bacry et al., 2013). Self-excitation means that the occurrence of an event increases the likelihood of the same types of events occurring, while mutual-excitation implies that the occurrence of one event can increase the likelihood occurrence of other types of events.

For the estimation, we use a long short-term memory (LSTM) network introduced by Hochreiter and Schmidhuber (1997). This is a type of recurrent neural network that is capable of learning long-term dependencies in data. LSTMs can be used for a variety of tasks that involve sequential data, including language modeling, machine translation, speech recognition, time series based on historical data, and financial analysis (Zhang et al., 2021; Ghosh et al., 2022). They are particularly useful for tasks where capturing long-term dependencies is important, as the gating mechanism allows the network to retain important earlier information in the sequence while discarding irrelevant or outdated information.

Thus, our method uses a neural network for parameter estimation. Similar attempts have been made in recent years in various fields (Wlas et al., 2008; Wang et al., 2022; Wei and Jiang, 2022), but there is still limited research on using neural networks for estimation in financial time series. Specifically, we use a direct parameter estimation approach in which the neural network is trained to directly predict the model parameters based on the observed data. This method is an example of a small aspect of network-based parameter estimation and expected to be applied to more complex models.

2 Method

2.1 Price model

First, we explain the stochastic model to describe high-frequency stock price movements. We model the up and down movements of the tick-level price process as a marked Hawkes process, which captures both the timing and size of the movements. This process is defined by the random measures,

| (1) |

in the product space of time and jump size, , for , where denotes the space of mark (jump) sizes for up and down price movements, respectively. Each measure in Eq. (1) is associated with a sequence of -valued random variables in addition to the sequence of random times for each . That is,

with the Dirac measure , which is defined as follows: for any time interval and

A vector of càdlàg counting processes is defined by

which counts the number of events weighted by their size, that is,

Assumption 1.

The stochastic intensity for is represented by the following:

| (2) |

where is a positive constant base intensity vector, is a positive constant matrix. is a decay function matrix and denotes the element-wise product. From the definition of Eq. (2), for simplicity, we assume that the future impact of an event on intensities is independent of jump size, as the integrand of the equation does not contain the jump variable . In addition, for further parsimony, we assume that:

| (3) |

Hence, the set of parameters to be estimated is . We also assume that the mark at time is independent from the -algebra generated by for . The intensity process is assumed to be stationary and that the spectral radius of is less than 1.

Under this assumption, the Hawkes volatility of price movements – the standard deviation of total up and down net movements – is represented by

| (4) |

where is an operator such that for a square matrix and denotes a diagonal matrix whose diagonal entry is composed of the argument. Furthermore,

| (5) |

and

| (6) |

and

| (7) |

and by the mark independent assumption,

To calculate the volatility of price changes, rather than the number of movements, we multiply the minimum tick size to Eq. (4). Further details can be found in Lee and Seo (2017) and Lee (2022).

2.2 Network model

Next, we construct a recurrent neural network for parameter estimation. The traditional method of estimating the parameters of a Hawkes process is MLE, which involves maximizing the log-likelihood function of the model:

to estimate the parameters most likely to generate the observed data.

In contrast, neural network based parameter estimation involves training a neural network to predict the parameters of a Hawkes process based on input data. To do this, numerous sample paths of inter-arrival times and movement types (up or down) are generated, where the parameters of each path are determined randomly. These sample paths are then used as feature variables, and the associated true parameter values are used as the target variables.

The neural network is trained on these data. Once trained, it can be used to predict the parameter values of a new sample path of Hawkes process data. These predicted parameter values can then be used to compute further complicated formulae, such as the Hawkes volatility in Eq. (4), which is a measure of the variability of the process over time.

Here, we use an LSTM model with three layers as the neural network. The LSTM network is known for its capability of retaining information over a long duration, making it appropriate for tasks that require context comprehension or state preservation. The gates mechanism in the LSTM architecture that regulates the flow of information between memory cells and the network enables the network to choose which information should be preserved or discarded. We also tested gated recurrent unit networks (Cho et al., 2014); however, the LSTM performed slightly better in our problem. A thorough account of the network’s implementation is presented in the following section.

3 Simulation result

In this simulation study, we generate a set of paths of Hawkes processes to create a training dataset for the neural network. The dataset comprises a sufficient quantity of synthetic data, which are utilized to train the network to predict the real parameters of the Hawkes process. The real parameters for each Hawkes process are randomly selected to cover the entire range of possible values, with each path having distinct parameters. For the ranges of the parameters, we use the ranges of the estimates obtained by fitting the past intraday price process of various stocks to the Hawkes model. Approximately 30 symbols of stocks, including AAPL, AMZN, C, FB, GOOG, IBM, MCD, MSFT, NVDA, and XOM from 2018 to 2019 are used.

For the estimation, we focus on high-frequency rather than ultra-high-frequency. More precisely, the raw data are filtered as follows. We observe the mid-price at intervals of seconds, noting any changes from the previously observed price. If a change is detected, we record the exact time of the change and the new price. If the price remains the same, we move on to the next interval of 0.1 seconds and repeat the process. This method allows us to filter out unnecessary movements, commonly referred to as microstructure noise, observed at ultra-high frequencies.

Once the set of estimates is obtained, we generate Hawkes process paths of a 2,000-time step. These are then used for neural network training together with estimates as target variables. This method yields tens of thousands of datasets, which are sufficient to construct a comprehensive training set.

The implementation of the LSTM network model is as follows. The first layer consists of 12 units, which manage sequential data. These data are a two-dimensional input of time series data that comprise inter-arrivals and types of movements (up or down). Up and down movements are encoded as 1 and 2, respectively. The output of this layer is a sequence of 12 length of vectors, where each vector is the output of the first layer at a given time step. Thus, if the original time series has a 2,000-time step, then the output of the first layer is a matrix, which is the time step the number of units.

The second layer has 12 units and produces a single (not a sequence of) vector of length 12. The final layer is a dense (fully connected) layer with four units, which produces output representing the parameters in the Hawkes model, and . If we extend the model for more complexity, the number of units in the last dense layer will be adjusted accordingly. This is because each unit in the last layer represents each parameter.

As pointed out by Mei and Eisner (2017), a natural extension of LSTM is deep LSTM, especially for complex structured data such as high-frequency financial data, where the effectiveness of multi-layering seems promising. However, we utilized a relatively parsimonious Hawkes model and achieved sufficient performance without employing a large number of layers, so we used the LSTM model proposed above, which is relatively faster to train. If the data structure and model become more complex, an extension to deep LSTM would be helpful.

For training, we use 75,000 sample data points; hence, the dataset for the neural network’s input has a shape of . The Adam (Kingma and Ba, 2014) optimizer is used for training. Generally, more than 300 epochs are used. For testing, we use 15,000 data points that were not used for training. This is done to evaluate the model’s ability to make predictions on these unseen data based on mean squared error (MSE). We then compare the results with a traditional MLE. The computation times were measured using a typical commercial PC. The result shows that the MLE has slightly better performance in terms of MSE; however, the neural network also shows a reasonable result. Meanwhile, the general numerical method of MLE requires many iterations and is time consuming. However, a well-trained neural network computes an estimate very quickly, which is less than a hundredth of the time required by MLE.

| Neural network | MLE | |

|---|---|---|

| MSE | 0.0513 | 0.0417 |

| Time (sec) | 0.0120 | 1.763 |

To understand the basic properties of the neural network estimator, we investigate its sampling distribution. To examine the sampling distribution, we generate 100,000 paths of length 2,000 using the fixed parameter values of , , , . We then compare the obtained sampling distributions using the neural network and MLE methods. Overall, MLE outperforms the neural network slightly. Even so, the general performance of neural networks is also quite good.

| Parameter | True | Neural network | MLE | ||

|---|---|---|---|---|---|

| Mean | S.D. | Mean | S.D. | ||

| 0.3000 | 0.3151 | 0.0358 | 0.3036 | 0.0314 | |

| 0.4000 | 0.4429 | 0.0661 | 0.3988 | 0.0500 | |

| 0.7000 | 0.5733 | 0.0697 | 0.7024 | 0.0608 | |

| 1.5000 | 1.5736 | 0.1364 | 1.5078 | 0.1145 | |

Specifically, the aforementioned example compares the performance of the numerical optimizer (used in MLE) and neural network. Owing to the nature of simulation studies, the numerical optimizer has several advantages. The outcome of a numerical optimizer is often influenced by its initial value. In the example provided above, because the true value of the parameter is known, it was directly used as the initial value. This may have improved the performance compared to the result from a random initial value. As finding a good initial value is sometimes challenging, a numerical optimizer may perform worse in real-world problems.

In addition, if the numerical optimizer exhibits unexpected behavior, such as failure to converge appropriately, human engagement may be necessary, such as adjustments to the initial value or retrying the procedure. As the complexity of the model and level of noise present in the empirical data increase, the advantages of the numerical optimizer may decrease. In such cases, further research may be required to determine whether the numerical optimizer still outperforms the neural network.

4 Empirical result

The approach in the previous section can be directly applied to empirical data. However, we need to consider whether robust estimation can be made in situations where the empirical data do not completely follow the Hawkes process. For example, in filtered high-frequency price process data, a subdue effect (where an event reduces intensity) can sometimes occur. This can result in negative estimates for the parameter , which violates the definition of the Hawkes model. To address this, a more complex model should be used; however, as this falls outside the scope of this study, an alternative method is to use a softplus activation function for the last layer in the neural network. This approach is similar to constraint optimization by ensuring positive estimates. Furthermore, instead of predicting directly, we trained and predicted . By using the softplus function, this method ensures that the branching ratio condition of the Hawkes model is met.

To further increase robustness, a combination of empirical data and its maximum likelihood estimates as training data can be used, rather than relying solely on simulation data. This approach accounts for the possibility of model mis-specification; for instance, the observed data may not perfectly align with the Hawkes process. By incorporating the MLE into the training data, the neural network can better mimic the MLE of the Hawkes model. Thus, if the goal is to construct a neural network that closely approximates the MLE, even under the possibility of model mis-specification, this method can be effective.

The following section explains the step-by-step procedure. We select segments of observed intraday data of inter-arrivals and movement types. Each segment consists of a 2,000-time step. These selected paths are used to fit the Hawkes model using MLE. The resulting dataset is then used to train the neural network, where the inter-arrivals and types of real data serve as feature variables and the maximum likelihood estimates are the target variables.

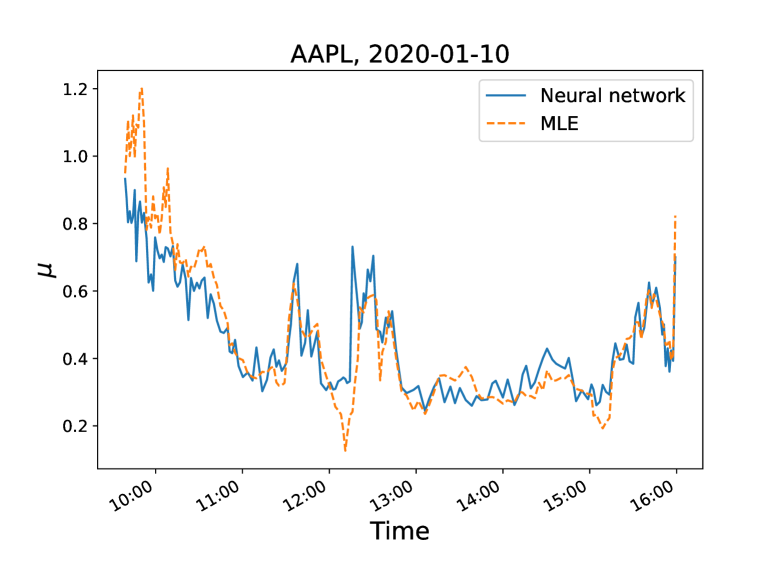

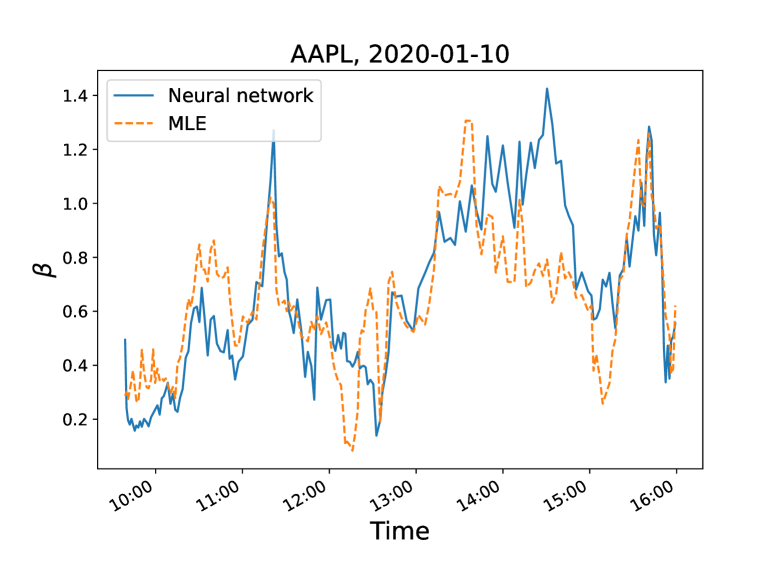

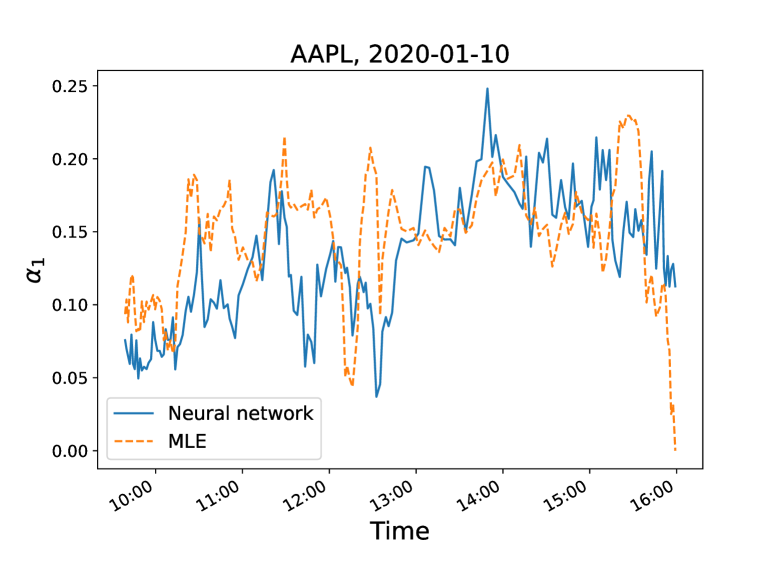

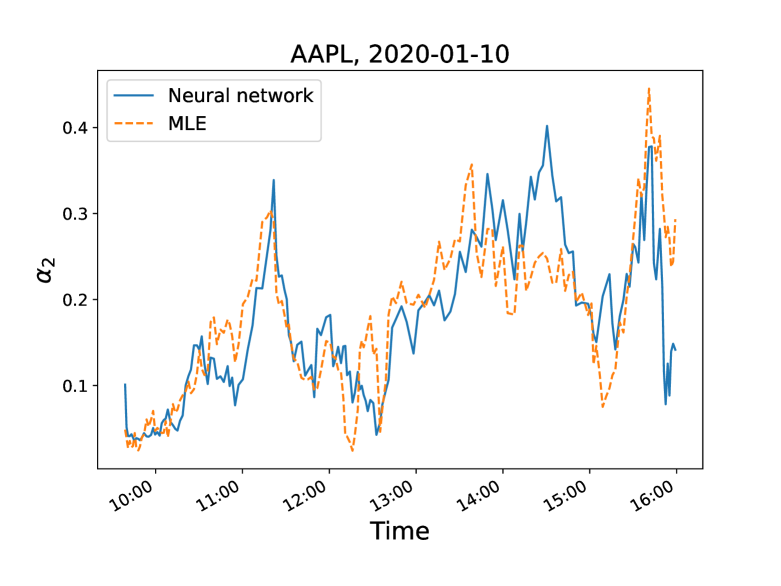

Figure 1 illustrates the intraday dynamics of estimates of the Hawkes model on a specific date. The data used for this illustration are out-of-sample that are not used for training. Specifically, it was estimated using segments of data corresponding to every 2,000-time step. This corresponds to a time horizon of approximately 10-20 minutes. To create a more continuous graph, the time windows for estimation were moved forward slowly with sufficient overlap. The neural network shows very consistent results with MLE.

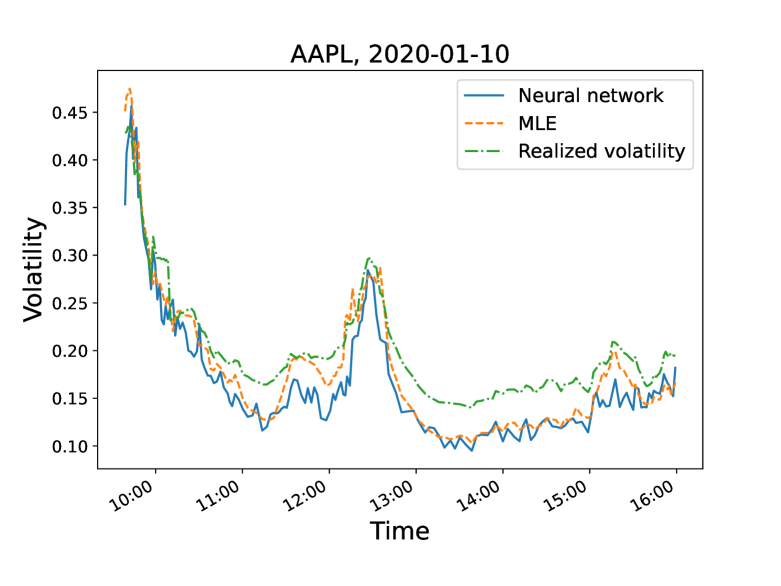

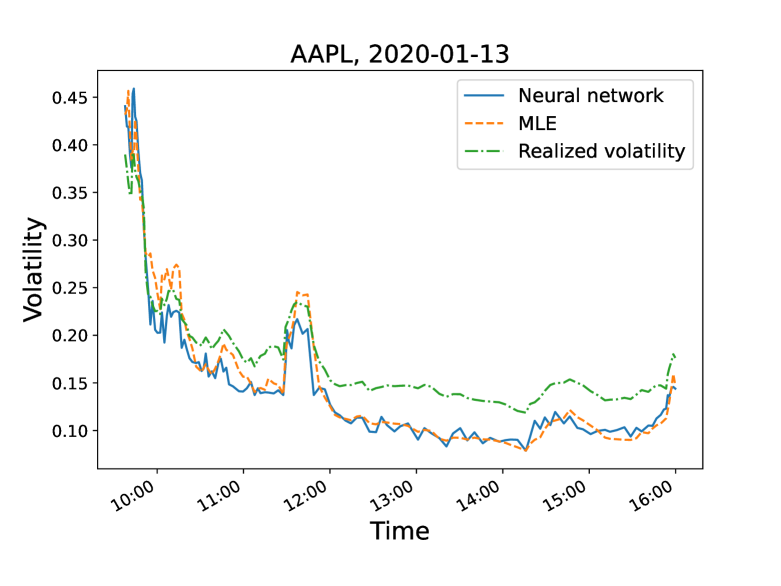

Figure 2 presents the instantaneous intraday annualized Hawkes volatility calculated using MLE, a neural network, and nonparametric realized volatility as a benchmark by Andersen et al. (2003). The realized volatility is calculated using the observed values at 1-second intervals for the price process of the period. All three measures have a similar trend throughout the day. Although it is not possible to present all the results examined, in some cases, MLE showed unstable dynamics of volatility. This is likely due to the fact that the 2,000-time length used for estimation is a relatively small sample size to estimate the parameters of the Hawkes model.

5 Conclusion

This study shows that a neural network can accurately estimate time series parameters, with an accuracy similar to MLE and much faster computation. While the example used here is for calculating Hawkes volatility, but our proposed method can be applied to various fields. It can be particularly useful in cases where the model is complex and traditional estimation procedures are challenging, such as modeling entire limit order book. Further research in this area is expected to be ongoing and diverse.

Acknowledgements

This work has supported by the National Research Foundation of Korea(NRF) grant funded by the Korea government(MSIT)(No. NRF-2021R1C1C1007692).

References

- Andersen et al. (2003) Andersen, T. G., T. Bollerslev, F. X. Diebold, and P. Labys (2003). Modeling and forecasting realized volatility. Econometrica 71, 579–625.

- Bacry et al. (2013) Bacry, E., S. Delattre, M. Hoffmann, and J.-F. Muzy (2013). Modelling microstructure noise with mutually exciting point processes. Quantitative Finance 13, 65–77.

- Cho et al. (2014) Cho, K., B. Van Merriënboer, D. Bahdanau, and Y. Bengio (2014). On the properties of neural machine translation: Encoder-decoder approaches. arXiv preprint arXiv:1409.1259.

- Ghosh et al. (2022) Ghosh, P., A. Neufeld, and J. K. Sahoo (2022). Forecasting directional movements of stock prices for intraday trading using lstm and random forests. Finance Research Letters 46, 102280.

- Hawkes (1971) Hawkes, A. G. (1971). Point spectra of some mutually exciting point processes. Journal of the Royal Statistical Society. Series B (Methodological) 33, 438–443.

- Hochreiter and Schmidhuber (1997) Hochreiter, S. and J. Schmidhuber (1997). Long short-term memory. Neural computation 9, 1735–1780.

- Kingma and Ba (2014) Kingma, D. P. and J. Ba (2014). Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980.

- Lee (2022) Lee, K. (2022). Application of hawkes volatility in the observation of filtered high-frequency price process in tick structures. arXiv 2207.05939.

- Lee and Seo (2017) Lee, K. and B. K. Seo (2017). Marked Hawkes process modeling of price dynamics and volatility estimation. Journal of Empirical Finance 40, 174–200.

- Mei and Eisner (2017) Mei, H. and J. M. Eisner (2017). The neural Hawkes process: A neurally self-modulating multivariate point process. Advances in Neural Information Processing Systems 30.

- Wang et al. (2022) Wang, X., J. Feng, Q. Liu, Y. Li, and Y. Xu (2022). Neural network-based parameter estimation of stochastic differential equations driven by lévy noise. Physica A: Statistical Mechanics and its Applications 606, 128146.

- Wei and Jiang (2022) Wei, Y. M. and Z. Jiang (2022). Estimating parameters of structural models using neural networks. USC Marshall School of Business Research Paper.

- Wlas et al. (2008) Wlas, M., Z. Krzeminski, and H. A. Toliyat (2008). Neural-network-based parameter estimations of induction motors. IEEE Transactions on Industrial Electronics 55, 1783–1794.

- Zhang et al. (2021) Zhang, Y., G. Chu, and D. Shen (2021). The role of investor attention in predicting stock prices: The long short-term memory networks perspective. Finance Research Letters 38, 101484.