Can Perturbations Help Reduce Investment Risks? Risk-Aware Stock Recommendation via Split Variational Adversarial Training

Abstract.

In the stock market, a successful investment requires a good balance between profits and risks. Based on the learning to rank paradigm, stock recommendation has been widely studied in quantitative finance to recommend stocks with higher return ratios for investors. Despite the efforts to make profits, many existing recommendation approaches still have some limitations in risk control, which may lead to intolerable paper losses in practical stock investing. To effectively reduce risks, we draw inspiration from adversarial learning and propose a novel Split Variational Adversarial Training (SVAT) method for risk-aware stock recommendation. Essentially, SVAT encourages the stock model to be sensitive to adversarial perturbations of risky stock examples and enhances the model’s risk awareness by learning from perturbations. To generate representative adversarial examples as risk indicators, we devise a variational perturbation generator to model diverse risk factors. Particularly, the variational architecture enables our method to provide a rough risk quantification for investors, showing an additional advantage of interpretability. Experiments on several real-world stock market datasets demonstrate the superiority of our SVAT method. By lowering the volatility of the stock recommendation model, SVAT effectively reduces investment risks and outperforms state-of-the-art baselines by more than in terms of risk-adjusted profits. All the experimental data and source code are available at https://drive.google.com/drive/folders/14AdM7WENEvIp5x5bV3zV_i4Aev21C9g6?usp=sharing.

1. Introduction

The stock market, one of the largest financial markets in the world, has been an attractive platform allowing millions of investors to manage their assets for wealth growth. However, its highly volatile nature presents not only opportunities for profits, but also risks of losses (Adam et al., 2016). In order to achieve a good balance between profits and risks, stock investors have been striving for methods that can accurately predict the future trend of the stock market (Cavalcante et al., 2016). Unfortunately, stock prediction is extremely challenging due to the highly stochastic and non-stationary nature of stock prices. Under such circumstances, more and more researchers have opted for advanced machine learning methods to study stock movements and make profitable predictions (Rouf et al., 2021).

Modern stock prediction solutions mainly fall into three categories, namely regression, classification, and recommendation methods (Rouf et al., 2021). Regression methods formulate stock prediction as a pure time series forecasting problem and predict the future stock prices/returns by learning from historical stock time series data (Schumaker and Chen, 2009; Tsay, 2010; Li et al., 2016; Qin et al., 2017; Cheng et al., 2020; Zhang et al., 2018; Malibari et al., 2021). On the other hand, classification methods treat stock prediction as a binary up/down classification problem and develop accurate classifiers to perform stock movement prediction (Xu and Cohen, 2018; Feng et al., 2019a; Li et al., 2022). Nevertheless, general regression and classification methods have a significant drawback that they are not directly optimized towards the target of investment (i.e., profit maximization) (Feng et al., 2019b; Sawhney et al., 2021), which may lead to abnormal results such that accurate prediction models earn less profit than inaccurate models. Figure 1 shows an example of how the problem occurs. To overcome this drawback, some researchers have proposed to employ reinforcement learning methods (Sun et al., 2023; Carta et al., 2021; Liu et al., 2020) to improve model profits by capturing trading signals in a dynamic prediction. Other researchers have developed recommendation methods to rank stocks with return ratios based on the comparison among multiple stocks (Gao et al., 2022). In this case, models are trained to select top- stocks with maximum expected profits so as to ensure their consistency with the investment target. Accordingly, various stock recommendation models have been proposed and shown a promising prospect in the stock prediction domain (Feng et al., 2019b; Gao et al., 2022; Sawhney et al., 2021; Wang et al., 2022).

The stock example of abnormal results

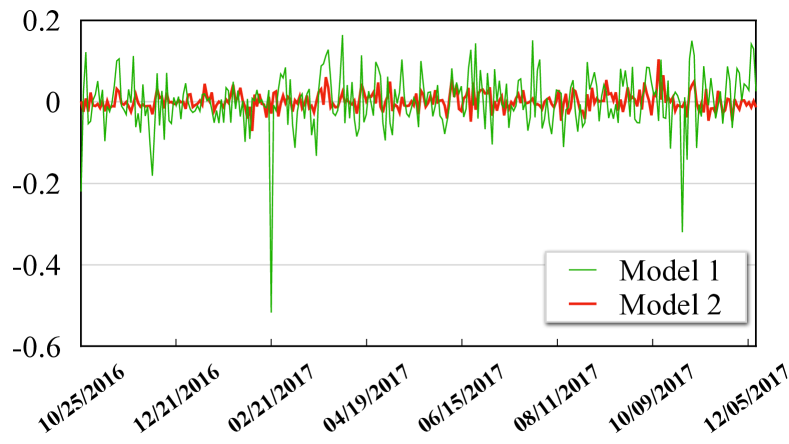

Despite the efforts to maximize profits for investors, many existing stock recommendation methods still have some limitations in risk control. Most of them mainly focus on developing powerful learning models to improve the investment profit, while ignoring effective risk modeling. Such a deficiency may limit their effectiveness in practical stock investing and cause painful consequences. For example, Figure 2a presents daily returns of two stock recommendation models backtested in the NASDAQ stock market from 10/25/2016 to 12/11/2017. Although both models attain nearly the same amount of profit (i.e., the sum of all daily returns), Model 1 is more volatile than Model 2 and suffers from a higher risk of potential losses. When employing Model 1 for stock trading, even if the final profit () is considerable, the huge paper loss of on 02/21/2017 can be intolerable to some investors and force them to stop investing halfway to prevent bankruptcy. In other words, the high volatility (risk) of Model 1 is prone to “kill the investor before the dawn”. To avoid such a disaster, it is imperative to reduce risks in addition to profit maximization when performing stock recommendation.

Motivation of the split AT design

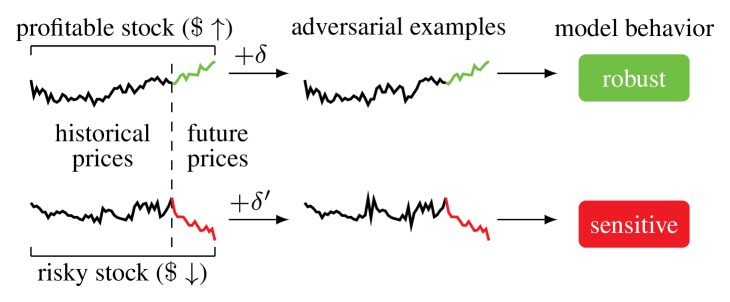

In this paper, we explore the possibility of leveraging adversarial perturbations (Goodfellow et al., 2015) to reduce stock recommendation risks. This motivation leads to Split Variational Adversarial Training (SVAT), a novel adversarial training (AT) framework for risk-aware stock recommendation. The first innovation of our method is the split AT design. Without external information such as financial reports, the risk of potential losses mainly comes from adverse movements of historical stock prices, which are difficult to identify from the stochastic price series. To address the challenge, we propose to capture stock risks through the model’s sensitivity to adversarial examples (AEs) (Goodfellow et al., 2015). As depicted in Figure 2b, for each stock example, we can generate AEs by adding small perturbations on their input features. Unlike conventional AT methods (Qian et al., 2022) which encourage the model to be robust to all AEs, we split the AT process to make the model robust to AEs of profitable stocks but sensitive to AEs of risky stocks. In this way, the recommendation model can recognize risks by learning from different perturbations, improving the capability of risk control.

Another challenge is how to craft representative AEs as risk indicators. Stock prices can be affected by multiple risk factors such as company performance and macroeconomics, which cannot be effectively modeled by traditional gradient-based AT methods. Hence, motivated by Variational Autoencoders (Kingma and Welling, 2014) and Adversarial Distributional Training (Dong et al., 2020), we devise a variational perturbation generator (VPG) to learn an adversarial distribution driven by multiple latent risk factors, from which diverse perturbations can be generated for comprehensive risk modeling. Furthermore, in the testing environment, we could roughly quantify the risk of each stock example by generating its AEs from VPG and computing the entropy using different adversarial outputs. The risk quantification shows an additional advantage of interpretability provided by our method.

In this work, we employ STHAN-SR (Sawhney et al., 2021) as the backbone recommendation model and combine it with SVAT to achieve the state-of-the-art (SOTA) results. Our contributions are of four-folds:

-

•

We investigate the limitation of risk modeling negligence and highlight the necessity of reducing stock recommendation risks.

-

•

We propose a novel Split Variational Adversarial Training method to enhance the risk sensitivity of the stock recommendation model, with the additional benefit of providing a rough risk quantification for investors.

-

•

To the best of our knowledge, this is the first work to engage adversarial training for risk modeling in stock recommendation, showing a new possibility for reducing investment risks with adversarial perturbations.

-

•

We conduct extensive experiments on three real-world datasets and show advantages of our model against state-of-the-art baselines, demonstrating the effectiveness and practicality of the SVAT method.

The remainder of this paper is organized as follows. Section 2 introduces the preliminary knowledge about stock recommendation and adversarial training, which forms the building blocks of our method. Section 3 presents our proposed SVAT method. Section 4 describes the extensive experiments we conduct. Finally, we review related work in Section 5 and draw a conclusion in Section 6.

2. Preliminary

2.1. Problem Formulation

We focus on the task of stock recommendation under the learning to rank paradigm. Given a set of stocks , for each stock on trading day , there is an associated close price and a 1-day return ratio computed as . According to the value of each , we can determine a ranking list of all stocks sorted by their ranking scores , where if and only if for any two stocks . Therefore, stocks with higher ranking scores indicate higher investment revenue on trading day . Formally, the goal of stock recommendation is to predict ranking scores given historical sequential data :

| (1) |

where represents the input features of all stocks on trading day (), is the feature dimension and is the length of the lookback window. is the ranking function with parameters to be learned. Following the previous work (Feng et al., 2019b; Sawhney et al., 2021; Wang et al., 2022), the loss function for optimizing is the combination of a pointwise regression loss and a pairwise ranking loss:

| (2) |

where is a hyperparameter to balance the two loss terms. If not otherwise specified, we usually set the ground-truth ranking score . After obtaining the prediction , we can select the top- stocks from the ranking list for trading.

2.2. Adversarial Training Definition

Traditional adversarial training aims to improve the adversarial robustness of DNN classifiers by adding perturbations on sample features. Given a dataset of training examples with (denoting the input features) and (denoting the ground-truth label), AT can be formulated as the following minimax optimization problem (Madry et al., 2018):

where is the DNN model with parameters , is a loss function, is a perturbation set with and denotes the -norm of a vector. To enrich the diversity of perturbations, Adversarial Distributional Training (ADT) (Dong et al., 2020) is further proposed to learn a perturbation distribution by minimizing

where is a set of distributions with support contained in . ADT solves the above minimax problem by simultaneously optimizing and in a single inseparable step, which is inapplicable to our split AT design. Hence, we devise a new training algorithm that combines the fast gradient approximation (Goodfellow et al., 2015) and the variational Bayes (Kingma and Welling, 2014) to learn and more flexibly.

3. Methodology

3.1. Motivation

We first explain our motivation for designing SVAT. From the perspective of investors, the main source of stock recommendation risks comes from that the model may incorrectly assign higher scores to risky stocks with losses () than profitable stocks (), after which risky stocks are recommended to investors, leading to high volatility of investment returns. One way to mitigate this problem is to train the recommendation model to be more fond of profitable stocks and more alert/sensitive to risky stocks. Adversarial training (AT) paves the way to obtain this “split” behavior since we can indirectly manipulate the model’s sensitivity to different individual examples through their adversarial perturbations (Lyu et al., 2015; Qian et al., 2022). While conventional AT methods aim to encourage the model to be robust to imperceptible perturbations (Goodfellow et al., 2015; Qian et al., 2022), researchers have found that increasing the sensitivity to perturbations could also help the model better capture the diversity of data samples, calling the Inverse Adversarial Training (IAT) (Zhou et al., 2021). Accordingly, we posticulate that the combination of AT and IAT, namely the split AT shown in Figure 2b, can help the model better discriminate between profitable and risky stocks by learning from their perturbations in a different way and thus further reduce the probability of recommending risky stocks. This is the main reason why we design two different perturbations for profitable stocks and risky stocks, respectively. In addition, Variational Autoencoder (VAE) (Kingma and Welling, 2014) is excellent in learning data distribution and can be used to model various stock factors (Duan et al., 2022). All considerations above finally converge to our SVAT method.

Although SVAT is designed to reduce stock recommendation risks, we believe that similar idea could also be applied to reduce ranking uncertainties of other learning to rank problems, such as recommender systems where positive items are more preferred than negative items.

3.2. Overview

For better illustration of the risk modeling w.r.t each stock example, we literally decompose the ranking model in Equation (1) into ranking submodules sharing the same parameters , with each predicting the ranking score of stock :

| (3) | ||||

where is the feature vector transformed from the historical sequential features of stock , and is the transformation function which could be simple row concatenation or temporal embedding with RNN architectures (Feng et al., 2019a; Sawhney et al., 2021). Similar to ADT, we model the adversarial perturbations around each stock example by a conditional distribution , whose support is contained in 111We empirically found that the -norm constraint is better for the stock recommendation problem.. Next, we can sample a perturbation from to construct an adversarial example , and obtain the perturbed output by

| (4) |

During the training phase, the adversarial loss for stock can be computed as

| (5) |

and the total adversarial loss is the sum of each weighted by the corresponding stock’s return ratio :

| (6) |

When we train the model by minimizing , the adversarial loss of stock examples with is minimized while the adversarial loss of stock examples with is maximized. In this way, the stock recommendation model is encouraged to be more robust to adversarial perturbations of profitable stock examples while more sensitive to adversarial perturbations of risky stock examples. This split adversarial training approach better enhances the risk awareness of the model by treating adversarial examples of profitable and risky stocks in an opposite way, which is consistent with the split behavior we described in the previous section.

Besides, when deploying the model to the testing environment, we can quantify the risk of each stock example by sampling multiple adversarial perturbations from . Specifically, for each testing example , we generate Monte Carlo perturbation samples from , and obtain different perturbed ranking scores from Equation (4). Comparing these scores with other stock examples produces rankings , which is used to compute the ranking entropy for :

| (7) |

where denotes the frequency of being ranked the -th stock and we have . Investors could roughly evaluate the risk of the current stock example according to the ranking entropy, where higher entropy generally indicates higher risk.

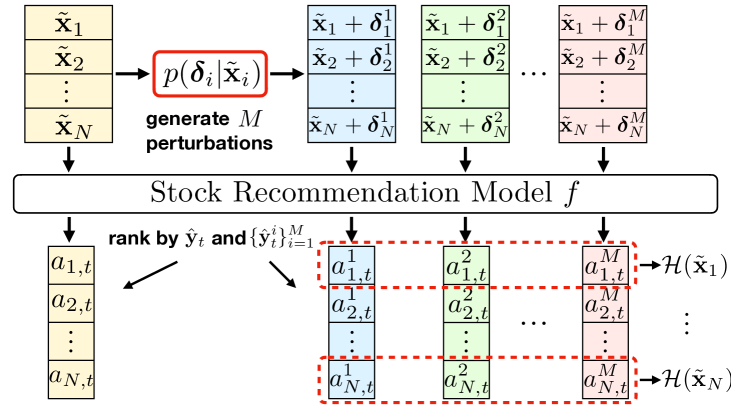

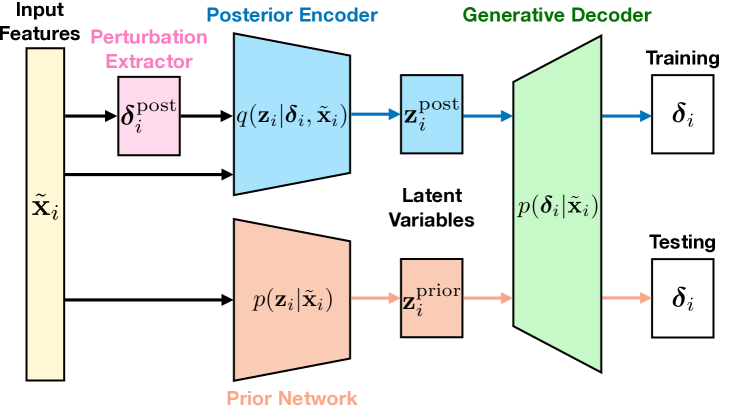

Figure 3a presents the workflow of our SVAT method. The core of SVAT lies in the learning of the perturbation distribution , which is detailed in the next section.

SVAT framework and VPG.

3.3. Variational Perturbation Generator

The key role of the perturbation distribution is to characterize potential risk factors of stocks and generate representative perturbation samples to help reduce investment risks. Since stock returns are typically affected by a variety of risk factors (e.g., macroeconomics, financial news), we decide to model these factors by some learnable latent variables that implicitly drive :

| (8) |

where is a learnable random vector containing risk-relevant latent variables. Although the integral of the marginal likelihood in Equation (8) is intractable, it can be approximated by VAE (Kingma and Welling, 2014), a reliable framework for neural approximation. In this spirit, we devise a Variational Perturbation Generator (VPG) to approximate with latent factors. As shown in Figure 3b, VPG contains three components: perturbation extractor, posterior encoder and generative decoder.

3.3.1. Perturbation Extractor

We first employ the fast gradient approximation method (Goodfellow et al., 2015; Feng et al., 2019a) as the perturbation extractor to extract a primitive perturbation sample from the gradient of the input features :

| (9) |

where is the prediction loss in Equation (2) and is the hyperparameter. provides the posterior information about real data to guide the approximation learning of VPG.

3.3.2. Posterior Encoder

The posterior encoder incorporates the primitive perturbation and the input features to learn a posterior distribution , from which posterior risk-relevant latent variables can be obtained:

| (10) | ||||

where can be any non-linear neural network such as the multi-layer perceptron (MLP), are learnable parameters, denotes the activation and is a latent vector sampled from the posterior Gaussian distribution .

3.3.3. Generative Decoder

Finally, combining the information of the latent variables and the input features , we train a generative decoder network to approximate the desired perturbation distribution and generate the risk-indicated perturbation :

| (11) |

after which is engaged in Equation (4) to produce an adversarial example. During the training phase we simply input to , which is however unrealizable in the testing environment since we cannot obtain the loss and gradients to extract of testing examples without knowing their ground-truth labels. Accordingly, we further design another network to learn a prior distribution :

| (12) | ||||

and enforce the prior distribution to approximate to the posterior distribution by minimizing

| (13) |

where is the Kullback-Leibler divergence between two distributions. In this way, we can sample multiple s from and generate representative perturbations for testing examples without computing their gradients, which facilitates the risk quantification in Equation (7) and improves the risk interpretability of the stock recommendation model.

3.3.4. Explanation for VPG

As discussed in Section 3.1, we aim to enhance the risk awareness of the stock recommendation model by encouraging the model to learn perturbations of profitable and risky stocks in a different way. Accordingly, the main goal of VPG is to provide an effective mechanism to generate perturbations for different stocks. As shown in Figure 3b, VPG follows an encoder-decoder architecture and generates perturbations from a latent space. Since there are a variety of complex risk factors affecting stock prices, it is feasible to encode these risk factors into a latent space. Based on the framework of Variational Autoencoder (VAE) (Kingma and Welling, 2014), we assume that the perturbation of each stock can be generated from a latent random variable in the risk-factor latent space. We first use an encoder to learn the posterior distribution of given and then employ a decoder to learn a perturbation distribution close to the posterior distribution during the training phase. Finally in the testing phase, we could sample representative perturbations of all stocks from the perturbation distribution efficiently without the overhead of computing the gradient of each stock example.

In summary, the VPG can characterize various risk factors in a latent space and generate representative perturbation samples of different stocks, which is critical to enhance the risk awareness of the stock recommendation model.

3.3.5. Theoretical Justification

We present the theoretical justification of VPG based on the theoretical framework of Variational Autoencoder (VAE) (Kingma and Welling, 2014). Given datapoints from the training dataset, the goal of VPG is to maximize the sum of the marginal likelihoods , where is driven by some risk-relevant latent variables :

| (14) | ||||

Without loss of generality, we assume that is a Gaussian distribution conditioned on and is a Gaussian distribution conditioned on both and :

| (15) | ||||

where are learnable functions that output the mean of the Gaussian and are learnable functions that output the covariance of the Gaussian, all of which can be approximated by neural networks. In this case, we can sample a large number of from and approximate the expectation in Equation (14) by average:

| (16) | ||||

However, this approach suffers from curse of dimensionality since the sample number grows exponentially as the dimension of increases. Besides, for any given observations and , most will contribute very little to the likelihood.

To solve the problem above, Variational Autoencoder (VAE) (Kingma and Welling, 2014) proposes to sample the latent variables from the posterior distribution and only pick a small number of values that contribute a significant amount to the likelihood. Specifically, VAE approximates the ground-truth posterior distribution by a learnable model with parameters . Considering the Kullback-Leibler divergence between and , we obtain:

| (17) | ||||

Rearranging Equation (17), we finally obtain the evidence lower bound (ELBO) proposed in (Kingma and Welling, 2014):

| (18) | ||||

Therefore, we can maxmize the marginal likelihood and minimize the Kullback-Leibler divergence (i.e., the LHS of Equation (18)) by equivalently maximizing and minimizing (i.e., the RHS of Equation (18)), which is exactly what VPG does. As shown in Figure 3b, VPG utilizes the Posterior Encoder and the Prior Network to model the approximated posterior distribution and the prior distribution , respectively. And we minimize their Kullback-Leibler divergence by minimizing the in Equation (13). On the other hand, since all perturbations generated from are expected to be representative risk indicators that can minimize the in Equation (6), we can maximize the likelihood by equivalently minimizing the . Finally, we conclude that the proposed SVAT loss is consistent with the theoretical framework of VAE.

Note that during the training phase, we only sample one from the approximated posterior distribution in each epoch and approximate the expectation by training the VPG for multiple epochs, thus avoiding a large number of sampling as in Equation (16) and the curse of dimensionality.

3.4. Model Training

We summarize the training process of SVAT as Algorithm 1. The stock recommendation model and all components of the VPG are trained end-to-end by minimizing the combined loss function of Equation (2), (6) and (13):

where and is a hyperparameter to control the contribution of the SVAT loss. We utilize the Adam (Kingma and Ba, 2015) algorithm for optimization.

4. Experiments

The core of this section is to evaluate whether our method can effectively reduce stock investment risks for investors. Accordingly, we conduct extensive experiments with the aim of answering the following research questions:

-

•

RQ1: How is the utility of our proposed SVAT method in a general economic environment? Can SVAT outperform state-of-the-art stock recommendation models in terms of risk-adjusted profits under normal circumstances?

-

•

RQ2: How is the utility of our SVAT method in an extreme economic environment such as the financial crisis? Can SVAT protect investors from risks better than other state-of-the-art stock recommendation models under extreme circumstances?

-

•

RQ3: Does SVAT capture different signals or recommend stocks different from other baseline methods? To what extent are all methods correlated with each other?

-

•

RQ4: How is the effectiveness of the split adversarial training design and the variational perturbation generator component of our proposed SVAT method?

-

•

RQ5: How does our proposed SVAT method perform under different backtesting strategies, different adversarial hyperparameter settings and different sampling methods?

-

•

RQ6: How does the adversarial perturbation of SVAT help reduce the risk of stock recommendation? What insights can investors learn from SVAT?

We next conduct different experiments to answer the RQs above, comprehensively demonstrating the effectiveness, practicality, and robustness of our approach.

4.1. Experimental Setting

4.1.1. Datasets

As shown in Table 1, our experiments are based on six real-world datasets from US and China stock markets, including three normal datasets in a general economic environment (RQ1) and three crisis datasets during the financial crisis period (RQ2):

-

•

Normal datasets:

-

–

NASDAQ (Feng et al., 2019b): This dataset contains the price data of equity stocks in the NASDAQ Global and Capital market from 01/02/2013 to 12/08/2017.

-

–

NYSE (Feng et al., 2019b): This dataset consists of the price data of equity stocks in the New York Stock Exchange market from 01/02/2013 to 12/08/2017.

-

–

CASE: This dataset collects the price data of equity stocks from the China A-share Stock Exchange market from 03/01/2016 to 03/04/2022.

-

–

-

•

Crisis datasets:

-

–

NASDAQ_08: This dataset contains the price data of equity stocks in the NASDAQ Global and Capital market from 01/02/2002 to 12/31/2008.

-

–

NYSE_08: This dataset consists of the price data of equity stocks in the New York Stock Exchange market from 01/02/2002 to 12/31/2008.

-

–

CASE_08: This dataset collects the price data of equity stocks from the China A-share Stock Exchange market from 01/04/2002 to 12/31/2008.

-

–

All the stock datasets above are collected every one day (i.e., daily price data), within which each data point consists of 5 features (i.e., the opening price, highest price, lowest price, closing price, and trading volume of the stock for the day). Among these datasets, NASDAQ and NYSE have been widely used in most previous work (Feng et al., 2019b; Sawhney et al., 2021; Wang et al., 2022) and we also use them here to ensure fair comparison with other state-of-the-art models. On the other hand, we collect the data of CASE and CASE_08 from RiceQuant222https://www.ricequant.com/, the data of NASDAQ_08 and NYSE_08 from Yahoo Finance333https://finance.yahoo.com/, respectively. In particular, NASDAQ_08, NYSE_08, and CASE_08 datasets contain the stock data covering the entire 2007-2008 global financial crisis period, which is crucial to test the anti-risk ability of stock prediction models.

| Dataset | NASDAQ | NYSE | CASE | NASDAQ_08 | NYSE_08 | CASE_08 |

|---|---|---|---|---|---|---|

| Train(Tr) Period | 01/2013-12/2015 | 01/2013-12/2015 | 03/2016-04/2019 | 01/2002-12/2006 | 01/2002-12/2006 | 01/2002-12/2006 |

| Valid(Va) Period | 01/2016-12/2016 | 01/2016-12/2016 | 04/2019-04/2020 | 01/2007-10/2007 | 01/2007-10/2007 | 01/2007-10/2007 |

| Test(Te) Period | 01/2017-12/2017 | 01/2017-12/2017 | 04/2020-03/2022 | 11/2007-12/2008 | 11/2007-12/2008 | 11/2007-12/2008 |

| Days(Tr:Va:Te) | 756:252:237 | 756:252:237 | 756:252:456 | 1259:211:295 | 1259:211:295 | 1205:201:289 |

| Stocks |

4.1.2. Baselines

Since we focus on reducing investment risks of stock recommendation, we compare our method with the stock market composite index and 7 stock recommendation baseline methods as follows:

-

•

Buy&Hold: This is the simplest trading strategy where we buy the composite index of all stocks and hold. The results of this buy and hold index represent the average benchmark performance of the stock market.

-

•

ARIMA (Ariyo et al., 2014): This method is the traditional Autoregressive Integrated Moving Average model for time series prediction. We use it to directly predict the return ratio of each stock and recommend stocks with the highest predicted return ratios.

-

•

LSTM (Bao et al., 2017): This method is the vanilla LSTM model which operates on the sequential stock price data and obtains a sequential embedding for stock recommendation. We finally combine it with a fully-connected layer to predict the ranking score of each stock.

-

•

GCN (Kipf and Welling, 2017): GCN is the typical and representative graph-based learning method. We use the vanilla GCN architecture to model the stock relation graph and combine it with a fully-connected layer to predict the ranking score of each stock.

-

•

RSR-E (Feng et al., 2019b): This method develops a temporal GCN model using price movement similarity to weight the relation between different stocks and improves the performance of stock relation learning.

-

•

RSR-I (Feng et al., 2019b): This method employs an implicit neural network to adatively learn the stock relation and improves the adaptability of the temporal GCN model.

-

•

ANN-SVM (Kurani et al., 2023): This method incorporates a non-linear Artificial Neural Network (ANN) and a Support Vector Machine (SVM) to perform stock recommendation.

-

•

STHAN-SR (Sawhney et al., 2021): This method leverages a hypergraph attention network to learn the stock relation and achieve great improvements on stock recommendation.

4.1.3. Evaluation Metrics

Following the previous work (Feng et al., 2019b; Gao et al., 2022; Sawhney et al., 2021; Wang et al., 2022), we also adopt a daily buy-hold-sell trading strategy and evaluate all stock recommendation methods by the following three metrics:

-

(1)

Investment Return Ratio (IRR):

where denotes the set of top- stocks selected on trading day and is the -day return ratio of stock on trading day . IRR only evaluates the model’s profit without risk consideration.

-

(2)

Sharpe Ratio (SR):

(19) where is a risk-free return444T-Bill rates: https://home.treasury.gov/ and STD denotes the standard deviation. SR is a risk-adjusted return metric considering both the profit and the volatility of the model.

-

(3)

Maximum Daily Drawdown (MDD):

MDD measures the maximum daily loss of the model in backtesting (e.g., the MDD of Model 1 in Figure 2a is ), which evaluates to what extent can the model protect investors from the risk of loss.

4.1.4. Training Setup

We implement the models with PyTorch555https://pytorch.org/ except ARIMA of which we use the Python statsmodels package implementation666https://www.statsmodels.org/stable/index.html. For fair comparison, we use grid search to select optimal hyperparameters regarding SR for each model. For all methods, we tune the length of sequential input within and the learning rate within . For the LSTM and the GCN model, we tune the number of hidden units within . For RSR-E, RSR-I, ANN-SVM and STHAN-SR models, we conduct the same hyperparameter tuning as reported in their original papers (Feng et al., 2019b; Kurani et al., 2023; Sawhney et al., 2021). As for our SVAT method, we employ STHAN-SR (Sawhney et al., 2021) as the backbone recommendation model and tune the adversarial constraint within , loss weighting factors within . We employ a two-layer MLP with hidden neurons and activation to construct , respectively. We set and thus select top- stocks each day for evluation. Finally, we train all models on a Tesla V100 GPU for epochs.

4.1.5. Discussion: Predictability of Stock Daily Returns

The core task of our SVAT method and other stock recommendation baseline methods is to predict the daily returns of each stock and perform stock ranking, which relies on the basic premise that the stock daily returns are predictable. Indeed, there are some references (Arora et al., 2012; Patro and Wu, 2004; Guo, 2006; Milobedzki, 2004) that provide reliable evidence for the predictability of stock daily returns and thus support the rationality and feasibility for current stock recommendation researches. However, most of the references above used the stock market data in 1978-2002 to produce their evidence. Since the information transparency and the speed of information spread in 1978-2002 may differ from that in the current Internet era, it is necessary to further verify the predictability of stock daily returns in the Internet era. Unfortunately, we have not yet found any references using recent data to provide relevant evidence so far. Hence, we remain cautious about the predictability of stock daily returns in the Internet era and will explore this topic further in future work.

4.2. RQ1: Performance Comparison of Normal Economic Environment

| Dataset | NASDAQ | NYSE | CASE | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Model | IRR | SR | MDD | IRR | SR | MDD | IRR | SR | MDD |

| Buy&Hold | |||||||||

| ARIMA | |||||||||

| LSTM | |||||||||

| GCN | |||||||||

| RSR-E | |||||||||

| RSR-I | |||||||||

| ANN-SVM | |||||||||

| STHAN-SR | |||||||||

| SVAT (Ours) | |||||||||

Table 2 summarizes the experimental results of the buy and hold index and all stock recommendation methods in terms of profitability and risk on the three normal datasets (NASDAQ, NYSE, and CASE). We can obtain the following observations:

-

•

Comparing the results of Buy&Hold with those of other stock recommendation methods, we observe that Buy&Hold achieves the smallest MDD and competitive SR on the three normal datasets, mainly because it reduces the volatility of returns by averaging the stock returns across the whole market. However, the IRR of Buy&Hold is more than less than other state-of-the-art stock recommendation models such as RSR, ANN-SVM, STHAN-SR, and our SVAT methods. Therefore, the buy and hold index cannot attain a good balance between profits and risks in the stock market and it is necessary to develop more advanced stock recommendation methods.

-

•

Among all stock recommendation methods, our SVAT method outperforms the other baselines on all datasets, showing the superiority of the split variational adversarial training design for stock recommendation. Specifically, SVAT improves the SR by an average of and reduces the MDD by an average of compared to the second best results of other methods. Such an improvement answers the RQ1 that SVAT does outperform state-of-the-art stock recommendation models in terms of risk-adjusted profits under normal circumstances.

-

•

As for profitability, SVAT improves the cumulative return ratio (IRR) by an average of on the three normal datasets. This shows that increasing the risk-sensitivity of the model also helps improve the investment profit, probably by encouraging the model to avoid selecting stock examples with high risks.

-

•

Compared to the original backbone model STHAN-SR, SVAT greatly improves IRR, SR, MDD by an average of , respectively, which demonstrates that our method does help the stock recommendation model to effectively reduce investment risks and control potential losses under a safer and more tolerable risk level.

-

•

Without explicit risk modeling, the state-of-the-art models RSR-I, ANN-SVM and STHAN-SR even attain worse MDDs than simple methods LSTM and GCN on the NYSE and/or CASE datasets, which indicates that recent advanced stock recommendation models may not have achieved improvement in risk control. Hence, it is necessary and promising to design a method like SVAT to enhance the risk awareness of stock recommendation.

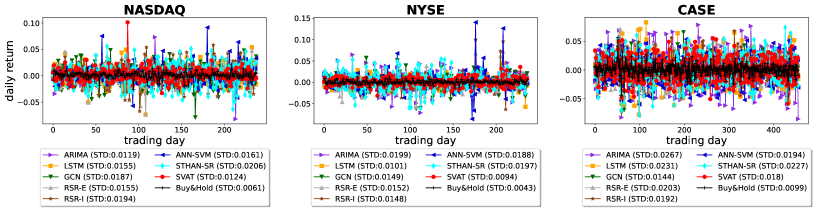

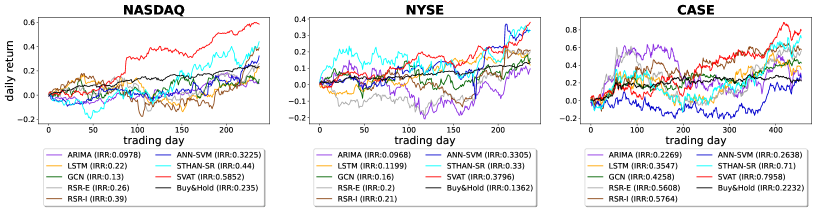

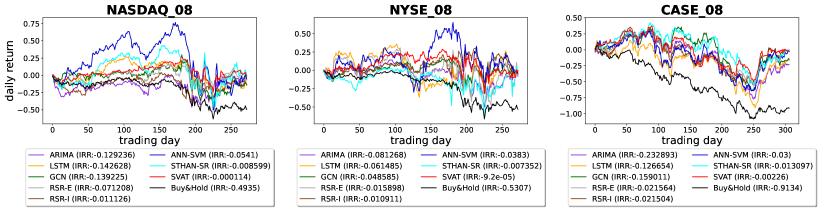

Daily and cumulative returns of all models.

Figure 4b presents the curves of daily returns and the cumulative investment return ratios (IRR) of all models backtested on the three normal datasets. Clearly, the standard deviation (STD) of SVAT’s daily returns is smaller and the IRR curve of SVAT is less volatile than recent advanced stock recommendation models RSR-E, RSR-I, ANN-SVM and STHAN-SR. Although the STD of SVAT’s daily returns is slightly larger than simple methods ARIMA/GCN on the NASDAQ/CASE dataset, SVAT obtains much larger IRR than ARIMA/GCN. Again, although the STD of Buy&Hold’s daily returns is the smallest, the IRR curve of Buy&Hold is inferior to other state-of-the-art stock recommendation models. All of these observations vividly shows that our method effectively reduces the volatility of the investment returns and achieves a good balance between profits and risks.

4.3. RQ2: Performance Comparison of Financial Crisis Period

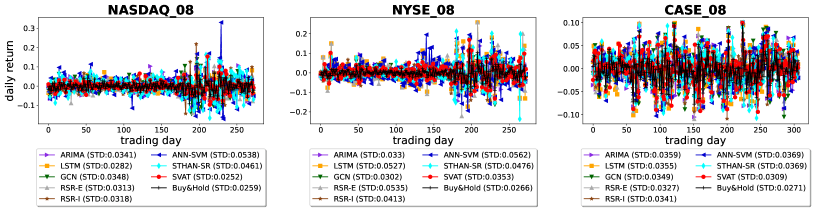

Table 3 shows the experimental results of the buy and hold index and all stock recommendation methods in terms of profitability and risk on the three crisis datasets (NASDAQ_08, NYSE_08, CASE_08), from which we observe that:

-

•

Due to the cruelty of the global financial crisis, all methods suffer investment losses (i.e., IRR ) on the three crisis datasets. In particular, although Buy&Hold achieves the smallest MDD across the three crisis datasets, the IRR and SR of Buy&Hold are much worse than other stock recommendation methods. This observation further demonstrates that a good stock recommendation model is critical to protecting investors from severe loss during the global financial crisis.

-

•

Remarkably, among all stock recommendation methods, our method SVAT achieves the best IRRs and MDDs across all crisis datasets, showcasing that SVAT successfully protects investors from more losses than the other baseline methods. This answers the RQ2 that SVAT can protect investors from risks better than other state-of-the-art stock recommendation models under the extreme circumstance of the global financial crisis.

-

•

As for volatility evaluation, SVAT attains the best SR on NYSE_08 and CASE_08 datasets but performs worse than the STHAN-SR model on NASDAQ_08 dataset. Nevertheless, Figure 5a shows that the volatility (i.e., the standard deviation (STD) of the model profit) of SVAT is lower than STHAN-SR on NASDAQ_08 dataset. This is mainly because according to Equation (19), the SR metric will decrease as the STD of the model profit decreases when IRR . Hence, the SR metric might be slightly distorted in the environment of global financial crisis, but Figure 5a demonstrates that our method can still effectively reduce the volatility of the stock recommendation model under extreme circumstances.

-

•

Similarly, although the state-of-the-art models RSR-E, RSR-I, ANN-SVM and STHAN-SR obtains better IRR and SR than simple methods ARIMA, LSTM, and GCN on the three crisis datasets, they perform poorly on the MDD metric. Instead, SVAT outperforms all stock recommendation methods on the MDD metric, showing the improvement on anti-risk ability during the global financial crisis period.

| Dataset | NASDAQ_08 | NYSE_08 | CASE_08 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Model | IRR | SR | MDD | IRR | SR | MDD | IRR | SR | MDD |

| Buy&Hold | |||||||||

| ARIMA | |||||||||

| LSTM | |||||||||

| GCN | |||||||||

| RSR-E | |||||||||

| RSR-I | |||||||||

| ANN-SVM | |||||||||

| STHAN-SR | |||||||||

| SVAT (Ours) | |||||||||

Daily and cumulative returns of all models on crisis datasets.

Again, we present the curves of daily returns and the cumulative investment return ratios (IRR) of all models backtested on the three crisis datasets in Figure 5b. As expected, the curves of the global financial crisis period are more volatile than that of the normal period shown in Figure 4b. However, our method still has better stability than other baseline stock recommendation methods and thus more effectively reduces the risk of losses for investors in the extreme environment of financial crisis. Similarly, although the STD of Buy&Hold’s daily returns is the smallest, the IRR curve of Buy&Hold is intolerable to most investors.

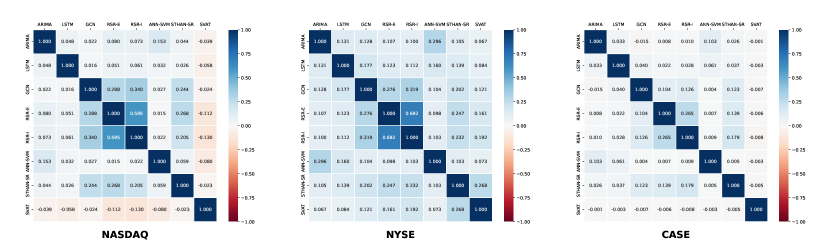

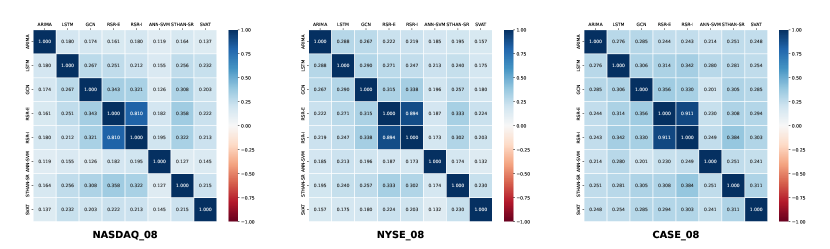

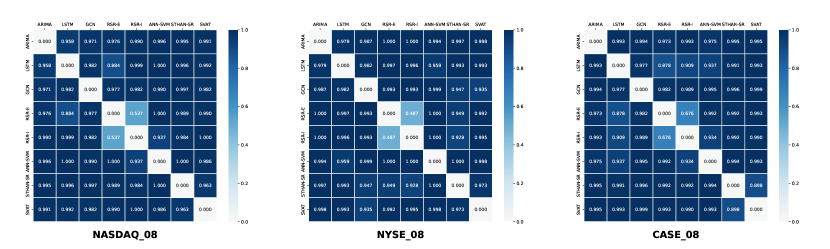

4.4. RQ3: Correlations between All Methods

From Figure 4b and Figure 5b, we observe that the cumulative investment returns of different methods behave differently under normal economic environment while exhibit high correlation with each other during the financial crisis period. Such differences inspire us to further investigate the extent to which all methods are correlated in different economic environments. Hence, in this section we aim to evaluate the correlation between different methods by the following two metrics:

-

(1)

Pearson Correlation Coefficient (PCC):

where denote any two of all the models, is the length of trading days, is the ranking score predicted by model on trading day and denote the expectation and the standard deviation w.r.t the set of all stocks , respectively. measures the linear correlation between any two of all the methods where a PCC value close to indicates a weak linear relationship between the two methods and vice versa.

-

(2)

Top- Stocks Difference ():

where denotes the set of top- stocks selected by model on trading day and thus is the number of different stocks among the top- stocks selected by models and . measures the extent of how any two of all the methods recommend stocks different from each other, with a value close to indicating a weak stock-selection relationship between the two methods and vice versa.

PCCs of all models.

TSDs of all models.

Figure 6b and Figure 7b show the PCC and between any two of all the methods, from which we can obtain the following observations about model correlation:

-

•

According to the PCC values in Figure 6b, the four models including GCN, RSR-E, RSR-I, and STHAN-SR are more correlated to each other than other models, mainly because that all of them are graph-based learning methods. Although our SVAT method employs STHAN-SR as the backbone model, it presents some different correlations compared to STHAN-SR and other graph-based models on the three normal datasets. Nevertheless, Figure 7b shows that the values between any two of all the methods are close to or above, except the two similar models RSR-E and RSR-I. The high values demonstrate that most methods have a weak stock-selection relationship and tend to independently recommend stocks different from other methods.

-

•

Particularly on the three normal datasets, our SVAT method exhibits weak negative correlations with other methods on NASDAQ and CASE datasets, while maintaining weak positive correlations on NYSE dataset. Recalling the fact that NASDAQ and CASE stock markets are more volatile than NYSE stock market (Sawhney et al., 2021), we infer that the proposed split variational adversarial training framework is better at capturing different trading signals in more volatile markets.

-

•

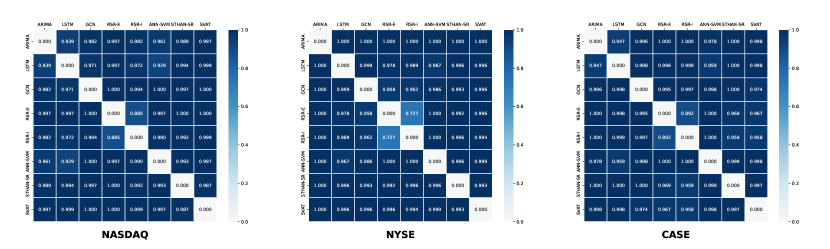

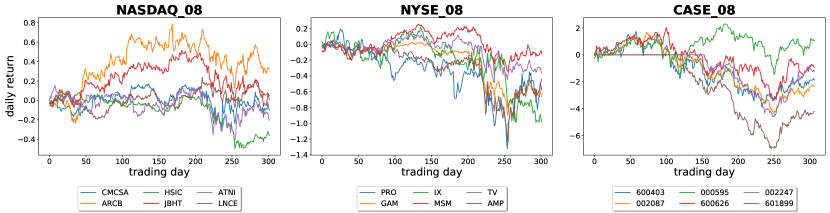

Paradoxically, both the cumulative investment returns in Figure 5b and the PCC values in Figure 6b show that all methods have relatively high correlations on the three crisis datasets, but the high values in Figure 7b reveals that most methods have weak stock-selection relationships. We speculate that under the extreme situation of the global financial crisis, most stocks suffered from similar drawdowns. Figure 8 presents the cumulative return curves of six stocks (randomly selected) of the three crisis datasets during the global financial crisis, from which we observe that all these stocks experienced similar drawdowns and their cumulative investment returns are highly correlated. Therefore, although different methods will recommend different stocks to investors, they produce highly correlated cumulative investment returns during the global financial crisis.

Stock returns on the crisis datasets.

4.5. RQ4: Effectiveness of Model Design

4.5.1. Effects of SVAT on Other Baselines

We have demonstrated that incorporating SVAT with the backbone model STHAN-SR can achieve the best results against other state-of-the-art baselines. In this section, we further evaluate the overall performance of the SVAT method by inspecting whether SVAT could also improve the performance of other baselines. Hence, we combine the SVAT method with LSTM, GCN, RSR-E, RSR-I, ANN-SVM models for stock recommendation, respectively, and compare their results with original models.

Table 4 shows the comparison results between other baselines and their SVAT-variants on the normal and the crisis datasets. Among the total 90 comparison cases, the SVAT-variants score 85 better results. This further demonstrates that SVAT is a general learning framework that can be incorporated with various stock recommendation models to enhance their risk awareness.

| Dataset | NASDAQ | NYSE | CASE | Better Results | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Model | IRR | SR | MDD | IRR | SR | MDD | IRR | SR | MDD | Count |

| LSTM | ||||||||||

| SVAT+LSTM | ||||||||||

| GCN | ||||||||||

| SVAT+GCN | ||||||||||

| RSR-E | ||||||||||

| SVAT+RSR-E | ||||||||||

| RSR-I | ||||||||||

| SVAT+RSR-I | ||||||||||

| ANN-SVM | ||||||||||

| SVAT+ANN-SVM | ||||||||||

| Dataset | NASDAQ_08 | NYSE_08 | CASE_08 | Better Results | ||||||

| Model | IRR | SR | MDD | IRR | SR | MDD | IRR | SR | MDD | Count |

| LSTM | ||||||||||

| SVAT+LSTM | ||||||||||

| GCN | ||||||||||

| SVAT+GCN | ||||||||||

| RSR-E | ||||||||||

| SVAT+RSR-E | ||||||||||

| RSR-I | ||||||||||

| SVAT+RSR-I | ||||||||||

| ANN-SVM | ||||||||||

| SVAT+ANN-SVM | ||||||||||

4.5.2. Ablation Study of Key Components

Our method consists of two key components, the split adversarial training mechanism (Equation (6)) and the variational perturbation generator (VPG), as shown in Figure 3b. In this experiment, we aim to evaluate whether these two components are necessary to reduce stock recommendation risks. Therefore, to show the effectiveness of each component, we compare SVAT with two variants:

-

•

SVATw/oS: We change the adversarial loss in Equation (6) to be without weighting by stocks’ return ratios, which reduces SVAT to conventional adversarial training without the split effect.

-

•

SVATw/oV: We remove the VPG from SVAT and only employ Equation (9) to generate the perturbation for each stock example.

Table 5 presents the results of comparison on the normal and the crisis datasets. We can observe that SVAT attains higher IRR and SR than all variants on most datasets. However, the MDD of SVAT is relatively inferior to its variants on NASDAQ, NYSE, and NYSE_08 datasets. We postulate the reason is that either the split effect or the VPG mainly works to reduce the risk of maximum daily loss without significant profit improvement, while combining them into the complete SVAT framework can achieve a better balance between profits and risks. As a result, both the split adversarial training mechanism and the variational perturbation generator are necessary to construct the complete SVAT architecture for better stock recommendation.

| Dataset | NASDAQ | NYSE | CASE | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Model | IRR | SR | MDD | IRR | SR | MDD | IRR | SR | MDD |

| SVATw/oS | |||||||||

| SVATw/oV | |||||||||

| SVAT | |||||||||

| Dataset | NASDAQ_08 | NYSE_08 | CASE_08 | ||||||

| Model | IRR | SR | MDD | IRR | SR | MDD | IRR | SR | MDD |

| SVATw/oS | |||||||||

| SVATw/oV | |||||||||

| SVAT | |||||||||

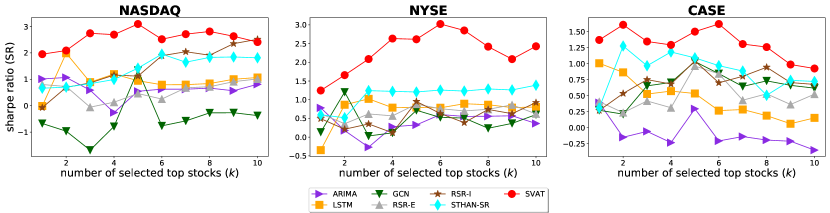

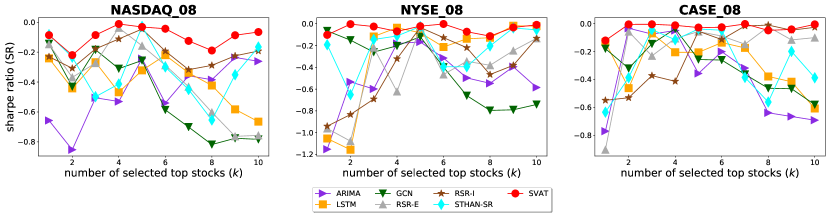

4.6. RQ5: Parameter Sensitivity Analysis

4.6.1. Performance under Different Backtesting Strategies

In the scenario of stock recommendation, the core strategy is to select top- stocks for investment, where different values of could derive diverse investment strategies. In previous experiments, we follow the previous work (Feng et al., 2019b; Sawhney et al., 2021; Wang et al., 2022) and generally set in order to make consistent comparison with other baseline methods. In practice, however, investors are free to choose different values of to develop more profitable investment strategies. Therefore, it is necessary to investigate the performance of our proposed method against other baselines under different backtesting strategies. In this section, we conduct backtesting on all methods with , corresponding to strategies of buying stocks with top-, top-, …, top- highest expected returns, respectively. Figure 9b presents the sharp ratios (SRs) of each model backtesting on the normal and the crisis datasets with different strategies, from which we have the following observations:

-

•

Clearly, our method SVAT achieves the best results under different backtesting strategies on almost all datasets, demonstrating the strong adaptability of SVAT such that it is applicable to a wide variety of strategies.

-

•

While most baseline methods stably attain good performance across different strategies on the normal datasets, they experience high volatility under different strategies on the crisis datasets. This observation exposes that under the extreme circumstances of the global financial crisis, existing stock recommendation baselines are prone to be vulnerable and their performance is highly dependent on the investment strategy. Instead, SVAT consistently shows great robustness across different strategies even on the crisis datasets, demonstrating the advantage of incorporating our split variational adversarial training framework for risk-aware stock recommendation.

Sensitivity of the parameter k on the normal and the crisis datasets.

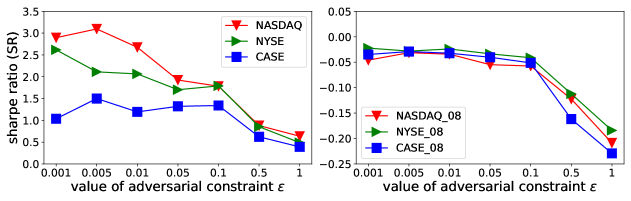

4.6.2. Impact of the Adversarial Hyperparameter

For adversarial learning methods, the adversarial hyperparameter in Equation (9) plays an important role in the model performance (Cheng et al., 2022). In this section, we investigate how the performance of our method SVAT varies with different . Figure 10 presents the sharp ratio (SR) of SVAT backtesting on all datasets with different values of . Obviously, the performance of SVAT drops significantly when , since a large may produce excessive perturbations that are harmful for model training. On the contrary, SVAT shows good robustness and stability when is controlled within a reasonable range .

Sensitivity of the parameter epsilon on the normal and the crisis datasets.

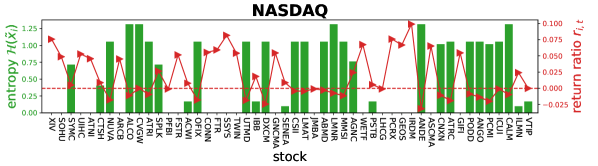

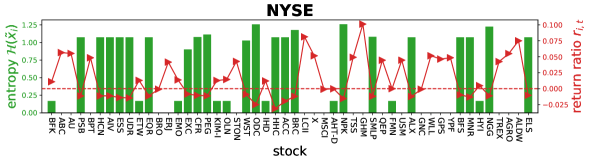

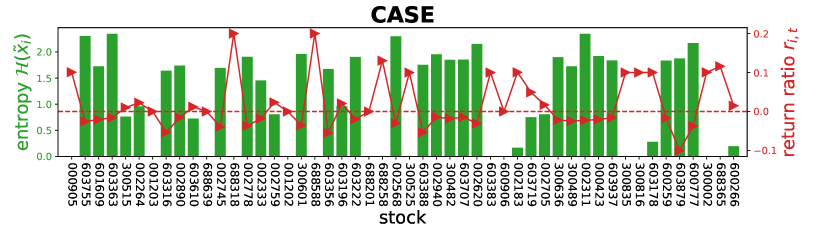

4.7. RQ6: Risk Quantification by Ranking Entropy

Relation between ranking entropy and return ratio.

In this section, we aim to investigate how the adversarial perturbation of SVAT works in reducing stock recommendation risks and provide some insights about risk quantification for investors. As discussed in Section 3.2, by sampling multiple adversarial perturbations from the perturbation distribution learned by the variational perturbation generator, one can compute the ranking entropy for each stock using Equation (7). We postulate that the relationship between ranking entropies and stock returns could indirectly reveal the truth about risk reduction. Accordingly, we sample perturbations for each stock example of the testing datasets and inspect the interactions between their ranking entropies and investment returns. Figure 11c shows an example of the relation between and the return ratio , where we randomly select stocks from NASDAQ, NYSE, and CASE datasets for illustration. Overall, the ranking entropy and the return ratio present an inverse relation, where:

-

•

For NASDAQ and NYSE datasets, most stocks with earn profits () and most stocks with indicate risks ().

-

•

For CASE datasets, most stocks with earn profits () and most stocks with indicate risks ().

Since all perturbations are sampled from the distribution , the ranking entropy actually reflects the uncertainty of , with higher entropy indicating larger uncertainty and thus higher risk of stock . In this case, Figure 11c shows that by increasing the ranking uncertainties of risky stocks with negative returns, the perturbations produced by SVAT probably help the model better recognize those risky stocks and thus avoid recommending such stocks, which reduces the possibility of potential losses and lowers the risk of stock recommendation. Also, the ranking entropy provides an effective tool for investors to roughly evaluate the risk of each stock before making investment decisions, demonstrating the additional advantage of risk interpretability brought by SVAT.

5. Related Work

Our work is directly related to the recent work on stock prediction, risk management, adversarial training and variational autoencoder.

5.1. Stock Prediction

Researchers have been studying the stock market for decades, developing various stock prediction methods to pursue excess investment profits (Cavalcante et al., 2016). As we mentioned in Section 1, recent work on stock prediction can be separated into three categories: stock price regression, stock trend classification, and stock recommendation (Rouf et al., 2021). Stock price regression formulates stock prediction as a pure time series forecasting problem and predict the future stock prices/returns by learning from historical stock time series. Traditional econometrics (Greene, 2003) employs simple linear models such as VAR and ARIMA (Tsay, 2010) to perform stock price regression prediction, while contemporary methods leverage advanced learning architectures such as SVM (Schumaker and Chen, 2009), Tensor Aggregation (Li et al., 2016), RNN (Qin et al., 2017; Cheng et al., 2020), GAN (Zhang et al., 2018; Xie et al., 2019), and Transformer (Malibari et al., 2021) to better capture non-linear relationships in the stock time series. On the other hand, stock trend classification treats stock prediction as a binary up/down classification problem and develop efficient classifiers to perform stock movement prediction. Advanced classification models include StockNet (Xu and Cohen, 2018), Adv-ALSTM (Feng et al., 2019a), STLAT (Li et al., 2022), etc. Nonetheless, both stock price regression and stock trend classification have a significant drawback that they are not directly optimized towards the target of investment (i.e., profit maximization), which limits their practicality (Sawhney et al., 2021). To overcome this drawback, reinforcement learning methods (Sun et al., 2023; Carta et al., 2021; Liu et al., 2020) have been proposed to improve model profits by capturing trading signals in a dynamic prediction. And stock recommendation proposes to rank stocks with return ratios based on the comparison among multiple stocks (Gao et al., 2022). In this case, models are trained to select top- stocks with maximum expected profits so as to ensure their consistency with the investment target. Recent stock recommendation models combine both the RNN and the GNN architectures to learn the relationships between multiple stocks (Feng et al., 2019b; Gao et al., 2022; Sawhney et al., 2021; Wang et al., 2022).

Although various stock recommendation methods have achieved promising results, literature on reducing stock recommendation risks with adversarial training is still scarce. In this work, we aim to tackle risk concerns of stock recommendation and demonstrate a new way to reduce investment risks with adversarial perturbations.

5.2. Risk Management

Risk management is essential to protect investors in a volatile stock market. Over the decades, numerous studies have been conducted to analyze and mitigate the potential risks associated with stock investments (Smithson and Simkins, 2005; Mashrur et al., 2020). One prominent approach is the application of modern portfolio theory (MPT) (Markowitz, 1952), which emphasizes the importance of diversification in reducing overall portfolio risk. Furthermore, researchers have proposed various financial models such as the Capital Asset Pricing Model (CAPM) (Sharpe, 1964) and Black-Scholes model (Black and Scholes, 1973) to better understand and quantify risk factors. Recently, advanced machine learning techniques have also found their significance on stock risk management (Liu and Yu, 2022) and some researchers have incorporated stock volatilities into reinforcement learning models to achieve better risk-adjusted profits (Yang et al., 2023; Liu et al., 2023). However, most of the existing risk management methods are designed for some specific scenarios or models, which cannot be directly applied to the stock recommendation model. In this paper, we innovatively propose a risk management approach tailored for stock recommendation and demonstrate the feasibility of adversarial learning in risk management.

5.3. Adversarial Training

Desipite the excellent learning ability, deep neural networks (DNNs) have been found to be vulnerable to adversarial perturbations on data, i.e., adversarial examples (Szegedy et al., 2014; Goodfellow et al., 2015). Therefore, lots of adversarial training (AT) methods have been proposed to enhance the adversarial robustness of DNN classifiers (Zhang et al., 2019; Qian et al., 2022), such as FGSM (Goodfellow et al., 2015), PGD (Madry et al., 2018), ADT (Dong et al., 2020), etc. As for stock classification, Adv-ALSTM (Feng et al., 2019a) might be the first work to engage adversarial training for stock movement prediction. All of the above conventional AT methods aim to improve model generalization by training the model to produce the same output on both original and perturbed examples. In contrast, researchers of dialogue generation have proposed Inverse Adversarial Training (IAT) to encourage the model to be sensitive to perturbations and generate more diverse responses (Zhou et al., 2021). In this paper, we combine advantages of AT and IAT to better enhance the risk awareness of the stock recommendation model.

5.4. Variational Autoencoder

As one of the mainstream deep generative models, the variational autoencoder (VAE) (Kingma and Welling, 2014) is good at learning the probability distribution of high-dimensional data through low-dimensional latent representations and generating high-quality data (Kalingeri, 2022; Asperti et al., 2021). During the past few years, VAE has received widespread attention in various research fields and achieved promising results in image and audio generation (Hou et al., 2021; Rezende et al., 2016; Li et al., 2021), speech processing (Rix et al., 2001; Do et al., 2020; Sayed et al., 2023), text processing (Miao et al., 2016) and biomedical informatics (Wei and Mahmood, 2021; Yu et al., 2022). In financial applications, (Choudhury et al., 2020) employs an LSTM-VAE framework to perform multi-step-ahead prediction of the stock closing price and (Xu and Cohen, 2018) develops a VAE-based model combining social media text and price signals for stock movement prediction. Recently, a more advanced model FactorVAE (Duan et al., 2022) has been proposed to predict cross-sectional stock returns by regarding stock factors as the latent random variables in VAE. Inspired by previous work, we also employ the VAE architecture to generate representative risk indicators for our stock recommendation model.

6. Conclusion

In this paper, we propose a novel adversarial learning framework (SVAT) for risk-aware stock recommendation. In the first level, we design a split adversarial training method to enhance model’s sensitivity to the adversarial perturbations of risky stock examples. In the second level, we devise a variational perturbation generator to model diverse risk factors and generate representative adversarial examples as risk indicators. Besides, the variational architecture enables our method to provide a rough risk quantification for investors, showing an additional advantage of interpretability. Experiments on three real-world datasets demonstrate that our method effectively reduces the volatility of the recommendation model and achieves the best risk-adjusted profit against 7 baselines. In addition, we demonstrate the efficiency of each component of the SVAT algorithm through ablative and qualitative experiments.

For the future research, we aim to explore the risk-aware adversarial learning for long-term stock prediction and incorporate additional data sources such as financial news for better risk modeling.

Acknowledgements.

The research is supported by the National Natural Science Foundation of China (92370119, 62032025, 62376113), the Key-Area Research and Development Program of Shandong Province (2021CXGC010108), and Jiangsu Science and Technology Program (BE2020006-4).References

- (1)

- Adam et al. (2016) Klaus Adam, Albert Marcet, and Juan Pablo Nicolini. 2016. Stock Market Volatility and Learning. J. Finance 71, 1 (2016), 33–82. https://doi.org/10.1111/jofi.12364 arXiv:https://onlinelibrary.wiley.com/doi/pdf/10.1111/jofi.12364

- Ariyo et al. (2014) Adebiyi Ariyo Ariyo, Aderemi Oluyinka Adewumi, and Charles K. Ayo. 2014. Stock Price Prediction Using the ARIMA Model. In UKSim-AMSS 16th International Conference on Computer Modelling and Simulation, UKSim 2014, Cambridge, United Kingdom, March 26-28, 2014, David Al-Dabass, Alessandra Orsoni, Richard J. Cant, Jasmy Yunus, Zuwairie Ibrahim, and Ismail Saad (Eds.). IEEE, 106–112. https://doi.org/10.1109/UKSIM.2014.67

- Arora et al. (2012) Ravinder Kumar Arora, Pramod Kumar Jain, and Himadri Das. 2012. Are Stock Returns Predictable? Evidence from Select Emerging Markets. Advances in Financial Planning and Forecasting 5 (Dec 2012), 97–120. https://doi.org/10.6292/AFPF.2012.05.04

- Asperti et al. (2021) Andrea Asperti, Davide Evangelista, and Elena Loli Piccolomini. 2021. A survey on Variational Autoencoders from a GreenAI perspective. CoRR abs/2103.01071 (2021). arXiv:2103.01071 https://arxiv.org/abs/2103.01071

- Bao et al. (2017) Wei Bao, Jun Yue, and Yulei Rao. 2017. A deep learning framework for financial time series using stacked autoencoders and long-short term memory. PLoS One 12, 7 (2017), 1–24.

- Black and Scholes (1973) Fischer Black and Myron S Scholes. 1973. The Pricing of Options and Corporate Liabilities. J. Polit. Econ. 81, 3 (May-June 1973), 637–654. https://doi.org/10.1086/260062

- Carta et al. (2021) Salvatore Carta, Anselmo Ferreira, Alessandro Sebastian Podda, Diego Reforgiato Recupero, and Antonio Sanna. 2021. Multi-DQN: An ensemble of Deep Q-learning agents for stock market forecasting. Expert Syst. Appl. 164 (2021), 113820. https://doi.org/10.1016/J.ESWA.2020.113820

- Cavalcante et al. (2016) Rodolfo C. Cavalcante, Rodrigo C. Brasileiro, Victor L. F. Souza, Jarley Palmeira Nóbrega, and Adriano L. I. Oliveira. 2016. Computational Intelligence and Financial Markets: A Survey and Future Directions. Expert Syst. Appl. 55 (2016), 194–211. https://doi.org/10.1016/J.ESWA.2016.02.006

- Cheng et al. (2020) Jiezhu Cheng, Kaizhu Huang, and Zibin Zheng. 2020. Towards Better Forecasting by Fusing Near and Distant Future Visions. In The Thirty-Fourth AAAI Conference on Artificial Intelligence, AAAI 2020, The Thirty-Second Innovative Applications of Artificial Intelligence Conference, IAAI 2020, The Tenth AAAI Symposium on Educational Advances in Artificial Intelligence, EAAI 2020, New York, NY, USA, February 7-12, 2020. AAAI Press, 3593–3600. https://doi.org/10.1609/AAAI.V34I04.5766

- Cheng et al. (2022) Minhao Cheng, Qi Lei, Pin-Yu Chen, Inderjit S. Dhillon, and Cho-Jui Hsieh. 2022. CAT: Customized Adversarial Training for Improved Robustness. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI 2022, Vienna, Austria, 23-29 July 2022, Luc De Raedt (Ed.). ijcai.org, 673–679. https://doi.org/10.24963/IJCAI.2022/95

- Choudhury et al. (2020) Ahana Roy Choudhury, Soheila Abrishami, Michael Turek, and Piyush Kumar. 2020. Enhancing profit from stock transactions using neural networks. AI Commun. 33, 2 (2020), 75–92. https://doi.org/10.3233/AIC-200629

- Do et al. (2020) Hao Duc Do, Tran Thai Son, and Duc Thanh Chau. 2020. Speech Source Separation Using Variational Autoencoder and Bandpass Filter. IEEE Access 8 (2020), 156219–156231. https://doi.org/10.1109/ACCESS.2020.3019495

- Dong et al. (2020) Yinpeng Dong, Zhijie Deng, Tianyu Pang, Jun Zhu, and Hang Su. 2020. Adversarial Distributional Training for Robust Deep Learning. In Advances in Neural Information Processing Systems 33: Annual Conference on Neural Information Processing Systems 2020, NeurIPS 2020, December 6-12, 2020, virtual, Hugo Larochelle, Marc’Aurelio Ranzato, Raia Hadsell, Maria-Florina Balcan, and Hsuan-Tien Lin (Eds.). https://proceedings.neurips.cc/paper/2020/hash/5de8a36008b04a6167761fa19b61aa6c-Abstract.html

- Duan et al. (2022) Yitong Duan, Lei Wang, Qizhong Zhang, and Jian Li. 2022. FactorVAE: A Probabilistic Dynamic Factor Model Based on Variational Autoencoder for Predicting Cross-Sectional Stock Returns. In Thirty-Sixth AAAI Conference on Artificial Intelligence, AAAI 2022, Thirty-Fourth Conference on Innovative Applications of Artificial Intelligence, IAAI 2022, The Twelveth Symposium on Educational Advances in Artificial Intelligence, EAAI 2022 Virtual Event, February 22 - March 1, 2022. AAAI Press, 4468–4476. https://doi.org/10.1609/AAAI.V36I4.20369

- Feng et al. (2019a) Fuli Feng, Huimin Chen, Xiangnan He, Ji Ding, Maosong Sun, and Tat-Seng Chua. 2019a. Enhancing Stock Movement Prediction with Adversarial Training. In Proceedings of the Twenty-Eighth International Joint Conference on Artificial Intelligence, IJCAI 2019, Macao, China, August 10-16, 2019, Sarit Kraus (Ed.). ijcai.org, 5843–5849. https://doi.org/10.24963/IJCAI.2019/810

- Feng et al. (2019b) Fuli Feng, Xiangnan He, Xiang Wang, Cheng Luo, Yiqun Liu, and Tat-Seng Chua. 2019b. Temporal Relational Ranking for Stock Prediction. ACM Trans. Inf. Syst. 37, 2 (2019), 27:1–27:30. https://doi.org/10.1145/3309547

- Gao et al. (2022) Jianliang Gao, Xiaoting Ying, Cong Xu, Jianxin Wang, Shichao Zhang, and Zhao Li. 2022. Graph-Based Stock Recommendation by Time-Aware Relational Attention Network. ACM Trans. Knowl. Discov. Data 16, 1 (2022), 4:1–4:21. https://doi.org/10.1145/3451397

- Goodfellow et al. (2015) Ian J. Goodfellow, Jonathon Shlens, and Christian Szegedy. 2015. Explaining and Harnessing Adversarial Examples. In 3rd International Conference on Learning Representations, ICLR 2015, San Diego, CA, USA, May 7-9, 2015, Conference Track Proceedings, Yoshua Bengio and Yann LeCun (Eds.). http://arxiv.org/abs/1412.6572

- Greene (2003) William H. Greene. 2003. Econometric analysis / William H. Greene. (5th ed. ed.). Prentice Hall.

- Guo (2006) Hui Guo. 2006. On the Out‐of‐Sample Predictability of Stock Market Returns. J. Bus. 79, 2 (2006), 645–670. http://www.jstor.org/stable/10.1086/499134

- Hou et al. (2021) Yingzhen Hou, Junhai Zhai, and Jiankai Chen. 2021. Coupled adversarial variational autoencoder. Signal Process. Image Commun. 98 (2021), 116396. https://doi.org/10.1016/J.IMAGE.2021.116396

- Kalingeri (2022) Vasanth Kalingeri. 2022. Latent Variable Modelling Using Variational Autoencoders: A survey. CoRR abs/2206.09891 (2022). https://doi.org/10.48550/ARXIV.2206.09891 arXiv:2206.09891

- Kingma and Ba (2015) Diederik P. Kingma and Jimmy Ba. 2015. Adam: A Method for Stochastic Optimization. In 3rd International Conference on Learning Representations, ICLR 2015, San Diego, CA, USA, May 7-9, 2015, Conference Track Proceedings, Yoshua Bengio and Yann LeCun (Eds.). http://arxiv.org/abs/1412.6980

- Kingma and Welling (2014) Diederik P. Kingma and Max Welling. 2014. Auto-Encoding Variational Bayes. In 2nd International Conference on Learning Representations, ICLR 2014, Banff, AB, Canada, April 14-16, 2014, Conference Track Proceedings, Yoshua Bengio and Yann LeCun (Eds.). http://arxiv.org/abs/1312.6114

- Kipf and Welling (2017) Thomas N. Kipf and Max Welling. 2017. Semi-Supervised Classification with Graph Convolutional Networks. In 5th International Conference on Learning Representations, ICLR 2017, Toulon, France, April 24-26, 2017, Conference Track Proceedings. OpenReview.net. https://openreview.net/forum?id=SJU4ayYgl

- Kurani et al. (2023) Akshit Kurani, Pavan Doshi, Aarya Vakharia, and Manan Shah. 2023. A Comprehensive Comparative Study of Artificial Neural Network (ANN) and Support Vector Machines (SVM) on Stock Forecasting. Ann. Sci. 10, 1 (February 2023), 183–208. https://doi.org/10.1007/s40745-021-00344-

- Li et al. (2021) Jing Li, Di Kang, Wenjie Pei, Xuefei Zhe, Ying Zhang, Zhenyu He, and Linchao Bao. 2021. Audio2Gestures: Generating Diverse Gestures from Speech Audio with Conditional Variational Autoencoders. In 2021 IEEE/CVF International Conference on Computer Vision, ICCV 2021, Montreal, QC, Canada, October 10-17, 2021. IEEE, 11273–11282. https://doi.org/10.1109/ICCV48922.2021.01110

- Li et al. (2016) Qing Li, Yuanzhu Chen, LiLing Jiang, Ping Li, and Hsinchun Chen. 2016. A Tensor-Based Information Framework for Predicting the Stock Market. ACM Trans. Inf. Syst. 34, 2 (2016), 11:1–11:30. https://doi.org/10.1145/2838731

- Li et al. (2022) Yang Li, Hong-Ning Dai, and Zibin Zheng. 2022. Selective transfer learning with adversarial training for stock movement prediction. Connect. Sci. 34, 1 (2022), 492–510. https://doi.org/10.1080/09540091.2021.2021143

- Liu et al. (2023) Peipei Liu, Yunfeng Zhang, Fangxun Bao, Xunxiang Yao, and Caiming Zhang. 2023. Multi-type data fusion framework based on deep reinforcement learning for algorithmic trading. Appl. Intell. 53, 2 (2023), 1683–1706. https://doi.org/10.1007/S10489-022-03321-W

- Liu and Yu (2022) Tao Liu and Zhongyang Yu. 2022. The analysis of financial market risk based on machine learning and particle swarm optimization algorithm. EURASIP J. Wirel. Commun. Netw. 2022, 1 (2022), 31. https://doi.org/10.1186/S13638-022-02117-3

- Liu et al. (2020) Yang Liu, Qi Liu, Hongke Zhao, Zhen Pan, and Chuanren Liu. 2020. Adaptive Quantitative Trading: An Imitative Deep Reinforcement Learning Approach. In The Thirty-Fourth AAAI Conference on Artificial Intelligence, AAAI 2020, The Thirty-Second Innovative Applications of Artificial Intelligence Conference, IAAI 2020, The Tenth AAAI Symposium on Educational Advances in Artificial Intelligence, EAAI 2020, New York, NY, USA, February 7-12, 2020. AAAI Press, 2128–2135. https://doi.org/10.1609/AAAI.V34I02.5587

- Lyu et al. (2015) Chunchuan Lyu, Kaizhu Huang, and Hai-Ning Liang. 2015. A Unified Gradient Regularization Family for Adversarial Examples. In 2015 IEEE International Conference on Data Mining, ICDM 2015, Atlantic City, NJ, USA, November 14-17, 2015, Charu C. Aggarwal, Zhi-Hua Zhou, Alexander Tuzhilin, Hui Xiong, and Xindong Wu (Eds.). IEEE Computer Society, 301–309. https://doi.org/10.1109/ICDM.2015.84

- Madry et al. (2018) Aleksander Madry, Aleksandar Makelov, Ludwig Schmidt, Dimitris Tsipras, and Adrian Vladu. 2018. Towards Deep Learning Models Resistant to Adversarial Attacks. In 6th International Conference on Learning Representations, ICLR 2018, Vancouver, BC, Canada, April 30 - May 3, 2018, Conference Track Proceedings. OpenReview.net. https://openreview.net/forum?id=rJzIBfZAb

- Malibari et al. (2021) Nadeem Malibari, Iyad Katib, and Rashid Mehmood. 2021. Predicting Stock Closing Prices in Emerging Markets with Transformer Neural Networks: The Saudi Stock Exchange Case. Int. J. Adv. Comput. Sci. Appl. 12, 12 (2021). https://doi.org/10.14569/IJACSA.2021.01212106

- Markowitz (1952) Harry Markowitz. 1952. Portfolio Selection. J. Finance 7, 1 (1952), 77–91. https://doi.org/10.2307/2975974

- Mashrur et al. (2020) Akib Mashrur, Wei Luo, Nayyar Abbas Zaidi, and Antonio Robles-Kelly. 2020. Machine Learning for Financial Risk Management: A Survey. IEEE Access 8 (2020), 203203–203223. https://doi.org/10.1109/ACCESS.2020.3036322

- Miao et al. (2016) Yishu Miao, Lei Yu, and Phil Blunsom. 2016. Neural Variational Inference for Text Processing. In Proceedings of the 33nd International Conference on Machine Learning, ICML 2016, New York City, NY, USA, June 19-24, 2016 (JMLR Workshop and Conference Proceedings, Vol. 48), Maria-Florina Balcan and Kilian Q. Weinberger (Eds.). JMLR.org, 1727–1736. http://proceedings.mlr.press/v48/miao16.html

- Milobedzki (2004) Pawel Milobedzki. 2004. Predictability of stock markets with disequilibrium trading. A commentary paper. Eur. J. Finance 10, 5 (2004), 345–352. https://doi.org/10.1080/1351847042000199033 arXiv:https://doi.org/10.1080/1351847042000199033

- Patro and Wu (2004) Dilip K. Patro and Yangru Wu. 2004. Predictability of short-horizon returns in international equity markets. J. Empir. Finance 11, 4 (2004), 553–584. https://doi.org/10.1016/j.jempfin.2004.02.003 Special Issue on Behavioral Finance.

- Qian et al. (2022) Zhuang Qian, Kaizhu Huang, Qiu-Feng Wang, and Xu-Yao Zhang. 2022. A survey of robust adversarial training in pattern recognition: Fundamental, theory, and methodologies. Pattern Recognit. 131 (2022), 108889. https://doi.org/10.1016/J.PATCOG.2022.108889

- Qin et al. (2017) Yao Qin, Dongjin Song, Haifeng Chen, Wei Cheng, Guofei Jiang, and Garrison W. Cottrell. 2017. A Dual-Stage Attention-Based Recurrent Neural Network for Time Series Prediction. In Proceedings of the Twenty-Sixth International Joint Conference on Artificial Intelligence, IJCAI 2017, Melbourne, Australia, August 19-25, 2017, Carles Sierra (Ed.). ijcai.org, 2627–2633. https://doi.org/10.24963/IJCAI.2017/366

- Rezende et al. (2016) Danilo Jimenez Rezende, Shakir Mohamed, Ivo Danihelka, Karol Gregor, and Daan Wierstra. 2016. One-Shot Generalization in Deep Generative Models. In Proceedings of the 33nd International Conference on Machine Learning, ICML 2016, New York City, NY, USA, June 19-24, 2016 (JMLR Workshop and Conference Proceedings, Vol. 48), Maria-Florina Balcan and Kilian Q. Weinberger (Eds.). JMLR.org, 1521–1529. http://proceedings.mlr.press/v48/rezende16.html

- Rix et al. (2001) Antony W. Rix, John G. Beerends, Michael P. Hollier, and Andries P. Hekstra. 2001. Perceptual evaluation of speech quality (PESQ)-a new method for speech quality assessment of telephone networks and codecs. In IEEE International Conference on Acoustics, Speech, and Signal Processing, ICASSP 2001, 7-11 May, 2001, Salt Palace Convention Center, Salt Lake City, Utah, USA, Proceedings. IEEE, 749–752. https://doi.org/10.1109/ICASSP.2001.941023

- Rouf et al. (2021) Nusrat Rouf, Majid Bashir Malik, Tasleem Arif, Sparsh Sharma, Saurabh Singh, Satyabrata Aich, and Hee-Cheol Kim. 2021. Stock Market Prediction Using Machine Learning Techniques: A Decade Survey on Methodologies, Recent Developments, and Future Directions. Electronics 10, 21 (2021). https://doi.org/10.3390/electronics10212717

- Sawhney et al. (2021) Ramit Sawhney, Shivam Agarwal, Arnav Wadhwa, Tyler Derr, and Rajiv Ratn Shah. 2021. Stock Selection via Spatiotemporal Hypergraph Attention Network: A Learning to Rank Approach. In Thirty-Fifth AAAI Conference on Artificial Intelligence, AAAI 2021, Thirty-Third Conference on Innovative Applications of Artificial Intelligence, IAAI 2021, The Eleventh Symposium on Educational Advances in Artificial Intelligence, EAAI 2021, Virtual Event, February 2-9, 2021. AAAI Press, 497–504. https://doi.org/10.1609/AAAI.V35I1.16127

- Sayed et al. (2023) Hadeer M. Sayed, Hesham E. ElDeeb, and Shereen A. Taie. 2023. Bimodal variational autoencoder for audiovisual speech recognition. Mach. Learn. 112, 4 (2023), 1201–1226. https://doi.org/10.1007/S10994-021-06112-5

- Schumaker and Chen (2009) Robert P. Schumaker and Hsinchun Chen. 2009. Textual analysis of stock market prediction using breaking financial news: The AZFin text system. ACM Trans. Inf. Syst. 27, 2 (2009), 12:1–12:19. https://doi.org/10.1145/1462198.1462204

- Sharpe (1964) William F. Sharpe. 1964. Capital Asset Prices: A Theory Of Market Equilibrium Under Conditions Of Risk. J. Finance 19, 3 (September 1964), 425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x arXiv:https://onlinelibrary.wiley.com/doi/pdf/10.1111/j.1540-6261.1964.tb02865.x

- Smithson and Simkins (2005) Charles Smithson and Betty J. Simkins. 2005. Does Risk Management Add Value? A Survey of the Evidence. J. Appl. Corp. Finance 17, 3 (2005), 8–17. https://doi.org/10.1111/j.1745-6622.2005.00042.x

- Sun et al. (2023) Shuo Sun, Rundong Wang, and Bo An. 2023. Reinforcement Learning for Quantitative Trading. ACM Trans. Intell. Syst. Technol. 14, 3 (2023), 44:1–44:29. https://doi.org/10.1145/3582560

- Szegedy et al. (2014) Christian Szegedy, Wojciech Zaremba, Ilya Sutskever, Joan Bruna, Dumitru Erhan, Ian J. Goodfellow, and Rob Fergus. 2014. Intriguing properties of neural networks. In 2nd International Conference on Learning Representations, ICLR 2014, Banff, AB, Canada, April 14-16, 2014, Conference Track Proceedings, Yoshua Bengio and Yann LeCun (Eds.). http://arxiv.org/abs/1312.6199

- Tsay (2010) Ruey S. Tsay. 2010. Analysis of Financial Time Series (3rd ed.). John Wiley & Sons, Ltd.

- Wang et al. (2022) Heyuan Wang, Tengjiao Wang, Shun Li, Jiayi Zheng, Shijie Guan, and Wei Chen. 2022. Adaptive Long-Short Pattern Transformer for Stock Investment Selection. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI 2022, Vienna, Austria, 23-29 July 2022, Luc De Raedt (Ed.). ijcai.org, 3970–3977. https://doi.org/10.24963/IJCAI.2022/551

- Wei and Mahmood (2021) Ruoqi Wei and Ausif Mahmood. 2021. Recent Advances in Variational Autoencoders With Representation Learning for Biomedical Informatics: A Survey. IEEE Access 9 (2021), 4939–4956. https://doi.org/10.1109/ACCESS.2020.3048309

- Xie et al. (2019) Fenfang Xie, Shenghui Li, Liang Chen, Yangjun Xu, and Zibin Zheng. 2019. Generative Adversarial Network Based Service Recommendation in Heterogeneous Information Networks. In 2019 IEEE International Conference on Web Services, ICWS 2019, Milan, Italy, July 8-13, 2019, Elisa Bertino, Carl K. Chang, Peter Chen, Ernesto Damiani, Michael Goul, and Katsunori Oyama (Eds.). IEEE, 265–272. https://doi.org/10.1109/ICWS.2019.00053