A new copula regression model for hierarchical data.

Abstract

This paper proposes multivariate copula models for hierarchical data. They account for two types of correlation: one is between variables measured on the same unit and the other is a correlation between units in the same cluster. This model is used to carry out copula regression for hierarchical data that gives cluster specific prediction curves. In the simple case where a cluster contains two units and where two variables are measured on each one, the new model is constructed within a D-vine. Then we focus on situations where two variables are measured on the units of a cluster of arbitrary size. The proposed copula density has an explicit form; it is expressed in terms of three copula families. We study the properties of the model; compare it to the linear mixed model and end with special cases. When the three copula families and the marginal distributions are normal, the model is equivalent to a normal linear mixed model with random, cluster specific, intercepts. The method to select the three copula families and to estimate their parameters are proposed. We perform a Monte Carlo study of the parameter estimators. A data set on the marks of students in several school is used to implement the proposed model and to compare its performance to standard normal mixed linear models.

keywords:

Exchangeability , Heterogeneity, Normal linear mixed models, Vine copula.1 Introduction

A simple bivariate copula regression predicts dependent variable using independent variable . It proceeds by selecting a bivariate copula summarizing the relationship between and . The copula regression predictor is then constructed using characteristics of the conditional distribution of given derived from the selected copula, see [17], [14] and [5] exemplify this method while [18] derive its asymptotic properties and [1] investigates predictions errors. This method is easily extended a multivariate explanatory variable .

The goal of this work is to generalize the basic copula regression model to hierarchical data: and are observed on units that are in clusters and one would like to include a cluster effect in the copula regression predictions. The classical regression model for hierarchical data is a normal linear mixed model, with cluster specific random slopes and intercepts, see [2], [25], [16] and [10]. The exchangeable copula families have been proposed to model the residual dependency within cluster in this context, see [20] and [11]; [23] provide a survival data application of this approach.

A model for the joint distribution of all the and the variables in a cluster is first constructed. The conditions that the model must fulfill in order to yield suitable predictions are given in Section 2. It is required to meet an exchangeability assumption: permuting the units in a cluster does not change the joint distribution of the variables. It also relies on a partial conditional independence assumption that insures that the prediction of for a unit does not depend on the values for the other units in the cluster. The proposed model is then constructed within a D-vine in the simple case of a cluster containing two units. The general model, for clusters of arbitrary size, is introduced in Section 3. Afterwards, we study its properties by showing that, in particular cases, conditional versions are equivalent to the models of [2] and of [20]. We use the proposed copula to do cluster specific predictions. The copula model is then implemented in a data set of [10] and compared with standard normal mixed linear models.

2 Model construction : Exchangeability and conditional independence

This section considers that variables are measured on all the units in a cluster; subscript represents a unit, , where is the size of the cluster. The dependent variable for unit is while is the corresponding vector of explanatory variables and , is the vector of the variables measured on unit . Let be the joint cumulative distribution function (cdf) of the variables measured in the cluster, where . The model is constructed using copulas; it is therefore of interest to define and as the marginal distributions of respectively and which are the same for all the units. We let and be random variables with uniform margins and be the copula density for the joint distribution of . We now give some conditions for the family of joint distributions to give useful regression models.

2.1 Exchangeability

We consider the family of cumulative distribution functions defined by

The familly is said to be -exchangeable if, for all , satisfies the following conditions

-

Permutation invariance : For all permutations of ,

(1) -

Closure on marginalization: For any ,

(2)

This definition is similar to the classical definition of univariate exchangeability that is given in [15]. A simple example of -exchangeability is a multivariate one way ANOVA model with random effects, , where and are independent random vectors and have the same distribution. The next proposition gives the form of the correlation matrix for a -exchangeable random vector.

Proposition 1.

Let be a set of random vectors, verifying the definition of -exchangeability given by (1) and (2). Then, the correlation matrix of Pearson, Spearman, and Kendall’s between these vectors have the form

| (3) |

where is and matrix of ones and denotes the Kroenecker product. Moreover, for Pearson and Spearman correlations, the matrices and are positive semi definite.

2.2 Partial conditional independence

This section proposes an assumption concerning the dependency within each cluster.

Definition 1.

The random variables and are assumed to be independent, given . This is a partial conditional independence assumption that can be written as

| (4) |

This condition is weaker than the conditional independence assumption underlying the standard regression model that can be formulated as

We now implement the exchangeability and the independence assumption within a -vine for the joint distribution of two units within a cluster when , that is when .

2.3 A D-vine construction of the model when

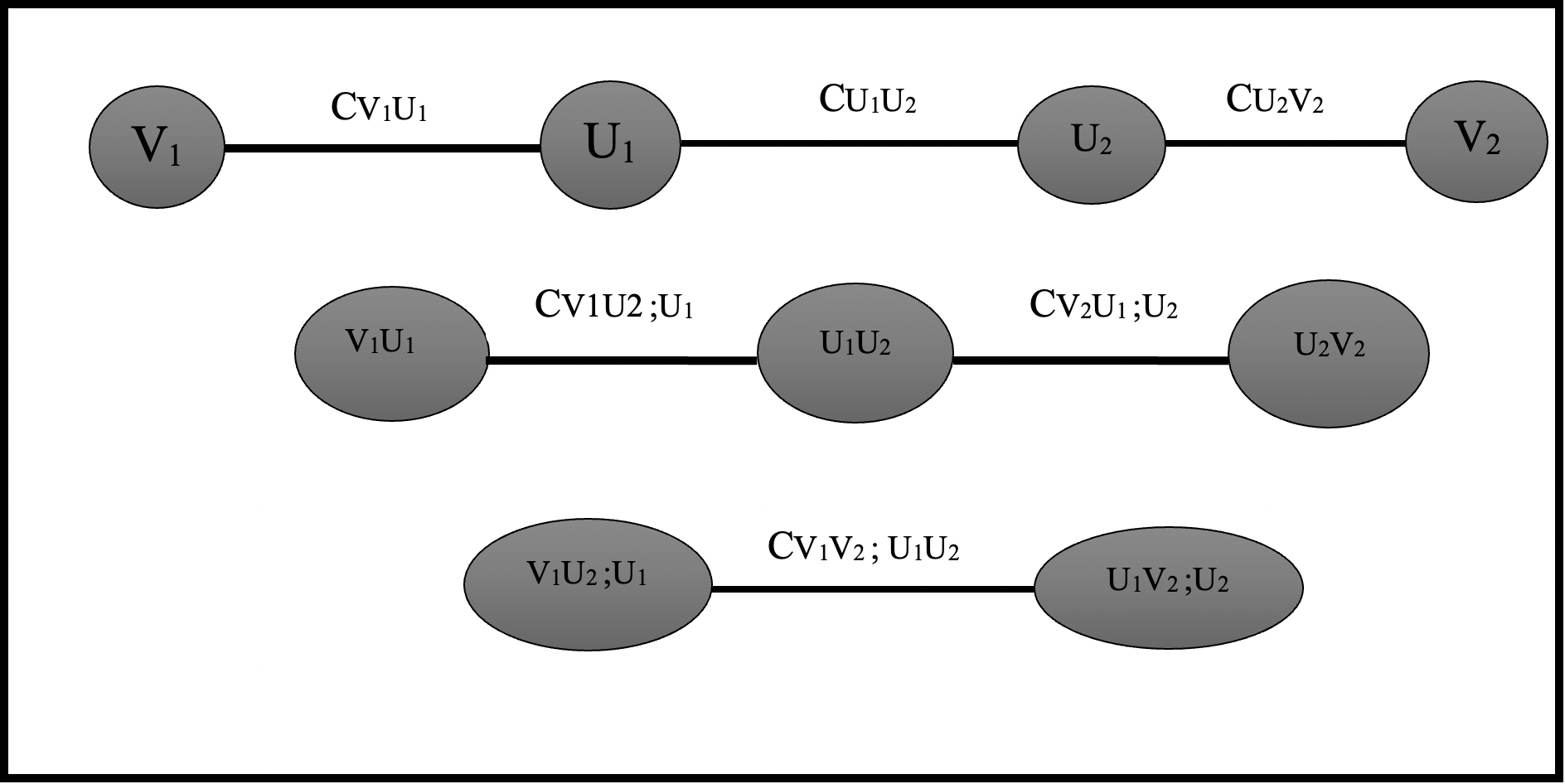

This section constructs a copula density function for the random variables in a cluster containing two units and verifying the properties of partial conditional independence and 2-exchangeability. The 4 random variables are , , and . The four trees for the proposed -vine are given in Figure 1.

The decomposition involves 6 bivariate copulas , , , , and . The density of the multivariate copula corresponding to the trees given in Figure 1 can be derived from Joe [13, pp. 108]. It is given by

| (5) | |||||

where the conditional distribution functions and are defined by

| (6) |

This vine is assumed to fulfill the simplifying assumption: the copulas associated to the second and third trees do not depend on the conditioning variables. Discussions of this vine decomposition can be found in [19], [8], and [7]. We would like the density (5) to fulfill the conditions for 2-exchangeability, see (1) and (2), and for partial conditional independence, see (4).

The density of the copula is 2-exchangeable if . This requires a unique copula density for the dependency between and , that is , for . Also, the copula for the dependency between and needs to be symmetric, that is and . This definition also entails restrictions on the conditional copula densities and . However for (5) to fulfill the partial conditional independence condition (4) these two copulas need to be equal to the independence copula. This leads to following copula density

| (7) |

It involves an arbitrary copula density for the relationship between and and two symmetric copula densities, and .

It is interesting to consider the special case where the three copulas in (7) are normal. Let represent the correlation between and , that between and and be the residual correlation. The joint copula density (7) for is normal, see Joe [13, pp. 119]. Its correlation matrix is given by

| (8) |

In (8), the result that is obtained by conditioning on while the variance-covariance matrix of knowing is used to find that .

Given that are distributed according to a normal copula with correlation , one obtains the normal copula with correlation matrix (8) for the joint distribution of if and are defined by

| (9) |

where are independent with a distribution. Model (9) is similar to the linear mixed model of [2]. The term represents the contribution of the explanatory variables to the regression; it is fixed if one conditions on . The cluster specific random intercept, , is independent of the experimental error, . One can easily show that the correlation matrix of entering in (9) is given by (8). Note also that (9) is easily generalized to clusters of size . This is also true of the general model (7). This leads to the general 2-exchangeable model that is proposed in the next section.

3 A multivariate 2-exchangeable copula model

This section proposes a method to construct densities for the joint distribution of , for that meets constraints of 2-exchangeability and of partial conditional independence presented in Section 2. The joint cdf for is denoted , where the first index, 2, refers to the dimension of while the index means that it concerns units labelled from 1 to . This joint distribution involves marginal distributions and for and and a copula density . This density depends on , a copula density for the relationship between and , and two families of 1-exchangeable copula densities, and for the dependency between the variables and the copula regression residuals within a cluster respectively. These two families are assumed to fulfill conditions (1) and (2) for .

The general form for the 2-exchangeable copula density is

| (10) |

where , and the conditional distribution is deduced from equation (6) with replaced by . For , equation (10) reduces to the -vine copula density (7)

To prove that (10) meets the conditions (1) and (2) for 2-exchangeability and (4) for conditional independence we integrate the proposed joint density for in (10) for . To carry this out, it is convenient to change variable, . The jacobian is . Using the closure on marginalization property of copula family , the integral is equal to

| (11) |

The variable only appears in . Using the closure on marginalization property of copula family , the integral on gives the density (10) for the pairs . Thus (10) defines a proper copula density that meets requirements (1) and (2) for 2-exchangeability. To prove the partial conditional independence assumption (4) one integrates (11) for . This is easily carried by changing variables, . The joint density of is given by ; thus, given , and are independent and (4) holds.

The derivations in the previous paragraph have highlighted a key property of the proposed model. If the density of

is (10) then the two vectors

and are independent with densities respectively given by and . This is summarized in the following proposition.

Proposition 2.

The result of Proposition 2 suggests the following algorithm to simulate a random vector with a density given of (10):

-

1.

Step 1 : Simulate according to the exchangeable copula ;

-

2.

Step 2 : Simulate according to the exchangeable copula ;

- 3.

This algorithm differs from the proposal of Czado [6, pp. 136] to simulate from a -vine, that goes through the vine sequentially.

It is interesting to construct the joint density of from (10). It involves the joint marginal density of ,

The conditional densities of given , for ,

and a term for the residual dependency within clusters:

This highlights a step wise construction of the 2-exchangeable model: first comes the specification of the marginal distribution for , then that for the conditional distribution of given and one finally adds a component for the residual dependency within a cluster.

We now assume that the copula is normal with correlation . The conditional distribution in (10) and its inverse are given by

for , see [3] for similar results. Using Proposition 2, the dependent variable for a unit in a cluster of size with explanatory variable can be expressed as , where is the entry of a vector with distribution . This gives the following linear model :

If, in addition, the marginal distributions of and are normal: and where are respectively the marginal means and variances, then the model becomes:

| (12) |

where , , and . In (12) the conditional marginal distribution of is normal.

The joint distribution depends on the copula . These models are investigated in [20]. If this copula is normal and exchangeable, with correlation , then (12) reduces to the normal mixed model of [2]. Finally note that the conditional density in (12) for given is given by

Thus model (12) can easily be fitted by maximum likelihood.

3.1 Predictions with the 2-exchangeable copula model

Suppose that units have been observed in a cluster. This section investigates the conditional distribution of given in that cluster. A closed form expression for the conditional expectation of given and is derived. Illustrations of the prediction curves for various specifications of the copula are presented.

The conditional density, of given and is expressed in terms of , . It is given by the ratio of (10) over (11), this yields

| (13) |

Observe that the conditional density of , given

, is simply

. This is the conditional distribution of , when is distributed according to copula . Thus one can easily simulate from (13). Starting from the equation (13) and making a change of variable , we easily obtain the result.

The best predictor of the unknown is its conditional expectation, given , where

it can be expressed as

| (14) |

If the copula is the independence copula this reduces to a standard, unconditional copula regression for , see [14], [5] or [18]. Taking the expectation of with respect to the distribution of also gives the unconditional copula regression curve for . Thus the proposed model gives regression curves that vary between clusters and their expectation is equal to the marginal copula regression based on .

We suppose that the copula is exchangeable normal with correlation . Thus if , then the cumulative distribution function of random vector is a multivariate normal distribution with an exchangeable correlation matrix whose entries are 1 on the diagonal and off the diagonal. Using standard properties of the multivariate normal distribution, the conditional distribution of knowing is univariate normal with mean and variance defined by

| (15) |

see for instance, [20]. Thus the conditional distribution of random variable is a . The final form of (14) when is a normal copula is therefore given by

| (16) |

where . The conditional expectation of the equation (16) is easily evaluated using the Gauss-Hermite quadrature method, see [22]. Note also that the density function (13) can be expressed as:

| (17) |

The corresponding quantile function of has a simple form, namely

Thus the median and various quantiles of the conditional distribution of are easily evaluated.

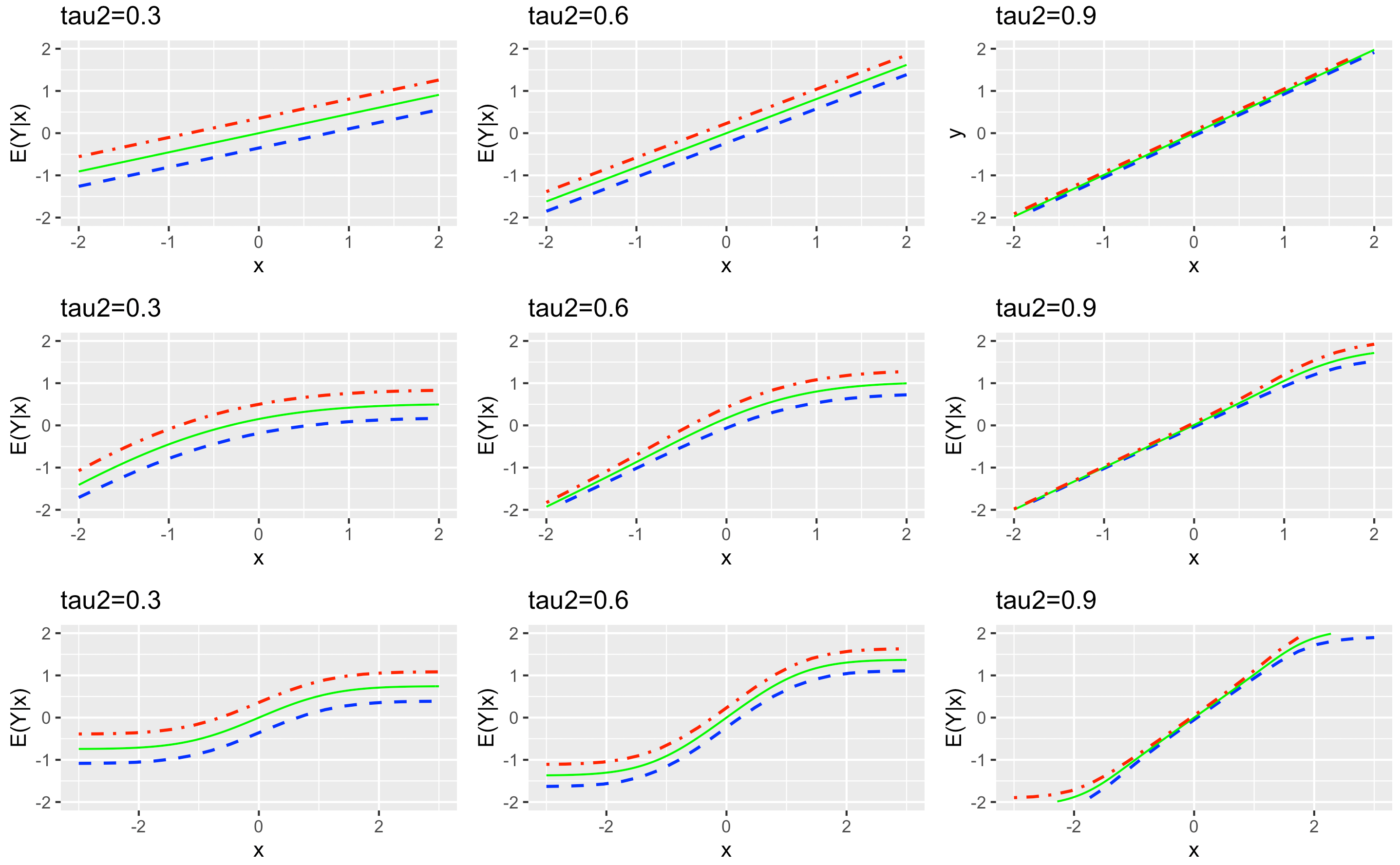

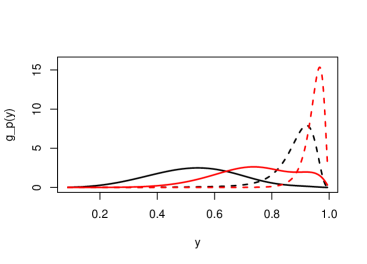

When is large, varies between clusters according to a distribution. This defines the range of possible cluster specific regression curves. Using equation (16), we construct the prediction curves for three copulas when the margins and are the standard normal distribution. The curves are presented in Figure 2. They correspond to Kendall correlation coefficient equal to for each copula . Three copula families are used: Normal, Frank and Clayton copulas. The dependence parameters are deduced from following Joe [13, pp. 58, 166 and 168] and using the function iTau of the R-package copula, see Ivan Kojadinovic and Jun Yan [12]. We also fix the size and the Kendall tau of is corresponding to . Prediction curves are plotted for the quantiles of whose approximate distribution is a .

The graphs exemplify the impact of the dependency in on the prediction curves. Indeed, when the copula is a normal copula, we obtain, in Figure 2, parallel regression lines corresponding to the mixed linear regression model of [2]. For Clayton’s copula, the regression curves are close for small values of ; this might be related to the lower tail dependency of that copula family. When the correlation increases, the regression curves tend to a unique straight lines. This agrees with the conditional form of the model given in equations (9) and (12) where the random part of the model tends to 0 as increases to 1. In Figure 2 we used a relatively small value for the error dependence parameter in ; such a small residual dependency is found in many applications such as the analysis presented in Section 5.

4 Copula selection and parameter estimation for a 2-exchangeable model

The data set to analyze is , where index is for clusters and is for units within clusters. We assume that the joint distribution of the variables in cluster is determined by two marginal distributions , and by copula density (10) that involves a bivariate copula density, for the marginal relationship between and and two 1-exchangeable copula families with densities, and . The goal of this section is to identify parametric families for the five components of this model and to estimate their parameters that are put in vector . Following the model building procedure presented in chapter 5 of Joe [13] and chapters 7 and 8 of Czado [6]. The model components are selected sequentially, using techniques that are presented in this section.

4.1 Determination of the model components

The determination of the marginal distributions is done independently for the two margins. Competing models are compared on the basis of AIC criteria calculated as if the units were independent. Preliminary, or IFM, estimators see Joe [13, section 5.5], are obtained by maximizing

The next step is to calculate the pseudo observations, defined by

| (18) |

The pairs are then used to select a copula for the dependency. Note that the bivariate empirical distribution function of the pseudo-observations is a consistent estimator of when the number of clusters goes to infinity provided that the cluster sizes are bounded, for each . The within cluster dependency impacts the variances of the estimators however this is overlooked at this stage and standard methods, proposed in Joe [13] and Czado [6], are used to select a copula family for the bivariate sample. Competing models are compared on the basis of their AIC and an IFM estimator of the parameter of the selected copula family is obtained by maximizing

To assess the within cluster dependency associated with copula families and , we use the unit level version of the exchangeable Kendall’s tau introduced in Romdhani et al. [21]. It is evaluated using the proportion of concordant pairs among the possible pairs of ordered observations coming from different clusters. Graphical methods to select a family of exchangeable copulas are proposed in Rivest et al. [20]. Models can also be compared on the basis of their AIC, and an IFM estimator of is obtained by maximizing

The selection of the copula family is based on the pseudo observations . The exchangeable Kendall’s tau evaluated on can be used to assess the within cluster dependency of the residuals. IFM estimator is obtained by maximizing

As note in Joe [13, section 5.5] the five estimating equations associated with the IFM estimation of can be combined in a multivariate estimating equation that yield the IFM estimator . The standard asymptotic theory, presented in Tsiatis [24, pp. 30], applies. It shows that the joint asymptotic distribution of , as the number of clusters goes to infinity, is a centered multivariate normal distribution with a sandwich covariance matrix. As expected, this sandwich variance estimator accounts for the within cluster dependence.

4.2 Maximum likelihood estimation of the parameters

Once parametric families for the five model components have been identified, optimal estimators of the parameters are obtained by maximum likekihood. This section discusses the properties of the maximum likelihood estimator for the parameter vector .

The log-likelihood for is equal to

This function is easily maximized once parametric families for the two margins in the model and the three copulas are selected. This yields the maximum likelihood estimator of the parameter vector. This maximization is carried out using an optimiser such the R-function optim or nlminb. Minus the hessian of , evaluated at , is the observed Fisher information for the model. Its inverse is the asymptotic covariance matrix of . It can be used to calculate standard error estimates for all the parameters that have been estimated. At this stage, likelihood ratio tests comparing nested candidate parametric families for can also be carried out to validate the IFM model selection step that ignored the within cluster dependency.

When the margins , and the copula are normal, the likelihood can be split into a marginal likelihood for the parameters of and times a conditional likelihood for the regression parameters and the parameter for , see equation (12). The standard normal mixed linear model of [2] falls into that category as its parameters are estimated using a conditional likelihood. In general the parameters are intertwined in a complicated way and their estimation relies the log-likelihood .

4.3 A Monte Carlo investigation of the sampling properties of IFM and ML estimators

For a 2-exchangeable copula model with parameters , and are the maximum likelihood and the IFM estimators. This section investigates their sampling properties when is finite. This is done using Monte-Carlo simulations where the expectation and the variance of an estimator are approximated by

where indexes the estimates obtained in the Monte-Carlo simulations. The expectations and the variances of IFM estimators are evaluated in a similar way.

Throughout this Monte Carlo study of the copula 2-exchangeable model, the margins and are normal distributions with mean and variance . The exchangeable copulas and belong to the normal family with correlation and respectively, corresponding to Kendall’s tau of 0.2 and 0.1. Such small levels of within cluster association are often found in applications. In the study correlations are parameterized in terms of their logit,

| (19) |

Three copulas are investigated: the normal copula, the Clayton copula and a two-parameter Khoudraji copula [9] that features an asymmetric relationship between and . It is defined by

| (20) |

where is a normal copula with correlation and is the asymmetry parameter. In the simulations is parameterized in terms of its logit, see (19). Two values for the Kendall’s tau of copula , 0.4 and 0.6, are considered. Two sample sizes, , are investigated; their corresponding cluster sizes are and respectively. Tables 1 to 2 present the expectations and the variances of the estimators of the copula parameters.

| Method | |||||

|---|---|---|---|---|---|

| 0.4(0.35) | 10 | MV | -0.96(1.90) | 0.35(0.37) | -1.81(2.29) |

| IFM | -1.00(2.20) | 0.34(0.62) | -1.89(2.41) | ||

| 50 | MV | -0.85(0.58) | 0.35(0.12) | -1.74(0.75) | |

| IFM | -0.86(0.63) | 0.35(0.16) | -1.76(0.80) | ||

| 0.6(1.44) | 10 | MV | -0.90(1.97) | 1.45(0.31) | -1.83(2.24) |

| IFM | -0.95(2.30) | 1.44(0.41) | -1.93(2.50) | ||

| 50 | MV | -0.84(0.53) | 1.44(0.09) | -1.73(0.70) | |

| IFM | -0.85(0.60) | 1.44(0.11) | -1.75(0.76) |

| Method | |||||

|---|---|---|---|---|---|

| 0.4(1.33) | 10 | MV | -0.88(1.63) | 1.35(0.66) | -1.82(2.36) |

| IFM | -0.98(2.18) | 1.33(0.84) | -1.91(2.68) | ||

| 50 | MV | -0.83(0.46) | 1.33(0.15) | -1.73(0.67) | |

| IFM | -0.85(0.60) | 1.32(0.19) | -1.75(0.73) | ||

| 0.6(3) | 10 | MV | -0.88(1.48) | 3.02(2.39) | -1.80(2.48) |

| IFM | -0.98(2.11) | 2.96(3.13) | -1.91(2.56) | ||

| 50 | MV | -0.82(0.45) | 3.01(0.61) | -1.73(0.71) | |

| IFM | -0.86(0.59) | 2.99(0.77) | -1.75(0.77) |

| Method | ||||||

|---|---|---|---|---|---|---|

| 0.4 | 10 | MV | -0.90(1.83) | 0.80(0.55) | 1.51(2.42) | -1.85(2.13) |

| IFM | -0.95(2.08) | 0.75(0.65) | 1.49(3.25) | -1.89(2.49) | ||

| 50 | MV | -0.82(0.51) | 0.77(0.12) | 1.51(0.98) | -1.73(0.63) | |

| IFM | -0.83(0.58) | 0.76(0.18) | 1.51(1.44) | -1.74(0.79) | ||

| Method | ||||||

| 0.6 | 10 | MV | -0.86(1.77) | 1.49(0.36) | 3.39(5.30) | -1.81(2.20) |

| IFM | -0.94(2.09) | 1.45(0.38) | 3.62(6.34) | -1.88(2.74) | ||

| 50 | MV | -0.81(0.49) | 1.47(0.11) | 3.48(2.14) | -1.77(0.73) | |

| IFM | -0.83(0.63) | 1.47(0.14) | 3.50(2.79) | -1.79(0.86) |

In Tables 1 to 3, all estimators have negligible biases. The discussion focuses on variances. As expected the strength of the - association in does not impact the precision of the two estimators for . The loss of precision for the IFM estimators is larger for the parameters of copula than for the parameters of the other 2 copula families. The efficiency of the maximum likelihood estimator is larger at than at . The Supplementary Material provides additional simulations for unequal sample sizes within clusters. Unequal sample sizes are associated to a small loss of precision for all estimators, especially at . This loss is, in general, more important for IFM estimators than for maximum likelihood estimators. Overall the two estimation methods give similar results; this supports the proposal of Section 4 to use IFM estimators to select the components of the proposed copula model. The detailed simulation results, including a presentation of the sampling properties of the estimators for for , are presented in the Supplementary Material.

5 Modeling math grades with a 2-exchangeable copula model

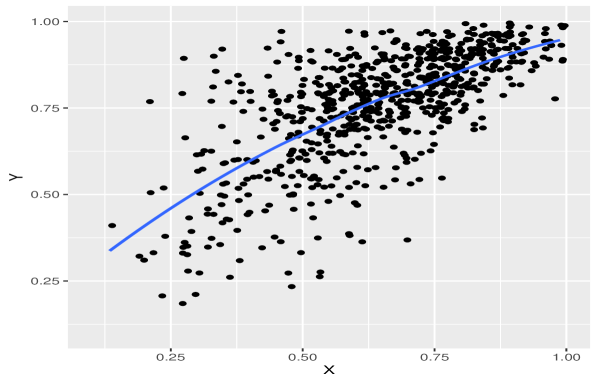

This section revisits a data set discussed in [10]. It concerns math grades in fourth and seventh year measured on students in primary schools. The cluster sample sizes vary between 4 and 40. The fourth year mark () and the seventh year mark () vary between 0 and 40. We map them to the (0,1) interval using the transform . To break ties in the grades a small random perturbation was added to each one.

One objective of the analysis presented here is to construct predictive models for given whose support is . Another objective is to investigate whether the 2-exchangeable copula model can capture the non-linearity seen in Figure 3 that gives a scatter plot of the data points and a smooth. The goal is to contrast an analysis carried out with copulas to the one reported in [10] that is based on standard normal linear mixed models.

5.1 Selection of the marginal distributions for and

The candidates families for and are the beta (denoted ) and the generalized beta (denoted ) distributions, see [4]. Indeed, by the construction of histogram of the distribution, we arrive at an asymmetric law. If has a distribution then has for a distribution whose density is given by

Table 4 compares the fit of these two distributions to the two margins. As stated in Section 4.1, this preliminary analysis does not account for the within cluster dependency. Thus the , for pseudo standard error, ignores the within classroom dependency.

| Variable | Model | AIC | ||

|---|---|---|---|---|

| (4.280,2.332) | (0.222,0.115) | -542.88 | ||

| (4.280,2.330,1) | (0.222,0.115,NA) | -540.80 | ||

| 5.24,1.79 | (0.28,0.08) | -789.57 | ||

| (2.616,2.319,0.29) | (0.303,0.241,0.069) | -826.96 |

The best fitting models are respectively the beta end the generalized beta for and .

5.2 Selection of the bivariate copula

The fist step is to calculate the pseudo observations et for and defined in (18). The Kendall’s tau is 0.49 () so there is a relatively strong association between the two variables. Following [13, chap. 1], Kendall’s tau is calculated for the sub-samples in the 4 quadrants of the unit square. This reveals a stronger association for large grades than for smaller ones. Also a 0.1 difference between the Kendall’s tau for the upper left and lower quadrant suggests that some of the asymmetry seen in the Figure 3 is left once the margins’ effect has been factored out.

Several copulas were fitted to this bivariate sample using the functions BiCopEst in the R package VineCopula and fitCopula in copula. To capture the asymmetry in the data we used to Khoudraji device, see (20) to create asymmetric alternatives. The best fitting copula in Table 5 is the survival Khoudraji normal copula given by

where is the bivariate normal copula with correlation . The density of a copula in this three parameter family can be evaluated using functions of copula. The conditional distribution, has the following explicit form.

| (21) |

In Table 5, Survival Khoudraji-Normal2 refers to a two parameter version of this copula obtained by setting .

| Copula | AIC | ||

|---|---|---|---|

| Normal | -454.32 | ||

| Survival-Gumbel | -459.5 | ||

| Survival Khoudraji-Normal | -474.10 | ||

| Survival Khoudraji-Normal2 | -468.64 |

5.3 Selection of the exchangeable copula families and

The exchangeable Kendall’s tau for and are respectively 0.046 () and 0.095 () showing a stronger school effect in the seventh year. The fit of several families of copulas for the joint distribution of and , evaluated using (21), are compared by maximizing the pseudo log-likelihoods and . The results are reported in Table 6. The normal family is the best choice for both and .

| Family | AIC | AIC | ||||

|---|---|---|---|---|---|---|

| Frank | 0.251 | 0.138 | -5.69 | 0.935 | 0.179 | -69.76 |

| Gumbel | 1.040 | 0.022 | -4.64 | 1.109 | 0.024 | -66017 |

| Normal | 0.064 | 0.025 | -12.76 | 0.167 | 0.035 | -80.03 |

To complete the analysis we carry out a full maximum likelihood estimation of the 10 parameters for the components of the proposed model. The parameter estimate for is very close to 1. We first carry out a likelihood ratio test for using the full likelihood. This gives for a p-value of 0.4%. Thus the full model, with 10 parameters, is definitive ; the estimates and standard errors () for the parameters are reported in Table 7.

| Component | ||

|---|---|---|

| () | ||

| () | ||

| (Normal) | ||

| (Survival Khoudraji-Normal ) | ||

| (Normal) |

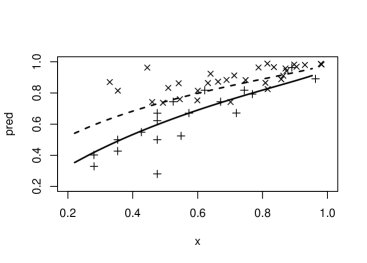

The fit of the final model summarized in Table 7 is illustrated using two schools, numbered 1, with , and 30, with . Their respective values of , see (15), are and ; this means that, for the same math4 mark, the math7 grade in School 30 are higher than in School 1. This can be seen in Figure 4 that gives the two regression curves, constructed using (16), that use the Gauss-Hermite quadrature method to approximate the normal integrals for each -value.

Conditional residuals for the fitted copula models can be defined as , where is evaluated as the predicted value at , using (16), where the values of and , see (15), are those for school . The conditional residuals of the copula model () can be compared to those of mixed linear models. The first one, , has a random school intercept while the second one, , has possibly dependent random slope and intercept. The mean squared errors and inter quartile ranges (IQR) of the residuals for , , and , are (0.0107, 0.0112, 0.0101) and (0.1082, 0.1186, 0.1098) respectively. Thus, in agreement with the analysis reported in Table 5, the fit of is poor. The fits of and are very similar as the latter captures the between school change in slope than can be seen in Figure 4. has a larger residual MSE; however it has a smaller residual IQR and it gives a smaller absolute residual than for of the data points.

The key advantage of the 2-exchangeable copula model is that it allows prediction intervals for to depend on both, the School and the -value. This is illustrated in Figure 5 that gives the predictive densities for mark , given by formula(17), for and in Schools 1 and 30. The variability of is larger at and in School 1. This can be seen by looking at the corresponding 95% prediction intervals for that are given in Table 8.

| School | ||

|---|---|---|

| 1 | (0.23, 0.89) | (0.66,0.97) |

| 30 | (0.44,0.97) | (0.86,0.99) |

6 Conclusion

The 2-exchangeable copula model proposed in this work provides flexible methods to predict variable knowning in a hierarchical data set. A key feature of the proposed methodology highlighted in Section 4 is the flexibility of the predictive densities for given . Its shape and its support can depend on the known value for and on the cluster. An outstanding problem is whether the proposed model can be generalized to two or more continuous explanatory variables. The key to such a generalization is the availability of flexible -exchangeable families for the joint distribution of the explanatory variables for all the unit in a cluster. An elliptical copula, with a correlation matrix given by (3) could be used. This specifies partially the copula for the joint distribution of the and the variables on a unit. A vine decomposition could possibly be used to complete the specification of . These problems will be the object of future investigations.

Supplementary Material

The supplementary material contains the proof of Proposition and additional results of the of the Monte Carlo simulation study.

Acknowledgments and Miscellaneous

We would like to thank Étienne Marceau for his critical reading of a previous version of this work.

Funding

The support of the Natural Sciences and Engineering Research Council of Canada is gratefully acknowledged.

Disclosure Statement

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability

The data is available upon request.

References

- Acar et al. [2019] E. F. Acar, P. Azimaee, M. E. Hoque, Predictive assessment of copula models, Canadian Journal of Statistics, 47 (2019) 8–26.

- Battese et al. [1988] G. E. Battese, R. M. Harter, W. A. Fuller, An error-components model for prediction of county crop areas using survey and satellite data, Journal of the American Statistical Association, 83 (1988) 28–36.

- Bernard and Czado [2015] C. Bernard, C. Czado, Conditional quantiles and tail dependence, Journal of Multivariate Analysis, 138 (2015) 104–126.

- Cockriel and McDonald [2018] W. M. Cockriel, J. B. McDonald, Two multivariate generalized beta families, Communications in Statistics - Theory and Methods, 47 (2018) 5688–5701.

- Crane and Van der Hoek [2008] G. J. Crane, J. Van der Hoek, Conditional expectation formulae for copulas, Australian and New Zealand Journal of Statistics 50 (2008) 53–67.

- Czado [2019] C. Czado, Analyzing dependent data with vine copulas : a practical guide with R, 2019.

- Czado and Nagler [2022] C. Czado, T. Nagler, Vine copula based modeling, Annual Review of Statistics and Its Application, 9 (2022) 453–477.

- Dissmann et al. [2013] J. Dissmann, E. C. Brechmann, C. Czado, D. Kurowicka, Selecting and estimating regular vine copulae and application to financial returns, Computational Statistics and Data Analysis, 59 (2013) 52–69.

- Genest et al. [1998] C. Genest, K. Ghoudi, L.-P. Rivest, Discussion of “understanding relationships using copulas, by E. Frees and E. Valdez”, North American Actuarial Journal, 3 (1998) 543–552.

- Goldstein [2011] H. Goldstein, Multilevel Statistical Models, Wiley, 2nd edition, 2011.

- Grover et al. [2020] K. Grover, E. F. Acar, M. Torabi, Copula-based predictions in small area estimation, Canadian Journal of Statistics, 48 (2020) 685–711.

- Ivan Kojadinovic and Jun Yan [2010] Ivan Kojadinovic, Jun Yan, Modeling multivariate distributions with continuous margins using the copula R package, Journal of Statistical Software, 34 (2010) 1–20.

- Joe [2014] H. Joe, Dependence modelling with copulas, Chapman and Hall, 2014.

- Kumar and Shoukri [2007] P. Kumar, M. Shoukri, Copula based prediction models: an application to an aortic regurgitation study, BMC Medical Research Methodology, 7 (2007) 1–9.

- Mai and Scherer [2012] J. F. Mai, M. Scherer, Simulating copulas: stochastic models, sampling algorithms, and applications, Quantitative Finance, 2012.

- McCulloch and Searle [2001] C. E. McCulloch, S. R. Searle, Generalized, linear, and mixed models, John Wiley et Sons, 2001.

- Nelsen [2006] R. B. Nelsen, A introduction to copulas, Springer, 2006.

- Noh et al. [2013] H. Noh, A. E. Ghouch, T. Bouezmarni, Copula-based regression estimation and inference, Journal of the American Statistical Association, 108 (2013) 676–688.

- Panagiotelis et al. [2012] A. Panagiotelis, C. Czado, H. Joe, Pair copula constructions for multivariate discrete data, Journal of the American Statistical Association, 107 (2012) 1063–1072.

- Rivest et al. [2016] L. Rivest, F. Verret, S. Baillargeon, Unit level small area estimation with copulas, The Canadian Journal of Statistics/ La revue Canadienne de statistique, 44 (2016) 397–415.

- Romdhani et al. [2014] H. Romdhani, L. Lakhal-Chaieb, L.-P. Rivest, An exchangeable kendall’s tau for clustered data, Canadian Journal of Statistics, 42 (2014) 384–403.

- Stefanski and Boos [2002] L. A. Stefanski, D. D. Boos, The calculus of m-estimation, The American Statistician, 56 (2002) 29–38.

- Su et al. [2019] C.-L. Su, J. G. Neslehova, W. Wang, Modelling hierarchical clustered censored data with the hierarchical kendall copula, Canadian Journal of Statistics, 47 (2019) 182–203.

- Tsiatis [2006] A. A. Tsiatis, Semiparametric theory and missing data, Springer, 2006.

- Verbeke and Molenberghs [2000] G. Verbeke, G. Molenberghs, Linear mixed models for longitudinal data, Springer, 2000.