Wong–Zakai approximation of regime-switching SDEs via rough path theory

Abstract

This paper investigates the convergence of Wong–Zakai approximations to regime-switching stochastic differential equations, generated by a collection of finite-variation approximations to Brownian motion. We extend the results of [NP21] to -valued RSSDE by utilising rough path theoretic tools, acquiring the same modification of rate.

AMS 2020 Mathematics Subject Classification: 60H10, 60L90, 60F15.

Keywords: Wong–Zakai approximation, regime-switching stochastic differential equations, rough path theory, strong convergence.

1 Introduction

The ability to incorporate uncertainty has become a standard aspect of modern applied models. Indeed, the specific class of models known as stochastic differential equations (SDE) has found a wide variety of applications in modelling continuous phenomena across fields such as quantitative finance, ecology, mathematical biology, dynamical systems, and so on. However, SDEs suffer in that they only account for continuous sources of uncertainty, typically driven by an -valued Brownian motion . This deficiency motivates the notion of regime-switching, in which the evolution of the stochastic process depends on an additional jump process with countable state space :

where and are a collection of drift and diffusion vector fields indexed by the (countable) state space of the jump process . Regime-switching SDEs (RSSDEs) allow one to account for discrete changes in environment that influence the continuous dynamics of . Think of a pressure sensor which is either operational or error-prone, or the trajectory of a stock price in a “good” or “bad” market.

Regime-switching models have found a number of applications in quantitative finance [DPR02, ZC13], in modelling rough volatility [YZ10], and more recently in mean-field games [BDTY20].

Naturally, the introduction of the jump process complicates the process of approximating such processes. Recently the first paper dealing with so-called Wong–Zakai approximations of 1-dimensional RSSDEs emerged [NP21]. The fundamental question addressed there is whether the strong convergence of finite-variation approximations to a Brownian motion passes to convergence of the approximating RSSDEs to , and how the rate of convergence is affected. Recall that a collection of stochastic processes is said to converge strongly to with rate function if for all

| (1) |

where is a constant dependent only on and , and denotes the supremum norm over the interval . To address this question, Nguyen and Peralta [NP21] utilised a local pathwise estimate of the form

| (2) |

where is a random variable with desirable probabilistic properties. The estimate (2) allows one to locally control the error of the regime-switching SDE approximation by the error in the driving processes, while the behaviour of is exploited to extend the strong convergence of to with a slightly worse rate, in the sense that

for all and .

Unfortunately, (2) fails to hold in the multi-dimensional case, due to the fact that the topology induced by the supremum norm is ill-suited to providing such estimates in dimension . In the higher-dimensional setting, one can introduce oscillations at small scales to the approximations such that the limit remains unaffected, but it no longer holds that . The approximations can in fact converge to a different limiting object given by , plus some correction term that vanishes in the scalar case or when vector fields built from commute (see [IW92, Theorem 7.2] for further discussion).

To resolve this problem we utilise rough path theory, introduced by Lyons [Lyo98] in the mid 90s. Rough path theory avoids the aforementioned problem by working with a stronger topology, induced by the so-called inhomogeneous rough path metric . This metric is built from a collection of path-norms, one of which is the -variation seminorm of a path

| (3) |

where denotes the Euclidean norm and the supremum is taken over all partitions of . Convergence of to in -variation norm not only implies convergence in supremum norm, but it also tracks small-scale oscillations. The payoff is that the local Lipschitz continuity of the solution map is restored, albeit in the different function space with a stronger topology that requires “higher order” information than just the path . We discuss this in further detail in Section 2.

To run a similar argument as in [NP21], we utilise a recent refinement [CFRS16] of the Lipschitz estimate that applies to a class of Gaussian processes (and approximations thereof), of which Brownian motion is included. This leads us to the main result:

Theorem 1.1.

Assumption 5.1 matches Assumption 4 of [NP21], which ensures that the jumps of are well-behaved by imposing bounds on the tail probability of the number of jumps over the compact interval . As noted in [NP21], this assumption is not overly restrictive in that it allows for deterministic, time-homogeneous Markov, time-inhomogeneous Markov, and semi-Markov processes. The conditions of Theorem 4.1 are those required to guarantee the existence of a unique solution to the corresponding rough regime-switching equation associated to the regime-switching SDE of interest. Notably, this requires much higher regularity than the standard assumption of local Lipschitz continuity and linear growth from SDE theory.

The structure of the paper is as follows. We briefly recall in Section 2 some main results and definitions from rough path theory. In Section 3 we formally define the partitioning scheme introduced in [CLL13], and describe how the functional of interest behaves under path concatenation and strong convergence. In Section 4 we extend the improved Lipschitz estimate for RDEs driven by Gaussian noise [CFRS16] to the regime-switching case. In Section 5, we establish the strong convergence of approximations to regime-switching RDEs by utilising tail behaviour of the greedy partition from Section 3 and the pathwise estimates from Section 4. We conclude with a brief application to the standard scheme of approximation via linear interpolation to a Brownian rough path.

2 Preliminaries

In this section we provide some background information on rough path theory, regime-switching SDEs and strong convergence.

2.1 Rough path theory

Rough path theory, first introduced in [Lyo98], provides a pathwise solution theory for stochastic differential equations. To make rigorous the notion of ‘roughness’, we use the -variation seminorm of a path as defined in (3). If one is interested in solving equations of the form

| (5) |

for paths and (the space of linear maps from into ), -variation turns out to be a natural scale with which to measure the roughness of paths. As Young [You36] discovered, the integral is defined classically via Riemann–Stieltjes integration if and are of bounded and -variation, with . This condition is sharp in the sense that examples of paths exist satisfying such that the Riemann–Stieltjes approximations of fail to converge. In the simplified setting where for some smooth , this implies that must be a path with finite -variation for . Remarkably, this is the exact threshold which the sample path regularity of Brownian motion fails to meet [FV10]. Thus, we call a path rough if it is of finite -variation only for some .

To deal with this problem when the driving path is a Brownian motion, stochastic calculus exploits the desirable probabilistic properties of Brownian motion by considering convergence of the approximates in probability, rather than almost surely, as the mesh size of the partition tends to zero. Rough path theory, on the other hand, takes a different approach.

The perspective of rough path theory is that the limit

fails to converge because the zeroth order approximation for is not good enough to account for the roughness of the driving path . If instead we take the first order approximation , the approximation of our integral becomes

| (6) |

where denotes the tensor product. When has finite -variation with , so that is classically defined, then the above approximation converges to the usual Riemann–Stieltjes integral. In the rough setting with , the iterated integral is no longer uniquely defined as a function of the path , and so we instead postulate values for the iterated integral by specifying a two-parameter path . Any choice of satisfying an algebraic condition known as Chen’s relation and having finite -variation is a suitable candidate, with different choices yielding different limits for (6). Equation (6) is then referred to as the rough path integral with respect to the -rough path . This approach works not only for functions of the path , but also for a class of paths known as controlled rough paths.

Definition 2.1.

Let be a path of finite -variation. We say that is controlled by if there exists a path such that

where and have finite -variation, and the remainder term has finite -variation. We denote the space of all paths controlled by by .

The space is a Banach space under the norm

with

This opens the door to fixed-point techniques, allowing us to establish the existence and uniqueness of solutions to rough differential equations by finding fixed-points in .

Although this procedure of making a particular choice of may seem arbitrary, there are some natural choices when is a Brownian motion. In this setting, we may simply enhance with its stochastic iterated integral , in either the Itô or Stratonovich sense. Here, we work with the Stratonovich iterated integrals , and refer to the object as the Brownian rough path, or enhanced Brownian motion.

Given the importance of the -variation of a path highlighted above, we introduce the inhomogeneous -rough path metric

with

Finally, we introduce the -Lipschitz norm of a map between two normed spaces. In the following, let be the largest integer which is strictly smaller than , so that we may always write with .

Definition 2.2 (-Lipschitz norm, [FV10]).

A map between two normed spaces and is called -Lipschitz (in the sense of E. Stein), in symbols

if is is times continuously differentiable and such that there exists a constant such that the supremum norm of its th-derivatives , and the Hölder norm of its th derivative are bounded by . The smallest satisfying the above conditions is the -Lipschitz norm of and denoted .

The payoffs to this approach are numerous. Whilst the solution map associated with the SDE , is in general only measurable, the solution map associated to a rough differential equation , is locally Lipschitz continuous (under some standard conditions) with respect to the initial condition, driving path, and the vector field . This leads to error estimates of the form

| (7) |

In particular, this estimate may be applied when we consider approximations of rough differential equations (RDEs) of the form (5). Given a rough path and a collection of finite-variation approximations of , we can lift these approximations to rough paths by enhancing them with the Riemann–Stieltjes integrals . Establishing convergence of to in rough path metric then implies convergence of via Equation (7), where is the solution of and is the solution of .

Remark 2.3.

The supremum norm in Equation (7) can generally be replaced by the -variation rough path metric. However, we return to the weaker supremum topology as it is a standard way to measure approximation error.

2.2 Gaussian rough paths

Unlike the semimartingale setting, there is no notion of stochastic integration we could use to lift a general -valued Gaussian process to a rough path . Recalling that the law of a (centred) Gaussian process is completely determined by its covariance function , it is perhaps not surprising that the question of finding a natural rough path lift boils down to the regularity of the rectangular increments of .

Definition 2.4.

Let be a centred -valued Gaussian process with covariance function . The rectangular increments of are given by

Given a set , the 2D -variation of is given by

Under the condition that is a Gaussian process with covariance of finite 2D -variation for , we may define the integral of against as the -limit

| (8) |

Further to this, we have an estimate of the form

where [Proposition 10.3, [HF14]]. Defining

it follows that if there exists and such that for every and

then the process is almost surely a -rough path for [Theorem 10.4, [HF14]]. This result can be pushed further to , but requires a third level of the rough path to be defined (see Chapter 15 of [FV10]).

Example 2.5 (Brownian motion).

Given a Brownian motion , the covariance function has the form . Since and are centred and independent for , . The on-diagonal terms then take the form

showing that has finite 2D -variation for . Lifting to a rough path using the Gaussian framework will yield a process which is indistinguishable from the Stratonovich lift [HF14].

Example 2.6 (Fractional Brownian motion).

Recalling fractional Brownian motion for is the -valued process with covariance function

[FV10] show that has finite 2D -variation for .

2.3 Regime-switching SDE via rough paths

The consistency between stochastic and rough integration, when both are defined, is a well-known feature of rough path theory [FV10]. Indeed, the standard regularity requirements that are imposed to guarantee the existence of a unique solution to a given RDE are enough to ensure the existence of a unique strong solution to the corresponding SDE.

Definition 2.7 (Regime-switching SDE).

Let be a jump process with finite activity on compact intervals and countable state space . Let and , and write , . Finally, let be an -valued Brownian motion independent of and . Then the equation

| (9) |

is referred to as a regime-switching stochastic differential equation.

Remark 2.8.

One can express the solution as a coupled process where is given by the stochastic integral with respect to a Poisson random measure [YZ10]. This can be useful in refining some arguments when working with jump processes with probabilistic behaviour depending on the trajectory of , but for our purposes (9) will be more useful.

Remark 2.9.

Under the conditions on in Definition 2.7, with suitable conditions on and , there exists a unique strong solution for the SDEs

Considering the stopping times and , we may write for

The almost sure finite jump activity of then implies that , so that the above holds for all , . Thus, we can recover solutions of (9) by concatenating solutions of SDEs within known regimes.

We now introduce the rough equivalent of regime-switching SDEs:

Definition 2.10.

Let be a jump process with a.s. finite activity on compact intervals and countable state space . Let be such that . Assume that

-

1.

is a collection of vector fields for ;

-

2.

; and

-

3.

is a Gaussian rough path.

Let be the jump times of on (with denoting the number of jumps of ) and let be the RDE solutions to

Then the path constructed by concatenating the individual paths is said to solve the regime-switching rough differential equation driven by and .

It remains to prove consistency between stochastic and rough regime-switching differential equations. Given that solutions to these equations are determined via fixed-points of the rough and stochastic integral respectively, we prove consistency for general regime-switching rough integration and regime-switching stochastic integration.

Theorem 2.11.

Let denote the Itô Brownian rough path, be a Markov chain with finite state space with , and suppose almost surely for each . Then the regime-switching rough integral

| (10) |

exists, with the limit taken along any sequence with mesh size tending to 0. In the case that and are adapted for every , then

almost surely.

Proof.

In the following we assume that

noting that if this is not the case we may proceed by localisation. Having defined the regime-switching rough integral for a fixed trajectory of and via concatenation of the rough integral over periods when is in a fixed regime, we must show that the approximation in Equation (10) converges to the same path. To this end, let denote the integral achieved by concatenation and by the proposed limit (10). Let denote the jump times of on the interval . Noting that for , we consider . We must deal with the fact that for any sequence of partitions , there will generally be consecutive points with such that we will be approximating the regime-switching rough integral by the wrong control. That is, if and , we will be approximating over the interval as if the jump process was in state over the whole interval. Adding and subtracting the ‘correct’ control we see that

where and we have used the fact that is additive and satisfies Chen’s relation to split the terms. Since for every , the first term converges to . The other three terms do not affect the limit, which we see from the bounds

for

We repeat this process for , and so on, noting that since almost surely we can cover in a finite number of steps, showing that almost surely for any .

Next, we show that the rough path and stochastic integrals coincide almost surely. To do so, we use the standard technique of showing that our rough path approximation converges in to the Itô integral . Then, since the approximation converges to the rough path integral almost surely and the stochastic integral in , these limits must coincide. We consider the specific partition of . Consider the error

where in the final step we condition on the -algebra generated by . Noting that the product of the stochastic integral over disjoint intervals has expectation zero and applying the (multivariate) Itô isometry to the remaining terms, we get

Now, if for all , then the integrand is controlled by for the fixed regime over the whole interval, meaning that , where is the remainder term. In such a case, we can bound the integral by writing

In the case that a jump occurs at time to state in the interval , we decompose the integral via

The first term can be bounded as before, while for the second we observe that

Since this occurs in at most of the intervals, we can bound (absorbing constants dependent on and ) by

provided and . ∎

2.4 Strong convergence

Let be a metric space, and suppose that is a family of -valued random variables with time horizon . We say that converges strongly to an -valued random variable if

Further, we say that converges with rate if there exists a function and constant such that

for all . Of particular interest is the case when we take to be the path space of a given stochastic process. For example, we may take the usual choice with to investigate the strong convergence of stochastic processes with continuous sample paths, as in [RW85, NP21]. In the sequel, we consider strong convergence in the rough path space equipped with the -variation rough path metric.

There are two approaches we will take to prove strong convergence. The first is a rudimentary application of the Markov inequality, while the second utilises Lipschitz estimates on bounded sets in . The second method is well suited to extend strong convergence of processes that drive regime-switching SDEs to the solutions of said RSSDEs.

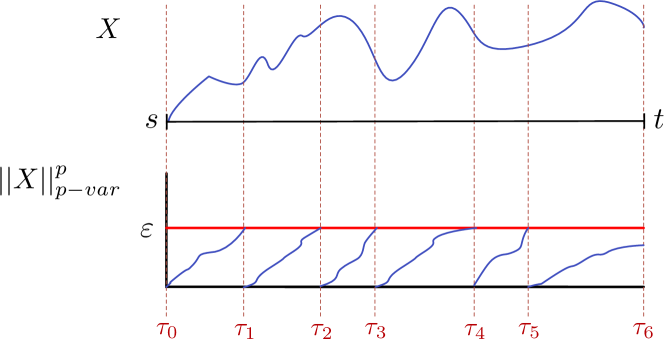

3 The greedy partition

We introduce the greedy partition first introduced in [CLL13] by Cass, Litterer and Lyons. In the following, let be shorthand for the 2-simplex on :

We first recall the definition of a control.

Definition 3.1.

A function is called a control if:

-

1.

is superadditive, so that for all

-

2.

for all , and

-

3.

is continuous.

Definition 3.2.

Let be a control. For , set

and define

The sequence is then called the greedy sequence, with counting the number of distinct elements in .

Lemma 4.9 and Corollary 4.10 in [CLL13] establish that is well-defined for the particular choice whenever is a -rough path, and that the greedy sequence (with the trivial tail removed) forms a partition of . As discussed in [FR13], the random functional enjoys far better probabilistic tail estimates than . This, combined with the Lipschitz estimate of Theorem 4 in [CFRS16], is the primary tool we will utilise in the proof of our main theorem.

Specifically, we use the tail estimate from Corollary 2 of [FR13],

which applies to a class of Gaussian -rough paths including Brownian motion, and where are constants dependent on the type of process chosen. Since for every polynomial there exists some such that

there exists some constant such that

for all , where depends on and depends on the previous constants.

Remark 3.3.

For the Brownian rough path case , we may choose , yielding Gaussian tails.

We now investigate the behaviour of under concatenation.

Lemma 3.4.

Let be a partition of . Then

Proof.

Let be the greedy sequence over for the control . If there exist such that , then , which follows from

Thus, without loss of generality we assume that there is at most one between any given pair . Next, we set for and write

with the last inequality following from the fact that .

∎

We now investigate the tail behaviour of an approximation to , under the assumption of strong convergence. We begin with a simple set inclusion:

Lemma 3.5.

Let and be -rough paths, and take . Then

Proof.

By the triangle inequality and Jensen’s inequality, we have

Then, if it follows that

yielding

For simplicity of notation, let us write

Consider the greedy sequence (resp. ) associated with the control (resp. ). Since for all , we have . Thus, given consecutive times , one can always find a value of such that . To see this, observe that taking , we have by the superadditivity of and that

It follows that setting , and also that . Thus we have

for . Finally we have

which completes the proof. ∎

Next, we investigate how the strong convergence of in the inhomogeneous -rough path metric affects the tails of and .

Lemma 3.6.

Suppose that strongly in the inhomogeneous -rough path metric , with rate . Then

for all .

Proof.

We note that if and only if there exists some such that . Since is superadditive, this implies . Thus,

Bounding the homogeneous norm by

we see that

with . Finally, we pick a such that for all . This yields

as required. ∎

Lemma 3.7.

Let be Gaussian rough paths of finite mixed variation, and suppose that strongly in inhomogeneous -rough path metric with rate , and . Then there exists some constant such that

4 Lipschitz estimates for rough RSSDE

In this section, we extend the (local) Lipschitz estimates for rough differential equations to the regime-switching case.

Theorem 4.1.

Let be a Gaussian rough path, a family of rough path lifts of finite-variation processes, and be a Markov process independent of , with state space and a.s. finite jump activity on compact intervals. Let , and be a family of vector fields such that is uniformly bounded by some , that is, .

Now, let be a partition of given by the jump times of . Define and to be the RDE solutions to

and

respectively, and define (resp. ) to be the concatenation of the (resp. ). Then, there exists some constant such that

where .

Proof.

Under the proposed conditions each and exists uniquely and is continuous, and these properties extend to the concatenation and . Theorem 4 of [FR13] yields the estimate

| (12) | ||||

for each . Noting that

we can rewrite Equation (12) as

Iterating back to yields

By Lemma 3.4 and the fact that if , we have

Finally, noting that

we arrive at the estimate

with and . ∎

5 Strong convergence

To establish the strong convergence of in supremum norm, we apply the methodology in [NP21] of utilising the probabilistic properties of the local Lipschitz coefficient of the solution map (Theorem 4.1). As in [NP21], we impose a constraint on the jump process to control the growth of the constant appearing in Theorem 4.1.

Assumption 5.1.

There exists some such that .

Assumption 5.1 clearly holds if is deterministic. We refer to Lemma 4.3 of [NP21] which implies that Assumption 5.1 holds whenever is of bounded jump intensity.

Lemma 5.2.

Let be a jump process satisfying Assumption 5.1. Then the number of jumps has finite expectation.

Proof.

Using the tail sum formula for expectation, we see that

Since , for large enough we have

∎

We are now in a position to show that strongly in supremum norm with rate slightly worse than in rough path metric.

Theorem 5.3.

Proof.

Using the estimate in Theorem 4.1, we see that

Let and as in [NP21]. Write

and introduce the events

As

| (14) |

we can show strong convergence by showing that every term on the RHS of (14) is . Lemma 3.7 shows that

while the Gaussian tails of yield

The proof of Theorem 4.6 of [NP21] shows . Thus, (14) becomes

Collecting constants that are independent of , the above becomes

for some constant . We will now show that

We have that from [NP21] via the asymptotic decomposition of Lambert–W functions. Next,

As a result, we may choose some such that , for all . Thus, for all ,

Finally, setting , we see that

as required. ∎

Theorem 5.4.

Let and be Gaussian rough paths, and a jump process independent of and satisfying Assumption 5.1. Suppose there exists with such that for all

where is a constant dependent on and only. Then there exists some constant such that for all ,

Proof.

6 Approximation schemes

Having proved Theorem 5.3, it remains to provide approximations of enhanced Gaussian processes that converge strongly. The following lemma will prove useful in this pursuit.

Lemma 6.1.

Let be a complete metric space, a -valued random variable and a collection of -valued random variables. If there exist constants and such that for all , then strongly with rate function , for .

Proof.

By Markov’s inequality, we write

To show that the RHS is , we simply set provided . ∎

The class of Gaussian rough path we work with are those introduced in [CFRS16]:

Condition 6.2 (Condition 10, [CFRS16]).

Let be a centred, continuous Gaussian process with independent components. Assume that the covariance of every component has Hölder dominated finite mixed -variation for some on , that is, there exists such that, for and uniformly over in ,

The notion of mixed variation is a more refined notion than -variation. Specifically, we note that fractional Brownian motion satisfies condition 6.2 with . The class of approximations to these processes that we work with are those satisfying the following condition, as presented in [CFRS16].

Condition 6.3.

Condition 6.3 implies the convergence of the rough path lift in -variation rough path metric for . Further to this, one can show that taking to be the linear interpolation of with mesh-size at most , that .

Acknowledgments

GTN and OP gratefully acknowledge the support of the Australian Research Council DP180103106 grant. Additionally, OP acknowledges financial support from the Swiss National Science Foundation Project 200021-191984.

References

- [BDTY20] Alain Bensoussan, Boualem Djehiche, Hamidou Tembine, and Sheung Chi Phillip Yam. Mean-Field-Type Games with Jump and Regime Switching. Dynamic Games and Applications, 10(1):19–57, 2020.

- [CFRS16] B. Christian, P. Friz, S. Riedel, and J. Schoenmakers. From rough path estimates to multilevel monte carlo. SIAM Journal on Numerical Analysis, 54(3):1449–1483, 2016.

- [CLL13] T. Cass, C. Litterer, and T. Lyons. Integrability and tail estimates for Gaussian rough differential equations. The Annals of Probability, 41(4):3026 – 3050, 2013.

- [DPR02] Jin-Chuan Duan, Ivilina Popova, and Peter Ritchken. Option pricing under regime switching. Quantitative Finance, 2(2):116, apr 2002.

- [FR13] P. Friz and S. Riedel. Integrability of (non-)linear rough differential equations and integrals. Stochastic Analysis and Applications, 31:336–358, 2013.

- [FR14] P. Friz and S. Riedel. Convergence rates for gaussian rough paths. 2014.

- [FV10] Peter K. Friz and Nicolas B. Victoir. Multidimensional Stochastic Processes as Rough Paths: Theory and Applications. Cambridge Studies in Advanced Mathematics. Cambridge University Press, 2010.

- [HF14] Martin Hairer and Peter Friz. Rough path theory: with an introduciton to regularity structures. Springer, 2014.

- [IW92] N. Ikeda and S. Watanabe. Stochastic differential equations and diffusion processes. 1992.

- [Lyo98] T. Lyons. Differential equations driven by rough signals. Rev. Mat. Iberoam., 14(2):215 – 310, 1998.

- [NP21] G.T. Nguyen and O. Peralta. Rate of strong convergence to solutions of regime-switching stochastic differential equations. 2021.

- [RW85] W. Römisch and A. Wakolbinger. On Lipschitz dependence in systems with differentiated inputs. Mathematische Annalen, 272:237–248, 1985.

- [You36] L. Young. An inequality of hölder type, connected with stieltjes integration. Acta Mathematica, 67(none):251 – 282, 1936.

- [YZ10] G. Yin and C. Zhu. Hybrid switching diffusions. Springer New York, NY, 1 edition, 2010.

- [ZC13] Wei Zou and Jiahua Chen. A markov regime-switching model for crude-oil markets: Comparison of composite likelihood and full likelihood. The Canadian Journal of Statistics / La Revue Canadienne de Statistique, 41(2):353–367, 2013.