[] \cormark[1]

url]https://www.as.ior.kit.edu/

[]

[2]

url]https://www.b-tu.de/fg-energiewirtschaft/

[]

[]

1]organization=Karlsruhe Institute of Technology (KIT), addressline=Institute for Operations Research, city=Karlsruhe, postcode=76131, country=Germany

2]organization=Brandenburg University of Technology (B-TU), addressline=Chair of Energy Economics, city=Cottbus, postcode=03046, country=Germany

A hybrid model for day-ahead electricity price forecasting: Combining fundamental and stochastic modelling

Abstract

The accurate prediction of short-term electricity prices is vital for effective trading strategies, power plant scheduling, profit maximisation and efficient system operation. However, uncertainties in supply and demand make such predictions challenging. We propose a hybrid model that combines a techno-economic energy system model with stochastic models to address this challenge. The techno-economic model in our hybrid approach provides a deep understanding of the market. It captures the underlying factors and their impacts on electricity prices, which is impossible with statistical models alone. The statistical models incorporate non-techno-economic aspects, such as the expectations and speculative behaviour of market participants, through the interpretation of prices. The hybrid model generates both conventional point predictions and probabilistic forecasts, providing a comprehensive understanding of the market landscape. Probabilistic forecasts are particularly valuable because they account for market uncertainty, facilitating informed decision-making and risk management. Our model delivers state-of-the-art results, helping market participants to make informed decisions and operate their systems more efficiently.

keywords:

Electricity price forecasting \sepHybrid model \sepEnergy system modelling \sepStochastic modelling \sepError improvement \sepProbabilistic forecasting1 Introduction

Accurate forecasting in the energy sector is crucial for multiple stakeholders, including industry practitioners, researchers and policymakers. The effectiveness of financial and operational decisions and regulatory interventions depends on accurate predictions of future developments in relevant areas. As a result, the forecasting of electricity prices has become a key area of focus (Weron, 2014). With companies facing increasingly intense competition due to deregulation and liberalisation in the electricity sector, day-ahead price forecasts and insight into the next day’s market situation are essential to the development of bidding strategies and production plans that maximise a company’s profit margins and ensure a reliable grid operation. Quantifying uncertainty has become increasingly important in recent years due to the growth of renewable energies and the need to integrate them alongside an increase in infrastructural challenges and fluctuating commodity prices, raising uncertainty in the energy market (Nowotarski and Weron, 2018; Hong et al., 2016, 2020). Probabilistic forecasts help in the planning and operation of energy systems, allowing for the assessment of uncertainty and the development of future strategies against the background of various probable future events (Amjady and Hemmati, 2006).

Our paper presents a novel, open-source hybrid model that forecasts day-ahead electricity prices punctually and probabilistically by combining two main methodological streams: techno-economic energy system modelling and stochastic modelling. Techno-economic models are fundamental energy system models that determine (partial) market equilibria through the bottom-up optimisation of an energy system. They can explain actual developments and reflect structural breaks by identifying techno-economic interdependencies in energy markets. However, when estimating prices in the short term (e.g., day-ahead, intraday), these models exhibit larger and more systematic errors than other model classes. Stochastic models, on the other hand, learn from history and are developed and trained with historical data, enabling them to capture fluctuations and uncertainties in the market, especially in the short term. They offer high flexibility and the ability to specify forecast ranges and distributions. Still, they can only capture structural breaks and changes in external influences ex-post due to their dependence on historical data.

Our proposed hybrid model combines the strengths of techno-economic energy system models and stochastic models to develop a more robust and accurate approach to forecasting electricity prices on the day-ahead market. The model retains the structural statements of techno-economic energy system models – and, thus, insights into the driving market mechanisms – while incorporating stochastic short-term structures and distribution functions to account for uncertainty. The model uses state-of-the-art methods to generate point and probabilistic price forecasts. These probabilistic price forecasts, with probabilities for each potential price scenario, are increasingly valuable to the industry (e.g., when assessing the probabilities of negative prices or when assessing the overall risk level of the price forecast).

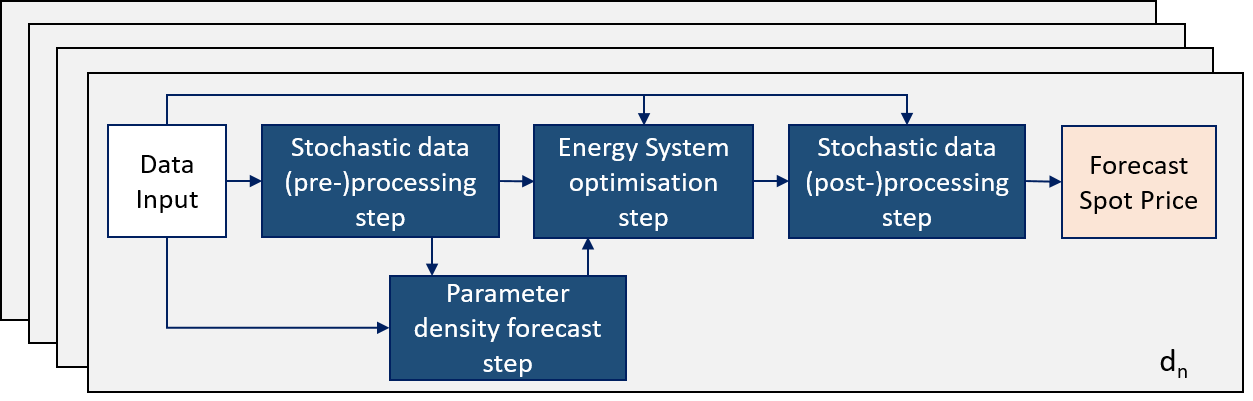

The model is schematically illustrated in Figure 1. It employs a rolling-window approach. In each iteration, it forecasts day-ahead prices exclusively through the use of data known prior to the day-ahead market’s closure, accurately reflecting the knowledge of stakeholders making decisions in these markets. The model is repeatedly applied each day () to generate forecasts for the following 24 hours of the day-ahead market. Each daily forecast includes four steps – stochastic data pre-processing, parameter density forecast, energy system optimisation and stochastic data post-processing – to produce point and probabilistic forecasts.

The first step, stochastic data pre-processing, aims to improve the accuracy of input data in advance of the energy system optimisation step and generates the basis for the parameter density forecast step. In the second step, the parameter density forecast generates prediction intervals for selected input parameters of the third step, energy system optimisation, enabling us to account for uncertainty in the operational decisions of market participants. This step considers the improved input data from the first and second steps. It forms a stochastic optimisation model that minimises total system costs, identifies the equilibrium between supply and demand and determines the hourly marginal system costs, which can be interpreted as price estimators.

These price estimators are the initial values in the fourth and final step, stochastic data post-processing. The errors of the price estimators are mapped using a multidimensional model in which seasonal effects and structures are captured using a combination of univariate and multivariate approaches, resulting in an enhanced price forecast. By modelling and improving the price forecast error, the model calculates forecast intervals and probability densities for the forecast prices, providing a quantification of uncertainty. Finally, our model can combine the strengths of both method classes to achieve excellent state-of-the-art price forecasts, including both point and probabilistic forecasts, to capture the stochastic uncertainty of the market.

This paper contributes to the literature in three main ways. First, it presents a novel hybrid model that provides a general framework to combine techno-economic and stochastic energy models. Since the model’s source code and algebra are available in full online, other researchers can apply our methodology and extend it to different time periods and electricity markets around the world. Second, it proves that techno-economic energy system models can contribute to short-term price forecasting, especially when paired with stochastic models for the sake of error improvement. Our hybrid model delivers highly accurate day-ahead price forecasts on top of the insights that techno-economic models provide. We demonstrate its value with an empirical analysis based on European data with a focus on Germany, the largest European electricity market. Third, our hybrid model provides probabilistic forecasts in addition to point forecasts, enabling power plant operators to, for example, quantify the likelihood of prices becoming negative at any given hour.

The remainder of this chapter is organised as follows. Section 2 reviews the existing literature. Afterwards, we provide all of the information necessary to use our model and replicate this study in Section 3. Section 4 describes our methodology. Following, Section 5 presents and evaluates the results of our hybrid model, while Section 6 closely analyses the individual model steps. Finally, Section 7 offers some concluding remarks.

2 Literature

Research on electricity prices has garnered the interest of many scholars due to the complexities and extraordinary challenges of achieving high accuracy in forecasting. They have developed and refined numerous methodological approaches to achieve high accuracy and adapt to changes in the electricity market. The number of relevant publications has increased rapidly over the last two decades.

Weron (2014) offers a detailed review of several approaches to forecasting electricity prices, including the following five model classes: multi-agent models, fundamental models, reduced-form models, statistical models, and artificial intelligence models. Previously, Aggarwal et al. (2009) provide an overview of the methods used in electricity price forecasting. However, their focus was on stochastic time-series, causal and artificial intelligence-based models. Weron and Ziel (2019) and Hong et al. (2020) present a general review of and outlook on energy forecasting. The most recent overview of forecasting theory and practice comes from Petropoulos et al. (2022), who provide an overview of a wide range of theoretical models, methods, principles and approaches to preparing, organising and evaluating forecasts. In addition, they provide several real-world examples of how these theoretical concepts are applied.

Many publications conduct time-series analysis based on time-series models, which are particularly suitable for short-term electricity price forecasting. Time series models constitute a special subtype of regression model in which target variables are represented, among other things, by past values of the time series as regressors . They include autoregressive moving-average (ARMA), generalised autoregressive conditional heteroscedastic (GARCH) and Markov regime-switching (MS) models. Steinert and Ziel (2019), for example, develop an auto-regressive model with 24 individual models – one for each hour of the day – that also incorporates electricity futures prices to produce hourly electricity price forecasts. Nowotarski and Weron (2016) refer to the decomposition of values into different components, which is common in time-series analysis, and show that the quality of time-series models benefits greatly from decomposing a set of electricity prices into a long-term seasonal component and a stochastic component, modelling them independently and combining their forecasts. In an extensive study, Ziel and Weron (2018) compare two options for the type of time-series modelling used with high-frequency data sets. They compare models with univariate model frameworks, with one of these models being constructed for the entire time series, featuring models with multivariate model frameworks, in which each hour of a day is modelled separately and independently. This is initiated by the organisation of electricity markets as day-ahead auctions, as in the U.S. or Europe. Their study shows no clear dominance by one framework, suggesting that the combination of both modelling approaches could improve predictive accuracy.

While Steinert and Ziel (2019), Nowotarski and Weron (2016) and Ziel and Weron (2018) focus on day-ahead electricity prices in general, Christensen et al. (2012) use a nonlinear variant of the autoregressive conditional risk model to predict price peaks, treating them collectively as a discrete-time point process, Eichler et al. (2014) an approach based on the autoregressive conditional hazard model, and Manner et al. (2016) the mapping of inter-regional linkages between different electricity markets in a dynamic multivariate binary choice model to predict electricity price spikes. Garcia et al. (2005) develop a GARCH model to predict day-ahead electricity prices, while Hickey et al. (2012) evaluate the accuracy of ARMAX-GARCH models in forecasting short-term prices in the U.S., determining that model choice depends largely on location, horizon and regulation, with asymmetric power auto-regressive conditional heteroskedastic (APARCH) models being more appropriate in deregulated markets and GARCH models being better for regulated markets. Bordignon et al. (2013) develop a linear regression model to account for relationships between prices and various price drivers, using a time-varying parameter (TVR) and an MS model to capture peaks and discontinuities. Other examples of applying MS models include Kosater and Mosler (2006) for the German market and Bierbrauer et al. (2004) for the Nordic market. Notably, in a recent paper, Mari and Mari (2022) uses deep learning-based regime-switching models to predict electricity prices.

Parameter-rich ARX models represent a special type of time-series model. The Lasso estimated autoregressive (LEAR) model introduced by Uniejewski et al. (2016) is further developed by Lago et al. (2021).

To provide a set of best practices for evaluating future model developments in electricity price forecasting and comparing state-of-the-art statistical and deep-learning methods, Lago et al. (2021) define a deep neuronal network (DNN) and a LEAR model based on the latest findings. Together with various evaluation metrics, these models are accessible in a Python toolbox to evaluate new algorithms. Accordingly, we compare our hybrid model with the statistical benchmark model.

Deep-learning models (e.g., artificial neural network (ANN), DNN, long short-term memory (LSTM) network, recurrent neural network (RNN), feed-forward neural network) are used in an increasing share of electricity price forecasts. In addition to the cited benchmark model, Panapakidis and Dagoumas (2016), as an example, study ANNs using different inputs and ANN typologies. These authors characterise such models as having comprehensive functionality and a high degree of flexibility. In their analysis of the impact of different markets on one another, Lago et al. (2018) develop a DNN that considers interconnected markets’ characteristics to boost forecasting accuracy. Notably, they show that predicting the price of two markets simultaneously enhances forecast accuracy. Amjady (2006) develops a fuzzy neuronal network that forecasts hourly electricity prices for the Spanish day-ahead market. Notably, the combination of deep learning and time-series models can be found in the nonlinear autoregressive neural network of Marcjasz et al. (2019).

To compare time-series and neural network models using external regressors, Lehna et al. (2022) use four different forecasting approaches to the German day-ahead electricity market: a seasonal integrated autoregressive moving average ((S)ARIMA(X)) model, an LSTM neural network, a convolutional neural network LSTM (CNN-LSTM) and an extended two-stage multivariate vector autoregressive (VAR) model. While the LSTM model achieves the highest average accuracy, the two-stage VAR model has advantages at shorter prediction horizons. A combination of both methods outperforms each of the individual models in terms of accuracy.

The methods presented so far are fundamentally based on historical day-ahead electricity price time series. Another approach entails using models that simulate the actions of individual market participants (agents). Qussous et al. (2022), for example, developed an agent-based model to derive day-ahead prices and simulate the bidding strategies of market participants. To evaluate their model, they reproduce day-ahead electricity prices in the 2016–2019 German bidding zone. Compared to other techno-economic approaches to short-term electricity price forecasting, this agent-based model achieves the highest accuracy. Consequently, we compare the hybrid model presented in this paper with this model.

Due to their explanatory character in identifying an efficient market outcome and their comprehensive modelling of the entire electricity system, techno-economic energy system models have been employed for the ex-post analysis of electricity prices. Muesgens (2006a) and Borenstein et al. (2002) replicate day-ahead prices to assess the existence of market power in Germany and the U.S., respectively. Keles et al. (2013) investigate on the importance of adequate wind power feed-in time series to obtain better results in electricity price simulation. Hirth (2013) determine the market value of renewables and Sensfuß et al. (2008) quantify the merit order effect computing day-ahead prices. The merit order effect describes the displacement of fossil fuel generation by renewable energy sources due to their lower marginal costs and the subsequent decline in total electricity costs. Pape et al. (2016) analyse to what extent day-ahead and intraday electricity prices can be explained and represented by techno-economic energy system models. Notably, however, they show that this method has significant weaknesses in explaining short-term electricity prices compared to other methods.

In contrast to ex-post analyses of electricity prices, which examine actual prices that have already occurred, this article focuses on ex-ante forecasts. Techno-economic energy system models, used for ex-ante prediction, have the key disadvantage they do not use recent historical prices to benchmark their price estimators. As a result, they may struggle to explain random short-term variations compared to econometric models that "learn from the past". However, energy system models possess an advantage in that they are based on established economic theory and replicate the workings of markets. As such, they are able to predict prices independently of past data and are less prone to structural changes in the market and other similar factors. In line with that, we did not find techno-economic energy system model applications to forecasts for ex-ante predictions of short-term electricity prices. However, there are such uses in ex-ante predictions of long-term electricity prices, where random short-term variations are less inherent (see, e.g., Muesgens, 2020; Green and Vasilakos, 2010; Lamont, 2008). In addition, technical-economic energy system models have been employed in bodies of literature that extend beyond price estimates (e.g., to determine the value of demand response (Misconel et al., 2021; Kirchem et al., 2020), to identify an optimal transmission-expansion plan (van der Weijde and Hobbs, 2012), to support decision-making at the municipal level (Scheller and Bruckner, 2019), to analyse the effect of power-to-gas (Lynch et al., 2019), to evaluate policy instruments to reduce CO2 emissions (Sgarciu et al., 2023)). Additionally, Plaga and Bertsch (2023) thoroughly examines how energy system models can account for climate uncertainty. A comprehensive overview of energy system modelling can be found in Ventosa et al. (2005).

In recent years, hybrid methods have garnered significant attention in electricity price forecasting. Hybrid models are those that combine two or more distinct methods. They aim to use the combined strengths of the employed methods while mitigating their individual weaknesses to achieve better overall results. Many hybrid methods have been developed that combine a wide variety of methods. Aggarwal and Tripathi (2017), for example, present a hybrid approach that uses a wavelet transform, a time-series time-delay neural network and an error-predicting algorithm to predict day-ahead electricity prices in the ISO New England market. Chang et al. (2019) combine an Adam-optimised LSTM neural network to generate electricity prices with a wavelet transform to decompose an electricity price time series into several series of electricity prices. A combination of an empirical wavelet transform, a support vector regression, a bi-directional LSTM and a Bayesian optimisation is proposed by Cheng et al. (2019). Nazar et al. (2018) apply a three-stage hybrid model to the DK2 area of Nordpool and the Spanish power market. The first stage features a wavelet and Kalman machines to decompose price data into different frequency components. The second stage uses an adaptive neuro-fuzzy inference system (ANFIS) to forecast price frequency components. In the third stage, the output of the second stage is fed into the ANFIS to boost forecasting accuracy. A wavelet transform and an ARMA are paired with a kernel-based extreme learning machine by Yang et al. (2017), and with a radial basis function neural network by Olamaee et al. (2016). Zhang et al. (2020) propose a hybrid model based on variational mode decomposition, self-adaptive particle swarm optimisation, SARIMA and a deep belief network for short-term electricity price forecasting.

Most of the hybrid models mentioned above use statistical and deep learning methods. However, a few applications also combine a techno-economic energy system model with another approach. For example, de Marcos et al. (2019) detail a short-term hybrid electricity price forecasting model for the Iberian market that combines a techno-economic cost-generation optimisation model with an ANN. Gonzalez et al. (2012) propose two hybrid approaches based on a techno-economic electricity market model. Focusing on the day-ahead market in the UK, they combine this model type separately with two other models: a linear autoregressive model with exogenous data on price drivers (ARX model) and a nonlinear logistic regression model with a smooth transition (LSTR model), which is a regime change in times of structural change. Their results support the idea of incorporating fundamental information for better price forecasting. Particularly in highly volatile periods, the nonlinear hybrid model achieves better results. In Möbius et al. (2023), our previous study, we introduced a techno-economic market model tailored to the day-ahead market and combined it with a stochastic model to enhance day-ahead load forecast accuracy in the estimation of day-ahead electricity prices. We highlighted the positive effects of better load forecasts on the day-ahead price estimators generated with an energy system model. However, this approach merely represents a first step; it does not fully realise the potential of a hybrid model, which seamlessly integrates the strengths of both the techno-economic and stochastic models.

The literature on electricity price forecasting mostly focuses on developing point forecasting methods for the day-ahead market. However, in recent years, there has been a growing interest in probabilistic forecasting methods (Hong et al., 2020). The Global Energy Forecasting Competition (GEFCom2014) (see Hong et al., 2016) served as a catalyst for this trend, and many studies have been published on this topic in the time since. Nowotarski and Weron (2018) provide a comprehensive overview of the different approaches used in this field. A hybrid model combining point and probabilistic forecasting in four steps was developed by Maciejowska and Nowotarski (2016) for the GEFCom2014.

Common approaches to probabilistic electricity price forecasting include using time-series models, such as ARIMA, GARCH and exponential smoothing (ETS) (e.g., Weron and Misiorek, 2008) and using deep learning models. Bootstrapping is widely used in combination with deep learning approaches (e.g., Chen et al., 2012; Wan et al., 2014; Rafiei et al., 2017; Khosravi et al., 2013). On top of deep learning, Zhao et al. (2008) use a support vector machine (SVM) to estimate prediction intervals and density forecasts, and Zhou et al. (2006) use an extended ARIMA model to do the same. An econometric model for probabilistic forecasting is proposed by Panagiotelis and Smith (2008). Manner et al. (2019) use vine-copula models to forecast quantiles for a vector of day-ahead electricity prices from interconnected electricity markets, while Grothe et al. (2023) propose an approach based on copula techniques that entails generating multivariate probabilistic forecasts by modelling cross-hour dependencies. Considering these dependencies in probabilistic forecasts is uncommon, in contrast to point forecasts. However, including them in the methodology for generating probabilistic price forecasts can enhance forecast accuracy.

Historical simulation and distribution-based prediction intervals are other popular approaches. Historical simulation estimates risk and generates prediction intervals in the simulation of multiple scenarios using historical data; it then uses the results to estimate the probability of different outcomes (e.g., Weron and Misiorek, 2008; Nowotarski and Weron, 2015). Distribution-based prediction intervals are calculated based on the distribution of historical data (e.g., Misiorek et al., 2006; Zhao et al., 2008; Dudek, 2016; Maciejowska et al., 2016; Panagiotelis and Smith, 2008). A theoretical introduction to the generation of prediction intervals based on distribution and historical simulation is provided by Weron (2006).

Quantile regression averaging (QRA) is a method that has risen in prominence recently in probabilistic electricity price forecasting. It combines predictions from multiple quantile regression models, each of which is trained to predict a different quantile of the response variable. This method was first formally introduced by Nowotarski and Weron (2015) and has since continued to be applied and developed further due to its accuracy (e.g., Maciejowska et al., 2016; Nowotarski and Weron, 2014; Marcjasz et al., 2020; Uniejewski et al., 2019; Uniejewski and Weron, 2021).

Despite the rising prominence of probabilistic forecasts in various models, there is still a general lack of approaches that combine probabilistic forecasting with techno-economic energy system models. This paper aims to fill this gap in the literature. By adapting and developing an energy system model specifically for the short-term electricity market and combining this model with common stochastic models through multiple steps, we can leverage the strengths of both models and open up the field of short-term electricity price forecasting for energy system models. Having already highlighted the positive effects of combining a stochastic model (for better load forecasts) with an energy system model (for the day-ahead market, developed by Möbius et al. (2023)), these building blocks are included in the hybrid model. We demonstrate that a multi-layer hybrid model makes point and probabilistic price forecasting with techno-economic and stochastic models possible.

3 Data

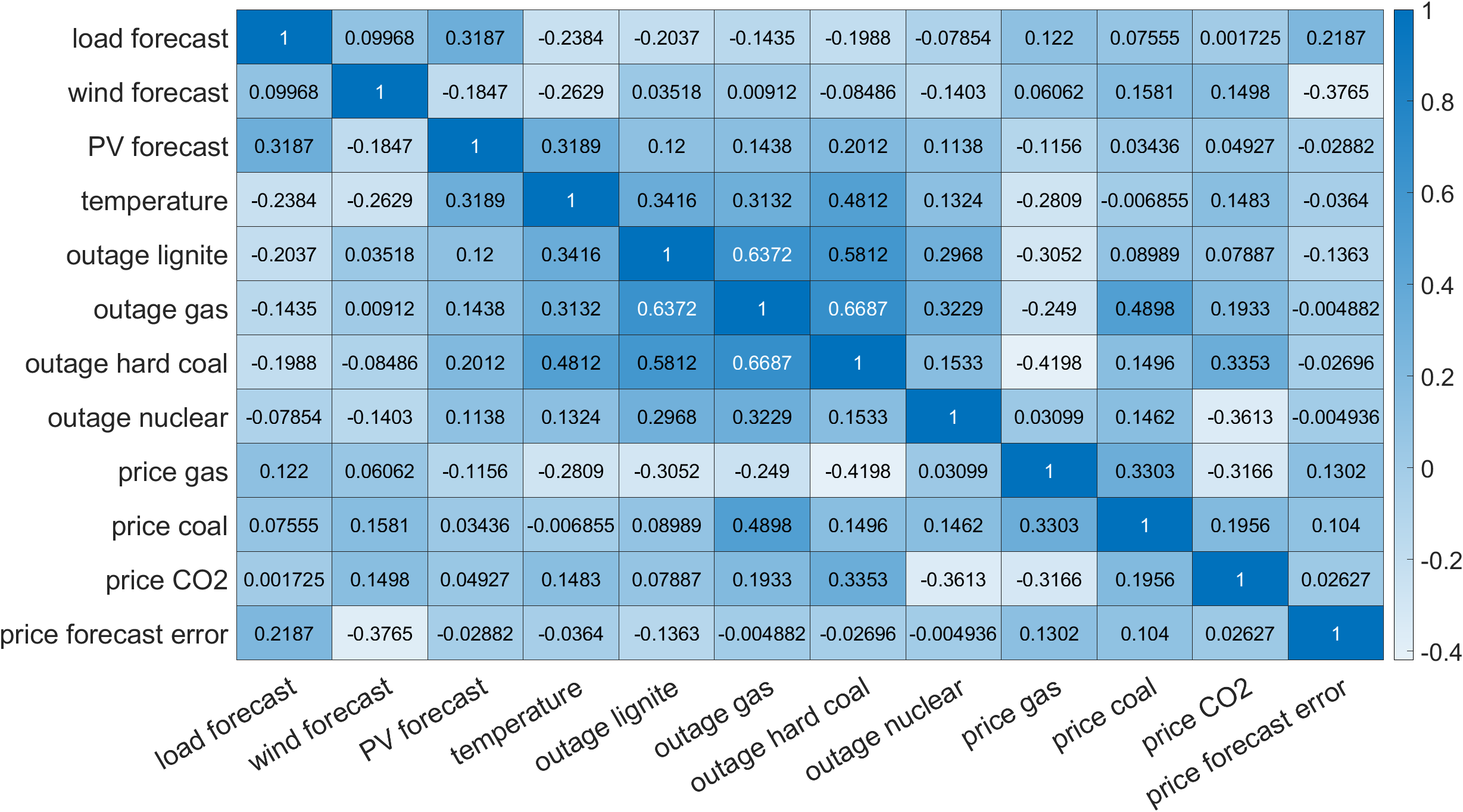

In our study, we develop a hybrid model that integrates stochastic modelling approaches and energy system optimisation to forecast wholesale electricity prices. Notably, this energy system optimisation requires multiple inputs. Table 1 provides an overview of the necessary input data. In this section, we provide more details on how the data is obtained and applied.

| Parameter | Source |

| CO2 prices | Sandbag (2020) |

| Control power procurement | Regelleistung.net (2018) |

| Efficiency of generation capacities | Schröder et al. (2013), |

| Open Power System Data (2020a) | |

| Efficiency losses at partial load | Schröder et al. (2013) |

| Electricity demand (load) | ENTSO-E Transparency Platform (2021a) |

| Energy-power factor (for storages) | own assumption: 9 |

| Fuel prices | Destatis Statistisches Bundesamt (2021), |

| (Lignite, nuclear, coal, gas, oil) | ENTSO-E (2018), ENTSO-E (2018), |

| EEX (2021) | |

| Generation and storage capacity | BNetzA (2021), UBA (2020), EBC (2021), |

| ENTSO-E Transparency Platform (2021b), | |

| Open Power System Data (2020b) | |

| Generation by CHP units | European Commission (2021) |

| Historic electricity generation | ENTSO-E Transparency Platform (2021c) |

| Load shedding costs | own assumption: 3,000 €/MWh |

| Minimum output levels | Schröder et al. (2013) |

| NTCs | ENTSO-E Transparency Platform (2021d), |

| JAO Joint Allocation Office (2021) | |

| Variable O&M costs | Schröder et al. (2013) |

| Power plant outages | ENTSO-E Transparency Platform (2021e) |

| RES feed-in | ENTSO-E Transparency Platform (2021f) |

| RES curtailment costs | own assumption: 20 €/MWh |

| Start-up costs | Schröder et al. (2013) |

| Seasonal availability of hydro power | ENTSO-E Transparency Platform (2021c) |

| Temperature (daily mean) | Open Power System Data (2020a) |

| Water value | ENTSO-E Transparency Platform (2021c), |

| ENTSO-E Transparency Platform (2021g) |

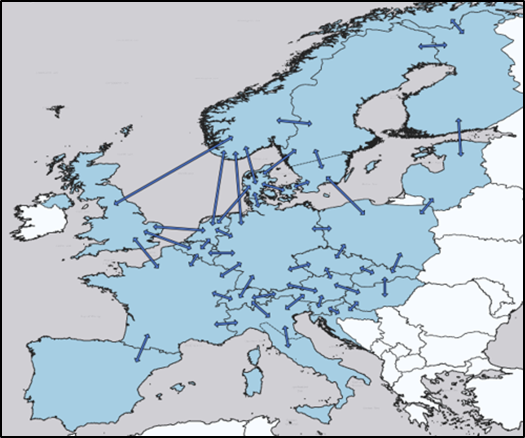

Although our modelling approach can be applied to many markets, our empirical exercise focuses exclusively on the German spot market. However, the high level of integration among European electricity markets and the resulting interdependencies require a comprehensive representation of these markets, particularly during the energy system optimisation step. Figure 2 shows the geographical scope of the collected data and the interconnection among European markets. We consider the bidding zones of most of the EU’s 27 member states111Bulgaria, Cyprus, Greece, Iceland, Ireland, Malta and Romania are omitted. as well as Norway, Switzerland and the United Kingdom.222Note that we aggregate the bidding zones of Spain and Portugal to a single ‘Iberian’ market and the bidding zones of Lithuania, Estonia and Latvia to a single ‘Baltic’ market. Additionally, note that we consider the distinct bidding zones within countries. However, we aggregate the following zones: in Norway, zones NO1–NO5; in Sweden, zones SE1–SE3; and in Italy, all zones but IT-North. Unless stated otherwise, the collected data is from 2016 to 2020.

Electricity demand is represented by hourly values for the system’s electrical load, of which both a day-ahead forecast and the actual values are published by the respective transmission system operators (TSOs) and provided by ENTSO-E Transparency Platform (2021a). The collected load data for the Germany-Luxembourg bidding zone represents 2015–2020. In energy system models, electricity demand is usually considered volatile and inflexible in the short term. However, there is typically an option to shed load amid supply scarcity. In our application, we assume the cost of load shedding to be 3,000 €/MWh, as this was the maximum bidding price prior to September 2022333The maximum bidding price was increased to 4,000 €/MWh on 20 September 2022..

The availability of intermittent renewable energy, namely onshore wind, offshore wind and photovoltaics (PV), depends on meteorological conditions and varies from hour to hour. The feed-in data of these energy sources are provided as hourly day-ahead forecasts by ENTSO-E Transparency Platform (2021f). Despite weather dependency, renewable energy electricity generation can still be intentionally curtailed. Acknowledging the various support schemes for renewable generation in Germany and Europe, which prevent renewable sources from being shut down immediately when negative prices occur, this study assumes a curtailment cost of 20 €.

For conventional thermal generation, we distinguish between ten technologies and divide further by age if their technical parameters (especially those that impact efficiency) have changed significantly over time. We use 30 capacity clusters to group power plants based on technology and date of commissioning. We derive technology- and age-based efficiencies from Open Power System Data (2020b) data and assign them to the corresponding capacity clusters.

Moreover, we assign the clusters minimum output levels and efficiency losses in part-load operations based on Schröder et al. (2013). Hence, supply that follows fluctuations in demand and renewables is incentivised to shut down due to physical barriers (minimum output levels) and economic incentives (efficiency losses). The capacity, fuel type, generation technology and date of commissioning for units in the German market are derived from BNetzA (2021), UBA (2020) and Open Power System Data (2020b). For the remaining markets considered in our study, we use data from ENTSO-E Transparency Platform (2021b), Open Power System Data (2020b) and EBC (2021).

Power plant efficiency and the costs of fuel and CO2 emissions form the variable generation costs of conventional thermal technologies. For fuel costs, we apply daily gas prices that are provided by EEX (2021), monthly coal prices taken from Destatis Statistisches Bundesamt (2021) and monthly oil prices from Destatis Statistisches Bundesamt (2021). Fuel costs for nuclear and lignite are derived from ENTSO-E (2018) and are assumed not to vary over the time horizon of our study. Prices for CO2 certificates are taken as weekly data from Sandbag (2020).

Due to the time and additional fuel used by power plants to heat up during a start-up process, fuel and CO2 prices also impact the cost of starting up a power plant. Further data regarding start-ups (e.g., secondary fuel usage, depreciation) are derived from Schröder et al. (2013).

Electricity generation relies on both the installed capacity and technical availability of power plants. As a result, we consider all scheduled and unscheduled outages that were known before the closure of the day-ahead market. Information on hourly outages is obtained from ENTSO-E Transparency Platform (2021e).

In most electricity markets, combined heat and power (CHP) plants are used, where electricity generation and heat supply are interconnected and reliant on each other. To account for this relationship, we apply a must-run condition to all CHP units to ensure operation at a minimum output level, as defined by the heat demand. These output levels are established in two steps. First, we calculate an hourly heat-demand factor consisting of temperature-dependent (spatial heating) and temperature-independent (warm water and process heat) components. The temperature-driven heat demand is calculated using heating degree days derived by mean temperature data obtained from Open Power System Data (2020a), while the temperature-independent heat demand is obtained from hourly and daily consumption patterns provided by Hellwig (2003). Second, we allocate annual electricity generation volumes from CHP plants to each hour of the year based on the hourly heat-demand factor. The data on annual technology-specific electricity generation from CHP units is sourced from European Commission (2021).

Control power is essential for system operators to ensure frequency stability at all times. The day-ahead market is affected by the market for control power provision, meaning that the capacities reserved for control power cannot be placed on the day-ahead market. The amount of control power to be procured is an average of the tender results taken from Regelleistung.net (2018).

In addition to conventional thermal technologies and intermittent renewables, we consider waste, biomass, energy storage, hydro-reservoirs and run-of-river hydroelectricity. Since the operation of both waste and biomass has largely been historically constant (compare with ENTSO-E Transparency Platform (2021c)), we implement both technologies as base-load.

The energy storage units are divided into high capacity-to-energy ratios and low capacity-to-energy ratios. Storage units with high capacity-to-energy ratios actively charge and discharge. We exclusively consider a subset of pumped storage plants (PSPs) in this group. The overall turbine capacity of these PSPs is detailed by ENTSO-E Transparency Platform (2021b), and the efficiency of a storage cycle is around 75 % (Schröder et al., 2013). For these PSPs, we assume a capacity-to-energy ratio of 1/9 (see DENA, 2010). This means that the plant can generate electricity at full load for nine hours before its storage is emptied. Storage units with low capacity-to-energy ratios comprise long-term PSPs as well as hydro-reservoirs. They are assigned a variable generation cost in the model (i.e., an opportunity cost for water consumption). Using historical electricity prices from ENTSO-E Transparency Platform (2021g) and the observed generation and pumping activities in the respective hour from ENTSO-E Transparency Platform (2021c), we construct a step-wise merit order for long-term PSPs and hydro-reservoirs. Run-of-river and high-capacity-to-energy PSPs are assigned a monthly availability factor derived from the historical generation data from ENTSO-E Transparency Platform (2021c). We assume that 70 % of pump storage capacity belongs to high-capacity-to-energy PSPs, while the remaining 30 % of pump storage capacity belongs to low-capacity-to-energy PSPs.

European electricity markets are highly interconnected through cross-border transmission capacities. Thus, the German electricity market is also integrated into the European electricity system, with a total interconnector capacity of 27 GW, representing more than 30 % of the German peak load.444Note that the availability of the interconnectors depends on various factors (e.g., congestion within a market zone). Annual aggregated exports, accounting for approximately 13 % of German consumption in 2019, and imports, making up around 7 % of consumption in the same year, are both significant. In our energy system model, net transfer capacities (NTCs) constrain transmission between market zones. We implement hourly day-ahead forecasts for NTCs that are made available by ENTSO-E Transparency Platform (2021d) and JAO Joint Allocation Office (2021).

4 Methodology

The implementation of the entire hybrid model is open-source; all data we could make public are available on GitHub at the following link: https://github.com/ProKoMoProject/A-hybrid-model-for-day-ahead-electricity-price-forecasting-combining-fundamental-and-stochastic-mod.

In this section, we present the components of the hybrid model, starting with the methodologies for the data pre-processing and parameter density forecast steps in Sections 4.1 and 4.2. Next, we introduce the dispatch market model used to generate the first price estimators in the energy system optimisation step in Section 4.3. Finally, we detail the model for the stochastic post-processing step in Section 4.4.

4.1 Stochastic Data Pre-Processing Step

Modelling the electricity market with a dispatch model requires an understanding of the several various fundamental variables, including demand (represented by load), which is a crucial element. The TSOs provide the actual load and a day-ahead load forecast, which has the potential to be improved, as demonstrated by, for example, Maciejowska et al. (2021) and Möbius et al. (2023). To enhance this forecast, we use a stochastic model for data pre-processing. Additionally, we model a two-day-ahead load forecast to capture power plant start-ups and shutdowns based on the load of the second following day, using the TSOs’ day-ahead load forecast as a starting point.

Day-Ahead Load Forecast

We use the approach initially presented in Möbius et al. (2023) to improve load forecasting. Thus, we occasionally refer to it for detailed specifications and analyses. We propose a purely endogenous time-series approach: a model for the TSOs’ load forecast error that depends only on past values of the forecast error itself and, in turn, on the TSOs’ load forecast . The forecast error is the difference between the actual load data and the TSOs’ load forecast . Designing a model for the error and forecasting it enables us to improve the TSOs’ load prediction. The resulting load prediction at time is given by the following equation:

| (1) |

where is our forecasted TSOs’ load prediction error. Thus, is an improved load forecast in which we adjust the original forecast for the predictable structure of its error. The sub-index denotes consecutive hours.

To model and forecast the forecast error , we use a decomposition model and decompose the error time series into the sum of a seasonal component and a stochastic component (see Lütkepohl (2005); Hyndman and Athanasopoulos (2021); Box et al. (2015) for comprehensive introductions to time series models):

| (2) |

where is a seasonal and is the remaining, stochastic component at time .

Capturing a weekly season, the seasonal component for time is defined by Eq. (3) with being the average of TSOs’ forecast errors for hour and day (Monday), …, (Sunday) and , describing dummy variables to address the hour of the day and the day of the week:

| (3) |

with

| (4) |

For the residual component of the time series, we propose an econometric SARMA x model given by the following equation:

| (5) | ||||

where the innovations are assumed to be homoscedastic and normally distributed. This model contains an additional 24-hour seasonal component, making it stochastic, flexible and dependent on the values of past hours and days. In contrast, describes a static seasonality.

The model is estimated over a calibration window of one year. Within the hybrid model, the window is constantly rolled over by full days, with the forecast of the next day’s 24 hours being made recursively. If no actual data are available due to time points in the future, we use forecast values for the model variables.

Two-Day-Ahead Load Forecast

Power plants make operational start-up and shut-down decisions based on the current day’s demand, the demand from the day before and the expected demand on the next day. To account for this in the dispatch model, a forecast of load consumption is needed two days in advance. We use the modelling and forecast of the current load (meaning the TSOs’ day-ahead load forecast ) as a starting point from which to forecast the day-ahead forecast for the second following day, resulting in a two-day-ahead forecast .

For the model, we propose an econometric SARMA x model with an additional exogenous variable, the TSOs’ load forecast at lag 168:

| (6) | ||||

The model’s innovations are assumed to be homoscedastic and normally distributed, meaning that . The model features 24-hour seasonality. Since we also observe weekly seasonality, we include the TSOs’ load forecast at the same hour one week earlier, , as a regressor.

We calibrate and estimate the model based on window length , which contains one year of historical data. The estimated model is used to recursively (i.e., on an hourly basis) predict the values of each hour of the next day. Since we rely on an autoregressive time-series model, day-ahead load forecasts from 168 hours to one hour before the predicted hour are in the model as explanatory variables for the two-day-ahead prediction. However, this means that some values are unavailable when the forecast is made. They are replaced with recursively forecasted values based on the most recently available observations.

Given the increased uncertainty associated with forecasting two days ahead, our hybrid model incorporates a parameter density forecast that considers various scenarios for the level and development of load, utilising the hourly two-day-ahead load forecast as an input variable.

4.2 Parameter Density Forecast Step

To account for uncertainty in two-day-ahead load predictions, scenarios are calculated at the 5 % and 95 % quantiles using QRA. It describes a method for determining quantiles of predictive cumulative distribution functions, which can then be used to construct prediction intervals. A prediction interval is calculated using the -th and -th quantile of the predictive cumulative distribution function, , as the lower and upper bound of the interval. QRA is based on quantile regression and aims to model quantiles of real-valued variables that depend on explanatory variables (see, e.g., Koenker and Bassett, 1978). It employs point predictions to explain the -th quantile of the conditional distribution of the observation, setting a fixed . Here, quantile regression uses a vector of regressors , including a value of one for the intercept and the two-day-ahead point prediction for the load at given time , to calculate the two-day-ahead load prediction in the -th quantile () (conditional on additional information):

| (7) |

Thereby, is a vector of parameters for the -th quantile. QRA estimates and, thus, the -th quantile by minimising the pinball loss function of the respective -th quantile, given by

| (8) |

where 1 is the indicator function (see, e.g., Nowotarski and Weron, 2015, 2018).

We use the two-day-ahead load prediction and the corresponding load from a one-year historical period to estimate the unknown parameter . After calculating the 5 % and 95 % quantiles, the scenarios cover 90 % of possible load forecast values with . With the parameter density forecast and the point forecast of expected value, this approach provides three possible scenarios for the two-day-ahead load: an expected scenario, described with the two-day-ahead load forecast, a low scenario described with the hourly estimated 5 % quantile, and a high scenario described with the hourly estimated 95 % quantile. Motivated by optimal integration rules in Grothe (2013) (and setting , as recommended in that work), we weight the expected value with and each quantile with to include the scenarios in the em.power dispatch model described below.

4.3 Energy System Optimisation Step

This section presents the energy system model em.power dispatch, which generates wholesale day-ahead price estimators in the hybrid model’s energy system optimisation step. The model considers a detailed representation of the key techno-economic aspects of an integrated European electricity sector, including transmission restrictions between markets, electricity production by CHPs, energy storage and control power provision. For all considered market zones, our model determines the optimal dispatch decisions for various generation and storage technologies, the most effective use of cross-border transmission capacities and the short-run marginal system costs555Technically, the dual variable of demand constraint derives the short-run marginal system cost, also called the ‘shadow price’., which determine the price estimator for the day-ahead market in hourly resolution.

Since our research focuses on day-ahead price forecasts, the energy system model is developed to reflect the level and quality of information available to market participants on the day before delivery. The model is formulated as a linear optimisation problem minimising total system costs. Ensuring the linear formulation of a highly complex system, we form capacity clusters, parameterising them as described in Section 3. Within each capacity cluster, capacity units can be started up, and electricity can be produced in marginal increments (see Muesgens, 2006b). This approach has two key advantages. First, it reduces computational requirements. Second, the problem is differentiable at each point, and the dual variable of the demand constraint can be interpreted as a wholesale market price estimator. Additionally, the accuracy of modelling large energy systems remains reasonably high for our purpose (Muesgens and Neuhoff, 2006).

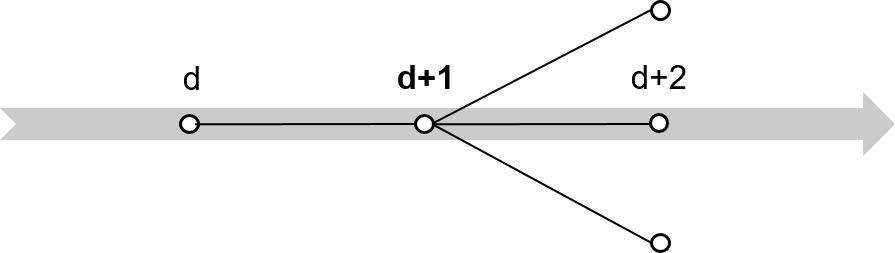

We implement the resultant imperfect forecasts with two model features. First, we implement a rolling window approach that repeatedly solves three days (), as shown in Figure 3. In this setting, the 24 hours of the target day are represented by the second day of the horizon (). This follows the EPEX spot market organisation, in which 24 hourly day-ahead prices are determined at 12 p.m. on the day before delivery (). In addition to the target day d+1, we include the day before () and the day after (). By considering three days in our rolling window, we reduce the problems of starting and ending values, particularly those stemming from power plant start-ups and pump storage plants. Second, we account for the increased uncertainty of the two-day-ahead estimate of key parameters. While parameters for the day are fully known, and forecasts for are made available by the European network transmission system operators for electricity (Entso-e), the realisation of key input parameters exhibits higher uncertainty in . Therefore, we implement probabilistic forecast intervals only in , as shown in Figure 3. All other days are provided through one scenario. The resulting stochastic rolling window is then repeatedly solved using only data available to market participants when they need to make their decisions. In each model run, we extract the information for the 24 hours of our ‘target day’ – the day ahead.

The optimisation problem is repeatedly solved each day. For the reader’s convenience, we provide a nomenclature in the appendix. Note that all endogenous variables are written in upper case, and all exogenous parameters are written in lower case.

The objective function in Eq. (9) minimises total system costs () consisting of the expected value of all operational costs () across all three days of a rolling window . Our empirical exercise considers three scenarios to be equally likely to appear.

| (9) |

The operational costs in Eq. (10) contain all of the short-term costs that generation units face. We include costs at full-load operation (), additional costs for units that operate at partial load () and start-up costs (). Note that we apply a linear unit commitment formulation and that all units must produce at least a certain minimum output level (see Eqs. (12) – (16)). Additionally, we account for load-shedding costs () and penalty payments for curtailing renewables (), as discussed in Section 3.

| (10) | ||||

As we apply our model with a rolling window, each model run considers three days with 24 hours each day, meaning 72 hours per daily model run. Modelling an additional day before and after the target day seems appropriate for storage units operated on a daily cycle. However, storage units (both PSPs and seasonal storage units without pumps) have a storage cycle longer than three days. Therefore, PSPs are divided into low-capacity-to-energy storage, which operates storage cycles longer than three days, and high-capacity-to-energy storage operating one or more storage cycles within a three-day horizon. The dispatch of the latter is determined endogenously. Low-capacity-to-energy PSPs are assigned a water value () that is implemented as a variable cost factor for electricity generation () and electricity consumption ().

Moving beyond pumped storage plants, hydro reservoirs have a natural water feed-in and do not have pumps installed. However, the water budget for electricity generation is limited by seasonal inflow volumes. We also apply a water value () to account for the opportunity costs of electricity generation from hydro reservoirs ().

Market clearing is ensured by Eq. (11). For all 72 hours of the given rolling window, demand () must equal the sum of generation (), load shedding () and electricity imports () minus the electricity consumption of mid-term energy storage () and long-term energy storage () as well as electricity exports (). The dual variable of the demand constraint Eq. (11) is used as an hourly day-ahead wholesale electricity price estimator.

| (11) | ||||

Note that we apply the improved point forecast for the load created in Section 4.1 to Germany in d and d+1, as we focus on price predictions for the German market. For all other markets, we implement the original Entso-e forecasts. For d+2 in Germany, we apply the probabilistic load forecast presented in Section 4.2. For the remaining markets, we use the actual realisation of the previous week as a more naive estimator.

Electricity generation by a capacity cluster is limited by upper and lower bounds. The upper bound is formalised in Eq. (12). It ensures that electricity generation does not exceed the running capacity () in the cluster. The potential to generate electricity by running capacity is further limited by the reserve for positive control power provision ( and ). The lower bound is presented in Eq. (13). It states that running capacities must operate at a minimum power level, including the capacity reserved for negative control power provision ( and ). Note that primary control power provision () in Germany is symmetrical (i.e., a unit must provide both positive and negative primary control power). Different positive and negative control power products were introduced for secondary control power. We do not include minute reserve requirements in the model for two reasons. First, fast-reacting units (e.g., hydro, open-cycle gas turbines) can be started up to provide positive minute reserve without being dispatched. Second, both positive and negative reserves can be provided by multiple market players other than the power plants included in the model (e.g., demand flexibility, P2X units, emergency power generators). The hours that belong to bidding blocks are mapped for primary control power by and for secondary control power by .

| (12) | |||

| (13) | |||

The installed capacity limits the running capacity of a power system () in combination with either the availability factor () or power plant outages (), as shown in Eq. (14). For thermal generation capacities, we use hourly power plant outages. Renewables are provided with an hourly availability factor, while hydroelectric units are provided with a monthly availability factor.

| (14) |

Eq. (15) tracks start-up activities () that increase running capacity from one hour to another. Due to the non-negativity condition, start-ups are either positive or zero. Eq. (16) tracks start-up activities from the last hour of a day to the first hour of the following day.

| (15) |

| (16) |

The difference between available feed-in from intermittent renewables and their actual generation defines the curtailment of renewables, as shown in Eq. (17):

| (17) | ||||

Some power plants are active in both the heat market and the electricity market. Thus, the model implements a must-run condition for such units on the electricity market, which varies over time (e.g., higher in the winter season due to space heating). Depending on hourly heat demand, Eq. (18) states that the output of a combined heat and power unit is at least equal to the electricity generation linked to the heat production ():

| (18) |

Eq. 19 constrains cross-border electricity transfer () via net transfer capacity ():

| (19) |

Eq. (20) describes the state of the storage level of mid-term storage units. A storage level decreases with electricity generation () and increases with charging (). The efficiency of an entire storage cycle () is assigned to the charging process. Eq. (21) ensures the functionality of the storage mechanism between two days:

| (20) | ||||

| (21) | ||||

The maximum energy storage capacity () of storage units with high capacity-to-energy ratios is defined by their maximum installed turbine capacity divided by their capacity-to-energy ratio (), as shown in Eq. (22):

| (22) |

Eq. (23) restricts both turbine capacity and pumping capacity, with pumping capacity assumed to be 10 % lower than the turbine capacity:

| (23) | ||||

At the beginning and at the end of each model run, all storage units with high capacity-to-energy ratios must be filled with at least 30 % of their energy level:

| (24) |

| (25) |

Storage plants with low capacity-to-energy ratios are not subject to a storage mechanism. However, these units’ electricity generation and consumption are restricted to their installed capacity by:

| (26) |

Eqs. (27), (28) and (29) ensure the control power provision for primary, positive secondary and negative secondary control power.

| (27) |

| (28) |

| (29) |

The non-negativity constraint ensures that the individual variables do not show negative values and is given by:

| (30) | ||||

4.4 Stochastic Data Post-Processing Step

In this step, we use a stochastic post-processing technique to refine the estimators produced by the techno-economic energy system model. Specifically, we forecast the errors of the day-ahead price estimators obtained from the energy system optimisation step, either by a time series based point forecast or by inferring the forecast errors distribution functions to generate probabilistic day-ahead price predictions. We incorporate exogenous variables such as renewable energy feed-in and weather, as well as lags of the forecast error itself into the time-series forecast of .

We start with the improved point prediction at time which is given by the following equation:

| (31) |

where is the price prediction from the last step, and is our model’s forecasted price prediction error. Thus, constitutes an improved price forecast in which we adjust the forecast from the last step for the stochastic but predictable structure in its error.

We employ two model frameworks – univariate and multivariate – as this approach has been proven to be useful in past research Ziel and Weron (2018). In the univariate framework, we interpret the forecast error time series as one high-frequency time series in an hourly resolution. In the multivariate framework, we split the time series into 24 individual time series, one for each hour, making them in a daily resolution.

For the post-processing setup, subindexes will denote hours one through 24 of day , with being consecutive days. So, , for instance, is the actual day-ahead price of the first hour of the first day of the considered period, and is the error of the price estimator of the fifth hour of the 432nd day. This fits best because it enables us to observe a realisation of 24 prices for the hours of the next day simultaneously for electricity prices. Please note that if were equal to or less than zero, we would need to shift one day backwards. Likewise, if were greater than 24, we would need to shift one day forward.

We chose a standard econometric time-series model for the univariate framework. It consists of endogenous (i.e., autoregressive with moving average structures) and exogenous variables, all of which are integrated into a regression model given by Eq. (32). To address several seasonal structures included in the time series of the prices’ forecast errors , we use the first and second observation backwards as well as the first back error of the estimated model. Additionally, we use the observation one day before (daily structure) and one week before (weekly structure) as endogenous explanatory variables. Considering daily effects, we include the minimum and maximum forecast errors for the day before . To account for the strong effects of forecast errors on public holidays, we use a dummy variable for public holidays as another factor. Additionally, we include an hourly wind forecast .

| (32) | ||||

As in the univariate framework, we use the well-known time-series model ARX in the multivariate framework. However, the autoregressive component refers to values of the same hour on previous days. The endogenous variables, and , are the forecast errors at the same hour one day prior and seven days prior, respectively. The exogenous variables are the same as in the univariate framework: minimum and maximum forecast errors for the day before, a dummy variable for public holidays and an hourly wind forecast. Thus, the model for the multivariate framework is given by the following equation:

| (33) | ||||

where describes the coefficients that need to be estimated. The innovations are assumed to be homoscedastic and normally distributed in both frameworks, meaning that .

Since we rely on an autoregressive time-series model, we need day-ahead spot prices from the last hours before prediction time as explanatory variables. In the multivariate framework, only one step into the future is forecasted at a time due to the separate modelling of each hour. In the univariate framework, 24 values are forecast for the future, with the hours of the next day predicted recursively (i.e., on an hour-by-hour basis). Unavailable variables are replaced with recursively forecasted variables based on the most recent available observations.

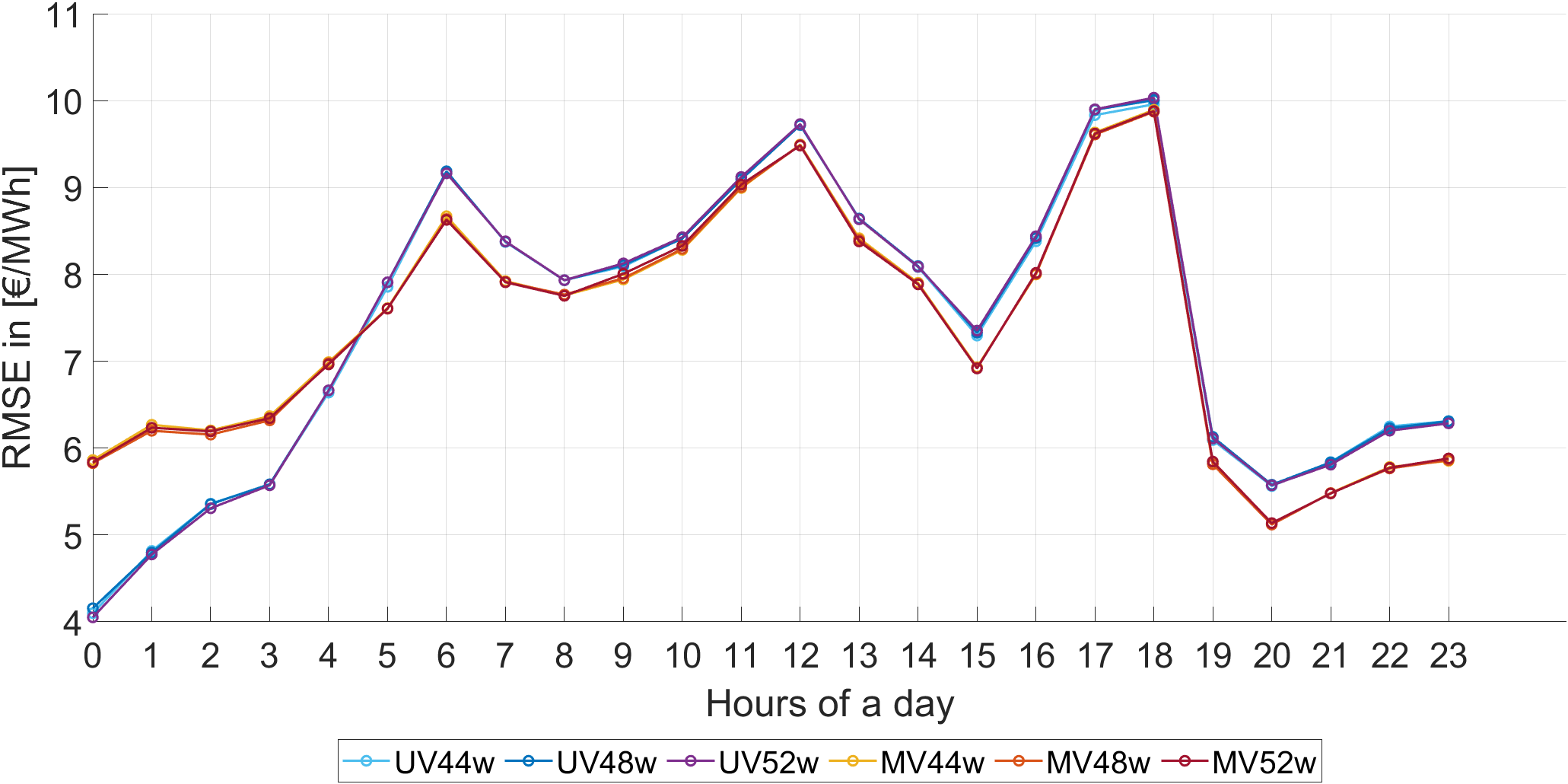

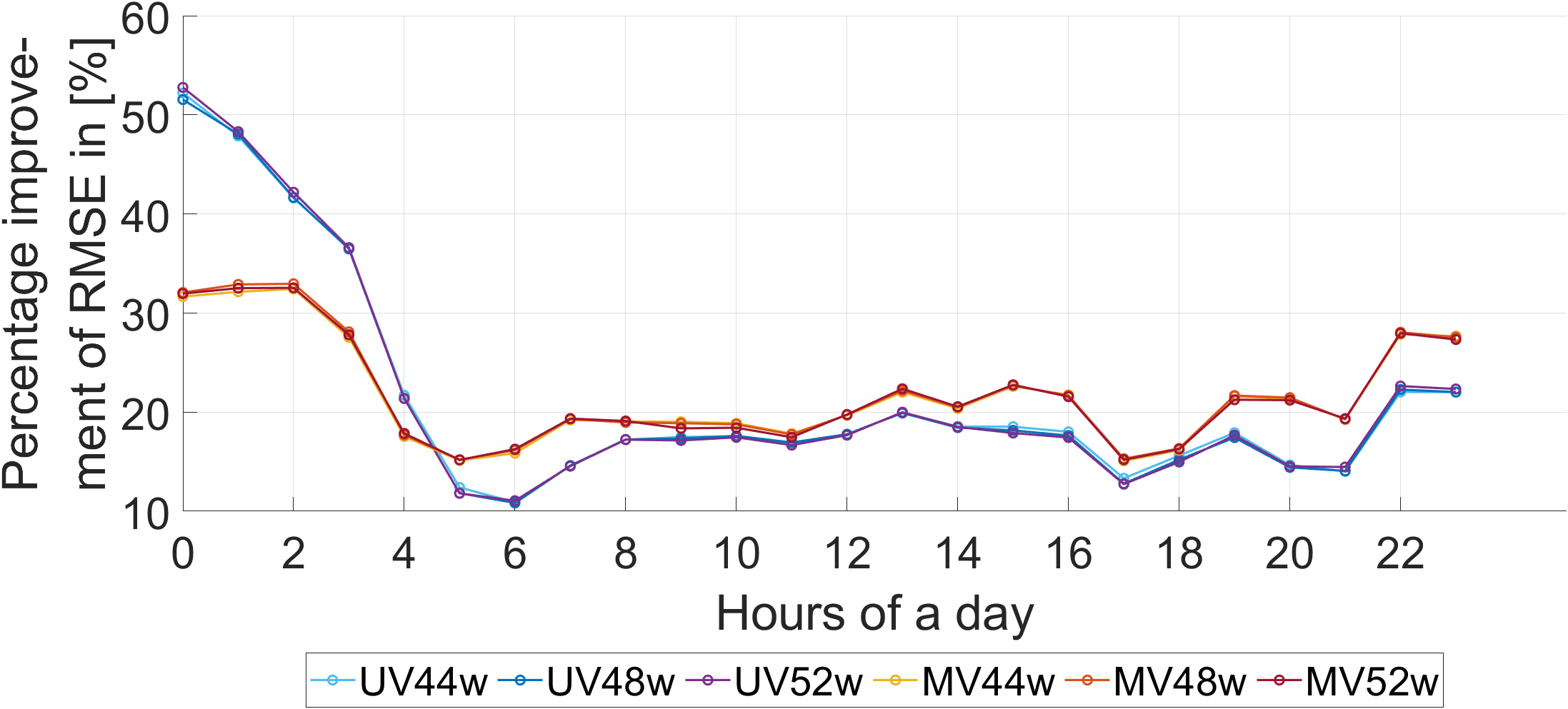

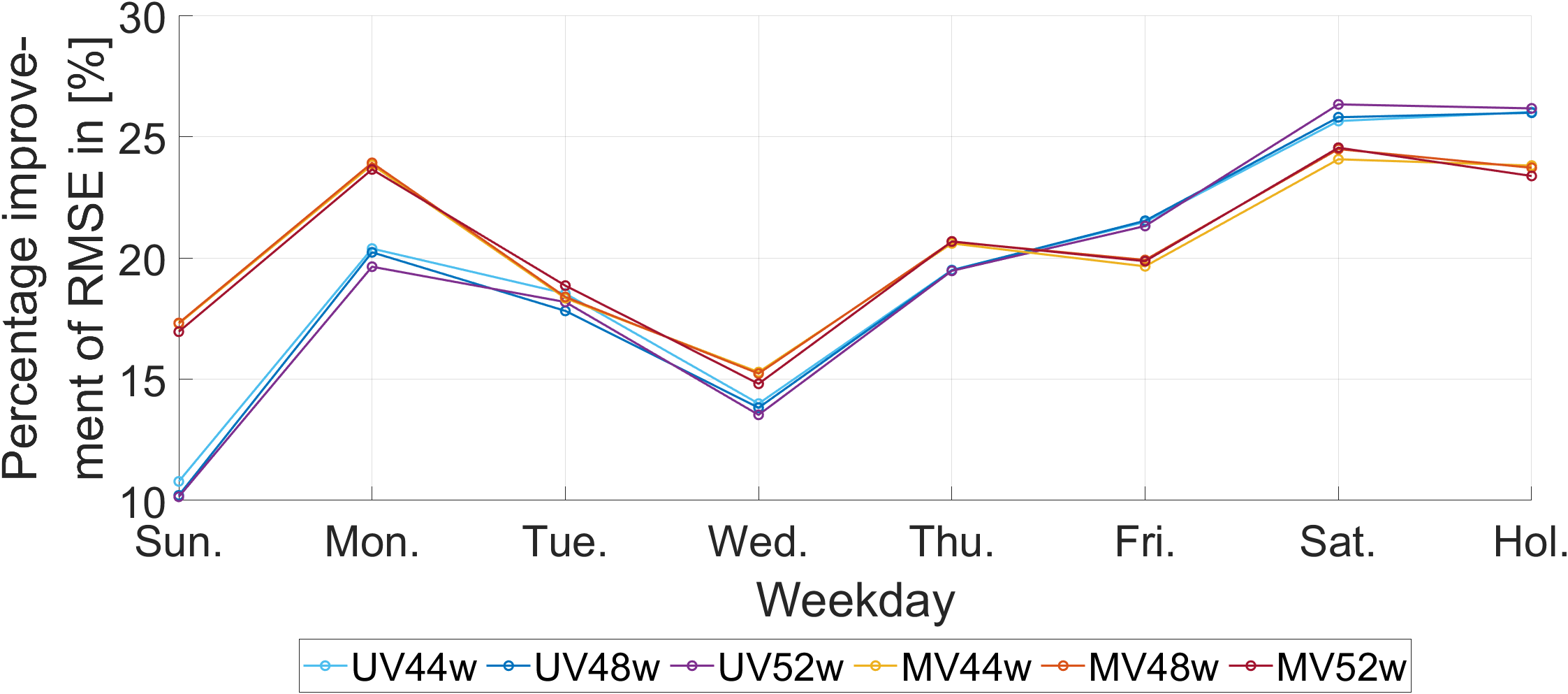

In line with approaches previously shown to be effective in the literature (see, e.g., Marcjasz et al., 2018), we vary the presented post-processing models by using different window lengths to estimate the model set-up and prevent random choice. We determine the calibration window for 44, 48 and 52 weeks. By using three window lengths and two model frameworks, we end up with six individual sub-models. These sub-models are used to predict the values of the hours of the next day , and we denote them by

Our final improved point forecast is obtained by taking the arithmetic average of the six prices. Despite the potential appeal of using seemingly more sophisticated methods, such as calculating optimal weights via linear regression based on past data, these methods resulted in predictors with higher root mean squared errors (RMSE) and mean absolute errors (MAE), even when we used rolling windows that look into the future. This is mainly due to the additional estimation noise that is introduced when using such methods and may lead to inefficiencies as discussed, e.g., in the context of financial literature in DeMiguel et al. (2009). As a result, we stick with the simpler, yet more robust method of averaging the six individual forecasts.

We now move on to generating probabilistic day-ahead price predictions. To achieve this, we use the six forecasts generated by the individual sub-models to estimate the cumulative distribution function of the day-ahead prices. The estimated function serves as our probabilistic forecast for the price of the next day. We represent the distribution in terms of its quantiles. Specifically, we employ quantile regression to model the conditional -th quantile of the cumulative distribution function of the day-ahead prices, where is a value between 0 and 1. This modelling is accomplished by utilising the six individual point predictions and the following equation:

| (34) |

where is the vector of regressors containing a value of 1 for the intercept and the six individual point predictions for the day-ahead price at time . is again estimated by minimising the pinball loss function. To determine the predictive distribution, we forecast multiple quantiles of the distribution.

The coefficients of the regressors are estimated by a calibration window of one year with a distinction made between peak and off-peak hours. Peak hours are defined as those between 8 a.m. and 8 p.m. from Monday to Friday, while off-peak hours are all remaining hours. This distinction is made because peak hours are characterised by high demand for electricity and, therefore, often exhibit higher day-ahead prices. For each quantile , we estimate two parameter vectors (see Eq. (8)). Estimating one parameter vector for all day hours proved to be less accurate. Additional information on this matter can be provided upon request.

In summary, our hybrid model includes the following steps. To predict the next day, we first enhance the TSO’s day-ahead load forecast and predict the two-day-ahead load forecast in the stochastic data pre-processing step. We then calculate the two-day-ahead load scenarios in the parameter density forecast step and include them in the em.power dispatch in the energy system optimisation step to generate the first price estimators for the day-ahead spot market. Finally, in the final stochastic post-processing step, we improve these price estimators with stochastic methods and conduct probabilistic price forecasts. This sequence is repeated continuously, day by day, for all points in time in our observation period. The hybrid model’s rolling window approach means that we always use the most up-to-date available data.

5 Hybrid Model Results

In this section, we present the electricity price forecasts of our hybrid model for Germany from January 2016 to December 2020666More precisely, prices cover the German-Austria-Luxembourg bidding zone from January 2016 to September 2018 and the German-Luxembourg bidding zone from October 2018 to December 2020.. Since the day-ahead market is organised in an hourly resolution, our hybrid model calculates point and probabilistic forecasts for each hour of the following day. As the central point of this paper, we present the overall results of the model (i.e., the point and probabilistic price predictions) and qualitatively detail their place in the literature.

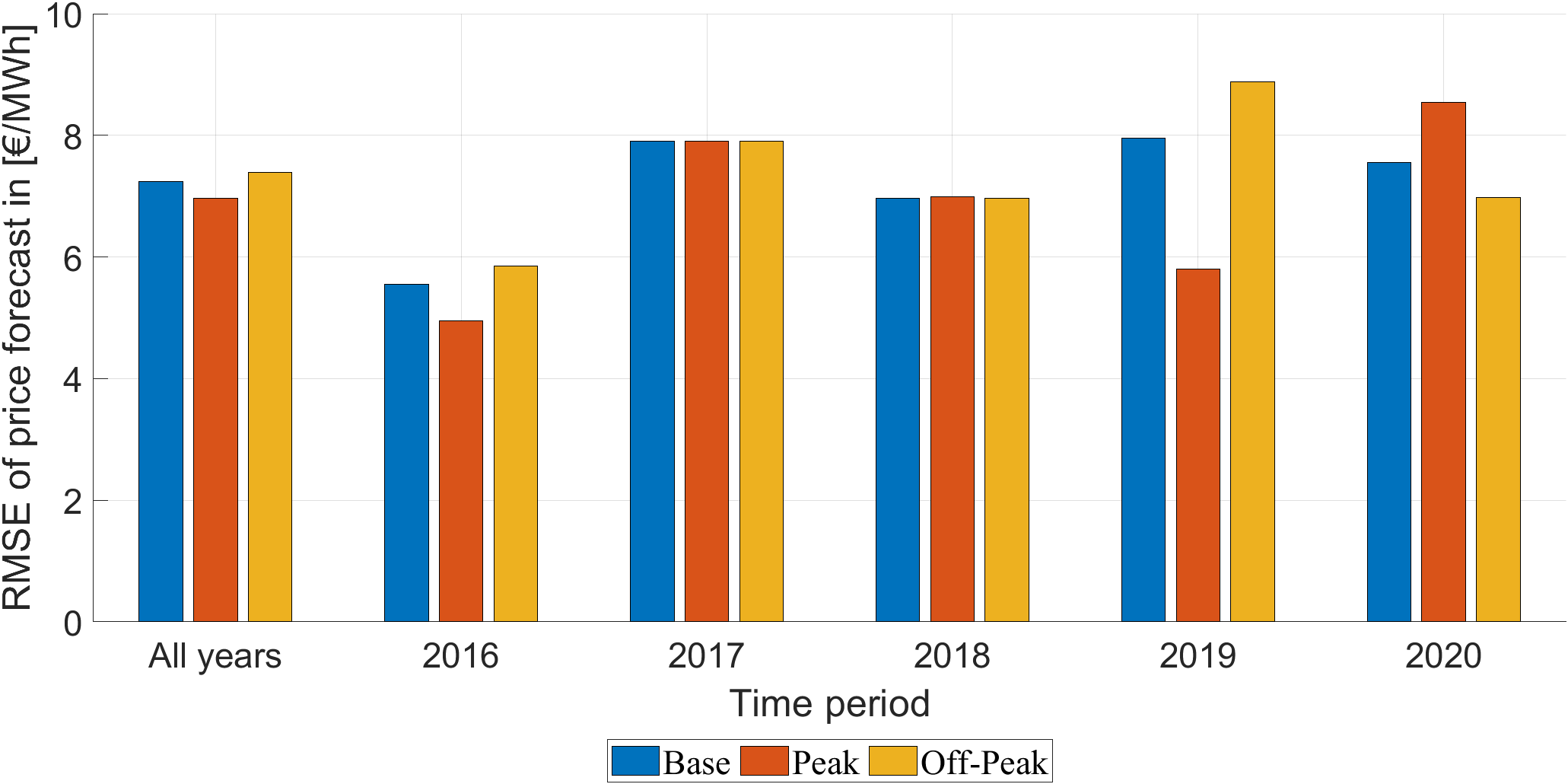

We start by comparing the point forecasts of our hybrid model to those in the literature. With an annual average RMSE of 7.38 €/MWh and MAE of 4.60 €/MWh over the five years from 2016 to 2020, our model aligns well with previous studies. An expert model developed by Ziel and Weron (2018) forecasted electricity prices with an overall MAE of 5.01 €/MWh for 2012 to 2016. Using an autoregressive model with exogenous variables, Maciejowska et al. (2021) achieved an RMSE of 8.43 €/MWh and MAE of 5.92 €/MWh for 2016 to 2019. For the same period, Qussous et al. (2022) obtained an RMSE of 11.21 €/MWh and MAE of 7.89 €/MWh, presenting an agent-based power market-simulation model with rule-based bidding strategies and, thus, a non-equilibrium-oriented techno-economic market model aimed at reproducing day-ahead electricity prices. Since they provided extensive information on the error measures, we can use these models for a detailed comparison. However, as the time periods in these studies are overlapping with but not identical to our observation period, we also perform a detailed comparison with the LEAR model developed by Lago et al. (2021). The LEAR model’s code is freely available, so we can extend it with data from the years up to 2020. Furthermore, its day-ahead price forecasts are among the most precise in the literature, and its authors are leading scholars in the field of price forecasting. Thus, we can perform a year-by-year comparison with our results. Table 2 presents the forecast accuracy of the hybrid model developed in this paper, the agent-based market simulation model and the LEAR model, showing the annual RMSE and MAE. It can be seen that the agent-based model has the highest error, which can be attributed to the general difficulties of techno-economic models in making short-term forecasts (the results of the em.power dispatch model without further post-processing steps are compiled in Section 6.2 and point in the same direction). In contrast, the LEAR model and the proposed hybrid model presented here exhibit similar error measures without larger gaps. Although the LEAR model more often takes the lead, its advantage is limited, as it is a statistical model primarily designed for generating price forecasts. Comparatively, the hybrid model’s forecast encompasses the entire market state represented by the energy system model, including information on additional parameters of interest to market participants (e.g., CO2 emissions, international electricity exchange, and power plant utilization).777Note that while this work focuses exclusively on prices, this model can also be informative about other factors, as discussed in the literature review.

| RMSE | MAE | |||||

| Hybrid | Agent | LEAR | Hybrid | Agent | LEAR | |

| All years | 7.38 | 11.21 | 7.24 | 4.60 | 7.89 | 4.38 |

| 2016 | 5.82 | 8.83 | 5.55 | 3.48 | 6.54 | 3.30 |

| 2017 | 8.79 | 13.01 | 7.91 | 5.25 | 9.44 | 4.56 |

| 2018 | 7.28 | 11.69 | 6.96 | 5.07 | 8.88 | 4.84 |

| 2019 | 7.05 | 10.91 | 7.95 | 4.43 | 6.69 | 4.53 |

| 2020 | 7.63 | 7.54 | 4.77 | 4.65 | ||

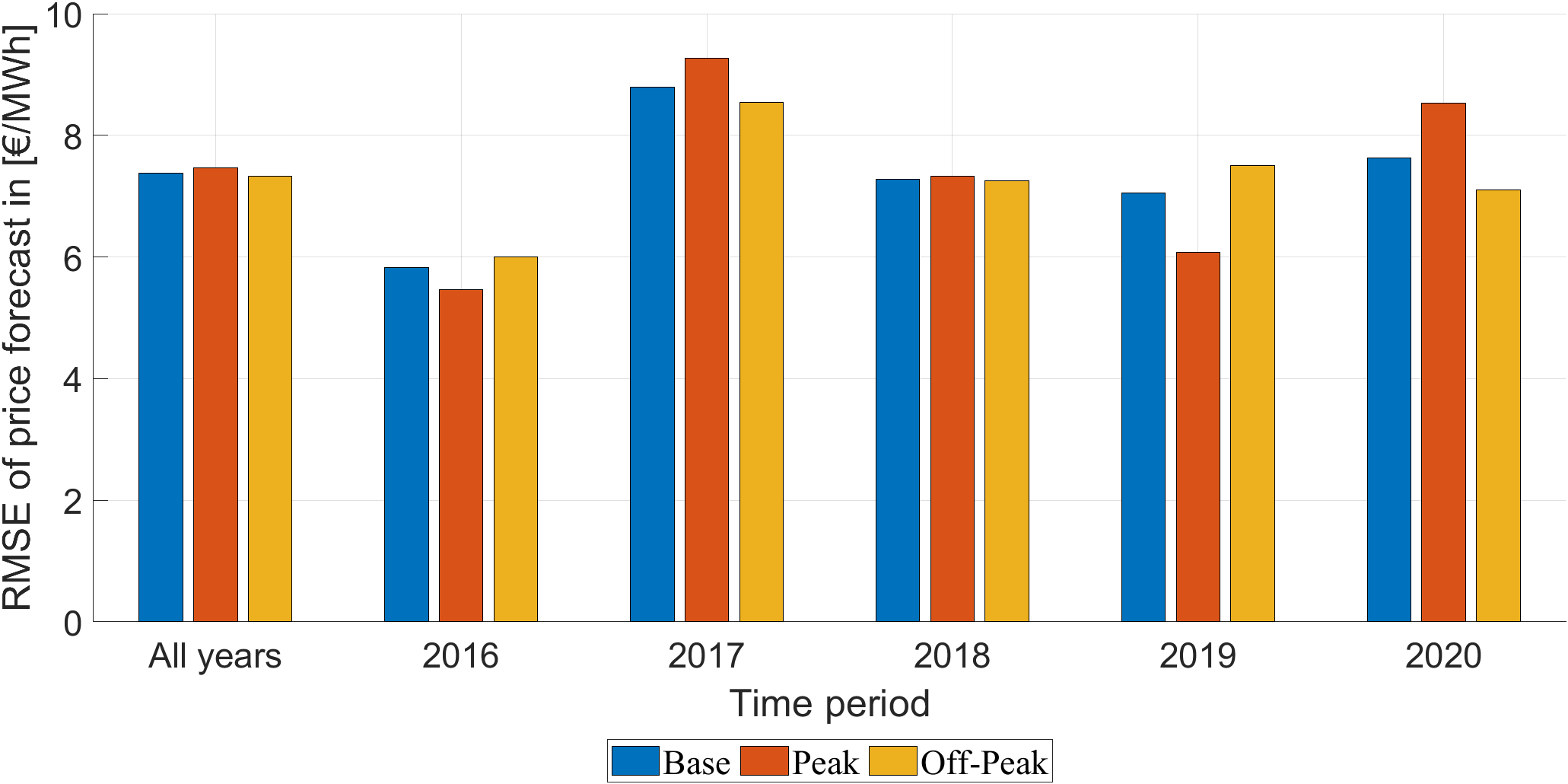

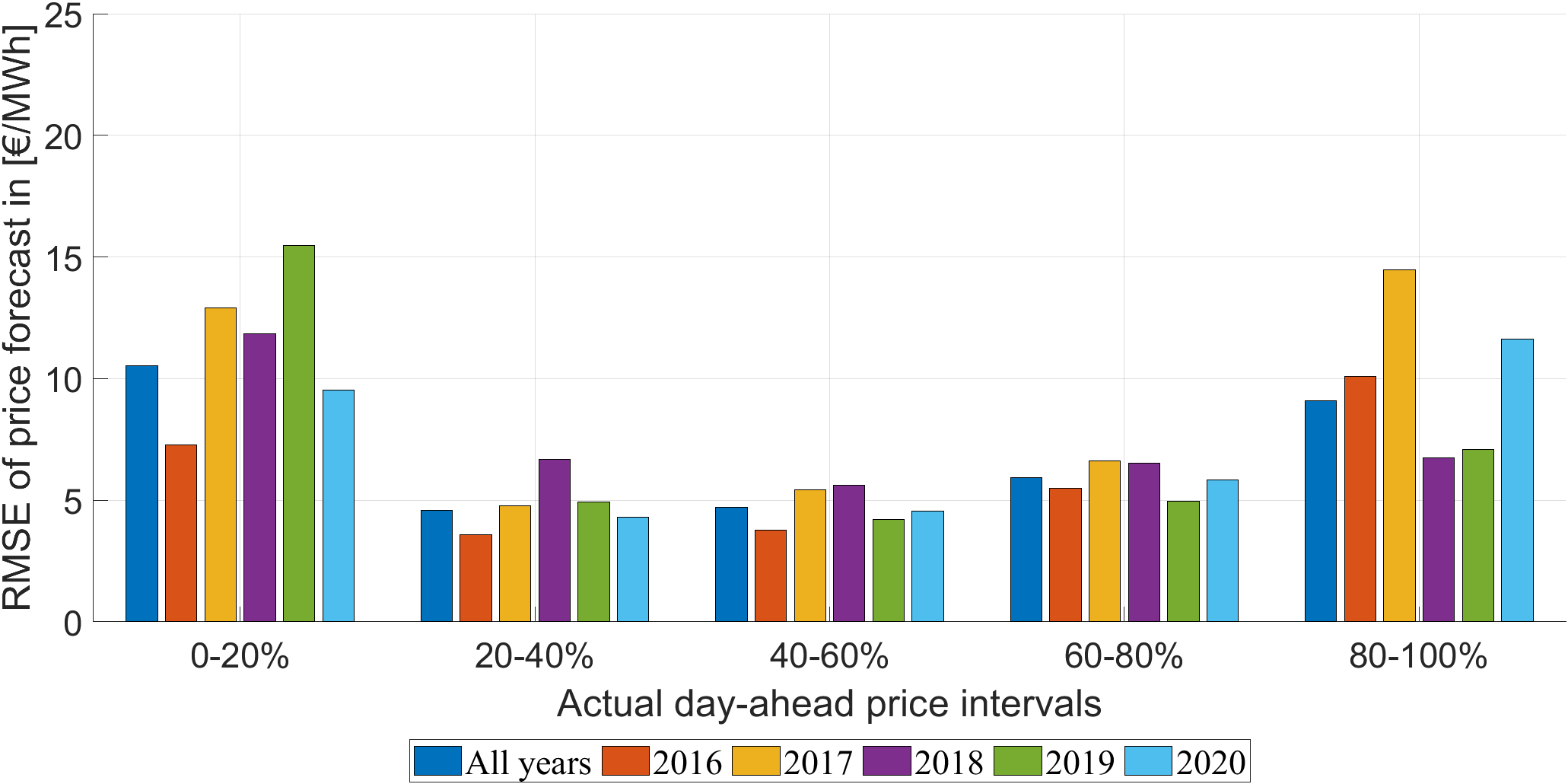

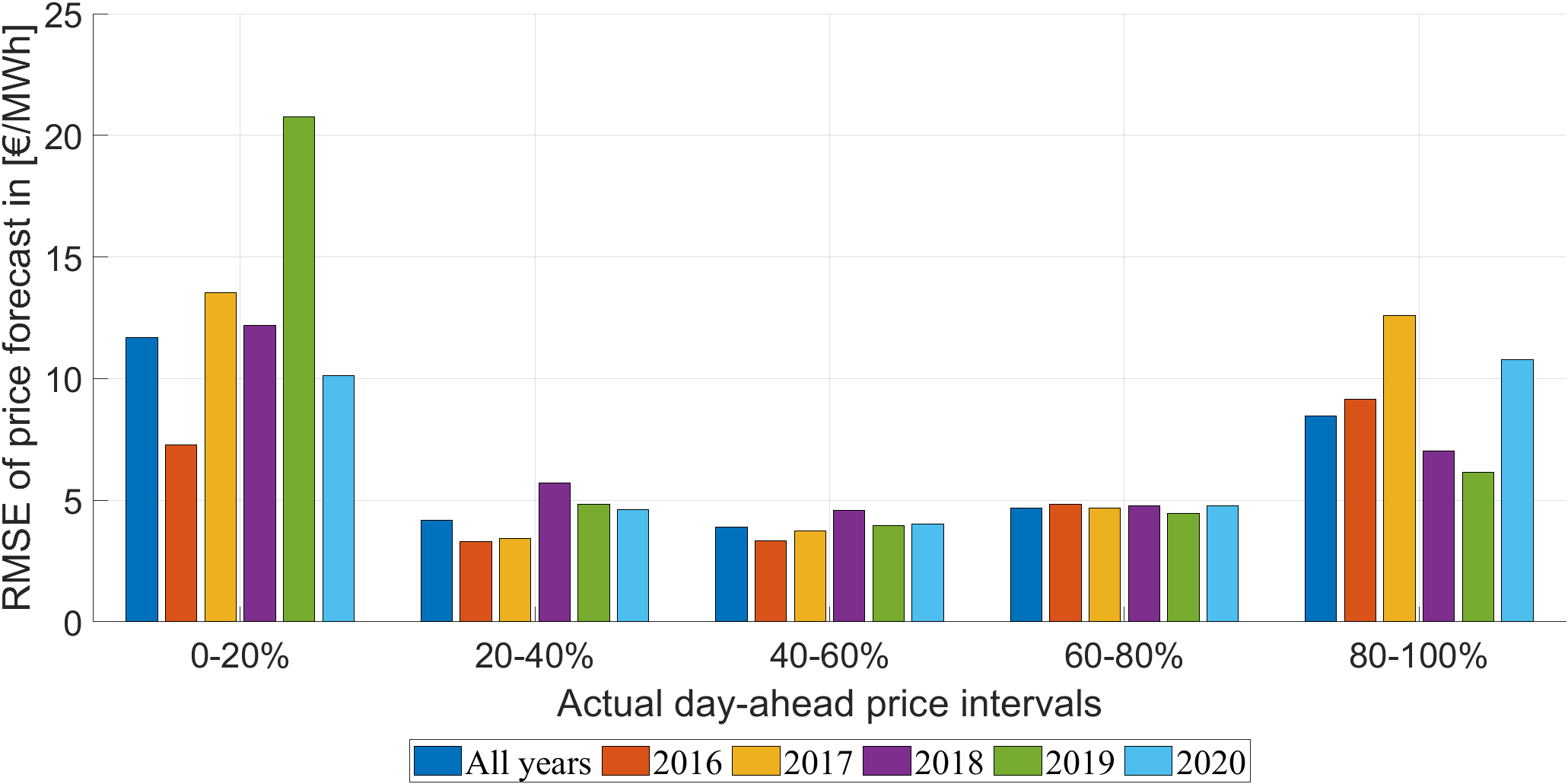

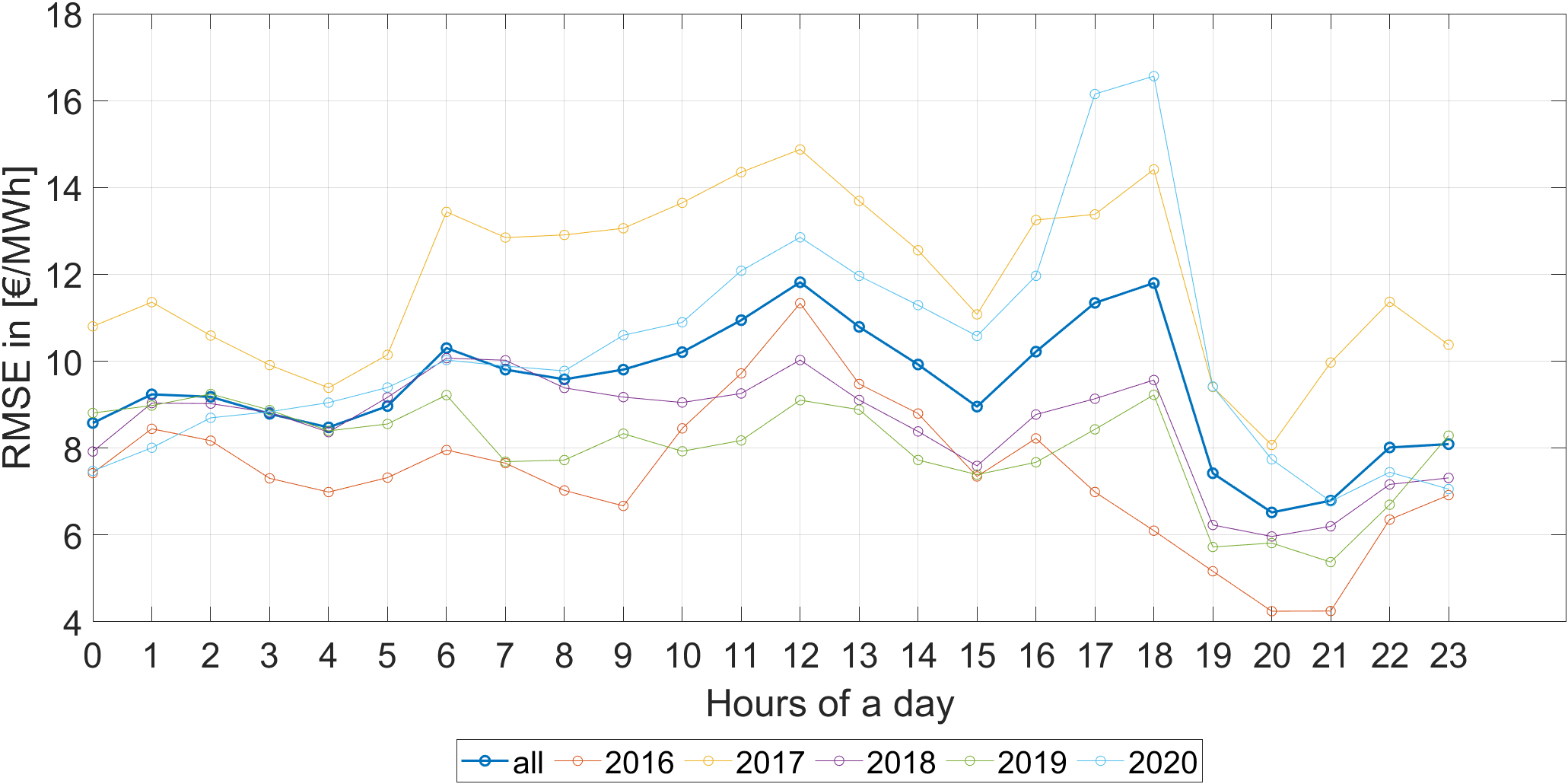

A more detailed evaluation of the prediction errors of the hybrid model is provided in Figures 4 and 5, which show the RMSE for different criteria, such as base, peak and off-peak hours, and the hours of actual day-ahead price quantiles, respectively. Again, peak hours are those between 8 a.m. and 8 p.m. from Monday to Friday; off-peak hours are the remaining hours. Base hours describe all hours of a day, regardless of the day of the week or hour of the day.

While the errors of 7.47 €/MWh in peak hours and 7.33 €/MWh in off-peak hours seem quite similar over the whole period, Figure 5 provides more insight. We separate the predicted hours into five groups presenting the hours for each confidence interval of realised day-ahead prices in 20 % steps. Therefore, we calculate and evaluate the RMSE for each group. The figure suggests a relationship between the error in price forecasts and the price level. Throughout the years, the highest RMSE has consistently been identified in the hours with the lowest 20 % and highest 20 % of prices. Based on economic theory, this finding can be explained by start-up costs and their impact on hourly prices. Assuming perfect foresight, Kuntz and Muesgens (2007) have shown that start-up costs are added to fuel costs exclusively during the hour of highest demand in a cycle because additional capacity must be started-up for that hour, which is not needed in any other hour. During the hour of lowest demand, start-up costs are deducted from variable production costs because power plants save costs on re-starts when allowed to continue operations throughout that hour. In contrast, start-up costs do not influence prices during any other hour of a load cycle. The em.power dispatch model follows this economic theory when determining wholesale electricity prices based on the shadow prices of the demand constraint. However, in reality, bidders on the day-ahead market face uncertainties with regard to which hour has the highest and lowest residual demand and what magnitude start-up costs have for that day. While uncertainty is always present, its impact is likely higher when start-up costs need to be considered in addition to fuel costs and thus increase price volatility around the highest and lowest price hours. Therefore, negative and positive price peaks are harder to capture and forecast than intermediate price levels. Note that this increased uncertainty in these market conditions affects all point forecasting models. Corresponding figures for the LEAR model, with a very similar pattern, are available in Appendix, Figures B.1 and B.2.

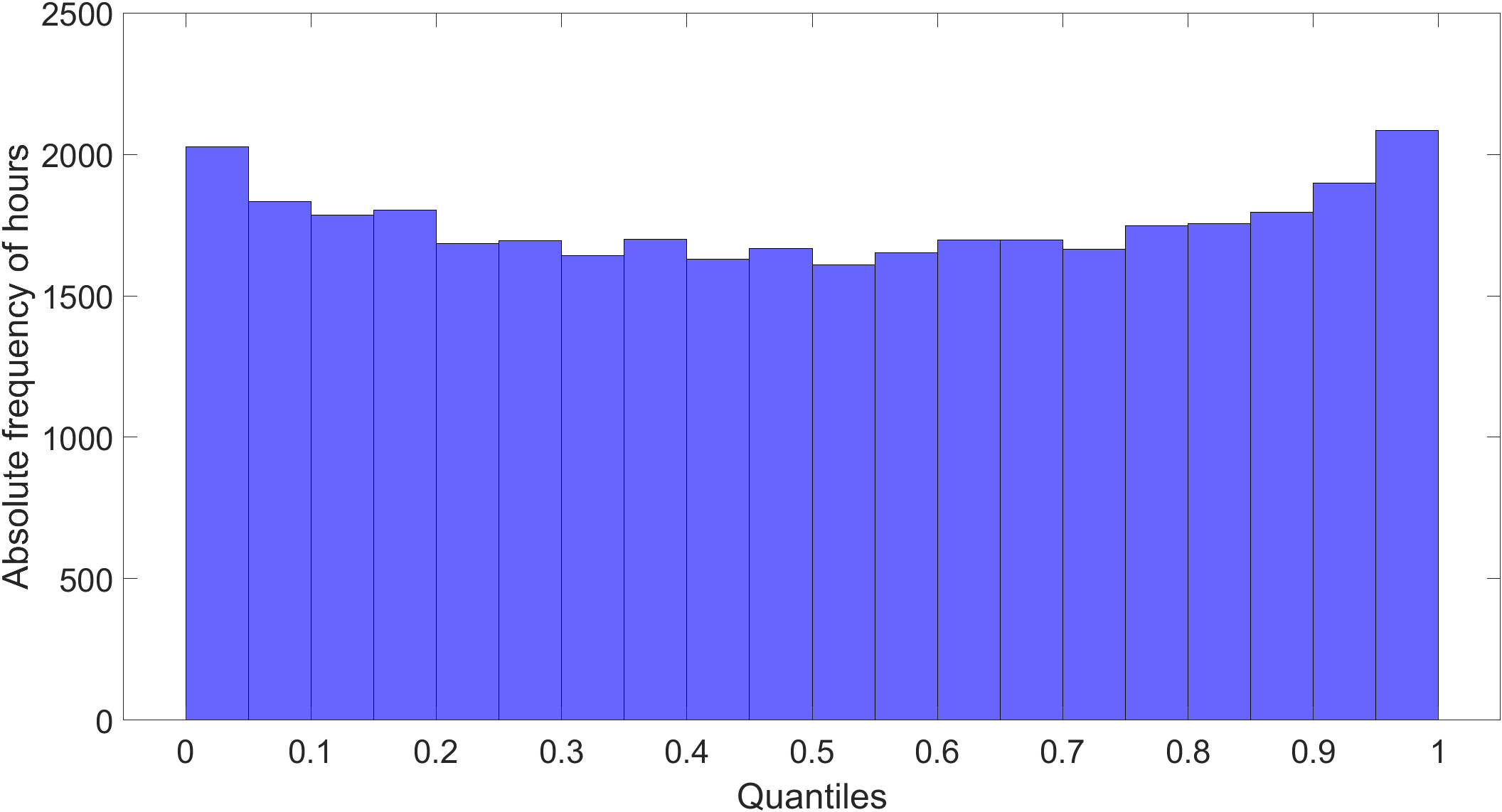

We now turn to the analysis of our probabilistic forecasts. We represent the forecast distribution of the day-ahead prices for each forecast hour with quantile estimates in 5 % steps. The quantile estimation for different quantile levels then enables the calculation of forecast intervals, which determine the probability of the day-ahead price being within a certain range.

The first thing to check about probabilistic forecasts is whether they are well calibrated (see, e.g., Gneiting et al., 2007), which means whether forecasted probabilities and observed frequencies coincide. Therefore, Figure 6 shows the actual frequency of all hours in which the day-ahead prices are above or below the forecast quantile limits. A forecast is considered calibrated if the predicted probabilities match the observed frequencies of the target variable over time. Thus, a fully calibrated forecast in a laboratory environment would correspond to a uniform distribution. The histogram below shows slightly increasing frequencies towards the outside but forms a good approximation of a uniform distribution generated by randomly drawn numbers. This serves as a quality check for our hybrid model and ensures that the predicted probabilities reflect the true probabilities of the day-ahead prices.

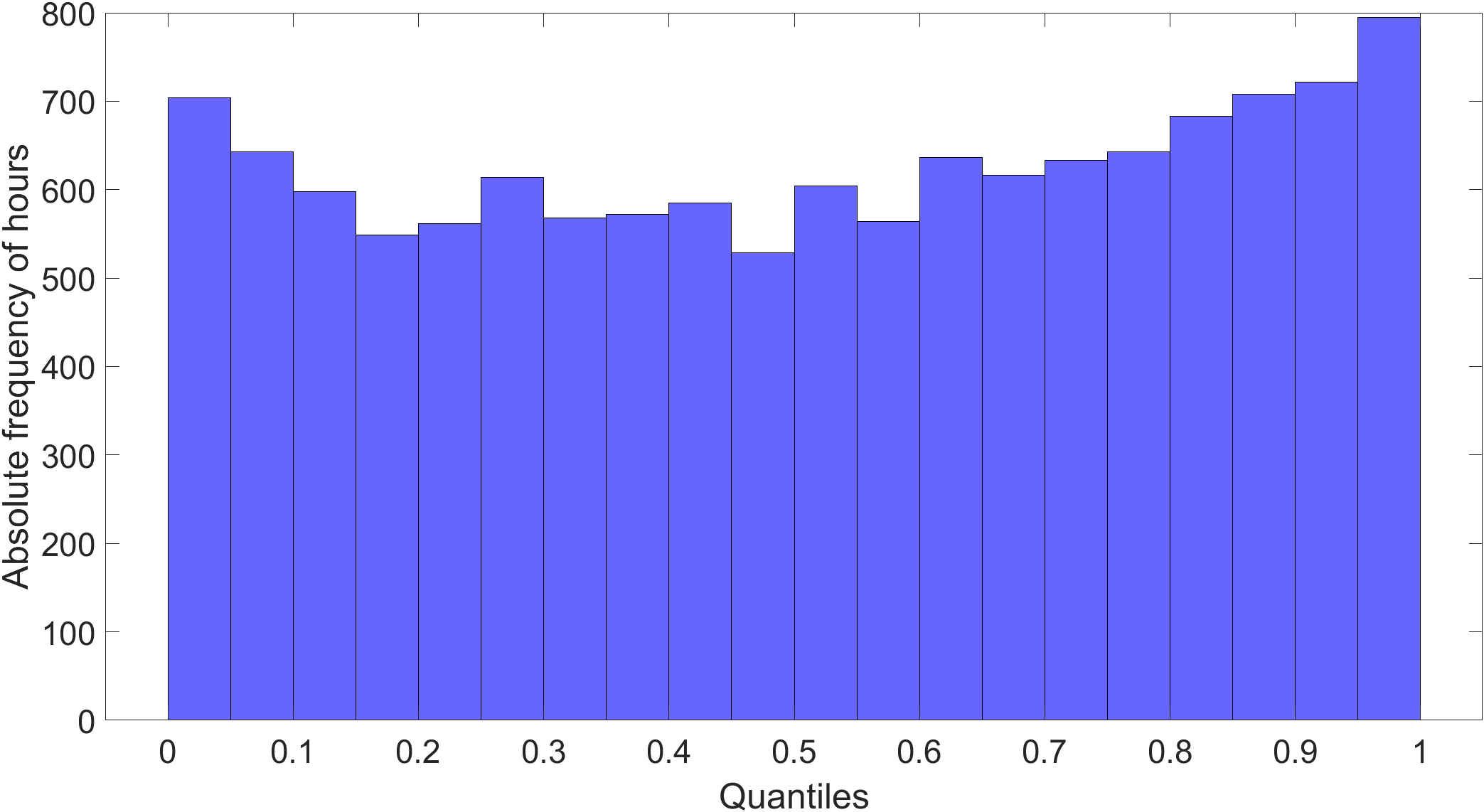

Since peak hours often have higher day-ahead prices than off-peak hours, our hybrid model predicts quantiles with two QRA estimations for each quantile, one for peak hours and one for off-peak hours. Thus, the probabilistic forecasts should be assessed for calibration separately in two disjunctive sub-sets. Figure 7 illustrates the calibration of the quantiles for peak hours on the left and off-peak hours on the right. During off-peak hours, there is a higher frequency in the outermost 5 % quantiles on both sides (i.e., at high and low price levels). During peak hours, more hours exceed the quantile values, especially on the right side of the median. For example, 6.3 % of the hours exceed the 95 % quantile value. With a higher frequency in the low 5 % quantile, the lowest prices can be attributed to the price-reducing influence of high electricity generation from renewable energy sources. This is consistent with the proportion of peak hours that show high demand for electricity but also a high feed-in of renewable energies due to high solar radiation or wind speeds and, thus, a high supply.

The calibration analysis of the predicted quantiles validates the calculated probabilistic forecasts. In the following, we evaluate the hourly distribution of the width of the forecast intervals to obtain more precise and quantified information about market uncertainty and the forecast accuracy that depends on it. Furthermore, we use probabilistic forecasts to calculate the probability of negative prices. Thus, we address the economic interest in including probabilistic forecasts in trading strategies and power plant deployment planning.

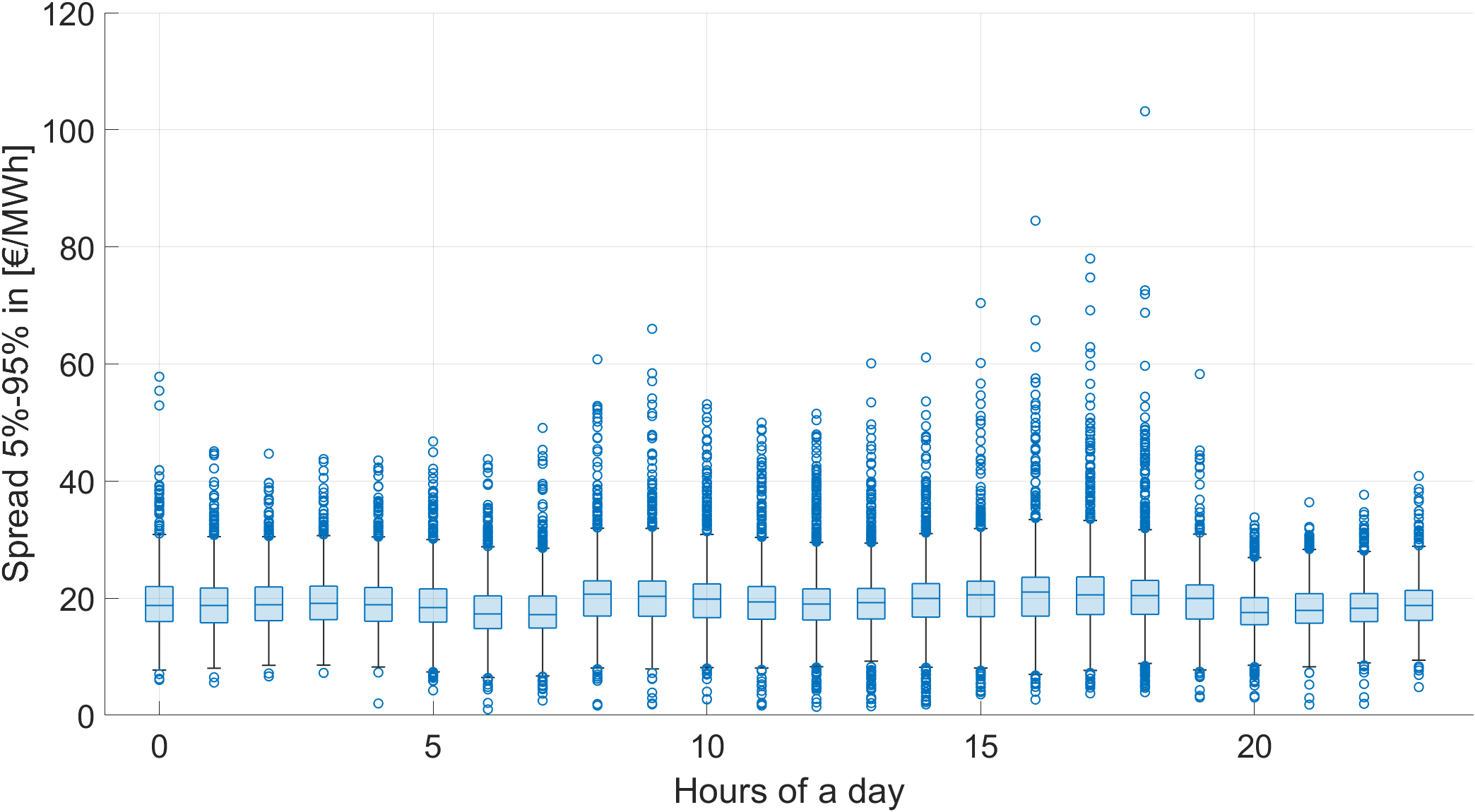

During peak hours, the uncertainty and fluctuations of the day-ahead prices are higher than during off-peak hours. This can be explained by a steeper merit order at high-load levels, the occurrence of start-ups during peak hours and the uncertainty of generation from renewable sources (especially PV plants, which produce more during peak hours). Our hybrid model captures this uncertainty with its probabilistic forecasts. Figure 8 presents box plots that visualise the distribution of the spread between the estimated 95 % quantile and the estimated 5 % quantile for each hour of the day (the width of the 90 % prediction interval. From 8 a.m. to 8 p.m. (daytime), the median spread is wider and outliers are higher than they are at night, reflecting the higher uncertainty and wider range of prices. Although the wider spread of the prediction interval covering 90 % of the potential prices shows that these hours are more difficult to forecast than the night hours, the hybrid model can forecast them as accurately as it can the night hours. Figure 4 shows comparable point forecast accuracy for peak and off-peak hours over the entire period. Additionally, the probabilistic forecasts effectively mirror the market’s uncertainty.

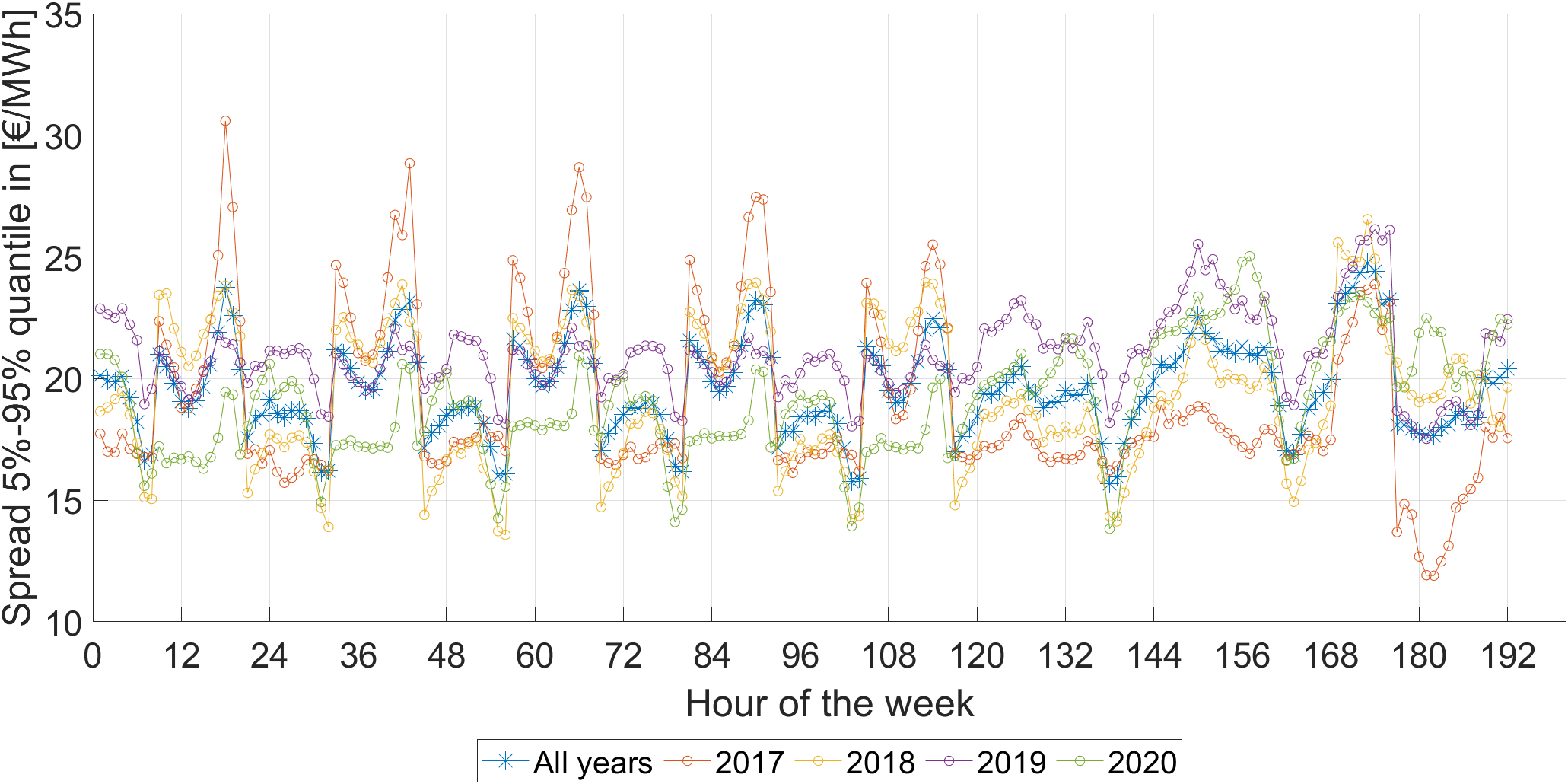

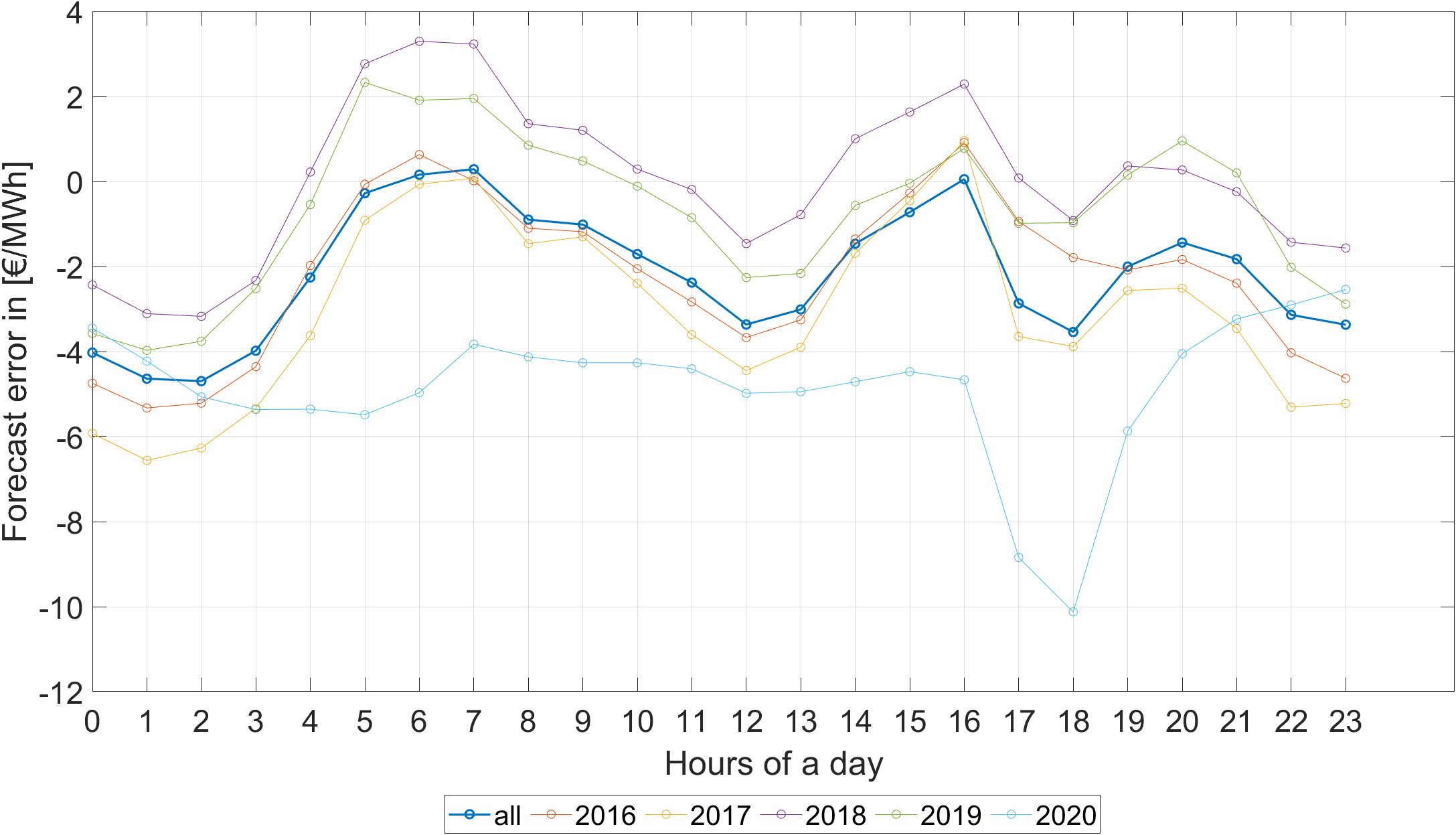

Figure 9 shows the average width of the 90 % prediction interval for each hour of the week, illustrating how easy or difficult it is to forecast the day-ahead electricity price for each individual hour of the week. A wider spread indicates greater uncertainty and less predictability, as the price may take on a wider range of potential values. As previously stated, daytime hours generally exhibit wider intervals than nighttime hours. However, more nuanced patterns are also discernible.

On weekdays (Monday to Friday), the spread of the prediction interval follows a distinct daily course featuring three concave curves with (local) maxima at 3 a.m., 8 a.m. and 4 p.m. The interval is relatively narrow from midnight to 7 a.m. From 7 a.m. to 8 a.m., the interval increases abruptly, posing a major challenge for the forecasting of electricity prices, especially between 4 p.m. and 6 p.m. On weekends (Saturday and Sunday), the interval width is more evenly distributed across all hours but remains high overall and still exhibits a notable decrease between 7 p.m. and 9 p.m. Therefore, predicting day-ahead electricity prices requires careful consideration of the hour of the day and the day of the week on top of all other factors that can affect market dynamics.

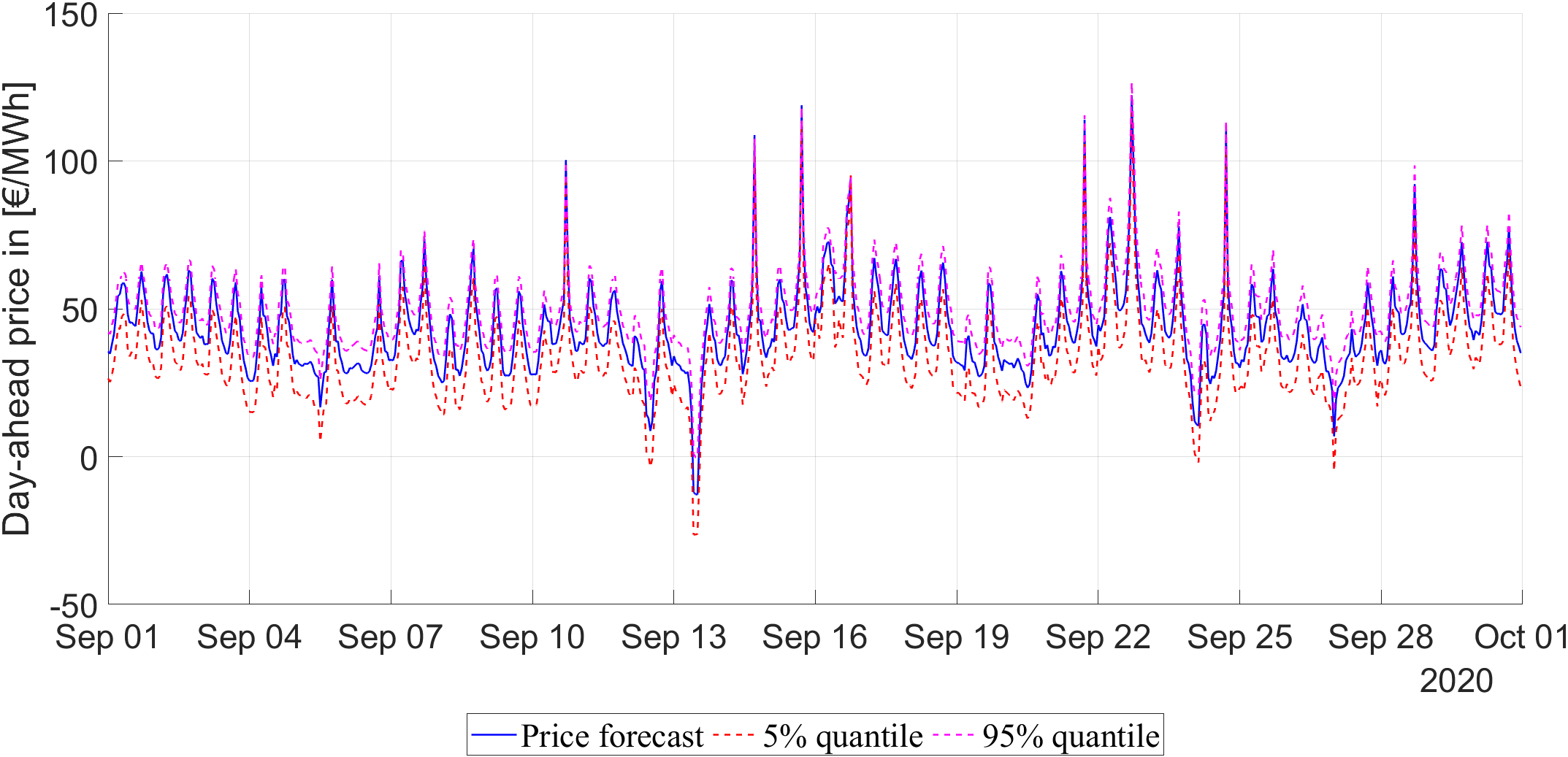

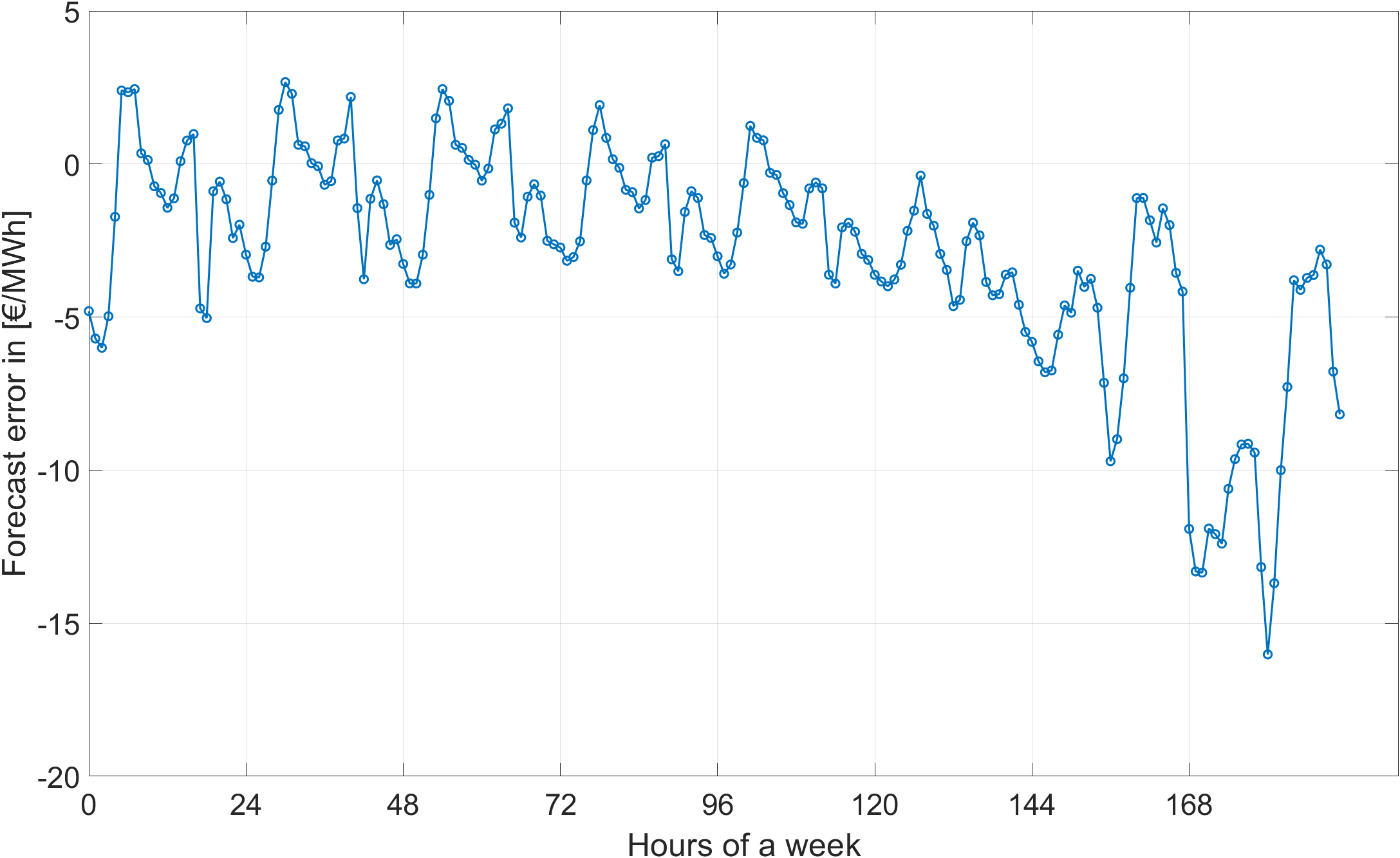

Figure 10 shows an example of how the probabilistic forecasts account for uncertainty. It shows the course of lower and upper limits in combination with the forecast’s expected price (the price’s point prediction). The presented limits correspond to the estimated 5 % and 95 % quantiles, respectively, and indicate the range of possible outcomes. More precisely, actual day-ahead electricity price has a 90 % chance of lying within this range. Using the density forecast and predicted bounds, we can make informed risk estimates and probability statements, which can be useful for decision-making amid uncertainty.

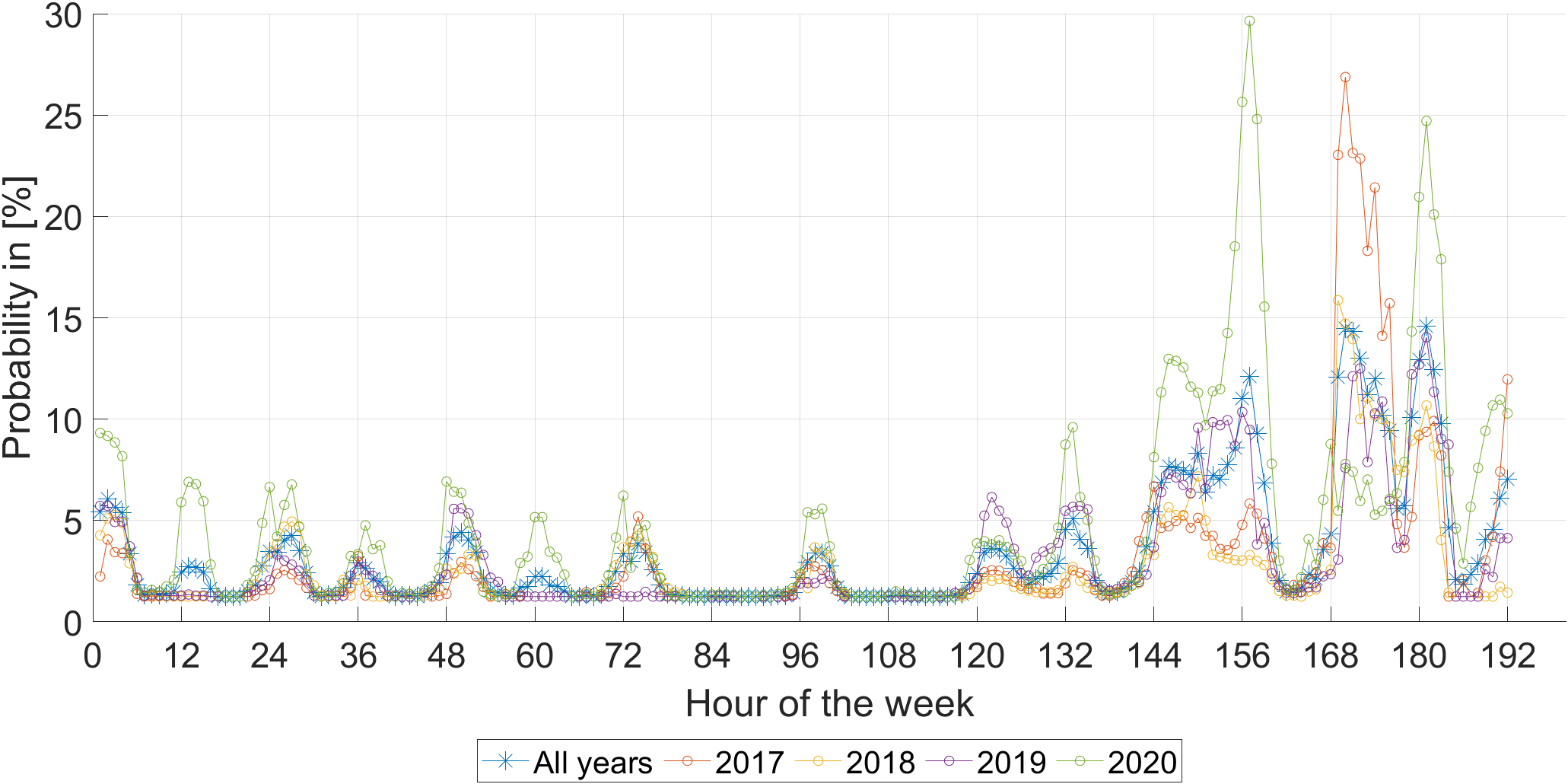

Figure 11 illustrates the probabilities of negative prices for each hour of the week, as estimated by the density forecast. Notably, negative prices can occur when, for example, increases in generation by renewable energy sources or a large share of must-run capacities (e.g., CHP) force conventional power plant units to shut down, leading to start-up costs when these capacities are needed again. The merit order effect of renewable energies and the regulation of renewable energies, in particular payments for production besides the wholesale electricity market, can exacerbate this situation.

Figure 11 reveals that the probability of negative prices is highest on Sundays and public holidays, reaching 10 to 15 % in some hours. This reflects the increased occurrence of negative prices in these hours in the actual day-ahead prices. This is due to the fact that electricity demand is relatively low during these periods, increasing the likelihood of negative price events. The probability of negative prices is also relatively high (above 5 %) in the early hours of Monday, followed by a slightly higher probability of negative prices in the early hours of the other days of the week. This pattern reflects the low-load behaviour of electricity demand in the early hours combined with the typically high wind feed-in during the night and early morning, which can lead to price drops. On Sundays and holidays, the daytime generation from PV and continuous wind feed-in can increase the likelihood of negative prices due to reduced demand.

The probability values for weekdays (Monday to Friday) are similar in their level and pattern, as these days have comparable fundamental parameters. With the probabilities determined by the density forecasts, bidding strategies, portfolios hedges and power plant usage can be optimised. The risks of negative prices or large price spreads can be incorporated into strategies through the probability statements.