capbtabboxtable[][\FBwidth] \newfloatcommandImportTableinput[][\FBwidth] \newfloatcommandcapthreepartthreeparttable[][\FBwidth] \DeclareFloatFontSmall \DeclareFloatFontSmall2 \DeclareFloatFontfootnote \DeclareFloatFontscriptsize \floatsetup[widefigure]margins=hangoutside,facing=yes \floatsetup[table]capposition=top \DeclareMarginSethangboth\setfloatmargins* \DeclareNewFloatTypefigurea placement=htbp, name=Figure, within=section, fileext=lofa \newfloatcommandffigaboxfigurea[\nocapbeside][] \floatsetup[figurea]capposition=top \floatsetup[figure]capposition=top \floatsetup[table]capposition=top 11affiliationtext: Faculty of Economics and Business, KU Leuven, Belgium. 22affiliationtext: Faculty of Economics and Business, University of Amsterdam, The Netherlands. 33affiliationtext: LRisk, Leuven Research Center on Insurance and Financial Risk Analysis, KU Leuven, Belgium. 44affiliationtext: LStat, Leuven Statistics Research Center, KU Leuven, Belgium.

On clustering levels of a hierarchical categorical risk factor

Abstract

Handling nominal covariates with a large number of categories is challenging for both statistical and machine learning techniques. This problem is further exacerbated when the nominal variable has a hierarchical structure. The industry code in a workers’ compensation insurance product is a prime example hereof. We commonly rely on methods such as the random effects approach (Campo and Antonio, 2023) to incorporate these covariates in a predictive model. Nonetheless, in certain situations, even the random effects approach may encounter estimation problems. We propose the data-driven Partitioning Hierarchical Risk-factors Adaptive Top-down (PHiRAT) algorithm to reduce the hierarchically structured risk factor to its essence, by grouping similar categories at each level of the hierarchy. We work top-down and engineer several features to characterize the profile of the categories at a specific level in the hierarchy. In our workers’ compensation case study, we characterize the risk profile of an industry via its observed damage rates and claim frequencies. In addition, we use embeddings (Mikolov et al., 2013; Cer et al., 2018) to encode the textual description of the economic activity of the insured company. These features are then used as input in a clustering algorithm to group similar categories. We show that our method substantially reduces the number of categories and results in a grouping that is generalizable to out-of-sample data. Moreover, when estimating the technical premium of the insurance product under study as a function of the clustered hierarchical risk factor, we obtain a better differentiation between high-risk and low-risk companies.

Keywords: feature engineering, clustering, multi-level factor, high-cardinality feature, nested classification, natural language processing, text embeddings

1 Introduction

At the heart of a risk-based insurance pricing model is a set of risk factors that are predictive of the loss cost. To model the relation between the risk factors and the loss cost, actuaries rely on statistical and machine learning techniques. Both approaches are able to handle different types of risk factors (i.e. nominal, ordinal, geographical or continuous). In this contribution we put focus on challenges imposed by nominal variables with a hierarchical structure. Such variables may cause estimation problems, due to an exceedingly large number of categories and a limited number of observations for some of the categories. Using default methods to handle these, such as dummy encoding, may result in unreliable parameter estimates in generalized linear models (GLMs) and may cause machine learning methods to become computationally intractable. We refer to this type of risk factor as a hierarchical multi-level factor (MLF) (Ohlsson and Johansson, 2010) or a hierarchical high-cardinality attribute (Micci-Barreca, 2001; Pargent et al., 2022). Within workers’ compensation insurance, a typical example hereof is the hierarchical MLF derived from the numerical codes of the NACE system. The NACE system is a hierarchical classification system used in the European Union to group similar companies based on their economic activity (Eurostat, 2008). A similar example is the Australian and New Zealand Standard Industrial Classification (ANZSIC) system (Australian Bureau of Statistics and New Zealand, 2006), which is closely related to the NACE system (Eurostat, 2008).

In predictive modelling, such risk factors are potentially a great source of information. In workers’ compensation insurance, certain industries (e.g., manufacturing, construction) and occupations (e.g., labouring, roofer) are associated with an increased risk of filing claims (Walters et al., 2010; Holizki et al., 2008; Wurzelbacher et al., 2021). Furthermore, companies operating in the same industry are exposed to similar risks. This creates a dependency among companies active in the same industry and heterogeneity between companies working in different industries (Campo and Antonio, 2023). Industry classification systems, such as the NACE and ANSZIC, allow to group companies based on their economic activity at varying levels of granularity. Most industry classification systems are hierarchical classifications that work top-down. The classification of a company starts at the highest level in the hierarchy and, from here, proceeds successively to lower levels in the hierarchy. At the top level of the hierarchy, the categories are broad and general, covering a wide range of economic activities. As we move down the hierarchy, the categories are broken down into increasingly specific subcategories that encompass more detailed economic activities. Further, industry classification systems typically provide a textual description for the categories at all levels in the hierarchy. This description explains why companies are grouped in the same category and can be used to judge the similarity of activities among categories.

To incorporate the hierarchical MLF in a predictive model, we can opt for the hierarchical random effects approach (Campo and Antonio, 2023). Here, we specify a random effect at each level in the hierarchy. The random effects capture the unobservable characteristics of the categories at the different levels in the hierarchy. Moreover, random effects models account for the within-category dependency and between-category heterogeneity. To estimate a random effects model, we can either use the hierarchical credibility model (Jewell, 1975), Ohlsson’s combination of the hierarchical credibility model with a GLM (Ohlsson, 2008) or the mixed models framework (Molenberghs and Verbeke, 2005). These estimation procedures rely on the estimation of variance parameters and we require these estimates to be non-negative (Molenberghs and Verbeke, 2011; Oliveira et al., 2017). In some cases, however, we obtain negative variance estimates and this can occur when there is low variability (Oliveira et al., 2017) or when the hierarchical structure of the MLF is misspecified (Pryseley et al., 2011). In these situations, the estimation procedure yields nonsensical results. With the random effects approach we implicitly assume that the risk profiles differ between the different categories (Tutz and Oelker, 2017). However, it is not an unreasonable assumption that certain categories have an identical effect on the response and that these should be grouped into homogeneous clusters. Decreasing the total number of categories leads to sparser models that are easier to interpret and less likely to experience estimation problems or to overfit. Additionally, individual categories will have more observations, leading to more precise estimates of their effect on the response.

To group data into homogeneous clusters, we typically rely on clustering techniques. These techniques partition the data points into clusters such that observations within the same cluster are more similar compared to observations belonging to other clusters (Hastie et al., 2009, Chapter 14). Within actuarial sciences, clustering methods recently appeared in a variety of applications. In motor insurance, for example, clustering algorithms are employed to group driving styles of policyholders (Wüthrich, 2017; Zhu and Wüthrich, 2021), to construct tariff classes in an unsupervised way (Yeo et al., 2001; Wang and Keogh, 2008) and to bin continuous or spatial risk factors (Henckaerts et al., 2018). Also in health insurance we find several examples. Rosenberg and Zhong (2022) used clustering techniques to identify high-cost health care utilizers who are responsible for a substantial amount of health expenditures.

Our aim is to use clustering algorithms in workers’ compensation insurance pricing, to group categories of the hierarchical MLF that are similar in riskiness and economic activity. To characterize the riskiness, we rely on risk statistics such as the average damage rate and the expected claim frequency. Moreover, we also use the textual description of the categories to obtain information on the economic activity. The risk statistics are expressed as numerical values, whereas the textual descriptions are presented as nominal categories. Both types of features are then used as input in a clustering algorithm to group similar categories of the hierarchical MLF. To create clusters, most algorithms rely on distance or (dis)similarity metrics to quantify the degree of relatedness between observations in the feature space (Hastie et al., 2009; Foss et al., 2019). These metrics, however, are different for numeric and nominal features which makes it challenging to cluster mixed-type data (Cheung and Jia, 2013; Foss et al., 2019; Ahmad et al., 2019). One approach to tackle this problem is to convert the nominal to numeric features. Hereto, we commonly employ dummy encoding (Hsu, 2006; Cheung and Jia, 2013; Ahmad et al., 2019; Foss et al., 2019). This encoding creates binary variables that represent category membership. Hereby, it results in a loss of information when the categories have textual labels. Labels provide meaning to categories and reflect the degree of similarity between different categories. A more suitable encoding is obtained using embeddings, a technique developed within natural language processing (NLP). Embeddings are vector representations of textual data that capture the semantic information (Verma et al., 2021; Schomacker and Tropmann-Frick, 2021; Ferrario and Naegelin, 2020). In the actuarial literature, Lee et al. (2020) show how embeddings can be used to incorporate textual data into insurance claims modelling. Xu et al. (2022) create embedding based risk factors that are used as features in a claim severity model. Zappa et al. (2021) used embeddings to create risk factors that predict the severity of injuries in road accidents.

Research on grouping categories of hierarchical MLFs is limited. Most of the research is focused on nominal variables that do not have a hierarchical structure. For example, the Generalized Fused Lasso (GFL) (Höfling et al., 2010; Gertheiss and Tutz, 2010; Oelker et al., 2014) groups MLF categories within a regularized regression framework. Here, categories are merged when there is a small difference between the regression coefficients. Nonetheless, the GFL does not scale well to high-cardinality features since the number of estimated coefficient differences grows exponentially with the number of categories. Another example to fuse non-hierarchically structured nominal variables is the method of Carrizosa et al. (2021). Here, the authors first specify the order of the categories and the number of clusters. Next, to create the prespecified number of clusters they group consecutive categories. For a specific number of clusters, multiple solutions exist and the solution with the highest out-of-sample accuracy is preferred. The disadvantages of this approach are three-fold. First, it only merges neighbouring categories. Second, there is no procedure to select the optimal number of groups and third, the procedure can not immediately be applied to hierarchical MLFs. To the best of our knowledge, the method described in Carrizosa et al. (2022) is the only approach that puts focus on reducing the number of categories of a hierarchical MLF. Here, the authors propose a bottom-up clustering strategy. This technique begins by considering the categories at the lowest level in the hierarchy. Hereafter, starting from the categories at the lowest level in the hierarchy, they consecutively merge categories at the lowest level into broader categories at higher levels in the hierarchy. As such, categories that are nested within the same category at a higher level in the hierarchy are grouped. Notwithstanding, their proposed optimization strategy is only suited for linear regression models. Further, it is not suitable when we want to maintain the levels in the hierarchical structure. Certain granular categories are replaced the broader categories they are nested in. Hence, it is possible that the optimal solution produces a hierarchical structure with a different depth in its representation.

Our paper contributes to the existing literature in the following ways. Firstly, we present a data-driven approach to reduce an existing granular hierarchical structure to its essence, by grouping similar categories at every level in the hierarchy. We devise a top-down procedure, where we start at the top level, to preserve the hierarchical structure. At a specific level in the hierarchy, we engineer several features to characterize the risk profile of each category. In a case-study with a workers’ compensation insurance product, we use estimated random effects obtained with a generalized linear mixed model for damage rates on the one hand and claim frequencies on the other hand. To extract the textual information contained in the category description, we use embeddings. Next, we use these features as input in a clustering algorithm to group similar categories into clusters. Hereafter, we proceed to grouping the categories at the next hierarchical level. The procedure stops once we grouped the categories at the lowest level in the hierarchy. Secondly, we provide a concise overview of important aspects and algorithms in cluster analysis. Furthermore, we demonstrate that the clustering algorithm and evaluation criterion affect the clustering solution. Thirdly, we show that embeddings can be used to group similar categories of a nominal variable. Contrary to Lee et al. (2020); Zappa et al. (2021); Xu et al. (2022), we do not employ embeddings to create new risk factors in a pricing model. Instead, we use embeddings to extract the textual information of category labels and to cluster categories based on their semantic similarities.

The remainder of this paper is structured as follows. In Section 2, we use a workers’ compensation insurance product as a motivating example with the NACE code as hierarchical MLF. We illustrate the structure of this type of data set, which information is typically available and we explain how to engineer features that characterize the risk profile of the categories. In Section 3, we define a top-down procedure to cluster similar categories at a specific level in the hierarchy and we discuss several aspects of clustering techniques. The results of applying our procedure to reduce the hierarchical structure to its essence are discussed in Section 4. Moreover, in this section we also compare the use of the original and the reduced structure in a technical pricing model for workers’ compensation insurance. Section 5 concludes the article.

2 Feature engineering for industrial activities in a workers’ compensation insurance product

To illustrate the importance of hierarchical MLFs in insurance pricing, a workers’ compensation insurance product is a particularly suitable example. This insurance product compensates employees for lost wages and medical expenses resulting from job-related injury (see Campo and Antonio (2023) for more information). In this type of insurance, we generally work with an industrial classification system to group companies based on their economic activity. Hereto, we demonstrate and discuss the NACE classification system in Section 2.1. We explain the typical structure of a workers’ compensation insurance data set and discuss which information is available. In Section 2.2 we show how we use this information to engineer features that characterize the riskiness and economic activity of categories at a specific level in the hierarchy.

2.1 A hierarchical classification scheme for industrial activities

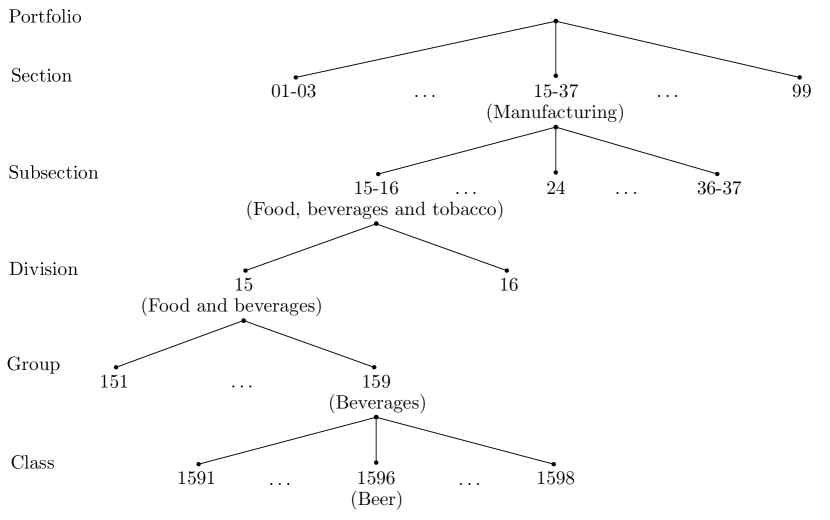

In a workers’ compensation insurance data set, it is common to work with an industrial classification system. Within the European Union, a wide range of organizations (e.g., national statistical institutes, business and trade associations, insurance companies and European national central banks (Eurostat, 2008; Stassen et al., 2017; European Central Bank, 2021)) work with the NACE system (Eurostat, 2008). This is a hierarchical classification system to group companies based on their economic activity. Each company is assigned a four-digit numerical code, which is used to identify the categories at different levels in the hierarchy. The NACE system works top-down, starts at the highest level in the hierarchy and then proceeds to the lower levels. In our paper, we work with NACE Rev. 1 (Statistical Office of the European Communities, 1996), which has five hierarchical levels (in descending order): section, subsection, division, group and class. Most member states of the EU have a national version which follows the same structural and hierarchical framework as the NACE. In Belgium, the national version of NACE Rev. 1 is called the NACE-Bel (2003) (FOD Economie, 2004) and adds one more level to the hierarchy by adding a fifth digit. We refer to this level as subclass. Insurance companies may choose to add a sixth digit to include yet another level, allowing for even more differentiation between companies. This level in the hierarchy is referred to as tariff group and we denote the insurance company’s version as NACE-Ins.

To illustrate how the NACE system works, suppose that we have a company that manufactures beer. Using NACE Rev. 1 (Statistical Office of the European Communities, 1996), this company gets the code 1596. At the top level section, the first two digits (i.e. 15) classify this company into manufacturing (see Figure 1). This category contains all NACE codes that start with numbers 15 to 37. Following, the first two digits categorize the company into manufacture of food products, beverages and tobacco at the subsection level, which is nested within the section manufacturing. The category manufacture of food products, beverages and tobacco includes all NACE codes starting with numbers 15 and 16. At the third level in the hierarchy - division - the company is classified into 15 - manufacture of food products and beverages. At the fourth level group, we use the first three digits to classify the company in 159 - manufacture of beverages. Finally, at the fifth and lowest level class, the four digit code assigns the company to 1596 - manufacture of beer.

This example also shows that, at all levels in the hierarchy, the NACE provides a textual description for each category. This text briefly describes the economic activity of a specific category, thereby explaining why certain companies are grouped. We illustrate this in Table 1. Herein, we show the textual information that is available for companies with NACE codes 1591, 1596, and 1598. This table displays a separate column for every level in the hierarchy. The corresponding value indicates which category the codes belong to. At the section, subsection, division and group level, the NACE codes 1591, 1596, and 1598 are grouped in the same categories (i.e. 15-37, 15-16, 15 and 159 respectively). At the class level, each of the codes is assigned to a different category. The column description presents the textual information for each corresponding category. For example, at the division level, 15 has the description manufacture of food products and beverages.

| Section | Subsection | Division | Group | Class | Description |

|---|---|---|---|---|---|

| 15-37 | Manufacturing | ||||

| 15-16 | Manufacture of food products, beverages and tobacco | ||||

| 15 | Manufacture of food products and beverages | ||||

| 159 | Manufacture of beverages | ||||

| 1591 | Manufacture of distilled potable alcoholic beverages | ||||

| 1596 | Manufacture of beer | ||||

| 1598 | Production of mineral waters and soft drinks |

The textual description of other categories in the NACE system is similar to the example in Table 1. Overall, the description is brief and consists of a single word or phrase. Further, categories at higher levels in the hierarchy have a more concise description using overarching terms such as manufacturing. Conversely, at lower levels in the hierarchy, the descriptions are typically more detailed and extensive (e.g. manufacture of distilled potable alcoholic beverages and production of mineral waters and soft drinks).

| Section | Subsection | Division | Group | Class | Subclass | |

|---|---|---|---|---|---|---|

| Number of categories: | ||||||

| NACE-Bel (2003) | 17 | 31 | 62 | 224 | 515 | 800 |

| Portfolio | 17 | 30 | 56 | 197 | 398 | 581 |

Selecting levels in the hierarchy

When working with NACE-Ins, we have seven levels in the hierarchy: section, subsection, division, group, class, subclass and tariff group. This results in an immense amount of categories, some of which contain few to no observations. In this paper, we work with a NACE-Ins that is based on the NACE-Bel (2003) (FOD Economie, 2004). Table 2 shows the unique number of categories at each level in the hierarchy. The first row indicates how many categories there are at each level in the NACE-Bel (2003) classification system. The second row specifies how many categories are present at each level in our portfolio. Due to the confidentiality of the data, we do not disclose the number of categories at the tariff group level.

The more levels in the hierarchy, the more complex a tariff model becomes that incorporates this hierarchical MLF in its full granularity. Consequently, in practice, the NACE-Ins may not be used in its entirety. In our database, we have access to a hierarchical MLF designed by the insurance company that offers the workers’ compensation insurance product. This structure has been created by merging similar NACE-Ins codes, based on expert judgment. This hierarchical MLF has two levels in the hierarchy, referred to as industry and branch in Campo and Antonio (2023). In our paper, we illustrate how such a hierarchical MLF can be constructed using our proposed data-driven approach, as an alternative for the manual grouping by experts. To demonstrate our method we put focus on two selected levels in the hierarchy of NACE-Ins. This is merely for illustration purposes. Our approach is applicable with any number of levels in the hierarchy.

To align with the insurance company’s hierarchical MLF, we select the subsection and tariff group level (see Figure 1) and aim to reduce the hierarchical structure consisting of these levels. We use to index the levels in the hierarchy, where denotes the total number of levels. In our illustration, subsection corresponds to the highest level in the hierarchy. At , we index the categories using where denotes the total number of categories. The tariff group level represents the second level in the hierarchy. Here, we use to index the categories nested within subsection . We refer to as the child category that is nested within parent category and denotes the total number of categories nested within . Due to confidentiality of the classification system and data, no comparisons between the company’s hierarchical MLF and our proposed clustering solutions will be provided in the paper.

2.2 Feature engineering

We start at the highest level in the hierarchy, subsection, and engineer a set of features that capture the riskiness and the economic activity of the categories. Using these features, the clustering algorithms can identify and group similar categories at the subsection level. Hereafter, we proceed to the tariff group level and engineer the same type of features for the categories at this level in the hierarchy.

We assume that we have a workers’ compensation insurance data set with historical, claim related information of the companies in our portfolio. For each company , we have the NACE-Ins code in year . We use this code to categorize company in subsection and tariff group . In our database, we have the total claim amount , the number of claims and the salary mass for year and company , a member of subsection and tariff group .

Riskiness

We express the riskiness of the subsection and tariff group in terms of their damage rate and their claim frequency. The higher the damage rate and claim frequency, the riskier the category. For an individual company , the damage rate in year is calculated as

| (1) |

To capture the subsection- and tariff group-specific effect on the damage rate and claim frequency, we use random effects models (Campo and Antonio, 2023). In this approach, the estimate of the category-specific random effect is dependent on how much information is available. The random effect estimates are shrunk towards zero for categories with high variability, a low number of observations or when the variability between categories is small (Breslow and Clayton, 1993; Gelman and Hill, 2017; Brown and Prescott, 2006; Pinheiro et al., 2009).

We start at the subsection level and model the damage rate as a function of the subsection using a (Tweedie generalized) linear mixed model

| (2) |

Here, denotes the intercept and the random effect of subsection . We include the salary mass as weight. As discussed in Campo and Antonio (2023), we typically model the damage rate by assuming either a Gaussian or Tweedie distribution for the response. The ’s represent the between-subsection variability and enable us to discern between low- and high-risk profiles. The higher , the higher the expected damage rate for subsection and vice versa. To engineer the first feature, we extract the ’s from the fitted damage rate model (2). Hereafter, we fit a Poisson generalized linear mixed model

| (3) |

to assess the subsection’s effect on the claim frequency. denotes the intercept and the random effect of subsection . We include the log of the salary mass as an offset variable. We extract the ’s from the fitted claim frequency model (3) to engineer the second feature. The ’s and ’s will be combined with the features representing the economic activity to group similar categories at the subsection level. We index the resulting grouped categories at the subsection level using .

Next, we engineer the features at the tariff group level. To capture the tariff group-specific effect on the damage rate, we fit a (Tweedie generalized) linear mixed model

| (4) |

where the random effect represents the tariff group-specific deviation from . As before, we include the as weight. The ’s reflect the between-tariff group variability, after having accounted for the variability between the grouped subsections. quantifies the tariff group-specific effect of tariff group , in addition to the (grouped) subsection-specific effect , on the expected damage rate. To characterize the riskiness of the categories at the tariff group level in terms of the claim frequency, we extend (3) to

| (5) |

In this model, represents the tariff group-specific deviation from . We extract the ’s and ’s from the fitted damage rate (4) and claim frequency model (5) to engineer the features at the tariff group level.

Economic activity

Next, we require a feature that expresses similarity in economic activity. Given that industry codes of similar activities tend to be closer, we might rely on their numerical values. The closer the numerical value, the more overlap there will be between categories at a specific level in the hierarchy. Hence, we could use the four-digit NACE codes as discussed in Section 2.1. Notwithstanding, not all categories can readily be converted to a numerical format. At the higher levels in the hierarchy we have categories that encompass various NACE codes, such as manufacture of pulp, paper and paper products: publishing and printing at the subsection level. This specific subsection consists of all NACE codes that start with numbers 21 to 22. To obtain a numerical representation of this subsection we can, for example, take the mean of these NACE codes. We then obtain the encodings as illustrated in Table 3. The column subsection indicates which category the NACE codes are appointed to at the subsection level and the column description gives the textual description of this category. The examples in this table highlight two issues with this approach. Firstly, the numerical distance may not reflect the similarity between economic activities. The difference between manufacture of wood and wood products and manufacture of pulp, paper and paper products: publishing and printing is the same as the difference between manufacture of pulp, paper and paper products: publishing and printing and manufacture of coke, refined petroleum products and nuclear fuel. Hence, using this encoding would imply that manufacture of pulp, paper and paper products: publishing and printing is as similar to manufacture of wood and wood products as it is to manufacture of coke, refined petroleum products and nuclear fuel. Secondly, there might be gaps between consecutive codes in the classification system. In NACE Rev. 1, for example, there are no codes that start with 43 or 44. Gaps such as these can be present at various levels in the hierarchy and generally exist to allow for future additional categories (Eurostat, 2008).

| Subsection | Encoding | Description |

| 20 | 20 | Manufacture of wood and wood products |

| 21-22 | 21.5 | Manufacture of pulp, paper and paper products: publishing and printing |

| 23 | 23 | Manufacture of coke, refined petroleum products and nuclear fuel |

| 24 | 24 | Manufacture of chemicals, chemical products and mad-made fibres |

| 36-37 | 36.5 | Manufacturing not elsewhere classified |

| 40-41 | 40.5 | Electricity, gas and water supply |

| 45 | 45 | Construction |

Alternatively, we use embeddings to encode the economic activity of a category (Mikolov et al., 2013). Embeddings map the textual information to a continuous vector. Hence, we use embeddings to map the description for subsection to a vector . For tariff group within subsection , we denote the embedding vector as . Here, is the dimension of the vector which depends on the encoder. The textual information from similar categories is expected to lie closer in the vector space and this enables us to group semantically similar texts (i.e. texts that are similar in meaning).

Consequently, we group categories with comparable economic activities based on the embeddings of their textual labels. To engineer these embeddings, we may train an encoder on a large corpus of text. Within the area of Natural Language Processing (NLP), researchers commonly use neural networks (NN) as encoders. By training the NN on large amounts of unstructured text data, it is able to learn high-quality vector representations (Mikolov et al., 2013). In addition, the encoders can be trained to either learn vector representations for words, phrases or paragraphs. The disadvantage of these models is that they generally need a large amount of data (Arora et al., 2020; Troxler and Schelldorfer, 2022). Furthermore, words that do not appear often are poorly represented (Luong et al., 2013). We therefore prefer pre-trained encoders, which are trained on large text corpuses, to encode the textual description of a subsection. For example, the universal sentence encoder of Cer et al. (2018) is trained on Wikipedia, web news, web question-answer pages and discussion forums. This encoder is publicly available via TensorFlow Hub (https://tfhub.dev/).

Feature matrix

After engineering the features at level in the hierarchy, we assemble them into a feature matrix . Table 4 shows an example of the feature matrix at the subsection level. Herein, represents the vector with the estimated random effects from the fitted damage rate GLMM (see (2)). denotes the vector with the estimated random effects of the claim frequency GLMM (see (3)) and we use the notation for the embeddings. Each row in corresponds to a numerical representation of a specific subsection , with . We denote the feature vector of subsection by .

| Subsection | |||||||

|---|---|---|---|---|---|---|---|

| 1 | -1.25 | -0.25 | -2.13 | 1.25 | 0.15 | … | -0.05 |

| … | … | … | … | … | … | … | … |

| 0.75 | 0.15 | 1.79 | -2.13 | 0.5 | … | 1.07 |

At the tariff group level, we gather the features in . An example hereof is given in Table 5. and denote the vectors of the tariff group-specific random effects. To denote the embeddings, we use . denotes the feature vector of tariff group , nested within subsection .

| Subsection | Tariff group | |||||||

|---|---|---|---|---|---|---|---|---|

| 1 | 11 | -1.55 | -0.01 | -0.54 | 1.08 | 2.12 | … | 0.10 |

| … | … | … | … | … | … | … | … | … |

| 1 | 0.15 | 0.96 | -0.37 | -0.26 | 0.58 | … | -0.99 | |

| … | … | … | … | … | … | … | … | … |

| 1 | -0.29 | -0.41 | -0.05 | -0.72 | 0.41 | … | -0.73 | |

| … | … | … | … | … | … | … | … | … |

| 0.11 | 0.26 | 0.16 | 0.69 | 0.87 | … | 1.59 | ||

| … | … | … | … | … | … | … | … | … |

| 1 | 0.11 | 0.26 | 0.16 | 0.69 | 0.87 | … | 1.59 | |

| … | … | … | … | … | … | … | … | … |

| 0.67 | -1.74 | 0.19 | 0.45 | 0.5 | … | -0.61 |

3 Clustering levels in a hierarchical categorical risk factor

3.1 Partitioning Hierarchical Risk-factors Adaptive Top-down

To group similar categories at each level in the hierarchy, we devise the PHiRAT to Partition Hierarchical Risk-factors in an Adaptive Top-down way, see Algorithm 1. We introduce some additional notation to explain how PHiRAT works. denotes the set of categories at a specific level in the hierarchy. Hence, when the total number of levels , and as illustrated in Tables 4 and 5, respectively. We use to indicate that child category has parent category and denotes the set of all child categories nested within parent category . represents the subset of feature matrix , which contains only those rows of that correspond to the child categories nested in parent category . For example, when , contains only the rows corresponding to the child categories of (see Table 5). Further, denotes the number of clusters at level in the hierarchy. For , we extend the notation to to indicate that, at level in the hierarchy, we group the child categories of into clusters. The subscript indicates at which level in the hierarchy we are. We use the additional subscript to specify that we only consider the set of child categories of parent category .

PHiRAT works top-down, starting from the highest level () and working its way down to the lowest level () in the hierarchy (see Algorithm 1). Every iteration consists of three steps. First, we engineer features for the categories in . Second, we combine these features in a feature matrix . Third, we employ clustering techniques to group the categories in using (a subset of) as input. The third step differs slightly when . At , we use the full feature matrix as input in the clustering algorithm. Conversely, when , we loop over the parent categories in and in every loop, we use a different subset of as input. For parent category , we only consider and use as input in the clustering algorithm. Hereby, we ensure that we only group child categories nested within parent category . Further, we remove a specific level from the hierarchy if is reduced to (i.e. all child categories, of each parent category in , are merged into a single group). The algorithm stops when the clustering at level is done.

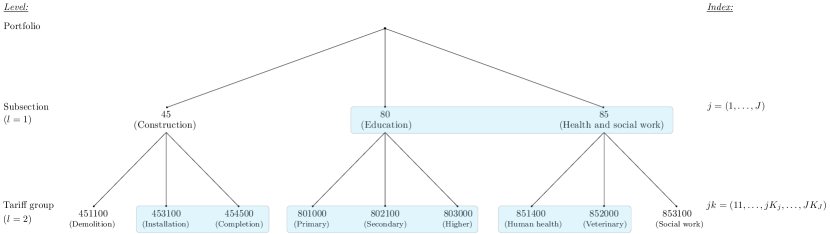

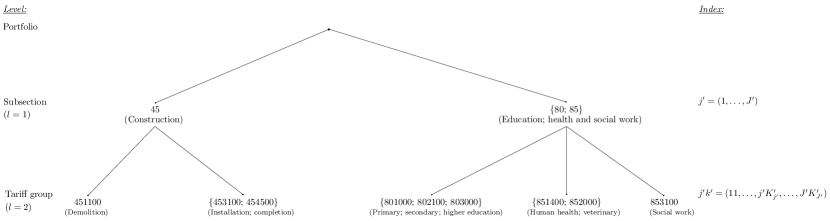

We visualize how the procedure works in Figure 2. In this fictive example, we focus on the subsection and tariff group level. At the subsection level, there are three unique categories and at the tariff group level, we have nine unique categories (see Figure 2(a)). We use the index at . At , we use to index the categories nested within . Using PHiRAT, we first group the categories 80 and 85 at . This is depicted in Figure 2(a) by the blue rectangle. Consequently, where denotes that categories 80 and 85 are merged. The grouped categories at are now indexed by . Hereafter, the algorithm iterates over the (fused) categories in and clusters the child categories at . Within subsection 45, it groups the categories 453100 and 454500. Within , the clustering results in three groups of categories: (1) ; (2) and (3) 853100. We index the fused categories at and nested within using . At this point the algorithm stops and Figure 2(b) depicts the clustering solution.

We opt for a top-down approach for several reasons. Firstly, at the highest level we have more observations available for the categories. The more data, the more precise the category-specific risk estimates will be. Conversely, categories at more granular levels have fewer observations, leading to less precise risk estimates. Secondly, we preserve the original hierarchical structure and maintain the parent-child relationship between categories at different levels in the hierarchy. Hereby, we divide the grouping of categories, at a specific level in the hierarchy, into smaller and more specific separate clustering problems.

Alternatively, it might be interesting to construct a similar algorithm that works bottom-up and groups child categories that have different parent categories. We leave this as a topic for future research.

3.2 Clustering analysis

To partition the set of categories into homogeneous groups, we rely on clustering algorithms using (a subset of) as input. At , for example, we employ clustering to divide the rows in into homogeneous groups such that categories in each cluster are more similar to each other compared to categories of other clusters . In the remainder of this section, we continue with the example of grouping the categories at to explain and illustrate the key concepts of the clustering methods used in this paper.

Most clustering algorithms rely on distance or (dis)similarity metrics to quantify the proximity between observations. Table 6 gives an overview of a selected set of (dis)similarity measures relevant to our paper. A dissimilarity measure expresses how different two observations and are (the higher the value, the more they differ). Dissimilarity metrics that satisfy the triangle inequality for any (Schubert, 2021; Phillips, 2021) are considered proper distance metrics. Most dissimilarity metrics can easily be converted to a similarity measure which expresses how comparable two observations are, with similar observations obtaining higher values for these measures. The most commonly used dissimilarity metric is the squared Euclidean distance . Here, and denotes the number of features considered. Euclidean based (dis)similarity measures, however, are not appropriate to capture the similarities between embeddings (Kogan et al., 2005). Within NLP, the cosine similarity is therefore most often used to measure the similarity between embeddings (Mohammad and Hirst, 2012; Schubert, 2021). Notwithstanding, the cosine similarity ranges from -1 to 1 and in cluster analysis we generally require the (dis)similarity measure to be non-negative (Everitt et al., 2011; Kogan et al., 2005; Hastie et al., 2009). In this case, we can convert the cosine similarity to the angular similarity which is restricted to [0, 1]. The angular similarity can be converted to the angular distance, which is a proper distance metric. Conversely, the cosine dissimilarity is not a distance measure since it does not satisfy the triangle inequality. In our study, we therefore rely on the angular similarity and angular distance to group comparable categories.

Using a selected (dis)similarity metric, we compute the proximity measure between all pairwise observations in the matrix with input features. We combine all values in a similarity matrix or dissimilarity matrix , which is used as input in a clustering algorithm. Most algorithms require these matrices to be symmetric (Hastie et al., 2009). In literature on unsupervised learning algorithms, clustering methods are typically divided into three different types: combinatorial algorithms, mixture modelling and mode seeking (Hastie et al., 2009). Both the mixture modelling and mode seeking algorithms rely on probability density functions. Conversely, the combinatorial algorithms do not rely on an underlying probability model and work directly on the data. In our paper we opt for a distribution-free approach and therefore focus on the combinatorial algorithms summarized in Section 3.2. For the interested reader, a detailed overview of these algorithms is given Appendix B.

l—L4.7cmL4.7cm[

code-before = 1,6,7,8,11,12

2,3,4,5,8,9,10

]

Algorithm Strengths Drawbacks

k-means - Well-known - Only suited for numeric

(MacQueen et al., 1967) features

- Simple and easy to implement - Sensitive to outliers and the initialization

- Computationally efficient - Local optima

k-medoids - Applicable to any feature type - Sensitive to the initialization

(Kaufman and Rousseeuw, 1990b) - Less sensitive to outliers - Local optima

Spectral clustering - Applicable to any feature type - Computationally expensive

(Hastie et al., 2009) - Less sensitive to outliers, initialization and local optima - Sensitive to the employed similarity metric

- Able to identify non-convex clustersa

HCAb - Applicable to any feature type - Computationally expensive

(Hastie et al., 2009) - Less sensitive to outliersc, initialization and local optima - Static; divisions or fusions of clusters are irrevocable

-

a

For every pair of points inside a convex cluster, the connecting straight line segment is within this cluster

-

b

Hierarchical clustering analysis

-

c

When using the single-linkage criterion

In most clustering techniques, the number of clusters can be considered a tuning parameter that needs to be carefully chosen from a range of possible (integer) values. Hereto, we require a cluster validation index to select the value for which results in the most optimal clustering solution. We divide the cluster validation indices into two groups: internal and external (Liu et al., 2013; Everitt et al., 2011; Wierzchoń and Kłopotek, 2019; Halkidi et al., 2001). Using external validation indices, we evaluate the clustering criterion with respect to the true partitioning (i.e. the actual assignment of the observations to different groups is known). Conversely, we rely on internal validation indices when we do not have the true cluster label at our disposal. With such indices, we evaluate the compactness and separation of a clustering solution. The compactness indicates how dense the clusters are and compact clusters are characterized by observations that are similar and close to each other. Clusters are well separated when observations belonging to different clusters are dissimilar and far from each other. Consequently, we employ internal validation indices to choose the value for which results in compact clusters that are well separated (Liu et al., 2013; Everitt et al., 2011; Wierzchoń and Kłopotek, 2019).

Several internal validation indices exist and each index formalizes the compactness and separation of the clustering solution differently. An extensive overview of internal (and external) validation indices is given in Liu et al. (2013), Wierzchoń and Kłopotek (2019) and in the benchmark study of Vendramin et al. (2010). The authors concluded that the silhouette and Caliński-Harabasz (CH) indices are superior compared to other validation criteria. While these indices are well-known within cluster analysis (Wierzchoń and Kłopotek, 2019; Govender and Sivakumar, 2020; Vendramin et al., 2010), the results of Vendramin et al. (2010) do not necessarily generalize to our data set. We therefore include two additional, commonly used criteria: the Dunn index and Davies-Bouldin index. Table 8 shows how these four indices are calculated. For the Caliński-Harabasz, Dunn and silhouette index, higher values are associated with a better clustering solution. Conversely, for the Davies-Bouldin index, we arrive at the best partition by minimizing this criterion. A more in-depth discussion of these criteria can be found in Appendix C.

Numerous papers compared the performance of different clustering algorithms using different data sets and various evaluation criteria (Mangiameli et al., 1996; Costa et al., 2004; de Souto et al., 2008; Kinnunen et al., 2011; Jung et al., 2014; Kou et al., 2014; Rodriguez et al., 2019; Murugesan et al., 2021). They concluded that none of the considered algorithms consistently outperforms the others and that the performance is dependent on the type of data (Hennig, 2015; McNicholas, 2016a, b; Murugesan et al., 2021). The authors advise to compare different clustering methods using more than one performance measure. Consequently, we test the PHiRAT algorithm (see Algorithm 1) with all possible combinations of the selected clustering methods (i.e. k-medoids, spectral clustering and HCA, see Section 3.2) and internal validation criteria (i.e. Caliński-Harabasz index, Davies-Bouldin index, Dunn index and silhouette index, see Table 8).

4 Clustering NACE codes in a workers’ compensation insurance product

We use a workers’ compensation insurance data set from a Belgian insurer to illustrate the PHiRAT procedure. The portfolio consists of Belgian companies that are active in various industries and occupations. The database contains claim-related information, such as the number of claims and the claim sizes, over a course of eight years. Additionally, for each of the companies we have the corresponding NACE-Ins code (see Section 2). In this section, we demonstrate how to reduce the NACE-Ins to its essence using PHiRAT. Our end objective is to incorporate the reduced version of the hierarchical MLF as a risk factor in a technical pricing model as discussed in Campo and Antonio (2023). We therefore also assess the effect of clustering on the predictive accuracy. Furthermore, if the reduced structure properly captures the essence, the predictive accuracy should generalize to out-of-sample and out-of-time data. We employ PHiRAT using the training data set, which contains data from the first seven years, to construct the reduced hierarchical risk factor. To examine the generalizability of the reduced structure to out-of-sample and out-of-time data, we use the test data set which contains data from the eight and most recent year.

4.1 Exploring the workers’ compensation insurance database

Claim-related information at the company level

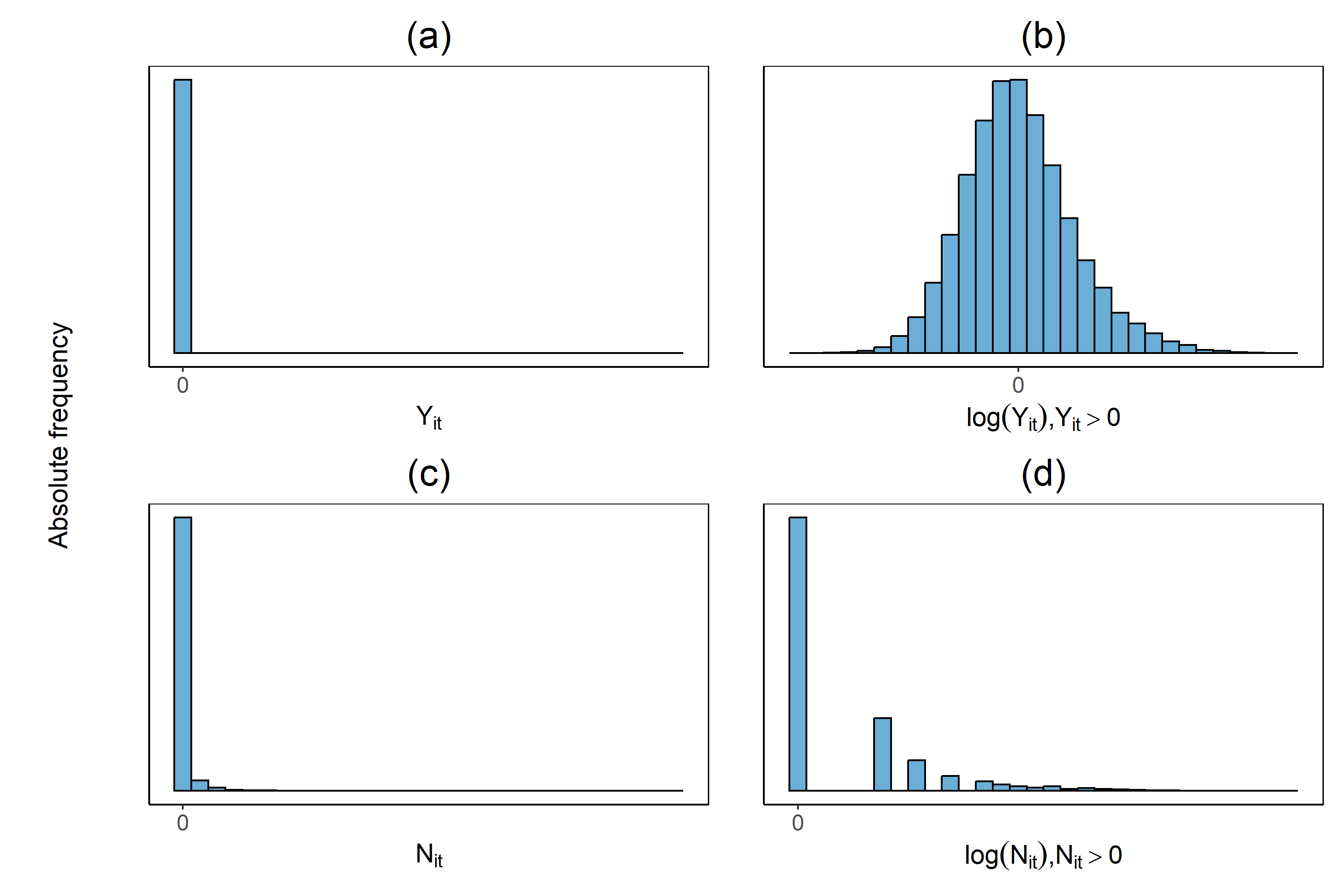

We first explore the distribution of the claim-related information in our database. We consider the damage rate and the number of claims of company in year . When calculating (see equation (1)), we use the capped claim amount for company in year to prevent that large losses have a disproportionate impact on the results (see Campo and Antonio (2023) for details on the capping procedure). To account for inflation and for the size of the company, we express the damage rate per unit of company- and year-specific salary mass . Figure 3 depicts the empirical distribution of the damage rates and number of claims of the individual companies. A strong right skew is visible in the empirical distribution of the (Figure 3(a)) and the (Figure 3(c)). Moreover, this right skewness persists in the log transformed counterparts (see panels (b) and (d) in Figure 3).

Claim-related information at different levels in the NACE-Ins hierarchy

The NACE-Ins partitions the companies according to their economic activity, at varying levels of granularity. We compute the category-specific weighted average damage rate and claim frequency at all levels in the hierarchy. Considering the top level in the hierarchy (as explained in Section 2), we calculate the weighted average damage rate for category as

| (6) |

and the expected claim frequency as

| (7) |

We then calculate the weighted average damage rate and expected claim frequency for child-category within parent-category as

| (8) |

When we consider more granular levels in the hierarchy, the computation is similar. To calculate these quantities for a specific category, we only use observations that are classified herein.

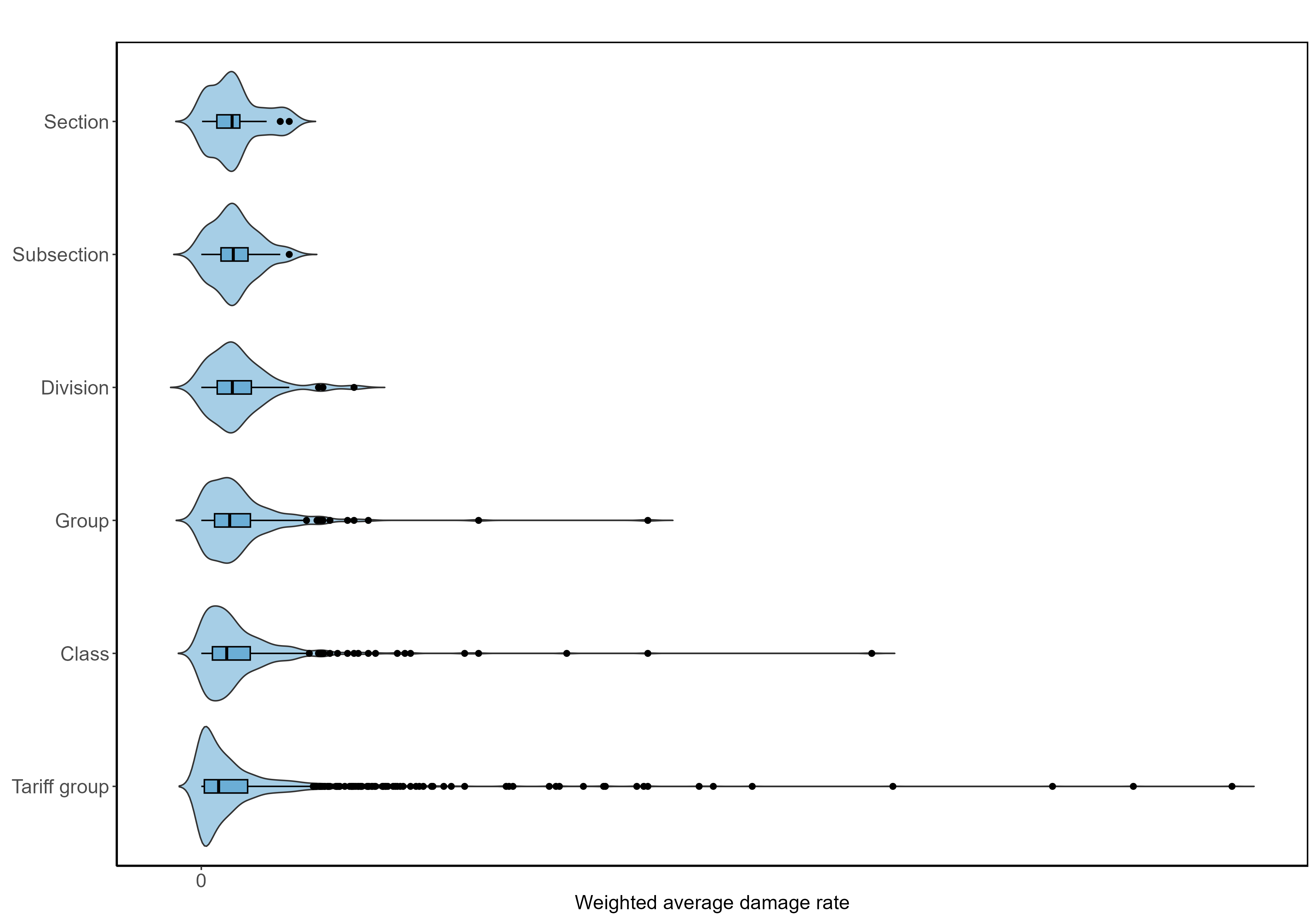

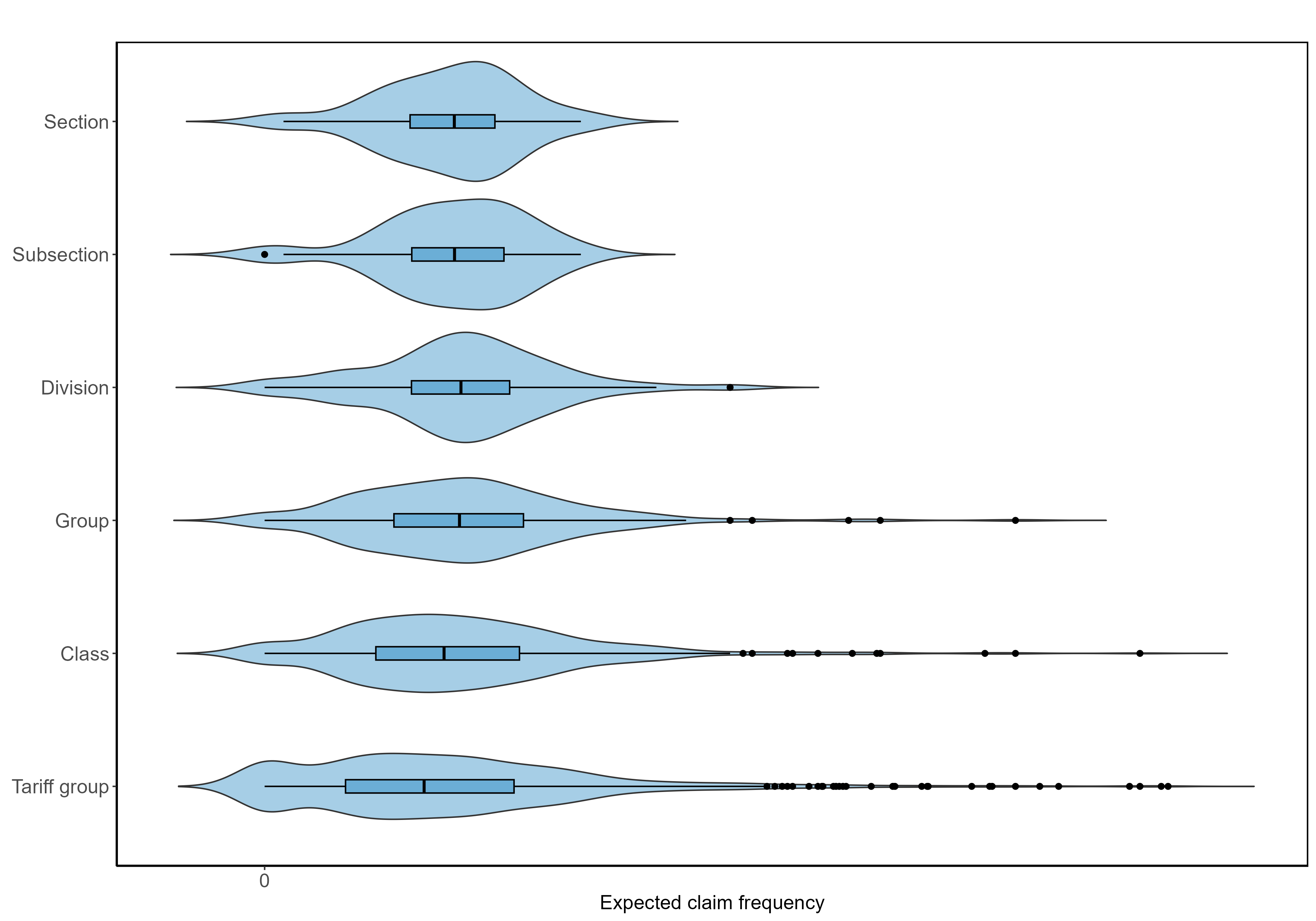

At different levels in the hierarchy, the empirical distribution of the category-specific weighted average damage rates and expected claims frequencies show a strong right skew (see Appendix Appendix D). The large range in values hinders the visual comparison of the weighted average damage rates and expected claim frequencies across categories at different levels in the hierarchy. We therefore apply a transformation solely for the purpose of visual comparison. Illustrating the procedure with , we first apply the following transformation

| (9) |

since we have categories for which . Hereafter, we cap using

| (10) |

where denotes the quantile of and IQR denotes the interquartile range of . The lower and upper bound of correspond to the inner fences of a boxplot (Schwertman et al., 2004). By transforming and capping the quantities, we focus on the pattern seen in the majority of the categories. Additionally, this facilitates the visual comparison across different categories.

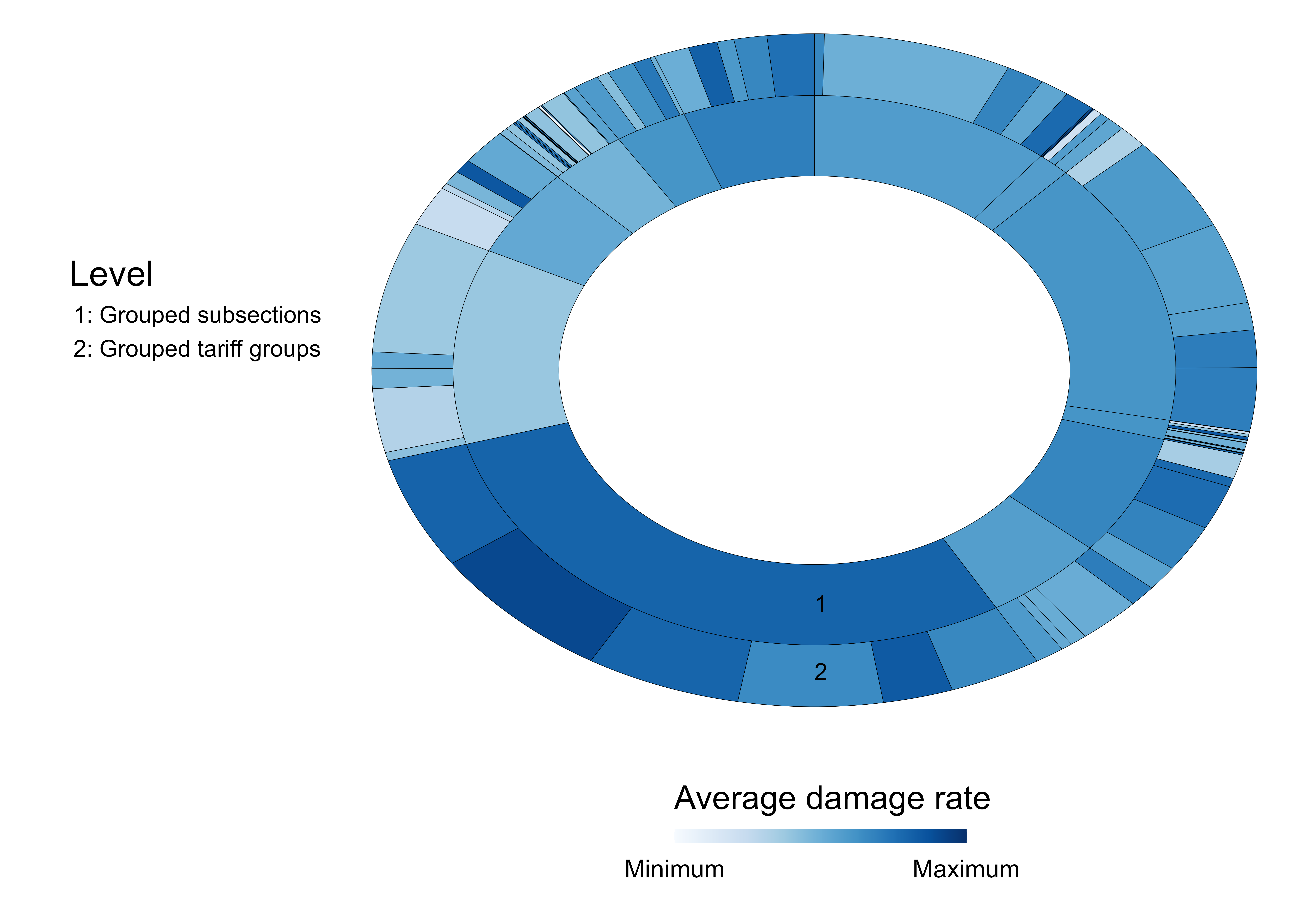

LABEL:fig:AvgDR visualizes the category-specific weighted average damage rates and salary masses. Panel (a) depicts the category-specific weighted averages at all levels in the hierarchy, panel (b) is close-up of the top right portion of panel (a) and panel (c) represents the averages at the subsection and tariff group level. We use a colour gradient for the weighted average damage rate. The darker the colour, the higher the weighted average damage rate. Further, each ring in the circle corresponds to a specific level in the hierarchy and the level is depicted by the number in the ring. To represent the categories at a specific level, the rings are split into slices proportional to the corresponding summed salary mass. The bigger the slice, the larger the summed salary mass that corresponds to a specific category at the considered level in the hierarchy. To preserve the confidentiality of the data, we randomly assign Greek letters to each of the categories at the section level.

At all levels in the hierarchy, there is variation in the category-specific weighted average damage rates. This is demonstrated in LABEL:fig:AvgDR(b), displaying a magnified view of the top right section of LABEL:fig:AvgDR(a). Here, the blue tone varies between the child categories of parent category at the section level. Additionally, at all levels in the hierarchy, there are categories with a low summed salary mass (e.g. at the section level). In LABEL:fig:AvgDR, this is depicted by the thin slices. These categories represent only a small part of our portfolio. Furthermore, most of the categories with a low salary mass have a less granular representation in the NACE system, having very few child categories compared to other categories. For example, the parent category at the section level, has a low salary mass and only a limited number of child categories across all levels in the hierarchy of the NACE system.

LABEL:fig:AvgCF depicts the category-specific expected claim frequency and salary masses. Similarly to LABEL:fig:AvgDR, we use a colour gradient for the claim frequencies and the size of a slice is again proportional to the summed salary mass. Overall, the findings are comparable to LABEL:fig:AvgDR. The category-specific expected claim frequency varies between the categories at all levels in the hierarchy.

Following, we focus only on the subsection and tariff group level. The category-specific weighted average damage rates and expected claim frequencies at the subsection and tariff group level are shown in LABEL:fig:AvgDR(c) and LABEL:fig:AvgCF(b), respectively. To illustrate PHiRAT, we group similar categories at these levels in the hierarchy and hereby, reduce the granularity of the hierarchical risk factor.

4.2 Engineering features to improve clustering results

Feature engineering is crucial to obtain a reliable clustering solution through PHiRAT. As discussed in Section 2.2, we therefore engineer a set of features to capture the riskiness and the economic activity of the categories. The estimated random effect from the damage rate and claim frequency model expresses the category-specific riskiness at the subsection and tariff group level. Further, we use LMMs to fit the damage rate random effects models in (2) and (4). LMMs are less complex, computationally more efficient and are less likely to experience convergence problems compared to GLMMs. Alternatively, we can consider Tweedie GLMMs to model the damage rate. We refer the reader to Campo and Antonio (2023) for a discussion on the effect of the distributional assumption on the response. We use embeddings to encode the category’s textual labels that describe the economic activity. In our database, we have a description for every category at the subsection and tariff group level.

To encode the textual information, we rely on pre-trained encoders. The first pre-trained encoder we use is a Word2Vec model (Mikolov et al., 2013) trained on part of the Google News data set that contains approximately 100 billion words (https://code.google.com/archive/p/word2vec/). This encoder is only able to give vector representations of words. As a result, when encoding a sentence for example, we get a separate vector for each word in the sentence. To obtain a single embedding for a sentence, we first remove stop words (e.g. the, and, ) and then take the element-wise average of the embedding vectors of the individual words (Troxler and Schelldorfer, 2022). We also use the Universal Sentence Encoder (USE) trained on Wikipedia, web news, web question-answer pages and discussion forums (Cer et al., 2018) (https://tfhub.dev/google/collections/universal-sentence-encoder/1). There are two different versions, v4 and v5, which are specifically designed to encode greater-than-word length text (i.e. sentences, phrases or short paragraphs). In our paper, we use both versions.

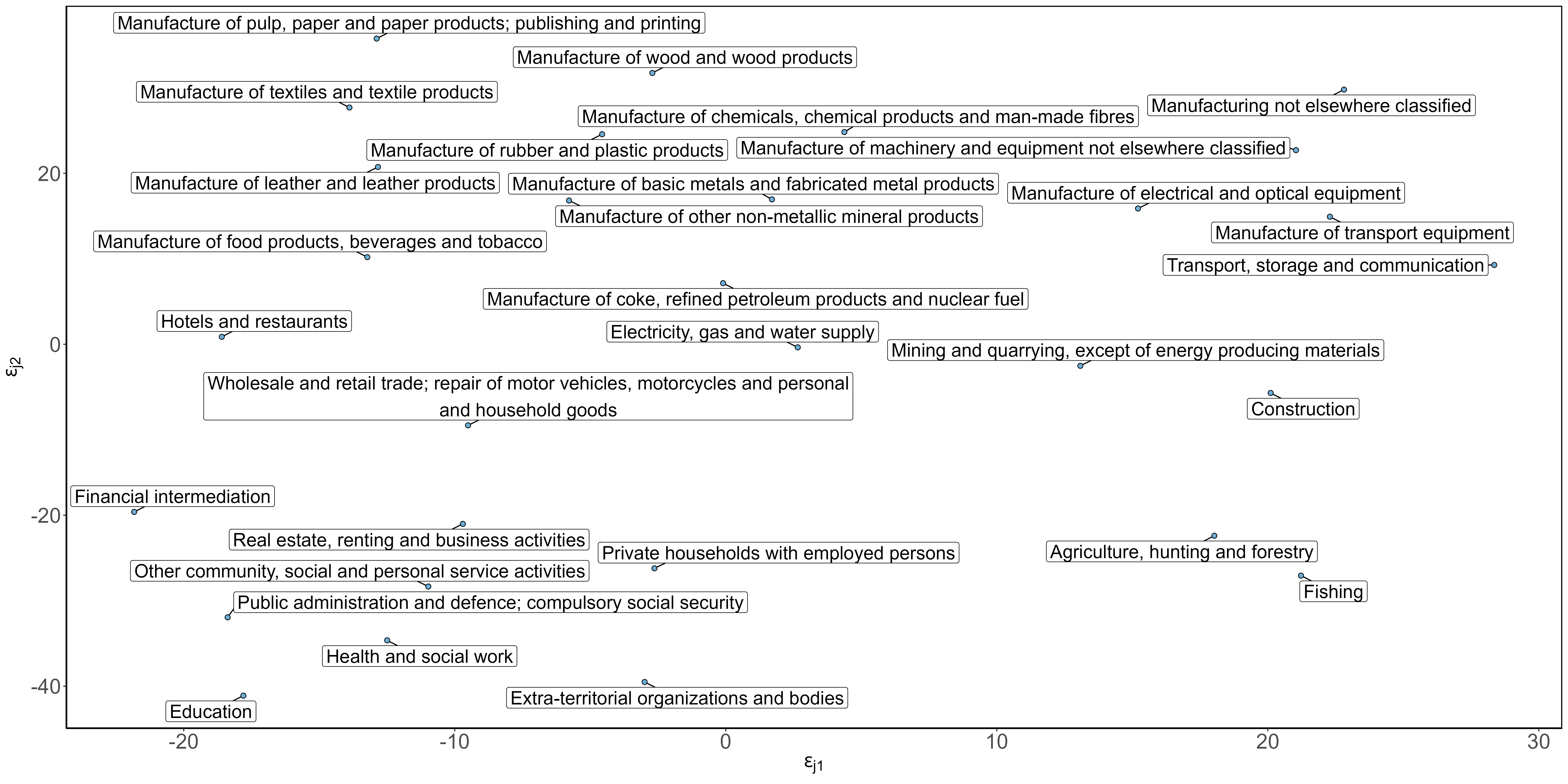

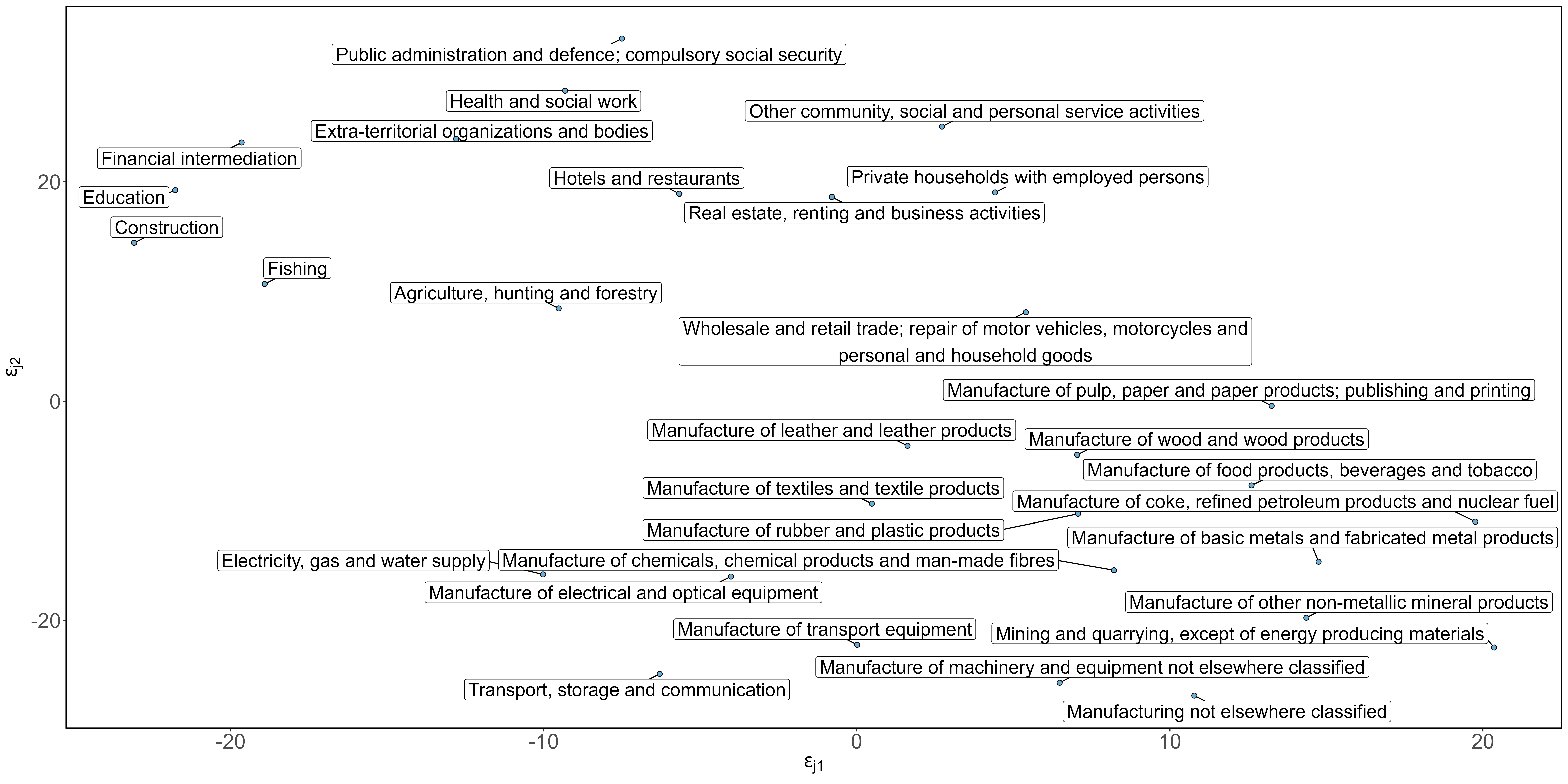

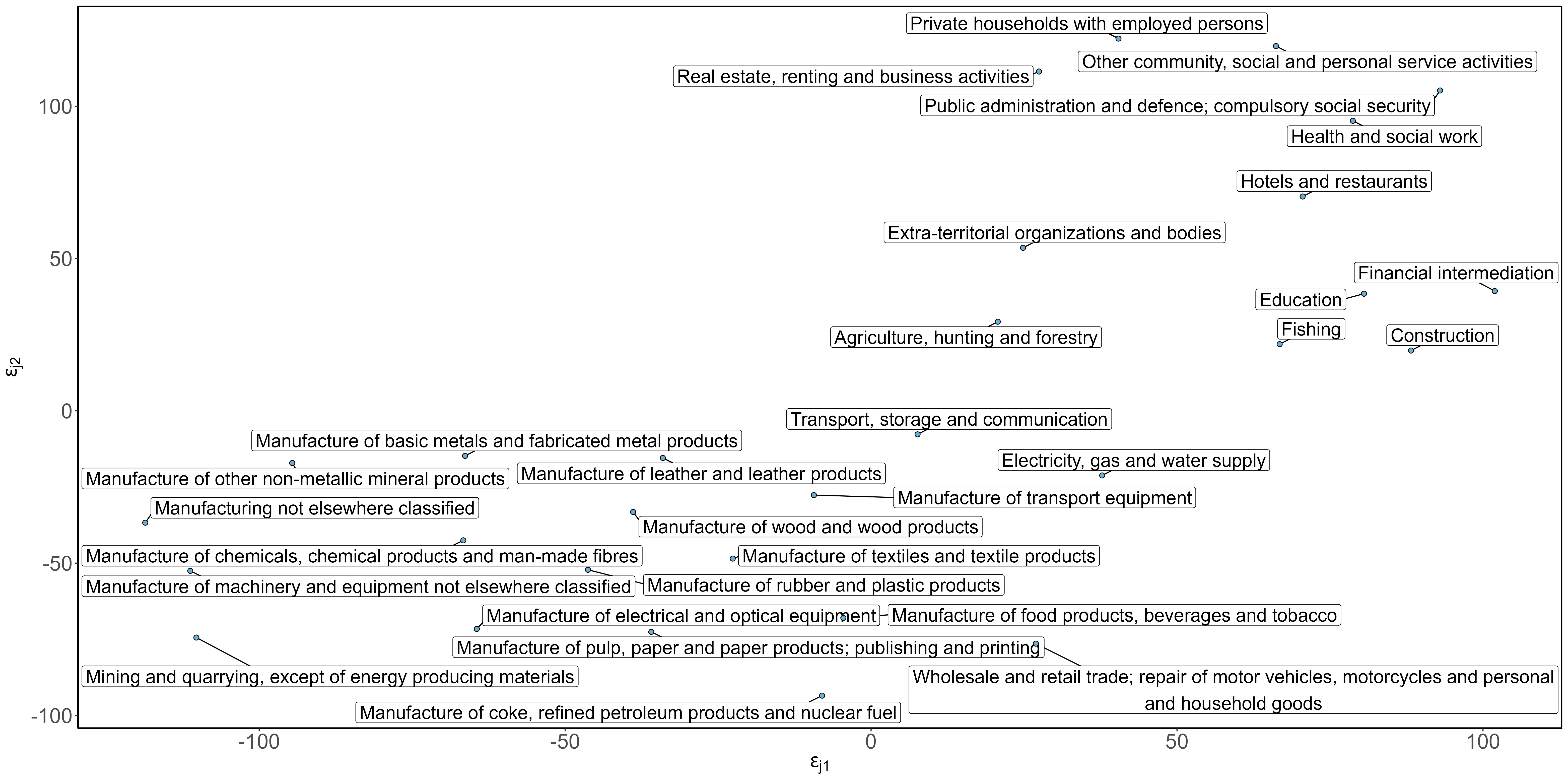

The pre-trained Word2Vec encoder outputs a 300-dimensional embedding vector and the USEs a 512-dimensional vector. To assess the quality of the resulting embeddings, we inspect whether embeddings of related economic activities lie close to each other in the vector space. We employ the dimension reduction technique t-distributed stochastic neighbour embedding (t-SNE) (Van Der Maaten and Hinton, 2008) to obtain a two-dimensional visualization of the embeddings constructed for different categories at the subsection level (see LABEL:fig:AvgCF). We opt to reduce the dimensionality to two dimensions, since it allows for an easy representation of the information in a scatterplot. t-SNE maps the high-dimensional embedding vector for category into a lower dimensional representation whilst preserving its structure, enabling the visualization of relationships and the identification of patterns and groups. Figure 4 visualizes the low-dimensional representation of the embeddings resulting from the pre-trained Word2Vec encoder (see Appendix E for similar figures of USE v4 and v5).

In Figure 4 we see that the embeddings of economically similar activities lie close to each other. All manufacturing related activities are situated at the top of the plot and in the left bottom corner, we have mostly activities that have a social component (e.g., education). In the right bottom corner, we have activities related to the exploitation of natural resources. Further, the more unrelated the activities are, the bigger the distance between their embedding vectors. For example, financial intermediation () and transport, storage and communication () lie at opposite sides of the plot.

4.3 Clustering subsections and tariff groups using PHiRAT

We illustrate the effectiveness of PHiRAT by applying it to cluster categories at the subsection and tariff group level, using the training set. We slightly adjust Algorithm 1 to ensure that each of the resulting categories at the subsection and tariff group level has sufficient salary mass. The minimum salary mass is based on previous analyses of the insurance company and we need to adhere to this minimum during clustering. Further, as discussed at the end of Section 3, we run PHiRAT with all possible combinations of the clustering methods (i.e. k-medoids, spectral clustering and HCA) and internal validation criteria (i.e. Caliński-Harabasz index, Davies-Bouldin index, Dunn index and silhouette index). Per run, a specific combination is used to cluster the categories at all levels in the hierarchy.

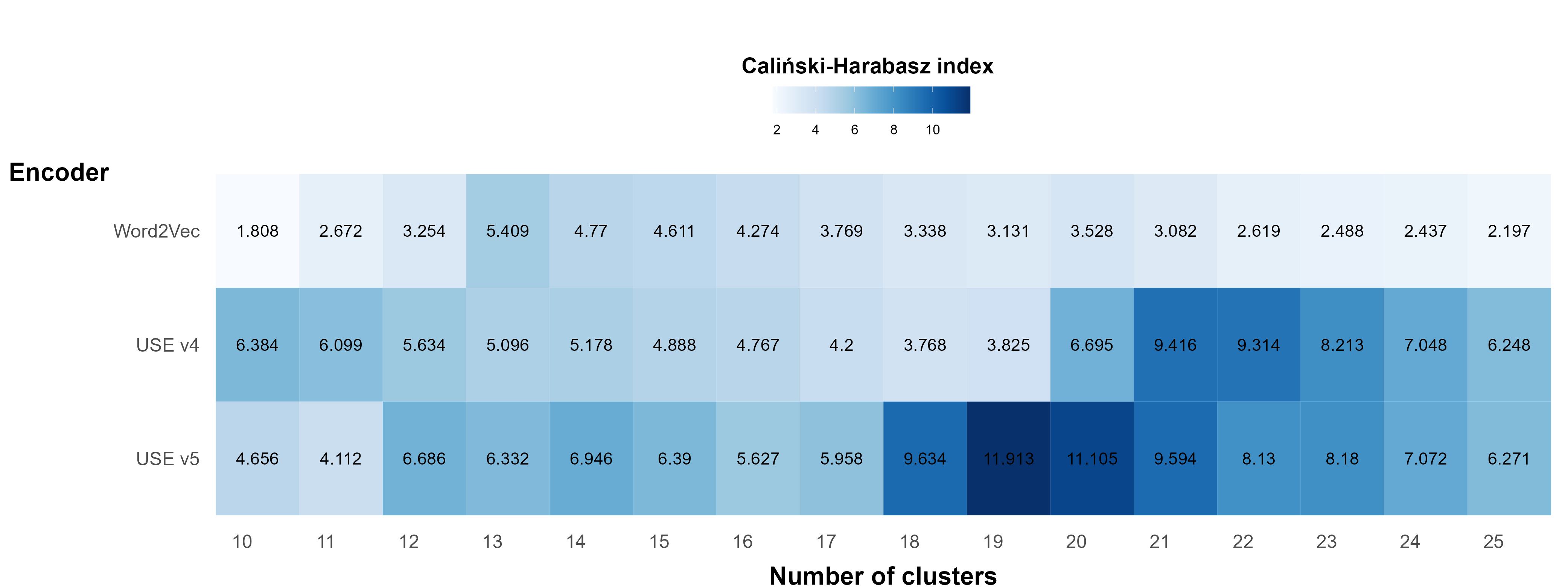

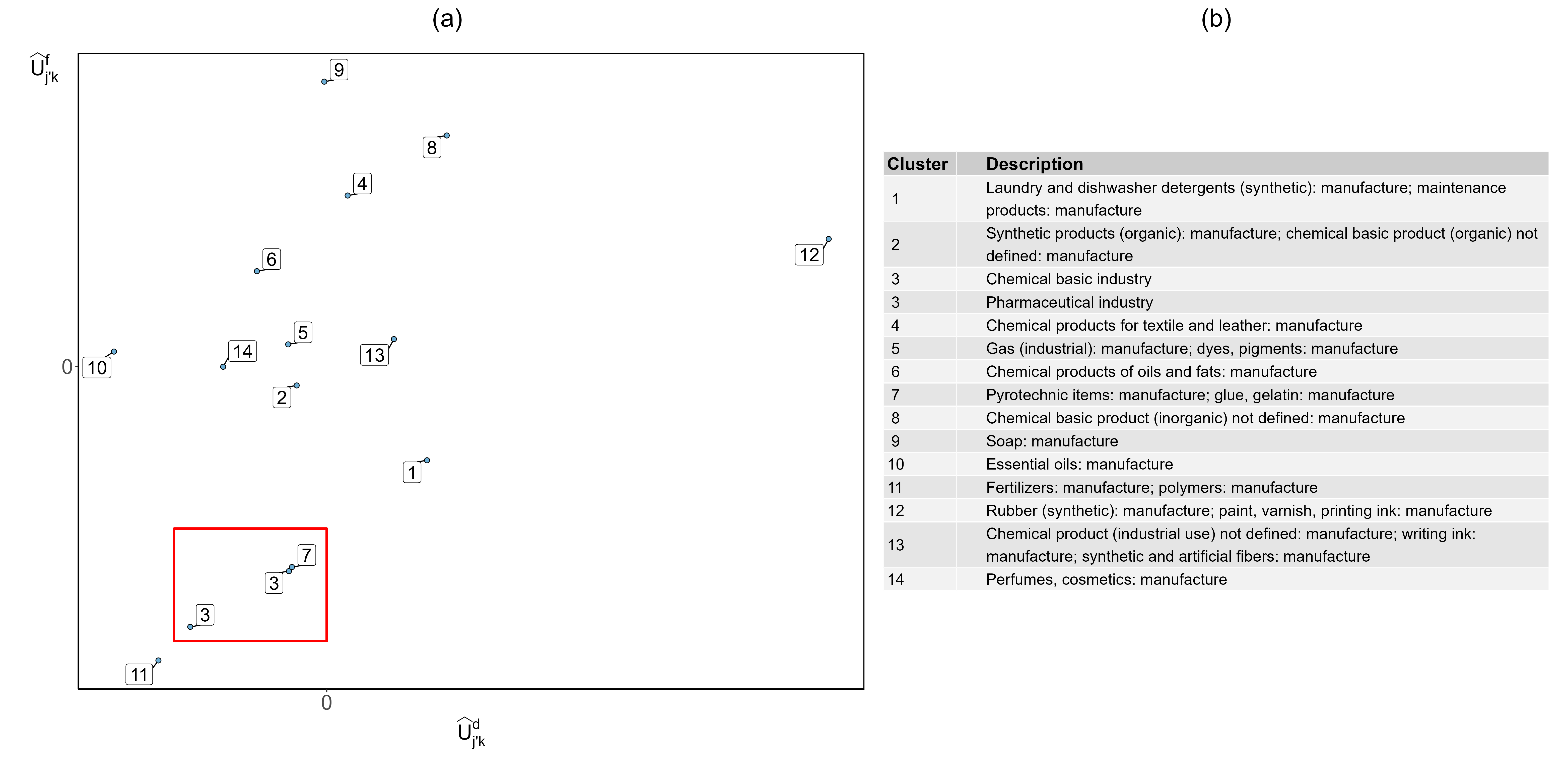

Figure 2 visualizes how PHiRAT works its way down the hierarchy. We start at the subsection level and construct the feature matrix . Part of is built using an encoder to capture the textual information (see Section 2.2 and Section 4.2). In our paper, we consider three different pre-trained encoders: (a) Word2Vec; (b) USE v4 and (c) USE v5. We use these encoders to obtain the embeddings and construct three separate feature matrices: (a) ; (b) and (c) . All three feature matrices contain the same estimated random effects vectors and . The difference between the feature matrices is that the embeddings are encoder-specific. Next, we define a tuning grid for the number of clusters . In combination with the encoder-specific feature matrices, this results in a search grid of three (i.e. the encoder-specific feature matrices) by 16 (i.e. the possible values for the number of clusters). For every combination in this grid, we run the clustering algorithm to obtain a clustering solution and calculate the value of the internal validation criterion. We select the combination that results in the most optimal clustering solution according to the validation measure. Figure 5 provides a visualization of this search grid. In this figure, we use k-medoids as clustering algorithm, the CH index as internal validation measure and we use a colour gradient for the value of the validation criterion. The darker the colour, the higher the value and the better the clustering solution. The -axis depicts the tuning grid for and the -axis the encoder-specific feature matrices. The CH index is highest () for in combination with . According to the selected validation measure, this specific combination results in the most optimal clustering solution. Hence, we use this clustering solution to group the categories into clusters (see Figure 2). Hereafter, we merge clusters with neighbouring clusters until each cluster has sufficient salary mass.

Next, we proceed to cluster the categories at the tariff group level. Within each cluster at the section level, we first group consecutive categories (i.e. those with consecutive NACE codes, see Section 2.1) at the tariff group level to ensure that the salary mass is sufficient for every category. As before, we construct three encoder-specific versions of . We then iterate over every parent category to group the child categories. At iteration , we use as input in a clustering algorithm. At the tariff group level, we use the tuning grid . Here denotes the total number of child categories of parent category . We select the combination of the encoder-specific feature matrix and that results in the most optimal clustering solution to group the categories , nested within , into subclusters (see Figure 2).

Distance measures and evaluation metrics

For k-medoids clustering and HCA we use the angular distance (see Section 3.2), as both algorithms require a distance or dissimilarity measure. For spectral clustering we use the angular similarity. We also need to define a distance measure for the selected internal evaluation criteria, except for the CH index. Hereto, we define as the angular distance. We calculate the evaluation criteria using all engineered features. However, since a large part of the feature vector consists of the high-dimensional embedding vector, too much weight might be given to the similarity in economic activity when choosing the optimal cluster solution. Therefore, we also evaluate a second variation of the internal evaluation criteria. When calculating the criteria, we remove the embedding vectors from the feature matrices. As such, we focus on constructing a clustering solution that is most optimal in terms of riskiness. In this evaluation we use the Euclidean distance for . Hence, at the subsection level, we define where . Similarly, at the tariff group level, and . In what follows we discuss the results obtained with this approach. Results obtained with the complete feature vector, including the embedding, are given in Appendix F.

Implementation

We perform the main part of the analysis using the statistical software R (R Core Team, 2022). For k-medoids and HCA, we rely on the cluster (Maechler et al., 2022) and stats package, respectively. For spectral clustering, we follow the implementation of Ng et al. (2001) and developed our own code. Spectral clustering partially depends on the k-means algorithm to obtain a clustering solution (see Appendix B). However, k-means is sensitive to the initialization and can get stuck in an inferior local minimum (Fränti and Sieranoja, 2019). One way to alleviate this issue is by repeating k-means with different initializations and to select the most optimal clustering solution. Hence, to prevent that spectral clustering results in a suboptimal clustering solution, we repeat the k-means step a 100 times.

4.4 Evaluating the clustering solution

The main aim of our procedure is to reduce the cardinality of a hierarchically structured categorical variable, which can then be incorporated as a risk factor in a predictive model to underpin the technical price list (Campo and Antonio, 2023). Ideally, we maintain the predictive accuracy whilst reducing the granularity of the risk factor. As discussed in Section 4.3, we employ PHiRAT to group similar categories at the subsection and tariff group level. We refer to the less granular version of the hierarchical risk factor as the reduced risk factor.

To assess the predictive accuracy of a clustering solution, we fit an LMM

| (11) |

where the reduced risk factor enters the model through the random effects and . We include the salary mass as weight. We opt for an LMM given its simplicity and computational efficiency (Campo and Antonio, 2023). Next, we calculate the predicted damage rate as for the training and test set as introduced in the beginning of Section 4.

Benchmark clustering solution

To evaluate the clustering solution obtained with the proposed data-driven approach, we need to compare it to a benchmark where we do not rely on PHiRAT. One possibility is to fit (11) with the nominal variable composed of the original categories at the subsection and tariff group level. However, this results in negative variance estimates and yields incorrect random effect estimates. Consequently, to obtain a benchmark clustering solution, we start at the subsection level and merge consecutive categories until the salary mass is sufficient (e.g. 01 agriculture and 02 forestry). Hereafter, within each of the (grouped) categories at the subsection level, we group consecutive categories (e.g. 142121 and 142122) at the tariff group level. Again, we use the minimum salary mass as defined by the insurance company.

Performance measures

Using the predicted damage rates on the training and test set, we compute the Gini-index (Gini, 1921) and loss ratio. The Gini-index assesses how well a model is able to distinguish high-risk from low-risk companies and is considered appropriate for the comparison of competing pricing models (Denuit et al., 2019; Campo and Antonio, 2023). The higher the value, the better the model can differentiate between risks. The Gini-index has a maximum theoretical value of 1. The loss ratio measures the overall accuracy of the fitted damage rates and is defined as , where denotes the total capped claim amount and the total fitted claim amount. To obtain , we transform the individual predictions as (see equation (1))

| (12) |

Due to the balance property (Campo and Antonio, 2023), the loss ratio is one when calculated using the training data set. We therefore compute the loss ratio only for the test set.

Predictive performance

Table 9 depicts the performance of the different clustering solutions on the training and test sets. In this table, denotes the total number of grouped categories at the subsection level and denotes the total number of grouped categories at the tariff group level. With the benchmark clustering solution, we end up with a large number of different categories at both hierarchical levels ( separate categories in total). Conversely, with our data-driven approach the maximum is 221 (14 + 207; k-medoids with Davies-Bouldin index) and the minimum is 97 (10 + 87; k-medoids with the CH index). Consequently, PHiRAT substantially reduces the number of categories. Moreover, we are able to retain the predictive performance. On both the training and test set, the Gini-indices of nearly all clustering solutions are higher than the Gini-index of the benchmark solution. Hence, we are better able to differentiate between high- and low-risk companies with the clustering solutions. On the training data set, the highest Gini-indices are seen for the k-medoids algorithm using the silhouette index and the spectral clustering algorithm using the Dunn index. On the test set, spectral clustering using the CH index and silhouette index result in the highest Gini-index whereas the benchmark has the lowest Gini-index. However, the loss ratio of most clustering solutions is higher than the loss ratio of the benchmark clustering solution (= 1.006). This indicates that, when we use the reduced risk factor in an LMM, we generally underestimate the total damage. One exception is the clustering solution resulting from HCA using the Davies-Bouldin index, which has the same loss ratio as the benchmark (= 1.006). In addition, for this solution the Gini-index is among the highest (0.675 on the training and 0.616 on the test set). Using the result from HCA with the Davies-Bouldin index, we are able to reduce the total number of categories to 207 (= 14 + 193). Compared to the benchmark solution, we obtain the same overall predictive accuracy (i.e. the loss ratio is approximately equal) and we can better differentiate between high- and low-risk companies.

| Training | Test | ||||

|---|---|---|---|---|---|

| Gini-index | Gini-index | Loss ratio | |||

| Benchmark | 18 | 641 | 0.658 | 0.585 | 1.006 |

| HCA: | |||||

| Silhouette index | 13 | 100 | 0.667 | 0.596 | 1.007 |

| Dunn index | 15 | 202 | 0.656 | 0.599 | 1.011 |

| Davies-Bouldin index | 14 | 193 | 0.675 | 0.616 | 1.006 |

| CH index | 15 | 140 | 0.667 | 0.614 | 1.010 |

| k-medoids: | |||||

| Silhouette index | 12 | 107 | 0.678 | 0.613 | 1.008 |

| Dunn index | 10 | 130 | 0.657 | 0.598 | 1.010 |

| Davies-Bouldin index | 14 | 207 | 0.670 | 0.619 | 1.010 |

| CH index | 10 | 87 | 0.676 | 0.605 | 1.011 |

| Spectral clustering: | |||||

| Silhouette index | 12 | 86 | 0.673 | 0.628 | 1.012 |

| Dunn index | 12 | 143 | 0.677 | 0.624 | 1.010 |

| Davies-Bouldin index | 12 | 166 | 0.669 | 0.618 | 1.010 |

| CH index | 12 | 102 | 0.670 | 0.628 | 1.013 |

The clustering solution resulting from HCA with the Davies-Bouldin index offers a good balance between reducing granularity and enhancing differentiation whilst preserving predictive accuracy. If, however, a sparse representation and good differentiation is more important than the overall predictive accuracy, the result from spectral clustering with the silhouette index is a better option. The latter clustering solution is visualized in Figure 6. This figure is similar to LABEL:fig:AvgDR(a) and depicts the cluster-specific weighted average damage rates at the subsection and tariff group level. The two figures show that PHiRAT substantially reduces the total number of categories (12 + 86 = 98). Furthermore, spectral clustering with the silhouette index is one of the combinations that results in the best differentiation between high- and low-risk companies (Gini index is 0.673 and 0.628 on the training and test set, respectively).

Interpretability

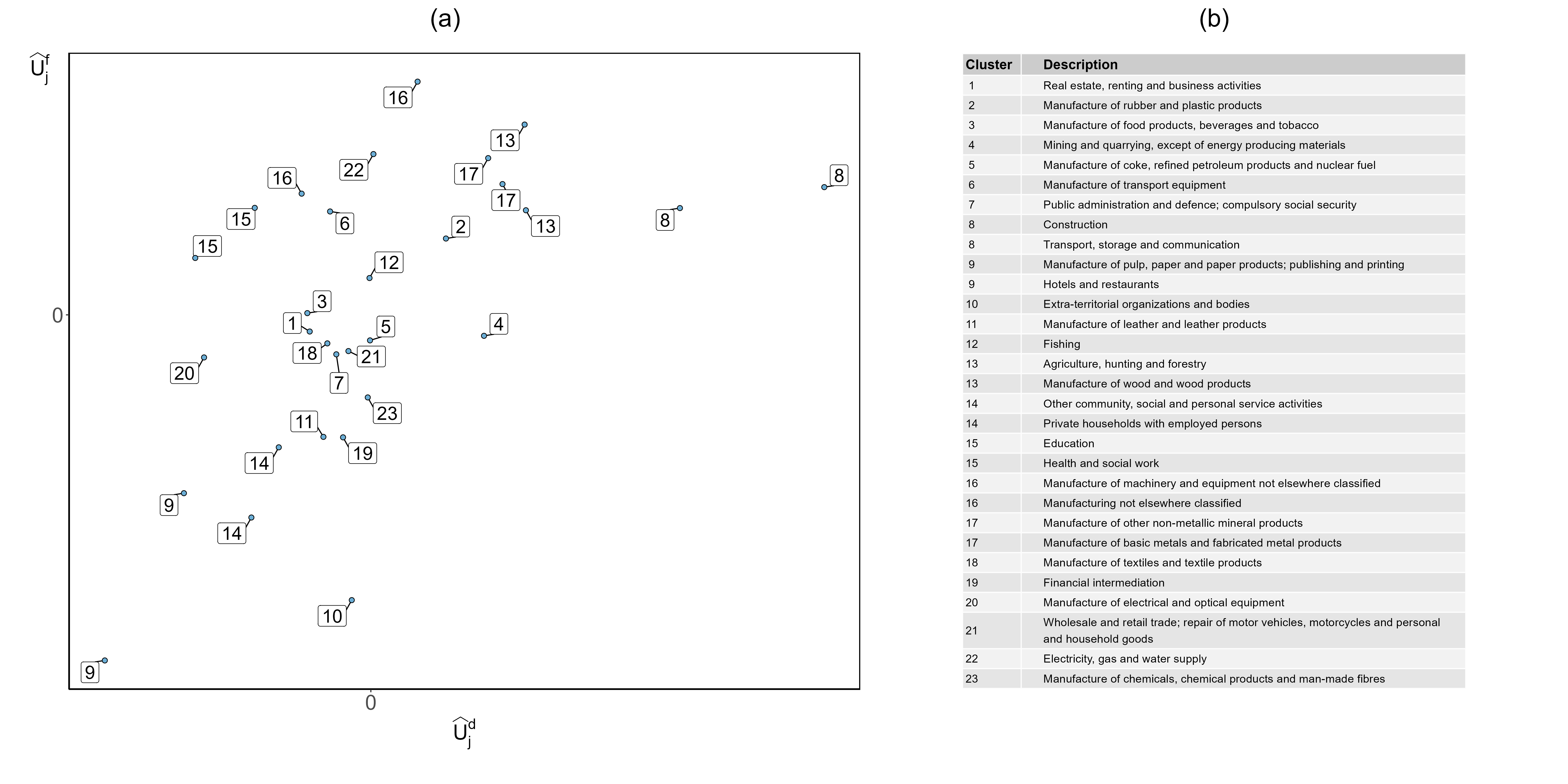

After clustering, it is imperative to evaluate the interpretability of the solution. The grouping should provide us with meaningful insights into the underlying structure of the data. Building on the strong predictive performance of the solution resulting from spectral clustering with the silhouette index, we examine this specific clustering solution in more detail.

Figure 7 visualizes which categories are clustered at the subsection level. At this point we have not yet merged neighbouring clusters to ensure sufficient salary mass (see Section 4.3). Figure 7(a) shows the and of the fitted damage rate and claim frequency random effects models (see (2) and (3)). The number in the plot indicates which cluster the categories are appointed to. The description of the category’s economic activity is given in Figure 7(b). In total we have 24 clusters, 19 of which consist of a single category. Inspecting the clusters in detail, we find that the riskiness and economic activity of grouped categories are similar. Moreover, categories that are similar in terms of riskiness (i.e. those with similar random effect estimates) but different in economic activity are assigned to different clusters. For example, the ’s and ’s are similar for: a) manufacture of rubber and plastic products; b) agriculture, hunting and forestry; c) manufacture of wood and wood products; d) manufacture of other non-metallic mineral product and e) manufacture of basic metals and fabricated metal products. These industries are partitioned into three clusters. The category in cluster 2 (i.e. manufacture of rubber and plastic products) manufactures organic products. Conversely, the categories in cluster 17 (i.e. manufacture of other non-metallic mineral product and manufacture of basic metals and fabricated metal products) use inorganic materials and the categories in cluster 13 (i.e. agriculture, hunting and forestry and manufacture of wood and wood products) utilize products derived from plants and animals.

Figure 8 depicts the clustered categories at the tariff group level, nested within category manufacture of chemicals, chemical products and man-made fibres at the subsection level. The and of the fitted damage rate and claim frequency random effects model (see (4) and (5)) are shown in the left panel of Figure 8 and the textual information in the right panel. When the text is separated by a semicolon, this indicates that categories are merged before clustering to ensure sufficient salary mass (see Section 4.3). Similar to Figure 7, both the riskiness and economic activity are taken into account when grouping categories. This is best illustrated for the categories in the red rectangle in Figure 8(a). Herein, we have three categories: (a) pyrotechnic items: manufacture; glue, gelatin: manufacture; (b) chemical basic industry and (c) pharmaceutical industry. Of these, pyrotechnic items: manufacture; glue, gelatin: manufacture (number 7 in the top right corner of the red rectangle) and chemical basic industry (number 3 in the top right corner of the red rectangle) have nearly identical random effect estimates. Notwithstanding, both categories are not grouped. Instead, the category chemical basic industry is merged with pharmaceutical industry (number 3 in the bottom left corner). The latter two categories manufacture chemical compounds. In addition, companies in chemical basic industry mainly produce chemical compounds that are used as building blocks in other products (e.g. polymers). Building blocks (or raw materials) that are needed by companies involved in manufacturing pyrotechnic items, glue and gelatin (e.g. glue is typically made from polymers (Ebnesajjad, 2011)).

5 Discussion

This paper presents the data-driven PHiRAT approach to reduce a hierarchically structured categorical variable with a large number of categories to its essence, by grouping similar categories at every level in the hierarchy. PHiRAT is a top-down procedure that preserves the hierarchical structure. It starts with grouping categories at the highest level in the hierarchy and proceeds to lower levels. At a specific level in the hierarchy, we first engineer several features to characterize the profile and specificity of each category. Using these features as input in a clustering algorithm, we group similar categories. The procedure stops once we grouped the categories at the lowest level in the hierarchy. When deployed in a predictive model, the reduced structure leads to a more parsimonious model that is easier to interpret, less likely to experience estimation problems or to overfit. Further, the increased number of observations of grouped categories leads to more precise estimates of the category’s effect on the response.

Using a workers’ compensation insurance portfolio from a Belgian insurer, we illustrate how to employ PHiRAT to reduce the granular structure of the NACE code. Using PHiRAT, we are able to substantially reduce the dimensionality of this hierarchical risk factor whilst maintaining its predictive accuracy. The reduced risk factor allows for better differentiation, has the same overall precision as the original risk factor and the grouping seems to generalize well to out-of-sample data. Moreover, the resulting clusters consist of categories that are similar in terms of riskiness and economic activity. Furthermore, the results show that embeddings are an efficient and effective method to capture textual information.

Future research can aim to improve our proposed solution in multiple directions. The final clustering solution depends on the engineered features, the clustering algorithm and the cluster evaluation criterion. Constructing appropriate and reliable features when employing PHiRAT is crucial to obtain a good clustering solution. In our paper, we rely on random effects models to capture the riskiness of the categories. Alternatively, we can characterize the risk profile using entity embeddings (Guo and Berkhahn, 2016). Here, we train a neural network to create entity embeddings that map the categorical values to a continuous vector, ensuring that categories with similar response values are located closer to each other in the embedding space. Additionally, we advise to run PHiRAT using different clustering algorithms and cluster evaluation criteria, since no algorithm consistently outperforms the others (Hennig, 2015; McNicholas, 2016a, b; Murugesan et al., 2021). Further, NLP is a rapidly evolving field and we only considered three pre-trained encoders. We did not include the pre-trained Bidirectional Encoder Representations from Transformers (BERT) model (Devlin et al., 2018), an encoder that is being increasingly used by actuarial researchers (see, for example, Xu et al. (2022); Troxler and Schelldorfer (2022)). Subsequent studies can assess whether BERT-based models result in higher quality embeddings, which in turn leads to better clustering solutions. In addition, researchers can employ alternative approaches to represent the parent-child relationships between categories in hierarchically structured data. Such as Argyrou (2009), for example, who formalizes the hierarchical relations using graph theory and applies a self-organizing map (Kohonen, 1995) to obtain a reduced representation of the hierarchical data.

Acknowledgements

We would like to express our deep gratitude to W.S., who played an important role in this research project. He provided us with valuable insights and expertise that helped shape our research.

References

References

- (1)

- Ahmad et al. (2019) Ahmad, A., Ray, S. K. and Aswani Kumar, C. (2019). Clustering mixed datasets by using similarity features. in ‘Sustainable Communication Networks and Application’. Lecture Notes on Data Engineering and Communications Technologies. Cham: Springer International Publishing. pp. 478–485.

- Argyrou (2009) Argyrou, A. (2009). Clustering hierarchical data using self-organizing map: A graph-theoretical approach. in ‘Advances in Self-Organizing Maps’. Vol. 5629 of Lecture Notes in Computer Science. Springer Berlin Heidelberg. Berlin, Heidelberg. pp. 19–27.

- Arora et al. (2020) Arora, S., May, A., Zhang, J. and Ré, C. (2020). Contextual embeddings: When are they worth it? arXiv: 2005.09117. Available at: https://arxiv.org/abs/2005.09117.

- Australian Bureau of Statistics and New Zealand (2006) Australian Bureau of Statistics and New Zealand (2006). Australian and New Zealand Standard Industrial Classification, (ANZSIC) 2006. Australian Bureau of Statistics : Statistics New Zealand.

- Breslow and Clayton (1993) Breslow, N. E. and Clayton, D. G. (1993). Approximate inference in generalized linear mixed models. Journal of the American Statistical Association 88(421), 9–25.

- Brown and Prescott (2006) Brown, H. and Prescott, R. (2006). Applied Mixed Models in Medicine. Wiley.

- Caliński and Harabasz (1974) Caliński, T. and Harabasz, J. (1974). A dendrite method for cluster analysis. Communications in Statistics 3(1), 1–27.

- Campo and Antonio (2023) Campo, B. D. and Antonio, K. (2023). Insurance pricing with hierarchically structured data an illustration with a workers’ compensation insurance portfolio. Scandinavian Actuarial Journal . Epub ahead of print, https://doi.org/10.1080/03461238.2022.2161413. https://doi.org/10.1080/03461238.2022.2161413

- Carrizosa et al. (2021) Carrizosa, E., Galvis Restrepo, M. and Romero Morales, D. (2021). On clustering categories of categorical predictors in generalized linear models. Expert Systems with Applications 182, 115245.

- Carrizosa et al. (2022) Carrizosa, E., Mortensen, L. H., Romero Morales, D. and Sillero-Denamiel, M. R. (2022). The tree based linear regression model for hierarchical categorical variables. Expert Systems with Applications 203, 117423.