Low-rank covariance matrix estimation for factor analysis in anisotropic noise: application to array processing and portfolio selection

Abstract

Factor analysis (FA) or principal component analysis (PCA) models the covariance matrix of the observed data as , where is the low-rank covariance matrix of the factors (aka latent variables) and is the diagonal matrix of the noise. When the noise is anisotropic (aka nonuniform in the signal processing literature and heteroscedastic in the statistical literature), the diagonal elements of cannot be assumed to be identical and they must be estimated jointly with the elements of . The problem of estimating and in the above covariance model is the central theme of the present paper. After stating this problem in a more formal way, we review the main existing algorithms for solving it. We then go on to show that these algorithms have reliability issues (such as lack of convergence or convergence to infeasible solutions) and therefore they may not be the best possible choice for practical applications. Next we explain how to modify one of these algorithms to improve its convergence properties and we also introduce a new method that we call FAAN (Factor Analysis for Anisotropic Noise). FAAN is a coordinate descent algorithm that iteratively maximizes the normal likelihood function, which is easy to implement in a numerically efficient manner and has excellent convergence properties as illustrated by the numerical examples presented in the paper. Out of the many possible applications of FAAN we focus on the following two: direction-of-arrival (DOA) estimation using array signal processing techniques and portfolio selection for financial asset management.

I Introduction and Problem Statement

We consider the following data model:

| (1) |

where {} are the observed data, is a transformation matrix, {} are the (unobserved or latent) factors, {} is the noise, and is the number of observations (or data samples). We assume that and are uncorrelated to one another and that the covariance matrices of the two terms in (1) are given by:

| (2) | ||||

It is also customary to assume that and that the data are independent and identically distributed. Under these assumptions the covariance matrix of can be written as:

| (3) |

(where depends on and in an obvious way).

The principal problem dealt with in this paper is the estimation of and in the above covariance model from data . Note that an orthogonal linear transformation of in (1) does not change (indeed for any that satisfies ) and therefore only the range of , can be uniquely estimated by means of a covariance fitting procedure. This is not a problem for most applications as in general an estimate of or suffices. However, as a preamble to the discussion in Section III, we note here that the model in (1) has other possible non-trivial ambiguities in the sense that even and corresponding to a given covariance matrix might not be unique. This is an important aspect of the parametrization in (1), from both a theoretical and practical standpoint, which will be discussed in Section III.

The central problem of FA or PCA is precisely the covariance matrix estimation problem stated above and there is a huge literature about it that goes back to the beginning of the previous century (see, e.g., [1, 2, 3, 4, 5]). Early applications were in psychometrics, econometrics and, more general, statistics; while more recent ones are in signal processing, marketing, biological sciences and, more general, big data analysis and machine learning. Even a partial review of the practical and theoretical works on FA and PCA published along the years is an immense task that we will not undertake. Instead we will refer only to the papers that we found to be directly relevant to the discussion and the approach presented in this paper. These papers, which include [6, 7, 8, 9, 10, 11, 12] and are discussed in the sections where they are most relevant, contain many references that can be consulted by the reader who is interested in the historical and more recent developments of the basic ideas and methods of FA and PCA.

II Critical review of previous methods

This section discusses three recently proposed methods for estimating the parameters of the covariance model in (3). While these methods appear to be state-of-the-art, we show that they are not without problems.

II-A Frobenius Norm Method

We will use the acronym to designate this method, with the index “o” being used to indicate the original version and distinguish it from the modified version presented later in the paper, which will be simply called FNM. Let

| (4) |

denote the sample covariance matrix (SCM). Quite possibly the most direct method for estimating and is via solving the following minimization problem:

| (5) |

where denotes the Frobenius norm. The following coordinate descent algorithm can be used to find the minimizers of the function in (5).

Input: , and .

For do:

-

•

Let denote the eigenvalues of () and let be the corresponding eigenvectors. Then, by a well-known result, the minimizer of , for given , is

(6) -

•

For given , the minimizer of is

(7) where, for any square matrix ,

-

•

If (where and for example) then goto Output; else and iterate.

Output: and

The above simple algorithm certainly has been known for quite some time to researchers working in the field. It was rediscovered many times, for example, relatively recently in [8] where an unnecessarily long derivation of it was presented. In an even more recent paper, [9], an algorithm was proposed that coincides with the above one with the initialization . As we explain next, in the latter algorithm (see below) the step of updating was implicit rather than explicit, which made it somewhat difficult to see that this algorithm was a variant of .

Input: , and .

For , do:

-

•

Let be as defined in but for the matrix

where the operator replaces the diagonal of the argument with zeros.

-

•

Update as in (6) and iterate until a convergence criterion is satisfied.

Output:

Because (see (7))

| (8) |

it readily follows that the algorithm of [9] is identical to the with (a fact that was apparently overlooked in [9]).

Our tests of have shown that quite often this algorithm converges to an infeasible solution, i.e., one for which either or are indefinite matrices. To illustrate this issue of , we will compare it in what follows with a slightly modified version that we call FNM for simplicity. In the cases that were problematic for we have observed that the matrix had negative elements. Consequently, we replace (7) in by

| (9) |

where the operator replaces replaces the negative elements on the diagonal of the argument with zeros and leaves the positive elements unchanged.

Example 1: Illustration of the infeasibility issue of

We apply and FNM to the following randomly generated sample covariance matrix (:

| (10) |

for and the following two initializations (the first one was suggested in [8], the second one was used in [9]):

| (11) | ||||

The two algorithms provide the following estimates:

| (12) |

| (13) |

()

| (14) |

FNM ())

| (15) |

In (12) and (14) is indefinite. In contrast to this, both and are positive semidefinite in (13) and (15), as required, and this despite the fact that FNM constrains only to have nonnegative elements. We have not encountered a case in which the matrix obtained with FNM was indefinite, but if this happens then FNM can be run with the constraint as well (however doing so may decrease the rank under ). Also note that FNM has converged to exactly the same matrices and from both initial points, see (13) and (15), whereas the estimates in (12) and (14) are somewhat different (possibly due to a slower convergence rate).

II-B Maximum likelihood (ML) method for deterministic

Under the assumption that the latent variables are deterministic and the noise in (1) has a normal distribution, the negative log-likelihood function of is given by (to within a constant):

| (16) |

where is the th element of and is the th row of . The so-called nonuniform ML method, proposed in and reviewed in [8], tries to minimize (16) to estimate both and as well as (in a parameterized form, see the cited references). The problem is that the ML estimate of the aforementioned parameters does not exist, which can be seen by an analysis similar to the one in [13]. Indeed, let us choose so that

| (17) |

Then the summand that depends on in the second term of (16) is equal to zero and consequently if we let , the function in (16) tends to . This simple observation, showing that the function in (16) is unbounded from below, implies that there is no global minimum and therefore the ML estimate does not exist (which was intuitively expected given the excessive number of unknowns in (16)).

II-C ML method for stochastic

Under the assumption that both and have normal distributions with means zero and covariances and , the negative log-likelihood function of is given by (neglecting some multiplicative and additive constants):

| (18) |

where is as defined in (3). The statistical properties of the maximum likelihood estimates that minimize (18) have been studied, for example, in [14] where the consistency, convergence rate, limiting distribution and asymptotic efficiency were proved.

An algorithm for minimizing the above function was proposed in [8] where it was called Iterative ML Subspace Estimation (IMLSE). The IMLSE minimizes (18) with respect to (wrt) , for given , and then updates , for given , using a fixed-point iteration. This combination of a partial minimizer (more exactly, a stationary point) and a fixed-point iterative scheme is not guaranteed to monotonically decrease the loss and in fact it may fail to converge as shown in the Example 2 below.

Before presenting the example we note that the IMLSE method suggested

in [8] is not new. Indeed, this type of method, which basically

tries to solve the equations satisfied by the stationary points of

the likelihood function by means of a fixed-point iteration, has been

known for many years and its problems are well documented in the literature

(see e.g., [15, 16] and references therein). Our experience is

that the method works in most cases if is small and is considerably

smaller than . As and increase this method fails to

work properly more and more frequently. The main problem appears to

be that, similarly to , the iterates can

step out the feasibility set and when this happens a matrix square-root

computed in the algorithm gets imaginary elements. Setting those problematic

elements to zero sometimes fixes the problem but not always (for instance,

it did not eliminate the problem in the case illustrated in Fig.

1). For a more detailed critical discussion on this type of method

for minimizing the likelihood function in (18) see [15].

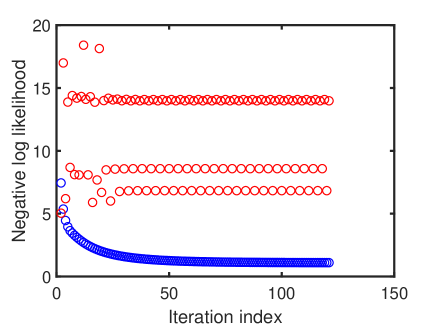

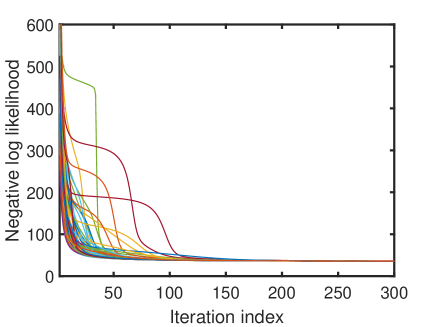

Example 2: Illustration of the convergence problem of IMLSE

We run IMLSE and FAAN (which will be introduced later on) for the sample covariance matrix in (19) with and initial value . Fig. 1 shows the variation of the loss in (18) versus the iteration number for both the algorithms. One can see that the loss corresponding to the IMLSE initially varies quite a bit and then, as the number of iterations increases, it oscillates between three values. In stark contrast to this, FAAN monotonically decreases the loss and has no convergence problem at all.

| (19) |

|

The FAAN algorithm is derived and discussed in Section IV. Before presenting FAAN, however, we need to discuss the uniqueness of the parametrization in (3).

III Identifiability of the parametrization

The parametrization of in (3) is said to be globally identifiable if it is unique. In other words, if , then there is no other (and , with ) such that . If this is true only in a small neighbourhood of , then the parametrization is said to be locally identifiable.

Identifiability (or uniqueness) of the parametrization is an important property without which the estimate of and (for example, obtained by minimizing the loss in (18)) may be unreliable. More specifically, if our goal is to obtain a more accurate estimate of the covariance matrix than , then a possible lack of identifiability may be acceptable, as all estimates of and yield the same estimate of . However, for applications in which we need an estimate of (such as FA and array signal processing, see Section V), identifiability is an essential property as without it the estimate of may be heavily biased.

The identifiability of any parametrization is related to the interplay between the number of free parameters (or unknowns) of the model, let us say , and the number of constraints imposed on them, denoted . In the present case,

| (20) |

and can be shown to be

| (21) |

(to verify (21), use an LQ decomposition of an invertible block of ; there remain free parameters in the said block, and the rest of the matrix has free parameters; furthermore this parametrization of is unique; and the last term in (21) is due to ). From (20) and (21) we have that:

| (22) |

The roots of the quadratic polynomial in (22) are

| (23) |

Only one of is less than (as it should be):

| (24) |

Note that for , the polynomial in (22) takes on a positive value, viz. . It follows that:

| (25) |

and

| (26) |

Therefore, it is intuitively expected that the parametrization is

identifiable for and unidentifiable for .

The index of is motivated by the fact that the author

of [4] was the first to introduce the bound in (24)

as well as the previous conjecture about identifiability based on

whether is smaller or larger than .

The above conjecture was shown to be true in [10] where

the following result was proved (below “generically” means for

almost any instance of and ,

except for some matrices and

that lie in a set of measure zero).

Identifiability result

-

a)

If , then the model (3) is generically globally identifiable.

-

b)

If , then the model is generically locally (and hence globally) unidentifiable.

-

c)

If , the model is generically locally identifiable.

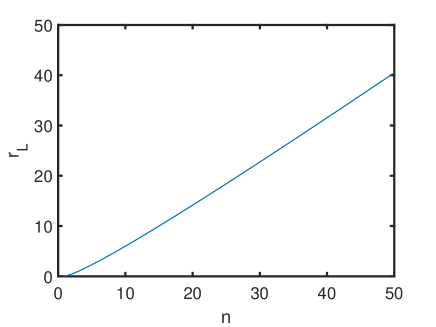

It can be seen from (24) that approaches , as increases. However for small , is significantly smaller than , see Fig. 2.

|

An interesting question in the present context, although not strictly related to identifiablity, is whether any can be written in the form (3) for a given . In other words, given and can we find and such that ? An answer to this question is important because, as is well known, the minimizer of the function in (18) wrt a general (unrestricted) is (assuming that ). Therefore, if can be written in the form (3) then the estimate of obtained by minimizing (18) wrt and is itself (of course, the same is true for the Frobenius norm loss in (5)). From the previous analysis of and , we can intuitively expect that for it may be possible to write in the form (3) (and not possible if ). The results in [11] confirm this intuition, but with the following caveat: can indeed be almost always (i.e. with probability one) be written in the form (3) for an , but the said can be significantly larger than and it is usually unknown.

A consequence of the previous discussion is that considering an makes little sense if the goal is to obtain a better estimate of the covariance matrix than : indeed, for we might end-up with and therefore we are back to square one. If on the other hand, the goal is to additively decompose as a low-rank matrix, , and a diagonal one, , then considering a rank might seem to make sense, but we should keep in mind that for such an the decomposition is almost surely not unique and therefore its use for any practical purpose may be questioned.

The discussion in the previous paragraph has some relevance for Frisch problem [3] [6]: find the minimum for which ( and ). It follows from what was said above that generically we must have and for such an the decomposition is not unique. This simple observation suggests that the Frisch problem should be reformulated as an approximation of rather than an exact decomposition: find the smallest for which and the approximation error is acceptably small in a sense that is important to the application in hand. A solution to this modified Frisch problem can be obtained using FAAN and BIC (the Bayesian Information Criterion), see Sections IV and V. For a different approach and algorithm, see [7].

At the end of this section, we will present another lower bound on the rank that makes it possible to write in the form (3). From equation (74) in Appendix B we have that

or equivalently

| (27) |

Under the assumption that can be written as in (3) for a certain rank , we have that

| (28) |

where the second matrix on the right-hand side (rhs) is positive semi-definite (see (27)). Let (for ) denote the eigenvalues of the three matrices in (28) starting with the left one. Using Weyl inequality, we deduce that

| (29) |

where the second inequality follows from the fact that . Because for we have from (29) that for and therefore that the matrix has at most strictly positive eigenvalues:

| (30) |

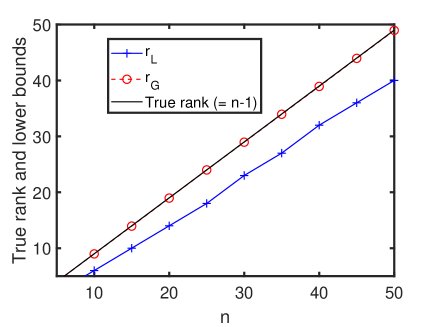

Above denotes the number of positive eigenvalues of the argument, and the index indicates the fact that it was the author of [17] who introduced the bound. Note that is a data-dependent lower bound and thus it applies to every realization unlike that is only generically valid.

We compare to in the next example.

Example 3. Comparison of the lower bounds on the rank

To study the tightness of a lower bound on we need to generate matrices that can be written in the form (3) for a known rank. An important result on the Frisch decomposition states that if then the minimum rank for which can be written in the form (3) is (see, e.g., [6] and references therein). We randomly generate matrices (for ) that satisfy the above condition, and compute using (30) ( denotes the round-up operator). Fig.3 compares the average (computed from Monte-Carlo runs) with and the true rank . As one can see the data-dependent lower bound is tighter than for all values of .

|

IV The proposed method (FAAN)

We will use a coordinate descent algorithm to minimize the loss in (18), which is repeated here for convenience:

| (31) |

While (31) is proportional to the negative log-likelihood

function only if the distribution of the data

is normal, the above loss is a good covariance fitting criterion for

many other distributions. Note that in a misspecified case, such as

when the normal distribution assumption does not hold, (31)

is usually called a quasi likelihood function (see, e.g., [14]).

Let the diagonal matrix and the (semi) orthogonal matrix

be so as

| (32) |

Hence is the eigenvalue decomposition (EVD) of the rhs of (32). We reparametrize the loss in (31) using the variables ():

| (33) |

where is the following function of ,

| (34) |

To simplify the notation, in what follows, we will use instead of . As we will show shortly using the reparametrization via (), instead of the more traditional parametrization via and , simplifies the minimization of (33) w.r.t. , for given (see step 2 below). If we reverted from to (see (32)), the minimization of (33) w.r.t. would be more complicated (see, e.g., [15]).

-

1.

First we minimize (33) wrt , for given . To do so, let be such that the matrix is orthogonal, and observe that :

(35) Using the above EVD in (33) we can rewrite the expression for as follows:

(36) Let denote the eigenvalues of , which are also the eigenvalues of . Using Ruhe lower bound on the trace of the product of two symmetric matrices (see [18] and also Appendix A) yields the following inequality:

(37) where the equality holds if

(38) In particular this implies that the minimizer of (36) is given by:

(39) Furthermore, it follows from (37) that the minimizers { of (36) are the solutions to the following problems (for ):

(40) The function in (40), let us say , has a unique (unconstrained) minimum at . Indeed, a simple calculation shows that:

and

Therefore, the minimizer of (40) is equal to if . If , then the infimum of (40) is attained at , which follows from the fact that in this case for . Combining these two observations shows that the minimizer of (40) is given by ():

(41) -

2.

In the second step of FAAN we minimize (33) wrt , for given and .

To verify that (47) is indeed a minimizer, note from (44) and (45) that the second-order derivative of (43) with respect to is given by:

| (49) |

(where the symbol denotes the fact that the two expressions have the same sign). The value of (49) at satisfies:

| (50) |

and this proves that (47) is a minimum point.

Remark 1.

By the same analysis as above one can verify that the negative root of (46) is also a minimum point but of the unconstrained minimization problem. If the negative root of (46) leads to a smaller value of the loss in (31) than that corresponding to the positive root, then one may expect that the unconstrained minimum of the negative likelihood function lies outside the feasibility set (in which ). Interestingly, even in such a case, FAAN (which picks up the positive root of (46)) never leaves the feasibility set despite the fact that, unlike other algorithms, it does not require any correction measures by the user. Note that in such cases FAAN may converge to a point near the boundary of the feasibility set thus approaching what is called a Heywood solution.

A summary of the FAAN algorithm follows.

Input: , and (for instance or or randomly generated).

For do:

- •

-

•

Compute using (47) (for ) where we use the updated estimates of for and . This step can be iterated a few times or until a convergence criterion is satisfied (note that the computational cost of iterating this step is basically negligible).

-

•

If (where and for example) then goto Output; else and continue the iterations.

Output: and .

Remark 2.

The above derivation of FAAN also provides the minimizers of the likelihood function (33) in the special case of isotropic noise: . In this case, and (39) becomes:

| (51) |

Let denote the eigenvalues of . The unique minimizer of the function of in (40) still is . Because , we have

| (52) |

where is yet to be determined. Under the assumption that at the minimum, which will be shown to be true below, (52) is the minimizer of (40) also when the constraint is enforced. Inserting (52) in (36) and (37) yields the following function of :

| (53) | ||||

The first-order derivative of (53) wrt is given by:

| (54) |

and thus the unique minimizer of (53) is:

| (55) |

which obviously satisfies (for ) as required for (52) to hold. This observation completes our derivation of the ML estimates in the case of , which appears to be simpler than the usual proof of this result in the literature.

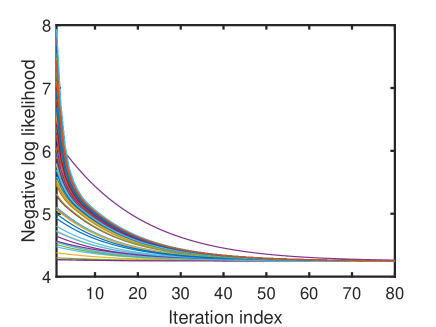

The convergence of FAAN to a local minimum of the loss function in (31) follows from theoretical results on coordinate descent (also called cyclic or alternating minimization) algorithms, see e.g., [19] [20]. Our empirical experience is in agreement with the theory: in all numerical experiments we have performed to date, we did not find a single case in which FAAN had convergence problems. An illustration of the monotonic convergence of FAAN is presented in Fig. 4 for multiple random initializations of .

|

|

In sum, it is our experience that the loss function in (31), despite being non-convex, appears to have a favourable landscape which makes its minimization by a coordinate descent method like FAAN a relatively straightforward task.

At the end of this section, we remind the reader that if is “sufficiently large” (in any case then it follows from the discussion in Section III that the estimated covariance matrix provided by FAAN, let us say , matches exactly:

| (56) |

Interestingly, for any the diagonals of and are identical:

| (57) |

(see Appendix B for the proof). A possible use of this result is as a partial test for convergence.

Finally we note that the present covariance modeling exercise may require not only estimation of and but also estimation of (if it is unknown). When estimation of the integer parameter is required, the fact that FAAN is a ML method is a clear advantage as we can directly make use of information criterion rules such as BIC (see, e.g., [21], [22]) to estimate along with and . A more detailed discussion of this aspect can be found in the next section.

V Numerical Applications

We will present two applications: 1) DOA estimation from the spatial samples collected by an array of sensors, where we need to estimate ; and 2) Portfolio selection for financial asset management, for which we aim to get a covariance matrix estimate that is more accurate than

V-A DOA estimation

We consider a uniform linear array comprising sensors on which impinge the signals emitted by sources. The output of the array (after a preprocessing step that includes quadrature sampling) can be described by the FA model in (1) where now , and are complex-valued, and the matrix is given by (see, e.g., [23]):

| (58) |

The DOAs of the sources can be readily obtained from the spatial frequencies in (58) (see, e.g., the cited paper), therefore the problem is to estimate .

The FAAN algorithm presented in the previous section can be directly applied to the complex-valued data with the only modification being that in (48) should be defined as the real part of the rhs. However, to keep the discussion within the framework of real-valued FA considered in the previous sections, we will use only the real part of , for which all variables in the FA model (1) are real-valued and the matrix is defined as:

| (59) |

We generate data with (1) and (59) where

-

•

, , , .

-

•

The elements of the signals are independently drawn from a standard normal distribution.

-

•

The th element of the noise vector is drawn from a normal distribution with mean zero and variance ; are independently drawn from a uniform distribution on and then fixed and also scaled so as the signal to noise ratio (SNR),

takes a desired value.

-

•

and SNR are varied in the intervals:

SNR

We run FAAN for each dataset generated as described above and use (with ) as an estimate of a basis of . Then we compute the estimates of using the MUSIC (MUltiple SIgnal Classification) algorithm (see, e.g., [8], [23] and references therein) applied to the FAAN estimate of and also to the whitened , i.e. , where denotes the estimate of provided by FAAN. In the former case, the MUSIC estimates of are given by the locations of the two largest peaks of the following function:

In the latter case, the MUSIC estimates of are obtained as follows. Let denote the estimate of the signal subspace given by the four principal eigenvectors of . The estimates of are then obtained as the locations of the two largest peaks of the function:

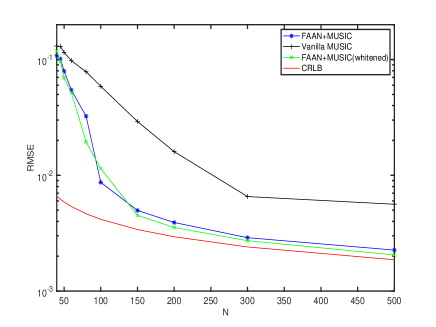

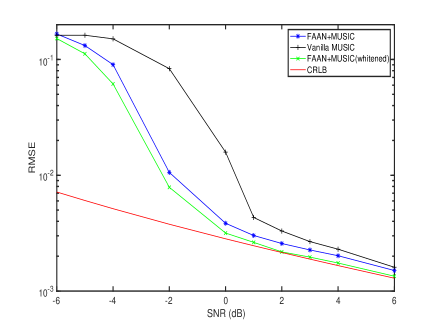

Using independent noise realizations, we estimate the average root mean square error (RMSE) of the frequency estimates

Figures 5(a) and 5(b) show the variation of RMSE versus and versus SNR, respectively. We have also included the Cramï¿œr-Rao Lower Bounds (CRLB) in these figures, which have been computed using the Slepian-Bangs formula (see Appendix B in [24]). As one can see, the RMSE of the MUSIC estimates obtained using FAAN approach the CRLB as or SNR increases and they are significantly lower than those of the vanilla MUSIC algorithm which estimates the signal subspace directly from the sample covariance matrix.

|

|

| a) RMSE vs (SNR= dB) | b) RMSE vs SNR () |

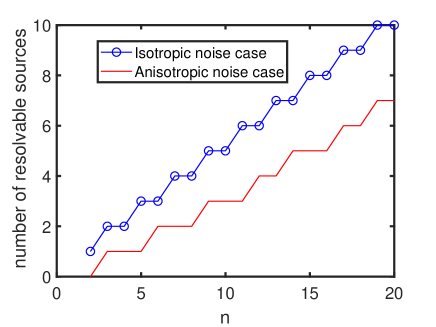

To conclude this application, we make use of the bound to determine the number of sources that can be uniquely resolved with an array of sensors. In the case of isotropic noise and for the matrix in (59) we have

| (60) |

For anisotropic noise, it follows from the discussion in Section III that must generically satisfy :

| (61) |

Fig. 6 compares the integer parts of rhs in (60) and (61). As expected, the maximum number of sources that can be resolved from data corrupted by anisotropic noise is smaller than in the case of isotropic noise, but the relative difference between these two cases decreases as increases.

V-B Portfolio selection

In this subsection we will discuss a portfolio selection application in which the assumption is that the covariance matrix of the stock returns satisfies the model in (3). This assumption is not unrealistic as the number of independent market factors that are internally driving the stock prices (and also their returns) is usually quite small. Consequently the data equation in (1) is well suited to model stock returns, the covariance matrix of which will therefore follow the FA model in (3). However, compared to DOA estimation, the portfolio selection problem is more challenging as the number of samples available to estimate is usually small and in some cases is even rank-deficient. In such cases in which is small, the MLE (ML estimate) of may not exist. The paper [25] has derived the necessary and sufficient conditions for the existence of MLE:

- a)

-

b)

For but the MLE also exists with probability one.

-

c)

For , the negative log-likelihood function in (18) is unbounded below, so the MLE does not exist.

In the portfolio selection problem the number of data samples is larger than that of the factors, thus usually we are in the safe cases a) or b).

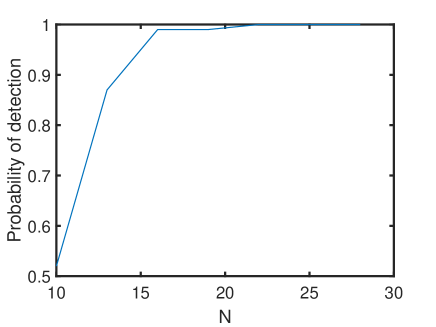

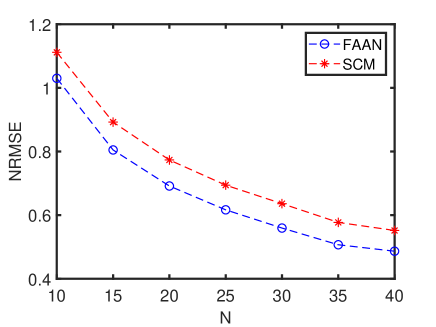

Before applying FAAN to financial data, we study its performance on synthetic data that mimic the real-world data. We simulate normal data samples of dimension whose covariance matrix (which was generated randomly) satisfies the model in (3) with and SNR dB. We run FAAN on the simulated data for different values of . In practical applications in addition to the estimation of and we also need to estimate the number of factors . We will estimate using BIC:

| (62) |

where

| (63) |

and where is the number of real-valued model parameters, see (21). In Fig. 7a we plot Prob() versus . As can be seen from this figure BIC can find the true rank with a probability close to one even when the number of samples is less than . In Fig. 7b we show the normalized where denotes either the SCM or the FAAN estimate of . It can be seen that FAAN outperforms the SCM by about .

|

|

| (a) Probability of detection vs | (b) NRMSE vs |

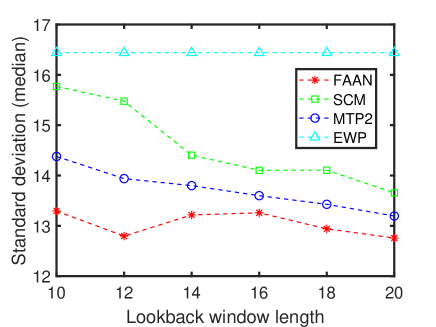

Next, we present the real-world financial data analysis. We will use the daily stock returns of assets over a period of days from the publicly available database of the Center for Research in Security Prices [26]. The samples are obtained from raw stock market data as in [27]. The stock market data corresponds to investment dates at intervals of one month, where each month comprises trading days. Using the most recent returns, we first estimate the covariance matrix corresponding to each investment date () using FAAN and BIC ( is also unknown and needs to be estimated in this application). We then solve the following minimum variance portfolio problem :

| (64) | ||||

| s.t. |

to obtain the portfolio weight vector for the -th month. The standard derivation of the portfolio returns is the performance metric since a good estimator of the covariance matrix will give a small value of the portfolio variance (). The standard deviation corresponding to each month is computed using the next months ( days) out-of-sample (future) returns. We use the equally weighted portfolio (EWP) as a baseline for comparison, and consider the SCM and a recently proposed method called MTP2 [27] as competing estimators. The lookback window length is varied between and , and the median of the standard deviations corresponding to different months is computed. Fig. 8 shows the median vs the lookback window length for each method. FAAN outperforms the other methods especially in the case of small .

|

VI Conclusions

We have presented a new method for Factor Analysis in the case of Anisotropic Noise (FAAN). The proposed method is a coordinate descent algorithm that monotonically maximizes the normal likelihood function, is easy to understand as well as implement (in particular it requires no tuning by the user), and has excellent convergence properties. Compared to FAAN, most of the existing algorithms are either more complex (both computationally and conceptually) and in need of some tuning by the user or are less reliable (for instance, they can converge to points outside the feasibility set, or may not converge at all). The following aspects, which were deemed to be important for FAAN and its use in practical applications, have been discussed: i) identifiability of the covariance matrix model (i.e., uniqueness of parametrization); ii) exact matching of the sample covariance matrix as the number of factor increases; iii) data independent/dependent lower bounds on the number of factors that are important for the previous two aspects; and iv) estimation of the number of factors using the Bayesian Information Criterion (BIC).

Out of the many possible applications of FAAN, we have selected two: a) DOA estimation from the signals collected by an array of sensors; and b) portfolio selection for financial asset management. As shown in the paper, FAAN has performed well in both cases. In the era of “big (high-dimensional) data”, applications that need dimensionality reduction techniques are abundant and the hope is that FAAN will be found to be a useful tool for FA in many other practical cases besides those considered in this paper. A MATLAB code for FAAN can be downloaded from https://github.com/ghaniafatima/FAAN

-A Ruhe trace lower bound

To make the paper as self-contained as possible, we state in this appendix a generalized version of Ruhe lower bound [18] and also provide a simple proof of it.

Let and be two symmetric matrices with eigenvalues and respectively. Then,

| (65) |

Evidently the above inequality holds (with equality) for . To prove the inequality in the general case we show that if it holds for then it also holds for . Let

denotes the EVD of , and let . Using this notation, we can write:

| (66) | ||||

| (67) |

The first term in is the trace of the product of a diagonal matrix with elements and an matrix denoted that is a principal block of .

-B Proof of the diagonal matching property

The stationary points of the loss function (31) are solutions of the equations:

| (69) |

To calculate the above derivatives, we use the fact that for a matrix which is a function of a variable , the following formulas hold true:

| (70) | ||||

Making use of these formulas we get after some straightforward calculations

(below denotes the column

of the identity matrix):

| (71) |

or equivalently,

| (72) |

and

or equivalently

| (73) |

By the matrix inversion lemma,

| (74) |

which implies that:

| (75) |

| (76) |

| (77) |

and the proof of (57) is concluded.

References

- [1] C. Spearman, “General intelligence, objectively determined and measured,” The American Journal of Psychology, vol. 15, pp. 201–292, 1904.

- [2] L. L. Thurstone, “Multiple factor analysis.,” Psychological review, vol. 38, no. 5, p. 406, 1931.

- [3] R. Frisch, Statistical confluence analysis by means of complete regression systems, vol. 5. Universitetets Økonomiske Instituut, 1934.

- [4] W. Ledermann, “On the rank of the reduced correlational matrix in multiple-factor analysis,” Psychometrika, vol. 2, no. 2, pp. 85–93, 1937.

- [5] T. Anderson and H. Rubin, “Statistical inference in factor analysis,” in Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, vol. 1, pp. 111–150, Univ of California Press, 1956.

- [6] L. Ning, T. Georgiou, A. Tannenbaum, and S. Boyd, “Linear models based on noisy data and the Frisch scheme,” SIAM Review, vol. 57, no. 2, pp. 167–197, 2015.

- [7] V. Ciccone, A. Ferrante, and M. Zorzi, “Factor models with real data: A robust estimation of the number of factors,” IEEE Transactions on Automatic Control, vol. 64, no. 6, pp. 2412–2425, 2018.

- [8] B. Liao, S. C. Chan, L. Huang, and C. Guo, “Iterative methods for subspace and DOA estimation in nonuniform noise,” IEEE Transactions on Signal Processing, vol. 64, no. 12, pp. 3008–3020, 2016.

- [9] A. Zhang, T. Cai, and Y. Wu, “Heteroskedastic PCA: Algorithm, optimality, and applications,” The Annals of Statistics, vol. 50, no. 1, pp. 53–80, 2022.

- [10] P. A. Bekker and J. M. Ten Berge, “Generic global indentification in factor analysis,” Linear Algebra and its Applications, vol. 264, pp. 255–263, 1997.

- [11] A. Shapiro, “Rank-reducibility of a symmetric matrix and sampling theory of minimum trace factor analysis,” Psychometrika, vol. 47, no. 2, pp. 187–199, 1982.

- [12] M. Pesavento and A. Gershman, “Maximum-likelihood direction-of-arrival estimation in the presence of unknown nonuniform noise,” IEEE Transactions on Signal Processing, vol. 49, no. 7, pp. 1310–1324, 2001.

- [13] P. Stoica and J. Li, “On nonexistence of the maximum likelihood estimate in blind multichannel identification,” IEEE Signal Processing Magazine, vol. 22, no. 4, pp. 99–101, 2005.

- [14] J. Bai and K. Li, “Statistical analysis of factor models of high dimension,” The Annals of Statistics, vol. 40, no. 1, pp. 436–465, 2012.

- [15] K. G. Jöreskog, “Some contributions to maximum likelihood factor analysis,” psychometrika, vol. 32, no. 4, pp. 443–482, 1967.

- [16] D. N. Lawley and A. E. Maxwell, “Factor analysis as a statistical method,” Journal of the Royal Statistical Society. Series D (The Statistician), vol. 12, no. 3, pp. 209–229, 1962.

- [17] L. Guttman, “Some necessary conditions for common-factor analysis,” Psychometrika, vol. 19, no. 2, pp. 149–161, 1954.

- [18] A. Ruhe, “Perturbation bounds for means of eigenvalues and invariant subspaces,” BIT Numerical Mathematics, vol. 10, no. 3, pp. 343–354, 1970.

- [19] P. Tseng, “Convergence of a block coordinate descent method for nondifferentiable minimization,” Journal of optimization theory and applications, vol. 109, no. 3, pp. 475–494, 2001.

- [20] A. Beck and L. Tetruashvili, “On the convergence of block coordinate descent type methods,” SIAM Journal on Optimization, vol. 23, no. 4, pp. 2037–2060, 2013.

- [21] P. Stoica and Y. Selen, “Model-order selection: a review of information criterion rules,” IEEE Signal Processing Magazine, vol. 21, no. 4, pp. 36–47, 2004.

- [22] P. Stoica and P. Babu, “False discovery rate (FDR) and familywise error rate (FER) rules for model selection in signal processing applications,” IEEE Open Journal of Signal Processing, vol. 3, pp. 403–416, 2022.

- [23] P. Stoica and A. Nehorai, “Music, maximum likelihood, and Cramér-Rao bound,” IEEE Transactions on Acoustics, Speech, and Signal Processing, vol. 37, no. 5, pp. 720–741, 1989.

- [24] P. Stoica and R. L. Moses, Spectral Analysis of Signals. Pearson Prentice Hall, Upper Saddle River, NJ, 2005, available at https://user.it.uu.se/ ps/ps.html.

- [25] D. Robertson and J. Symons, “Maximum likelihood factor analysis with rank-deficient sample covariance matrices,” Journal of Multivariate Analysis, vol. 98, no. 4, pp. 813–828, 2007.

- [26] Center for Research in Security Prices. CRSP Stock File Guide, University of Chicago, Chicago, 1994.

- [27] R. Agrawal, U. Roy, and C. Uhler, “Covariance matrix estimation under total positivity for portfolio selection,” Journal of Financial Econometrics, vol. 20, no. 2, pp. 367–389, 2022.