Exploring Gender and Race Biases in the NFT Market

Abstract

Non-Fungible Tokens (NFTs) are non-interchangeable assets, usually digital art, which are stored on the blockchain. Preliminary studies find that female and darker-skinned NFTs are valued less than their male and lighter-skinned counterparts. However, these studies analyze only the CryptoPunks collection. We test the statistical significance of race and gender biases in the prices of CryptoPunks and present the first study of gender bias in the broader NFT market. We find evidence of racial bias but not gender bias. Our work also introduces a dataset of gender-labeled NFT collections to advance the broader study of social equity in this emerging market.

Keywords: NFT; non-fungible tokens; biases; race; gender

1 Introduction

Are darker-skinned Non-Fungible Tokens (NFTs) sold for less than lighter-skinned NFTs? Or, are female NFTs worth less than male NFTs? Egkolfopoulou and Gardner [8] raises diversity concerns by reporting preliminary results on price differences based on gender and race. Determining whether diversity issues are present in the early-stage NFT space is important to raise awareness and bring change.

NFTs are tokens on a blockchain to represent ownership of a unique item. While the item can range from music, videos, or tweets, it usually represents the ownership of art. NFT’s popularity has boomed since 2021 as the public became accustomed to the concept. We analyze NFTs stored on the Ethereum network [9]

As NFTs are such a new concept, the dynamics of the NFT market has not been well studied. There has been previous work about NFT economics with focus on the trade networks [14], the predictability of NFT sales [14], and the risk and returns of NFT investments, [13]. Other topics of interest include how NFT art may change the dynamics of art markets [3], how NFTs can affect game development by making the art tradable [10], and how it can revolutionize digital ownership in different industries [16]. Among the studies, one specific collection that is most analyzed to represent the NFT market is CryptoPunks [12] [18] [6].

The CryptoPunk collection is one of the most well-known NFT collections and consists of 10,000 avatars on the Ethereum blockchain created by Larva Labs in 2017. They are commonly credited for starting the NFT boom in 2021 [20]. As shown in Figure 1, CryptoPunks are avatars that can be used to represent oneself in the digital world and therefore are of interest when studying the NFT diversity problem.

We are interested in whether racial bias or gender bias exists in the NFT art market. In the December 2021 Bloomberg article “Even in the Metaverse, Not All Identities Are Created Equal”, Egkolfopoulou and Gardner [8] examined graphs of sales prices of CryptoPunks over time across different genders and different races. They found that female avatars were sold for less than male avatars, and darker-skinned avatars were sold for less than lighter-skinned NFTs. However, their evidence for gender and racial biases is limited to visual inspection of CryptoPunk’s historical price graphs instead. Thus, we test the statistical significance of race and gender biases in the prices of CryptoPunks and present the first study investigating gender bias in the broader NFT market.

Our first goal is to analyze the gender and race biases of CryptoPunks rigorously through hypothesis testing. This will indicate whether price differences are significant enough to not be attributed to random chance. We find that darker-skinned CryptoPunks are sold for more than lighter-skinned CryptoPunks, but contrary to the analysis in [8], the difference in price for male and female CryptoPunks was not statistically significant.

Our second goal is to extend our analysis to other collections to determine whether there are gender biases for the broader NFT market. To that end, we analyze NFT collections labeled with gender tags and apply a hypothesis test to each collection to determine if male-looking NFTs sell at higher prices than female-looking ones. Like in CryptoPunks, we conclude that the price difference in male and female is not statistically significant. Because of the lack of race labels, we were only able to find collections to categorize between light and dark skinned NFTs, with analysis suggesting lighter-skinned NFTs are sold for more than darker-skinned NFTs.

2 Methodology

We describe the methods of analyzing the gender and race biases in the prices of NFTs. We first summarize our data collection process (Section 2.1 and 2.2) and then describe how we statistically quantify the gender and racial biases among different NFTs (Section 2.3). The steps are shown in Figure 2. More detailed description of methods and implementation can be found in the Appendix.

2.1 Initial Data Collection

Our dataset consists of NFTs transacted on OpenSea, which is the primary marketplace for NFTs on Ethereum. We query the OpenSea “v1/collections” endpoint at the end of November 2022 [15] to retrieve NFT metadata and last sale price. We choose 790 collections from the Kaggle Ethereum NFTs dataset [11] and NFTs from the top 30-day and all-time OpenSea volume leaderboard around November 2021. After the data collection process, we end up with NFTs, each that have been transacted upon.

| Number of Collections | 790 | ||

| Number of NFTs | 2.5 million | ||

|

44 |

2.2 Retrieving Race and Gender Labels

Many NFT collections do not represent humans, and therefore cannot be directly studied through the lens of race and gender. We select collections that have metadata with the words “male” and “female” and end with a total of such collections with gender labels representing different avatars. Statistics on these collections with gender labels can be found in Table 6 in Appendix A.2.

As far as we know, this is the first NFT dataset with gender labels across many collections. However, race labels often do not exist in the metadata, so we are limited to only CryptoPunks, Avastar, and Dynamic Duelers for collections with race labels.

2.3 Statistical Tools to Analyze Bias in Gender and Race

To determine the statistical significance of the hypothesis that female NFTs are sold for less than male NFTs, we run both paired and unpaired one-sided Student’s t-tests [22].

Unpaired vs Paired t-test: For unpaired t-test, we compare the mean of all NFT sale prices for male versus for female. For paired t-test, we calculate t-statistics on the paired difference of male and female prices marked to the daily mean price and the weekly mean price of the NFT. The paired t-test is used to isolate the male versus female price difference by fixing price variation across time.

Log Transformation: As t-test assume normality of the data, we apply a log transformation to address this. With rare NFTs worth significantly more than common NFTs, NFT price distributions tend to follow a power law distribution [14]. Inspired by how stock prices follow a log-normal distribution [1], we applied the same transformation and found the distribution of log of price to be more normal. We refer to running the t-test on the log of prices as log t-test.

Outlier Trimming: Outliers may occur due to very high selling prices for rare NFTs or very low selling prices due to humans errors while listing. We address outliers using Winsorization [19], or trimming outliers past a certain percentile. We report results for , , , and percentiles.

The approach described above is also used to compare the prices of light and dark CryptoPunks. We report results from combinations of different t-tests and outlier detection methods to show our conclusion remains consistent regardless of the way we conduct the statistical significance test. For the figures and statistics in this paper, unless otherwise stated, we remove outliers at the percentile.

3 Results

Our goal is to investigate biases in pricing with respect to gender and race for NFT collections. We first analyze CryptoPunks, as it is one of the first NFT collections and is commonly credited for starting the 2021 NFT revolution [20]. The dataset we use is compiled from querying the OpenSea API as described in Section 2.1.

3.1 CryptoPunks

While [8] identifies biases in prices for both gender and race for CryptoPunks, we find only darker-skinned CryptoPunks are sold for less than lighter-skinned CryptoPunks.

3.1.1 Gender

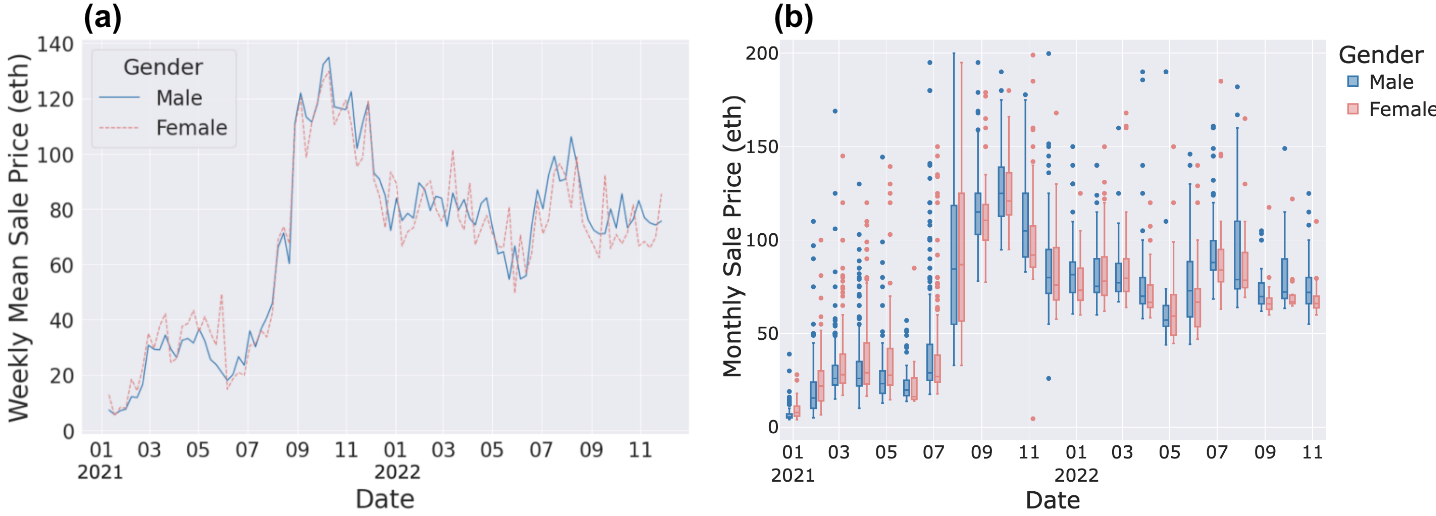

We found price difference across gender was not significant. In Figure 3a, male and female weekly mean sale price are roughly equal with blue and red lines being roughly level. This conclusion is corroborated by the male and female box plots at similar price levels for different months in Figure 3b.

We supplement the visual analysis with statistical anylsis. From 2021-01 to 2022-11, the median selling price of male CryptoPunks ( eth) is greater than median price of female CryptoPunks ( eth), but the mean selling price of male CryptoPunks ( eth) is less than that of female CryptoPunks ( eth). Because the means and medians yield different conclusions, we also analyze the p-value of different one-sided t-tests on whether male prices are greater than female prices. As shown in Table 2, we vary outlier detection percentiles, whether to run unpaired or paired t-test, and whether to apply the log transformation. Only at a outlier percentile level do some of the t-tests imply male price is greater than female price. This is reasonable because from Figure 3b, male outliers tend to be higher priced than female outliers. As a precondition for the t-test is the absence of outliers, t-tests at other outlier levels ( and may be more informative. Thus, there is not enough statistical evidence to conclude there is gender bias in CryptoPunks.

| Outlier Percentile | 0.1% | 2.5% | 5.0% |

|---|---|---|---|

| Paired t-test (marked to day) | 0.027 | 0.719 | 0.803 |

| Paired t-test (marked to week) | 0.103 | 0.815 | 0.778 |

| Unpaired t-test | 0.647 | 0.978 | 0.886 |

| Log Paired t-test (marked to day) | 0.000 | 0.144 | 0.250 |

| Log Paired t-test (marked to week) | 0.114 | 0.240 | 0.129 |

| Log Unpaired t-test | 0.005 | 0.623 | 0.549 |

3.1.2 Race

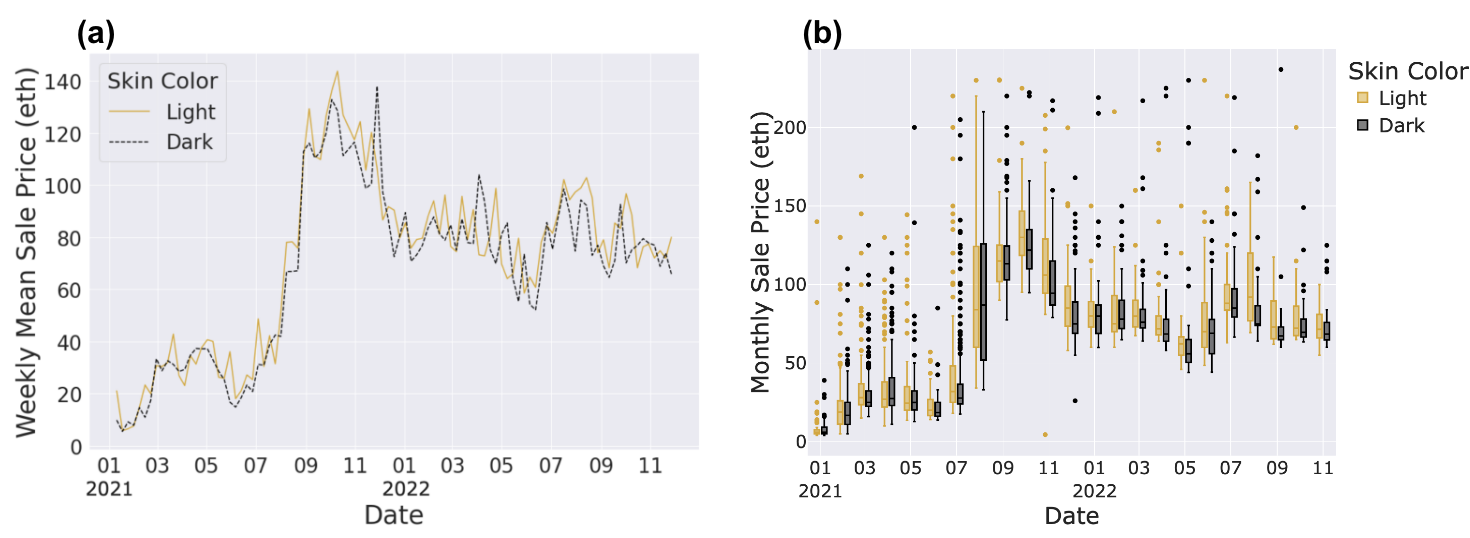

Although we do not find gender bias in the pricing of CryptoPunks, we corroborate the visual analysis in [8] with statistical results that lighter-skinned CryptoPunks are valued more than darker-skinned CryptoPunks.

We first plot the weekly mean sale prices of Dark and Light CryptoPunks between 2021-01 and 2022-11 in Figure 4a and find that Light CryptoPunks are consistently sold at a higher price than Dark CryptoPunks. Examining the box plot in Figure 4b for CryptoPunks prices across different months, we observe similar results. At a trim level, the median sale price for Light CryptoPunks ( eth) is greater than that of Dark CryptoPunks ( eth), and the mean sale price for Light CryptoPunks ( eth) is also greater than that of Dark CryptoPunks ( eth). In addition, from Table 3, every paired t-test across different outlier detection schemes supports this hypothesis with very low p-values, indicating the effect is large. Furthermore, the unpaired t-test results were above at and outlier trim levels may be due to CryptoPunks’ large price variation across time that increases standard deviation and lowers t-stat. Thus, the evidence suggests that Light CryptoPunks are sold for more than Dark CryptoPunks.

| Outlier Percentile | 0.1% | 2.5% | 5.0% |

|---|---|---|---|

| Paired t-test (marked to day) | 2.53E-04 | 2.00E-06 | 1.00E-06 |

| Paired t-test (marked to week) | 6.00E-06 | 3.00E-06 | 2.72E-07 |

| Unpaired t-test | 3.46E-07 | 1.20E-01 | 1.17E-01 |

| Log Paired t-test (marked to day) | 2.50E-07 | 2.81E-04 | 3.57E-04 |

| Log Paired t-test (marked to week) | 1.28E-07 | 4.50E-05 | 3.70E-05 |

| Log Unpaired t-test | 1.01E-02 | 3.63E-01 | 2.39E-01 |

3.2 Aggregate NFT Market

We conduct similar analysis for gender and race bias across the NFT market. We found collections with gender labels but only with race labels.

3.2.1 Gender

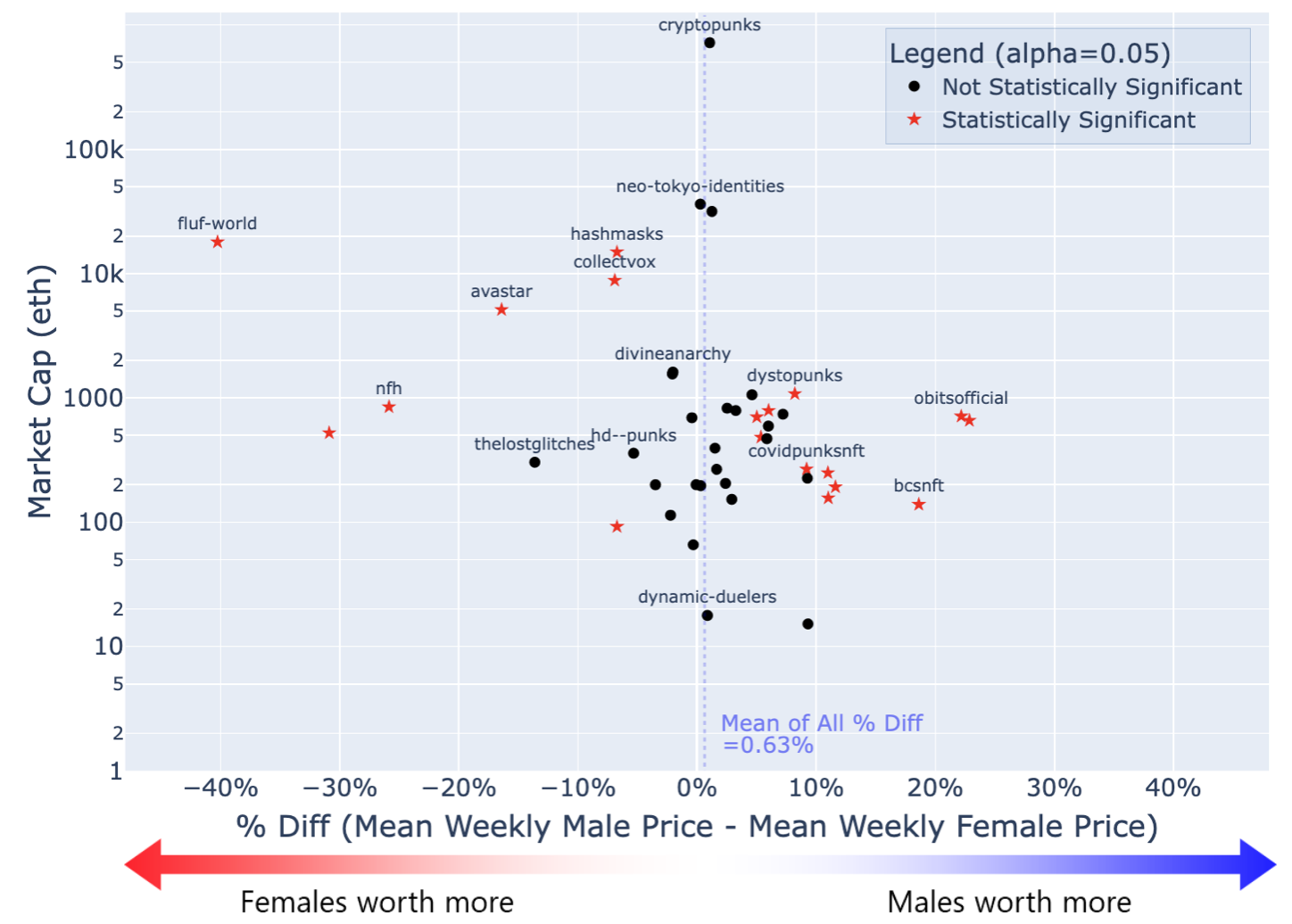

For the NFT collections chosen as detailed in Section 2.2, we calculate p-values to determine whether male NFT prices are greater than female NFT prices. P-values are calculated from a paired log t-test marked to weekly mean with a outlier trim percentile of . To satisfy preconditions of a t-test, we apply a log transformation to make prices follow a more normal distribution and remove outliers. We mark to weekly mean price, which is common for low transaction volume markets such as NFT markets [7]. From the analysis, we find no clear relationship between market cap and gender bias. However, we do demonstrate that male prices are not statistically significantly higher than female prices for the broader NFT market.

Figure 5 displays collections with male price statistically significantly () higher than female price (right red dots), female price statistically significantly higher than male price (left red dots), and no statistically significant difference (black dots). There is no clear relationship between market cap and mean price difference across gender, but the figure does answer whether male NFTs are priced higher than female NFTs across the aggregate market.

First, the mean across all collections of the price difference of male and female NFTs is only . Furthermore, at a significance level of , only out of collections have male NFTs valued more than female NFTs, whereas collections have female NFTs valued more than male NFTs. Therefore, there is not enough evidence to conclude there is a statistically significant difference between male and female prices for the broader NFT market.

3.2.2 Race

In addition to CryptoPunks, we obtained race labels for the Avastar and Dynamic Duelers collections. From mean and median statistics in Table 4, we find that light-skinned NFTs on average tend to be sold for higher prices that darker-skinned counterpart. The result is less significant for Dynamic Duelers. For statistics in Table 4 and 5, we use outlier trim level of .

| Light Mean | Dark Mean | Light Median | Dark Median | |

|---|---|---|---|---|

| avastar | 0.235 | 0.229 | 0.219 | 0.2 |

| dynamic_duelers | 0.064 | 0.063 | 0.06 | 0.06 |

| avastar | dynamic_duelers | |

|---|---|---|

| Log Paired t-test (marked to day) | 0.158 | 0.190 |

| Log Paired t-test (marked to week) | 0.733 | 0.162 |

| Log Unpaired t-test | 0.024 | 0.573 |

We also conduct hypothesis tests in Table 5 to determine the statistical significance of whether lighter-skinned NFTs are worth more than darker-skinned NFTs. With a majority of the p-values less than and our conclusion from CryptoPunks, the results suggest lighter-skinned NFTs are worth more than darker-skinned NFTs, though not necessarily at a statistically significant level. Because this analysis is on a small subset of the entire NFT market, more data is required to generalize our conclusion to the entire NFT market.

4 Discussion

We seek to determine what mechanisms produce the different biases and why there exists racial bias but not gender bias in the prices of NFTs. Most NFTs in the market, especially those with gender and race attributes, represent avatars. These NFTs, especially expensive ones like CryptoPunks, can be used as profile picture, and thus people may prefer NFTs that look similar to themselves. We thus believe the demographics of NFT investors are the mechanisms that produce these biases.

According to a data by Statistica [2] [4], among the age group (18-34) with the largest interest in NFTs, men and women own NFTs fairly equally with 24% men and 21% women of total investor population. Thus, the fact we do not observe gender bias in NFT prices could be due to investors being roughly balanced across gender.

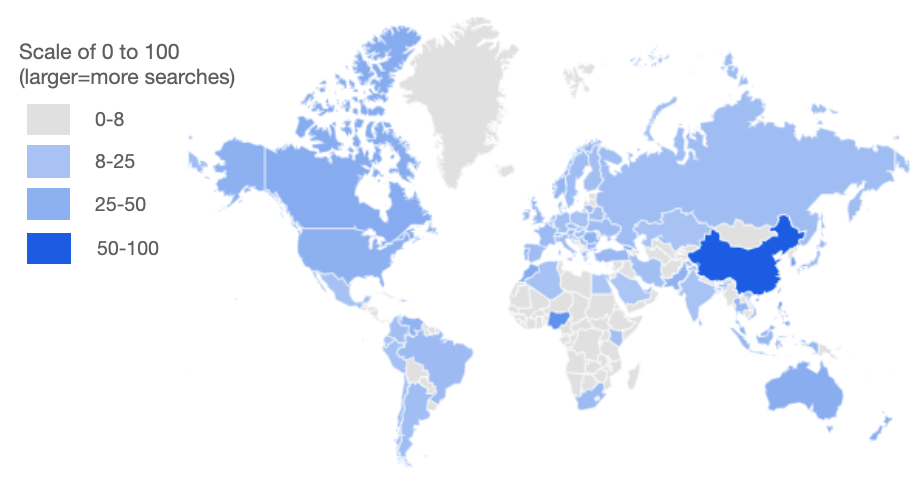

However, the distribution of NFT buyers may be skewed white, which explains the existence of racial bias. Using Google searches as a proxy on the amount of NFT investors in a region, in the past five years, we found that the term “NFT” was most searched in East Asia and North America and least searched in Africa and India. Thus, more lighter-skinned people are interested in NFTs compared to darker-skinned people and may be why lighter-skinned NFTs are more in demand. The full map of Google searches can be found in Figure 7 in Appendix A.3.

5 Conclusion

In this paper, we provide a rigorous statistical analysis of the gender and race biases of CryptoPunks and the NFT market as a whole. We found that gender bias is not statistically significant for CryptoPunks, but racial bias is. Regardless of how we remove outliers, whether we apply a log transform, or whether we used a paired or unpaired t-test, our conclusion remains consistent. As CryptoPunks are well-known and commonly credited for starting the rise of NFTs, biases in prices reflect early-investors’ perceptions of NFTs representing different races.

When we analyzed the NFT market as a whole, we also found there was not a statistically significant difference in price between male and female NFTs. For future work, we plan to label race for more NFT datasets to be able to conclude whether the trend of lighter-skinned CryptoPunks being sold for more than darker-skinned CryptoPunks holds for the general NFT market. We believe this price disparity may be due to the demographics of NFT investors. For avatars that are NFTs, people may tend to buy ones that look similar to their appearance.

Investigating the gender and race biases are important from a culture standpoint due to the popularity of NFTs. As the metaverse is at its seed stage of creation with egalitarian values at the forefront of decentralization, it is important that inequity and biases in society do not propagate into it. Identifying these racial biases is the first step to drive initiatives that bring equity to NFTs and the metaverse. Possible countermeasures of improving fairness include raising awareness to the issue and increasing access to NFTs to other parts of the world, especially in developing countries. We hope future investors will purchase NFTs with racial sensitivity in mind.

6 Acknowledgements

This work is supported by the MIT Advanced Undergraduate SuperUROP program and supported by the National Science Foundation under Grant DGE-1747486. Any opinions, findings, and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the National Science Foundation.

References

- [1] I Antoniou, Vi V Ivanov, Va V Ivanov and PV Zrelov “On the log-normal distribution of stock market data” In Physica A: Statistical Mechanics and its Applications 331.3-4 Elsevier, 2004, pp. 617–638

- [2] Raynor de Best “U.S. NFT user characteristics 2021” In Statista, 2022 URL: https://www.statista.com/statistics/1265821/us-nft-user-demographics/

- [3] Sheila Bsteh and Filip Vermeylen “From Painting to Pixel: Understanding NFT Artworks” In Retrieved June 15, 2021, pp. 2021

- [4] Team Colormatics “NFT audience insights: Who buys nfts and why?” In Full Service Ad Agency URL: https://www.colormatics.com/article/nft-audience-insights-whos-buying-nfts-and-why/

- [5] Cryptopunksnotdead “Programming-cryptopunks” In GitHub, 2021 URL: https://github.com/cryptopunksnotdead/programming-cryptopunks/blob/master/07_humans.md

- [6] Dipanjan Das et al. “Understanding security Issues in the NFT Ecosystem” In arXiv preprint arXiv:2111.08893, 2021

- [7] Michael Dowling “Fertile LAND: Pricing non-fungible tokens” In Finance Research Letters 44 Elsevier, 2022, pp. 102096

- [8] Misyrlena Egkolfopoulou and Akayla Gardner “Even in the Metaverse, Not All Identities Are Created Equal” In Bloomberg.com Bloomberg URL: https://www.bloomberg.com/news/features/2021-12-06/cryptopunk-nft-prices-suggest-a-diversity-problem-in-the-metaverse

- [9] “Ethereum Whitepaper”, 2014 URL: https://ethereum.org/en/whitepaper

- [10] Allan Fowler and Johanna Pirker “Tokenfication-The potential of non-fungible tokens (NFT) for game development” In Extended Abstracts of the 2021 Annual Symposium on Computer-Human Interaction in Play, 2021, pp. 152–157

- [11] “Kaggle Dataset: Ethereum NFTs” In kaggle.com kaggle URL: https://www.kaggle.com/datasets/simiotic/ethereum-nfts

- [12] De-Rong Kong and Tse-Chun Lin “Alternative investments in the Fintech era: The risk and return of Non-Fungible Token (NFT)” In Available at SSRN 3914085, 2021

- [13] Mieszko Mazur “Non-Fungible Tokens (NFT). The Analysis of Risk and Return” In Available at SSRN 3953535, 2021

- [14] Matthieu Nadini et al. “Mapping the NFT revolution: market trends, trade networks, and visual features” In Scientific reports 11.1 Nature Publishing Group, 2021, pp. 1–11

- [15] “OpenSea API Docs: Retrieve Collections” URL: https://docs.opensea.io/reference/retrieving-collections

- [16] Andrei-Dragos Popescu “Non-Fungible Tokens (NFT)–Innovation beyond the craze” In 5th International Conference on Innovation in Business, Economics and Marketing Research, 2021

- [17] “PySpark” URL: https://spark.apache.org/docs/latest/api/python

- [18] Luisa Schaar and Stylianos Kampakis “Non-fungible tokens as an alternative investment: Evidence from cryptopunks” In The Journal of The British Blockchain Association The British Blockchain Association, 2022, pp. 31949

- [19] John W Tukey and Donald H McLaughlin “Less vulnerable confidence and significance procedures for location based on a single sample: Trimming/Winsorization 1” In Sankhyā: The Indian Journal of Statistics, Series A JSTOR, 1963, pp. 331–352

- [20] Sandra Upson “The 10,000 faces that launched an NFT revolution” In Wired Conde Nast, 2021 URL: https://www.wired.com/story/the-10000-faces-that-launched-an-nft-revolution/

- [21] Pauli Virtanen et al. “SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python” In Nature Methods 17, 2020, pp. 261–272 DOI: 10.1038/s41592-019-0686-2

- [22] Ronald E Walpole, Raymond H Myers, Sharon L Myers and Keying Ye “Probability and Statistics for Engineers and Scientists” Prentice Hall, 2012

A Appendix

A.1 Implementation Details

We elaborate on the methods and the implementation details. This sections follows the structure Section 2.

A.1.1 Initial Data Collection

Our dataset only includes NFTs transacted on OpenSea, which is the primary marketplace for NFTs on the Ethereum blockchain. We query the OpenSea “v1/collections” endpoint at the end of November 2022 [15] to retrieve collection metadata as well as each individual NFT’s metadata and last sale price. We choose 790 collection names from the Kaggle Ethereum NFTs dataset [11] and NFTs from the top 30-day and all-time OpenSea volume leaderboard around November 2021. Most collections have around 5,000 to 10,000 items, and our queries yield around 70-80% of the data as the other 20-30% do not have transactions.

After querying the Application Programming Interface (API) using a script written with the PySpark framework [17] on Databricks, we create a dataframe containing each NFT’s collection name, id, sale information, metadata, and image url. We then loop through this dataframe with multiple workers to download the images in parallel. In the end, we obtain a dataset of about NFTs, each that have been transacted upon.

A.1.2 Retrieving Race and Gender Labels

To get gender-labelled data, we select collections that have metadata with the words “male” and “female” to find collections where at least of the images have gender labels. We filter out collections that have more than male or female to avoid rarity factors affecting the price. We find a total of such collections with gender labels that satisfy the criteria.

These collections with gender labels are

It is more challenging to determine the race of an NFT collection because most collections do not directly annotate this information. For the CryptoPunks collection, we label each NFT based on the frequencies of the four different pixel values representing the four different skin tones as displayed in Figure 6. The above process was inspired by [5]. For our analysis, we group darkest and mid as Dark and lighter and lightest as Light. For other collections, we were unable to retrieve race labels from the metadata.

We also attempted to find race labels for a subset of the collections with gender labels with the criteria that there were a high proportion of items that could be categorized as either dark or light skinned. We filtered out collections that have more than light-skinned or dark-skinned to avoid rarity factors affecting the price. This required manual review because most collections do not have easy-to-search race labels in the metadata, or even way to categorize race. For Avastar, we categorized “Amber Brown” as dark-skinned and “Pale Pink” as light-skinned in the “skin_tone” attribute. For Dynamic Duelers, we categorized “Black” as dark-skinned and “White” as light-skinned in the “Skin color” attribute.

A.1.3 Statistical Tools to Analyze Bias in Gender and Race

We detail the statistical methods used to analyze the bias in NFT pricing for gender and race. Specifically, we go into more detail about the implementation and underlying assumptions of these tests.

Unpaired t-test assumes

-

1.

independence of observations and each point belongs to either male or female

-

2.

the variances of male and female prices are equal for the population

-

3.

the prices follows a normal distribution

-

4.

no significant outliers in each group

The unpaired t-test is robust to all but large deviation from these assumptions. Assumption 1 and 2 are satisfied, but 3 and 4 require more careful consideration.

Log Transformation: For assumption 3, with rare NFTs worth significantly more than common NFTs, NFT price distributions tend to follow a power law distribution [14]. Because it’s well known that stock prices follow a log-normal distribution [1], we apply the same transformation and found log of price tended to be closer to a normal distribution. We thus decided to also run the t-test on the log of prices, which we refer to as log t-test.

Outlier Trimming: For assumption 4, as outliers may occur due to very high selling prices for rare NFTs or very low selling prices due to humans errors while listing, we address this issue by Winsorization [19], or trimming outliers past a certain percentile. Specifically, we report t-test results while trimming both left and right tails of the distribution at , , , and percentiles.

Paired t-test: In addition to the unpaired t-test for independent samples, we also run a paired t-test for two dependent samples in order to better isolate the male versus female price difference while fixing time. Specifically, we calculate t-statistics on the paired difference of male and female prices marked to the daily mean price and the weekly mean price of the NFT. Assumptions 1 and 2 are now (1) male - female price must be continuous and (2) observations are independent of one another. Assumptions 3 and 4 from unpaired test remain the same and. We address assumptions 3 and 4 with the log-transformation and Winsorization, as described earlier.

The approach described above is also used to compare the prices of lighter-skinned and darker-skinned CryptoPunks. We utilize the SciPy Python package [21] to implement both types of t-tests.

A.2 Detailed NFT Information

The 44 collections that we sampled and analyzed are all NFTs representing avatars. In Table 6, month created, mean sale price, median sale price, 2.5% trim mean sale price, and total supply are listed.

| collection | month created | mean | median | mean (trim 2.5%) | total supply |

| avariksagauniverse | 2021-09 | 0.15 | 0.10 | 0.11 | 8888 |

| avastar | 2020-02 | 0.45 | 0.20 | 0.27 | 25458 |

| bcsnft | 2021-09 | 0.09 | 0.08 | 0.08 | 7777 |

| bored-mummy-baby-waking-up | 2021-08 | 0.13 | 0.10 | 0.11 | 3888 |

| collectvox | 2021-07 | 1.85 | 0.60 | 1.14 | 8888 |

| covidpunksnft | 2021-07 | 0.20 | 0.08 | 0.11 | 10000 |

| crypto-hodlers-nft | 2021-07 | 0.14 | 0.07 | 0.08 | 10000 |

| cryptomutts-official | 2021-09 | 0.12 | 0.06 | 0.08 | 10000 |

| cryptopunks | 2017-06 | 78.41 | 33.00 | 45.88 | 10000 |

| currencypunks | 2021-09 | 0.04 | 0.03 | 0.03 | 10000 |

| cyphercity | 2021-07 | 0.07 | 0.03 | 0.04 | 8886 |

| divineanarchy | 2021-11 | 0.32 | 0.29 | 0.29 | 10011 |

| doobits | 2021-07 | 0.02 | 0.02 | 0.02 | 10024 |

| dynamic-duelers | 2021-08 | 0.06 | 0.06 | 0.06 | 983 |

| dystopunks | 2021-06 | 2.39 | 1.10 | 1.87 | 2077 |

| evaverse | 2021-07 | 0.28 | 0.22 | 0.25 | 10000 |

| expansionpunks | 2021-08 | 0.30 | 0.17 | 0.23 | 10000 |

| fluf-world | 2021-08 | 3.05 | 1.33 | 2.06 | 10000 |

| fourierpunks | 2021-06 | 0.13 | 0.10 | 0.11 | 420 |

| guardians-of-the-metaverse | 2021-09 | 0.16 | 0.14 | 0.15 | 10000 |

| hashmasks | 2021-01 | 43.34 | 1.31 | 1.47 | 16384 |

| hd–punks | 2021-06 | 0.10 | 0.04 | 0.05 | 10000 |

| heavencomputer | 2021-08 | 0.27 | 0.17 | 0.25 | 7777 |

| influence-crew | 2021-09 | 0.24 | 0.10 | 0.15 | 7562 |

| lucha-libre-knockout | 2021-08 | 0.05 | 0.02 | 0.02 | 10000 |

| metahero-generative | 2021-09 | 5.69 | 5.25 | 5.44 | 6458 |

| misfit-university-official | 2021-06 | 0.05 | 0.02 | 0.03 | 10000 |

| mutant-punks-nft | 2021-10 | 0.05 | 0.04 | 0.04 | 10000 |

| neo-tokyo-identities | 2021-10 | 14.75 | 11.00 | 13.67 | 2021 |

| nfh | 2021-09 | 0.17 | 0.12 | 0.14 | 8888 |

| obitsofficial | 2021-09 | 0.23 | 0.16 | 0.18 | 7132 |

| octohedz | 2021-08 | 2.05 | 1.48 | 1.83 | 888 |

| octohedz-reloaded | 2021-10 | 0.10 | 0.07 | 0.09 | 8001 |

| pixls-official | 2021-03 | 0.25 | 0.15 | 0.20 | 5468 |

| role-for-metaverse | 2021-09 | 0.15 | 0.13 | 0.14 | 9800 |

| rug-wtf | 2021-07 | 0.06 | 0.03 | 0.05 | 10000 |

| skvllpvnkz-hideout | 2021-09 | 0.11 | 0.08 | 0.09 | 10000 |

| spunks-nft | 2021-06 | 0.21 | 0.09 | 0.12 | 10000 |

| srsc | 2021-06 | 240.37 | 0.07 | 0.07 | 8888 |

| stoned-ape-saturn-club | 2021-09 | 0.08 | 0.05 | 0.07 | 6969 |

| theantimasks | 2021-04 | 0.06 | 0.06 | 0.05 | 1551 |

| thelostglitches | 2021-08 | 0.18 | 0.09 | 0.13 | 9999 |

| wearetheoutkast | 2021-09 | 0.07 | 0.07 | 0.07 | 9996 |

| zunks | 2021-08 | 0.16 | 0.08 | 0.11 | 10000 |

A.3 Google NFT Searches Map

Below is a map of Google search data for the term “NFT” in the past 5 years (as of January 2023). Most searches occur in East Asia, North America, and Australia. Europe, South America, Middle East, and India roughly have the same amount of searches. Africa has the least number of searches.