Nonparametric Confidence Intervals for Generalized Lorenz Curve Using Modified Empirical Likelihood

Abstract

The Lorenz curve portrays income distribution inequality. In this article, we develop three modified empirical likelihood (EL) approaches, including adjusted empirical likelihood, transformed empirical likelihood, and transformed adjusted empirical likelihood, to construct confidence intervals for the generalized Lorenz ordinate. We demonstrate that the limiting distribution of the modified EL ratio statistics for the generalized Lorenz ordinate follows scaled Chi-Squared distributions with one degree of freedom. We compare the coverage probabilities and mean lengths of confidence intervals of the proposed methods with the traditional EL method through simulations under various scenarios. Finally, we illustrate the proposed methods using real data to construct confidence intervals.

Keywords: generalized Lorenz curve; empirical likelihood; modified empirical likelihood; confidence intervals; coverage probability

1 Introduction

The Lorenz curve developed by American economist Max Lorenz (Lorenz, (1905)) is a graphical representation used to describe income and wealth inequality. A Lorenz curve with perfect equality follows a diagonal line (45∘ angle) in which the income percentage is always proportional to the population percentage; however, in the real world, the Lorenz curve falls below this line. As the actual income distribution is rarely known, the distribution is typically estimated from income data. Several researchers have made contributions to Lorenz curves analysis, for example, Sen, (1973), Jakobsson, (1976), Goldie, (1977), and Marshall and Olkin, (1979). The full joint variance-covariance structure for the Lorenz curve ordinates was developed by Beach and Davidson, (1983). John et al., (1989) proposed new results on generalized Lorenz ordinate analysis that are relevant for proving second-degree stochastic dominance. Allen, (1990), Lambert, (2001), and Mosler and Koshevov, (2007) have made recent advances, with their findings leading to a wide range of applications, particularly in reliability theory. Ryu and Slottje, (1996) proposed an exponential polynomial expansion and a Bernstein polynomial expansion as two flexible functional form approaches for approximating Lorenz curves. Hasegawa and Kozumi, (2003) proposed a Bayesian non-parametric analysis approach with the Dirichlet process prior to Lorenz curve estimation with contaminated data. In particular, their method allows for heteroscedasticity in individual incomes. Further, the Lorenz curve has been used by several researchers to analyze physician distributions. For example, Chang and Halfon, (1997) examined variations in the distribution of pediatricians among the states between 1982 and 1992 using Lorenz curves and Gini indices. Kobayashi and Takaki, (1992) used the Lorenz curve and the Gini coefficient to study the disparity in physician distribution in Japan.

Empirical likelihood (EL) is a nonparametric method introduced by Owen, (2001), an alternative to the standard parametric likelihood that inherits many alluring features such as its extension of Wilks’ theorem, asymmetric confidence interval, better coverage for small sample sizes, and so on. Many researchers have studied EL for the Lorenz curve. For instance, Belinga-Hall, (2007) and Yang et al., (2012) developed plug-in empirical likelihood-based inferences to construct confidence intervals for the generalized Lorenz curve. Qin et al., (2013) studied EL-based confidence interval for the Lorenz curve under the simple random sampling and the stratified random sampling

designs. Shi and Qin, (2019) proposed new nonparametric confidence intervals using the influence function-based empirical likelihood method for the Lorenz curve and showed that the limiting distributions of the

empirical log-likelihood ratio statistics for the Lorenz ordinates were standard chi-square

distributions. Luo and Qin, (2019) suggested a kernel smoothing estimator for the Lorenz curve and developed a smoothed jackknife empirical likelihood approach for constructing confidence intervals of Lorenz ordinates.

Despite being widely used, the EL-based approach has two major drawbacks: (1) The convex hull must have vector zero as its interior point in order to solve the profile empirical likelihood problem. According to Owen, (2001), the empirical likelihood function should be set to if the convex hull does not have zero as an interior point. However, Chen et al., (2008), pointed out that this makes it difficult to find the maximum of the EL function. (2) The EL technique frequently experiences under-coverage problems, see Tsao, (2013) for more details. To address these problems, numerous strategies have been proposed in the literature. Chen et al., (2008) proposed adjusted empirical likelihood method (AEL), for example, confirms the existence of a solution in the maximization problem while preserving asymptotic optimality properties. Further, Jing et al., (2017) suggested the transformed empirical likelihood to tackle the under-coverage problem for small sample sizes (TEL). Stewart and Ning, (2020) proposed the transformed adjusted empirical likelihood (TAEL), a strategy that combines the AEL and TEL approaches. The AEL, TEL, and TAEL approaches are proven to be effective in many applications, for example, Li et al., (2022) investigated modified EL-based confidence intervals for quantile

regression models with longitudinal data. Ratnasingam and Ning, (2022) studied all three modified versions of EL procedures to construct confidence intervals of the mean residual life function with length-biased data.

In this research, we develop three modified EL-based inference procedures to construct confidence intervals for the generalized Lorenz curve. These modified EL methods aim to address the shortcomings of traditional EL, including the issue of under-coverage, while also ensuring the existence of a solution for the maximization procedure. To the best of our knowledge, this is the first study to investigate AEL, TEL, and TAEL methods for constructing confidence intervals for the generalized Lorenz ordinate.

The remainder of this paper is organized as follows. In Section 2, we briefly describe the fundamental properties of EL for the generalized Lorenz curve and provide the methodology of AEL, TEL, and TAEL for the generalized Lorenz curve. In Section 3, we conduct an extensive simulation study to compare the finite sample performances of the proposed confidence intervals for the generalized Lorenz ordinates. In Section 4, we use an income dataset to illustrate the proposed intervals. In Section 5, we discuss our results and draw conclusions.

2 Empirical Likelihood Based Methods

2.1 Empirical Likelihood

Let be a random variable with cumulative distribution function (CDF) denoted by with finite support. For instance, denotes the CDF of income or wealth distribution. Following Gastwirth, (1971), a general definition of the Lorenz curve is provided below.

| (1) |

where denotes the mean of , and is the th quantile of . For a fixed , the Lorenz ordinate is the ratio of the mean income of the lowest -th fraction of households and the mean income of total households. The generalized Lorenz curve is defined as follows.

| (2) |

Because the income distribution is rarely known in practice, the Lorenz curve is typically estimated from income data. Hence, the empirical estimator for is defined as

| (3) |

where is the empirical distribution function of the ’s, is the sample mean, is the th sample quantile of the ’s. From the definition of the generalized Lorenz curve, we observe that

Therefore, the empirical likelihood of can be expressed as

| (4) |

where is a probability vector satisfying and for all , and . It can be seen that in (4) depends on the unknown quantile . As a result, the generalized Lorenz ordinate is the mean of the random variable truncated at . Using sample data, the empirical likelihood for as follows:

| (5) |

where . When the vector is contained within the convex hull defined by equation (5) attains its unique maximum value. By applying the Lagrange multiplier method, we can determine, as follows.

where is the solution to

Note that , subject to , attains its maximum at . Thus, the EL ratio for is given as

| (6) |

Hence, the profile empirical log-likelihood ratio for is

| (7) |

Theorem 2.1.

If and for any given then the limiting distribution of is a scaled chi-square distribution with one degree of freedom,

| (8) |

where and .

Although the scale constant is unknown, it can be consistently estimated by using the following formula.

| (9) | ||||

Thus, an asymptotic confidence interval for generalized Lorenz ordinate, at a fixed time is given as follows

| (10) |

where is the upper quantile of the distribution of . For more details, we refer to Yang et al., (2012). As previously stated, the original EL method experiences low coverage probability, particularly for small sample sizes, for example, Chen et al., (2008) and Jing et al., (2017). Next, we describe the technical details of three modified EL-based methods for constructing confidence intervals. These methods are called AEL, TEL, and TAEL, and they are used for constructing confidence intervals for the generalized Lorenz ordinate , at a fixed time for .

2.2 Adjusted Empirical Likelihood for Generalized Lorenz Ordinate

Chen et al., (2008) proposed the adjusted empirical likelihood (AEL) in order to address the challenge of the non-existence of a solution in the equation (7). We adopted the idea of the AEL method for generalized Lorenz ordinate. We define . The pseudo value where . Using the observations, we define the adjusted empirical likelihood as

| (11) |

Thus, the adjusted empirical log-likelihood ratio is given by

| (12) |

Theorem 2.2.

Assume that . For all , let be the adjusted log-empirical likelihood ratio function defined by (12) and . We have

| (13) |

in distribution.

Thus, an asymptotic confidence interval for at a fixed time is given as follows

| (14) |

where is the upper quantile of the distribution of .

2.3 Transformed Empirical Likelihood for Generalized Lorenz Ordinate

Jing et al., (2017) proposed the transformed empirical likelihood (TEL) as a simple transformation of the original EL to tackle the under-coverage problem. They claimed that TEL is superior in small sample sizes and multidimensional situations. The transformed empirical log-likelihood ratio can be defined as

| (17) |

where is given in (7) and . It should be noted that ensures the maximum expansion without violating the conditions (C2) stated in Jing et al., (2017). Hence, the transformed empirical log-likelihood ratio is defined as

| (18) |

Thus, the transformed empirical log-likelihood ratio is given as

| (19) |

Further, Jing et al., (2017) showed that the TEL ratio meets four conditions that ensure the likelihood ratio’s asymptotic properties.

Theorem 2.3.

Assume that for all let be the transformed log-empirical likelihood ratio function defined by (18). We have

| (20) |

in distribution.

Thus, an asymptotic confidence interval for at a fixed time is given as follows

| (21) |

where is the upper quantile of the distribution of .

Proof.

The proof is omitted as it is similar to the proof of Theorem 3.2 in Ratnasingam and Ning, (2022). ∎

2.4 Transformed Adjusted Empirical Likelihood for Generalized Lorenz Ordinate

Stewart and Ning, (2020) developed a hybrid method based upon AEL and TEL methods called transformed adjusted empirical likelihood (TAEL). The TAEL method combines the benefits of both AEL and TEL methods. Let . We define

| (22) |

where defined in (12). Thus, for , the transformed empirical log-likelihood ratio is defined as,

| (23) |

This can be further viewed as

| (24) |

Theorem 2.4.

Assume that for all let be the transformed log-empirical likelihood ratio function defined by (24). We have

| (25) |

in distribution.

Thus, an asymptotic confidence interval for at a fixed time is given as follows

| (26) |

where is the upper quantile of the distribution of .

3 Simulation Study

In this section, we conduct a simulation study to compare the performance of the proposed AEL, TEL, and TAEL-based confidence regions for the generalized Lorenz curve with EL-based confidence regions under various sample sizes in terms of coverage probabilities (CP) and mean lengths (ML) of the confidence intervals. The CP represents the proportion of times that the confidence regions contain the true value of the parameter among simulation runs.

Since most income distributions are positively skewed, the Weibull, Chi-square, and Skew-Normal distributions appear to provide a good fit for the income data. Thus, in our simulation study, we consider that the overall distribution function is:

-

1.

Weibull distribution with shape parameter , scale parameter . The pdf of the Weibull distribution is given by

-

2.

distribution with degrees of freedom. The pdf of the Chi-square distribution is given by

-

3.

Skew-Normal distribution with location parameter , scale parameter , and shape parameter . The pdf of the skew-normal distribution is given by:

where and are the pdf and cdf of the standard normal distribution. Further, in short-hand notation, we denote the skew-normal distribution by .

We choose the sample size, and representing a range from small to large, and values of }. Further, we set the nominal significance level . The results are based on 10000 iterations. To assess the performance of the proposed methods, we consider two commonly used criteria for evaluating the goodness of a confidence interval procedure. These criteria are:

-

1.

Coverage probability: Preferably, close to 95%.

-

2.

Mean lengths: Smaller is preferable.

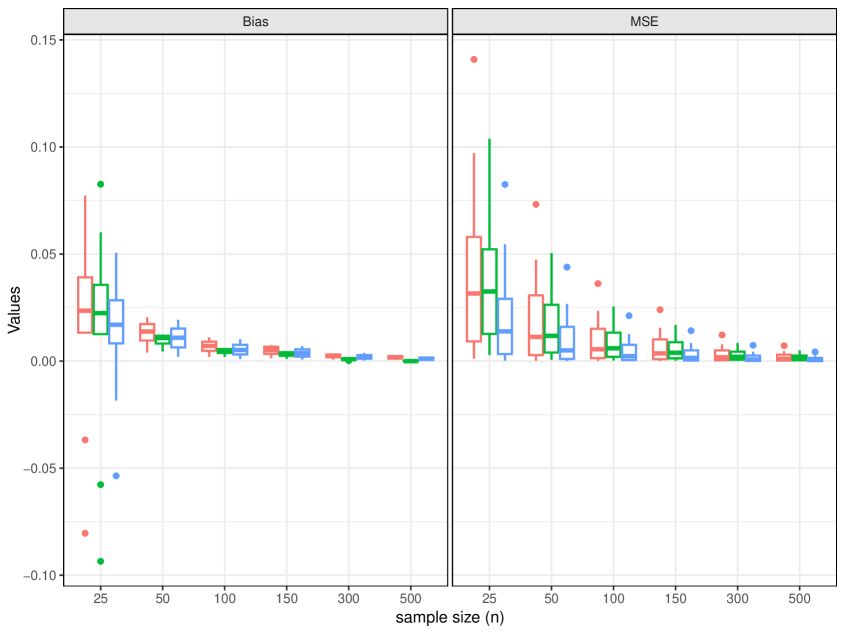

First, we compute bias and mean squared error (MSE) of the estimates for the generalized Lorenz ordinates for various distributions, including Weibull (1,2), , and . The results are summarized in Table 1 and graphed in Figure 1. It is evident that the bias of the estimate is consistently close to zero across all scenarios. Moreover, as the sample size increases, both bias and MSE generally decrease. Furthermore, it’s notable that irrespective of the sample size, both bias and MSE increase as the value of increases.

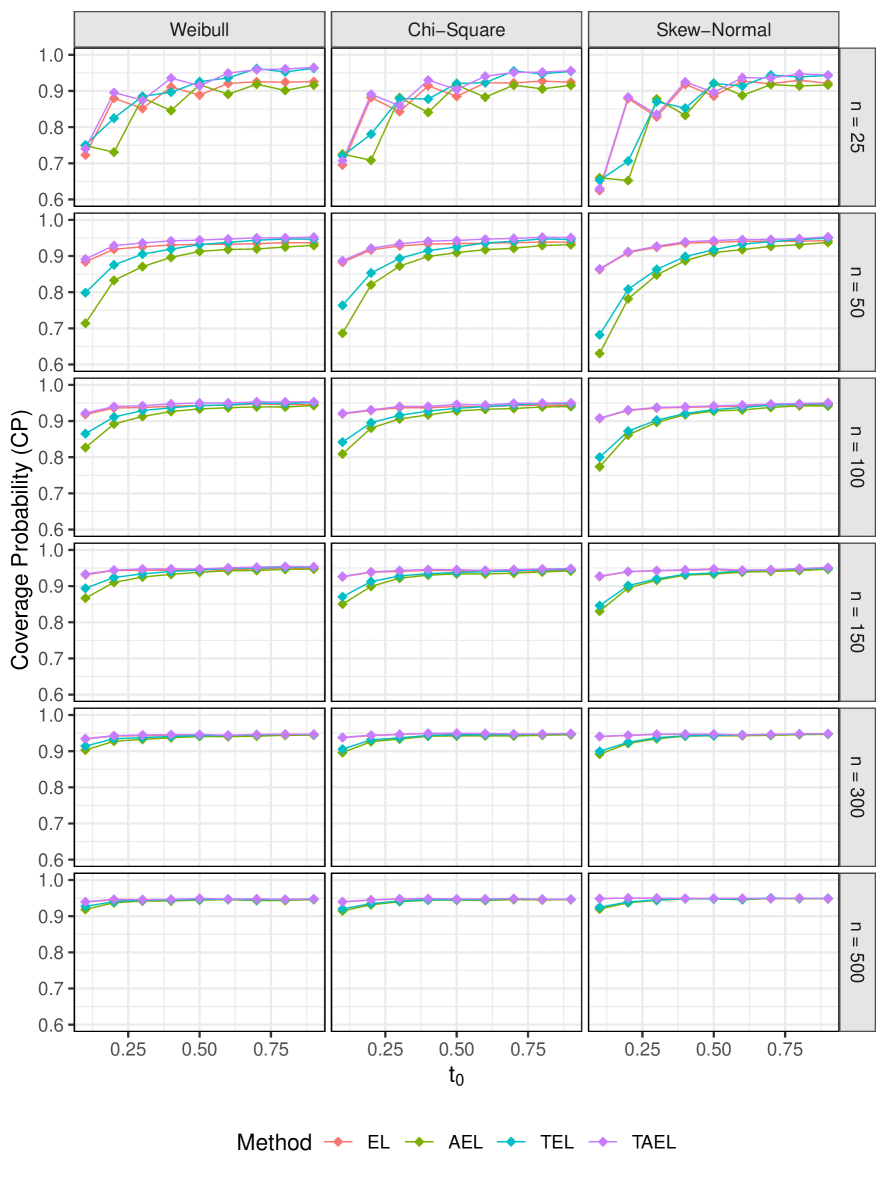

Next, we compute the coverage probability and mean lengths of the confidence regions for the generalized Lorenz ordinates . The coverage probabilities are graphed in Figures 2. In all cases, the CP tends to increase as the sample size increases. Among all four methods, the TAEL method consistently provides the highest CP. In particular, the TAEL approach occasionally results in over-coverage issues. For , the TEL method outperforms EL, and AEL performs either slightly better or on par with the EL method. However, for , the EL approach performs significantly better than AEL and slightly better than the TEL method.

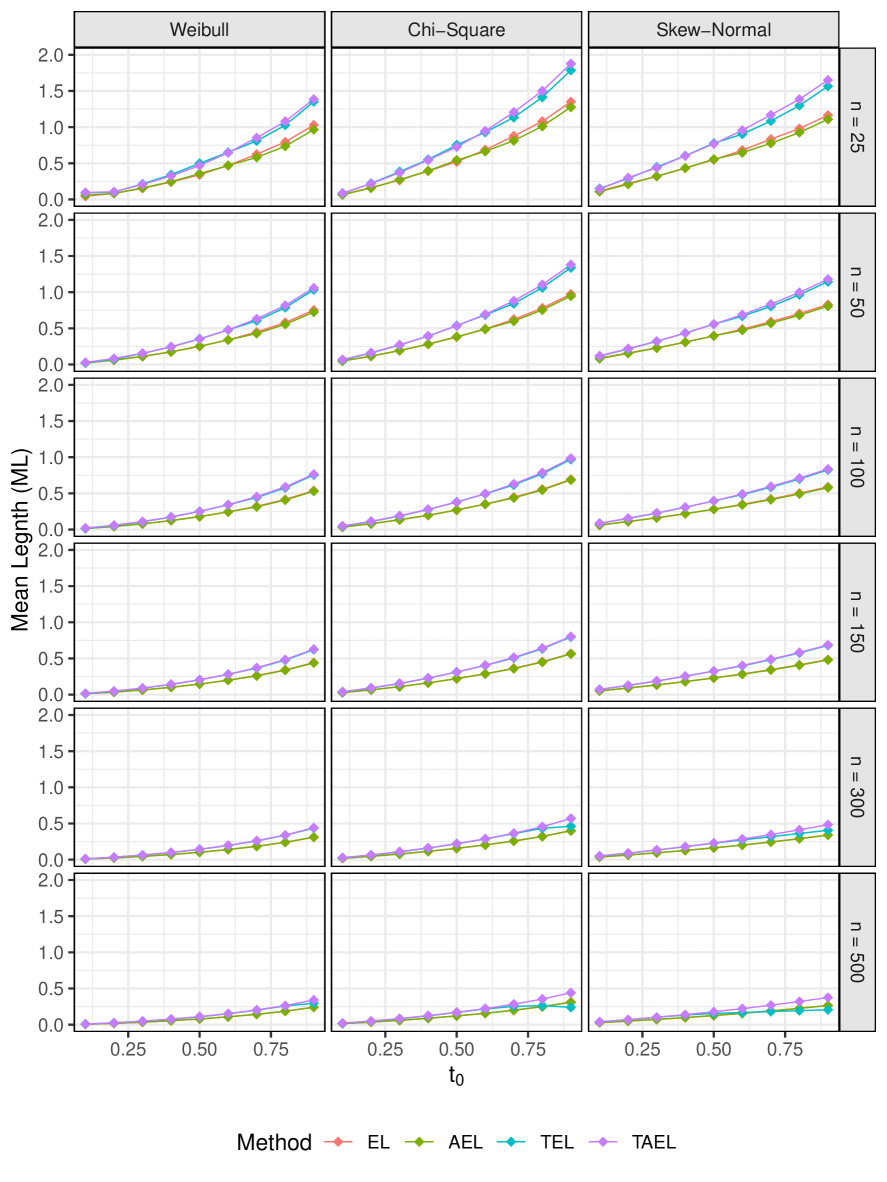

When considering the mean lengths of confidence intervals, the TAEL method yields a slightly longer mean length, but it remains within an acceptable range. Among all four methods, the AEL results in the shortest confidence intervals. For , the confidence intervals based on the TEL and TAEL approaches have approximately the same mean lengths. In addition, regardless of the method, as increases, the mean length also increases. However, as the sample size increases, the mean length of the confidence interval decreases. The mean lengths of confidence intervals are illustrated in Figure 3.

| Weibull(1,2) | |||||||

|---|---|---|---|---|---|---|---|

| Bias | MSE | Bias | MSE | Bias | MSE | ||

| 25 | 0.1 | 0.0095 | 0.0002 | 0.0214 | 0.0011 | 0.0356 | 0.0028 |

| 0.2 | 0.0083 | 0.0007 | 0.0133 | 0.0023 | 0.0126 | 0.0039 | |

| 0.3 | 0.0284 | 0.0033 | 0.0489 | 0.0092 | 0.0601 | 0.0127 | |

| 0.4 | 0.0170 | 0.0052 | 0.0235 | 0.0129 | 0.0184 | 0.0147 | |

| 0.5 | 0.0506 | 0.0139 | 0.0773 | 0.0316 | 0.0826 | 0.0325 | |

| 0.6 | 0.0253 | 0.0191 | 0.0319 | 0.0398 | 0.0224 | 0.0365 | |

| 0.7 | -0.0184 | 0.0291 | -0.0368 | 0.0580 | -0.0577 | 0.0522 | |

| 0.8 | 0.0328 | 0.0545 | 0.0391 | 0.0972 | 0.0236 | 0.0744 | |

| 0.9 | -0.0536 | 0.0825 | -0.0804 | 0.1409 | -0.0935 | 0.1038 | |

| 50 | 0.1 | 0.0020 | 0.0000 | 0.0040 | 0.0002 | 0.0045 | 0.0006 |

| 0.2 | 0.0042 | 0.0003 | 0.0070 | 0.0010 | 0.0065 | 0.0019 | |

| 0.3 | 0.0064 | 0.0010 | 0.0096 | 0.0028 | 0.0082 | 0.0040 | |

| 0.4 | 0.0087 | 0.0024 | 0.0118 | 0.0060 | 0.0096 | 0.0072 | |

| 0.5 | 0.0109 | 0.0050 | 0.0138 | 0.0113 | 0.0108 | 0.0118 | |

| 0.6 | 0.0130 | 0.0092 | 0.0156 | 0.0192 | 0.0118 | 0.0181 | |

| 0.7 | 0.0152 | 0.0160 | 0.0173 | 0.0307 | 0.0123 | 0.0263 | |

| 0.8 | 0.0173 | 0.0267 | 0.0190 | 0.0474 | 0.0124 | 0.0369 | |

| 0.9 | 0.0193 | 0.0439 | 0.0205 | 0.0732 | 0.0114 | 0.0505 | |

| 100 | 0.1 | 0.0010 | 0.0000 | 0.0020 | 0.0001 | 0.0020 | 0.0003 |

| 0.2 | 0.0020 | 0.0001 | 0.0035 | 0.0005 | 0.0030 | 0.0009 | |

| 0.3 | 0.0031 | 0.0005 | 0.0048 | 0.0014 | 0.0038 | 0.0020 | |

| 0.4 | 0.0042 | 0.0011 | 0.0059 | 0.0029 | 0.0046 | 0.0036 | |

| 0.5 | 0.0052 | 0.0023 | 0.0071 | 0.0055 | 0.0051 | 0.0060 | |

| 0.6 | 0.0064 | 0.0043 | 0.0082 | 0.0093 | 0.0054 | 0.0091 | |

| 0.7 | 0.0076 | 0.0076 | 0.0091 | 0.0151 | 0.0057 | 0.0133 | |

| 0.8 | 0.0090 | 0.0127 | 0.0101 | 0.0235 | 0.0058 | 0.0186 | |

| 0.9 | 0.0102 | 0.0212 | 0.0111 | 0.0362 | 0.0055 | 0.0255 | |

| 150 | 0.1 | 0.0007 | 0.0000 | 0.0014 | 0.0001 | 0.0011 | 0.0002 |

| 0.2 | 0.0014 | 0.0001 | 0.0025 | 0.0003 | 0.0019 | 0.0006 | |

| 0.3 | 0.0021 | 0.0003 | 0.0034 | 0.0009 | 0.0025 | 0.0013 | |

| 0.4 | 0.0029 | 0.0007 | 0.0043 | 0.0020 | 0.0031 | 0.0024 | |

| 0.5 | 0.0037 | 0.0015 | 0.0052 | 0.0036 | 0.0036 | 0.0039 | |

| 0.6 | 0.0045 | 0.0029 | 0.0061 | 0.0062 | 0.0039 | 0.0060 | |

| 0.7 | 0.0055 | 0.0050 | 0.0067 | 0.0101 | 0.0041 | 0.0088 | |

| 0.8 | 0.0063 | 0.0085 | 0.0072 | 0.0156 | 0.0043 | 0.0123 | |

| 0.9 | 0.0070 | 0.0142 | 0.0075 | 0.0240 | 0.0042 | 0.0169 | |

| 300 | 0.1 | 0.0003 | 0.0000 | 0.0007 | 0.0000 | 0.0002 | 0.0001 |

| 0.2 | 0.0007 | 0.0000 | 0.0013 | 0.0002 | 0.0005 | 0.0003 | |

| 0.3 | 0.0011 | 0.0001 | 0.0018 | 0.0004 | 0.0007 | 0.0006 | |

| 0.4 | 0.0015 | 0.0004 | 0.0021 | 0.0010 | 0.0009 | 0.0012 | |

| 0.5 | 0.0019 | 0.0008 | 0.0026 | 0.0018 | 0.0010 | 0.0020 | |

| 0.6 | 0.0023 | 0.0015 | 0.0030 | 0.0031 | 0.0010 | 0.0030 | |

| 0.7 | 0.0028 | 0.0026 | 0.0032 | 0.0050 | 0.0011 | 0.0044 | |

| 0.8 | 0.0034 | 0.0044 | 0.0032 | 0.0079 | 0.0010 | 0.0062 | |

| 0.9 | 0.0038 | 0.0074 | 0.0030 | 0.0122 | 0.0008 | 0.0085 | |

| 500 | 0.1 | 0.0002 | 0.0000 | 0.0005 | 0.0000 | -0.0002 | 0.0001 |

| 0.2 | 0.0004 | 0.0000 | 0.0009 | 0.0001 | -0.0001 | 0.0002 | |

| 0.3 | 0.0007 | 0.0001 | 0.0012 | 0.0003 | 0.0000 | 0.0004 | |

| 0.4 | 0.0009 | 0.0002 | 0.0015 | 0.0006 | 0.0000 | 0.0007 | |

| 0.5 | 0.0011 | 0.0005 | 0.0018 | 0.0011 | 0.0000 | 0.0012 | |

| 0.6 | 0.0014 | 0.0009 | 0.0021 | 0.0019 | 0.0000 | 0.0018 | |

| 0.7 | 0.0016 | 0.0015 | 0.0023 | 0.0030 | 0.0000 | 0.0026 | |

| 0.8 | 0.0019 | 0.0026 | 0.0024 | 0.0047 | -0.0001 | 0.0037 | |

| 0.9 | 0.0022 | 0.0043 | 0.0024 | 0.0072 | -0.0002 | 0.0050 | |

4 Application to Real Data

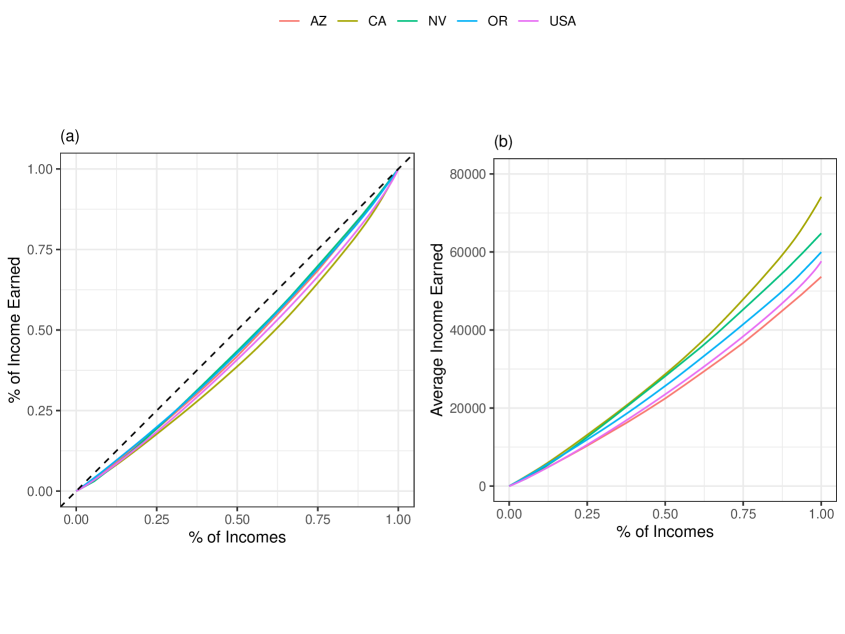

In this section, we demonstrate the effectiveness of the proposed AEL, TEL, and TAEL methods for generalized Lorenz ordinate by constructing confidence intervals for Median Household Income in 2020. The data set is available https://www.ers.usda.gov/data-products/county-level-data-sets/download-data/, which contains 3194 observations of the median household income in 2020, and they are grouped by state or county name. We mainly focus on examining the median income distribution of households in Arizona (AZ), California (CA), Nevada (NV), Oregon (OR), and the US as a whole. The Lorenz curves and the generalized Lorenz curves for the four states and the US are graphed in Figure 4. The black dashed line represents the equality line. It is evident that Arizona has the Lorenz curve that is closest to the equality line. Further, the USA has the most unequal income distribution, followed by California and Nevada. We also compute a 95% confidence interval for the generalized Lorenz ordinate using EL, AEL, TEL, and TAEL methods with various values considering . We considered all 3194 observations for the purposes of this analysis. The results are summarized in Table 2 and they are plotted in Figure 5. We notice that EL and AEL perform similarly while TEL and TAEL roughly produce the same confidence intervals. Additionally, the AEL approach consistently yields a shorter confidence length than the other three methods.

| Method | Lower | Upper | Length | ||

|---|---|---|---|---|---|

| 0.1 | 3815.195 | EL | 3759.1760 | 3871.7118 | 112.5535 |

| AEL | 3757.9974 | 3870.5021 | 112.5048 | ||

| TEL | 3756.8501 | 3871.6701 | 114.8200 | ||

| TAEL | 3758.0284 | 3872.8800 | 114.8516 | ||

| 0.2 | 8240.058 | EL | 8145.7837 | 8334.8855 | 189.1324 |

| AEL | 8143.2260 | 8332.2851 | 189.0591 | ||

| TEL | 8140.5307 | 8335.0126 | 194.4819 | ||

| TAEL | 8143.0881 | 8337.6133 | 194.5251 | ||

| 0.3 | 13027.020 | EL | 12896.9940 | 13157.5745 | 260.6236 |

| AEL | 12908.4210 | 13168.9741 | 260.5531 | ||

| TEL | 12903.4394 | 13173.9962 | 270.5568 | ||

| TAEL | 12892.0084 | 13162.6007 | 270.5923 | ||

| 0.4 | 18138.190 | EL | 17973.2271 | 18303.5235 | 330.3522 |

| AEL | 17967.5732 | 18297.8236 | 330.2504 | ||

| TEL | 17959.0887 | 18306.3482 | 347.2595 | ||

| TAEL | 17964.7429 | 18312.0477 | 347.3048 | ||

| 0.5 | 23514.140 | EL | 23312.6016 | 23715.7678 | 403.2358 |

| AEL | 23322.5887 | 23725.6854 | 403.0967 | ||

| TEL | 23307.9250 | 23740.3629 | 432.4379 | ||

| TAEL | 23297.9302 | 23730.4531 | 432.5230 | ||

| 0.6 | 29186.760 | EL | 28947.5843 | 29425.4732 | 477.9736 |

| AEL | 28956.5766 | 29434.2810 | 477.7044 | ||

| TEL | 28930.0349 | 29460.7166 | 530.6816 | ||

| TAEL | 28921.0092 | 29451.9423 | 530.9331 | ||

| 0.7 | 35224.900 | EL | 34941.7069 | 35506.5735 | 564.9692 |

| AEL | 34929.3294 | 35494.0013 | 564.6719 | ||

| TEL | 34863.9490 | 35558.6065 | 694.6575 | ||

| TAEL | 34876.1887 | 35571.3135 | 695.1248 | ||

| 0.8 | 41650.550 | EL | 41323.3627 | 41974.1675 | 650.9197 |

| AEL | 41328.4634 | 41979.0655 | 650.6021 | ||

| TEL | 41191.9480 | 42112.0198 | 920.0719 | ||

| TAEL | 41186.8051 | 42107.1635 | 920.3584 | ||

| 0.9 | 48694.690 | EL | 48301.5894 | 49079.4584 | 777.9221 |

| AEL | 48304.5085 | 49082.1298 | 777.6213 | ||

| TEL | 48139.2496 | 49239.0692 | 1099.8196 | ||

| TAEL | 48136.2785 | 49236.4482 | 1100.1697 |

5 Discussions

In this article, we proposed powerful nonparametric EL-based methods for constructing confidence intervals for generalized Lorenz ordinate. These methods include the adjusted empirical likelihood (AEL), the transformed empirical likelihood (TEL), and the transformed adjusted empirical likelihood (TAEL). We derive the limiting distributions of the generalized Lorenz ordinate based on the AEL, TEL, and TAEL methods. Simulations show that the proposed TEL and TAEL methods improve the coverage probability compared to the EL method. According to the simulation study, we highly recommend the TAEL method for and small sample sizes. When , both the EL and AEL approaches yield comparable results for medium and large samples, making AEL an additional option. While the TEL method is suitable for large samples , the TAEL method is appropriate for all sample sizes. In real-world applications, we recommend the TAEL approach as it consistently offers superior coverage compared to the other three methods. It’s worth noting although the confidence intervals based on the TAEL approach are longer than others, they remain within an acceptable range. Our real-world data application demonstrates that the proposed methods are competitive with the EL method while also addressing its limitations.

Declarations

Conflict of interest The authors declare that they have no conflict of interest.

Acknowledgements

We would like to thank two anonymous referees for their comments, which have contributed to this improved version of the work. We also would like to express our appreciation to the Office of Student Research (OSR) at California State University, San Bernardino, for creating a supportive environment for conducting this research.

References

References

- Allen, (1990) Allen, A. (1990). Probability, statistics, and queuing theory with computer science applications. 2nd ed., Academic Press.

- Beach and Davidson, (1983) Beach, C. M. and Davidson, R. (1983). Distribution-free statistical inference with lorenz curves and income shares. The Review of Economic Studies, 50(4):723–735.

- Belinga-Hall, (2007) Belinga-Hall, N. (2007). Empirical likelihood confidence intervals for generalized lorenz curve. Thesis, Georgia State University.

- Chang and Halfon, (1997) Chang, R. and Halfon, N. (1997). Graphical distribution of pediatricians in the united states: An analysis of the fifty states and washington, dc. Pediatrics, 100:172–179.

- Chen et al., (2008) Chen, J., Variyath, A., and Abraham, B. (2008). Adjusted empirical likelihood and its properties. Journal of Computational and Graphical Statistics, 17(2):426–443.

- Gastwirth, (1971) Gastwirth, J. L. (1971). A general definition of lorenz curve. Econometrica, 39:1037–1039.

- Goldie, (1977) Goldie, C. M. (1977). Convergence theorems for empirical lorenz curves and their inverses. Advances in applied probability, 9:765–791.

- Hasegawa and Kozumi, (2003) Hasegawa, H. and Kozumi, H. (2003). Estimation of lorenz curves: a bayesian nonparametric approach. Journal of Econometrics, 115(2):277–291.

- Jakobsson, (1976) Jakobsson, U. (1976). On the measurement of the degree of progression. Journal of Public Economics, 5:161–168.

- Jing et al., (2017) Jing, B.-Y., Tsao, M., and Zhou, W. (2017). Transforming the empirical likelihood towards better accuracy. The Canadian Journal of Statistics, 45(3):340–352.

- John et al., (1989) John, A. B., Chakraborti, S., and Paul, D. T. (1989). Asymptotically distribution-free statistical inference for generalized lorenz curves. The Review of Economics and Statistics, 71(4):725–727.

- Kobayashi and Takaki, (1992) Kobayashi, Y. and Takaki, H. (1992). Geographic distribution of physicians in japan. Lancet., 340:1391–1393.

- Lambert, (2001) Lambert, P. J. (2001). The distribution and redistribution of income: A mathematical analysis. 2nd Edition., Manchester University Press, Manchester.

- Li et al., (2022) Li, M., Ratnasingam, S., and Ning, W. (2022). Empirical-likelihood-based confidence intervals for quantile regression models with longitudinal data. Journal of Statistical Computation and Simulation, 92(12):2536–2553.

- Lorenz, (1905) Lorenz, M. C. (1905). Method of measuring the concentration of wealth. J. Ame. Statist., 9:209–219.

- Luo and Qin, (2019) Luo, S. and Qin, G. (2019). Jackknife empirical likelihood-based inferences for lorenz curve with kernel smoothing. Communications in Statistics-Theory and Methods, 48(3):559–582.

- Marshall and Olkin, (1979) Marshall, W. and Olkin, I. (1979)). Inequalities: Theory of majorization and its applications. Academic Press, New York.

- Mosler and Koshevov, (2007) Mosler, K. and Koshevov, G. (2007). Multivariate lorenz dominance based on zonoids. ASTA: Advances in Statistical Analysis,, 91:57–76.

- Owen, (2001) Owen, A. B. (2001). Empirical likelihood. Chapman & Hall, New York. 1st edtion.

- Qin et al., (2013) Qin, G., Yang, B., and Belinga-Hall, N. (2013). Empirical likelihood-based inferences for the lorenz curve. Annals of the Institute of Statistical Mathematics volume, 65:1–21.

- Ratnasingam and Ning, (2022) Ratnasingam, S. and Ning, W. (2022). Confidence intervals of mean residual life function in length-biased sampling based on modified empirical likelihood. Journal of Biopharmaceutical Statistics, DOI: 10.1080/10543406.2022.2089157.

- Ryu and Slottje, (1996) Ryu, H. K. and Slottje, D. J. (1996). Two flexible functional form approaches for approximating the lorenz curve. Journal of Econometrics, 72:251–274.

- Sen, (1973) Sen, A. (1973). On economic inequality. Oxford: Clarendon Press;, New York, Norton.

- Shi and Qin, (2019) Shi, Y. Liu, B. and Qin, G. (2019). Influence function-based empirical likelihood and generalized confidence intervals for the lorenz curve. Statistical Methods & Applications, 29:427–446.

- Stewart and Ning, (2020) Stewart, P. and Ning, W. (2020). Modified empirical likelihood-based confidence intervals for data containing many zero observations. Computational Statistics, 35 (4):2019–2042.

- Tsao, (2013) Tsao, M. (2013). Extending the empirical likelihood by domain expansion. Can J Stat, 41(2):257–274.

- Yang et al., (2012) Yang, B. Y., Qin, G. S., and Belinga-Hill, N. E. (2012). Non-parametric inferences for the generalized lorenz curve. Sci Sin Math, 42(3):235–250.