[1]organization=Department of Mathematics and Systems Analysis, addressline=Aalto University, School of Science, postcode=FI-00076 Aalto, country=Finland \affiliation[2]organization=Finnish Meteorological Institute, city=Helsinki, country=Finland

Solving decision problems with endogenous uncertainty and conditional information revelation using influence diagrams

Abstract

Despite methodological advances for modeling decision problems under uncertainty, representing endogenous uncertainty still proves challenging both in terms of modeling capabilities and computational requirements. A novel reformulation based on rooted junction trees (RJTs) provides an approach for solving such decision problems using off-the-shelf mathematical optimization solvers. This is made possible by using influence diagrams to represent a given decision problem and reformulating them as RJTs, which are then represented as a mixed-integer linear programming problem.

In this paper, we focus on the type of endogenous uncertainty that received less attention in the rooted junction tree approach: conditionally observed information. Multi-stage stochastic programming models use conditional non-anticipativity constraints to represent such uncertainties, and we show how such constraints can be incorporated into RJT models. This allows us to consider the two main types of endogenous uncertainty simultaneously, namely decision-dependent information structure and decision-dependent probability distribution. Finally, the extended framework is illustrated with a large-scale cost-benefit problem regarding climate change mitigation.

keywords:

endogenous uncertainty , stochastic programming , junction trees , climate change mitigation1 Introduction

Stochastic programming (SP) is one of the most widespread mathematical programming-based frameworks for decision-making under uncertainty. In general, SP casts decision problems subject to parametric uncertainty as deterministic equivalents in the form of large-scale linear or mixed-integer programming (LP/MIP) problems that can be solved with standard optimization techniques. A common assumption in SP models is that the stochastic processes, particularly the state probabilities and/or observed values, are not influenced by the previously made decisions. The uncertainty is thus exogenous. This is methodologically convenient, for the deterministic equivalent model has the same nature as its stochastic counterpart, retaining important characteristics such as linearity, or more generally, convexity.

In this paper, we focus on a much less explored class of stochastic problems presenting endogenous uncertainty. In this more general setting, the decisions made at previous stages can affect the uncertainty faced in later stages. It is common to classify SP problems according to the nature of the endogenous structure arising in the decision problem. Hellemo et al. (2018) propose a taxonomy of such problems, classifying the endogenous uncertainties into two distinct types. In Type 1 problems, earlier decisions influence the later events’ probability distribution (i.e., realizations and/or the probabilities associated with each realization). For example, deciding to perform maintenance on a car engine influences the probability of it breaking in the future. In Type 2 problems, the information structure is influenced by the decision-making. Continuing with the car example, deciding to inspect the engine does not affect the probability of it breaking, but provides information that enables a better-informed maintenance decision. It is noteworthy that Type 2 is more common in the literature on decision-making under endogenous uncertainty. Hellemo et al. (2018) also introduce Type 3, which combines the Type 1 and Type 2 endogenous uncertainties.

Our main contribution is to provide a framework general enough to address both types simultaneously, resulting in Type 3 endogenously uncertain SP (T3ESP) problems, while still retaining prior computationally favorable properties of the mathematical model such as linearity or convexity. Our proposed framework builds upon the work by Parmentier et al. (2020) and Herrala et al. (2023) and expands the models to consider Type 2 endogenous uncertainty. A major advantage of this approach is the ability to incorporate Type 1 endogenous uncertainties in the decision process in an intuitive way by using an influence diagram representation of the problem. This representation is then reformulated into a rooted junction tree and further converted to a mixed-integer linear programming (MILP) problem, for which powerful off-the-shelf solvers exist. The intermediate step is not strictly necessary, as Salo et al. (2022) present an alternative formulation directly converting the influence diagram into a MILP. However, as discussed in Herrala et al. (2023), the RJT representation results in better computational performance. Salo et al. (2022) present a simple problem with Type 2 endogenous uncertainty using their Decision Programming framework but do not discuss this class of endogenous uncertainty in detail. This paper explores Type 2 endogenous uncertainty further, showing explicitly how the RJT reformulation can be enhanced to become a suitable framework for T3ESP problems comprising both Type 1 and 2 endogenous uncertainties.

The formulation presented in Parmentier et al. (2020) accommodates only discrete decisions, and Salo et al. (2022) acknowledge the limitations of using influence diagram-based formulations for problems involving continuous decisions, discussed in more detail in Bielza et al. (2011). In addition to discussing T3ESP problems, we show that if the problem has a separable structure, it is possible to incorporate continuous decisions that do not affect the endogenous probabilities in the model. This is demonstrated in a climate change mitigation case study, but we note that similar structures are likely to arise in other problems as well. Indeed, Lee et al. (2021) show how such structures can be used in a submodel-tree decomposition for influence diagrams. In the case study that originally motivated our developments, we consider uncertain climate parameters and technological progress and the problem of determining the optimal strategy for climate and technology research, as well as the optimal emission levels for 2030-2070.

This paper is structured as follows. In Section 2, we present an overview of multi-stage stochastic programming. In Section 3, our methodological contributions are described in detail, starting from the formulation in Parmentier et al. (2020) and continuing with conditionally observed information. In Section 4 we illustrate the use of the framework by considering a larger-scale problem of climate change cost-benefit analysis. Section 5 concludes and provides directions for further development.

2 Modeling problems with endogenous and exogenous uncertainties

Solution approaches for MSSP are often based on formulating the deterministic equivalent problem using a scenario tree, as described in, e.g., Ruszczyński (1997). A scenario tree represents the structure of the uncertain decision process, and non-anticipativity constraints (NACs) (Rockafellar and Wets, 1991) are employed to enforce the information structure in the formulation. NACs state that a decision must be the same for two scenarios if those scenarios are indistinguishable when making the decision.

In endogenously uncertain problems, the decisions can affect the timing, event probabilities, or outcomes of uncertain events further in the process. As previously discussed, endogenous uncertainty is often divided into decision-dependent probabilities (Type 1) and decision-dependent information structure (Type 2) (Hellemo et al., 2018). In this context, information structure often refers to when the realization of each uncertain event is observed, if ever. In contrast, exogenously uncertain problems have a fixed information structure with the timing of observations known a priori.

Type 2 uncertainty has been more widely addressed in the SP literature, perhaps due to one of its subclasses having a strong connection to exogenously uncertain problems. In the taxonomy presented in Hellemo et al. (2018), this specific type of endogenous uncertainty is called conditional information revelation. In this subclass, the decisions only affect the time at which the (exogenous) uncertainty is revealed to the decision maker. One of the earliest publications on such uncertainty is Jonsbråten et al. (1998), where the authors describe a branching algorithm for solving a subcontracting problem. Goel and Grossmann (2006) consider a process network problem where the yield of a new process is uncertain prior to installation. Other applications include open pit mining (Boland et al., 2008), clinical trial planning for drug development (Colvin and Maravelias, 2010) and technology project portfolio management (Solak et al., 2008).

Similar solution methods are employed in problems with exogenous uncertainty and conditionally revealed information. The main difference is that conditional information revelation requires the use of conditional non-anticipativity constraints (C-NACs), as the distinguishability is dependent on earlier decisions. This conditional dependency results in disjunctive constraints that require specific reformulation techniques (Apap and Grossmann, 2017). The main challenge arising from this approach is that the number of constraints rapidly increases with problem size, resulting in computational intractability for large problems. Apap and Grossmann (2017) also propose omitting redundant constraints, in an attempt to mitigate the tractability issues. In their example production planning problem, this results in roughly a 99% decrease in the problem size. Despite these substantial improvements, the reduced model is still very large and cannot be solved to the optimum within a reasonable computation time under their experimental setting, illustrating how challenging such problems are.

In addition to conditional information revelation, Type 2 uncertainty also encompasses problems where the information structure is altered by modifying the support of decision variables and changing the objective or constraint coefficients. Hellemo et al. (2018) report a 2SSP problem where the recourse costs depend on first stage decisions (Ntaimo et al., 2012). Gustafsson and Salo (2005) present a model for contingent portfolio programming, a project scheduling problem where projects can be expanded or terminated before they are finished. The decisions thus affect the decision spaces of future decision variables, resulting in additional consistency constraints, e.g., that a project can be continued in period only if it was ongoing in period .

Type 1 endogenous uncertainty is more challenging from a mathematical modeling standpoint because the uncertain events depend on earlier decisions, which, in turn, precludes a scenario tree-based representation as the scenario probabilities in a tree cannot depend on decisions. Therefore, the well-established solution techniques for MSSP cannot be directly applied to these problems. Despite these challenges, some discussion on Type 1 endogenous uncertainty is found in the literature. Peeta et al. (2010) discuss the fortification of a structure in a network, where the probability of failure depends on the fortification decision. Lauritzen and Nilsson (2001) present the “pig farm problem”, where the health of a pig depends on the treatment decisions, introducing the concept of limited memory influence diagrams (LIMID), thus relaxing the no-forgetting assumption in influence diagrams. The no-forgetting assumption states that when making a decision, all prior decisions and outcomes of uncertain events are known. This assumption results in significant limitations for distributed decision-making and leads to computational challenges in multi-period problems where the decisions towards the end are conditional on the full history of the problem. Dupačová (2006) presents a summary of problems with Type 1 uncertainties and Escudero et al. (2020) present solution approaches to multi-stage problems where the first-stage decisions influence the scenario probabilities in later stages. Examples of such problems can be found in Zhou et al. (2022) and Li and Liu (2023). Finally, reformulations and custom algorithms for various Type 1 problems are further summarized in Hellemo et al. (2018). However, these approaches assume specific relationships between decisions and probabilities and result in non-convex nonlinear formulations. Consequently, these approaches are not easily generalizable to different problems.

In this paper, we present a general solution framework for problems with both types of endogenous uncertainty discussed here. Modeling Type 1 endogenous uncertainty has previously relied on specific problem structures and reformulations, and the ability to model these uncertainties in a general setting makes the proposed framework versatile compared to these earlier methods. Additionally, we present two alternative approaches for incorporating Type 2 endogenous uncertainty in the decision models formulated with our framework. The ease of considering any combination of the two types of endogenous uncertainty also makes the framework more generally applicable to problems with endogenous uncertainty than the approaches discussed earlier.

3 Rooted junction trees with conditionally observed information

3.1 Influence diagrams

An influence diagram is an acyclic graph formed by nodes and arcs 111We use the subscript for and to distinguish between influence diagrams and rooted junction trees. Rooted junction trees are described in Section 3.2.. Nodes and are the sets of chance and decision nodes, respectively, and is a collection of value nodes representing the consequences incurred from the decisions made at nodes and the chance events realized at nodes . In Fig. 1, the decision nodes are represented by squares, the chance nodes by circles, and the value nodes by diamonds.

Each decision and chance node can assume a state from a discrete and finite set of states . For a decision node , represents the available choices; for a chance node , is the set of possible realizations. The arcs in represent influence between nodes. In Fig. 1, the arcs are represented by arrows between the nodes. Before defining this notion of influence further, let us first define a few necessary concepts.

The information set comprises the immediate predecessors of a given node and is defined as . In the graphical representation, this corresponds to the set of nodes that have an arrow pointing directly to node . For example, in Fig. 1, the information set of consists of and . The decision made in each decision node and the conditional probabilities of the states in each chance node depend on their information state , where . Referring back to our example, the probabilities of different outcomes in are conditional on the decision in and the random outcome in . Let us define as the realized state at a chance node . Using the notion of information states, the conditional probability of observing a given state for is .

For a decision node , let be a mapping between each information state and decision . That is, defines a local decision strategy, which represents the choice of some in , given the information . Note that we do not consider mixed strategies, where each information state would be mapped to an arbitrary probability distribution over . Instead, we only consider deterministic strategies that can be represented by an indicator function defined so that

| (1) |

A (global) decision strategy is the collection of local decision strategies in all decision nodes: , selected from the set of all possible strategies .

3.2 Rooted junction trees

As shown in Salo et al. (2022), it is possible to obtain a mixed-integer linear programming (MILP) model directly from the influence diagram representation of the problem. However, the authors observe that the model size increases exponentially with the number of nodes, resulting in computational challenges with relatively small problems. To mitigate this exponential growth, Parmentier et al. (2020) proposes first reformulating the influence diagram into a rooted junction tree (RJT) , a directed graph consisting of clusters of nodes , and arcs between these clusters, with the underlying undirected graph (obtained by replacing the directed edges with undirected edges) being a tree. The first important property of an RJT is the running intersection property, i.e., if a node is in two clusters of the tree, it is also in all clusters on the (undirected) path between these clusters. For example, in Fig. 2, the node appears in the four leftmost clusters. From this property, it follows that the subgraph of induced by a node (formed by clusters for which , and the arcs connecting such clusters) is a rooted tree.

More specifically, Parmentier et al. (2020) consider gradual RJTs, where each cluster is the root cluster of exactly one node , and the root cluster of node is denoted with . A root cluster is defined as the root of the subgraph of the RJT induced by a node . For example, the subgraph induced by consists of the four leftmost clusters in Fig. 2 and the arcs connecting them. The root of this subtree (and the full RJT) is the leftmost cluster. Finally, it is required that for all . These properties result in a convenient structure where for each pair of adjacent clusters , we have , and the joint probability distribution of all nodes in can thus always be obtained from the probability distribution of and . As will be described next, this allows the problem to be formulated as a mixed-integer programming (MIP) model, which allows for employing standard techniques widely available in off-the-shelf solvers. For more detailed description of the properties of gradual RJTs, we refer the reader to Parmentier et al. (2020) and Herrala et al. (2023).

Let us define the binary variable that takes value 1 if , and 0 otherwise, for all , , and . These variables correspond to the indicator function (1), representing local decision strategies at each decision node . Additionally, we define variables representing the joint probability distribution of nodes . The expected utility maximization problem corresponding to the gradual RJT can then be formulated as

| (2) | ||||

| s.t. | (3) | |||

| (4) | ||||

| (5) | ||||

| (6) | ||||

| (7) | ||||

| (8) |

The objective function (2) is the expected utility associated with the strategy represented by the decision variables . The first constraint states that probability distributions must sum to one, and constraint (4) enforces local consistency between adjacent clusters. Here, local consistency means that the distribution must be the same when obtained as a marginal distribution from or . Constraints (5) and (6) propagate the probability information in the junction tree. For notational brevity, we use , for which . It should be noted that while constraint (6) contains a product of two decision variables, the decision strategy variables are binary, making (6) an indicator constraint. This allows one to linearize the product using methods discussed in, e.g., Mitra et al. (1994), and the problem can be considered an instance of mixed integer linear programming (MILP).

3.3 Conditionally observed information

As originally proposed, the approaches to formulate influence diagrams as MILP models can only be applied to problems with Type 1 endogenous uncertainty, i.e., decision-dependent probabilities. However, many MSSP problems involve conditionally observed information, often also referred to as conditional information revelation.

Consider again an example of inspecting the engine of a car, where the decision maker (DM) can pay an expert to reveal information about the uncertain state of the engine before deciding whether or not to perform maintenance. A key concept with conditionally observed information is distinguishability. Suppose we represent the state of the engine as a chance node . The outcome of this node is independent of the DM’s choice to inspect the engine and is observed after inspection. If we have two different states that the engine can be observed to be, say and , from the DM’s perspective, there is no difference between and if the engine is not inspected and the state is thus not observed. In this case, such states are indistinguishable.

In conditionally observed information, the two key elements are the decisions or random events that the observation is conditional on, and the condition that the observation depends on. We refer to these as the distinguishability set and the distinguishability condition , respectively. Here, denotes the conditionally observed node, usually a chance node, and is the decision node where that information is available if the distinguishability condition is fulfilled. Note that both and must be contained in the cluster , which can be achieved by making them a part of the information set when converting the ID to an RJT.

In some cases, the conditionally observed node could also be a decision node. Such cases might arise in the context of distributed decision-making, where the decisions are made by multiple agents and observing the decision of another agent does not happen automatically, or problems in which previous decisions are not remembered by default and the decision maker must instead pay a price to retrieve information on past decisions. Distributed decision making in the context of influence diagrams is discussed in, e.g., Detwarasiti and Shachter (2005), and Piccione and Rubinstein (1997) point out that decision makers can often affect what they remember by choosing to keep track of information (including decisions) they would otherwise forget.

Using the notion of distinguishability sets and conditions, we can define conditional arcs

| (9) |

to describe conditionally observed information in influence diagrams. Specifically, we say that a conditional arc from node to node is active (i.e., node is observed when making the decision corresponding to node ) if the condition is fulfilled by the states of the nodes in the distinguishability set . If is empty, there is no conditional observation of in and, thus, no conditional arc between these nodes exists. The concept is illustrated in Fig. 3.

Using the example of inspecting a car engine before making a maintenance decision, the chance node in Fig. 3 corresponds to the state of the engine, decision node to the inspection decision, and to a maintenance decision. The information about the engine is available when making the maintenance decision only if the decision maker chooses to inspect the engine. The distinguishability set is , and the distinguishability condition is , where the indicator function is defined as

If the distinguishability set includes more than one node, alternative functions might be employed for modeling the conditional dependencies between the nodes. For example, if there are several projects that reveal the same information in node and completing any of these projects is sufficient for information revelation, can be used; or if all of the projects are required for the information revelation, is appropriate. An example of such conditions is found in Tarhan et al. (2009), where different uncertainties in oil field development are gradually revealed, and the uncertainty in the amount of recoverable oil in a reservoir can be resolved in two different ways, namely drilling a sufficient number of wells or using the reservoir for production for long enough.

3.4 Incorporating conditionally observed information in rooted junction trees

The conditional arcs are designed to describe conditionally observed information in influence diagrams. However, they are a general representation of the concept, not a modeling solution. In what follows, we present two alternative approaches for incorporating this concept into the RJT models, which ultimately enables solving Type 3 endogenously uncertain stochastic problems. The first approach employs observation nodes, used in decision analysis problems such as the used car buyer problem (Howard and Matheson, 2005) or the oil wildcatter problem (Raiffa, 1968). The second approach utilizes conditional non-anticipativity constraints, which are used in stochastic programming for modeling the decision-dependent information structure.

Observation nodes portray how the decision maker observes the information. By enforcing that earlier decisions affect the probability distribution of the observations, Type 2 uncertainty is effectively transformed into Type 1 uncertainty, making it directly amenable to an influence diagram. This approach is also used in Salo et al. (2022).

In effect, each conditional arc is replaced with an observation node, as illustrated in Fig. 4. The information set of the observation node is the union of the chance node and the distinguishability set ( in the example from Fig. 3), and the state space is . Then, the observation node replaces the node in the information set of , controlling whether or not the information in is available in . A benefit of this approach is that the modifications are done to the influence diagram, and the RJT formed from the resulting diagram can immediately be used in (2)-(8). Additionally, wrong or imperfect observations can also be modeled, e.g., if the inspector in the car engine example only provided an educated but nevertheless uncertain guess on the state of the engine.

One can also utilize the ideas of Ruszczyński (1997) and Apap and Grossmann (2017) for modeling conditional information revelation, in which the information structure can be connected to the decisions by using disjunctive constraints called conditional non-anticipativity constraints (C-NACs). These constraints are similar to the more traditional non-anticipativity constraints (Rockafellar and Wets, 1991) in stochastic programming, but the constraints are only imposed if the distinguishability conditions between the corresponding paths are satisfied.

To integrate C-NACs into our model, the conditional arcs introduced earlier need to be supplemented with the conditional information set to represent the conditionally available information at node . The C-NACs then control whether or not this information is available when making the decision in node . For the upcoming developments, we require that and . We observe that two cluster states and are always distinguishable at node if the non-conditional information states and are different. Instead, C-NACs are needed when the conditional information states differ between cluster states with the same non-conditional information state. For notational clarity, we separate the conditional and non-conditional information sets and . C-NACs are used to enforce conditional non-anticipativity when only the conditional information states differ between and , and we use this notation to emphasize the fact that C-NACs are only introduced for such pairs.

If the conditional information states differ (i.e., node has different states in and ), distinguishability is dependent on the corresponding distinguishability condition(s) . This distinguishability of two cluster states at node can be formulated as a Boolean variable , defined as

The value of is True (i.e., 1) if the conditionally revealed information makes scenarios and distinguishable at node , and False (i.e., 0) otherwise.

Finally, we extend the definition of the local decision strategy and the corresponding binary variables to include the conditional information set . If the value of is False, the local strategies and must be the same. Combining these ideas, we can define C-NACs in the context of our model as

| (10) |

In light of the above, the C-NACs for binary variables can also be conveniently written as

| (11) |

Notice that the absolute value function used in the left-hand side of (11) can be trivially linearized without significantly increasing the model complexity. This constraint states that for each decision node , if the non-conditional information states are the same for two cluster states and , and conditionally revealed information does not make these cluster states distinguishable either, the local decision strategy represented by the -variables must be the same between them.

In practice, the main challenge with using C-NACs is that the number of constraints (11) quickly becomes overwhelmingly large. With this in mind, Apap and Grossmann (2017) present a number of C-NAC reduction properties that can be exploited to decrease the number of such constraints. By making use of these C-NAC reduction properties, representing the decision-dependent information structure within the RJT model might be more compact with C-NACs than the corresponding model using observation nodes. However, C-NACs lack the ability to model Type 1 endogenous uncertainty. Observation nodes are more versatile, allowing for modeling both types of endogenous uncertainty within one observation node, making it possible to model and solve T3ESP problems. In Section 4, we present a large-scale example problem involving different endogenous uncertainties.

4 Cost-benefit analysis for climate change mitigation

4.1 Model description

To illustrate the setting, we now consider the cost-benefit analysis on mitigating climate change under uncertainty (see, e.g., Ekholm, 2018). Climate change is driven by greenhouse gas (GHG) emissions and can be mitigated by reducing these emissions, which incurs costs. However, mitigation reduces the negative impacts of climate change, referred to as climate damage. In cost-benefit analysis, the objective is to minimize the discounted sum of mitigation costs and climate damage over a long time horizon. However, multiple uncertainties complicate the analysis.

Here, we consider three salient uncertainties involving both decision-dependent probabilities (Type 1) and conditionally observed information (Type 2). Moreover, some decision nodes involve continuous variables. The resulting problem is a multi-stage mixed-integer nonlinear problem (MINLP) with Type 3 endogenous uncertainty, thus demonstrating the proposed novel features to the rooted junction tree framework described in this paper.

The considered uncertainties concern 1) the sensitivity of climate to GHG emissions, 2) the severity of climate change damages to society, and 3) the cost of reducing emissions. Decisions can be made to first conduct costly research and development (R&D) efforts towards each source of uncertainty. For the uncertainties regarding climate sensitivity and damages, a successful R&D effort results in an earlier revelation of the parametrization, whereas an unsuccessful or no R&D effort reveals this information later. Similar models of R&D pipeline optimization under (Type 2) endogenous uncertainty are considered in Colvin and Maravelias (2011).

For the mitigation costs, the model considers that technological R&D can be conducted to decrease the costs of bioenergy with carbon capture and storage (BECCS). These can take place at three intensity levels and in two distinct stages. The first stage is a choice between low or medium R&D effort. The low-effort choice represents a business-as-usual perspective, which carries throughout the decision process. If the medium effort is chosen, one observes whether the R&D looks promising or not, and can then decide whether to continue with the medium or switch to a higher R&D effort. The three R&D effort levels and whether the development seems promising or not all affect the probabilities for achieving either low, medium or high mitigation costs later during the century. For a related discussion, we refer the reader to Rathi and Zhang (2022), who consider endogenous technology learning on power generation.

The presented model is an extension from Ekholm and Baker (2022), which in turn is a simplification from the SCORE model (Ekholm, 2018). Compared to the formulation proposed here, these earlier analyses have assumed that the uncertainties are resolved exogenously over time and dealt with the mitigation cost uncertainty through separate scenarios. The details of the model structure and parametrization are described in Appendix B.

The influence diagram for the problem is presented in Fig. 5, and a corresponding RJT in Fig. 6. For converting the influence diagram into a rooted junction tree, we use the algorithm from Parmentier et al. (2020). The algorithm takes a set of nodes and their information sets, along with a topological order for the nodes and returns a gradual rooted junction tree. A topological order for a graph assigns a unique index to each node, so that for each arc , the index of node is larger than that of node .

The first stage of the diagram involves R&D decisions towards climate sensitivity (), damages () and technology (). If successful, the climate parameter (climate sensitivity and damage exponent) R&D efforts modify the information structure so that the parametrization is partially revealed in 2050 instead of 2070. This is represented by the nodes and and the outcome (success/failure) of the projects by and . Because the value nodes represent deterministic mappings , the value nodes are not explicitly represented in the RJT. Instead, the components of the expected utility can be extracted from the clusters containing , following the ideas used in the computational experiments of Parmentier et al. (2020).

Decisions over emission reductions () are made in three stages: in 2030, 2050 and 2070, which represent the medium-term and long-term climate actions. The technological R&D potentially lowers the costs of emission reductions in 2050 and 2070. We connect our example to the discussion on the feasibility of large-scale deployment of BECCS, which has been a crucial but contested result of many mitigation scenarios (Calvin et al., 2021). The R&D costs and probabilities for the three levels of BECCS costs are parametrized using expert-elicited estimates in Baker et al. (2015). These are then reflected in the overall emission reduction costs. It is worth noting the major challenges in long-term technological foresight, which is manifested in the wide spectrum of responses from the experts; but elicitation data is nevertheless useful for illustrating the importance of technological progress.

After 2070, the level of climate change is observed based on the chosen emission reductions and the observed branch of climate sensitivity, which then determines the climate damages along with the observed branch of climate damages.

4.2 Modifying the influence diagram

As discussed in Section 3, the original formulation is limited to problems with discrete and finite state spaces for all nodes. However, discretizing the emission levels would inevitably result in suboptimal solutions, thereby limiting the representability of the naturally continuous nature of the decision variables representing the emission levels.

To achieve this, we observe that the utilities in the value node(s) can be thought of as representing solutions to optimization problems. We thus modify the influence diagram and move the nodes to a subproblem whose solution becomes the utility value in the main problem, loosely following the ideas in Lee et al. (2021). The influence diagram resulting from this decomposition is presented in Fig. 7.

As a result, there is no Type 1 endogenous uncertainty in the subproblem and it can be modeled as a nonlinear three-stage stochastic programming problem with continuous decision variables. The nonlinearity comes from the SCORE model described in B. The impact of the decomposition on computational performance is discussed in Section 4.4.

4.3 Model results

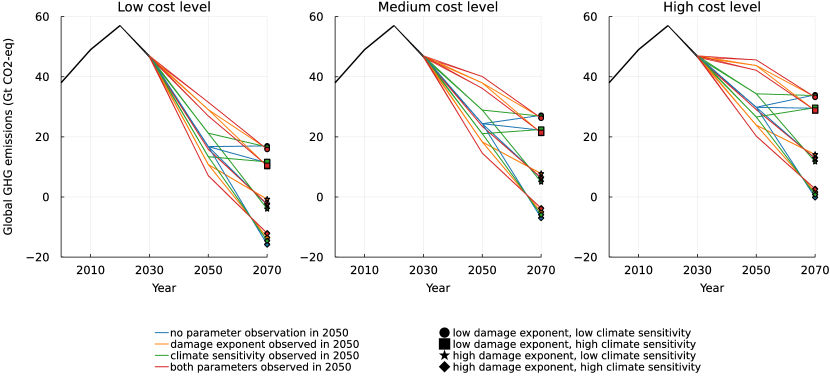

The optimal R&D strategy for this problem is to carry out all R&D projects. Fig. 8 presents the emission levels of the optimal mitigation strategy. The effect of the technology R&D on optimal emission pathways is shown with the three subfigures corresponding to the final R&D outcome after 2030. Intuitively, successful research and therefore cheaper abatement leads to more abatement. This has also a major impact on the total costs of the optimal strategy: with the low cost curves, the total expected cost is roughly 30% lower than with medium costs, and with high abatement costs 30% higher than with the medium cost curve.

The climatic parameter R&D, the other endogenous effect in this model has a magnitude smaller effect on the expected costs than the technology R&D, but the effect on abatement levels is remarkable. The branches after 2030 represent different realizations of the technology research and partial learning of the climate parameters. If the research efforts for both parameters fail (blue lines in Fig. 8), the 2050 abatement decisions are made knowing only the outcome of the technology projects, and the four scenarios of partial learning only occur after 2050. Learning the parameters before 2050 results in more dispersed abatement strategies. Finally, the underlying parameter branching is represented with shapes in 2070. It can be seen that the impact of climate sensitivity is considerably smaller than that of the damage exponent. This is in line with the results in Ekholm and Baker (2022) and shows that the proposed framework could be applied in planning for optimal R&D pathways.

4.4 Computational aspects

Using the decomposed model presented in Fig. 7, the main problem is solved in 0.4 seconds, while solving all of the subproblems takes one second. If we instead solve a problem corresponding to Fig. 5 without decomposition, the framework requires discretizing the abatement levels. Using discrete decision spaces to approximate a continuous variable leads to suboptimal solutions. Furthermore, even with only five levels for each abatement decision, the problem becomes more computationally demanding than the continuous version. The damage costs are calculated in a tenth of a second, but solving the model takes four seconds. In larger problems, the discretized problem could quickly become intractable. The decomposed problem instead uses continuous decision variables to represent the abatement decisions, precluding the need for a discretization. As a consequence, it is faster to solve than the rudimentary approximation with five abatement levels.

The discretized model has 2172 constraints and 4332 variables, of which 327 are binary; and the main problem of the decomposed model has 40 constraints and 66 variables, of which 12 are binary. The discretized model is thus two orders of magnitude larger than the decomposed model, but the damage costs in the discretized model are calculated almost instantaneously. However, the trade-off of moving some of the computational burden into the subproblems makes it possible to solve the continuous problem to optimality. The discretized model can technically also be solved to optimality, but it requires a very rough discretization of the abatement levels, which are continuous decisions by nature. Even with a low number of abatement options, the solution times are larger than those for the decomposed model. In addition, such a rough discretization is likely to result in solutions that are far from the optimal values. While discretizing the decision spaces may seem like an obvious approach, as it enables direct implementation using the MIP formulation (2)-(8), it is not computationally viable in all cases. Overall, this case study provides an illustrative example of an application where the developments in this paper make it possible to consider settings that are challenging both from modelling and computational standpoints.

5 Conclusion

In this paper, we propose a framework for Type 3 endogenously uncertain stochastic programming (T3ESP) problems. Our contributions consist of two different modelling approaches to consider conditionally observed information, making the framework more generally applicable to decision-making problems in contexts such as capacity expansion. The proposed framework is based on the work by Parmentier et al. (2020), originally developed for solving decision problems with decision-dependent uncertainties by converting an influence diagram representation of the problem to a mixed-integer programming (MIP) problem.

To the best of our knowledge, and in line with Hellemo et al. (2018), Type 3 endogenously uncertain stochastic programming (T3ESP) problems have not been previously addressed in the literature. To make RJT a framework applicable to such problems, we show how Type 2 endogenous uncertainties can be modeled by either adding observation nodes to the influence diagram or by adding conditional non-anticipativity constraints (C-NACs) to the model. We note that with minimal modifications, the developments presented in this paper can also be applied to extend the Decision Programming framework (Salo et al., 2022; Hankimaa et al., 2023).

In practice, both approaches have their advantages and disadvantages. Adding observation nodes only requires modifying the influence diagram by adding new nodes, while C-NACs are additional constraints that must be added to the decision model. On one hand, it would be beneficial to not require explicit modification of the decision model, i.e., the MIP model. On the other hand, if one allows for modifying the decision problem by using C-NACs, this might also allow for representing other parts of the decision process explicitly as added variables or constraints. Further research in this direction is thus relevant.

However, if decision-dependent probability distributions and conditional information revelation are intertwined in the problem structure, for example, by the presence of imperfect conditional observations, one cannot employ C-NAC constraints. An example of such a problem would be a version of the climate CBA problem in Section 4 where the climate parameter research does not reveal the correct branch, that is, remove one of the extreme parameter values, but instead gives a probability distribution that provides better information than the original. However, observation nodes can be applied even for such uncertainties.

Considering alternative modeling paradigms would make the framework suitable to a broader set of problems. Interesting examples of such research ideas are (distributionally) robust optimization and further examination of multi-objective decision-making. For large problems, it might be necessary to improve the computational performance using, e.g., decomposition methods for solving the MIP formulation (2)-(8), and solution heuristics. Influence diagram decomposition (e.g., Lee et al., 2021) can be used for improving the computational efficiency of finding maximum expected utility strategies for influence diagrams, and in the climate CBA problem, we demonstrate a simple influence diagram decomposition. Perhaps more interestingly, in the context of our MILP reformulations, we also show that such decomposition approaches can allow for solving decision problems with continuous decision variables, significantly improving the general applicability of the formulation.

In conclusion, the proposed developments turned the framework sufficiently general to model a challenging example problem with Type 3 endogenous uncertainty. It should also be noted that the influence diagrams are reformulated as MILP problems, guaranteeing global optimality of solutions despite the challenging nature of the underlying decision problems.

Acknowledgements

Funding: The work of Herrala and Oliveira was supported by the Research Council of Finland [Decision Programming: A Stochastic Optimization Framework for Multi-Stage Decision Problems, grant number 332180]; the work of Ekholm was supported by the Research Council of Finland [Designing robust climate strategies with Negative Emission Technologies under deep uncertainties and risk accumulation (NETS), grant number 331764].

Appendix A Computational environment

All problems are solved using an Intel E5-2680 CPU at 2.5GHz and 128GB of RAM, provided by the Aalto University School of Science Science-IT project. The problem code was implemented in Julia v1.7.3 (Bezanson et al., 2017) with the Gurobi solver v10.0.0 (Gurobi Optimization, LLC, 2022) and JuMP v1.5.0 (Dunning et al., 2017). All the code used in the computational experiments is available at a GitHub repository (Herrala, 2023).

Appendix B Cost-benefit model description

The idea in climate change cost-benefit analysis (CBA) is the minimization of emission reduction costs and climate damages. The abatement cost calculation is based on marginal abatement cost curves, as presented in equation (12), using numerical estimates from the SCORE model (Ekholm, 2018). Coefficients and are the parameters of the cost curves, is the total abatement level and is the marginal cost of abatement. In (14), is the total cost for abatement level . The subscript has been omitted for clarity, but parameters and change between stages due to assumed technological progress.

| (12) | ||||

| (13) | ||||

| (14) |

Departing from the predetermined technological progress that was assumed by Ekholm (2018), the parameter in the model depends here on the result of technological R&D, as presented in Figure 5. We consider three levels of R&D effort in 2020 and 2030, which can then lead to three possible levels of MAC curves for years 2050 and 2070.

For the effect of R&D efforts on bioenergy and carbon capture and storage (CCS) costs, we used expert elicited estimates from Baker et al. (2015). To convert these into emission reduction costs, we assume a coal power plant as a baseline and calculate the additional costs from bioenergy with carbon capture and storage (BECCS) relative to the amount of reduced emissions by switching from coal to BECCS. Both plants were assumed to have a lifetime of 30 years and operate at 80% capacity on average. The coal power plant was assumed to have a 40% efficiency and produce 885 tonnes of CO2 per GWh of electricity. The generation cost was assumed to be 50$/MWh. Costs were discounted at 5% rate.

Compared to coal, BECCS accrues additional costs per generated unit of electricity from the higher cost of biofuel and lower efficiency, and the additional investment to CCS and loss of efficiency from using some of the generated electricity in the carbon capture process. Baker et al. (2015) presented probability distributions for these parameters following three different levels of R&D efforts (low, medium and high). To calculate the cost differential to coal power plant, we performed a Monte Carlo sampling of these four parameters, separately for each R&D level, which was then compared to the amount of reduced emissions per generated unit of electricity. This yields a distribution of emission reduction costs for BECCS for each R&D level.

We generalize the impact of R&D on BECCS’s emission reduction cost to the overall marginal abatement cost (MAC) curve. This is obviously a simplification, but nevertheless reflects the major role that BECCS might have in decarbonizing the economy (e.g. Fuss et al., 2018; Rogelj et al., 2018). We take the high MAC from Ekholm (2018) as the starting point and define two MAC curves that are proportionally scaled down from the high MAC.

The low R&D level yields an average emission reduction cost of around 100 $/t. We set three bins for three cost levels: high costs correspond to above 75 $/t, medium costs are between 25 and 75 $/t, and low costs are below 25 $/t. The probabilities of achieving high, medium or low emission reduction costs are then estimated from the Monte Carlo sampling for each R&D level, and presented in Table 1. With medium and high R&D effort, the average cost in the low cost bin is around 20 $/t. Therefore we assign the reduction in the MAC as 50% for medium costs and 80% for low costs. The corresponding parameters are listed in Table 2. These are still within the range of costs used in Ekholm (2018), where the low-cost MAC yielded the same emission reductions than the high-cost MAC with approximately 90% lower costs in 2050.

| Low R&D | Medium R&D | High R&D | |

|---|---|---|---|

| High costs | 73 % | 31 % | 9 % |

| Medium costs | 27 % | 64 % | 73 % |

| Low costs | 0 % | 5 % | 18 % |

| year | ||||

|---|---|---|---|---|

| 2030 | 3.57 | 3.57 | 3.57 | 0.340 |

| 2050 | 11.2 | 13.3 | 16.7 | 0.250 |

| 2070 | 21.1 | 24.3 | 29.3 | 0.203 |

The climate damage cost calculation is from DICE (Nordhaus, 2017). The damage function is presented in (15), where is the world gross economic output at time , is a scaling parameter and is the damage exponent. While climate change and the abatement decisions have an effect on the economic output, the effect is assumed small and is defined exogenously in SCORE.

| (15) |

Finally, the temperature change is approximated with (16), where is the climate sensitivity (the temperature increase from doubling of CO2 emissions), is the sum of emissions in 2030-2070 and are coefficients.

| (16) |

In SCORE, both the DICE damage parameter and the climate sensitivity are uncertain with three options, low, medium and high, as presented in Table 3, and the uncertainty is revealed in two steps in a binomial lattice. First, between 2050 and 2070, one of the extreme alternatives is removed from both uncertainties, that is, for both parameters, we know either that the value is not high or that it is not low. Then, after 2070, we learn the actual value.

The implementation here combines influence diagrams and MSSP in a way that the underlying branching probabilities are used as the probabilities of the observations and in Fig. 5. For the damage exponent, all branching probabilities are 50%. The observation thus has a 50% probability of removing either the high or low value. Depending on the branch, the low or high value then has a 50% probability in the later branching, with the other 50% for the medium value. This makes the medium branch have a 50% probability in total, while the two extreme values both have a 25% probability. For the climate sensitivity, the first branching is with a 50% probability for both branches. However, the second branching is different. If the high sensitivity is excluded in the first branch, there is a 21% conditional probability of the low branch in the second branching, meaning a 10.5% total probability for the low sensitivity. Similarly, there is a 23% conditional probability of high damages in the other branch, resulting in a 11.5% probability for the high sensitivity. The remaining 78% is the final probability of medium sensitivity.

| Climate sensitivity | Damage exponent | |

| High | 6 | 4 |

| Medium | 3 | 2 |

| Low | 1.5 | 1 |

This uncertain process is modeled by means of a multi-stage stochastic programming problem, where new information is obtained gradually. It is possible to perform research on these parameters. If the research succeeds, one of the extreme values is excluded already before 2050, revealing the first branching in the observation process earlier than without or with failed research. The observation of the actual parameter value (the second branching) still happens after 2070, after all abatement decisions have been made. The total cost we aim to minimize is then a discounted sum of research costs, abatement costs (14) for years 2030, 2050 and 2070, and damage costs (15).

References

- Apap and Grossmann (2017) Apap, R.M., Grossmann, I.E., 2017. Models and computational strategies for multistage stochastic programming under endogenous and exogenous uncertainties. Computers & Chemical Engineering 103, 233–274. https://doi.org/10.1016/j.compchemeng.2016.11.011.

- Baker et al. (2015) Baker, E., Bosetti, V., Anadon, L.D., Henrion, M., Aleluia Reis, L., 2015. Future costs of key low-carbon energy technologies: Harmonization and aggregation of energy technology expert elicitation data. Energy Policy 80, 219–232. https://doi.org/10.1016/j.enpol.2014.10.008.

- Bezanson et al. (2017) Bezanson, J., Edelman, A., Karpinski, S., Shah, V.B., 2017. Julia: A fresh approach to numerical computing. SIAM Review 59, 65–98. https://doi.org/10.1137/141000671.

- Bielza et al. (2011) Bielza, C., Gómez, M., Shenoy, P.P., 2011. A review of representation issues and modeling challenges with influence diagrams. Omega 39, 227–241.

- Boland et al. (2008) Boland, N., Dumitrescu, I., Froyland, G., 2008. A multistage stochastic programming approach to open pit mine production scheduling with uncertain geology. Optimization online , 1–33.

- Calvin et al. (2021) Calvin, K., Cowie, A., Berndes, G., Arneth, A., Cherubini, F., Portugal-Pereira, J., Grassi, G., House, J., Johnson, F.X., Popp, A., Rounsevell, M., Slade, R., Smith, P., 2021. Bioenergy for climate change mitigation: scale and sustainability. GCB Bioenergy 13, 1346–1371. https://doi.org/10.1111/gcbb.12863.

- Colvin and Maravelias (2010) Colvin, M., Maravelias, C.T., 2010. Modeling methods and a branch and cut algorithm for pharmaceutical clinical trial planning using stochastic programming. European Journal of Operational Research 203, 205–215. https://doi.org/10.1016/j.ejor.2009.07.022.

- Colvin and Maravelias (2011) Colvin, M., Maravelias, C.T., 2011. R&d pipeline management: Task interdependencies and risk management. European Journal of Operational Research 215, 616–628. https://doi.org/10.1016/j.ejor.2011.06.023.

- Detwarasiti and Shachter (2005) Detwarasiti, A., Shachter, R.D., 2005. Influence diagrams for team decision analysis. Decision Analysis 2, 207–228.

- Dunning et al. (2017) Dunning, I., Huchette, J., Lubin, M., 2017. JuMP: A Modeling Language for Mathematical Optimization. SIAM Review 59, 295–320. https://doi.org/10.1137/15M1020575.

- Dupačová (2006) Dupačová, J., 2006. Optimization under exogenous and endogenous uncertainty, in: Proceedings of the 24th International conference on Mathematical Methods in Economics, pp. 131–136. https://doi.org/10.13140/2.1.2682.2089.

- Ekholm (2018) Ekholm, T., 2018. Climatic Cost-benefit Analysis Under Uncertainty and Learning on Climate Sensitivity and Damages. Ecological Economics 154, 99–106. https://doi.org/10.1016/j.ecolecon.2018.07.024.

- Ekholm and Baker (2022) Ekholm, T., Baker, E., 2022. Multiple Beliefs, Dominance and Dynamic Consistency. Management Science 68, 529–540. https://doi.org/10.1287/mnsc.2020.3908.

- Escudero et al. (2020) Escudero, L.F., Garín, M.A., Monge, J.F., Unzueta, A., 2020. Some matheuristic algorithms for multistage stochastic optimization models with endogenous uncertainty and risk management. European Journal of Operational Research 285, 988–1001. https://doi.org/10.1016/j.ejor.2020.02.046.

- Fuss et al. (2018) Fuss, S., Lamb, W.F., Callaghan, M.W., Hilaire, J., Creutzig, F., Amann, T., Beringer, T., De Oliveira Garcia, W., Hartmann, J., Khanna, T., Luderer, G., Nemet, G.F., Rogelj, J., Smith, P., Vicente, J.V., Wilcox, J., Del Mar Zamora Dominguez, M., Minx, J.C., 2018. Negative emissions - Part 2: Costs, potentials and side effects. Environmental Research Letters 13. https://doi.org/10.1088/1748-9326/aabf9f.

- Goel and Grossmann (2006) Goel, V., Grossmann, I.E., 2006. A Class of stochastic programs with decision dependent uncertainty. Mathematical Programming 108, 355–394. https://doi.org/10.1007/s10107-006-0715-7.

- Gurobi Optimization, LLC (2022) Gurobi Optimization, LLC, 2022. Gurobi Optimizer Reference Manual. URL: https://www.gurobi.com.

- Gustafsson and Salo (2005) Gustafsson, J., Salo, A., 2005. Contingent portfolio programming for the management of risky projects. Operations research 53, 946–956. https://doi.org/10.1287/opre.1050.0225.

- Hankimaa et al. (2023) Hankimaa, H., Herrala, O., Oliveira, F., Tollander de Balsch, J., 2023. Decisionprogramming.jl – a framework for modelling decision problems using mathematical programming. arXiv:2307.13299.

- Hellemo et al. (2018) Hellemo, L., Barton, P.I., Tomasgard, A., 2018. Decision-dependent probabilities in stochastic programs with recourse. Computational Management Science 15, 369–395. https://doi.org/10.1007/s10287-018-0330-0.

- Herrala (2023) Herrala, O., 2023. Source code repository: Type 2 RJT. URL: https://github.com/solliolli/type2-rjt.

- Herrala et al. (2023) Herrala, O., Terho, T., Oliveira, F., 2023. Risk measures in rooted junction tree models. In preparation .

- Howard and Matheson (2005) Howard, R.A., Matheson, J.E., 2005. Influence diagrams. Decision Analysis 2, 127–143. https://doi.org/10.1287/deca.1050.0020.

- Jonsbråten et al. (1998) Jonsbråten, T.W., Wets, R.J., Woodruff, D.L., 1998. A class of stochastic programs with decision dependent random elements. Annals of Operations Research 82, 83–106. https://doi.org/10.1023/A:1018943626786.

- Lauritzen and Nilsson (2001) Lauritzen, S.L., Nilsson, D., 2001. Representing and solving decision problems with limited information. Management Science 47, 1235–1251. https://doi.org/10.1287/mnsc.47.9.1235.9779.

- Lee et al. (2021) Lee, J., Marinescu, R., Dechter, R., 2021. Submodel decomposition bounds for influence diagrams, in: Proceedings of the AAAI Conference on Artificial Intelligence, pp. 12147–12157.

- Li and Liu (2023) Li, X., Liu, Q., 2023. Strategic ignorance: Managing endogenous demand in a supply chain. Omega 114, 102729. https://doi.org/10.1016/j.omega.2022.102729.

- Mitra et al. (1994) Mitra, G., Lucas, C., Moody, S., Hadjiconstantinou, E., 1994. Tools for reformulating logical forms into zero-one mixed integer programs. European Journal of Operational Research 72, 262–276.

- Nordhaus (2017) Nordhaus, W.D., 2017. Revisiting the social cost of carbon. Proceedings of the National Academy of Sciences 114, 1518–1523. https://doi.org/10.1073/pnas.1609244114.

- Ntaimo et al. (2012) Ntaimo, L., Arrubla, J.A.G., Stripling, C., Young, J., Spencer, T., 2012. A stochastic programming standard response model for wildfire initial attack planning. Canadian Journal of Forest Research 42, 987–1001. https://doi.org/10.1139/x2012-032.

- Parmentier et al. (2020) Parmentier, A., Cohen, V., Leclère, V., Obozinski, G., Salmon, J., 2020. Integer programming on the junction tree polytope for influence diagrams. INFORMS Journal on Optimization 2, 209–228.

- Peeta et al. (2010) Peeta, S., Sibel Salman, F., Gunnec, D., Viswanath, K., 2010. Pre-disaster investment decisions for strengthening a highway network. Computers and Operations Research 37, 1708–1719. https://doi.org/10.1016/j.cor.2009.12.006.

- Piccione and Rubinstein (1997) Piccione, M., Rubinstein, A., 1997. On the interpretation of decision problems with imperfect recall. Games and Economic Behavior 20, 3–24.

- Raiffa (1968) Raiffa, H., 1968. Decision analysis : introductory lectures on choices under uncertainty. Random House, New York.

- Rathi and Zhang (2022) Rathi, T., Zhang, Q., 2022. Capacity planning with uncertain endogenous technology learning. Computers & Chemical Engineering 164, 107868. https://doi.org/10.1016/j.compchemeng.2022.107868.

- Rockafellar and Wets (1991) Rockafellar, R.T., Wets, R.J.B., 1991. Scenarios and policy aggregation in optimization under uncertainty. Mathematics of operations research 16, 119–147. https://doi.org/10.1287/moor.16.1.119.

- Rogelj et al. (2018) Rogelj, J., Popp, A., Calvin, K.V., Luderer, G., Emmerling, J., Gernaat, D., Fujimori, S., Strefler, J., Hasegawa, T., Marangoni, G., Krey, V., Kriegler, E., Riahi, K., Van Vuuren, D.P., Doelman, J., Drouet, L., Edmonds, J., Fricko, O., Harmsen, M., Havlík, P., Humpenöder, F., Stehfest, E., Tavoni, M., 2018. Scenarios towards limiting global mean temperature increase below 1.5 C. Nature Climate Change 8, 325–332. https://doi.org/10.1038/s41558-018-0091-3.

- Ruszczyński (1997) Ruszczyński, A., 1997. Decomposition methods in stochastic programming. Mathematical Programming, Series B 79, 333–353. https://doi.org/10.1007/BF02614323.

- Salo et al. (2022) Salo, A., Andelmin, J., Oliveira, F., 2022. Decision programming for mixed-integer multi-stage optimization under uncertainty. European Journal of Operational Research 299, 550–565. https://doi.org/10.1016/j.ejor.2021.12.013.

- Solak et al. (2008) Solak, S., Clarke, J.P., Johnson, E., Barnes, E., 2008. A stochastic programming model with decision dependent uncertainty realizations for technology portfolio management, in: Operations Research Proceedings 2007, Springer. pp. 75–80. https://doi.org/10.1007/978-3-540-77903-2\_12.

- Tarhan et al. (2009) Tarhan, B., Grossmann, I.E., Goel, V., 2009. Stochastic programming approach for the planning of offshore oil or gas field infrastructure under decision-dependent uncertainty. Industrial and Engineering Chemistry Research 48, 3078–3097. https://doi.org/10.1021/ie8013549.

- Zhou et al. (2022) Zhou, R., Bhuiyan, T.H., Medal, H.R., Sherwin, M.D., Yang, D., 2022. A stochastic programming model with endogenous uncertainty for selecting supplier development programs to proactively mitigate supplier risk. Omega 107, 102542. https://doi.org/10.1016/j.omega.2021.102542.