Liang et al.

Online Joint Assortment-Inventory Optimization

Online Joint Assortment-Inventory Optimization under MNL Choices

Yong Liang††thanks: Authors are listed in alphabetical order. \AFFResearch Center for Contemporary Management, Key Research Institute of Humanities and Social Sciences at Universities, School of Economics and Management, Tsinghua University, 100084 Beijing, China, \EMAILliangyong@sem.tsinghua.edu.cn \AUTHORXiaojie Mao††footnotemark: \AFFDepartment of Management Science and Engineering, School of Economics and Management, Tsinghua University, 100084 Beijing, China, \EMAILmaoxj@sem.tsinghua.edu.cn \AUTHORShiyuan Wang††footnotemark: \AFFDepartment of Management Science and Engineering, School of Economics and Management, Tsinghua University, 100084 Beijing, China, \EMAILwangshiy20@mails.tsinghua.edu.cn

We study an online joint assortment-inventory optimization problem, in which we assume that the choice behavior of each customer follows the Multinomial Logit (MNL) choice model, and the attraction parameters are unknown a priori. The retailer makes periodic assortment and inventory decisions to dynamically learn from the realized demands about the attraction parameters while maximizing the expected total profit over time. In this paper, we propose a novel algorithm that can effectively balance the exploration and exploitation in the online decision-making of assortment and inventory. Our algorithm builds on a new estimator for the MNL attraction parameters, a novel approach to incentivize exploration by adaptively tuning certain known and unknown parameters, and an optimization oracle to static single-cycle assortment-inventory planning problems with given parameters. We establish a regret upper bound for our algorithm and a lower bound for the online joint assortment-inventory optimization problem, suggesting that our algorithm achieves nearly optimal regret rate, provided that the static optimization oracle is exact. Then we incorporate more practical approximate static optimization oracles into our algorithm, and bound from above the impact of static optimization errors on the regret of our algorithm. At last, we perform numerical studies to demonstrate the effectiveness of our proposed algorithm.

assortment planning, inventory management, multi-armed bandit, multinomial logit, online optimization, upper confidence bound \HISTORY

1 Introduction

In the realm of modern retail, the success of retailers hinges on their ability to optimize their product assortment and inventory levels. The assortment optimization problem involves selecting a subset of products from a pool of similar alternatives to offer to customers. Finding the optimal assortment has a significant impact on retailers’ profits, and thus it is prioritized by consultants, software providers, and retailers alike (Kok et al. 2008). Nonetheless, merely selecting the “optimal” assortment falls short of maximizing profits. In most offline and many online retail practices, managing inventory comes at a significant cost, and inventory capacity is often limited. Therefore, optimizing inventory decisions is just as vital to profit maximization as optimizing product assortment. Consequently, in order to maximize profit, the retailer must jointly optimize the assortment and inventory decisions that produce the optimal sequence of assortments. Despite its significance, the joint optimization problem of assortment and inventory is challenging, and the literature on this topic appears limited.

In order to optimize assortment and inventory decisions, retailers need to accurately model customers’ choice preferences. While existing literature typically assumes fully-specified models with known parameters, in practice, the parameters are usually unknown and need to be inferred from sales data. If a sufficiently large and high-quality dataset already exists, retailers can estimate model parameters and use them to optimize decisions. However, acquiring such data is often a challenge, particularly when retailers expand into new territories where data must be acquired from scratch to learn local customers’ preferences. Moreover, even when historical data is available, the data may not accurately reflect current customers’ preferences when new products are introduced or existing products are removed. Consequently, the “estimate-then-optimize” approach may be impractical. Instead, the retailers effectively face an online decision-making setting where they need to learn customers’ preferences on-the-fly while making decisions.

In this paper, we focus on the online optimization problem of joint assortment and inventory decisions. Specifically, we assume that customers’ choice behaviors follow the widely-used Multinomial Logit (MNL) choice model, and the attraction parameters are unknown to the retailer a priori. The retailer needs to determine a sequence of periodic assortment and inventory decisions to optimize the expected total profit over a long planning horizon, while learning the choice model parameters on-the-fly. The planning horizon is discretized into periods that correspond to inventory cycles. At the beginning of each inventory cycle, the retailer determines both the assortment and the inventory levels for the assorted products. Customers then arrive sequentially, each making a purchase decision for at most one product from the assortment set available upon arrival. At the end of each inventory cycle, unsold products are salvaged. For this online joint assortment and inventory optimization problem, the key to design an effective algorithm is to strike a balance between exploration and exploitation. That is, we need to balance the exploration of seemingly suboptimal products to collect more informative data and the exploitation of products that appear to belong to the optimal assortment according to existing data.

The focal problem studied in this paper presents significant challenges, arising from complicated product substitution behaviors due to stochastic stockout events. As previously noted, stockout events happen constantly when the initial inventory is limited, leading to the censoring of demand within an inventory cycle. Depending on different realizations of customers’ choices, the number of possible sequences of product stockout events is overwhelmingly large, so is the number of possible ways the assortment can evolve. Since the assortment directly affects each customer’s choices, the overall choice probability for a particular product across an inventory cycle can evolve in an intractable way. Consequently, even with known attraction parameters, efficiently calculating the expected demand for a product remains an open question (Aouad and Segev 2022). This is even a more grave challenge when the attraction parameters are unknown and need to be estimated from data, particularly noting that parameter estimation itself is also challenging based on data resulting from complicated choice distributions. Moreover, the stochastic stockout events also pose serious challenges to the design of exploration-exploitation algorithms. In order to balance exploration and exploitation, the retailer needs to make decisions not only according to the estimates of the expected profit of different assortment and inventory decisions, but also the uncertainty in the profit estimates. However, due to the stockout events, the expected profit and the attraction parameters generally display intricate relationships, so even when the uncertainty in the attraction parameter estimates can be characterized, propagating the uncertainty to the profit estimates is difficult. In particular, we will illustrate how this cannot be achieved by directly extending some existing upper confidence bound methods.

The main contributions of this paper are as follows. First, we propose an exploration-exploitation algorithm that addresses the aforementioned challenges. To the best of our knowledge, this is the first algorithm for the online joint assortment and inventory optimization problem under the MNL choice model with unknown attraction parameters. Specifically, the proposed algorithm offers two key contributions: a consistent estimator for the unknown attraction parameters and a novel exploration-exploitation algorithm that deliberately tunes products’ unit profits to achieve sufficient exploration, even though their true values are known. In particular, the tuning of known parameters appears an unconventional exploratory strategy, which could be useful for other complex online decision-making problems. Second, we evaluate the performance of the decisions yielded by the proposed algorithm by comparing them with the optimal decisions obtained when the attraction parameters of all products are known a priori. In particular, we adopt the widely-used relative profit gap, also known as the regret, as a performance metric. We show that our algorithm achieves nearly optimal regret rate by establishing and matching a non-asymptotic upper bound and a worst-case lower bound on the regret. Third, while the above results rely on an oracle that can exactly solve the static joint assortment and inventory optimization problem, we extend our algorithm by incorporating approximate optimization oracles. Then, we demonstrate that the resulting regret automatically adapts to the errors of the approximate oracle.

The remainder of this paper is organized as follows. Section 2 reviews the related literature. Section 3 formulates the problem. Section 4 discusses the main challenges of the online optimization problem and presents our algorithm which consists of both a novel estimation approach and a novel exploration-exploitation algorithm. Section 5 derives upper and lower regret bounds. Section 6 incorporates into the proposed algorithm approximation oracles for the static joint assortment and inventory optimization problem. At last, Section 7 performs numerical experiments to demonstrate the performance of the proposed algorithm, and Section 8 concludes this paper.

2 Literature Review

We review three lines of closely related research: assortment optimization, joint assortment and inventory optimization, and the multi-armed bandit (MAB) problem.

MNL choice model and assortment optimization. In the literature, there exist a variety of choice models describing the choice preferences of customers. The multinomial logit (MNL) model is arguably one of the most popular models due to its convenience and its superior performance in practice (Feldman et al. 2022). In particular, under an MNL choice model with known parameters, the (static) assortment optimization problem, where the retailer selects the assortment to maximize the profit from the next customer, can be solved efficiently (van Ryzin and Mahajan 1999, Talluri and van Ryzin 2004). Several studies further extend the MNL assortment optimization problem by incorporating practice-driven constraints, such as the cardinality constraint (Rusmevichientong et al. 2010) and the totally unimodular constraints (Sumida et al. 2021). Some literature builds on the MNL model to optimize assortment under complex channel structures (Dzyabura and Jagabathula 2018) or to jointly optimize assortment with other decisions such as pricing (Gao et al. 2021). In addition, more complex choice models extending from the MNL model, including the mixture-of-logits (Rusmevichientong et al. 2014) and the nested logit models (Li et al. 2015), have been proposed, leading to more complicated assortment optimization problems. It worth noting that besides parametric choice models such as the MNL model, there are also non-parametric approaches to model customer choices (Farias et al. 2013). Our study builds on the MNL choice model, but we study the joint optimization of assortment and inventory.

A current line of research focuses on online assortment optimization, where customer preferences are unknown a priori and need to be estimated from data while making the assortment decisions. Early studies often rely on strong assumptions that are not needed in our paper. For example, Caro and Gallien (2007) assume that the demands of different products are independent, while the MNL model considered in our paper captures demand substitutions among products. Other studies, such as those by Rusmevichientong et al. (2010) and Sauré and Zeevi (2013), consider the online assortment optimization under the MNL model but require prior knowledge of “separability”, which refers to a constant gap between the expected revenue of the optimal assortment and those of other alternative assortments. However, the knowledge of separability is often not available in practice.

Our study is closely related to recent works by Agrawal et al. (2017, 2019) and Chen et al. (2021b), which address online assortment optimization under the MNL choice model with cardinality constraints on the assortment set. Agrawal et al. (2017) and Agrawal et al. (2019) formulate the assortment optimization problem as a multi-armed bandit (MAB) problem and extend the classic Thompson sampling and the upper confidence bound algorithms, respectively. Chen et al. (2021b) derive a trisection search algorithm. All three algorithms achieve worst-case regret upper bounds of the same order. Chen and Wang (2018) further establish a regret lower bound that matches the upper bound up to logarithmic factors when the cardinality constraint is sufficiently tight. It is noteworthy that the online assortment optimization problem can be viewed as a special case of our problem with only one customer arrival in each inventory cycle. In particular, when specialized to this setting, the regret upper bound derived for our algorithm agrees with those of the three aforementioned algorithms.

Joint assortment and inventory planning. While the aforementioned literature focus on assortment management, in practice inventory management is also important. In particular, when the inventory is limited, stockout events can occur frequently and change the assortments available to customers accordingly. The stochastic stockout events lead to dynamic demand substitutions and significantly impact total profits (Smith and Agrawal 2000, Mahajan and van Ryzin 2001). Thus, optimizing profit requires a joint optimization of assortment and inventory. However, even the static joint assortment and inventory optimization problem can be notoriously difficult to solve (Goyal et al. 2016), where the expected profit function generally lacks desirable properties such as quasi-concavity (Mahajan and van Ryzin 2001) nor submodularity (Aouad et al. 2019). Consequently, various heuristics have been developed (see, e.g. Mahajan and van Ryzin 2001, Honhon et al. 2010, Honhon and Seshadri 2013). Alternatively, some recent literature alleviates the challenge by imposing assumptions that effectively restrict the possible sequences of stockout events (see, e.g. Goyal et al. 2016, Segev 2019).

A recent stream of literature investigates approaches to approximately solve the static joint assortment and inventory optimization problem under the MNL choice model with known parameters. Notably, Aouad et al. (2018) propose a greedy-like algorithm with a theoretical guarantee. Aouad and Segev (2022) develop a polynomial-time approximation scheme and establish the “stability” property of expected demand with respect to the MNL attraction parameters. This stability property is also used in our analyses. Liang et al. (2021) design a heuristic method based on fluid approximation and demonstrate its asymptotic optimality when the expected number of arriving customers during one inventory cycle approaches infinity. While our focus is on solving the online joint assortment and inventory optimization problem, these aforementioned approximation algorithms and heuristics can be directly used as optimization oracles in our algorithm. Details will be discussed in Section 6.

In contrast, the literature on the online joint assortment and inventory optimization problem is scarce, although there exists abundant literature on online assortment optimization problems (as reviewed above) and on online inventory optimization (e.g. Chen and Chao 2020, Gao and Zhang 2022) separately. In the online joint assortment and inventory optimization problem, we find that the estimation of choice model parameters and the balance of exploration and exploitation are both very challenging due to stochastic stock-out events (see Section 4.1 for an overview). To the best of our knowledge, our study is the first to investigate this problem under the MNL model.

Multi-armed bandit problem. Another closely related line of research is on the multi-armed bandit (MAB) problem (Lai and Robbins 1985, Auer et al. 2002), a classic problem that exemplifies the exploration–exploitation tradeoff. There has been very rich literature on MAB, and we refer to Bubeck et al. (2012), Slivkins (2019), Agrawal (2019) and Lattimore and Szepesvári (2020) for more comprehensive reviews and recent advances. MAB has been widely adopted to model the online assortment optimization problems under a variety of choice models, including the MNL model (Rusmevichientong et al. 2010, Sauré and Zeevi 2013, Agrawal et al. 2017, 2019, Chen and Wang 2018, Chen et al. 2021b), the contextual MNL model (Oh and Iyengar 2019, Chen et al. 2020), and the nested logit model (Chen et al. 2021a). Additionally, MAB has also been utilized to model online inventory management problems (Gao and Zhang 2022, Cheung et al. 2022). The most famous exploration–exploitation algorithms for the MAB problem include the upper confidence bound (UCB) algorithm (Agrawal 1995, Auer et al. 2002) and the Thompson sampling (TS) algorithm (Thompson 1933, Agrawal and Goyal 2012, 2017). In this paper, we propose an exploration–exploitation algorithm for online joint assortment and inventory optimization based on a non-trivial extension of the UCB algorithm.

A notable extension of the MAB problem is the combinatorial multi-armed bandit (CMAB) problem that involves NP-hard combinatorial optimization (e.g. Chen et al. 2013). Chen et al. (2013) assume the availability of an approximation oracle that approximately solves the combinatorial optimization, and define the regret as the expected profit of the online solutions against that of the clairvoyant approximate solutions. Our online joint assortment and inventory optimization problem is also combinatorial, and thus we also consider using approximation oracles in our exploration-exploitation algorithm. We analyze the corresponding regret that incorporates both the regret from profit estimation errors and that from optimization errors of approximation oracles. The crucial difference between our work and that of Chen et al. (2013) is that they assume the outcome of one arm is independent of that of another, while we have no such restrictive assumption.

3 Problem Formulation

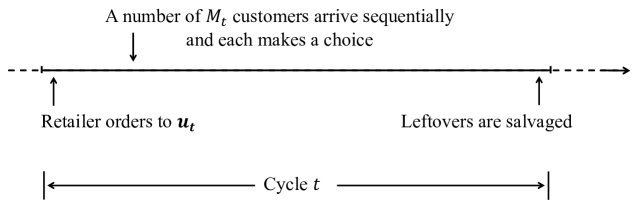

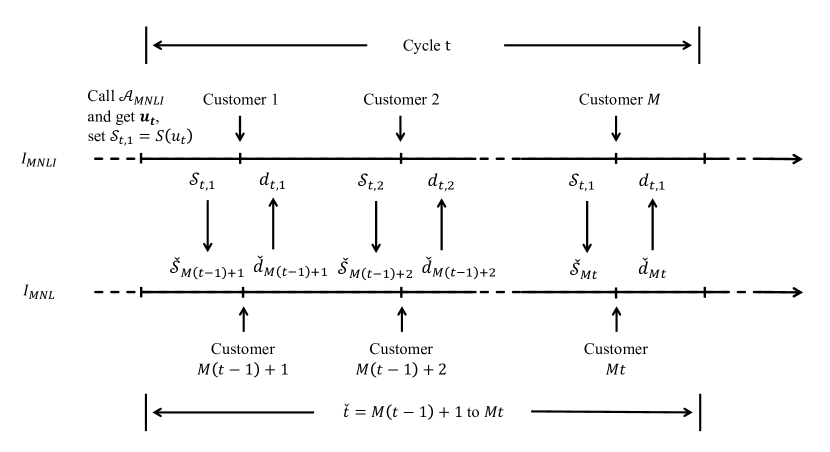

We consider a retailer making periodic joint assortment-inventory decisions for a set of substitutable products, denoted by . The attraction of each product is unknown to the retailer a priori. The objective of the retailer is to maximize the cumulative expected profit over inventory cycles, where is not known to the retailer from the very beginning. Figure 1 illustrates a sequence of events occurring in an arbitrary inventory cycle .

First, at the beginning of each cycle , the retailer determines the inventory order-up-to levels for the products, denoted by , where represents the order-up-to level of product . Note that incorporates both the inventory and assortment decisions, as a zero inventory level indicates that product is not assorted. This implies that products with non-zero inventory must be assorted. We use to denote the set of products assorted by the inventory decision , namely, . We assume zero lead-time, and thus inventory orders are received instantaneously.

Next, customers arrive sequentially and make purchasing decisions. Let denote the number of customer arrivals during cycle . The number can be either a constant or a random variable whose distribution is known to the retailer and does not change over time . Upon the arrival of customer , the assortment set available to the customer, denoted by , consists of products that were initially assorted at the beginning of cycle and have not been depleted yet. The customer either purchases one unit of product from or chooses to not purchase at all (which we refer to as the “outside” option). We capture customers’ choice behaviors by the multinomial logit (MNL) model. Specifically, the MNL model involves a vector of attraction parameters corresponding to the products, and an additional attraction parameter corresponding to the outside option (i.e., no purchase) indexed as . We assume that for all , where and are positive constants known to the retailer while ’s are unknown. Let denote the vector of choices made by customers arriving in cycle , where represents the choice of customer in cycle . Following the MNL model, the probability that customer in cycle purchases product when offered assortment is given by:

| (1) |

Without loss of generality, we normalize to . It is noteworthy that although the random choice is conditionally independent of given the event , they are unconditionally dependent. Indeed, the probability distribution of each customer’s choice depends on the available assortment, and the assortment constantly changes throughout an inventory cycle as previous customers’ choices deplete the inventory of certain products. Due to these stockout events, customers can display complicated substitution behaviors and the choices of customers in the same inventory cycle also have complicated dependence. Consequently, the joint distribution of customers’ choices is generally intractable. As we will discuss in Sections 3.1 and 4.1, this poses serious challenges to our design of algorithms.

Finally, at the end of each cycle, we assume that all unsold products are salvaged at given values. This means that the leftovers of each cycle do not constrain the ordering decisions of the next cycle. Thus if the attraction parameters were known, we could decompose the joint assortment-inventory optimization problem over cycles into disjoint single-cycle problems and solve them separately. Of course, the attraction parameters are actually unknown, so we need to estimate them and gradually refine our estimates as we collect more data over the inventory cycles. Accordingly, the decision-making in one cycle needs to be based on data accumulated in previous cycles, so the decision problems in different cycles are connected due to learning attraction parameters. This is intimately related to the exploration and exploitation trade-off in online assortment-inventory decision-making, a key challenge that we tackle in this paper (see Section 4.3). Regardless of this, the assumption of leftover salvage still significantly simplifies our problem.

We remark that the assumption that inventory leftovers are salvaged at the end of each inventory cycle is common both in the literature and in practice. For example, Bensoussan et al. (2007), Ding et al. (2002) and Lu et al. (2005) investigate learning from censored demands in the multi-cycle newsvendor setting, where it is common to assume that inventory leftovers are salvaged at the end of each inventory cycle. In practice, this assumption suits particularly well for perishable products, such as newspapers, dairy products and fresh fruits, and has evolved into a standard operation for many retailers. For example, Bianlifeng, a Chinese brand that operates a chain of more than 2,500 convenience stores, salvages unsold prepared foods and meal kits on a daily basis. Admittedly, the setting where the inventory leftovers can be carried over to subsequent inventory cycles is also important, but the corresponding online optimization problem is substantially more involved. In this setting, the decision in one cycle can impact all subsequent ones through leftovers, and dynamic programming is generally needed to solve such problems. However, even if the true attraction parameters are known, the optimization problem in our setting with salvage is difficult (see Section 3.1). The setting without salvage appears to be significantly more challenging. In this paper, we focus on the simpler but practical setting where the inventory leftovers are salvaged at the end of each cycle. This allows us to highlight the core challenge of exploration and exploitation trade-off in the online joint optimization of assortment and inventory decisions. We leave for future study the setting where inventory leftovers are carried over to subsequent cycles.

3.1 Static assortment-inventory optimization problem

Then, we describe the one-cycle optimization problem for the retailer, to which we refer as the static assortment-inventory optimization problem. Note that in this problem there still exists dynamic demand substitution triggered by stockout events, and we adopt the notion of “static” to highlight that in this problem the joint assortment-inventory decision is to be determined once to maximize the one-cycle expected profit. Dropping the subscript indexing cycle, we consider several natural cardinality and capacity constraints for the retailer’s decision . In particular, we assume that at most different products can be assorted in any inventory cycle. In addition, we consider two types of capacity constraints. The first one requires that the total inventory that can be ordered in one cycle to be no more than , and the second restricts the maximum inventory of each product to . In practice, the first type of capacity constraint may correspond to the limited transportation capacity or warehouse space, while the second one may correspond to the maximum shelf space for each separate product. Then, the set of feasible inventory decisions, , is given by

The objective of the static assortment-inventory optimization problem is to maximize the one-cycle expected profit, consisting of the expected revenue and the expected salvage values, netting the ordering costs. For the clarity of exposition, we make the following simplified assumption. {assumption} The salvage values of all products are equal to their respective ordering costs. The assumption implies that the leftovers at the end of each cycle do not contribute to any profit or cost, so the expected profit in the cycle equals the total net profit of only products sold in the cycle. We make this assumption merely for the exposition simplicity. In Appendix Section 13, we relax this assumption and show that our proposed algorithm still works once it is slightly modified.

To formulate the expected profit in a single cycle, we let denote the number of times that product is purchased in the cycle, when the initial inventory level is and the attraction parameter value is . Obviously, for any product , the number of total purchases cannot exceed the inventory level . It is noteworthy that is a random variable because customers’ choices are random and their arrival process may also be stochastic. In addition, we let be a known vector of unit profits of the products, where represents product ’s per-unit selling price netting its per-unit ordering price. Without loss of generality, we assume that . Next, given the vector of attraction parameters and the vector of unit profits , for an initial inventory level of , the one-cycle expected profit is

| (2) |

where the expectation is taken over the distribution of random variables for all . Finally, let denote an optimal solution to the static assortment-inventory optimization problem, that is,

| (3) |

In other words, maximizes the expected one-cycle profit given parameters and . The optimal solution is referred to as a clairvoyant solution, and is known as the clairvoyant optimal one-cycle expected profit, both defined in terms of the true attraction parameter . However, in the context of online optimization, the attraction parameter is not known to the retailer, so she cannot act according to clairvoyant solution in (3).

Before closing this subsection, we remark that even when the value is given, the problem of evaluating the expected profit in (2) for any given initial inventory decision is generally intractable (Aouad et al. 2018), and the optimization problem in (3) is even harder (Aouad et al. 2018, Aouad and Segev 2022). This is because the distribution of is determined by the joint distribution of customers’ choices, while the latter is generally intractable due to complicated substitution effects and customer choice’s dependence induced by stochastic stockout events (see discussions below (1)). In the remainder of this paper, we will first assume the existence of a black box oracle that can exactly solve problem (3) with any given parameters and , in order to focus on the exploration-exploitation trade-off. Given the exact optimization oracle, We propose an algorithm that can effectively balance exploration and exploitation, and analyze the performance of this algorithm. Later in Section 6, we further incorporate into our algorithm approximation oracles that can solve problem (3) up to certain error and analyze the corresponding performance guarantees.

3.2 Online joint assortment-inventory optimization problem

In the online problem setting, the attraction parameter is unknown a priori. The retailer needs to dynamically learn the attraction parameters from the realized customers’ choices in each inventory cycle and adjust the inventory decisions accordingly, aiming to maximize the expected total profit over inventory cycles. Specifically, the retailer needs to design a policy that generates the ordering decisions according to historical observations and potentially some additional sources of randomization encoded by a random variable . The policy is a vector of measurable mappings such that

Particularly, when prescribing the inventory decision for cycle , the policy can only use historical choice observations and inventory decisions prior to cycle , but not any future information. Moreover, the policy has to comply with the inventory constraints so for all . This formally defines an admissible policy. Additionally, let and denote the probability distribution and expectation value over the random decision path of policy , respectively.

The expected total profit when applying policy can be written as

| (4) |

where is the sequence of history-dependent inventory decisions generated by policy . For the clarity of exposition, we drop the superscript from when it is clear from the context. The objective of the online joint assortment-inventory optimization problem is to identify a policy that maximizes the expected total profit in (4). This is equivalent to minimizing the regret. Specifically, the regret of a policy , denoted by , measures the expected total profit loss of policy relative to the optimal policy based on known attraction parameters, that is,

| (5) |

where is the clairvoyant solution in Equation 2. However, it is generally intractable to find an optimal policy that exactly minimizes the regret. Instead, a more realistic goal is to find a policy whose regret grows with at a slow sub-linear rate (e.g., Lattimore and Szepesvári 2020, Bubeck et al. 2012). In the next section, we will propose an algorithm that can provably achieve this goal provided that an exact oracle to static optimization problems of the form in (3) is available.

4 The Online Optimization Algorithm

Since the attraction parameters are unknown, an online optimization algorithm needs to fulfill two contradictory tasks, namely, exploration and exploitation. Exploration refers to employing inventory decisions in order to collect data towards more accurate estimation of unknown parameters, even if the decision appears suboptimal given the latest estimation results. Exploitation refers to making profit-maximizing decisions according to the parameter estimates obtained from the latest data. Both exploration and exploitation can lead to suboptimal decisions and thus result in regret.

In order to achieve a small regret, we propose an exploration-exploitation algorithm based on a non-trivial extension of the legacy upper confidence bound (UCB) algorithm for multi-armed bandit (MAB) problems (Auer et al. 2002). The UCB algorithm builds on the renowned principle of “optimism in the face of uncertainty”, that is, it makes sequential decisions based on optimistic estimates of the expected rewards/profits of decisions. This optimism incentivizes exploration, and by properly adjusting the level of optimism we can effectively balance exploration and exploitation to achieve rate-optimal regret. Since UCB-based algorithms have been proven highly successful in numerous sequential decision-making applications, we adopt this strategy in our algorithm.

Although the principle of optimism is well known, implementing it in our joint assortment-inventory optimization problem turns out to be challenging. This is because customers’ choices display complicated substitution effects and intricate dependence and they are often censored, all due to stochastic product stockout events. As a result, serious challenges arise both for the estimation of unknown parameters and the balancing of exploration and exploitation. In this section, we first explain these challenges in Section 4.1. Then, we discuss the details of estimation in Section 4.2 and balancing exploration and exploitation in Sections 4.3 and 4.4.

4.1 Main Challenges

The UCB algorithm builds on a sequence of estimates of the expected profits of decisions, where the profits are functions of the unknown attraction parameters. Therefore, it is crucial to form increasingly accurate estimates of the attraction parameters. The first challenge arises from the estimation of attraction parameters in the MNL model. Because the inventory is limited, products may run out of stock over the time. Whenever stockout events occur, the assortment set available to all subsequent customers and thus their choice probabilities changes accordingly. This means that a customer’s demand can be censored, if earlier customers already deplete certain products. In turn, the customer’s choice may further change the assortment set and impact the choices of later customers. Worse yet, the assortment set depends on customers’ random choices and is thus highly unpredictable; in principle, there can be exponentially many possible assortments that an arriving customer can face in a single inventory cycle. As a result, customers’ choices display highly complicated substitution behaviors and intricate dependence, so their probability distributions are generally intractable. With such complicated choice observations, accurately estimating the attraction parameters is very challenging. In particular, standard maximum likelihood estimators do not have tractable finite-sample non-asymptotic theoretical guarantees. Although some other existing estimators in the online assortment optimization literature (see Agrawal et al. 2019) do have finite-sample guarantees, they are no longer valid in presence of product stockout events. In Section 4.2, we overcome the challenge by proposing novel consistent estimators for the reciprocals of attraction parameters (i.e., ). These estimators are based on the observation that certain summary statistics of customers’ choices have tractable distributions parameterized by the reciprocals of attraction parameters.

The second challenge is in balancing the exploration and exploitation. We adopt a UCB-based algorithm, where we need to form increasingly accurate optimistic estimates for the expected profits of different decisions to properly incentivize exploration. If there were no inventory control and only assortment decision was needed, then the expected profit could be shown to be monotone in the attraction parameters. Thus optimistic profit estimates could be easily formed by evaluating the expected profits at upper confidence bounds on the attraction parameters , as suggested by Agrawal et al. (2019). However, such a monotone relation between the expected profit and the attraction parameters is invalid in general joint assortment-inventory optimization problems, because the distributions of customers’ choices depend on the attraction parameters in a very complicated way. We show in a counterexample that a heuristic approach directly motivated from Agrawal et al. (2019) may not give sufficiently optimistic profit estimates so it can lead to very high regret due to lack of exploration (see Example 4.5 in Section 4.3). In Section 4.4, we propose a novel approach that further tunes up the products’ unit profits to incentivize stronger exploration. Importantly, we adaptively tune the unit profits according to the estimation errors of attraction parameters, so that we can effectively balance the exploration and exploitation.

At last, as explained in Section 3.1, it is also challenging to evaluate and optimize the static assortment-inventory problem (3) with any given values of attraction parameters and unit profits. For simplicity, we put aside this additional challenge for now and assume the existence of an exact oracle to solve static assortment-inventory problems. This enables us to focus on the central challenges of estimation and exploration-exploitation in online decision-making. We will relax this assumption and incorporate more practical approximate static optimization oracles in Section 6.

4.2 Estimation of MNL Model Parameters

In this section, we discuss the estimation of attraction parameters in the MNL model. As explained above, this is a very challenging task, because the assortment set can dynamically change due to stochastic stockout events. As a result, the choice probability for each product can dynamically change in an unpredictable manner, and customers’ choices can be censored by limited inventory. In this setting, existing estimators proposed in Agrawal et al. (2019) for online assortment optimization without inventory limit are not applicable. In this section, we propose a novel method to consistently estimate the attraction parameters based on certain summary statistics carefully constructed from the choice observations. The main idea of our estimation method is to repeatedly offer the same inventory decision in every inventory cycle, until every assorted product has been purchased at least once. Then, the number of no-purchases before each assorted product’s first purchase is a useful summary statistic for the attraction parameter of that product.

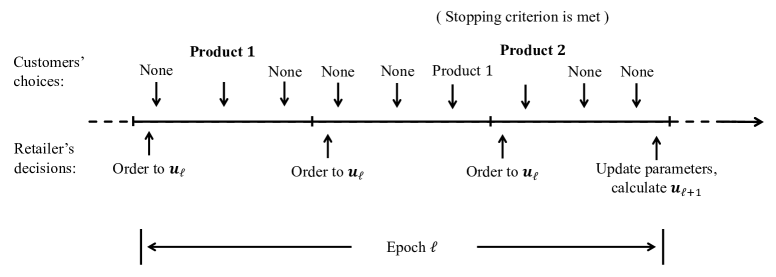

Formally, we group the whole inventory cycles into different epochs consisting of consecutive cycles. For an epoch , we offer the same inventory levels at the beginning of every inventory cycle within epoch , and end the epoch when every product assorted in (i.e., every product in ) has been purchased at least once. We denote the set of inventory cycles in epoch by and its cardinality by . Obviously, is a random variable since it depends on customers’ arrivals and their random choices. Next, we count the number of no-purchases for each assorted product from the beginning of epoch to the first time that product is purchased. Then, we use the summary statistics to update the estimates of the attraction parameters as we will describe shortly. With the new parameter estimates, we decide on a new inventory level that we will offer throughout epoch . We repeat this process until the end of the decision horizon. The total number of epochs is given by the smallest positive integer such that . The number of epochs is also a random variable and its value may range from to .

Example 4.1

We illustrate the epoch structure in an example with products. Figure 2 plots an epoch consisting of consecutive inventory cycles. In epoch , the retailer orders to the inventory level at the beginning of each cycle. Since the first two products are assorted (i.e., ), epoch ends only after both products are purchased at least once. At the end of epoch , we count the number of no-purchases (marked as “None” in Figure 2) in epoch up to the first purchases of products and respectively, and obtain and . These data are then used to update the parameter estimates before proceeding to the next epoch.

To motivate our estimator, we first establish the distributions of the summary statistics .

Lemma 4.2

Consider an arbitrary product . For all epochs in which product is assorted, the random variables ’s are i.i.d. and geometrically distributed with parameter :

| (6) |

Accordingly, the expectation of is given by

| (7) |

In Lemma 4.2, we prove that the summary statistic for each product follows a geometric distribution, and its expectation is given by the reciprocal of the corresponding attraction parameter . This expectation is well-defined within the range between and . Intuitively, reflects the attraction of the no-purchase option relative to the assorted product , so not surprisingly its expectation is given by the ratio of the attraction over . Importantly, this ratio is independent of the assortment set, so the distribution of the summary statistic remains fixed and simple even with a dynamically changing assortment set. By leveraging the summary statistics, we sidestep the complication brought by stochastic stockout events.

Motivated by Lemma 4.2, we propose to estimate the reciprocal attraction of each product by aggregating all summary statistics available for that product. Formally, for each product and epoch , we consider the subset of all epochs up to in which product is assorted, namely, . According to Equation 7, the summary statistic for any provides an unbiased observation for . Thus we average all of them to obtain the following estimator for :

| (8) |

Accordingly, we can estimate the attraction parameter by . In the lemma below, we bound the estimation error of the proposed estimator.

Lemma 4.3

For any epoch and product , if , then we have

| (9) |

Lemma 4.3 establishes that is a consistent estimator for the reciprocal attraction parameter , as the estimation error of vanishes to zero when grows indefinitely. The error bound in Equation 9 also quantifies the uncertainty of the estimator, which will be useful in designing our exploration-exploitation algorithm (see Section 4.3 Lemma 4.4). Based on Lemma 4.3, we can also establish the consistency and error bound of the attraction parameter estimator . Note that for the error bound in Lemma 4.3 to hold for a product , we need product to be assorted in sufficiently many epochs so that . We refer to this condition as the adequate exploration condition. In our algorithm, we will force exploring products that fail to satisfy the condition, so that the errors of our proposed estimators are always well controlled. We will show that the forced exploration has a negligible cost and does not change the overall regret rate.

Lemma 4.3 shows that our proposed estimator is valid despite the ever-changing assortment set due to stockout events. This is possible because the distributions of our summary statistics ’s are free of the complication caused by stockout events. We note that Agrawal et al. (2019) estimate MNL attraction parameters by some alternative summary statistics for an online assortment optimization problem. Their strategy also has an epoch structure: they repeatedly offer the same assortment to customers in an epoch, and end the epoch as soon as a no-purchase choice occurs. Then the summary statistic for each product in an epoch is the number of purchases of that product within the epoch, and it is shown to be an unbiased observation for the corresponding attraction parameter. Crucially, this unbiasedness holds because there is no inventory limit in their setting and the assortment set is fixed in each epoch. However, in our setting with limited inventory, the assortment set is not under control; instead, it can change stochastically due to stockout events. In particular, customers’ demands for the products can be censored by the limited inventory. If some products are out of stock before the first no-purchase occurs, then their purchases cannot faithfully capture customers’ true demands. As a result, the estimator in Agrawal et al. (2019) is not effective in our problem setting, which we confirm numerically in Appendix Section 14. In contrast, our summary statistics ’s count no-purchases so they are never censored by the inventory.

Finally, we remark that our proposed estimator is based on the information only up to the first purchases of the products in each epoch, even if some products are purchased multiple times in the epoch. Thus our estimator does not use all data information. Fortunately, we will show the algorithm based on our estimator achieves a nearly optimal regret rate, so not using all data information in estimation has negligible cost at least for a very large time horizon . Designing more efficient parameter estimators is an interesting problem that we leave for future study.

4.3 The Failures of Directly Extending the UCB Algorithm

In this subsection, we outline the main idea of balancing exploration and exploitation in our problem by a direct extension of the UCB algorithm for MAB problems (Auer et al. 2002). We will show that this extension, although intuitively simple, is in general computationally intractable. In particular, it cannot be remedied by an appealing heuristic approach motivated from the existing literature, since we show in a counterexample that this heuristic cannot incentivize sufficient exploration. This counterexample provides valuable insights that motivate our novel algorithm in the next subsection.

To extend the UCB algorithm to our problem, we make inventory decisions according to certain optimistic estimates for the expected profits of all possible decisions. That is, we construct high-confidence upper bounds on the true expected profits for all feasible inventory levels from the data available in each epoch, and then choose the inventory level that achieves the largest upper confidence bound. The optimistic estimates given by the upper bounds incentivize us to explore inventory decisions whose expected profits are highly uncertain. Moreover, the optimistic estimates should gradually approach the true expected profits as more data are collected, so that we can also exploit the knowledge revealed by rich data observations.

Before forming UCBs on the expected profits, we first note that we can form high probability confidence bounds on the unknown attraction parameters using the proposed estimators ’s in Equation 8. Specifically, define the following confidence bounds on the parameter based on data collected in the first epochs:

| (10) |

where is the confidence radius given by

The reciprocals of the confidence bounds in Equation 10 give confidence bounds for :

| (11) |

Note that the confidence radius is nearly identical to the vanishing error bound in Lemma 4.3, except that only involves observable quantities. The confidence radius also vanishes to zero as the data size grows indefinitely, so the confidence bounds above tightly concentrate around the true parameter values when a large amount of data are available. By slightly revising Lemma 4.3, we can show that the confidence bounds proposed above have high coverage probabilities.

Lemma 4.4

For any epoch and product , if , then we have

With the confidence bounds above, a direct extension of the UCB algorithm would pick the inventory level as follows:

| (12) |

Apparently, Lemma 4.4 implies that upper bounds the true expected profit for all inventory levels with high probability. Moreover, the upper bound gradually approaches the corresponding true expected profit as the data size grows to infinity, since in the limit the confidence bounds ’s all converge to the true values of the attraction parameters. So we can expect the decision to converge to the clairvoyant optimal decision in (3) as grows. Thus Equation 12 would give a reasonable UCB algorithm if we could implement it in practice.

Unfortunately, the optimization problem in (12) is generally intractable except in extreme cases. This is because the expected profit , as a function of the value of attraction parameters, is generally highly complex, so maximizing it over the values of the attraction parameters within the confidence bounds is very difficult. This is a particularly grave challenge noting that the evaluation and optimization of at even a single value is already very difficult (Aouad et al. 2018, Aouad and Segev 2022). Because of this computational intractability, directly following Equation 12 is not practical for general online assortment-inventory decision-making.

A special case where Equation 12 can be efficiently solved is when only a single customer arrives in each inventory cycle (i.e., ). In this special case, the inventory limit is vacuous, and our online joint assortment-inventory optimization problem degenerates to the MNL-bandit problem in Agrawal et al. (2019). The profit function in this special setting is monotonically increasing in (Lemma A.3 in Agrawal et al. (2019)), so , where is the upper confidence bound on . The latter optimization problem under is also polynomial-time solvable. This constitutes a key step of the MNL-bandit algorithm in Agrawal et al. (2019).

One may wonder if we can implement the same idea as a heuristic approach for more general settings. That is, even when ’s take general deterministic or stochastic values, we still implement

| (13) |

This corresponds to a static assortment-inventory optimization problem (3) with parameters and , for which we assume the existence of optimization oracles. However, this heuristic approach actually does not work, because the expected profit function is in general not monotone in , so may not be a valid profit upper bound to incentivize enough exploration. Below we show the failure of this heuristic approach in a simple counterexample.

Example 4.5

Consider a small-scale instance of the online optimization problem, where the number of products is 2, the product-wise capacity vector is , the total capacity is 2, and the numbers of customer arrivals are all equal to 2. Suppose that the attraction parameters of the no-purchase option and product are , and the unit profit of product is . The attraction parameter and the unit profit of product are left undetermined.

There are four feasible inventory decisions: , , , and , where is trivially sub-optimal and can be shown to be dominated by . In Section 10, we show that there exist a range of values of and such that , i.e., the inventory decision that assorts both products is optimal. However, if the initial upper confidence bound on the attraction parameters are high enough, as they would be due to the lack of data at the beginning, then we will have . This means the heuristic approach in (13) starts with implementing the inventory decision . Since this decision does not assort product 2, the upper confidence bound of cannot be updated. Consequently, the algorithm will persistently select throughout, resulting in linear total regret in the long run. In Section 10, we provide all calculation details and also show that the dependence of on is not monotonic.

As shown in Example 4.5, the heuristic approach in (13) may not incentivize sufficient exploration and thus miss the optimal decision altogether, despite that it significantly eases the computational burden of the exact approach in (12). In the next subsection, we propose a novel algorithm that modifies the heuristic approach, so that we can effectively balance exploration and exploitation while still maintaining the same level of computational costs.

4.4 Proposed Exploration-Exploitation Algorithm

Recall that a direct extension of the UCB algorithm shall implement the optimistic inventory decision prescribed by (12). However, the optimization problem is intractable to solve. The heuristic approach in (13), although computationally easier, cannot incentivize sufficient exploration. This is because the heuristic objective function is generally not an upper bound on the unknown true profit and thus fails to provide valid optimistic profit estimates. In this subsection, we propose a novel algorithm that further adjusts the heuristic objective function. The resulting new objective can provide desirable optimistic profit estimates, thereby enabling us to effectively balance the exploration and exploitation.

In our proposed algorithm, we consider not only the upper confidence bound on the unknown attraction parameters , but also an upper bound on the known unit profits in each epoch . Specifically, we define as an -dimensional vector with its element given by

| (14) |

That is, each tunes up the corresponding unit profit by an amount determined by the relative magnitude of the confidence radius . By tuning up the unit profits, we can unambiguously bring in more optimism, since the expected profit increases linearly with the unit profits (see Equation 2). Importantly, we tune up the profits judiciously according to the confidence radius , so that we encourage more optimism for under-explored products whose attraction parameters have higher uncertainty. Below we show that this additional profit tuning can indeed remedy the heuristic objective function in Equation 13.

Lemma 4.6

For any epoch , if and , satisfy that for all , then for all feasible inventory decisions .

Lemma 4.6 shows that the expected profit , when evaluated at both the parameter upper bound and the unit profit upper bound , provides an upper bound on the true expected profit. Moreover, this upper bound is expected to be increasingly tight as grows, since both and converge to the truth and respectively. So can provide valid optimistic estimates that meet all desiderata to make a valid UCB algorithm. Therefore, we propose to make inventory decisions by solving the following optimization problem for each epoch :

| (15) |

Just like the heuristic approach in (13), our proposal above also corresponds to a static assortment-inventory optimization problem (3) for which we assume solution oracles. But unlike the heuristic approach, our proposal additionally tunes up the unit profits to balance the exploration and exploitation. We will rigorously prove that our proposal can achieve a nearly optimal regret rate in the next section. In this section, we only briefly validate the effectiveness of our algorithm in Example 4.5, the counterexample we previously used to demonstrate the heuristic approach’s failure.

Example 4.5, Cont’d. In Example 4.5, the heuristic approach only uses the attraction parameters’ upper confidence bounds in its objective function. This approach may end up with only choosing the sub-optimal inventory decision and never exploring the second product. Now with our novel algorithm, in the first epoch we additionally tune up to . We can show that even if is very high, so our proposed algorithm implements the decision and successfully explores both products in the first epoch. After collecting the data in the first epoch, our algorithm updates the upper bounds on attraction parameters and unit profits, and continue to explore decisions with high uncertainty in all subsequent epochs.

The effectiveness of our algorithm crucially rests on the conclusion in Lemma 4.6. We now outline the proof of Lemma 4.6 to provide a deeper understanding of our proposed algorithm. Define and as maps from any vector to and respectively, with their -th components given by

| (16) |

We can consider the expected profit parameterized by any vector . In particular, our proposed objective function in (15) is a special example given by the all-one vector . In fact, it is the maximum of over , since we can show that the expected profit is monotone in .

Lemma 4.7

Let and be two vectors in such that . Then for any inventory decision and any epoch , we have .

Lemma 4.7 asserts that, although is not necessarily monotone in with a fixed , is monotone in as and simultaneously vary with . The main idea of the proof of Lemma 4.7 is to demonstrate that any possible decrement of due to an increase in can be compensated by an appropriate increase in as described in (16). Given Lemma 4.7, we can reformulate our proposal in (15) as follows:

| (17) |

It is now easy to explain why Lemma 4.6 is true. Given that for all , there exists a vector such that . Then the conclusion of Lemma 4.6 follows from

Here the leftmost inequality holds because . The rightmost inequality follows from the fact that linearly increases with and . In summary, Lemma 4.6 follows from the monotonicity of as and vary along the path specified in Equation 16.

We remark that our proposal of tuning known parameters (i.e., the unit profits) appears an unconventional exploratory strategy, as existing online decision-making literature typically tunes values of unknown parameters for exploration (e.g., Lattimore and Szepesvári 2020). Our proposal presents a novel way to incentivize exploration, which we believe can be useful in other online decision-making problems, especially when the dependence of the objective function on unknown parameters is complex but its dependence on known parameters is fairly simple.

Summary of the proposed algorithm.

We finally summarize our proposed exploration-exploitation algorithm for the online joint assortment-inventory optimization problem in Algorithm 1. This algorithm puts together the estimators in (8), the parameter confidence bounds in (10)(11), and the decision rule in (15). Moreover, Lemma 4.4 shows that our confidence bounds rest on the adequate exploration condition , so we introduce additional exploration to meet this condition in Algorithm 1 line 1. Specifically, for any epoch where the adequate exploration condition fails for some products, that is, for any exploratory epoch in the set

| (18) |

we choose an inventory decision consisting of only inadequately explored products. In Appendix Section 11, we further provide a step-by-step explanation to Algorithm 1.

5 Regret Analysis

In this section, we analyze the total regret of our proposed exploration-exploitation algorithm and establish its rate-optimality. This section is organized as follows. In Section 5.1, we introduce a class of customer arrival processes under which our analyses of regret bounds hold. Next, in Section 5.2, we present a non-asymptotic upper bound on the regret of Algorithm 1. At last in Section 5.3, we derive a matching regret lower bound and discuss the optimality of Algorithm 1.

5.1 Customer arrivals

In previous sections, we leave the customer arrival process unspecified and only assume the number of customers arrivals per cycle have known and stationary distributions. Since the decision regret depends on the distribution of customer arrivals, we need to impose some regularity conditions on the customer arrivals before we can analyze the regret of our proposed algorithm. Specifically, define filtration generated by customers’ purchase process, such that captures the entire information history up to the end of inventory cycle . We require the customer arrival process to satisfy the following assumption.

The sequence of the number of customer arrivals per inventory cycle, denoted by for , are independent and identically distributed (i.i.d) and is independent of . Moreover, they satisfy the “-Sub-Poisson” condition, that is, the moment generating function of for any satisfies

| (19) |

Section 5.1 formalizes the distribution stationarity of the number of customer arrival and excludes serial dependence of as well as the dependence between and , which encapsulates retailer’s past decisions and customers’ past choice behaviors up to the beginning of inventory cycle . Section 5.1 further restricts the tail distribution of the number of customer arrivals ’s by a “Sub-Poisson” condition. Under this condition, the distribution tail of each needs to decay at least at fast as the tail of a Poisson distribution, since the upper bound in (19) corresponds to the moment generating function of a Poisson distribution with parameter . This condition is satisfied by a range of arrival processes. For example, if customer arrivals follow a Poisson process, then ’s have Poisson distributions so they are obviously Sub-Poisson. For an arrival process where ’s are all equal to a deterministic constant , the Sub-Poisson condition holds trivially. More generally, if ’s are i.i.d -Sub-Gaussian random variables with expected value , then the Sub-Poisson condition also holds (see Chapter 2.3, Vershynin 2018).

Section 5.1 is useful in bounding the regret of our proposed algorithm in multiple ways. First of all, the regret incurred in a single inventory cycle is upper bounded by , the expected number of customer arrivals per cycle. That is, for any feasible decision , we have

| (20) |

where the first inequality trivially holds and the second inequality holds because one customer purchases at most one product and generates at most one unit of profit (recall that ) while on average customers arrive in each inventory cycle.

Moreover, Section 5.1 can be used to upper bound the expected number of cycles within an epoch in our proposed algorithm. Recall that in our algorithm, an epoch ends only after every assorted product has been purchased at least once. Clearly, the number of cycles in epoch , denoted by , is random and can take values ranging from 1 to infinity, due to the stochastic arrival process, the MNL-choice behaviors, and the stochastic stockout events. Nevertheless, the expected value of can be upper bounded under Section 5.1, using the expected number of customer arrivals and the maximum assortment size .

Lemma 5.1

If the customer arrivals satisfy Section 5.1, then there exists a constant such that the expected number of cycles in any epoch satisfies

| (21) |

Lemma 5.1 shows that the expected value of the epoch length decreases with the expected number of single-cycle customer arrival but increases with the maximum assortment size . That is, if on average more customers arrive in each cycle (i.e., higher ) and fewer products are allowed to be assorted (i.e., lower ), then on expectation it takes fewer inventory cycles for all assorted products to be chosen by at least one customer. Moreover, the maximum assortment size , except in trivial cases, is typically constrained by both the total number of products and the total inventory capacity , namely, . Consequently, the upper bound in Lemma 5.1 is often not excessively large in many real-world applications. For instance, consider a brick-and-mortar store where there are typically dozens of substitutable products in a specific product category. Since the number of daily customer arrivals can range from hundreds to thousands, the expected number of cycles in each epoch can be well bounded.

At last, our algorithm involves some exploratory epochs designed to accelerate the exploration of under-explored products (see Equation 18). Below we show that under Section 5.1, the total length of the exploratory epochs scales only logarithmically in the total horizon , so the exploration in the exploratory epochs incurs only limited costs.

Lemma 5.2

If customers arrivals satisfy Section 5.1, then there exists a constant such that the expected total number of cycles in exploratory epochs satisfies

In the next subsection, we will leverage Equation 20 and Lemmas 5.1 and 5.2 to bound the total regret of Algorithm 1.

5.2 Regret Upper Bound

In this subsection, we derive an upper bound on the total regret of Algorithm 1 and outline its proof. Let denote the policy given by Algorithm 1, and let denote the total regret of implementing policy as defined in Equation 5. Our main result is the following upper bound on the total regret of our proposed algorithm.

Theorem 5.3

For any instance of the online joint assortment-inventory optimization problem with products, attraction parameters , unit profits , maximum assortment cardinality of , and a customer arrival process satisfying Section 5.1 with parameter , the total regret of the policy generated by Algorithm 1 over inventory cycles satisfies

According to Theorem 5.3, the order of the dependence of regret on and is . Moreover, when or and are of the same order of magnitude, the dependence of the regret bound on is approximately . Next, we outline the proof of Theorem 5.3.

Proof outline.

To derive the regret upper bound in Theorem 5.3, we decompose the total regret into three parts according to whether certain events happen, and then upper bound each of the three parts separately. We first define the events used in the regret decomposition.

Definition 5.4

For all , define the event as

Moreover, define as the complementary event of .

In Definition 5.4, the event corresponds to the event that the true value of the parameter lies in the confidence interval and the width of that interval is bounded above by a vanishing term, for any product . Then, by the reciprocal relationship between and , we also have that , and that is bounded above by a vanishing term given the event . Note that the former is the sufficient condition in Lemma 4.6 for our proposed objective to provide valid optimistic profit estimates, and the latter is useful in showing that the optimistic estimates are increasingly accurate (see Lemma 5.6 below). Thus the events for define a sequence of desirable events for our proposed algorithm. We now show that these desirable events hold with high probability, provided that the adequate exploration condition holds for all products (i.e., ).

Lemma 5.5

For any epoch , event happens with a probability of at least , that is, .

Then we decompose the total regret into three separate parts as follows:

| (22) |

where the second equality follows from re-writing the summation from over cycles to over epochs, and the third equality from decomposing the regret according to whether it is incurred in exploratory or non-exploratory epochs, and, if in non-exploratory epochs, whether the corresponding desirable event happens. Next, we explain the three parts of Equation 22 in more detail, and sketch how to upper bound each of them.

(i) Upper bounding .

This term is the expected total regret of the exploratory epochs . According to Equation 20, the single-cycle regret can be upper bounded by the expected number of single-cycle customer arrivals . Therefore,

Moreover, Lemma 5.2 shows that the expected total length of exploratory epochs is at most logarithmic in . Thus the first part of Equation 22 is also at most logarithmic in .

(ii) Upper bounding .

This term captures the expected total regret incurred in non-exploratory epochs , in which the desirable event does not hold. Again, the single-cycle regret is bounded by , so

According to Lemma 5.1, the expected length of each non-exploratory epoch can be bounded by . This result, in conjunction with Lemma 5.5 that bounds the probability of for by , leads to the conclusion that the second part of Equation 22 is also at most logarithmic in .

(iii) Upper bounding .

This term calculates the expected total regret of all non-exploratory epochs where the desirable event holds. This is also the dominant term in the total expected regret. According to Lemma 5.5, the event happens with high probability, thus in order to obtain a tight regret upper bound, we need to carefully bound the single-cycle regret given that is true. We note that for all epochs where the desirable event holds, we have

| (23) |

where the first inequality holds because according to Lemma 4.6, and the second inequality holds because is chosen to maximize over . As a result, we can bound the single-cycle regret by the estimation error of the optimistic expected profit at the chosen decision . It then remains to bound this estimation error.

Lemma 5.6

For every , if the event is true, then there exists a constant such that

Lemma 5.6 asserts that the single-cycle regret can be bounded by an increasingly tight upper bound when is true. We can then sum up these upper bounds across all to get an upper bound on the third part of Equation 22. To establish Lemma 5.6, we leverage some structural properties of the MNL choice model to show that the expected profit function is Lipschitz in the parameter vectors and . This means that the profit estimation error can be upper bounded by the size of the parameter estimation errors and . Then Lemma 5.6 results from upper bounds on the parameter estimation errors implied by the desirable events ’s.

Finally, by putting together the upper bounds described above for the three parts of (22), we can reach the regret upper bound in Theorem 5.3. The detailed proof is provided in Appendix LABEL:app-proof-thm1.

5.3 Regret Lower Bound

In this section, we show that any admissible policy for the online joint assortment-inventory optimization problem must incur a worst-case regret of , which implies that our proposed Algorithm 1 achieves nearly optimal regret rate.

Theorem 5.7

For any admissible policy , there exists an instance of online joint assortment-inventory optimization problem with products, inventory cycles satisfying , maximum assortment size , and a customer arrival process satisfying Section 5.1 with parameter , such that the total regret of the policy on this instance satisfies

Theorem 5.7 shows that our proposed Algorithm 1 achieves nearly optimal regret rate. According to Theorem 5.7, when the maximum assortment size is small enough compared to the total number of products so that , no policy can achieve regret rate better than uniformly over all instances. This regret rate is nearly achieved by our proposed Algorithm 1, only up to an additional factor and a logarithmic factor (see Theorem 5.3). In particular, the factor may be fairly close to if the expected number of single-cycle customer arrivals is much larger than the maximum assortment size , as is common in real-world applications. Thus our proposed algorithm achieves a nearly optimal regret rate when and . In contrast, when , the regret upper bound in Theorem 5.3 involves an extra factor compared to the lower bound in Theorem 5.7. We note that a similar phenomenon also appears in Agrawal et al. (2019), as the regret upper bound for their online assortment optimization algorithm also involves an extra factor relative to their regret lower bound. How to eliminate this extra factor, either by more refined regret analysis or better algorithms, is still an open question even for the simpler online assortment optimization problem.

Furthermore, we can compare our regret bounds with the regret bounds in Agrawal et al. (2019), Chen and Wang (2018) for the MNL-bandit problem of online assortment optimization. The MNL-bandit problem can be viewed as a special case of our problem with deterministic all equal to . When specialized to this setting, our regret upper bound in Theorem 5.3 has nearly the same rate with respect to as the dominating term in the regret upper bound for the MNL bandit algorithm in Agrawal et al. (2019), despite worse dependence on . Our lower bound in Theorem 5.7 specialized to recovers the lower bounds in Agrawal et al. (2019), Chen and Wang (2018), since the proof of Theorem 5.7 directly builds on their lower bounds, as we will explain shortly. However, our novel algorithm and regret analysis can handle more general and various challenges caused by stochastic stockout events under limited inventory, thereby advancing the existing literature.

Finally, we briefly sketch the proof for the lower bound in Theorem 5.7. The proof is based on constructing a reduction of the MNL-bandit problem for assortment optimization to our problem. In particular, it suffices to focus on problem instances with deterministic as they trivially satisfy Section 5.1. For , our problem is equivalent to the MNL-bandit problem, so Theorem 5.7 directly follows from Chen and Wang (2018) when and from Agrawal et al. (2019) when . For , we show that for any MNL-bandit problem instance with customer arrivals, we can construct an online assortment-inventory optimization problem instance with inventory cycles and customer arrivals per cycle, such that any admissible policy on instance induces an admissible policy on instance with identical total regret. Then we can again obtain Theorem 5.7 from the corresponding MNL-bandit lower bounds in Chen and Wang (2018), Agrawal et al. (2019). This proof provides a convenient template to translate lower bounds for the MNL-bandit problem to lower bounds for the online joint assortment-inventory optimization problem. Therefore, whenever tighter lower bounds for the MNL-bandit problem are discovered in the future, they can be readily adapted to our problem in the same way. See Appendix Section 12 for more details.

6 Incorporating Approximate Static Optimization Oracles

In previous sections, we assume the existence of an exact oracle to solve static joint assortment-inventory optimization problems. This simplified assumption allows us to ignore errors in solving static optimization problems, so that we can focus on the central challenge of exploration-exploitation trade-off in online decision-making. In this section, we relax this assumption by incorporating approximate static optimization oracles into our algorithm.

Specifically, recall that at the beginning of each epoch , our algorithm needs to solve

Previously, we assume these optimization problems can be solved exactly by an oracle. However, to the best of our knowledge, at present there is no such efficient exact oracle. Indeed, even efficiently evaluating the expected profit of given assortment and inventory decisions is notoriously difficult, let alone solving for the profit-maximizing decision (Aouad and Segev 2022, Aouad et al. 2018). Fortunately, although exact oracles do not exist, there exist a variety of approximation algorithms or heuristics that can serve as approximate oracles. For instance, Liang et al. (2021) propose a linear programming approach that is asymptotically optimal when customer arrivals follow a Poisson process and the expected number of customers is large. In particular, the suboptimality gap of their approach in terms of expected profit can be bounded by . Aouad et al. (2018) propose a greedy-like algorithm consisting of a combination of greedy procedures for a big class of customer arrival processes. Their algorithm achieves a -approximation with probability at least , for any and . Aouad and Segev (2022) devise a polynomial-time approximation scheme (PTAS) for arbitrarily distributed customer arrivals, such that for any and , their polynomial-time approximation algorithm achieves a -approximation with a probability of at least .

Based on the examples above, we formalize - oracles to the static joint assortment-inventory optimization problem. The aforementioned approximation algorithms or heuristics are all examples of - oracles with appropriate error parameters and .

Definition 6.1

An oracle to the static joint assortment-inventory optimization problem is called an - oracle if for any instance with any known value of parameters and , the oracle can obtain a decision such that with a probability of at least .

We can easily incorporate an - oracle into our Algorithm 1. Specifically, we apply the oracle to obtain an approximate solution for every epoch , such that with a probability of at least ,

Then we can extend Equation 23 and upper bound the single-cycle regret of the approximate solution in epoch , in terms of both the profit estimation error and the optimization error.

Lemma 6.2

For each epoch such that the event is true, the approximate solution obtained by an - oracle satisfies the following inequality with a probability of at least :

| (24) |

In the following theorem, we extend the analyses in Section 5.2 to upper bound the regret of Algorithm 1 based on an - oracle.

Theorem 6.3

Consider the policy generated by Algorithm 1 based on an - oracle. For any instance stated in Theorem 5.3, the total regret of policy over inventory cycles satisfies

Compared to Theorem 5.3, the regret bound in Theorem 6.3 includes an additional term accounting for the approximation errors of the - oracle. Note that the regret automatically adapts to the errors of the approximate static optimization oracle, even if we do not know the magnitude of the errors when implementing our algorithm. Importantly, Theorem 6.3 asserts that the regret caused by the exploration-exploitation trade-off is still sublinear in .

7 Numerical Experiments

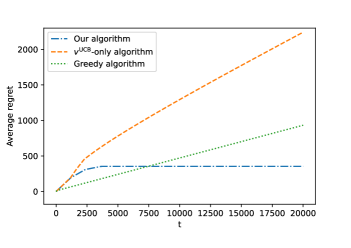

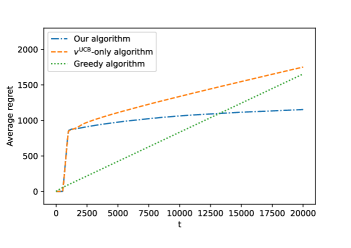

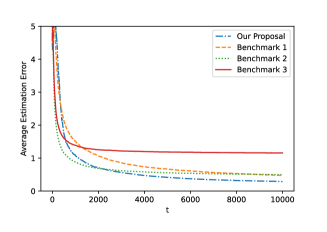

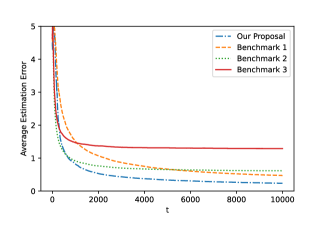

In this section, we numerically assess our proposed algorithm via simulations. In particular, we compare the regret of our proposed exploration-exploitation algorithm with two benchmarks. These two benchmarks use the same parameter estimators as our proposed algorithm, but they use different ways to determine the inventory decisions. We use them to highlight the effectiveness of our proposal to adaptively tune the unit profits and the importance of exploration.

The first benchmark algorithm is the heuristic approach motivated from Agrawal et al. (2019), which we describe in Section 4.3. This approach differs from our proposed algorithm only in the decisions made for non-exploratory epochs. Specifically, for each non-exploratory epoch , the heuristic approach picks the inventory decision by maximizing over all feasible inventory levels . Since the heuristic approach only uses the upper confidence bound on the attraction parameter while fixing the values of unit profits , we refer to it as the “-only” algorithm. The second benchmark is a purely greedy algorithm. Specifically, in every epoch , the greedy algorithm exploits the latest attraction parameter estimate , and determines the inventory decision by maximizing over . This greedy algorithm also abandons the exploratory epochs described in Equation 18, so it does not implement any exploration.