11email: jakespertus@berkeley.edu

COBRA: Comparison-Optimal Betting for Risk-limiting Audits

Abstract

Risk-limiting audits (RLAs) can provide routine, affirmative evidence that reported election outcomes are correct by checking a random sample of cast ballots. An efficient RLA requires checking relatively few ballots. Here we construct highly efficient RLAs by optimizing supermartingale tuning parameters—bets—for ballot-level comparison audits. The exactly optimal bets depend on the true rate of errors in cast-vote records (CVRs)—digital receipts detailing how machines tabulated each ballot. We evaluate theoretical and simulated workloads for audits of contests with a range of diluted margins and CVR error rates. Compared to bets recommended in past work, using these optimal bets can dramatically reduce expected workloads—by 93% on average over our simulated audits. Because the exactly optimal bets are unknown in practice, we offer some strategies for approximating them. As with the ballot-polling RLAs described in ALPHA and RiLACs, adapting bets to previously sampled data or diversifying them over a range of suspected error rates can lead to substantially more efficient audits than fixing bets to a priori values, especially when those values are far from correct. We sketch extensions to other designs and social choice functions, and conclude with some recommendations for real-world comparison audits.

Keywords:

risk-limiting audit, election integrity, comparison audit, nonparametric testing, betting martingale1 Introduction

Machines count votes in most American elections, and (reported) election winners are declared on the basis of these machine tallies. Voting machines are vulnerable to bugs and deliberate malfeasance, which may undermine public trust in the accuracy of reported election results. To counter this threat, risk-limiting audits (RLAs) can provide routine, statistically rigorous evidence that reported election outcomes are correct—that reported winners really won—by manually checking a demonstrably secure trail of hand-marked paper ballots [4, 1, 12]. RLAs have a user-specified maximum chance—the risk limit—of certifying a wrong reported outcome, and will never overturn a correct reported outcome. They can also be significantly more efficient than full hand counts, requiring fewer manually tabulations to verify a correct reported outcome and reducing costs to jurisdictions.

There are various ways to design RLAs. Ballots can be sampled in batches (i.e. precincts or machines) or as individual cards. Sampling individual ballots is more statistically efficient than sampling batches. In a polling audit, sampled ballots are checked directly without reference to machine interpretations. Ballot-polling audits sample and check individual ballots. In a comparison audit, manual interpretations of ballots are compared to their machine interpretations. Ballot-level comparison audits check each sampled ballot against a corresponding cast vote record (CVR)—a digital receipt detailing how the machine tallied the ballot. Not all voting machines can produce CVRs, but ballot-level comparison audits are the most efficient type of RLA.

The earliest RLAs were formulated for batch-level comparison audits, which are analogous to historical, statutory audits [6]. Subsequently, the maximum across contest relative overstatement (MACRO) was used for comparison RLAs [7, 8, 9, 5], but its efficiency suffered from conservatively pooling observed errors across candidates and contest. SHANGRLA [10] unified RLAs as hypotheses about means of lists of bounded numbers and provided sharper methods for batch and ballot-level comparisons. Each null hypothesis tested in a SHANGRLA-style RLA posits that the mean of a bounded list of assorters is less than 1/2. If all the nulls are declared false at risk limit , the audit can stop. Any valid test for the mean of a bounded finite population can be used to test these hypotheses, allowing RLAs to use a wide range of risk-measuring functions.

Betting supermartingales (BSMs)—described in Waudby-Smith et al. [15] and Stark [11]—provide a particularly useful class of risk-measuring functions. BSMs are sequentially valid, allowing auditors to update and check the measured risk after each sampled ballot while maintaining the risk limit. They can be seen as generalizations of risk-measuring functions used in earlier RLAs, including Kaplan-Markov, Kaplan-Kolmogorov, and related methods [7, 10]. They have tuning parameters called bets, which play an important role in determining the efficiency of the RLA. Previous papers using BSMs for RLAs have focused on setting for efficient ballot-polling audits; betting for comparison audits has been treated as essentially analogous [15, 11]. However, as we will show, comparison audits are efficient with much larger bets than are optimal for ballot-polling.

This paper details how to set BSM bets for efficient ballot-level comparison audits, focusing on audits of plurality contests. Section 2 reviews SHANGRLA notation and the use of BSMs as risk-measuring functions. Section 3 derives optimal “oracle” bets under the Kelly criterion [3], which assumes knowledge of true error rates in the CVRs. In reality, these error rates are unknown, but the oracle bets are useful in constructing practical betting strategies, which plug in estimates of the true rates. Section 4 presents three such strategies: guessing the error rates a priori, using past data to estimate the rates adaptively, or positing a distribution of likely rates and diversifying bets over that distribution. Section 5 presents two simulation studies: one comparing the oracle strategy derived in Waudby-Smith et al. [15] for ballot-polling against our comparison-optimal strategy, and one comparing practical strategies against one another. Section 6 sketches some extensions to betting while sampling without replacement and to social choice functions beyond plurality. Section 7 concludes with a brief discussion and recommendations for practice.

2 Notation

2.1 Population and parameters

Following SHANGRLA [10] notation, let denote the CVRs, denote the true ballots, and be an assorter mapping CVRs or ballots into . We will assume we are auditing a plurality contest, in which case , if the ballot shows a vote for the reported winner, if it shows an undervote or vote for a candidate not currently under audit, and if it shows a vote for the reported loser. The overstatement for ballot is . is the average of the assorters computed on the CVRs. Finally, the comparison audit population is comprised of overstatement assorters:

where is the diluted margin: the difference in votes for the reported winner and reported loser, divided by the total number of ballots cast.

Let be the average of the comparison audit population and be the average of the assorters applied to ballots. Section 3.2 of Stark [10] establishes the relations

As a result, rejecting the complementary null at risk limit provides strong evidence that the reported outcome is correct.

Throughout this paper, we ignore understatement errors—those in favor of the reported winner with . Understatements help the audit end sooner, but will generally have little effect on the optimal bets. We comment on this choice further in Section 7. With this simplification, overstatement assorters comprise a list of numbers where corresponds to the value on correct CVRs, corresponds to 1-vote overstatements, and 0 corresponds to 2-vote overstatements. This population is parameterized by 3 fractions:

-

•

is the rate of correct CVRs.

-

•

is the rate of 1-vote overstatements.

-

•

is the rate of 2-vote overstatements.

The population mean can be written .

2.2 Audit data

Ballots may be drawn by sequential simple random sampling with or without replacement, but we first focus on the with replacement case for simplicity. Implications for sampling without replacement are discussed in Section 6. We have a sequence of samples , where is a three-point distribution with mass at , at , and at .

2.3 Risk measurement via betting supermartingales

Let where is a freely-chosen tuning parameter that may depend on past samples . Define and

is a betting supermartingale (BSM) for any bets whenever the complementary holds because

where the first implication comes from simple random sampling with replacement.

Ville’s inequality [13] then states that the truncated reciprocal is a sequentially-valid -value for the complementary null in the sense that

when for any risk limit . More details on BSMs are given in Waudby-Smith and Ramdas [14], Waudby-Smith et al. [15] and Stark [11]. To obtain an efficient RLA, we would like to make as large as possible ( as small as possible) when .

3 Oracle betting

We begin with deriving oracle bets by assuming we can access the true rates , , and and optimizing the expected growth of the logged martingale. Naturally, oracle bets are not accessible in practice, but they are approximated in the practical betting strategies discussed in the next section.

3.1 Error-free CVRs

In the simple case where there is no error at all in the CVRs, and for all . When computing the BSM, it doesn’t matter which ballot is drawn:

Because , the best strategy is to bet as aggressively as possible, setting . Under such a bet, . Setting this equal to yields the stopping time:

| (1) |

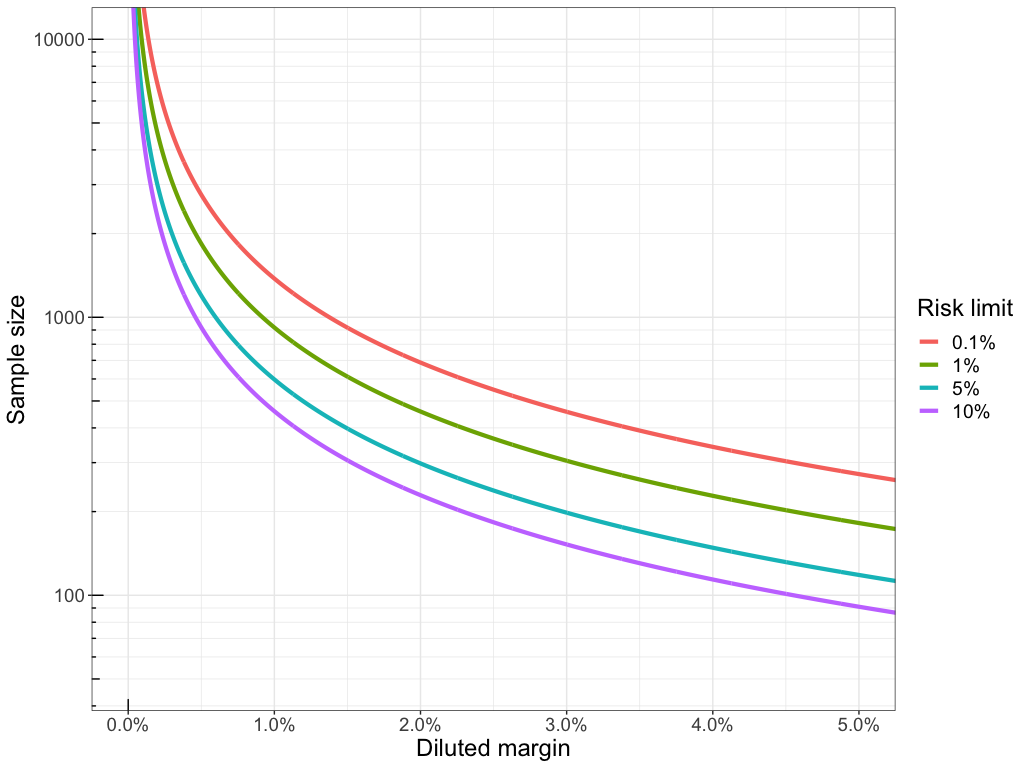

where is the diluted margin. Ignoring understatement errors, (1) is a deterministic lower bound on the sample size of a comparison audit when risk is measured by a BSM. Figure 1 plots this bound as a function of the diluted margin for a range of risk limits .

3.2 Betting with CVR Error

Usually CVRs will have at least some errors, and maximal bets are far from ideal when they do. We now show why this is true before deriving an alternative oracle strategy. In general,

Suppose we fix and try to maximize by maximizing the expected value of each :

This is linear with a positive coefficient on , since under any alternative. Therefore, the best strategy seems to be to set as before. However, unless , will eventually “go broke" with probability 1: if a 0 is drawn while the bet is maximal. Then for all future times and we cannot reject at any risk limit . In this case, we say the audit stalls: it must proceed to a full hand count to confirm the reported winner really won.

To avoid stalls we follow the approach of Kelly Jr. [3], instead maximizing the expected value of . Taking the derivative of with respect to :

| (2) |

The oracle bet can be found by setting this equal to 0 and solving for using a root-finding algorithm.

Alternatively, we can find a simple analytical solution by assuming no 1-vote overstatements and setting . In this case, solving for yields:

| (3) |

Note that since under the alternative, and since .

3.3 Relation to ALPHA

There is a one-to-one correspondence between oracle bets for the BSM and oracle bets for the ALPHA supermartingale, which reparameterizes . Note that the list of overstatement assorters is upper bounded by the value of a 2-vote understatement, . Section 2.3 of Stark [11] shows that the equivalently optimal for use with ALPHA is:

Naturally, when , , which is the maximum value allowed for while maintaining ALPHA as a non-negative supermartingale.

4 Betting in Practice

In practice, we have to estimate the unknown overstatement rates to set bets. We posit and evaluate three strategies: fixed, adaptive, and diversified betting. Throughout this section, we use to denote a generic estimate of for . When the estimate adapts in time, we use the double subscript . In all cases, the estimated overstatement rates are ultimately plugged into (2) to estimate the optimal bets.

4.1 Fixed betting

The simplest approach is to make a fixed, a priori guess at using historic data, machine specifications, or other information. For example, and will prevent stalls and may perform reasonably well when there are few overstatement error. However, this strategy is analagous to apKelly for ballot-polling, which Waudby-Smith et al. [15] and Stark [11] show can become quite poor when the estimate is far from correct. This potential gap motivates more sophisticated strategies.

4.2 Adaptive betting

In a BSM, the bets need not be fixed and can be a predictable function of the data . This allows us to estimate the rates based on past samples as well as a priori considerations. We adapt the “shrink-trunc” estimator of Stark [11] to rate estimation111Shrink-trunc stands for shrinkage-truncation, and was originally designed for adaptive betting in the ballot-polling context, targeting the population mean.. For we set a value , capturing the degree of shrinkage to the a priori estimate , and a truncation factor , enforcing a lower bound on the estimated rate. Let be the sample rates at time , e.g., . Then the shrink-trunc estimate is:

| (4) |

The rates are allowed to learn from past data in the current audit through , while being anchored to the a priori estimate . The tuning parameter reflects the degree of confidence in the a priori rate, with large anchoring more strongly to . Finally, should generally be set above 0. In particular, will prevent stalls.

4.3 Diversified betting

A weighted average of BSMs:

where and , is itself a BSM. The intuition is that our initial capital is split up into pots, each with units of wealth. We then bet on each pot at each time, and take the sum of the winnings across all pots as our total wealth at time . Waudby-Smith and Ramdas [14] construct the “grid Kelly" martingale by defining along an equally spaced grid on and giving each the weight . Waudby-Smith et al. [15] refine this approach into “square Kelly” for ballot-polling RLAs by placing more weight at close margins.

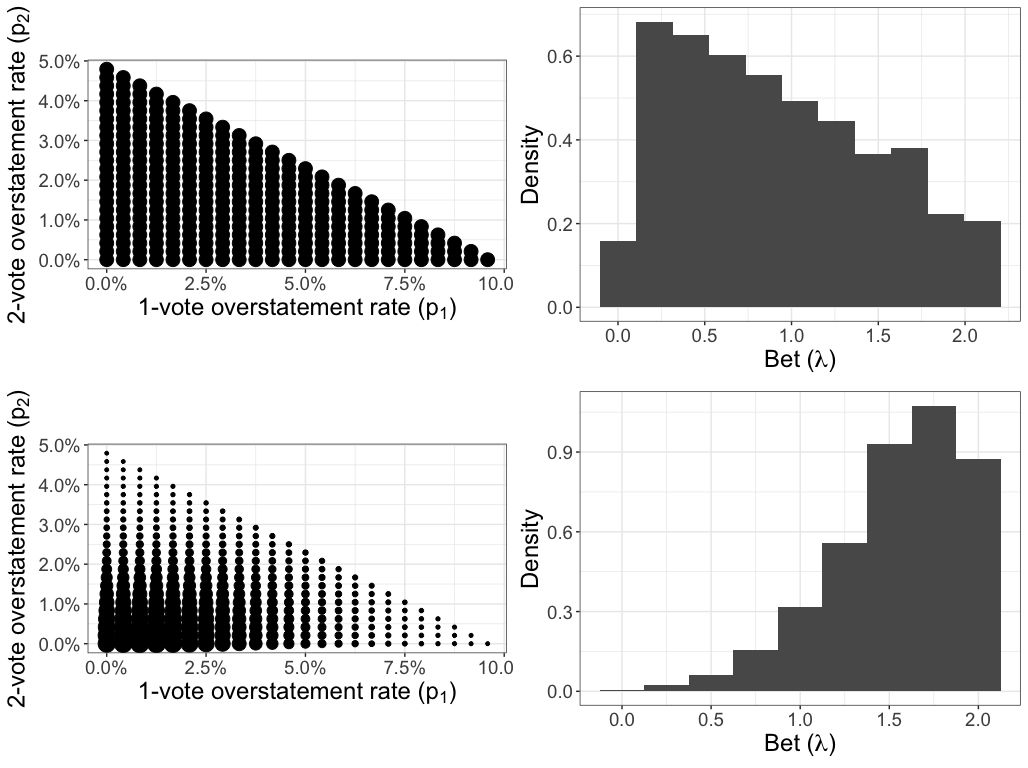

We adapt these ideas to the comparison audit context by parameterizing a discrete grid of weights for and . We first note that are jointly constrained by the hyperplane under the alternative, since otherwise there is enough error to overturn the reported result. A joint grid for can be set up by separately constructing two equally-spaced grids from 0 to , computing the Cartesian product of the grids, and removing points where . Once a suitable grid has been constructed, the weights at each point can be flexibly defined to reflect the suspected rates of overstatements. At each point , is computed by passing the rates into (2) and solving numerically; the weight for is . Thus a distribution of weights on the grid of overstatement rates induces a distribution on the bets.

Figure 2 illustrates two possible weighted grids for a diluted margin of , and their induced distribution on bets . In the top row, the weights are uniform with . In the bottom row, the weights follow a bivariate normal density with mean vector and covariance matrix respectively specified to capture a prior guess at and the uncertainty in that guess. The density is truncated, discretized, and rescaled so that the weights sum to unity.

5 Numerical evaluations

We conducted two simulation studies. The first evaluated stopping times for bets using the oracle comparison bets in (3) against the oracle value of apKelly from Waudby-Smith et al. [15]. The second compared stopping times for oracle bets and the 3 practical strategies we proposed in Section 4. All simulations were run in R (version 4.1.2).

5.1 Oracle simulations

We evaluated stopping times of oracle bets at multiple diluted margins and 2-vote overstatement rates when sampling with replacement from a population of size . At each combination of diluted margin and 2-vote overstatement rates we ran 400 simulated comparison audits. We set : no 1-vote overstatements.

The bets corresponded to oracle bets in Equation (3) or to , the “oracle” value of the apKelly strategy in Section 3.1 of Waudby-Smith et al. [15] and Section 2.5 of Stark [11]222 implies a bet of in the ALPHA parameterization., which were originally derived for ballot-polling. uses the true population mean instead of an estimate based on reported tallies. In each scenario, we estimated the expected and 90th percentile workload from the empirical mean and 0.9 quantile of the stopping times at risk limit over the 400 simulations. To compare the betting strategies, we computed the ratios of the expected stopping time for over in each scenario. We then took the geometric mean across scenarios as the average reduction in expected workload.

Table 1 presents the mean and 90th percentile (in parentheses) stopping times over the 400 simulations. BSM comparison audits with typically require counting fewer than 1000 ballots, and fewer than 100 for wide margins without CVR errors. On average, betting by provides an enormous advantage over : the geometric mean workload ratio is 0.072, a 93% reduction.

| Stopping times | |||

|---|---|---|---|

| DM | 2-vote OR | ) | Oracle () |

| 5% | 1.5% | 10000 (10000) | 1283 (2398) |

| 1.0% | 10000 (10000) | 482 (813) | |

| 0.5% | 7154 (7516) | 242 (389) | |

| 0.1% | 4946 (5072) | 146 (257) | |

| 0.0% | 4559 (4559) | 119 (119) | |

| 10% | 1.5% | 2233 (2464) | 177 (323) |

| 1.0% | 1705 (1844) | 131 (233) | |

| 0.5% | 1346 (1429) | 83 (116) | |

| 0.1% | 1130 (1167) | 65 (60) | |

| 0.0% | 1083 (1083) | 59 (59) | |

| 20% | 1.5% | 339 (371) | 52 (78) |

| 1.0% | 304 (335) | 42 (57) | |

| 0.5% | 272 (289) | 35 (61) | |

| 0.5% | 249 (258) | 30 (29) | |

| 0.0% | 245 (245) | 29 (29) | |

5.2 Practical simulations

We evaluated oracle betting, fixed a priori betting, adaptive betting, and diversified betting in simulated comparison audits with ballots, a diluted margin of 5%, 1-vote overstatement rates , and 2-vote overstatement rates .

Oracle bets were set using the true values of and in each scenario. The other methods used prior guesses and as tuning parameters in different ways. The fixed method derived the optimal bet by plugging in as a fixed value. The adaptive method anchored the shrink-trunc estimate displayed in equation (4) to , but updated using past data in the sample. The tuning parameters were , , . The larger value for reflects the fact that very low rates (expected for 2-vote overstatements) are harder to estimate empirically, so the prior should play a larger role. The diversified method used to set the mode of a mixing distribution, as in the lower panels of Figure 2. Specifically, the mixing distribution was a discretized, truncated, bivariate normal with mean vector , standard deviation , and correlation . The fact that reflects more prior confidence that 2-vote overstatement rates will be concentrated near their prior mean, while encodes a prior suspicion that overstatement rates are correlated: they are more likely to be both high or both low. After setting the weights at each grid point according to this normal density, they were rescaled to sum to unity.

We simulated 400 audits under sampling with replacement for each scenario. The stopping times were capped at 20000, the size of the population, even if the audit hadn’t stopped by that point. We estimated the expected value and 90th percentile of the stopping times for each method by the empirical mean and 0.9 quantile over the 400 simulations. We computed the geometric mean ratio of the expected stopping times of each method over that of the oracle strategy as a summary of their performance across scenarios.

Table 2 presents results. With few 2-vote overstatements, all strategies performed relatively well and the audits concluded quickly. When the priors substantially underestimated the true overstatement rates, the performance of the audits degraded significantly compared to the oracle bets. This was especially true for the fixed strategy. For example, when and , the expected number of ballots for the fixed strategy to stop was more than 20 that of the oracle method. On the other hand, the adaptive and diversified strategies were much more robust to a poor prior estimate. In particular, the expected stopping time of the diversified method was never more than 3 worse than that of the oracle strategy, and the adaptive method was never more than 4 times worse. The geometric mean workload ratios of each strategy over the oracle strategy were 2.4 for fixed, 1.3 for adaptive, and 1.2 for diversified. The diversified method was the best practical method on average across scenarios.

| True ORs | Prior ORs | Stopping Times | |||||

|---|---|---|---|---|---|---|---|

| Oracle | Fixed | Adaptive | Diversified | ||||

| 0.01% | 0.1% | 0.01% | 0.1% | 124 (147) | 125 (119) | 124 (147) | 131 (152) |

| 1% | 124 (147) | 125 (147) | 125 (147) | 131 (154) | |||

| 0.1% | 0.1% | 125 (147) | 129 (151) | 131 (151) | 133 (155) | ||

| 1% | 127 (147) | 132 (153) | 130 (152) | 135 (157) | |||

| 1% | 0.01% | 0.1% | 174 (229) | 167 (229) | 166 (229) | 177 (236) | |

| 1% | 168 (229) | 172 (229) | 167 (229) | 180 (235) | |||

| 0.1% | 0.1% | 176 (229) | 169 (232) | 175 (262) | 181 (262) | ||

| 1% | 159 (205) | 174 (233) | 180 (265) | 184 (264) | |||

| 0.1% | 0.1% | 0.01% | 0.1% | 146 (256) | 153 (338) | 159 (350) | 149 (271) |

| 1% | 151 (256) | 154 (174) | 150 (147) | 145 (154) | |||

| 0.1% | 0.1% | 147 (256) | 152 (256) | 146 (182) | 153 (259) | ||

| 1% | 149 (256) | 151 (244) | 147 (256) | 152 (265) | |||

| 1% | 0.01% | 0.1% | 209 (351) | 227 (420) | 225 (460) | 214 (400) | |

| 1% | 200 (324) | 240 (457) | 232 (500) | 211 (378) | |||

| 0.1% | 0.1% | 204 (351) | 208 (364) | 210 (358) | 208 (344) | ||

| 1% | 208 (324) | 205 (324) | 205 (341) | 219 (371) | |||

| 1% | 0.1% | 0.01% | 0.1% | 526 (996) | 13654 (20000) | 1581 (3517) | 888 (2090) |

| 1% | 525 (984) | 12685 (20000) | 1585 (3731) | 739 (1708) | |||

| 0.1% | 0.1% | 528 (1032) | 9589 (20000) | 1112 (2710) | 812 (1982) | ||

| 1% | 534 (985) | 7247 (20000) | 915 (2294) | 686 (1586) | |||

| 1% | 0.01% | 0.1% | 999 (1908) | 15205 (20000) | 3855 (7811) | 2637 (5873) | |

| 1% | 1110 (2002) | 15641 (20000) | 3477 (7529) | 1803 (4331) | |||

| 0.1% | 0.1% | 1030 (1868) | 13113 (20000) | 2795 (5996) | 2064 (4884) | ||

| 1% | 1127 (2256) | 13094 (20000) | 2437 (5452) | 1604 (3758) | |||

6 Extensions

6.1 Betting while sampling without replacement

When sampling without replacement, the distribution of depends on past data . Naively updating an a priori bet to reflect what we know has been sampled may actually harm the efficiency of the audit.

Specifically, recall that, for , denotes the sample proportion of the overstatement rate at time . If we fix initial rate estimates to , then the updated estimate at time given that we have removed would be

This can be plugged into (2) to estimate the optimal for each draw. Fixing and using equation (3) yields the closed form optimum:

where we have truncated at 2 to guarantee that is even a valid bet. This is necessary because the number of 2-vote overstatements in the sample can exceed the number hypothesized to be in the entire population. If this occurs, the audit will stall if even one more 2-vote overstatement is discovered. More generally, this strategy has the counterintuitive (and counterproductive) property of betting more aggressively as more overstatements are discovered. To avoid this pitfall we suggest using the betting strategies we derived earlier under IID sampling, even when sampling without replacement.

6.2 Other social choice functions

SHANGRLA [10] encompasses a broad range of social choice functions beyond plurality, all of which are amenable to comparison audits. Assorters for approval voting and proportional representation are identical to plurality assorters, so no modification to the optimal bets is required. Ranked-choice voting can also be reduced to auditing a collection of plurality assertions, though this reduction may not be the most efficient possible [2]. On the other hand, some social choice functions, including weighted additive and supermajority, require different assorters and will have different optimal bets.

In a supermajority contest, the diluted margin is computed differently depending on the fraction required to win, as well as the proportion of votes for the reported winner in the CVRs. In the population of overstatement assorters error-free CVRs still appear as , but 2-vote overstatements are and 1-vote overstatements are . So that the population attains a lower bound of 0, we can make the shift and test against the shifted mean . Because there are only 3 points of support, the derivations in Section 3.2 can be repeated, yielding a new solution for in terms of the rates and the shifted mean.

Weighted additive schemes apply an affine transformation to ballot scores to construct assorters. Because scores may be arbitrary non-negative numbers, there can be more than 3 points of support for the overstatement assorters and the derivations in Section 3.2 cannot be immediately adapted. If most CVRs are correct then most values in the population will be above 1/2, suggesting that an aggressive betting strategy with will be relatively efficient. Alternatively, a diversified strategy weighted towards large values of can retain efficiency when there are in fact high rates of error. It should also be possible to attain a more refined solution by generalizing the optimization strategy in Section 3.2 to populations with more than 3 points of support.

6.3 Batch-level comparison audits

Batch-level comparison audits check for error in totals across batches of ballots, and are applicable in different situations than ballot-level comparisons, since they do not require CVRs. SHANGRLA-style overstatement assorters for batch-level comparison audits are derived in Stark [11]. These assorters generally take a wide range of values within . Because they are not limited to a few points of support, there is not a simple optimal betting strategy. However, assuming there is relatively little error in the reported batch-level counts, will again place the majority of the assorter distribution above 1/2. This suggests using a relatively aggressive betting strategy, placing more weight on bets near 2 (or near the assorter upper bound in the ALPHA parameterization).

Stark [11] evaluated various BSMs in simulations approximating batch-level comparison audits, though the majority of mass was either at 1 or spread uniformly on , not at a value . Nevertheless, in situations where most of the mass was at 1, aggressive betting () was most efficient. Investigating efficient betting strategies for batch-level comparison audits remains an important area for future work.

7 Conclusions

We derived optimal bets for ballot-level comparison audits of plurality contests and sketched some extensions to broader classes of comparison RLAs. The high-level upshot for practical audits is that comparison should use considerably more aggressive betting strategies than polling, a point made abundantly clear in our oracle simulations. Our practical strategies approached the efficiency of these oracle bets, except in cases where . Such a high rate of 2-vote overstatements is unlikely in practice, and would generally imply something has gone wrong: votes for the loser should very rarely be flipped to votes for the winner.

Future work should continue to flesh out efficient strategies for batch-level comparison, and explore the effects of understatement errors. We suspect that understatements will have little effect on the optimal strategy. If anything, they imply bets should be even more aggressive. However, we already suggest placing most weight near the maximal value of in practice, diversifying or thresholding to prevent stalls if 2-vote overstatements are discovered. We hope our results will guide efficient real-world comparison RLAs, and demonstrate the practicality of their routine implementation for trustworthy, evidence-based elections.

Acknowledgements

My work on RLAs has been joint with my thesis advisor, Philip Stark, who provided helpful guidance on earlier drafts of this paper. My research is supported by NSF grant 2228884.

Code

Code implementing our simulations and generating our figures and tables is available on Github at https://github.com/spertus/comparison-RLA-betting.

References

- Appel et al. [2020] A. Appel, R. DeMillo, and P. Stark. Ballot-marking devices cannot assure the will of the voters. Election Law Journal, Rules, Politics, and Policy, 2020. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3375755.

- Blom et al. [2019] M. Blom, P. Stuckey, and V. Teague. RAIRE: Risk-limiting audits for IRV elections. https://arxiv.org/abs/1903.08804, 2019.

- Kelly Jr. [1956] J. L. Kelly Jr. A New Interpretation of Information Rate. Bell System Technical Journal, 35(4):917–926, 1956. ISSN 1538-7305. doi: 10.1002/j.1538-7305.1956.tb03809.x. URL https://onlinelibrary.wiley.com/doi/abs/10.1002/j.1538-7305.1956.tb03809.x. _eprint: https://onlinelibrary.wiley.com/doi/pdf/10.1002/j.1538-7305.1956.tb03809.x.

- Lindeman and Stark [2012] M. Lindeman and P. Stark. A gentle introduction to risk-limiting audits. IEEE Security and Privacy, 10:42–49, 2012.

- Ottoboni et al. [2018] K. Ottoboni, P. Stark, M. Lindeman, and N. McBurnett. Risk-limiting audits by stratified union-intersection tests of elections (SUITE). In Electronic Voting. E-Vote-ID 2018. Lecture Notes in Computer Science. Springer, 2018. https://link.springer.com/chapter/10.1007/978-3-030-00419-4_12.

- Stark [2008] P. Stark. Conservative statistical post-election audits. Ann. Appl. Stat., 2:550–581, 2008. URL http://arxiv.org/abs/0807.4005.

- Stark [2009a] P. Stark. Risk-limiting post-election audits: -values from common probability inequalities. IEEE Transactions on Information Forensics and Security, 4:1005–1014, 2009a.

- Stark [2009b] P. Stark. Efficient post-election audits of multiple contests: 2009 California tests. http://ssrn.com/abstract=1443314, 2009b. 2009 Conference on Empirical Legal Studies.

- Stark [2010] P. Stark. Super-simple simultaneous single-ballot risk-limiting audits. In Proceedings of the 2010 Electronic Voting Technology Workshop / Workshop on Trustworthy Elections (EVT/WOTE ’10). USENIX, 2010. URL http://www.usenix.org/events/evtwote10/tech/full_papers/Stark.pdf.

- Stark [2020] P. Stark. Sets of half-average nulls generate risk-limiting audits: SHANGRLA. Financial Cryptography and Data Security, Lecture Notes in Computer Science, 12063, 2020. Preprint: http://arxiv.org/abs/1911.10035.

- Stark [2022] P. Stark. ALPHA: Audit that learns from previously hand-audited ballots. Annals of Applied Statistics, Conditionally accepted, 2022. Preprint: https://arxiv.org/abs/2201.02707.

- Stark and Xie [2019] P. B. Stark and R. Xie. They may look and look, yet not see: Bmds cannot be tested adequately, 2019. URL https://arxiv.org/abs/1908.08144.

- Ville [1939] J. Ville. Étude critique de la notion de collectif. 1939. URL http://eudml.org/doc/192893.

- Waudby-Smith and Ramdas [2020] I. Waudby-Smith and A. Ramdas. Estimating means of bounded random variables by betting, 2020. URL https://arxiv.org/abs/2010.09686.

- Waudby-Smith et al. [2021] I. Waudby-Smith, P. Stark, and A. Ramdas. RiLACS: Risk Limiting Audits via Confidence Sequences. In R. Krimmer, M. Volkamer, D. Duenas-Cid, O. Kulyk, P. Rønne, M. Solvak, and M. Germann, editors, Electronic Voting, pages 124–139, Cham, 2021. Springer International Publishing. ISBN 978-3-030-86942-7.