Learning Optimal Bidding Strategy: Case Study in E-Commerce Advertising

Abstract

Although the bandits framework is a classical and well-suited approach for optimal bidding strategies in sponsored search auctions, industrial attempts are rarely documented. This paper outlines the development process at Zalando, a leading fashion e-commerce company, and describes the promising outcomes of a bandits-based approach to increase profitability in sponsored search auctions. We discuss in detail the technical and theoretical challenges that were overcome during the implementation, as well as the mechanisms that led to increased profitability.

1 Introduction

Search engine advertising is essential for e-commerce companies, and bidding algorithms have significantly improved their efficiency by enabling more precise ad targeting. In the context of online advertising, a bidding problem typically refers to the challenge faced by advertisers in optimizing bids in sponsored search auctions for maximum profitability or conversions. To achieve this goal, advertisers must carefully balance the cost of bidding with the potential value of gaining clicks or conversions from their ad.

As a leading European company for clothing and beauty products (cosmetics), Zalando made efficient marketing investments a key objective. This paper documents a promising attempt at Zalando to optimize bids in sponsored search auctions for maximum profitability using the bandits approach. Bandits is a reinforcement learning (RL) approach that provides a formal framework for sequential decision-making in repeated interactions with an environment. Despite the extensive theoretical research on bandits (and RL in general) in the past decade and their widespread usage in content placement, recommendations, and e-commerce, there are only a few documented instances of their industrial applications for bid optimization. Our work proves that maximizing profitability through the RL approach can yield substantial value, but it requires overcoming significant challenges that have yet to be encountered in popular RL benchmarks.

As of independent interest, we introduce a computationally efficient bid placement system and a substantial data collection mechanism that are prone to the most challenges encountered in real-life scenarios (described in Section 1.2). Furthermore, the developed infrastructure is versatile and can be readily adapted to any contextual decision-making setting.

1.1 Background and framework

Pay-per-click sponsored search auctions emerged in the late 1990s as a quintessential example of auction theory and have become an indispensable part of the business model of web hosts. Typically, the host (the seller) runs a separate auction for each search query, and at each auction, the entity being sold is the right to place an ad in a slot. Advertisers (bidders) repeatedly bid for slots on a search engine and pay the seller only if their ad gained a click. There is a fixed number of slots for advertisements, and the advertisers have different valuations for these slots. The complexity of the underlying auction mechanism of sponsored search engines and the large volume of repeated auctions has given rise to an abundance of automated bidding tools, where bidders were constantly changing their bids in response to new information and changing information from other bidders [1].

In this paper, we take the bidder’s perspective and aim to develop an algorithm that maximizes total profitability. Using a sequential decision-making paradigm, we model repeated interactions between the seller (Google Ads) and the bidder (Zalando). Specifically, we take an online learning perspective and formulate a problem using adversarial bandits [2]. At each iteration, the bidder has some (unknown) private value and submits a bid , based on the empirical importance-weighted performance of the bids. The auction mechanism then outputs an outcome . Using the bandit language, the bidder selects action and consequently observes reward .

1.2 Challenges of learning in sponsored search auctions

In sponsored search auctions, the business goal is to optimize bids for maximum profitability. It causes practitioners to focus on a complex and long-term event, typically a conversion such as a sale. As such, learning in sponsored search auctions poses a unique interplay between challenges from various disciplines, including auctions and online advertising.

-

•

Blackbox auction mechanism. Most of the theoretical work assumes a structured underlying auction mechanism, with some papers positing a generalized second-price auction lying at the heart of the allocation process, while others describe it as a first-price auction. However, for bidders participating in Google Ads sponsored search auctions, the underlying auction mechanism remains a black box, as Google does not disclose the type of auction mechanism being used [3, 4].

-

•

Unknown valuation of the goods at sale. A standard assumption in the literature on auction theory is that participants arriving in the market have a clear assessment of their valuation for the goods at sale (see, e.g., [5, 6, 7, 8]). However, this assumption is severely violated in online advertising where the high-frequency auction mechanism is subject to changing market conditions and user behavior. This can amend the balance between exploration and exploitation and complicate learning behavior [9].

-

•

Delayed feedback. While clicks can be observed shortly after an ad is displayed, it may take hours or even days for the corresponding sale to occur. This delay in feedback can make it challenging to optimize bids or other decisions in online advertising, as the true value of action may take time to be apparent [10].

-

•

Batch update. In sponsored search auctions, a large volume of multiple-item auctions takes place per iteration, where bidders typically submit a batch of bids. Consequently, bidders have access only to information aggregated over a certain period, leading to batched feedback - where the rewards for a group of actions are revealed together and observed at the end of the batch. In contrast to traditional online feedback, where the reward for each action is immediately revealed after it is chosen, learning from batched feedback can be more efficient when obtaining feedback is costly or time-consuming but comes at the cost of learning performance [11].

-

•

Reward sparsity. Sparse reward refers to a situation where the reward signal provided to the learner is infrequent or incomplete. This is especially cumbersome in marketing applications, where conversion rates are typically low and observational data does not capture behavioral patterns. This scarcity of information makes it difficult for advertisers to make informed decisions, and, as a result, the optimization process becomes more challenging. RL algorithms that depend on frequent and informative feedback to learn tend to struggle in such settings.

-

•

Clicks attribution. After observing a desired outcome (a single conversion event), it is challenging to attribute credit to a specific action in a coherent way: a customer clicking on an advertisement might delay ordering or buy another product if they buy a product at all. A user might furthermore have been exposed to different ads at other points before the order conversion happened, and assigning credit to a specific bid that was active at the conversion time, can lead to an inability to evaluate its effectiveness accurately.

-

•

Measurement. Beyond the click attribution to order, a company might be interested in favoring clicks that lead, for instance, to recurring orders or new customer acquisitions. This purpose is usually incorporated in a complex mechanism, which measures which clicks led to such events. Hence, the click value can be a complex quantity, making the measurement challenging. Furthermore, the data we incorporate into learning are subject to various biases, such as normalization or selection bias. It is crucial to be able to construct an unbiased estimate of a desired metric to achieve reliable results. This is particularly important in repeated interactions, where the goal is to establish a causal relationship between the action and outcome [12].

This list is incomplete, and there are many more challenges in real-life. We focus on the successful resolution of the most pressing, in our view, challenges.

1.3 Contribution

Addressing the aforementioned challenges requires a synthesis of RL techniques as well as a bidding system. In this paper, we develop a systematic and practical approach that explicitly optimizes bids for maximum profitability and addresses most of the challenges. Our RL methodology captures Blackbox auction mechanism, Unknown valuation of the goods at sale, Batch update, and Measurement challenges. It does not, however, fully addresses the Clicks attribution nor the data collection issues caused by Batched and Delayed feedback, which we incorporate by a bid placement system on the deployment side. Thus, only Reward sparsity issues remain unaddressed by our approach, which we elaborate on in Sections 4.2 and 5.2.

The evaluation of our solution demonstrates an increase in partial profit during the test duration. The mechanism by which this profit increase occurs is nonetheless complex and varies depending on the product at sale. The main source of profitability improvement comes from reduced costs: the algorithm stopped advertising a certain number of low-profitable products to favour more efficient bid values for a small selection of high-profitable products.

In summary, the paper makes the following contributions to the literature:

-

•

We document a successful attempt to learn optimally and efficiently in complex sponsored search auctions.

-

•

We introduce an extension of the EXP3 algorithm to the batched and delayed feedback setting, which we call Batch EXP3.

-

•

We develop a computationally efficient bid placement system that is, in combination with the methodology, robust against many challenges arising in real life. Moreover, the developed system is versatile and can be readily adapted to any contextual decision-making setting.

-

•

To the best of our knowledge, we are the first to present an RL-based bidding system, which is deployed in a live environment system.

1.4 Outline

Section 2 briefly recalls previous relevant work. Section 3 is devoted to the methodological setup and contains problem definition (Section 3.1) and translating it into the bandit setting (Section 3.2). The bidding system deployment and live test design are given in Section 4. In Section 5, we evaluate our solution and elaborate on mechanisms by which the profitability is improved (Section 5.1). Consequently, in Section 6, we discuss the limitations of our work and future directions. Finally, we conclude with Section 7.

2 Related work

Auctions

The majority of auction theory research has focused on designing truthful auction mechanisms to maximize the seller’s revenue by optimizing a reserve price (a price below which no transaction occurs) [13, 14, 15]. A more traditional approach takes a game-theoretic view, where the seller has perfect or partial knowledge of bidders’ private valuations modeled as probability distributions [16]. However, this approach has a major limitation as it relies on perfect knowledge of the bidders’ value distribution which is unlikely to be known to the seller in practice [5, 6].

In recent years the ubiquitous collection of data has presented new opportunities where unknown quantities, such as the bidders’ value distributions, may potentially be learned from past observations [17]. This has led to the emergence of the online learning approach in repeated auctions from both seller’s and bidder’s perspectives. Sellers usually seek to set a reserve price to optimize revenues [18, 19, 20, 21, 22, 23]. In fact, this is the main mechanism by which a seller can influence the auction revenue in today’s electronic markets [18]. By contrast, bidders try to maximize their reward while simultaneously learning the value of a good sold repeatedly [17, 24]. In particular, this triggered the emergence of a large number of various RL approaches, which we describe below in more detail.

RL for bid optimization.

Unlike much of the mechanism design literature, RL approaches for bid optimization are not searching for the optimal revenue under a truthful auction mechanism. Rather, they focus on maximizing either seller’s or bidder’s revenue. The existing research to optimize bidding strategy falls into two main categories: methods based on the bandits formulation and methods based on the full RL formulation.

The origin of the full RL methods in application to auctions can be traced back to [25]. In this paper, the authors modeled a budget-constrained bidding problem as a finite Markov Decision Process (MDP). The authors utilize a model-based RL setting for the optimal action selection assuming the perfect knowledge of the MDP. This work led to various improvements, such as proposing model-free RL algorithms [26, 27], where the learner cannot obtain perfect information, and considering continuous action space using policy gradient methods [28]. However, this line of work has two major limitations: first, it lacks theoretical guarantees, and, second, it does not tackle the real-life challenges described in Section 1.2. For example, most of these papers rely heavily on simulation and replay of datasets and focus on simpler impression-based reward definitions. Additionally, their high complexity makes them difficult to apply in real-life scenarios due to weak debuggability.

On the other hand, bandit-based methods have proved to be effective in optimizing bidding strategies for the second-price auctions [17, 18, 29], first-price auctions [7, 8, 30], and generalized auction mechanisms [9]. Due to the truthfulness of second-price auctions, methods developed for such a mechanism are based on optimism in the face of uncertainty principle [17, 18, 29], whereas first-price and generalized auction mechanisms leverage the adversarial nature of the problem 111First-price and generalized auctions are known to be untruthful, making the environment from the bidders’ perspective adversarial. and use exponential weighting methods [7, 8, 9, 30].

One paper that we found particularly relevant to our approach is [9]. In this paper, a general auction mechanism is considered, where the product valuation is unknown, evolving in an arbitrary manner and observed only if the bidder wins the auction. The authors decompose the reward of placing bid at iteration as , where is the allocation function and is the revenue function. Consequently, they assume that while is subject to bandit feedback, is subject to online feedback, i.e., the learner gets to observe for each bid and not only for the placed bid . Based on this, they develop an exponentially faster algorithm (in action space) than a generic bandit algorithm (, where is a horizon and is the cardinality of a bid space). Unfortunately, due to the complexity of our setting, we could not make use of their assumption and had to recover to a more classical bandit approach in our solution [2].

3 Learning in sponsored search auctions

In this section, we formulate the learning problem in repeated sponsored search auctions, with discussions on various assumptions. Subsequently, we describe our approach from a methodological perspective.

3.1 Problem setup

Online advertising

The user journey starts in a search engine with a keywords query. The search engine analyses the query and presents the user with a selection of advertisements for products by different bidders. From the bidder’s perspective, it means presenting a large number of products to a large amount of customers simultaneously. The corresponding bidding model is developed in steps of increasing complexity to simplify the exposition.

Single item single auction per iteration

We start with a single auction per iteration first. In this situation, the bidder bids sequentially on one product. We focus on a single bidder in a large population of bidders during a time horizon of , where is unknown and possibly infinite. At the beginning of each iteration , , the bidder has a value per unit of a good and, based on the past observations, submits a bid , where is a finite set of bids (will be specified later). The outcome of the auction is as follows: if (click occurred), the bidder gets a good and pays ; if (no click occurred) the bidder does not get the good and pays nothing. Consequently, the instantaneous profitability of the bidder is

| (1) |

In general, the allocation function and the payment function depend on the underlying auction mechanism as well as the bid profile of other bidders, and for formulating the problem from an auction perspective should take these dependencies into account. However, as we mentioned in Section 1.2, Google Ads does not explicitly specify what kind of auction mechanism is being used in reality, nor does it provide the auctions contexts to the bidder (numbers of bidders, winning bids, etc.). Therefore, we take an online learning perspective and formulate the problem as stated in (1), assuming that the bidder gets to observe and if auction is won; and observes only is auction is lost. Note that is unknown to the bidder before auction starts and is only revealed if the auction is won.

The goal of the bidder, therefore, is to maximize the total profitability:

| (2) |

In real life, additional subtleties arise. Further, we describe practical nuances in more detail, gradually complicating the setting and, after all, reaching the real-life formulation that we address in this paper.

Single item multiple auctions per iteration

First, the sponsored search engine runs multiple auctions per iteration, and only aggregated information is available to the bidder. Formally, every iteration is associated with a set of reward contests . The bidder picks a bid , which is used at all reward contests. 222Note, changing a bid within the reward contest would not make any sense, as the bidder does not have access to granular information about every single auction. At the end of iteration , the bidder observes aggregated values of gain , payment , and click-through-rate in the reward contest . Since only aggregated information is revealed to the bidder, this makes learning in the multiple auctions per iteration setting more complex.

We denote , and define the instantaneous aggregated profitability as follows:

and the bidder’s goal becomes to maximize the total aggregated profitability

| (3) |

Since we are solely working with aggregated data, we omit ′ and write and instead of and .

Remark 1.

is a random variable which distribution is unknown to the learner. Moreover, different allocation and payment functions might be used for different auctions, i.e., and depend on as opposed to [9].

Single item multiple auctions per iteration under delayed batched feedback

Next, due to the complex reward definition, the bidder does not observe the outcome of bid immediately after reward contest ends. Instead, the outcomes are batched in groups and observed after some delay. To define it formally, we borrow notations from [31]. Let be a grid of integers such that . It defines a partition where and for . The set is the -th batch. Next, for each , let be the index of the current batch . Then, for each , the bidder observes the outcome of reward contest only after batch ends, for some positive integer .

Although the bidder’s goal (3) remains unchanged in the batched feedback setting, we emphasize that the complexity of the problem increases greatly, as the decision at round can only depend on observations from batches ago. In fact, [11] shows that, in the worst case, the performance of the batch learning deteriorates linearly in the batch size for stochastic linear bandits.

Multiple items multiple auctions per iteration under batched feedback

Finally, bidders are rarely presented with a single item, and in real life, they strive to optimize bids for multiple items simultaneously. Let be a finite set of possible contexts. Every iteration is associated with a unique set of contexts . Given , the bidder selects a vector of bids , one for each context, and observes vectors of aggregated values and , where is vector functions from to . The instantaneous profitability, in this case, is defined as the inner product between the vector of profits and vector of ones 1:

| (4) |

and the goal becomes to maximize the total profitability for multiple items

| (5) |

Assumptions

Assumption 1 (Independence of goods at sale).

A set of possible contexts is represented by unit vectors, for every .

Such context set definition corresponds to the situation when the bidder is presented with items to bid for, and the bidder treats these items independently from each other. In this case, we can consider instances of the learner, each solving a single-item problem (3).

Alternatively, [7] and [30] propose to use valuation or its estimate as a context. However, we consider a stricter setting, assuming that is unknown for the bidder, nor data is available for its estimation. Nevertheless, we emphasize that Assumption 1 is not critical, as a simple partition of private valuations to groups and considering separate instances for each group reduces to our approach. We will discuss it further in Section 6.

Assumption 2 (Fixed batch size and delay).

Grid divides the horizon in equal partitions, i.e., for all in , , for some positive integer , and delay is fixed for all rounds. Moreover, values of and are known to the bidder in advance.

Although restrictive from the problem formulation perspective, the batch size and delay are controlled by our bidding system and can be wholly justified in practice (see Section 4). Moreover, our algorithm, which we introduce in Section 3.3, is adaptable to unknown and random batch sizes and delays.

3.2 Bandit formulation

We formalize the goal (3) using the adversarial bandits setting and assume that the bidder (learner) is presented with a discrete set of bids (actions) . At each auction (round) , the learner picks an action and the adversary constructs reward by secretly choosing reward components , payment functions , and allocation functions , which is further observed by the learner. 333In the subsequent sections, we will use pairs bidder-learner, bid-action, and outcome-reward interchangeably, depending on the context.

The advantage of the adversarial setting is that it avoids imposing any assumptions on the reward components (except that ), which is perfectly combined with the black-box nature of Google Ads sponsored search auctions. Moreover, as we mentioned in Section 2, the adversarial setting allows accounting for the untruthfulness of the underlying auction mechanism.

Remark 2.

Note, restricting the bid space to a discrete set is justified as in Google Ads, the bids are integer numbers of cents and take values between 0.01$ and 2$ [32].

The bandit formulation, therefore, accounts for Blackbox auction mechanism and Unknown valuation of the goods at sale challenges.

3.3 Algorithm

We introduce an adaptation of the EXP3 algorithm to the batch setting, which we call Batch EXP3. Batch EXP3 enables strong theoretical guarantees by building on top of the basic algorithm and extensions to more complex settings with batched and delayed feedback. Specifically, Batch EXP3 maintains instances of the learner, each instance for a separate item, and performs -steps delayed update at the end of each batch. Importantly, the update mechanism of Batch EXP3 preserves the importance-weighted unbiased estimator of rewards, thus, making our adaptation resilient to Batch update and Measurement challenges. Algorithm 1 formalizes the description above.

Theoretical guarantees

Theoretical guarantees of the Batch EXP3 algorithm follow from a classical analysis of the EXP3 algorithm (see, e.g., [2]). For completeness and theoretical rigor, we formulate a separate statement on Batch EXP3 theoretical performance. In order to do that, we start with the definition of the theoretical success metric called regret. Regret is the difference between the learner’s total reward and reward obtained by any fixed vector of bids in hindsight:

Theorem 3 (Regret of Batch EXP3).

The regret of the Batch EXP3 algorithm with the learning rate is: .

| (6) |

Proof.

We start analyzing regret for , :

where is due to batch execution of Batch EXP3 and the fact that the first steps no update is happening, is because of Assumption 2, and follows from standard analysis of EXP3. Then, summing over gives . ∎

4 Deployment

While our RL methodology accounts for Blackbox auction mechanism, Unknown valuation of the goods at sale, Batch update, and Measurement challenges, it takes system support to fully address Clicks attribution and the data collection issues caused by Batched and Delayed feedback. For example, Algorithm 1 simply assumes data is correctly provided as input, but this is nontrivial in practice.

To provide a systematic solution that explicitly optimizes bids for maximum profitability, we fill these gaps on the deployment side. Subsequently, we describe the live test design for our bidding system.

4.1 Bidding system architecture

Clicks attribution

It is rarely the case when a single click leads to a desired outcome. Usually, a customer journey starts with a single click, but it is a chain of clicks that results in a conversion event. Identifying click chains and attributing credit to a single click in each click chain is a complex independent task that requires great engineering efforts. At Zalando, the performance measurement pipeline takes up these challenges and measures the performance of online marketing at scale. In short, the pipeline sources all marketing clicks, sales, as well as more complex conversion events such as customer acquisitions, and creates the customers’ journeys across all their devices, from first ad interaction to conversion. Then, an attribution module comes into play and determines how much incremental value was created by every ad click by iterating many different attribution models. We refer the interested reader to [33] for more details.

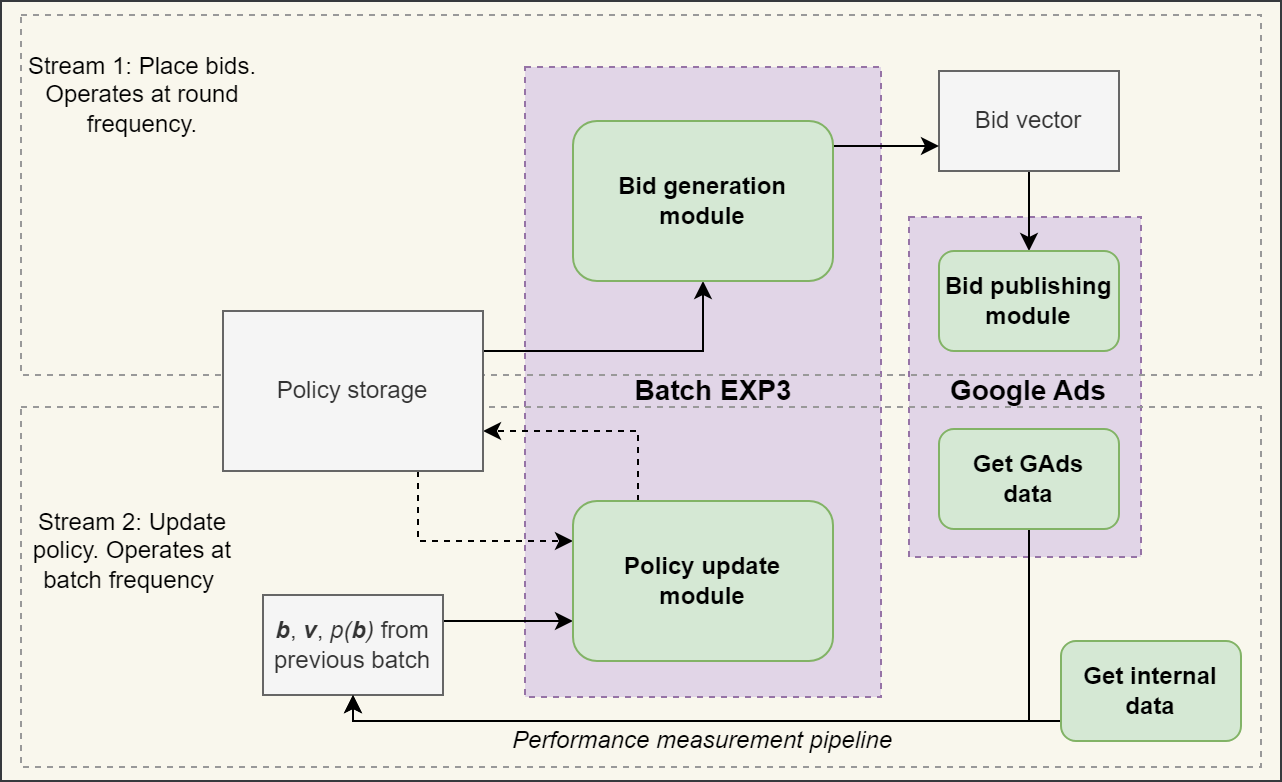

Bidding system architecture

Our solution is designed to match the modularity of the RL methodology in an efficient way, including the bid generation and policy update components and the performance measurement pipeline. The bidding system contains two streams: the first stream is responsible for bid placement in Google Ads; the second stream unifies the performance measurement pipeline and the policy update component.

Ideally, both streams are to be synchronized and run as frequently as possible, one right after the other. However, the performance measurement pipeline is subject to daily execution due to its compoundness and complexity, making any attempt to increase the frequency of the second stream meaningless. Keeping the same frequency for the first stream would admit placing one bid a day, which slows down the learning process considerably.

To account for this limitation, we desynchronize two streams and execute the first stream with a higher frequency, updating bids every 3 hours. Such improvement allowed us to speed up the learning process substantially. Therefore, the first stream runs every 3 hours and samples bids from the latest policy (3-hour time period corresponds to round ), while the second stream is subject to daily execution and performs an update based on batched feedback (scheduled by grid ). 444The first stream is scheduled at midnight, 3am, 6am, etc. The second stream runs at midnight. The architecture is illustrated in Figure 1.

4.2 Live test design and unfolding

Test scope

The test took place from December 16th, 2022 (date of deployment) to January 29th, 2023, in a large European country. A list of 180 () clothing products was selected to be steered by the bandits algorithm. Because of the data sparsity, we chose to focus for this test on products for which the traffic was deemed high enough. The selection criterion was that they should meet a threshold of ten average daily clicks over a period of six months. The products selected for the test were randomly sampled amongst those satisfying this traffic threshold.

Profit metric

In Section 3, we defined the reward as the aggregated difference between the valuation and costs . While costs causes no problems and correspond to the expenditure during the round (which is (almost) immediately available to the bidder), the valuation is abstract and requires special attention.

We assumed that the valuation is unknown to the bidder before auction starts. In fact, it is difficult to evaluate even when auction is over. Typically, the ground truth of valuation is assumed to be the gain auction has generated over days, where might correspond to several months due to return and cancellation policies. Therefore, it is impractical to learn a bidding system when is too big.

Although a vast literature on bandits with delayed feedback provides solutions with delay-corrected estimations, these solutions are not infallible and cannot completely eliminate delay. Therefore, there are primarily two practical ways of dealing with delays: shortening the feedback loop by decreasing or developing a delay-free method by substituting with some approximation. Due to the lack of historical data, we have taken a more pragmatic approach and shortened the delay to 2 days (we will discuss this further in Section 6). As a result, we focus on maximizing the 2 days partial profit, i.e., profit attributed within 2 days conversion window after the bid placement.

Profit metric normalization

We apply two normalization steps to the 2 days partial profit. The first normalization step is a naive yet pragmatic way of incorporating side information into the modeling, and it eliminates the difference between time periods. Since users’ activity is different during the nighttime and daytime, rewards that we observe from 3am - 6am are incomparable to rewards that we observe from 3pm - 6pm. We reduce rewards to a common medium of expression by normalization:

where is the time period number within the batch , and is the ratio of average traffic during time period to the average traffic of the most active time period, .

Next, the bandit formulation requires rewards to be in the range, which is far from the truth in a real-life application. In order to account for that, we apply minimax normalization to rewards by

where and are the 5-th and 95-th quantities of the historical 2 days partial profit.

The coefficients were calculated on the market level and remain constant for all products ; whereas the coefficients and are product-dependent and were calculated individually for each product.

Bid space

The bandit formulation described in Section 3.2 supports a discrete and finite set of bids. The conducted analysis of historical data demonstrated that bids higher than 40 cents are unprofitable, which, due to Remark 2, narrows the potential bid space values to range from 1 cent to 40 cents. To trade off the total number of bids and coverage of the bid space, we decided to include more options for lower bids (with step 2 cents) and fewer options for higher bids (with steps 3-5 cents). The final bid space consists of 14 possible bids and is

| (7) |

Test reset

We started the experiment with a generic value of the learning rate . After we rolled out the solution, we spotted unstable learning behavior in the bidding system. On December 30, we decided to reset the test with the learning rate , which corresponds to less aggressive exploitation by the learner. While this adjustment did not resolve the issue completely, it mitigated the level of instability and facilitated the learning process. We will detail this phenomenon in the next section.

5 Evaluation

Profitability behavior

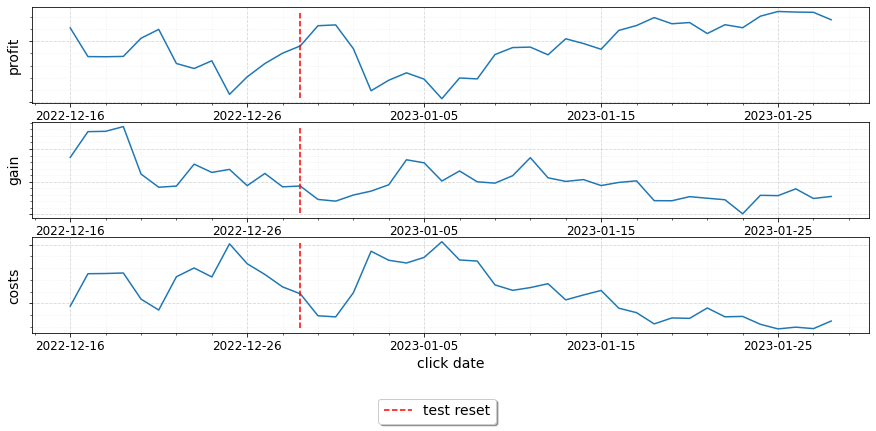

Figure 2 presents the 2 days partial profit (top), gain (middle), and costs (bottom) dynamics over 180 products during the test period. To protect business-sensitive information, we have concealed the axis and only report the relative behavior. As of January 5, we can see a strong upward trend of 2 days partial profit, which suggests the bandit bidding system indeed increases the total profitability. Taking a closer look at the reward components, see Figure 2, we see that both total gain and costs are decreasing, but overall the decrease in costs covers the decrease in gain, which allows profitability to grow.

While it is consistent with the logic at the global level, it is necessary to explain how profitability is increasing at the product level. Two mechanisms are available to increase profits: selecting bids to increase gains and selecting bids to decrease costs. These mechanisms can either complement each other or compete with each other. In order to understand the mechanism by which the profitability is increasing at the product level, a more thorough analysis is required to identify the products which are driving cost reduction while maintaining a sufficiently high level of gain.

5.1 Detailed analysis

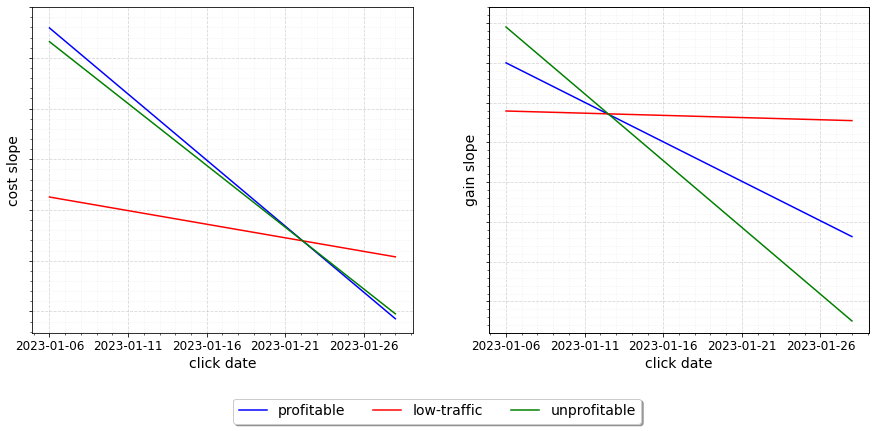

First, we concentrate on products with high traffic by removing 60 products (33%) with a low number of clicks (we will revisit low-traffic products later). Further, we split high-traffic products into a profitable sample and an unprofitable sample. The profitable sample is a group of 23 products (13%) with the highest gain-to-cost ratio. The unprofitable sample is the rest high-traffic product which numbered 97 products (54%). Table 1 presents statistics for each group.

Figure 3 demonstrates this split and outlines the mechanisms by which the algorithm increases profitability. Specifically, it shows that the costs of the profitable sample decrease faster than the costs of the unprofitable sample. Simultaneously, the gains for the profitable sample decrease slower than the gain of the unprofitable sample. In other words, the algorithm is driving the increasing profitability by spending the budget more efficiently for the profitable sample, while, for the unprofitable sample, it is just decreasing costs. To support this even stronger, we provide individual examples of both profitable and unprofitable samples.

| Product group | % products | % clicks | % costs | % gain |

|---|---|---|---|---|

| profitable | 12.8% | 51.3% | 45.7% | 57.1% |

| unprofitable | 53.9% | 41.6% | 46.9% | 34.8% |

| low-traffic | 33.3% | 7.4% | 7.4% | 8.1% |

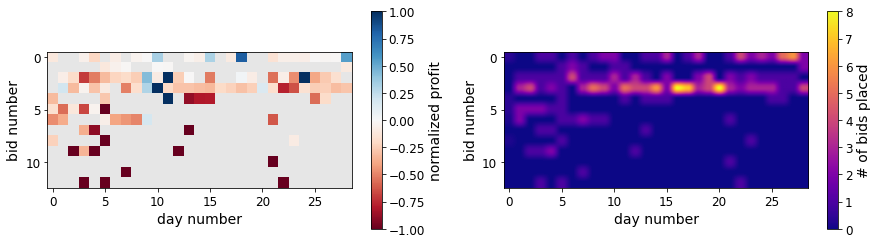

High-traffic products: profitable sample

Figure 4 illustrates individual behavior of profit and bid placement for 3 different products. We can clearly see that policies concentrate around the optimal bid value exploring other options from time to time. These examples demonstrate a meaningful learning behavior by spending the budget more efficiently and optimizing bids for maximum profitability.

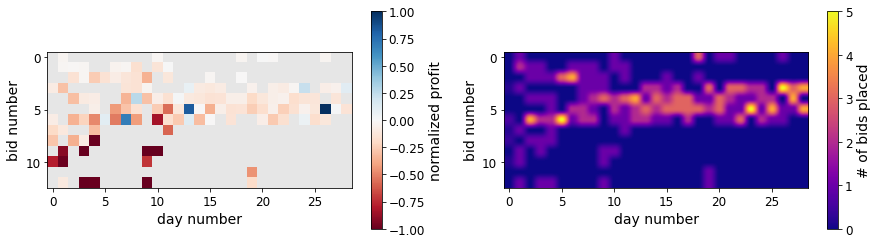

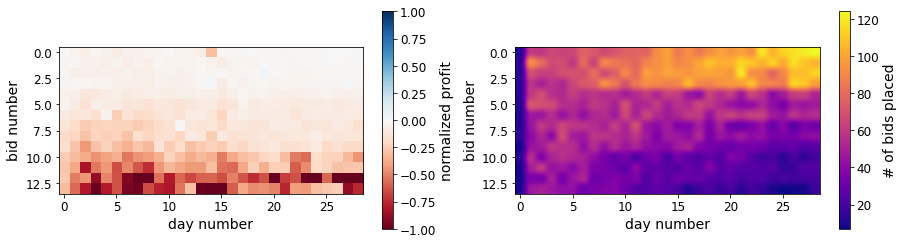

High-traffic products: unprofitable sample

Unlike the profitable sample, products from the unprofitable sample follow the same pattern, and it is easier to visualize them on an aggregated level. Figure 5 shows the profit (left) and the bids placement (right) heatmaps aggregated over 97 products from the unprofitable sample. We can see that the aggregated policy strongly concentrates around lower bid values due to the high unprofitability of the higher bid values. While this is a desired behavior, this shift to lower bid values does not seem to be as profitable as in the example before, suggesting that this sample contributes to increasing profitability mostly due to the lowering costs.

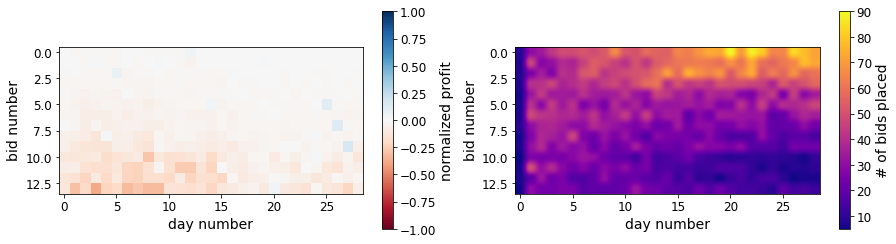

Low traffic products

Lastly, we return to the low-traffic products, which include 60 products (33%) with the lowest number of clicks in January. Heatmaps for the low-traffic group (Figure 6) illustrate similar behavior to what we saw in the unprofitable sample behavior. Nevertheless, we emphasize that the low-traffic products have very little data, which might suggest that, due to the low exploration, the algorithm switched to lower bid values a little bit early and could have given more chance to high bid values in this case. This group requires fine-tuning of the hyperparameters and further monitoring.

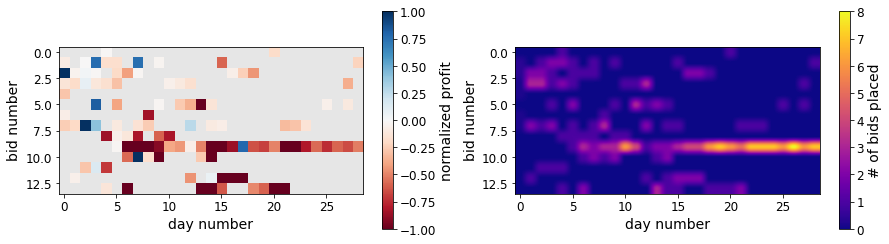

5.2 Example of counterintuitive behavior

One product from the profitable sample demonstrates counterintuitive behavior, which deserves special attention. As we can see in Figure 7, after starting with lower bid values, it switched to higher bid values on days 5-6. Intuitively, we would expect the policy to switch back after it verifies that higher bid values performing worse, but this is not happening. Instead, it chooses an unprofitable bid more intensively, and things get even worse.

The answer to this behavior lies in the update rule (6). According to (6), the incremental score gain at round

| (8) |

is equal to 1 for bids that were not placed to encourage exploration and is equal to for a placed bid to punish bids for poor performance. The latter is a loss-driven mechanism that might take values in depending on the values of and . There are two intermediate conclusions can be made: (1) due to the loss-driven approach, bids that were not placed in a round never get punished more than the bid that was placed in that round, no matter how well it performed, and (2) due to importance-weighted sampling, bids with low probabilities experience more severe punishment than bids with high probabilities for providing the same reward value.

Both these observations are theoretically reasonable. However, in combination with Reward sparsity, it led to a snowballing effect of being unreasonably confident in bids that did not happen to be placed at the very beginning. Indeed, because of observation 1, higher bid values (that the model didn’t place for the first 5-6 days) appeared more appealing as other bids experienced some punishment. Next, because of observation 2, the higher bids were flourishing, perhaps even producing worse outcomes, as other bids had a lower probability.

Although theoretically the system will eventually recover from such behavior, it highlights the risk associated with the algorithm in environments with sparse rewards due to the sensitivity of the learning behavior. At the beginning of the live test, the learning rate parameter was misspecified with respect to reward sparsity. This led to a high sensitivity of the learning system, such that omitting placing a bid for 1-2 days resulted in a massive degeneration of policies. That was the reason for the test reset and the learning rate decrease.

6 Discussion and further work

One challenge that our solution does not address directly relates to the sparse reward signal. We have seen that the same reward definition led to conceptually different behaviors for various products/groups of products, making the system highly susceptible to imbalances between exploration and exploitation. Moreover, the marketing nature and the blackbox auction mechanism further complicate the problem due to the low conversion rate and complex reward structure.

A potential solution to deal with the reward sparsity issue is to compensate for it by exploring more aggressively. Different methods exist to achieve this, such as decreasing the learning rate, using EXP3-IX algorithm [34], or mixing policies with uniform distribution. However, we believe that these remedies only mitigate the snowballing effect and do not completely solve it. As we discussed in Sections 5.1 and 5.2, the sparse reward signal can cause the system to exhibit trivial behavior or destabilize the system at all.

We believe the essence of the problem lies in the loss-driven update rule (6). More precisely, in environments where the positive outcomes are gems, the system should distinguish between punishment for losses and encouragement due to lack of exploration. But in reality, these outcomes are taken for granted. While this line of thought has something in common with the reward shaping techniques, which usually require additional hand-crafted reward functions, it is highly unclear how to extend these techniques to the auction domain. Somewhat surprisingly, this issue remains unaddressed in the theoretical literature, nor are practical approaches known.

Alternatively, one can overcome the reward sparsity issue by modeling the reward signal. That is, instead of waiting for the true outcome to appear, one could substitute it with an approximation modeled by an independent supervised learning module, which, in its term, is trained based on the true outcome with delay . If an accurate enough approximation can be developed, this method can mitigate two limitations of our current approach, which include a large number of products and a long delay . While the larger values of can be modeled as context using approximate valuation (as suggested in [7, 30]), the delay should not be as critical for supervised learning as it is for reinforcement learning. Studying how to integrate these two modules is an interesting direction for future work.

7 Conclusion

In this paper, we introduced a systematic solution to learning optimal bidding strategies in a complex auction problem. Our solution relies on the adversarial bandit framework: to optimize the exploration-exploitation trade-off by maintaining empirical importance-weighted rewards of the actions. Alternatively to classical bandit algorithms that rely on immediate online feedback, the developed Batch EXP3 is robust to batched and delayed feedback. The theoretical appeal of our solution can be motivated by the relationship of Batch EXP3 to the classical EXP3 algorithm. We have outlined the theoretical guarantees of the underlying algorithm in Theorem 3.

On the deployment side, we introduced a bidding architecture that complements the RL techniques. Although the technical infrastructure was heavy and incorporated the non-trivial implementation of the clicks attribution pipeline, the practical appeal of our solution is motivated by its computational advantages: the resulting system is computationally efficient, reliable, and debuggable. Furthermore, it can be readily applied to many more contextual decision problems.

Our solution has demonstrated its effectiveness in increasing the partial profit at the group level. Additionally, our system optimizes bids for maximum profitability at the product level, particularly for a group of high-traffic products. However, we acknowledge that finer tuning is needed for low-traffic products. Overall, the live test has yielded promising results indicating that many real-life challenges can be addressed pragmatically within a reinforcement learning system.

Acknowledgments

We wish to thank Joshua Hendinata and Aleksandr Borisov for their engineering support. Furthermore, we would like to thank Amin Jamalzadeh, head of the Traffic Platform Applied Science and Analytics at Zalando, for guidance, support with administrative processes related to the project, and the review of the final draft. Danil Provodin would like to thank Maurits Kaptein and Mykola Pechenizkiy, whose thoughts influenced his ideas.

References

- [1] Michelle Morgan. Bid management tools, 2023. Accessed on March 10, 2023.

- [2] Peter Auer, Nicolò Cesa-Bianchi, Yoav Freund, and Robert E. Schapire. The nonstochastic multiarmed bandit problem. SIAM Journal on Computing, 32(1):48–77, 2002.

- [3] Google. Auction, 2023. Accessed on March 10, 2023.

- [4] Google. About ad rank, 2023. Accessed on March 10, 2023.

- [5] Jason D. Hartline and Tim Roughgarden. Simple versus optimal mechanisms. In Proceedings of the 10th ACM Conference on Electronic Commerce, EC ’09, page 225–234, New York, NY, USA, 2009. Association for Computing Machinery.

- [6] Hu Fu, Jason Hartline, and Darrell Hoy. Prior-independent auctions for risk-averse agents. In Proceedings of the Fourteenth ACM Conference on Electronic Commerce, EC ’13, page 471–488, New York, NY, USA, 2018. Association for Computing Machinery.

- [7] Yanjun Han, Zhengyuan Zhou, and Tsachy Weissman. Optimal no-regret learning in repeated first-price auctions, 2020.

- [8] Yanjun Han, Zhengyuan Zhou, Aaron Flores, Erik Ordentlich, and Tsachy Weissman. Learning to bid optimally and efficiently in adversarial first-price auctions, 2020.

- [9] Zhe Feng, Chara Podimata, and Vasilis Syrgkanis. Learning to bid without knowing your value. Proceedings of the 2018 ACM Conference on Economics and Computation, 2018.

- [10] Claire Vernade, Olivier Cappé, and Vianney Perchet. Stochastic bandit models for delayed conversions. In Proceedings of the 2017 Conference on Uncertainty in Artificial Intelligence, page 1–10, 2017.

- [11] Danil Provodin, Pratik Gajane, Mykola Pechenizkiy, and Maurits Kaptein. The impact of batch learning in stochastic linear bandits. In IEEE International Conference on Data Mining, ICDM 2022, Orlando, FL, USA, November 28 - Dec. 1, 2022, pages 1149–1154.

- [12] Kelly Zhang, Lucas Janson, and Susan Murphy. Inference for batched bandits. In Advances in Neural Information Processing Systems, volume 33, pages 9818–9829, 2020.

- [13] Roger B. Myerson. Optimal auction design. Mathematics of Operations Research, 6(1):58–73, 1981.

- [14] John G. Riley and William F. Samuelson. Optimal auctions. The American Economic Review, 71(3):381–392, 1981.

- [15] Robert B. Wilson. Competitive bidding with disparate information. Management Science, 15(7):446–448, 1969.

- [16] Robert B. Wilson. Game-theoretic analysis of trading processes. 1985.

- [17] Jonathan Weed, Vianney Perchet, and Philippe Rigollet. Online learning in repeated auctions. In 29th Annual Conference on Learning Theory, volume 49 of Proceedings of Machine Learning Research, pages 1562–1583, Columbia University, New York, New York, USA, 23–26 Jun 2016. PMLR.

- [18] Nicolò Cesa-Bianchi, Claudio Gentile, and Yishay Mansour. Regret minimization for reserve prices in second-price auctions. IEEE Transactions on Information Theory, 61(1):549–564, 2015.

- [19] Shuchi Chawla, Jason Hartline, and Denis Nekipelov. Mechanism design for data science. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, EC ’14, page 711–712, New York, NY, USA, 2014. Association for Computing Machinery.

- [20] Kareem Amin, Rachel Cummings, Lili Dworkin, Michael Kearns, and Aaron Roth. Online learning and profit maximization from revealed preferences. In Proceedings of the Twenty-Ninth AAAI Conference on Artificial Intelligence, AAAI’15, page 770–776, 2015.

- [21] Avrim Blum, Yishay Mansour, and Jamie Morgenstern. Learning valuation distributions from partial observations. In Proceedings of the Twenty-Ninth AAAI Conference on Artificial Intelligence, AAAI’15, page 798–804, 2015.

- [22] Mehryar Mohri and Andres Munoz Medina. Learning theory and algorithms for revenue optimization in second price auctions with reserve. In Proceedings of the 31st International Conference on Machine Learning, volume 32 of Proceedings of Machine Learning Research, pages 262–270, Bejing, China, 22–24 Jun 2014. PMLR.

- [23] Kareem Amin, Afshin Rostamizadeh, and Umar Syed. Repeated contextual auctions with strategic buyers. In Advances in Neural Information Processing Systems, volume 27, 2014.

- [24] R. Preston McAfee. The design of advertising exchanges. Review of Industrial Organization, 39(3):169–185, 2011.

- [25] Han Cai, Kan Ren, Weinan Zhang, Kleanthis Malialis, Jun Wang, Yong Yu, and Defeng Guo. Real-time bidding by reinforcement learning in display advertising. In Proceedings of the Tenth ACM International Conference on Web Search and Data Mining, WSDM ’17, page 661–670, New York, NY, USA, 2017. Association for Computing Machinery.

- [26] Di Wu, Xiujun Chen, Xun Yang, Hao Wang, Qing Tan, Xiaoxun Zhang, Jian Xu, and Kun Gai. Budget constrained bidding by model-free reinforcement learning in display advertising. CIKM ’18, page 1443–1451, New York, NY, USA, 2018. Association for Computing Machinery.

- [27] Mengjuan Liu, Jinyu Liu, Zhengning Hu, Yuchen Ge, and Xuyun Nie. Bid optimization using maximum entropy reinforcement learning. Neurocomputing, 501:529–543, 2022.

- [28] Mengjuan Liu, Li Jiaxing, Zhengning Hu, Jinyu Liu, and Xuyun Nie. A dynamic bidding strategy based on model-free reinforcement learning in display advertising. IEEE Access, 8:213587–213601, 2020.

- [29] Arthur Flajolet and Patrick Jaillet. Real-time bidding with side information. In Advances in Neural Information Processing Systems, volume 30, 2017.

- [30] Wei Zhang, Yanjun Han, Zhengyuan Zhou, Aaron Flores, and Tsachy Weissman. Leveraging the hints: Adaptive bidding in repeated first-price auctions, 2022.

- [31] Vianney Perchet, Philippe Rigollet, Sylvain Chassang, and Erik Snowberg. Batched bandit problems. In Proceedings of The 28th Conference on Learning Theory, volume 40 of Proceedings of Machine Learning Research, pages 1456–1456, Paris, France, 03–06 Jul 2015. PMLR.

- [32] Google. Maximum cpc bid: Definition, 2023. Accessed on March 10, 2023.

- [33] Mathias Deschamps, Anael Quevrin, and Stefan Haase. On the effectiveness of online marketing, 2019. Accessed on March 20, 2023.

- [34] Tomáš Kocák, Gergely Neu, Michal Valko, and Remi Munos. Efficient learning by implicit exploration in bandit problems with side observations. In Advances in Neural Information Processing Systems, volume 27, 2014.