High Probability and Risk-Averse Guarantees

for a Stochastic Accelerated Primal-Dual Method

Abstract

We consider stochastic strongly-convex-strongly-concave (SCSC) saddle point (SP) problems which frequently arise in applications ranging from distributionally robust learning to game theory and fairness in machine learning. We focus on the recently developed stochastic accelerated primal-dual algorithm (SAPD), which admits optimal complexity in several settings as an accelerated algorithm. We provide high probability guarantees for convergence to a neighborhood of the saddle point that reflects accelerated convergence behavior. We also provide an analytical formula for the limiting covariance matrix of the iterates for a class of stochastic SCSC quadratic problems where the gradient noise is additive and Gaussian. This allows us to develop lower bounds for this class of quadratic problems which show that our analysis is tight in terms of the high probability bound dependency to the parameters. We also provide a risk-averse convergence analysis characterizing the “Conditional Value at Risk”, the “Entropic Value at Risk”, and the -divergence of the distance to the saddle point, highlighting the trade-offs between the bias and the risk associated with an approximate solution obtained by terminating the algorithm at any iteration.

1 Introduction

We consider strongly convex/strongly concave (SCSC) saddle point problems of the form:

| (1.1) |

where and are finite-dimensional Euclidean spaces, and are closed convex functions, and is a smooth convex-concave function such that is strongly convex in and strongly concave in , i.e., SCSC – see Assumption 1 for details. Throughout the paper, we assume that and are strongly convex; since is SCSC, we emphasize that this assumption is without loss of generality as strong convexity/concavity can be transferred from to and by adding and subtracting simple quadratics.

Such saddle point (SP) problems arise in many applications and different contexts. In unconstrained and constrained optimization problems, saddle-point formulations arise naturally when the problems are reformulated as a minimax problem based on the Lagrangian duality. Furthermore, the SP formulation in (1.1) encompasses many key problems such as robust optimization (Ben-Tal et al., 2009) – here is selected to be the indicator function of an uncertainty set from which nature (adversary) picks an uncertain model parameter , and the objective is to choose that minimizes the worst-case cost , i.e., a two-player zero-sum game. Other applications involving SCSC problems include but are not limited to supervised learning with non-separable regularizers (where may not be bilinear) (Palaniappan and Bach, 2016), fairness in machine learning (Liu et al., 2022), unsupervised learning (Palaniappan and Bach, 2016) and various image processing problems, e.g., denoising, (Chambolle and Pock, 2011).

In this work, we are interested in SCSC problems where the partial gradients and are not deterministically available; but, instead we postulate that their stochastic estimates and are accessible. Such a setting arises frequently in large-scale optimization and machine learning applications where the gradients are estimated from either streaming data or from random samples of data (see e.g. (Zhu et al., 2023; Gürbüzbalaban et al., 2022; Bottou et al., 2018)). First-order (FO) methods that rely on stochastic estimates of the gradient information have been the leading computational approach for computing low-to-medium-accuracy solutions for these problems because of their cheap iterations and mild dependence on the problem dimension and data size. In this paper, our focus will be on first-order primal-dual algorithms that rely on stochastic gradient estimates for solving (1.1).

Existing relevant work.

Stochastic primal-dual algorithms for solving SP problems generate a sequence of primal and dual iterate pairs starting from an initial point . Two popular metrics to assess the quality of a random solution returned by a stochastic algorithm are the expected gap and the expected squared distance defined as

| (1.2) |

respectively, where denotes the unique saddle point of (1.1), due to the strong convexity of and . The iteration complexity of FO-methods in these two metrics depend naturally on the block Lipschitz constants , , and , i.e., Lipschitz constants of , , and as well as on the strong convexity constants and of the functions and . In particular, Fallah et al. (2020) show that a multi-stage variant of Stochastic Gradient Descent Ascent (SGDA) algorithm generates such that within gradient oracle calls, where , while and are bounds on the variance of the stochastic gradients and , respectively; and are the worst-case strong convexity and Lipschitz constants and is defined as the condition number. SGDA analyzed in (Fallah et al., 2020) consists of Jacobi-type updates in the sense that stochastic gradient descent and ascent steps are taken simultaneously. Jacobi-type updates are easier to analyze than Gauss-Seidel updates in general, and can be viewed as solving a structured variational inequality (VI) problem, for which there are many existing techniques that directly apply, e.g., (Gidel et al., 2018; Chen et al., 2017). Zhang et al. (2022) consider deterministic SCSC problems, when gradient descent ascent (GDA) with Gauss-Seidel-type updates is considered, i.e., the primal and dual variables are updated in an alternating fashion using the most recent information obtained from the previous update step. Their results show that an accelerated asymptotic convergence rate, i.e., iteration complexity scales linearly with instead of , can be obtained for the Gauss-Seidel variant of GDA. However, as discussed in (Zhang et al., 2022), this comes with the price that Gauss-Seidel style updates greatly complicate the analysis because every iteration of an alternating algorithm is a composition of two half updates. Furthermore, extending the acceleration result to non-asymptotic rates requires using momentum terms in either the primal or the dual updates, and this further complicates the convergence analysis. Fallah et al. (2020) also considered using momentum terms both in the primal and dual updates, and show that the multi-stage Stochastic Optimistic Gradient Descent Ascent (OGDA) algorithm using Jacobi-type updates achieves an iteration complexity of in expected squared distance. There are also several other algorithms that can achieve the accelerated rate, i.e., has the coefficient instead of - see, e.g. (Beznosikov et al., 2022). We call this term that depend on the condition number as initialization bias since it captures how fast the error due to initial conditions decay and reflects the behavior of the algorithm in the noiseless setting. Among the algorithms that achieve an accelerated rate, the most closely related work to ours is (Zhang et al., 2023) which develops a stochastic accelerated primal-dual (SAPD) algorithm with Gauss-Seidel type updates. SAPD using a momentum acceleration only in the dual variable can generate such that within iterations; this result implies in expected squared distance. This complexity is optimal for bilinear problems. To our knowledge, SAPD is also the fastest single-loop algorithm for solving stochastic SCSC problems in the form of (1.1) that are non-bilinear. Furthermore, using acceleration only in one update, as opposed to in both variables (Fallah et al., 2020), leads to smaller variance accumulation (see Zhang et al. (2023) for more details).

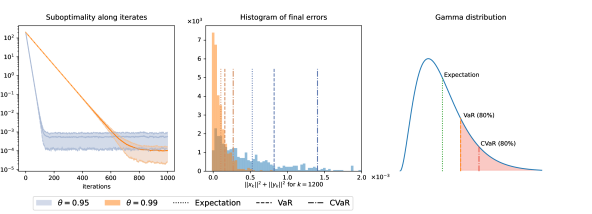

While the aforementioned results provide performance guarantees in expectation based on the metrics defined in (1.2) and their variants, unfortunately having guarantees in these metrics do not allow us to control tail events, i.e., the expected gap and distance can be smaller than a given target threshold ; but, the iterates can still be arbitrarily far away from the saddle point with a non-zero probability. In this context, high probability guarantees are key in the sense that they allow us to control tail probabilities and quantify how many iterations are needed for the iterates to be in a neighborhood of the saddle point with a given probability level . This is illustrated on the right panel of Figure 1 where we run the SAPD algorithm for two different values of the momentum parameter and for a toy problem with strong convexity parameters admitting a saddle point at . SAPD is initialized at , primal and dual stepsizes are chosen according to the Chambolle-Pock parametrization as suggested in (Zhang et al., 2023). For simplicity, the stochastic gradients and are set to and perturbed with additive i.i.d. Gaussian noise, and we assume that and are independent from each other and also from the past history of the algorithm. For each parameter choice, we run SAPD for 500 runs, and for iterations for every run –see Figure 1 (Left), and plot the distribution of the squared distance of to the unique saddle point , i.e., , in Figure 1 (Middle). As we can see, the random error can take significantly larger values than its expectation . This motivates estimating the -th quantile of the error , which is also called the value at risk at level , traditionally abbreviated as in the financial literature. While represents a worst-case error associated with a probability , it does not capture the behavior if that worst-case threshold is ever crossed. Conditional value at risk (CVaR) at level , on the other hand, is an alternative risk measure that can be used characterizing the expected error if that worst-case threshold is ever crossed. CVaR is in fact a coherent risk measure with some desirable properties (Rockafellar and Royset, 2013). In Fig. 1(Middle), we report and for and . We can see that and capture the tail behavior better compared to expectation. Similar behavior can be seen on other distributions, e.g., in Figure 1(Right), we illustrate the expectation, , i.e., -th quantile, and of a gamma-distributed random variable with shape parameter , and scale parameter corresponding to . We see that estimates the average of the tails after the -th quantile; therefore, it is useful for capturing the average risk associated to tail events beyond the -th quantile. In addition to CVaR, there are also other coherent risk measures such as entropic value at risk (EVaR) and -divergence which have been of interest in the study of stochastic optimization algorithms as they can provide risk-averse guarantees capturing the worst-case tail behavior and deviations from the mean performance (Can and Gürbüzbalaban, 2022).

While high-probability guarantees (VaR guarantees) and risk guarantees in terms of risk measures such as CVaR and EVaR are available in the optimization setting for the iterates of stochastic gradient descent-like methods (Harvey et al., 2019; Rakhlin et al., 2012; Davis and Drusvyatskiy, 2020; Can and Gürbüzbalaban, 2022), results in a similar nature are considerably more limited in the SP setting. Among existing results, Juditsky et al. (2011) obtained high-probability guarantees for the stochastic mirror-prox algorithm for solving stochastic VIs with Lipschitz and monotone operators. This algorithm can be used to solve smooth stochastic convex/concave SP problems (which corresponds to the case with being smooth, convex in and concave in ) and implies that with probability , after iterations, the gap metric for the VI will be bounded by assuming that the domain is bounded and the stochastic gradient noise is light-tailed with a sub-Gaussian distribution. In (Gorbunov et al., 2022), it is shown that the same high-probability results as in (Juditsky et al., 2011) can be attained by clipping the gradients properly without the sub-Gaussian and bounded domain assumptions. In another line of work (Yan et al., 2020), it is shown for the SGDA algorithm that the expected gap with probability at least after oracle calls for possibly non-smooth SCSC problems. Also, in (Wood and Dall’Anese, 2022), high probability bounds are given for online algorithms applied to stochastic saddle point problems where the objective is time-varying and is revealed in a sequential manner, and the data distribution over which stochastic gradients are estimated depends on the decision variables. However, these high-probability guarantees are obtained for non-accelerated algorithms with Jacobi-style updates; therefore, the high probability bounds do not exhibit accelerated decay of the initialization bias, and scale as , i.e., quadratically with the condition number , instead of a linear scaling. Also, to our knowledge, high-probability bounds for SP algorithms with Gauss-Seidel style updates are not available in the literature even if they do not incorporate momentum, see e.g. the survey by Beznosikov et al. (2022)). Similarly, we are not aware of any risk guarantees (in terms of CVaR and EVaR of the performance metric over iterations) for any primal-dual algorithm for solving stochastic SP problems.

Contributions.

In this paper, we present a risk-averse analysis of the SAPD method (Zhang et al., 2023) to solve saddle point problems of the form (1.1). A key novelty of our work lies in providing the first analysis of an accelerated algorithm for SCSC problems with high probability guarantees, where our bounds reflect the accelerated decay of the initialization bias scaling linearly with the condition number . More specifically, our high-probability bounds provided in Section 3 imply that given target accuracy , SAPD, with a proper choice of parameters that we explicit, can generate a solution that satisfies with probability after

|

|

(1.3) |

iterations where . When the partial gradients and are continuously differentiable (which is the case for bilinear problems and for many SCSC problems arising in practice (Zhang et al., 2023; Palaniappan and Bach, 2016; Chambolle and Pock, 2011)), then we can take (as discussed in Remark 9) and the complexity (1.3) simplifies to

hiding constants depending on the initialization. Simplifying the terms further, this implies iterations are sufficient where . To achieve this, under a light-tail (subGaussian) assumption for the norm of the gradient noise, we develop concentration inequalities tailored to the specific Gauss-Seidel structure of SAPD. In particular, the Gauss-Seidel type updates and the use of a momentum term complicate the analysis significantly where the evolution of the iterates and the performance metric over the iterations need to be studied with respect to a non-standard filtration for having the right measurability properties (as discussed in Section 5.2 in detail). A crucial step for the development of these results is a new Lyapunov function we construct that has favorable contraction properties. To our knowledge, these are the first high-probability guarantees for a SP algorithm with Gauss-Seidel style updates and first high-probability guarantees that are accelerated in the sense that the dependency of the iteration complexity to the initialization bias scales linearly with the condition number . We also provide finite-time risk guarantees, where we measure the risk in terms of the CVaR, EVaR and -divergence of the distance to the saddle point. In addition, we provide an in-depth analysis of the behavior of SAPD on a class of quadratic problems subject to i.i.d. isotropic Gaussian noise where we can characterize the behavior of the distribution of the iterates explicitly. In particular, we derive an analytical formula for the limiting covariance matrix of SAPD’s iterates, which demonstrates the tightness of our high probability bounds with respect to several parameter choices in SAPD. To our knowledge, these are the first risk-averse guarantees that quantify the risk associated with an approximate solution generated by a primal-dual algorithm for SP problems.

Notations.

Throughout this manuscript, and denote finite dimensional vector spaces equipped with the Euclidean norm , and . We adopted for positive integers and . For , we denote the vector composed of the vertical concatenation of the columns of , and the Kronecker product of and . We let denote the spectral norm of and let denote the spectral radius of , i.e., the largest modulus of the eigenvalues of . For a finite sequence of reals (resp. matrices ), we denote (resp. ) the associated (block) diagonal matrix. If is diagonalizable, denotes the set of the eigenvalues of . For any convex set , denotes the indicator function of , i.e., if , and equal to otherwise. For a given proper, closed and convex function , denotes the associated proximal operator: . We use the Landau notation to describe the asymptotic behavior of functions. That is, for , a function in a neighborhood of if as , whereas if there exist a positive constant such that in some neighborhood of . Similarly, we say , if and . Given random vectors for , we let if converges in distribution to another random vector .

2 Preliminaries and Background

2.1 Stochastic Accelerated Primal-Dual (SAPD) Method

SAPD, displayed in Algorithm 1, is a stochastic accelerated primal-dual method developed in (Zhang et al., 2023) which uses stochastic estimates and of the partial gradients and . SAPD extends the accelerated primal-dual method (APD) proposed in (Hamedani and Aybat, 2021) to the stochastic setting, which itself is an extension of the Chambolle-Pock (CP) method developed for bilinear couplings . Given primal and dual stepsizes and and a number of iterations , SAPD applies momentum averaging to the partial gradients with respect to the dual variable, and updates the primal and the dual variables in an alternating fashion computing proximal-gradient steps.

The high-probability convergence guarantees of SAPD derived in this paper rely on several standard assumptions on , , , and the noisy estimates and of the partial gradients of . The first assumption on the smoothness properties of the coupling function is standard for first-order methods (see e.g.. (Mokhtari et al., 2020; Gidel et al., 2018; Zhang et al., 2021)).

Assumption 1.

and are strongly convex with convexity modulii , respectively; and is continuously differentiable on an open set containing such that

-

(i)

is convex on , for all ;

-

(ii)

is concave on , for all ;

-

(iii)

there exist and such that

for all .

By strong convexity/strong concavity of from Assumption 1, the problem in (1.1) admits a unique saddle point which satisfies

| (2.1) |

Following the literature on stochastic saddle-point algorithms (Nemirovski et al., 2009; Juditsky et al., 2011; Chen et al., 2017), we assume that only (noisy) stochastic estimates of the partial gradients are available, where are random variables that are being revealed sequentially. Specifically, we let , be two sequences of random variables revealed in the following order in time which is the natural order for the SAPD updates:

and we let and denote the associated filtrations, i.e., is the sigma algebra generated by the random variable , and

For any , we introduce the following random variables to represent the gradient noise:

Often times, stochastic gradients are assumed to be unbiased with a bounded variance conditional on the history of the iterates. Such an assumption is standard in the study of stochastic optimization algorithms and stochastic approximation theory (Harold et al., 1997) and frequently arises in the context of stochastic gradient methods that estimate the gradients from randomly sampled subsets of data (Bottou et al., 2018).

Assumption 2.

For any , there exists scalars such that

Under Assumptions 1 and 2, given a set of parameters , SAPD iterates were shown to converge to a neighborhood of the solution linearly in expectation where the size of the neighborhood gets smaller when the gradient noise levels gets smaller (Zhang et al., 2023); in particular, in the absence of noise (when ), the iterates converges to at a linear rate provided that there exists some for which the following inequality holds:

| (2.2) |

An important class of solutions to the matrix inequality in (2.2) takes the following form: Given an arbitrary , choose

| (2.3) |

for some explicitly given in (Zhang et al., 2023, Corollary 1) – satisfying (2.3) solves (2.2) with and with . SAPD generalizes the primal-dual algorithm CP proposed in (Chambolle and Pock, 2011) – CP algorithm can solve SP problems with a bilinear coupling function when a deterministic first-order oracle for exists; indeed, for bilinear coupling functions with deterministic first-order oracles, SAPD reduces to the CP algorithm. It is shown in (Chambolle and Pock, 2011) that for a particular value111see (Chambolle and Pock, 2011, Eq.(48)). of , the choice of primal and stepsizes according to (2.3) achieves acceleration of the CP algorithm proposed in (Chambolle and Pock, 2011). For SAPD, Zhang et al. (2023) study the squared distance of iterates to the saddle point in expectation and extends the same acceleration result to the case when is not bilinear and when one has only access to a stochastic first-order oracle rather than a deterministic one.

As we focus on SCSC problems, we can rely on the squared distance of the iterates to the solution to quantify sub-optimality. Precisely, sub-optimality will be measured in terms of a weighted squared distance to the solution, i.e.,

| (2.4) |

for some . This weighted metric turns out to be more convenient for the convergence analysis of SAPD, but it is clearly equivalent to the unweighted squared distance up to a constant that depends on the choice of . For the sake of completeness of the paper, we first recall the convergence of SAPD in expected weighted squared distance, established in (Zhang et al., 2023).

Theorem 1 ((Zhang et al., 2023), Theorem 1).

As stated above, the convergence of SAPD in expected squared distance presents the classical bias-variance trade-off, which can be controlled through adjusting the SAPD parameter choice. The bias term , captures the rate at which the error due to initialization (bias) decays, ignoring the noise. It is shown in (Zhang et al., 2023) that for certain choice of parameters, convergence of initialization bias to occurs at an accelerated rate instead of the non-accelerated rate of methods such as (Jacobi-style) SGDA. The variance term constitutes the (remaining part) second term at the right-hand side of (2.5) and is due to noise accumulation that scales with the stepsize and the noise variance. For a particular choice of SAPD parameters, it is shown that SAPD exhibits an optimal complexity in expectation, up to logarithmic factors, and achieves an accelerated decay rate for the bias term; however, in a number of risk-sensitive situations, convergence in expectation can prove to be insufficient. In this paper, we further investigate the properties of SAPD for several measures of risks, that we detail in Section 2.3.

2.2 Assumptions on the gradient noise

Although according to Theorem 1, (2.2) describes a general set of parameters for which SAPD will admit guarantees in terms of the expected weighted distance squared to the solution, risk-sensitive guarantees for SAPD, including high-probability bounds are not known. In the forthcoming sections, we study SAPD for parameters satisfying (2.2), and we obtain convergence guarantees in high probability, in , in , and also in the -divergence-based risk measures, which are properly defined in Section 2.3. In other words, our focus here is to obtain high probability guarantees as well as bounds on the risk associated with . To this end, we will make a “light-tail" assumption on the magnitude of the gradient noise adopting a subGaussian structure. Before giving our assumption on the gradient noise precisely, we start with introducing the family of norm-subGaussian random variables, and recall their basic properties.

Definition 2.1.

A random vector is norm-subGaussian with proxy , denoted by , if we have .

Random vectors with Norm-subGaussian distribution were introduced in (Jin et al., 2019), and encompass a large class of random vectors including subGaussian random vectors. First, note that given an arbitrary and a random variable such that for some , we immediately have the following implication:

| (2.6) |

For instance, is norm-subGaussian when is subGaussian, or it is bounded, i.e., such that with probability . As discussed in (Jin et al., 2019, Lemma 3), the squared norm of a norm-subGaussian vector admits a sub-Exponential distribution, which is defined next.

Definition 2.2.

A random variable is subExponential with proxy if it satisfies

In particular, if we take for with , then, the following result shows that is subExponential with proxy .

Lemma 2.

Let be such that . Then, for any ,

| (2.7) |

Lemma 3.

Let such that . Then, for any and , it holds that .

For completeness, the proofs of these two elementary results are provided in Section A.1 of the appendix. Next, we will introduce an assumption which says that gradient noise terms and are light-tailed admitting a norm-subGaussian structure when conditioned on the natural filtration of the past iterates.

Assumption 3.

For any the random variables and are conditionally unbiased and norm-subGaussians with respective proxy parameters . More precisely, for all , we have and

We note that such subGaussian noise assumptions are common in the study of stochastic optimization algorithms (Rakhlin et al., 2012; Ghadimi and Lan, 2012; Harvey et al., 2019). In machine learning applications, where stochastic gradients are often estimated on sampled batches, noisy estimates typically behave Gaussian for moderately high sample sizes, as a consequence of the central limit theorem (Panigrahi et al., 2019). Furthermore, there are applications in data privacy where i.i.d. subGaussian noise is added to the gradients for privacy reasons (Levy et al., 2021; Varshney et al., 2022). In such settings, we expect Assumption 3 to hold naturally. In the rest of the paper, together with Assumption 1, we will assume that Assumption 3 holds in lieu of Assumption 2.

2.3 VaR, CVaR, EVaR and -divergences

For any given , to quantify the risk associated with , i.e., the distance to the unique saddle point, we will resort to -divergence-based risk measures borrowed from the risk measure theory (Ben-Tal and Teboulle, 2007), including , and -divergence. The first risk measure of interest is the quantile function, also known as value at risk, defined for any random variable as

Quantile upper bounds correspond to high-probability results, which have been already fairly studied to assess the robustness of stochastic algorithms (Ghadimi and Lan, 2012; Rakhlin et al., 2012; Harvey et al., 2019). One key contribution of this paper is the derivation of an upper bound on the quantiles of the weighted distance metric , defined in (2.4), such that this upper bound exhibits a tight bias-variance trade-off –see Section 4.2.

Furthermore, we investigate the robustness of SAPD with respect to three convex risk measures based on -divergences (Ben-Tal and Teboulle, 2007). Generally speaking, for a given proper convex function satisfying and , the associated -divergence, is defined as , for any input probability measures such that , i.e., is absolutely continuous with respect to . Different choices of -divergence result in different risk measures as discussed next.

Definition 2.3.

For any , the -divergence based risk measure at level is defined as

| (2.8) |

where denotes an arbitrary reference probability measure.

We refer the reader to (Ben-Tal and Teboulle, 2007; Shapiro, 2017) for more on -divergence based risk measures. In this paper, we investigate the performances of SAPD under three -divergence based risk measures, summarized in Table 2.3.

| o X[c] X[c] X[c] Risk measure | Formulation | Divergence |

| , | ||

| , | ||

| , |

First, given , we consider the conditional value at risk at level , i.e., , defined as

| (2.9) |

The CVaR measure admits the variational representation (2.8) with for any . As an average of the higher quantiles of , holds intuitively as a statistical summary of the tail of , beyond its -quantile. While high-probability bounds do not take into account the price of failure tied to the event , the CVaR presents the advantage of averaging the whole tail of the distribution; therefore, it can quantify the risk associated with tail events in a robust fashion.

The second convex risk measure we investigate is the Entropic Value at Risk (Ahmadi-Javid, 2012), denoted , and is defined as . The admits the variational representation (2.8) with and the parameter is set to for given –see e.g. (Shapiro, 2017). exhibits a higher tail-sensitivity than , in the sense that for all whenever . Finally we will also derive results in terms of the -divergence based risk measure, defined as (2.8) with .

3 Main Results

In this section, we present the main results of this paper, which consists of convergence analysis of SAPD in high-probability and provide guarantees in terms of the three convex risk measures presented in Table 2.3. Later in Section 4, we derive analytical expressions related to convergence behavior of SAPD applied on quadratic SP problems, and in Section 4.2 we discuss some tight characteristics of our main results provided in this section. Finally, in Section 5, we provide the proofs of our main result stated in Theorem 4.

Theorem 4.

Suppose Assumption 1 and Assumption 3 hold. Given and satisfying (2.2) for some and , let denote the corresponding SAPD iterates, initialized at an arbitrary tuple . For all , , it holds that

| (3.1) |

| (3.2) |

where , , and for depend only on the algorithm parameters ( and the problem parameters . Furthermore, all these constants can be made explicit222These constants are explicitly given within the proof, provided in Section 5. and in particular, under the CP parameterization in (2.3), they satisfy , , and for all , as , which implies that

Proof.

The proof is provided in Section 5.2.1. ∎

Remark 6.

For any given , to check if there exists SAPD parameters such that the bias component of decreases to linearly with a rate coefficient bounded above by , one needs to solve a 5-dimensional SDP, i.e., after fixing , checking the feasibility of (2.2) reduces to an SDP problem, see (Zhang et al., 2023) for details. Below in Corollary 5, we provide a particular solution to (2.2), in the form of (2.3), for which the choice of leads to an accelerated behavior with a complexity of where . Thus, the bias term in Theorem 4 decays at an accelerated rate, which differs from the standard decay of non-accelerated Jacobi-style algorithms where the initialization (bias) error scales proportionally to (Fallah et al., 2020).

Remark 7.

Next, we provide the oracle complexity of SAPD in high probability, which can be derived as a corollary to our main Theorem 4.

Corollary 5.

For and , set as

| (3.4) |

with , and for universal positive constants for that are large enough333For simplicity of the presentation, we do not provide these universal constants explicitly here; that said, the constants can be made explicit in a straightforward manner following the step-by-step computations in Section F of the Appendix.. Then, (2.2) is satisfied for and SAPD guarantees that for all satisfying (1.3).

Proof.

Remark 9.

By Assumption 1, the partial gradients and are Lipschitz continuous; therefore, they are almost everywhere differentiable by Rademacher’s Theorem. If we assume slightly more, i.e., if and are continuously differentiable, then the partial derivatives commute and we have , as a consequence of Schwarz’s Theorem. In this case, we can take in Assumption 1 and in Theorem 5.

Using Theorem 4 and building on the representation of the CVaR in terms of the quantiles, we can deduce a bound on as shown in Theorem 10, where we also provide bounds on the entropic value at risk and on the -based risk measure, as defined in Table 2.3.

Theorem 10 (Bounds on Risk Measures).

Proof.

The proof is provided in Section 5.2.2. ∎

In the next section, we discuss a family of quadratic SP problems for which we can compute the limiting covariance matrix of the iterates in expectation explicitly, assuming additive i.i.d. Gaussian noise on the partial gradients. This will allow us to gain insights about the effect of parameter choices and argue about the tightness of our analysis.

4 Analytical solution for quadratics

In this section, we study the behaviour of SAPD on quadratic problems subject to isotropic Gaussian noise. More specifically, we consider

| (4.1) |

where is a symmetric matrix, and are two regularization parameters. The unique saddle point of (4.1) is the origin . At each iteration , suppose we have access to noisy estimates and of the partial gradients of , where the and denote i.i.d. centered Gaussian vectors satisfying for some . In this special case, we have the gradient noise vectors , . Our main motivation to study this toy problem is to gain some insights into the sample paths SAPD generates, and use these insights while studying the tightness of high-probability bounds provided in Section 3.

This problem was first studied in (Zhang et al., 2023) where it was shown that, under certain conditions on , the sequence of iterates generated by SAPD, where , converges in distribution to a zero-mean multi-variate Gaussian random vector whose covariance matrix satisfies a certain Lyapunov equation of dimension . The authors of (Zhang et al., 2023) manage to split this equation into many Lyapunov equations:

| (4.2) |

i.e., for each eigenvalue of , there is a Lyapunov equation to be solved, where depend only on , and –for completeness, we provide these steps in detail in Section C.1 of the appendix.

Given an arbitrary symmetric matrix , in (Zhang et al., 2023), the small-dimensional Lyapunov equation in (4.2) is solved numerically. On the other hand, to establish the tightness of our high-probability bounds for the class of SCSC problems with a non-bilinear subject to noisy gradients with subGaussian tails (see Section 3), we need to analytically solve (4.2). However, analytically solving (4.2) for general parameters satisfying the matrix inequality (2.2) is a challenging problem that standard symbolic computation tools were not in a position to properly address our needs. That said, as we shall discuss next, we can provide analytical solutions for (4.2) under the Chambolle-Pock (CP) parameterization in (2.3), where primal and dual stepsizes are parameterized in , i.e., the momentum parameter, and for this choice the rate . We should note that CP parameterization represents a rich enough class of admissible SAPD parameters in the sense that under this parameterization SAPD can achieve accelerated bias decay in the expected squared distance metric (Zhang et al., 2023) and the accelerated high probability results we derived in Theorem 5.

4.1 Covariance matrix of the iterates under the CP parameterization

The main result of this section is the analytical solution of a Lyapunov equation corresponding to the limiting covariance for as , which is similar to the Lyapunov equation in (4.2) corresponding to the limiting covariance for , for the parameterization in (2.3). The proof yields closed-form solutions, useful for understanding the effect of parameters on the solution. Due to lengthy calculations involved, the proof is provided in Section C.2 of the Appendix. Our proof technique is based on identifying the conditions on the parameters so that the Lyapunov matrix in (4.2) admits a unique solution and we solve it as a function of by diagonalizing given in (4.2) with a proper change of basis.

Theorem 11.

Let . For any given fixed, set and . Suppose gradient noise sequences are i.i.d. centered Gaussian satisfying . Then, the iterates generated by SAPD applied to the SCSC problem in (4.1) with parameters , converges in distribution to a centered Gaussian distribution with covariance matrix satisfying where is orthogonal, and is block diagonal with blocs for , where denote the eigenvalues of . Specifically, for each , block has the following form: For ,

| (4.3) |

otherwise, for ,

| (4.4) |

where , and for , and are polynomials of , can be made explicit and are provided in Table 4 of Appendix D. Moreover, for any , all elements of the matrix scale with as .

Proof.

The proof is given in Section C.2. ∎

According to Theorem 11, the matrix has the property that it scales with as ; we leverage this fact to establish the tightness of our analysis in the next section (Section 4.2).

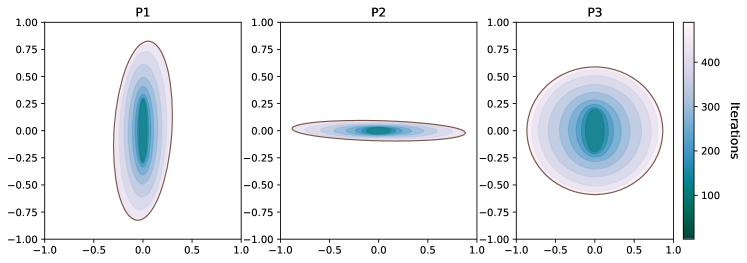

In Figure 2, we illustrate Theorem 11 on a simple quadratic problem where primal and dual iterates are scalar, i.e., and is a scalar. In the three panels of Figure 2, we consider three problems P1, P2, P3 from left to right where the problem constants, , are chosen as P1: - P2: - P3: . SAPD was run times for iterations using CP parameterization in (2.3) with . For each problem, we estimate the empirical covariance matrix for . The level set for the theoretical covariance matrix derived in Theorem 11 is represented by a brown edged ellipse on each plot. Figure 2 suggests the linear convergence of the matrices to the equilibrium matrix . Subsequently, we observe on these three examples how noise accumulates along iterations, producing covariance matrices that are non-decreasing in the sense of the Loewner ordering. This monotonicity behavior is intuitively expected as the noise accumulates over the iterations, but can also be proven using the fact that covariance matrix of follows a Lyapunov recursion (Laub et al., 1990; Hassibi et al., 1999). We elaborate further on this property by showing below that convergence of to happens at a linear rate characterized by the spectral radius of a particular matrix related to the SAPD iterations. The proof builds on the spectral characterizations of the covariance matrix obtained in the proof of Theorem 11.

Corollary 2.

In the premise of Theorem 11, for any , the sequence of covariance matrices satisfies

| (4.5) |

where , with .

Proof.

The proof is provided in Appendix C.3. ∎

4.2 Tightness analysis

We discuss in this section that the constants given in Theorem 4 are tight in the sense that under the CP parameterization given in (2.3), which corresponds to a particular solution of the matrix inequality in (2.2), the dependency of these constants to and cannot be improved when the number of iterations is sufficiently large. To this end, we consider quadratic problems subject to additive isotropic Gaussian noise for which we can do exact computations, i.e., both and are i.i.d zero-mean Gaussian random vector sequences with isotropic covariances, and these sequences are independent from each other as well.

In Section 4.1, under the isotropic Gaussian noise assumption, we show that the distribution of the iterates converges to a Gaussian distribution with mean and a covariance matrix for which we provide a formula in (4.4). If we let denote a random variable with the stationary distribution , Theorem 4 implies that

| (4.6) |

as . This upper bound (grows) scales linearly with respect to and , and a natural question is whether this scaling can be improved. In the next proposition we provide lower bounds on the quantiles of that also grows linearly with respect to and , matching the upper bound in (4.6). Therefore, we conclude that our analysis is tight in the sense that we cannot expect to improve our bound in (4.6) in terms of its dependency to and .

Theorem 12.

Proof.

The proof is provided in Section C.4 of the appendix. ∎

5 Proof of Main Results

5.1 Concentration inequalities through recursive control

This section presents general concentration inequalities that will be specialized later for the analysis of SAPD. The first result is a recursive concentration inequality extending the result provided in (Cutler et al., 2021, Proposition 6.7), which is used in the analysis of the stochastic gradient descent (SGD) method for minimization of a smooth strongly convex function in (Cutler et al., 2021). Our variant of this inequality enables us to analyze saddle point problems with acceleration, providing new insights on their robustness properties.

Proposition 13.

Let be a filtration on . Let , , and , be three scalar stochastic processes adapted to with following properties: there exist such that for all ,

-

•

is non-negative;

-

•

for all , i.e., conditioned on is subGaussian;

-

•

for all , i.e., conditioned on is subExponential.

If there exists such that

| (5.1) |

then for all , it holds that , for .

Proof.

Our proof follows closely the arguments of (Cutler et al., 2021, Proposition 6.7). The main difference is in the term which takes the specific form in (Cutler et al., 2021), where conditioned on is assumed to be subGaussian. For any , (5.1) together with Cauchy-Schwarz inequality implies that

Thus for , we have . Setting and taking the non-conditional expectation, we ensure that . This completes the proof. ∎

Unrolling the above recursive property on the moment generating function of provides us with high probability results on , given in the next result.

Proposition 14.

Let be defined as in Proposition 13. Then, for all and ,

| (5.2) |

Furthermore, if is constant, then

| (5.3) |

Alternatively, if can be expressed as such that is constant and satisfies , for all , for some constants and , then for any and where , we have

| (5.4) |

Proof.

Let us first prove by induction on that for all ,

| (5.5) |

For , this property holds trivially with the convention when . Assuming the inequality holds for some , next we show it also holds for . According to Proposition 13,

where the second inequality follows from the induction hypothesis since

and this completes the induction. Thus, (5.2) follows from using within (5.5). The remaining statements follow from a Chernoff bound; indeed, if is constant, we obtain

for and , which implies the desired result. Next, suppose for some constant and as in the hypothesis. First, observe that for ,

| (5.6) |

Thus, for all ,

Fixing an arbitrary non-negative such that , we have , which proves (5.4). ∎

Based on Proposition 14, as a corollary, one can derive convergence rates for the CVaR and EVaR risk measures of the scalar process .

Corollary 15.

Let be defined as in Proposition 14. Then, for any and ,

| (5.7) |

Proof.

Corollary 16.

Let be defined as in Proposition 14. Then, for any , and ,

| (5.8) |

Proof.

The bound in (5.4) of Proposition 14 ensures that for all and , the -th quantile of satisfies

hence, non-negativity of , Lemma 21 and sub-additivity of together imply that

| (5.9) |

For , let and note that (5.9) implies

| (5.10) |

Therefore, following standard arguments from (Vershynin, 2018), we have for any that

where we used (5.10). On the other hand,

where we used for . Finally, by translation invariance of the , we obtain . ∎

We finish with a bound on the -based risk measure, as defined in Table 2.3.

Corollary 17.

Let be defined as in Proposition 14. Then, for any , and ,

| (5.11) |

Proof.

5.2 Proofs of Theorem 4 and Theorem 10

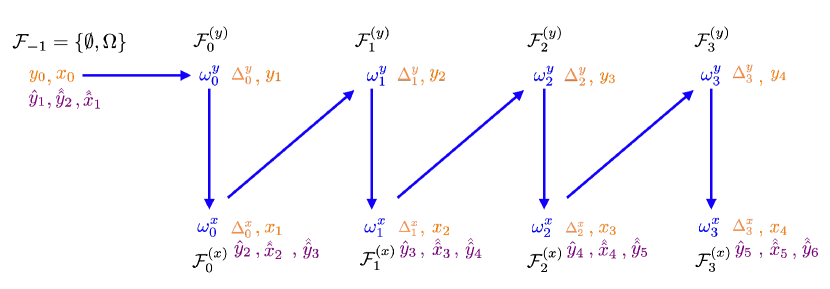

For proving the main results of this paper, namely Theorem 4 and Theorem 10, the application of the recursive control inequality from Section 5.1 is not straightforward. In particular, Gauss-Seidel type updates within SAPD significantly complicate the measurability properties of SAPD iterate sequence, as illustrated in Figure 3: the iterates and are measurable with respect to different filtrations and . We circumvent this issue by introducing a stochastic process that almost surely upper bounds the distance to the saddle point while exhibiting simpler measurability characteristics as discussed next. We note that even though algorithms with Gauss-Seidel type updates, such as SAPD, are significantly more complicated to analyze than their Jacobi counterparts, such an analysis is rewarding in the sense that algorithms with Gauss-Seidel type updates can often be faster than those using Jacobi type updates, see (Zhang et al., 2023, 2022). Indeed, our analysis for SAPD allowed us to obtain high-probability bounds that demonstrate an accelerated behavior for a stochastic primal-dual algorithm for SP problems.

5.2.1 Proof of Theorem 4

Our proof combines several ingredients. Let be a solution to the matrix inequality in (2.2). Recall the weighted distance square metric we introduced in (2.4). In the proof, we use a scaled version for that simplifies the analysis. We first introduce the following auxiliary iterates which can be interpreted as the “noise-free counterparts" to the actual iterates in the sense they represent roughly how the algorithm would behave if the gradients were deterministic in lieu of being stochastic at step :

| (5.12) | |||||

| (5.13) | |||||

| (5.14) | |||||

where we recall that and (see Algorithm 1). These auxiliary iterates whose measurability properties are illustrated in Figure 3, will be key for being able to apply Proposition 14 to obtain high-probability results for SAPD. Our proof is based on establishing an almost sure upper bound of the quantity by a scalar process , and then showing that our choice of satisfies the assumptions of Proposition 13. This will then directly yield the desired high-probability estimates for SAPD. We start with a proposition that provides an almost sure bound to the scaled squared distance metric . Although this bound is already present in substance in (Zhang et al., 2023), it does not appear explicitly. For completeness, in Appendix B.1, we provide its proof based on various arguments developed in (Zhang et al., 2023).

Proposition 18.

Let be the sequence generated by SAPD, intialized at an arbitrary tuple . Provided that there exists , and that satisfy (2.2) for some and , the following almost sure bound on ,

| (5.15) |

holds for all , where , and .

Proof.

The proof is provided in Appendix B.1. ∎

Now, equipped with Proposition 18, we can write

| (5.16) | ||||

For , introducing the scalar quantities

| (5.17a) | |||

| (5.17b) | |||

rearranging the sums in (5.16) and using , we may write (5.16) equivalently as follows:

Now notice that for ,

| (5.18) |

We next present a lemma which bounds the terms on the right-hand side of the above equality.

Lemma 19.

Proof.

The proof is provided in Appendix B.2.1. ∎

Applying Lemma 19 to the inequality (5.18), we obtain

| (5.19) |

For , we define , and as follows:

| (5.20) |

therefore, (5.19) implies that

| (5.21) |

Next, we argue that satisfies the assumptions of the recursive control inequality in (13). To achieve this goal, we will use the following lemma.

Lemma 20.

For any and , the following inequalities,

| (5.22) |

hold almost surely with the convention that , for some vectors which are explicitly provided in Table 3 of Appendix D.

Proof.

The proof is provided in Appendix B.2.2. ∎

Let us now show that satisfies the assumptions of the recursive control inequality in (13). Indeed, for any , , which is equivalent to . Let be the filtration defined as , and , for all . We first observe that for all , , and are -measurable; moreover, is non-negative due to (5.21). Second, for any , since and are norm-subGaussian conditioned respectively on and , for any , we get that

where we used Lemma 3 and the inequality for scalars in the last step, noting that , , are all -measurable. Hence, in view of Lemma 20 provided above and the bound in (5.21), we have

| (5.23) |

where we used (5.21) to obtain the second inequality. Third, for all and , we have in view of Lemma 2

| (5.24) |

Finally, we next argue that can be expressed as for some satisfying , for some constants and . First, note that and are all deterministic quantities as they depend only on the initialization; hence, using the inequality for any , we observe that for all , we have

Thus,

where the first inequality follows from Lemma 2, in the second inequality we used Lemma 20 given above, and the relation , which follows from and the relations , . Hence, we can apply Proposition 14 to the sequence defined in (5.20) with the following choice of parameter values,

| (5.25) |

where is defined in the statement of Theorem 4. When we invoke Proposition 14, we set within (5.4) for some particular such that as required by the proposition. Thus, for any and , the following inequality

holds with probability at least , with the choice of

| (5.26) |

where

| (5.27) |

In view of (5.21), and noting that , we obtain . Therefore,

| (5.28) | ||||||

completes the proof of (3.1). The remaining items to prove regarding the asymptotic properties of and as follows from straightforward but tedious computations; for completeness, we provide the details in the separate Lemma 29, provided in Section F.1 of the Appendix).

5.2.2 Proof of Theorem 10

We can deduce Theorem 10 from the above analysis. Indeed, the CVaR bound in (3.5) directly follows from Corollary 15 applied to the process introduced in (5.20), with the associated constants defined in (5.25). Furthermore, the EVaR bound in (3.6) follows from Corollary 16 applied to the same . Finally, the bound on follows from Corollary 17.

6 Numerical Results

In this section, we illustrate the robustness properties of SAPD when solving bilinear games and distributionally robust learning problems involving both synthetic and real data. First we consider the regularized bilinear game presented in (4.1),

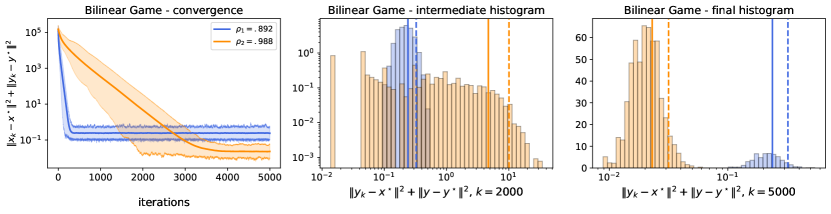

where is a matrix with entries sampled from i.i.d standard normal variables. We set the regularization variables as . We explore two values of the momentum parameter as and , with computed based on the threshold value from Theorem 11. We then determine the stepsizes according to the CP parameterization (2.3) where . Finally, SAPD is initialized at a random tuple , where have entries sampled from i.i.d. standard normal distributions. In Figure 4, we report the histogram of the distance squared to the saddle point after (top, middle panel) and iterations (top, right panel) based on 500 sample paths and for both choice of (momentum) parameter values. The expected distance over iterations is also reported on the top, left panel along with the error bars around it. The continuous vertical line in the convergence plots represents the sample average (estimating the expectation ), while the dashed vertical line represents with , i.e., the percentile of the error . We observe that the performance is sensitive to the choice of parameters and there are bias/risk trade-offs in the choice of parameters; indeed, when the number of steps is smaller (for ), the noise accumulation is not dominant and a smaller rate parameter allows faster decay of the initialization bias, resulting in better guarantees for the value at risk with or equivalently for the 90-th quantile. On the other hand when the number of steps is larger (for ), there is more risk associated to accumulation of noise and a larger choice of close to is preferable, as this results in smaller primal and dual stepsizes which allows to control the tail risk at the expense of a slower decay of the initialization bias.

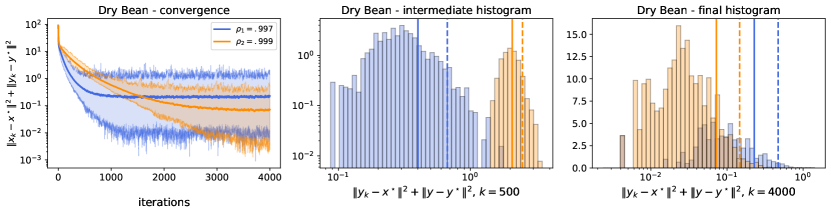

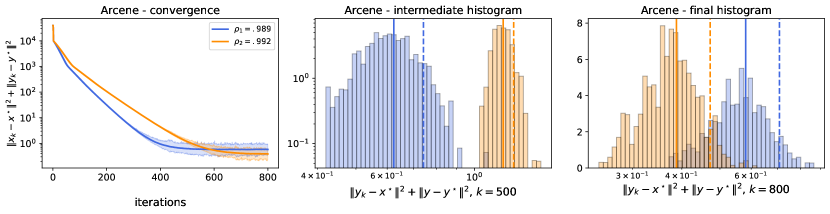

Next, we aim to solve the following distributionally robust logistic regression problem introduced in (Zhang et al., 2023): , where , and , with . We consider two datasets from the UCI Repository444https://archive.ics.uci.edu/ml/index.php, DryBean, and Arcene, and follow the preprocessing protocol outlined in (Zhang et al., 2023). For each dataset, we run SAPD with two values that are greater than the threshold value given in (Zhang et al., 2023, Corollary 1). SAPD is initialized for both datasets at and . In the middle and bottom panels of Figure 4, we display the average of the error over the course of the iterations as well as the error histogram for SAPD over runs as we did in the previous experiment. Our numerical findings are similar to the bilinear case, i.e., to obtain the best risk guarantees, one needs to choose the algorithm parameters in a careful fashion –which is inline with our theoretical results, where obtaining the accelerated iteration complexity in Theorem 5 requires choosing the parameters in an optimized fashion over the class of admissible CP parameters.

7 Conclusion

We consider a first-order primal-dual method that relies on stochastic estimates of the gradients for solving SCSC saddle point problems. We focused on the stochastic accelerated primal dual (SAPD) method Zhang et al. (2023).We obtained high-probability bounds for the iterates to lie in a given neighborhood of the saddle point that reflects accelerated behavior. For a class of quadratic SCSC problems subject to i.i.d. isotropic Gaussian noise and under a particular parameterization of the SAPD parameters, we were able to compute the distribution of the SAPD iterates exactly in closed form. We used this result to show that our high-probability bound is tight in terms of its dependency to target probability , primal and dual stepsizes and the momentum parameter . We also provide a risk-averse convergence analysis characterizing the “Conditional Value at Risk", -divergences and the “Entropic Value at Risk" of the distance to the saddle point, highlighting the trade-offs between the bias and the risk associated with an approximate solution.

Acknowledgements

Yassine Laguel and Mert Gürbüzbalaban acknowledge support from the grants Office of Naval Research N00014-21-1-2244, National Science Foundation (NSF) CCF-1814888, NSF DMS1723085, NSF DMS-2053485. Necdet Serhat Aybat’s work was supported in part by the grant Office of Naval Research Award N00014-21-1-2271.

References

- Ahmadi-Javid [2012] Amir Ahmadi-Javid. Entropic value-at-risk: A new coherent risk measure. Journal of Optimization Theory and Applications, 155:1105–1123, 2012.

- Ben-Tal and Teboulle [2007] Aharon Ben-Tal and Marc Teboulle. An old-new concept of convex risk measures: the optimized certainty equivalent. Mathematical Finance, 17(3):449–476, 2007.

- Ben-Tal et al. [2009] Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust optimization, volume 28. Princeton University Press, 2009.

- Beznosikov et al. [2022] Aleksandr Beznosikov, Boris Polyak, Eduard Gorbunov, Dmitry Kovalev, and Alexander Gasnikov. Smooth monotone stochastic variational inequalities and saddle point problems–survey. arXiv preprint arXiv:2208.13592, 2022.

- Bottou et al. [2018] Léon Bottou, Frank E Curtis, and Jorge Nocedal. Optimization methods for large-scale machine learning. SIAM review, 60(2):223–311, 2018.

- Can and Gürbüzbalaban [2022] Bugra Can and Mert Gürbüzbalaban. Entropic risk-averse generalized momentum methods. arXiv preprint arXiv:2204.11292, 2022.

- Chambolle and Pock [2011] Antonin Chambolle and Thomas Pock. A first-order primal-dual algorithm for convex problems with applications to imaging. Journal of mathematical imaging and vision, 40:120–145, 2011.

- Chen et al. [2017] Yunmei Chen, Guanghui Lan, and Yuyuan Ouyang. Accelerated schemes for a class of variational inequalities. Mathematical Programming, 165:113–149, 2017.

- Cutler et al. [2021] Joshua Cutler, Dmitriy Drusvyatskiy, and Zaid Harchaoui. Stochastic optimization under time drift: iterate averaging, step-decay schedules, and high probability guarantees. Advances in Neural Information Processing Systems, 34:11859–11869, 2021.

- Davis and Drusvyatskiy [2020] Damek Davis and Dmitriy Drusvyatskiy. High probability guarantees for stochastic convex optimization. In Conference on Learning Theory, pages 1411–1427. PMLR, 2020.

- Fallah et al. [2020] Alireza Fallah, Asuman Ozdaglar, and Sarath Pattathil. An optimal multistage stochastic gradient method for minimax problems. In 2020 59th IEEE Conference on Decision and Control (CDC), pages 3573–3579. IEEE, 2020.

- Ghadimi and Lan [2012] Saeed Ghadimi and Guanghui Lan. Optimal stochastic approximation algorithms for strongly convex stochastic composite optimization i: A generic algorithmic framework. SIAM Journal on Optimization, 22(4):1469–1492, 2012.

- Gibbs and Su [2002] Alison L Gibbs and Francis Edward Su. On choosing and bounding probability metrics. International statistical review, 70(3):419–435, 2002.

- Gidel et al. [2018] Gauthier Gidel, Hugo Berard, Gaëtan Vignoud, Pascal Vincent, and Simon Lacoste-Julien. A variational inequality perspective on generative adversarial networks. arXiv preprint arXiv:1802.10551, 2018.

- Gorbunov et al. [2022] Eduard Gorbunov, Marina Danilova, David Dobre, Pavel Dvurechensky, Alexander Gasnikov, and Gauthier Gidel. Clipped stochastic methods for variational inequalities with heavy-tailed noise. arXiv preprint arXiv:2206.01095, 2022.

- Gürbüzbalaban et al. [2022] Mert Gürbüzbalaban, Andrzej Ruszczyński, and Landi Zhu. A stochastic subgradient method for distributionally robust non-convex and non-smooth learning. Journal of Optimization Theory and Applications, 194(3):1014–1041, 2022.

- Hamedani and Aybat [2021] Erfan Yazdandoost Hamedani and Necdet Serhat Aybat. A primal-dual algorithm with line search for general convex-concave saddle point problems. SIAM Journal on Optimization, 31(2):1299–1329, 2021.

- Harold et al. [1997] J Harold, G Kushner, and George Yin. Stochastic approximation and recursive algorithm and applications. Application of Mathematics, 35, 1997.

- Harvey et al. [2019] Nicholas JA Harvey, Christopher Liaw, Yaniv Plan, and Sikander Randhawa. Tight analyses for non-smooth stochastic gradient descent. In Conference on Learning Theory, pages 1579–1613. PMLR, 2019.

- Hassibi et al. [1999] Babak Hassibi, Ali H Sayed, and Thomas Kailath. Indefinite-Quadratic estimation and control: a unified approach to H 2 and H theories. SIAM, 1999.

- Inglot [2010] Tadeusz Inglot. Inequalities for quantiles of the chi-square distribution. Probability and Mathematical Statistics, 30(2):339–351, 2010.

- Jin et al. [2019] Chi Jin, Praneeth Netrapalli, Rong Ge, Sham M Kakade, and Michael I Jordan. A short note on concentration inequalities for random vectors with subGaussian norm. arXiv preprint arXiv:1902.03736, 2019.

- Juditsky et al. [2011] Anatoli Juditsky, Arkadi Nemirovski, and Claire Tauvel. Solving variational inequalities with stochastic mirror-prox algorithm. Stochastic Systems, 1(1):17–58, 2011.

- Laub et al. [1990] P Gahinet A Laub, Ch Kenney, and G Hewer. Sensitivity of the stable discrete-time Lyapunov equation. IEEE Trans. Automat. Control, 35:1209–1217, 1990.

- Levy et al. [2021] Daniel Levy, Ziteng Sun, Kareem Amin, Satyen Kale, Alex Kulesza, Mehryar Mohri, and Ananda Theertha Suresh. Learning with user-level privacy. Advances in Neural Information Processing Systems, 34:12466–12479, 2021.

- Liu et al. [2022] Chengchang Liu, Shuxian Bi, Luo Luo, and John CS Lui. Partial-Quasi-Newton methods: Efficient algorithms for minimax optimization problems with unbalanced dimensionality. In Proceedings of the 28th ACM SIGKDD Conference on Knowledge Discovery and Data Mining, pages 1031–1041, 2022.

- Mokhtari et al. [2020] Aryan Mokhtari, Asuman Ozdaglar, and Sarath Pattathil. A unified analysis of extra-gradient and optimistic gradient methods for saddle point problems: Proximal point approach. In International Conference on Artificial Intelligence and Statistics, pages 1497–1507. PMLR, 2020.

- Nemirovski et al. [2009] Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4):1574–1609, 2009.

- Palaniappan and Bach [2016] Balamurugan Palaniappan and Francis Bach. Stochastic variance reduction methods for saddle-point problems. In Advances in Neural Information Processing Systems, pages 1416–1424, 2016.

- Panigrahi et al. [2019] Abhishek Panigrahi, Raghav Somani, Navin Goyal, and Praneeth Netrapalli. Non-Gaussianity of stochastic gradient noise. arXiv preprint arXiv:1910.09626, 2019.

- Rakhlin et al. [2012] Alexander Rakhlin, Ohad Shamir, and Karthik Sridharan. Making gradient descent optimal for strongly convex stochastic optimization. In Proceedings of the 29th International Coference on International Conference on Machine Learning, pages 1571–1578, 2012.

- Rockafellar and Royset [2013] R Tyrrell Rockafellar and Johannes O Royset. Superquantiles and their applications to risk, random variables, and regression. In Theory Driven by Influential Applications, pages 151–167. Informs, 2013.

- Shapiro [2017] Alexander Shapiro. Distributionally robust stochastic programming. SIAM Journal on Optimization, 27(4):2258–2275, 2017.

- Varshney et al. [2022] Prateek Varshney, Abhradeep Thakurta, and Prateek Jain. (nearly) optimal private linear regression for sub-gaussian data via adaptive clipping. In Conference on Learning Theory, pages 1126–1166. PMLR, 2022.

- Vershynin [2018] Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Wood and Dall’Anese [2022] Killian Wood and Emiliano Dall’Anese. Online Saddle Point Tracking with Decision-Dependent Data. arXiv e-prints, art. arXiv:2212.02693, December 2022. doi: 10.48550/arXiv.2212.02693.

- Yan et al. [2020] Yan Yan, Yi Xu, Qihang Lin, Wei Liu, and Tianbao Yang. Optimal epoch stochastic gradient descent ascent methods for min-max optimization. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 5789–5800. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/3f8b2a81da929223ae025fcec26dde0d-Paper.pdf.

- Zhang et al. [2022] Guodong Zhang, Yuanhao Wang, Laurent Lessard, and Roger B Grosse. Near-optimal local convergence of alternating gradient descent-ascent for minimax optimization. In International Conference on Artificial Intelligence and Statistics, pages 7659–7679. PMLR, 2022.

- Zhang et al. [2021] Junyu Zhang, Mingyi Hong, and Shuzhong Zhang. On lower iteration complexity bounds for the convex concave saddle point problems. Mathematical Programming, 194(1-2):901–935, jun 2021. doi: 10.1007/s10107-021-01660-z.

- Zhang et al. [2023] Xuan Zhang, Necdet Serhat Aybat, and Mert Gürbüzbalaban. Robust accelerated primal-dual methods for computing saddle points, 2023. Available at https://arxiv.org/pdf/2111.12743.

- Zhu et al. [2023] Landi Zhu, Mert Gürbüzbalaban, and Andrzej Ruszczyński. Distributionally robust learning with weakly convex losses: Convergence rates and finite-sample guarantees. arXiv preprint arXiv:2301.06619, 2023.

Appendix A Elementary proofs for subGaussians and convex risk measures

We provide in this section proofs of elementary properties of subGaussian vectors and convex risk measures.

A.1 Elementary Properties of Norm-subGaussian Vectors

In this section, we provide elementary proof of Lemma 2 and Lemma 3. The proofs follow from standard arguments that can be found in textbooks such as [8, 6].

A.1.1 Proof of Lemma 2

We follow standard arguments from [Vershynin, 2018]. First note that, for any , we have

where denotes the gamma function. Hence, noting that , by the monotone convergence theorem,

the last equality being valid for any . Since for any , , we obtain for any . Finally, last inequality follows from , where we chose .

A.1.2 Proof of Lemma 3

For , the inequality to prove is trivial. Assume . From Lemma 2 and Cauchy-Schwarz inequality, we have

| (A.1) |

for all . Thus, for any such , noticing that for , we obtain , where the second inequality follows from (A.1) and the assumption that . Moreover, for , we have by Cauchy Schwarz’s inequality and Lemma 2 that , where the last inequality is due to for .

A.2 Elementary properties of Convex Risk Measures

The following lemma is used in the derivation of and bounds.

Lemma 21.

For any non-negative random variable , we have for all :

Proof.

We first show that for any . Indeed, for any , we have which follows from non-negativity of and definition of . This implies ; thus, . Conversely, we note that , which implies ; hence, . Using this result,

where denotes the uniform distribution on , and the last inequality follows from the identity . ∎

Appendix B Intermediate results and proofs for the non-quadratic case

To start with, for the sake of completeness, we cite two results from [Zhang et al., 2023]. The first lemma is used to derive the almost sure bound result of Proposition 18, which is provided below in Appendix B.1, while the second lemma is used for deriving the convex inequalities provided in Appendix B.2.

Lemma 22 (See [Zhang et al., 2023, Lemma 1]).

The iterates of SAPD satisfy

for all , where

Lemma 23 (See [Zhang et al., 2023, Lemma 3]).

Let denote the SAPD iterate sequence. Then, the following inequalities hold for all ,

B.1 Proof of Proposition 18 (Almost sure domination of SAPD iterates)

Letting , and , with , by Jensen’s inequality , we have for all ,

Hence, in view of Lemma 22,

| (B.1) | ||||

where . By Cauchy-Schwarz inequality, observe that

Hence, using due to our initialization of , we have

From (B.1), it follows that

where . Now, observe that for all ,

where and are defined for as

and . By [Zhang et al., 2023, Lemma 5], the matrix inequality condition (2.2) is equivalent to having . In this case, we almost surely have

| (B.2) |

Finally, denoting

we have in view of [Zhang et al., 2023, Lemma 6]; thus,

Therefore, using (B.2), we can conclude that . Finally, by non-negativity of , we obtain (5.15).

B.2 Convex inequalities

B.2.1 Proof of Lemma 19

We first start with a technical result we will use in the proof of Lemma 19.

Lemma 24.

Proof.

Since is a solution of (1.1), and are fixed points of two deterministic proximal gradient maps, i.e.,

| (B.4) |

Thus, by the contraction properties of the prox for strongly convex functions, and convexity of the squared norm, we have

By the triangular inequality and smoothness assumptions on , we deduce

|

|

The statement finally follows from Cauchy-Schwarz inequality. ∎

Now we are ready to prove Lemma 19. By Young’s inequality, for any ,

Setting and , we ensure that

| (B.5) |

where and is defined in (2.4). Moreover, we also have for any . Hence, setting leads to

| (B.6) |

Finally, observe that for any ,

where the last inequality follows from Lemma 24 and the simple inequality for any . Setting ensures that

| (B.7) |

Hence, using the trivial upper bound and combining the bounds eqs. B.5, B.6 and B.7 we obtained above, we get

Let us now introduce for ; then, by similar computations the following bounds follow from Lemma 23:

and we deduce that

We now treat the sum . Observe first that for all , Lemma 23,

which, after organizing the terms and using for any scalars , becomes

Thus, we obtain for some constants (that are explicitly given in Table 2 of Appendix D). Hence, setting , we obtain,

therefore, rearranging the terms together we get

where and . This completes the proof.

B.2.2 Proof of Lemma 20

Let be fixed. In view of (B.4), we have

where the third inequality follows from the smoothness assumptions on and , and for the case, we have and . Using similar arguments, we also obtain

from which we deduce the following bound:

|

|

Combining the above bounds with Cauchy-Schwarz inequality implies (5.22) and we conclude.

Appendix C Details and proofs for the quadratic setting

C.1 Properties of SAPD on the quadratic SP problem given in (4.1)

In this section, we briefly recall the discussion in [Zhang et al., 2023] regarding the convergence behaviour of SAPD on the SP problem in (4.1). Precisely, denoting and , the authors observe that satisfies the recurrence relation where and are defined as

| (C.1) |

As a result, the covariance matrix of satisfies for all ,

| (C.2) |

where . Using the independence assumptions on the ’s and ’s, elementary derivations lead to expressing as

Provided that the spectral radius of is less than , the sequence converges to a matrix satisfying

| (C.3) |

Leveraging the spectral theorem, it is shown in [Zhang et al., 2023] that an orthogonal change of basis enables to reduce the Lyapunov equation to systems of the following form for each :

| (C.4) |

such that and are matrices defined for each as

and is similar to the matrix . Therefore, we have .

C.2 Proof of Theorem 11

In this section, we solve the Lyapunov equations (C.4) analytically under the parameterization in (2.3). Throughout, given , we introduce the quantity which is closely related to the condition number . Indeed, for , we have . For each , let be a solution to (C.4), i.e., solves the following Lyapunov equation:

| (C.5) |

Furthermore, such a solution is unique if [Laub et al., 1990, Hassibi et al., 1999]. The following result provides an explicit formula to whose proof is deferred to Section C.5.

Proposition 25.

Proof of Theorem 11.

Proposition 25 characterizes the asymptotic covariance matrix of in the limit as , which we will use to deduce the covariance matrix of in the limit as . First, recall from [Zhang et al., 2023] that the orthogonal matrix leading to the reduced Lyapunov (C.4) is given by where is the permutation matrix associated to the permutation of defined as , for all , and where describes an orthogonal basis for with . Now, since , we have where

Thus, , and noting that admits the block diagonalization where and

we obtain , where . Finally, we observe that where

Plugging into the expression of computed in Proposition 25, we obtain , if ; otherwise,

where the polynomials and are given explicitly in the bottom part of Table 4 of Appendix D. From the closed-form expressions of these polynomials, the fact that the elements of the matrix scale with as can be checked in a straightforward manner. ∎

C.3 Proof of Corollary 2

Let denote the Jordan decomposition of . For , let , , and . In view of the recursion (C.2), we have , and vectorizing again this recursion lead to , i.e., . Hence, noting that we obtain

and the claimed convergence rate follows from observing that . Note that here because by Proposition 25 we have for every and .

C.4 Proof of Theorem 12

We start with proving the lower bound, and then we will proceed to the upper bound.

C.4.1 Lower bound

In view of Theorem 11, follows a centered Gaussian distribution with covariance matrix as defined in (4.4). Hence, let be such that . We almost surely have . By [Inglot, 2010], we have , where we used . Thus, it suffices to show that as . Given the bloc decomposition of in (4.4), we have

We will now show that for all , , as . If , given (4.3), we have

where second equality follows from having . If is in , in view of Table 4 of Appendix D, we have as ,

and , so that

Hence, we deduce that

and it suffices to show that . Now given the identity for , we have

which completes the proof.

C.4.2 Upper bound

The CP parametrization corresponds to choosing in the matrix inequality [Zhang et al., 2023, Cor. 1]. Under this parameterization, since , we have and we have . Since converges in distribution to , (3.1) implies that the -quantile of satisfies for any , where Thus, the asymptotic property of our upper bound follows from Lemma 29.

C.5 Proof of Proposition 25

We first note that under the parameterization (2.3), the matrices and simplify to

| (C.6) |

If , then . Hence, using the relation , we have

Noting that , we obtain for any . It remains to consider the case when . We first provide an eigenvalue decomposition to the matrix .

Lemma 26.

For any and , the matrix introduced in (C.4) admits the diagonalization where

| (C.7) |

with complex eigenvalues , , and . Moreover, in this case, and .

Proof.

Noting that and , the characteristic polynomial of has for discriminant . Note also that since by assumption, and

and in such case, it is straightforward to check that admits the two complex conjugate values . Furthermore, observe that as and and for , ,

Therefore, the columns of the matrix are in fact eigenvectors corresponding to the complex conjugate eigenvalues and , and we conclude that the eigenvalue decomposition holds. Finally, so that we have and if and only if . Observing that , we deduce that and . Hence, we conclude for any . ∎

In the following lemma, we also provide basic identities satisfied by the eigenvalues and which will be key for the exact computation of . The proof of this lemma is omitted as it follows from straightforward calculations.

Lemma 27.

The following lemma says that the solution of (C.5) can be computed by solving 4-dimensional linear equations.

Lemma 28.

Proof.

Equipped with the representation (C.8), we complete the proof of Proposition 25 in three steps: (I) explicit computation of , (II) explicit computation of from based on (C.8), (III) explicit computation of from based on the relationship given in Lemma 28.

-

(I)

Computation of . Using the Cramer rule, first observe that satisfies

from which we deduce

where

(C.9) - (II)

- (III)

While (C.10) provides a formula for , the dependence of this formula to and are not very clear. We provide in Section E of this Appendix a simplification of the terms in (C.10) in terms of their dependence to and . As a consequence, in view of (C.10), we may write

where the and are polynomials in , defined in the top part of Table 4. This proves Proposition 25.

Appendix D Symbols and constants used in the paper

The convergence analysis of SAPD relies on a series of convex inequalities that we wrote in matrix form for compactness. All the constants arising in these inequalities (including those mentioned in the statement of Lemma 19 and Lemma20) are made explicit as follows in Table 2 and Table 3. For convenience of the reader, in Section G of this Appendix, we also provide the expressions of the these constants under the CP parameterization (2.3) which is a particular class of parameters where our complexity results can be achieved. We finally detail in Table 4 the polynomials involved in the entries of the covariance matrix given in Theorem 11.

| , |

| . |

Appendix E Supplementary derivations for the quadratic case

In this section, we outline how the constants , and that are defined by (C.11) in the proof of Proposition 25 can be simplified and reorganized under a common denominator that is related to the polynomial given in Table 4 of Appendix D. This requires tedious but otherwise straightforward computations as follows:

(I) Simplification of .

Given the expressions (C.9) and (C.11), we have

where , defined in (C.1), admits the expression (C.6) under the CP parameterization, and are its eigenvalues, provided Lemma 26. First note that

where the last line can be deduced from Lemma 27. Second, we observe that

and

| (E.1) |

and finally, noting that

| (E.2) |

and using again Lemma 27, we obtain

Hence, grouping together the terms which have a factor and those which do not, we obtain

| (E.3) |

where and are polynomials in and .

(II) Simplification of .

(III) Simplification of .

By going through similar steps, we obtain

| (E.5) |

Finally, we notice that if we write for and in a common denominator, the following term would arise:

| (E.6) |

Appendix F Proof of Corollary 5

Our choice of parameters is a special case of the CP parameterization derived in [Zhang et al., 2023, Corollary 1]. Let us first assume that . Then, by [Zhang et al., 2023, Corollary 1], , with and is a solution of the matrix inequality (2.2). Thus, our Theorem 4 is applicable. In particular, noting that , we have

Therefore, Theorem 4 gives

Let us fix . To show the claimed iteration complexity bound, it suffices to show that the right hand-side is at most for the given choice of parameters. For this purpose, sufficient conditions are

| (F.1) | ||||

| (F.2) | ||||

| (F.3) | ||||

| (F.4) |

where we recall that

| (F.5) |

In the remainder of this proof, we show that each of the above conditions (F.1)-(F.4) will be satisfied if is set according to the following two conditions:

| (F.6) | |||||

| (F.7) |

for some universal constants that are large enough. Then, we will use these lower bounds on to characterize the number of steps required to reach -accuracy in high probability. We next consider each of the four conditions (F.1)-(F.4) separately and argue that our choice of stepsize according to (F.6)- (F.7) will satisfy each condition.

(I) Satisfying Condition (F.3).

Based on (F.5), in order to satisfy (F.3) it suffices that and . Noting that , and using that , we have in view of Lemma 31,

Thus, to ensure that , it suffices to set

| (F.8) |

with universal constants that are large enough and for any constant . Through similar derivations, one can ensure that can be guaranteed via

| (F.9) |

for universal positive constants that are large enough.

We conclude that the choice of stepsize according to (F.6) and (F.7) with large enough constants will satisfy Condition (F.3).

(II) Satisfying Condition (F.2).

Observe now that the constraint (F.2) is satisfied if we ensure the following two conditions:

Among the last two constraints, using the definitions of given in (5.28), the first constraint will be satisfied whenever

and using that , it can be checked that

both constrains are valid under assumptions of the same form as (F.8).