[table]capposition=bottom \floatsetup[figure]capposition=bottom

Reconstructing firm-level input-output networks from partial information

Abstract

There is a large consensus on the fundamental role of firm-level supply chain networks in macroeconomics. However, data on supply chains at the fine-grained, firm level are scarce and frequently incomplete. For listed firms, some commercial datasets exist but only contain information about the existence of a trade relationship between two companies, not the value of the monetary transaction. We use a recently developed maximum entropy method to reconstruct the values of the transactions based on information about their existence and aggregate information disclosed by firms in financial statements. We test the method on the administrative dataset of Ecuador and reconstruct a commercial dataset (FactSet). We test the method’s performance on the weights, the technical and allocation coefficients (microscale quantities), two measures of firms’ systemic importance and GDP volatility. The method reconstructs the distribution of microscale quantities reasonably well but shows diverging results for the measures of firms’ systemic importance. Due to the network structure of supply chains and the sampling process of firms and links, quantities relying on the number of customers firms have (out-degrees) are harder to reconstruct. We also reconstruct the input-output table of globally listed firms and merge it with a global input-output table at the sector level (the WIOD). Differences in accounting standards between national accounts and firms’ financial statements significantly reduce the quality of the reconstruction.

Keywords: Network reconstruction, supply chain, production network, input-output table, maximum entropy, missing information

JEL codes: C80, D57, E32, L14, F12

1 Introduction

Recent events, such as the war in Ukraine and the evermore frequent natural disasters, have highlighted the fragility of global supply chains. Shocks to individual firms or a cluster of firms, sometimes located in a particular geographical region, can quickly spread through the network with severe repercussions on the global economy. Most of the research has so far been conducted at the sector level (Acemoglu et al., , 2012; Carvalho, , 2014; Pichler and Farmer, , 2021). However, analysing such shocks at the level of sectors can lead to misleading results (Diem et al., , 2022). The value of firm-level data is thus increasingly recognised, but research efforts are constrained by data availability.

Due to confidentiality and the data collection process, supply chain data are scarce, hard to access, and frequently incomplete. Countries collect the best data sources through VAT filings, but only a handful of countries collect them (for a comprehensive review and discussion of the different datasets Bacilieri et al., , 2023). Some datasets of broader global coverage derived from US disclosure requirements are available. Given their wider breadth of coverage and relatively easier access, such datasets are used in many studies (e.g., Wu, , 2016; Wang et al., , 2021; Pankratz and Schiller, , 2019; Taschereau-Dumouchel, , 2020; Boehm and Sonntag, , 2022; Barrot and Sauvagnat, , 2016; Atalay et al., , 2011; Herskovic et al., , 2020). In contrast to national datasets, which report the monetary values of the transactions (i.e., the weighted network), global datasets do not provide this valuable information.

Reconstructing firm-level production networks is thus an important topic, showing growing research interest. The reconstruction problem concerns mainly two features of the production network: supplier-customer relations and transaction values. Several studies develop methods to infer both links and transaction values (Reisch et al., , 2021; Ialongo et al., , 2022; Hooijmaaijers and Buiten, , 2019; Hillman et al., , 2021) or links only (Brintrup et al., , 2018; Mungo et al., , 2022; Kosasih and Brintrup, , 2022), and two focus on inferring weights given the binary topology (Inoue and Todo, , 2019; Welburn et al., , 2020). The assessment of the quality of the weights reconstruction is usually missing and sometimes carried out on aggregate quantities or compared to empirical facts about another country’s network.

In this paper, we focus on reconstructing the transaction values using partial information on the supply chain relations and aggregate information about firms’ revenues and expenditures. We provide a rigorous assessment of a recently developed maximum entropy reconstruction method (Parisi et al., , 2020) using the administrative dataset of Ecuador. We evaluate the method on microscale, higher-order and macroscale quantities that are widely used in economic input-output (I-O) models.

We assess the method’s performance at recovering the link weights, and the technical and allocation coefficients (i.e., normalised weights). We also use two indicators of firms’ systemic importance, the output multipliers and the influence vector, that are prominent in macroeconomic I-O models of shock propagation. While the reconstruction method reproduces the weights (normalised or not) rather poorly, it reconstructs their distributions reasonably well. In contrast, the reconstruction shows diverging results for higher-orders quantities: the output multipliers are in remarkable agreement with the empirical values, while the influence vector is overestimated. We then use a general equilibrium I-O model (Acemoglu et al., , 2012) to assess how shocks to firms’ total factor productivity (TFP) propagate through the network, ultimately affecting aggregate GDP fluctuations. We show that aggregate volatility is overestimated by the reconstruction method we employ.

Our results suggest that quantities relying more prominently on the number of customers firms have are more adversely affected by missing firms and links due to the structure of supply chain networks (Bacilieri et al., , 2023) and the sampling process underpinning the observed firms and links. We also find that including a proxy node, to represent the rest of the economy that is not captured by the network, is of help in predicting microscale and higher-order quantities but not for predicting aggregate volatility.

An additional contribution we make in this paper is to construct the I-O table of globally listed firms using the dataset collected by FactSet. We merge FactSet with the World Input-Output Database (WIOD). Key challenges related to differences in accounting standards between national accounts and firms’ financial statements prevent us from (1) merging the two datasets at the desired country-sector or even sector level, and (2) carrying out an accurate quantification (at the firm level) of the key variables making up an I-O table. We then reconstruct and compute weights, coefficients and higher-order quantities for FactSet as well. The inability to accurately quantify the variables of the I-O table at the firm level dramatically reduces the quality of the final dataset and thus of the reconstruction.

The remainder of the paper is organised as follows. In Section 2, we explain the notation and define the production network at the firm level. In Section 3, we discuss the two datasets we use. In Section 4, we review the literature on network reconstruction, briefly describe the maximum entropy method we employ and the metrics we use to assess the performance of the reconstruction method. We then show and discuss the results for microscale, higher-order and macroscale properties for Ecuador and FactSet. Section 4.5 shows results for different numbers of unknown links and Section 5 concludes.

2 Firm-level input-output tables

This section describes firm-level production networks and gives an example of the supply chain network of publicly listed firms we aim to reconstruct. We then explain I-O tables and outline key differences between I-O tables at the sector and firm level.

The production or supply chain network is composed of firms (nodes) and links between firms indicate yearly trading relationships. Links may be weighted, where each weight represents firm ’s intermediate input expenditure on goods produced by . We label the weighted adjacency and the binary adjacency matrix. Figure 1 shows the binary (left) and weighted (right) adjacency matrices depicting the empirical data collected by FactSet. Both matrices have on the -th row the customers of firm , while column lists the suppliers of the -th firm. The unknown weights are labelled as question marks. Given (and other aggregate information about firms that we outline below), we aim to reconstruct .

For each firm, we can define its (total) intermediate expenditure and sales as, respectively, the column and row sums of the weighted adjacency matrix. The column and row sums are also called the weighted in- and out-degrees or in- and out-strengths; they are given by

| (1) |

| (2) |

where is a vector of ones of appropriate size.

The supply chain network just described captures only a part of the economic activity, namely firm-to-firm trades. Transactions with other economic actors (e.g., households) are captured in an input-output table, usually at the sector level. One can also define an input-output table at the firm level, however with notable differences. For a more in-depth discussion, we refer to Appendix A.3 and Bacilieri et al., (2023).

In I-O studies of production networks, the weighted adjacency matrix is usually normalised using firms’ total costs instead of their in-strengths. A firm’s total costs are the costs of intermediate inputs plus value-added, which is itself composed of labour costs, depreciation, amortisation and profit (see Appendix A.1.3). The weights so normalised are called the technical coefficients and represent the percentage of inputs firm buys from firm . The technical coefficients are given by

| (3) |

where is value-added of firm .

Similar to the technical coefficients, one can define the allocation coefficients, . tells us the percentage of output firm sells to firm . Letting be the amount of final demand satisfied by firm , the allocation coefficient is defined as

| (4) |

3 Data

FactSet is the global production network that we aim to reconstruct and for which we do not know the values of the monetary transactions. Therefore, we test the reconstruction method on the administrative dataset of Ecuador, for which we know the monetary values of the transactions.

3.1 FactSet

We use three primary data sources provided by FactSet: Fundamentals, Supply Chain Relationships and Supply Chain Shipping Transactions.111 The datasets were downloaded in April 2020. FactSet covers mainly listed firms around the world. The supply chain relationships of these companies are collected through two primary sources: company filings required by US Federal Accounting Standards (Supply Chain Relationships) and import and export declarations at ports from the US Bill of Lading (Supply Chain Shipping Transactions).222 The Statement of Financial Accounting Standards No. 131 requires publicly traded firms on US stock exchanges to report customers that account for 10% or more of their annual revenues, formally called major customers. FactSet also collects information on supply chain relationships from investor presentations, company websites and press releases. Due to the nature of the data collection process, coverage is biased toward companies listed on US stock exchanges, large firms and large transactions. For a more detailed description of FactSet see Appendix A.1 and Bacilieri et al., (2023).

We aggregate customer-supplier relations within a fiscal year to ensure time consistency between the formation of supplier-customer relations and financial statements.333 The fiscal year goes from June to May, meaning that if a company’s fiscal year end-month falls between January and May, the fiscal year is the current calendar year minus one; otherwise, it is the current calendar year. We further aggregate all three datasets at the parent company level. For each company, we also have information on the sector (NACE Rev.2 codes at the 4-digit level) and the country where the company’s headquarters are located.

We use several variables from companies’ income statements (FactSet Fundamentals): revenues, the cost of goods sold, labour expenses, earnings before interest and taxes (EBIT), depreciation and amortisation. We convert all the variables to USD using the currency conversion tables provided by FactSet. We define value-added as the sum of labour expenses, EBIT, amortisation and depreciation (Appendix A.1.3). Some firms do not disclose their labour costs and include them in the costs of goods sold; we estimate these firms’ labour expenses (see Appendix A.1.2).

For simplicity, we limit ourselves to the 2014 network, which we call henceforth “FactSet”. We keep firms with positive sales, intermediate expenses and value-added, and with non-negative labour costs (see Appendix A.1.4). We exclude firms in financial and insurance, extraterritorial organisations and bodies and activities of households as employers. The number of firms in the 2014 cleaned dataset is 5,442; these are involved in 15,916 trading relations. The average degree is 2.9.

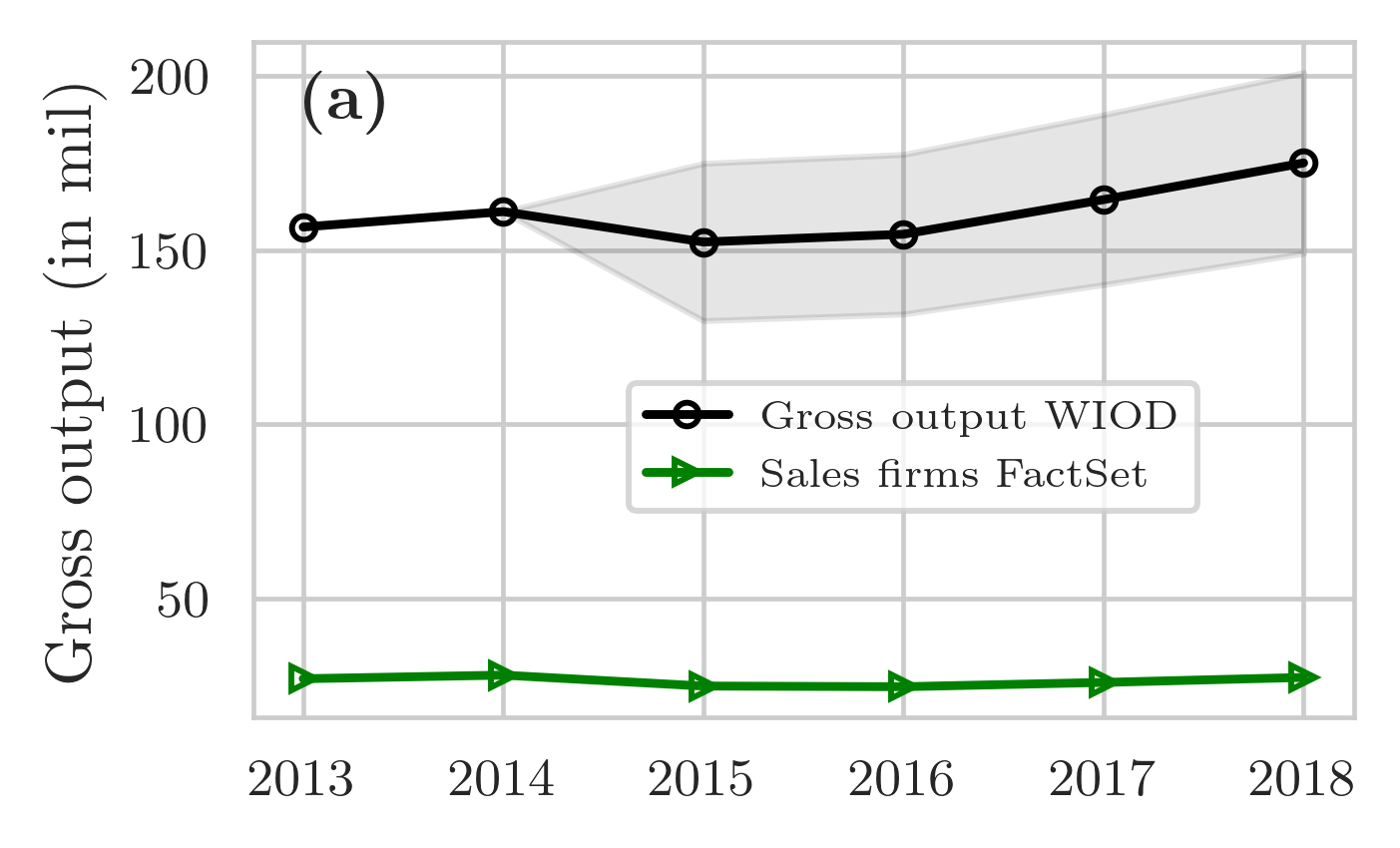

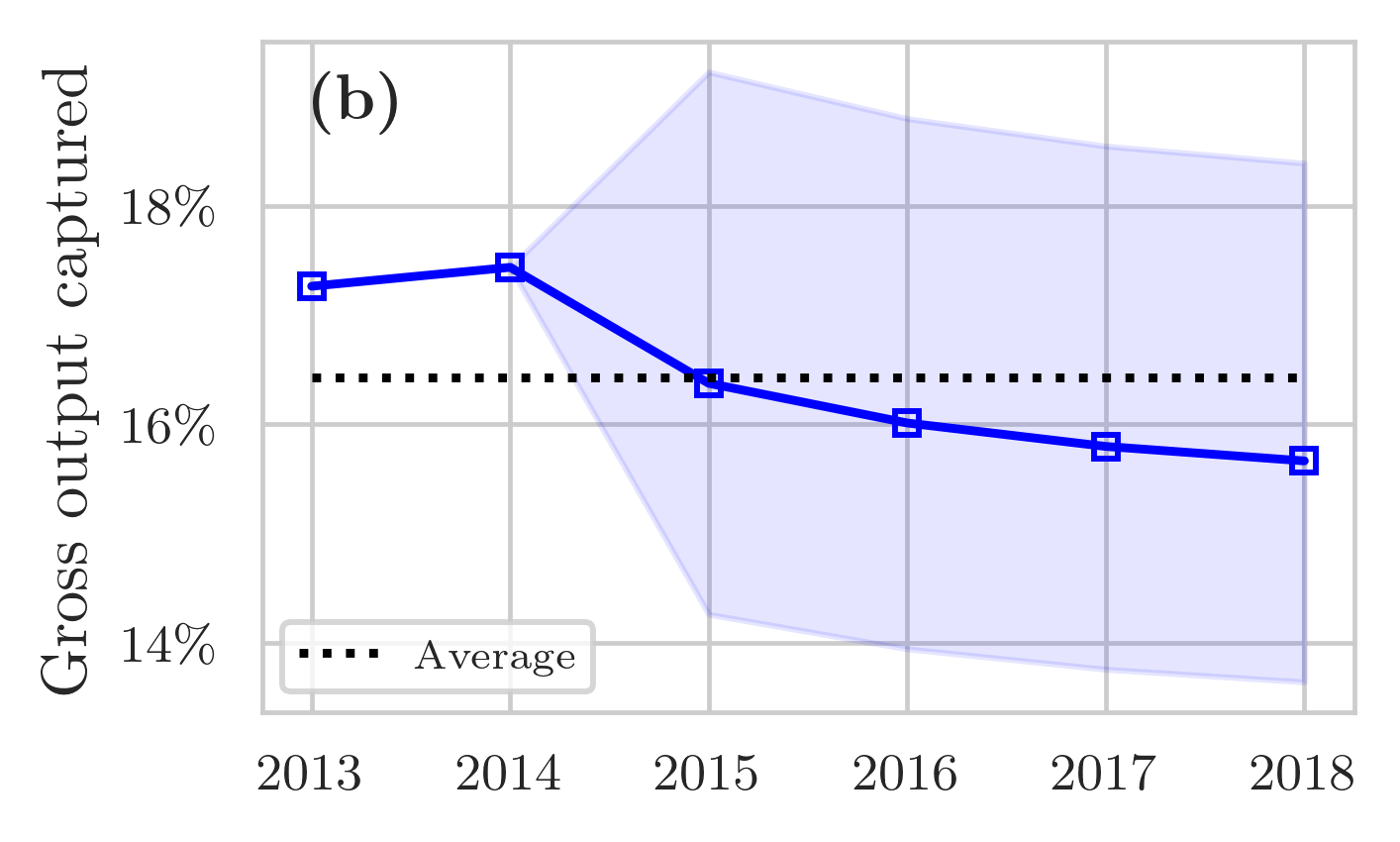

Evaluation of coverage and proxy node.

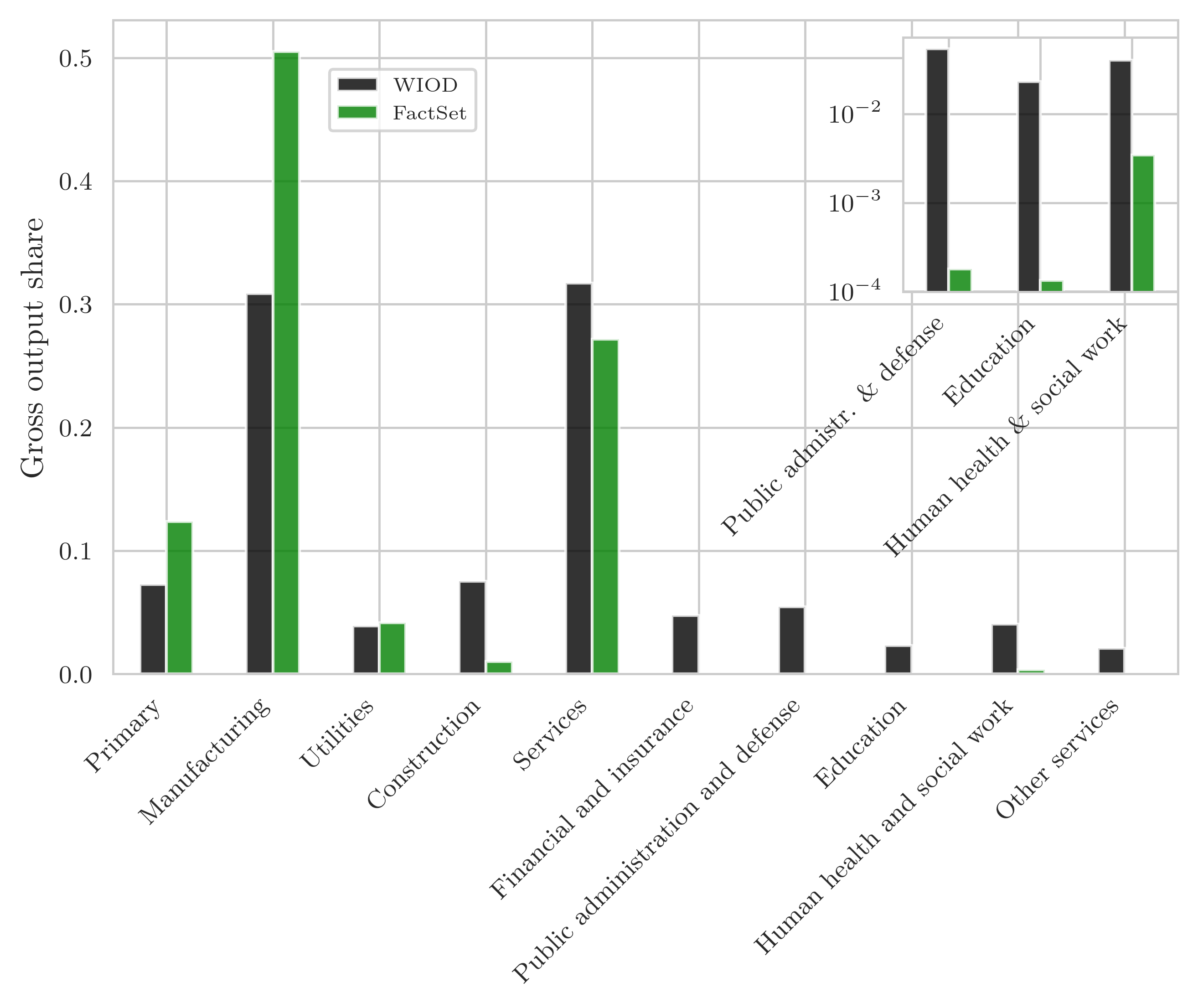

In 2014, FactSet captures around 16.4% of world gross output as reported in the WIOD (see Appendix A.2.4). To capture the rest of the economic activity that we do not capture in FactSet, we introduce a “proxy” node in the network to which all firms are connected. We construct the proxy node’s variables (gross output, intermediate sales and expenditure, etc.) using the WIOD aggregated at the world level.

A good approach would be to integrate FactSet with the WIOD at the country and sector level. However, due to differences between national accounting standards and firms’ financial statements, we had to aggregate the WIOD at the world level. We refer to Appendix A.3 for a detailed discussion of how we integrated the two datasets.

3.2 Ecuador

Ecuador collects customer-supplier relations through VAT filings, which are mandatory for firms and natural persons. We do not have access to firms’ financial statements, so we do not know their revenues, labour costs or profit, but we know the sectors’ firms are in (ISIC Rev. 4 codes). The Ecuador dataset was provided by Ecuador’s government to one of the authors. We refer to Astudillo-Estevez, (2021) and Bacilieri et al., (2023) for more information about the dataset.

Constructing the test network.

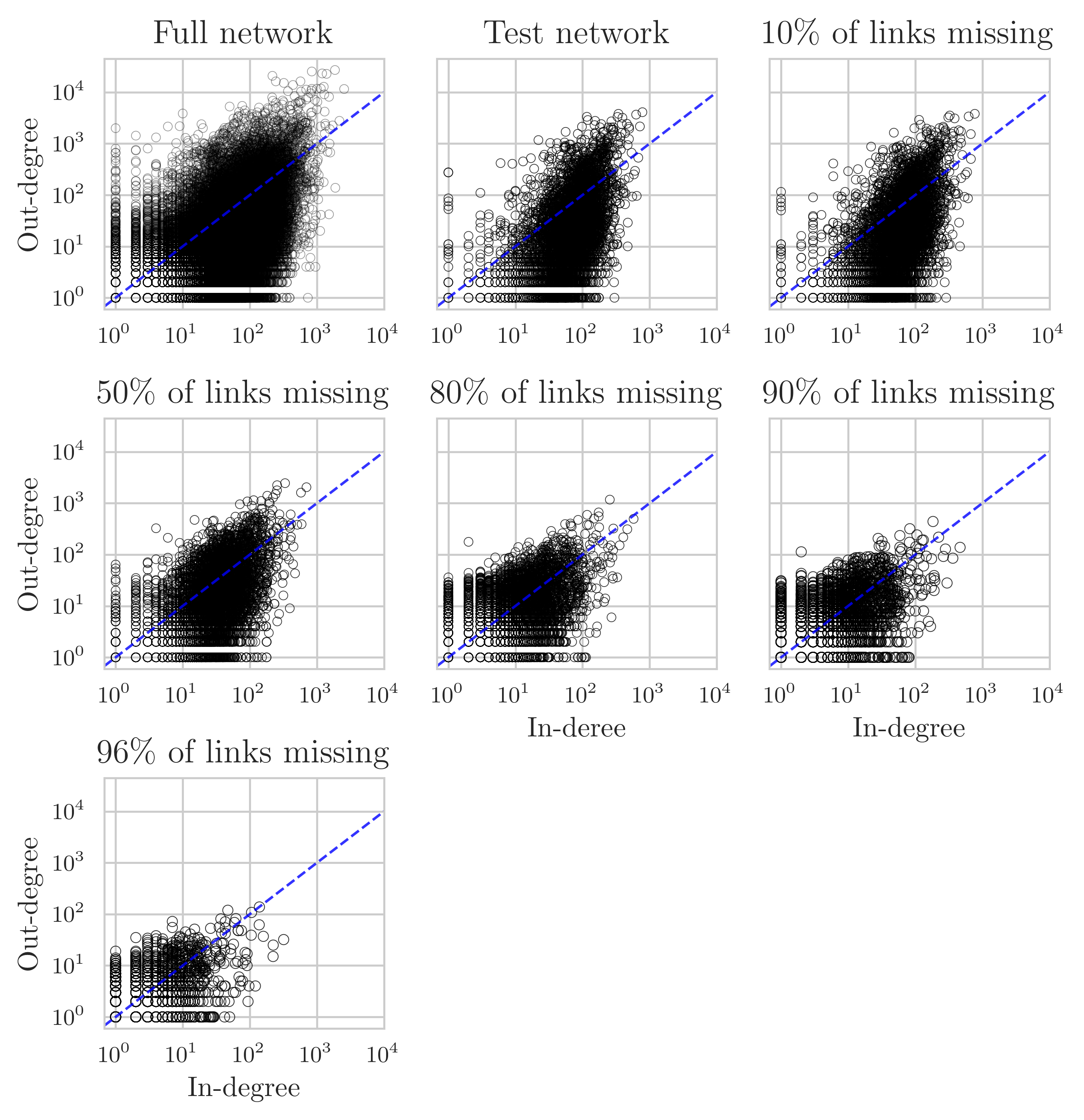

While Ecuador’s dataset has comprehensive coverage, FactSet does not. Therefore, we construct a test network that mimics the missing firms and links in FactSet. To mimic the missing firms in FactSet, we keep the same number of firms in Ecuador that we have in FactSet. We choose to keep the largest firms (in terms of out-strength) since we observed predominantly large firms in FactSet. We also require firms to have positive in-strengths, meaning that firms need to buy some inputs from the other firms in the subgraph.444 4 firms are further dropped because they do not have any links with the other firms in the sampled subgraph. The resulting network, which we call “test network” (third column in Table 1), has a much higher average degree compared to FactSet, meaning that the average Ecuadorian firm is connected to many more firms than the average firm in FactSet.

To mimic the missing links in FactSet, we eliminate links at random in the “test network” until we match FactSet’s average degree. Since FactSet’s supply chain relations mostly cover customers that account for 10% or more of a firm’s annual revenues, we delete links with a smaller weight with a higher probability: we set the link deletion probability to be inversely proportional to the link weight . We do this procedure 50 times and reconstruct each of the 50 randomised networks. The summary statistics for these networks, which we call “trimmed test network”, are shown in the last column of Table 1. In deleting links to match FactSet’s average degree, 96% of the links among firms in the test network are deleted. Consequently, our results can be interpreted as an approximate lower bound on the quality of the reconstruction.

We aggregate the firms and transactions left out of the test network in one proxy node representing the rest of the economy. As done for FactSet, we establish an incoming and outgoing link between each firm and the proxy node.

| Summary statistics | Full network | Test network | Trimmed test network |

|---|---|---|---|

| N. nodes | 84,978 | 5,440 | 5,440 |

| N. edges | 3,439,975 | 432,910 | 15,776 |

| Average degree | 40.5 | 79.6 | 2.9 |

Inferring missing data.

For Ecuador, we do not have information on final demand, revenues and the variables that compose value-added (i.e., labour costs, depreciation, amortisation and profits). To carry out the analyses described in Section 4.2, we need final demand and value-added of each firm. Therefore, we simulate final demand and value-added using the 2014 I-O table of Ecuador at the sector level.555 The sector-level I-O table is available at https://contenido.bce.fin.ec/documentos/PublicacionesNotas/Catalogo/CuentasNacionales/Anuales/Dolares/MenuMatrizInsumoProducto.htm. Consider value-added (a similar procedure is done for final demand), for each sector , we calculate the ratio of value-added to intermediate expenditure . Assuming that a firm’s ratio is the same as that of the sector the firm is in, a firm’s value-added is given by .

4 Network reconstruction

Methods for reconstructing networks with missing information have mostly been developed for financial or trade networks (e.g., Moussa, , 2011; Mastrandrea et al., , 2014; Cimini et al., 2015b, ; Gandy and Veraart, , 2017; Anand et al., , 2015) and I-O tables at the sector level (e.g., Golan et al., , 1994; Robinson et al., , 2001; Lenzen et al., , 2009). Only a few studies develop methods for reconstructing firm-level production networks (Inoue and Todo, , 2019; Welburn et al., , 2020; Reisch et al., , 2021; Hooijmaaijers and Buiten, , 2019; Ialongo et al., , 2022; Hillman et al., , 2021). We start with a brief overview of the different reconstruction methods developed in the literature, which we divide into deterministic and ensemble methods, and subsequently give a more detailed account of the methods developed to reconstruct firm-level networks. We refer to Squartini et al., (2018) and Cimini et al., (2021) for reviews on reconstruction methods developed mostly for financial and trade networks, and to Miller and Blair, (2009), McDougall, (1999) and Lahr and De Mesnard, (2004) for reviews on sector-level reconstruction methods and matrix balancing problems.

The network reconstruction problem, being it for financial, trade or production networks, boils down to inferring a matrix of bilateral flows among entities (e.g., banks, countries or sectors) given constraints on the total in- and out-flows of each entity and other information when available (e.g., degrees or a prior bilateral flows matrix). Most of the reconstruction methods are based on the maximum entropy principle, of which there are two strands: deterministic and ensemble methods. Deterministic methods yield a single reconstruction of the weighted network while meeting the constraints exactly. Instead, ensemble methods sample many networks from a distribution that is constructed to respect the constraints on average. Therefore, while ensemble methods generate a probability distribution over the likely networks, deterministic methods assign a probability of one to the reconstructed network and a zero probability to all the other networks – which likely include the true network (Parisi et al., , 2020). The shortcomings that most deterministic and ensemble methods share are that they tend to create a fully connected network with weights distributed as uniformly as possible given the imposed constraints on the in- and out-flows. To create sparser networks, algorithms with tunable (Moussa, , 2011; Upper, , 2011; Mastromatteo et al., , 2012) or exact network density (Mastrandrea et al., , 2014; Cimini et al., 2015b, ) have been developed.

The most well-known deterministic method is known as MaxEnt. It maximises an entropy-like functional subject to constraints on the in- and out-strength of each node. The solution to this maximisation yields the well-known gravity model (without distance) in the international trade literature (first proposed by Tinbergen, , 1962 and Pöyhönen, , 1963; see also Squartini and Garlaschelli, , 2014 for a discussion). MaxEnt displays all the shortcomings mentioned above: it generates a fully connected network and the weights are distributed as equally as possible given the constraints. To enhance the MaxEnt reconstruction, if some prior information about the binary topology or the weights is available, it can be integrated using a cross-entropy method (Golan et al., , 1994; Di Gangi et al., , 2018; Upper, , 2011; Wells, , 2004). The cross-entropy method reconstructs a network that has minimum distance to the prior while accounting for the imposed constraints. The cross-entropy method is equivalent to the iterative proportional fitting (IPF) algorithm, which iteratively distributes the weights (coming from the MaxEnt solution or any other prior) among the non-zero edges until the row and column sums are satisfied. The IPF algorithm is also known as the RAS technique in the I-O literature (Miller and Blair, , 2009). If the network is fully connected, the IPF algorithm is equivalent to MaxEnt.

There are different ensemble methods depending on the information used for the reconstruction (e.g., in- and out-degrees or strengths sequences). We discuss the method developed by Cimini et al., 2015b since it is one of the best performing (Anand et al., , 2018; Lebacher et al., , 2021). To enhance the reconstruction of the weighted network, Cimini et al., 2015b impose constraints on both the in- and out-strength sequences and on the degrees. Their strategy is motivated by recent results showing that the strengths do not encode information about the binary topology (although they are correlated with degrees) and that the degrees are “fundamental” local structural properties of weighted networks (Mastrandrea et al., , 2014). Combining constraints on the degrees and strengths thus greatly enhances the reconstruction of weighted networks since the degrees provide information about the binary topology that strengths do not, enabling to identify better the matrix of link probabilities as well as higher-order properties (Mastrandrea et al., , 2014; Gandy and Veraart, , 2017).

The method proposed by Mastrandrea et al., (2014) requires knowledge of the degrees and strengths of all the nodes, which are not always available. Cimini et al., 2015b note that in financial networks, the in- and out-strengths are usually known while the degrees might be known for a subset of nodes only. To account for these two pieces of information, Cimini et al., 2015b restore to the fitness ansatz. The fitnesses are nodes’ non-topological futures that relate to the ability of nodes to establish connections: nodes with higher fitness attract more connections and are thus likely to become hubs (Squartini et al., , 2018; Mazzarisi and Lillo, , 2017). Given the empirical correlation frequently observed among strengths and degrees, strengths are often used as a proxy for nodes’ fitnesses. To estimate the binary topology, Cimini et al., 2015b thus develop a fitness-induced configuration model that estimates link probabilities using the nodes’ fitnesses and the degrees of only a few nodes. The weights are estimated in a second step using a degree-corrected gravity model that accounts for the sparsity of the adjacency matrix inferred in the first step.

How does one choose which reconstruction method to use? Anand et al., (2018), Lebacher et al., (2021) and Ramadiah et al., (2020) find that the choice of the reconstruction method ultimately depends on the feature of the network one aims to reconstruct, which usually boils down to connectivity structure versus weights. If one cares about inferring links, methods that focus on reconstructing a sparse connectivity structure are better suited. Anand et al., (2018), Lebacher et al., (2021) and Mazzarisi and Lillo, (2017) conclude that the best-performing ones are the degree-corrected gravity model (Cimini et al., 2015b, ), the minimum density (Anand et al., , 2015) and the Bayesian hierarchical fitness (Gandy and Veraart, , 2017). If one cares about inferring the link weights, methods based on MaxEnt or the IPF algorithm perform best. Since financial networks have many link weights of relatively equal size (something that is less likely to be the case in firm-level networks; Bacilieri et al., , 2023), they score well on weight-based similarity measures (Anand et al., , 2015). In their horse races, Anand et al., (2018) and Lebacher et al., (2021) identify the methods developed by Cimini et al., 2015b and Baral and Fique, (2012) to be the best performing. Altogether, the reconstruction method proposed by Cimini et al., 2015b seems to be the best in reconstructing both binary and weighted topological features.

Firm-level network reconstruction.

Welburn et al., (2020) reconstruct the network of listed firms in the US available through a dataset similar to FactSet but covering only their major customers.666 They retrieved the customer-supplier relations from firms’ filings available through the EDGAR database. Therefore, they know the binary topology only partially. To reconstruct the weighted network, they use a two-step procedure. In the first step, they infer missing links using a logistic regression. In the second step, they develop a linear programming method to reconstruct the unknown weights given the links. Since they do not observe the whole economy, they introduce a proxy node that captures the rest of the economy and to which each firm is linked. The cumulative in- and out-flows of the proxy node are then minimised subject to constraints on firms’ revenues and the cost of goods sold. While there are almost 6,000 firms in their network, they only reconstruct the network composed of 1,000 firms due to the high computational complexity of the second step of their procedure. Inoue and Todo, (2019) reconstruct the weighted network of Japanese firms given the binary topology.777 The network is collected by a private company. Although the coverage is extensive, comprising almost 890,000 firms, it is not exhaustive. Firstly, they assume that the link weight is proportional to the supplier and customer’s sales. Subsequently, they re-adjust the estimated weights using the sector-level I-O tables to ensure that if the firm-level network is aggregated at the sector level, it is consistent with national accounts. In a similar fashion and using the same Japanese dataset, Carvalho et al., (2021) assume that the technical coefficient between two firms is proportional to the technical coefficient between the sectors those two firms are in.

Hillman et al., (2021) reconstruct the global network of private and public firms in the ORBIS database. As done in other reconstruction methods, they build the firm-level network so that it is consistent with sector-level I-O data (OECD). In each step, a firm is chosen at random and its sales are split into units that are then sold to different customers. ’s customers are chosen according to the industry they are in based on sector-level I-O tables, meaning that if firm is in industry , its customers need to be in one of the industries to which sells (in the sector-level I-O table). They further calibrate their model on the observation that larger firms tend to have more customers (Bernard et al., , 2019). This feature can be controlled by changing how, at the beginning of each step, firm ’s sales are split into units. For computational reasons, they only use 5,000 firms among the more than 200 million firms in the Orbis database. Hooijmaaijers and Buiten, (2019) reconstruct the supply chain network of the Netherlands using several microdata sources available to the Office of National Statistics. They describe their method as being akin to maximum entropy methods with exact link density (as classified in Squartini et al., , 2018), but they pose additional constraints thanks to the richness of their microdata and to findings in the literature about empirical facts of firm-level supply chain networks. A novel feature of their reconstruction is the disaggregation of firms’ output into different goods.

None of the studies just described can assess how well their method recovers the empirical weighted network because none of them has access to it. Two studies assess their reconstruction method, at least to some extent. First, Reisch et al., (2021) reconstruct a firm-level production network using mobile communication data. To guarantee anonymity, the company providing the data and the country are not disclosed. Roughly speaking, links are inferred by assuming that if two firms communicate with each other, they are involved in a supply-chain relationship. To determine the link direction, they use the national I-O table at the sector level and information about the sectors the customer and supplier are in. A gravity model is then used to estimate the link weights, where a firm’s size is given by its total assets. To assess the reconstruction of the binary topology, they compare to the Hungarian network, whereas to assess the performance of the method regarding the weights reconstruction, they use the Economic Systemic Risk Index and compare with results obtained for Hungary by Diem et al., (2022). They find similarities between results obtained for Hungary and their reconstructed network. Second, Ialongo et al., (2022) develop the stripe-corrected gravity model, which builds on the degree-corrected gravity model (Cimini et al., 2015a, ) by adding constraints on the in-strength of each industry. They test their method on two transaction data made available by two Dutch banks. The assessment is carried out on the degree and strength distributions, degree-strength correlations and average nearest neighbour strength.

4.1 Method

To reconstruct the weighted network given the binary topology, we use the conditional maximum entropy ensemble reconstruction method developed by Parisi et al., (2020). We do not use any of the previously developed methods for reconstructing firm-level networks because either they are too computationally expensive (Welburn et al., , 2020; Hillman et al., , 2021), demand too many data inputs that we do not have (Hooijmaaijers and Buiten, , 2019) or would imply constraining the firm-level network with sector-level I-O tables (Inoue and Todo, , 2019; Ialongo et al., , 2022). We disregard the latter methodologies because we think using sector-level data in the way proposed by Inoue and Todo, (2019) or in the spirit of Ialongo et al., (2022) could bias the reconstruction in unwanted ways given the underlying differences in accounting standards between national I-O tables and firms’ financial statements (see Appendix A.3, but also Bacilieri et al., , 2023).

Parisi et al., (2020) develop a maximum entropy method that reconstructs an ensemble of likely weighted networks given some prior information about the binary ensemble and aggregate information about each node. The procedure is flexible in that it allows to use of an observed binary topology or to infer it in a previous step and account for the additional uncertainty. They proposed two methods that use different constraints. One method constrains the in- and out-strength sequences, while the other one constrains the expected link weights (and the in- and out-strengths indirectly). We choose the second method for two reasons. First, it is computationally more efficient since it involves solving (the number of links) decoupled equations, while the method constraining the in- and out-strengths require solving coupled equations, where is the number of firms. Second, the authors show that it predicts the weights better compared to the model constraining the in- and out-strengths.

The method consists of two steps. The first step constrains the in- and out-strengths (total intermediate expenditure and sales) of each firm and determines the values of the expected link weights used as constraints in the second step. As discussed in Section 4, MaxEnt reconstructs the weights best among the other methods (Anand et al., , 2018; Lebacher et al., , 2021); thus, MaxEnt is used in the first step. The second step allows us to account for any prior information about the binary topology and generates an ensemble of weighted networks compatible with this information and with the constraints on the expected link weights.

As discussed, MaxEnt assumes a fully connected network; however, the conditional maximum entropy method assumes no self-loops. Additionally, in our case, we know the binary topology. To redistribute the weights corresponding to , where is the edge set, we employ the IPF algorithm. The IPF algorithm redistributes the weights in an iterative procedure until the constraints on the in- and out-strengths are met (see Appendix B.1). Parisi et al., ’s (2020) method turns the IPF algorithm into a probabilistic method and allows calculating confidence intervals around each reconstructed weight. We give a brief outline of the method below and describe it in detail in Appendix B.1.

First step.

The method derives values for the expected link weights to enforce as constraints in the second step. The values of the weights are derived by solving the MaxEnt problem, which maximises an entropy-like functional subject to constraints on intermediate sales and costs of each firm. The value of each weight is given by

where is the total weight of the empirical network.

Second step.

The method maximises the conditional entropy defined over the probability density function of the weighted networks compatible with the prior on the binary ensemble and subject to constraints on the expected weights. Solving the conditional maximum entropy problem yields that the probability of observing a weight given that there is a link between and is of exponential form with parameter (which also corresponds to the Lagrange multiplier):

| (5) |

To find the values of the ’s, one maximises the log-likelihood function, which leads to the first order conditions

| (6) |

Since for each link the expected weight , the Lagrange multipliers are given by

| (7) |

We set .

Confidence interval on the expected edge weight.

For each expected weight, the confidence interval is . The lower bound is given by

| (8) |

where is a desired confidence level and the upper bound is given by

| (9) |

We set . We refer to Appendix E in Parisi et al., (2020) for the derivation.

4.2 Assessing the reconstruction

We assess how well the reconstruction method can recover the empirical network at three scales. First, we look at microscale quantities: weights, and technical and allocation coefficients. Second, we evaluate the reconstruction of higher-order properties (i.e., multipliers): the output multipliers and the influence vector. Third, we turn to macroscale properties and use a general equilibrium I-O model to study how the propagation of shocks through the network affects GDP volatility. We conclude this section by defining the statistical indicators used to compare the empirical and reconstructed quantities.

4.2.1 Weights

4.2.2 Higher-order properties

We look at two higher-order properties widespread in the economic literature: the output multipliers and the influence vector. These are two centrality measures that quantify firms’ contributions to economy-wide fluctuations.

The output multipliers.

The output multipliers are derived from the Leontief model (Miller and Blair, , 2009) and are defined as

| (10) |

where is the identity matrix and a vector of ones, both of appropriate size. The output multiplier captures the upstream propagation channel of an exogenous shock to a firm’s final demand and its economy-wide impacts (where final demand increases by one monetary unit; Miller and Blair, , 2009). It can also be seen as the average length of a firm’s production chain (McNerney et al., , 2022; Fally, , 2012; Miller and Temurshoev, , 2017). The higher the output multiplier is, the longer the production chain is on average and the greater the impact of a change in a firm’s final demand is on the whole economy.

The influence vector.

The influence vector is derived from the Cobb-Douglas model proposed by Acemoglu et al., (2012). The influence vector is defined as

| (11) |

where is the matrix of input shares with being the share of input used in ’s production process (), is the share of labour and is the number of firms.

Contrary to the output multipliers, the influence vector captures the downstream propagation channel of TFP shocks and it gauges the contribution of firms to fluctuations in aggregate GDP. Positive TFP shocks can be thought of as firms’ innovating their production processes and becoming more efficient in using their inputs. The influence vector is equivalent to a Reverse Weighted PageRank with a damping factor equal to .

4.2.3 Macroscale properties

As highlighted by recent crises and natural disasters, assessing how different shocks affect the economy is of paramount importance to be better prepared in preventing or alleviating crises. Therefore, after assessing the weights and the multipliers, we study how supply-side shocks at the firm level propagate through the network to downstream firms, ultimately leading to fluctuations in aggregate GDP.

Supply-side shocks and aggregate volatility.

We model supply shocks as shocks to firms’ TFP. We use the model developed by Acemoglu et al., (2012) and refer to the paper for a derivation. In the competitive equilibrium, aggregate volatility is given by

| (12) |

where is the influence of firms (Equation 11), is the TFP shock of firm and is an i.i.d. random variable with mean zero and bounded variance. Equation 12 shows that productivity shocks at the firm level affect aggregate value-added through the production network. Initially, the shock propagates to the customers of the affected firm and, subsequently, propagates downstream to the customers’ customers and so on, potentially spreading through the whole supply chain network.

Note that the model gives a static representation of the economy in equilibrium and firms’ input shares are exogenous; therefore, the network structure and hence the influence vector are constant over time. We use Equation 12 to assess the impact of firms’ TFP shocks on GDP volatility using either the empirical or the reconstructed weighted network given the TFP shocks.

Simulating TFP shocks.

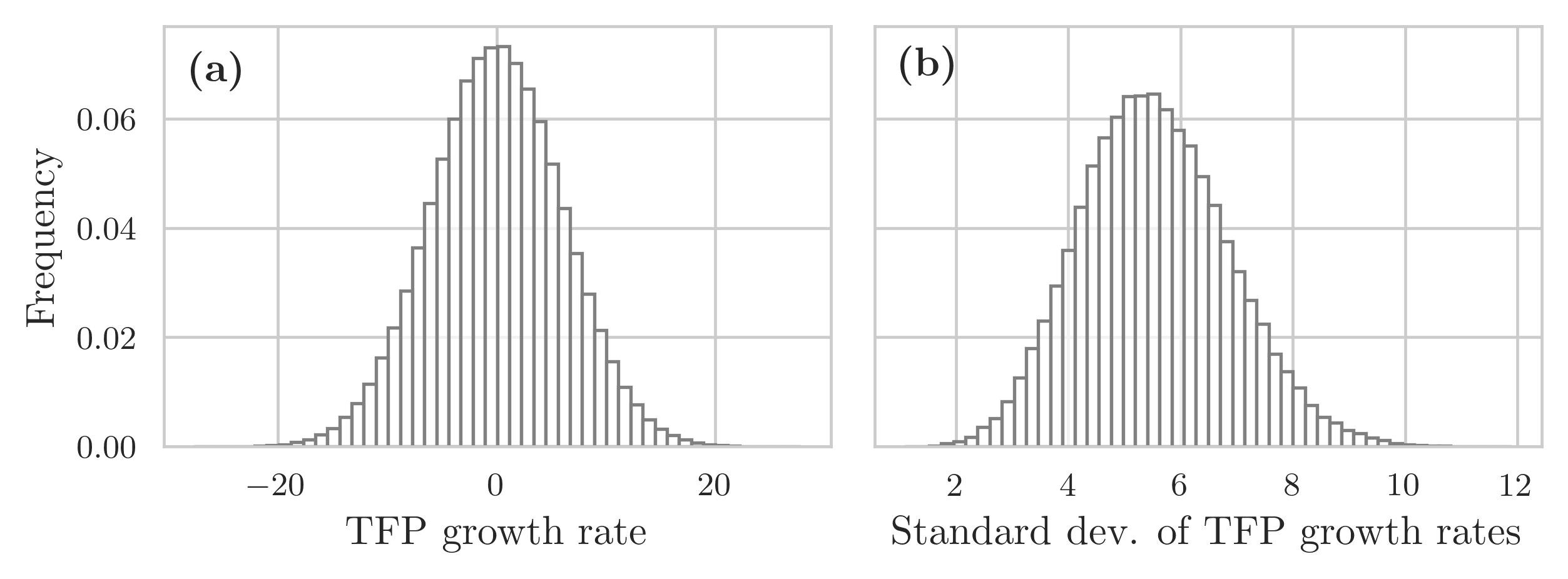

To estimate TFP shocks, we cannot use an econometric technique (e.g., Magerman et al., , 2016) because it requires knowledge of several variables that we do not observe for Ecuador. Besides requiring all the variables describing a firm’s production function, the estimation of TFP requires a time series of these variables. Since our goal is not to empirically validate the economic model but to assess the discrepancy in the predicted GDP volatility when the reconstructed influence vector is used instead of the empirical one, we simulate firm-level TFP shocks. For FactSet, we do not perform this test since it would entail estimating TFP, which is outside of the scope of this paper.

We simulate TFP shocks from a normal distribution with mean zero and standard deviation of 6. We chose a zero mean in line with the empirical mean reported for the Belgian production network by Magerman et al., (2016). Since they do not report the variance, we set the variance to 6 so that GDP volatility, calculated using the model with the true network, matches the observed country-level volatility.888 To calculate the GDP volatility in Ecuador, we use data from the IMF; available at https://data.imf.org/?sk=388DFA60-1D26-4ADE-B505-A05A558D9A42&sId=1479331931186. We use nominal GDP since our data are not adjusted for inflation. Since we simulate 10 years, we calculate GDP volatility for the period 2005-2015, which is 6.35%. We tried different parametrisations of the normal distribution, which do not match the volatility in the empirical data, and results do not change, at least qualitatively. We set the TFP shock of the proxy sector equal to the median of the TFP shocks of firms that were excluded from our test network. We simulate 10 time periods. Figure 2 shows the distribution of the simulated TFP growth rates in Panel (a) and the distribution of their standard deviation in Panel (b). Once we simulate the TFP volatilities, we use Equation 12 to predict the fluctuation in aggregate GDP using either the empirical or the reconstructed influence vector. We then compare the empirical volatility with that predicted by the reconstruction.

4.2.4 Statistical indicators

To compare how well the reconstruction method can recover the quantities defined in Section 4.2.1, 4.2.2 and 4.2.3, we employ metrics that are standard in the literature: the -error, the root-mean-squared error (RMSE), the mean and median absolute error (MAE and MedAE, respectively) and the cosine similarity.

The -error assesses the degree to which constraints on intermediate sales and costs are violated. It is defined as

is firm ’s in-strength in the reconstructed network and its out-strength in the reconstructed network; quantities with a ∗ refer to observed, empirical values.

In what follows, we define the error measures using the technical coefficients, but they similarly apply to any other quantity of interest. We do not use the RMSE, the MAE and the MedAE to assess the raw weights because their distribution has heavy tails. For the technical and allocation coefficients, and the multipliers, we further normalise the metrics to allow their comparison across variables that have different scales. We rescale by , the difference between the maximum and minimum value (excluding the zeros) of the empirical quantity of interest. Our rescaled measures compare the variation in the residuals to the range of the empirical data. For instance, a normalised RMSE of 0.1 means that the variation in the residuals is 10% of the range of variation of the empirical data. The lower the normalised error metric is, the better the reconstruction is. The normalised root-mean-square error is given by

where is the number of links. The normalised mean absolute error is given by

The normalised median absolute error is defined as

The cosine similarity is defined as

4.3 Results: link weights

In this section, we show the results of the reconstruction method for the weights, and the technical and allocation coefficients. We start by discussing the results for our test network, Ecuador, and then show the results for FactSet, for which we do not know the ground truth.

We compare weights (normalised or not) for firms only and not those of the proxy node since the proxy node can be thought of as a sink node and does not meaningfully represent either a firm or a sector. For parsimony, we show plots for one of the 50 randomised reconstructions (always the same one throughout the paper) since they all yield virtually identical results; the same holds for the summary statistics. Regarding the statistical indicators described in Section 4.2, we compute them for each of the 50 randomised test networks and report the average value of each metric across the 50 randomised networks.

4.3.1 Ecuador

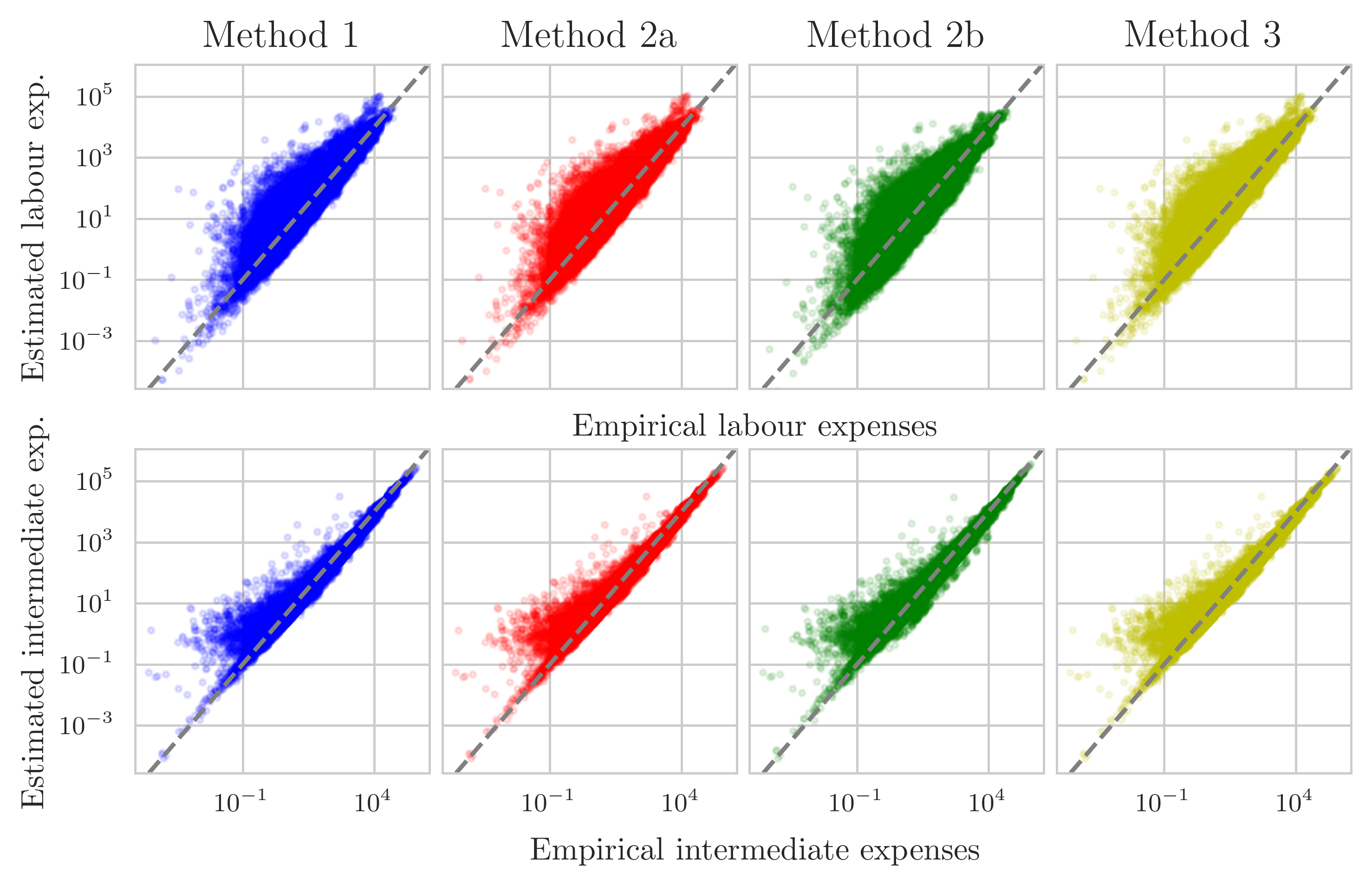

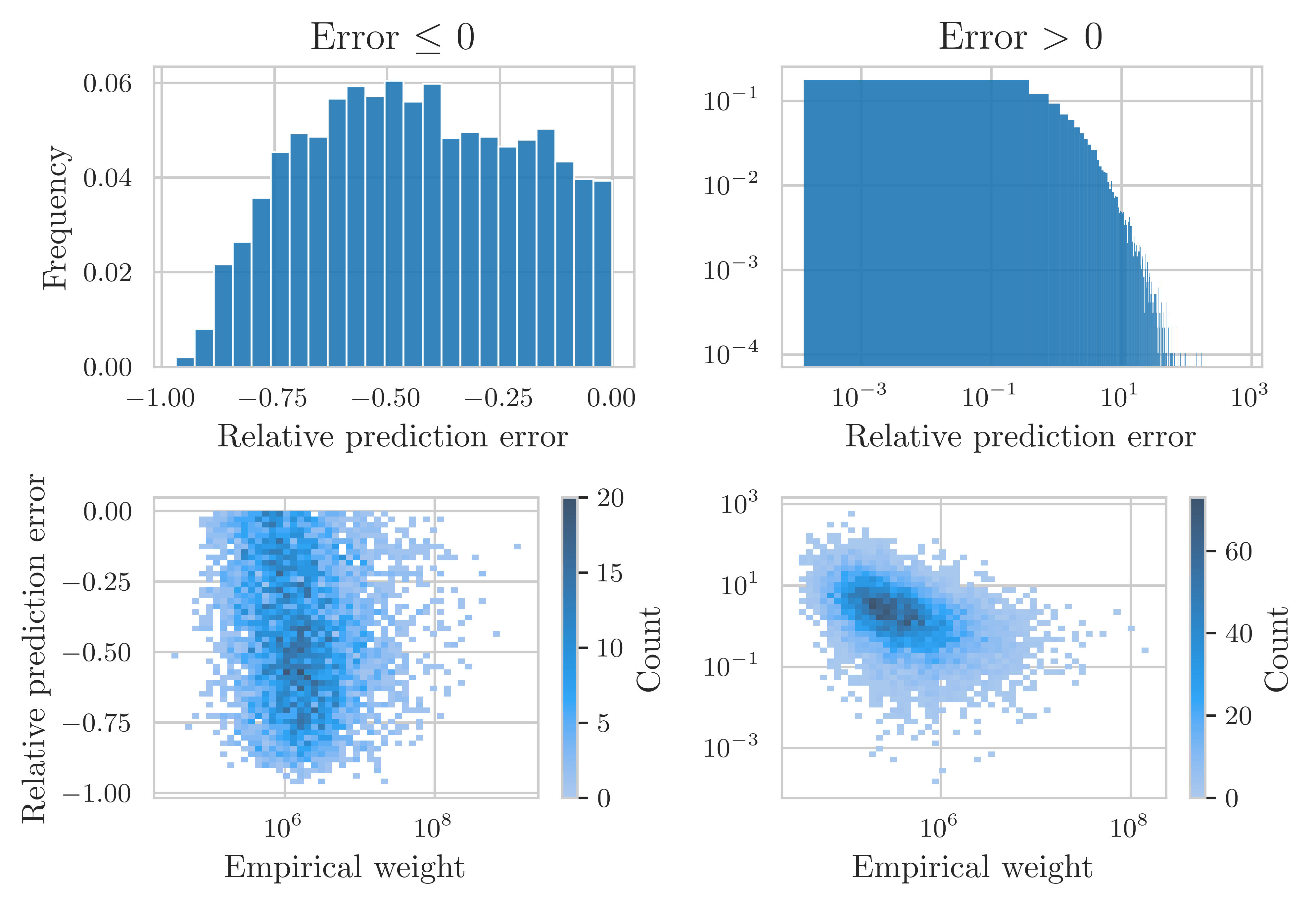

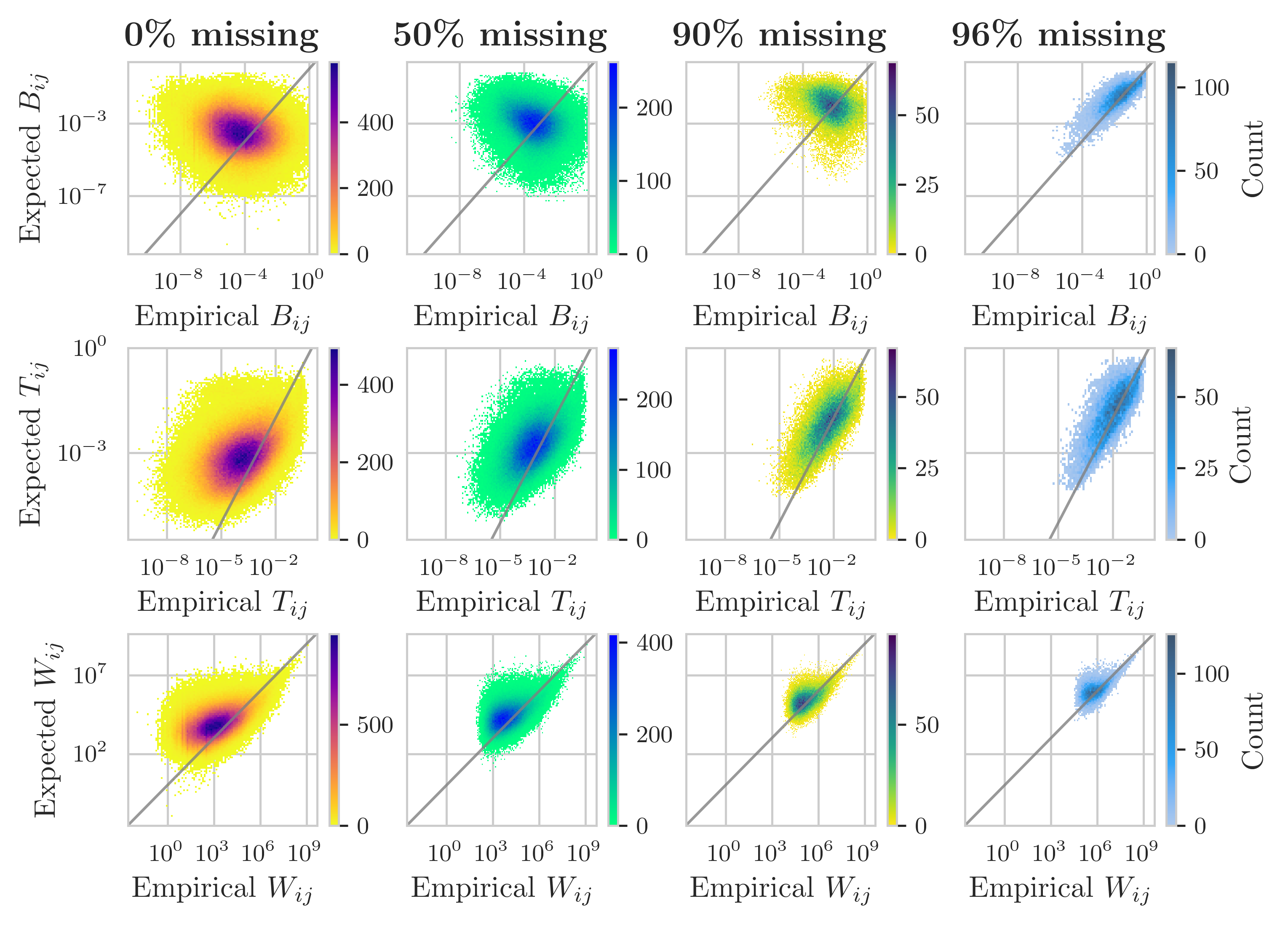

The constraints on the intermediate sales and costs are always satisfied (-error ). The reconstruction of individual weights is rather poor, as shown in Figure 3a; perfect prediction is achieved when points lie on the 45-degree line (grey dashed line). The reconstruction method tends to underpredict weights of high values and overpredict weights with intermediate or low values, although there is significant dispersion. (We show the histogram of the relative prediction errors and the empirical weights against their prediction errors in Figure C.2.) On average, 47% of the weights fall in the 50% confidence interval (CI).

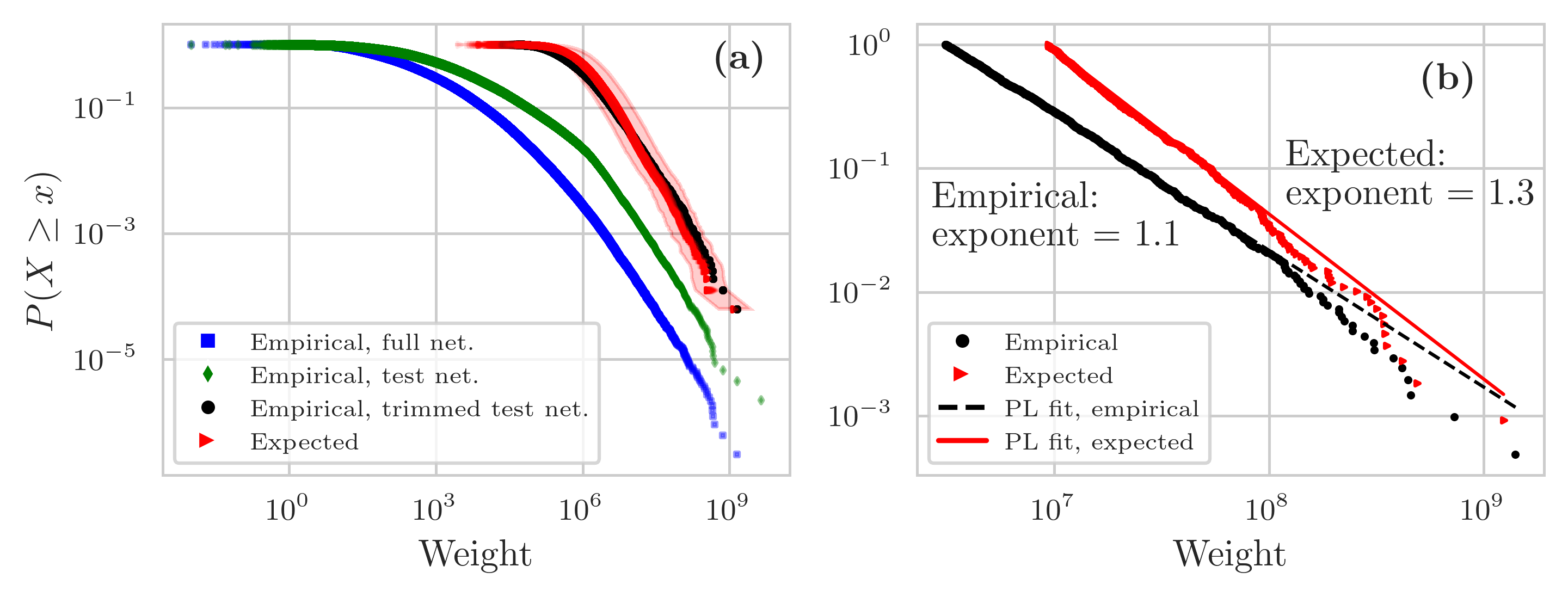

Although the reconstruction cannot recover individual weights particularly well, the weight distribution is recovered quite well. The weight distribution has heavy tails in both the empirical and the reconstructed networks (Figure 3b; see Figure C.1a for a comparison of the weight distribution across the 50 randomised networks, the empirical test network and the full network). As expected from maximum entropy methods, the expected weight distribution is less heterogeneous than the empirical distribution. Bacilieri et al., (2023) find that the weight distribution is likely to follow a power-law with an exponent that varies between 1.0 and 1.4 depending on the country, year and estimation method. Therefore, we check whether we can recover a similar power-law exponent. We can recover it pretty well (see Figure C.1b). The power-law exponent is 1.1 for the empirical weight distribution and 1.3 for the reconstructed one.999 To fit a power-law distribution to our data, we use the method of Clauset et al., (2009) since (1) it yields a single exponent estimate and (2) it is the most widely used estimator in the literature. See Bacilieri et al., (2023) for an in-depth discussion. Bacilieri et al., (2023) use also the estimators developed by Voitalov et al., (2019), which are based on extreme value theory. We abstain from such an analysis in this paper. Although the exponent of the reconstructed distribution is slightly higher, it still implies a divergent second moment.

In Table 2, we do not report the RMSE, MAE or MedAE for the weights since there is too much variation to obtain a meaningful metric; additionally, the weights likely have a diverging second moment. Therefore, we report only the cosine similarity, which is 0.93.

| Type | RMSE | MAE | MedAE | Cosine similarity |

|---|---|---|---|---|

| Weight | – | – | – | 0.928 |

| (0.006) | ||||

| Technical | 0.081 | 0.041 | 0.013 | 0.723 |

| (0.001) | (0.000) | (0.000) | (0.004) | |

| Allocation | 0.105 | 0.054 | 0.019 | 0.758 |

| (0.001) | (0.000) | (0.000) | (0.003) |

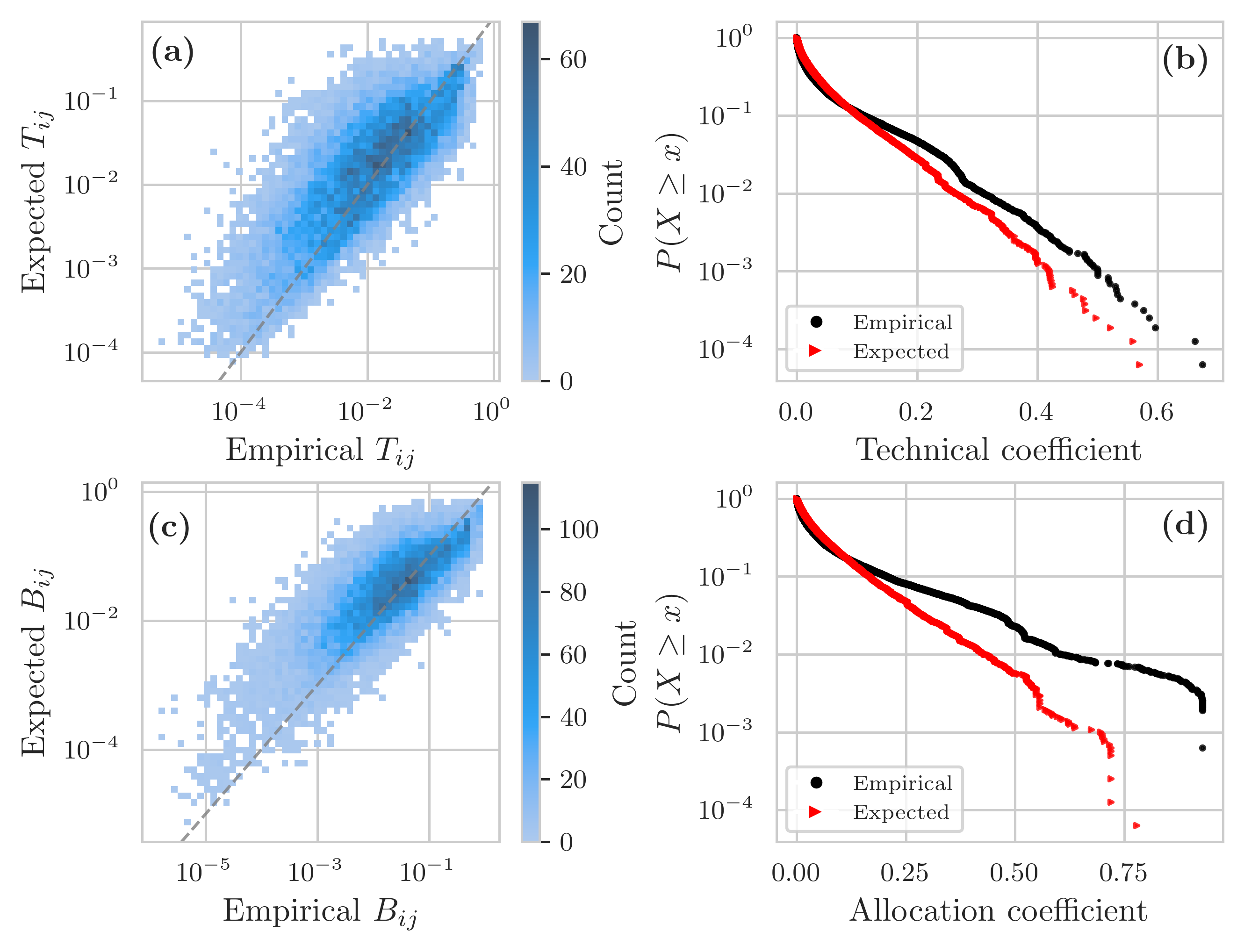

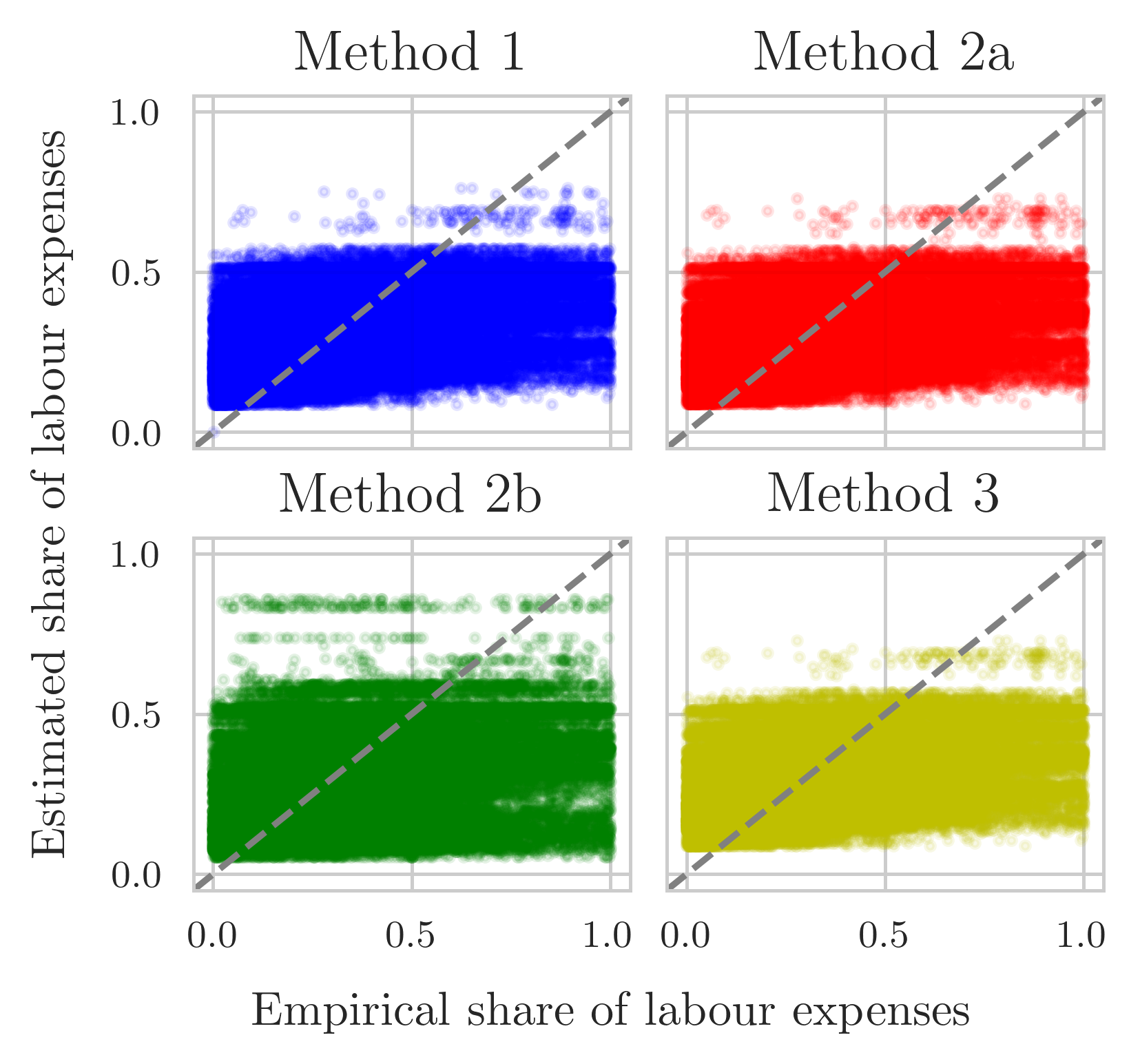

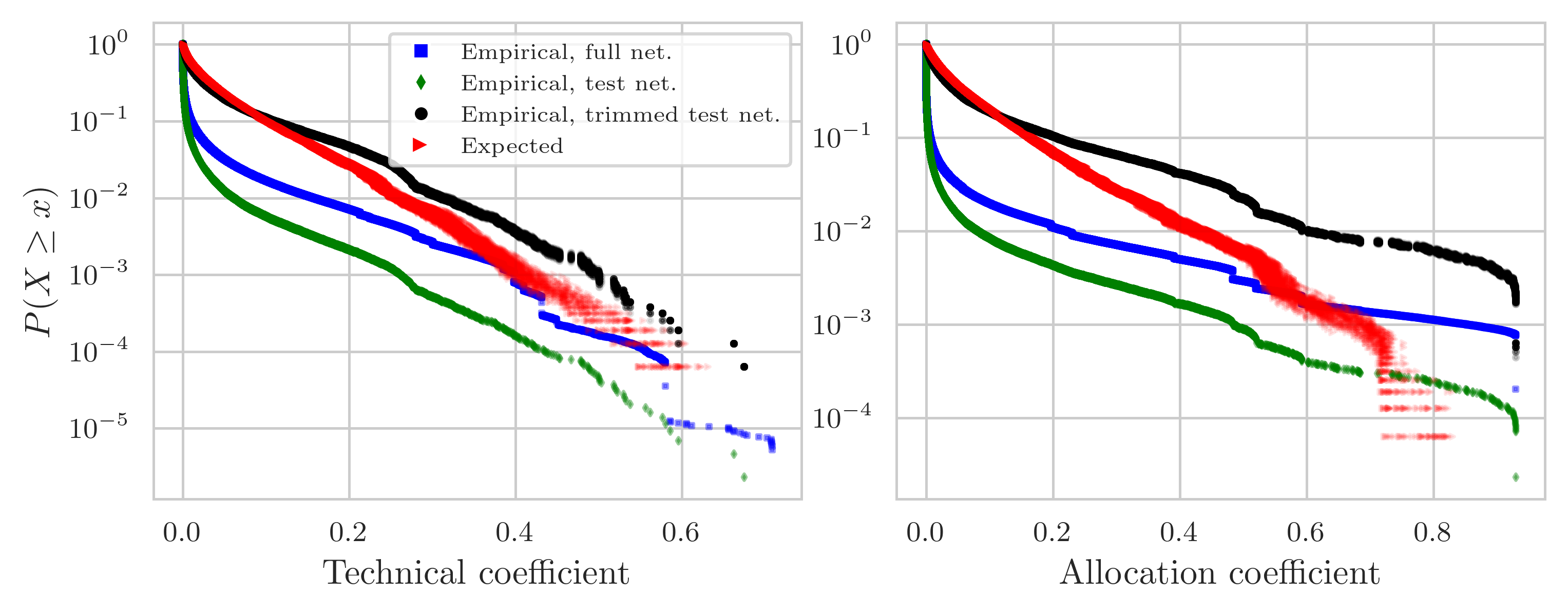

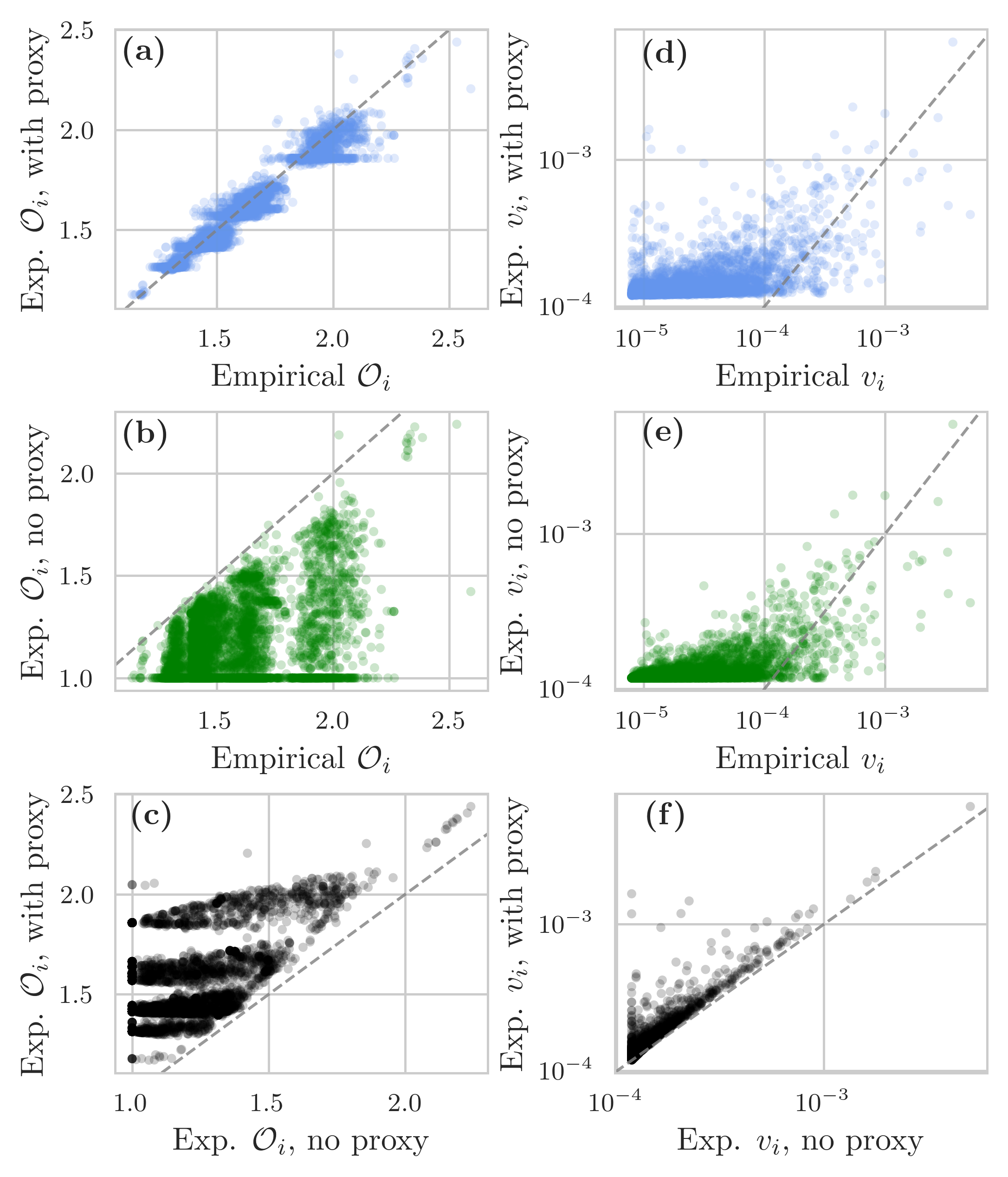

Figure 4a and 4c show, respectively, the empirical technical and allocation coefficients on the x-axis and their expected values on the y-axis. As for the weights, the reconstruction method does not perform particularly well in recovering either of the coefficients. Although less pronounced for the coefficients than for the weights, the method tends to overpredict coefficients of small values and underpredict coefficients with high values, again with considerable dispersion. This is further highlighted in Figure 4b and 4d, showing the empirical and reconstructed CCDF of the technical and allocation coefficients, respectively. Figure 4b and 4d further show that we can reconstruct the technical coefficients better, which also have smaller error metrics (Table 2) and for which we can recover the moments more accurately (Table 3). However, the cosine similarity is slightly higher for the allocation coefficients: 0.76 compared to 0.72.

| Technical coefficients | Allocation coefficients | ||||

|---|---|---|---|---|---|

| Empirical | Expected | Empirical | Expected | ||

| Mean | 0.037 | 0.038 | 0.071 | 0.065 | |

| Median | 0.010 | 0.016 | 0.019 | 0.031 | |

| Standard dev. | 0.067 | 0.057 | 0.132 | 0.088 | |

4.3.2 FactSet

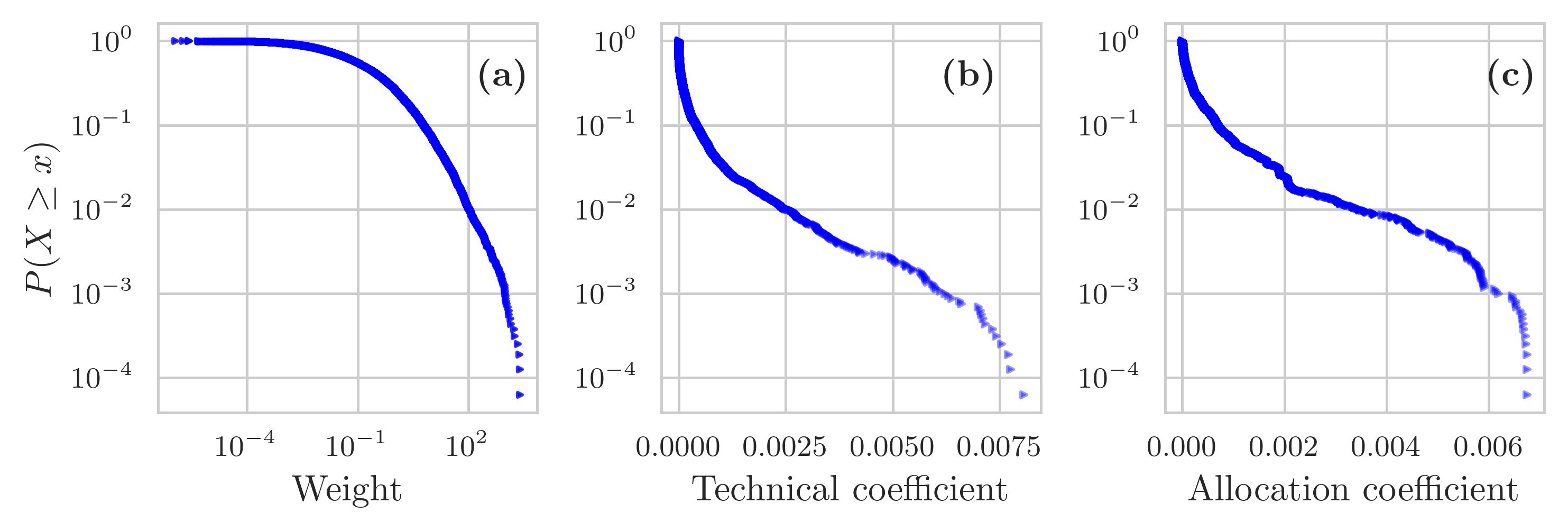

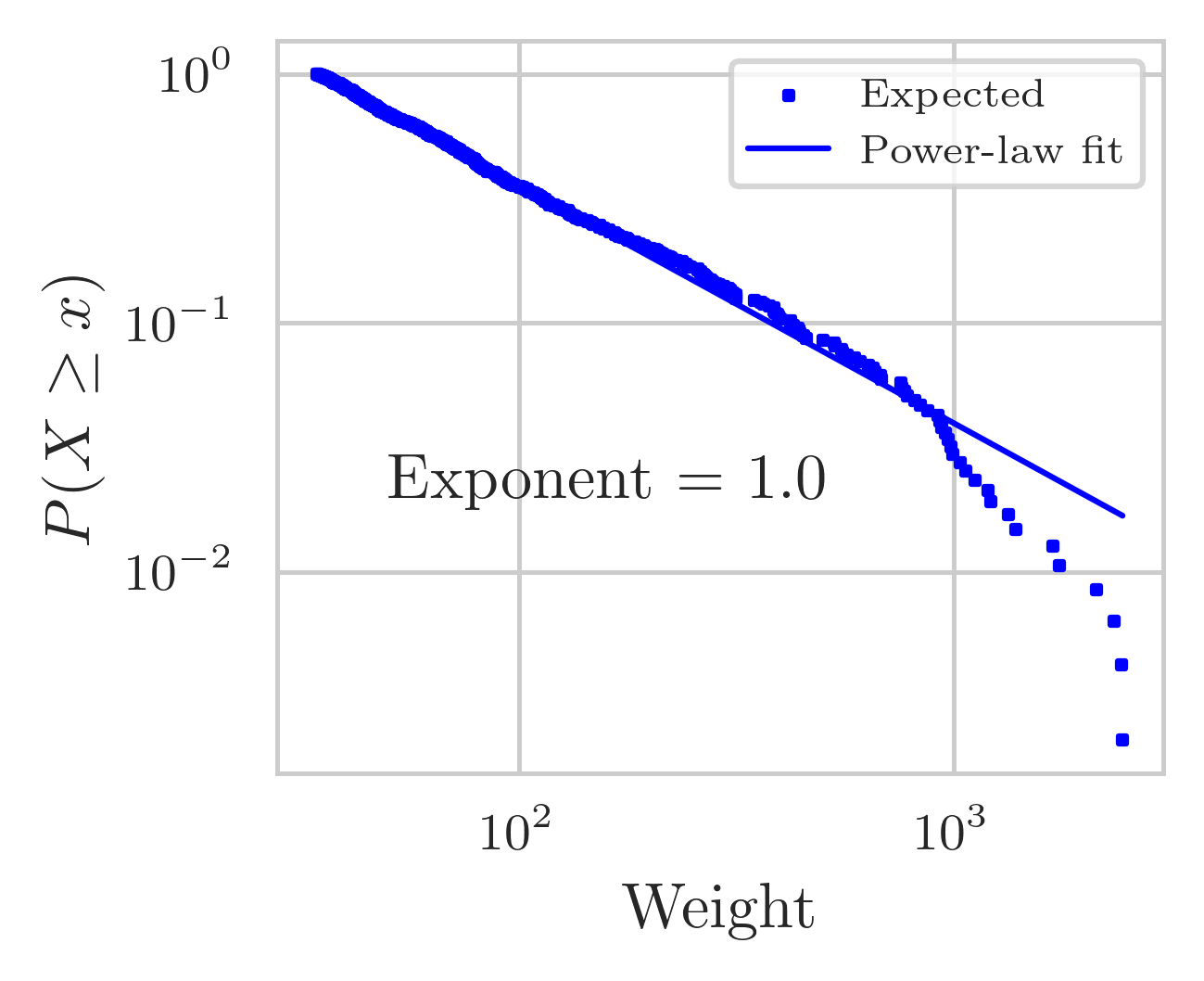

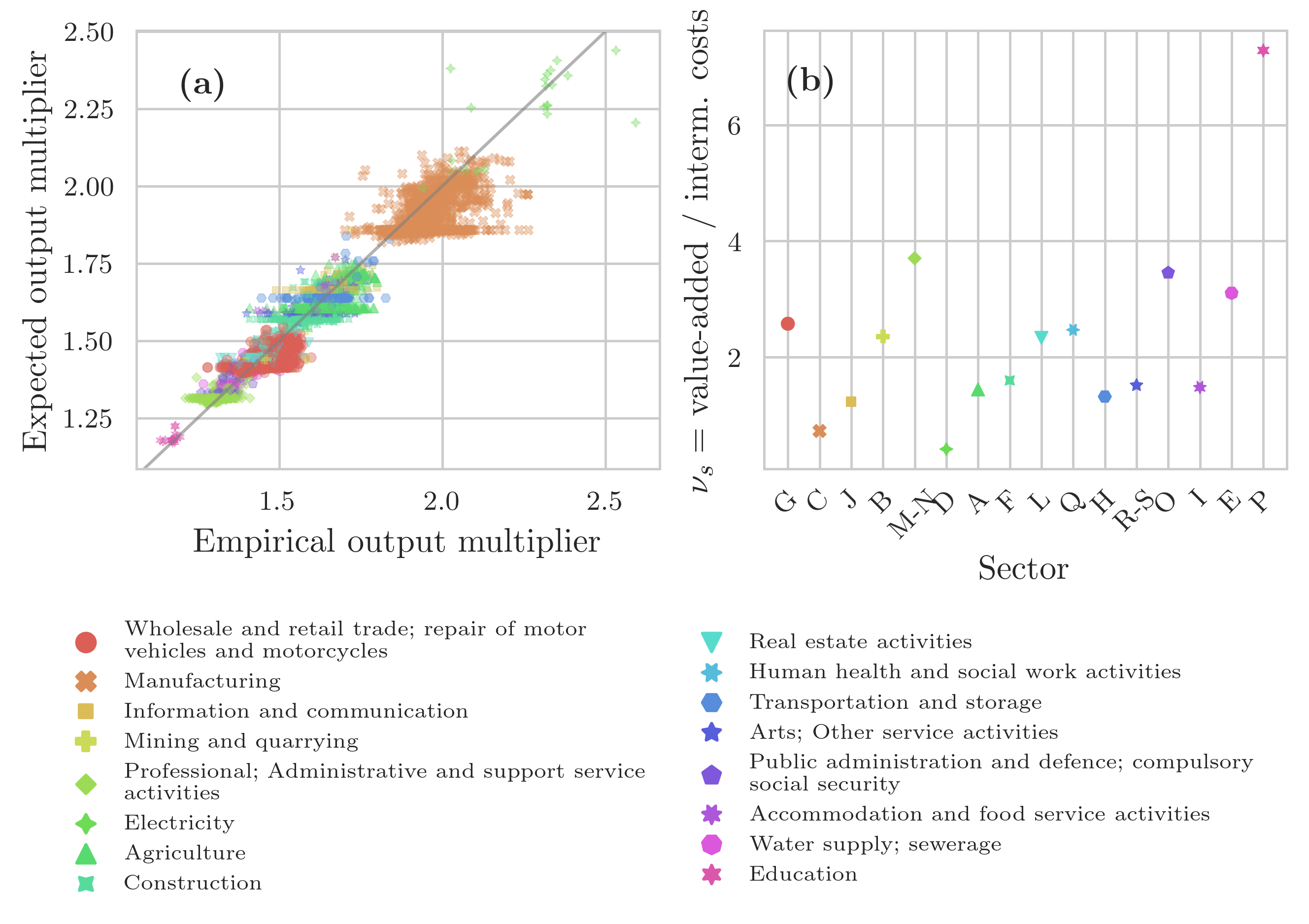

The constraints on the total intermediate expenditure and sales are satisfied (-error ). Figure 5a shows the reconstructed weight distribution, which visually appears to have heavy tails. As done for Ecuador, we fit a power-law distribution. The estimated power-law exponent is lower than that recovered for Ecuador (1.0 for FactSet and 1.3 for Ecuador, see Figure C.3) and on the lower end of what is observed for other supply chain networks (Bacilieri et al., , 2023). The reconstructed technical coefficients (Figure 5b) and allocation coefficients (Figure 5c) have a narrow range of variation and tend to be much smaller than those reconstructed for Ecuador. For FactSet, the technical coefficients reach a maximum value of approximately 0.008, while for the expected Ecuadorian network, they can be as high as 0.570. Similarly, the allocation coefficients are not higher than 0.007 in FactSet, while in Ecuador, they reach a maximum value of 0.778.

Given the data collection method of customer-supplier relations in FactSet, there is a bias towards observing links with customers that account for 10% or more of a firm’s annual revenues. Therefore, we would expect the CCDF of the allocation coefficients to have most of the mass around, or at the very least include this 10% threshold. Instead, the maximum value is around 0.7%, well below this threshold. The average expected allocation coefficient is while the median is (Table 4), both of which are three to four orders of magnitude smaller than what we would have expected given the data collection method.

| Expected | ||

|---|---|---|

| Technical coefficient | Allocation coefficient | |

| Mean | 2 | 3 |

| Median | 3 | 8 |

| Standard dev. | 5 | 6 |

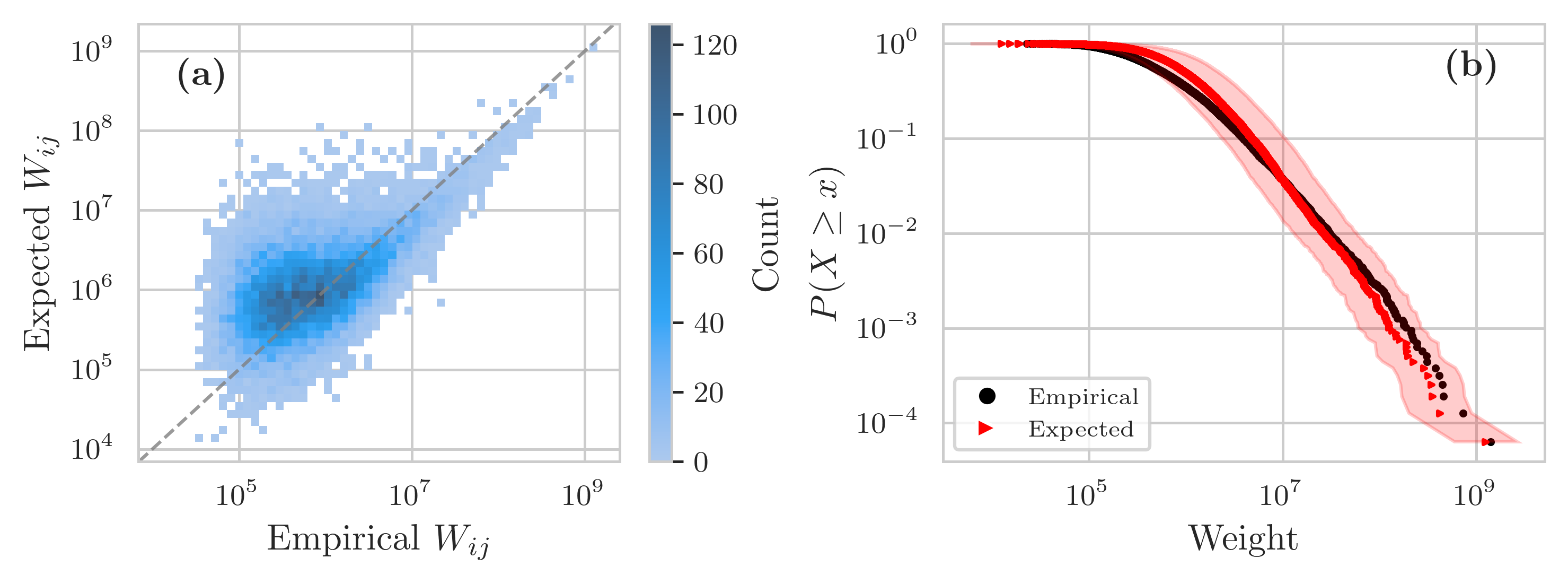

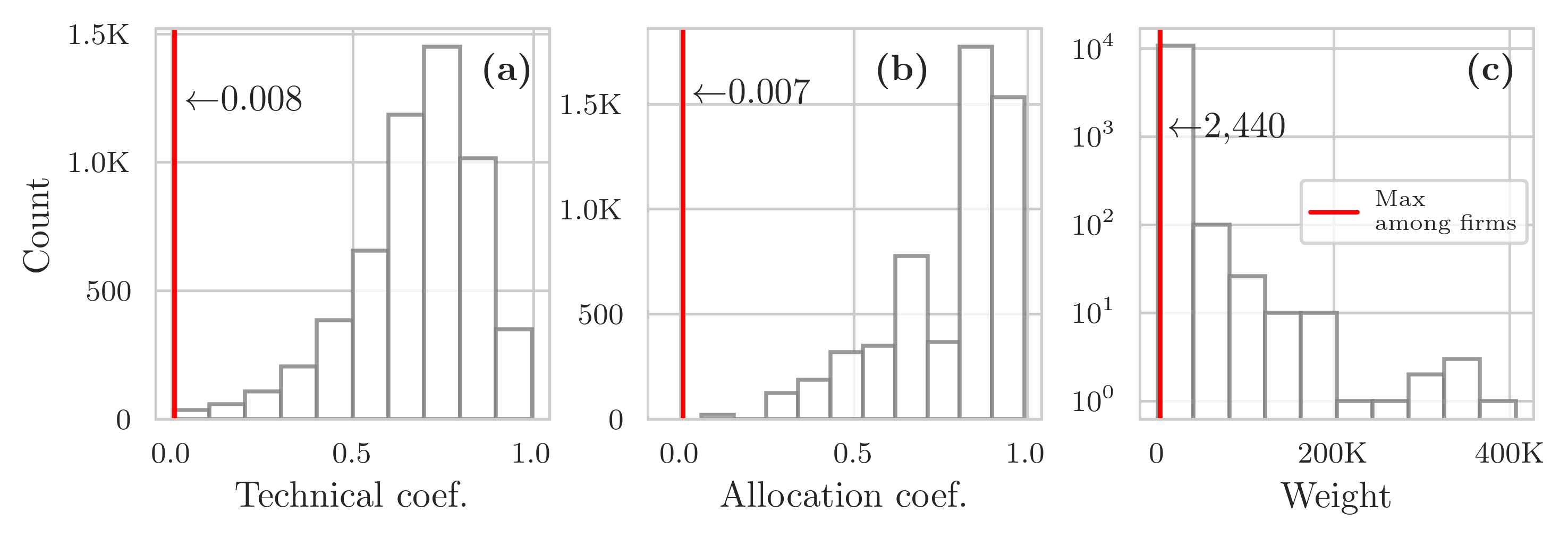

All three quantities have a narrow range of variation and are smaller than expected because total intermediate sales and expenditure of the proxy node (which represent the constraints that need to be satisfied in the weights allocation) are much bigger than those of the other firms. The proxy node accounts for 80% of intermediate expenditure and 75% of intermediate sales. To compare, in Ecuador, the proxy node accounts for 29% and 14%, respectively. Therefore, in FactSet, firms make most of their trades with the proxy node (Figure 6). The maximum transaction value for transactions between firms and the proxy node is $407 million. But, the overall maximum is between the proxy node and itself, where it is $48 billion, 3 orders of magnitude bigger than the maximum value among firms as well as among firms and the proxy node. Consequently, the coefficients representing trades among firms are much smaller than those representing the trades between firms and the proxy node, as shown in Figure 6.

4.3.3 Discussion

Since the other studies that reconstruct firm-level production networks do not assess how their network reconstruction method performs on reconstructing weights, technical and allocation coefficients (Inoue and Todo, , 2019; Welburn et al., , 2020; Hooijmaaijers and Buiten, , 2019; Reisch et al., , 2021; Ialongo et al., , 2022; Hillman et al., , 2021), we cannot compare our results with these studies. Moreover, although several studies assess network reconstruction methods on the international trade network (ITN) or financial networks, few assess the reconstruction of the weights. Most of the studies look at higher-order network properties or dynamic indicators of systemic risk, which we discuss in Section 4.4.

Table 5 shows a comparison of our results with those of the literature. Parisi et al., (2020) test the reconstruction method on the ITN and the Electronic Market for Interbank Deposits (e-MID). They find a similar percentage of empirical weights that fall in the 50% CI. For the e-MID network, depending on the year, between 35% and 55% of the empirical weights fall in the 50% CI, while around 30% of the weights fall in the 50% CI for the ITN. They find that the empirical and expected link weights have a Pearson correlation of 0.50 for the e-MID and 0.75 for the ITN. The only other study we could find providing a comparison metric for link weights is Ramadiah et al., (2020). The authors test several reconstruction methods on Japan’s bipartite bank-firm credit network. For the most disaggregated network, their reconstruction yields a cosine similarity of around 0.68 for the MaxEnt method (for bi-partite networks) and of 0.63 for the configuration fitness model with weights allocated using the IPF algorithm; these are lower than what we find for the weights but similar to our results for the technical and allocation coefficients.

| Data set | Method | Quantity | Pct in 50% CI | Measure | Score | Source | ||

|---|---|---|---|---|---|---|---|---|

| Ecuador SC | CReM | Weight | 47% | Cosine | 0.93 | This paper | ||

| Ecuador SC | CReM |

|

Cosine | 0.72 | This paper | |||

| Ecuador SC | CReM |

|

Cosine | 0.76 | This paper | |||

| ITN | CReM | Weight | 30% | Pearson | 0.75 | Parisi et al., (2020) | ||

| e-MID | CReM | Weight | 35-55% | Pearson | 0.50 | Parisi et al., (2020) | ||

|

MaxEnt | Weight | Cosine | 0.68 | Ramadiah et al., (2020) | |||

|

BFiCM + IPF | Weight | Cosine | 0.63 | Ramadiah et al., (2020) |

While the power-law exponent of FactSet’s weight distribution is in the ranges of what had been found for other supply chain networks (Bacilieri et al., , 2023), the reconstructed weights and coefficients among firms are much smaller than expected. There are two main factors that deteriorate the quality of the reconstruction and act mainly through the constraints on intermediate sales and expenditure: the data cleaning procedure and the data imputations. On the one hand, the data cleaning procedure implies that we had to exclude many firms from the network (see Appendix A.1.4); this leads to (1) a higher share of the proxy node in the economy and (2) excluding many existing supply-chain relations. On the other hand, the data imputations concerning final demand and labour costs affect the values of firms’ intermediate sales and expenditures. Because firms report the cost of goods sold, which often includes labour costs, we do not always know intermediate costs exactly. Similarly, firms disclose their revenues (intermediate sales plus sales to final demand), so for all firms, we do not know their intermediate sales exactly. As shown in Appendix A.1.2, labour costs tend to be overestimated. Although we cannot test whether final demand is over or underestimated, we think we are very likely overestimating it for the majority of firms. The main reason for overestimating final demand is the use of national I-O tables at the sector level, which have a very different treatment of the wholesale and retail sectors compared to firm-level data. National accounts treat wholesale and retail as “pass-through” sectors, accounting only for the trade margin they make and re-distribute the rest of their output among the other industries.101010 If wholesale is trading service goods, then all of its output is distributed to other products. The final demand of these other industries thus becomes (fictitiously) higher. In firm-level data quite the opposite happens, with many firms selling to retail and wholesale firms that then sell to final demand. We refer to Appendix A.3 and Bacilieri et al., (2023) for a longer discussion on differences between national accounts and firm-level data.

The data cleaning and data imputation problems just discussed imply that the constraints on intermediate sales and expenditure of the proxy sector are much bigger than those of other firms. Therefore, to satisfy the constraints posed in the maximum entropy procedure, the weights allocated to the proxy node need to be much bigger than those among firms, meaning that firms buy most of their inputs and sell most of their output to the proxy node. This deteriorates the reconstruction of the weights, and of the technical and allocation coefficients among firms.

Lastly, the findings for both Ecuador and FactSet suggest that additional mechanisms, not captured by the constraints we pose, may be at work that are essential to the formation of network weights. Further unravelling what these mechanisms are could improve the reconstruction.

4.4 Results: higher-order and macroscale properties

First, this section discusses the results for the output multipliers and the influence vector; we start with Ecuador and then FactSet. Second, we show the results for aggregate volatility. We do not assess aggregate volatility for FactSet as that would entail estimating TFP using an econometric technique such as that outlined in Magerman et al., (2016), which is outside of the scope of this paper. We conclude this section with a discussion.

4.4.1 Multipliers

Ecuador.

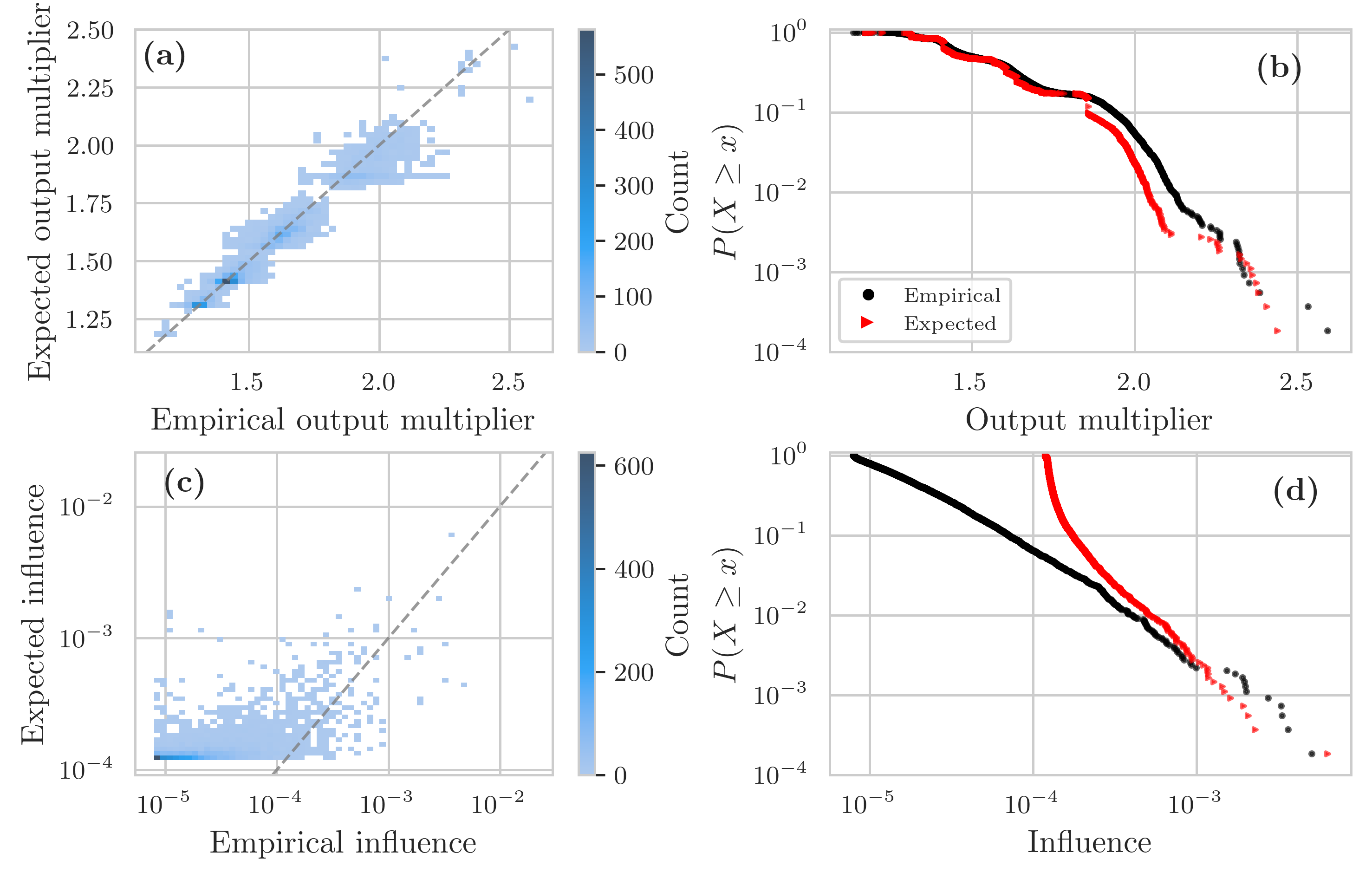

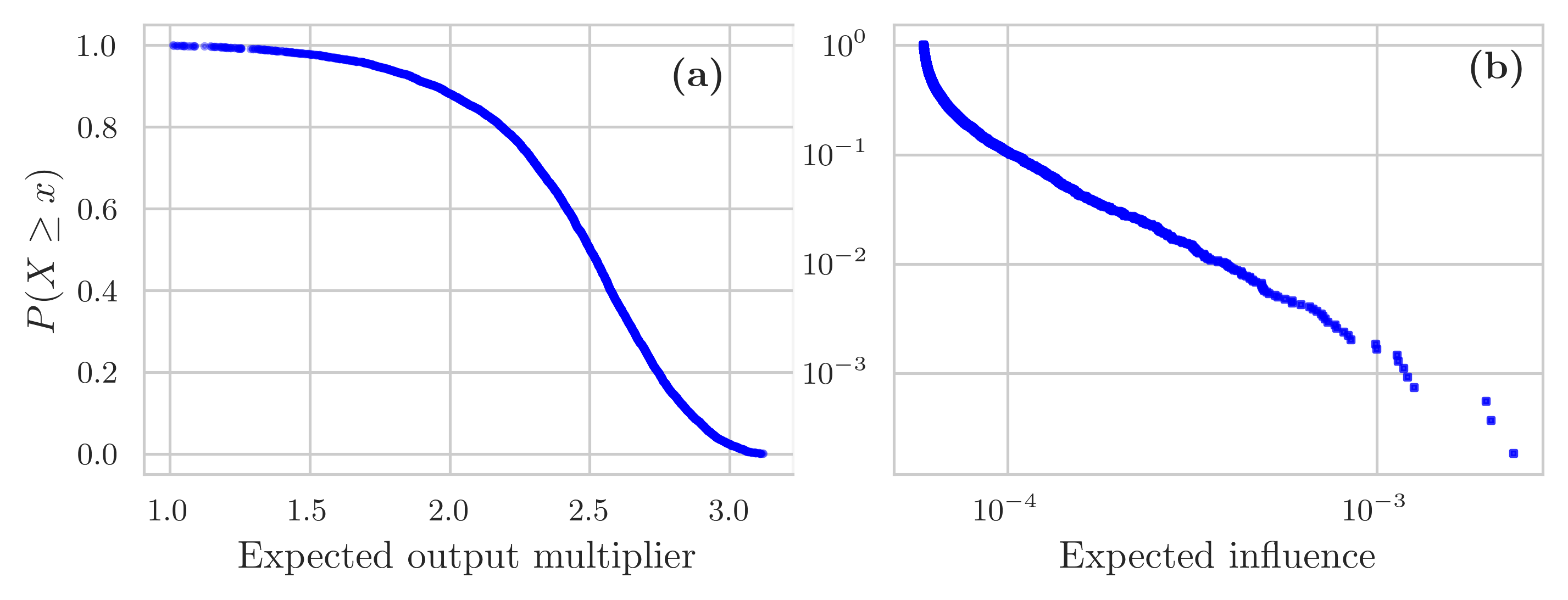

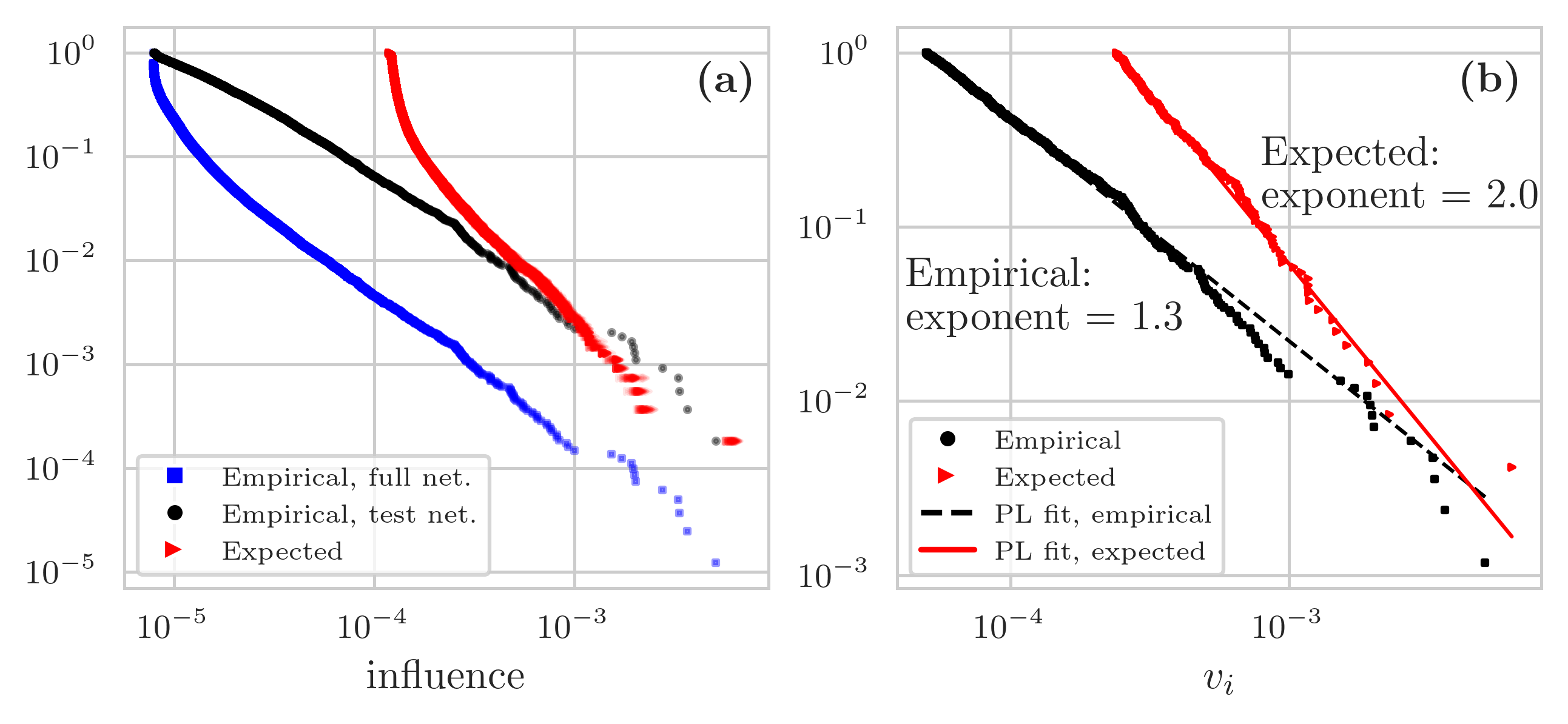

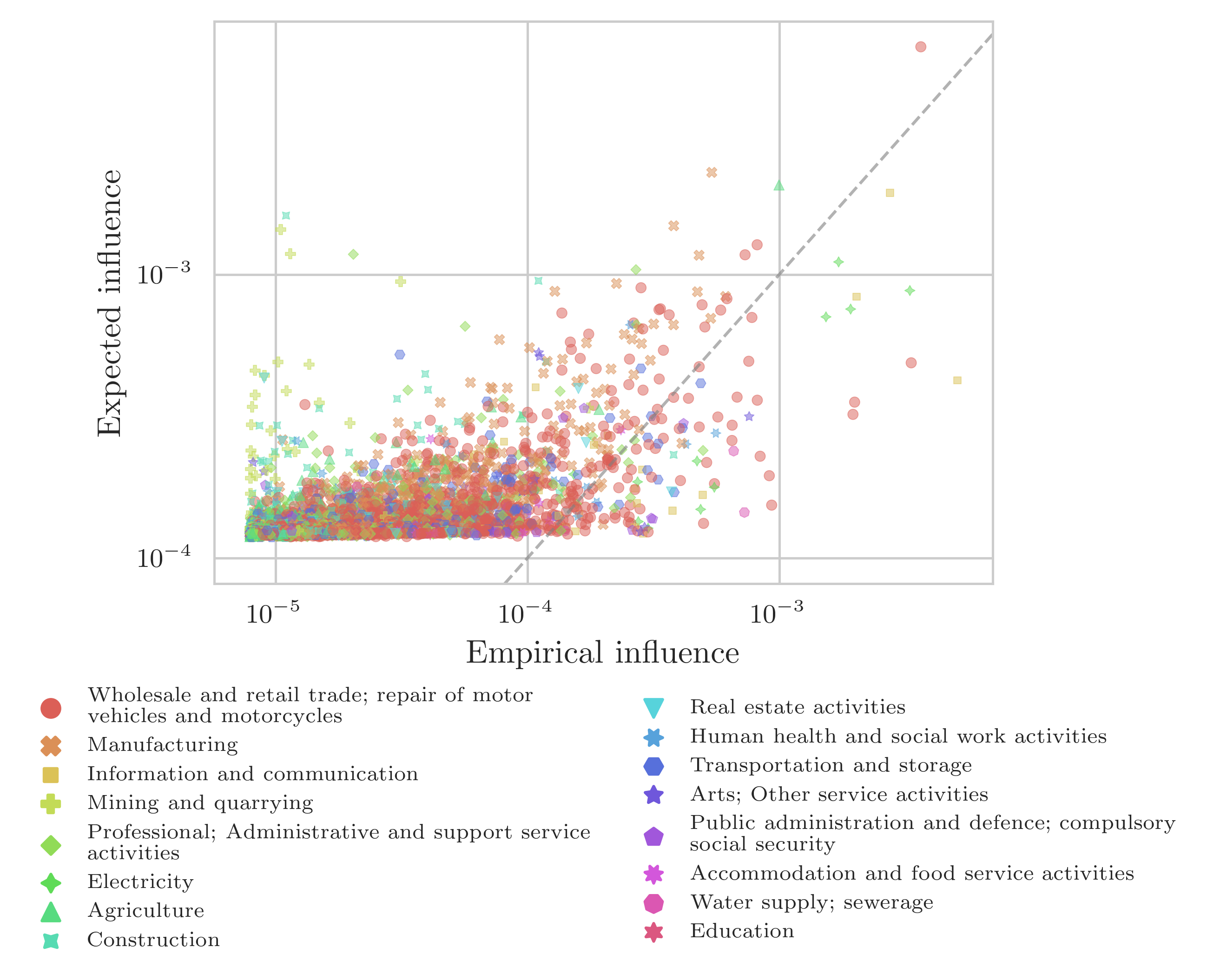

The reconstruction method performs well at reproducing the empirical output multipliers but not that well at reconstructing the influence vector. Figure 7a and 7b show the empirical (x-axis) and the expected (y-axis) output multipliers and influence vector, respectively. For the output multipliers, points cluster fairly tightly around the identity line (dashed grey line), while for the influence vector most points are located at the bottom left corner, suggesting that the influence is consistently overestimated. However, there are a few exceptions, which tend to be firms with higher influence (Figure C.7). These findings are further confirmed in Figure 7c and 7d, showing the CCDF of the (empirical and reconstructed) output multipliers and influence vector, respectively. It also highlights that the minimum of the empirical influence vector is around one order of magnitude smaller than the reconstructed one. The cosine similarity of the output multipliers is higher than that of the influence vector (0.99 and 0.56, respectively); however, the other error metrics are less clear cut (Table 7). The reconstruction method can recover the first two moments and the median of the output multipliers (Table 6). For the influence vector, we can recover only the standard deviation.

In Figure 7a clusters tend to form. Clusters arise because, for the output multipliers, we simulated firms’ value-added using sector-level data. The interaction of firms’ intermediate expenditures, sectoral ’s and the binary topology produces those clusters; see Appendix C.3.3 for more details.

| Output multiplier | Influence vector | ||||

|---|---|---|---|---|---|

| Empirical | Expected | Empirical | Expected | ||

| Mean | 1.423 | 1.553 | 4 | 1 | |

| Median | 1.420 | 1.475 | 2 | 1 | |

| Standard dev. | 0.247 | 0.202 | 1 | 1 | |

| Type | RMSE | MAE | MedAE | Cosine similarity |

|---|---|---|---|---|

| Output multipliers | 0.036 | 0.024 | 0.015 | 0.999 |

| (3) | (1) | (2) | (8) | |

| Influence vector | 0.033 | 0.024 | 0.022 | 0.560 |

| (2) | (2) | (1) | (3) |

FactSet.

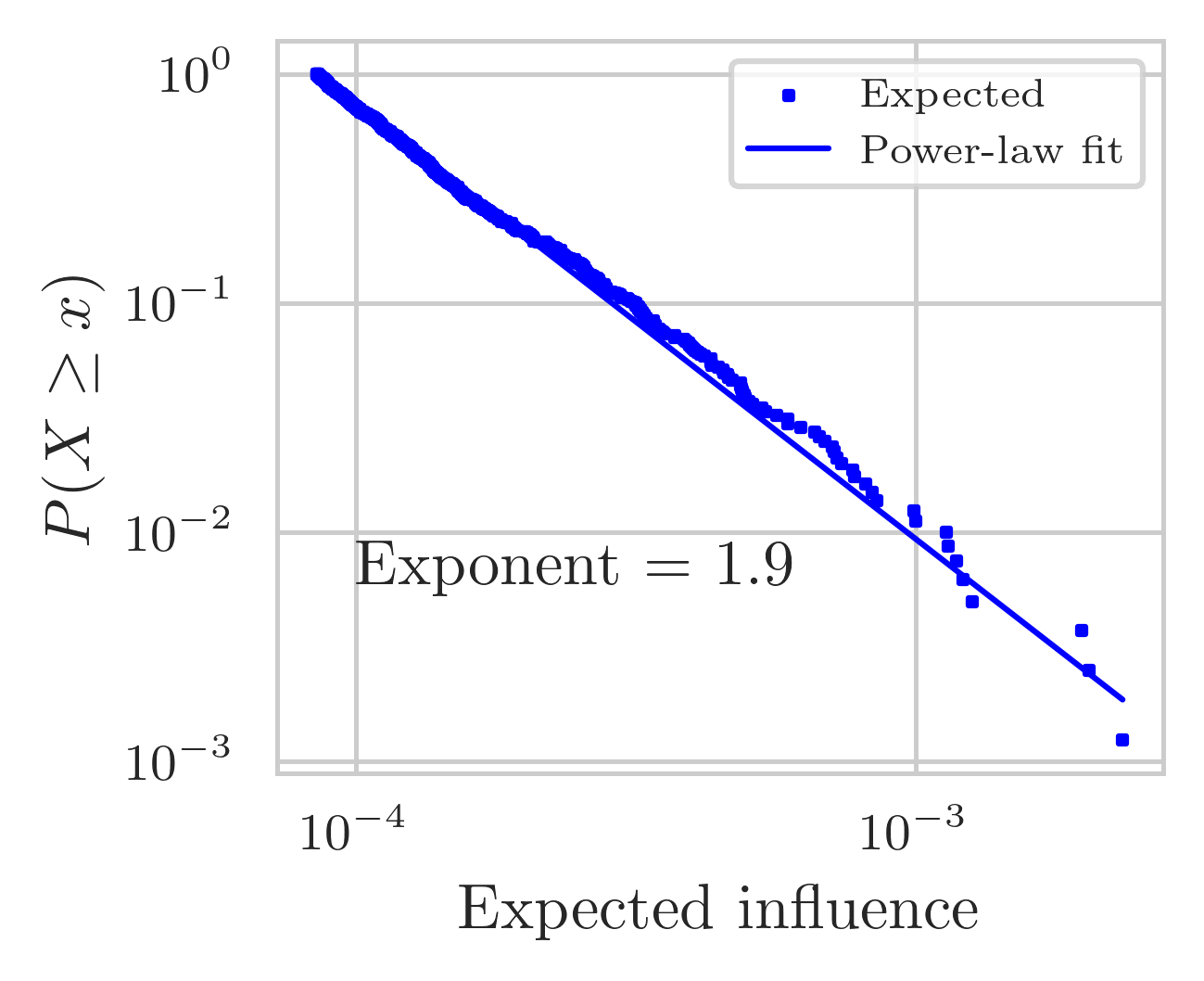

Figure 8a and 8b show the CCDF of, respectively, the expected output multipliers and the expected influence vector for FactSet. While the CCDF of the influence vector displays heavy tails, that of the output multipliers does not. As done for the weight distribution, we compare with empirical findings of other networks where the influence vector is found to have heavy tails and likely follows a power-law with a divergent second moment (Bacilieri et al., , 2023). The estimated power-law exponent is equal to 1.9, higher than what found for Belgium (1.12, Magerman et al., , 2016), Hungary and Ecuador (around 1.3-1.5 and 1.2-1.4, respectively, Bacilieri et al., , 2023). We show the CCDF and its power-law fit in Appendix C.3.1.111111We also fit a power-law distribution to Ecuador’s influence vector and recover an exponent of 2.0. However, the fit was rather poor. We show results for Ecuador in Appendix C.3.1. The output multipliers have a much higher median, first and second moment in FactSet (Table 8) compared to Ecuador (Table 6), while the influence vector has lower moments.

| Expected | ||

|---|---|---|

| Output multiplier | Influence vector | |

| Mean | 2.443 | 8 |

| Median | 2.501 | 6 |

| Standard dev. | 0.364 | 8 |

4.4.2 Supply-side shocks and aggregate volatility

We measure how firm-level TFP shocks affect macroeconomic output by propagating through the supply chain network using Equation 12. We simulate TFP shocks as explained in Section 4.2.3. We then use the empirical influence vector to calculate the empirical volatility and the reconstructed influence vector to calculate the predicted volatility. The volatility predicted by our reconstructed network is much higher than the empirical one. Using the empirical network, GDP volatility is 6.4%, while the mean across the 50 reconstructions is 102.3% with a standard deviation of 0.002 (Table 9).

To understand why we predict such a high GDP volatility, we do a variance decomposition analysis and look at the role of the proxy node in explaining aggregate volatility:

where the first term on the RHS is the contribution to total GDP volatility of the firms in the test network and the second term is the contribution of the proxy node, indexed by . We further look at shares

where is the set of observations for which we are computing the share of the variance. We use the variance to ensure that shares sum up to 1. The proxy node contributes to 99.3% of the variance, while all the other firms to 0.7%. If we calculate GDP volatility without including the proxy node, the predicted GDP volatility drops to 8.8%.

| Reconstructed | Benchmark | |||||

|---|---|---|---|---|---|---|

| Empirical | Proxy node | No proxy node | Proxy node | No proxy node | ||

| GDP volatility | 6.4% | 102.3% | 8.8% | 94% | 7.0% | |

| (0.0020) | (0.0010) | (0.0030) | (0.0002) | |||

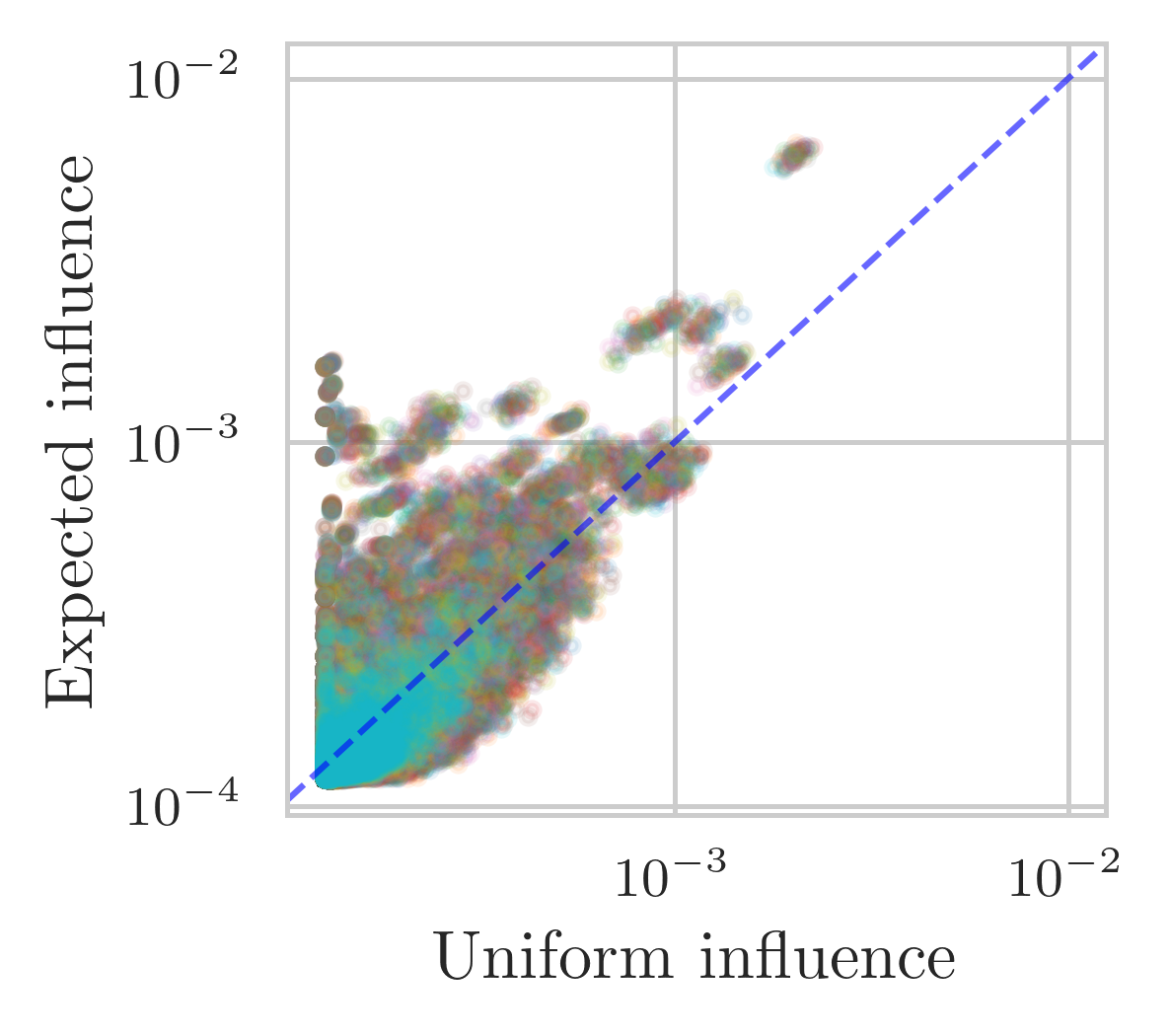

Benchmark.

To benchmark our results, we first calculate the influence vector assuming that each firm buys the same proportion of inputs from its suppliers (i.e., we modify in Equation 11) and then compute aggregate volatility using Equation 12. Assigning homogeneous input shares for each firm still satisfies the constraints on the intermediate costs, but the constraints on intermediate sales are not guaranteed to be satisfied. Our benchmark yields a volatility of 94% when the proxy node is included and 7.0% when excluded (Table 9). The volatility predicted by the benchmark is 0.6 percentage points higher than the empirical volatility, while the volatility of the reconstruction is 2.4 percentage points higher than the empirical volatility.

4.4.3 Discussion

As noticed in Section 4.3.3, we cannot compare with previous results of other studies reconstructing firm-level production networks. For financial networks and the ITN, different reconstruction methods perform reasonably well in reconstructing higher-order network properties such as the weighted clustering coefficient (e.g., Mastrandrea et al., , 2014; Cimini et al., 2015b, ; Cimini et al., 2015a, ; Parisi et al., , 2020). Table 10 reports some of the findings in the literature. For financial networks, Ramadiah et al., (2020) find that all the reconstruction methods they employ underestimate the level of systemic risk, except for a small region of the parameter space. Anand et al., (2015) report similar findings for MaxEnt, but find that the minimum density method overestimates systemic risk. Di Gangi et al., (2018) find that the cross-entropy capital asset pricing model can reproduce very well systemic risk while the other ensemble methods overestimate or underestimate it depending on the shock scenario. Differently, individual banks’ systemic risk and indirect vulnerability, which could be seen as akin to the multipliers we test, are consistently underestimated across all the methods they assess. The degree-corrected gravity model can reproduce DebtRank (also akin to the multipliers), with a Person correlation equal to 1 (Cimini et al., 2015b, ).

| Dataset | Method | Finding | Source |

| Ecuador SC | CReM | Overestimates influence vector, cosine sim. = 0.56 | This paper |

| Ecuador SC | CReM | Under/Overestimates output multipliers, cosine sim. = 1. | This paper |

| e-Mid | DcGM | DebtRank: correlation = 1 | Cimini et al., 2015b |

| ITN | DcGM | DebtRank: corrrelation = 1 | Cimini et al., 2015b |

| US bank-asset | CE CAPM, Max. entropy CAPM, BWCM, BECM | Underestimate banks’ measures of systemic risk | Di Gangi et al., (2018) |

| Ecuador SC | CReM | Overestimates aggregate volatility | This paper |

| German banks | MaxEnt | Underestimates systemic risk | Anand et al., (2015) |

| German banks | Minimum density | Overestimates systemic risk | Anand et al., (2015) |

| US bank-asset | Cross-entropy CAP model | Reproduces well aggregate vulnerability | Di Gangi et al., (2018) |

| US bank-asset | Max. entropy CAP model, BWCM, BECM | Over/underestimate aggregate vulnerability depending on the shock scenario | Di Gangi et al., (2018) |

| Japan bank-firm credit | MaxEnt, Min. density, CF + IPF, BFiCM + IPF | Underestimate the average probability of default | Ramadiah et al., (2020) |

While the vast majority of the studies find that systemic risk is underestimated, for Ecuador, we find that the conditional maximum entropy reconstruction method we employ overestimates aggregate volatility, similar to what Anand et al., (2018) find for the minimum density method. First, while including the proxy node in the calculations of aggregate volatility is supposed to capture the volatility of the firms that were excluded from the test network, there is a fundamental difference between the role the proxy node has in the network and that of the firms that we excluded. The proxy node is connected to all the other firms in the test network. In contrast, the firms excluded from the test network are less well connected in the empirical network. Additionally, the proxy node has the biggest influence, which equals 0.19. Therefore, when the proxy node is shocked, it immediately passes 19% of the shock to all the other firms in the network. To compare, the firm with the biggest influence in the empirical network has an influence of 0.005, with the biggest influence among the firms excluded from the test network being much lower and equal to 0.0002. Noting also that the firms excluded from the test network contribute to a mere 7% of aggregate volatility while the firms included in the test network to 93%, it makes sense to exclude the proxy node from the calculation of aggregate volatility as it is not a good aggregate representation of the rest of the economy, at least in this context. In fact, while the inclusion of the proxy node degrades the prediction of aggregate volatility, it enhances the reconstruction of the multipliers; see Appendix C.3.4.

Second, aggregate volatility is still overestimated even when the proxy node is excluded because the influence vector tends to be overestimated. Notice that the benchmark can predict aggregate volatility more accurately since it tends to overestimate influences lightly less than the reconstruction (see Appendix C.3.5). The reconstructed influence vector is overestimated for a combination of two factors, one of which is related to the binary topology and the other to the weighted topology. We can see how the binary topology affects the influence vector by looking at the out-degrees, which are highly affected by the selection of firms and the link deletion. In creating the test network, firms lose more customers than suppliers (see Appendix C.4.1). Already at the first step (selecting the firms to keep in our test network), the maximum number of customers (out-degree) decreases almost 7 folds, while the maximum number of suppliers only 3 folds. Since the influence vector calculates the weighted sum of the number of walks from firm to firm (so following the outgoing edges starting at ) for walks of various lengths and the out-degrees have been considerably truncated, it cannot capture walks of longer lengths. Instead, the output multipliers, relying on the incoming edges and thus the in-degrees, are that not affected. The weighted topology comes into play because the reconstruction method tends to overestimate weighted quantities for intermediate and small values, which are numerous. Although higher (and other) weights can be underestimated, these are not abundant enough and the magnitude of the underestimation is not big enough compared to the quantity and the size of the overestimation of low and intermediate weights.

For FactSet, a significant result is that the estimated power-law exponent of the distribution of the influence vector implies a divergent second moment. Acemoglu et al., (2012) show, at a theoretical level, that the influence vector affects aggregate volatility, so it is important that we can recover an exponent more or less in line with empirical observations.121212 Acemoglu et al., ’s (2012) theoretical result is exemplified in Equation 12, which shows that aggregated volatility scales with the Euclidean norm of the influence vector. Luca’s diversification argument implies that aggregate volatility decays as . However, if the CCDF of the influence vector is Pareto distributed with parameter , the diversification argument no longer holds and aggregate volatility decays much more slowly, as (Carvalho and Tahbaz-Salehi, , 2019).

4.5 Results: different numbers of unknown links

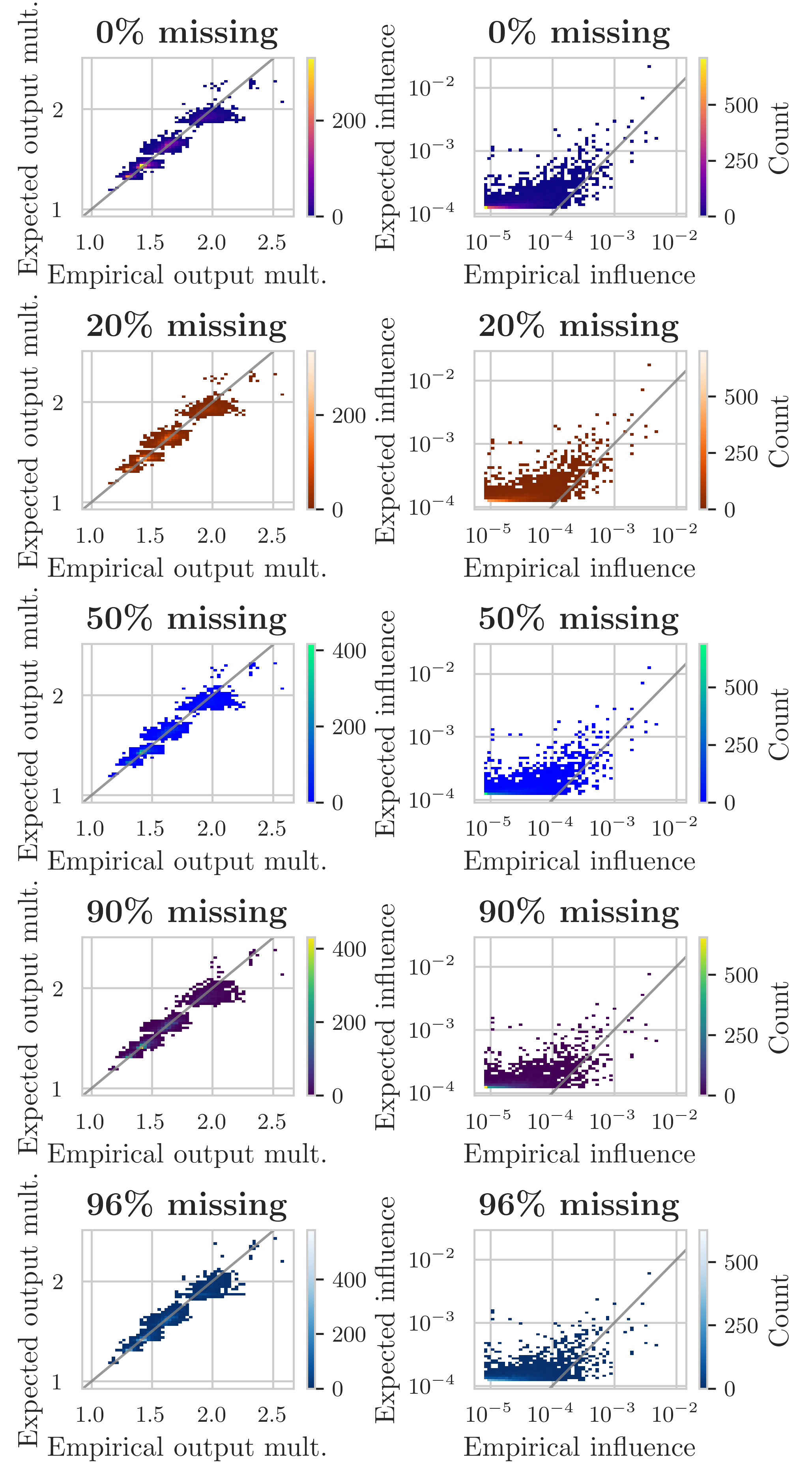

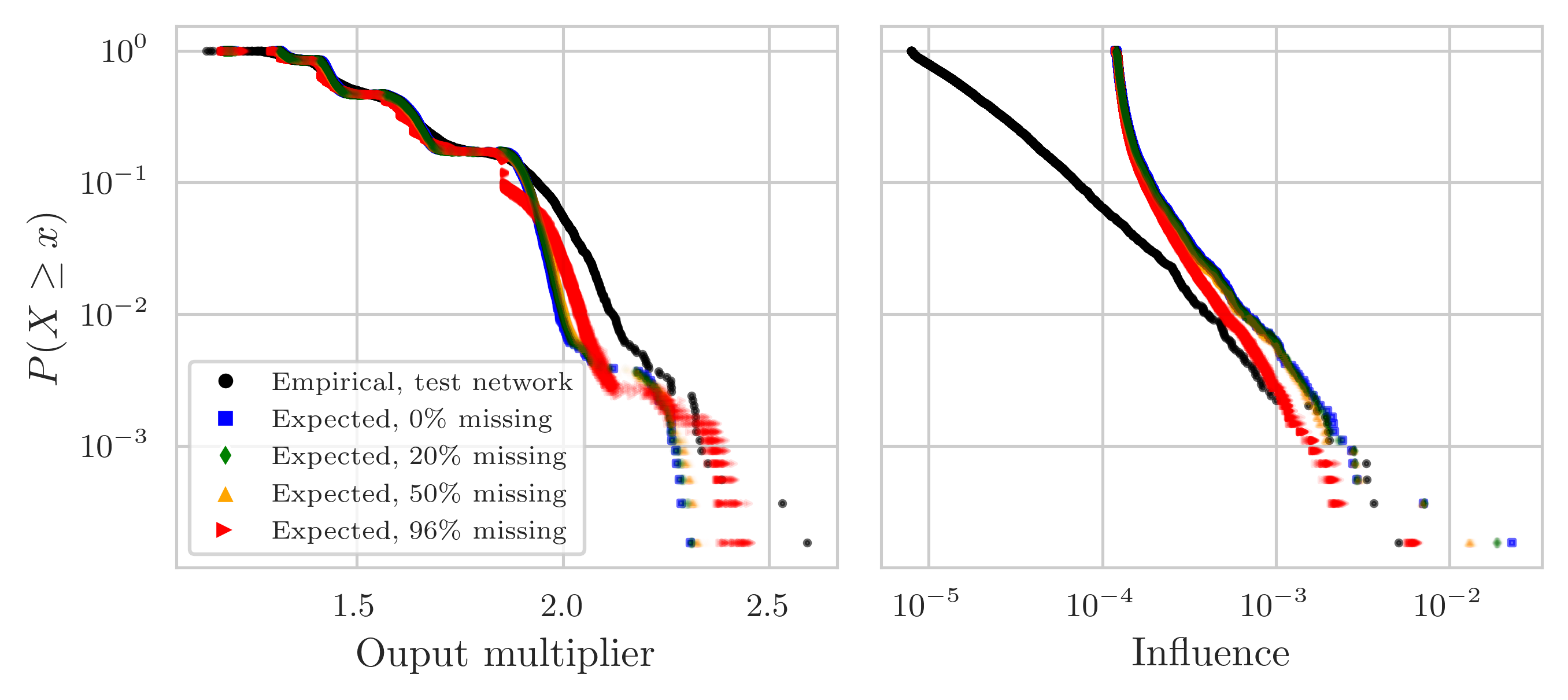

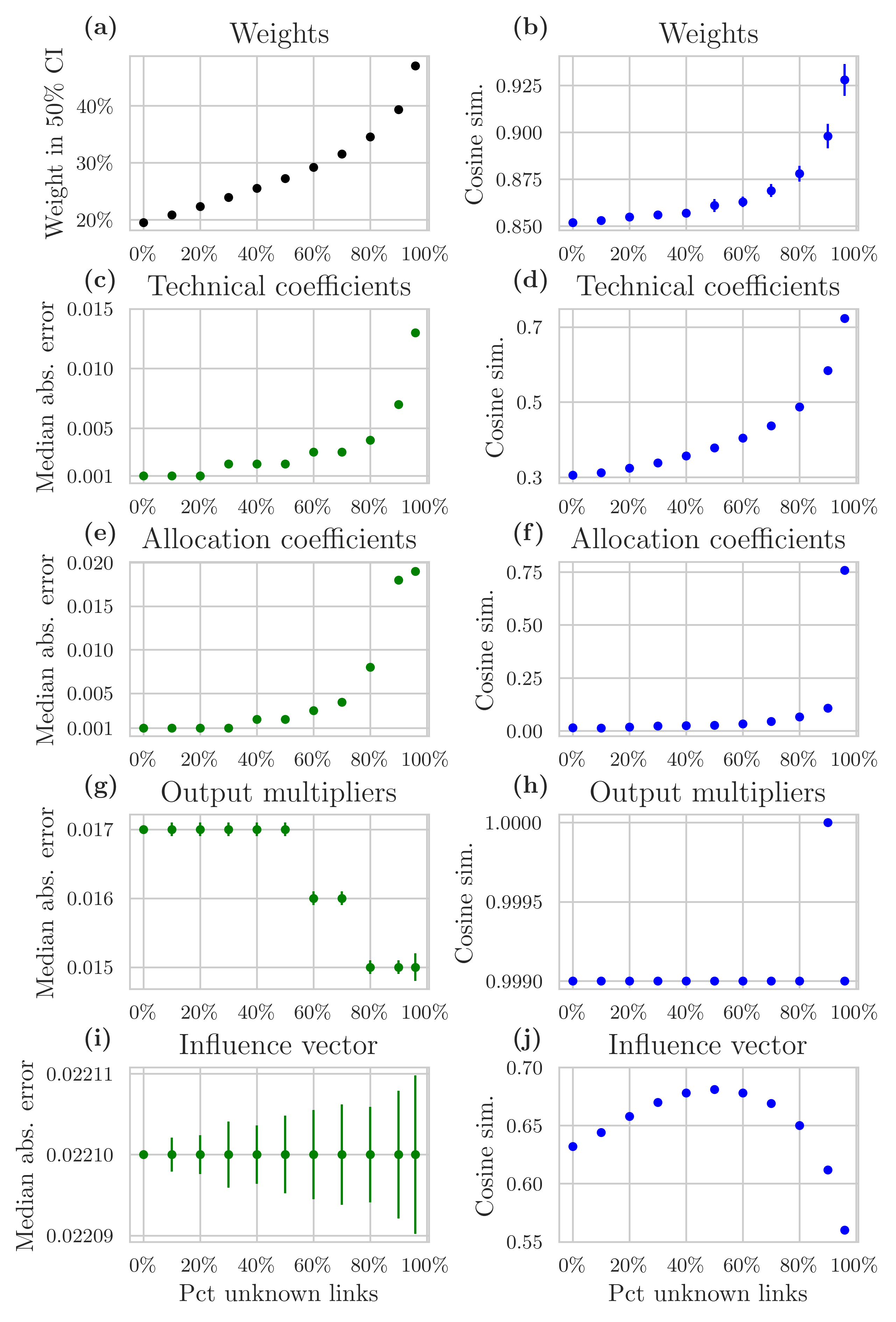

We now discuss how the reconstruction method performs when the number of unknown links in the test network changes; we keep the number of firms constant. We delete 0%, 10%, 20% and so on up to 90% of the links; we also show results for the reconstruction matching the mean degree of FactSet, which has 96% of unknown links. For each percentage of unknown links, we simulate 50 randomised networks and investigate the number of weights that fall into the 50% CI, and the median absolute error and the cosine similarity for microscale and higher-order quantities. We also assess aggregate volatility.

Microscale and higher-order quantities.

Figure 9 shows the different metrics used for assessing the quality of the reconstruction of the weights, and the technical and allocation coefficients, and the multipliers. For the weights, we show the percentage of weights that fall in the 50% CI (Figure 9a) and the cosine similarity (Figure 9b). For all the other quantities, we show the median absolute error (left column) and the cosine similarity (right column). The overall trend is that as the number of unknown links increases, so do the metrics.

As the number of unknown links increases, the cosine similarity increases, with the two multipliers being the only exceptions. Such a counter-intuitive finding arises from the link deletion mechanism. We are deleting links with a smaller weight with a higher probability, hence as the number of unknown links increases, the empirical weights associated with the known links are less heterogeneous. Since maximum entropy methods allocate weights as uniformly as possible given the constraints, the higher the number of unknowns, the better it can reconstruct the weights associated with the known links. Consequently, also more weights fall into the 50% confidence interval.

For the allocation coefficients, the cosine similarity is considerably lower than that of all the other quantities and it jumps from 0.05 to 0.76 when the number of unknown links increases from 90% to 96%. This jump is associated with a considerable decrease in the number of customers firms have when the number of unknown links increases from 90% to 96% (see Appendix C.4.1). Therefore, the allocation coefficients, which gauge the percentage of total output firm sells to firm , are highly affected by a drastic decrease in the number of customers (see Appendix C.4.2). However, we would have expected this to have a negative effect. Instead, it enhances the predictions. On the contrary, the technical coefficients, which measure the percentage of inputs that buys from , do not experience such a jump because the same drastic change does not happen for the number of suppliers. Moreover, firms tend to have more customers than suppliers (see Appendix C.4.1 and Bacilieri et al., , 2023), making it easier to guess the weights correctly from the supply side and thus reconstruct the technical coefficients better than the allocation coefficients throughout.

The output multipliers always have the same cosine similarity. Since the output multipliers are derived from the technical coefficient matrix and depend on the incoming edges, hence the number of suppliers firms have, they are not that affected by the number of unknown links. Instead, the influence vector relies on the number of customers firms have (out-degree), which we saw being more affected by the deletion of firms and links, so the influence vector has a much lower cosine similarity than the output multipliers. It is not so clear why the cosine similarity has an inverted U-shaped curve, with the maximum value of 0.68 reached when 50% of the links are unknown. It is however the case that the cosine similarity increases from 0.63 when all links are known to 0.68 (50% unknown links) and then decreases again until it drops to 0.56 when 96% of the links are unknown. It might be that these are small fluctuations of no particular value and that the reconstruction of the influence vector starts deteriorating when more than 50% of the links are unknown because the out-degrees start being too affected by the deletion of the links.

The median absolute error slightly increases for the technical and allocation coefficients because higher errors (in absolute value) tend to occur for higher weights. The median absolute error is constant for the multipliers.

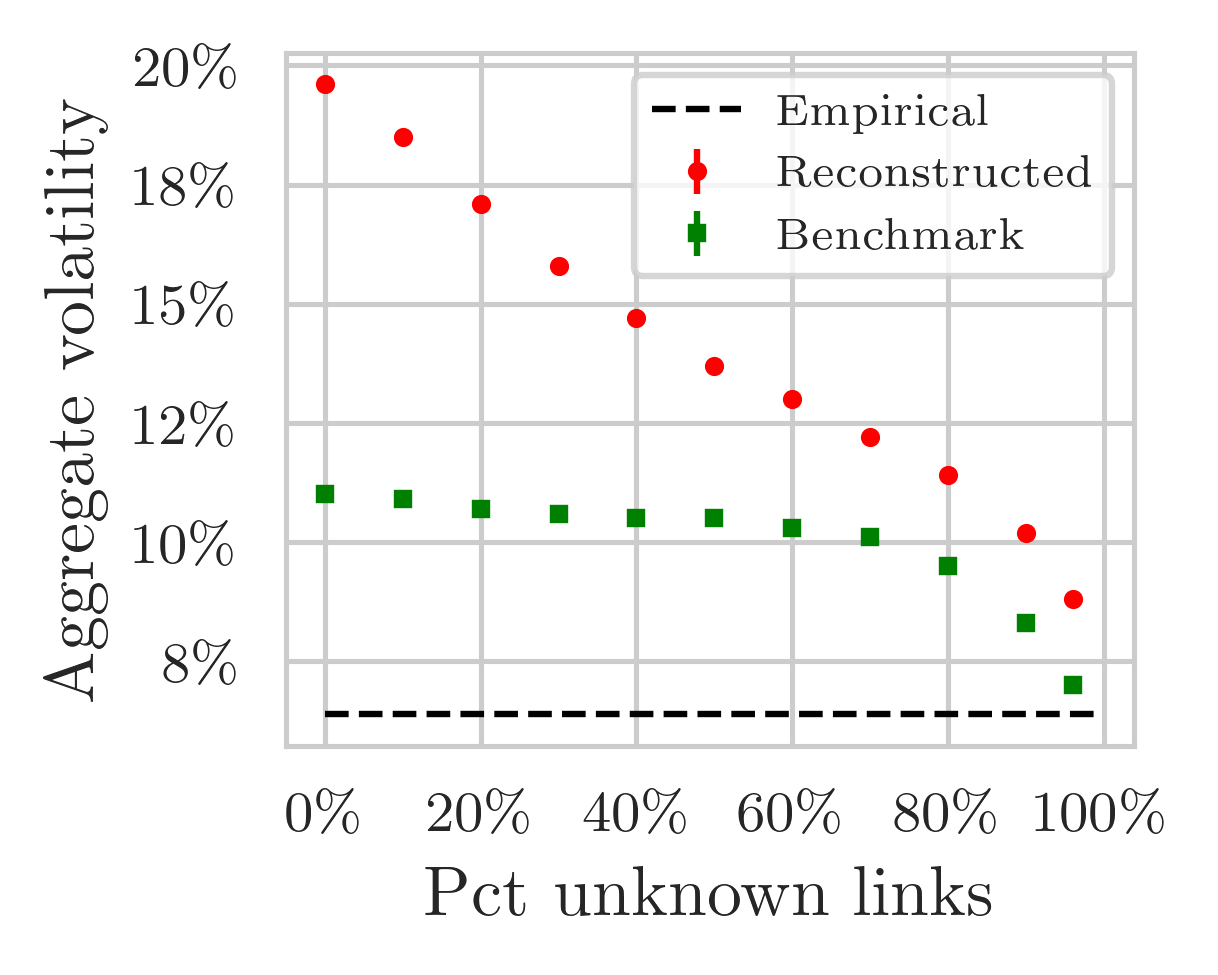

Aggregate volatility.

Figure 10 shows the predicted aggregated volatility (calculated excluding the proxy node) as the number of unknown links increases for the reconstruction (red dots), the benchmark (green squares) and the empirical volatility ( black dashed line). In line with the results for the case of 96% of unknown links, the reconstruction always predicts a much higher volatility, as does the benchmark. Although the benchmark’s predictions are closer to the empirical volatility. One would think that the higher the number of known links, the better we get at predicting aggregate volatility. However, this is not the case. In fact, the fewer links we know, the better we can predict GDP volatility. This is because the more links we know, the more we overestimate the influences (especially bigger influences, see Appendix C.4.2).

5 Conclusions

There is widespread interest in modelling the global economy from the bottom up. There is also widespread agreement that supplier-customer relations are an essential feature of such modelling efforts. However, data are scarce, have missing information and are not easily accessible. In this paper, we have made a couple of first steps in bringing this agenda forward.

First, we provided the first rigorous assessment of a network reconstruction method (Parisi et al., , 2020) on the administrative dataset of Ecuador. We focused on reconstructing the weighted network given the binary topology when many links and firms are missing. An interesting finding is that the quality of the reconstruction of different quantities seems to depend on network features that are particularly sensitive to the sampling strategy of firms and links, something that future research should explore further. Second, we assessed whether a global dataset of listed firms, where many links and firms are missing, can be enhanced by merging it with sector-level data. We then used this “augmented” dataset for inferring the link weights using a conditional maximum entropy method (Parisi et al., , 2020). Our results show that further work needs to be done, especially in reconciling firms’ financial accounts with national accounts, which is essential for better reconstructing the weighted production network, in particular when many firms are missing.

In our study, we assumed to know the binary topology (although partially) to cover a use case that could help reconstruct commercial datasets. A natural next step would be to predict links and then reconstruct weights, possibly with different degrees of knowledge of the production network. It is of particular value to understand the performance of reconstruction methods when one does not know the binary topology, as it could unlock the study of economies for which no such data is available. The reconstruction method we employed can easily accommodate the prediction of the binary topology, either partially or in its entirety.

Our assessment of macroscale quantities was rather limited and restricted to a standard general equilibrium I-O model (Acemoglu et al., , 2012). Therefore, there is much research to be done on different models (and scenarios), especially agent-based models, where we believe that the accuracy of the reconstruction of microscale quantities matters more for the model’s outcomes than for general equilibrium models.

While many reconstruction methods are available, the high number of nodes and links in firm-level networks renders almost all of them infeasible. Future research is thus necessary to develop different reconstruction methods suited for large-scale firm-level networks. It is also important to conduct similar analyses on other firm-level datasets for which the ground truth network is available, as ours was only one of the first initial steps.

Aknowledgments

We thank François Lafond, Jose Moran, R. Maria del Rio-Chanona, Anton Pichler, Luca Mugo and Fabian Dablander for useful comments. We thank Doyne J. Farmer, Jangho Yang, Giancarlo Antonucci and the Complexity group at the Institute for New Economic Thinking at the Oxford Martin School for inspiring discussions. We have benefited from many comments from audiences at Cambridge IfM and CSH Vienna. We also thank the Servicio de Rentas Internas (SRI) and its Centro de Estudios Fiscales that provided the raw data of Ecuador for research purposes. This work was supported by the Oxford Martin Programme on the Post-Carbon Transition, the Institute for New Economic Thinking at the Oxford Martin School and Baillie Gifford. This research is based upon work supported in part by the Office of the Director of National Intelligence (ODNI), Intelligence Advanced Research Projects Activity (IARPA), via contract no. 2019-1902010003. The views and conclusions contained herein are those of the authors and should not be interpreted as necessarily representing the official policies, either expressed or implied, of ODNI, IARPA, or the U.S. Government. The U.S. Government is authorised to reproduce and distribute reprints for governmental purposes notwithstanding any copyright annotation therein. FactSet had the opportunity to review the paper.

Author contributions