*format=pnasformat

Inferring networks from time series:

a neural approach

Abstract

Network structures underlie the dynamics of many complex phenomena, from gene regulation and foodwebs to power grids and social media. Yet, as they often cannot be observed directly, their connectivities must be inferred from observations of the dynamics to which they give rise. In this work we present a powerful computational method to infer large network adjacency matrices from time series data using a neural network, in order to provide uncertainty quantification on the prediction in a manner that reflects both the degree to which the inference problem is underdetermined as well as the noise on the data. This is a feature that other approaches have hitherto been lacking. We demonstrate our method’s capabilities by inferring line failure locations in the British power grid from its response to a power cut, providing probability densities on each edge and allowing the use of hypothesis testing to make meaningful probabilistic statements about the location of the cut. Our method is significantly more accurate than both Markov-chain Monte Carlo sampling and least squares regression on noisy data and when the problem is underdetermined, while naturally extending to the case of non-linear dynamics, which we demonstrate by learning an entire cost matrix for a non-linear model of economic activity in Greater London. Not having been specifically engineered for network inference, this method in fact represents a general parameter estimation scheme that is applicable to any high-dimensional parameter space.

Keywords: Network inference, Neural differential equations, Model calibration, Power grids.

-

1Department of Applied Mathematics and Theoretical Physics, University of Cambridge, Cambridge CB3 0WA, United Kingdom; 2Department of Mathematics, Imperial College London, London SW7 2AZ, United Kingdom; 3Department of Engineering, University of Cambridge, Cambridge CB2 1PZ, United Kingdom; 4The Alan Turing Institute, London NW1 2DB, United Kingdom

⋆To whom correspondence should be addressed: trg34@cam.ac.uk

Introduction

Networks are important objects of study across the scientific disciplines. They materialise as physical connections in the natural world, for instance as the mycorrhizal connections between fungi and root networks that transport nutrients and warning signals between plants [1, 2], human traffic networks [3, 4], or electricity grids [5, 6]. However, they also appear as abstract, non-physical entities, such as when describing biological interaction networks and food webs [7, 8, 9], gene or protein networks [10, 11, 12, 13], economic cost relations [14, 15], or social links between people along which information (and misinformation) can flow [16, 17, 18]. In all examples, though the links constituting the network may not be tangible, the mathematical description is the same. In this work, we are concerned with inferring the structure of a static network from observations of dynamics on it. The problem is of great scientific bearing: for instance, one may wish to understand the topology of an online social network from observing how information is passed through it, and some work has been done on this question [19, 20, 21]. Another important application is inferring the connectivity of neurons in the brain by observing their responses to external stimuli [22, 23]. In an entirely different setting, networks crop up in statistics in the form of conditional independence graphs, describing dependencies between different variables, which again are to be inferred from data [24, 25].

Our approach allows inferring network connectivities from time series data with uncertainty quantification. Uncertainty quantification for network inference is important for two reasons: first, the observations will often be noisy, and one would like the uncertainty on the data to translate to the uncertainty on the predicted network. Secondly however, completely inferring large networks requires equally large amounts of data – typically at least equations per node, being the number of nodes – and these observations must furthermore be linearly independent. Data of such quality and quantity will often not be available, leading to an underdetermined inference problem. The uncertainty on the predicted network should thus also reflect (at least to a certain degree) the ‘non-convexity’ of the loss function, i.e. how many networks are compatible with the observed data. To the best of our knowledge, no current network inference method is able to provide this information.

Network inference can be performed using ordinary least squares (OLS) regression [6, 26], but this is confined to the case where the dynamics are linear in the adjacency matrix. An alternative are sampling-based methods that generalise to the non-linear case [27, 28, 29], but these tend to struggle in very high-dimensional settings and can be computationally expensive. Efficient inference methods for large networks have been developed for cascading dynamics [19, 20, 21], but these are highly specialised to a particular type of observation data and give no uncertainty quantification on the network prediction. Our method avoids these limitations. Its use of neural networks is motivated by their recent and successful application to low-dimensional parameter calibration problems [30, 31], both on synthetic and real data, as well as by their conceptual proximity to Bayesian inference, e.g. through neural network Gaussian processes or Bayesian neural networks [32, 33, 34, 35, 36, 37]. Our method’s underlying approach ties into this connection, and in fact, since it has not been specifically engineered to fit the network case, constitutes a general and versatile parameter estimation method.

Method description

We apply the method proposed in [31] to the network case. The approach consists of training a neural network to find a graph adjacency matrix that, when inserted into the model equations, reproduces the observed time series . A neural network is a function , where represents the number of time series steps that are passed as input. Its output is the (vectorised) estimated adjacency matrix , which is used to run a numerical solver for iterations ( is the batch size) to produce an estimated time series . This in turn is used to train the internal parameters of the neural net (the weights and biases) via a loss function . The likelihood of any sampled estimate is simply proportional to

| (1) |

and by Bayes’ rule, the posterior density is then

| (2) |

with the prior density [38]. As , we may calculate the gradient and use it to optimise the internal parameters of the neural net using a backpropagation method of choice; popular choices include stochastic gradient descent, Nesterov schemes, or the Adam optimizer [39]. Calculating thus requires differentiating the predicted time series , and thereby the system equations, with respect to . In other words: the loss function contains knowledge of the dynamics of the model. Finally, the true data is once again input to the neural net to produce a new parameter estimate , and the cycle starts afresh. A single pass over the entire dataset is called an epoch.

Using a neural net allows us to exploit the fact that, as the net trains, it traverses the parameter space, calculating a loss at each point. Unlike Monte-Carlo sampling, the posterior density is not constructed from the frequency with which each point is sampled, but rather calculated directly from the loss value at each sample point. This entirely eliminates the need for rejection sampling or a burn-in: at each point, the true value of the likelihood is obtained, and sampling a single point multiple times provides no additional information, leading to a significant improvement in computational speed. Since the stochastic sampling process is entirely gradient-driven, the regions of high probability are typically found much more rapidly than with a random sampler, leading to a high sample density around the modes of the target distribution. We thus track the neural network’s path through the parameter space and gather the loss values along the way. Multiple training runs can be performed in parallel, and each chain terminated once it reaches a stable minimum, increasing the sampling density on the domain, and ensuring convergence to the posterior distribution in the limit of infinitely many chains.

We begin this article with two application studies: first, we infer locations of a line failure in the British power grid from observations of the network response to the cut; and secondly, we infer economic cost relations between retail centres in Greater London. Thereafter we conduct a comparative analysis of our method’s performance, before finally demonstrating the connection between the uncertainty on the neural net prediction and the uncertainty of the inference problem.

Inferring line failures in the

British power grid

Power grids can be modelled as networks of coupled oscillators using the Kuramoto model of synchronised oscillation [40, 41, 42, 43, 44]. Each node in the network either produces or consumes electrical power while oscillating at the grid reference frequency . The nodes are connected through a weighted undirected network , where the link weights are obtained from the electrical admittances and the voltages of the lines. The network coupling allows the phases of the nodes to synchronise according to the differential equation [43]

| (3) |

where , , and are the inertia, friction, and coupling coefficients respectively. A requirement for dynamical stability of the grid is that , i.e. that as much power is put into the grid as is taken out through consumption and energy dissipation [42].

A power line failure causes the network to redistribute the power loads, causing an adjustment cascade to ripple through the network until equilibrium is restored [5]. In this work we recover the location of a line failure in the British power grid from observing these response dynamics. Figure 1a shows the high-voltage transmission grid of Great Britain as of January 2023, totalling 630 nodes (representing power stations, substations, and transformers) and 763 edges with their operating voltages. Of the roughly 1300 power stations dotted around the island, we include those 38 with installed capacities of at least 400 MW that are directly connected to the national grid [45]; following [5, 42] we give all other nodes a random value such that .

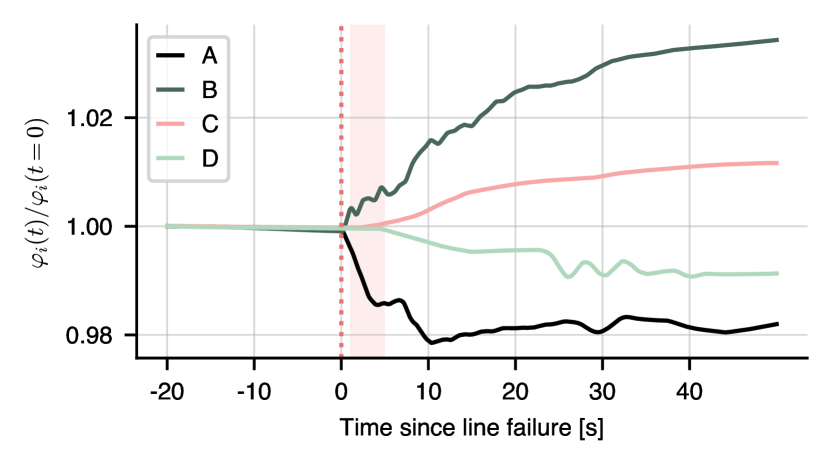

We simulate a power cut in the northeast of England by iterating the Kuramoto dynamics until the system reaches a steady state of equilibrium (defined as ) and then removing two links and recording the network response (fig. 1b). From the response we can infer the adjacency matrix of the perturbed network (with missing links) and, by comparing with the unperturbed network (without missing links), the line failure locations.

(a) Power grid topology

![[Uncaptioned image]](/html/2303.18059/assets/x1.png)

(b) Network response to line failure

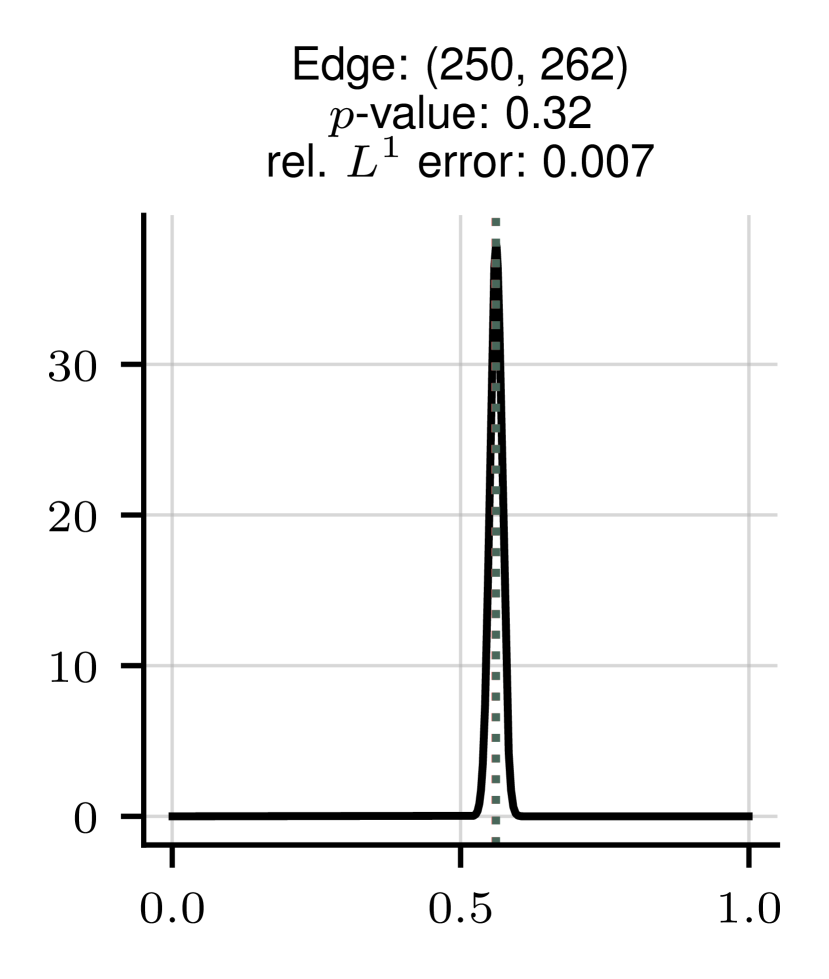

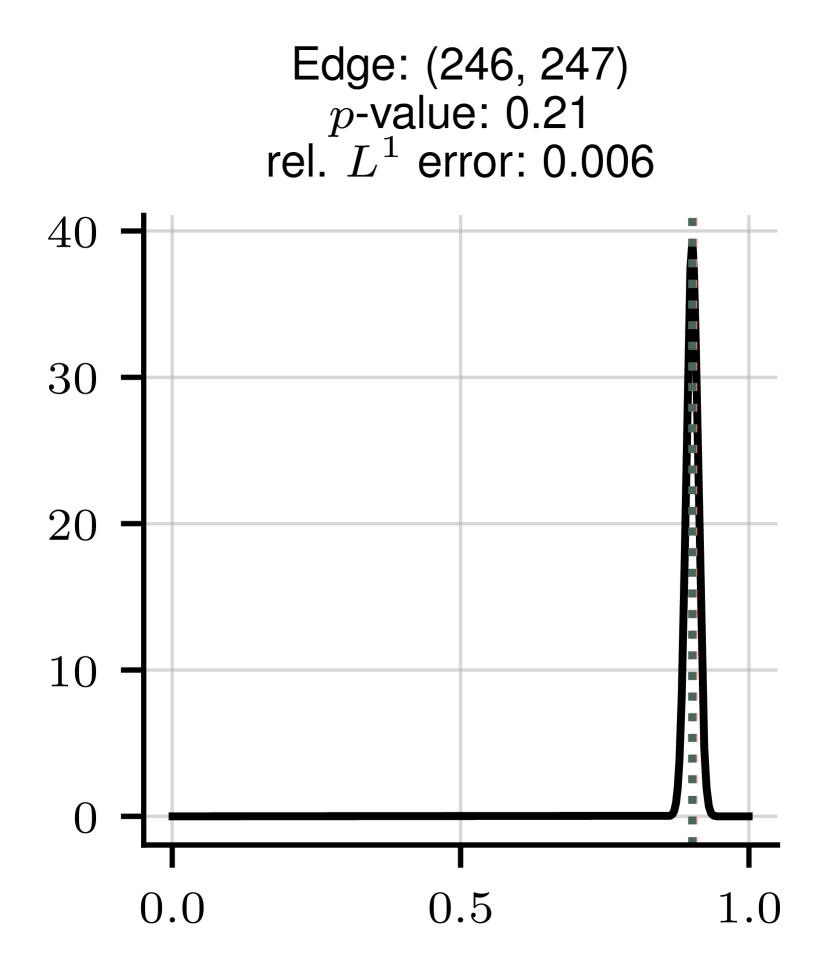

(a) Densities on edges with highest relative error

(b) True (black) and predicted network response

We let a neural network output a (vectorised) adjacency matrix and use this estimated adjacency matrix to run the differential equation [3], which will produce an estimate of the observed time series of phases . A hyperparameter sweep on synthetic data showed that using a deep neural network with 5 layers, 20 nodes per layer, and no bias yields optimal results (see figs. S2—S4 in the appendix). We use the hyperbolic tangent as an activation function on each layer except the last, where we use the ‘hard sigmoid’ [49, 50]

which allows neural net output components to actually become zero, and not just asymptotically close, thereby ensuring sparsity of the adjacency matrix – a reasonable assumption given that the power grid is far from fully connected. We use the Adam optimizer [39] with a learning rate of for the gradient descent step. Since the neural network outputs are in , we scale the network weights such that , and absorb the scaling constant into the coupling constant ; see the Supplementary Information for details on the calculations.

We use the following loss function to train the internal weights of the neural network such that it will output an adjacency matrix that reproduces the observed data:

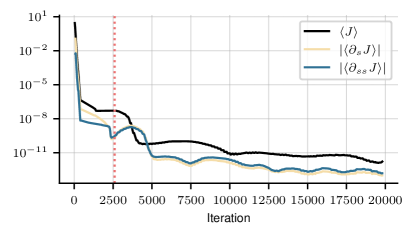

The first summand is the data-model mismatch, the second penalises asymmetry to enforce undirectedness of the network, and the third sets the diagonal to zero (which cannot be inferred from the data, since all terms for ). is a function of the iteration count designed to let the neural network search for in the vicinity of , since we can assume a priori that the two will be similar in most entries. To this end we set while the loss function has not yet reached a stable minimum, quantified by and , and thereafter. Here, is a rolling average over a window of iterations, see fig. 2. In other words, we push the neural network towards a stable minimum in the neighbourhood of and, once the loss stabilises, permanently set .

In theory observations are needed to completely infer the network, though symmetries in the data usually mean is required in practice [51]. In this experiment we purposefully underdetermine the problem by only using steps; additionally, we train the network on data recorded simulated second after the power cut, where many nodes will still be close to equilibrium. Though the neural network may be unable to completely infer the network, it can nevertheless produce a joint distribution on the network edge weights , recorded during the training, that allows us to perform hypothesis testing on the line failure location. The marginal likelihood on each network edge is given by

| (4) |

where the subscript indicates we are omitting the -th component of in the integration. We assume uniform priors on each edge. In high dimensions, calculating the joint of all network edge weights can become computationally infeasible, but we can circumvent this by instead considering the two-dimensional joint density of the edge weight under consideration and the likelihood, and then integrating over the likelihood,

| (5) |

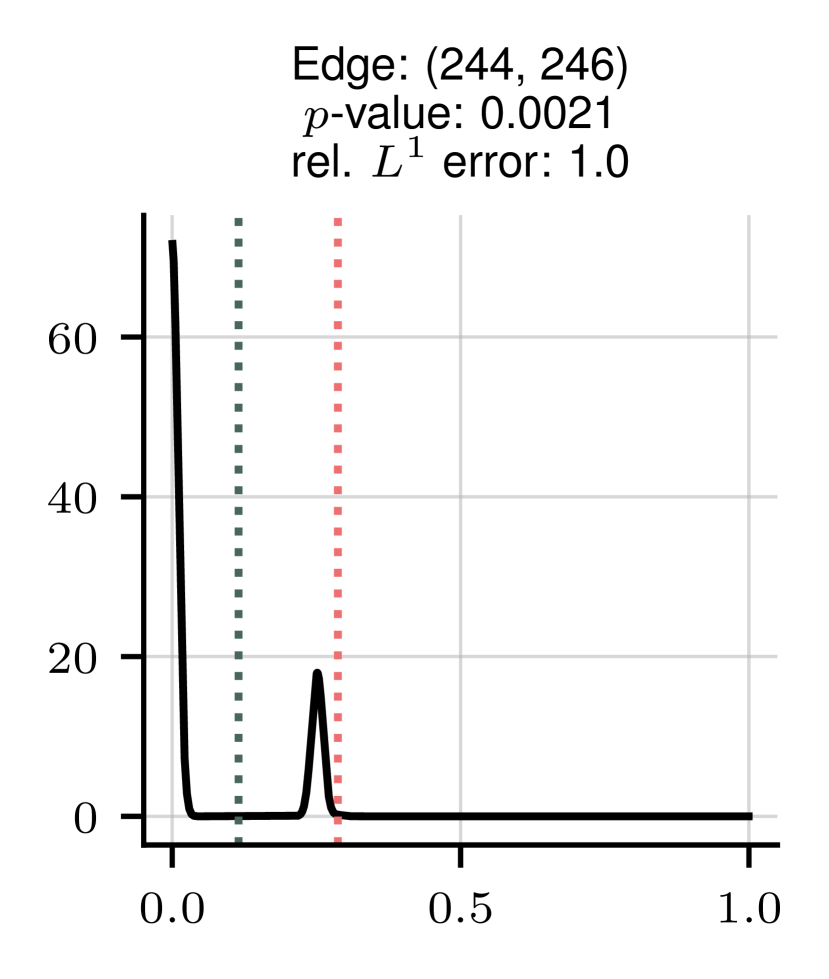

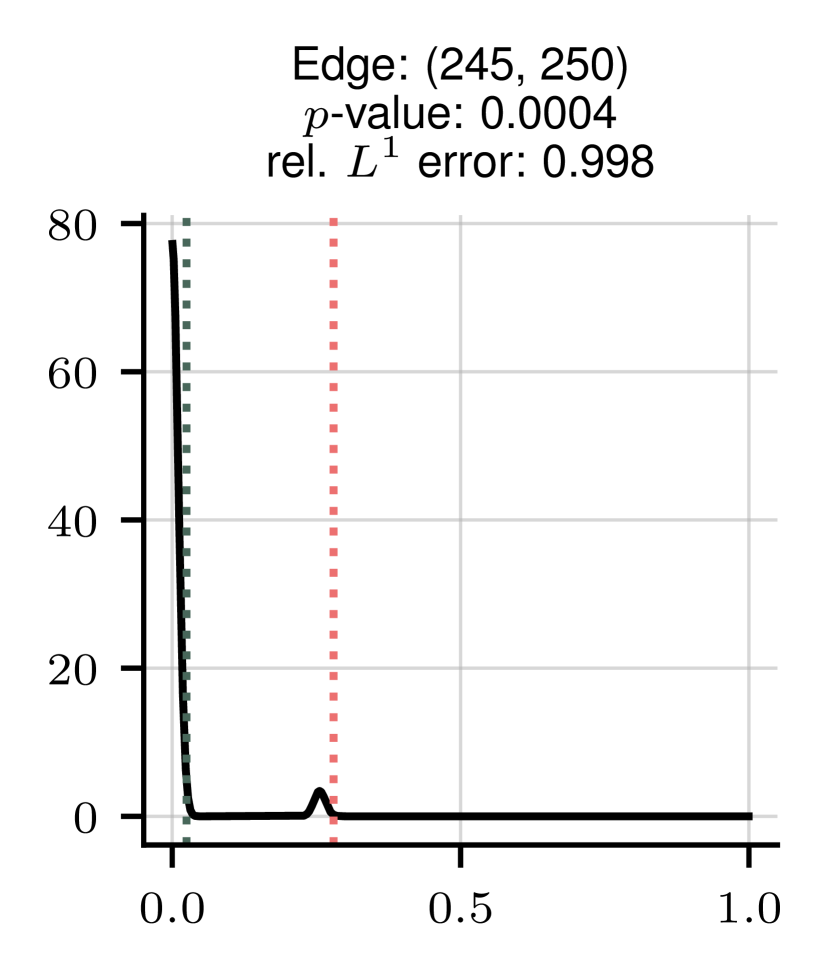

We show the results in fig. 3. Given the marginal distributions with modes , we plot the densities on the four network edges with the highest relative prediction error . The advantage of obtaining uncertainty quantification on the network is now immediately clear: even in the underdetermined case we are able to make meaningful statistical statements about the line failure location. We see that the missing edges consistently have the highest relative prediction errors, and that the -values for measuring the unperturbed value under the null are 0.2% and 0.04% respectively, while being statistically insignificant for all other edges. It is interesting to note that the other candidate locations are also within the vicinity of the line failure, though their predicted values are much closer to the unperturbed value. In fig. 3b, we see that the predicted network reproduces the response dynamics for the range covered by the training data when inserted into eq. [3], but, since the problem was purposefully underdetermined, the errors in the prediction cause the predicted and true time series to diverge for larger . Densities on all 200.000 potential edges were obtained in about twenty minutes on a regular laptop CPU.

Inferring economic cost networks

from noisy data

(a) Model dynamics

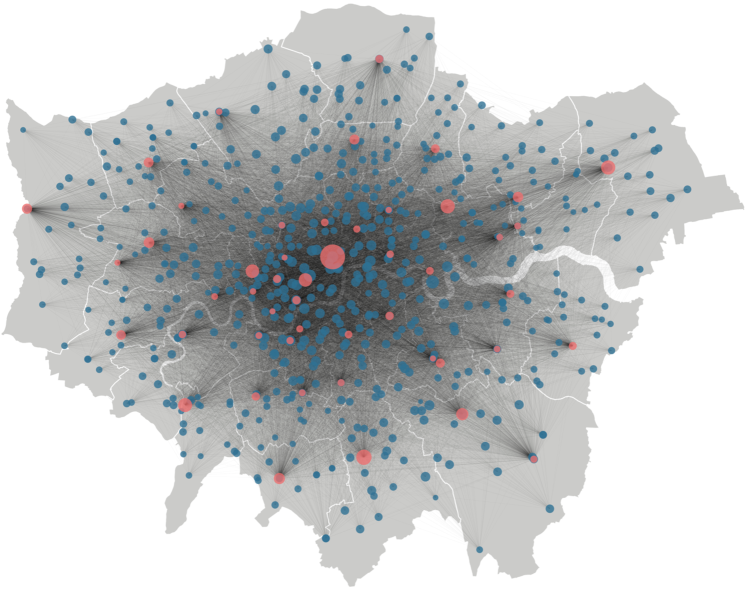

(b) Initial data and travel times network

(c) Inferred weighted degree distribution

In the previous example the underlying network was a physical entity, but in many cases networks model abstract connections. We therefore now consider a commonly used economic model of the coupling of supply and demand [55, 15, 14] and a dataset of economic activity across Greater London. The goal is to learn the entire coupling network, not just to infer the (non-)existence of individual edges. In the model, origin zones of sizes , representing economic demand, are coupled to destination zones of sizes , modelling the supply side, through a network whose weights quantify the convenience with which demand from zone can be supplied from zone : the higher the weight, the more demand flows through that edge (see fig. 4a). Such a model is applicable e.g. to an urban setting [14], the origin zones representing residential areas, the destination zones e.g. commercial centres, and the weights quantifying the connectivity between the two (transport times, distances, etc.). The resulting cumulative demand at destination zone depends both on the current size of the destination zone and the network weights :

| (6) |

The sizes are governed by a system of coupled logistic Stratonovich stochastic differential equations

| (7) |

with given initial conditions , see fig. 4a. , , , and are scalar parameters. Our goal is to infer the cost matrix from observations of the time series and . The model includes multiplicative noise with strength , where the are independent white noise processes and signifies Stratonovich integration [56]. Crucially, the model depends non-linearly on .

We apply this model to a previously studied dataset of economic activity in Greater London [15, 31]. We use the ward-level household income from wards for 2015 [53] and the retail floor space of the largest commercial centres in London [52] as the initial origin zone and destination zone sizes respectively, i.e. and , and from this generate a synthetic time series using the parameters estimated in [31] for a high noise level of . For the network we use the Google Distance Matrix API111developers.google.com/maps/documentation/distance-matrix to extract the shortest travel time between nodes, using either public transport or driving. The network weights are derived in [57] as

where the scale factor ensures a unitless exponent.

We generate a synthetic time series of time steps, from which we subsample 2-step windows, giving a total training set size of time steps. This is to ensure we sample a sufficiently broad spectrum of the system’s dynamics, thereby fully determining the inference problem and isolating the effect of the training noise. A hyperparameter sweep on synthetic data showed that using a neural network with layers, 20 nodes per layer, and no bias yields optimal results. We use the hyperbolic tangent as the activation function on all layers except the last, where we use the standard sigmoid function (since the network is complete, there is no need to use the hard sigmoid as all edge weights are nonzero). To train the neural network we use the simple loss function

where and are the predicted and true time series of destination zone sizes. Since the dynamics are invariant under scaling of the cost matrix , we normalise the row sums of the predicted and true networks, .

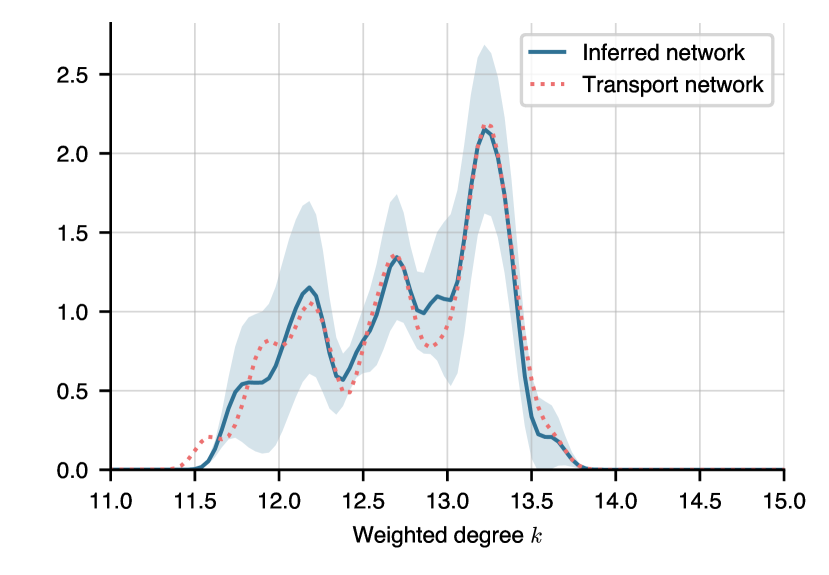

Figure 4c shows the inferred distribution of the (weighted) origin zone node degrees . The solid line is the maximum likelihood prediction, and the dotted red line the true distribution . Even with a high level of noise, the model manages to accurately predict the underlying connectivity matrix, comprising over 30.000 weights, in under 5 minutes on a regular laptop CPU. Uncertainty on is given by the standard deviation,

| (8) |

where is the maximum likelihood estimator. As we will discuss in the last section, this method meaningfully captures the uncertainty due to the noise in the data and the degree to which the problem is underdetermined.

Comparative performance analysis

We now analyse our method’s performance, both in terms of prediction quality and computational speed, by comparing it to a Markov-Chain Monte Carlo approach (MCMC) as well as a classical regression method, presented e.g. in [58, 6]. As mentioned in the introduction, computationally efficient network learning methods have been developed for specific data structures; however, we compare our approach with MCMC and OLS since both are general in the types of data to which they are applicable.

Consider noisy Kuramoto dynamics,

| (9) |

with independent white noise processes with strength , and the eigenfrequencies of the nodes. Given observations of each node’s dynamics, we can gather the left side into a single vector for each node, and obtain equations

| (10) |

with the -th row of the adjacency matrix , and the observations of the the interaction terms . From this we can then naturally estimate the -th row of using ordinary least squares:

| (11) |

Given sufficiently many linearly independent observations, the Gram matrices will all be invertible; in the underdetermined case, a pseudoinverse can be used to approximate their inverses. As before, the diagonal of is manually set to 0.

In addition to regression, we also compare our method to a preconditioned Metropolis-adjusted Langevin sampling scheme (MALA) [27, 28, 59, 29], which constructs a Markov chain of sampled adjacency matrices by drawing proposals from the normal distribution

| (12) |

Here, is the integration step size, a preconditioner (note that we are reshaping into an -dimensional vector), and its average eigenvalue. Each proposal is accepted with probability

| (13) |

with the transition probability

| (14) |

We tune so that the acceptance ratio converges to the optimum value of [60].

We set the preconditioner to be the inverse Fisher information covariance matrix

| (15) |

which has been shown to optimise the expected squared jump distance [29]. The expectation value is calculated empirically over all samples drawn using the efficient algorithm given in [29]. In all experiments, we employ a ‘warm start’ by initialising the sampler close to the minimum of the problem. We found this to be necessary in such high dimensions (between 256 and 490.000) to produce decent results. Unlike the MCMC sampler, the neural network is initialised randomly.

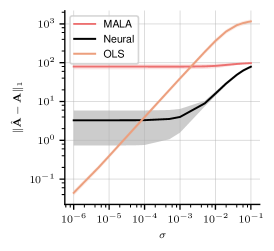

(a) Accuracy as a function of noise

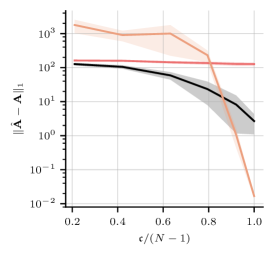

(b) Accuracy as a function of convexity

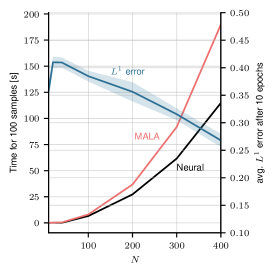

(c) Compute times

(d) Degree distribution,

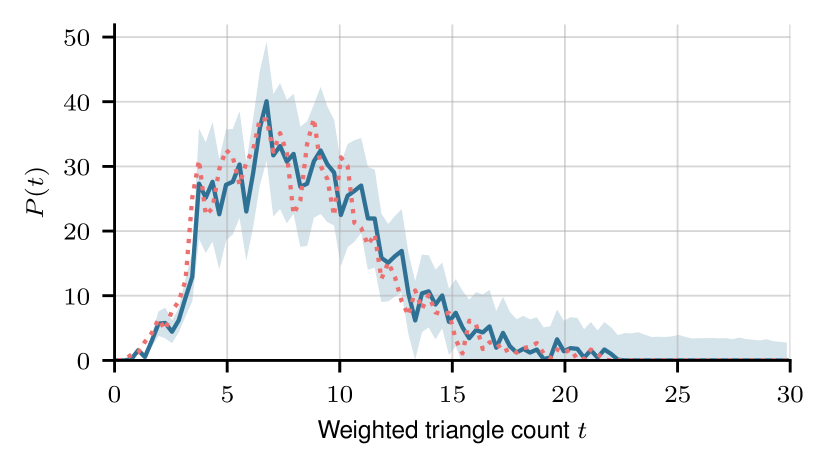

(e) Triangle distribution,

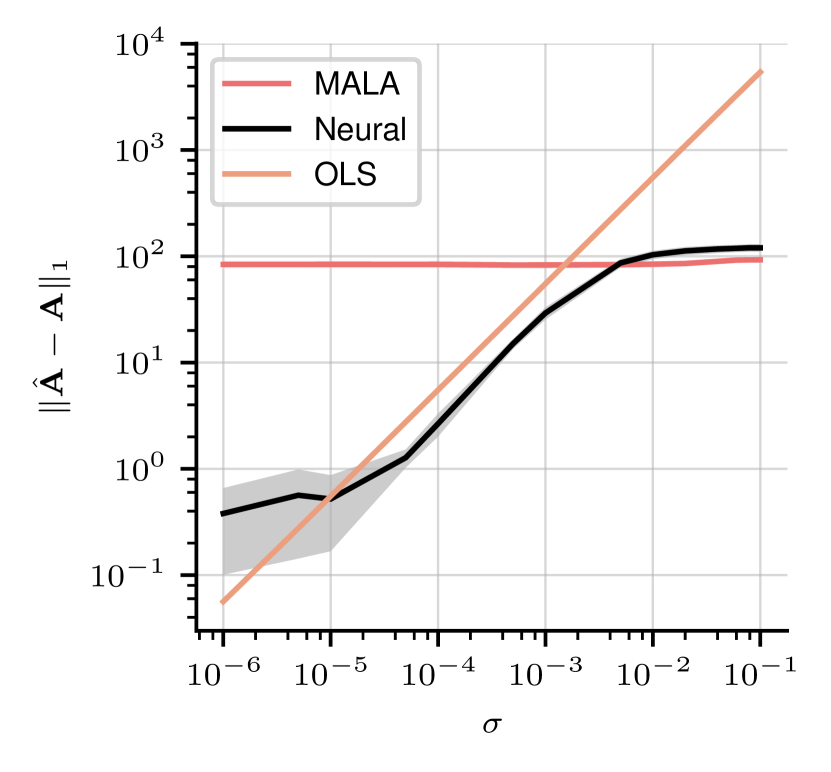

Figures 5a–b show our method’s prediction accuracy alongside that of OLS regression and preconditioned MALA on synthetic Kuramoto data; the accuracy here is defined as the error

| (16) |

where is the mode of the posterior. In fig. 5a, the accuracy is shown as a function of the noise on the training data. We generate enough data to ensure the likelihood function is unimodal. For the practically noiseless case of , the regression scheme on average outperforms the neural approach; however, even for very low noise levels and above, the neural approach proves far more robust, outperforming OLS by up to one order of magnitude and maintaining its prediction performance up to low noise levels of . Meanwhile, we find that in the low- to mid-level noise regime, the neural scheme approximates the mode of the distribution by between one to two orders of magnitude more accurately than the Langevin sampler. For high levels of noise (), the performances of the neural and MALA schemes converge. These results hold both for first-order () and second-order Kuramoto dynamics [3]; in the second-order case, the neural method begins outperforming OLS at even lower levels of than in the first-order case, though the improvement is not as significant (cf fig. S6 in the appendix).

In figure 5b we show the accuracy as a function of the convexity of the loss function. In general, it is hard to quantify the convexity of , since we do not know how many networks fit the equation at hand. However, when the dynamics are linear in the adjacency matrix , we can do so using the Gram matrices of the observations of each node , , where we quantify the (non-)convexity of the problem by the minimum rank of all the Gram matrices,

| (17) |

The problem is fully determined if and all Gram matrices are invertible. As shown, regression is again more accurate when the problem is close to fully determined; however, as decreases, the accuracy quickly drops, with the neural scheme proving up to an order of magnitude more accurate. Meanwhile, the MCMC scheme is consistently outperformed by the neural scheme, though it too eclipses regression for . In summary, regression is only viable for the virtually noiseless and fully determined case, while the neural scheme maintains good prediction performance even in the noisy and highly underdetermined case (see also fig. 5d–e).

(a) Convexity uncertainty on

(b) Noise uncertainty on

(c) Noise uncertainty on

In figure 5c we show compute times to obtain 100 samples for both the neural and MALA schemes. The complexity of the neural scheme is , with the number of training epochs. This is because each epoch of the model equation requires operations for the vector-matrix multiplication in eq. [11], and for the stochastic gradient descent update, where we are holding constant to ensure comparability. As is visible, the average error per edge weight remains constant over , showing that the number of epochs required to achieve a given node-averaged prediction accuracy is independent of . The preconditioned MALA scheme is considerably slower, due to the computational cost of calculating the preconditioner and the Metropolis-Hastings rejection step.

Lastly, figures 5d–e show the estimated weighted degree and triangle distributions of a large graph with 1000 nodes, or 1 million edge weights to be estimated, for noisy training data. The number of weighted, undirected triangles on each node is given by . The model robustly finds the true adjacency matrix, and we again quantify uncertainty on the prediction using the standard deviation eq. [8]. Estimating a network with 1000 nodes on a standard laptop CPU took about 1 hour, which reduces to 6 minutes when using a GPU. Most high-performance network inference techniques demonstrate their viability on graphs with at most this number of nodes, e.g. ConNIe [19] and NetINF [21]. In [19], the authors state that graphs with 1000 nodes can typically be inferred from cascade data in under 10 minutes on a standard laptop. Similarly, the authors of NetINF [21] state that it can infer a network with 1000 nodes in a matter of minutes, though this algorithm does not infer edge weights, only the existence of edges, and neither technique provides uncertainty quantification.

Quantifying uncertainty

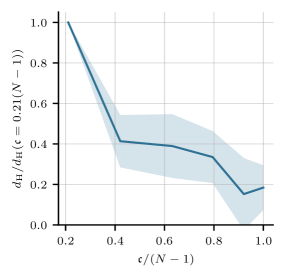

There are two sources of uncertainty when inferring adjacency matrices: the non-convexity of the loss function , and the noise on the data. In figure 6a we show the expected Hellinger error

| (18) |

on the predicted degree distribution as a function of . As is visible, the error on the distribution decreases as tends to its maximum value of . For , some residual uncertainty remains due to the uncertainty on the neural network parameters .

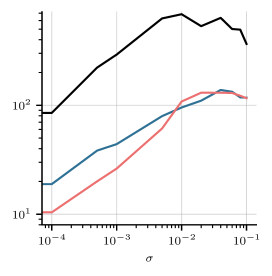

In figures 6b–c we show the expected Hellinger error (eq. [18]) on the maximum likelihood estimator as a function of , for both the degree and triangle distributions, i.e. . In addition, we also show the behaviour of the expected relative entropy

| (19) |

and the total standard deviation

| (20) |

All three metrics reflect the noise on the training data, providing similarly behaved, meaningful uncertainty quantification. As the noise tends to 0, some residual uncertainty again remains, while for very high noise levels the uncertainty begins to plateau. Our method thus manages to capture the uncertainty arising from both sources: the non-convexity of and the noise on the data.

Discussion

In this work we have demonstrated a performative method to estimate network adjacency matrices from time series data. We showed its effectiveness at correctly and reliably inferring networks in a variety of scenarios: convex and non-convex cases, low to high noise regimes, and equations that are both linear and non-linear in . We were able to reliably infer power line failures in the national power grid of Great Britain, and the connectivity matrix of an economic system covering all of Greater London. We showed that our method is well able to handle inference of hundreds of thousands to a million edge weights, while simultaneously giving uncertainty quantification that meaningfully reflects both the non-convexity of the loss function as well as the noise on the training data. Our method is significantly more accurate than MCMC sampling, and outperforms OLS regression in all except the virtually noiseless and fully determined cases. This is an important improvement since large amounts of data are typically required to ensure the network inference problem is fully determined, which may often not be available, as suggested in the power grid study. Unlike regression, our method also naturally extends to the case of non-linear dynamics. In conjunction with our previous work [31], we have now also demonstrated the viability of using neural networks for parameter calibration in both the low- and high-dimensional case. Our method is simple to implement as well as highly versatile, giving excellent results across a variety of problems. All experiments in this work were purposefully conducted on a standard laptop CPU, typically taking on the order of minutes to run.

Many lines for future research open up from this work. Firstly, a thorough theoretical investigation of the method is warranted, establishing rigorous convergence guarantees and bounds on the error of the posterior estimate. Another direction is further reducing the amount of data required to accurately learn parameters, and in future research the authors aim to address the question of learning system properties from observations of a single particle trajectory at the mean-field limit [61, 62]. In this work we have also not considered the impact of the network topology on the prediction performance, rather focusing on the physical dynamics of the problem. An interesting question is to what degree different network structures themselves are amenable to or hinder the learning process.

Over the past decade much work has been conducted into graph neural architectures [63, 64], the use of which may further expand the capabilities of our method. More specialised architectures may prove advantageous for different (and possibly more difficult) inference tasks, though we conducted a limited number of experiments with alternatives (e.g. autoencoders, cf. fig. S4) and were unable to find great performance improvements. Finally, one drawback of our proposed method in its current form is it that it requires differentiability of the model equations in the parameters to be learned; future research might aim to develop a variational approach to expand our method to weakly differentiable settings.

Data, materials, and Software Availability

Code and synthetic data can be found under https://github.com/ThGaskin/NeuralABM. It is easily adaptable to new models and ideas. The code uses the utopya package222utopia-project.org, utopya.readthedocs.io/en/latest [65, 66] to handle simulation configuration and efficiently read, write, analyse, and evaluate data. This means that the model can be run by modifying simple and intuitive configuration files, without touching code. Multiple training runs and parameter sweeps are automatically parallelised. The neural core is implemented using pytorch333pytorch.org. All synthetic datasets as well as the London dataset have been made available, together with the configuration files needed to reproduce the plots. Detailed instructions are provided in the supplementary material and the repository. The British power grid data [46, 47, 48] is property of the respective organisations and cannot be made available without permission; however, as of early 2023 it is freely available from those organisations upon request. The code used to run the experiments is available in the repository.

Author contributions

TG, GP, MG designed and performed the research and wrote the paper; TG wrote the code and performed the numerical experiments.

Acknowledgements

The authors are grateful to Dr Andrew Duncan (Imperial College London) for fruitful discussions on power grid dynamics, and to the anonymous reviewers for their helpful comments during the peer review process. TG was funded by the University of Cambridge School of Physical Sciences VC Award via DAMTP and the Department of Engineering, and supported by EPSRC grants EP/P020720/2 and

EP/R018413/2. The work of GP was partially funded by EPSRC grant EP/P031587/1. MG was supported by EPSRC grants EP/T000414/1, EP/R018413/2,

EP/P020720/2, EP/R034710/1, EP/R004889/1, and a Royal Academy of Engineering Research Chair.

References

- [1] SW Simard, et al., Mycorrhizal networks: Mechanisms, ecology and modelling. Fungal Biology Reviews 26, 39–60 (2012).

- [2] C Hettenhausen, et al., Stem parasitic plant Cuscuta australis (dodder) transfers herbivory-induced signals among plants. Proceedings of the National Academy of Sciences 114, E6703–E6709 (2017).

- [3] D Brockmann, D Helbing, The Hidden Geometry of Complex, Network-Driven Contagion Phenomena. Science 342, 1337–1342 (2013).

- [4] N Molkenthin, M Schröder, M Timme, Scaling Laws of Collective Ride-Sharing Dynamics. Physical Review Letters 125 (2020).

- [5] I Simonsen, L Buzna, K Peters, S Bornholdt, D Helbing, Transient Dynamics Increasing Network Vulnerability to Cascading Failures. Physical Review Letters 100 (2008).

- [6] SG Shandilya, M Timme, Inferring network topology from complex dynamics. New Journal of Physics 13, 013004 (2011).

- [7] U Stelzl, et al., A Human Protein-Protein Interaction Network: A Resource for Annotating the Proteome. Cell 122, 957–968 (2005).

- [8] SR Proulx, DE Promislow, PC Phillips, Network thinking in ecology and evolution. Trends in Ecology & Evolution 20, 345–353 (2005) Special issue: Bumper book review.

- [9] S Allesina, D Alonso, M Pascual, A General Model for Food Web Structure. Science 320, 658–661 (2008).

- [10] J Tegnér, MKS Yeung, J Hasty, JJ Collins, Reverse engineering gene networks: Integrating genetic perturbations with dynamical modeling. Proceedings of the National Academy of Sciences 100, 5944–5949 (2003).

- [11] BO Palsson, Systems Biology: Properties of Reconstructed Networks. (Cambridge University Press, New York, NY, USA), (2006).

- [12] D Sarmah, et al., Network inference from perturbation time course data. npj Systems Biology and Applications 8 (2022).

- [13] B Shen, G Coruzzi, D Shasha, EnsInfer: a simple ensemble approach to network inference outperforms any single method. BMC Bioinformatics 24 (2023).

- [14] M Batty, R Milton, A new framework for very large-scale urban modelling. Urban Studies 58, 3071–3094 (2021).

- [15] L Ellam, M Girolami, GA Pavliotis, A Wilson, Stochastic modelling of urban structure. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences 474, 20170700 (2018).

- [16] MD Vicario, et al., The spreading of misinformation online. Proceedings of the National Academy of Sciences 113, 554–559 (2016).

- [17] S Aral, L Muchnik, A Sundararajan, Engineering social contagions: Optimal network seeding in the presence of homophily. Network Science 1, 125–153 (2013).

- [18] S Vosoughi, D Roy, S Aral, The spread of true and false news online. Science 359, 1146–1151 (2018).

- [19] SA Myers, J Leskovec, On the Convexity of Latent Social Network Inference in Proceedings of the 23rd International Conference on Neural Information Processing Systems - Volume 2, NIPS’10. (Curran Associates Inc., Red Hook, NY, USA), pp. 1741–1749 (2010).

- [20] M Gomez-Rodriguez, D Balduzzi, B Schölkopf, Uncovering the Temporal Dynamics of Diffusion Networks in Proceedings of the 28th International Conference on International Conference on Machine Learning, ICML’11. (Omnipress, Madison, WI, USA), pp. 561–568 (2011).

- [21] M Gomez-Rodriguez, J Leskovec, A Krause, Inferring Networks of Diffusion and Influence. ACM Transactions on Knowledge Discovery from Data 5, 1–37 (2012).

- [22] VA Makarov, F Panetsos, O de Feo, A method for determining neural connectivity and inferring the underlying network dynamics using extracellular spike recordings. Journal of Neuroscience Methods 144, 265–279 (2005).

- [23] FV Bussel, Inferring synaptic connectivity from spatio-temporal spike patterns. Frontiers in Computational Neuroscience 5 (2011).

- [24] N Meinshausen, P Bühlmann, High-dimensional graphs and variable selection with the Lasso. The Annals of Statistics 34, 1436 – 1462 (2006).

- [25] M Yuan, Y Lin, Model Selection and Estimation in the Gaussian Graphical Model. Biometrika 94, 19–35 (2007).

- [26] M Timme, J Casadiego, Revealing networks from dynamics: an introduction. Journal of Physics A: Mathematical and Theoretical 47, 343001 (2014).

- [27] M Girolami, B Calderhead, Riemann manifold Langevin and Hamiltonian Monte Carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 73, 123–214 (2011).

- [28] C Li, C Chen, D Carlson, L Carin, Preconditioned Stochastic Gradient Langevin Dynamics for Deep Neural Networks in Proceedings of the Thirtieth AAAI Conference on Artificial Intelligence, AAAI’16. (AAAI Press), pp. 1788–1794 (2016).

- [29] MK Titsias, Optimal Preconditioning and Fisher Adaptive Langevin Sampling (2023).

- [30] S Göttlich, C Totzeck, Parameter calibration with stochastic gradient descent for interacting particle systems driven by neural networks. Mathematics of Control, Signals, and Systems 34, 185–214 (2021).

- [31] T Gaskin, GA Pavliotis, M Girolami, Neural parameter calibration for large-scale multi-agent models. Proceedings of the National Academy of Sciences 120 (2023).

- [32] J Lee, et al., Deep Neural Networks as Gaussian Processes in International Conference on Learning Representations. (2018).

- [33] AGdG Matthews, M Rowland, J Hron, RE Turner, Z Ghahramani, Gaussian Process Behaviour in Wide Deep Neural Networks (2018).

- [34] R Novak, et al., Bayesian Deep Convolutional Networks with Many Channels are Gaussian Processes in International Conference on Learning Representations. (2019).

- [35] DP Kingma, M Welling, Auto-Encoding Variational Bayes (2013).

- [36] C Blundell, J Cornebise, K Kavukcuoglu, D Wierstra, Weight Uncertainty in Neural Networks in Proceedings of the 32nd International Conference on International Conference on Machine Learning - Volume 37, ICML’15. (JMLR.org), pp. 1613–1622 (2015).

- [37] Y Gal, Z Ghahramani, Dropout as a Bayesian Approximation: Representing Model Uncertainty in Deep Learning. Proceedings of The 33rd International Conference on Machine Learning 48, 1050–1059 (2016).

- [38] AM Stuart, Inverse problems: A Bayesian perspective. Acta Numerica 19, 451–559 (2010).

- [39] DP Kingma, J Ba, Adam: A Method for Stochastic Optimization. arXiv 1412.6980 [cs.LG] (2014).

- [40] Y Kuramoto, Self-entrainment of a population of coupled non-linear oscillators in International Symposium on Mathematical Problems in Theoretical Physics, ed. H Araki. (Springer-Verlag), pp. 420–422 (1975).

- [41] G Filatrella, AH Nielsen, NF Pedersen, Analysis of a power grid using a Kuramoto-like model. The European Physical Journal B 61, 485–491 (2008).

- [42] M Rohden, A Sorge, M Timme, D Witthaut, Self-Organized Synchronization in Decentralized Power Grids. Phys. Rev. Lett. 109, 064101 (2012).

- [43] T Nishikawa, AE Motter, Comparative analysis of existing models for power-grid synchronization. New Journal of Physics 17, 015012 (2015).

- [44] YP Choi, Z Li, Synchronization of nonuniform Kuramoto oscillators for power grids with general connectivity and dampings. Nonlinearity 32, 559–583 (2019).

- [45] Department for Business, Energy and Industrial Strategy, Digest of UK Energy Statistics 5: Electricity (2022).

- [46] National Grid, Transmission Network Shapefiles (https://www.nationalgrid.com/electricity-transmission/network-and-infrastructure/network-route-maps) (2023).

- [47] SP Energy Networks, Transmission Network GIS Shapefiles (https://www.spenergynetworks.co.uk/pages/utility_map_viewer.aspx) (2023).

- [48] Scottish and Southern Electricity Networks, Transmission Network GIS Shapefiles (https://www.ssen.co.uk/globalassets/library/connections---useful-documents/network-maps/5-gis-guide-shape-files-v1.pdf) (2023).

- [49] Hardsigmoid – Pytorch Documentation, Hardsigmoid (2023).

- [50] Hardsigmoid – Tensorflow Documentation, Hardsigmoid (2023).

- [51] F Basiri, J Casadiego, M Timme, D Witthaut, Inferring power-grid topology in the face of uncertainties. Phys. Rev. E 98, 012305 (2018).

- [52] Greater London Authority, 2017 Health Check Report (2017).

- [53] Greater London Authority, 2015 ward profiles and atlas (2015) Online.

- [54] Greater London Authority, Statistical boundary files for London (2011).

- [55] B Harris, AG Wilson, Equilibrium Values and Dynamics of Attractiveness Terms in Production-Constrained Spatial-Interaction Models. Environment and Planning A: Economy and Space 10, 371–388 (1978).

- [56] GA Pavliotis, Stochastic Processes and Applications. (Springer New York), (2014).

- [57] A Wilson, A statistical theory of spatial distribution models. Transportation Research 1, 253–269 (1967).

- [58] M Timme, Revealing Network Connectivity from Response Dynamics. Physical Review Letters 98, 224101 (2007).

- [59] S Chewi, et al., Optimal dimension dependence of the Metropolis-Adjusted Langevin Algorithm in Proceedings of Thirty Fourth Conference on Learning Theory, Proceedings of Machine Learning Research, eds. M Belkin, S Kpotufe. (PMLR), Vol. 134, pp. 1260–1300 (2021).

- [60] GO Roberts, JS Rosenthal, Optimal Scaling of Discrete Approximations to Langevin Diffusions. Journal of the Royal Statistical Society Series B: Statistical Methodology 60, 255–268 (2002).

- [61] GA Pavliotis, A Zanoni, A method of moments estimator for interacting particle systems and their mean field limit. arXiv 2212.00403 [math.NA] (2022).

- [62] N Zagli, GA Pavliotis, V Lucarini, A Alecio, Dimension reduction of noisy interacting systems. Phys. Rev. Res. 5, 013078 (2023).

- [63] MM Bronstein, J Bruna, Y LeCun, A Szlam, P Vandergheynst, Geometric Deep Learning: Going beyond Euclidean data. IEEE Signal Processing Magazine 34, 18–42 (2017).

- [64] L Wu, P Cui, J Pei, L Zhao, Graph Neural Networks: Foundations, Frontiers, and Applications. (Springer Singapore, Singapore), p. 725 (2022).

- [65] L Riedel, B Herdeanu, H Mack, Y Sevinchan, J Weninger, Utopia: A Comprehensive and Collaborative Modeling Framework for Complex and Evolving Systems. Journal of Open Source Software 5, 2165 (2020).

- [66] Y Sevinchan, B Herdeanu, J Traub, dantro: a Python package for handling, transforming, and visualizing hierarchically structured data. Journal of Open Source Software 5, 2316 (2020).

- [67] National Grid ESO, What is Frequency? (https://www.nationalgrideso.com/electricity-explained/how-do-we-balance-grid/what-frequency) (2023).

Supporting Information

Neural networks

Notation and Terminology

A neural network is a sequence of length of concatenated transformations. Each layer of the net consists of neurons, connected through a sequence of weight matrices . Each layer applies the transformation

to the input from the previous layer, where is the bias of the -th layer. The function is the activation function; popular choices include the rectified linear unit (ReLU) activation function , and the sigmoid activation function . A neural net has an input layer, an output layer, and hidden layers, which are the layers in between the in- and output layers. If a network only has one hidden layer, we call it shallow, else we call the neural net deep.

[height=7, nodesize=25, nodespacing=12mm, layerspacing=28mm]

; ; ; ;

[count=5, bias=true, title=Input layer, text=[count=4, bias=true, text=\hiddenlayer[count=5, bias=true, title=Hidden layers, text=\hiddenlayer[count=6, bias=true, text=\outputlayer[count=3, title=Output layer, text=

Choice of architecture

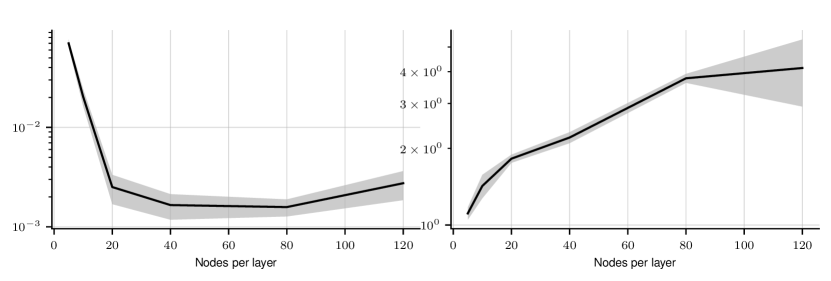

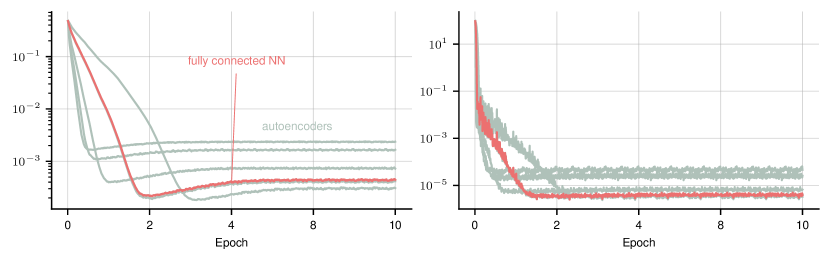

Here we provide additional studies to justify our choice of neural architecture. To select an appropriate architecture, we ran a hyperparameter sweep on synthetic Kuramoto data with nodes, 70 training datasets and time steps per dataset. Using a simple feed-forward architecture, we performed a sweep over the number of layers, nodes in each layer and activation functions used. Figures S2a—d show that using 5 layers with 20 nodes per layer reduces the training loss optimally, and that further increasing the layer size only marginally reduces the prediction error. In addition, using very large, highly overparametrised models has the disadvantage of increased computational cost. Similar results hold for the Harris-Wilson dynamics eq. [6].

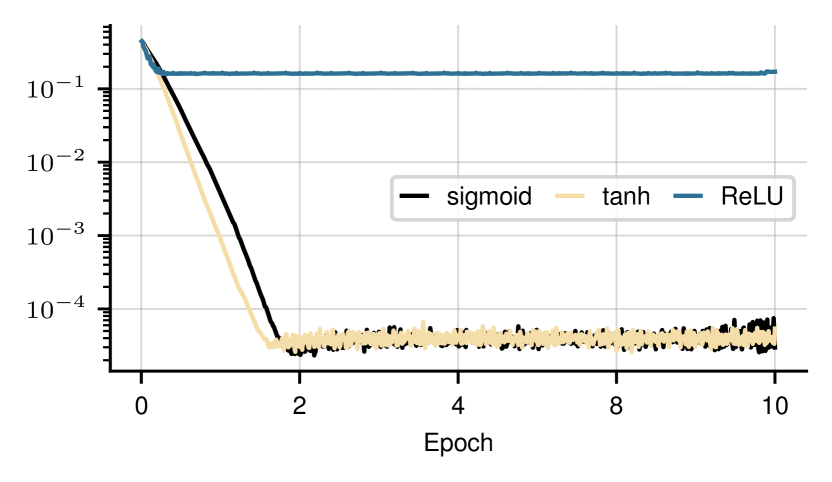

We also considered the use of different activation functions on the deep and final layers of the neural network (cf. fig. S3). On the inner layers, both a sigmoid and a hyperbolic tangent produce good results, while using anything other than the hard sigmoid on the final layer leads to poor results.

Lastly, using an autoencoder architecture instead of a feed-forward network produces no tangible benefits, so in the interest of simplicity we choose a simple feed-forward architecture S4.

(a) prediction error

(b) Training loss

(c) prediction error

(d) Avg. compute time per epoch [s]

(a) Deep layer activation functions

(b) Final layer activation function

(a) prediction error

(b) Training loss

(a) Distances

(b) Voltages

(c) Admittances

(d) Scaled edge weights

Inferring line failures in the British power grid

Initialisation of the neural network weights

We initialise the neural network’s weights with a prior in such a way that the prior is a delta distribution on the complete graph, . This can easily be achieved by training the neural network using the simple loss function

with a matrix of ones in all entries except on the diagonal, where it is zero. This only requires a few training steps, and helps maximise the sampling domain on each edge, making the calculations of p-values in our example more straightforward. However, we should stress that this initialisation is not necessary to obtain good calibration results.

Constructing the admittance matrix

Here we provide some additional information on the calculation of the network edge weights from the data. The weights quantify the admittance (inverse impedance) of the line, that is, how easily the line can transmit electrical current. The characteristic impedance of a transmission line is given by

| (21) |

with the complex unit, the grid frequency [67], the cable inductance, and its capacitance. We use the following values for a copper conductor with a cross-section of 1000 mm2, provided by a standard manufacturer444caledonian-cables.co.uk/products/hv/400kv.shtml of power grid cables: /km (AC resistance), mH/km, F/km (assuming a single core). The total impedance along the line is then given by

| (22) |

where is the length of the line, and the propagation constant is given by

| (23) |

In these calculations we neglect the conductance of the dielectric along the line, which is neglibile at the distances present in the network. The admittance of the line is then given by

| (24) |

and the total edge weight by

| (25) |

Long lines typically carry two to four times as many cables as shorter lines. We account for this by multiplying the admittance of lines over 10 km by a factor of 2, and those over 80 with a factor of 3 (admittances are additive). Since the neural network outputs values in , we scale the edge weights to this range. However, a small number of short lines artificially skew the distribution (see figure S5); these are mainly small segments designed to more accurately capture the geometry of a longer line, though sometimes they represent short lines to transformers, power stations, etc. To reduce their impact on the weight distribution, instead of dividing the weights by the maximum value, we divide by the mean and truncate all weights to :

| (26) |

The scaling factor is absorbed into the coupling coefficient . Those edges with weight exactly equal to 1 are reassigned a value chosen uniformly at random in . As is visible in fig. S5d, the resulting distribution of the weights is more uniform than that of the distances and admittances , since longer lines’ lower admittance is often compensated by a higher voltage.

These calculations do not account for, among other things, the fact that we are connecting the nodes with straight lines rather than the real line trajectory, are not discerning between overground and underground lines, are assuming a single core per cable, and are not considering differences in transmission line heights, geometries, and materials. These inaccuracies are absorbed into the coefficients and , which we tune manually in order to allow for stable phase-locking.

Comparative performance analysis

In figure S6 we show the equivalent of fig. 5a for the case of second-order Kuramoto dynamics (eq. [3] with ). We again see the neural scheme outperforming OLS regression at very low levels of the noise, though the performance improvement is less stark than in the first-order case. MALA marginally outperforms the neural scheme at very high noise levels. Enough data is used to ensure full invertibility of the Gram matrix ().

Details on the code

The code is uploaded to the Github repository as given in the main text. The two models relevant to this work are Kuramoto and HarrisWilsonNW.

Installation

Detailed installation instructions are given in the repository. First, clone the repository, install the utopya package and all the required additional components into a virtual environment, for example via PyPi. In particular, install pytorch. Enter the virtual environment. Then, from within the project folder, register the project:

You should get a positive response from the utopya CLI and your project should appear in the project list when calling:

Note that any changes to the project info file need to be communicated to utopya by calling the registration command anew. You will then have to additionally pass the --exists-action overwrite flag, because a project of that name already exists. See

for more information. Finally, register the project and its models via

Running the code

To run a model, execute the following command:

By default, this runs the model with the settings in the <model_name>_cfg.yml file. All data and the plots are written to an output directory, typically located in ~/utopya_output. To run the model with different settings, create a run_cfg.yml file and pass it to the model like this:

This is recommended rather than changing the default settings, because the defaults are parameters that are known to work and you may wish to fall back on in the future.

Plots are generated using the plots specified in the <model_name>_plots.yml file. These too can be updated by creating a custom plot configuration, and running the model like this:

See the Utopia tutorial for more detailed instructions.

All the images in this article can be generated using so-called configuration sets, which are complete bundles of both run configurations and evaluation configurations. For example, to generate the predictions on the random network with nodes (fig. 5d–e) for the Kuramoto model, you can call

This will run and evaluate the Kuramoto model with all the settings from the Kuramoto/cfgs/N_100_example/run.yml and eval.yml configurations.

Parameter sweeps

Parameter sweeps are automatically parallelised by utopya, meaning simulation runs are always run concurrently whenever possible. The data is automatically stored and loaded into a data tree. To run a sweep, simply add a !sweep tag to the parameters you wish to sweep over, and specify the values, along with a default value to be used if no sweep is performed:

Then in the run configuration, add the following entry:

Alternatively, call the model with the flag --run-mode sweep. The configuration sets used in this work automatically run sweeps whenever needed, so no adjustment is needed to recreate the plots used in this work.

Initialising the neural net

The neural net is controlled from the NeuralNet entry of the configuration:

num_layers specifies the depth of the net; nodes_per_layer controls the architecture: provide a default size, and optionally any deviations from the default under layer_specific. The keys of the layer_specific entry should be indices of the layer in question. The optional biases entry determines whether or not biases are to be included in the architecture, and if so how to initialise them. A default and layer-specific values can again be passed. Setting an entry to default initialises the values using the pytorch default initialiser, a Xavier uniform initialisation. Passing a custom interval instead initialises the biases uniformly at random on that interval, and passing a tilde ~ (None in YAML) turns the bias off. activation_funcs is a dictionary specifying the activation functions on each layer, following the same logic as above. Any pytorch activation function is permissible. If a function requires additional arguments, these can be passed as in the example above. Lastly, the optimizer keyword takes any argument allowed in pytorch. The default optimizer is the Adam optimizer [39] with a learning rate of .

The neural net can be initialised from different initial values in the parameter space by changing the random seed in the configuration:

Sweeping over different initialisations is achieved by sweeping over the seed, as described in the previous section.

Training the neural net

The Training entry of the configuration controls the training process:

You must specify the noise level to use for the ABM during training; the default value is . Under the loss_function key you can specify the loss function to use, and pass any arguments or keyword arguments it may require using an args or kwargs key. You can use any available pytorch loss function.

The device key sets the training device. The default is the CPU, but you can also train on the GPU by setting the device to cuda. Note that on Apple Silicon, the device name is mps. Make sure you have installed the correct package for your device, and note that, as of writing, some pytorch functions required for our code (e.g., the trace and hard sigmoid functions) had not yet been implemented for MPS, hence GPU training on Apple Silicon devices was not possible.

Kuramoto model

Neural Network Architecture

The following is the default configuration for the neural network and training settings used for the Kuramoto model:

Training

We rewrite [3] as a vector-matrix equation,

which is more amenable to machine learning purposes, since it can make use of fast matrix-multiplication operations. is the interaction kernel matrix, . We the train the model using the following numerical operation: let be the current phases of the nodes, the vector of phase derivatives, the vector of eigenfrequencies, and ; then in each iteration of the first-order Kuramoto model (), we do

| (27) |

where takes the diagonal elements of the matrix. For the second-order model (), we do

| (28) |

In the first-order case, the initial conditions required are , in the second order case, we need and (i.e. the initial phases and initial velocities).

Running the code

Configuration sets to reproduce all numerical experiments except the British power grid inference are provided; for instance, to produce the predictions for a random network with nodes, simply run

Harris-Wilson model

Neural Network Architecture

The following is the default configuration for the neural network and training settings used for the Harris-Wilson model:

Training

We use the following matrix form of the Harris-Wilson equations to train the neural net. Let , , be the demand vector, origin zone size vector, and destination zone size vector respectively. The the dynamics are given by

| (29) |

with indicating the Hadamard product, and elementwise exponentiation. is the vector of normalisation constants

| (30) |

The dynamics then read

| (31) |

with given initial conditions . This formulation is more conducive to machine learning purposes, since it contains easily differentiable matrix operations and does not use for-loop iteration.

Running the code

This is analogous to the Kuramoto case. To reproduce the plot from the main article, run the following command: