The Online Pause and Resume Problem: Optimal Algorithms and An Application to Carbon-Aware Load Shifting

Abstract

We introduce and study the online pause and resume problem. In this problem, a player attempts to find the lowest (alternatively, highest) prices in a sequence of fixed length , which is revealed sequentially. At each time step, the player is presented with a price and decides whether to accept or reject it. The player incurs a switching cost whenever their decision changes in consecutive time steps, i.e., whenever they pause or resume purchasing. This online problem is motivated by the goal of carbon-aware load shifting, where a workload may be paused during periods of high carbon intensity and resumed during periods of low carbon intensity and incurs a cost when saving or restoring its state. It has strong connections to existing problems studied in the literature on online optimization, though it introduces unique technical challenges that prevent the direct application of existing algorithms. Extending prior work on threshold-based algorithms, we introduce double-threshold algorithms for both the minimization and maximization variants of this problem. We further show that the competitive ratios achieved by these algorithms are the best achievable by any deterministic online algorithm. Finally, we empirically validate our proposed algorithm through case studies on the application of carbon-aware load shifting using real carbon trace data and existing baseline algorithms.

1 Introduction

This paper introduces and studies the online pause and resume problem (OPR), considering both minimization (OPR-min) and maximization (OPR-max) variants. In OPR-min, a player is presented with time-varying prices in a sequential manner and decides whether or not to purchase one unit of an item at the current price. The player must purchase units of the item over a time horizon of and they incur a switching cost whenever their decision changes in consecutive time steps, i.e., whenever they pause or resume purchasing. The goal of the player is to minimize their total cost, which consists of the aggregate price of purchasing units and the aggregate switching cost incurred over slots. In OPR-max, the setting is exactly the same, but the goal of the player is to maximize their total profit, and any switching cost they incur is subtracted. In both cases, the price values are revealed to the player one by one in an online manner, and the player has to make a decision without knowing the future values.

Our primary motivation for introducing OPR is the emerging importance of carbon-aware computing and, more specifically, carbon-aware temporal workload shifting, which has seen significant attention in recent years [RKS+22, ALK+23, BGH+21, WBS+21]. In carbon-aware temporal workload shifting, an interruptible and deferrable workload may be paused during periods of high carbon intensity and resumed during periods of low carbon intensity. The workload needs to be running for units of time to complete and must be finished before its deadline . However, pausing and resuming the workload typically comes with overheads such as storing the state in memory and checkpointing; hence frequent pausing and resuming is undesirable. The objective of temporal workload shifting is to minimize the total carbon footprint of running the workload, which includes both the original compute demand and the overhead due to pausing and resuming (a.k.a., the switching cost). The carbon intensity of the electric grid is time-varying due to the intermittency of renewable energy, and thus finding the best pause and resume strategy is challenging due to the unknown future fluctuations of carbon intensity. Note that OPR can also capture other potentially interesting applications where pricing changes over time and switching frequently is undesirable. One example is renting spot virtual machines from a cloud service provider in the setting where pricing is set according to supply-demand dynamics [ZLW17, ABI+20, SRI16].

On the theory front, the OPR problem has strong connections to various existing problems in the literature on online optimization. We extensively review the prior literature in Section 7 and focus on the most relevant theoretical problems below. The OPR problem is strongly connected to the -search problem [LPS08, LSLH22], which belongs to the broader class of online conversion problems [SLH+21], a.k.a, time series search and one-way trading [EYFKT01]. In the minimization variant of the -search problem, an online decision-maker aims to buy units of an item for the least cost over a sequence of time-varying cost values. At each step, a cost value is observed, and the decision is whether or not to buy one unit at the current observed cost without knowing the future values. In contrast to -search, the OPR problem introduces the additional component of managing the switching cost, which poses a significant additional challenge in algorithm design.

The existence of the switching cost in OPR connects it to the well-studied problem of smoothed online convex optimization (SOCO) [LLWA12], also known as convex function chasing (CFC) [FL93], and its generalizations including metrical task systems (MTS) [BLS92]. In SOCO, a learner is faced with a sequence of cost functions that are revealed online, and must choose an action after observing . Based on that decision, the learner incurs a hitting cost, as well as a switching cost, , which captures the cost associated with changing the decision between rounds. In contrast to SOCO, OPR includes the long-term constraint of satisfying the demand of units over the horizon , which poses a significant challenge not present in SOCO-like problems.

The coexistence of these differentiating factors, namely the switching cost and the long-term deadline constraint, make OPR uniquely challenging, and means that prior algorithms and analyses for related problems such as -search and SOCO cannot be directly adapted.

Contributions. We introduce online algorithms for the minimization and maximization variants of OPR and show that our algorithms achieve the best possible competitive ratios. We also evaluate the empirical performance of the proposed algorithms on a case study of carbon-aware load shifting. The details of our contributions are outlined below.

Algorithmic idea: Double-threshold

To tackle OPR, we focus our efforts on online threshold-based algorithms (OTA), the prominent design paradigm for classic problems such as -search [LPS08, LSLH22], one-way trading [EYFKT01, SLH+21], and online knapsack problems [ZCL08, SYH+22, YZH+21]. In the -min search problem, for example, a threshold-based algorithm specifies threshold values and chooses to trade the -th item only if the current price is less than or equal to the value suggested by the -th threshold value.

Direct application of prior OTA algorithms to OPR results in undesirable behavior (such as frequently changing decisions) since their threshold function design is oblivious to the switching cost present in OPR. To address this challenge, we seek an algorithm that can simultaneously achieve the following behaviors: (1) when the player is in “trading mode,” they should not impulsively switch away from trading in response to a price that is only slightly worse, since this will result in a switching penalty; and (2) the player should not switch to “trading mode” unless prices are sufficiently good to warrant the switching cost. These two ideas motivate an algorithm design that uses two distinct threshold functions, each of which captures one of the above two cases. We present our algorithms DTPR-min and DTPR-max for OPR-min and OPR-max, respectively, in Section 3, which build upon this high-level idea of a double-threshold.

Main results

While OTA algorithms are intuitive and simple to describe, it is highly challenging to design threshold functions that lead the corresponding algorithms to be competitive against the offline optimum. The addition of switching cost in OPR further exacerbates the technical challenge of designing optimal threshold functions. The key result which enables our double-threshold approach is a technical observation (see Observation 3), which shows that the difference between the functions guiding the algorithm’s decisions should be a factor of , where represents the fixed switching cost incurred by changing the decision in OPR.

Identifying this relationship between the two threshold functions significantly facilitates the competitive analysis of both DTPR-min and DTPR-max, enabling our derivation of a closed form of each threshold. Using this idea, we characterize the competitive ratios of DTPR-min and DTPR-max as a function of problem parameters, including an explicit dependence on the magnitude of the switching cost (see Theorems 4 and 5). Furthermore, we derive lower bounds for the competitive ratio of any deterministic online algorithm, showing that our proposed algorithms are optimal for this problem (formal statements in Theorems 8 and 9). The competitive ratios we derive for both DTPR-min and DTPR-max exactly recover the best prior competitive results for the -search problem [LPS08], which corresponds to the case of in OPR, i.e., no switching cost. Formal statements and a more detailed discussion of our main results are presented in Section 4.

Case study.

Finally, in Section 6, we illustrate the performance of our proposed algorithm by conducting an experimental case study simulating the carbon-aware load shifting problem. We utilize real-world carbon traces from Electricity Maps [Map20], which contain carbon intensity values for grid-sourced electricity across the world. Our experiments simulate different strategies for scheduling a deferrable and interruptible workload in the face of uncertain future carbon intensity values. We show that our algorithm’s performance significantly improves upon existing baseline methods and adapted forms of algorithms for related problems such as -min search.

2 Problem Formulation and Preliminaries

We begin by formally introducing the OPR problem and providing background on the online threshold-based algorithm design paradigm, which is used in the design of our proposed algorithms. Table 1 summarizes the core notations for OPR. Recall that this formulation is motivated by the setting of carbon-aware temporal workload shifting, as described in the introduction.

2.1 Problem Formulation

There are two variants of the online pause and resume problem (OPR).111We use OPR whenever the context is applicable to both minimization (OPR-min) and maximization (OPR-max) variants of the problem, otherwise, we refer to the specific variant. The same policy applies to DTPR, our proposed algorithm for OPR. In OPR-min (OPR-max) a player must buy (sell) units of some asset (one unit at each time step) with the goal of minimizing (maximizing) their total cost (profit) within a time horizon of length . At each time step , the player is presented with a price , and must immediately decide whether to accept this price () or reject it (). The player is required to complete this transaction for all units by some point in time . Both and are known in advance. Thus, the requirement of transactions is a hard constraint, i.e., , and if at time the player still has units remaining to buy/sell, they must accept the prices in the subsequent slots to accomplish transactions.

Additionally, in both variants of OPR, the player incurs a fixed switching cost whenever they decide to change decisions between two adjacent time steps (i.e., when ). We assume that and , implying that any player must incur a minimum switching cost of , once for switching “on” and once for switching “off”. While the player incurs at least a switching cost of , note that the total switching cost incurred by the player is bounded by the size of the asset since the switching cost cannot be larger than .

In summary, the offline version of OPR-min can be summarized as follows:

| (1) |

while the offline version of OPR-max is

| (2) |

| Notation | Description |

|---|---|

| Number of units which must be bought (or sold) | |

| Deadline constraint; the player must buy (or sell) units before time | |

| Current time step | |

| Decision at time . if price is accepted, if is not accepted | |

| Switching cost incurred when algorithm’s decision | |

| Upper bound on any price that will be encountered | |

| Lower bound on any price that will be encountered | |

| Price fluctuation ratio | |

| (Online input) Price revealed to the player at time | |

| (Online input) The actual minimum and maximum prices in a sequence |

Of course, our focus is the online version of OPR, where the player must make irrevocable decisions at each time step without the knowledge of future inputs. More specifically, in both variants of OPR the sequence of prices is revealed sequentially – future prices are unknown to an online algorithm, and each decision is irrevocable.

Competitive analysis

Our goal is to design an online algorithm that maintains a small competitive ratio [BLS92], i.e., performs nearly as well as the offline optimal solution. For an online algorithm ALG and an offline optimal solution OPT, the competitive ratio for a minimization problem is defined as: where denotes a valid input sequence for the problem and is the set of all feasible input instances. Further, is the optimal cost given this input, and is the cost of the solution obtained by running the online algorithm over this input. Conversely, for a problem with a maximization objective, the competitive ratio is defined as . With these definitions, the competitive ratio for both minimization and maximization problems is always greater than or equal to one, and the lower the better.

Assumptions and additional notations.

We make no assumptions on the underlying distribution of the prices other than the assumption that the set of prices arriving online has bounded support, i.e., , where and are known to the player. We also define as the price fluctuation. These are standard assumptions in the literature for many online problems, including one-way trading, online search, and online knapsack; and without them the competitive ratio of any algorithm is unbounded. We use and to denote the minimum and maximum encountered prices for any valid OPR sequence .

2.2 Background: Online Threshold-Based Algorithms (OTA)

Online threshold-based algorithms (OTA) are a family of algorithms for online optimization in which a carefully designed threshold function is used to specify the decisions made at each time step. At a high level, the threshold function defines the “minimum acceptable quality” that an arriving input/price must satisfy in order to be accepted by the algorithm. The threshold is chosen specifically so that an agent greedily accepting prices meeting the threshold at each step will be ensured a competitive guarantee. This algorithmic framework has seen success in the online search and one-way trading problems [LSLH22, SLH+21, LPS08, EYFKT01] as well as the related online knapsack problem [ZCL08, SYH+22, YZH+21]. In these works, the derived threshold functions are optimal in the sense that the competitive ratios of the resulting threshold-based algorithms match information-theoretic lower bounds of the corresponding online problems. As discussed in the introduction, the framework does not apply directly to the OPR setting, but we make use of ideas and techniques from this literature. We briefly detail the most relevant highlights from the prior results before discussing how these related problems generalize to OPR in the next section.

1-min/1-max search.

In the online 1-min/1-max search problem, a player attempts to find the single lowest (respectively, highest) price in a sequence, which is revealed sequentially. The player’s objective is to either minimize their cost or maximize their profit. When each price arrives, the player must decide immediately whether to accept the price, and the player is forced to accept exactly one price before the end of the sequence. For this problem, El-Yaniv et al. [EYFKT01] presents a deterministic threshold-based algorithm. The algorithm assumes a finite price interval, i.e., the price is bounded by the interval , where and are known. Then, it sets a constant threshold , and the algorithm simply selects the first price that is less than or equal to (for the maximization version, it accepts the first price greater than or equal to ). This algorithm achieves a competitive ratio of , which matches the lower bound; hence, it is optimal [EYFKT01].

-min/-max search.

The online -min/-max search problem extends the 1-min/1-max search problem – a player attempts to find the lowest (conversely, highest) prices in a sequence of prices revealed sequentially. The player’s objective is identical to the 1-min/1-max problem, and the player must accept at least prices by the end of the sequence. Several works have developed a known optimal deterministic threshold-based algorithm for this problem, including [LPS08, EYFKT01]. Leveraging the same assumption of a finite price interval , the threshold function is a sequence of thresholds , which is also called the reservation price policy. At each step, the algorithm accepts the first price, which is less than or equal to , where is the number of prices that have been accepted thus far (for the maximization version, it accepts the first price which is ). In the -min setting, this algorithm is -competitive, where is the unique solution of

| (3) |

For the -max variant, this algorithm is -competitive, where is the unique solution of

| (4) |

The sequence of thresholds for both variants of the problem are constructed by analyzing possible input cases, “hedging” against the risk that future (unknown) prices will jump to the worst possible value, i.e., for -min search, for -max search. These potential cases can be enumerated for different values of , where denotes the number of prices accepted so far. By simultaneously balancing the competitive ratios for each of these cases (setting each ratio equal to the others), the optimal threshold values and the optimal competitive ratios are derived. We refer to this technique as the balancing rule and a rigorous proof of this approach, with corresponding lower bounds, can be found in [LPS08]. The lower bounds highlight that the and which solve the expressions for the competitive ratios above are optimal for any deterministic -min and -max search algorithms, respectively. Further, and provide insight into a fundamental difference between the minimization and maximization settings of -search. As discussed in [LPS08], for large , the best algorithm for -max search is roughly -competitive, while the best algorithm for -min search is at best -competitive. Similarly, for fixed and large , the optimal competitive ratio for -max search is roughly , while the optimal competitive ratio for -min search converges to .

3 Double Threshold Pause and Resume (DTPR) Algorithm

A fundamental challenge in algorithm design for OPR is how to characterize threshold functions that incorporate the presence of switching costs in their design. Our key algorithmic insight is to incorporate the switching cost into the threshold function by defining two distinct threshold functions, where the function to be used for price admittance changes based on the current state (i.e., whether or not the previous price was accepted by the algorithm).

To provide intuition for the state-dependence of the threshold function, consider the setting of OPR-min. At a high level, if the player has not accepted the previous price, they should wait to accept anything until prices are sufficiently low to justify incurring a cost to switch decisions. On the other hand, if the player has accepted the previous price, they might be willing to accept a slightly higher price – if they do not accept this price, they will incur a cost to switch decisions. While this high-level idea is intuitive, characterizing the form of threshold functions such that the resulting algorithms are competitive is challenging.

The DTPR-min algorithm

Our proposed algorithm, Double Threshold Pause and Resume (DTPR) for OPR-min is summarized in Algorithm 1. Prior to any prices arriving online, DTPR-min computes two families of threshold values, and , where , whose values are defined as follows.

Definition 1 (DTPR-min Threshold Values).

For each integer on the interval , the following expressions give the corresponding threshold values of and for DTPR-min.

| (5) |

where is the competitive ratio of DTPR-min defined in Equation (9).

The role of these thresholds is to incorporate the switching cost into the algorithm’s decisions, and to alter the acceptance criteria of DTPR-min based on the current state. For OPR-min, the current state is whether the previous item was accepted, i.e., whether is or . As prices are sequentially revealed to the algorithm at each time , the th price accepted by DTPR-min will be the first price which is at most if , or at most if . Note that, as indicated in Line 6, DTPR-min may be forced to accept the last prices of the sequence, which can be “worse” than the current threshold values, to satisfy the deadline constraint of OPR.

The DTPR-max algorithm

Pseudocode is summarized in the appendix, in Algorithm 2. The logical flow of DTPR-max shares a similar structure to that of DTPR-min, with a few important differences highlighted here. For OPR-max, the th price accepted by DTPR-max will be the first price which is at least if , or at least if . Further, the threshold functions are defined as follows.

Definition 2 (DTPR-max Threshold Values).

For each integer on the interval , the following expressions give the corresponding threshold values of and for DTPR-max.

| (6) |

where is the competitive ratio of DTPR-max defined in Equation (10).

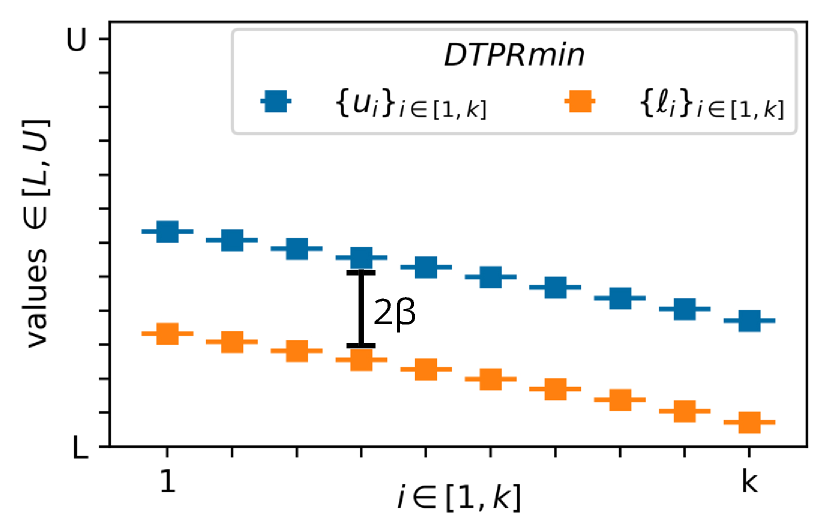

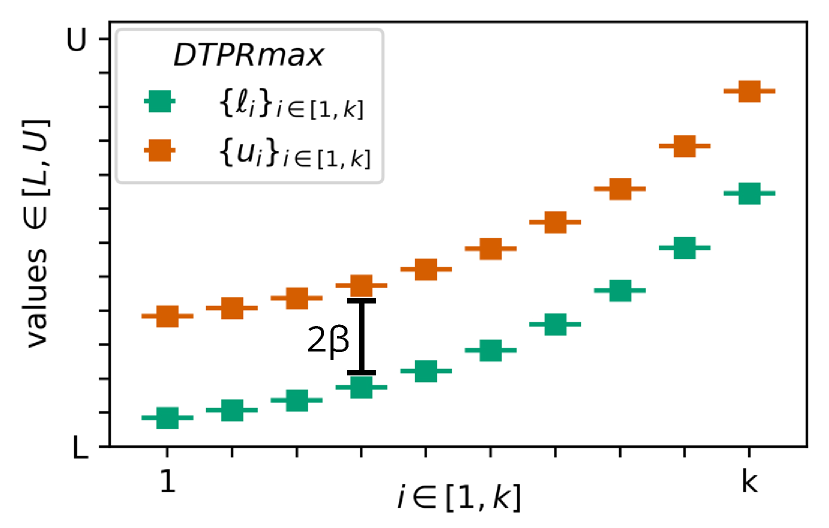

In Figures 2 and 2, we plot threshold values for DTPR-min and DTPR-max, respectively, using example parameters of and . We annotate the difference of between and ; recall that each of these thresholds corresponds to a current state for DTPR, i.e. whether the previous item was accepted. Note that the DTPR-min threshold values decrease as gets larger, while the DTPR-max threshold values increase as gets larger. At a high-level, each th threshold “hedges” against a scenario where none of the future prices meet the current threshold. In this case, even if the algorithm is forced to accept the worst possible prices at the end of the sequence, we want competitive guarantees against an offline OPT. Such guarantees rely on the fact that in the worst-case, OPT cannot accept prices that are all significantly better than DTPR’s th “unseen” threshold value because such prices did not exist in the sequence.

Designing the Double Threshold Values

A key component of the DTPR algorithms for both variants are the thresholds in Equations (5) and (6). The key idea is to design the thresholds by incorporating the switching cost into the balancing rules as a hedge against possible worst-case scenarios. To accomplish this, we enumerate three difficult cases that DTPR may encounter. (CASE-1): Consider an input sequence where DTPR does not accept any prices before it is forced to accept the last prices. Here, the enforced prices in the worst-case sequence will be for OPR-min and for OPR-max. This sequence occurs only if no price in the sequence meets the first threshold for acceptance. On the other hand, in the case that DTPR does accept prices before the end of the sequence, we can further divide the possible sequences into two extreme cases for the switching cost it incurs. (CASE-2): In one extreme, the algorithm incurs only the minimum switching cost of , meaning that contiguous prices are accepted by DTPR. (CASE-3): In the other extreme, DTPR incurs the maximum switching cost of , meaning that non-contiguous prices are accepted. Intuitively, in order for DTPR to be competitive in either of these extreme cases, the prices accepted in the latter case should be sufficiently “good” to absorb the extra switching cost of .

Given the insight from these cases, we use can use the balancing rule (see Section 2.2) to derive the two threshold families. Let be any arbitrary sequence for OPR. Given these extreme input sequences, we now concretely show how to write the balancing rule equations. We consider the cases of DTPR-min and DTPR-max separately below.

Balancing equations for DTPR-min

To balance between possible inputs for OPR-min, consider the following examples for three different values of . If , we know that OPT cannot do better than . Suppose that is the target competitive ratio, and we balance between these and other potential cases:

| (7) | |||

As an example, consider and the corresponding cases enumerated above. Suppose DTPR-min accepts one price before the end of the sequence , and the other prices accepted are all . In the first case, where the competitive ratio is , we consider the scenario where DTPR-min switches twice: once to accept the price , and once to accept prices at the end of the sequence, incurring switching cost of .

In the second case, where the competitive ratio is , we consider the hypothetical scenario where DTPR-min only switches once to accept some value followed by prices at the end of the sequence, incurring switching cost of . By enumerating cases in this fashion for the other possible values of , we derive a relationship between the lower thresholds and the upper thresholds in terms of the switching cost.

Balancing equations for DTPR-max

The same idea extends to balance between possible inputs for OPR-max. Consider the following examples for a few values of . If , we know that OPT cannot do better than . Suppose that is the target competitive ratio, and we balance between these and other potential cases:

| (8) | |||

Solving for the threshold values

Given the above balancing equations for both the minimization and maximization variants, the next step is to solve for the unknown values of and . The following observation summarizes the key insight that enables this. We show that one can express each in terms of and , which facilitates the analysis required to solve for thresholds in each balancing equation (given by Equations (7) and (8)).

Observation 3.

By letting , we obtain each possible worst-case permutation of thresholds, thresholds, and switching cost. Let denote the number of switches incurred by DTPR.

For DTPR-min, suppose that . By the definition of DTPR-min, we know that accepting any helps avoid a switching cost of in the worst case. Thus,

For DTPR-max, suppose that . By the definition of DTPR-max, we know that accepting any helps avoid a switching cost of in the worst case. Thus,

With the above observation, for DTPR-min, one can substitute for each . By comparing adjacent terms in Equation (7), standard algebraic manipulations give a closed form for each in terms of . Setting , we obtain the explicit expression for , yielding a closed formula for and in Equation (5). Considering the balancing rule in Equation (7) for the case where , it follows that , and thus . By substituting this value into Definition 1, we obtain an explicit expression for as shown in Equation (9).

Conversely, for DTPR-max, we substitute for each . By comparing adjacent terms in Equation (8), standard methods give a closed form for each in terms of . Setting , we obtain the explicit expression for , yielding the closed formula for and in Equation (6). Considering the balancing rule in Equation (8) for the case where , it follows that , and thus . By substituting this value into Definition 2, we obtain an explicit expression for as shown in Equation (10).

4 Main Results

We now present competitive results of DTPR for both variants of OPR and discuss the significance of the results in relation to other algorithms for related problems. Our results for the competitive ratios of DTPR-min and DTPR-max are summarized in Theorems 4 and 5. We also state the lower bound results for any deterministic online algorithms for OPR-min and OPR-max in Theorems 8 and 9. Proofs of the results for DTPR-min and DTPR-max are deferred to Section 5 and Appendix B, respectively. Formal proofs of lower bound theorems are given in Appendix D, and a sketch is shown in Section 5.2. Note that in the competitive results, denotes the Lambert function, i.e., the inverse of . It is well-known that behaves like [HH08, Ste09]. We start by presenting our competitive bounds on DTPR-min and DTPR-max.

Theorem 4.

DTPR-min is an -competitive deterministic algorithm for OPR-min, where is the unique positive solution of

| (9) |

Theorem 5.

DTPR-max is an -competitive deterministic algorithm for OPR-max, where is the unique positive solution of

| (10) |

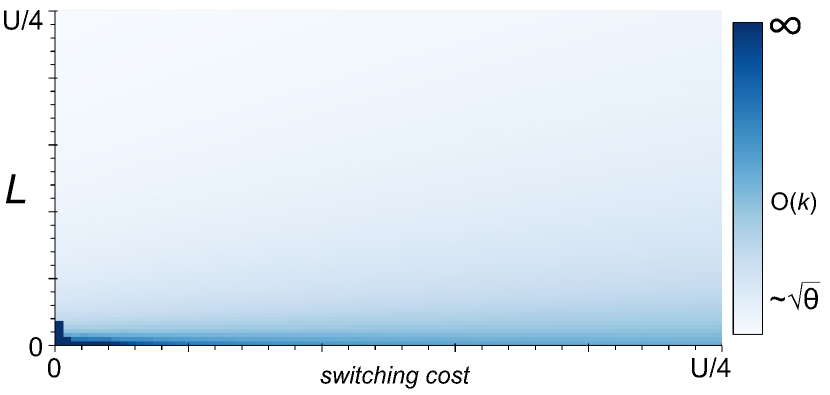

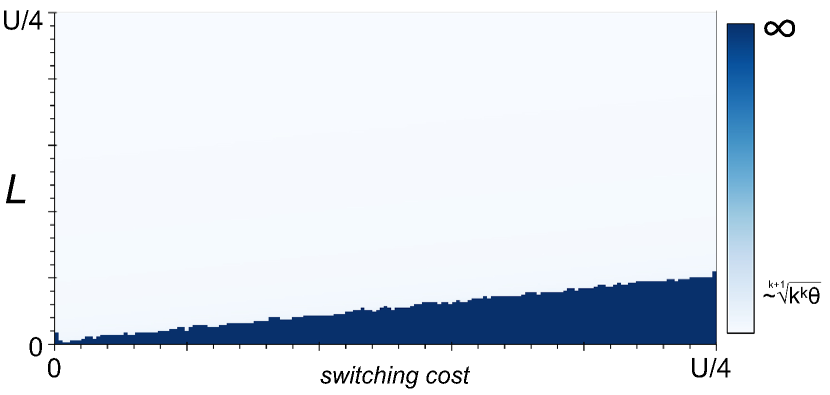

These theorems present upper bounds on the competitive ratios, showing their dependence on the problem parameters. To investigate the behavior of these competitive ratios, in Figures 4 and 4, we show the competitive ratios of both algorithms as problem parameters are varied. More specifically, in Figure 4, we visualize as a function of and , where and are fixed. The color (shown as an annotated color bar on the right-hand side of the plot) represents the order of . If and , Figure 4 shows that is roughly , which we discuss further in Corollary 6(a). In Figure 4, we visualize as a function of and , where and are fixed. The color represents the order of . In the dark blue region of the plot, Figure 4 shows that when , which provides insight into the extreme case for switching cost when .

To obtain additional insight into the form of the competitive ratios in Theorems 4 and 5, we present the following corollaries for two asymptotic regimes of interest: REGIME-1 captures the order of the competitive ratio when is fixed and or are sufficiently large, and REGIME-2 captures the order of the competitive ratio when .

Corollary 6.

(a) For REGIME-1, with fixed and , the competitive ratio of DTPR-min is

(b) Furthermore, for REGIME-2, with and , the competitive ratio of DTPR-min is

Corollary 7.

(a) For REGIME-1, with fixed and , the competitive ratio of DTPR-max is

and (b) for REGIME-2, with and , the competitive ratio of DTPR-max is

Corollary 6(a) contextualizes the behavior of (the competitive ratio of DTPR-min) in the most relevant OPR-min setting (when ). Let us also briefly discuss the other cases for the switching cost , and why this interval makes sense. When , the switching cost is large enough such that OPT only incurs a switching cost of . In this regime, does not fully capture the competitive ratio of DTPR-min, since every value in the threshold family is at least ; in other words, whenever the algorithm begins accepting prices, it will accept prices in a single continuous segment, incurring minimal switching cost of . As , the competitive ratio of DTPR-min approaches .

Conversely, Corollary 7(a) contextualizes the behavior of in the most relevant OPR-max setting (when ), but we also discuss the other cases for the switching cost , and why this interval makes sense. When , the switching cost is too large, and the competitive ratio may become unbounded. Note that this is shown explicitly in Figure 4. Consider an adversarial sequence which forces any OPR-max algorithm to accept prices with value at the end of the sequence. On such a sequence, even a player which incurs the minimum switching cost of achieves zero or negative profit of , and this is not well-defined.

Next, to begin to investigate the tightness of Theorems 4 and 5, it is interesting to consider special cases that correspond to models studied in previous work. In particular, when , i.e., there is no switching cost, OPR degenerates to the -search problem [LPS08]. For fixed and , the optimal competitive ratios shown by [LPS08] are for -min, and for -max (see Section 2.2). Both versions of DTPR exactly recover the optimal -search algorithms [LPS08].222To see this, note that by eliminating all terms from Equations (9) and (10), we exactly recover Equations (3) and (4), which are the definitions of the -search algorithms. When as , DTPR-min and DTPR-max match each -search result exactly when . In Corollaries 6(b) and 7(b), DTPR-min and DTPR-max also match each search result exactly when and . (See Sec. 2.2) Figure 4 shows that if and , then , which matches the -min result of . Similarly, Figure 4 shows that if and , then , which matches the -max result of .

More generally, one can ask if the competitive ratios of DTPR can be improved upon by other online algorithms outside of the special case of -search. Our next set of results highlights that no improvement is possible, i.e., that DTPR-min and DTPR-max maintain the optimal competitive ratios possible for any deterministic online algorithm for OPR.

Theorem 8.

Let , , and . Then given by Equation (9) is the best competitive ratio that a deterministic online algorithm for OPR-min can achieve.

Theorem 9.

Let , , and . Then given by Equation (10) is the best competitive ratio that a deterministic online algorithm for OPR-max can achieve.

By combining Theorems 4 and 5 with Theorems 8 and 9, these results imply that the competitive ratios of DTPR-min and DTPR-max are optimal for OPR-min and OPR-max.

Finally, it is interesting to contrast the upper and lower bounds for OPR with those for -search, since the contrast highlights the impact of switching costs. In OPR-min with , DTPR-min improves on existing optimal results for -min search, particularly in the case where approaches (i.e., ). Since Theorem 8 implies that DTPR-min is optimal, this shows that the addition of switching cost in OPR-min enables an online algorithm to achieve a better competitive ratio compared to -min search, which is a surprising result. In contrast, for OPR-max with , DTPR-max’s competitive bounds are worse than existing results for -max search, particularly for large . Since Theorem 9 implies that DTPR-max is optimal, this suggests that OPR-max is fundamentally a more difficult problem compared to -max search.

5 Proofs

We now prove the results described in the previous section. In Section 5.1, we prove the DTPR-min results presented in Theorem 4 and Corollary 6. In Section 5.2, we provide a proof sketch for the lower bound results in Theorems 8 and 9, and defer the formal proofs to Appendix D. The competitive results for DTPR-max in Theorem 5 and Corollary 7 are deferred to Appendix B.

5.1 Competitive Results for DTPR-min

We begin by proving Theorem 4 and Corollary 6. The key novelty in the proof of the main competitive results (Theorems 4 and 5) lies in our effort to derive two threshold functions and balance the competitive ratio in several worst-case instances with respect to these thresholds, as outlined in Section 3.

Proof of Theorem 4.

For , let be the sets of OPR-min price sequences for which DTPR-min accepts exactly prices (excluding the prices it is forced to accept at the end of the sequence). Then, all of the possible price sequences for OPR-min are represented by . Also, recall that by definition, . Let be a fixed constant, and define the following two price sequences and :

There are two special cases for and . For , we have that , and this sequence simply consists of repeated times, followed by repeated times. For , we also have that , and this sequence consists of one price with value and one price with value , followed by repeated times and repeated times.

Observe that as , and are sequences yielding the worst-case ratios in , as DTPR-min is forced to accept worst-case values at the end of the sequence, and each accepted value is exactly equal to the corresponding threshold.

Note that and also represent two extreme possibilities for the additive switching cost. In , DTPR-min only switches twice, but it mostly accepts values . In , DTPR-min must switch times because there are many intermediate values, but it only accepts values .

In the worst case, we have

Also, the optimal solutions for both sequences are lower bounded by the same quantity: .

For any sequence in , we have that , so .

By definition of the threshold families and , we know that for any value :

Note that whenever , we have that , and . Thus, holds for any value of .

By definition of , we simplify to

. Then, for any sequence , we have the following:

| (11) |

Before proceeding to the next step, we use an intermediate result stated in the following lemma with a proof given in Appendix C.

Lemma 10.

For any , by definition of and ,

For , the competitive ratio is exactly :

and thus for any sequence ,

Since for any sequence , this implies that DTPR-min is -competitive. ∎

Proof of Corollary 6.

To show part (a) for REGIME-1, with fixed , observe that we can expand the right-hand side of Equation (9) using the binomial theorem to obtain the following:

Next, observe that solving the following expression satisfies , (i.e. is an upper bound of ):

By solving the above for , we obtain

Last, note that as , we obtain the following result: .

To show part (b) for REGIME-2, we first observe that the right-hand side of Equation 9 can be approximated as when . Then by taking limits on both sides, we obtain the following:

For simplification purposes, let , where is a small constant on the interval .

We then obtain the following:

By definition of Lambert function, solving this equation for obtains the result in Corollary 6(b). ∎

5.2 Lower Bound Analysis: Proof Sketch for Theorems 8 and 9

Here we present a proof sketch for the lower bound construction that is used to prove both Theorems 8 and 9. We show how to formalize it in the case of Theorem 8 in Appendix D.1, and in the case of Theorem 9 in Appendix D.2.

Suppose that ALG is a deterministic online algorithm for OPR. The lower bound proofs for both OPR-min and OPR-max leverage the same instance, where ALG plays against an adaptive adversary.

To describe the instance, we first need some preliminaries. Define a sequence of prices , which are the prices the adversary will present to ALG. The “worst-case value” that ALG can encounter is defined based on the problem variant. Since we assume that prices are bounded on the interval , these values are for OPR-min, and for OPR-max.

The adversary begins by presenting to ALG, at most times or until ALG accepts it. If ALG never accepts , the adversary presents the worst-case value at least times for the remainder of the sequence. In the formal proof, we show that this case causes ALG to achieve a competitive ratio of at least for OPR-min, or at least for OPR-max.

If ALG does accept , the adversary continues the sequence by presenting the worst-case value to ALG, at most times or until ALG switches to reject it. This essentially forces ALG to switch immediately after accepting . In the formal proof, we show that any algorithm which does not switch away immediately achieves a competitive ratio worse than and for OPR-min and OPR-max.

After ALG has switched away, the adversary continues the sequence by presenting to ALG at most times or until ALG accepts it. Again, if ALG never accepts , the adversary presents the worst-case value at least times for the remainder, and ALG cannot do better than or .

The adversary continues in this fashion, presenting each at most times (or until ALG accepts it and the adversary forces ALG to switch away immediately afterward). Whenever ALG does not accept some after it is presented times, the adversary sends the price to the worst-case value for the remainder of the sequence. If ALG accepts prices before the end of the sequence, the adversary concludes by presenting the best-case value ( for OPR-min, for OPR-max) at least times.

In the formal proofs presented in Appendix D, we show that any deterministic strategy that ALG uses to accept prices on this sequence achieves a competitive ratio of at least for OPR-min, and at least for OPR-max.

6 Case Study: Carbon-Aware Temporal Workload Shifting

We now present experimental results for the DTPR algorithms in the context of the carbon-aware temporal workload shifting problem. We evaluate DTPR-min (and DTPR-max in Appendix A) as compared to existing algorithms from the literature that have been adapted for OPR.

6.1 Experimental Setup

We consider a carbon-aware load shifting system that operates on a hypothetical data center. An algorithm is given a deferrable and interruptible job that takes time slots to complete, along with a deadline , such that the job must be completed at most slots after its arrival. The objective is to selectively run units of the job such that the total carbon emissions are minimized while still completing the job before its deadline.

For the minimization variant (OPR-min) of the experiments, we consider carbon emissions intensities, as the price values. At each time step , the electricity supply has a carbon intensity , i.e., if the job is being processed during the time step (), the data center’s carbon emissions during that time step are proportional to . If the job is not being processed during the time step (), we assume for simplicity that carbon emissions in the idle state are negligible and essentially . To model the combined computational overhead of interrupting, checkpointing, and restarting the job, the algorithm incurs a fixed switching cost of whenever , whose values are selected relative to the price values.

Carbon data traces

We use real-world carbon traces from Electricity Maps [Map20], which provide time-series information about the average carbon emissions intensity of the electric grid. We use traces from three different regions: the Pacific Northwest of the U.S., New Zealand, and Ontario, Canada. The data is provided at an hourly granularity and includes the current average carbon emissions intensity in grams of CO2 equivalent per kilowatt-hour (gCO2eq/kWh), and the percentage of electricity being supplied from carbon-free sources. In Figure 9 (in Appendix A), we plot three representative actual traces for carbon intensity over time for a 96-hour period in each region.

Parameter settings

We test for time horizons () of 48 hours, 72 hours, and 96 hours. The chosen time horizon represents the time at which the job with length must be completed. As is given in the carbon trace data, we consider time slots of one hour.

The online algorithms we use in experiments take and as parameters for their threshold functions. To set these parameters, we examine the entire carbon trace for the current location. For the Pacific NW trace and the Ontario trace, these values represent lower and upper bounds of the carbon intensity values for a full year. For the New Zealand trace, these values are a lower and upper bound for the values during a month of data, which is reflected by a smaller fluctuation ratio. We set and to be the minimum and maximum observed carbon intensity over the entire trace.

| Location | PNW, U.S. | New Zealand | Ontario, Canada |

| Number of Data Points | 10,144 | 1,324 | 17,898 |

| Max. Carbon Intensity () | 648 gCO2eq/kWh | 165 gCO2eq/kWh | 181 gCO2eq/kWh |

| Min. Carbon Intensity () | 18 gCO2eq/kWh | 54 gCO2eq/kWh | 15 gCO2eq/kWh |

| Duration (mm/dd/yy) | 04/20/22 - 12/06/22 | 10/19/21 - 11/16/21 | 10/19/21 - 12/06/22 |

To generate each input sequence, a contiguous segment of size is randomly sampled from the given carbon trace. In a few experiments, we simulate greater volatility over time by “scaling up” each price’s deviation from the mean. First, we compute the average value over the entire sequence. Next, we compute the difference between each price and this average. Each of these differences is scaled by a noise factor of . Finally, new carbon values are computed by summing each scaled difference with the average. If , we recover the same sequence, and if , any deviation from the mean is proportionately amplified. Any values which become negative after applying this transformation are truncated to . This technique allows us to evaluate algorithms under different levels of volatility. Performance in the presence of greater carbon volatility is important, as on-site renewable generation is seeing greater adoption as a supplementary power source for data centers [RKS+22, ALK+23].

Benchmark algorithms

To evaluate the performance of DTPR, we use a dynamic programming approach to calculate the offline optimal solution for each given sequence and objective, which allows us to report the empirical competitive ratio for each tested algorithm. We compare DTPR against two categories of benchmark algorithms, which are summarized in Table 3.

The first category of benchmark algorithms is carbon-agnostic algorithms, which run the jobs during the first time slots in order, i.e., accepting prices . This approach incurs the minimal switching cost of , because it does not interrupt the job while it is being processed. The carbon-agnostic approach simulates the behavior of a scheduler that runs the job to completion as soon as it is submitted, without any focus on reducing carbon emissions. Note that the performance of this approach significantly varies based on the randomly selected sequence, since it will perform well if low-carbon electricity is available in the first few slots, and will perform poorly if the first few slots are high-carbon.

We also compare DTPR against switching-cost-agnostic algorithms, which only consider carbon cost. We have two algorithms of this type, each drawing from existing online search methods in the literature. Although they do not consider the switching cost in their design, they still incur a switching cost whenever their decision in adjacent time slots differs.

The first such algorithm is a constant threshold algorithm, which uses the threshold value first presented for online search in [EYFKT01]. In our minimization experiments, this algorithm runs the workload during the first time slots where the carbon intensity is at most .

The other switching-cost-agnostic algorithm tested is the -search algorithm shown by [LPS08] and described in Section 2.2. The -min search algorithm chooses to run the th hour of the job during the first time slot where the carbon intensity is at most .

| Algorithm | Carbon-aware | Switching-aware | Description |

|---|---|---|---|

| OPT (offline) | YES | YES | Optimal offline solution |

| Carbon-Agnostic | NO | YES | Runs job in the first time slots |

| Const. Threshold | YES | NO | Runs job if carbon meets threshold |

| -search | YES | NO | Runs th slot of job if carbon meets threshold |

| DTPR | YES | YES | This work (algorithms proposed in Section 3) |

6.2 Experimental Results

We now present our experimental results. Our focus is on the empirical competitive ratio (a lower competitive ratio is better). We report the performance of all algorithms for each experimental setting, in each tested region. Throughout the minimization experiments, we observe that DTPR-min outperforms the benchmark algorithms. The 95th percentile worst-case empirical competitive ratio achieved by DTPR-min is a % improvement on the carbon-agnostic method, a % improvement on the -min search algorithm, and a % improvement on the constant threshold algorithm.

(a): Ontario, Canada carbon trace, with (b): U.S. Pacific Northwest carbon trace, with

(c): New Zealand carbon trace, with

(a): Changing job length w.r.t. time horizon (-axis), vs. competitive ratio (b): Changing switching cost w.r.t. (-axis), vs. competitive ratio (c): Different volatility levels w.r.t. (-axis), vs. competitive ratio

(d): Cumulative distribution function of competitive ratios

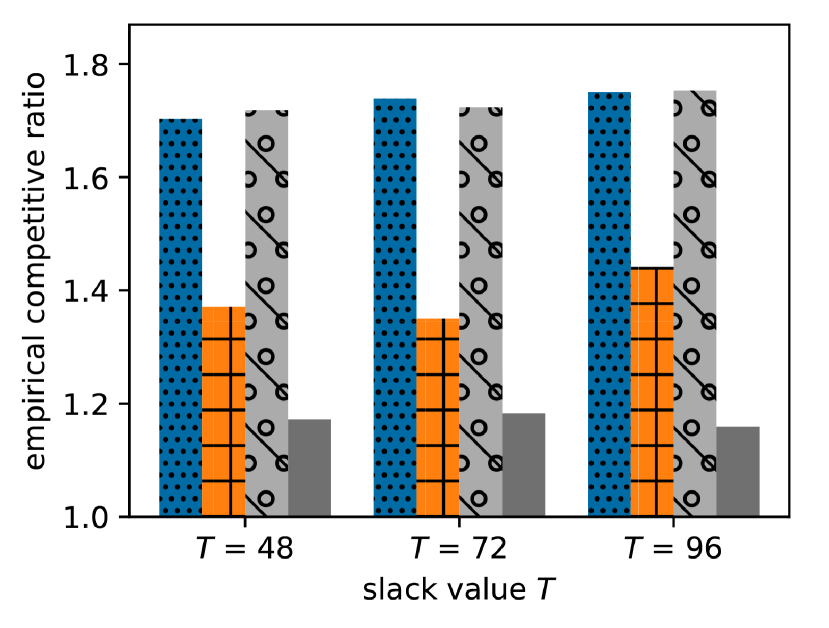

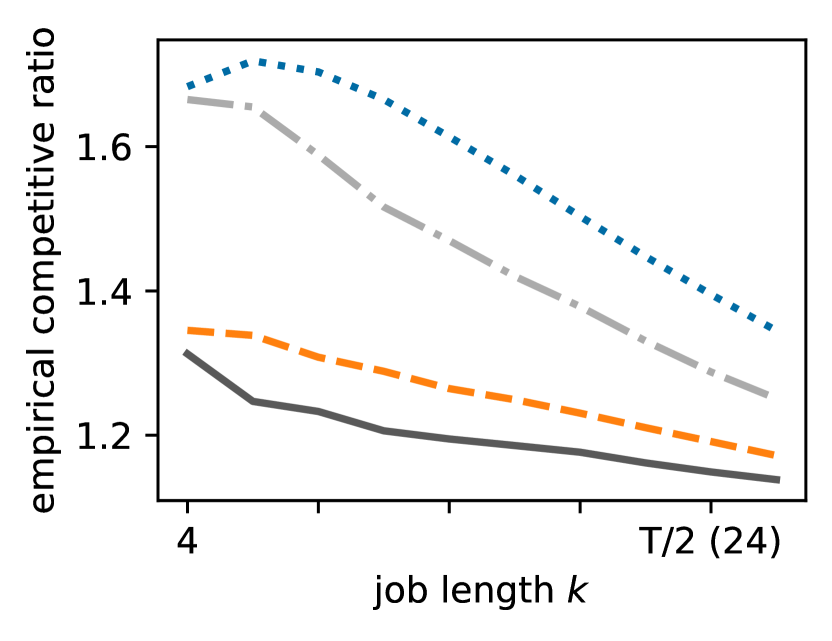

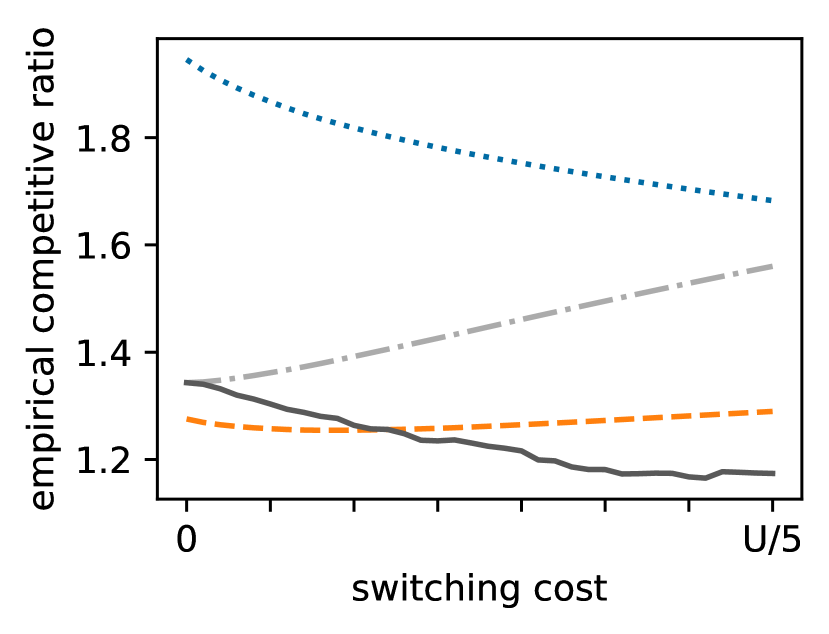

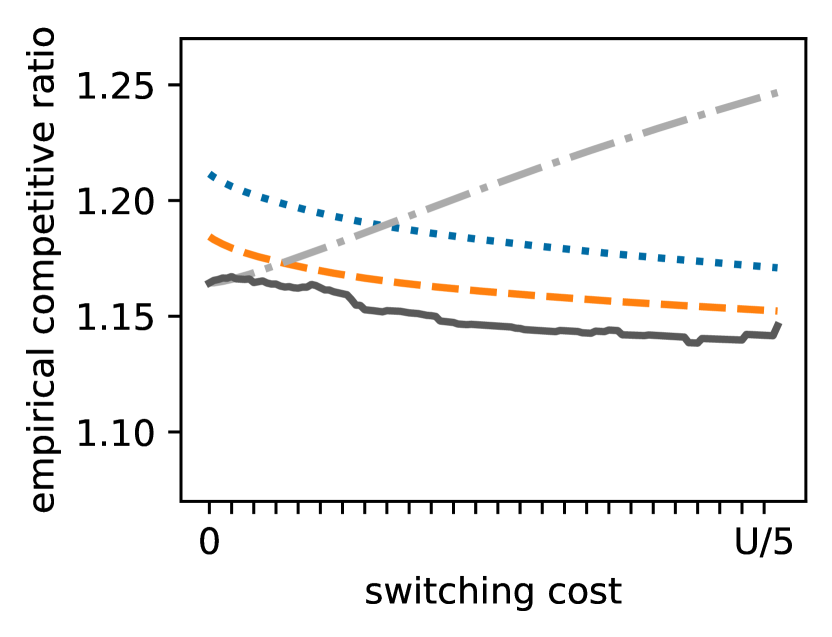

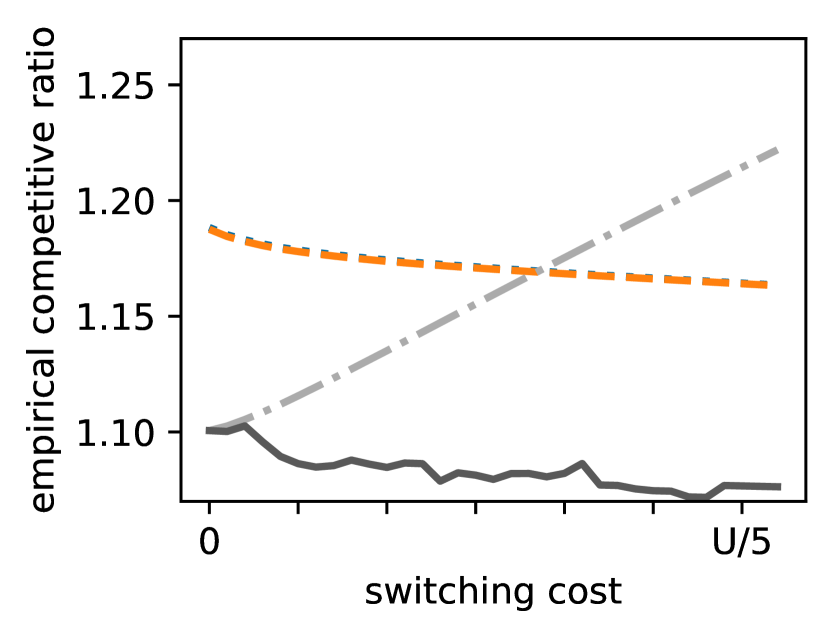

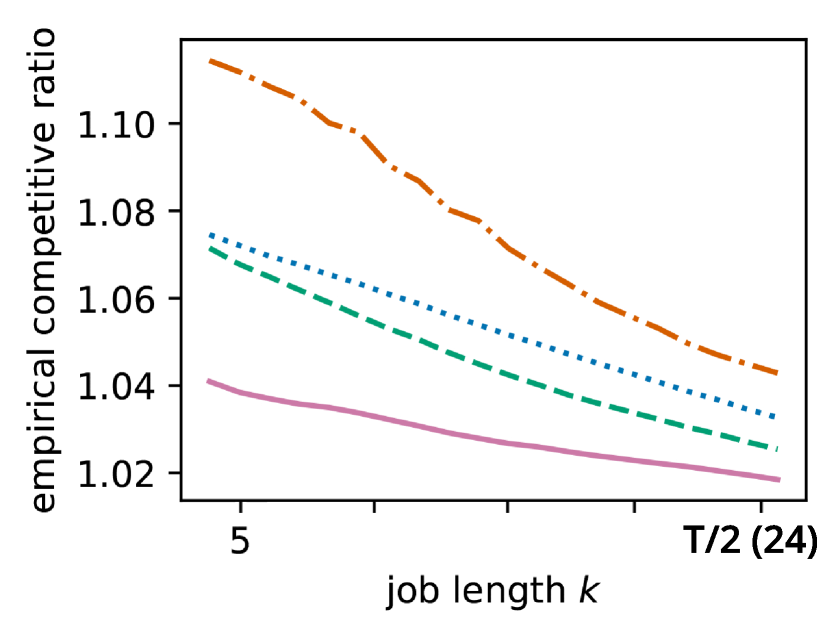

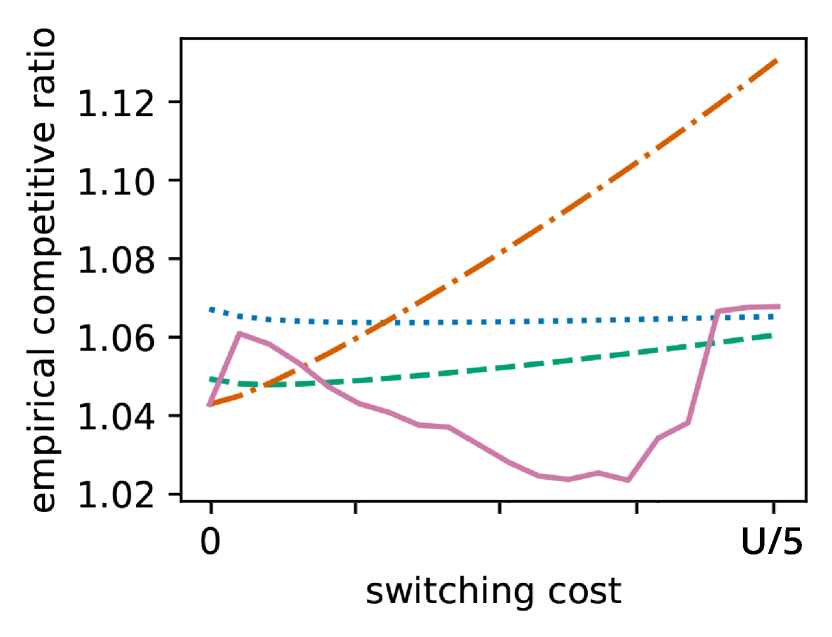

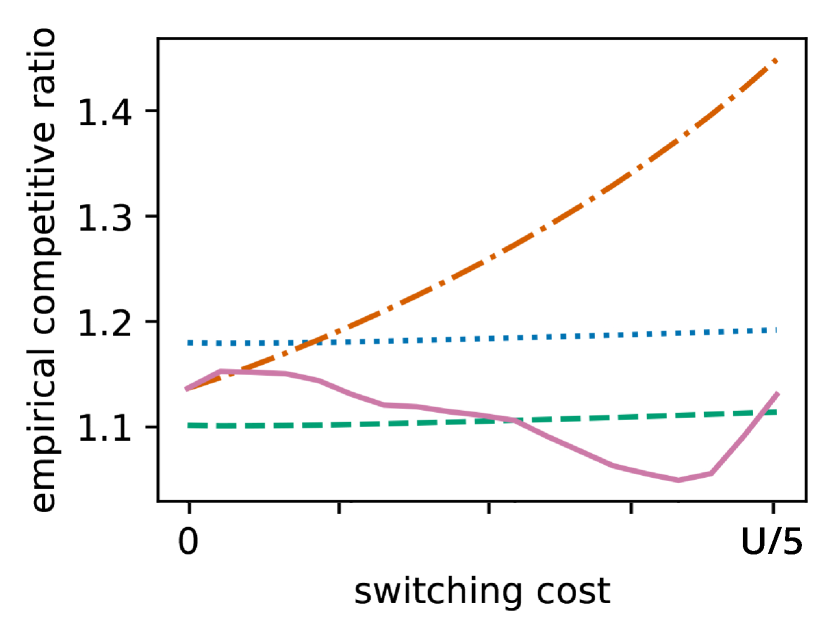

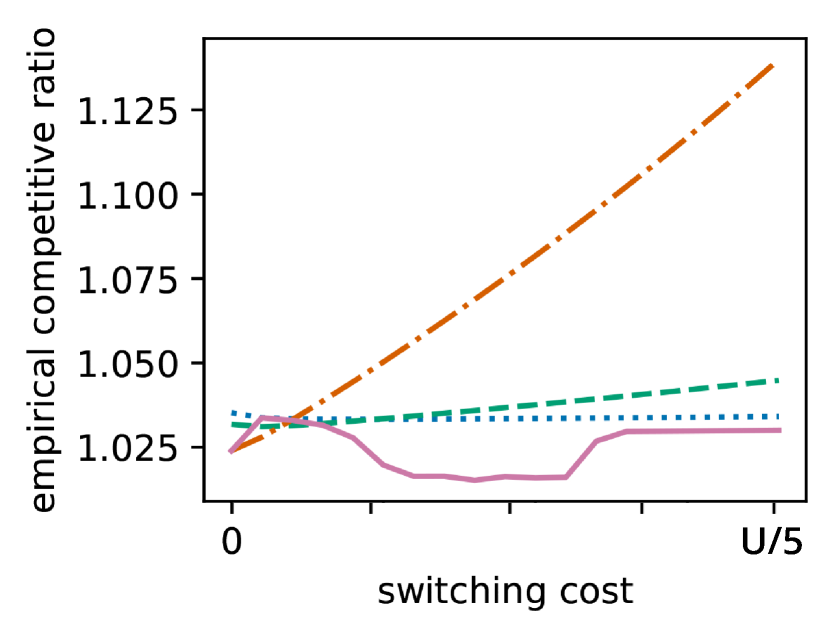

In Figure 5, we show results for three different values of time horizon in each carbon trace, with fixed , fixed , and no added volatility. Although our experiments test three distinct values for , we later observe that the ratio between and is the primary factor which changes the observed performance of the algorithms we test; in this figure, DTPR and the benchmark algorithms compare very similarly on the same carbon trace for different values. As such, we set in the rest of the experiments in this section for brevity. This represents a slack value of hours.

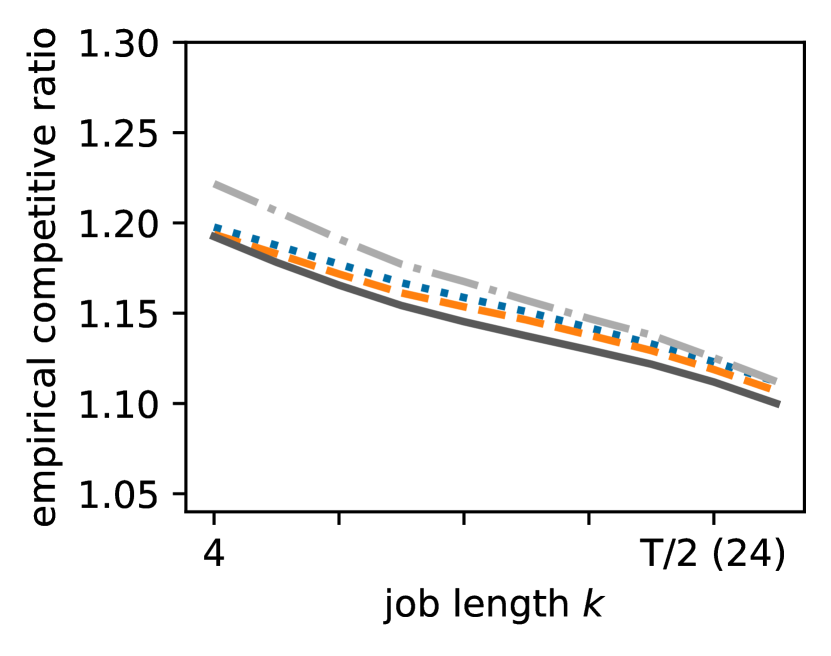

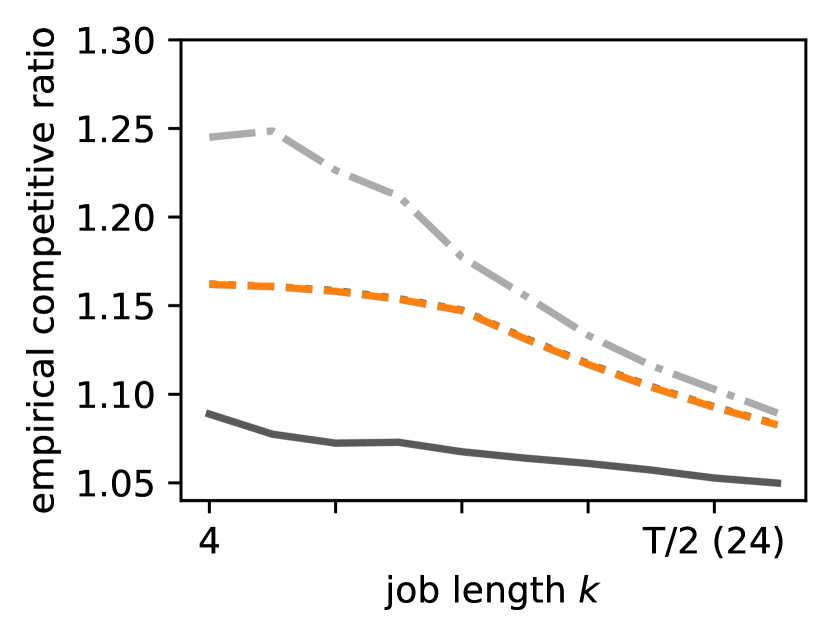

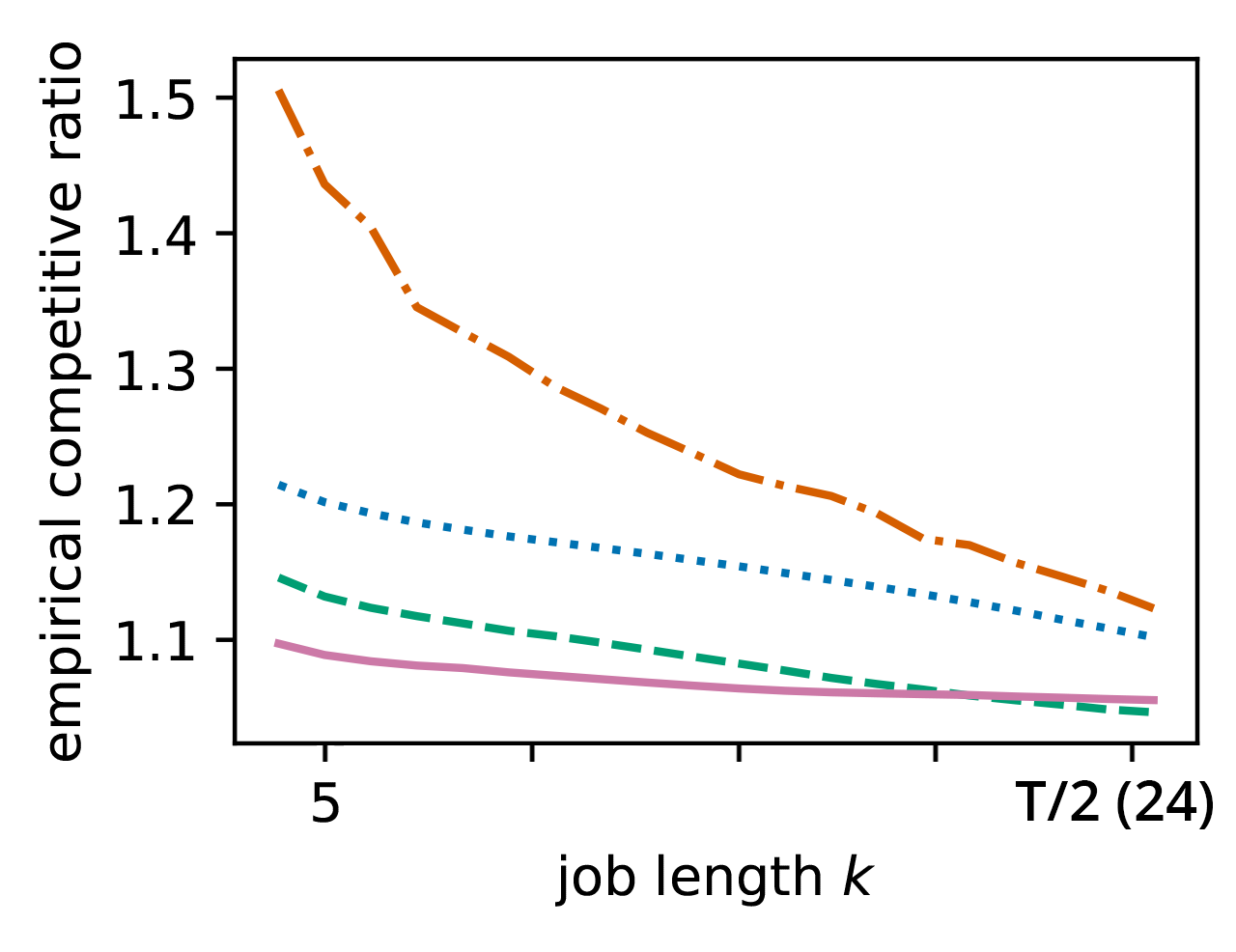

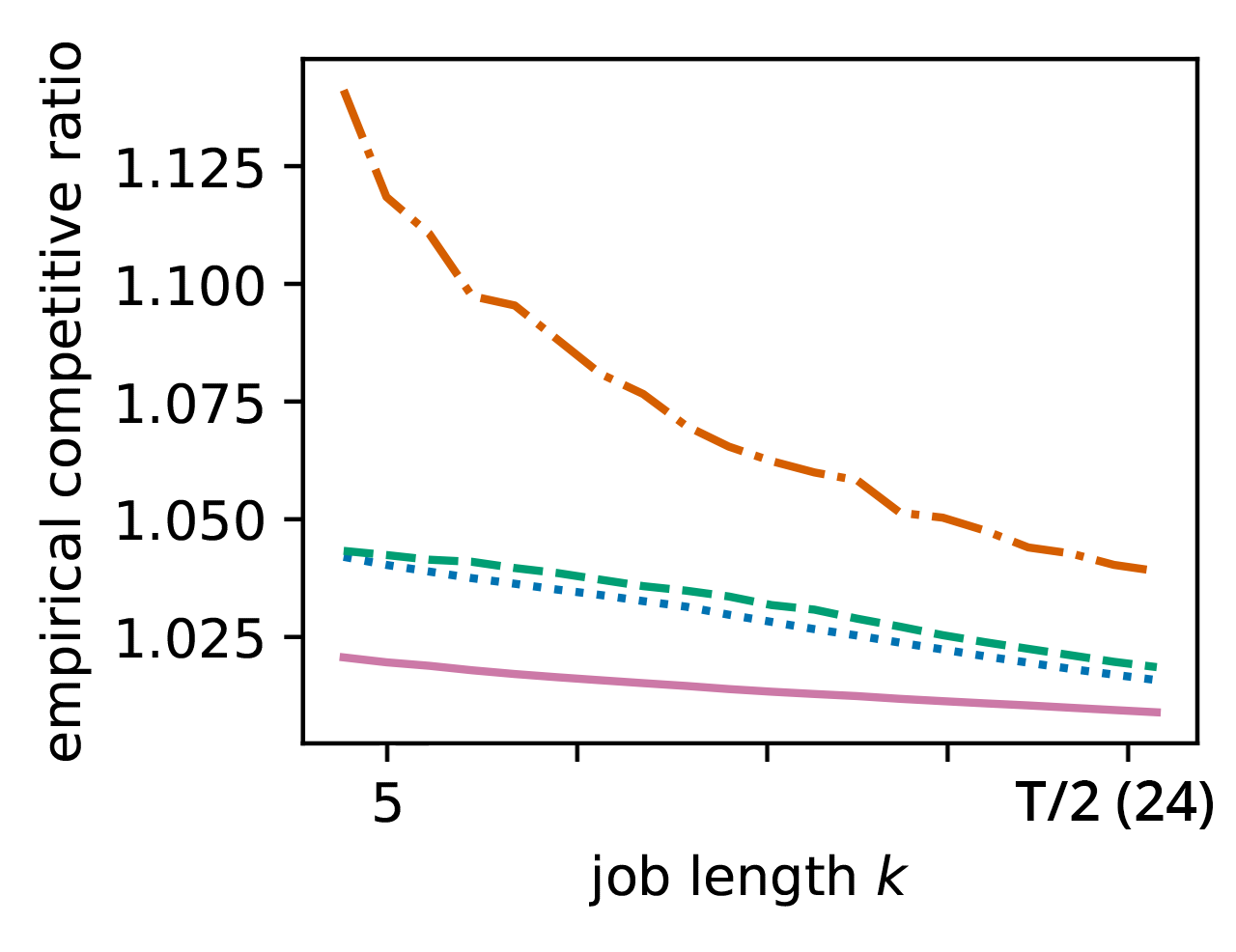

In the first experiment, we test all algorithms for different job lengths in the range from hours to ( hours). The switching cost is non-zero and fixed, and no volatility is added to the carbon trace. By testing different values for , this experiment tests different ratios between the workload length and the slack provided to the algorithm. In Figures 6(a), 7(a), and 8(a), we show that the observed competitive ratio of DTPR-min outperforms the benchmark algorithms, and it compares particularly favorably for short job lengths. Averaging over all regions and job lengths, the competitive ratio achieved by DTPR-min is a % improvement on the carbon-agnostic method, a % improvement on the -min search algorithm, and a % improvement on the constant threshold algorithm.

(a): Changing job length w.r.t. time horizon (-axis), vs. competitive ratio (b): Changing switching cost w.r.t. (-axis), vs. competitive ratio (c): Different volatility levels w.r.t. (-axis), vs. competitive ratio

(d): Cumulative distribution function of competitive ratios

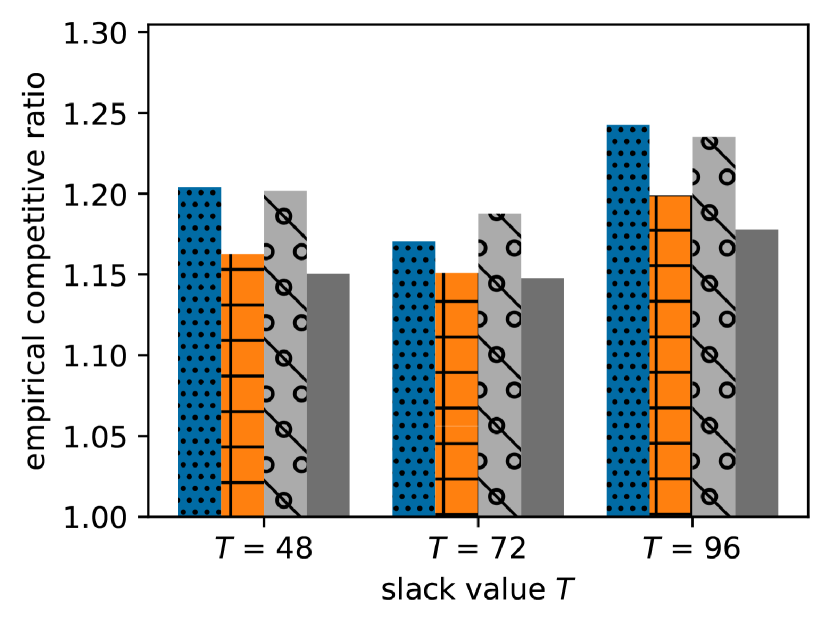

In the second experiment, we test all algorithms for different switching costs in the range from to . The job length is set to hours, and no volatility is added to the carbon trace. By testing different values for , this experiment tests how an increasing switching cost impacts the performance of DTPR-min with respect to other algorithms which do not explicitly consider the switching cost. In Figures 6(b), 7(b), and 8(b), we show that the observed competitive ratio of DTPR-min outperforms the benchmark algorithms for most values of in all regions. Unsurprisingly, the carbon-agnostic technique (which incurs minimal switching cost) performs better as grows. While the constant threshold algorithm has relatively consistent performance, the -min search algorithm performs noticeably worse as grows. Averaging over all regions and switching cost values, the competitive ratio achieved by DTPR-min is a % improvement on the carbon-agnostic method, a % improvement on the -min search algorithm, and a % improvement on the constant threshold algorithm.

(a): Changing job length w.r.t. time horizon (-axis), vs. competitive ratio (b): Changing switching cost w.r.t. (-axis), vs. competitive ratio (c): Different volatility levels w.r.t. (-axis), vs. competitive ratio

(d): Cumulative distribution function of competitive ratios

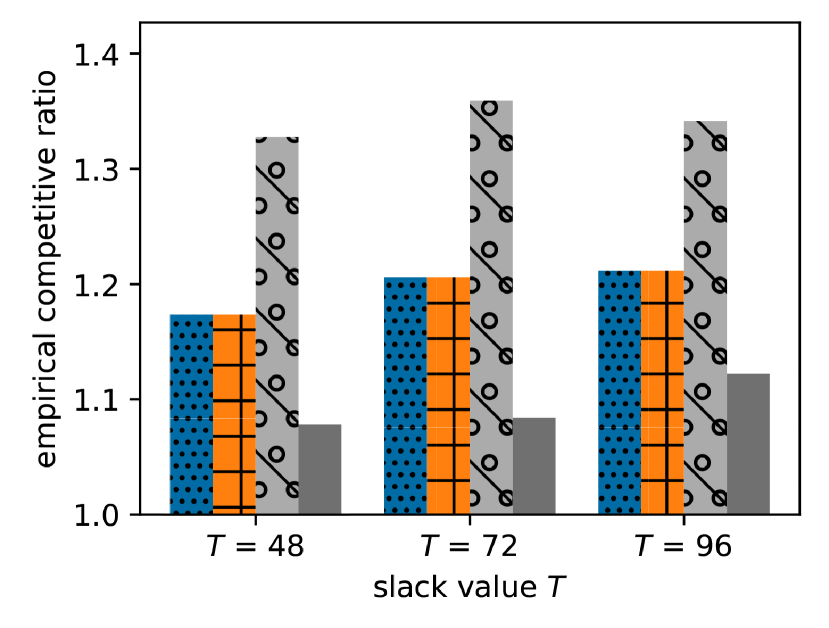

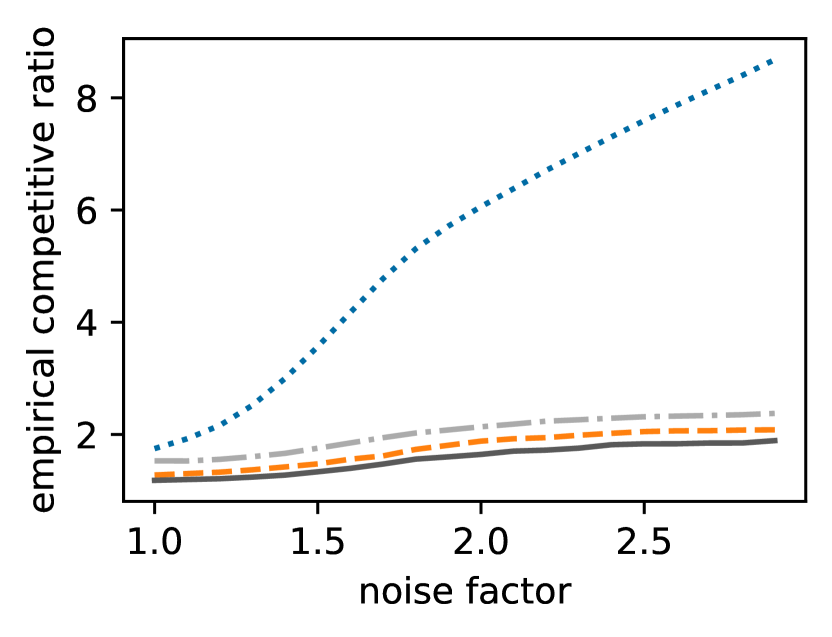

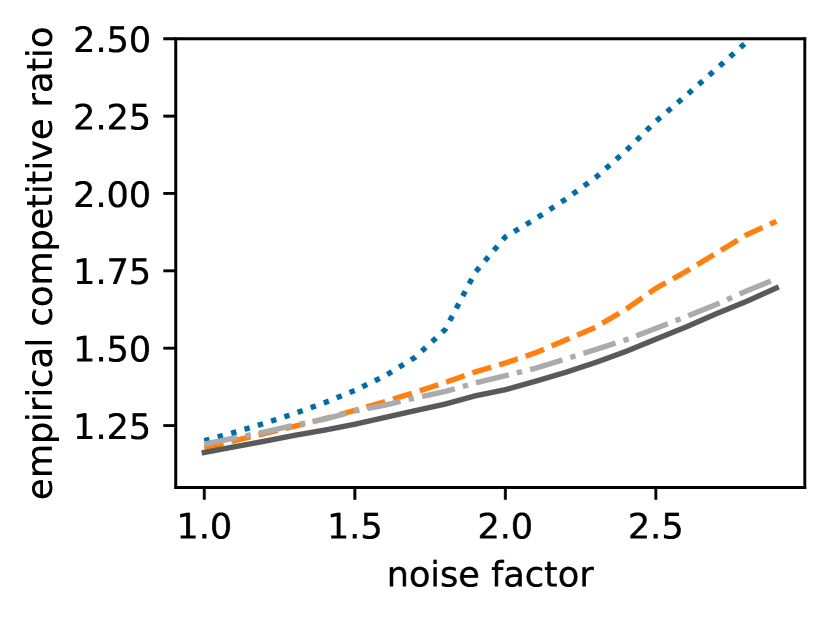

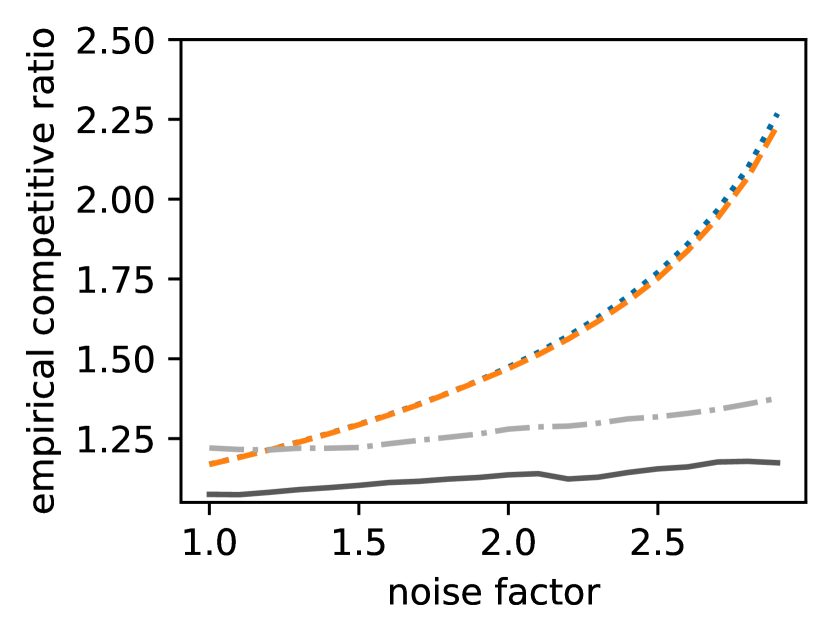

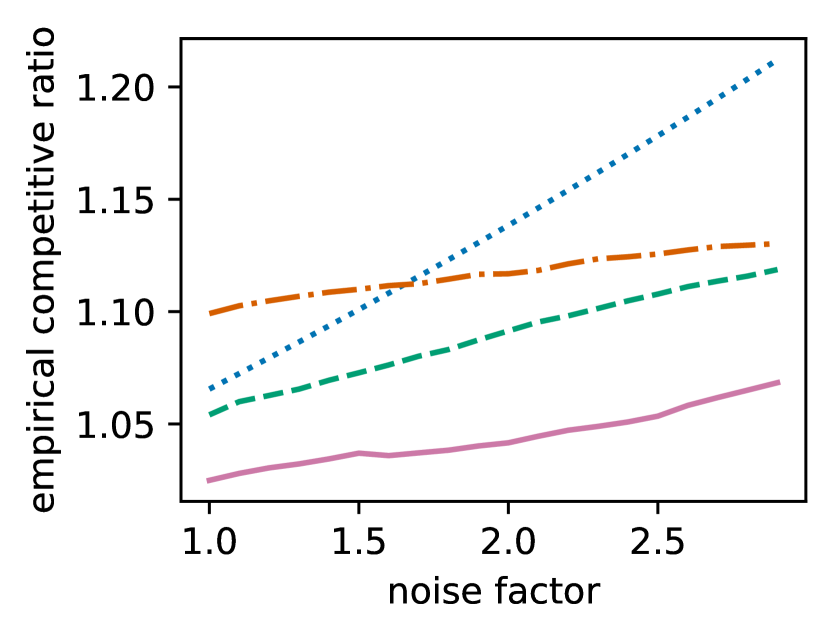

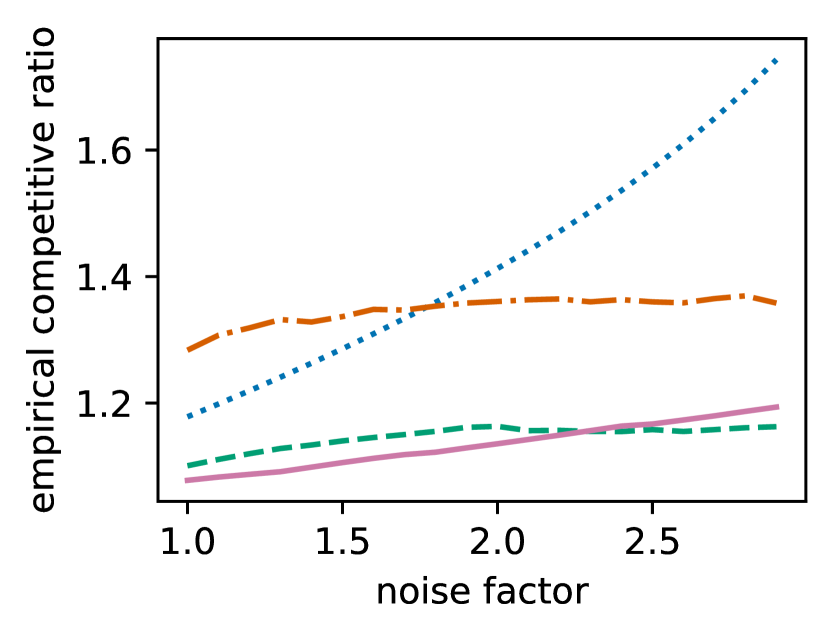

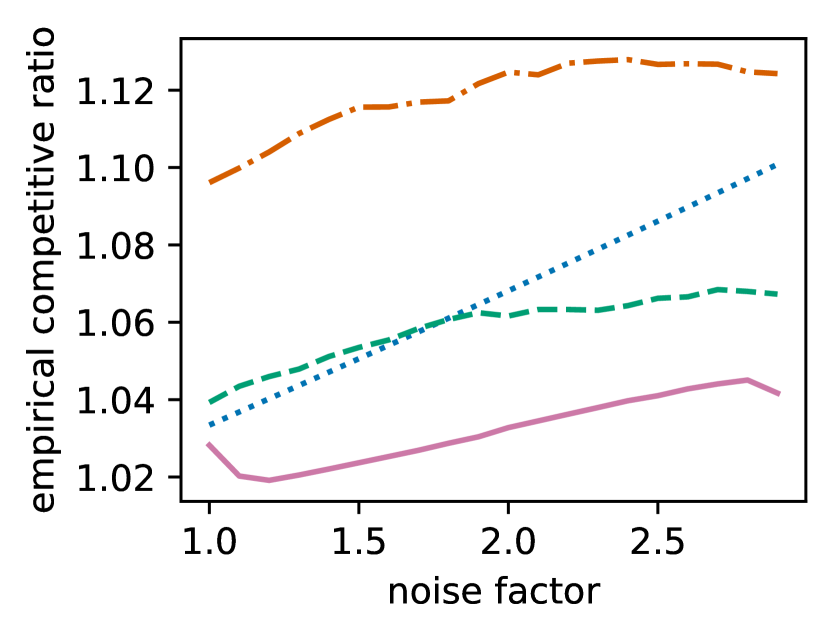

In the final experiment, we test all algorithms on sequences with different volatility. The job length and switching cost are both fixed. We add volatility by setting a noise factor from the range to . By testing different values for this volatility, this experiment tests how each algorithm handles larger fluctuations in the carbon intensity of consecutive time steps. In Figures 6(c), 7(c), and 8(c), we show that the observed competitive ratio of DTPR-min outperforms the benchmark algorithms for all noise factors in all regions. Intuitively, higher volatility values cause the online algorithms to perform worse in general. Averaging over all regions and noise factors, the competitive ratio achieved by DTPR-min is a % improvement on the carbon-agnostic method, a % improvement on the -min search algorithm, and a % improvement on the constant threshold algorithm.

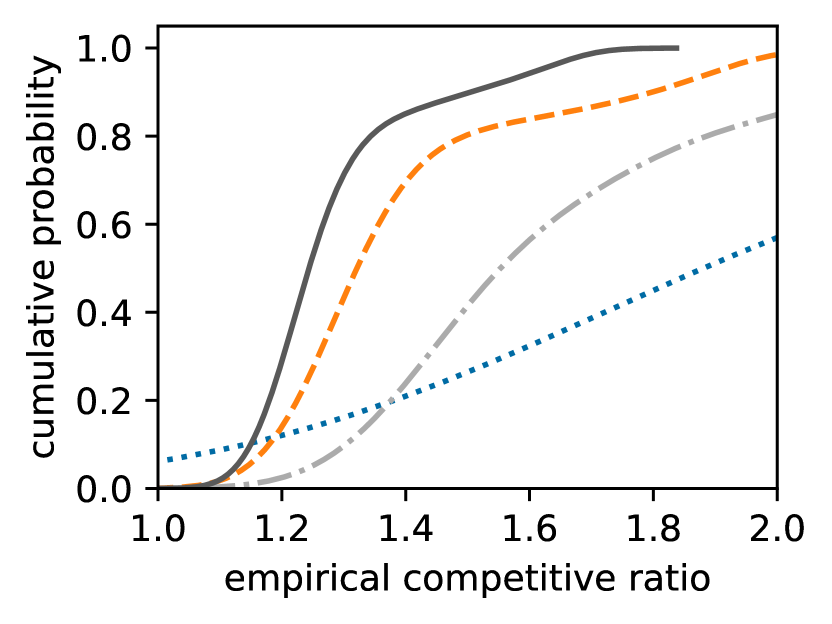

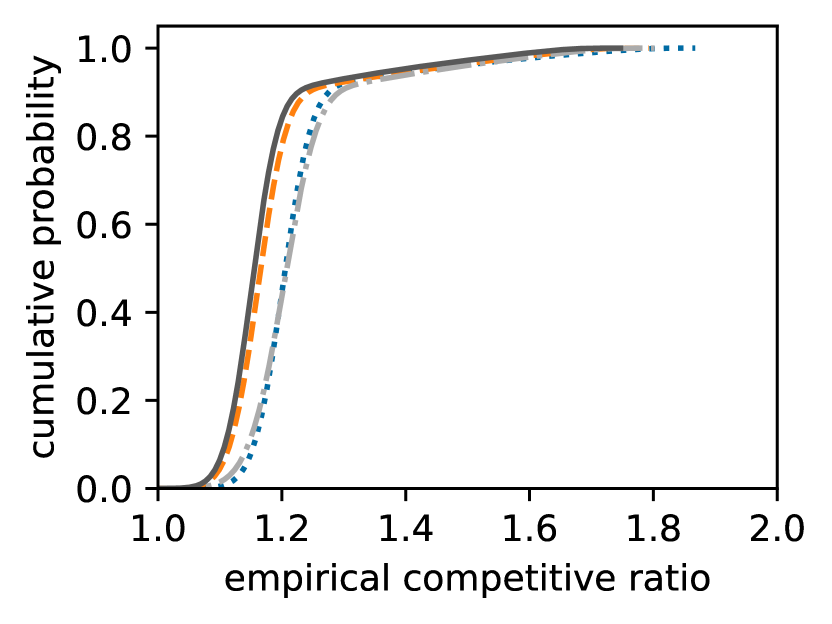

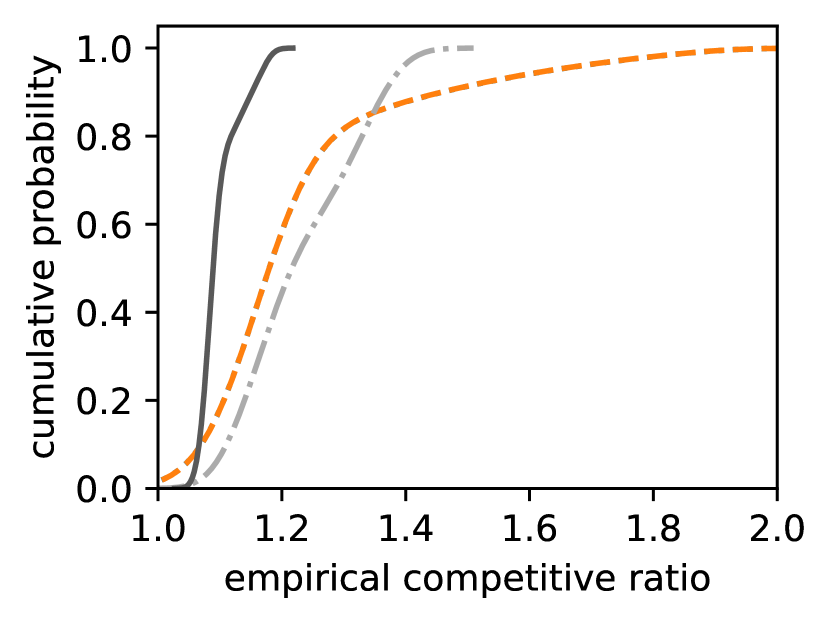

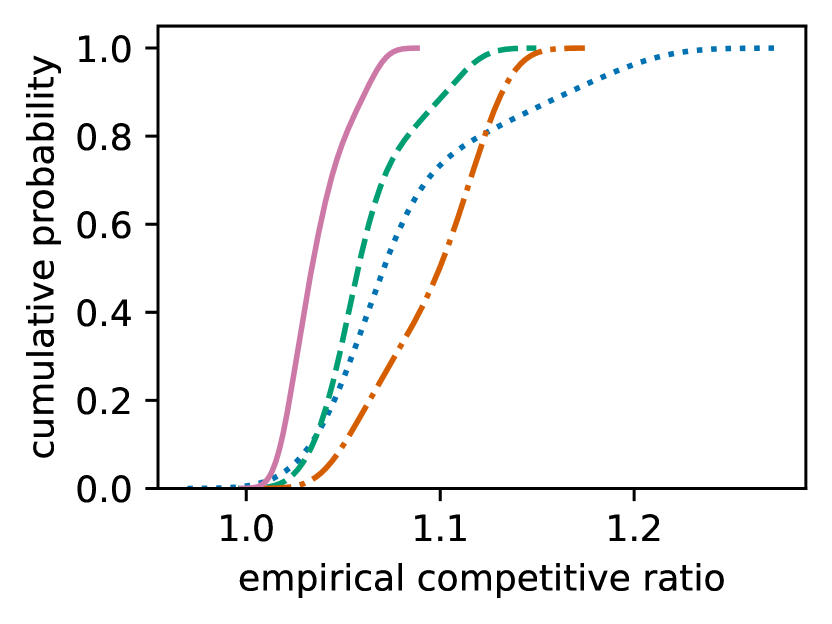

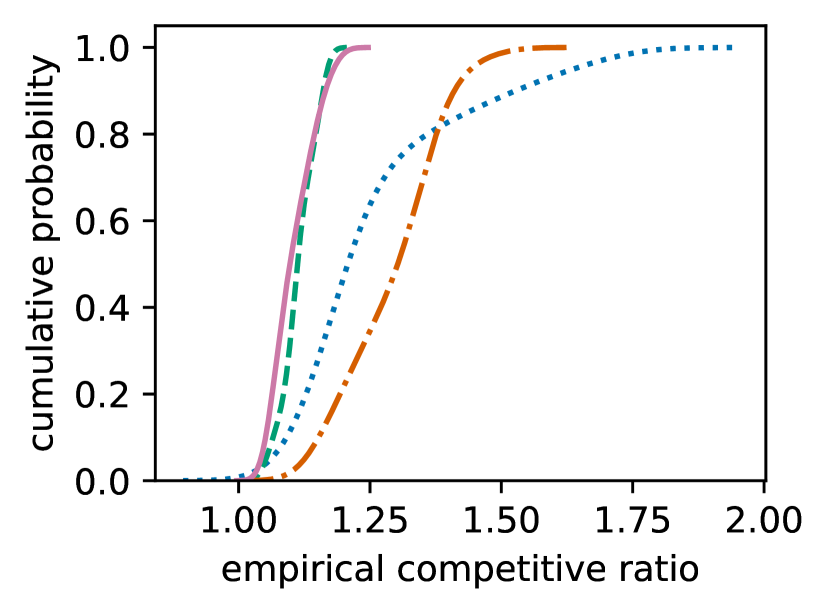

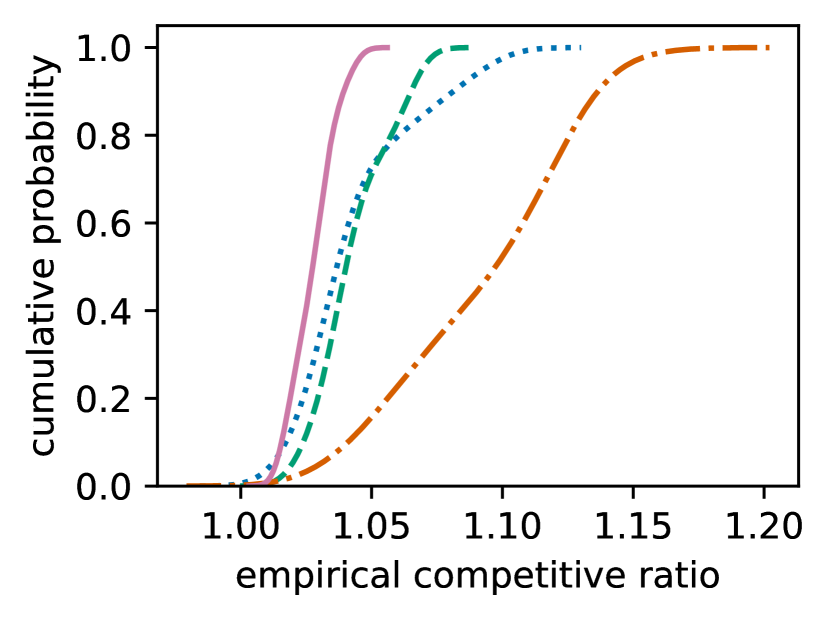

By averaging over all experiments for a given region, we obtain the cumulative distribution function plot for each algorithm’s competitive ratio in Figures 6(d), 7(d), and 8(d). Compared to the carbon-agnostic, constant threshold, and -min search algorithms, DTPR-min achieves a lower average empirical competitive ratio distribution for all tested regions. Across all regions at the 95th percentile, DTPR-min achieves a worst-case empirical competitive ratio of . This represents a % improvement over the carbon-agnostic algorithm, and improvements of % and % over the -min search and constant threshold switching-cost-agnostic algorithms, respectively.

7 Related Work

This paper contributes to three lines of work: (i) work on online search and related problems, e.g., -search, one-way trading, and online knapsack; (ii) work on online optimization problems with switching costs, e.g., metrical task systems and convex function chasing; and (iii) work on carbon-aware load shifting. We describe the relationship to each below.

Online Search.

The OPR problem is closely related to the online -search problem [LSLH22, LPS08], as discussed in the introduction and Section 2.2. It also has several similar counterparts, including online conversion problems such as one-way trading [EYFKT01, MAS14, SLH+21, DHT07] and online knapsack problems [ZCL08, SYH+22, YZH+21], with practical applications to stock trading [LPS08], cloud pricing [ZLW17], electric vehicle charging [SZL+20], etc. The -search problem can be viewed as an integral version of the online conversion problem, while the general online conversion problem allows continuous one-way trading. The basic online knapsack problem studies how to pack arriving items of different sizes and values into a knapsack with limited capacity, while its extensions to item departures [ZLW17, SYH+22] and multidimensional capacity [YZH+21] have also been studied recently. Another line of research leverages machine learning predictions of unknown future inputs to design learning-augmented online algorithms for online -search [LSLH22] and online conversion [SYH+22]. However, to the best of our knowledge, none of these works consider the switching cost of changing decisions. Thus, this work is the first to incorporate switching costs to the -search framework.

Metrical Task Systems.

The metrical task systems (MTS) problem was introduced by Borodin et al. in [BLS92]. Several decades of progress on upper and lower bounds on the competitive ratio of MTS recently culminated with a tight bound of for the competitive ratio of MTS on an arbitrary -point metric space, with being possible on certain metric spaces such as trees [BCLL21, BCR22]. Several modified forms of MTS have also seen significant attention in the literature, such as smoothed online convex optimization (SOCO) and convex function chasing (CFC), in which the decision space is an -dimensional normed vector space and cost functions are restricted to be convex [FL93, LLWA12]. The best known upper and lower bounds on the competitive ratio of CFC are and , respectively, in -dimensional Euclidean spaces [BKL+19, Sel20]. However, algorithms with competitive ratios independent of dimension can be obtained for certain special classes of functions, such as -polyhedral functions [CGW18]. A number of recent works have also investigated the design of learning-augmented algorithms for various cases of CFC/SOCO and MTS which exploit the performance of machine-learned predictions of the optimal decisions [ACE+20, CHW22, CSW23, LYR22, RCMW22]. The key characteristic distinguishing OPR from MTS and its variants is the presence of a terminal deadline constraint. None of the algorithms for MTS-like problems are designed to handle such long-term constraints while maintaining any sort of competitive guarantee.

Carbon-Aware Temporal Workload Shifting.

The goal of shifting workloads in time to allow more sustainable operations of data centers has been of interest for more than a decade, e.g., [GSS19, LLW+11, LCB+12, LWAT12]. Traditionally, such papers have used models that build on one of convex function chasing, -search, or online knapsack to design algorithms; however such models do not capture both the switching costs and long-term deadlines that are crucial to practical deployment. In recent years, the load shifting literature has focused specifically on reducing the carbon footprint of operations, e.g., [RKS+22, ALK+23, BGH+21, WBS+21]. Perhaps most related to this paper is [WBS+21], which explores the problem of carbon-aware temporal workload shifting and proposes a threshold-based algorithm that suspends the job when the carbon intensity is higher than a threshold value and resumes it when it drops below the threshold. However, it does not consider switching nor does it provide any deadline guarantees. Other recent work on carbon-aware temporal shifting seeks to address the resultant increase in job completion times. In [SBM+23], authors leverage the pause and resume approach to reduce the carbon footprint of ML training and high-performance computing applications such as BLAST [fBI22]. However, instead of resuming at normal speed () during the low carbon intensity periods, their applications resume operation at a faster speed (), where the scale factor depends on the application characteristics. It uses a threshold-based approach to determine the low carbon intensity periods but does not consider switching costs or provide any deadline guarantees. An interesting future direction is to extend the DTPR algorithms to consider the ability to scale up speed after resuming jobs.

8 Conclusion

Motivated by carbon-aware load shifting, we introduce and study the online pause and resume problem (OPR), which bridges gaps between several related problems in online optimization. To our knowledge, it is the first online optimization problem that includes both long-term constraints and switching costs. Our main results provide optimal online algorithms for the minimization and maximization variants of this problem, as well as lower bounds for the competitive ratio of any deterministic online algorithm. Notably, our proposed algorithms match existing optimal results for the related -search problem when the switching cost is , and improve on the -min search competitive bounds for non-zero switching cost. The key to our results is a novel double threshold algorithm that we expect to be applicable in other online problems with switching costs.

There are a number of interesting directions in which to continue the study of OPR. We have highlighted the application of OPR to carbon-aware load shifting, but OPR also applies to many other problems where pricing changes over time and frequent switching is undesirable. Pursuing these applications is important. Theoretically, there are several interesting open questions. First, considering the target application of carbon-aware load shifting, some workloads are highly parallelizable [SBM+23], which adds another dimension of scaling to the problem (i.e., instead of choosing to run 1 unit of the job in each time slot, the online player must decide how many units to allocate at each time slot). This makes the theoretical problem more challenging, and is an important consideration for future work. Additionally, very recent work has incorporated machine-learned advice to achieve better performance on related online problems, including -search [LSLH22, SLH+21], CFC/SOCO [CHW22, LYR22], and MTS [ACE+20, CSW23, RCMW22]. Designing learning-augmented algorithms for OPR is a very promising line of future work, particularly considering applications such as carbon-aware load shifting, where predictions can significantly improve the algorithm’s understanding of the future in the best case.

References

- [ABI+20] Pradeep Ambati, Noman Bashir, David Irwin, Mohammad Hajiesmaili, and Prashant Shenoy. Hedge your bets: Optimizing long-term cloud costs by mixing vm purchasing options. In 2020 IEEE International Conference on Cloud Engineering (IC2E), pages 105–115, 2020.

- [ACE+20] Antonios Antoniadis, Christian Coester, Marek Elias, Adam Polak, and Bertrand Simon. Online metric algorithms with untrusted predictions. In Proceedings of the 37th International Conference on Machine Learning, pages 345–355. PMLR, November 2020.

- [ALK+23] Bilge Acun, Benjamin Lee, Fiodar Kazhamiaka, Kiwan Maeng, Udit Gupta, Manoj Chakkaravarthy, David Brooks, and Carole-Jean Wu. Carbon explorer: A holistic framework for designing carbon aware datacenters. In Proceedings of the 28th ACM International Conference on Architectural Support for Programming Languages and Operating Systems, Volume 2, ASPLOS 2023, page 118–132, New York, NY, USA, 2023. Association for Computing Machinery.

- [BCLL21] Sébastien Bubeck, Michael B. Cohen, James R. Lee, and Yin Tat Lee. Metrical Task Systems on Trees via Mirror Descent and Unfair Gluing. SIAM Journal on Computing, 50(3):909–923, January 2021.

- [BCR22] Sébastien Bubeck, Christian Coester, and Yuval Rabani. The Randomized $k$-Server Conjecture is False!, November 2022.

- [BGH+21] Noman Bashir, Tian Guo, Mohammad Hajiesmaili, David Irwin, Prashant Shenoy, Ramesh Sitaraman, Abel Souza, and Adam Wierman. Enabling sustainable clouds: The case for virtualizing the energy system. In Proceedings of the ACM Symposium on Cloud Computing, SoCC ’21, page 350–358, New York, NY, USA, 2021. Association for Computing Machinery.

- [BKL+19] Sébastien Bubeck, Bo’az Klartag, Yin Tat Lee, Yuanzhi Li, and Mark Sellke. Chasing Nested Convex Bodies Nearly Optimally. In Proceedings of the 2020 ACM-SIAM Symposium on Discrete Algorithms (SODA), Proceedings, pages 1496–1508. Society for Industrial and Applied Mathematics, December 2019.

- [BLS92] Allan Borodin, Nathan Linial, and Michael E. Saks. An optimal on-line algorithm for metrical task system. J. ACM, 39(4):745–763, Oct 1992.

- [CGW18] NiangJun Chen, Gautam Goel, and Adam Wierman. Smoothed Online Convex Optimization in High Dimensions via Online Balanced Descent. In Proceedings of the 31st Conference On Learning Theory, pages 1574–1594. PMLR, July 2018.

- [CHW22] Nicolas Christianson, Tinashe Handina, and Adam Wierman. Chasing convex bodies and functions with black-box advice. In Proceedings of the 35th Conference on Learning Theory, volume 178, pages 867–908. PMLR, 02–05 Jul 2022.

- [CSW23] Nicolas Christianson, Junxuan Shen, and Adam Wierman. Optimal robustness-consistency tradeoffs for learning-augmented metrical task systems. In International Conference on Artificial Intelligence and Statistics, 2023.

- [DHT07] Peter Damaschke, Phuong Hoai Ha, and Philippas Tsigas. Online search with time-varying price bounds. Algorithmica, 55(4):619–642, December 2007.

- [EYFKT01] R. El-Yaniv, A. Fiat, R. M. Karp, and G. Turpin. Optimal search and one-way trading online algorithms. Algorithmica, 30(1):101–139, May 2001.

- [fBI22] National Center for Biotechnology Information. Basic Local Alignment Search Tool (BLAST). https://blast.ncbi.nlm.nih.gov, Accessed March 2022.

- [FL93] Joel Friedman and Nathan Linial. On convex body chasing. Discrete & Computational Geometry, 9(3):293–321, March 1993.

- [GSS19] Vani Gupta, Prashant Shenoy, and Ramesh K Sitaraman. Combining renewable solar and open air cooling for greening internet-scale distributed networks. In Proceedings of the Tenth ACM International Conference on Future Energy Systems, pages 303–314, 2019.

- [HH08] Abdolhossein Hoorfar and Mehdi Hassani. Inequalities on the lambert w function and hyperpower function. Journal of Inequalities in Pure and Applied Mathematics, 9(51), January 2008.

- [LCB+12] Zhenhua Liu, Yuan Chen, Cullen Bash, Adam Wierman, Daniel Gmach, Zhikui Wang, Manish Marwah, and Chris Hyser. Renewable and cooling aware workload management for sustainable data centers. In Proceedings of the 12th ACM SIGMETRICS/PERFORMANCE joint international conference on Measurement and Modeling of Computer Systems, pages 175–186, 2012.

- [LLW+11] Zhenhua Liu, Minghong Lin, Adam Wierman, Steven H Low, and Lachlan LH Andrew. Greening geographical load balancing. ACM SIGMETRICS Performance Evaluation Review, 39(1):193–204, 2011.

- [LLWA12] Minghong Lin, Zhenhua Liu, Adam Wierman, and Lachlan L. H. Andrew. Online algorithms for geographical load balancing. In 2012 International Green Computing Conference (IGCC). IEEE, June 2012.

- [LPS08] Julian Lorenz, Konstantinos Panagiotou, and Angelika Steger. Optimal algorithms for k-search with application in option pricing. Algorithmica, 55(2):311–328, August 2008.

- [LSLH22] Russell Lee, Bo Sun, John C. S. Lui, and Mohammad Hajiesmaili. Pareto-optimal learning-augmented algorithms for online k-search problems, November 2022.

- [LWAT12] Minghong Lin, Adam Wierman, Lachlan LH Andrew, and Eno Thereska. Dynamic right-sizing for power-proportional data centers. IEEE/ACM Transactions on Networking, 21(5):1378–1391, 2012.

- [LYR22] Pengfei Li, Jianyi Yang, and Shaolei Ren. Expert-Calibrated Learning for Online Optimization with Switching Costs. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 6(2):1–35, May 2022.

- [Map20] Electricity Maps. Electricity Map. https://www.electricitymap.org/map, Accessed September 2020.

- [MAS14] Esther Mohr, Iftikhar Ahmad, and Günter Schmidt. Online algorithms for conversion problems: a survey. Surveys in Operations Research and Management Science, 19(2):87–104, 2014.

- [RCMW22] Daan Rutten, Nicolas Christianson, Debankur Mukherjee, and Adam Wierman. Smoothed Online Optimization with Unreliable Predictions, October 2022.

- [RKS+22] Ana Radovanovic, Ross Koningstein, Ian Schneider, Bokan Chen, Alexandre Duarte, Binz Roy, Diyue Xiao, Maya Haridasan, Patrick Hung, Nick Care, et al. Carbon-aware computing for datacenters. IEEE Transactions on Power Systems, 2022.

- [SBM+23] Abel Souza, Noman Bashir, Jorge Murillo, Walid Hanafy, Qianlin Liang, David Irwin, and Prashant Shenoy. Ecovisor: A virtual energy system for carbon-efficient applications. In Proceedings of the 28th ACM International Conference on Architectural Support for Programming Languages and Operating Systems, Volume 2, ASPLOS 2023, page 252–265, New York, NY, USA, 2023. Association for Computing Machinery.

- [Sel20] Mark Sellke. Chasing convex bodies optimally. In Proceedings of the Thirty-First Annual ACM-SIAM Symposium on Discrete Algorithms, SODA ’20, pages 1509–1518, USA, January 2020. Society for Industrial and Applied Mathematics.

- [SLH+21] Bo Sun, Russell Lee, Mohammad H Hajiesmaili, Adam Wierman, and Danny HK Tsang. Pareto-optimal learning-augmented algorithms for online conversion problems. In Advances in Neural Information Processing Systems (NeurIPS), 2021.

- [SRI16] Supreeth Shastri, Amr Rizk, and David Irwin. Transient guarantees: Maximizing the value of idle cloud capacity. In SC’16: Proceedings of the International Conference for High Performance Computing, Networking, Storage and Analysis, pages 992–1002. IEEE, 2016.

- [Ste09] Seán M. Stewart. On certain inequalities involving the lambert w function. Journal of Inequalities in Pure and Applied Mathematics, 10(96), November 2009.

- [SYH+22] Bo Sun, Lin Yang, Mohammad Hajiesmaili, Adam Wierman, John CS Lui, Don Towsley, and Danny HK Tsang. The online knapsack problem with departures. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 6(3):1–32, 2022.

- [SZL+20] Bo Sun, Ali Zeynali, Tongxin Li, Mohammad Hajiesmaili, Adam Wierman, and Danny HK Tsang. Competitive algorithms for the online multiple knapsack problem with application to electric vehicle charging. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 4(3):1–32, 2020.

- [WBS+21] Philipp Wiesner, Ilja Behnke, Dominik Scheinert, Kordian Gontarska, and Lauritz Thamsen. Let’s Wait AWhile: How Temporal Workload Shifting Can Reduce Carbon Emissions in the Cloud. In Proceedings of the 22nd International Middleware Conference, pages 260–272, 2021.

- [YZH+21] Lin Yang, Ali Zeynali, Mohammad H. Hajiesmaili, Ramesh K. Sitaraman, and Don Towsley. Competitive algorithms for online multidimensional knapsack problems. 5(3), Dec 2021.

- [ZCL08] Yunhong Zhou, Deeparnab Chakrabarty, and Rajan Lukose. Budget constrained bidding in keyword auctions and online knapsack problems. In Lecture Notes in Computer Science, pages 566–576. Springer Berlin Heidelberg, 2008.

- [ZLW17] ZiJun Zhang, Zongpeng Li, and Chuan Wu. Optimal posted prices for online cloud resource allocation. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 1(1):1–26, 2017.

Appendix A Case Study Results for DTPR-max Algorithm

This section presents and discusses the deferred experimental results for the DTPR-max algorithm (pseudocode summarized in Algorithm 2) in the carbon-aware temporal workload shifting case study. We evaluate DTPR-max against the same benchmark algorithms described in Section 6.1.

For the maximization metric, we consider the percentage of carbon-free electricity powering the grid. At each time step , the electricity supply has a carbon-free percentage , i.e., if the job is being processed during time slot (), the electricity powering the data center’s is carbon-free, and the objective is to maximize this percentage over all slots of the active running of the workload.

In these maximization experiments, the switching-cost-agnostic -max-search algorithm chooses to run the th hour of the job during the first time slot where the carbon-free supply is at least . Similarly, the constant threshold algorithm chooses to run the job whenever the carbon-free supply is at least . We set and to be the minimum and maximum carbon-free supply percentages over the entire trace being studied.

(a): Changing job length w.r.t. time horizon (-axis), vs. competitive ratio (b): Changing switching cost w.r.t. (-axis), vs. competitive ratio (c): Different volatility levels w.r.t. (-axis), vs. competitive ratio (d): Cumulative distribution function of competitive ratios

As in Section 6.2, our focus is on the competitive ratio (lower competitive ratio is better). We report the performance of all algorithms for each experiment setting, in each tested region.

In the first experiment, we test all algorithms for different job lengths in the range from hours to . The switching cost is non-zero and fixed, and no volatility is added to the carbon trace. By testing different values for , this experiment tests different ratios between the workload length and the slack provided to the algorithm. In Figures 10(a), 11(a), and 12(a), we show that the observed average competitive ratio of DTPR-max narrowly outperforms the benchmark algorithms for all values of in all regions, and it compares particularly favorably for short job lengths. Averaging over all regions and job lengths, the competitive ratio achieved by DTPR-max is a % improvement on the carbon-agnostic method, a % improvement on the -max search algorithm, and a % improvement on the constant threshold algorithm.

In the second experiment, we test all algorithms for different switching costs in the range from to . The job length is set to hours, and no volatility is added to the carbon trace. By testing different values for , this experiment tests how an increasing switching cost impacts the performance of DTPR-max with respect to other algorithms which do not explicitly consider the switching cost. In Figures 10(b), 11(b), and 12(b), we show that the average competitive ratio of DTPR-max notably outperforms the other algorithms for a wide range of values in all regions. Unsurprisingly, the carbon-agnostic technique (which only incurs a switching cost of ) is more competitive as grows. The -max search algorithm performs noticeably worse as grows. While the constant threshold algorithm has relatively consistent performance, the -max search algorithm performs noticeably worse as grows. Averaging over all regions and switching cost values, the competitive ratio achieved by DTPR-max is a % improvement on the carbon-agnostic method, a % improvement on the -max search algorithm, and a % improvement on the constant threshold algorithm.

(a): Changing job length w.r.t. time horizon (-axis), vs. competitive ratio (b): Changing switching cost w.r.t. (-axis), vs. competitive ratio (c): Different volatility levels w.r.t. (-axis), vs. competitive ratio (d): Cumulative distribution function of competitive ratios

(a): Changing job length w.r.t. time horizon (-axis), vs. competitive ratio (b): Changing switching cost w.r.t. (-axis), vs. competitive ratio (c): Different volatility levels w.r.t. (-axis), vs. competitive ratio (d): Cumulative distribution function of competitive ratios

In the final experiment, we test all algorithms on sequences with different volatility. The job length and switching cost are both fixed. We add volatility by setting a noise factor from the range to . By testing different values for this volatility, this experiment tests how each algorithm handles larger fluctuations in the carbon intensity of consecutive time steps. In Figures 10(c), 11(c), and 12(c), we show that the observed average competitive ratio of DTPR-max outperforms the other algorithms for most noise factors in all regions, with a slight degradation in the Pacific Northwest region. Intuitively, higher volatility values cause the online algorithms to perform worse in general. Averaging over all regions and noise factors, the competitive ratio achieved by DTPR-max is a % improvement on the carbon-agnostic method, a % improvement on the -max search algorithm, and a % improvement on the constant threshold algorithm.

By averaging over all experiments for a given region, we obtain the cumulative distribution function plot for each algorithm’s competitive ratio in Figures 10(d), 11(d), and 12(d). Compared to the carbon-agnostic, constant threshold, and -max search algorithms, DTPR-max generally exhibits a lower average empirical competitive ratio over the tested regions. Notably, all of the algorithms are nearly 1-competitive in our experiments. Compared to our minimization experiments, DTPR-max outperforms the baseline algorithms by a smaller margin. Across all regions at the 95th percentile, DTPR-max achieves a worst-case empirical competitive ratio of . This represents a % improvement over the carbon-agnostic algorithm, and improvements of % and % over the -max search and constant threshold switching-cost-agnostic algorithms, respectively.

We conjecture that one dynamic contributing to this is the relatively low values of observed for the carbon-free supply percentage in these real-world carbon traces.

Appendix B Competitive Analysis of DTPR-max: Proof of Theorem 5

Proof of Theorem 5.

For , let be the sets of OPR-max price sequences for which DTPR-max accepts exactly prices (excluding the prices it is forced to accept at the end of the sequence). Then all of the possible price sequences for OPR-max are represented by . By definition, . Let be fixed, and define the following two price sequences and :

We have two special cases for and . For , we have that , and this sequence simply consists of repeated times, followed by repeated times. For , we also have that , and this sequence consists of one price with value and one price with value , followed by repeated times and repeated times.

Observe that as , and are sequences yielding the worst-case ratios in , as DTPR-max is forced to accept worst-case values at the end of the sequence, and each accepted value is exactly equal to the corresponding threshold.

and also represent two extreme possibilities for the switching cost. In , DTPR-max only switches twice, but it mostly accepts values . In , DTPR-max must switch times because there are many intermediate values, but it only accepts values which are at least .

Observe that . First, the optimal solution for both sequences is exactly the same: .

For any sequence in , we also know that , so .

By definition of the threshold families and , we know that

for any value :

Note that whenever , we have that , and . Thus, holds for any value of .

By definition of , we simplify to . For any sequence , we have the following:

| (12) |

Lemma 11.

For any , by definition of and ,

For , the competitive ratio is exactly :

and thus for any sequence ,

Since for any sequence , this implies that DTPR-max is -competitive.∎

Proof of Corollary 7.

For simplification purposes, let , where is a real constant on the interval . To show part (a) for REGIME-1, with fixed , observe that for sufficiently large , we have the following:

Let . Then, for sufficiently large , we have the following:

Furthermore, let and set .

A similar calculation as above shows that for sufficiently large we have:

Thus, satisfies (10) for sufficiently large , fixed , and

.

To show part (b) for REGIME-2, observe that the right-hand side of (10) can be approximated as when . Then by taking limits on both sides, we obtain the following:

Let as outlined above. We then obtain the following:

By definition of the Lambert function, solving this equation for obtains part (2). ∎

Appendix C Proofs of Lemmas 10 and 11

In this section, we give the deferred proofs of Lemmas 10 and 11, which are used in the proofs of Theorem 4 and Theorem 5, respectively.

Proof of Lemma 10.

Appendix D Proofs of Lower Bound Results

This section formally proves the lower bound results for both OPR-min and OPR-max, building on the proof sketch provided in Section 5.2.

D.1 Proof of Theorem 8 (OPR-min Lower Bound)

Proof of Theorem 8.

Let ALG be a deterministic online algorithm for OPR-min, and suppose that the adversary uses the price sequence , which is exactly the sequence defined by (5). is presented to ALG, at most times or until ALG accepts it. If ALG never accepts , the remainder of the sequence is all , and ALG achieves a competitive ratio of , as defined in (7).

If ALG accepts , the next price presented is , repeated at most times or until ALG switches to reject . After ALG has switched, is presented to ALG, at most times or until ALG accepts it. Again, if ALG never accepts , the remainder of the sequence is all , and ALG achieves a competitive ratio of at least , as defined in (7).

As the sequence continues, whenever ALG does not accept some after it is presented times, the adversary increases the price to for the remainder of the sequence. Otherwise, if ALG accepts prices before the end of the sequence, the adversary concludes by presenting at least times.