Relaxed Optimal Control Problem for a Finite Horizon G-SDE with Delay and Its Application in Economics

Omar Kebiri1,2 and Nabil Elgroud3,1 1Institute of Mathematics, Brandenburgische Technische Universität

Cottbus-Senftenberg, Cottbus, Germany.

2Institute of Mathematics, The free University of Berlin, Berlin, Germany.

3Lab. of Probability and Statistics (LaPS), Department of

Mathematics, Badji Mokhtar University, Annaba, Algeria

Abstract

This paper investigates the existence of a G-relaxed optimal control of a controlled stochastic differential delay equation driven by G-Brownian motion (G-SDDE in short). First, we show that optimal control of G-SDDE exists for the finite horizon case. We present as an application of our result an economic model, which is represented by a G-SDDE, where we studied the optimization of this model. We connected the corresponding Hamilton Jacobi Bellman equation of our controlled system to a decoupled G-forward backward stochastic differential delay equation (G-FBSDDE in short). Finally, we simulate this G-FBSDDE to get the optimal strategy and cost.

The classical stochastic optimal control problem for delayed systems has

received a lot of attention. Systems where the dynamics are

influenced by the current value of the state, as well as the past values, are called stochastic differential delay equations (SDDEs).

This type of model is useful in situations where there is some memory in the

dynamics, such as economics and finance, as well as the population growth

models in biology (see [17], [20], [32]).

Elsanosi et al [9] studied the stochastic maximum principle with delay and proved a verification theorem of a variational inequality. In [17], Ivanov studied the optimal control of stochastic

differential delay equations and gave an application to a stochastic model

in economics. Menoukeu-Pamen [21] obtained a necessary and sufficient

condition of optimality of stochastic maximum principle for delayed

stochastic differential games for a general non-Markovian stochastic

control problem under model uncertainty and delay. In [22]

the authors studied sufficient and necessary stochastic maximum principles of

time-delayed stochastic differential equations with jumps. Agram et al [1] derived stochastic maximum principles for optimal control under

partial information in the infinite horizon for a system governed by

forward-backward stochastic differential equations (FBSDEs in short) with

delay. The existence of optimal control of non-linear

multiple-delay systems having an implicit derivative with quadratic

performance criteria by suitably adopting some of the techniques treated by

[3]. Rosenblueth [29] proposed two different

relaxation procedures for optimal control problems involving transformations

of the state, and the control functions show that the resulting relaxed

problem has a solution, for which the existence of a minimizer is

assured. The optimal control of systems is described by delay differential

equations with a quadratic cost functional (see [23]).

Motivated by a concept of uncertainty which appears in many areas of sciences

contains inaccurate parameters, in general, the liquidity in the markets, risks

resulting from dark fluctuations, and their impact on the movement of the asset

prices and financial crises. In particular, the optimal portfolio choice

problems where the risk premium processes and the volatility are unknown.

Peng [24, 25]involved the sublinear

or G-expectation space with a process called G-Brownian motion, also

constructed Itô’s stochastic calculus with respect to the G-Brownian

motion, and Gao [13] proved the existence and uniqueness of the solution of stochastic

differential equations driven by G-Brownian motion (G-SDEs). Furthermore, Fei et al [10] studied the existence and stability of solutions

to highly nonlinear stochastic differential delay equations driven by G-Brownian motion (G-SDDEs). Some properties of

numerical solutions for semilinear stochastic delay differential equations

driven by G-Brownian motion have been studied by [36].

Xu in [33] studied the existence and uniqueness theorem of backward

stochastic differential equations (BSDEs) under super linear expectation to provide probabilistic interpretation for the viscosity

solution of a class of Hamilton-Jacobi-Bellman (HJB in short) equations, he also shows that

BSDEs under super linear expectation could characterize a class of

stochastic control problems. The authors in [14] used the HJB equations that are recognized as the dynamic

programming equations of the optimal control problems.

Recently, the formulation of optimal control problem in a G-Brownian

motion was studied by [5, 16, 15, 35, 27, 28]. Moreover in [26] they also study the

problem of the existence of optimal relaxed control for

stochastic differential equations driven by a G-Brownian motion. Moreover in [8] the authors studied the existence of relaxed optimal control for G-neutral stochastic functional differential equations with simulations results based on [34].

In this paper, we consider an optimal control of systems governed by a

stochastic differential delay equation driven by a G-Brownian motion (G-SDDE)

(1)

where , , and is a -dimensional

G-Brownian motion defined on a space of sublinear expectation , with a universal filtration , and using the space of probability measures

on , where is the

-algebra of Borel subsets of the set of values taken by the strict controls. is called a strict control, with value in the action space , where we denote is a set of strict controls, and is a compact polish subspace of .

is a quadratic variation process of G-Brownian motion.

Within the G-Brownian motion framework studied in [24, 25], the controlled system that minimizes the cost functional with the finite horizon in which the coefficient of the initial cost depends on not

only on the current value of the state but also on past value, which is given by

(2)

Our results are based on the aggregation property and the tightness

arguments of the distribution of the control problem.

This paper is organized as follows: In section 2, we

recall some notions and preliminaries, and we formulate our problem. In section 3, first, we introduce the

space of relaxed control and the problem of G-relaxed control of G-SDDE.

In section 4, we established the existence of a minimizer of the cost function

for the finite horizon. Then, we prove our main result, which is the existence of G-relaxed optimal control. In the last section, we provide a stochastic model in economics and its

optimization that have delay and randomness in the production cycle, In the last section, where the noise of the system is big, which prevents us to estimate the noise parameter. This will lead to a G-SDDE.

To minimize the

investment capital under the assumptions of labor, we obtain a probabilistic representation of the solution to the HJB equation, expressed in the form of a system of decoupled forward backward stochastic differential delay equations driven by G-Brownian motion. In the end, we present the simulation result of this G-FBSDDE.

2 Preliminaries and formulation of problem

This section aims to give some basic concepts and results

of G-stochastic calculus. More details about these are included in [7, 6, 30, 31, 24, 25], and we introduce the formulation of the problem of optimal control for n-dimensional

stochastic differential delay equation is driven by G-Brownian motion (G-SDDE).

Let , be the space of real valued continuous functions on such that equipped with the following distance

and , is the canonical process on and let be the natural filtration generated by . In addition, for each we set

with denotes a -negligible set on a -algebra given by

Consider the following space, for

with denotes a space of bounded and Lipschitz on

Let be a fixed time.

We have the following lemma

Lemma 1

For any arbitrary probability measure on There is a -a.s. unique -measurable random variable for each such that, for every -measurable random variable , we have

For every -progressively

measurable process , there is a unique -progressively measurable process such that

Furthermore, if is - continuous, then can

be chosen to - continuous.

To follow the details see (Lemma 2.1, [30]).

The G-expectation , constructed by [24], is a

consistent sublinear expectation on the lattice of real

functions, it satisfies:

1.

Sub-additivity: for all

2.

Monotonicity: for all

3.

Constant preserving: for all

4.

Positive homogeneity: for all

If and are only satisfied, the triple is said to be sub-linear expectation space,

is also referred to as a nonlinear

expectation and the triple

is called a nonlinear expectation space.

We suppose that, if , then for all

Definition 2

Under if for any the

random vector is said to be independent from another

random vector

Definition 3

Under the G-expectation an -dimensional random

vector on is said to be

G-normally distributed for any , if the function defined by

is the unique viscosity solution of the parabolic equation

with denotes the Hessian matrix of and let define the nonlinear operator G by

where denotes a symmetric matrix and is a

given non-empty, bounded, and closed subset of . The transpose of the vector is denoted by . denotes the G-normal distribution, where .

Definition 4 (G-Brownian Motion)

The canonical process on

is called a G-Brownian

motion if the following properties hold:

•

•

For each the increment is -distributed.

•

is independent of

for and

For we use to signify the completion of under the natural norm

and define as the space of -progressively

measurable, -valued simple processes of the form

with denotes a subdivision of . The space is called the closure of

with respect to the norm

Note that if . For each , let be the set of -measurable

functions. We set

For each , the related Itô integral of is defined by

where is the

mapping continuously extended to The quadratic variation

process of is

not always a deterministic process, and can be formulated in by the continuous -symmetric-matrix-valued process given by

(3)

where a diagonal is constituted of non-decreasing processes. Here, for

, the symmetric matrix is defined by for , where ”” represents the

scalar product in .

Let the mapping for each , given by

Then can be extended continuously to

for each

We have the following properties (formulated for the case d = 1, for

simplicity).

([7]) Assume . There exists a weakly compact family of

probability measures on

such that

Then is the associated regular Choquet capacity related to defined by

Definition 7

If or equivalently if for all A set is polar if a property holds outside a polar set.

It is called quasi surely ().

Let us define the -polar sets

For the possibly mutually singular probability measures , in [31], we must utilise the following

universal filtration

The dual expression of the G-expectation gives the following aggregation property.

Lemma 8

Let . Then, is Itô-integrable for every . Moreover, for every ,

where the right-hand side is the standard Itô integral. As a result, the quadratic variation process defined in (3) agrees with the standard quadratic variation process

quasi-surely. For more details see (Proposition 3.3, [31]). In the sequel, we will start by removing the notation G from both the G-stochastic integral and the G-quadratic variation.

Among the results of stability obtained in [6], we quote the following which plays an essential part in our analysis.

In view of the dual formulation of the G-expectation, we end this section

by giving the following one-dimensional G-Burkholder-Davis-Gundy (G-BDG in short) type

estimates.

([13]) For each and then there exists a positive constant such that we have

We study the existence of optimal control problem for -dimensional

G-SDDE. We are concerned with the controlled system described by a G-SDDE, which

is given by

(4)

where is adapted -value random variable, where is a space of continuous functions equipped with the norm ,

as well as Then, the integral equation is given by

(5)

with is a quadratic

variation process of -dimentional G-Brownian motion

defined on a space of sublinear expectation , with an universal filtration and are called

the strict control variables for each

Moreover, the functions

as well as for each and for

each strict control .

3 Relaxed control of the G-SDDE.

The strict control problem may not have an optimal solution

in the absence of convexity assumptions because is too small

to contain a minimizer. Then the strict control space must then be injected

into a larger space with good compactness and convexity properties. is the space of probability measures

on , endowed with its Borel -algebra whith is the set of compact polish space.

For that we consider the class of G-relaxed stochastic controls on

.

Definition 12 (G-Relaxed stochastic control)

An -progressively measurable random measure of the

form is a G-relaxed

stochastic control on , such that

(6)

where .

It is important to note that, the set of ’strict’ controls constituted of -adapted processes each strict control taking values in the set , can be

considered as a G-relaxed control into the set of G-relaxed

controls via the mapping

(7)

where is a Dirac measure charging

for each

Remark 13

We mean by “the process the - progressively measurable” that for every and every , the mapping described by is -measurable, and the process is -adapted.

The class of G-relaxed stochastic controls is denoted by .

To consider the control problem (5), we must first study the existence and uniqueness of the solution to the following equation

(8)

where

The following assumptions are required to ensure the existence and

uniqueness of the solution of the equation

The functions and are bounded and Lipschitz continuous with respect to the space variables uniformly in .

There exist such that

and

for each and .

By the result of [10], under our assumptions and the G-SDDE (5) has

a unique solution , for each fixed control.

4 Approximation and existence of G-relaxed optimal control

We consider a relaxed control problem (6). Let denotes the solution of equation ( 6)

related to the G-relaxed control. Let establish the existence of a

minimizer of the cost for finite horizon

corresponding to .

where the functions,

fulfill the following important assumption

The functions , are bounded, and the coefficient is Lipschitz continuous, and is Lipschitz continuous with respect to the space variables uniformly in time and control .

We recall that in the strict control problem

(9)

From the set ,

(10)

then, we have

(11)

Moreover, for each ,

(12)

We use the relaxed control problem to introduce the definition of stable

convergence to define the next lemma, which according to the classical

Chattering lemma states that each G-relaxed control in can

be approximated by a sequence of strict controls from .

Definition 14 (stable convergence)

([8]) Let . We say that, we have a stable convergence, if for any

continuous function we have

(13)

Lemma 15 (G-Chattering lemma)

Let the process is an -

progressively measurable with values in . Then there exists a sequences of -progressively measurable

processes with values in such that

converges in terms of stable convergence (thus weakly).

Proof. Given the G-relaxed control which is -progressively measurable, the precise pathwise development of the approximating sequence

of G-relaxed control in (see lemma after theorem 3, [11]), which easily need extend to consider the strict controls -progressively measurable.

Let the corresponding solution of G-SDDE (5), associated with

and

satisfy that

(14)

The following important lemma prove the stability results for the G-SDDE (11), and gives for every.

Lemma 16 (stability results)

Suppose that and satisfy assumption . Let be a G-relaxed control, and let be a sequence defined in Lemma 15. Then we have

For every it

holds that

(15)

and

(16)

Let and are the corresponding cost functionals to and respectively. Then,

there exists a sub-sequence of such that

(17)

and, for every

(18)

Furthermore,

(19)

then, there exists a G-relaxed optimal control such that

(20)

Since, by using the property of aggregation in Lemma 8, under

the singularity for every , the G-SDDE becomes a standard SDDE, this result was confirmed by the technique

in [2].

Proof.

We set

and note that for each .

If there is indeed a such that

we can find a probability such that

There exists a sub-sequence that

converges weakly to some , according to is weakly compact. Then, we have

(21)

This is a contradiction to the fact from (15).

The proof of (15) is based on G-BDG inequalities and the standard Gronwall inequality as well as the

Dominated Convergence theorem, according to stable convergence in Lemma 14 of converges to , and the proof method does not extend to proving (16) because the

Dominated Convergence theorem (and even the celebrated Fatou’s lemma) is no

longer valid under sublinear expectation, but the G-BDG inequalities hold

true for G-stochastic integrals and G-SDDEs.

Assume that and satisfy

assumption .

We have converges weakly

to quasi-surely. Then, there exists a

sub-sequence of we obtain

(22)

By using Proposition 17 in [6] and (16) it follows that, there exists a sub-sequence

that converges quasi-surely to -, for all ,

uniformly in . We can use (16) for every to obtain that

The following theorem constitutes the main result of our problem, which gives that the two problems have the same Infinium of the expected costs.

Theorem 17

For every and , we

have

(23)

Furthermore, there is a G-relaxed optimal control such that

(24)

recall that

(25)

where for each , the relaxed cost functional is

given as follow

(26)

To prove (23), using Lemma 15 of G-Chattering lemma and Lemma 16 of stability results for the G-SDDE (11). According to Lemma 15,

given a G-relaxed control , and there is a sequence of strict controls such that converges weakly to quasi-surely i.e. -, for all . The existence of a G-relaxed optimal control for

each and a tightness argument is used to

prove (24).

Proof. From (7) and (22) we can easily obtain that

Therefore, for every , , we

have

Hence,

which proves (23).

Since and are continuous and bounded, for each we turn now to the proof of existence of G-relaxed

optimal control.

Then, the sequence

converges weakly to .

Assume there is an such that, for each

Next, by according to Lemma 16, for each there exists a G-relaxed optimal control such that

we get that

However, there exists for every , such that

We can extract a sub-sequence , from the sequence being weakly compact, which converges weakly to some .

Thus, As a result of (27) for each , it follows that

Particularly, we obtain for a given

,

which is a contradiction with the fact that .

5 Economics model

As an application of our theoretical result, an economics model describing the rate of change of capital and labor in a market by a system of ODEs introduced by F. R. Ramsey in (for more details, can see [Ramsey1928]), given by

(28)

where

: production,

: consumption rates.

: the rate of growth of labor (population),

In [Gandolfo1997] the production, capital and labor

related by the Cobb-Douglas formula as follow

(29)

where are a constants. If , we get the linearity of (29) under certain scenarios, which we will assume throughout our problem. The labor is constantly given by , which verifies specific markets, or we take in many years relatively short time intervals. As a result, the production rate and capital have a dependent formula , where .

Large random disturbances (big noise), which come from political decisions, wars, and the atmosphere situations, are the real reasons for influencing the change in the economy. Then, we can define the production rate by

where is a standard Brownian motion,

with is an unknown parameter and the coefficient depends on because is strongly affected by factors that change the economy due to a big noise.

Usually, the essential period is needed for transition due to the influence and change of the economy, such as the length of the production cycle in many economic situations during the war such as the increase in oil and the impact on wheat production.

Therefore, the most accurate assumption given

the change in the rate of capital depends on the investment made at time , where is the current time and is the duration of the cycle required to create working capital during wartime delays and political decisions delays, and as time passes, the noise increases.

(32)

which means that we can not estimate the value of , the only information that we can know is that gamma in , for some

the idea is to consider the worst-case scenario; i.e.,

where is an expected valued over , with is the probability indexed induced by (32), and is the non-linear expectation, with is a given function, and is the solution of the following equation

(33)

where is the G-Brownian motion follow . It is necessary to study how we make decisions when we are often faced with probabilistic uncertainty. The main question is to control the consumption rate by a control , i.e., it is of the form , then

(34)

with

(35)

For this, we suggest studying the modified Ramsey model uncertainty

with delay introduced by (34) and (35). We want to minimize the investment capital under the above assumptions, by the following cost function

The idea is to get our capital in the future at time closer to with minimal energy, with as a random variable.

5.1 Optimization problem

To solve our optimal control, we connect its HJB with a G-FBSDDE that we solve numerically. In fact, the condition of quasi-continuity is not required for random variables and processes in [25].

As a result, see [25] may be applied to practical situations that are not in quasi-continuous spaces. We assume some independence among components of G-Brownian motion in the framework of super-linear expectation and derive an obvious type of HJB equation with a vector-valued control variable. It can be observed that the result in the next provides an application of stochastic control and the uncertainty volatility model.

Let define , as a -valued stochastic processes from the space , and the norm defined by

(36)

with C-continuous paths.

The gradient at is an -tuple of finite Borel measures on . Let define

(37)

with is a total

variation norm and define

where

is a vector in which represent the

masse at point of the component of , such that we have the following continuous map on for every

(38)

for more details see [12].

Then the value function define by

(39)

Then, the HJB equation given by

(40)

where is a control variable is selected dynamically within .

In this section, we present numerical results for G-FBSDE with delay (46) based on a variant of the least-squares Monte Carlo algorithm proposed in [4]. It comprises two phases, as do most numerical methods for G-FBSDE:

•

The explicit time discretization of G-FBSDE with delay.

•

The approach for approximation of conditional expectations.

First, for the time discretization, we consider a partition of the

interval as , , ···.

For the pair We motivate a natural time discretization that

goes backward in time. Defining for , we have

(47)

where

By taking a conditional expectation on both sides of G-BSDE in (47) to get an approximation of , given from the joint process which is adapted to the filtration generated by , and by using the property of symmetric martingale, we obtain that

Let use the value of to get .

By least square method [19],

(49)

iterates through all measurable functions with .

Finally, we get that

(50)

By using for some , where is the coefficients of the basis . By least-square method

(51)

where

then, we get that

is the solution to the least-squares problem (51), and for further information (see [18]).

In order to solve the forward G-SDDE, we have first to simulate the increment of the G-Brownian motion, for this later we use the same approach provided on [34] to simulate the density (resp. distribution) of the G-Normal BM by employing the finite difference method to simulate its corresponding G-PDE.

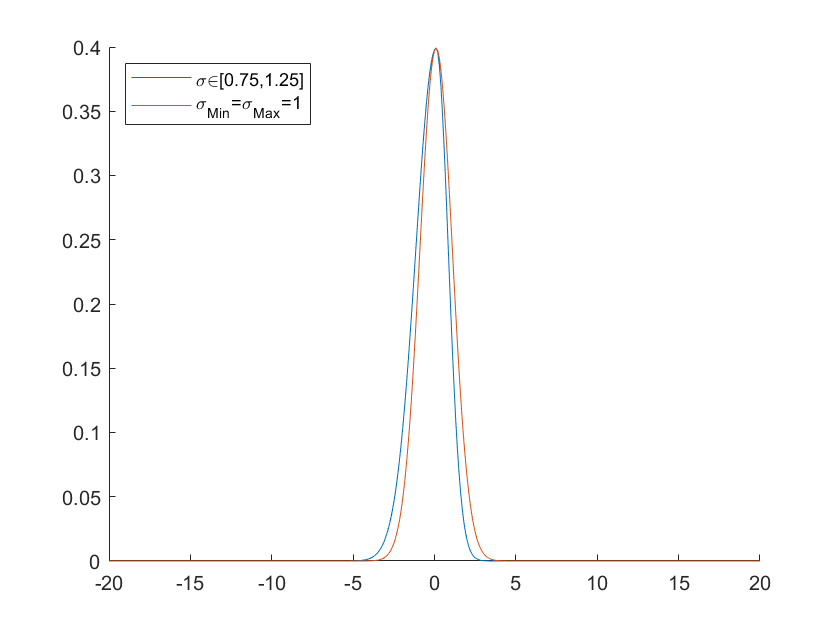

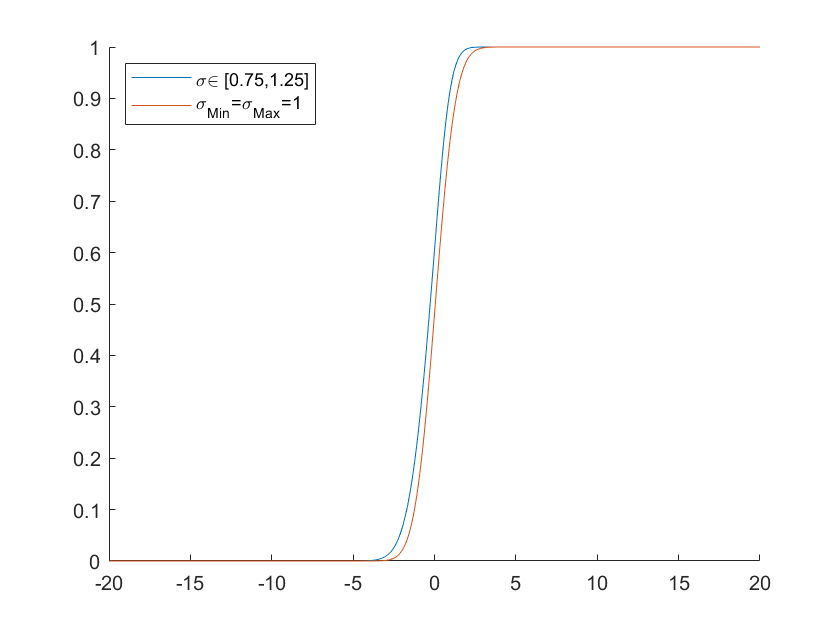

The simulated result in Figure 1 (resp. Figure 2) illustrate the G-Normal density (resp. distribution) with and .

Figure 1: The G-Normal density for and the standard normal density.Figure 2: The G-Normal-distribution for and the standard normal density.

Concerning the choice of the parameters, we take the value of and . We take the value of in the interval are uniform random values in the interval For this choice of coefficients and data, we obtain the following simulation result:

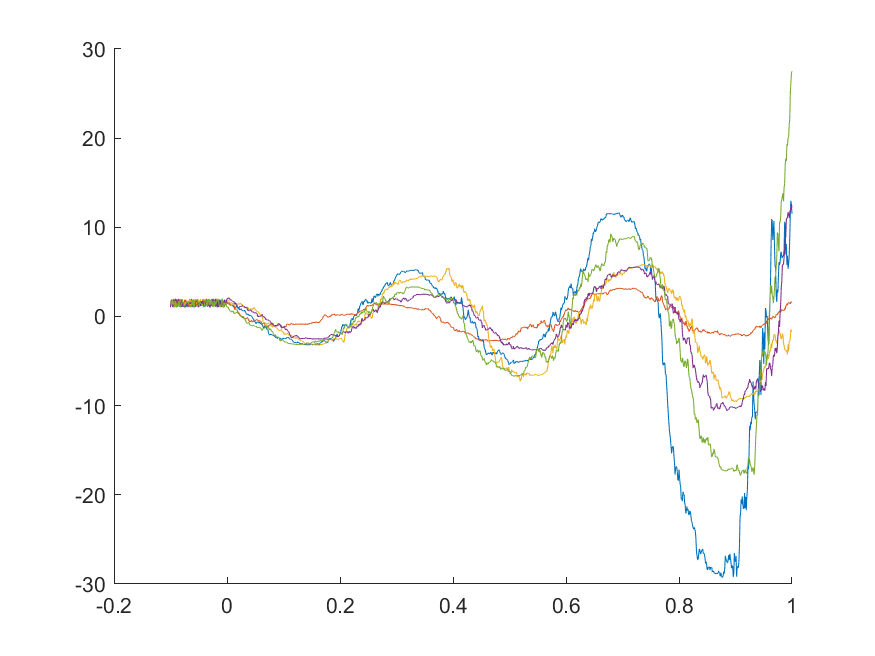

Figure 3, shows that the trajectories of the solution of the G-FSDDE corresponding to

Figure 3: The solution of the G-FSDDE.

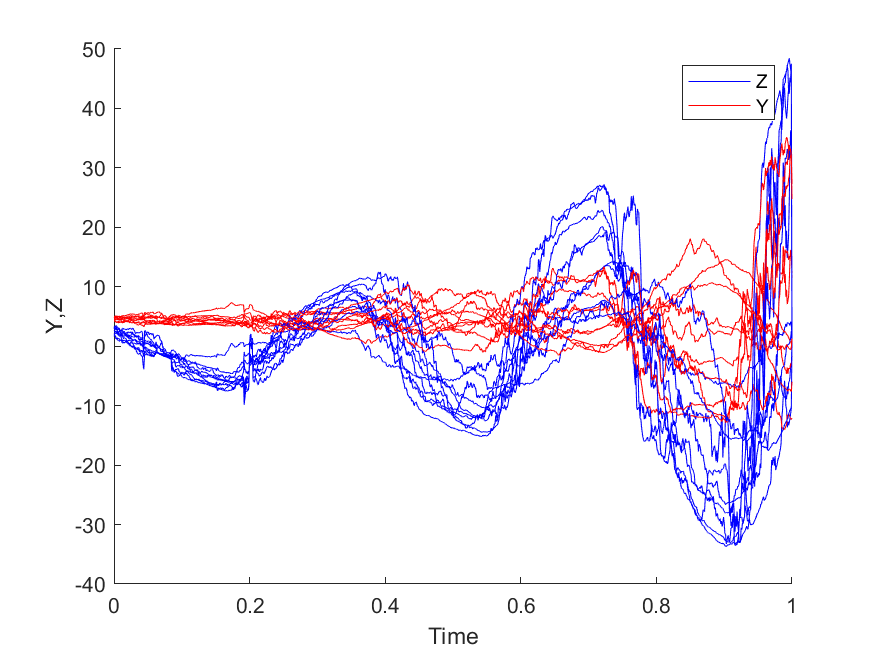

In Figure 4, we represent the trajectories of the solution of the G-BSDDE. According to a least-square Monte Carlo scheme and based on the Euler discretization.

Figure 4: The solution of the G-BSDDE.

The simulation of G-FBSDDE gives us the value of Y at initial time , which represents the optimal cost of our optimal control.

Acknowledgements

The author’s knowledge of the funding of the ERASMUS KA107 project

- Omar Kebiri knowledge of the funding of the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) under Germany’s Excellence Strategy. The Berlin Mathematics Research Center MATH+ (EXC-2046/1, project ID: 390685689), project EF4-6.

References

[1]

Nacira Agram and Bernt Øksendal.

Infinite horizon optimal control of forward-backward stochastic

differential equations with delay.

Journal of Computational and Applied Mathematics, 259:336–349,

2014.

[2]

Seïd Bahlali, Brahim Mezerdi, and Boualem Djehiche.

Approximation and optimality necessary conditions in relaxed

stochastic control problems.

Journal of Applied Mathematics and Stochastic Analysis, 2006,

2006.

[3]

Krishnan Balachandran.

Existence of optimal control for non-linear multiple-delay systems.

International Journal of Control, 49(3):769–775, 1989.

[4]

Christian Bender and Jessica Steiner.

Least-squares monte carlo for backward sdes.

Springer, 2012.

[5]

Francesca Biagini, Thilo Meyer-Brandis, Bernt Øksendal, and Krzysztof Paczka.

Optimal control with delayed information flow of systems driven by

G-Brownian motion.

Probability, Uncertainty and Quantitative Risk, 3(1):1–24,

2018.

[6]

Laurent Denis, Mingshang Hu, and Shige Peng.

Function spaces and capacity related to a sublinear expectation:

application to G-Brownian motion paths.

Potential analysis, 34:139–161, 2011.

[7]

Laurent Denis and Claude Martini.

A theoretical framework for the pricing of contingent claims in the

presence of model uncertainty.

The Annals of Applied Probability, 16(2):827–852, 2006.

[8]

Nabil Elgroud, Hacene Boutabia, Amel Redjil, and Omar Kebiri.

Existence of relaxed optimal control for G-neutral stochastic

functional differential equations with uncontrolled diffusion.

Bulletin of the Institute of Mathematics Academia Sinica,

17(2):143–172, 2022.

[9]

Ismail Elsanosi, Bernt Øksendal, and Agnes Sulem.

Some solvable stochastic control problems with delay.

Stochastics: An International Journal of Probability and

Stochastic Processes, 71(1-2):69–89, 2000.

[10]

Chen Fei, Wei-yin Fei, and Li-tan Yan.

Existence and stability of solutions to highly nonlinear stochastic

differential delay equations driven by G-Brownian motion.

Applied Mathematics-A Journal of Chinese Universities,

34(2):184–204, 2019.

[11]

Wendell H Fleming and Makiko Nisio.

On stochastic relaxed control for partially observed diffusions.

Nagoya Mathematical Journal, 93:71–108, 1984.

[12]

Marco Fuhrman, Federica Masiero, and Gianmario Tessitore.

Stochastic equations with delay: Optimal control via bsdes and

regular solutions of hamilton–jacobi–bellman equations.

SIAM Journal on Control and Optimization, 48(7):4624–4651,

2010.

[13]

Fuqing Gao.

Pathwise properties and homeomorphic flows for stochastic

differential equations driven by G-Brownian motion.

Stochastic Processes and their Applications,

119(10):3356–3382, 2009.

[14]

Carsten Hartmann, Ralf Banisch, Marco Sarich, Tomasz Badowski, and Christof

Schütte.

Characterization of rare events in molecular dynamics.

Entropy, 16(1):350–376, 2013.

[15]

Mingshang Hu, Shaolin Ji, and Shuzhen Yang.

A stochastic recursive optimal control problem under the

G-expectation framework.

Applied Mathematics & Optimization, 70(2):253–278, 2014.

[16]

Mingshang Hu and Falei Wang.

Stochastic optimal control problem with infinite horizon driven by

G-Brownian motion.

ESAIM: Control, Optimisation and Calculus of Variations,

24(2):873–899, 2018.

[17]

Anatoli F Ivanov and Anatoly V Swishchuk.

Optimal control of stochastic differential delay equations with

application in economics.

International Journal of Qualitative Theory of Differential

Equations and Applications, 2(2):201–213, 2008.

[18]

Omar Kebiri, Lara Neureither, and Carsten Hartmann.

Singularly perturbed forward-backward stochastic differential

equations: application to the optimal control of bilinear systems.

Computation, 6(3):41, 2018.

[19]

Omar Kebiri, Lara Neureither, and Carsten Hartmann.

Adaptive importance sampling with forward-backward stochastic

differential equations.

In Stochastic Dynamics Out of Equilibrium: Institut Henri

Poincaré, Paris, France, 2017, pages 265–281. Springer, 2019.

[20]

Mahmoud BA Mansour and Asmaa H Abobakr.

Stochastic differential equation models for tumor population growth.

Chaos, Solitons & Fractals, 164:112738, 2022.

[21]

Olivier Menoukeu Pamen.

Optimal control for stochastic delay systems under model uncertainty:

a stochastic differential game approach.

Journal of Optimization Theory and Applications, 167:998–1031,

2015.

[22]

Bernt Øksendal, Agnes Sulem, and Tusheng Zhang.

Optimal control of stochastic delay equations and time-advanced

backward stochastic differential equations.

Advances in Applied Probability, 43(2):572–596, 2011.

[23]

NK Patel, PC Das, and SS Prabhu.

Optimal control of systems described by delay differential equations.

International Journal of Control, 36(2):303–311, 1982.

[24]

Shige Peng.

G-expectation, G-Brownian motion and related

stochastic calculus of itô type.

In Stochastic Analysis and Applications: The Abel Symposium

2005, pages 541–567. Springer, 2007.

[25]

Shige Peng.

Nonlinear expectations and stochastic calculus under uncertainty.

arXiv preprint arXiv:1002.4546, 24, 2010.

[26]

Amel Redjil and Salah Eddine Choutri.

On relaxed stochastic optimal control for stochastic differential

equations driven by G-Brownian motion.

ALEA, Lat.Am. J. Probab. Math. Stat, 15:201–212, 2018.

[27]

Yong Ren, Jun Wang, and Lanying Hu.

Multi-valued stochastic differential equations driven by

G-Brownian motion and related stochastic control problems.

International Journal of Control, 90(5):1132–1154, 2017.

[28]

Yong Ren, Wensheng Yin, and Rathinasamy Sakthivel.

Stabilization of stochastic differential equations driven by

G-Brownian motion with feedback control based on discrete-time

state observation.

Automatica, 95:146–151, 2018.

[29]

Javier F Rosenblueth.

Strongly and weakly relaxed controls for time delay systems.

SIAM journal on control and optimization, 30(4):856–866, 1992.

[30]

H Mete Soner, Nizar Touzi, and Jianfeng Zhang.

Martingale representation theorem for the G-expectation.

Stochastic Processes and their Applications, 121(2):265–287,

2011.

[31]

Mete Soner, Nizar Touzi, and Jianfeng Zhang.

Quasi-sure stochastic analysis through aggregation.

Electronic Journal of Probability, 16:1844–1879, 2011.

[32]

George Stoica.

A stochastic delay financial model.

Proceedings of the American Mathematical Society,

133(6):1837–1841, 2004.

[33]

Yuhong Xu.

Backward stochastic differential equations under super linear

G-expectation and associated hamilton-jacobi-bellman equations.

arXiv preprint arXiv:1009.1042, 2010.

[34]

Jie Yang and Weidong Zhao.

Numerical simulations for G-Brownian motion.

Frontiers of Mathematics in China, 11:1625–1643, 2016.

[35]

Wensheng Yin, Jinde Cao, and Guoqiang Zheng.

Further results on stabilization of stochastic differential equations

with delayed feedback control under -expectation framework.

Discrete and Continuous Dynamical Systems-B, 27(2):883–901,

2022.

[36]

Haiyan Yuan.

Some properties of numerical solutions for semilinear stochastic

delay differential equations driven by G-Brownian motion.

Mathematical Problems in Engineering, 2021:1–26, 2021.