The inverse Black-Scholes problem in Radon measures space revisited: towards a new measure of market uncertainty

Abstract

In this paper, we revisit the inverse Black-Scholes model, the existence of the solution is proved in more rigorous way, and the empirical study is done using different approach based on finite element method.

The article leads to a measure of incertitude in the option market.

† Université Mohammed V de Rabat, Maroc111nizar.riane@gmail.com

‡ Sorbonne Université

CNRS, UMR 7598, Laboratoire Jacques-Louis Lions, 4, place Jussieu 75005, Paris, France222Claire.David@Sorbonne-Universite.fr

Keywords: Black-Scholes equation - fractal differential equations - inverse problem - finite elements.

AMS Classification: 37F20- 28A80-05C63-91G50.

1 Introduction

In 1997, R. Merton and M. Scholes for their works, in particular, the Black-Scholes model [BS73], which continue to be a reference for the option pricing.

Despite the genius behind this construction, the model present many weaknesses when he confront the data, in particular, when the model underprices the option out of the money, and overprices in the money [GFS99].

Another weakness of the model is that consider that the market to be isotropic in physicians terminology, while the option price can be affected by incertitude about the future, leading to anisotropic reactions.

In [RD20b], [RD21b], we introduced an upgraded version of this model, satisfying the economic foundations of finance and taking into account an important market factor : incertitude.

In this paper, we revisit the inverse Black-Scholes model, as presented in [RD20b], we give a more rigorous justification of the existence of the solution, and we fit the data using different approach based on finite element method.

At the end of this work, we will prove that the measure based Black-Scholes model is a better candidate to fit financial data, in addition, we will get an interpretation in terms of market incertitude.

2 The measure based Black-Scholes formula

Next, we will refer to the following functional spaces:

Notations (Sobolev spaces).

Given a strictly positive integer , a subset of , , and , we recall that the classical Sobolev spaces on are:

and:

The subspace of functions which vanish on is:

The measure based Black-Scholes model was introduced in [RD21b] in the following variational form:

where represents the volatility, the risk-free interest rate, the maturity of the option and the option price. The underlying asset price is supposed to be bounded by some strictly positive number .

We suppose the measure to be any finite Radon measure supported in and satisfies the following assumptions

Assumption 2.1.

There exists two strictly positive constant and such that:

where denote the space of test functions on , i.e. the space of smooth functions with compact support in .

Remark 2.1.

We proved In [RD21b] the first assumption for all finite Radon measures, and we proved the second assumption for all absolute continuous measures with respect to the Lebesgue one.

We recall the following restrictions on the parameters and to ensure existence and uniqueness results:

Assumption 2.2.

-

1.

The risk-free interest rate is bounded on :

-

2.

There exist two positive constants, and , such that:

-

3.

There exists a positive constant such that:

The existence and uniqueness of the solution proof can be found in [RD20b].

Notations.

Set:

The dual space of will be denoted by .

Proposition 2.3 (Poincaré’s inequality ).

The space is dense in , and, for any , the following inequality is satisfied:

This inequality induces a second norm on , given, for any in , by:

Proposition 2.4.

(Continuity and Gårding inequality) [AP05]

The bilinear form is continuous on , and satisfies the Gårding inequality:

where denotes a strictly positive constant.

Remark 2.2.

Given in , we use the transformation trick [Zei90]:

for the Gårding constant and at stake in the second conjecture 2.1. Then:

Without affecting the solution spaces, one obtains the continuity and the coercivity of the form :

and:

The following result follows directly from [Zei90].

Theorem 2.5 (Measure based Black-Scholes weak solution).

Let us define the Gelfand triple (or equipped Hilbert space) . For in , the measure based Black-Scholes problem admits a unique weak solution. Moreover, for , the solution map:

is continuous.

Theorem 2.6.

Regularity

We have the estimate, for :

Proof.

Using the remark before by setting and integrating the variational formula between and :

The last inequality follows from the second assumption. ∎

Theorem 2.7.

Regularity

For , we have the estimate:

Proof.

Using the transformation :

leading to the differential form

By Gronwall lemma

Back to the original form:

∎

Theorem 2.8.

Maximum principle

If then -almost everywhere on .

Proof.

Set . We use Stampacchia truncation [Bre83] : Let such that

-

1.

, for some constant .

-

2.

is increasing on .

-

3.

for .

Define, for , the function

Set to be

Then

and

Take , the positive part, then

Which means that , then -almost everywhere on .

∎

3 The inverse problem

For normalization purpose, we restrict ourselves to finite Radon measure with total mass equals to , this enable ones to take into account the classical Black-Scholes model. For simplicity, we consider probability measures on , then we multiply by the constant to get .

Definition 3.1 (Inverse problem).

We recall the inverse problem as defined in [RD21b], which consists in finding the measure associated with the Black-Scholes equation, given a very small parameter , and a noisy measure of the solution of the solution such that:

Notation.

We denote by (respectively ) the space of finite Radon (resp. probability) measures on , and by the space of (uniformly) continuous functions on .

Proposition 3.1.

[BP13]

The space of finite Radon measures equipped with the total variation norm :

is complete and separable, and is also the dual space of :

Definition 3.2.

A sequence of measures converges in the weak sense ⋆ towards a measure if and only if

Moreover, every bounded sequence in has a weak ⋆ convergent subsequence.

Remark 3.1 ([BP13]).

For , let be an open non-empty subset. Then:

-

i.

the space of all finite linear combinations of -peaks

-

ii.

the space , equipped with the injection , for the Lebesgue measure ,

are weakly⋆ dense subsets of .

Proposition 3.2.

The space of probability measures equipped with the Prokhorov metric :

where

and is the Borel -algebra on , is a compact metric space for the weak⋆ topology.

Remark 3.2.

For normalization purpose, we restrict ourselves to the space , since the total measure of with respect to Lebesgue measure is . Writing for , this space inherit the properties of the space of probability measures .

Notation.

In the spirit of [BP13], we introduce the solution operator of the measure based Black-Scholes problem

Notations.

Given two probability measures and in , we introduce the respective solutions , , of:

and:

Remark 3.3.

-

1.

Non linearity: for any in :

Then implies

Choose

Integrate between ant :

Moreover, for

Multiply the identity for by

Clearly and the related operator is thus not linear.

-

2.

Weak⋆-strong Continuity: for a sequence of probability measures converging towards a given one , it follows from the regularity of the solutions that the sequences and are bounded. Set and :

Subtracting the inequalities defining and for , and set

Then

Equivalently

Since is bounded in and , then it is bounded in , for all , it follows from Cauchy-Schwartz inequality and the definition of that is a Cauchy sequence in and then converges to a limit .

Definition 3.3 (Tikhonov regularized solution).

The Tikhonov minimization problem is the solution of

where denotes the regularization parameter.

Theorem 3.3.

Thikhonov regularized problem admit a solution.

Proof.

The operator is weak⋆-strong continuous, so is Tikhonov functional from composition properties. Since the space is compact for the weak⋆ topology, the result follows.

∎

4 Finite element

In [RD21b], we solved the inverse measure problem using the finite difference technique, based on our articles [RD19], [RD20a] and [RD21a].

In order to construct a finite element approximation, we need to recall the weak form of measure based Black-Scholes equation:

where is the non-symmetric bilinear form defined, for any pair of , through:

We will proceed as in [Mau07] :

4.1 elements

Notation.

For , we introduce the uniform subdivision of the set into equidistant points , :

for .

Definition 4.1 (Finite element basis functions [All07]).

Define the vector space

the space of piecewise linear finite element basis functions where are given by

Using the same approach to establish the existence and uniqueness of the solution in , we can establish the following result:

Property 4.1 (Finite element approximation).

The variational problem

has a unique solution in .

Write the approximated solution as

for . The variational formula can be transformed to

Set, for :

More precisely

and

We impose the limit conditions and . The problem satisfies then the dynamic

where, for ,

4.2 Convergence and error estimate

Let proceed without affecting the solution spaces, as in the remark of the first section by setting and , where is the solution of the transformed problem

The bilinear form , satisfies continuity and coercivity:

J. L. Lions and E. Magenes theory [LM68] implies the existence and uniqueness of the solution for the approximated problem.

We use the decomposition to consider the homogeneous part .

Define the projector by

Lemma 4.2.

There is a constant independent of such that, for all

Proof.

Let . For :

for and . We get from Cauchy-Schwartz inequality

integrating over and summing

The result follows then by density.

∎

It follows the following theorem

Theorem 4.3.

Let and be respectively, the solution and the finite element approximation of the measure based Black-Scholes equation. Then the finite element method converges.

In addition, if , then there exist a constant , independent of , such that

Proof.

It suffice to resonate in terms of the transformed problem.

Consider the variational inequalities involving and , by taking

subtract the two inequalities and define the error , this yield to the the formula

It follows from coercivity and continuity of that

for some constant . Using the regularity solution estimate, the first assumptions and the lemma before, we get for

∎

We deduce from the existence and uniqueness of the transformed solution, the existence and uniqueness of the original one, and then it’s finite element approximation.

4.3 Discretization of the Tikhonov problem

Given , , and , we denote by the finite element approximation of the solution . The coefficient vector follows the differential system

as stated before. Define the approximation measure as a Dirac linear combination

for , which is dense in . The matrix simplifies to a diagonal matrix

Now consider an empirical measure of the solution, we introduce the finite element approximation operator , such that:

This construction justify the discretized Tikhonov problem:

Definition 4.2 (Discretized Tikhonov problem).

We define the discretized Tykhonov problem as

where .

Theorem 4.4.

The discretized Tikhonov minimization problem admits a unique solution .

Proof.

The existence follows from the continuity of , which follows from the continuous dependence of the solution of the linear differential system

to the matrix (continuity of the exponential), combined with the form of

where , is the finite element basis. The uniqueness follows by strict convexity of Tikhonov functional and the exponential. ∎

4.4 Empirical results

To confront our theory to reality, we will establish comparison the classical and the measure based Black-Scholes models, based on their adjustment qualities of financial data. For this purpose, we used a sub-sample of data from Vance L. Martin [LMM05]. The sample consist of observations on the European call options written on the SP stock index on the of April, , we refer to [RD21b] for detailed description.

We recall the main characteristics of these options:

-

ii.

The strike : .

-

iii.

The maturity : .

-

v.

The interest rate : .

-

vi.

The volatility : .

The table 2 gives the data range for the option and the stock index prices:

| Statistic | Option price | Stock price |

|---|---|---|

| Max | ||

| Min | ||

| Mean |

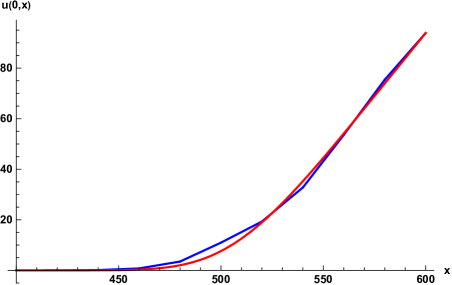

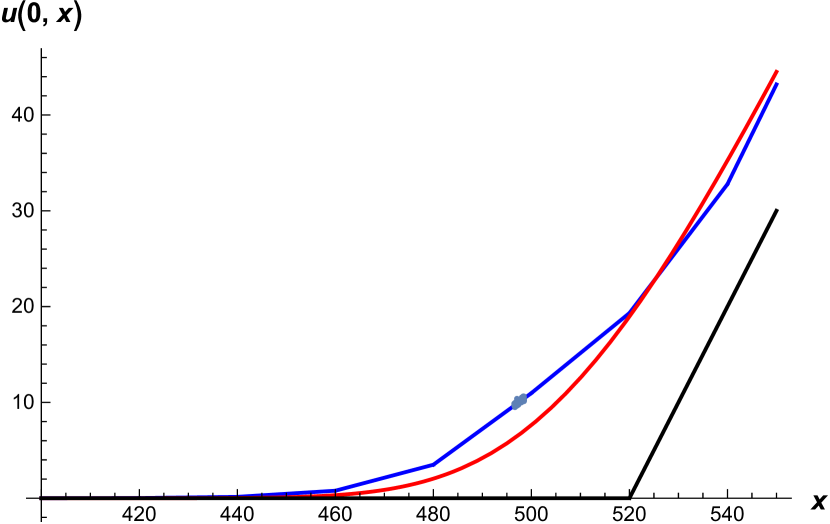

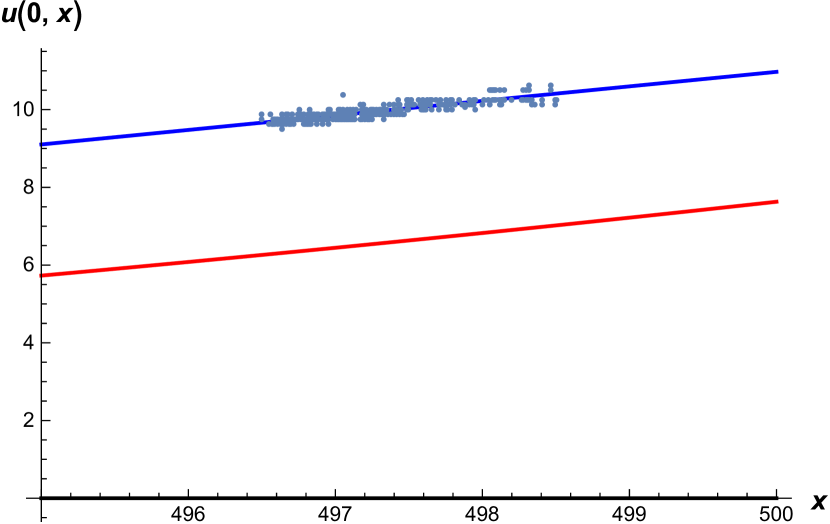

Next, we represent the classical solution versus the measure based one. The approximation parameter is fixed to :

To evaluate the adjustment quality of the measure based model, we plot the two models versus the scatter plot of the data:

The measure based model offer a much better approximation of the solution, which can be measured by Tikhonov functional:

| Classical BS | Measure based BS | |

|---|---|---|

| Tikhonov functional |

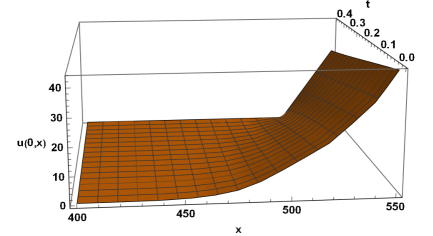

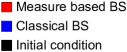

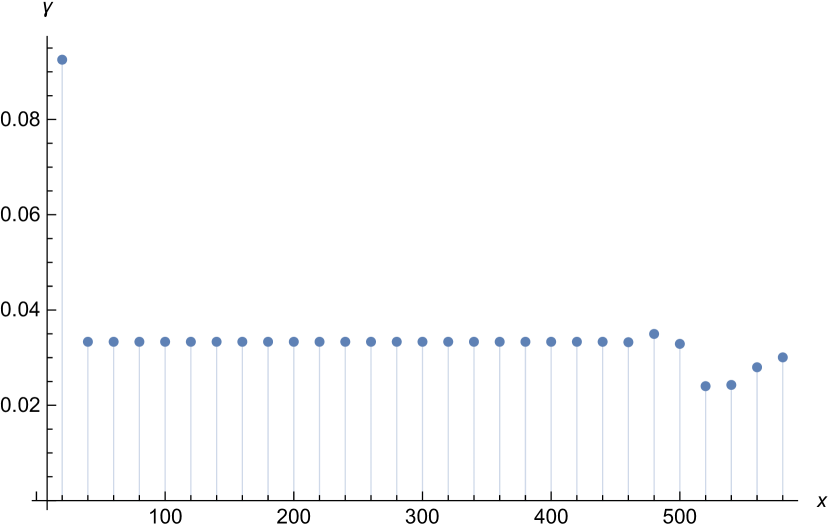

We represent the parameters in terms of a probability density function. To focus on those belonging to the data region, we will use an adaptive mesh:

We remark that the parameters grows up entering the data region before they start decreasing. A quick look at the solution dynamic equation, shows as that the represent the market rigidity : higher is more stable is the call price at the value , we can see that the origin represent the most stable price (no one expect the price to vary there) and the region present more confidence in the market. Moreover, the parameters are much smaller than the classical model, except the origin, proving that the classical model represent an isotropic market with uniform uncertainty distribution.

5 Discussion

The results established in this work demonstrate the superiority of the measure based Black-Scholes model in term of market data fit, while the classical model underestimate the option price.

The measure based Black-scholes offer a new information on the market consisting in the measure which can be interpreted as a market confidence measure : by considering the probability version , the parameter represent the option price rigidity at the stock price , higher is more stable is the option price.

One remarkable fact is the parameters for the estimated model are lower than the uniform case of the Black-Scholes model, reflecting more instability in the market than the classical theory predict.

The model based on the measure open a new field of research by quantifying the market confidence (in opposition with market incertitude) : reflect the market confidence at the stock price , inducing more rigidity and a slow change in the option price. This is just a measure of incertitude in the market, which was considered to be unmeasurable.

References

- [All07] G. Allaire. Conception optimale de structures. Springer, 2007.

- [AP05] Y. Achdou and O. Pironneau. Computational Methods for Option Pricing. Society for Industrial and Applied Mathematics, 2005.

- [BP13] K. Bredies and H. K. Pikkarainen. Inverse problems in spaces of measures. ESAIM: Control, Optimisation and Calculus of Variations, 19:190–218, 2013.

- [Bre83] H. Brezis. Analyse fonctionnelle : théorie et applications. Éditions Masson, 1983.

- [BS73] F. Black and M. Scholes. The pricing of options and corporate liabilities. The Journal of Political Economy, 81:637–654, 1973.

- [GFS99] R. C. Stapleton G. Franke and M. G. Subrahmanyam. When are options overpriced? the black–scholes model and alternative characterisations of the pricing kernel. European Finance Review, 3:79–102, 1999.

- [LM68] J. L. Lions and E. Magenes. Problèmes aux limites non homogènes et applications. Dunod, 1968.

- [LMM05] G. C. Lim, G. M. Martin, and V. L. Martin. Parametric pricing of higher order moments in s&p500 options. Journal of Applied Econometrics, 20(3):377–404, 2005.

- [Mau07] Karin Mautner. Numerical treatment of the black-scholes variational inequality in computational finance. 2007.

- [RD19] N. Riane and C. David. The finite difference method for the heat equation on sierpiński simplices. International Journal of Computer Mathematics, 96(7):1477–1501, 2019.

- [RD20a] N. Riane and C. David. Sierpiński gasket versus arrowhead curve. Communications in Nonlinear Science and Numerical Simulation, 89:105311, 2020.

- [RD20b] N. Riane and Cl. David. Towards the self-similar Black-Scholes equation, 2020.

- [RD21a] N. Riane and C. David. The finite volume method on sierpiński simplices. Communications in Nonlinear Science and Numerical Simulation, 92:105468, 2021.

- [RD21b] N. Riane and Cl. David. An inverse Black-Scholes problem. Optimization and Engineering, 2021.

- [Zei90] E. Zeidler. Nonlinear functional analysis and its applications. II/A. : Linear monotone operators. Springer, 1990.