Coarse correlated equilibria for continuous time mean field games in open loop strategies

Abstract

In the framework of continuous time symmetric stochastic differential games in open loop strategies, we introduce a generalization of mean field game solution, called coarse correlated solution. This can be seen as the analogue of a coarse correlated equilibrium in the -player game. We justify our definition by showing that a coarse correlated solution for the mean field game induces a sequence of approximate coarse correlated equilibria with vanishing error for the underlying -player games. Existence of coarse correlated solutions for the mean field game is proved by a minimax theorem. An example with explicit solutions is discussed as well.

Keywords: Mean field games, coarse correlated equilibria, open loop strategies, minimax theorem, relaxed controls, propagation of chaos.

1 Introduction

Coarse correlated equilibria are a concept of equilibria for games with many players which allows for correlation between players’ strategies, thus generalizing the notion of Nash equilibria. In this paper, we propose a notion of coarse correlated equilibria for a class of continuous time symmetric stochastic differential games and study the corresponding mean field formulation as the number of players goes to infinity.

Mean field games (MFGs) have been an active theme of research for almost two decades, started in the mid 2000’s from the seminal works of Lasry and Lions [32] and of Huang, Malhamé and Caines [24]. Roughly speaking, MFGs arise as the limit formulation of symmetric stochastic -player games with mean field interactions between the players. Thanks to the mean field interaction and propagation of chaos type results, one expects that the empirical distribution of players’ states converges to the law of some representative player. In the limit, the concept of Nash equilibrium translates into a fixed point problem in the space of flows of measures. For a probabilistic approach to MFGs, we refer to the two-volume book by Carmona and Delarue [13]. The relation between the MFG and the -player game is commonly understood in two ways: on the one hand, a solution of the MFG allows to construct approximate Nash equilibria for the corresponding -player games, if is sufficiently large, see, e.g., [9, 12, 16, 24]. On the other hand, approximate Nash equilibria can be shown to converge to solutions of the corresponding MFG. The choice of admissible strategies, while always important, is crucial for results of this kind: see [19, 29] for earlier results in open loop strategies and Cardaliaguet et al. [11], Lacker [30], and Lacker and Le Flem [31] for convergence in closed loop strategies.

The notion of coarse correlated equilibrium (CCE) makes its first appearances implicitly in Hannan’s work [20] and explicitly in Moulin’s and Vial’s [35]. The idea of CCEs can be summarized as follows: The game includes a correlation device or a mediator, who picks a strategy profile randomly according to some probability distribution over the set of strategy profiles, which is assumed to be common knowledge among the players. Each player must decide whether to commit or not to the strategies selected for her by the mediator before the mediator runs the lottery. If a player deviates, she will do so without any information on the outcome of the lottery. If a player commits, the mediator informs her of her own recommendation, without revealing the recommendation to any other player. In equilibrium, it is best to commit to the anticipated outcome of the lottery if one believes that every other player is doing the same. This notion of equilibrium is weaker than that of correlated equilibrium (CE) à la Aumann (see [1, 2]), where players decide whether to accept the mediator’s recommendation after having been informed (in private) of the strategies extracted for them. When the distribution used by the mediator is a product distribution, CCEs reduce to usual Nash equilibria in mixed strategies, because in this case the mediator’s recommendations do not carry any additional information over what is common knowledge. Among the nice features of CCEs, we notice the fact that they may lead to higher payoffs than Nash equilibria, even when true CEs do not exist (see Moulin et al. [34, 33] for an example in a two-person static linear quadratic game), and they naturally arise from a learning procedure of the players, such as the so called regret-based dynamics (see, e.g., Hart and Mas-Colell [21] and Roughgarden [42, Section 17.4]).

Recently, correlation between players’ strategy choices has been considered in the context of mean field games. Bonesini, Campi and Fischer [6, 10] establish the existence of symmetric CEs in a class of symmetric games with discrete time and finite state and action spaces, give a definition of CE in the mean field limit and provide both approximation and convergence results. As usual, the mean field interaction in the -player game is modeled via the empirical measure of players’ private states. In the mean field limit, they propose a notion of correlated MFG solution, which is defined as a probability distribution over all the pairs of strategies and flows of measures. Remarkably, the flow of measures is naturally stochastic, as the aggregation of individual behaviours preserves the stochasticity of the correlation device. In a second group of papers by Müller et al. [36, 37], notions of both CCEs and CEs are studied for a class of symmetric games with discrete time, finite states and finite actions, in a setting close to the one in [6, 10]. Interestingly, they propose a different definition of CE for the mean field game from that in [6, 10], and in [36] the authors discuss on how the two definitions of CE can be seen as equivalent. In addition, [36, 37] contain an extensive discussion of learning algorithms for approximating Nash equilibria, CEs and CCEs in the mean field limit. Finally, [8] introduces the notion of CCEs in a class of continuous time linear quadratic MFGs. A methodology to compute CCEs in such class of MFGs is provided, and, through the study of a simple yet important example with applications in environmental economics, the authors show that there exist infinitely many CCEs for the MFG which both yield higher payoffs than the classical MFG solutions and are more efficient with respect to the environmental goals, highlighting the benefits provided by CCEs over MFGs solutions.

In this work, we consider MFGs with general dependence on the flow of measures, and we deal both with existence of CCEs in the MFG and the relation between CCEs in the -player game and in the MFG. In the -player game, the state dynamics follow stochastic differential equations (SDEs), driven by independent standard Brownian motions representing additive idiosyncratic noise, and the interaction between players is given through the empirical distribution of their states, which appears both in the drift of the SDEs and in each player’s payoff functional. Players’ strategies are assumed to be open loop, i.e., the correlation device would recommend the players to use strategies adapted to the filtration generated by noises and initial data. More precisely, the correlation device, or recommendation to the players, is modeled as a random variable taking values in the set of open loop strategy profiles; we require it to be independent of the random shocks and the initial states which determine players’ states’ evolution. We deal very carefully with the measurability properties the recommendation has to fulfill so that the players’ states are well-defined and the recommended strategies are implementable by the players. In the mean field limit, the notion of coarse correlated solution we present corresponds to a pair given by a recommendation with values in the set of open loop strategies for the representative player and a random flow of measures fulfilling the following two properties:

-

–

Optimality: the representative player has no incentive to deviate from the recommended strategy before the extraction has happened.

-

–

Consistency: the flow of measures at any time equals the marginal law of the representative player’s state conditioned on the -algebra generated by the whole flow of measures up to terminal time.

Through the study of a simple example, our notion of coarse correlated solution to the MFG is compared to the more usual notion of MFG solution, (as defined, e.g., in [12]) and the notion of weak MFG solution of [29]. Our main contributions are as follows:

-

–

We justify our notion of coarse correlated solution for the MFG by showing that any coarse correlated solution for the MFG induces a sequence of approximate CCEs in the -player game, with vanishing error as goes to infinity.

-

–

Under an additional convexity assumption, we prove the existence of a coarse correlated solution for the mean field game.

Both results will be established using a genuinely probabilistic approach. As for the approximation result, we use the limit flow of measures to act as a correlation device between players’ strategies in the -player game, in the same spirit of [6, 10]. Then, the proof of the inverse convergence relies on propagation of chaos arguments, which are in part reminiscent of [12, 16]. On the other hand, to prove existence, we associate a zero-sum game to the search of a coarse correlated solution for the MFG, inspired by the works of Hart and Schmeilder [22] (for static games), Nowak [38, 39] (for continuous time dynamic games) and Bonesini [5, Appendix 1.B] (for mean field games with discrete time and finite states and actions, in the setting of [10]), which require us to apply a minimax theorem. To do so, compactness arguments are exploited, adapting some of the techniques used in Lacker’s works [28, 30].

The rest of the paper is organised as follows: in Section 2 we collect some notations and state the main assumptions, which will be in force throughout the whole paper. In Section 3, we define the -player game and present a notion of CCE; coarse correlated solutions for the MFG are defined in Section 4. The approximation and existence results are presented in Sections 5 and 6, respectively. In Section 7, we consider a simple class of games, already discussed in the literature (see [3, 29, 30]): we show that it has coarse correlated solutions which are different from the classical MFG solution, and we compare them with the notions of solution of the previous literature. Finally, some auxiliary technical results are gathered in the Appendix.

2 Notations and standing assumptions

Here, we collect the most frequent notations that occur in this work and state the assumptions.

For a metric space , we denote by the Borel -algebra generated by the topology of . When the context allows, we will drop the dependence upon , and just denote it by . We denote by the set of continuous bounded function .

We will denote by the set of probability measures on . For , we denote by the set of probability measures so that, for some point , and thus for any, it holds . Let denote the -Wasserstein distance on , defined as

Any time we will be given two metric spaces and , we will regard as a metric space itself, with the distance . The -Wasserstein distance on will always be meant with respect to such distance on . For fixed, we denote by the set of continuous functions from in , , i.e. . We endow with the norm . Occasionally, we will use the semi-norm , for . We will denote as the law of a standard -dimensional Brownian motion, and by the set of continuous functions from in , i.e. , where is endowed with the -Wasserstein distance. We endow with the supremum distance , for any and in .

When given a filtered probability space , we regard as the -augmentation of the filtration the filtration , where and stands for the -null sets of . Such a filtration satisfies the usual assumptions.

We end this section by stating our standing assumptions on the state dynamics and on the costs of the players in both the -player game and the limit game. We are given a finite time horizon , a control actions space , an initial state distribution , and the following functions:

which will be referred to, respectively, as the drift function, the running cost and the terminal cost. The following Assumptions A will be in force throughout the whole manuscript.

Assumptions A.

-

(A.1)

, for some , is a compact set.

-

(A.2)

, for some .

-

(A.3)

The functions , and are jointly measurable in .

-

(A.4)

is Lipschitz in , and , uniformly in :

for every , and in .

-

(A.5)

The functions are bounded, for some .

-

(A.6)

and are locally Lipschitz in for every fixed with at most quadratic growth, i.e., there exists a positive constant so that

for every , and in .

3 Formulation of the -player game

Consider the following canonical space

| (3.1) |

We define a sequence of random variables and of Brownian motions , by taking the projections:

| (3.2) |

By definition of , and are mutually independent, are independent and identically distributed with law and are independent -dimensional standard Brownian motions.

Let , , be the number of players. We define the filtration as the -augmentation of the filtration generated by the first random variables and Brownian motions . Therefore, for the -player game, we work on the space

| (3.3) |

We stress that, for every , we keep the probability space fixed while the filtration varies.

Consider the set of -progressively measurable processes taking values in :

| (3.4) |

Provided that we identify processes which are equal -a.e., we can regard as

where stands for the progressive -algebra on , using the filtration . We call any element an open loop strategy for the -player game. We regard a vector as an open loop strategy profile for the players, which will be occasionally denoted by . We endow such a space with the norm

| (3.5) |

and consider the Borel -algebra associated to that. We observe that, since is Polish and is closed, is a separable Banach space. In the following, we will make no distinction between an -progressively measurable process and any other process which is equal to it -almost everywhere.

Definition 1 (Admissible recommendation profile and correlated strategy profile).

We call admissible recommendation profile to the players a pair so that the following holds:

-

1.

, is a complete probability space; is a Polish space and is its corresponding Borel -algebra.

-

2.

is a random vector with values in :

(3.6) -

3.

is admissible in the following sense: Let be the product space of and :

We complete the -algebra with the -null sets and endow the product probability space with the -augmentation of the filtration

Given an -valued random variable as in (3.6), we say that is admissible if there exists a process with values in , defined on and -progressively measurable, so that, for every , for -a.e. , the section is equal to in :

(3.7)

If is an admissible recommendation to the players, we write

| (3.8) |

where equality is to be understood in the sense of (3.7). We call correlated strategy profile associated to the admissible recommendation profile , the -progressively measurable process satisfying (3.8).

We remark that, by Proposition B.2, given any admissible recommendation to the players , the correlated strategy profile associated to it is unique -almost everywhere. We point out that in general, for instance when a recommendation profile takes uncountably many values, we cannot recover the progressive measurability property of the strategy associated to the recommendation . The essential reason is that we cannot deduce the measurability of a set in the product -algebra from the measurability of its sections, as shown, e.g., in [43, p. 5]. Therefore, the admissibility requirement on is necessary. Nevertheless, we give some examples of admissible recommendations in Example 1 in the following Section 4.

Remark 1.

As usual, we can extend random variables defined on to random variables defined on . Indeed, suppose is a random variable with values in some measurable space . We can then regard as defined on the space via the identification , and analogously for . In this sense, via the identification for every , we can regard the Brownian motions and initial data as defined on ; we observe that are independent standard Brownian motions with respect to the filtration as well. Moreover, we can identify each process , which is defined on , with a process defined on via the identification . Such a process is progressively measurable with respect to the filtration and independent of .

We interpret the admissible recommendation as follows: A correlation device or a mediator runs a lottery over open loop strategy profiles according to some publicly known distribution and communicates privately to each player a strategy according to the selected profile. The extraction of the strategy profile happens before the game starts and it is independent of the idiosyncratic shocks that determine the random evolution of players’ states. These features are captured by the construction of the underlying probability space as a product of , which contains the information used to correlate players’ strategies, and , where noises and open loop strategies are defined, and by the choice of the filtration , since for every . We stress that, by definition, the realization is an -progressively measurable process in , for any scenario and . Observe that, even though and are independent, the correlated strategy profile is in general not independent of either of them, since it is the result of both the recommendation profile and the random shocks and initial data.

Let be an admissible recommendation profile. On the space defined at point 3 of Definition 1, we assign players state dynamics and define the cost functionals. If all players follow the recommendation , players’ state dynamics are given by the following system of stochastic differential equations:

| (3.9) |

for every , where is the empirical measure of the state processes of all players at time :

| (3.10) |

Suppose player deviates, while the other players follow the recommendations they receive from the mediator. The deviating player will pick instead an open loop strategy . In other words, at every time and for every scenario , player plays the action instead of playing the recommended action . Then, players’ state dynamics are given by the following system of stochastic differential equations:

| (3.11) |

where is defined as in (3.10). Assumptions A ensure that there always exists an -adapted continuous solution to both equations (3.9) and (3.11) so that is finite. Moreover, pathwise uniqueness holds so that, by Theorem A.1, uniqueness in law holds as well.

Remark 2.

We notice that there is an asymmetry between the information available to the mediator and the deviating player: if a player deviates, she chooses her strategy on her own, ignoring the information contained in mediator’s recommendation, since, by definition of the process on the product space, deviating player’s strategy is independent of the recommendation profile . We can interpret player ’s deviation in the following way: either the player commits to the moderator ex-ante or she does not; if she does not, she will not exploit any of the additional information the mediator would give away when communicating the recommended strategies to the players.

As for the cost functional, let be an admissible recommendation profile. If all players follow the recommendation, then the cost functional of each player is given by

with dynamics given by (3.9). If instead player does not play according to the recommendation and plays a different strategy , while the other players stick to the recommendation profile , we define the cost functional of each player as

where the dynamics are given by (3.11). We stress that the expectation in the cost functional is taken with respect to the product probability measure , although we omit this dependence for conciseness. Finally, we give the notion of -coarse correlated equilibrium:

Definition 2 (-coarse correlated equilibrium).

Let . An admissible recommendation profile is an -coarse correlated equilibrium for the -player game (-CCE) if

| (3.12) |

for all open loop strategies and all players . We call an admissible recommendation profile a coarse correlated equilibrium for the -player game if it is an -coarse correlated equilibrium with .

The usual notion of Nash equilibrium in open loop strategies is consistent with the definition of coarse correlated equilibrium: Suppose we are given an -Nash equilibrium in open loop strategies. We choose as the trivial probability space and as constant and equal to . It is then straightforward to see that the triple is an -CCE according to Definition 2.

Notice that a Nash equilibrium in open loop strategies is -progressively measurable, while a correlated strategy profile associated to an admissible recommendation contains the information carried by itself, which is the information the mediator uses to randomize players’ strategies. Moreover, while in both cases the deviating player will use an open loop strategy, CCEs present a certain asymmetry between the information available to the mediator and the deviating player, as pointed out in Remark 2, while, when dealing with Nash equilibria, the deviating player has access to the same information of the other players, since they all use -progressively measurable strategies.

Remark 3 (Role of the probability space ).

According to Definition 1, the probability space is part of the definition of admissible recommendation. The natural interpretation is that the mediator chooses the auxiliary space he uses to correlate players’ strategies. Moreover, according to equations (3.9) and (3.11), it determines the probability space on which state processes are defined. In order to keep the notation as simple as possible, by abuse of notation, we mostly refer only to as the admissible recommendation instead of the pair .

Remark 4 (Relationship with correlated equilibria of [6, 10]).

It is worth to briefly compare our notion of coarse correlated equilibria with the notion of correlated equilibria of [10] and [6]. Besides the fact that the sets of times, individual states and control actions are finite, therein strategies recommended to the players are in restricted closed loop form, that is, they are Markovian functions of each player’s private state, hence of the form , with measurable, for each . Recommendations thus take values in the set of such functions of time and state. Most importantly, in their framework, the deviating player reacts to the recommended strategy: she observes the recommendation the mediator gives her and decides whether or not to play accordingly after receiving it. Therefore, using our notation, the deviating player has access to the information carried by . This feature is not present in our model, as previously discussed.

4 Formulation of the mean field game

Consider the following canonical space

| (4.1) |

Define and as

| (4.2) |

By definition of , and are independent, is an -valued random variable with law and is a standard Brownian motion. Define the filtration as the -augmentation of the filtration generated by and .

Consider the set of -progressively measurable processes taking values in :

| (4.3) |

Provided that we identify processes which are equal -a.e., we can regard as

where stands for the progressive -algebra on , using the filtration . We call any element an open loop strategy for the mean field game. We endow such a space with the norm

| (4.4) |

and consider the Borel -algebra associated to that. We observe that, since is Polish and is closed, is a separable Banach space. Finally, we will make no distinction between an -progressively measurable process and any other process which is equal to it -almost everywhere.

Definition 3 (Admissible recommendation for the mean field game).

We call admissible recommendation a pair where:

-

1.

, is a complete probability space; is a Polish space and is its corresponding Borel -algebra.

-

2.

is a random variable with values in :

(4.5) -

3.

is admissible, in the following sense: let be the product space of and :

We complete the -algebra with the -null sets and endow the product probability space with the -augmentation of the filtration

Given an -valued random variable as in (4.5), we say that is admissible if there exists an -valued process , defined on and -progressively measurable, so that, for -a.e. , the section is equal to in :

(4.6)

If is an admissible recommendation, we write

| (4.7) |

where equality is to be understood in the sense of (4.6). We call strategy associated to the admissible recommendation the -progressively measurable process satisfying (4.7).

We remark that, by Proposition B.2, given any admissible recommendation , the strategy associated to it is unique -almost everywhere.

Definition 4 (Correlated flow).

A correlated flow is a triple where:

-

1.

is an admissible recommendation.

-

2.

is a random continuous flow of measures in .

The same considerations as in Remark 1 about the extension of random variables on the product space hold for correlated flows as well.

Let be a correlated flow. On the product probability space defined at point 3 of Definition 3, we assign state dynamics. If the representative player decides to play according to the admissible recommendation , the dynamics is given by the following SDE:

| (4.8) |

If instead the representative player decides to ignore the mediator’s recommendation and to use a possibly different strategy , the dynamics is given by the following SDE:

| (4.9) |

By Assumptions A, on any space there exists a solution to equation (4.8) and pathwise uniqueness holds. By Theorem A.1, uniqueness in law holds. Analogous considerations apply to equation (4.9).

Let be a correlated flow. The cost functionals for the representative player and the deviating player, whose state dynamics follow (4.8) and (4.9), respectively, are given by:

| (4.10) | ||||

As in the -player game, the expectation in the cost functional is taken with respect to the product probability measure ; in particular, it depends on the mediator’s randomization also when the representative player deviates. Finally, we give the definition of coarse correlated solution of the mean field game:

Definition 5 (Coarse correlated solution).

A correlated flow is a coarse correlated solution of the mean field game if the following properties hold:

-

(i)

Optimality: for every deviation , it holds

(4.11) -

(ii)

Consistency: for every time , is a version of the conditional law of given , that is,

(4.12)

We will refer to coarse correlated solutions of the mean field game as coarse correlated mean field solutions and mean field coarse correlated equilibria (CCE) as well.

Remark 5 (Role of ).

Analogously as in the -player game, although the probability space is part of the definitions of admissible recommendation and correlated flow, when it is clear from the context we refer to and , instead of the pair and the triple , as admissible recommendation and correlated flow, respectively.

As in [6, 10], the consistency condition (4.12) should be read in the following way: the mediator imagines what the flow of measures will be, up to the terminal horizon , before the game starts, and gives a recommendation to each player according to his idea. Since the flow of measures is expected to be stochastic as a result of the mediator’s randomization only, we request it to be measurable with respect to , and, since the randomization is performed before the game starts, we have for any . If all players commit to the mediator’s lottery for generating recommendations, then the flow of measures should arise from aggregation of the individual behaviors, consistently with what imagined by the mediator. Since the generation of the recommendation is performed on the basis of the whole flow of measures, we formulate consistency condition (4.12) with respect to conditioning on the whole flow. Regarding the strategy of the deviating player, as in the -player game, if the player deviates, she chooses her strategy on her own, without using any of the information carried by or : the only information she has about or comes from the knowledge of the distribution , which is assumed to be known by the representative player, in analogy to the -player game.

Remark 6 (Relation with MFGs with common noise).

Given the consistency condition (4.12), it is worth comparing coarse correlated solutions to the MFG and solutions to MFGs with common noise (see, e.g., [14, 29, 31] and in [13, Volume II]). In the latter, the flow of measures is stochastic due to a common noise that equally impacts the state dynamics of all players in the underlying -player game. As a consequence, the flow of measures is expected to be adapted to the filtration generated by the common noise (the so called strong solutions); if this is not the case, compatibility conditions between the noises and the flow of measures itself are needed in order to guarantee that the flow picks into the future in a minimal way (the so called weak solutions). In the case of a coarse correlated solution to the MFG, on the other hand, the flow of measures is expected to be stochastic as a result of the mediator’s randomization only, which is generated before the beginning of the game. More formally, this implies that the flow of measure is -measurable with for any . Recommendations to the representative player are given according to the mediator’s idea of the whole flow, which leads to the consistency condition with conditioning with respect to the whole flow up to terminal time. In this sense, the mediator sees into the future, and consequently no compatibility condition is needed.

One might be tempted to regard the randomness driving the mediator’s lottery for selecting recommendations as a common noise that affects the state dynamics only through the control. There are at least two major differences though: First, such a common noise will have no impact on the controls of a deviating player. To put it differently, only the pre-committing players’ dynamics are directly affected by the mediator’s lottery over strategy profiles. Second, such a common noise would not be exogenous; instead, it is built into the correlation device used by the mediator, as represented by the auxiliary probability space , and as such is part of the solution.

Example 1 (Admissible recommendations).

Fix a complete probability space . We provide some simple examples of random variables which are admissible recommendations in the sense of Definition 3.

-

1.

Suppose that takes only finitely many values, say , , i.e. , with for every , . We can easily define the associated strategy as

We explicit the dependence upon the scenario :

By the same line of reasoning of Remark 1, we have that this process is -progressively measurable, since the processes , , are -progressively measurable and the -measurable real-valued random variables can be regarded as defined on the product space and -measurable, therefore -progressively measurable. Finally, condition (4.6) is satisfied by itself.

-

2.

Suppose takes at most countably many values. We can define as

Set and observe that, by the same argument of the previous point, is an -progressively measurable process for each . Furthermore, for each , the sequence is eventually constant, being a partition of . Therefore, the sequence converges pointwise to . Being the pointwise limit of , we deduce that is a progressively measurable process with values in which satisfies (4.6), so that is admissible.

-

3.

Let be a complete probability space, with Polish and the corresponding Borel -algebra, and let be an -valued process defined on the -completion of the product space with values in . Assume that it is progressively measurable with respect to the -augmentation of the filtration . We can define a function by setting

(4.13) where is a -null set and is an arbitrary point in . By Lemma B.1 in Appendix B, the pair is an admissible recommendation, with strategy associated to the recommendation given by the process itself.

5 Approximate -player coarse correlated equilibria

The next result shows how to construct a sequence of approximate -player coarse correlated equilibria with approximation error tending to zero as , provided we have a coarse correlated solution to the mean field game.

Theorem 5.1.

Let , be a coarse correlated solution of the mean field game. For each , there exist:

-

(i)

an admissible recommendation to the players ;

-

(ii)

a real valued , with as ,

so that is an -coarse correlated equilibrium for the -player game.

5.1 Construction of the admissible recommendation profiles to the -player game

With respect to the probability space defined in (3.3), let us denote by the -augmentation of the filtration generated by . Let us introduce the following set of strategies:

| (5.1) |

We stress that, by construction, for each , open loop strategies for the -player game are defined on the same probability space and we have the inclusions and for every .

We build a probability space large enough to carry any sequence of admissible recommendations such that

-

1.

for every , is supported on the set ;

-

2.

for every , has the same distribution as ,

-

3.

for every , is exchangeable.

Then, we define the probability space as , where is a suitable sub -field of that will be defined below.

Let us denote by the distribution of . Let

be the regular conditional probability of given , which exists and is unique since both and are Polish spaces. Here and in the following, stands for the Borel -algebra on . Let denote the joint law of under , let be a version of the regular conditional probability of given , that is, the stochastic kernel so that it holds

| (5.2) |

Define the probability space in the following way:

| (5.3) |

and define so that, for every cylinder with basis , with for every , , , it holds

| (5.4) |

We complete the space with the -null sets. Let denote a scenario in . Let be the projection on , that is

| (5.5) |

Lemma 5.2.

There exists a sequence of recommendations from to so that, for each , the following holds:

-

(a)

is an admissible recommendation, and it takes values in .

-

(b)

The joint law of under is supported on and it is given by

(5.6) As a consequence, for every , has the same distribution as and are conditionally independent given .

Proof.

Recall from (3.3) and (4.1) the definitions of the spaces and . Observe that, up to completion, it holds

| (5.7) |

so that a scenario can be written as . Moreover, by definition of in (3.2), for every it holds

so that can be seen as a sequence of independent copies of . Define the filtered probability space as in point 3 of Definition 1. Let , , be independent copies of , the strategy associated to the admissible recommendation according to (4.7), so that

For every , is -progressively measurable: indeed, since by definition the measures and coincide on the cylinders of the form

| (5.8) |

for any , every -null set can be identified with a -null cylinder of the form (5.8) with basis . Therefore, for every , the -augmentation of the filtration contains all the cylinders with basis

for any in the -augmentation of . This is enough to conclude that is progressively measurable with respect to the -augmentation of , and so with respect to the filtration as well. We define as in (4.13), that is

| (5.9) |

where is a -null set and is an arbitrary point in . By Lemma B.1, is an admissible recommendation from to , for every . Since the associated strategies coincide pointwise, it holds -a.s., as ensured by Proposition B.2. In particular, this implies that only takes values in , since for every fixed the control process is -progressively measurable. This proves point (a).

As for point (b), for every , takes values in by construction. Hence, we may restrict the attention to Borel sets , for every . Let . Since for every -a.s., by definition of , we have

This shows also that are identically distributed as and that are conditionally i.i.d. given . ∎

For each , set and . Then,

is the candidate -coarse correlated equilibrium to the -player game, with to be determined.

Remark 7.

The construction of the probability spaces is rather involved, but has the advantage of making the admissible recommendation to the -players easy to define. Besides this technical reason, we notice that, both in the -player game and in the mean field game, the mediator may choose the space he uses to randomize players’ strategies, as already pointed out in Sections 3 and 4. Then, it is natural to use the same space on which the coarse correlated solution to the mean field game is defined to randomize players’ strategies in the -player game as well.

5.2 Proof of Theorem 5.1

By symmetry, let us consider only possible deviations of player . For every let be given by

| (5.10) |

is an -coarse correlated equilibrium for every . We must show that . For each , choose so that

Let be the solution of

| (5.11) |

and define the corresponding cost as

Let be the solution of

| (5.12) |

with associated cost

Observe that, by construction, under is distributed as under . Therefore, by Theorem A.1 the joint distribution of under is the same as under , where * denotes the state process resulting from the mean field CCE . Moreover, note that by construction is -progressively measurable, where

By the Lipschitz continuity of , may be taken to be -adapted as well.

To prove the theorem, it is enough to show the following:

| (5.13a) | |||

| (5.13b) | |||

| (5.13c) | |||

If these hold, then we can conclude by noticing that

so that, taking the , we have , which proves as .

We start by proving (5.13a). We observe that we cannot just deduce it from the optimality property (4.11) of : since may belong to , it may not be identifiable with an open loop strategy for the MFG, for which inequality (5.13a) would hold. Instead, we prove it by using the regular conditional probability of given . Denote by a point , and let denote the joint law of under . Let be a version of the regular conditional probability of given . We rewrite (5.13a) as

| (5.14) | ||||

We analyse separately the two terms in the last equality. Let us start with the term depending upon . Since , , and are independent of under and is -adapted, is independent of as well. We deduce that, under , is an -Brownian motion, solves equation (5.12) and , for -a.e. . In particular, this implies that

| (5.15) | ||||

for -a.e. .

As for the term depending upon , we note that, since , there exists a progressively measurable functional so that

Under , it holds

| (5.16) |

since are almost surely constant under . Since the joint law of , and is the same under both and , (5.16) implies that satisfies

| (5.17) |

under , with -progressively measurable. For every , define the strategy

| (5.18) |

Then belongs to for every , and it depends measurably upon . For every , let be the solution of

Since , it follows that

| (5.19) | ||||

We note that the left-hand side of (5.15) depends measurably upon due to a monotone class argument. Being a mean field CCE by assumption, (5.15) and (5.19) imply that

which yields (5.13a).

As for (5.13b) and (5.13c), they must be handled by continuity arguments on the cost functions and propagation of chaos as stated in Lemma C.1. We give the details only for (5.13b), since (5.13c) is analogous. We have:

For , Assumptions A ensure that is locally Lipschitz with at most quadratic growth. Therefore, by straightforward estimates, we have:

By Lemma C.1, the right-hand side tends to as goes to infinity. The convergence of is shown analogously.

6 Existence of a coarse correlated solution of the mean field game

Taking inspiration from [22, 38, 39] and [5, Appendix 1.B], we associate a zero-sum game to the search of a mean field CCE. Loosely speaking, the game should be of the following type: player A, the maximizer, chooses a correlated flow , while player B chooses a deviating strategy . The payoff functional is the following:

| (6.1) |

Player A aims at maximizing , while player B chooses her strategy in order to minimize . In order to get an equilibrium, one should restrict to correlated flows so that the consistency condition (4.12) is satisfied. If we could show that the game has a positive value and player A has an optimal strategy , then we would have established that such a strategy would satisfy the optimality property (4.11) as well, and therefore would be a mean field CCE. In order to get a convenient structure for the sets of strategies and good continuity and convexity properties of the payoff functionals, we embed our auxiliary problem in a more general zero-sum game which, roughly speaking, extends the payoff functional in equation (6.1). Care is needed in dealing with the term depending both on and , since it must reflect independent strategy choices of the opponents. Using Fan’s minimax theorem, we will show that the auxiliary game has positive value and admits an optimal strategy for the maximizing player. Finally, such an optimal strategy is used to induce a coarse correlated solution of the mean field game.

Remark 8.

Under similar assumptions to Assumptions A, the existence of weak or also strong MFG solutions has been established in the literature; see, for instance, [28, 29, 31]. As already noticed, strong MFG solutions are coarse correlated solutions to the MFG as well, and, at least in some cases, this is also true for weak MFG solutions (see upcoming Section 7.1). Nevertheless, we think that the existence result of Theorem 6.4 is of independent interest, for two main reasons. Firstly, the proof shows directly the existence of a coarse correlated solutions without relying on existence results for stronger notions of equilibria, which are usually based on fixed point theorems. Such a direct proof is instead based on a minimax theorem, which, to the best of our knowledge, is used for the first time in continuous time MFG literature. Secondly, since we reduce the search of a coarse correlated solution to the MFG to finding an equilibrium for an auxiliary linear zero-sum game on spaces of measures, our formulation paves the way to the use of linear programming methods for computing mean field CCEs. We further discuss this point in the following Remark 9.

6.1 Relaxed controls

Since we are going to use compactness arguments, it is useful to provide some information about relaxed controls before introducing the auxiliary zero-sum game in the next section. Relaxed controls have a long history in control theory (see, e.g., [17] and [23]), and also in mean field games (see the series of works [15, 28, 29, 30], or [9] in a slightly different framework). We will use them in a similar way.

Denote by the set of positive measures on so that the time marginal is equal to the Lebesgue measure, i.e., for every . We endow with the topology of weak convergence of measures, which makes a Polish space. It is a well known fact that, when the set is compact, is compact as well. Moreover, for every measure , there exists a measurable map so that , with unique up to -a.e. equality. We can equip the measurable space with the filtration defined by

We observe that is countably generated for every , by reasoning as in the proof of [4, Proposition 7.25]. Finally, one can prove that there exists an -predictable process such that, for each , for a.e. (see, e.g., [28, Lemma 3.2]). By an abuse of notation, we write .

Consider a filtered probability space . A relaxed control is a -valued random variable. We say that is -adapted if is a real valued -measurable random variable for every . Observe that every -valued progressively measurable process , which is often referred to as strict control, induces a relaxed control by setting

Finally, using the map described above, we can safely identify every -adapted relaxed control with the unique (up to -a.e. equality) -progressively measurable process with values in so that

In the following, we will use mostly the notation for a relaxed control and will make no distinction between a -valued random variable and a -valued process.

6.2 The auxiliary zero-sum game

We now formally define and study the auxiliary zero-sum game.

Definition 6 (Strategies for player A).

A strategy for player A is a probability measure so that there exists a tuple with the following properties:

-

(i)

is a filtered probability space satisfying the usual assumptions; is Polish and is its corresponding Borel -algebra.

-

(ii)

is an -Brownian motion and is an -measurable independent -valued random variable with law .

-

(iii)

is an -measurable random variable with values in ; it is independent of both and .

-

(iv)

is an -progressively measurable relaxed control with values in .

-

(v)

Let be the solution of

(6.2) Then -a.s for every .

-

(vi)

is the joint law under of , and : .

We denote by the set of strategies for player A.

We observe that, by Assumptions A, there exists a unique solution to equation (6.2) for every tuple satisfying properties (i-iv).

Definition 7 (Strategies for player B).

A stochastic kernel from to is a strategy for player B if there exists a tuple so that

-

(i)

is a filtered probability space satisfying the usual assumptions; is Polish and is its corresponding Borel -algebra.

-

(ii)

is an -Brownian motion and is an -measurable independent -valued random variable with law .

-

(iii)

is an -progressively measurable relaxed control with values in .

-

(iv)

For every , is the joint law under of , where is the solution to

(6.3) that is:

(6.4)

We denote by the set of strategies for player B.

By Lemma D.1, the set of strategies for player B is well defined in the sense that the map is truly a stochastic kernel.

We now define the payoff functional for the zero-sum game. Let us introduce the function defined by

| (6.5) |

Definition 8 (Auxiliary zero-sum game).

The auxiliary zero-sum game is a zero-sum game where:

-

•

The set of strategies for player A, the maximizer, is the set introduced in Definition 6.

-

•

The set of strategies for player B, the minimizer, is the set introduced in Definition 7.

-

•

The payoff functional is the function defined as

(6.6) where denotes the marginal of on .

We denote the lower and upper values of the game as, respectively, and :

If the lower and upper values of the game are equal, we set and call the value of the game. We say that a strategy is optimal for player A if

6.3 Relationship between the zero-sum game and the mean field game

The goal of this section is to show how to use an optimal strategy for the maximizing player of the auxiliary game to induce a coarse correlated solution to the mean field game. The next proposition shows that, for every correlated flow so that consistency condition (4.12) is satisfied and every deviation , there exists a pair of strategies so that the following equality holds:

| (6.7) |

Proposition 6.1.

Let , be a correlated flow. Denote by the law of . Let be the strategy associated to the admissible recommendation and let .

Proof.

In the following, we work on the probability space defined in point (3) of Definition 3. Recall that, as pointed out in Remark 1, we can think of , and as independent random variables, each of them defined on the same probability space . Observe that the -valued process is -progressively measurable since is admissible by assumption. Let be the solution to equation (4.8). Since obviously satisfies (6.2) for such a process and the condition holds by assumption, belongs to .

As for point (ii), recall from Remark 1 that we can regard as defined on the product space , and that and are mutually independent by construction. Therefore, the -valued process is independent of . Let be the solution of equation (4.9). By Lemma D.2 in Appendix D, equation (6.8) holds.

Finally, since and are defined on the same filtered probability space , we can write the integrals in as expectations:

This proves (6.7). ∎

The next result ensures existence of an optimal strategy for the maximizing player:

Theorem 6.2 (Existence of the value of the game and of an optimal strategy for the maximizing player).

Consider the game described in Definition 8. The following holds:

-

(i)

The game has a value, i.e. .

-

(ii)

There exists a strategy which is optimal for player .

-

(iii)

The value of the game is non negative: .

The proof of this theorem is deferred to Section 6.4. The following result is some sort of mimicking result: it will allow us to find, given any measure , a probability measure so that and share the same payoff for every opponent’s strategy and is induced by a correlated flow, as in Proposition 6.1:

Lemma 6.3.

Let . There exists a measure so that the following holds:

-

•

The marginal distributions of and on are the same: .

-

•

Let be such that . Then is of the form , where is a measurable function.

-

•

For every , it holds

The proof of this lemma is postponed to Appendix D. In order to prove Theorem 6.4, we need the following additional assumption, which are standard when dealing with relaxed controls (see, e.g., [23]):

Assumption B.

For every , the set

| (6.9) |

is closed and convex.

Finally, we prove the existence of a coarse correlated solution to the mean field game:

Theorem 6.4 (Existence of a coarse correlated solution of the MFG).

Proof.

Let be an optimal strategy for player A, which exists by Theorem 6.2. Consider the strategy given by Lemma 6.3, so that it holds

| (6.10) |

Let be as in Definition 6, so that . Recall that, by Lemma 6.3, -a.s.. By Assumption B, the set defined by (6.9) is convex for every . Therefore, by a well known measurable selection argument (see, e.g., [23, Lemma A.9]) there exists a measurable function so that

| (6.11) | |||

It follows that is a solution to equation

| (6.12) |

as well, and the consistency condition (4.12) is still satisfied. By Lemma D.3, we deduce that the solution to equation (6.12) can be taken adapted to the -augmentation of the filtration , and therefore there exists a progressively measurable function so that

| (6.13) |

Set

| (6.14) | ||||

Then, the progressively measurable processes and are equal -a.s., which implies that solves

as well, and the consistency condition is still satisfied. Set . By Lemma B.1, there exists a -null set so that the pair defined by

| (6.15) | ||||

is a correlated flow, where is an arbitrary point in . Let be the solution of (4.9) on the product probability space defined in point 3 of Definition 3. Note that the strategy associated to the admissible recommendation strategy is equal to -almost surely. Since uniqueness in law holds by Theorem A.1, it follows that

| (6.16) |

which implies that the consistency condition (4.12) is satisfied.

Remark 9.

As described in this section, the first step to find a coarse correlated solution is to find an optimal strategy for the maximizing player in the auxiliary zero-sum game in Definition 8, which exists by Theorem 6.2. Since this optimization problem is given by a linear payoff functional defined over a convex set of probability measures, linear programming methods could be employed to find approximate solutions. The study of computational methods for finding coarse correlated solutions to the MFG is beyond the scope of this work. We refer to [26, 40] for a linear programming approach to the computation of (true) correlated equilibria in -player games.

6.4 Proof of Theorem 6.2.

The main instrument is the following Minimax Theorem, due to K. Fan:

Theorem 6.5 ( [18], Theorem 2 ).

Let be a compact Hausdorff space and an arbitrary set (not topologized). Let be a real-valued function such that, for every , is lower semi-continuous on . If is concave on for every and convex on for every , then

| (6.17) |

The following results aims at verifying that the auxiliary zero-sum game in Definition 8 satisfies the assumptions of Theorem 6.5. We start with some useful moment estimates for the solution to (6.2):

Lemma 6.6 (Estimates).

The proof is omitted as it is just a straightforward application of Gronwall’s lemma. We recall the following fact, which will be used extensively and whose proof can be found in [44, Theorem 7.12]: given a metric space , a sequence is relatively compact if and only if it is tight and satisfies

| (6.19) |

Lemma 6.7.

is pre-compact in .

Proof.

Let be a sequence in , let us show that it is pre-compact, which is equivalent to show that is tight and condition (6.19) is satisfied. Moreover, by [28, Lemma A.2], relative compactness of the sequence is equivalent to the relative compactness of each sequence of marginals on , and .

Since is compact by Assumption A, the space is compact as well. Then, we automatically get both tightness of the sequence of the marginals on of and property (6.19).

In the following, for every , let and be as in Definition 6, so that . Let be the law of under . We prove the tightness by means of Kolmogorov-Čentsov criterion, as stated, e.g., in [27, Corollary 16.9]. Let , . We have:

for some positive constant which is updated from line to line. For every , we have

| (6.20) | ||||

where the last inequality follows from Lemma 6.6, with independent of . Such a uniform bound implies that

Set , so that we get

| (6.21) |

with . Since for every , we have the tightness of the initial laws as well. This concludes of the proof of the tightness of . As for condition (6.19), we have:

for some positive constant independent of . By Markov’s inequality and estimate (6.18) again, we get

Finally, we turn to the sequence , where . Let be the regular conditional distribution of given . Then, -a.s. and -a.e. for every , which implies that, for every , we have

for -a.e. . Integrating with respect to yields

where the last inequality follows from (6.21) with . Since , it is enough to apply again Kolmogorov-Čentsov criterion and deduce the tightness of . Finally, we verify condition (6.19). To this extent, we note that, for every , there exists a continuous modification of the process , so that it holds

Indeed, estimate (6.21) on the moments of implies that the process satisfies

where we have used Cauchy-Schwartz inequality, (6.18) and (6.21) to bound and , respectively. Therefore, by choosing and as above, we deduce from [27, Theorem 3.3], that there exists a continuous modification of . Then, observe that

Since both processes are almost surely continuous, we can take the supremum over every to conclude that

| (6.22) |

We are now ready to show that (6.19) holds for : by applying (6.22) in the first inequality, Cauchy-Schwartz and Markov inequalities, we have

since the suprema over are finite by Lemma 6.6. ∎

Lemma 6.8.

is closed in .

Proof.

It is enough to prove that, for every sequence converging to as in , we have . We work on the following canonical space: let be given by

We equip such a space with the filtration given by

where . Let , and denote the projection from in , and , respectively. Define the process as

| (6.23) |

Observe that is a continuous process on and, by [28, Corollary A.5], for every is a continuous with at most linear growth function of .

For every , let and be as in Definition 6, so that . Since , we have that the tuple satisfies the requirements of Definition 6, where denotes the -augmentation of the filtration . We show that the tuple satisfies the requirements of Definition 6, which implies .

We start by the independence property of , and under . Let , for , , be bounded continuous functions. Since , and are independent under and weakly, we have

where the first equality holds since for every -a.s.. Then, since is a continuous function of for every , weak convergence implies that

| (6.24) | ||||

This is enough to ensure the mutual independence under of , and for every , which yields the independence of , and . Moreover, by taking and identically equal to , equation (6.24) implies that is natural Brownian motion under , since the finite dimensional distributions of coincide with the ones of a Brownian motion. Let us verify the independence of increments properties. Let , -measurable, -measurable, and . Then, we have:

where the last equality holds since is a -Brownian motion under , is -measurable and and are both -adapted. By working with an approximating sequence, this holds also for bounded measurable , , and , which is enough to conclude the independence of increments. Finally, since is -Brownian motion, it remains so under the -augmentation of .

Since , we have that as well. Moreover, since is a -Brownian motion and is -adapted by definition of the filtration, equation (6.23) implies that is a solution to (6.2).

As for the consistency condition, observe that, for every , , , we have

since is a version of the conditional law under of given . Therefore, by weak convergence we have both

where the second limit holds since the function , which implies

This is enough to conclude that -a.s for every , since the random element takes values in a Polish space. ∎

Lemma 6.9 (Convexity).

and are convex.

Proof.

We start by proving that is convex. Let , , be in , and let . Let be as in Definition 6, so that . Set . Without loss of generality, we can suppose that the tuples are defined on the same probability space which supports also a Bernoulli random variable , so that and are mutually independent. If needed, we can enlarge the filtration so that is -measurable. Let us consider the following random variables:

| (6.25) | ||||||

Set and . Observe that the law of under is the same as the law of conditionally to , as the two tuples coincide on the set , and analogously for . Therefore, for every Borel set , we have

| (6.26) | ||||

In particular, (6.26) implies that . Let us show that the tuple satisfies the requirements of Definition 6. By (6.26), has law and is a natural Brownian motion. To see that it is an -Brownian motion, let , , : then

since is -measurable by assumption. As for the mutual independence of , and , we have that the joint law factorizes in the product of the marginals: by using (6.26), since share the same joint law, one gets

With similar arguments, one can show that for every , , bounded and measurable, it holds

which implies that is a version of the conditional distribution of given . Finally, consider the set

and define analogously . We have that and , since satisfies the equation above -a.s., and analogously , so that . On such a set, satisfies the equation

Since is -adapted, is a solution to equation (6.2), which concludes this part of the proof.

Let us turn to the convexity of the set . Let , , be in , and . Let , be as in Definition 7 so that , where is the solution to equation (6.3) on when is evaluated at . Let , and consider the maps defined by

| (6.27) | ||||

Similarly as for the set , suppose that the tuples are defined on the same probability space supporting also a Bernoulli random variable , so that and are mutually independent. If needed, we can enlarge the filtration so that is -measurable. Let , and be as in (6.25), and, for every , define

Let and consider the map , defined analogously to above. By point (ii) of Lemma D.1, it induces a stochastic kernel . By working in the same way as in the case of , we can show that for each , which implies that . ∎

Proposition 6.10.

The map is bilinear. Moreover, is continuous for every .

Proof.

Bilinearity is clear, hence we focus on the continuity of for fixed . Take , in and suppose in the 2-Wasserstein distance. We treat separately the term depending just upon and the term depending also upon in (6.6).

By [44, Theorem 7.12], in 2-Wasserstein metrics if and only if

| (6.28) |

for every continuous with at most quadratic growth; hence, we just need to show that the functional defined in (6.5) is continuous with at most quadratic growth. By Assumptions A and [28, Corollary A.5], we have that is continuous. It is straightforward to verify that has at most quadratic growth, in the sense that

Therefore, we get continuity of the term depending only upon .

Denote by and the marginal of and on . We can manipulate the term depending both upon and as

where we set

We must show that is continuous with at most quadratic growth with respect to the 2-Wasserstein distance. As for the growth condition, estimate (D.6) in Lemma D.1 proves that has at most quadratic growth in . As for the continuity, let so that in . Note that in , as implied by Lemma D.1. Define . Since the cost functions are locally Lipschitz, we have that converges to uniformly on bounded sets of . This is enough to conclude that

∎

We can now prove points (i) and (ii) of Theorem 6.2: take , and in the statement of Theorem 6.5. By Lemmata 6.7 and 6.8, is compact with the topology of convergence in 2-Wasserstein distance and both sets and are convex by Lemma 6.9. By Proposition 6.10, the payoff is both concave and continuous in for every fixed and convex in for every fixed . Therefore, Theorem 6.5 yields the existence of both the value of the auxiliary zero-sum game and an optimal strategy for player A. The next proposition proves point (iii), concluding the proof of Theorem 6.2.

Proposition 6.11 (Positivity of the value of the auxiliary zero-sum game).

Let be the value of the zero-sum game defined in Definition 8 has a value . Then .

Proof.

We show that, for every there exists a strategy so that . Fix , let be a tuple as in Definition 7 so that , for every . On this probability space, consider the following stochastic differential equation of McKean-Vlasov type:

| (6.29) |

Under Assumptions A, there exists a unique pair satisfying (6.29), where is an -adapted continuous process so that , as ensured by, e.g., [13, Volume 1,Theorem 4.21], which implies that actually belongs to . Define the deterministic flow of measures by setting . Define as . Since is deterministic and is a solution to (6.29), is -measurable and independent of and , and consistency condition holds trivially. This implies that belongs to . By writing the integrals in as expectations, we have:

where denotes the marginal law of on . Since such a construction holds for every , we have

Taking the infimum with respect to , we have

which shows that is non-negative. Since , this proves that the value of the auxiliary zero-sum game is non-negative. ∎

7 An example of coarse correlated solution to the mean field game

Taking inspiration from the work of Bardi and Fischer [3] and Lacker’s papers [29, 30], we provide a simple example of a mean field game possessing mean field CCEs with non-deterministic flow of measures .

Let . Set , with , and . For , denote by its mean . Consider the following coefficients and cost functions:

with a positive constant. Observe that they satisfy the requirements of Assumption A. We want to find a coarse correlated solution for the mean field game whose payoff functional, to be maximized, is given by

| (7.1) |

under the constraint

| (7.2) |

where is the strategy associated to an admissible recommendation in the sense of (4.7).

Set , the power set and, given some probability measure , we set , so that for all and . Consider the following open loop strategies and flows of measures:

| (7.3) | |||

It was shown in [3] that the pairs and are two non-equivalent open-loop solutions of the mean field game, with initial distribution , where by “non-equivalent” we mean that the flows of measures and do not coincide. We point out that this result holds for more general initial distributions , see [3, Definition 3.1 and Theorem 3.1]. Choose , and set:

| (7.4) | |||

Define in the following way:

| (7.5) |

We claim that, as long as , for every there exists a probability measure and a suitable choice of the parameters so that the tuple is a coarse correlated solution of the mean field game according to Definition 5.

First of all, as shown in Example 1 in Section 4, since takes only two values, it is admissible. Therefore, the tuple is a correlated flow.

Let us begin with the consistency condition. We first observe that, when the state equation is controlled by (respectively, ), the law of the state process at time , , is exactly (respectively, ), for every time .

Suppose that and are both strictly positive. Then, observe that

We can compute explicitly such a conditional probability. Fix :

In order to satisfy the consistency condition, it must hold

for every . By definition of and ,

which holds if and only if

| (7.6) |

We can regard (7.6) as the consistency condition.

We now turn our attention to the optimality condition. Consider and . Since takes finitely many values and it is independent of under the product measure , we can rewrite the optimality condition using disintegration of measures as

where

for in and in on the left-hand side of the inequality above and in on the right-hand side. We rewrite explicitly the inequality as

| (7.7) | ||||

Therefore, using (7.1), we have

where . We can set . Observe that , being the mean of an -valued process, and , since for every the constant process belongs to . We divide by to obtain the following condition:

| (7.8) | ||||

The condition above can be seen as a positivity condition for a real affine function of , , i.e.

| (7.9) | ||||

We now impose the consistency condition (7.6) to get:

| (7.10) | ||||

Observe that imposing the consistency condition (7.6) reduces the number of parameters but makes the problem nonlinear in the probabilities .

Looking at (7.9) and (7.10), we observe that it implies that every randomization of the open loop MFG solutions and is a coarse correlated solution to the MFG as well, and it covers the case treated in [3], for any choices of . To see this, consider a probability measures so that and, therefore, and . For any , such probability measure is a randomization of the MFG solutions and . Equations (7.10) take the simpler form

| (7.11) | ||||

If , then condition (7.9) becomes

which is satisfied if and , for any . If instead , we have

which is again satisfied if and , for every . Observe that, when , , while, when , . This shows that the deterministic correlated flows and are indeed mean field CCE in the sense of Definition 5.

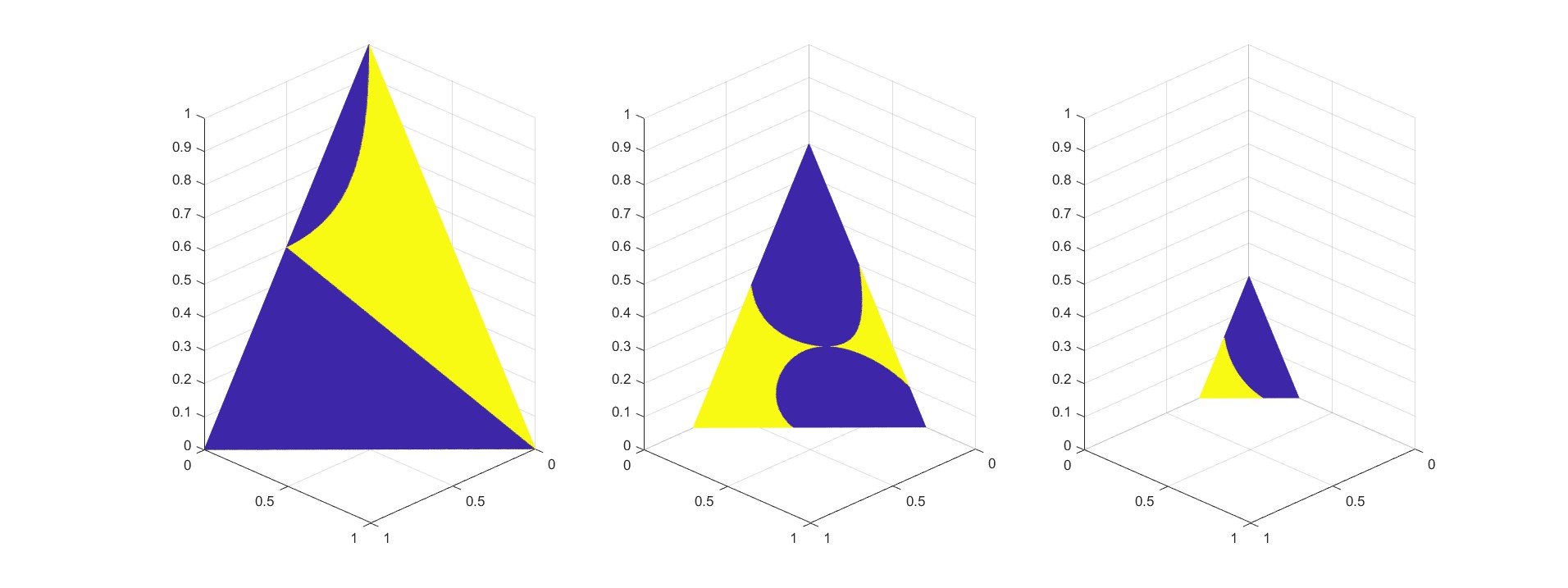

Turning to more interesting cases, consider . The choice of a symmetric interval is not necessary, but it has been made to ease the comparison with previous results in the literature (see the next subsection). Figure 1 shows the existence of coarse correlated mean field equilibria as the probability measure varies. In particular, it shows the existence of infinitely many coarse correlated mean field equilibria for the system.

Yellow spots in Figure 1 refer to those probability measures on so that is indeed a mean field CCE. Observe that there exist infinitely many coarse correlated solutions of the mean field game so that is not a deterministic function of , i.e., they are not a randomization of the solutions and . They correspond to yellow points so that one between and is non null.

7.1 Comparison with weak mean field game solutions without common noise of [29]

Consider , . With this choice of control actions and time horizon, the example we proposed matches the setting of Lacker’s \sayilluminating example of [29, Section 3.3]. We show that there exists a coarse correlated solution of the MFG which is not a weak MFG solution without common noise as defined in Definition 3.1 therein. In particular, the most important feature is the fact that the recommendation can not be expressed as a deterministic function of the flow of measures.

To be consistent with the notation and the setup of Lacker’s paper, we use the notion of relaxed controls, which are used extensively in Section 6 (see, in particular, Section 6.1 for definitions, notation and some important properties). Let be so that and are strictly positive. We introduce the relaxed controls and , by setting

Consider the correlated flow defined by (7.5) and observe that the strategy associated to the admissible recommendation can be rewritten as a relaxed control as

| (7.12) |

We point out that does not depend on since and do not depend on . Starting from , we define a random variable with values in by setting

| (7.13) |

We observe that : we have since, by definition of regular conditional probability, must be measurable; to get the opposite inclusion, for every , let be the push forward of through the map . Then, by exploiting the consistency condition (4.12), we have

for every , i.e. -a.s, for every . Let be the natural filtration of the identity process on , i.e. , and let be the natural filtration of , that is

We observe that, for every , we have . To see this, observe that

where the last equality holds for every , as can be verified by explicit calculations. Finally, for , we have . Having established the relations between such -algebras, it is straighforward to verify that the tuple satisfies properties (1-4) and (6) of [29, Definition 3.1]. Now, pick a probability measure so that and , . Figure 1 shows that such a choice is possible (actually, there exist infinitely many measures with the desired property). For such a choice of , the relaxed control does not satisfy the optimality condition (5) of [29, Definition 3.1], since, as shown in [29, Section 3.3], every optimal control must be of the form for -a.e. , with

Here, . Since is trivial and for , the optimal control must be equal to

| (7.14) |

and equal to an arbitrary value at . In particular, observe that such a control is a deterministic function of the measure . For every so that , this is not the case of the correlated flow defined in (7.5), since is not a deterministic function of .

The essential reason for the lack of optimality, in the sense of Lacker, of the relaxed control defined by (7.12) resides in the differences between allowed deviations: on one hand, for weak mean field games solutions in the sense of [29], all adapted compatible controls are allowed, where “compatible” means that is conditionally independent of given for every , which leads to a very rich class of controls. On the other hand, for coarse correlated solution of the MFG, only -progressively measurable strategies are allowed as deviations. Therefore, many more solutions exist.

More generally, one can not compare weak MFG solutions without common noise of [29] and mean field CCEs, due to the difference between the respective consistency conditions. Nevertheless, we can make an additional assumption on the random measure which makes it possible to define a mean field CCE starting from a weak MFG solution. Let be a weak MFG solution without common noise. Let be the push forward of through the map . Define a random flow of measures by setting . Assume that the flow of measures carries the same information as the random measure , i.e.

| (7.15) |

If a weak MFG solution satisfies condition (7.15), then does induce a mean field CCE. Indeed, set . By (7.15), we have , i.e. consistency condition (4.12) is satisfied. Moreover, the assumption on equality of the filtrations ensures that there exists a progressively measurable function so that

Then, we define and as

| (7.16) | ||||

By Lemma B.1, the tuple is a correlated flow. Let be the solution of (7.2) on the product probability space defined in point 3 of Definition 3. Since uniqueness in law holds by Theorem A.1, it follows that has the same joint law as , which implies that the consistency condition (4.12) is satisfied. Since , satisfies optimality condition (4.11) as well and therefore it is a mean field CCE.

We observe that the additional assumption on the filtrations (7.15) is satisfied both by the weak MFG solution exhibited in [29, Proposition 3.7] and in our case, as shown above. We point out that this CCE has been already considered: suppose that the flow of measures as law , , for and given by (7.4). Then, the correlated flow corresponds to the probability measures so that , and , which, as shown, always satisfy the condition (7.9). Roughly speaking, it corresponds to the case when -a.s., for some deterministic measurable .

Appendix

Appendix A Weak and strong existence for controlled equations

We state and prove a Yamada-Watanabe type result for stochastic differential equations with random coefficients as the ones encountered so far. Recall from Section 6.1 the definition of the space and of relaxed controls.

Let be a tuple composed by a filtered probability space satisfying usual assumptions, an -Brownian motion , an -valued -measurable random variable , an -measurable random flow of measures taking values in and an -adapted -valued random variable , in the sense that the random variables are -measurable for every . Let us consider the following stochastic differential equation:

| (A.1) |

where is jointly measurable and progressively measurable in ; progressive measurability must be understood in the following sense: for every , for every , it holds:

Definition 9 (Strong solution and pathwise uniqueness).

Let be a tuple as above. A strong solution to equation (A.1) on is a continuous -adapted process adapted to the -augmentation of so that

| (A.2) |

holds -almost surely.

Definition 10 (Weak solution and uniqueness in law).

Theorem A.1.

Proof.

Let and be two weak solutions of equation (A.1) in the sense of Definition 10 above. Since pathwise uniqueness holds for equation (A.1) by assumption, our goal is to bring together the solution on the same filtered probability space. Let us define the following probability measures:

Observe that and are well defined, since share the same joint law by assumption. Let us consider the following space:

where

In order to equip the space with a probability measure, we disintegrate the measures , , in the following way: let be a regular conditional probability of for given , so that it holds

for every , , or more briefly

Then, we set

Observe that the joint law under of the coordinate projections , , , and is exactly , and analogously when considering the coordinate process instead of . Finally, complete the -algebra with the -null sets and consider the complete right continuous filtration given by

By Lemma A.2, the coordinate process is a -Brownian motion under . Furthermore, it holds

for . Since pathwise uniqueness in the sense of Definition 9 holds by assumption, it follows that and are indistinguishable under , which implies . This proves the desired result. ∎

Lemma A.2.

In the construction of Theorem A.1, is a Brownian motion under with respect to the filtration .

Proof.

Observe that is a natural Brownian motion under . In order to show that it is a Brownian motion with respect to the filtration , we just need to prove that its increments are independent, and the conclusion follows.

Fix , , , and . By Cauchy-Schwartz inequality, we have, for every and :

Therefore, it suffices to show that

| (A.3) |

Since the integrand does not depend upon , we may rewrite such an expectation only with respect to :

Then, we introduce another disintegration of the measure : let be a regular conditional probability for given :

| (A.4) |

for every , , , and , or more briefly

As in [25, Lemma IV.1.1], it can easily be shown that, for every , the map

is -measurable, for every . Therefore, we can compute the left-hand side of (A.3):

since is -measurable and is an -Brownian motion under by assumption. ∎

Appendix B On admissible recommendations

Lemma B.1.

Let be a complete probability spaces and be a filtered probability space satisfying the usual assumptions. Fix a bounded -valued process defined on the completion of the product space . Assume that it is progressively measurable with respect to the filtration , where is the -augmentation of the filtration . Define a function by setting

| (B.1) |

where is a -null set and is some point in . The function defined in (B.1) is an admissible recommendation.

Proof.

Take any bounded -progressively measurable process defined on the product space taking values in , and not necessarily in .

Observe that it is always possible to define a function from to as in (B.1), where denotes the progressive -algebra associated to the filtration . Indeed, by construction of the filtration , since is -progressively measurable, there exists a set , , so that the section is -measurable for every . Set for and for , where is any point in , which is exactly (B.1).