Conditional Generative Models are Provably Robust: Pointwise Guarantees for Bayesian Inverse Problems

Abstract

Conditional generative models became a very powerful tool to sample from Bayesian inverse problem posteriors. It is well-known in classical Bayesian literature that posterior measures are quite robust with respect to perturbations of both the prior measure and the negative log-likelihood, which includes perturbations of the observations. However, to the best of our knowledge, the robustness of conditional generative models with respect to perturbations of the observations has not been investigated yet. In this paper, we prove for the first time that appropriately learned conditional generative models provide robust results for single observations.

1 Introduction

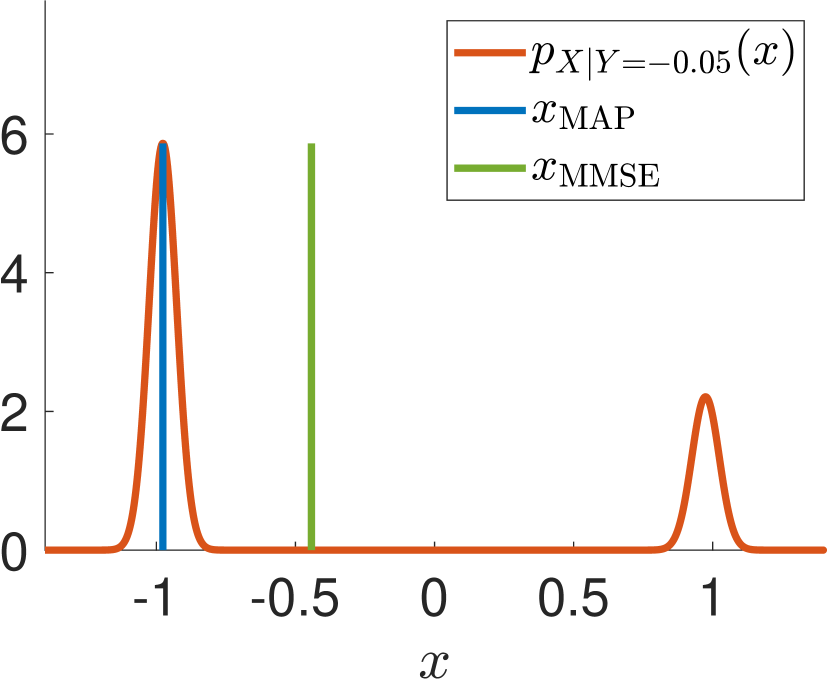

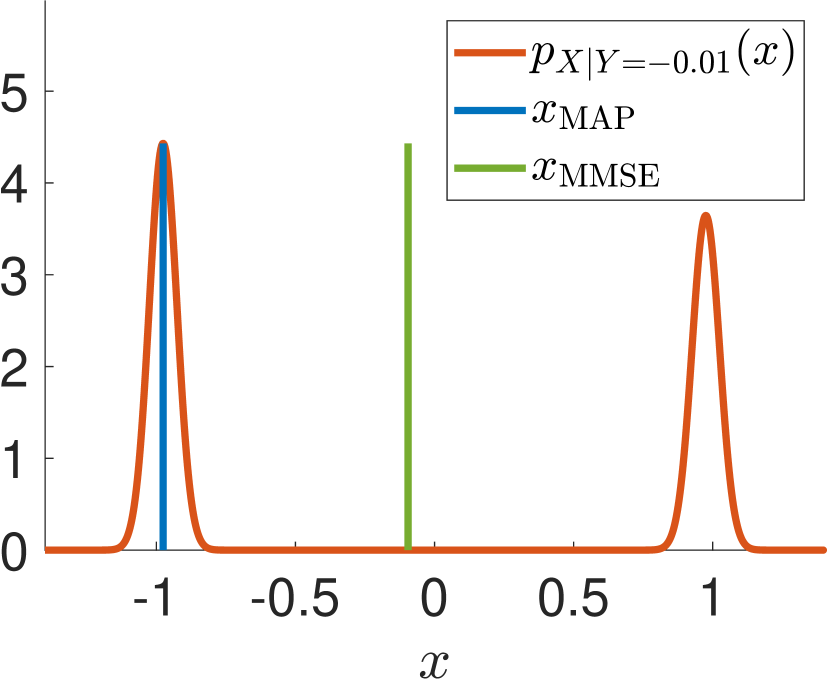

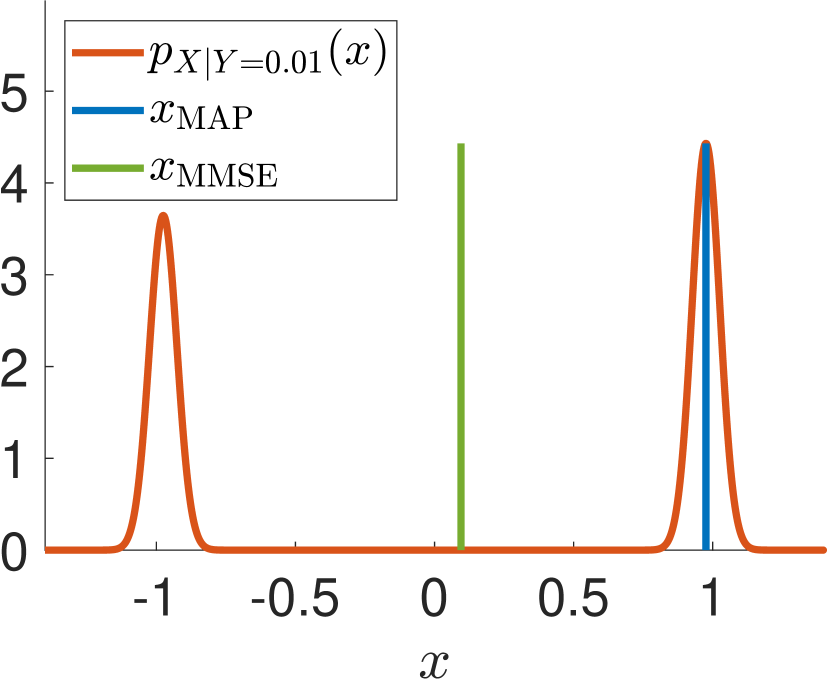

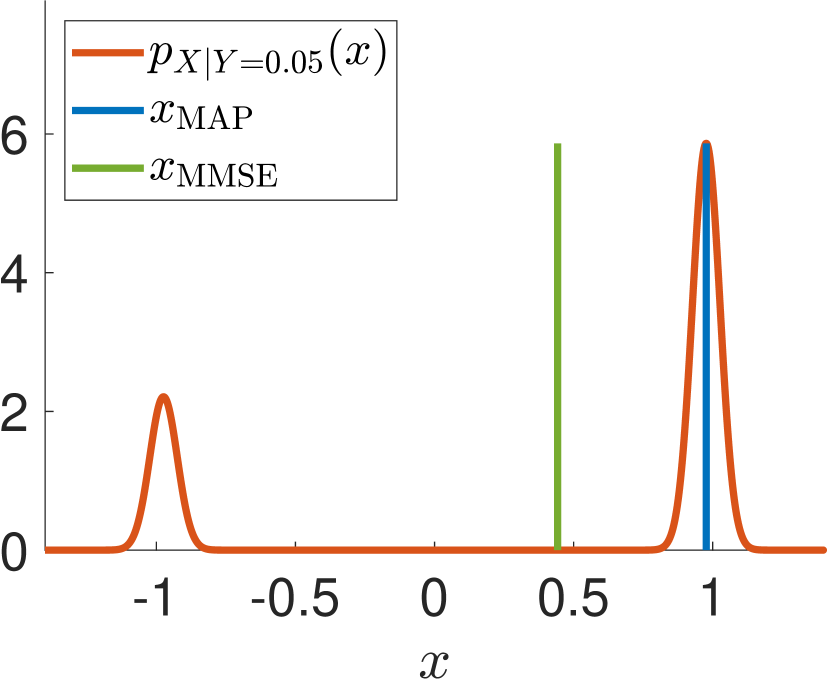

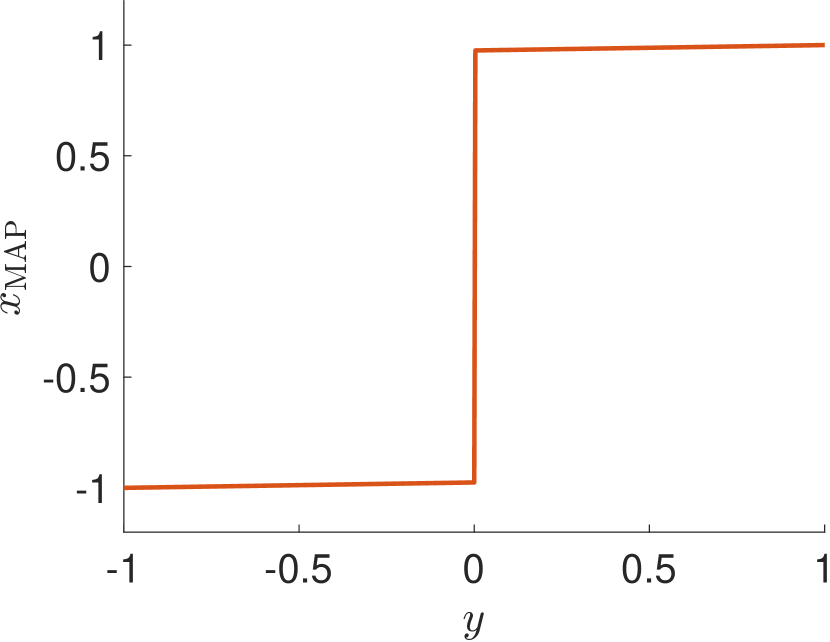

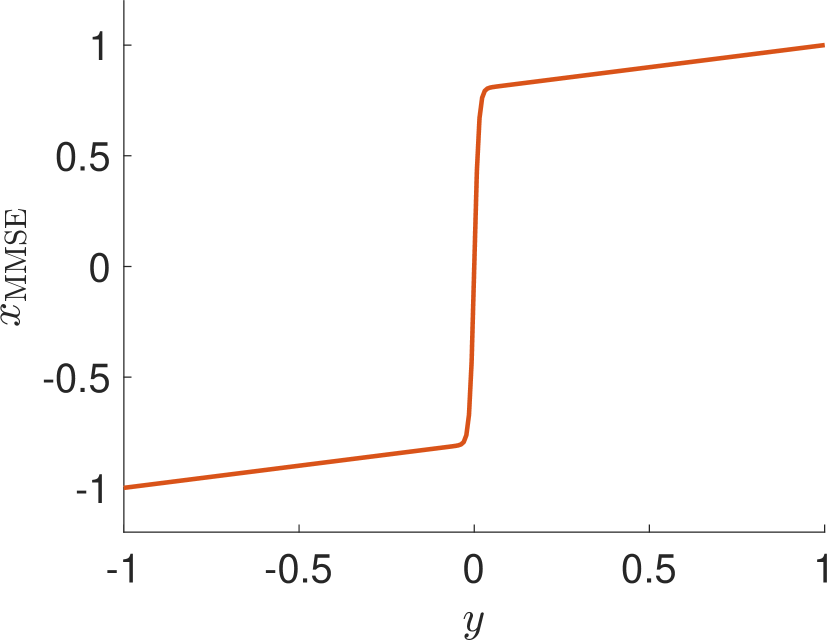

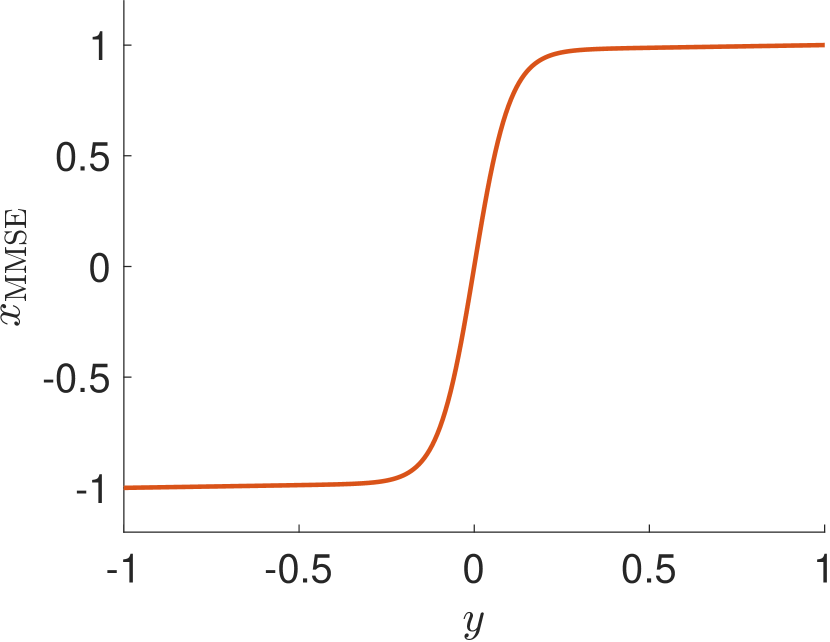

Recently, the use of neural networks (NN) in the field of uncertainty quantification has emerged, as one often is interested in the statistics of a solution and not just in point estimates. In particular, Bayesian approaches in inverse problems received great interest. In this paper, we are interested in learning the whole posterior distribution in Bayesian inverse problems by conditional generative NNs as proposed, e.g., in (Adler & Öktem, 2018; Ardizzone et al., 2019; Batzolis et al., 2021; Hagemann et al., 2022). Addressing the posterior measure instead of end-to-end reconstructions has several advantages as illustrated in Figure 1. More precisely, if we consider a Gaussian mixture model as prior distribution and a linear forward operator with additive Gaussian noise, then the posterior density (red) can be computed explicitly. Obviously, these curves change smoothly with respect to the observation , i.e., we observe a continuous behaviour of the posterior also with respect to observations near zero. In particular, (samples of) the posterior can be used to provide additional information on the reconstructed data, for example on their uncertainty. As can be seen in the figure, for fixed the minimum mean squared error (MMSE) estimator delivers just an averaged value. In contrast to the non robust maximum a-posteriori (MAP) estimator, this is not the one with the highest probability. Even worse, the MMSE can output values which are not even in the prior distribution. For a more comprehensive comparison of MAP estimator, MMSE estimator and posterior distribution, we refer to Appendix A

Several robustness guarantees on the posterior were proved in the literature. One of the first results in the direction of stability with respect to the distance of observations was obtained by Stuart (2010) with respect to the Hellinger distance, see also Dashti & Stuart (2017). A very related question instead of perturbed observations concerns the approximations of forward maps, which was investigated by Marzouk & Xiu (2009). Furthermore, different prior measures were considered in (Hosseini, 2017; Hosseini & Nigam, 2017; Sullivan, 2017), where they also discuss the general case in Banach spaces. Two recent works (Latz, 2020; Sprungk, 2020) investigated the (Lipschitz) continuity of the posterior measures with respect to a multitude of metrics, where Latz (2020) focused on the well-posedness of the Bayesian inverse problem and Sprungk (2020) on the local Lipschitz continuity. Most recently, in Garbuno-Inigo et al. (2023) the stability estimates have been generalized to integral probability metrics circumventing some Lipschitz conditions done in Sprungk (2020). Our paper is based on the findings of Sprungk (2020), but relates them with conditional generative NNs that aim to learn the posterior.

More precisely, in many machine learning papers, the following idea is pursued in order to solve inverse problems simultaneously for all observations : Consider a family of generative models with parameters , which are supposed to map a latent distribution, like the standard Gaussian one, to the absolutely continuous posteriors , i.e., . In order to learn such a conditional generative model, usually a loss of the form

is chosen with some \saydistance between measures like the Kullback-Leibler (KL) divergence used in Ardizzone et al. (2019) for training normalizing flows or the Wasserstein-1 distance appearing, e.g., in the framework of (conditional) Wasserstein generative adversarial networks (GANs) (Adler & Öktem, 2018; Arjovsky et al., 2017; Liu et al., 2021). Also conditional diffusion models (Igashov et al., 2022; Song et al., 2021b; Tashiro et al., 2021) fit into this framework. Here De Bortoli (2022) showed that the standard score matching diffusion loss also optimizes the Wasserstein distance between the target and predicted distribution.

However, in practice we are usually interested in the reconstruction quality from a single or just a few measurements which are null sets with respect to . In this paper, we are interested in the important question, whether there exist any guarantees for the NN output to be close to the posterior for one specific measurement . Our main result in Theorem 5 shows that for a NN learned such that the loss becomes small in the Wasserstein-1 distance, say , the distance becomes also small for the single observation . More precisely, we get the bound

where is a constant and is the dimension of the observations. To the best of our knowledge, this is the first estimate given in this direction.

We like to mention that in contrast to our paper, where we assume that samples are taken from the distribution for which the NN was learned, Hong et al. (2022) observed that conditional normalizing flows are unstable when feeding them out-of-distribution observations. This is not too surprising given some literature on the instability of (conditional) normalizing flows (Behrmann et al., 2021; Kirichenko et al., 2020).

Outline of the paper.

The main theorem is shown in Section 2. For this we introduce several lemmata for the local Lipschitz continuity of posterior measures and conditional generative models with respect to the Wasserstein distance. In Section 3, we discuss the dependence of our derived bound on the training loss for different conditional generative models. In Appendix A, we illustrate by a simple example with a Gaussian mixture prior and Gaussian noise, why posterior distributions can be expected to be more stable than maximum a-posteriori (MAP) estimations and have more desirable properties than minimum mean squared error (MMSE) estimations.

2 Pointwise Robustness of Conditional Generative NNs

Let be a continuous random variable with law determined by its density function and a measurable function. We consider a Bayesian inverse problem

| (1) |

where "noisy" describes the underlying noise model. A typical choice is additive Gaussian noise, resulting in

| (2) |

Let be a conditional generative model trained to approximate the posterior distribution using the latent random variable . We will assume that all appearing measures are absolutely continuous and that the first moment of is finite for all . In particular, the posterior density is related via Bayes’ theorem through the prior and the likelihood as

where means quality up to a multiplicative normalization constant. Since the posterior density is only almost everywhere unique, we choose the unique continuous representative. Further, we assume that the negative log-likelihood is bounded from below with respect to , i.e., . In particular, this includes mixtures of additive and multiplicative noise , if , and are independent, or log-Poisson noise commonly arising in computerized tomography.

We will use the Wasserstein-1 distance (Villani, 2009), which is a metric on the space of probability measures with finite first moment and is defined for measures and on the space as

| (3) |

where contains all measures on with and as its marginals. The Wasserstein distance can be also rewritten by its dual formulation (Villani, 2009, Remark 6.5) as

| (4) |

First, we show the local Lipschitz continuity of our generating measures with respect to , where we assume a local boundedness of the Jacobian of the generator with respect to the observation.

Lemma 1 (Local Lipschitz continuity of generator).

For all , there exists some such that for any parameterized family of generative models with for all and all with it holds

for all with .

Proof.

We use the mean value theorem which yields for every and all with

Next, we apply the dual formulation of the Wasserstein-1 distance to estimate

∎

We want to highlight that there is a trade-off between regularity of the generator due to a small Lipschitz constant (Gouk et al., 2021; Miyato et al., 2018) and expressivity of the generator requiring a large Lipschitz constant (Hagemann & Neumayer, 2021; Salmona et al., 2022).

Remark 2.

If is supported on a compact set, then the assumption in Lemma 1 is fulfilled for generators which are, e.g., continuously differentiable and then it follows from the extreme value theorem. Note that if we choose to be a Gaussian distribution, then it holds . Thus, for continuously differentiable generators it is not clear that this assumption is fulfilled, but at least the weaker assumption for all with and all with holds true. In this case, we can show that Lemma 1 holds true up to an arbitrary small additive constant, see Appendix B for more details.

By the following lemma, which is just (Sprungk, 2020, Corollary 19) for Euclidean spaces, the local Lipschitz continuity of the posterior distribution with respect to the Wasserstein-1 distance is guaranteed under the assumption of a locally Lipschitz likelihood.

Lemma 3 (Local Lipschitz continuity of the posterior).

Let the forward operator and the likelihood in (1) be measurable. Assume that there exists a function which is monotone in the first component and non-decreasing in the second component such that for all with for and for all it holds

| (5) |

Furthermore, assume that . Then, for any there exists a constant such that for all with we have

The Lipschitz constants of the family of generative models and the posterior distributions can be related to each other under some convergence assumptions. Let the assumptions of Lemma 3 be fulfilled, assume further that there exists a family of generative models satisfying

with respect to the -distance and consider observations with . Then, by the triangle inequality it holds

Hence, under the assumption of convergence, we expect the Lipschitz constant of our conditional generative models to behave similar to the one of the posterior distribution.

Remark 4.

The assumption (5) is for instance fulfilled for additive Gaussian noise . In this case

Hence is differentiable with respect to and we get local Lipschitz continuity of the negative log-likelihood.

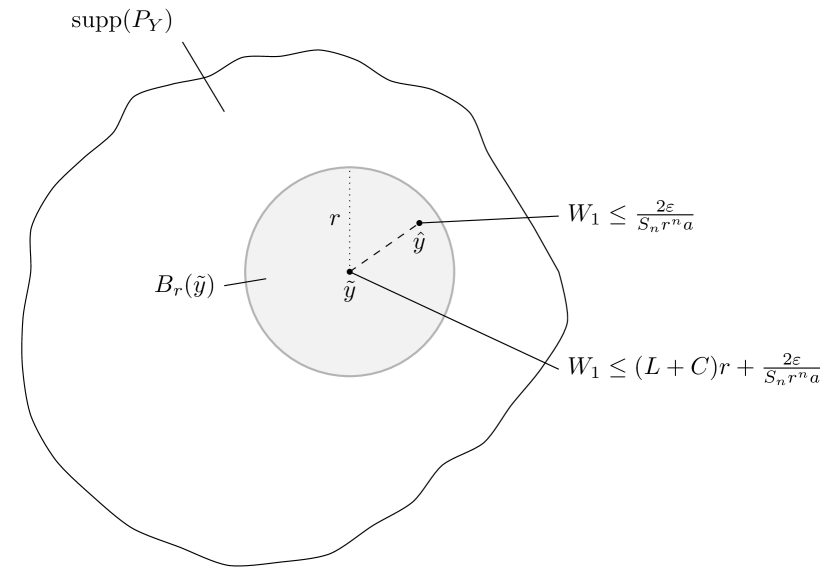

Now we can prove our main theorem which ensures pointwise bounds on the Wasserstein distance between posterior and generated measure, if the expectation over is small. In particular, the bound depends on the local Lipschitz constant of the conditional generator with respect to the observation which may depend on the architecture of the generative model, the local Lipschitz constant of the inverse problem, the expectation over and the probability of the considered observation . We want to highlight that the bound depends on the evidence of an observation and indicates that we generally cannot expect a good pointwise estimate for out-of-distribution observations, i.e., . This is in agreement with the empirical results presented in Hong et al. (2022). The proof of Theorem 5 has a nice geometric interpretation, which is visualized in Figure 2.

Theorem 5.

Let the forward operator and the likelihood in (1) fulfill the assumptions of Lemma 3. Let be an observation with . Further, assume that is differentiable with for and all . For fixed , assume that we have trained a family of generative models which fulfills for all and all with for some such that

| (6) |

for some . Then we have for that

| (7) |

where and is the Lipschitz constant from Lemma 3. If additionally satisfies , then it holds

| (8) |

Proof.

Let . Then, for , there exists by the mean value theorem some such that

Consequently, each has at least probability . Moreover, by the volume of the -dimensional ball it holds that

| (9) |

Now we claim that there exists with

| (10) |

If this would not be the case, this would imply a contradiction to (6) by

Next, we show the local Lipschitz continuity of on by combining Lemma 1 and Lemma 3. Let , so that . Let be the local Lipschitz constant from Lemma 1 and the local Lipschitz constant from Lemma 3. Using the triangle inequality and its reverse, we get

| (11) | ||||

Combination of the results in (10) and (2) yields the estimate

If , we can choose which results in (7). On the other hand, the radius , for which the right-hand side becomes minimal, is given by

Plugging this in, we get (8), which has the same asymptotic rate.. However, we need that which implies

∎

Note that in (6) we assume that the expectation over of the Wasserstein distance is small. When training a generator, usually a finite training set is available. The measure can be approximated by the empirical training set with a rate on compact sets, where is the size of the training set and the dimension, see, e.g., Weed & Bach (2019).

Remark 6.

We can get rid of the dimension scaling by choosing the radius as , which yields

This comes at the disadvantage that the first term is constant with respect to .

The following corollary provides a characterization of a perfect generative model. If the expectation (6) goes to zero, then for all with the posteriors get predicted correctly.

Corollary 7.

Let the assumptions of Lemma 1 and Lemma 3 hold true and assume a global Lipschitz constant in Lemma 1. Let be differentiable with for some and all . Consider a family of generative networks fulfilling

| (12) |

and assume that the Lipschitz constants of from Lemma 1 are bounded by some . Then for all observations with it holds

| (13) |

Proof.

We can assume that , then the statement follows immediately from Theorem 5. ∎

Finally, we can use Theorem 5 for error bounds of adversarival attacks on Bayesian inverse problems. Following the concurrent work of Gloeckler et al. (2023), an adversarial attack on a conditional generative model consists in finding a perturbation to the observation so that the prediction of the conditional generative model is as far away as possible from the true posterior, i.e.,

Note that Gloeckler et al. (2023) use the KL divergence for their adversarial attack, but for our theoretical analysis the Wasserstein distance is more suitable.

The following corollary yields a worst case estimate on the possible attack. In the case of imperfect trained conditional generative models the attack can be very powerful depending on the strength of observation and the Lipschitz constant of the generator. If the conditional generative model is trained such that the expectation in (6) is small, then the attack can only be as powerful as the Lipschitz constant of the inverse problem allows.

Corollary 8.

Let the forward operator and the likelihood in (1) fulfill the assumptions of Lemma 3. Let and with be an observation with . Further, assume that is differentiable with for and all . For fixed , assume that we have trained a family of generative models which fulfills for all and all with for some such that

| (14) |

for some . Then we have the following control on the strength of the adversarial attack

3 Conditional Generative Models

In this section, we discuss whether the main assumption, namely that the averaged Wasserstein distance in (6) becomes small, is reasonable for different conditional generative models. Therefore we need to relate the typical choices of training loss with the Wasserstein distance. For a short experimental verification in the case of conditional normalizing flows we refer to Appendix C.

In the following we assume that the training loss of the corresponding models become small. This can be justified by universal approximation theorems like (Teshima et al., 2020; Lyu et al., 2022) for normalizing flows or (Lu & Lu, 2020) for GANs.

3.1 Conditional Normalizing Flows

Conditional normalizing flows (Altekrüger & Hertrich, 2023; Andrle et al., 2021; Ardizzone et al., 2019; Winkler et al., 2019) are a family of normalizing flows parameterized by a condition, which in our case is the observation . The aim is to learn a network such that is a diffeomorphism and for all , where means that two distributions are similar in some proper distance or divergence. This can be done via minimizing the expectation on of the forward KL divergence , which is equal, up to a constant, to

where the inverse is meant with respect to the second component, see Hagemann et al. (2022) for more details. Training a network using the forward KL has many desirable properties like a mode-covering behaviour of . Now conditional normalizing flows are trained using the KL divergence, while the theoretical bound in Section 2 relies on the metric properties of the Wasserstein-1 distance. Thus we need to show that we can ensure a small in (6) when training the conditional normalizing flow as proposed. Following Gibbs & Su (2002, Theorem 4), we can bound the Wasserstein distance by the total variation distance, which in turn is bounded by KL via Pinsker’s inequality (Pinsker, 1963), i.e.,

where is a constant depending on the support of the probability measures. However, by definition . By Altekrüger et al. (2023, Lemma 4) the density decays exponentially. Therefore, we expect in practice that the Wasserstein distance becomes small if the KL vanishes even though (Gibbs & Su, 2002, Theorem 4) is not applicable.

3.2 Conditional Wasserstein GANs

In Wasserstein GANs (Arjovsky et al., 2017), a generative adversarial network approach is taken in order to sample from a target distribution. For this, the dual formulation (4) is used in order to calculate the Wasserstein distance between measures and . Then the 1-Lipschitz function is reinterpreted as a discriminator in the GAN framework (Goodfellow et al., 2014). If the corresponding minimizer in the space of 1-Lipschitz functions can be found, then optimizing the adversarial Wasserstein GAN loss directly optimizes the Wasserstein distance. The classical Wasserstein GAN loss for a target measure and a generator is given by

where is the dimension of the latent space.

The Wasserstein GAN framework can be extended to conditional Wasserstein GANs (Adler & Öktem, 2018; Liu et al., 2021) for solving inverse problems. For this, we aim to train generators and average with respect to the observations

Hence minimizing this loss (or a variant of it) directly enforces a small in assumption (6).

3.3 Conditional Diffusion Models

In diffusion models, a forward SDE, which maps a data distribution to an approximate Gaussian distribution is considered (Song et al., 2021a; b). Then the theory of reverse SDEs (Anderson, 1982) allows to sample from the data distribution by learning the score , where is the path density of the forward SDE. The forward SDE usually reads

while the reverse SDE is given by

where describes the schedule of the SDE. However, the path density is usually intractable, so that the score is learned with a NN such that for all and . This can be ensured using the so-called score matching loss (Song et al., 2021b) defined by

In order to solve inverse problems, we can consider a conditional reverse SDE

where is the conditional path density given an observation . Consequently, we consider conditional diffusion models, where a NN is learned to approximate for all , and all observations . Then the score matching loss for conditional diffusion models is given in Batzolis et al. (2021, Theorem 1) as

| (15) |

Denote by the solution to the approximated SDE starting at and the solution of the approximated SDE conditioned on an observation . Then we can use the bound derived in Pidstrigach et al. (2023, Theorem 2) which gives

where is a constant depending on the length of the interval and the Lipschitz constant of the conditional score Finally, Hölders inequality yields for the Wasserstein-1 distance

Hence, when training the conditional diffusion model by minimizing (15) we also ensure that (6) becomes small. For more in depth discussion with less restrictive assumptions on the score, see also (De Bortoli, 2022).

3.4 Conditional Variational Autoencoder

Variational Autoencoder (VAE) (Kingma & Welling, 2013) aim to approximate a distribution by learning a stochastic encoder determining parameters of the normal distribution for sampled from and pushing to a latent distribution with density of dimension . In the reverse direction, a stochastic decoder determines parameters of the normal distribution for and pushes back to . By definition, the densities of and are given by and , respectively. These networks are trained by minimizing the so-called evidence lower bound (ELBO)

By Hagemann et al. (2023, Theorem 4.1), the loss is related to KL by

| (16) |

We can solve inverse problems by extending VAEs to conditional VAEs (Lim et al., 2018; Sohn et al., 2015) and aim to approximate the posterior distribution for a given observation . The conditional stochastic encoder and conditional stochastic decoder are trained by

| (17) |

By the same argument as above, the KL can be bounded by

| (18) |

and, using similar arguments as in Section 3.1, we get the estimate

| (19) |

4 Conclusion

We showed a pointwise stability guarantee of the Wasserstein distance between the posterior of a Bayesian inverse problem and the learned distribution of a conditional generative model under certain assumptions. In particular, the pointwise bound depends on the Lipschitz constant of the conditional generator with respect to the observation, the Lipschitz constant of the inverse problem, the training loss with respect to the Wasserstein distance and the probability of the considered observation.

The required training accuracy of the bound depends on the Wasserstein-1 distance between the target distribution and the learned distribution. However, some conditional networks as the conditional normalizing flow are not trained to minimize the Wasserstein-1 distance. Consequently, a direct dependence of the bound on the training accuracy with respect to the KL divergence would be helpful. Under very strong assumptions, the continuity in Lemma 1 has been shown for KL in Baptista et al. (2023). This could be used to derive a similar statement.

Furthermore, our bound is a worst case bound and is not always practical if the constants are large. It would be interesting to check whether tightness of the bound can be shown for some examples.

Acknowledgement

P.H. acknowledges funding by the German Research Foundation (DFG) within the project of the DFG-SPP 2298 “Theoretical Foundations of Deep Learning” and F.A. within project EF3-7 of Germany‘s Excellence Strategy – The Berlin Mathematics Research Center MATH+. The authors want to thank B. Sprungk for posing the question considered in this paper, namely if there are guarantees that conditional generative NNs work well for single observations. Moreover, many thanks to J. Hertrich for fruitful discussions and for suggesting the example in the appendix.

References

- Adler & Öktem (2018) Jonas Adler and Ozan Öktem. Deep Bayesian inversion. arXiv preprint arXiv:1811.05910, 2018.

- Altekrüger & Hertrich (2023) Fabian Altekrüger and Johannes Hertrich. WPPNets and WPPFlows: The power of Wasserstein patch priors for superresolution. SIAM Journal on Imaging Sciences, 16(3):1033–1067, 2023.

- Altekrüger et al. (2023) Fabian Altekrüger, Alexander Denker, Paul Hagemann, Johannes Hertrich, Peter Maass, and Gabriele Steidl. PatchNR: learning from very few images by patch normalizing flow regularization. Inverse Problems, 39(6), 2023.

- Anderson (1982) Brian D.O. Anderson. Reverse-time diffusion equation models. Stochastic Processes and their Applications, 12(3):313–326, 1982.

- Andrle et al. (2021) Anna Andrle, Nando Farchmin, Paul Hagemann, Sebastian Heidenreich, Victor Soltwisch, and Gabriele Steidl. Invertible neural networks versus MCMC for posterior reconstruction in grazing incidence x-ray fluorescence. In Abderrahim Elmoataz, Jalal Fadili, Yvain Quéau, Julien Rabin, and Loïc Simon (eds.), Scale Space and Variational Methods in Computer Vision, pp. 528–539. Springer International Publishing, 2021.

- Ardizzone et al. (2019) Lynton Ardizzone, Carsten Lüth, Jakob Kruse, Carsten Rother, and Ullrich Köthe. Guided image generation with conditional invertible neural networks. arXiv preprint arXiv:1907.02392, 2019.

- Arjovsky et al. (2017) Martin Arjovsky, Soumith Chintala, and Léon Bottou. Wasserstein generative adversarial networks. In International Conference on Machine Learning, pp. 214–223. PMLR, 2017.

- Baptista et al. (2023) Ricardo Baptista, Bamdad Hosseini, Nikola B. Kovachki, Youssef M. Marzouk, and Amir Sagiv. An approximation theory framework for measure-transport sampling algorithms. arXiv preprint arXiv:2302.13965, 2023.

- Batzolis et al. (2021) Georgios Batzolis, Jan Stanczuk, Carola-Bibiane Schönlieb, and Christian Etmann. Conditional image generation with score-based diffusion models. arXiv preprint arXiv:2111.13606, 2021.

- Behrmann et al. (2021) Jens Behrmann, Paul Vicol, Kuan-Chieh Wang, Roger Grosse, and Joern-Henrik Jacobsen. Understanding and mitigating exploding inverses in invertible neural networks. In Arindam Banerjee and Kenji Fukumizu (eds.), Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pp. 1792–1800. PMLR, 2021.

- Dashti & Stuart (2017) M. Dashti and A. M. Stuart. The Bayesian approach to inverse problems. In Handbook of Uncertainty Quantification, pp. 311–428. Springer, 2017.

- De Bortoli (2022) Valentin De Bortoli. Convergence of denoising diffusion models under the manifold hypothesis. Transactions on Machine Learning Research, 2022.

- Garbuno-Inigo et al. (2023) Alfredo Garbuno-Inigo, Tapio Helin, Franca Hoffmann, and Bamdad Hosseini. Bayesian posterior perturbation analysis with integral probability metrics. arXiv preprint arXiv:2303.01512, 2023.

- Gibbs & Su (2002) Alison L. Gibbs and Francis Edward Su. On choosing and bounding probability metrics. International Statistical Review / Revue Internationale de Statistique, 70(3):419–435, 2002.

- Gloeckler et al. (2023) Manuel Gloeckler, Michael Deistler, and Jakob H. Macke. Adversarial robustness of amortized Bayesian inference. In Andreas Krause, Emma Brunskill, Kyunghyun Cho, Barbara Engelhardt, Sivan Sabato, and Jonathan Scarlett (eds.), Proceedings of the 40th International Conference on Machine Learning, volume 202 of Proceedings of Machine Learning Research, pp. 11493–11524. PMLR, 23–29 Jul 2023.

- Goodfellow et al. (2014) Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Y. Bengio. Generative adversarial networks. Advances in Neural Information Processing Systems, 3, 2014.

- Gouk et al. (2021) Henry Gouk, Eibe Frank, Bernhard Pfahringer, and Michael J. Cree. Regularisation of neural networks by enforcing Lipschitz continuity. Machine Learning, 110(2):393–416, 2021.

- Grana et al. (2017) Dario Grana, Torstein Fjeldstad, and Henning Omre. Bayesian Gaussian mixture linear inversion for geophysical inverse problems. Mathematical Geosciences, 49(4):493–515, 2017.

- Hagemann et al. (2023) P. Hagemann, J. Hertrich, and G. Steidl. Generalized Normalizing Flows via Markov Chains. Elements in Non-local Data Interactions: Foundations and Applications. Cambridge University Press, 2023.

- Hagemann & Neumayer (2021) Paul Hagemann and Sebastian Neumayer. Stabilizing invertible neural networks using mixture models. Inverse Problems, 37(8), 2021.

- Hagemann et al. (2022) Paul Hagemann, Johannes Hertrich, and Gabriele Steidl. Stochastic normalizing flows for inverse problems: A Markov chains viewpoint. SIAM/ASA Journal on Uncertainty Quantification, 10(3):1162–1190, 2022.

- Hong et al. (2022) Seongmin Hong, Inbum Park, and Se Young Chun. On the robustness of normalizing flows for inverse problems in imaging. arXiv preprint arXiv:2212.04319, 2022.

- Horrace (2005) William C. Horrace. Some results on the multivariate truncated normal distribution. Journal of Multivariate Analysis, 94(1):209–221, 2005.

- Hosseini (2017) B. Hosseini. Well-posed bayesian inverse problems with infinitely divisible and heavy-tailed prior measures. SIAM/ASA Journal on Uncertainty Quantification, 5(1):1024–1060, 2017.

- Hosseini & Nigam (2017) B. Hosseini and N. Nigam. Well-posed Bayesian inverse problems: priors with exponential tails. SIAM/ASA Journal on Uncertainty Quantification, 5(1):436–465, 2017.

- Igashov et al. (2022) Ilia Igashov, Hannes Stärk, Clément Vignac, Victor Garcia Satorras, Pascal Frossard, Max Welling, Michael Bronstein, and Bruno Correia. Equivariant 3d-conditional diffusion models for molecular linker design. arXiv preprint arXiv:2210.05274, 2022.

- Kingma & Ba (2015) Diederik P. Kingma and Jimmy Ba. Adam: A method for stochastic optimization. In International Conference on Learning Representations, 2015.

- Kingma & Welling (2013) Diederik P Kingma and Max Welling. Auto-encoding variational bayes. arXiv preprint arXiv:1312.6114, 2013.

- Kirichenko et al. (2020) Polina Kirichenko, Pavel Izmailov, and Andrew Gordon Wilson. Why normalizing flows fail to detect out-of-distribution data. In Advances in Neural Information Processing Systems, NIPS’20, Red Hook, NY, USA, 2020. Curran Associates Inc.

- Latz (2020) Jonas Latz. On the well-posedness of Bayesian inverse problems. SIAM/ASA Journal on Uncertainty Quantification, 8(1):451–482, 2020.

- Lim et al. (2018) Jaechang Lim, Seongok Ryu, Jin Woo Kim, and Woo Youn Kim. Molecular generative model based on conditional variational autoencoder for de novo molecular design. Journal of cheminformatics, 10(1):1–9, 2018.

- Liu et al. (2021) Shiao Liu, Xingyu Zhou, Yuling Jiao, and Jian Huang. Wasserstein generative learning of conditional distribution. arXiv preprint arXiv:2112.10039, 2021.

- Lu & Lu (2020) Yulong Lu and Jianfeng Lu. A universal approximation theorem of deep neural networks for expressing probability distributions. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 3094–3105. Curran Associates, Inc., 2020.

- Lyu et al. (2022) Junlong Lyu, Zhitang Chen, Chang Feng, Wenjing Cun, Shengyu Zhu, Yanhui Geng, Zhijie Xu, and Yongwei Chen. Para-CFlows: -universal diffeomorphism approximators as superior neural surrogates. In Alice H. Oh, Alekh Agarwal, Danielle Belgrave, and Kyunghyun Cho (eds.), Advances in Neural Information Processing Systems, 2022.

- Marzouk & Xiu (2009) Y. Marzouk and D. Xiu. A stochastic collocation approach to Bayesian inference in inverse problems. Communications in Computational Physics, 6(4):826–847, 2009.

- Miyato et al. (2018) Takeru Miyato, Toshiki Kataoka, Masanori Koyama, and Yuichi Yoshida. Spectral normalization for generative adversarial networks. In International Conference on Learning Representations, 2018.

- Pidstrigach et al. (2023) Jakiw Pidstrigach, Youssef Marzouk, Sebastian Reich, and Sven Wang. Infinite-dimensional diffusion models for function spaces. arXiv preprint arXiv:2302.10130, 2023.

- Pinsker (1963) MS Pinsker. Information and information stability of random quantities and processes. Technical report, Foreign Technology DIV Wright-Patterson AFB, Ohio, 1963.

- Salmona et al. (2022) Antoine Salmona, Valentin De Bortoli, Julie Delon, and Agnès Desolneux. Can push-forward generative models fit multimodal distributions? In Alice H. Oh, Alekh Agarwal, Danielle Belgrave, and Kyunghyun Cho (eds.), Advances in Neural Information Processing Systems, 2022.

- Sohn et al. (2015) Kihyuk Sohn, Honglak Lee, and Xinchen Yan. Learning structured output representation using deep conditional generative models. In Corinna Cortes, Neil D. Lawrence, Daniel D. Lee, Masashi Sugiyama, and Roman Garnett (eds.), Advances in Neural Information Processing Systems 28: Annual Conference on Neural Information Processing Systems, Montreal, Quebec, Canada, pp. 3483–3491, 2015.

- Song et al. (2021a) Yang Song, Conor Durkan, Iain Murray, and Stefano Ermon. Maximum likelihood training of score-based diffusion models. Advances in Neural Information Processing Systems, 34:1415–1428, 2021a.

- Song et al. (2021b) Yang Song, Jascha Sohl-Dickstein, Diederik P Kingma, Abhishek Kumar, Stefano Ermon, and Ben Poole. Score-based generative modeling through stochastic differential equations. In International Conference on Learning Representations, 2021b.

- Sprungk (2020) Björn Sprungk. On the local Lipschitz stability of Bayesian inverse problems. Inverse Problems, 36(5), 2020.

- Stuart (2010) A. M. Stuart. Inverse problems: A Bayesian perspective. Acta Numerica, 19:451–559, 2010.

- Sullivan (2017) T. J. Sullivan. Well-posed Bayesian inverse problems and heavy-tailed stable quasi-banach space priors. Inverse Problems in Imaging, 11(5):857–874, 2017.

- Tallis (1963) G. M. Tallis. Elliptical and radial truncation in normal populations. Annals of Mathematical Statistics, 34:940–944, 1963.

- Tashiro et al. (2021) Yusuke Tashiro, Jiaming Song, Yang Song, and Stefano Ermon. CSDI: Conditional score-based diffusion models for probabilistic time series imputation. In A. Beygelzimer, Y. Dauphin, P. Liang, and J. Wortman Vaughan (eds.), Advances in Neural Information Processing Systems, 2021.

- Teshima et al. (2020) Takeshi Teshima, Isao Ishikawa, Koichi Tojo, Kenta Oono, Masahiro Ikeda, and Masashi Sugiyama. Coupling-based invertible neural networks are universal diffeomorphism approximators. In Proceedings of the 34th International Conference on Neural Information Processing Systems, Vancouver, BC, Canada, 2020.

- Villani (2009) Cédric Villani. Optimal Transport: Old And New, volume 338. Springer, 2009.

- Weed & Bach (2019) Jonathan Weed and Francis Bach. Sharp asymptotic and finite-sample rates of convergence of empirical measures in Wasserstein distance. Bernoulli, 25(4A):2620 – 2648, 2019.

- Winkler et al. (2019) Christina Winkler, Daniel Worrall, Emiel Hoogeboom, and Max Welling. Learning likelihoods with conditional normalizing flows. arXiv preprint arXiv:1912.00042, 2019.

Appendix A Example on the Robustness of the MAP and Posterior

We like to provide an example that illustrates the stability of the posterior distribution in contrast to the MAP estimator and highlights the role of the MMSE estimator.

By the following lemma, see, e.g., (Grana et al., 2017; Hagemann et al., 2023), the posterior of a Gaussian mixture model given observations from a linear forward operator corrupted by white Gaussian noise can be computed analytically.

Lemma 9.

Let be a Gaussian mixture random variable. Suppose that

where is a linear operator and . Then the posterior is also a Gaussian mixture

with

and

Now, for some small we consider the random variable with simple prior distribution

and observations from with noise . The MAP estimator is given by

| (20) | ||||

| (21) | ||||

| (22) |

The above minimization problem has a unique global minimizer for which we computed numerically. Figure 3 (top) shows the plot of the function for and different values of . Clearly, small perturbations of near zero lead to qualitatively completely different -values, where a smaller noise level lowers the distance between the values for and . In other words, the MAP estimator is not robust with respect to perturbations of the observations near zero.

In contrast, using Lemma 9, we can compute the posterior

| (23) |

with

| (24) | ||||

| (25) |

Then the MMSE estimator is given by the expectation value of the posterior

| (26) | ||||

| (27) | ||||

| (28) | ||||

| (29) |

In Figure 3 (bottom), we see that the MMSE estimator shows a smooth transition in particular for larger noise levels, meaning that the estimator is robust against small perturbations of the observation near zero. Note that in case of a Gaussian prior in and white Gaussian noise, the MAP and MMSE estimators coincide.

Appendix B Local Lipschitz continuity of the generator for a latent space with infinite support

Here we show a weakened version of Lemma 1 leading to an arbitrary small additive constant. The main difference is the weaker assumption for all with and all with , which is fulfilled for continuously differentiable generators. For this we use the so-called truncated normal distribution (Horrace, 2005; Tallis, 1963). Let be the density of the standard normal distribution , then the density of the truncated normal distribution is given by

| (30) |

Lemma 10.

Let be the latent space. For any parameterized family of generative models with for all with and all with for some and some , it holds

for all with . The additive constant fulfills for .

Proof.

Let with , then it holds

| (31) | ||||

| (32) |

By the assumption on the generator , Lemma 1 yields

| (33) |

Consequently, it suffices to show that for with the term vanishes for . By definition, it holds

| (34) | ||||

| (35) | ||||

| (36) | ||||

| (37) | ||||

| (38) |

The first term vanishes exponentially in by the density , and for the second term note that for .∎

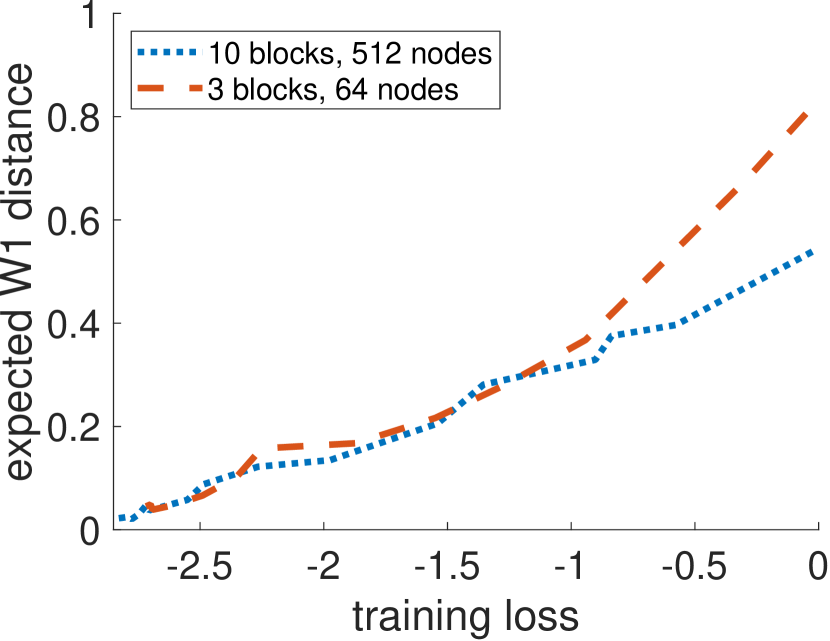

Appendix C Experimental demonstration of assumption (6)

Here we experimentally demonstrate that the expectation in (6) gets small when training a conditional generative network. For this, we consider a conditional normalizing flow as an example, consisting of three and ten Glow coupling blocks111available at https://github.com/VLL-HD/FrEIA with fully connected subnets with one hidden layer and 64 and 512 nodes, respectively. As in Appendix A, we choose a two-dimensional Gaussian mixture model with six modes as prior distribution and additive Gaussian noise with standard deviation 0.5 for the noise model. The forward operator is chosen to be the identity. Then we train the conditional normalizing flow for 100000 optimizer steps using Adam Kingma & Ba (2015) with a learning rate of and a batch size of 1024. Note that we can analytically compute the posterior distribution by Lemma 9.

In Figure 4 we visualize the expectation in (6) with respect to the training loss of the conditional normalizing flow, which is, up to a constant, equal to the KL, see Section 3.1. Obviously, the expectation (6) gets small when minimizing the training loss of the conditional normalizing flow. We computed the Wasserstein distance using POT 222available at https://github.com/PythonOT/POT and draw 20000 samples from each distribution. Moreover, we discretized the expectation by drawing 30 observations.