Clustering Multivariate Time Series using Energy Distance

Abstract

A novel methodology is proposed for clustering multivariate time series data using energy distance defined in Székely and Rizzo (2013). Specifically, a dissimilarity matrix is formed using the energy distance statistic to measure separation between the finite dimensional distributions for the component time series. Once the pairwise dissimilarity matrix is calculated, a hierarchical clustering method is then applied to obtain the dendrogram. This procedure is completely nonparametric as the dissimilarities between stationary distributions are directly calculated without making any model assumptions. In order to justify this procedure, asymptotic properties of the energy distance estimates are derived for general stationary and ergodic time series. The method is illustrated in a simulation study for various component time series that are either linear or nonlinear. Finally the methodology is applied to two examples; one involves GDP of selected countries and the other is population size of various states in the U.S.A. in the years 1900–1999.

Keywords: Characteristic function; clustering; dissimilarity measure; energy distance; hierarchical clustering; stationarity; time series

Mathematics Subject Classification: Primary 62M10, 62H30; Secondary 62H20, 62H12.

1 Introduction

Clustering is an important concept in statistics in which data is partitioned into groups where within each group, the data share similar characteristics. By now, there are a plethora of clustering algorithms for forming such partitions (e.g., K-means and to some extent CART). Most of these algorithms group data according to some notion of similarity (or dissimilarity) from which the data are then clustered into various groups; see Xu and Tian (2015) for a review of such procedures. That is, the data are partitioned into the same group if each member is close to each other relative to a similarity measure. The goal of this paper is to consider clustering of the component series in a multivariate time series setting, based on energy distance (see Székely and Rizzo, 2013) applied to the joint distributions of the component time series. A key advantage of this method is that the procedure is nonparametric and based on measures of closeness of joint distributions as measured through their characteristic functions. This is in contrast to parametric procedures where the clustering is performed via the parametric fitting to some family of models or to second order properties derived from autocorrelation functions; see references below. Shumway (1982) is an early and important contribution to discriminant analysis of time series that can be viewed as a precursor to the more general approach of our paper. The characteristic function is always well defined even in cases where we deal with multivariate (not necessarily normal) distributions. Lemma 2.1 shows that calculation of a suitable distance between characteristic functions is equivalent to calculation of the Euclidean distance between observations. Therefore, applying characteristic function techniques relieves the burden of distributional assumptions (which can be quite challenging in high dimensions) and at the same time provides a computationally feasible way to implement multivariate time series clustering. Zhang and An (2018) considers clustering based on pairwise distributions via copulas. However, due to the complexity of estimating joint distributions, their method was not extended to joint distributions beyond lagged pairs of observations.

To fix ideas, consider a -dimensional time series whose component series are to be clustered. Based on consecutive observations, say , the prototypical strategy is to form a measure of dissimilarity between each pair of component series. Once a measure of dissimilarity between the component series is decided upon, then a dissimilarity matrix is computed. This matrix is then used as the input to obtain the clustering via algorithms such as K-means, fuzzy C-means, spectral clustering and hierarchical clustering. The true number of clusters, which is required for the former three methods, is typically not known a priori; for this reason we shall focus on hierarchical clustering. In this method each component at the initial step belongs to its own cluster; at each successive step, the most similar pairs of clusters are recursively merged. The standard algorithms that facilitate cluster merging include complete linkage, single linkage, average linkage, centroid linkage and Ward’s linkage (Batagelj, 1988; James et al., 2013; Murtagh and Legendre, 2014). A hierarchy is obtained wherein the most similar components are in the same cluster and as one moves up the hierarchy, the clusters become more and more dissimilar. The hierarchy is visualized as a dendrogram and is the main output of this algorithm. Procedures such as the average silhouette width (see Kaufman and Rousseeuw, 2009) can be used to determine the final number of clusters from the dendrogram.

Various dissimilarity measures for clustering time series are catalogued in Liao (2005); Fu (2011); Montero and Vilar (2014); Aghabozorgi et al. (2015); Maharaj et al. (2019) and the references therein. Typically one considers features such as autocorrelation, partial autocorrelation, periodogram, spectral density or the copula of joint distributions—the distances between these features forms the dissimilarity measure (see Galeano and Peña, 2000; Caiado et al., 2006; Díaz and Vilar, 2010; Zhang and An, 2018). Dynamic time warping (DTW) utilizes a different approach where one finds an optimal mapping such that, the paired time series under the mapping minimizes a specific distance (see Berndt and Clifford, 1994). Particularly relevant to our work is the paper of Zhang and Chen (2018), where a two dimensional version of the Kolmogorov-Smirnov statistic is used as the dissimilarity measure between distributions of lagged components. The methods mentioned so far are nonparametric, but with the exception of the copula procedure, are based primarily on second order properties of the processes. As such the “distance” employed for clustering compares moments, not distributions, as it is developed later in this article. Model based approaches typically assume the component time series are realizations of ARIMA or GARCH processes; clustering is then performed via the parametric fitting to the specified model. Examples for distances in this class include Piccolo distance, Maharaj distance and cepstral-based distance (see Piccolo, 1990; Maharaj, 2000; Kalpakis et al., 2001; Savvides et al., 2008). General dissimilarity measures between time series which are based on their spectral densities have been studied by Kakizawa et al. (1998), Taniguchi and Kakizawa (2000, Ch. 6). Given two time series with spectral density matrices , , these authors defined a dissimilarity (or disparity) measure by

for a suitable function which has to satisfy that and when . For instance, choosing we have the Kullback-Leibler divergence.

In a time series setting, it is important to have dissimilarity measures that go beyond just the marginal distribution of the individual components. That is, the dissimilarity measure should be based on the joint distributions of the individual lagged components. Specifically, for a fixed lag , we consider the dissimilarity between the distributions of the dimensional time series and which will be measured through the energy distance of Székely and Rizzo (2013).

Energy distance, denoted by , see Section 2 for the definition, is nonnegative and has the property that holds if and only if the joint distributions of and are the same. This property for a dissimilarity measure holds only for the copula case. We provide theoretical justification for the use of the energy distance statistic. In particular, we derive asymptotic properties for the energy distance statistic for stationary ergodic time series. Additionally, energy distance works well with heavy tailed data which is generally not the case for other dissimilarity measures. Although we assume the components are of equal length, this is only for the sake of convenience; the results of this paper can be easily extended to the situation where the lengths of the time series vary across components.

The rest of the paper is organized as follows. Section 2 defines the energy distance between any two distributions. In Section 3 we present the main theorems on consistency and characterizing limit distributions of the energy distance statistic. Section 4 discusses the multivariate time series clustering algorithm. Various clustering tasks on simulated data are considered in Section 5; we experimentally obtain and compare the performance of the proposed methodology to some competing methods. Our proposed procedure performed generally better when clustering nonlinear and multivariate VAR time series than other methods. The ACF/PACF based procedures did well when the underlying component series are well differentiated by their second order properties such as, for example, Gaussian linear models. In these situations, some of the periodogram based methods outperformed our method as did the ARMA-model based method. However, this is not too surprising since these particular procedures are tuned well for this special class of models. Further details on the simulations and performance can be found in Section 5. Two real world data sets are also considered. The first is the annual GDP data for selected countries and the second involves the population growth for a number of states in the U.S.A. in the years 1900–1999. Proofs of all the main results in this paper are deferred to the Appendix.

2 Energy Distance between Distributions

Before introducing energy distance, it will be helpful to first fix some notation. Throughout this paper, the inner-product between vectors is denoted by and let . For a complex number , where is the imaginary number and the complex modulus is denoted by . Further, if is a random vector then and denote i.i.d copies of .

Let and denote -dimensional random vectors with characteristic functions and respectively. The energy distance (Székely and Rizzo, 2013) between and is defined by

| (2.1) |

where is the infinite measure given by

| (2.2) |

and . Other weight functions can also be used; see Remark 1 for more details. The significance of using this particular weight function in evaluating (2.2) is that the integral (2.1) can be explicitly calculated, as shown in the following lemma.

Lemma 2.1.

Consider random vectors in . If then . Furthermore,

| (2.3) |

The proof is provided in the Appendix. Note that (2.3) provides a simple formula for and it only depends on Euclidean distances between random vectors. Lemma 2.1 implies calculation of requires finite first moments to guarantee finiteness of the energy distance statistic. The expression we obtain here is similar to the maximum mean discrepancy (MMD), as given by Gretton et al. (2012).

It is clear from (2.1) that is nonnegative and equality holds if and only if and have the same distribution. As mentioned earlier, this simple observation is the basis for the clustering methodology that we consider in the following section. Indeed we can obtain sample estimates for and then calculate a dissimilarity measure between the distributions of and ; consequently, can be employed for clustering. The method is completely nonparametric and easy to implement. For illustration purposes we display the theoretically calculated energy distance in the two examples below.

Example 1.

Let have a standard normal distribution. For a straightforward calculation yields , where is the cdf of the standard normal. It then follows that for any and ,

where .

Example 2.

Let have a Laplace distribution with density , where . For , . Then,

Remark 1.

Alternatively, consider probability measures instead of in (2.2), such as a Gaussian measure; see Hong et al. (2017). Employing a probability measure guarantees finiteness of the integral without assuming that the random vectors and have finite means. Although we use the in (2.2) associated with energy distance, similar results can be obtained with replaced by a probability measure. We give a few details to be more specific: let denote the distance (2.1) with replaced by a probability measure . Then, easy calculations show that the counterpart of (2.3) is given by

where is the characteristic function of and denotes the real part of a complex number. Hence, choosing whose characteristic function is explicitly known yields different formulas for . For example if is the Gaussian measure given by for and some , then so that

3 Empirical Energy Distance Statistic for Time Series

Let be a stationary and ergodic time series, where . Denote the stationary distribution of this process by . We will now show how to empirically estimate based on observations using the empirical characteristic function and obtain the asymptotic properties of this estimator. Although we have assumed that the sample sizes of and are the same, this is not necessary since we are only interested estimating the marginal characteristic functions. It is straightforward to adapt our results to the case of unequal sample sizes. Let and similarly define . The estimate of is given by

Leveraging (2.3) we can write as the -statistic,

| (3.1) |

We thus have the sample estimate that can be computed easily and it is based solely on the distance between the observations. Note that (3.1) is computable even in the case of multivariate observations (dependent or not). The following theorem shows that is a consistent estimator for :

Theorem 3.1.

Consider stationary and ergodic time series , where and let have the same distribution as . Assuming , we have as

| (3.2) |

The proof is provided in the Appendix and it involves studying the asymptotic behavior of the empirical characteristic function process. To obtain the asymptotic distribution, we need additional moment assumptions and the notion of weak dependence. In what follows, assume that is an -mixing time series with rate function . Recall the definition of -mixing (Doukhan, 1994, p. 18): for integers , the mixing rate function is defined by

where the suprema is taken over , and , respectively. The process is then said to be -mixing if as . The following theorem characterizes the asymptotic distributions, whereby the rate of convergence differs according to whether or not the distributions of and are equal.

Theorem 3.2.

Consider stationary and ergodic time series where such that for some . Set and write and . Assume that for some the following hold:

| (3.3) |

-

1.

If and have the same distribution then,

where is a complex-valued mean-zero Gaussian process with covariance structure for given by

(3.4) -

2.

If and do not have the same distribution then,

where .

Theorems 3.1 and 3.2 state that under minimal assumptions is a consistent estimator for and under additional moment and mixing conditions, converges in distribution, suitably normalized. The rates of convergence are different depending on whether or not is equal in distribution to . In particular, we see that converges to a non-degenerate random variable when and have the same distribution, but tends to infinity otherwise.

4 Multivariate Time Series Clustering

4.1 Dissimilarity metric based on -dimensional joint distributions

Consider observations from a multivariate time series in . In this section, a general methodology for clustering component time series based on -dimensional distributions, for a fixed lag , is presented. We compute a pairwise dissimilarity matrix using the energy distance on these joint distributions and then apply a hierarchical clustering algorithm to classify the data.

The dissimilarity measure based on the -lagged and components of is given by , where and for The energy distance dissimilarity measure is given by ; see also Fokianos and Pitsillou (2018). Note that and due to symmetry, . In this way, we form the energy distance dissimilarity matrix .

To obtain the clustering, an agglomerative hierarchical clustering method (see for example, Batagelj, 1988) is used which we briefly describe below. We start with the original components, as nodes, and successively merge nodes (or clusters) to form new clusters. The inter-cluster dissimilarities are then obtained as for . The least dissimilar pair of components, say and , are now merged; note that only inter-cluster dissimilarities need to be updated. We employ the generalized Ward’s linkage algorithm in this paper which has an update formula for computing the dissimilarity between the merged cluster with for . This formula, known as the Lance-Williams formula for generalized Ward’s linkage, is given by

| (4.1) |

where denotes the number of components in cluster . Proceeding forward, suppose now there are clusters with a inter-cluster dissimilarity matrix . The pair with the least dissimilarity are merged with the resulting inter-cluster dissimilarities (for the clusters) are given by (4.1). The clustering algorithm is summarized in Algorithm 1.

If the true number of clusters () is known, then one can obtain clusters from the hierarchical clustering. As the true number of clusters are usually not known, metrics such as the average silhouette width (Kaufman and Rousseeuw, 2009) can be used to determine the final number of clusters. The silhouette coefficients are defined for each component and are based on the tightness and separation of the clusters using the dissimilarity matrix . Specifically, if we obtain clusters from the hierarchical clustering, then the -node silhouette coefficient is defined as

where is the average dissimilarity of component to all components in , is the cluster that contains the component and is the cluster which satisfies . Clearly and the closer is to one, the better the quality of the clustering. The average silhouette width is obtained as the average value of among all the components. The average silhouette width is computed for clusters for . The value of which maximizes the average silhouette width is the most appropriate choice for the number of clusters.

4.2 Clustering via Lagged Bivariate Distributions

Instead of using -dimensional distributions for comparison one could simplify and restrict attention to lagged bivariate distributions. More precisely, for each compute the energy distance , where and . We also include , the lag zero dissimilarity matrix which computes the pairwise dissimilarity between the marginal distributions of the components. This yields dissimilarity matrices, for which contain the distances between and . An overall (total) dissimilarity matrix is defined by . A similar approach can be found in Zhang and An (2018) and Zhang and Chen (2018) where a (weighted) sum of dissimilarity matrices up to some maximum lag is used as the final dissimilarity matrix. The hierarchical clustering method described Subsection 4.1 is then applied to .

5 Empirical Comparisons and Applications

To assess the performance of our method we consider several simulated data sets. In addition, we apply our method to two real data sets in this section. Three clustering tasks with simulated data are considered, where for the first two, the experiments of Díaz and Vilar (2010) are performed for comparison. Next, the third simulated data set consists of clustering the components of a 40 dimensional VAR time series. The two real data sets concern the G.D.P data of the world’s most developed countries between, as observed between 1990 to 2011, and the populations of a subset of states in the U.S.A. between the years of 1900 to 1999.

5.1 Simulation Examples

In the experiments we applied Algorithm 1 with different lags and . See Remark 2 below for comments on the choice of lag . For comparison, various competing clustering methods using different dissimilarity measures (15 in total) that have been proposed in the existing literature were considered. In the ACF based methods (see Galeano and Peña, 2000), the dissimilarity measure is equal to a geometrically downweighted distance between the estimated ACF of each pair of components. In symbols, if and represent the estimated autocorrelations of the and components at lag respectively, then the dissimilarity measure is given by , where is the maximum lag considered and . In our simulations we take and . The analogous PACF based methods are also considered wherein the estimated ACF coefficients are replaced with the corresponding estimated PACF coefficients. In the graphs displaying the results below, these procedures are labeled by ACFLh and PACFLh while the energy-based methods are labeled EnergyLh, where is the lag.

We also compared these methods with periodogram-based methods of Caiado et al. (2006) that calculates Euclidean distances between the periodograms and log-periodograms. In addition, integrated periodogram of Casado de Lucas (2010), which computes the integral difference between the cumulative versions of the periodograms, is also included. Finally, the ARMA model based dissimilarity measures developed in Piccolo (1990) and Maharaj (2000) were also compared. The above methods obtain different dissimilarity matrices from which hierarchical clustering is then performed using generalized Ward’s method. We found that in our simulations, the clustering performance with energy distance was the highest with Ward’s linkage. Other linkage algorithms with respect to competing dissimilarity measures did not have significantly different performance. These methods are labeled as PER, PER.LP, INT.PER, AR.MAH, and AR.PIC in the graphs below.

When the ground truth is known, we can compare the clustering methods using clustering evaluation metrics. Specifically, we consider the similarity index of Gavrilov et al. (2000) which is defined as

where is the ground truth of the clusters, is the clustering to be assessed, and

Here denotes the cardinality of a set. The similarity index takes values between 0 and 1, with 1 corresponding to perfect clustering, that is, and are identical. Other metrics were also considered such as the Rand index (Rand, 1971), adjusted Rand index (Hubert and Arabie, 1985) and a leave-one-out cross-validation (Tan et al., 2006). However, the choice of metric did not have much impact on the relative comparisons between the various methods and we will only report the similarity index in our results.

Example 5.1

For the first experiment, a time series consisting of 16 independent components is generated. Each component is of length and is rescaled to have mean zero and standard deviation one. We consider four clusters each of which contain four time series generated by the following models: (i) threshold autoregressive (TAR) , (ii) exponential autoregressive (EXPAR) , (iii) linear moving average (MA) and (iv) nonlinear moving average (NLMA) . The sequence is assumed to be iid with a standard normally distribution in all cases. The similarity index is obtained against the ground truth of clusters, for each of the 15 methods. This experiment was repeated 200 times and the boxplots of the similarity index are shown in Figure 1. The dots in the figure denote the outliers in the boxplots. In particular, our methods with positive lags have perfect clustering in all but three instances in our experiments. It is clear that the energy distance based methods, except for lag 0, are nearly perfect in recovering the true clusters.

Example 5.2

A very similar setup is considered in this example where we instead have five clusters, with four time series each, from the following ARMA models: (i) AR(1): , (ii) MA(1): , (iii) AR(2): , (iv) MA(2): , (v) ARMA(1,1): . The sequence is iid normally distributed. In this simulation we consider the lengths of the time series to be . From Figure 2 we see that the best performance is achieved by , and the PACF based methods, followed by and . This is due to the ARMA coefficients, PACF and log-periodograms being separated. It is not surprising that with lag 0 performed the worst because all the marginal distributions were standard normal in the case. The ACF based methods performed worse because the theoretical auto-covariance coefficients are not well separated. Indeed, the true ACFs of the AR(2) and ARMA(2) considered here are very close to each other. Furthermore, the autocorrelation at lag 1 of the AR(1) is 0.5 and that of MA(1) is 0.47; even though the true ACF of the MA(1) process is exactly zero for higher lags while that of the AR(1) decreases geometrically by a factor of 0.5, in practice this means that the estimated ACFs of the MA(1) and AR(1) will be rather close as well. As the ACF determines the joint distributions for Gaussian ARMA time series, the energy based methods do see a reduction in performance. However, with the correct specification of the lag , we observe that the energy distance find the correct clustering most of the time.

Example 5.3

In this example, we consider clustering a 40 dimensional time series. We generate four independent multivariate time series, each belonging to according to the following models. (i) VAR(1), : , where the matrix is constructed as equally spaced numbers between and column-wise which is then standardized to have spectral norm less than . The sequence is iid . (ii) VAR(1), : where is the same as above and the only change being that the components of are independent with a Student’s t distribution with 2 degrees of freedom. (iii) VAR(2), : , where similar to , the matrices and are constructed using equally spaced numbers between and , and and respectively. and are standardized using the maximum eigenvalue of . The is iid . (iv) VAR(2), : with the only change being that the components of are independent and distributed as Student’s t with 2 degrees of freedom. With these four underlying clusters, the clustering performance with respect to similarity index is shown in Figure 3. Our proposed method outperformed all the competing methods. The clustering performance was nearly the same for the energy distance based method for lags . This suggests that components with the same marginal distributions have been clustered correctly and inclusion of further lagged joint distributions did not appreciably improve clustering performance.

Remark 2.

In applications we need to decide on a suitable choice for , the size of the joint distributions used for clustering. If there is clustering at lag , then one would expect clustering to also be present at lags . However, the nature of the clustering could be different as a function of lag. For instance there might be strong associations or disassociation in the component time series at lag 3 which is not so evident at lags 0–2. The other hurdle is that as the lag increases, the dissimilarity measure may incur more noise and hence less useful for providing meaningful clusters. On the other hand, for small, there may not be much power in discriminating the individual time series. To some extent, this sort of behavior is manifested in Figures 2 and 3. In the case our proposed clustering procedure does a reasonably good job in correctly identifying the clusters. This performance is only improved as one uses and . However, for there is a slight falloff in the performance of the clustering. The idea of choosing an optimal will be the subject of a future investigation.

5.2 Real Data Examples

Application to annual G.D.P. data

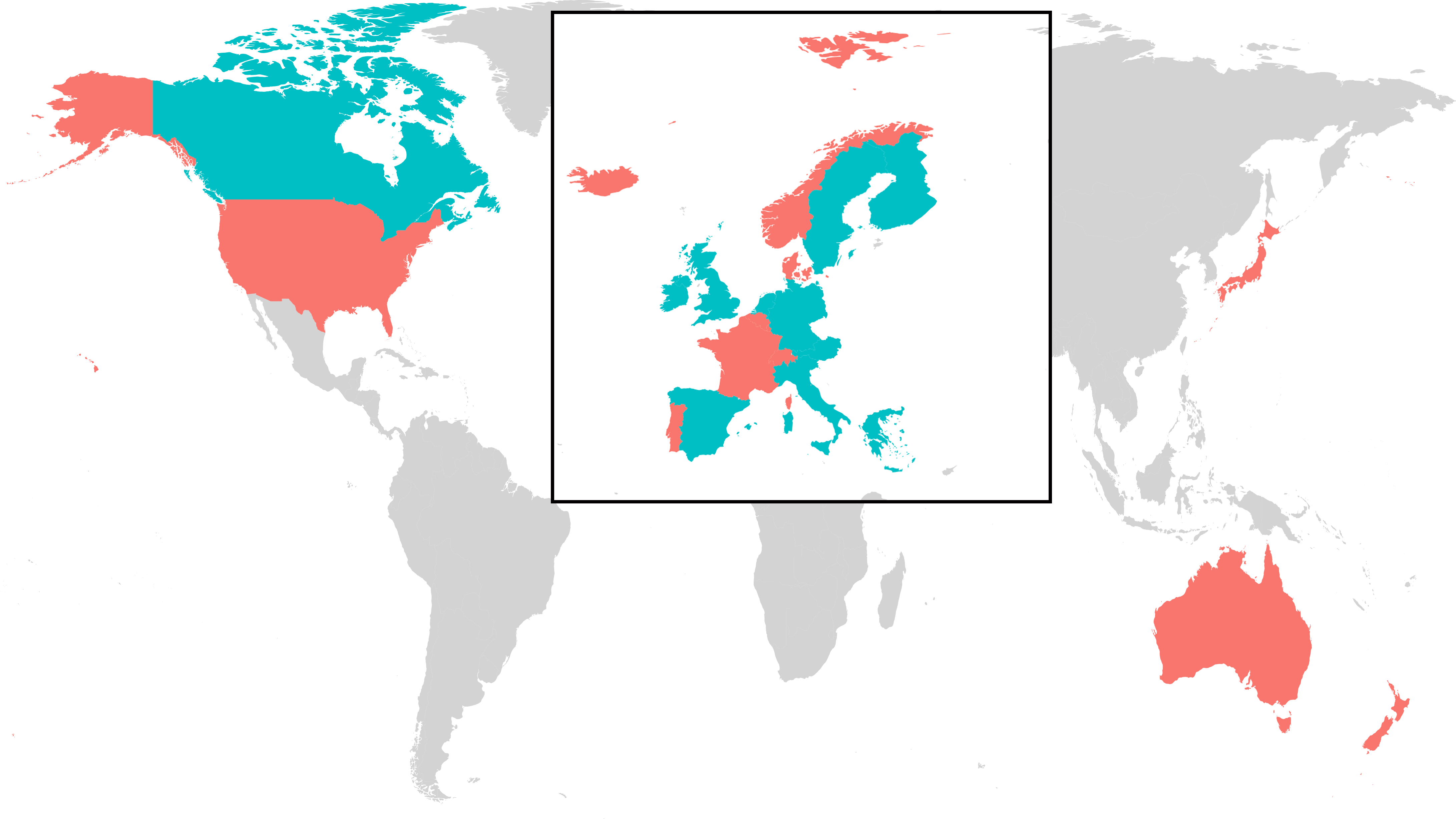

In this example, we considered the annual real gross domestic product (GDP) data obtained from https://www.conference-board.org/us/, which was also studied in Zhang and An (2018). A set of 23 of the most developed countries in the world was used for the years 1980–2019: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, United Kingdom, Canada, United States, Australia, New Zealand and Japan. In total this is a 23 dimensional time series with observations each. We used the annual log growth rate, calculated for the country as as the input time series. Each components was re-normalized to have mean zero and standard deviation one. Energy distance with lag 1 is applied to this dataset; higher values of lag did not work well due to being too small.

In this case, the maximum average silhouette width was obtained with 2 clusters and is shown in Figure 4. Figure 5 presents the the clustering on a world map. Spain, Netherlands, Finland, Ireland, Greece, Austria, Canada, Sweden, Germany, United Kingdom and Italy form the blue cluster. This cluster consists of most mainland European countries and includes the United Kingdom, Ireland and Canada. The red cluster consisted of France, Belgium, Australia, Denmark, United States, Ireland, Iceland, New Zealand, Switzerland, Portugal, Norway, Japan and Luxembourg. A possible interpretation of this result is that the blue group includes countries that spend a considerable amount of their budget on safety net programs when compared to most of the countries in the red cluster.

U.S.A. Population Data

Consider the population of twenty states in the U.S.A. between the years of 1900–1999. This dataset, with dimension 20 and length , was studied in Kalpakis et al. (2001); Zhang and An (2018); Zhang and Chen (2018) and is made available from https://www.csee.umbc.edu/ kalpakis/TS-mining/ts-datasets.html. Kalpakis et al. (2001) identified two clusters, where one set of states had an exponentially increasing trend whereas the second set of states had a stabilizing trend. The states in the first cluster were California, Colorado, Florida, Georgia, Maryland, North Carolina, South Carolina, Tennessee, Texas, Virginia and Washington. The latter cluster consisted of Illinois, Massachusetts, Michigan, New Jersey, New York, Oklahoma, Pennsylvania, North Dakota and South Dakota. The raw data was used to calculate the log growth rate for each state, that is, , where is the population of state at time . Each of the time series were normalized to have zero mean and unit standard deviation. The results of clustering with are shown in Figure 6; the corresponding map of the U.S.A. is displayed in Figure 7. In this example the clustering was remarkably consistent when varied from 0 to 5. This suggests that the stationary distributions differ between clusters. The average silhouette score suggest three clusters in this case. California, Colorado, Florida, Georgia, Maryland, Virginia, Washington, Illinois and Massachusetts are included in the red cluster and all but the last two have exponentially increasing trends. North Carolina, South Carolina and Tennessee however were assigned to the green cluster. Texas forms it’s own separate cluster; the population growth data of Texas has different distribution compared to all the other states in this experiment. The trend based clustering assignments of Kalpakis et al. (2001) are partially recovered and our method identifies the differences in the underlying (lagged) stationary distributions among the obtained clusters.

Acknowledgements

The research of R. A. Davis was supported in part by NSF grant DMS 2015379 to Columbia University. We acknowledge computing resources from Columbia University’s Shared Research Computing Facility project, which is supported by NIH Research Facility Improvement Grant 1G20RR030893-01, and associated funds from the New York State Empire State Development, Division of Science Technology and Innovation (NYSTAR) Contract C090171, both awarded April 15, 2010. We also thank the referees for their helpful remarks which led to a greatly improved exposition.

References

- Aaronson et al. (1996) Aaronson J, Burton R, Dehling H, Gilat D, Hill T, Weiss B. 1996. Strong laws for - and -statistics. Transactions of the American Mathematical Society, 348(7):2845–2866.

- Aghabozorgi et al. (2015) Aghabozorgi S, Shirkhorshidi AS, Wah TY. 2015. Time-series clustering–a decade review. Information systems, 53:16–38.

- Batagelj (1988) Batagelj V. 1988. Generalized Ward and Related Clustering Problems. Classification and Related Methods of Data Analysis, 30:67–74.

- Berndt and Clifford (1994) Berndt DJ, Clifford J. 1994. Using Dynamic Time Warping to Find Patterns in Time Series. In Proceedings of the 3rd International Conference on Knowledge Discovery and Data Mining, AAAIWS’94, 359–370. AAAI Press.

- Caiado et al. (2006) Caiado J, Crato N, Peńa D. 2006. A periodogram-based metric for time series classification. Computational Statistics & Data Analysis, 50(10):2668–2684.

- Casado de Lucas (2010) Casado de Lucas D. 2010. Classification techniques for time series and functional data. Ph.D. thesis, Universidad Carlos III de Madrid.

- Davis et al. (2018) Davis RA, Matsui M, Mikosch T, Wan P. 2018. Applications of distance correlation to time series. Bernoulli, 24(4A):3087–3116.

- Díaz and Vilar (2010) Díaz SP, Vilar JA. 2010. Comparing several parametric and nonparametric approaches to time series clustering: a simulation study. Journal of Classification, 27(3):333–362.

- Doukhan (1994) Doukhan P. 1994. Mixing, volume 85 of Lecture Notes in Statistics. New York: Springer-Verlag.

- Fokianos and Pitsillou (2018) Fokianos K, Pitsillou M. 2018. Testing independence for multivariate time series via the auto-distance correlation matrix. Biometrika, 105:337–352.

- Fu (2011) Fu TC. 2011. A review on time series data mining. Engineering Applications of Artificial Intelligence, 24(1):164–181.

- Galeano and Peña (2000) Galeano P, Peña D. 2000. Multivariate analysis in vector time series. Resenhas do Instituto de Matemática e Estatística da Universidade de São Paulo, 4(4):383–403.

- Gavrilov et al. (2000) Gavrilov M, Anguelov D, Indyk P, Motwani R. 2000. Mining the stock market (extended abstract) which measure is best? In Proceedings of the sixth ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, 487–496.

- Gretton et al. (2012) Gretton A, Borgwardt KM, Rasch MJ, Schölkopf B, Smola A. 2012. A kernel two-sample test. The Journal of Machine Learning Research, 13(1):723–773.

- Hong et al. (2017) Hong D, Gu Q, Whitehouse K. 2017. High-dimensional time series clustering via cross-predictability. In Artificial Intelligence and Statistics, 642–651. PMLR.

- Hubert and Arabie (1985) Hubert L, Arabie P. 1985. Comparing partitions. Journal of Classification, 2(1):193–218.

- James et al. (2013) James G, Witten D, Hastie T, Tibshirani R. 2013. An Introduction to Statistical Learning. New York: Springer.

- Kakizawa et al. (1998) Kakizawa Y, Shumway RH, Taniguchi M. 1998. Discrimination and clustering for multivariate time series. Journal of the American Statistical Association, 93:328–340.

- Kalpakis et al. (2001) Kalpakis K, Gada D, Puttagunta V. 2001. Distance measures for effective clustering of ARIMA time-series. In Proceedings 2001 IEEE International Conference on Data Mining, 273–280. IEEE.

- Kaufman and Rousseeuw (2009) Kaufman L, Rousseeuw PJ. 2009. Finding Groups in Data: An Introduction to Cluster Analysis. New York: Wiley.

- Krengel (1985) Krengel U. 1985. Ergodic Theorems. Berlin: Walter de Gruyter & Co.

- Liao (2005) Liao TW. 2005. Clustering of time series data—a survey. Pattern Recognition, 38(11):1857–1874.

- Maharaj (2000) Maharaj EA. 2000. Cluster of Time Series. Journal of Classification, 17(2):297–314.

- Maharaj et al. (2019) Maharaj EA, D’Urso P, Caido J. 2019. Time Series Clustering and Classification. Computer Science and Data Analysis. Australia: CRC Press.

- Montero and Vilar (2014) Montero P, Vilar JA. 2014. TSclust: An Package for Time Series Clustering. Journal of Statistical Software, 62(1):1–43.

- Murtagh and Legendre (2014) Murtagh F, Legendre P. 2014. Ward’s Hierarchical Agglomerative Clustering Method: Which Algorithms Implement Ward’s Criterion? Journal of Classification, 31(3):274–295.

- Piccolo (1990) Piccolo D. 1990. A distance measure for classifying ARIMA models. Journal of Time Series Analysis, 11(2):153–164.

- Rand (1971) Rand WM. 1971. Objective criteria for the evaluation of clustering methods. Journal of the American Statistical Association, 66(336):846–850.

- Savvides et al. (2008) Savvides A, Promponas VJ, Fokianos K. 2008. Clustering of biological time series by cepstral coefficients based distances. Pattern Recognition, 41(7):2398–2412.

- Shumway (1982) Shumway RH. 1982. Discriminant analysis for time series. In Classification, pattern recognition and reduction of dimensionality, volume 2 of Handbook of Statistics, 1–46. Amsterdam: North-Holland.

- Stout (1974) Stout WF. 1974. Almost sure convergence. New York-London: Academic Press.

- Székely and Rizzo (2013) Székely GJ, Rizzo ML. 2013. Energy statistics: A class of statistics based on distances. Journal of Statistical Planning and Inference, 143(8):1249–1272.

- Székely et al. (2007) Székely GJ, Rizzo ML, Bakirov NK. 2007. Measuring and testing dependence by correlation of distances. The Annals of Statistics, 35(6):2769–2794.

- Tan et al. (2006) Tan PN, Steinbach M, Kumar V. 2006. Data Mining Introduction. Boston: Pearson Addison Wesley.

- Taniguchi and Kakizawa (2000) Taniguchi M, Kakizawa Y. 2000. Asymptotic Theory of Statistical Inference for Time Series. New York: Springer.

- Xu and Tian (2015) Xu D, Tian Y. 2015. A comprehensive survey of clustering algorithms. Annals of Data Science, 2(2):165–193.

- Zhang and An (2018) Zhang B, An B. 2018. Clustering time series based on dependence structure. PLoS ONE, 13(11):1–22.

- Zhang and Chen (2018) Zhang B, Chen R. 2018. Nonlinear Time Series Clustering Based on Kolmogorov-Smirnov 2D Statistic. Journal of Classification, 35(3):394–421.

Appendix A Appendices

A.1 Proof of Lemma 2.1

A.2 Proof of Theorem 3.1

We follow the steps from the proofs of Theorem 3.1 in Davis et al. (2018) and Theorem 2 in Székely et al. (2007). Accordingly, for we set

| (A.2) |

The processes and are sample means of i.i.d bounded processes. By the ergodic theorem (Theorem 3.5.7 in Stout (1974)) and on , the space of continuous functions on ; see Krengel (1985). So,

Thus it suffices to show

| (A.3) |

First, since we have almost surely

Fix . From the proof of Lemma 2.1, we rewrite

Let , where is the first component of . Due to a change of variables,

Applying the ergodic theorem for U-statistics according to Aaronson et al. (1996), as

Using the continuity of at zero we see via dominated convergence. Similarly for the remaining two terms. It then follows that almost surely,

Hence (A.3) holds, which concludes the proof.

A.3 Proof of Theorem 3.2

In the proof below, the symbol will denote a positive constant, whose value might change from line to line but it is not of particular interest. For , due to stationarity of ,

An application of Theorem 3(a) of Section 1.2.2 in Doukhan (1994) yields

Then, for

Due to the summability assumption ,

Similarly, . It then follows that

| (A.4) |

where . The proof of the theorem will rely on Lemma A.1(2) of Davis et al. (2018) stated below.

Lemma A.1.

Assume that for some and set . If the moment conditions (3.3) are satisfied with , then on compact sets for some complex-valued mean-zero Gaussian field with covariance structure

Due to Lemma A.1, on compact sets . But . So on the compact set defined in (A.2) for some , we obtain , where is a complex-valued mean-zero Gaussian process. The covariance structure is then given by

Proof of Theorem 3.2(i).

If , then so that on . By the continuous mapping theorem,

Let . From Markov’s inequality, dominated convergence and (A.4),

∎

Proof of Theorem 3.2(ii).

Now and have different distributions. Note that

From the almost sure convergence of on compact sets and the continuous mapping theorem,

where . Note that for complex numbers we have

Using this for and ,

Therefore, by Markov’s inequality, Jensen’s inequality, the dominated convergence theorem and (A.4), for any given ,

∎