Robustifying likelihoods by optimistically re-weighting data

Abstract

Likelihood-based inferences have been remarkably successful in wide-spanning application areas. However, even after due diligence in selecting a good model for the data at hand, there is inevitably some amount of model misspecification: outliers, data contamination or inappropriate parametric assumptions such as Gaussianity mean that most models are at best rough approximations of reality. A significant practical concern is that for certain inferences, even small amounts of model misspecification may have a substantial impact; a problem we refer to as brittleness. This article attempts to address the brittleness problem in likelihood-based inferences by choosing the most model friendly data generating process in a discrepancy-based neighbourhood of the empirical measure. This leads to a new Optimistically Weighted Likelihood (OWL), which robustifies the original likelihood by formally accounting for a small amount of model misspecification. Focusing on total variation (TV) neighborhoods, we study theoretical properties, develop inference algorithms and illustrate the methodology in applications to mixture models and regression.

Keywords: Coarsened Bayes; Data contamination; Mixture models; Model misspecification; Outliers; Robust inference; Total variation distance.

1 Introduction

Likelihood-based inference remains a broad and principled workhorse for conducting modern statistical analyses. Indeed, when the likelihood is correctly specified, there is arguably no substitute for likelihood-based inferences (see e.g. Zellner, 1988). Crucially, this need no longer be true if the statistical model is misspecified: in this setting, likelihood-based inferences may be misleading and lead to undesirable outcomes (Huber, 1964; Tsou and Royall, 1995; Huber, 2011; Rousseeuw et al., 2011). This has motivated a broad battery of methods for model comparison and goodness-of-fit assessment (see e.g Huber-Carol et al., 2012; Claeskens and Hjort, 2008). A key intent of any such analysis is to verify that the assumed likelihood is indeed consistent with the data at hand—so as to pre-emptively avoid model misspecification and the unreliable inferences this can lead to.

Yet, even with substantial care in model assessment, some amount of model misspecification is inevitable. Unfortunately, even small degrees of model misspecification can have dire consequences in certain settings; a problem we refer to as brittleness. Brittleness can occur in various applications, including in high dimensional problems (e.g. Bradic et al., 2011; Bradic, 2016; Zhou et al., 2020), in the presence of outliers and contaminating distributions (e.g. Huber, 1964, 2011), or for mixture models (e.g. Markatou, 2000; Miller and Dunson, 2019; Diakonikolas et al., 2020). This article is focused on robustifying likelihoods to avert such brittleness.

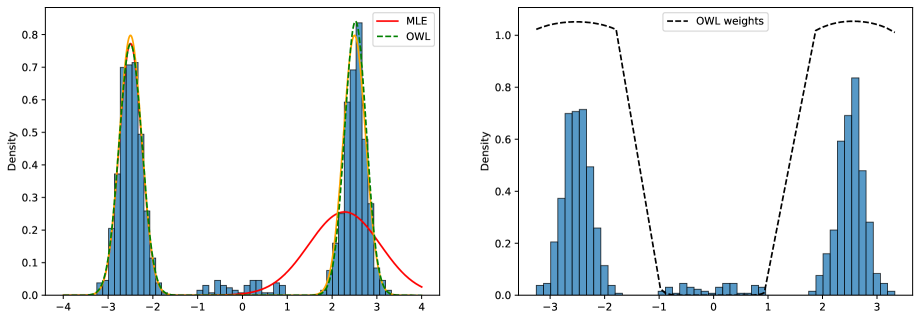

Figure 1 illustrates the problem of brittleness and our proposed solution for the setting of model-based clustering with kernel mixture models. Here, the vast majority of the data is perfectly modeled by a mixture of two well-separated Gaussians. However, a small fraction of the data have been corrupted, and are instead drawn uniformly from the space between the two modes. As the left hand panel demonstrates, the maximum likelihood estimate (MLE) accommodates the relatively small corruption by sacrificing a good fit on the much larger uncorrupted fraction of the data. Our proposal is to instead maximise an optimistically weighted likelihood (OWL) 111The code for the OWL methodology and all of the analysis in this paper can be found online at https://github.com/cjtosh/owl, which re-weights the likelihood terms according to how reasonable the data are under the posed model. The left hand panel shows that maximising OWL rectifies the issue of MLE, and the right hand panel shows the corresponding weights that achieve this outcome.

The origin of brittleness is intimately tied to the foundations of statistical science. Specifically, much of statistical theory and methodology assumes a domain expert capable of precisely modelling real-world phenomena. This idealised setting is sometimes referred to as the M-closed world (see Bernardo and Smith, 2009); and assumes that for a fixed but unknown parameterisation of the likelihood, we can recover the data-generating mechanism accurately. Conveniently for the statistician, this leaves computation and estimation as the only problems to be resolved. Unfortunately, the real world is not M-closed: even the most seasoned scientists often struggle with developing models that are flawless descriptions of all aspects of the data they seek to model. As a result, inferences built on this assumption are often brittle (see e.g. Lindsay, 1994; Müller, 2013; Grünwald, 2011), and the advent of large scale and high-dimensional data has only exacerbated this problem.

Perhaps the oldest strategy for addressing this is to try to explicitly model the complexities of real data settings—such as outliers and data contamination—by using a more flexible model. Often, the corresponding likelihood functions correspond to mixture models, models with heavier tails, or semiparametric and nonparametric extensions. However, as one increases the complexity of the likelihood to combat model misspecification, one creates a host of new challenges. These include decreased interpretability, problems with parameter identifiability, and increased computational complexity. In addition, even with a more complex likelihood, some degree of model misspecification remains inevitable. As a result, even highly flexible likelihoods do not provide guaranteed protection against brittleness.

This has led to a renewed interest in robust statistics: rather than trying to adjust the likelihood function, many modern approaches instead derive guarantees that continue to hold under various forms of misspecification. This includes a large potpourri of contributions, ranging from model- and algorithm-specific methods (e.g. Bhatia et al., 2023; Diakonikolas et al., 2017, 2019, 2020) to general frameworks of obtaining robustified inferences (e.g. Bissiri et al., 2016; Jewson et al., 2018; Lyddon et al., 2018; Knoblauch et al., 2022; Lecué and Lerasle, 2020). Much of the methodological work in this area has taken one of three approaches: distance-based estimation Barp et al. (2019); Knoblauch et al. (2018); Cherief-Abdellatif and Alquier (2020); Briol et al. (2019); Matsubara et al. (2022); Dellaporta et al. (2022); Alquier et al. (2022); Chérief-Abdellatif and Alquier (2022), novel means of uncertainty quantification with a Bayesian flavour Lyddon et al. (2018); Huggins and Miller (2020); Pompe and Jacob (2021); Fong et al. (2021), or modified likelihood functions Hooker and Vidyashankar (2014); Ghosh and Basu (2016); Field and Smith (1994); Windham (1995); Markatou et al. (1997); Hadi and Luceño (1997); Markatou et al. (1998); Dupuis and Morgenthaler (2002). We will propose a novel methodology that roughly falls into this last category and focuses on finding robust parameter estimates based on a modification of the likelihood function. This means that our methodology is universally applicable to both frequentist and Bayesian methods, and is easier to interpret than distance-based methods.

A particular subclass of modified likelihoods that have been of great practical interest are (locally) weighted likelihoods. For a likelihood function , the weighted likelihood replaces by the weighted counterpart {IEEEeqnarray}rCl L(x_1:n—θ) & = ∏_i=1^n f(x_i—θ)^w_i for a collection of weights that typically are allowed to depend on the data as well as . Weighting schemes like this have been proposed for local likelihood methods that interpolate between parameter and density estimation (Hunsberger, 1994; Copas, 1995; Hjort and Jones, 1996; Loader, 1996; Eguchi and Copas, 1998), for improving predictive performance (Shimodaira, 2000), as well as in the context of Bayesian methods (Newton and Raftery, 1994; Greco et al., 2008; Agostinelli and Greco, 2013; Lyddon et al., 2019). Motivated by robustness, re-weighting schemes first arose in the context of linear regression (see e.g. Green, 1984; Gervini and Yohai, 2002; Marazzi and Yohai, 2004). The first mentions of a general construction to enhance the robustness of arbitrary likelihoods are due to Beran (1981) and Pregibon (1982). While the weighting schemes proposed in Beran (1981) are computationally unattractive, they inspired a range of alternative schemes that also aim at robustness and are more computationally tractable (Field and Smith, 1994; Windham, 1995; Markatou et al., 1997; Hadi and Luceño, 1997; Markatou et al., 1998; Dupuis and Morgenthaler, 2002). The most important of these are density-weighted approaches (Windham, 1995) which coincide with robust distance-based estimation methods for a particular sub-class of statistical models (Basu et al., 1998), weights based on the cumulative density function and quantiles (Field and Smith, 1994; Hadi and Luceño, 1997), and weights based on Pearson residuals (Markatou et al., 1997, 1998).

While there are some asymptotic results for certain weighted likelihood constructions (Lenth and Green, 1987; Hu, 1997; Wang et al., 2004; Wang and Zidek, 2005; Majumder et al., 2021), most of these only hold if models are well-specified and under conditions that are generally hard to verify. Furthermore, while various weighted likelihood schemes have been proposed for robustness, the nature of this robustness often lacks interpretability. Beyond that, most weighting schemes are not universally applicable and rely on additional knowledge that may not be generally available. For example, the approaches of Field and Smith (1994); Hadi and Luceño (1997) rely on the availability of cumulative density functions for the statistical model underlying the likelihood function. Similarly, Markatou et al. (1997, 1998) require Pearson residuals, which are generally difficult to compute on continuous spaces.

In this paper, we introduce the optimistically weighted likelihood (OWL) methodology. This approach does not suffer the drawbacks of these previous proposals: Specifically, OWL is provably well-behaved in the asymptotic regime, guarantees robustness by means of an interpretable construction, and is universally applicable. The key intuition behind our approach is that parameter inference based on the weighted likelihood is equivalent to inference based on the standard-likelihood for a re-weighted empirical distribution. The weights are then chosen so that the re-weighted empirical measure (a) is within an -neighborhood of the observed data distribution with respect to a suitable distance all while (b) being close to an element of the model class. The robustness of OWL follows from the choice of distance in (a). In particular, OWL inherits the particular robustness properties of the distance it is based on. Meanwhile, the optimism of (b) allows OWL to recover parameters that are -close to the data generating distribution, if such parameters exist. In this paper, we choose the total variation (TV) distance for step (a): It is easy to interpret, is a proper metric, and is robust to outliers and contamination (see e.g. Yatracos, 1985). While it is conceptually easy to modify our methodology for alternative distances, there may be substantial computational hurdles.

Although directly inferring optimistic weights that satisfy (a) and (b) in the TV setting is intractable, we develop an alternating optimization scheme that can be easily implemented in a variety of settings. Empirically, the weights recovered by this procedure behave as theory would predict: they assign near-zero values to observations that are in strong disagreement with the likelihood model. The right panel of Figure 1 illustrates this: as theory predicts, the weights are very small on the region containing the corrupted data, and much higher on regions that produce a good fit for the posed likelihood model.

We also show that OWL is intimately connected with the principle of coarsened inference (Miller and Dunson, 2019). The coarsened likelihood is a natural generalization of standard likelihood; and posits that the empirical distribution of idealized data generated from the assumed statistical model is within a discrepancy of the empirical distribution of the observed data—rather than the two being equal, which is the assumption implicitly underlying inference for well-specified models. Despite its natural interpretation, coarsened likelihoods are difficult to evaluate or approximate directly, except in the special case when the discrepancy is chosen to be the Kullback Leibler (KL) divergence (Miller and Dunson, 2019). While directly computing coarsened likelihoods is intractable in finite samples, we use techniques from large deviation theory (Dembo and Zeitouni, 2010) to show that coarsened likelihoods converge to their corresponding optimistically weighted likelihood for a broad class of discrepancies. This result provides an alternate motivation of OWL as a tool for approximating coarsened likelihoods.

In summary, our contribution is a robust OWL methodology based on neighborhoods of the data measured in TV distance. While computing the optimal weights is generally intractable, we propose an easily implementable alternating optimization scheme to approximately solve this problem. Beyond that, we also demonstrate an asymptotic equivalence between OWL and coarsened likelihoods. The resulting inferences exhibit desirable properties, both in theory and practice.

The remainder of the paper discusses these findings as follows: Section 2 presents the OWL methodology and the associated alternating optimization scheme. Section 3 discusses the computational details of each of the steps in the alternating optimization procedure. Section 4 demonstrates the asymptotic connection between OWL and coarsened inference. Section 5 presents a suite of simulation experiments for the OWL methodology in both regression and clustering tasks. Section 6 applies the OWL methodology to a clustering application for single-cell RNAseq data. Section 7 uses the OWL methodology to estimate the average intent-to-treat effect in the micro-credit study by Angelucci et al. (2015), whose inference was shown to be brittle to the removal of an handful of observations (Broderick et al., 2020).

2 Optimistically Weighted Likelihoods

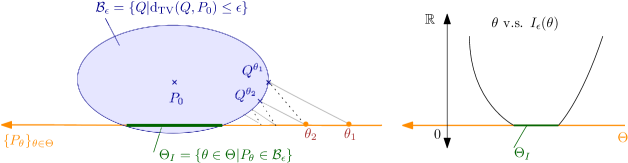

As Figure 1 shows, maximum likelihood estimation can be brittle when the data generating distribution is allowed to have a small degree of misspecification with respect to the model family . To assuage the problem of brittleness under misspecification, we propose an Optimistically Weighted Likelihood (OWL) approach that iterates between (1) optimistically re-weighting the observed data points and (2) updating the parameter estimate by maximizing a weighted likelihood based on the current data weights.

In Section 2.1, we study this parameter inference methodology at the population level where we formally allow to be misspecified. Here we introduce the population level optimistic Kullback Leibler (OKL) function with parameter (Equation 1), and show that its minimizer will be a parameter for which is -close to in TV distance. Under suitable conditions, the minimization of the OKL can be performed by iterating the two steps of a) projection of the current model estimate onto the TV neighborhood around in a Kullback Leibler sense (information projection), and b) finding the parameter that maximizes a suitably weighted integral of the log likelihood.

Motivated by this population analysis, in Section 2.2, we derive the OWL-based parameter estimation methodology when only samples from are available.

2.1 Population level Optimistic Kullback Leibler minimization

Let denote the space of probability distributions on the data space . Our methodology can accommodate misspecification in terms of a variety of probability metrics (e.g. MMD or Wasserstein) on , but here we mainly focus on the total variation (TV) distance for concreteness and interpretability. Let denote the TV metric between two probability distributions . Given a model family , we assume that the data generating distribution for the data population in question satisfies for a known value and some unknown . In other words, we make the following assumption:

Assumption 2.1.

Given and the true data distribution , the set of parameters is non-empty.

Assumption 2.1 encompasses Huber’s -contamination model (Huber, 1964) since the condition follows whenever , for an arbitrary contaminating distribution . However, Assumption 2.1 is strictly more general, since does not imply that is an -contamination of . Indeed, Lemma 25 in the appendix shows that for fixed , , and , for some contaminating distribution if and only if the Radon Nikodym derivative exists and is bounded from above by , almost surely.

In general, under Assumption 2.1, it may only be possible to identify the set , rather than any particular . Although such indeterminacy may be inherent, it is practically insignificant whenever is sufficiently small so that the distinction between two elements from is practically irrelevant (Huber, 1964). In line with this insight, the goal throughout the rest of the paper will be to identify some parameter in .

At the population level, usual maximum likelihood parameter estimation amounts to minimizing the Kullback Leibler (KL) function on the parameter space . Even under small amounts of misspecification, KL minimizers are very brittle. The origin of this phenomenon is that any minimizers of the KL function must place sufficient probability mass wherever does, including on outliers. In contrast, TV distance is far less sensitive to the geometry of misspecifaction. Hence one may minimize as a robust alternative, particularly under Assumption 2.1. However, direct minimization of TV distance over the parameter space is difficult to implement in practice due to the lack of suitable optimization primitives (e.g. maximum likelihood estimators) and the non-convex and non-smooth nature of the optimization problem (see e.g. Yatracos, 1985).

An approach minimizing the KL divergence with its second argument constrained within an -neighborhood under the Lévy-Prokhorov metric—as opposed to the TV distance—was proposed in Yang and Chen (2018) to provide Neyman-Pearson optimal tests for a robust version of the universal hypothesis testing problem for univariate distributions. Our motivation is estimation and inference rather than testing. Indeed, asymptotic analysis of the coarsened likelihood (Miller and Dunson, 2019) using Sanov’s theorem (see Section 4) gives rise to a similar KL objective constrained by an -neighbourhood. The resulting function, which we term the Optimistic Kullback Leibler (OKL), is defined as follows.

Definition 2.1.

(Optimistic Kullback Leibler) Given and , the OKL function is defined as:

| (1) |

where is the TV ball of radius around . If , the underlying optimization over has a unique minimizer called the I-projection (Csiszár, 1975).

The function measures the fit of a model to the data allowing for a degree of data re-interpretation in TV distance before assessing model fit. Our terminology Optimistic Kullback Leibler emphasizes that is the KL divergence between the most optimistic re-interpretation of the data within the data neighborhood and the model distribution . Here we use the term optimistic re-interpretation in the sense that, if is our current parameter estimate, our methodology calculates the KL divergence optimistically, by supposing that the true data are generated from the model-friendly distribution rather than . Here, regulates the permitted degree of re-interpreting the data by controlling the neighborhood size.

The OKL function enables us to perform robust parameter inference by finding a parameter from the set : Since , under Assumption 2.1, the minimum OKL value of zero will be attained exactly on (since if and only if ). This implies that finding a minimizer of amounts to finding a robust parameter estimate. However, the OKL may be non-convex, so that calculating the global minimizer of OKL may not be straightforward. Fortunately, the OKL lends itself to a feasible alternating optimization scheme that will reach a saddle point under suitable conditions.

Global minimization of the OKL function is equivalent to the joint global minimization of the function given by , since . Thus we will use alternating minimization to jointly minimize the function , i.e. for we perform the -step: and the -step: . For simplicity, suppose that the model family and have densities and with respect to a common measure , then the I-projection will also have a density with respect to , and the iterations will take the following form. Starting from such that , compute the following steps for :

-

1.

Q-step: Compute the I-projection of on the ball . This corresponds to solving a convex optimization problem over the space of probability densities with respect to .

-

2.

-step: Maximize the average log-likelihood . Note that with the convention that . Hence the optimization step can be re-written as:

The above iterations provide a scheme to minimize the OKL function in which the -step can approximately be performed using tools from convex optimization, while the -step can be approximated by maximization of a suitably weighted log-likelihood, which can be computed for many standard models. Our resulting population level methodology is illustrated in Figure 2.

Assuming that there is always a unique minimizer in the -step, it is straightforward to show that the objective value is a strictly decreasing function of as long as . Thus if lie in a compact set and suitable continuity assumptions hold, any limit point of the sequence will satisfy the saddle point condition . This saddle point condition is satisfied by all the parameters in the identifiable set .

We remark that one can use optimization of the OKL function as a subroutine to minimize the function . Namely, we can perform binary search over , increasing whenever we have and decreasing whenever we have . Used this way, OKL optimization can be seen as a computationally-palatable approach to minimizing the TV distance over a model class.

2.2 Optimistically Weighted Likelihood (OWL) estimation

We now extend the population level methodology from Section 2.1 to handle the practical case when samples are available, and provide a computable approximation for the -step and -step from Section 2.1. Namely, the -step (now called -step) will be approximated by a suitable convex optimization problem over weights that lie within the intersection of an -dimensional probability simplex and the ball of radius around the vector with uniform weights; these optimal weights can be interpreted as an optimistic re-weighting of the original data points to match the current model estimate. Further, the -step will then be approximated by maximizing a weighted likelihood with the weights found in the previous step. Since this methodology involves the repeated steps of parameter estimation using a weighted likelihood (i.e. the -step) and re-estimating the weights on the data points to optimistically match the estimated model (i.e. the -step), we call this the Optimistically Weighted Likelihood (OWL) method.

2.2.1 Approximating OKL by a finite dimensional optimization problem

We derive the OWL methodology by approximating the OKL function in terms of a finite dimensional optimization problem defined in terms of observed data . Henceforth, let us assume that the model family and measure have densities and with respect to a common measure . We will focus on two cases of interest: when is a finite space and is the counting measure, and when and is the Lebesgue measure.

When is finite, we look to solve the optimization problem in eq. 1 over data re-weighting as the weight vector varies over the -dimensional probability simplex and satisfies the TV constraint where is the vector with uniform weights. Formally, our finite space OKL approximation is given by

| (2) |

where is the histogram estimator for the data generating distribution when is a finite space. An application of the log sum inequality (Cover and Thomas, 2006, Theorem 2.7.1) shows that the weights that solve eq. 2 have the appealing and natural property that whenever . Moreover, when the support of contains the support of , converges to at rate , as demonstrated by the following result.

Theorem 1.

Suppose that for some and pick and . If and , then with probability at least ,

where .

See Appendix B for the proof and a more general theorem statement with explicit constants.

When , the above approximation strategy needs to be modified, since is unbounded whenever is supported on all of and is a discrete distribution. In this case, eq. 1 should be formulated in terms of measures that have density with respect to . Namely, we start with the formulation:

| (3) |

where is the space of probability densities with respect to . Next, using a suitable probability kernel , we restrict the domain of the optimization problem in eq. 3 to the finite dimensional subspace of densities , where denotes the probability density indexed by weight vector . As an example, we may use the Gaussian kernel for a bandwidth parameter .

For a probability kernel , using the finite dimensional approximation for the space of densities, and a suitable Monte Carlo approximation to the integral objective in eq. 3, we obtain the approximation:

| (4) |

where is a suitable density estimator for based on , is an matrix with entries , and is the image of the -dimensional probability simplex under linear operator . We will typically take to be the kernel-density estimate based on the same kernel , in which case is the stochastic matrix obtained by normalizing the rows of the kernel matrix to sum to one.

The continuous space approximation in eq. 4 yields the finite space approximation in eq. 2 as a special case when is taken to be the indicator kernel. The weights vectors in are always non-negative and approximately sum to one for large values of , since . The derivation of eq. 4 along with large sample consistency can be found in Appendix C, but we briefly describe the main result here.

Proving the convergence of is technically challenging, as it requires proving uniform-convergence of the objective in eq. 4 when the weights are allowed to vary over the entire range . To get around this, we restrict the optimization domain to where for a suitably small constant . Thus, the estimator that we theoretically study is given by

| (5) |

Given this change, we can show the following result.

Theorem 2.

Suppose is a compact subset of and there exists a constant such that for all . Suppose that we use the probability kernel having bandwidth , with positive semi-definite and bounded above by a constant and having exponentially-decaying tails. Assume that and are -Hölder smooth over , and suppose that we use the clipped density estimator . Then for any constant

with probability at least , where , is the -dimensional Lebesgue measure, , and hides constants and logarithmic factors.

Observe that measures the fraction of the volume of that is contained in the envelope of width closest to the boundary. For well-behaved sets, we expect to decrease to 0 as . For example, if is a -dimensional ball of radius , then .

We prove our theory with the truncated estimator instead of for techincal reasons. By a suitable version of the sandwiching lemma (Section A.2), under the assumptions of Theorem 2, we conjecture that the optimal weights in (4) lie in the set for a small enough constant , in which case we will have .

2.2.2 OWL Methodology

With a computable approximation (or ) to the OKL function in hand, we follow the alternating minimization strategy described in Section 2.1 to minimize the function . In more detail, we replace the density (or more precisely the relative density ) in the -step with the weight vector that minimizes eq. 4 for . We rename this the -step to emphasize the new setup. Next, the -step corresponds to minimizing the function , which is equivalent to maximizing the weighted likelihood .

The resulting procedure is summarized in Algorithm 1. In Section 3, we expand on the computational details for the -step and -steps, but note for now that the -step involves solving a convex optimization problem for which standard tools are available, while the -step corresponds to maximizing a weighted likelihood, which can be performed for many models through simple modifications of procedures for the corresponding maximum likelihood estimation.

Finally, it is straightforward to see that the iterates of Algorithm 1 must decrease the objective function , as we have

Since eq. 4 is a convex optimization problem with a strictly convex objective, the first inequality is strict unless . Hence the objective must decrease strictly at each step.

In practice, when the data lie in a continuous space, we often avoid using the kernel-based estimator eq. 4 to determine the weights in the -step of Algorithm 1 because it greatly slows down the computation (see Section 3.1), and the resulting weights are sensitive to the choice of kernel . Instead, setting , we perform the -step by solving the unkernelized optimization problem:

obtained from eq. 4 when all the data points are distinct. We demonstrate in Section 5.1 that the unkernelized version of the OWL procedure has equally good performance compared to the kernelized version with a suitably tuned bandwidth. A potential explanation for this is that the primary role of the -step is to down-weight outliers under the model density , which is controlled by the first term in the optimization objective above; in contrast, the second term in the optimization objective controls the regularity of the non-outlying weights, and plays a secondary role in the -step.

2.2.3 Setting the corruption fraction

So far we have assumed that the parameter , which can be interpreted as the fraction of corrupted samples in the population distribution, is fixed at a known value that satisfies Assumption 2.1. Now let us see how the population level analysis (Section 2.1) can inform our choice of . Assumption 2.1 is satisfied as long as , where

Hence, in principle, we could set to use OWL to perform minimum-TV estimation (Yatracos, 1985), which has the following advantages: (1) while directly minimizing TV distance is computationally intractable, the OWL methodology decomposes this problem into alternating convex optimization and weighted MLE steps, both of which are standard problems that often tend to be well-behaved, and (2) the OWL methodology provides us with weight vectors that can indicate outlying observations and relates minimum TV-estimation to likelihood based inference.

In order to choose in practice, we define the function , where is the parameter estimate computed by the OWL procedure for a given . At the population level, the corresponding function is monotonically decreasing in until , at which point it remains at 0. This introduces a kink, or elbow, at that we hope to identify in the sample estimate . Thus, our -search procedure is to compute over a fixed grid of -values, smooth the resulting grid, and then select amongst the points of largest curvature (computed numerically), where the curvature of a twice-differentiable function at a point is given by (Satopaa et al., 2011). Despite the various approximations involved, our simulation results (Section 5) show that the OWL procedure with such a tuned value of provides almost identical performance when compared with the OWL procedure with the true value of .

2.3 OWL extension to non-identically-distributed data

While the population level analysis and theoretical results for the OKL estimator were derived under the assumption that data are generated i.i.d. from a distribution , the OWL procedure can be adapted to robustify likelihood based inference in the setting where the data are conditionally independent, but not necessarily identically distributed.

Suppose data are conditionally independent, with the likelihood having the product form , for known functions . For example, if for , this includes the case of regression models under the setup . Another example of this setup includes mixture models if we expand the parameter space to also include cluster assignments (see Section 3.2.2).

To robustify inference based on the product likelihood , we can replace the - and - steps in Algorithm 1 by analogous steps in the product likelihood case. In particular, the modified -step is given by

and the modified -step is given by

Despite our lack of theory in the non-identically-distributed case, we continue to see good empirical performance of the OWL estimator in this setup when evaluated on synthetic data (see Section 5).

3 Performing OWL computations

In this section, we expand on the computational details of the OWL methodology. Specifically, in Section 3.1 we discuss our approach to solving the constrained convex optimization problems in eqs. 2 and 4, and in Section 3.2 we discuss the details of optimizing a weighted likelihood for exponential families and mixture models.

3.1 Computing the -step (I-projection)

3.1.1 Unkernelized I-projection

Suppose that is finite. Then the finite approximation to the OKL of eq. 2 is given by the solution to the convex optimization problem

where is the number of times that occurs in our sample.

This is a convex optimization problem for which there are a number of candidate solutions. Our approach is based on (consensus) Alternating Direction Method of Multipliers (ADMM) (Boyd et al., 2011; Parikh and Boyd, 2014). To frame the OKL optimization problem in the language of ADMM, we rewrite it as

| (6) |

where is 0 whenever the condition is true and otherwise. Written in this form, ADMM boils down to implementing the individual proximal operators for the ’s, where the proximal operator of a closed proper convex function and parameter is defined as the function

In our setting, the proximal operator for the KL term can be computed element-wise using the Lambert-W function (Barratt et al., 2021), or in log-scale via the Wright omega function, for which fast algorithms exist (Lawrence et al., 2012), leading to computational complexity. The proximal operator for corresponds to projection onto the -dimensional scaled probability simplex, which can be computed in time (Condat, 2016). The proximal operator for corresponds to projection onto an -ball, and in fact it can be reduced to projection onto the simplex (Condat, 2016).

To simplify our discussion on the implementation of ADMM, we rewrite eq. 6 for an arbitrary number of convex functions as

For penalty parameters , the augmented Langrangian associated with this problem is given by

where are the primal variables, are the dual variables, and is the consensus variable. Then the consensus ADMM algorithm is derived by iteratively optimizing the augmented Langrangian coordinate-wise. That is, starting from some initialization , we perform the following updates

Algorithm 2 displays the full consensus ADMM algorithm. In our implementation, we use the self-adaptive rule suggested by He et al. (2000) to independently update each of the penalty parameters.

3.1.2 Kernelized I-projection

In the Euclidean case with , beyond the sample and parameter , we additionally have a kernel matrix with induced row sums and row-normalized matrix . The optimization problem of eq. 4 translates to

| (7) |

Although all the terms in eq. 7 remain convex in , the proximal operators for the KL objective and the constraint are no longer available in closed form. To circumvent this issue, we can rewrite problems of this form as

where each . The augmented Langrangian in this case becomes

which leads to the ADMM updates

In our setting, each is either equal to or to the identity matrix . Thus, the matrix inverse in the update of can be computed efficiently using a single singular value decomposition of , even if the penalty parameters change between iterations. To see this, suppose that is the SVD of and let . Then the update can be written as

where and .

3.1.3 Computational complexity and generalization to other distances

As mentioned above, each of the three proximal operators in eq. 6 and eq. 7 can be implemented in time. For the non-kernelized version of the ADMM algorithm in Algorithm 2, the remaining linear algebraic steps can also be implemented in time, bringing the total computational complexity of the procedure to , where is the number of ADMM steps taken. For the kernelized version of the ADMM algorithm, we require an SVD computation as a preprocessing step, which takes time, and each step additionally involves matrix-vector products, taking time . Thus, the total time complexity of the kernelized ADMM procedure amounts to , which is polynomial in but not feasible for large values of .

We remark here that from an optimization perspective, for both eqs. 6 and 7, the -distance is not special. We may substitute in any distance that is convex in its arguments and for which there are computationally efficient methods for projection onto the corresponding balls with a specified center and radius. This includes -distance, whose projection can be computed by a simple shift and rescaling, and maximum mean discrepancy (Gretton et al., 2006) whose projection operator is onto an ellipsoid and can be reduced to a one-dimensional root finding problem (Kiseliov, 1994).

3.2 Computing the -step: maximizing weighted likelihoods

We now shift focus to the second step in the OWL procedure, maximizing a weighted likelihood:

We will expand on this problem for two settings: exponential families and mixture models.

3.2.1 Weighted maximum likelihood for exponential families

Consider the setting where is an exponential family and is the natural parameter space so that

where is a sufficient statistic, is a base measure, and is the log-normalizing factor. Then for , the weighted maximization step solves

| (8) |

This solution satisfies the gradient condition

For exponential families, whenever is positive definite for , the function is invertible. Thus, this step can be solved quickly whenever we can compute the inverse of . When is not strictly positive definite, or more generally when the inverse of is not available in closed form, the objective in eq. 8 is still convex in and can be solved using tools from convex optimization.

3.2.2 Weighted maximum likelihood for mixture models

In the mixture model setting, the parameters encode mixing weights and component parameters such that denotes a probability density over . Then the likelihood under can be written as

To compute the maximum likelihood estimate, it is standard to introduce latent categorical random variables , and rewrite the likelihood as

The above can then be maximized using the EM algorithm (Dempster et al., 1977). Unfortunately, the introduction of weights into the likelihood no longer allows for an easy decomposition via these latent variables.

However, consider the likelihood with respect to the augmented latent variables :

Then, following the setup from Section 2.3, the weighted log-likelihood can be written as

Thus, to maximize the above for fixed latent variables , we can maximize the weighted log-likelihood of the individual component parameters over its assigned (weighted) data. For many component distributions (e.g., Gaussians, Poissons), this can be computed in closed-form. On the other hand, for fixed component variables , we can maximize this weighted log-likelihood over the by assigning each data point to the component that maximizes its individual likelihood. This suggests the following scheme, reminiscent of the ‘hard EM’ algorithm (Samdani et al., 2012):

In general, optimizing over the augmented parameter space implicitly assumes a generative model different from the one assumed by optimizing over . In particular, when one optimizes over , the assumed generative model is that the data come from some distribution that is -close to for some . The implied generative model when optimizing over is that the data come from some mixture distribution such that each component is -close to some . For most settings, the first generative model is a strict generalization of the second. However, in the -contamination model, these are equivalent, as implied by the following result.

Proposition 1.

Let denote probability measures, , and . Then the following are equivalent.

-

•

There exists a probability measure such that .

-

•

There exist probability measures such that .

The proof of Proposition 1 follows from simple algebraic substitution.

4 Asymptotic connection to coarsened inference

The development of the OWL methodology in Section 2 followed from a presumed form of misspecification given by Assumption 2.1. An alternative way to frame and address such misspecifications in a probabilistic framework was proposed by Miller and Dunson (2019) who introduced Bayesian methodology centered around the concept of a coarsened likelihood defined as

| (9) |

where is a suitably chosen discrepancy between empirical probability measures. Here, denotes the empirical distribution of data , and the probability is computed under —the distribution underlying the artificial data from which the random measure is constructed. The coarsened likelihood implicitly captures the likelihood of a probabilistic procedure in which idealized data are first generated by some model in the model class under consideration, but are then corrupted in such a way that the discrepancy between empirical measures of the idealized data and the observed data is bounded by .

When is an estimator for the KL-divergence and an exponential prior is placed on , Miller and Dunson (2019) showed that the Bayes posterior based on could be approximated by raising the likelihood to a power less than one in the formula for the standard posterior. However, to obtain a robustified alternative to maximum likelihood estimation, one may wish to maximize directly for a choice of that guarantees robustness (e.g. Maximum Mean Discrepancy or the TV distance). Such an approach would in general be quite challenging since evaluating eq. 9 corresponds to computing a high-dimensional integral.

In this section, we show that for large , the coarsened likelihood can be approximately maximized by using the OWL methodology when is an estimator for the TV distance. Specifically, if the observed data are generated i.i.d. from some distribution and satisfies appropriate regularity conditions, then the negative rescaled coarsened likelihood asymptotically converges as to a variant of based on . Hence, the OWL methodology asymptotically maximizes the coarsened likelihood . In Sections 4.1 and 4.2, we develop this asymptotic connection for finite and continuous spaces, respectively. All proofs for this section can be found in Appendix D.

4.1 Asymptotic connection in finite spaces

Let be a finite set and denote the space of probability distributions on by the simplex . Let denote the collection of model distributions, and denote the true data generating distribution. To establish connection of OKL with the coarsened likelihood eq. 9, we will take to be the TV distance.

Given this setting, we can show that converges in probability to the OKL function at rate , as demonstrated by the following theorem.

Theorem 3.

Suppose that for some and let . If and , then with probability at least ,

Our proof hinges on analyzing a quantity that is closely related to :

Instead of looking at the distance to the empirical estimator as in , the quantity considers the distance to the distribution itself. This simplifies matters greatly, and allows us to establish the following result, which is essentially a consequence of Sanov’s theorem from large deviation theory (Dembo and Zeitouni, 2010).

Lemma 1.

If for some , then

for all .

The rest of the proof of Theorem 3 amounts to establishing that is close to , which follows from continuity arguments and the fact that converges to in distance.

4.2 Asymptotic connection in continuous spaces

Suppose and denotes the set of densities on with respect to the Lebesgue measure. Let denote the set of model densities and let denote the density of the data generating measure .

Similar to the finite case, we can use Sanov’s theorem from Large Deviation theory to establish the following asymptotics for the coarsened likelihood for a suitable class of discrepancies , which includes the Wasserstein distance, Maximum Mean Discrepancy with suitable choice of kernels (Simon-Gabriel and Schölkopf, 2018), and the smoothed TV distance (Definition 4.1).

Theorem 4.

Suppose for some and is a pseudometric that is convex in its arguments and continuous with respect to the weak convergence topology on . If and , then

Recall that the limiting expression in the above theorem has the same form as that of the OKL function given in eq. 3. However, in order to establish connection between the OKL function and the coarsened likelihood, unlike in the finite case, we cannot merely take the discrepancy in the coarsened likelihood to be the TV distance, since the TV distance between the two empirical distributions in eq. 9 will almost surely be equal to one. Instead, we will take to be a smoothed version of TV distance calculated by first convolving the empirical measures with a smooth kernel function indexed by a bandwidth parameter .

To formally define the smoothed TV distance, let be a continuous and bounded probability density function (e.g. standard Gaussian density), let be a bandwidth parameter. Then the kernel is defined as , and for any measure , the convolved density is defined as .

Definition 4.1.

Given two measures and bandwidth , the smoothed total variation (TV) distance is defined as:

We extend the notion of smoothed TV distance to densities based on their induced measures .

We show in Section D.2.2 that satisfies conditions of Theorem 4. Further, when has fast tail-decay and densities satisfy appropriate regularity conditions, standard results on kernel density estimation (e.g. Rinaldo and Wasserman (2010); Jiang (2017)) show the pointwise convergence of densities as . This, when combined with Scheffe’s lemma and the triangle inequality, shows that . In other words, for suitably small bandwidth parameter , the neighborhoods based on the smoothed total variation distance approximate those based on the total variation distance.

Thus, by invoking Theorem 4 with the choice , one expects when is large and is small. As in the finite setting, we again see that maximizing the coarsened likelihood is closely related to minimizing the OKL function in the large sample regime. Hence the OWL methodology can be used to approximately maximize the coarsened likelihood when for large sample size and a suitably small bandwidth . In fact for many other metrics satisfying the conditions of Theorem 4, one can adapt the OWL methodology to maximize the function as .

5 Simulation Examples

We now turn to applications of the optimistic weighted likelihood methodology in simulated examples with artificially-injected corruptions. In each simulation, we considered two methods for choosing the points to corrupt: (i) max-likelihood corruption where we fit a maximum likelihood estimate to the uncorrupted data and select the points with the highest likelihood; and (ii) random corruption where we choose the points to corrupt uniformly at random. For clarity and space, we only present the results for max-likelihood corruptions in this section, and we defer the results for randomly-selected corruptions to Appendix F. Unless otherwise stated, the -step for the OWL solutions was computed using the finite approximation to the OKL in eq. 2.

In all comparisons, OWL refers to our methodology with the data based choice of the corruption fraction as described in Section 2.2.3, while OWL ( known) refers to our methdology with equal to the true level of corruption in the data. For the other robust estimation methods requiring hyperparameters, we either used commonly-accepted values (as in Huber regression), or we set them based on knowledge of the true corruption fraction (as in RANSAC regression). In all settings, we measured the performance of the maximum-likelihood estimator (MLE) that was fit using the entire uncorrupted dataset as a gold-standard benchmark.

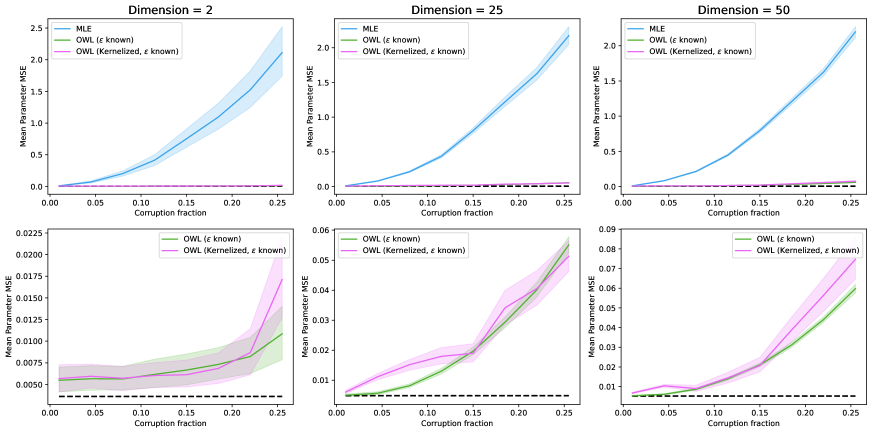

5.1 Gaussian simulations

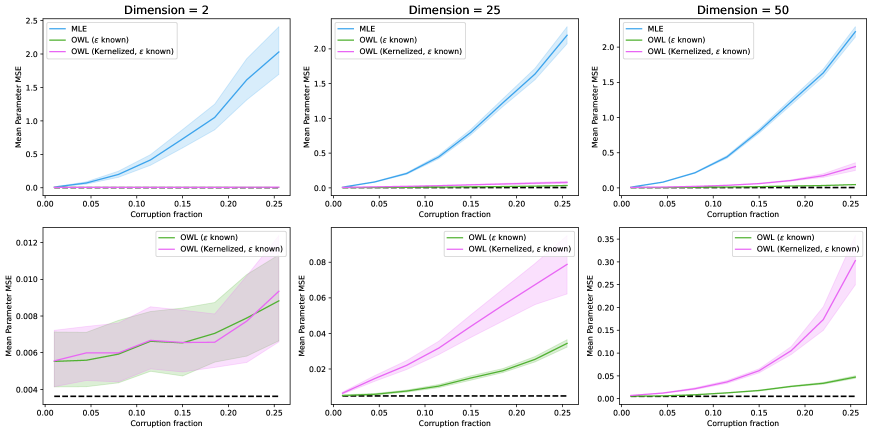

To investigate the performance of the OWL methodology with and without kernelization, we fit a multivariate normal distribution with mean and covariance matrix . We make two observations about this setting. First, maximizers of the weighted log-likehood can be computed in closed form, removing optimization difficulties. Second, this simple problem setting falls squarely within the i.i.d. framework of Section 2.

We generated synthetic datasets for dimensions , 25, and 50, by drawing independently from the uniform distribution over and drawing the uncorrupted data points independently from the spherical Gaussian , where . The corrupted data points had coordinates drawn independently from the uniform distribution over . The total size of the training set was set to 200. We measured the mean-squared error reconstruction of , i.e. for parameter estimates and :

For the kernelized OWL procedure, we used the Gaussian/RBF kernel: . We adaptively set the bandwidth by searching over a fixed grid and using the final parameter’s OKL estimator in eq. 4 as the criterion to be minimized. To focus only on the role of kernelization, we set the corruption fraction equal to the true level of corruption in the dataset.

Figure 3 shows the results for the Gaussian simulations. Across the range of dimensions, both kernelized and un-kernelized OWL perform much better than MLE. Moreover, the performance of OWL without kernelization is comparable to that of OWL with kernelization. This is somewhat surprising, as our theory currently cannot explain why one should be able to run OWL in continuous spaces without some form of density estimation. For the rest of this section, we will only consider OWL without kernelization.

5.2 Regression simulations

We applied OWL to two regression settings: linear regression and logistic regression.

Linear regression.

We considered a homoscedastic model with parameters , and observations assumed to follow the distribution

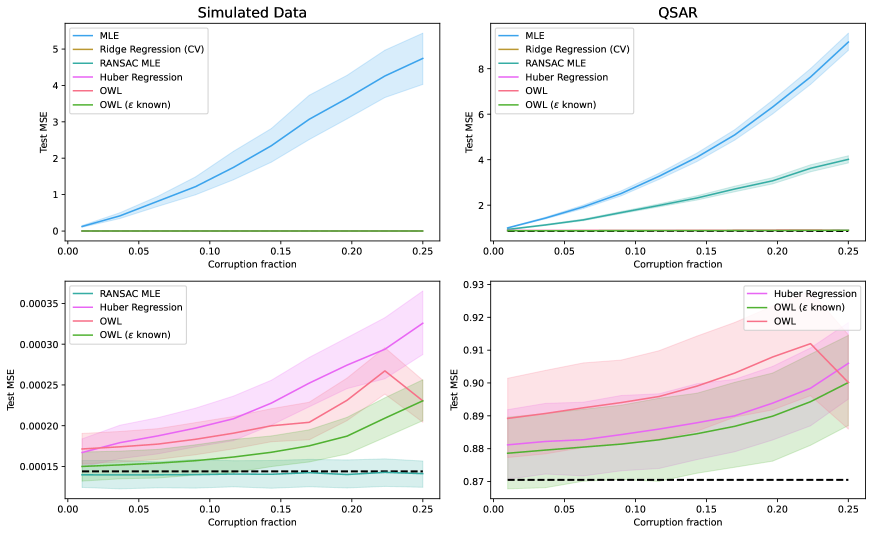

The maximizers of the weighted likelihood can be computed in closed form, as in the unweighted setting. In addition to the standard least-squares maximum likelihood estimate (MLE), we compared with (1) Ridge regression, with L2 penalty chosen via cross validation; (2) Huber regression, using the Huber penalty of 1.345 (Huber, 1981); and (3) Random Sample Consenus (RANSAC) linear regression.

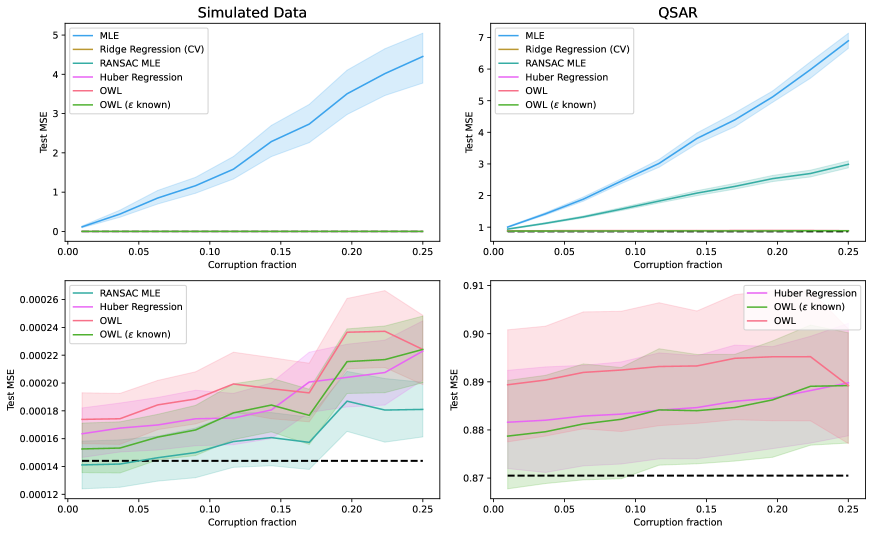

We compared these methods on two datasets. The first is a simulated dataset with 10-dimensional i.i.d. standard normal covariates. The ground-truth regression coefficients were drawn independently from , and the residual standard deviation was . The training set consisted of 1,000 data points. For the test set, we drew 1,000 new data points and computed the MSE on the underlying response value, i.e.

The second dataset was taken from a quantitative structure activity relationship (QSAR) dataset compiled by Olier et al. (2018) from the ChEMBL database. It consists of 5012 chemical compounds whose activities were measured on the epidermal growth factor receptor protein erbB1. The activities were recorded as the negative log of the chemical concentration that inhibited 50% of the protein target, i.e. the pIC50 value. Each compound had 1024 associated binary covariates, corresponding to the 1024-dimensional FCFP4 fingerprint representation of the molecule (Rogers and Hahn, 2010). We used PCA to reduce the dimension to 50. For every random seed, we computed a random 80/20 train/test split. The test MSE on this dataset is the standard MSE over the test responses. In both datasets, for each data point selected to be corrupted, we corrupted the responses by fitting a least squares solution and observing the residuals: if the residual is positive, we set the response to be where is the largest absolute value observed value in the training set responses, otherwise setting it to .

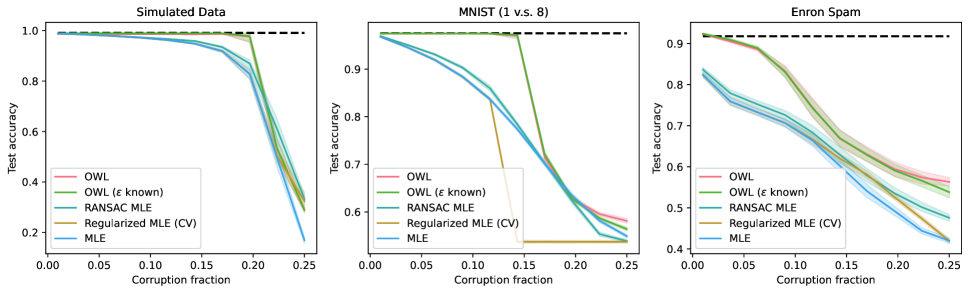

Figure 4 shows the results of the linear regression simulations for the max-likelihood corruptions. Across both datasets, we see that OWL is competitive with the best of the robust regression methods, whether that method is RANSAC or Huber regression.

Logistic regression.

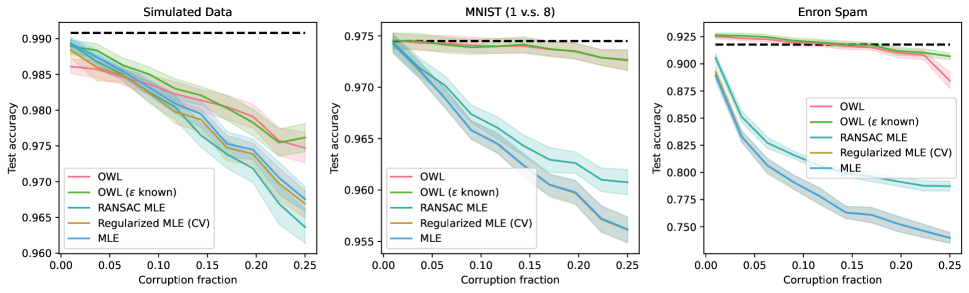

For the logistic regression setting, we have parameters , and observations assumed to follow the distribution

In addition to the standard maximum likelihood estimate (MLE), we compared against two other baselines: (i) L2-regularized MLE, with L2 penalty chosen via cross validation. (ii) Random Sample Consenus (RANSAC) logistic regression.

We compared these methods on three datasets. The first is a simulated dataset using the same parameters as the linear regression setting. The training labels are created according to the generative model. For test accuracy, we computed the zero-one loss over the true sign-values, i.e.

The second dataset is taken from the MNIST handwritten digit classification dataset (LeCun et al., 1998). We considered the problem of classifying the digit ‘1’ v.s. the digit ‘8,’ resulting in a dataset with 14702 data points and 784 covariates, representing pixel intensities. The third dataset is a collection of 5172 documents from the Enron spam classification dataset, preprocessed to contain 5116 covariates, representing word counts (Metsis et al., 2006). For both the MNIST and the Enron spam datasets, we reduced the dimensionality to 10 via PCA and used a random 80/20 train/test split.

Figure 5 shows the results of the logistic regression simulations. Across all datasets, we again see that OWL outperforms the other approaches in the presence of both corruption and misspecification.

5.3 Mixture model simulations

We applied OWL to two mixture modeling settings: mixtures of spherical Gaussians and mixtures of Bernoulli products.

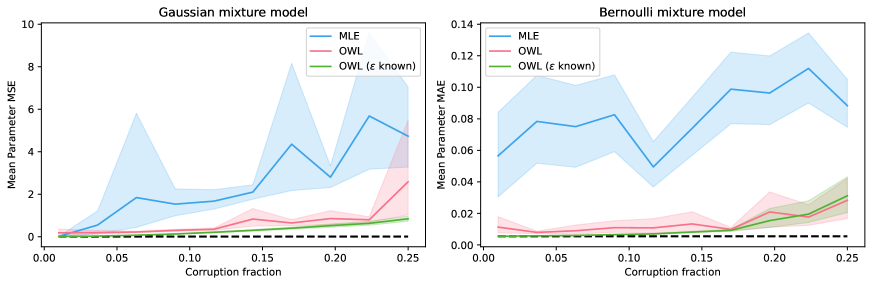

Gaussian mixture models.

Recall the standard Gaussian mixture modeling setup: there are a collection of means , standard deviations , and mixing weights . Data points are drawn i.i.d. according to

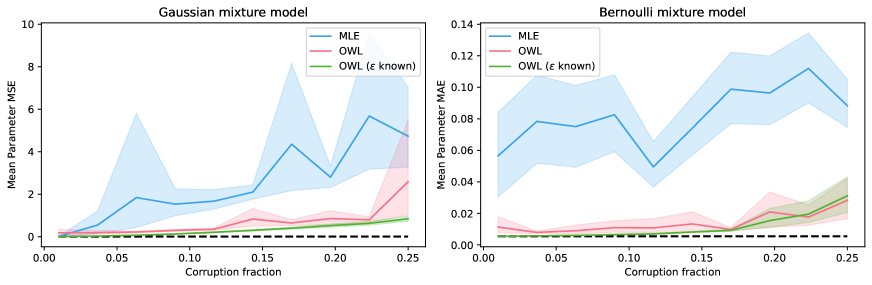

For our simulations, we generated a synthetic dataset of 1000 points in by first drawing means whose coordinates are i.i.d. Gaussian with standard deviation 2. The standard deviations of the component Gaussians were set to , and the mixing weights were uniform. We compared against MLE on the corrupted data. As a metric, we measured the average mean squared Euclidean distance between the means of the fitted model and the ground truth model. To corrupt a data point, we randomly selected half of its coordinates and set them randomly to either a large positive value or a large negative value (here, 10 and -10).

Because the likelihood function of a Gaussian mixture model is non-concave, the EM algorithm is only guaranteed to converge to a local optimum. Thus, for maximum likelihood estimation we used EM with random restarts, choosing the final model to be the one with largest likelihood. For the OWL procedure, we also used random restarts with the alternating optimization algorithm of Section 3. To choose the final model, we selected the one whose weights and parameters minimized the OKL estimator of eq. 2.

The left panel of Figure 6 shows the results of the Gaussian mixture model simulations. We see that OWL remains robust against varying levels of corruptions.

Bernoulli product mixture models.

Consider the following model for -dimensional binary data: there are a collection of probability vectors and mixing weights . Each data point is drawn i.i.d. according to the process

For our simulations, we generated a synthetic dataset of 1000 points in by first drawing means whose coordinates are i.i.d. from a Beta distribution. The mixing weights were chosen to be uniform over the components. As a metric, we measured the average mean -distance between the parameters of the fitted model and the ground truth model.

To corrupt a data point, we flipped each zero coordinate with probability 1/2. The right panel of Figure 6 shows the results of the Bernoulli mixture model simulations. We see that OWL remains robust against varying levels of corruptions.

6 Application to scRNA-seq Clustering

In this section, we apply our OWL methodology to a single-cell RNA sequencing (scRNA-seq) clustering problem. The GSE81861 cell line dataset (Li et al., 2017) contains single-cell RNA expression data for 630 cells from 7 cell lines across 57,241 genes. We followed the preprocessing steps of Chandra et al. (2020): we dropped cells with low reads, normalized according to Lun et al. (2016), and dropped uninformative genes with M3Drop (Andrews and Hemberg, 2019). After preprocessing, the dataset contains 531 cells and 7666 genes. Table 1 shows the breakdown of the remaining cells across cell lines. Finally, we used PCA to project down to 10 dimensions. We implemented OWL using a mixture of general Gaussians, , using the same optimization procedure as in the clustering simulations of Section 5.

| Cell line | A549 | GM12878 | H1 | H1437 | HCT116 | IMR90 | K562 |

|---|---|---|---|---|---|---|---|

| Counts | 74 | 126 | 164 | 47 | 51 | 23 | 46 |

6.1 Cluster recovery with OWL

We measured the ability of OWL to recover the ground-truth clustering of samples. For baseline methods, we compared against maximum likelihood estimation with the same model class and K-means. As a metric of cluster recovery, we measured the adjusted Rand index (ARI) (Rand, 1971; Hubert and Arabie, 1985). In all our comparisons, we fixed the number of clusters for all methods to be 7, the number of ground truth cell lines.

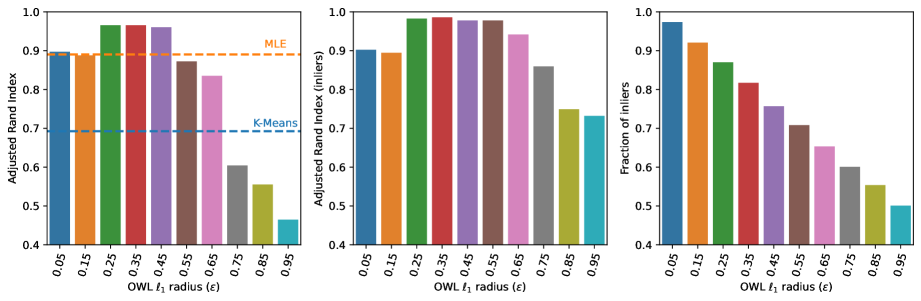

The left panel of Figure 7 shows the ARI for OWL over a range of values for the radius parameter , where we also display the performance of MLE and K-means for comparison. We see that OWL performs best when takes on values between and , but generally has reasonable performance when is not too large. Moreover, we see that performance of OWL varies smoothly as a function of , which may reflect the continuity of the OKL function with respect to predicted by our theory.

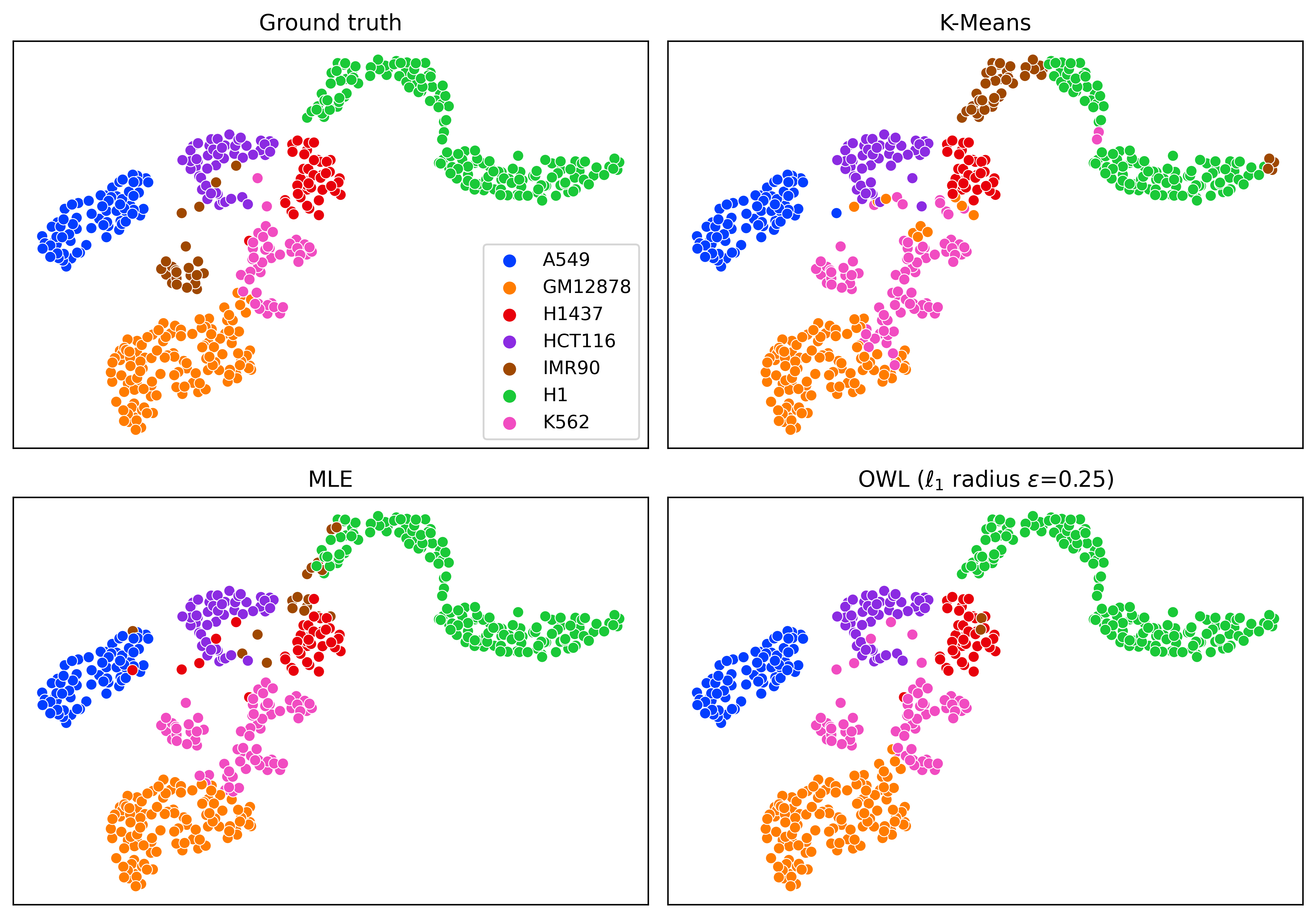

Figure 8 shows Uniform Manifold Approximation and Projection (UMAP) visualizations of the dataset clustered under the various methods (for one arbitrary run). We see that of all the methods, K-means performs worst by a significant margin. The improved performance of OWL (with ) over MLE can be mostly attributed to the better resolution the boundary between the K562 and GM12878. However, all methods struggle to identify the IMR90 cell lines as a cluster distinct from K562.

6.2 Exploratory analysis with OWL

In some settings, it is desirable to segment a dataset into those data points that are well-described by a model in the class (so-called inliers) and those that do not conform well to the model class (outliers). One interpretation of the weights that are learned by the OWL procedure is that, subject to the constraint that they are close in TV distance to the empirical distribution, they represent the most optimistic reweighting of the data relative to the model class. Thus, one might suspect that data points with higher weights are inliers and those with lower weights are outliers. Here, we explore inlier/outlier detection with OWL weights by classifying all data points with weights less than (the average value) as outliers, and the remainder as inliers.

The middle panel of Figure 7 shows the ARI of the OWL procedure when we restrict to the detected inliers. We observe that for all values of , the ARI is no lower on the selected inliers than on the whole dataset, and in some cases is significantly higher. This suggests that the OWL procedure identifies a ‘core’ set of points that are both well-described by a mixture of Gaussians as well as aligned with the ground truth clustering. The right panel of Figure 7 shows the fraction of data points that are classified as inliers. Although it is theoretically possible for the OWL weights to classify anywhere from 1 to points as outliers for any value of , we see that the fraction of outliers is relatively small for low values of and only increases gradually as increases.

| OWL radius () | 0.05 | 0.15 | 0.25 | 0.35 | 0.45 | 0.55 | 0.65 | 0.75 | 0.85 | 0.95 |

|---|---|---|---|---|---|---|---|---|---|---|

| Selected | 6 | 6 | 8 | 7 | 7 | 7 | 5 | 4 | 4 | 4 |

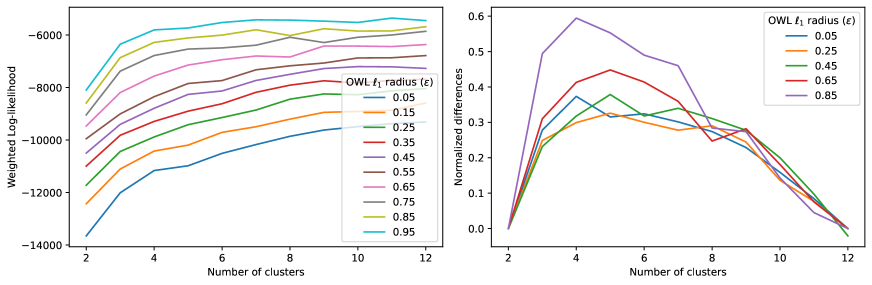

In many settings, the number of ground truth clusters are not known a priori. A common way to deal with this problem is to plot a metric such as sum-of-squares errors or log-likelihood and look for ‘elbows’ or ‘knees’ in the graph where there are diminishing returns for increasing model capacity. Here, we apply the ‘kneedle’ algorithm (Satopaa et al., 2011) to the weighted log-likehood produced by the OWL procedure. The kneedle algorithm computes the normalized differences of a given function and selects the value that maximizes the corresponding normalized differences. Figure 9 shows both the weighted log-likelihoods as well as a subset of the normalized difference graphs. Table 2 shows the selected numbers of clusters for various values of . We see that for relatively small values of , this results in number of clusters that is close to the ground truth. While for larger values of , this procedure underestimates the number of clusters in the data. This agrees with the observation in the right panel of Figure 7 that larger values of result in fewer points being identified as inliers, and thus fewer clusters are needed to describe those points.

7 Application to micro-credit study

In this section we apply the OWL methodology to data from a micro-credit study (Angelucci et al., 2015) for which standard methods of parameter inference have been shown to be brittle to the removal of a handful of observations (Broderick et al., 2020). In Angelucci et al. (2015) the authors conducted a (clustered) randomized trial in Mexico to study the impact of availability of micro-credit on outcome measures in the community including micro-entrepreneurship, income, labor supply, consumption, social status, and subjective well-being. The authors worked with Compartamos Banco, one of the largest micro-lenders in Mexico, to randomize their rollout across 238 geographical regions in the north-central Sonora state in Mexico (close to the Mexico and United States border); within 18-34 months after this rollout, the authors surveyed households from these regions for various outcome measures to study the impact of the rollout.

While it is possible to perform a detailed analysis using more outcomes and covariates from the survey data (Angelucci et al., 2015), following Broderick et al. (2020), here we focus on the Average Intention to Treat effect (AIT) of the rollout on household profits. More precisely for , let denote the profit of the th household during the last fortnight (measured in USD PPP), and let be a binary variable that is one if and only if the household falls in the geographical region where the credit rollout happened. The AIT on household profits is defined as the coefficient in the linear model:

| (10) |

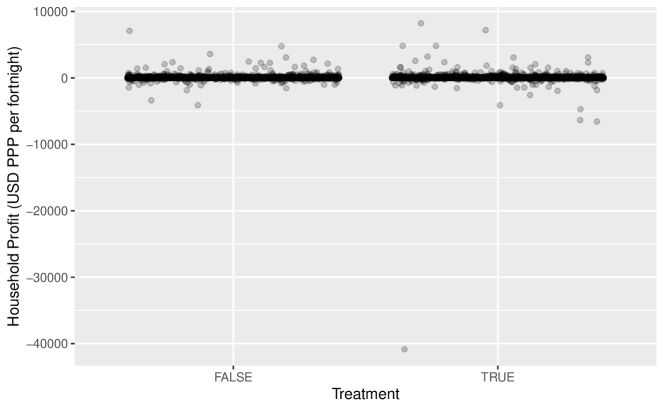

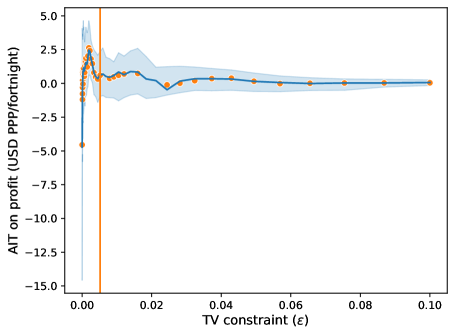

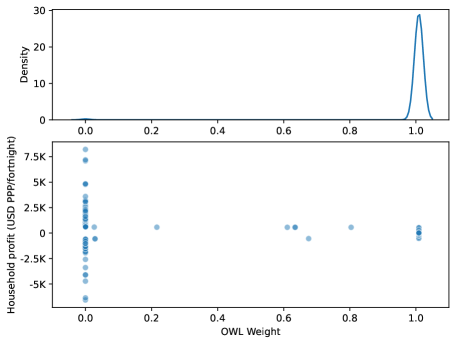

To reproduce the brittleness in estimating the AIT on household profits demonstrated in Broderick et al. (2020), we first obtained the profit data (originally from Angelucci et al. (2015)) as imputed and scaled by Meager (2019). The MLE estimate of USD PPP per fortnight (standard error [s.e.] of 5.88), changes to USD PPP per fortnight (s.e. 3.19) if we remove a single household identified by the zaminfluence R package (Broderick et al., 2020). Moreover, by removing 14 further observations which were identified by the zaminfluence package, we observe that the non-significant value of the MLE estimate can be changed to a significant value of USD PPP (s.e. 2.57). As seen in a scatter-plot summarizing the data (Appendix G, Figure 15), this brittleness of the MLE is likely due to a small fraction of households with outlying profit values.

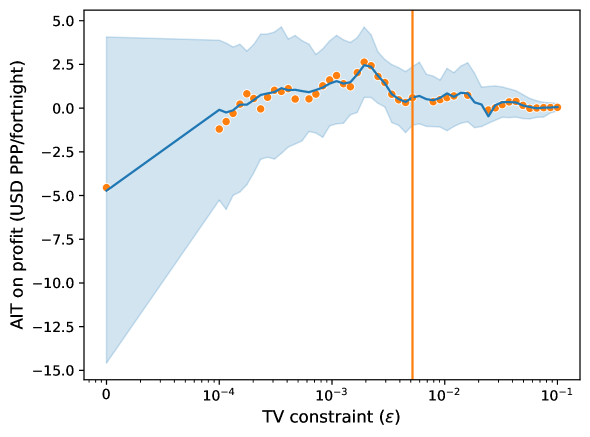

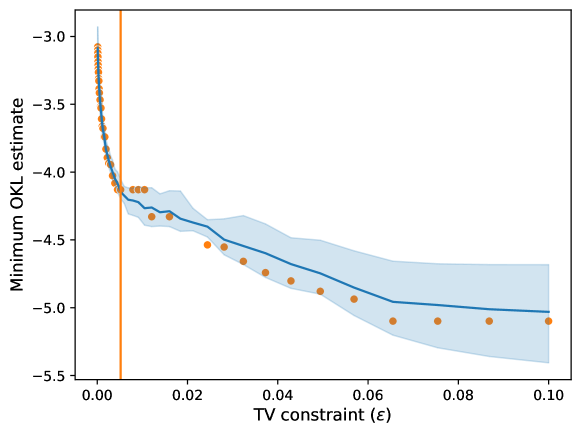

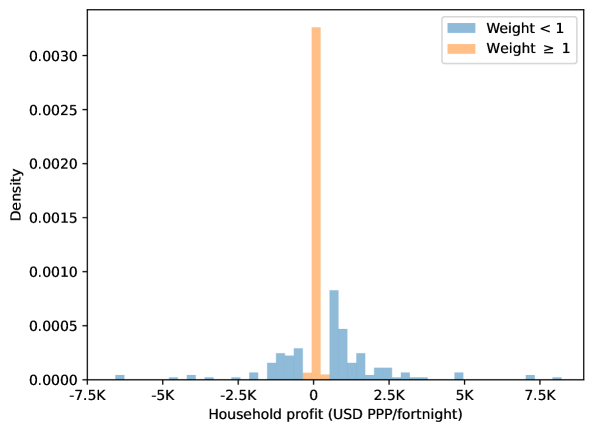

Here we compare OWL to this data deletion approach by fitting the model (10) to the full data set using 50 -spaced -values between and , and used the tuning procedure in Section 2.2.3 to obtain the value where the minimum-OKL versus epsilon plot (Appendix G, Figure 17) has its most prominent kink. We also calculate the MLE, which corresponds to the OWL procedure with . The AIT on household profit estimated by OWL as a function of can be seen in the left panel of Figure 10. For values of below , the AIT estimates change rapidly as changes, while for values of above , the AIT estimates are quite stable with changes in . This is due to OWL automatically down-weighting the outlying observations, as seen in the right panel of Figure 10.

To quantify uncertainty in the AIT estimates obtained by OWL at the aforementioned grid of values for , we reran the above analysis on independently bootstrapped data sets of size each. Since we wanted to retain a small fraction of outlying observations in each data set, we used an outlier-stratified (OS) sampling strategy. Namely, in each iteration, the new data set was obtained by combining a bootstrap sample of the (roughly ) households that were down-weighted by the OWL procedure at and a bootstrap sample from the remaining households that were not down-weighted.

The resulting 90% OS-bootstrap confidence bands for estimates of AIT and minimum-OKL as a function of can be found in Appendix G (also see the left panel in Figure 10). From Figure 16 in Appendix G, the confidence bands for AIT estimates from OWL are much wider when than they are when . Hence, if we presume that the outlying households are the ones down-weighted by OWL at , the relatively narrow bootstrap confidence bands for the AIT estimates at suggest that OWL is able to successfully prevent brittleness in estimation due to those outliers.

In summary, the OWL procedure chose to down-weight roughly 1% of the households with extreme profit values and estimated an AIT of USD PPP per fortnight based on the selected value of . The value , tuned using the procedure in Section 2.2.3, roughly coincides with the point at which the AIT estimates become stable with respect to and also with the point at which the 90% OS-bootstrap confidence bands for AIT become narrower — both suggesting that OWL with the choice has identified and down-weighted outliers that may be causing brittleness in estimating AIT.

8 Discussion

In this paper, we introduced the optimistically weighted likelihood (OWL) methodology, motivated by brittleness issues arising from misspecification in statistical methodology based on standard likelihoods. On the theoretical side, we established the consistency of our approach and showed its asymptotic connection to the coarsened inference methodology. We also proposed a feasible alternating optimization scheme to implement the methodology and demonstrated its empirical utility on both simulated and real data.

The OWL methodology opens up several interesting future directions. One practical open problem is how to scale to larger datasets. As a weighted likelihood method, OWL requires solving for a weight vector whose dimension is the size of the dataset. While we can solve the resulting convex optimization problem for thousands of data points, the procedure becomes significantly more complicated when the size of the dataset exceeds computer memory. How do we maintain a feasible solution, i.e. one that lies in the intersection of the simplex and some probability ball, when the entire vector cannot fit in memory?

Another practical question is how to apply the OWL approach in more complex models; for example, involving dependent data. This may be relatively straightforward for models in which the likelihood can still be written in product form due to conditional independence given random effects. This would open up its application to nested, longitudinal, spatial and temporal data, as random effects models are routinely used in such settings.

On the theoretical side, there remain important gaps to fill between our theory and practice. In particular, our theory for continuous spaces required the use of kernels to smooth our approximations to the OKL. However, in practice, we observed that generally no such smoothing is necessary, and we may simply use the finite space approximation to the OKL to achieve excellent results. Resolving this gap would have important implications for the general applicability of the OWL methodology.

Finally, a very interesting question is how to choose the corruption parameter for our procedure. In our simulation study (Section 5) we chose in two ways: using the data based tuning procedure in Section 2.2.3, and using knowledge of the true corruption fraction at the population level, both of which lead to an equally robust performance. In contrast, for our application (Section 6) we explored model fit on a range of values. The population setup based on a general distance (recall Section 2.1 focused on ) can provide more insights on how the choice of affects parameter inference. The OWL procedure interpolates between the maximum-likelihood estimate at and minimum-distance estimate at , where , while choosing much larger values of will eventually degrade performance. Is it possible that OWL with well-chosen can get us the best of both worlds—efficiency from the likelihood and robustness from the distance? Some of these properties can be understood by studying asymptotic properties of the parameter estimates from OWL, which is an open direction for future work.

References

- Agostinelli and Greco [2013] C. Agostinelli and L. Greco. A weighted strategy to handle likelihood uncertainty in Bayesian inference. Computational Statistics, 28(1):319–339, 2013.

- Alquier et al. [2022] P. Alquier, B.-E. Chérief-Abdellatif, A. Derumigny, and J.-D. Fermanian. Estimation of copulas via maximum mean discrepancy. Journal of the American Statistical Association, 0(0):1–16, 2022.

- Amari [2016] S. Amari. Information geometry and its applications. Springer, 2016.

- Andrews and Hemberg [2019] T. S. Andrews and M. Hemberg. M3Drop: Dropout-based feature selection for scRNASeq. Bioinformatics, 35(16):2865–2867, 2019.

- Angelucci et al. [2015] M. Angelucci, D. Karlan, and J. Zinman. Microcredit impacts: Evidence from a randomized microcredit program placement experiment by Compartamos Banco. American Economic Journal: Applied Economics, 7(1):151–182, 2015.

- Barp et al. [2019] A. Barp, F.-X. Briol, A. Duncan, M. Girolami, and L. Mackey. Minimum Stein discrepancy estimators. In Advances in Neural Information Processing Systems, pages 12964–12976, 2019.

- Barratt et al. [2021] S. Barratt, G. Angeris, and S. Boyd. Optimal representative sample weighting. Statistics and Computing, 31(2):1–14, 2021.

- Bartlett and Mendelson [2002] P. L. Bartlett and S. Mendelson. Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3:463–482, 2002.

- Basu et al. [1998] A. Basu, I. R. Harris, N. L. Hjort, and M. Jones. Robust and efficient estimation by minimising a density power divergence. Biometrika, 85(3):549–559, 1998.

- Beran [1981] R. Beran. Efficient robust estimates in parametric models. Zeitschrift fuer Wahrscheinlichkeitstheorie und verwwandte Gebiete, 55:91–108, 1981.

- Bernardo and Smith [2009] J. M. Bernardo and A. F. Smith. Bayesian Theory. John Wiley & Sons, 2009.

- Bhatia et al. [2023] K. Bhatia, Y.-A. Ma, A. D. Dragan, P. L. Bartlett, and M. I. Jordan. Bayesian robustness: A nonasymptotic viewpoint. Journal of the American Statistical Association, 0(0):1–25, 2023.

- Billingsley [2013] P. Billingsley. Convergence of probability measures. John Wiley & Sons, 2013.

- Bissiri et al. [2016] P. G. Bissiri, C. C. Holmes, and S. G. Walker. A general framework for updating belief distributions. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(5):1103–1130, 2016.

- Boucheron et al. [2005] S. Boucheron, O. Bousquet, and G. Lugosi. Theory of classification: A survey of some recent advances. ESAIM: Probability and Statistics, 9:323–375, 2005.

- Boyd et al. [2011] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3(1):1–122, 2011.

- Bradic [2016] J. Bradic. Robustness in sparse high-dimensional linear models: Relative efficiency and robust approximate message passing. Electronic Journal of Statistics, 10(2):3894–3944, 2016.

- Bradic et al. [2011] J. Bradic, J. Fan, and W. Wang. Penalized composite quasi-likelihood for ultrahigh dimensional variable selection. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73(3):325–349, 2011.

- Briol et al. [2019] F.-X. Briol, A. Barp, A. B. Duncan, and M. Girolami. Statistical inference for generative models with maximum mean discrepancy. arXiv preprint arXiv:1906.05944, 2019.

- Broderick et al. [2020] T. Broderick, R. Giordano, and R. Meager. An automatic finite-sample robustness metric: When can dropping a little data make a big difference? arXiv preprint arXiv:2011.14999, 2020.

- Budhiraja and Dupuis [2019] A. Budhiraja and P. Dupuis. Analysis and approximation of rare events. Springer, 2019.

- Chandra et al. [2020] N. K. Chandra, A. Canale, and D. B. Dunson. Escaping the curse of dimensionality in Bayesian model based clustering. arXiv preprint arXiv:2006.02700, 2020.

- Cherief-Abdellatif and Alquier [2020] B.-E. Cherief-Abdellatif and P. Alquier. MMD-Bayes: Robust Bayesian estimation via maximum mean discrepancy. In Proceedings of The 2nd Symposium on Advances in Approximate Bayesian Inference, pages 1–21, 2020.

- Chérief-Abdellatif and Alquier [2022] B.-E. Chérief-Abdellatif and P. Alquier. Finite sample properties of parametric MMD estimation: Robustness to misspecification and dependence. Bernoulli, 28(1):181–213, 2022.

- Claeskens and Hjort [2008] G. Claeskens and N. L. Hjort. Model selection and model averaging. Cambridge University Press, 2008.

- Condat [2016] L. Condat. Fast projection onto the simplex and the ball. Mathematical Programming, 158(1):575–585, 2016.

- Copas [1995] J. Copas. Local likelihood based on kernel censoring. Journal of the Royal Statistical Society: Series B (Methodological), 57(1):221–235, 1995.

- Cover and Thomas [2006] T. M. Cover and J. A. Thomas. Elements of information theory. John Wiley & Sons, second edition, 2006.

- Csiszár [1975] I. Csiszár. I-divergence geometry of probability distributions and minimization problems. The Annals of Probability, 3(1):146–158, 1975.

- Dellaporta et al. [2022] C. Dellaporta, J. Knoblauch, T. Damoulas, and F.-X. Briol. Robust Bayesian inference for simulator-based models via the MMD posterior bootstrap. In Proceedings of The 25th International Conference on Artificial Intelligence and Statistics, pages 943–970, 2022.

- Dembo and Zeitouni [2010] A. Dembo and O. Zeitouni. Large Deviations Techniques and applications. Springer Berlin Heidelberg, 2010.

- Dempster et al. [1977] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society: Series B (Methodological), 39(1):1–22, 1977.

- Diakonikolas et al. [2017] I. Diakonikolas, G. Kamath, D. M. Kane, J. Li, A. Moitra, and A. Stewart. Being robust (in high dimensions) can be practical. In Proceedings of the 34th International Conference on Machine Learning, pages 999–1008, 2017.

- Diakonikolas et al. [2019] I. Diakonikolas, D. Kane, S. Karmalkar, E. Price, and A. Stewart. Outlier-robust high-dimensional sparse estimation via iterative filtering. In Advances in Neural Information Processing Systems, 2019.

- Diakonikolas et al. [2020] I. Diakonikolas, S. B. Hopkins, D. Kane, and S. Karmalkar. Robustly learning any clusterable mixture of Gaussians. arXiv preprint arXiv:2005.06417, 2020.

- Dupuis and Morgenthaler [2002] D. J. Dupuis and S. Morgenthaler. Robust weighted likelihood estimators with an application to bivariate extreme value problems. Canadian Journal of Statistics, 30(1):17–36, 2002.

- Eguchi and Copas [1998] S. Eguchi and J. Copas. A class of local likelihood methods and near-parametric asymptotics. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 60(4):709–724, 1998.

- Field and Smith [1994] C. Field and B. Smith. Robust estimation: A weighted maximum likelihood approach. International Statistical Review/Revue Internationale de Statistique, 62(3):405–424, 1994.

- Fong et al. [2021] E. Fong, C. Holmes, and S. G. Walker. Martingale posterior distributions. arXiv preprint arXiv:2103.15671, 2021.

- Gervini and Yohai [2002] D. Gervini and V. J. Yohai. A class of robust and fully efficient regression estimators. The Annals of Statistics, 30(2):583–616, 2002.

- Ghosh and Basu [2016] A. Ghosh and A. Basu. Robust Bayes estimation using the density power divergence. Annals of the Institute of Statistical Mathematics, 68:413–437, 2016.

- Ghourchian et al. [2017] H. Ghourchian, A. Gohari, and A. Amini. Existence and continuity of differential entropy for a class of distributions. IEEE Communications Letters, 21(7):1469–1472, 2017.

- Greco et al. [2008] L. Greco, W. Racugno, and L. Ventura. Robust likelihood functions in Bayesian inference. Journal of Statistical Planning and Inference, 138(5):1258–1270, 2008.

- Green [1984] P. J. Green. Iteratively reweighted least squares for maximum likelihood estimation, and some robust and resistant alternatives. Journal of the Royal Statistical Society: Series B (Methodological), 46(2):149–170, 1984.

- Gretton et al. [2006] A. Gretton, K. Borgwardt, M. Rasch, B. Schölkopf, and A. Smola. A kernel method for the two-sample-problem. In Advances in Neural Information Processing Systems, 2006.