Classification and calibration of affine models driven by independent Lévy processes

Abstract

The paper is devoted to the study of the short rate equation of the form

| (1) |

with deterministic functions and independent Lévy processes of infinite variation with regularly varying Laplace exponents. The equation is supposed to have a nonnegative solution which generates an affine term structure model. A precise form of the generator of is characterized and a related classification of equations which generate affine models introduced in the spirit of Dai and Singleton [9]. Each class is shown to have its own canonical representation which is an equation with the same drift and the jump diffusion part based on a Lévy process taking values in , with independent coordinates being stable processes with stability indices in the range . Numerical calibration results of canonical representations to the market term structure of interest rates are presented and compared with the classical CIR model. The paper generalizes the classical results on the CIR model from [12], as well as on its extended version from [3] and [4] where was a one-dimensional Lévy process.

1 Introduction

The study of continuous state branching processes with immigration (CBI) by Kawazu and Watanabe [16] revealed attractive analytical properties of affine processes which motivated Filipović to bring them, in the pioneering paper [14], in the field of finance. Affine processes are widely used in various areas of mathematical finance. They appear in term structure models, by credit risk modelling and are applied within the stochastic volatility framework. Solid fundamentals of affine processes in finance were laid down by Filipović [14] and by Duffie, Filipović and Schachermeyer [10]. The results obtained in these papers settled a reference point for further research and proved the usefulness and strength of the Markovian approach. Missing questions on regularity and existence of càdlàg versions were answered by Cuchiero, Filipović and Teichmann [7] and Cuchiero and Teichmann [8].

The systematic study of affine processes in finance was motivated by classical stochastic short rate models, like CIR (Cox, Ingersoll, Ross) [12], Vasiček [19] and model with diffusion factors of Dai and Singleton [9], and resulted in discovering new stochastic equations, also with jumps; see, among others, [14], Duffie and Gârleanu [11], Barndorff-Nielsen and Shephard [2], Jiao, Ma and Scotti [15]. Nevertheless, the full description of affine processes representable in terms of stochastic equations is far from being clear. This is because the Markovian description of affine processes based on generators does not, in general, allow encoding the form of a possible underlying stochastic equation. The framework based on stochastic dynamics offers, however, unquestionable advantages like discretization schemes enabling Monte Carlo simulations which are essential for example for pricing exotic, i.e. path-dependent, derivatives. A comprehensive treatment of simulating schemes for affine processes and pricing methods can be found in [1]. Stochastic equations allow also identifying the number of random sources in the model which is of some use by calibration and hedging. In this paper we focus on recovering from the Markovian setting those affine processes which are given by stochastic equations driven by a multidimensional Lévy process with independent coordinates. Specifically, we focus on the equation

| (1.1) |

where is a nonnegative constant, , are deterministic functions and are independent Lévy processes and martingales. A solution , if nonnegative, will be identified here with the short rate process which defines the bank account process by

Related to the savings account are zero coupon bonds. Their prices form a family of stochastic processes , parametrized by their maturity times . The price of a bond with maturity at time is equal to its nominal value, typically assumed, also here, to be , that is . The family of bond prices is supposed to have the affine structure, which means that

| (1.2) |

for some smooth deterministic functions , . Hence, the only source of randomness in the affine model (1.2) is the short rate process given by (1.1). As the resulting market constituted by should exclude arbitrage, the discounted bond prices

are supposed to be local martingales for each . This requirement affects in fact our starting equation (1.1). Thus the functions , and the noise should be chosen such that has a nonnegative solution for any and such that, for some functions , and each , is a local martingale on . If this is the case, (1.1) will be called to generate an affine model or to be a generating equation, for short.

The description of all generating equations with one-dimensional noise is well known, see Section 2.2.2 for a brief summary. This paper deals with (1.1) in the case . The multidimensional setting makes the description of generating equations more involved due to the fact that two apparently different generating equations may have solutions which are Markov processes with identical generators. For brevity, we will call such solutions ’identical’ or ’the same solutions’. The resulting bond markets are then the same, so such equations can be viewed as equivalent. This phenomenon does not appear in the one-dimensional case, but was a central point in the study of a multi-factor affine models by Dai and Singleton [9]. Recall, in the class of affine models considered in [9] the short rate is an affine function of factors , which are given by a diffusion equation of the form

| (1.3) |

where is a specific affine function, are matrices, is a vector in and the value of is the diagonal matrix with the coordinates of on the diagonal. Above stands for the Wiener process in . By particular choices of parameters, one may recognize in (1.3) many specific models used in practice, for details see [9]. The question of characterization of equations (1.3) which generate affine models was handled in [9], see also [6], by classifying the structure of factors. The classification is based on the parameter interpreted as a degree of dependence of the conditional variances on the number of factors. Each equation (1.3) which generates an affine model is classified as a member of one of disjoint subfamilies

of equations. All equations within a chosen subfamily provide the same short rate and the short rates differ across subfamilies. Moreover, each subfamily is shown to have its own canonical representation for which (1.3) simplifies, i.e. the diffusion matrix in (1.3) is diagonal. Although our setting based on equation (1.1) differs, our approach of characterizing generating equations has much in common with that of Dai and Singleton. The main results of the paper, i.e. Theorem 3.1, Corollary 3.2 and Proposition 3.3 imply that under mild assumptions any generating equation (1.1) has the same solution as that of the following equation

| (1.4) |

with some and parameters , , , , driven by independent stable processes with indices such that . All generating equations having the same solutions as (1.4) form a set which we denote by

| (1.5) |

where , is the Gamma function. We call (1.4) a canonical representation of (1.5). By changing values of the parameters in (1.5) one can thus split all generating equations into disjoint subfamilies with a tractable canonical representation for each of them.

The number and structure of generating equations which form (1.5) depend on the noise dimension in (1.1). As one may expect, the set (1.5) is getting larger as increases. In Section 3.3 we determine all generating equations on a plane by formulating concrete conditions for and in (1.1). For the class consists of a wide variety of generating equations while turns out to be a singleton. The passage to the case makes, however, a non-singleton. This phenomenon is discussed in Section 3.4.

A tractable form of canonical representations is supposed to be an advantage for applications. One finds in (1.4) with the classical CIR equation and may expect that additional stable noise components improve the model of bond market. For and equation (1.4) becomes the alpha-CIR equation studied in [15]. It was shown in [15] that empirical behaviour of the European sovereign bond market is closer to that implied by the alpha-CIR equation than by the CIR equation due to the permanent overestimation of the short rates by the latter one. The alpha-CIR equation allows also reconciling low interest rates with large fluctuations related to the presence of jump part whose tail fatness is controlled by the parameter . In the last part of the paper we focus on the calibration of canonical representations to market data. Into account are taken the spot rates of European Central Bank implied by the - ranked bonds, Libor rates and six-month swap rates. We compute numerically the fitting error for (1.1) in the Python programming language with in the range from up to . This illustrates, in particular, the influence of on the reduction of fitting error which is always less than in the CIR model. The freedom of choice of stability indices makes the canonical model curves more flexible, hence with shapes better adjusted to the market curves. The effect is especially visible for market data after March 2022 when the curves started to change their shapes.

The structure of the paper is as follows. In Section 2 we discuss the Laplace exponents of Lévy processes, in particular, the Laplace exponents of the projections of along , defined as the processes

| (1.6) |

which play a central role in the sequel. The second part of Section 2 is based on the preliminary characterization of generating equations, i.e. Proposition 2.2, which is a version of the result from [14] characterizing the generator of a Markovian short rate. This leads to a precise formulation of the problem studied in the paper. Further we describe one dimensional generating equations and discuss the non-uniqueness of generating equations in the multidimensional case. In Example 2.4 we show two different equations with the same solutions. Section 3 is concerned with the classification of generating equations. Section 3.1 contains the main results of the paper which provide a precise description of the generator of (1.1). This makes more specific the, rather abstract, result from [14] and motivates introducing the classification of generating equations. The required assumption on the Laplace exponent of the noise to vary regularly at zero is reformulated in terms of Lévy measure in Section 3.2. Section 3.3 and Section 3.4 are devoted to generating equations on a plane and an example in the three-dimensional case, respectively. In Section 4 we discuss the calibration of canonical representations.

2 Preliminaries

In this section we recall some facts on Lévy processes needed in the sequel and present a version of the result on generators of Markovian affine processes [14], see Proposition 2.2, which is used for a precise formulation of the problem considered in the paper. We explain the meaning of the projections of the noise (1.6) and show in Example 2.4 two different generating equations having the same projections, hence identical solutions. For illustrative purposes we keep referring to the one-dimensional case where the forms of generating equations are well known, see Section 2.2.2 below. For the sake of notational convenience we often use a scalar product notation in and write (1.1) in the form

| (2.1) |

where and is a Lévy process in .

2.1 Laplace exponents of Lévy processes

Let be an -valued Lévy process with characteristic triplet . Recall, describes the drift part of , is a non-negative, symmetric, covariance matrix, characterizing the coordinates’ covariance of the Wiener part of , and is a measure on describing the jumps of . It is called the Lévy measure of and satisfies the condition

| (2.2) |

Recall, admits a representation as a sum of four independent processes of the form

| (2.3) |

called the Lévy-Itô decomposition of . Above and stand for the jump measure and the compensated jump measure of , respectively. If

| (2.4) |

then is of infinite variation. If (2.4) does not hold and has no Wiener part, the variation of is finite. The coordinates of are independent if and only if is diagonal and is concentrated on axes.

We consider the case when is a martingale and call it a Lévy martingale for short. Its drift and the Lévy measure are such that

| (2.5) |

Consequently, the characteristic triplet of is

| (2.6) |

and (2.3) takes the form

where and are independent. The martingale will be called the jump part of . Its Laplace exponent , defined by the equality

| (2.7) |

has the following representation

| (2.8) |

and is finite for satisfying

By the independence of and we see that

so the Laplace exponent of equals

| (2.9) |

Example 2.1 (-stable martingales with )

A real valued stable martingale with index and positive jumps only is a Lévy process without Wiener part with Lévy measure of the form

Its Laplace exponent is given by

| (2.10) |

with

| (2.11) |

where stands for the Gamma function. Analogously one defines an -stable process with negative jumps only.

Note that the case of Lévy martingale with the stability index corresponds to the case when is a Wiener process without drift and with vanishing Lévy measure.

2.1.1 Projections of the noise

For equation (2.1) we consider the projections of along given by

| (2.12) |

As linear transformations of , the projections form a family of Lévy processes parametrized by . If is a martingale, then is a real-valued Lévy martingale for any . It follows from the identity

and (2.9) that the Laplace exponent of equals

| (2.13) |

Formula (2.13) can be written in a simpler form by using the Lévy measure of , which is the image of the Lévy measure under the linear transformation . This measure is given by

| (2.14) |

From (2.13) we obtain that

| (2.15) |

Thus the characteristic triplet of the projection has the form

| (2.16) |

Above we used the restriction by cutting off zero which may be an atom of .

2.2 Preliminary characterization of generating equations

In Proposition 2.2 below we provide a preliminary characterization for (2.1) to be a generating equation. Note that the independence of coordinates of is not assumed here. The central role here play the noise projections (2.12). The result is deduced from Theorem 5.3 in [14], where the generator of a general non-negative Markovian short rate process for affine models was characterized.

Proposition 2.2

Let be a Lévy martingale with characteristic triplet (2.6) and be its projection (2.12) with the Lev́y measure given by (2.14).

-

(A)

Equation (1.1) generates an affine model if and only if the following conditions are satisfied:

-

a)

For each the support of is contained in which means that has positive jumps only, i.e. for each , with probability one,

(2.17) -

b)

The jump part of has finite variation, i.e.

(2.18) -

c)

The characteristic triplet (2.16) of is linear in , i.e.

(2.19) (2.20) for some and a measure

(2.21) -

d)

The function is affine, i.e.

(2.22)

-

a)

-

(B)

Equation (1.1) generates an affine model if and only if the generator of is given by

(2.23) for , where is the linear hull of and stands for the set of twice continuously differentiable functions with compact support in . The constants and the measures are those from part (A).

The poof of Proposition 2.2 is postponed to Appendix.

Note that conditions (2.19)-(2.20) describe the distributions of the noise projections. In the sequel we use an equivalent formulation of (2.19)-(2.20) involving the Laplace exponents of (2.12). Taking into account (2.15) we obtain the following.

Remark 2.3

2.2.1 Problem formulation

In virtue of part of Proposition 2.2 we see that the drift of a generating equation is an affine function while the function and the noise must provide projections with particular distributions. Their characteristic triplets are characterized by a constant carrying information on the variance of the Wiener part and two measures , describing jumps. A pair for which the projections satisfy (2.18)-(2.21) will be called a generating pair. Note that the concrete forms of the measures , are, however, not specified. As for with independent coordinates of infinite variation necessarily , see Proposition 3.5, and, consequently, vanishes, our goal is to determine the measure in this case.

Having the required form of at hand one knows the distributions of the noise projections and, by part of Proposition 2.2, also the generator of the solution of (2.1). The generating pairs can not be, however, uniquely determined, except the one-dimensional case. This issue is discussed in Section 2.2.2 and Section 2.2.3 below. For this reason we construct canonical representations - generating equations with noise projections corresponding to a given form of the measure .

2.2.2 One-dimensional generating equations

Let us summarize known facts on generating equations in the case . If is a Wiener process, the only generating equation is the classical CIR equation

| (2.26) |

with , , see [12]. The case with a general one-dimensional Lévy process was studied in [3], [4] and [5] with the following conclusion. If the variation of is infinite and , then must be an -stable process with index , with either positive or negative jumps only, and (1.1) has the form

| (2.27) |

with and such that it has the same sign as the jumps of . Clearly, for equation (2.27) becomes (2.26). If is of finite variation then the noise enters (1.1) in the additive way, that is

| (2.28) |

Here can be chosen as an arbitrary process with positive jumps, and

where stands for the Lévy measure of . The variation of is finite, so is the right side above. Recall, (2.28) with being a Wiener process is the well known Vasiček equation, see [19]. Then the short rate is a Gaussian process, hence it takes negative values with positive probability. This drawback is eliminated by the jump version of the Vasiček equation (2.28), where the solution never falls below zero.

2.2.3 Non-uniqueness in the multidimensional case

In the case one should not expect a one to one correspondence between the triplets and the generating equations (2.1). The reason is that the distribution of the noise projections does not determine the pair in a unique way. Our illustrating example below shows two different equations driven by Lévy processes with independent coordinates which provide the same short rate .

Example 2.4

Let us consider the following two equations

| (2.29) | ||||

| (2.30) |

where

and

with a fixed index . We assume that the coordinates of and are independent. Above stand for -stable martingales like in Example 2.1 and are martingales with Lévy measures

respectively, where is a Borel subset of such that

The projections related to (2.29) and (2.30) take the forms

Since both processes and are -stable and have the same finite dimensional distributions, we obtain that

in the sense of distribution. Moreover, the Lévy measure of has the form

so it follows from (2.20) that is a generating pair and that the solutions of (2.29) and (2.30) are identical.

Note that the triplet from Proposition 2.2 is, for both pairs, of the form

so it coincides with the triplet in Section 2.2.2. Consequently, the solutions of (2.29) and (2.30) are the same as the solution of the equation

with a one-dimensional -stable process .

It follows, in particular, that the noise coordinates of a generating equation do not need to be stable processes.

3 Classification of generating equations

3.1 Main results

This section deals with equation (2.1) in the case when the coordinates of the martingale are independent. In view of Proposition 2.2 we are interested in characterizing possible distributions of projections over all generating pairs . By (2.17) the jumps of the projections are necessarily positive. As the coordinates of are independent, they do not jump together. Consequently, we see that, for each and

holds if and only if, for some ,

| (3.1) |

Condition (3.1) means that and are of the same sign. We can consider only the case when both are positive, i.e.

because the opposite case can be turned into this one by replacing with , . The Lévy measure of is thus concentrated on and, in view of (2.9), the Laplace exponent of takes the form

| (3.2) |

with . Recall, stands on the diagonal of - the covariance matrix of the Wiener part of . We will assume that are regularly varying at zero. Recall, this means that

for some function . In fact is a power function, i.e.

with some and is called to vary regularly with index . A characterization of regularly varying Laplace exponent in terms of the corresponding Lévy measure is presented in Section 3.2.

The distribution of noise projections are described by the following result.

Theorem 3.1

Let be independent coordinates of the Lévy martingale in . Assume that satisfy

| (3.3) |

or

| (3.4) |

Further, let us assume that for all the Laplace exponent (3.2) of varies regularly at zero and the components of the function satisfiy

Then (2.1) generates an affine model if and only if , , and the Laplace exponent of is of the form

| (3.5) |

with some and for .

Corollary 3.2

Let the assumptions of Theorem 3.1 be satisfied. If equation (2.1) generates an affine model then the function defined in (2.25) takes the form

| (3.6) |

with , (for the case we set , which means that disappears). Above if and otherwise. This means that is a weighted sum of stable measures with indices , i.e.

| (3.7) |

with , where is given by (2.11) .

Note that each generating equation can be identified by the numbers appearing in the formula for the function and from (3.5). Since , see Proposition 3.5 in the sequel, the related generator of takes, by (B), the form

| (3.8) |

with in (3.7). Recall, the constant above comes from the condition

| (3.9) |

and, in view of Remark 2.3, if and otherwise. The class of processes with generator of the form (3.1) will be denoted by

| (3.10) |

All generating equations with -dimensional noise satisfying assumptions of Theorem 3.1 are thus splitted into disjoint subfamilies providing different short rates. Any two equations from (3.10) with fixed parameters provide the same short rate, hence the same bond prices. For any class (3.10) we construct below a canonical representation, which is an equation with the generator required in (3.10) but with reduced noise dimension from to and stable noise coordinates. This construction allows interpreting the parameter in (3.10) as a minimal number of random factors necessary to obtain the short rate corresponding to (3.10) and are the stability indices of the noise coordinates. This idea of classifying is similar to that of Dai and Singleton applied for multi-factor affine short rates in [9].

Proposition 3.3 (Canonical representation of )

Let be the solution of (2.1) with satisfying the assumptions of Theorem 3.1. Let be a Lévy martingale with independent stable coordinates with indices , respectively, and , , where and are given by (2.11), . Then

Consequently, if is the solution of the equation

| (3.11) |

then the generators of and are equal.

Equation (3.11) will be called the canonical representation of the class . Proof: By (3.5) we need to show that

Recall, the Laplace exponent of equals . By independence and the form of we have

as required. The second part of the thesis follows from Proposition 2.2(B).

Clearly, in the case the noise dimension can not be reduced, so and corresponds to the classical CIR equation (2.26) while to its generalized version (2.27). Both classes are singletons and (2.26), (2.27) are their canonical representations. The alpha-CIR equation from [15] is a canonical representation of the class with .

3.1.1 Proofs

The proofs of Theorem 3.1 and Corollary 3.2 are preceded by two auxiliary results, i.e. Proposition 3.4 and Proposition 3.5. The first one provides some useful estimation for the function

| (3.12) |

where the measure on satisfies

| (3.13) |

The second result shows that if all components of are of infinite variation then .

Proposition 3.4

Proof: Let us start from the observation that the function

is strictly decreasing, with limit at zero and at infinity. This implies

| (3.15) |

and, consequently,

This means, however, that

So, we have

and integration over some interval , where , yields

which gives that

To see that it is sufficient to use de l’Hôpital’s rule, (3.13) and dominated convergence

To see that we also use de l’Hôpital’s rule, (3.13) and dominated convergence. If , then we have

If then we apply de l’Hôpital’s rule twice and obtain

Proposition 3.5

If is a generating pair and all components of are of infinite variation then .

Proof: Let be a generating pair. Since the components of are independent, its characteristic triplet (2.6) is such that is a diagonal matrix, i.e.

and the support of is contained in the positive half-axes of , see [18] p.67. On the positive half-axis

| (3.16) |

for . The coordinate of is of infinite variation if and only if its Laplace exponent (3.2) is such that or

| (3.17) |

see [Kyprianou, Lemma 2.12]. It follows from (2.19) that

so if then . If it is not the case, using (3.16) and (2.18) we see that the integral

is finite, so if (3.17) holds then .

Proof of Theorem 3.1: By assumption (3.3) and Proposition 3.5 or by assumption (3.4) we have , so it follows from Remark 2.3 that

| (3.18) |

where , and is given by (2.25). This yields

| (3.19) |

where in the case we set . Without loss of generality we may assume that , ,, are non-zero (thus positive for positive arguments). By assumption, , vary regularly at with some indices , , so for

| (3.20) |

Assume that

where . Let us denote and

| (3.21) |

We can rewrite equation (3.19) in the form

| (3.22) |

By passing to the limit as , from (3.20) and (3.22) we get

| (3.23) |

thus

| (3.24) |

provided that the limits , , exist. Thus it remains to prove that for the limits indeed exist and that .

First we will prove that exists. Assume, by contrary, that this is not true, so

| (3.25) |

It follows from (3.18) that

| (3.26) |

Let now be small enough so that

| (3.27) |

Let us set in (3.22) and then divide both sides of (3.22) by . It follows from (3.26) that each term , , is bounded by . From this and (3.20) for sufficiently close to we have

and

thus from (3.22), two last estimates and (3.27)

But this contradicts (3.25) since we must have

Having proved the existence of the limits , …, we can proceed similarly to prove the existence of the limit . Assume that does not exist, so

| (3.28) |

Let be small enough so that

| (3.29) |

Let us set in (3.22) and then divide both sides of (3.22) by . For sufficiently close to we have

and

thus from (3.22), last three estimates and (3.29)

But this contradicts (3.28).

Now we are left with the proof that for , . Since the Laplace exponent of is given by (3.2), by Proposition 3.4 we necessarily have that varies regularly with index . Thus it remains to prove that . If it was not true we would have in (3.24) and . Then

but, again, by Proposition 3.4 it is not possible.

Proof of Corollary 3.2 : From Remark 2.3 and Theorem 3.1 we know that

where , , , , , . Without loss of generality we may assume that . Thus, since the Laplace exponent is nonnegative, is of the form

| (3.30) |

or

| (3.31) |

In the case (3.30) we need to show that . If it was not true, we would have

but this contradicts Proposition 3.4. In the same way we prove that in (3.31). This proves the required representation (3.6).

3.2 Characterization of regularly varying Laplace exponents

In this section we reformulate the assumption that , vary regularly at zero in terms of the behaviour of the Lévy measures of . As our considerations are componentwise, we write for simplicity for the Lévy measure of and for its Laplace exponent.

Proposition 3.6

Let be such that

| (3.32) |

Let be the measure

and its cumulative distribution function, i.e.

Then, for , the following conditions are equivalent

| (3.33) |

If, additionally, has a density function such that

| (3.34) |

then (3.33) is equivalent to the condition

Proof: Under (3.32) the function given by (3.12) is well defined for , twice differentiable and

see [17], Lemma 8.1 and Lemma 8.2. This implies that

Consequently, by (3.33)

| (3.35) |

Notice, that the left side is a quotient of two transforms of the measure . By the Tauberian theorem, see Theorem 1, Sec. XIII.5 in [13], we have that (3.35) holds if and only if

If has a density satisfying (3.34) then

It follows that

which proves the result.

Remark 3.7

By general characterization of regularly varying functions we see that the functions and from Proposition 3.6 must be of the forms

where and are slowly varying functions at , i.e.

3.3 Generating equations on a plane

In this section we characterize all equations (2.1), with , which generate affine models by a direct description of the classes and . Our analysis requires an additional regularity assumption that the components of are strictly positive outside zero and

| (3.36) |

Then consists of the following equations

where , are positive constants and is an -stable process,

where , is any function such that

and are stable processes with index .

The class is a singleton.

The classification above follows directly from the following result.

Theorem 3.8

Let be continuous functions such that and (3.36) holds. Let have independent coordinates of infinite variation with Laplace exponents varying regularly at zero with indices , respectively, where .

-

I)

If is of the form

(3.37) with , then is a generating pair if and only if one of the following two cases holds:

-

a)

(3.40) where and the process

is -stable.

-

b)

is such that

(3.41) with some constants , and are -stable processes.

-

a)

-

II)

If is of the form

(3.42) with then is a generating pair if and only if

(3.43) with some and is -stable, is -stable.

Proof: In view of Theorem 3.1 the generating pairs are such that

| (3.44) |

where takes the form (3.37) or (3.42). We deduce from (3.44) the form of and characterize the noise . First let us consider the case when

| (3.45) |

Then can be written in the form

with some function , and constants . Equation (2.1) amounts then to

which is an equation driven by the one dimensional Lévy process . It follows that is -stable with and that . Notice that , so and . Hence (3.37) holds and this proves .

If (3.45) is not satisfied, then

| (3.46) |

for some interval . In the rest of the proof we consider this case and prove and .

From the equation

| (3.47) |

we explicitly determine unknown functions. Inserting for yields

| (3.48) |

Differentiation over yields

Using (3.46) and dividing by leads to

By inserting for one computes the derivative of :

Fixing and integrating over provides

| (3.49) |

with some . Actually as is of infinite variation and can not disappear.

By the symmetry of (3.47) the same conclusion holds for , i.e.

| (3.50) |

with . Using (3.49) and (3.50) in (3.47) gives us (3.41). This proves .

Solving the equation

| (3.51) |

in the same way as we solved (3.47) yields that

| (3.52) |

with , . From (3.51) and (3.52) we can specify the following conditions for :

| (3.53) | ||||

| (3.54) |

We will show that by excluding the opposite cases.

If , one computes from (3.53)-(3.54) that

| (3.55) |

This means that, for each , the value is a solution of the following equation of the -variable

| (3.56) |

with . If or we compute from (3.56) and see that or must be negative either for sufficiently close to or sufficiently large. Now we need to exclude the case . However, in the case equation (3.56) has no solutions because, for sufficiently large , the left side of (3.56) is strictly less then the right side. This inequality follows from Proposition 3.9 proven below.

So, we proved that and similarly one proves that . The case can be rejected because then would vary regularly with index and with index , which is a contradiction. It follows that and in this case we obtain (3.43) from (3.53) and (3.54).

Proposition 3.9

Let , , . Then for sufficiently large the following inequalities are true

| (3.57) |

| (3.58) |

3.4 An example in 3D

In Section 3.3 we proved that in the case the set is a singleton. Here we show that this property breaks down when . In the example below we construct a family of generating pairs such that

| (3.60) |

with and such that the related generating equations differ from the canonical representation of .

Example 3.10

Let us consider a process with independent coordinates such that is -stable, is -stable, is a sum of an - and -stable processes. Then

where . We are looking for non-negative functions solving the equation

| (3.61) |

It follows from (3.61) that

and, consequently,

Thus we obtain the following system of equations

which allows us to determine and in terms of , that is

| (3.62) | |||

| (3.63) |

The positivity of means that satisfies

| (3.64) |

It follows that with any satisfying (3.64) and given by (3.62), (3.63) constitutes a generating pair.

4 Applications

Motivated by the form of canonical representations (3.11) we focus now on the equation

| (4.1) |

where and is an -stable process with and . By Proposition 3.3, (4.1) is the canonical representation of the class where

| (4.2) |

and is given by (2.11). After characterizing bond prices in the resulted affine model we investigate the flexibility of fitting of (4.1) to risk-free market curves. Our numerical implementations show better performance of (4.1) in comparison to the standard CIR equation (2.26).

Let us start with recalling the concept of pricing based on the semigroup

| (4.3) |

which was developed in [14]. The formula provides the price at time of the claim paid at time given . By Theorem 5.3 in [14] for we know that

| (4.4) |

where satisfies the equation

and is given by

The functions depend on the generator of , which for (4.1) takes the form

where

| (4.5) |

Recall, if , then and . Otherwise and . Then

| (4.6) |

Using (4.5) yields

| (4.7) |

Application of the pricing procedure above for with allows us to obtain from (4.4) the prices of zero-coupon bonds. Using the closed form formula (4) leads to the following result.

Theorem 4.1

In the case when and equation (4.9) becomes a Riccati equation and its explicit solution provides bond prices for the classical CIR equation. In the opposite case (4.9) can be solved by numerical methods which exploit the tractable form of the function given by (4). Note that is continuous, and . Thus is a positive number and

| (4.11) |

The function

| (4.12) |

is strictly increasing and its behaviour near can be estimated by substituting in (4.12) and using the inequality

For the case when this yields for

| (4.13) |

It follows from (4) and (4.11) that

so is invertible and exists on . Writing (4.9) as

we see that

and consequently

Representing as the inverse of enables its numerical computation. Hence, with at hand we can derive bond prices, spot rates and swap rates in the model generated by (4.1). The dependence of on the parameters plays a central role in the problem of fitting the model to real data. In what follows we present the results of calibration of (4.1) to market quotes of spot rates, Libor and swap rates.

4.1 Calibration of canonical models to market data

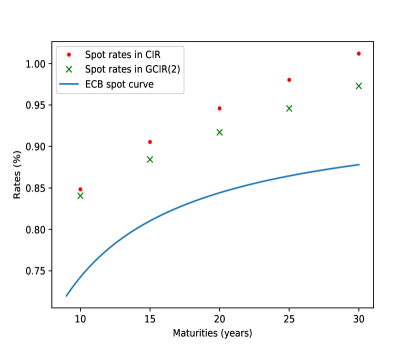

Our first calibration procedure is concerned with the spot yield curves of European Central Bank (ECB) computed from the zero coupon AAA-rated bonds. The maturity grip consists of points starting from months and ending with 30 years. This set was, however, restricted to points to speed up computations. All maturities less than years were included to save rapid changes of the curves near zero. A glance at the historical data from 2016 to 2023 reveals significant changes in the shape of curves appearing after March 2022. The classical CIR model could be fitted relatively well to previous curves but performed much worse for the newer ones. In both cases, however, the addition of new stable noise components resulted in reduction of the calibration error. For a calibration based on maturities the fitting error measures a relative distance of the model spot rates

| (4.14) |

from the empirical ones . It is given by the formula

| (4.15) |

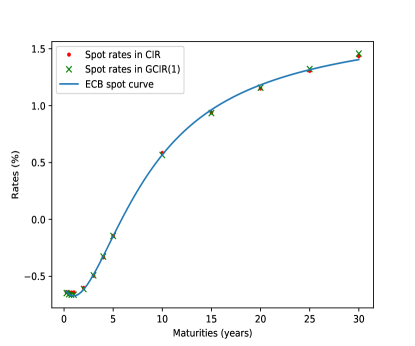

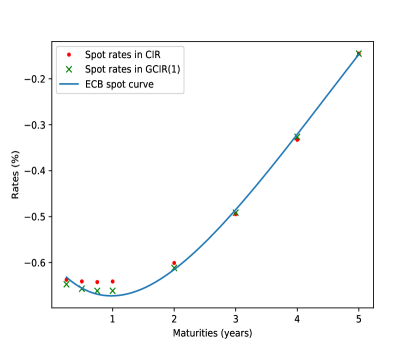

For the curve from 10.01.2018 we can see that a good fitting of the CIR model can be substantially improved by replacing the Wiener process by a stable noise with index . The effect is strongly apparent especially for small maturities, see Fig. 1. The increase of the number of noise components causes further decrease of the fitting error but in a lesser extent, see Tab. 1, where GCIR(g) stands for the generalized CIR equation (4.1) with components.

| Model | Calibration error | Stability indices |

|---|---|---|

| CIR | 0.95141785 | |

| GCIR(1) | 0.44735953 | |

| GCIR(2) | 0.44505444 | , |

| GCIR(3) | 0.44148324 | , , |

| GCIR(4) | 0.43932515 | , , , |

| GCIR(5) | 0.43918035 | , , , , |

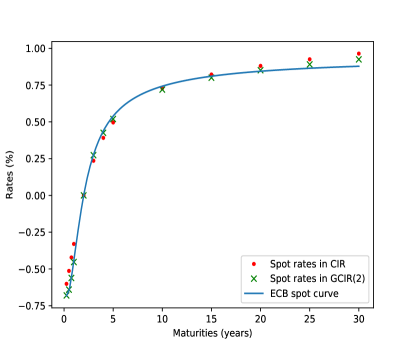

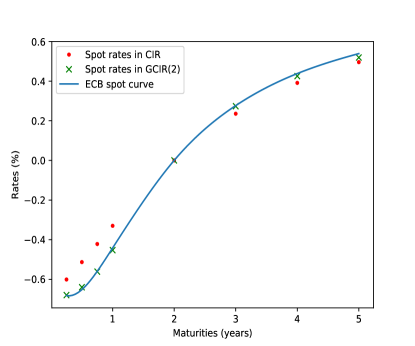

For the data from 8.04.2022 the CIR model turned out to be the most efficient among one dimensional models, though the fitting error is much greater then in the previous example, see Tab. 2 and Fig. 2. Models with higher noise dimension provide, however, better results starting from the gratest error reduction by the alpha-CIR model of [15] with .

| Model | Calibration error | Stability indices |

|---|---|---|

| CIR | 24.10280133 | |

| GCIR(2) | 0.83059934 | , |

| GCIR(3) | 0.83055904 | , , |

| GCIR(4) | 0.83050323 | , , , |

| GCIR(5) | 0.83049801 | , , , , |

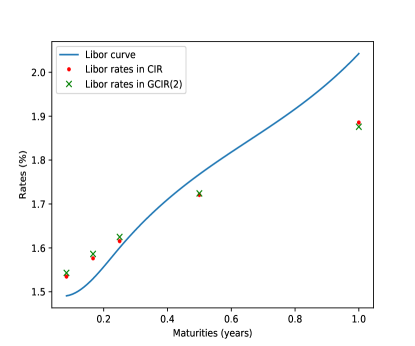

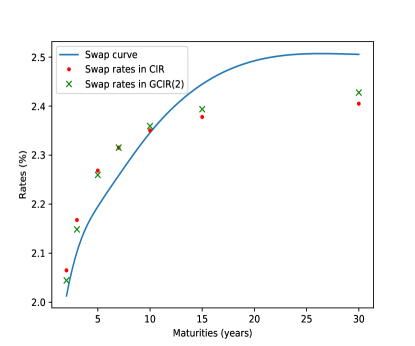

Our second calibration procedure was based on Libor and -months swap rates with maturities resp. and . The term structure of interest rates for maturities below one year are represented by Libor quotes while swap rates correspond to selected maturities from 1 year up to 30 years. A direct extention of (4.15) leads to the calibration error of the form

where Libor rates are defined like (4.14) and swap rates by

The best one dimensional model for the data from 14.12.2017 was CIR, but, again, multivariate models generated better results. The passage from to , i.e. to the -CIR model with , gave the highest error reduction, which was particularly effective for the swap rates. All of them were pushed closer the empirical swap curve. The results are presented in Fig.3 and Tab. 3.

| Model |

|

|

|

Stability indices | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| CIR | 1.42225593 | 0.84831146 | 0.57394447 | |||||||

| GCIR(2) | 1.37316050 | 1.00280671 | 0.37035379 | , | ||||||

| GCIR(3) | 1.37309034 | 1.00987818 | 0.36321216 | , , | ||||||

| GCIR(4) | 1.37308709 | 1.00989365 | 0.36319344 |

|

4.1.1 Remarks on computational methodology

Our computation were performed in the Python programming language. The calibration error was minimized with the use of the Nelder-Mead algorithm which turned out to be most effective among all available algorithms for local minimization in the Python library. The computation time of calibration which depends, of course, on the number of noise components, lied in the range 100-13.000 seconds but often did not exceed 800 seconds. This stays in a strong contrast to the CIR model for which the closed form formulas shorten the calibration to the 2 second limit. We suspect that global optimization algorithms would provide even better fit, but they were to slow for the data with more than several maturities.

5 Appendix

Proof of Proposition 2.2: It was shown in [14, Theorem 5.3] that the generator of a general positive Markovian short rate generating an affine model is of the form

| (5.1) | ||||

for , where is the linear hull of and stands for the set of twice continuously differentiable functions with compact support in . Above , and , are nonnegative Borel measures on satisfying

| (5.2) |

The generator of the short rate process given by (2.1) equals

where is a bounded, twice continuously differentiable function.

By Proposition 5.1 below, the support of the measure is contained in , thus it follows that

| (5.3) |

| (5.4) |

Comparing the left and the right sides of (5.4) we see that the left side grows no faster than a quadratic polynomial of while the right side grows faster that for some , unless the support of the measure is contained in . It follows that is concentrated on , hence follows, and

| (5.5) |

Dividing both sides of the last equality by and using the estimate

we get that that the left side of (5.5) converges to as , while the right side converges to . This yields (2.19), i.e.

| (5.6) |

Next, fixing and comparing (5) with (5.1) applied to a function from the domains of both generators and such that we get

for any such a function, which yields

| (5.7) |

This implies also

| (5.8) |

Setting in (5.7) yields

| (5.9) |

To prove (2.18), by (5.2) and (5.9), we need to show that

| (5.10) |

It is true if and for the following estimate holds

(2.20) follows from (5.7) and (5.9). To prove (2.21) we use (2.20), (2.18) and the following estimate for :

Proposition 5.1

Let be continuous. If the equation (2.1) has a non-negative strong solution for any initial condition , then

| (5.11) |

In particular, the support of the measure is contained in .

Proof: Let us assume to the contrary, that for some

Then there exists such that

Let be a Borel set separated from zero. By the continuity of we have that for some :

| (5.12) |

Let be a Lévy processes with characteristics , where and be defined by . Then are independent and is a compound Poisson process. Let us consider the following equations

For the exit time of from the set and the first jump time of we can find such that . On the set we have and therefore

In the last inequality we used (5.12). This contradicts the positivity of .

References

- [1] Alfonsi A.: Affine Diffusions and Related Processes: Simulation, Theory and Applications, (2015), Springer,

- [2] Barndorff-Nielsen O.E., Shephard N.: Modelling by Lévy processes for financial econometrics, (2001), In: Barndorff-Nielsen, O.E., et al. (eds.) Lévy Processes: Theory and Applications, 283 - 318. Birkhäuser,

- [3] Barski M., Zabczyk J.: On CIR equations with general factors, (2020), SIAM J.Financial Mathematics, 11,1,131-147,

- [4] Barski M., Zabczyk J.: Bond Markets with Lévy Factors, (2020), Cambridge University Press,

- [5] Barski M., Zabczyk J.: A note on generalized CIR equations, (2021), Communications in Information and Systems, 21, 2, 209-218,

- [6] Cheridito P., Filipović D., Kimmel R.L.: A note on the Dai - Singleton canonical representation of Affine Term Structure Models, (2010), Mathematical Finance , 20, 3, 509-519,

- [7] Cuchiero C., Filipović D., Teichmann J.: Affine models, (2010), Encyclopedia of Quantitative Finance,

- [8] Cuchiero C., Teichmann J.: Path properties and regularity of affine processes on general state spaces, (2013), Séminaire de Probabilités XLV,

- [9] Dai Q., Singleton K.: Specification Analysis of Affine Term Structure Models, (2000), The Journal of Finance, 5, 1943-1978,

- [10] Duffie D., Filipović D., Schachermayer W.: Affine processes and applications in finance, (2003), The Annals of Applied Probability, 13(3), 984-1053,

- [11] Duffie, D., Gârleanu, N.: Risk and valuation of collateralized debt obligations, (2001), Financial Analysts Journal, 57, 41-59,

- [12] Cox, I., Ingersoll, J., Ross, S.: A theory of the Term Structure of Interest Rates, (1985), Econometrica, 53, 385-408,

- [13] Feller W.: An Introduction to Probability Theory and Its Applications vol II, John Willey and Sons (1970);

- [14] Filipović, D.: A general characterization of one factor affine term structure models, (2001), Finance and Stochastics, 5, 3, 389-412,

- [15] Jiao Y., Ma C., Scotti S.: Alpha-CIR model with branching processes in sovereign interest rate modeling, (2017) Finance and Stochastics, 21, 789-813,

- [16] Kawazu K., Watanabe S.: Branching processes with immigration and related limit theorems, (1971) Theory Probab. Appl., 16, 36–54,

- [17] Rusinek, A.: Invariant measures for forward rate HJM model with Lévy noise. Preprint IMPAN 669 (2006), http://www.impan.pl/Preprints/p669.pdf

- [18] Sato, K.I.: Lévy Processes and Infinite Divisible Distributions, Cambridge University Press (1999),

- [19] Vasiček, O.: An equilibrium characterization of the term structure, (1997), Journal of Financial Economics, 5, (2), 177-188.