Mean field game of mutual holding with defaultable agents,

and systemic risk

Abstract

We introduce the possibility of default in the mean field game of mutual holding of Djete and Touzi [11]. This is modeled by introducing absorption at the origin of the equity process. We provide an explicit solution of this mean field game. Moreover, we provide a particle system approximation, and we derive an autonomous equation for the time evolution of the default probability, or equivalently the law of the hitting time of the origin by the equity process. The systemic risk is thus described by the evolution of the default probability.

Keywords. Mean field McKean-Vlasov stochastic differential equation, hitting time coupling, mean field game, default probability.

MSC2010. 60K35, 60H30, 91A13, 91A23, 91B30.

1 Introduction

This paper addresses the strategic interaction between economic agents in order to build a structural model for the equilibrium equity processes observed on financial markets, and to better understand the most important determinants of systemic risk and default contagion.

Among the huge economic literature on this problem, we refer to Allen and Gale [3], Giesecke and Weber [18], Shin [24], Eisenberg and Noe [14], and Acemoglu, Ozdaglar, and Tahbaz-Salehi [1]. We also refer to the financial regulation works on system-wide stress tests, which emerged from the last financial crisis, see Aikman, Chichkanov, Douglas, Georgiev, Howat, and King [2]. The main purpose of this paper is to provide an economic foundation for the agent based dynamics used in the simulation of the shock propagation addressed in this literature very connected with highly relevant practical regulatory decisions.

This paper builds on the mutual holding model introduced by Djete and Touzi [11] which focuses on the strategic connection between economic agents through equity cross holding, while ignoring other (important) aspects as debt interconnection, which are still left for future work. Our main task in this paper is to introduce the possibility of default, which represents a major technical difficulty left open in the first work of [11] in this direction.

We assume that default occurs at the first time that the underlying equity value hits the origin. Given the idiosyncratic risk process driven by independent Brownian motions , and defined by the drift and diffusion coefficients and , the microscopic dynamics of the equity value processes of homogeneous defaultable economic agents are defined by,

where, similar to [11], we denote , and

-

•

denotes the number of shares of agent held by agent at time , which is assumed to be a decision variable at the hand of Agent ,

-

•

the coefficients and of the idiosyncratic risk process illustrate the anonymity with the population of agents by its dependence on the the empirical measure ,

-

•

as a new feature of the present paper, is the default time of the th economic agent, which is modeled here by an absorption at the origin, meaning that no possibly recovery is considered in this model.

The natural mean field limit suggested by this microscopic model is:

| (1.1) |

where is an independent copy of , and denotes expectation operator conditional to .

Our first objective in this paper is to provide a solution of the mean field game of mutual holding as introduced in [11] with the above additional feature of defaultable agents. The coupling of the population through the hitting time of zero introduces additional technical difficulties as the equilibrium dynamics turn out to be characterized by nontrivial singularities of the coefficients (in Wasserstein space) which were not encountered in the previous non-defaultable model of [11]. Theorem 3.3 provides an explicit characterization of a mean field game equilibrium of mutual holding, thus extending the non-defaultable setting of [11].

Our second main result concerns the systemic risk of the connected agents through mutual holding at equilibrium as described by the time evolution of the default probability or, equivalently, of the law of the default time of a representative agent. In addition to the expected particle system approximation induced by the propagation of chaos results of Theorem 3.9 and Proposition 3.11, we provide in Theorem 3.5 an original expression of the equilibrium marginal law of the equity process in terms of the marginal law of the corresponding non-mean field and non-absorbed process. In particular, when the coefficients of the idiosyncratic risk are not coupled, this equation induces an autonomous equation for the default probability, which doest not require the full knowledge of the law of the equilibrium equity value. Due to the singularity of the coefficients of the equilibrium dynamics, we are unfortunately not able to exploit further this equation. However, when the drift coefficient of the idiosyncratic risk have constant sign and are free from interaction, Theorem 3.7 states that the default probability is uniquely defined by this equation, and we then deduce that our equilibrium dynamics have a unique strong solution. We obtain this result as a consequence of the uniqueness of a solution to our autonomous equation for the evolution of the default probability, which is proved by some delicate estimates on diffusions densities by the so-called Parametrix method.

We notice that similar McKean-Vlasov stochastic differential equations (SDE) coupled through hitting time of the origin was considered in recent models by Hambly and Søjmark [19], Nadtochiy and Shkolnikov, [22], [23], Delarue, Nadtochiy, and Shkolnikov [10], Cuchiero, Rigger, and Svaluto-Ferro [9], Bayraktar, Guo, Tang, and Zhang [5], [6]. We also refer to the related literature modeling interacting economic agents by McKean-Vlasov SDEs, see e.g. Garnier, Papanicolaou, and Yang [16] Carmona, Fouque, and Sun [8], Sun [25].

The paper is organized as follows. The rigorous formulation of the mean field game of mutual holding with defaultable agents is reported in Section 2. Our main results are collected in Section 3. The existence result of our equilibrium McKean-Vlasov SDE is proved in Section 4 by means of appropriate approximation arguments. In particular, Subsection 4.2 contains the proof of our autonomous equation for the default probability. Finally, Section 5 specializes to the special case of constant sign non-interacting coefficients of the idiosyncratic risk, and prove that the equilibrium McKean-Vlasov SDE has a unique strong solution in this case.

Notations For a generic Polish space , we denote the collection of all Borel subsets of , and by the collection of all probability measures . We denote similarly , integrable function .

For , the subset consists of all measures with finite -th moment , and we denote by the corresponding Wasserstein distance.

Finally, is the space of continuous real-valued functions on , and denotes the corresponding subset of bounded functions.

2 Problem formulation

Let be endowed with the compact convergence topology. Denote by its coordinate process and by its natural filtration, i.e. for and . Define further to be the filtration given by with , where denotes the completion of by .

2.1 Equilibrium dynamics

Throughout this paper, we fixed a probability distribution such that , for some , and we denote by the subset of probability measures under which is an Itô process, absorbed at zero, and satisfying the dynamics

| and |

for some scalar Brownian motion , and progressively maps satisfying

Introducing its first hitting time at the origin , we may rewrite the last stochastic differential equation (SDE) as

In order to introduce our mutual holding problem, we introduce the set of holding strategies consisting of all measurable functions . Here, represents the proportion of Agent ’s equity held by Agent at time .

For , and , the mutual holding problem discussed in the introduction leads to the mean field SDE driven by Brownian motion on some filtered complete probability space :

where and we use the notation

for all measurable functions with appropriate integrability. Rewriting the last SDE in differential form and collecting the terms in “”, we obtain for all

| (2.1) |

Define to be the subset of such that (2.1) has a weak solution with . Hence, by identification, and must hold with

2.2 Mean field game formulation

Next, we introduce a mean field game (MFG) formulation to determine the mutual holding strategy. For and , we introduce the deviation of the representative agent from to an alternative strategy by means of an equivalent probability measure defined via

| (2.2) |

where and the stochastic process is given as

| (2.3) |

To ensure the wellposedness of and , we assume that the diffusion coefficient is bounded away from zero. It follows from Girsanov’s theorem that is a Brownian motion under , so that the dynamics of the process are rewritten as

thus mimicking the controlled dynamics in (1.1). Therefore, the representative agent seeks for the optimal mutual holding strategy by maximizing the criterion over , where is an arbitrary time horizon and denotes a non-decreasing utility function.

Definition 2.1.

A pair is called an MFG equilibrium of the mutual holding problem if and .

3 Main results

The paper is concerned with the existence of an MFG equilibrium for the mutual holding problem where, in contrast with the previous work [11], we introduce here the default risk upon hitting the zero equity value. Our main results show that the dynamics of the equilibrium equity process is defined by the following mean field SDE

| (3.1) |

where are defined by

| and | (3.2) |

and is, in view of Lemma A.1, the unique solution of the equation

| (3.3) |

The measurable functions stand for the drift and volatility of the idiosyncratic equity process. Notice that both coefficients and exhibit singularities in the variables and , so that the wellposedness of the last mean field SDE will be the first issue to be clarified.

Notice that the expressions (3.2) and (3.3) are closely related to the corresponding expressions in [11] where the equity process was not absorbed at zero, i.e. no default, so that is replaced in the above expression by in their context, and our in (3.3) coincides with their map .

We also observe that the coefficients of the last mean field SDE exhibit a dependence on , where is the cdf of the hitting time of the origin . This is a similar feature to the models studied by Hambly and Søjmark [19], Nadtochiy and Shkolnikov [22], [23], Nadtochiy and Shkolnikov [10], Cuchiero, Rigger, and Svaluto-Ferro [9], Bayraktar, Guo, Tang, and Zhang [5], [6].

Remark 3.1.

By a straightforward computation, we see that the expressions of the equilibrium coefficients take the following simple form when the idiosyncratic drift coefficient has a constant sign:

-

•

If , then and ;

-

•

If , then and ;

-

•

If with constant sign, then and .

3.1 Existence of an MFG equilibrium

We start by stating the conditions on the maps and .

Assumption 3.2.

For every , are Lipschitz in , uniformly in , and is bounded from below away from zero, uniformly in . In addition,

-

(i)

either for each , for a.e. ,

-

(ii)

or for all , and for a.e. the Borel set

has full Lebesgue measure in , i.e. its complement is Lebesgue–negligible.

Our first result ensures the existence of solutions to (3.1), and states the existence of an MFG equilibrium with a complete characterization of the corresponding equilibrium mutual holding strategy.

Theorem 3.3.

Let Assumption 3.2 hold. Then for every , and all initial law :

(i) the mean field SDE (3.1) has a weak solution on , with ;

(ii) in addition, if is nondecreasing and Lipschitz, any weak solution of (3.1) induces an MFG equilibrium of the mutual holding problem where .

The proof of Theorem 3.3 (i) is based on an approximation argument reported in Section 4, and differs from that in [11] by the additional difficulty induced by the lack of regularity (in Wasserstein distance) of and in and the possible degeneracy of the SDE (3.1). As for (ii), we follow the same argument as in [11], which we now report for completeness.

Proof of Theorem 3.3 (ii).

Fix an arbitrary (weak) solution to (3.1) and define the pair , where , and . Consider the optimization problem , where we recall that and the dynamics of in terms of the –Brownian motion are given by

The Hamiltonian corresponding to this control problem is:

with maximizer . The value function can be characterized by means of the following backward SDE, which is the non-Markovian substitute of the HJB equation:

This backward SDE has a unique solution satisfying . Moreover, arguing as in [11], we see that the nondecrease of the function implies that . Then , and we obtain In order to complete the proof, we now show that , for all . Indeed, using the representation of in terms of :

Substituting the dynamics of , it follows from appropriate localization that

where the last inequality follows from the definition of . By the same argument, we see that the control process allows to reach the last upper bound .

Remark 3.4.

Similar to [11], we may use the equilibrium mutual holding strategy of Theorem 3.3 in order to build an approximate Nash equilibrium for the finite population mutual holding game. Due to the coupling by the hitting time of the origin, this would require nontrivial technical developments. We refrain from exploring this question in the present paper, and we leave it for future work. Instead, our focus in the next subsections is mainly on the evolution of the default probability which describes the systemic risk induced by the equilibrium connection between the agents.

3.2 Autonomous characterization of the default probability

In general, the uniqueness of the solution to (3.1) may not hold. Nevertheless, we may always select a solution that admits an autonomous characterization of its default probability. Given a solution of (3.1), we define and we consider the map , defined by:

| (3.4) |

where is defined in (3.3) and is the probability that the representative agent defaults prior to time . Alternatively, is the cumulative distribution function (cdf) of the default time defined as the equity process hitting time of the origin.

Introduce further the coefficients with frozen distribution dependence by

| and |

Notice that the above functions are all related to the given solution through its marginal laws ; this dependence is omitted for notation simplicity.

Theorem 3.5.

Remark 3.6.

(i) The proof of the last result actually provides an expression of the marginal distributions of the process in terms of those of the process , see (4.12). However as the coefficients of the SDE defining the process depend on , this representation is not explicit.

(ii) In the situation where the coefficients of the idiosyncratic risk process are independent of the distribution variable, i.e. and , the characterization of Theorem 3.5 is particularly useful. In this case, the coefficients and depend on only through , and we denote in this case . Theorem 3.5 provides here an autonomous equation for the function . In particular, the probability of default does not require the full knowledge of . See Subsection 3.4 for a numerical illustration. Moreover, once is determined, the equilibrium dynamics (3.1) would reduce to a standard SDE without mean field interaction in the case where (3.1) admits a unique solution.

When the drift has constant sign, recall from Remark 3.1 that the coefficients and contain no singularity in , and the solution of (3.5) is unique. Together with the last characterization result, this observation allows to establish the uniqueness of the solution to (3.1) under additional conditions.

Theorem 3.7.

Let the conditions of Theorem 3.5 hold, and assume further that

-

(i)

has constant sign, is differentiable in with bounded derivative, and Hölder-continuous in ;

-

(ii)

is twice differentiable in with bounded , and Hölder-continuous in ;

-

(iii)

, with continuous density satisfying .

Then the mean field SDE (3.1) has a unique strong solution with corresponding maps uniquely defined by (3.6), and continuous and strictly decreasing.

Remark 3.8.

A sufficient condition for is that , and . for some . To see this, observe that

-

•

,

-

•

Moreover, , by direct integration by parts, so that our first condition implies that , and therefore by our second condition.

3.3 Propagation of chaos

As mentioned earlier, our strategy to prove Theorems 3.3 and 3.5 is to use an approximation argument. This section provides the concrete approximation which yields in particular a particle system approximation satisfying a result of propagation of chaos. Denoting by the Heaviside function, we introduce the following sequences:

-

•

with for all , and

for instance, we may take ;

-

•

with , , and converging to under , one may consider for instance , where is a standard Gaussian random variable independent of ;

-

•

with in , Lipschitz in , and converging to , uniformly in and a.e. in .

For all we may define by Lemma A.1, the map as the solution of

and we introduce the functions by

| (3.7) |

Theorem 3.9.

Let Assumption 3.2 hold.

(i) For every , there exists a unique strong solution satisfying and

(ii) We have in , for all ;

(iii) Denoting and , the sequence is relatively compact in . Furthermore, the limit of any convergent subsequence is a weak solution of (3.1), and satisfies:

| and |

Remark 3.10.

(i) As previously mentioned, we do not have a uniqueness result for the SDE (3.1), and choosing different approximating coefficients may lead to different limits.

(ii) The convergence result of Theorem 3.9 (ii) implies that for all

We next introduce a particle system approximation which induces in particular an approximation method for the survival probability . For all , let be the process defined by the SDE

and started from any initial data satisfying , as , in . The following propagation of chaos result is a direct consequence of [12, Proposition 4.15].

Proposition 3.11.

Let . Then, under Assumption 3.2, we have , as , in , for all .

3.4 A numerical example

In order to illustrate the effect of mutual holding, we end Section 3 by the following example where the Ornstein–Uhlenbeck SDE is used to model the idiosyncratic risk process. Namely, for

where and stand for the dynamics of a representative agent without and with the mutual holding. In particular, the new drift and volatility functions are defined by

| and |

where, in view of (4.7), is a fixed point of the map defined by

and is defined by the stochastic differential equation

We examine the evolution of the default probabilities and . Clearly,

By using similar arguments as in Lemma A.2 (ii), we may also prove that . We fix a time horizon and adopt the iteration for all with some initial guess . To do so, we approximate by time discretization and Monte Carlo simulation, i.e. taking , , and independent random variables distributed according to some , one has

where and for , and are independent standard Gaussian random variables. Notice that we are ignoring here the major difficulty related to the discontinuity of , as this is not the main concern of the present paper.

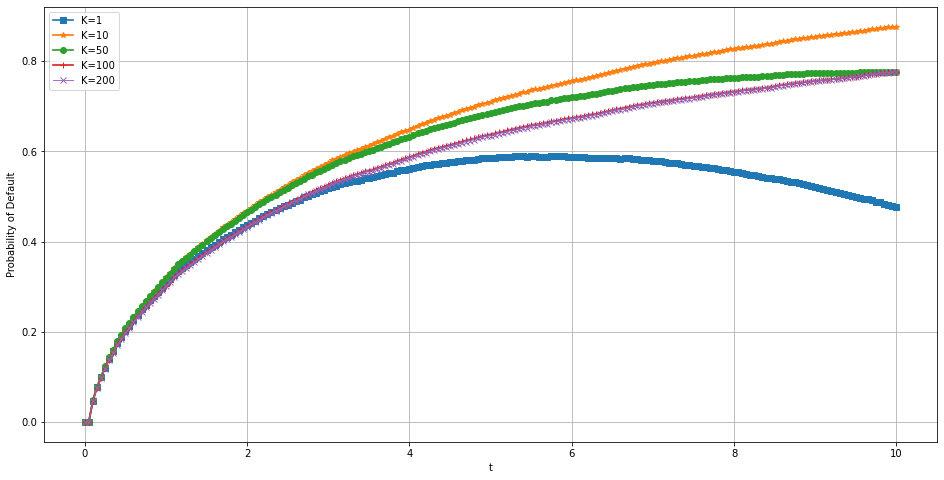

With and , we illustrate in Figure 1 the convergence of our iteration.

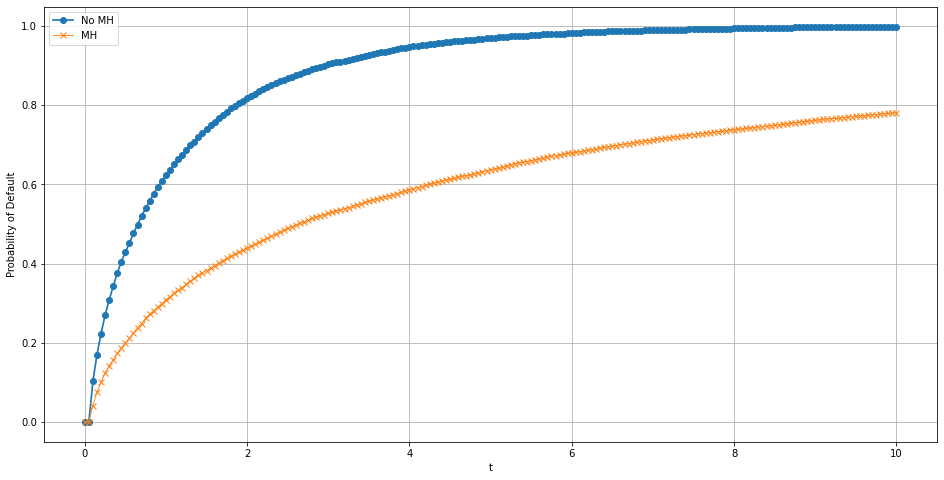

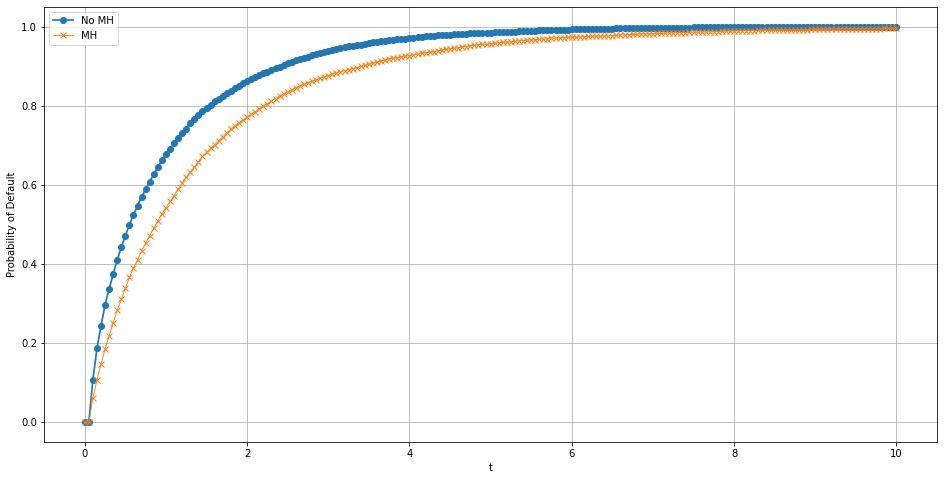

Next, with different parameters , we see in Figures 2 and 3 that the mutual holding significantly decreases the propagation of defaults, and that a larger mean reversion level induces a more significant effect of mutual holding on the default probability. In other words a larger mean reversion level leads to an equilibrium equity process with lower systemic risk.

4 Particle system approximation

This section is devoted to the proof of Theorems 3.3 and 3.9. Note that Theorem 3.3 (i) is an immediate consequence of Theorem 3.9 (iii).

4.1 Proof of Theorem 3.9

(i) Let us introduce the map defined by

Using , we can rewrite the dynamics of as

As the map is Lipschitz, it follows that is Lipschitz. Moreover, by Lemma A.1, the coefficients are Lipschitz in uniformly in . Then, the existence and uniqueness of follow from the path dependent extension of standard results, see e.g. [13, Theorem A.3]

(ii) Denote . After possibly passing to a subsequence, we may assume without loss of generality that the bounded sequence has a limit. In order to prove the required result, we now show that this limit is zero. Let be such that

and observe that for all we have

| (4.1) |

Since converges under with , the sequence is relatively compact in . Then, after possibly passing to a subsequence in . Using [11, Proposition 9.1], we see that is the distribution of that solves an SDE of non–degenerate diffusion coefficient. Up to a subsequence again, we can assume that for some . Then, for any where . By the Portmanteau Theorem and the Lebesgue dominated convergence Theorem, we have

| and |

Then, for any limit of the convergent (sub–)sequence , it follows from (4.1), together with the convergence of , that .

(iii) We recall that , so that , where . Using this SDE representation of , we deduce that is relatively compact in . Since , we deduce that

Then, after possibly passing to a subsequence, we may assume that in . Denote with and . For all Lipschitz function ,

Therefore,

In particular, in as .

(iv) We next prove the convergence of . For , one has

where the last convergence follows from the Portmanteau Theorem and . Applying the dominated convergence theorem, one has . Using again the Portmanteau Theorem and , it follows that

Finally, combining the obtained convergence results, we find

(v) To prove the convergence of , we compute

where

By convergence assumption of , holds. Moreover by the previous step. Using similar arguments as those developed for the convergence , we obtain

Hence, .

(vi) We now have all the ingredients for the convergence of . Passing to the limit in the equation satisfied by , it follows from the convergence of , and that for all . Let be Lipschitz. Notice that

As is the distribution of that solves an SDE of non–degenerate diffusion coefficient, it follows that admits a density w.r.t. the Lebesgue measure over . Therefore, thanks to the assumptions satisfied by in 3.2, we can check that . Since for all , we can deduce by the Portemanteau theorem that

With similar techniques to those used previously, we get by taking and , for a.e. ,

where the last equality is ensured by Assumption 3.2 (ii). Again by the Portemanteau theorem, one has for a.e. ,

which implies that for a.e.

As and , using the previous result, we may deduce that

On the other hand, since has a density with respect to the Lebesgue measure on , then it must hold that a.e. .

(vii) Given the dynamics of in the statement of Theorem 3.9, it follows from the convergence results established in the previous steps that

Therefore, by noticing and , where , we have showed that . It is straightforward that satisfies (3.1). It remains to prove that

To see this, let and , and observe that by Portemanteau Theorem, since . As converges (along the subsequence), this allows to identify its limit to .

4.2 Derivation of the autonomous characterization of the default probability

This section is devoted to the proof of Theorem 3.5. Unless otherwise specified, we use throughout the approximation arising in Theorem 3.9, see also Remark 3.10 (ii). Notice that, the process , with the running minimum of the process satisfies

and recall the notations and .

Lemma 4.1.

Let the conditions of Theorem 3.5 hold.

(i) The map is Hölder continuous in and Lipschitz in .

(ii) For each , there exists a sub–probability density supported on such that

| and |

Proof.

(i) By assumption, and have linear growth in . Therefore, there exists such that

It is clear that and inherit the Lipschitz property of , and in . Moreover, it follows from Lemma A.1 that there exist and , such that

As , for some constant , this provides the required result.

(ii) Define and notice that on the event , where

By Kusuoka [21], the distribution of is absolutely continuous with respect to the Lebesgue measure for all . As for all Borel subset , we deduce that inherits the absolute continuity of with respect to the Lebesgue measure. ∎

4.2.1 The case of smooth coefficients

We first establish the desired equality (3.6) for the approximating process . Notice that is fixed and we write in Section 4.2.1 and for the sake of simplicity. By construction, there exist and such that

Notice that with a smooth density . By Garroni and Menaldi [17, Chapter VI, Lemma 1.10 & Theorem 2.2] and [17, Theorem 2.2.], the Fokker–Planck equation on the half space

| (4.2) |

has an unique classical solution satisfying

| (4.3) |

Further, it follows from Figalli [15, Lemma 2.3] that the marginal distribution has the following decomposition

| and | (4.4) |

Similarly, the corresponding non–absorbed SDE

| (4.5) |

has a unique solution with marginal distributions absolutely continuous with respect to the Lebesgue measure, i.e. , where the density function is the unique solution of the backward Kolmogorov equation parameterized by :

| (4.6) |

Proposition 4.2.

The density function introduced in (4.4) satisfies

| (4.7) |

Moreover, denoting and , we have

| (4.8) |

where is the left-continuous inverse of the non-increasing function .

Proof.

Denote . Integrating the Fokker–Planck equation on , it follows from the estimate (4.3) that

Using again (4.3), we have for all that . As , we see by Fubini’s theorem that

| (4.9) |

Observe next that Integrating both sides over , we obtain by appropriately changing the order of integration thanks to Fubini’s theorem, and by using the initial and boundary conditions together with (4.9)

which is exactly (4.7). Integrating over , one obtains

where the last equality follows from the change of variable . ∎

4.2.2 The general case

Our next objective is to send in the expression (4.7) of . Recall that the sequence , with and marginals , satisfies the SDE

As we showed in the proof of Theorem 3.9, after possibly passing to asubsequence, we may assume that in , where the limit satisfies the SDE

In particular, one has for a.e. that

| (4.10) |

Proof of Theorem 3.5.

By Proposition 4.2, we have for arbitrary that

| (4.11) | |||||

where is the generalized inverse of the map . Notice first that , by the weak convergence of . As a.e. we may pass to the limit in (4.11) by using (4.10), and obtain:

| (4.12) |

By the arbitrariness of , this proves the existence of a Borel measurable map satisfying , for all , where

| (4.13) |

with a version of the density of the process defined by the limiting SDE (3.5). Finally the required statement of Proposition 4.2 follows by direct integration of the function . ∎

5 Uniqueness in the case of constant sign drift coefficient

This section is devoted to the proof of Theorem 3.7. We specialize the discussion to the case where the coefficients are independent of the distribution variable and has constant sign. We aim at justifying the uniqueness of the solution to (3.1).

First, if , then , and the solution to the absorbed SDE

is the stopped process , where is the unique solution to the SDE Consequently the uniqueness of is inherited from that of .

In the rest of this section, we focus on the non-trivial case on , and recall that the MFG equilibrium SDE in this case is

where the coefficients are defined by

| and |

for an arbitrary solution to (3.1) with . Throughout this section, we use to denote generic constants that may vary from line to line during the proof. For a measurable map , set with . By a straightforward computation, there exist such that for all maps

| (5.1) | |||

| (5.2) |

Lemma 5.1.

Let the conditions of Theorem 3.7 hold.

(i) The function is Hölder continuous. In particular, are Hölder continuous in and Lipschitz in .

(ii) For each , there exists a sub–probability density supported on such that

| and |

Proof.

The proof of (ii) is as same as that for Lemma 4.1 and we thus omit it. We start proving (i) for . Let be the unique solution to the SDE

such that . Then it follows that with . Hence, is Höder continuous by Lemma A.2 (i). The Hölder continuity of follows from the probabilistic representation

The required Hölder continuity now follows by standard estimates. Finally the Hölder continuity of and in follows by immediate composition, while the Lipschitz continuity in is directly inherited from that of and . ∎

Thanks to the Hölder continuity of the coefficients in , the autonomous characterization (3.6) of in Proposition 4.2 also holds. Hence, we see that the uniqueness of can be derived by showing the uniqueness of such . We first rewrite the representation (3.6) by using the notation , and after an integration by parts:

where we recall that denotes the density function of .

Let be the subset of non-negative Hölder continuous functions. Define the operator , defined for all and by

with obvious definition of and . Define further by

Therefore, any corresponding to a solution of (3.1) must be a fixed point of , i.e. , and the following uniqueness result of implies the required uniqueness result of Theorem 3.7.

Proposition 5.2.

has at most one fixed point on and thus the solution to (3.1) is unique.

To prove Proposition 5.2, we need some stability estimates for the map , which are summarized in Proposition 5.3. Recall the Parametrix expressions of the density for , see e.g. Aronson [4] and Konakov, Kozhina & Menozzi [20]:

where we used the space-time convolution notation

for all scalar functions defined on the appropriate spaces, and

Proof of Proposition 5.2.

We argue by contradiction. Let be two different fixed points of and suppose to the contrary that . We claim that

| (5.3) |

for some . Before proving this, let us show that it induces the required contradiction. For

as and have the same first component . Then, it follows from (5.3) that

which yields a contradiction as is sufficiently close to .

It remains to prove (5.3). Without loss of generality, we may reduce to the case . Recall that

for , which yields

| (5.4) | |||||

| with | |||||

| and |

Applying (componentwise) the estimates (5.5) and (5.6) of Proposition 5.3 below, one has for :

as by Condition (iii) of Theorem 3.7, and

Applying (again componentwise) the estimates (5.9) and (5.10) of Proposition 5.3 below, it follows that

Finally, by (5.7) and (5.8) of Proposition 5.3 below, we get:

Plugging the last estimates in (5.4) yields (5.3) for , and thus completing the proof. ∎

The last proof refers to the following statement which uses the Gamma function .

Proposition 5.3.

Let , and be with bounded derivative. Then, under the conditions of Theorem 3.7, there exist s.t. the following inequalities hold for all , , and :

| (5.5) | |||||

| (5.6) | |||||

| (5.7) | |||||

| (5.8) | |||||

| (5.9) | |||||

| (5.10) |

Proof.

Denote and . Throughout this proof, are constants which may change from line to line.

(i) We first prove estimates (5.5), (5.7), and (5.9) corresponding to . We start by writing that

| (5.11) |

Dropping the arguments and which play no role here, we compute that

Then, it follows from direct integration by parts that

Note that, under our conditions, , , , and hold for some . Plugging these estimates in the last expression, and substituting in (5.11), directly yields (5.5). For later use, notice that the same argument also provides

| (5.13) |

Fix . Differentiating both sides of (5) with respect to and integrating wrt to , we obtain

Using the facts and , we obtain the estimate (5.7) by the same reasoning of (i). For later use, notice that the same argument also provides

| (5.14) |

By following similar arguments as above, we also obtain the estimate (5.9), together with the following estimate which wil be needed later:

| (5.15) |

(ii) We next focus on (5.6). By direct adaptation from Konakov, Kozhina & Menozzi [20], there exist constants such that, for , and ,

| (5.16) | |||||

| (5.17) |

Combining with (5.13), we deduce that for all :

| (5.18) |

which yields (5.6) by direct integration with respect to over , after multiplying by .

(iii) The rest of this proof justifies (5.8); the remaining estimate (5.10) is also proved by similar arguments that we do not report here for brevity. By definition, we have , where

Then,

| (5.19) |

by (5.17) together with the fact that as has affine growth. We next decompose

where

- •

- •

-

•

and , and is now the only remaining term to complete the proof of the required estimate (5.8). To do so, we need the following estimation and we start with . As , we have

Hence,

Fix any , e.g. . We distinguish two cases. If , then

If , then

and thus

We compute for all

Finally, one obtains

(5.22) The required estimate (5.8) now follows by plugging (5.20), (5.21), (5.22) into (5.19).

∎

Appendix A Technical results

A.1 Definition and first properties of

Lemma A.1.

Proof.

Consider the function , By a straightforward verification, one finds , , is strictly increasing and continuous on by the dominated convergence theorem. Therefore, there exists a unique root, denoted by , i.e. . In view of the inequality

the bound for follows. The same argument applies for .

(i) For any and , one has

which yields the required inequality. The reasoning for is the same.

(ii) Similar to (i), we compute the difference and obtain the desired inequality using the definitions of and .

(iii) Again, we compute the difference and obtain

We may conclude by the dominated convergence theorem by using the fact that converges uniformly to and is of linear growth on . ∎

A.2 On hitting times of Itô processes

Lemma A.2.

Let be an Itô-process given by

where , is bounded and takes values in some interval . Define its first hitting time at zero and running minimum . Then,

-

(i)

for all ;

-

(ii)

The map is strictly decreasing and takes values in ;

-

(iii)

If in addition the maps and are Lipschitz in , uniformly in , then

Proof.

By introducing the equivalent probability measure defined via

the dynamics can be rewritten as in view of Girsanov’s theorem, where is a Brownian motion under .

To prove (iii), we compute for that

where the second last inequality follows from Doob’s inequality. By [21, Theorem 2.5], has a density denoted by satisfying for all , where are constants depending only on . Hence,

On the other hand, we note that by Doob’s inequality. Therefore,

where the existence of follows from a straightforward computation by distinguishing the three cases , and . Finally, one has

where the second inequality follows from the Hölder inequality together with the boundedness of .

By the equivalence between and , we now prove (i) by showing that , where . Notice that

where the second equality holds as by (i). Conditioning on , is a time-changed Brownian motion, i.e. , and we deduce from the fact that is bounded from below away from zero by some constant that

Then, it follows from the trajectorial properties of the Brownian motion that

It remains to prove (ii). Suppose to the contrary that the map is flat on some open interval , then In particular, one has . Using the above time-change argument, one has

contradiction ! To show it suffices to show and we use the same time-change argument. Namely, . ∎

A.3 Convergence of sequence of SDEs starting at different initial times

This section justifies the convergence of a sequence of processes starting at different times. For simplicity, we restrict to driftless SDEs with scalar continuous paths in :

| and |

where, for all , and , for some , are Borel bounded maps, Lipschitz in uniformly in , and , for some .

Proposition A.3.

Assume and a.e. and let . Then,

(i) the sequence of measures is relatively compact in ;

(ii) The limit of any convergent subsequence satisfies where the process satisfies, for a.e. ,

| and |

Proof.

We proceed in 3 steps.

Step 1: Relative compactness. Notice that and

Then, is relatively compact in , and converges to some limit , after possibly passing to a subsequence.

Step 2 We next prove the following technical result which will be used in the next step to identify the nature of this limit . Let be a sequence of bounded Borel maps continuous in the third variable s.t. , a.e. Then, we claim that

To see this, notice first that, by the a.e. convergence of to together with the continuity of in the third variable, it follows from the weak convergence of that for all :

Then, in order to prove the required result, we now show that

| where | (A.1) |

For an arbitrary , we first estimate by the Chebychev inequality that

Since is uniformly bounded from below above zero, it follows from [7, Theorem 6.3.1–(i)] that we may find a constant , independent of , such that

The required result (A.1) follows by taking the limits , then , and finally .

Step 3: Identification of the limit. It is obvious that for all . Then, we can write where the map is Borel measurable. For any bounded map and twice differentiable map , it follows from Itô’s formula that

for all and . Notice that for a.e. . We may then take the limit in the last equality by using the technical result of Step 2, and obtain:

By the arbitrariness of , this implies that

completing the proof by equivalence between the Fokker–Planck equation and the corresponding SDE. ∎

References

- Acemoglu et al. [2015] D. Acemoglu, A. Ozdaglar, and A. Tahbaz-Salehi. Systemic risk and stability in financial networks. American Economic Review, 105(2):564–608, 2015.

- Aikman et al. [2019] D. Aikman, P. Chichkanov, G. Douglas, Y. Georgiev, J. Howat, and B. King. System-wide stress simulation. 2019.

- Allen and Gale [2000] F. Allen and D. Gale. Financial contagion. Journal of political economy, 108(1):1–33, 2000.

- Aronson [1967] D. G. Aronson. Bounds for the fundamental solution of a parabolic equation. Bull. Amer. Math. Soc, 73:890–896, 1967.

- Bayraktar et al. [2020] E. Bayraktar, G. Guo, W. Tang, and Y. Zhang. Mckean-vlasov equations involving hitting times: blow-ups and global solvability. arXiv preprint arXiv:2010.14646, 2020.

- Bayraktar et al. [2022] E. Bayraktar, G. Guo, W. Tang, and Y. Zhang. Systemic robustness: a mean-field particle system approach. arXiv preprint arXiv:2212.08518, 2022.

- Bogachev et al. [2015] V. I. Bogachev, N. V. Krylov, M. Röckner, and S. V. Shaposhnikov. Fokker–Planck–Kolmogorov Equations. Mathematical Surveys and Monographs. American Mathematical Society, 2015.

- Carmona et al. [2013] R. Carmona, J.-P. Fouque, and L.-H. Sun. Mean field games and systemic risk. Available at SSRN 2307814, 2013.

- [9] C. Cuchiero, S. Rigger, and S. Svaluto-Ferro. Propagation of minimality in the supercooled stefan problem. arXiv preprint arXiv:2010.03580, year=2020.

- Delarue et al. [2019] F. Delarue, S. Nadtochiy, and M. Shkolnikov. Global solution to super-cooled stefan problem with blow-ups: regularity and uniqueness. arXiv preprint arXiv:1902.05174, 2019.

- Djete and Touzi [2022] M. F. Djete and N. Touzi. Mean field game of mutual holding. arXiv preprint arXiv:2104.03884, 2022.

- Djete et al. [0] M. F. Djete, D. Possamaï, and X. Tan. Mckean–vlasov optimal control: Limit theory and equivalence between different formulations. Mathematics of Operations Research, 0(0):null, 0. doi: 10.1287/moor.2021.1232. URL https://doi.org/10.1287/moor.2021.1232.

- Djete et al. [2022] M. F. Djete, D. Possamaï, and X. Tan. McKean–Vlasov optimal control: The dynamic programming principle. The Annals of Probability, 50(2):791 – 833, 2022. doi: 10.1214/21-AOP1548. URL https://doi.org/10.1214/21-AOP1548.

- Eisenberg and Noe [2001] L. Eisenberg and T. H. Noe. Systemic risk in financial systems. Management Science, 47(2):236–249, 2001.

- Figalli [2008] A. Figalli. Existence and uniqueness of martingale solutions for sdes with rough or degenerate coefficients. Journal of Functional Analysis, 254(1):109–153, 2008. ISSN 0022-1236. doi: https://doi.org/10.1016/j.jfa.2007.09.020. URL https://www.sciencedirect.com/science/article/pii/S0022123607003709.

- Garnier et al. [2013] J. Garnier, G. Papanicolaou, and T.-W. Yang. Large deviations for a mean field model of systemic risk. SIAM Journal on Financial Mathematics, 4(1):151–184, 2013.

- Garroni and Menaldi [1992] M. Garroni and J. Menaldi. Green Functions for Second Order Parabolic Integro-Differential Problems. Chapman & Hall/CRC Research Notes in Mathematics Series. Taylor & Francis, 1992. ISBN 9780582021563. URL https://books.google.fr/books?id=_TfvAAAAMAAJ.

- Giesecke and Weber [2004] K. Giesecke and S. Weber. Cyclical correlations, credit contagion, and portfolio losses. Journal of Banking & Finance, 28(12):3009–3036, 2004.

- Hambly and Søjmark [2019] B. Hambly and A. Søjmark. An spde model for systemic risk with endogenous contagion. Finance and Stochastics, 23(3):535–594, 2019.

- Konakov et al. [2015] V. D. Konakov, A. Kozhina, and S. Menozzi. Stability of densities for perturbed diffusions and markov chains. arXiv: Probability, 2015.

- Kusuoka [2017] S. Kusuoka. Continuity and gaussian two-sided bounds of the density functions of the solutions to path-dependent stochastic differential equations via perturbation. Stochastic Processes and their Applications, 127(2):359–384, 2017. ISSN 0304-4149. doi: https://doi.org/10.1016/j.spa.2016.06.011. URL https://www.sciencedirect.com/science/article/pii/S0304414916300850.

- Nadtochiy and Shkolnikov [2019] S. Nadtochiy and M. Shkolnikov. Particle systems with singular interaction through hitting times: application in systemic risk modeling. Ann. Appl. Probab., 29(1):89–129, 2019.

- Nadtochiy and Shkolnikov [2020] S. Nadtochiy and M. Shkolnikov. Mean field systems on networks, with singular interaction through hitting times. Ann. Probab., 48(3):1520–1556, 2020.

- Shin [2009] H. S. Shin. Securitisation and financial stability. The Economic Journal, 119(536):309–332, 2009.

- Sun [2022] L.-H. Sun. Mean field games with heterogenous groups: Application to banking systems. Journal of Optimization Theory and Applications, 192(1):130–167, 2022.