Deep incremental learning for financial temporal tabular datasets with distribution shifts

Abstract

We present a robust deep incremental learning framework for regression-based ranking tasks on financial temporal tabular datasets which is built upon the incremental use of commonly available tabular and time series prediction models to adapt to distributional shifts typical of financial datasets. The framework uses a simple basic building block (decision trees) to build hierarchical models of any required complexity to deliver robust performance under adverse situations such as regime changes, fat-tailed distributions, and low signal-to-noise ratios. As a detailed study, we demonstrate our scheme using XGBoost models trained on the Numerai dataset and show that a two layer deep ensemble of XGBoost models over different model snapshots delivers high quality predictions under different market regimes. We also show that the performance of XGBoost models with different number of boosting rounds in three scenarios (small, standard and large) is monotonically increasing with respect to model size and converges towards the generalisation upper bound. We also evaluate the robustness of the model under variability of different hyperparameters, such as model complexity and data sampling settings. Our model has low hardware requirements as no specialised neural architectures are used and each base model can be independently trained in parallel.

Keywords Machine Learning, Time Series Prediction, Deep Learning,

1 Introduction

Many important applications of machine learning (ML), such as the Internet of Things (IoT) [1] and cyber-security [2], involve data streams, where data is regularly updated and predictions are made point-in-time. Such applications pose challenges to standard ML approaches, specifically with regard to the balance between model learning and their update in response to new data arrivals [3].

Incremental learning (IL) techniques [4, 5, 6] are used to adapt deployed machine learning systems to changes in data streams. For example, in image classification systems, class incremental learning [7, 8, 9] is used where the categories of images cannot be known in advance. A key challenge in IL is the presence of distributional shifts in data (or concept drifts) [10] which results in model degradation [11] during inference, i.e., deterioration of out-of-sample performance when the model learns relationships from the training set that significantly differ from those in the test set.

Reinforcement Learning (RL) [12, 13, 14] provides an alternative approach to prediction tasks in systems under data innovation. In RL, a model (agent) learns a policy to optimise its reward by interacting and eliciting a response from the environment. RL is therefore useful when the actions of the model influence the environment, and when multiple agents interact with each other [15]. However, if the actions of models have no influence on the data stream, (i.e., there is no feedback between agent and environment), then RL reduces to incremental learning. Furthermore, applying trained RL agents to unknown situations (e.g., trading [16], self-driving cars [17], or robotics [18]) remains a challenge, and complex algorithms have been introduced to bridge the gap between controlled environments and real-life situations [19, 20]. Hence the applicability of RL models can suffer from lack of robustness[21] and interpretability [22] of agent behaviour, and from the large amount of computational resources required.

The deep incremental learning (DIL) framework introduced here is a hybrid approach which allows predictions from base learner models to be reused in future predictions for tasks on data streams. Unlike RL, deep incremental learning only allows a single direction of information flow, from one layer to the next. Importantly, the point-in-time nature of predictions is preserved so that no look-ahead bias is introduced. DIL can be thought of as an extension of model stacking [23] but taking into account the stream nature of the data. Here, we consider an incremental problem in finance, which consists of ranking stocks for neutral portfolio optimisation applied to obfuscated data streams of tabular features and targets, corresponding to stocks and computed features. Such data sets are affected by strong non-stationarity and distribution shifts caused by regime changes in the market. Here, we expand on our previous work [24] and develop an IL framework that uses different data and feature sampling schemes and deep incremental model ensemble techniques appropriate for data streams with a high level of concept drift and non-stationarity.

Adopting an IL approach is crucial for data streams, as traditional assumptions of machine learning algorithms are not applicable. For instance, single-pass cross-validation that splits the data into fixed training, validation and test periods is not suitable. Under an IL framework, a model is represented by a continuous stream of parameters. Further, the procedure adds new hyperparameters to the model, such as training size and retrain period, which have a non-negligible impact on prediction performances for non-stationary datasets [25]. The distinction between features, targets and predictions is also blurred in the IL setting, as predictions from models learnt from different spans of data can be used as additional features when building other models, and targets can be created by subtracting against the predictions made. Therefore, model training is a multi-step problem, rather than a single-step problem. For an illustration of these issues, see Fig. 1.

Reusing model predictions within an IL framework provides a natural hierarchical structure, in which successive models can be interpreted as an improvement of previous ones in response to distributional shifts in data—this is akin to a feedback learning loop where model predictions correct themselves incrementally. Importantly, the prediction quality of each of the models can be inspected independently. Further, the IL setting allows models to process data streams with a finite memory usage by fixing the number of previous models that can be used by a model, so that the size of the training set (consisting of new features and predictions of previous models) remains bounded. There are many other possibilities for the design of IL models to deal with concept drifts in data. See [3, 10] for a survey on recent methods in modelling data streams with different change detection and adaptive learning techniques.

Our framework applies this hierarchical IL setting to a collection of machine learning models in parallel, which can be thought of as layers of models. However, in contrast to standard neural network architectures, such as the multilayer perceptron (MLP), the training is done in a single forward pass without back-propagation. This approach allows us to train complex model with reduced computational resources, as there is no need to put the whole model in distributed memory to pass gradients between layers. In this way, each model within a layer can be trained independently, and training becomes parallelised across GPUs without the need for specialised software packages to distribute data between GPUs. Recent work in deep learning suggests that backpropagation is not strictly necessary for model training [26]. For instance, Deep Regression Ensemble (DRE) [27] is built by training layers of ridge regression models with random feature projections. The deep incremental model presented here, on the other hand, focuses on data streams and temporal data and imposes no restrictions on the ML models used as building blocks forming the layers.

2 Temporal data formulations

Our work deals with prediction tasks motivated by financial temporal data streams, whereby the ranking of a group of stocks needs to be predicted based on the information available at era . Such temporal data streams are treated under different formulations.

2.1 Temporal Tabular Datasets

Our temporal data is compiled into temporal tabular datasets, whereby the data at each time point is represented by features that have been computed from the time series up to that time.

Definition (Temporal Tabular Dataset).

A temporal tabular dataset is a set of matrices collected over time eras 1 to . Each matrix represents data available at era with dimension , where is the number of samples in era and is the number of features describing the samples. The are the targets to be predicted from the features , and can be single-dimensional or multi-dimensional. The definition of the features is fixed throughout the eras, in the sense that the same computation is used to obtain the same number of features at each era. Although the features can be in different formats (i.e., numerical, ordinal or categorical), they are usually transformed into equal-sized or Gaussian-binned numerical (ordinal) values. Note that the number of data samples does not have to be constant across time.

Remark (Data Lag).

Unlike standard online learning problems, where newly arrived data are used immediately to generate predictions and to update the models, in financial applications there is usually a fixed time lag for the targets from an era to become known (also known as data embargo). If the data embargo is, e.g., equal to eras, the targets of era become known at era , and only then can they be used to calculate the quality of predictions according to a suitably chosen metric.

2.2 Time Series Data

In contrast, many traditional methods use time series directly to infer models for prediction.

Definition (Multivariate time series).

A multivariate time series of steps and channels can be represented as a matrix , where and each (column) vector contains the values of the channels at time . In many applications, the number of channels is assumed to be fixed throughout time, with regular and synchronous sampling, i.e. the values in each vector from the channels arrive simultaneously at a fixed frequency.

Although here we will concentrate on methods to predict temporal tabular datasets, there is a large variety of time series models that predict the time series directly.

Definition (Time Series Model).

Given a time series , a (one-step ahead) time series model is a function that predicts the vector from . In practice, the function is often learned by training statistical or ML models using different instances of obtained by shifting across the time dimension.

A simple example of such a model, which will be used below, is the Exponential Moving Average (EMA). Moving averages are commonly used to capture trends in time series as follows.

Definition (Exponential Moving Average).

Given a univariate time series , the exponential moving average of the time series at time with decay is defined as

| (1) |

with initialisation .

Remark.

More complex time series models have been developed, including sequence models in deep learning, such as LSTM [28] and Transformers [29]. However, these models tend to be overparameterised and lack robustness to regime changes [30]. They also involve heavy computational costs associated with the training and updating of models.

2.3 Transforming time series into temporal tabular datasets: feature extraction

There are a myriad of methods commonly used to transform multivariate time series into temporal tabular datasets. These feature engineering (FE) methods consist of feature extraction applied over a look-back window:

-

•

Feature extraction: a function that maps the time series to a feature space where is the number of features. Feature extraction methods can help reduce the dimension and noise in time series data.

-

•

Look-back window: Feature extraction is applied to data within a look-back window (memory) of fixed length . Multiple look-back windows can also be used to extract features that capture short-term and long-term trends, and concatenated to represent the state of the time series.

In this paper, we will employ two feature engineering methods that have been proposed for financial time series:

-

•

Signature Transform (ST): STs [31, 32, 33] are deterministic transformations, recently proposed by Lyons, which can extract features at increasing orders of complexity from multivariate data, including time series. See [33] for a review of different applications of signature transforms in machine learning. For details on how STs are applied to the Numerai dataset, see Section 11.1 in the Supplementary Information.

-

•

Random Fourier Transform (RFT): RFTs have been used in [34] to model the return of financial price time series but can also be applied to extract features from time series at each time step. The key idea is to approximate a mixture model of Gaussian kernels with trigonometric functions [35]. Details on how RFTs are applied on the Numerai dataset are given in the Supplementary Information, see Algorithm 12 in Section 11.1.

Remark.

As discussed in Section 3.2 in more detail, once feature extraction methods have been applied and temporal tabular datasets generated, traditional ML models such as ridge regression, gradient-boosting decision trees (GBDTs), and multi-layer perceptron (MLP) networks can be used to carry out predictions point-wise in time [24], without relying on complex and expensive advanced neural network architectures such as Recurrent Neural Networks (RNN), Long-Short-Term-Memory (LSTM) Networks or Transformers [29].

3 Machine learning for temporal data

Before describing our deep incremental learning approach, we give some relevant background and brief links to standard methods used for prediction of temporal tabular data. These methods will be used as the building blocks of our incremental learning approach.

3.1 Prediction of Temporal Tabular Datasets from time series data: Factor-timing models

Factor-timing models [36] are a well-used approach to produce predictions for a temporal tabular dataset from time series, whereby the raw predicted values from a time series model (e.g., the EMA (1)) are converted into normalised rankings, which are then used as weights for the linear factor-timing model (see Algorithm 1). As baseline for comparison, we apply below factor-timing models to time series that are derived from temporal tabular datasets through a transformation, as follows.

Definition (Derived Time Series).

A transformation is applied to the tabular features and targets at era to generate a multivariate time series: , where . For example, can be the Pearson correlation between feature and targets.

This procedure generates a time series of feature performances from the temporal tabular dataset, which can be used within a factor-timing model, as in Algorithm 1 avoiding look-ahead bias.

3.2 Machine Learning Models for Temporal Tabular Dataset prediction

In contrast to factor-timing models, ML methods can be applied directly to temporal tabular datasets for prediction tasks. There is a rich literature comparing different machine learning approaches on tabular datasets [37, 38, 39, 40]. Several benchmarking studies [37, 38, 39] have demonstrated that advanced deep learning methods, such as transformers [41] and other neural network (NN) models , underperform for regression/classification tasks on tabular datasets relative to traditional approaches, such as GBDT or MLP models. In particular, recent research [37] has shown that GBDTs with moderate hyperparameter tuning perform closely to much more complex NN models.

Further, previous studies had focused on datasets with relatively small numbers of features and samples ( features, data rows or samples), whereas we are interested in large datasets with more than 1000 features and more than 200,000 data rows. For larger datasets, it has been shown [37] that GBDTs performed better than 11 neural-network-based approaches and 5 other baseline approaches, such as Support Vector Machines. GBDT models also display higher performance when feature distributions are skewed or heavy-tailed.

Finally, our objective is the prediction of data streams that are not static or stationary, but rather dynamic and subject to distribution shifts. Previous work has shown that GBDTs and MLPs outperform other deep learning approaches for temporal tabular datasets, with higher robustness and lower computational requirements for training (and retraining) of models [24, 38, 39].

In this paper, GBDT models are studied in detail for tabular prediction, as it has demonstrated strong performances in benchmarking studies [37, 38, 39, 24] and there exist efficient implementations that allow scalable model training and inference.

Details of the GBDT and MLP models can be found in section and in the Supplementary Information.

4 Deep (hierarchical) Incremental Learning algorithm for temporal data

Our deep incremental learning model is built layer by layer, using component models of a given type (e.g., factor-timing models or GBDTs) composed hierarchically across layers, as follows. At any time, we split our temporal dataset into segments of temporal history. Each segment is assigned to a layer, and for each layer we train an ensemble of models computed with different random seeds. We thus define the number of layers , the sizes of the training data (‘lookback window’) for each layer , and the number of models in the ensemble within each layer .

The models are learnt using information from different temporal segments sequentially and hierarchically, layer by layer, so that past predictions can be used to refine future predictions. Operationally, at the start of the training in a layer , we prepare the features and targets that are shared by all component models within the layer using the most recent data from the specified lookback window. Importantly, the features used as inputs to a layer consist of both original features from the temporal tabular dataset plus predictions obtained from models trained in previous layers (see Fig. 1).

Regarding the type of component models that form the ensemble in each layer, any model that uses tabular features as input and predicts tabular targets can be used. This expands the class of models from standard tabular models, such as GBDT and MLP, to other multi-step models, such as factor-timing models. The overall model is therefore a composition of such component models.

Each component model within a layer is trained in an incremental manner. This means that the model parameters are updated at regular intervals as new data arrives only using the data from the given lookback window. Other hyperparameters of the model (e.g., boosting rounds for GBDTs) remain unchanged. For example, if the dataset in total has 1000 eras and we update the models every 50 eras with lookback window equal to 600 eras we would obtain 9 models, with model training at Eras 600,650,700, …, 1000.

The component models within each layer can be trained in parallel, which allows the incremental learning model to be efficient and scalable.

The pseudocode in Algorithm 2 outlines the overall structure of the computational framework.

This framework leads to a deep hierarchical ensemble of models, where each layer takes advantage of model ensembling, and the integration of information across layers through functional composition enables the incremental learning necessary to adapt to non-stationarity and regime changes. We now discuss briefly some characteristics of the model:

Hierarchical nature of the model and self-similarity:

The proposed framework is hierarchical: the ensemble of models in any given layer, which is used to generate predictions in time beyond the latest data arrival, integrates hierarchically both data and predictions obtained from the models in the preceding layers, themselves fitted to previous time periods. Indeed, the model has characteristics of self-similarity, since the layered structure can be seen as performing a functional composition of learning models of the same type, e.g., the component models within each layer can be chosen to be GBDTs (or MLPs) so that the learning mechanism of each individual component is similar to the overall model, and the structure is extended repeatedly in a self-similar manner by interpreting a component model as a base learner for another component model in a higher layer.

Universal Approximation Property:

It is well known that MLP and GBDT models have the universal function approximation property [42], and Deep Learning models for sequences, such as LSTM [43], also have the universal function approximation property for any dynamical system. Since the DIL model is a composition of models each of which has the universal function approximation property, it also has the universal approximation property for the underlying stochastic process that drives the data generation of the temporal tabular dataset.

Model stacking: bagging and boosting across time

Our model can also be interpreted as a stacked model with a total of base learners, such that base learners are trained in the -th iteration, corresponding to each of the layers. Ideas from bagging and boosting are integrated within the model. Each layer consists of multiple models trained in parallel, as in bagging, so that variance is reduced by combining predictions from different models within a layer. Further, our model can be considered as a degenerate case of boosting, where the learning rate of the target is set to zero inter-layers, such that the target is not adjusted based on predictions from previous layers. However, the architecture can be modified to allow for target adjustment (boosting) between layers if needed.

Adaptive nature of the model

A key characteristic of the DIL model is that it is designed to support dynamic model training, with parameters of each component model updated regularly to adapt to distributional shifts in data. Under the traditional machine learning framework, hyperparameters are selected by cross-validation on splits of the training data. Yet optimal hyperparameters based on a single test period might not work in future. In the DIL model, predictions from previous layers based on different model hyperparameters are combined in the successive layer, corresponding to a later span of time, acting as a dynamic soft selection of hyperparameters. It has been shown that stacking of models with different random seeds [44], hyperparameters [45] and architectures [46] leads to robust performance for static datasets. The DIL model can thus be seen as an extension of stacking techniques to stream datasets, so that models incrementally trained with incoming data streams are stacked to obtain more robust predictions.

5 Prediction tasks for neutral portfolio optimisation using financial data from the Numerai competition

Numerai dataset and prediction task

As discussed above, financial time series data can be used directly for prediction [47, 29], yet such methods tend to be overfitted, making them less robust to regime changes and to the high stochasticity inherent to financial data. Alternatively, feature engineering is applied at each era to compute features that capture different aspects of the time history over look-back periods. This approach leads to a temporal tabular dataset, which can be used for prediction without considering time explicitly. The Numerai competition is based on one such professionally curated temporal tabular dataset, formed by matrices that contain stock market features (computed by Numerai) for stocks updated weekly (i.e., eras are weeks). The definition and computation of the features is fixed throughout the eras. Importantly, the dataset is obfuscated, i.e., the identity of the stocks present each week is unknown. The task is then to predict the stock rankings each week, from lowest to highest expected return. This ranking is used to construct a market-neutral portfolio.

Features and Targets

Two versions of the Numerai dataset, V4.1 (Sunshine) and V4.2 (Rain) [48, 49] are used in this study, starting on 2003-01-03 (Era 1) and extending up to 2023-06-30 (Era 1070) 111The data keeps updating every week. The dataset is weekly, i.e., eras correspond to weeks.

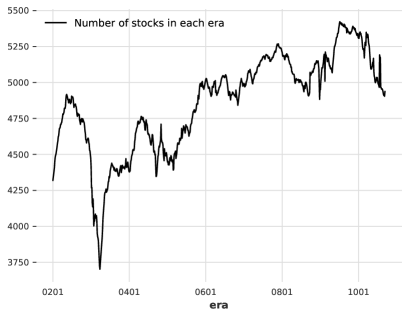

Each week, Numerai makes public a feature matrix of 1586 (V4.1)/ 2131 (V4.2) features for a changing selection of (unidentified) stocks, selected according to risk management rules by the Numerai hedge fund, plus several targets corresponding to stock returns normalised by different proprietary statistical methods. In Figure 2, the number of stocks in each week (era) from Era 201 to Era 1070 are shown, which demonstrates the number of stocks traded varied in each week.

The features are normalised into 5 equal-sized integer bins, from -2 to 2, so that the bins have zero mean. The targets are scaled between 0 and 1, and grouped into 5 bins (0, 0.25, 0.5, 0.75, 1.0) following a Gaussian-like distribution, and then subtracting 0.5 to make the bins zero-mean. For a more extended discussion of the Numerai dataset, including features and targets, see Ref. [24].

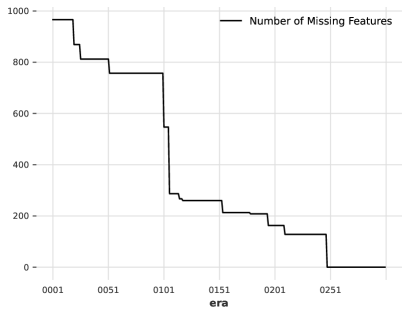

In V4.2 dataset, some features have completely missing values up to Era 251. In Figure 3, we show the number of features with completely missing values in each era between Era 1 and Era 300. In the first 100 eras, we have around of features with completely missing values. Therefore, we train XGBoost models using data from Era 201 onwards to ensure less than of features have completely missing values.

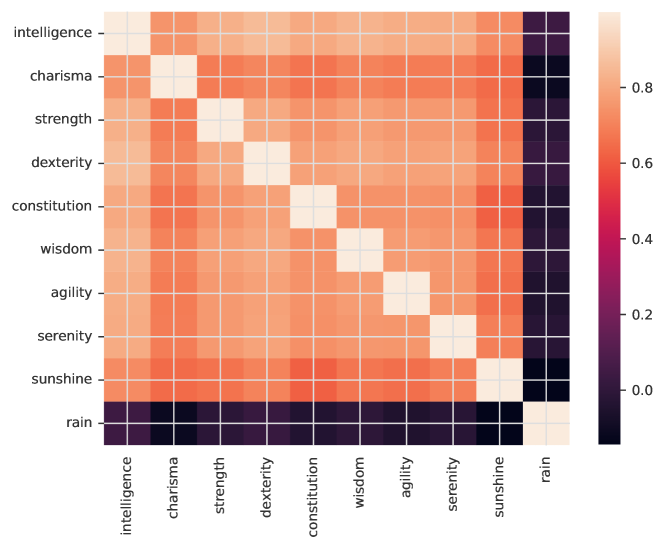

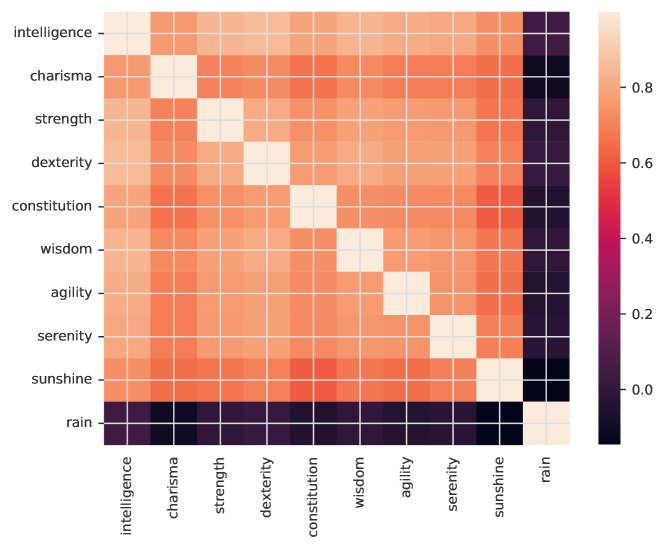

Each feature is now assigned to one or more groups. There are 10 feature groups in total, namely Intelligence, Charisma, Strength, Dexterity, Constitution, Wisdom, Agility, Serenity, Sunshine and Rain. For all feature groups except the last one (Rain), they represent features that behave similarly, as they are derived from similar data sources [49]. The Rain feature group consists of features that are created synthetically from features in other groups using information up to Era 585 222Numerai suggests most features are derived by fitting weights to the time-series of other features..

Data Lag

The data lag for predictions depends on the practicalities of the data pipeline. For Numerai, a lower bound for the scoring target to be resolved is 5 weeks (4 weeks of market data and 1 week for data processing). To take account into both the data lag for the data generation process from Numerai, and the time needed to train models, a conservative data lag of 15 weeks is used here.

Scoring Function

Numerai calculates a variant of Pearson correlation for all predictions in a single era , as follows [50]: Let be the predictions ranked between 0 and 1, the targets centred between -0.5 and 0.5, the (cumulative) distribution function of a standard Gaussian, and the element-wise sign and absolute value function, respectively, then the Numerai correlation score for era , , is given by:

where is the Pearson correlation function. Note that the 3/2 power is taken to emphasise the contribution from the highest and lowest predictions. The correlation score is collected for each era over the test period to calculate the following portfolio metrics:

-

•

Mean Corr: average of over all eras in the test period

-

•

Maximum Drawdown: maximum difference between the cumulative peak (high watermark) and the cumulative sum of correlation scores in the test period

-

•

Sharpe ratio: ratio of Mean corr and standard deviation of over all eras in the test period

-

•

Calmar ratio: ratio of Mean Corr and Maximum Drawdown

We will use these metrics to score our models throughout the paper. Specifically, high values of ‘Mean Corr’, ‘Sharpe ratio’ and ‘Calmar ratio’ are all indicative of good model performance. We use the main target decided by Numerai, ’target-cyrus-v4-20’ for scoring the trained models.

Example of concept drift

The presence of regime changes is one of the reasons why machine learning trading strategies suffer from significant losses. Machine learning trading strategies learn historical patterns from a vast amount of financial data. When there are regime changes, these patterns become obsolete, or even incorrect, such that they are no longer able to predict the future return of financial assets.

Regime changes are often unpredictable. For example, considering the return from Numerai hedge fund [51], the risk-adjusted return of hedge fund from September 2019 up to March 2023 is spectacular, where the maximum drawdown is less than . However, from March 2023 there are 4 consecutive months of negative returns, giving a cumulative drawdown of more than . Indeed, most risk-management metrics based on historical performances, such as Value-at-Risk (VaR) [52] would not be able to foresee this downturn.

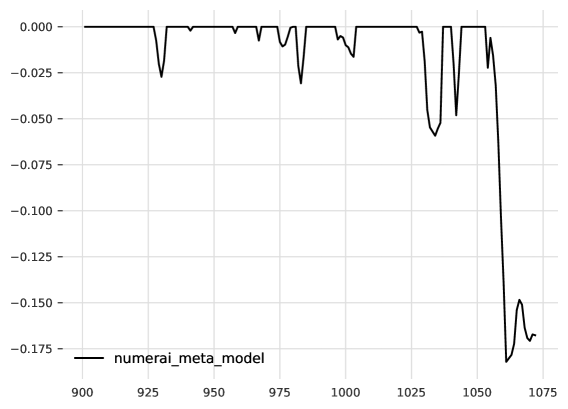

The challenging period for Numerai hedge fund corresponds to Era 1055 to Era 1070 in the dataset. Similar to the hedge fund, predictions from models submitted by participants in the competition also suffered from a large drawdown in the same period. In Figure 4, we show the Underwater (Drawdown) plot of the Numerai Meta Model. The drawdown between Era 1055–Era 1070 is around 4 times bigger than historical drawdown, suggesting there could be concept drift in the data.

Here, we define market regime post hoc based on performances. 2023-02-17 (Era 1051) to 2023-06-30 (Era 1070) is defined as the bear market. 2020-04-04 (Era 901) to 2023-02-10 (Era 1050) is defined as the bull market. In Table 1, we report the performances of the Numerai Meta Model from Era 901 to Era 1070 for the whole period and under both market regimes. Under bull market, we have a better than average performance while under bear market we have a negative performance. Over a long enough period, model predictions have a positive return but models can experience large drawdown in bear market, causing a lot of volatility to the portfolio.

| Regime | Mean Corr | Sharpe | Calmar |

|---|---|---|---|

| All | 0.0175 | 0.7915 | 0.0962 |

| Bull (Eras 901-1050) | 0.0207 | 1.0085 | 0.3491 |

| Bear (Eras 1051-1070) | -0.0062 | -0.3220 | -0.0341 |

6 Incremental Learning for Numerai prediction: Non-hierarchical models

Before presenting results from our hierarchical (deep) incremental learning model, we develop non-hierarchical incremental learning models for the Numerai dataset. These types of models have already been used in the literature [34, 53, 54] and will serve here both as a baseline comparison and to guide some our choices in model type, training methods and hyperparameter selection. We note that although these models are updated incrementally (i.e., they do incorporate information of new data arrivals) they do not incorporate information hierarchically across multiple layers, and hence fail to generalise well, due to severe distribution shifts in the data.

To enhance the breadth of our comparison, we study here two types of IL models: (i) factor-timing models that use explicit time series derived from the Numerai dataset, and (ii) ML algorithms (GBDTs, MLP) for tabular datasets which are used directly on the Numerai temporal tabular dataset.

6.1 Factor Timing Models

We generate three factor-timing (FT) models (based on Exponential Moving Average, Signature Transform, and Random Fourier Transform), all of which follow the setup in Algorithm 1 but are generated using specific transformations of the data, as follows.

We obtain a multivariate time series from the V4.2 dataset as described in Section Definition, i.e., we generate the time series , where each is derived by computing the correlation between each feature and the target . Once the time series is computed, we train factor timing models at each era using all the available data up to that point, bar the data embargo of 15 eras. In particular, we train the following FT models:

-

•

Exponential Moving Average factor-timing model: An EMA model (1) is computed for each of the 2132 feature series independently. This multivariate model is used to produced predictions for each era , which are then used within the FT model to produce model predictions , as given by Algorithm 1. These predictions are then scored using our portfolio metrics.

-

•

Feature Transform factor-timing models (ST and RFT): From a random subset of the 2132 variables of the time series we generate transformed features (ST or RFT) with lookback period using all available data. This process is repeated for a varying number of randomly drawn subsets of the variables in to explore the importance of model complexity , defined as the ratio of number of features and length of the time series. For example, for a time series of length , we may wish to generate models with complexity . Therefore, we obtain ST features by taking 60 subsets randomly sampled from , where each random subset of 4 time series generates 20 ST features (taking signatures up to level 2). An analogous procedure is followed for RFT. The transformed features (ST/RFT) from all subsets are then concatenated, and ridge regression with L2-regularisation is applied to generate the linear model for .

The FT models are retrained at every era using all data available up to that point; hence by construction these models are all incremental. In Algorithm 3, we describe the incremental learning procedure to train FT models.

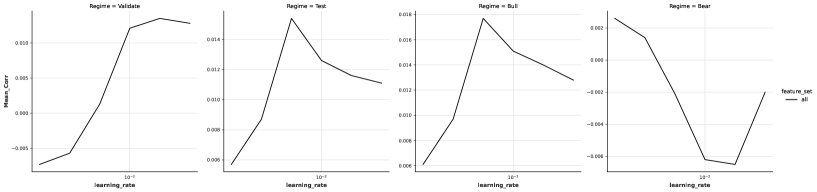

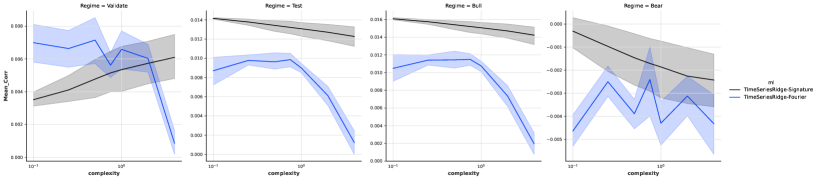

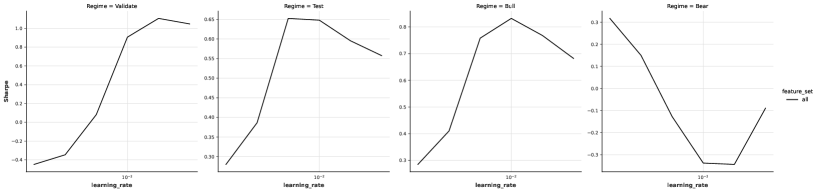

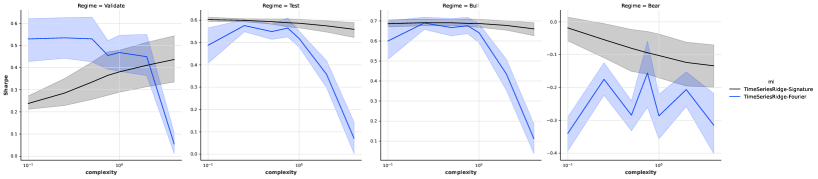

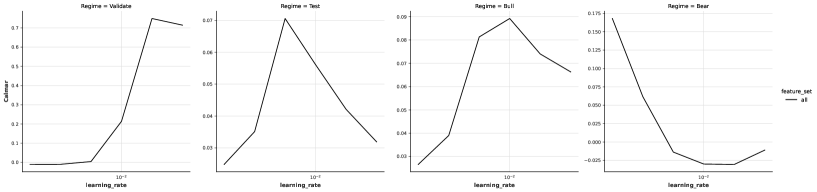

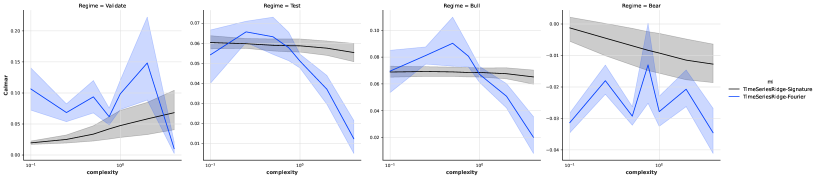

To optimise the key hyperparameters of the FT models (decay for EMA models, and complexity for ST/RFT models), we evaluate their one-step ahead performance over the validation period from Era 801-Era 885. Figure 5(a) shows the performances of EMA models with different weight decays under different market regimes for weight decays . Note that the best weight decay for Mean Corr in the validation period is 0.02, whereas it is 0.005 in the test period. This is another example of the effect of regime changes and why time-series cross-validation cannot always select the best weight decay for out-of-sample data. In particular, and as expected, models with a smaller decay constant perform better in Bear market but are the worst in Bull market. The key hyperparameter for the signture FT models (complexity) is explored in Figure 5(b) under different market regimes, averaged over 4 different random seeds. We train Feature Transform factor-timing models with different complexities . RFT performs better than ST models in the validation period for small model complexity () but not in the test period. For RFT models, Mean Corr decreases as model complexities increases. For ST models, Mean Corr increases as model complexity increases in the validation period but not in the test period. This suggests using more complex factor-timing models do not always give better results for FT models and reinforces the suggestion that hyperparameters selected based on time-series cross-validation might not be robust in out-of-sample data.

6.2 Benchmark IL model for XGBoost models

Two key hyperparameters for IL models are (i) training size, which for a temporal tabular dataset corresponds to the number of eras of data to be used in training; and (ii) retraining period, which governs how often the model is retrained/updated using the latest data.

In this section, we train IL models with different training sizes and retrain periods, using XGBoost models with two different sets of hyperparameters:

-

•

a set found by grid search with fixed number of boosting rounds and learning rate , which we denote the Ansatz hyperparameter set

-

•

a set provided by Numerai in their example Python script, denoted here the Numerai hyperparameter set.

In each model retrain, we use all the available data from Era 201 to train the models. For example, at Era 1000 which is the retrain of model, we use 800 eras of data from Era 201 to train the models. The first retrain at Era 801 uses 600 eras of data, which is roughly equal to the training period of the Numerai example models using the first 12 years of data ( eras).

For completeness, and as a reference comparison, we also create benchmark models that are not regularly retrained, which we call Ansatz-Fixed and Numerai-Fixed respectively.

The details on the procedure to create hyperparameter sets and model training are described in Sections 11.2 and 11.2.3 in the SI. To speed up training, we train models using only around half of data in each era by removing observations with target equal to the Median value (0.5). We show in SI Section 11.2.1 that this sampling method does not deteriorate model performance, while reducing computational costs by half compared to training using all data.

Finally, in order to manage the computational constraints, we produce regular samples of the data eras in the training period such that only of the data eras is used in model training. We then train 4 models each using of data without overlap. For example, we use data from Era 1,5,9, to train the first model, and similarly for the other 3 models. We call this procedure regular era sampling.

We create benchmark models of size . The train size of models are fixed to 600 (with the last 15 eras of data for embargo) with the start of training data at Era 201. For models with , we regularly retrain models every 50th era, which corresponds to updating the model once per year. We do not retrain models with due to computational limitations. The learning rates of the model are determined using the Ansatz formula , which is explained in detail in Section 11.2.2 in SI.

We report performances of the benchmark models from Era 801 to Era 1070 according to the following regimes:

-

•

Validation: Era 801 - Era 885

-

•

Test: Era 901 - Era 1070

-

–

Bull: Era 901 - Era 1050

-

–

Bear: Era 1051 - Era 1070

-

–

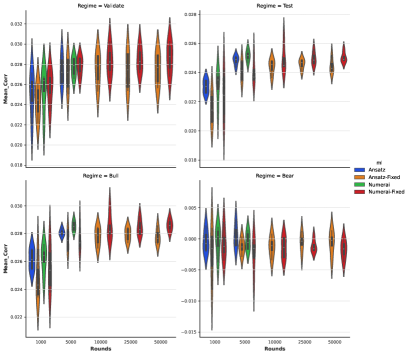

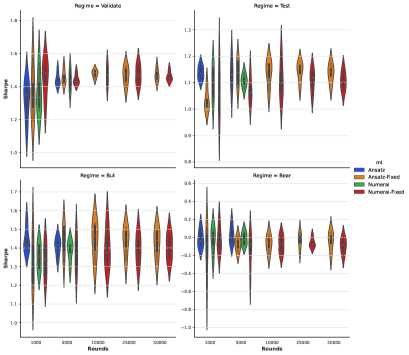

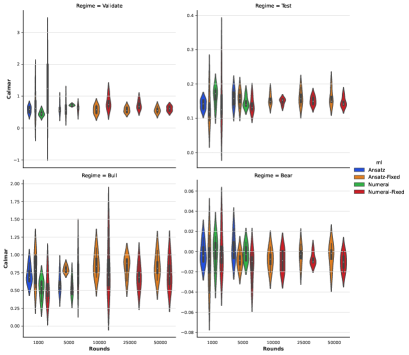

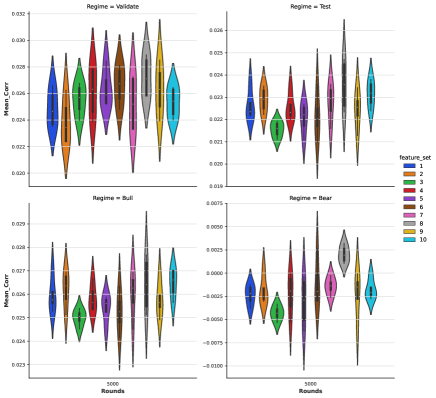

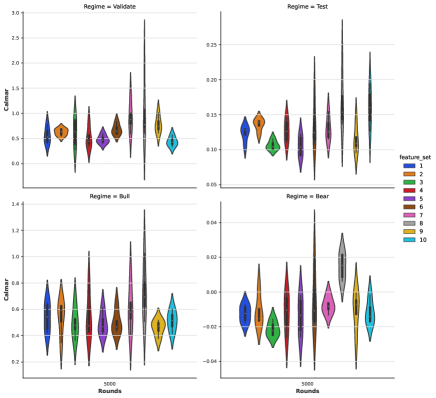

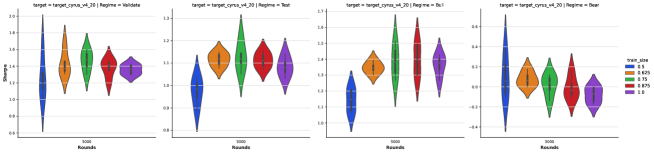

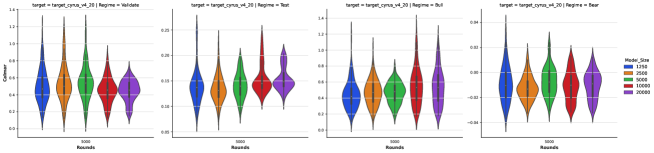

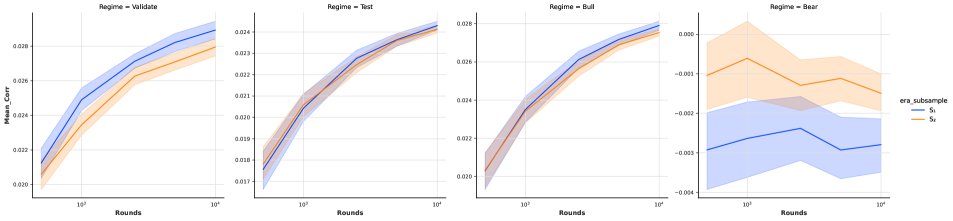

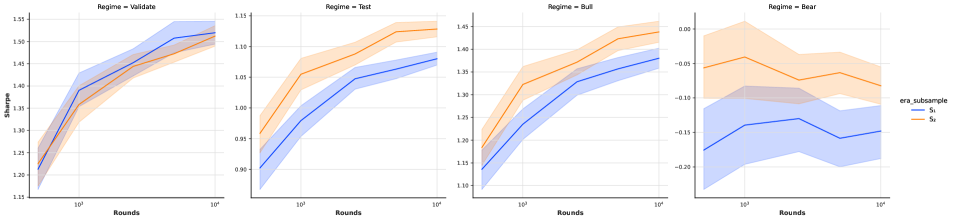

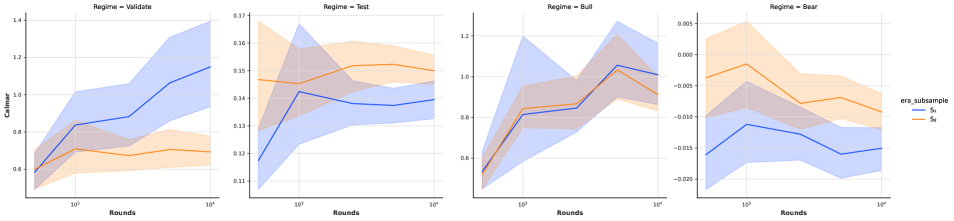

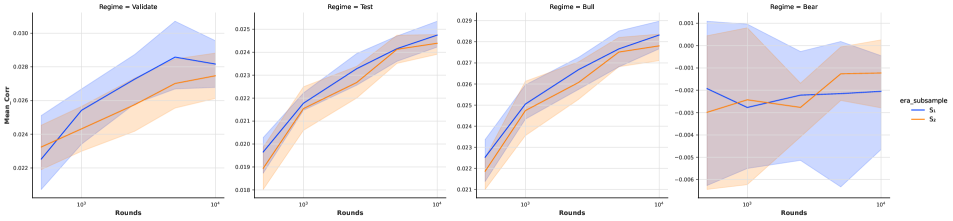

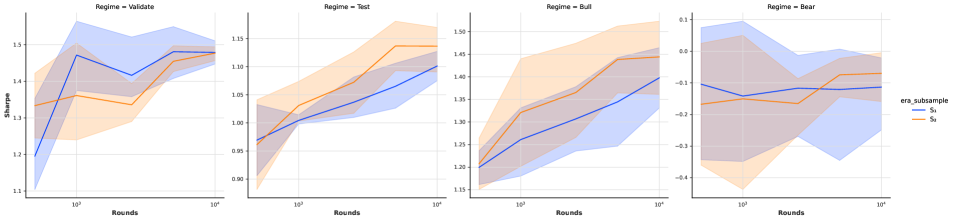

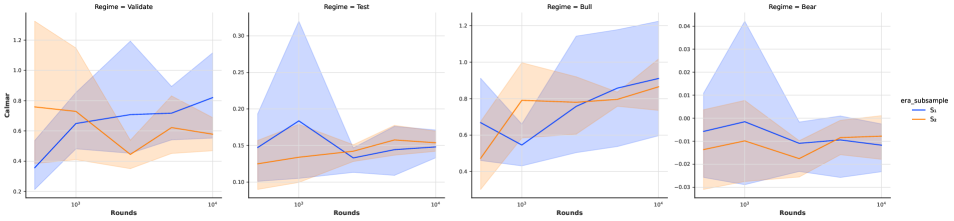

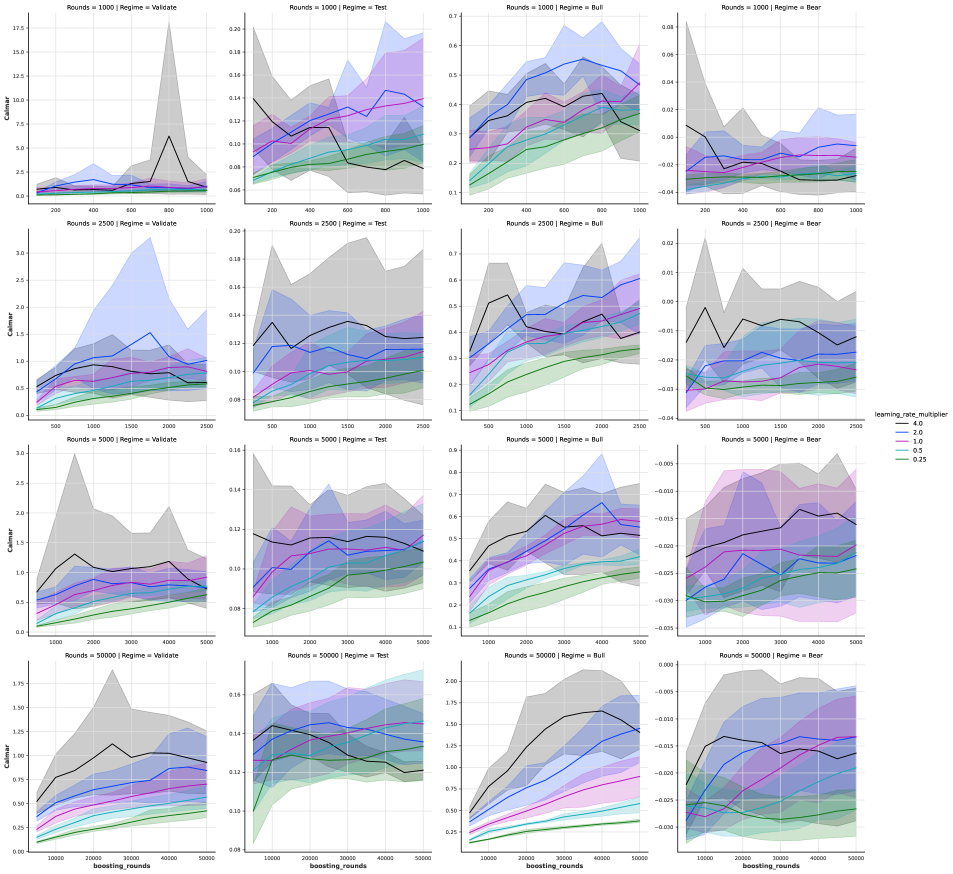

Figure 6 shows the performance of the benchmark models with different number of boosting rounds . Model performances for models with are not significantly different in both validation and test period. Within different market regimes in the test period, there are also no significant differences in model performance for .

Furthermore, there are no significant differences between each pair of models using the two different hyperparameter sets Ansatz and Numerai for a fixed data sampling method (regular retrain vs no retrain) in both the validation and test period. Yet as the number of boosting rounds increases, the performance differences between models with different hyperparameters narrows. This suggests that the differences between models performances are more due to differences between data sampling schemes used and to a lesser extent due to the hyperparameters.

To select our benchmark model hyperparameters, we consider both model performance and computational resources. Despite Numerai models having a slightly better Mean Corr than Ansatz models, they suffer from higher computational time and memory costs (explained in detail in SI Section 11.2) and do not exhibit an improvement in Mean Corr in the validation period. Further, models with Ansatz hyperparameters also have a lower variance than those with Numerai hyperparameters across different risk metrics (Mean Corr, Sharpe ratio). Given their similar performance and characteristics, we select the Ansatz hyperparameter set to train different deep IL models in the next section.

How to measure the similarity between two GBDT models

To measure the similarity between two GBDT models, we need to consider the overall structure similarity between two models also using feature importance, as this counts how many times a feature is used in a decision rule for a node within one of the trees in the GBDT model. It is not enough to consider only correlation between predictions because predictions that are similar but based on different decision rules can still offer diversification benefits to the ensemble by providing different learning pathways. If multiple independent learners arrive at similar predictions based on different information, the prediction becomes more robust to drifts in the data.

Definition (Structural Similarity of GBDT models).

For simplicity, a correlation based measure is used here to measure the overall similarity of two GBDT models, as follows Given two GBDT models A and B with the same number of features , let be the feature importance of the models, the structural similarity between two GBDT models is defined as the correlation between the normalised feature importance of the two models

| (2) | ||||

| (3) | ||||

| (4) |

where is the Pearson correlation function.

Note that this measure considers the averaged contribution of each feature towards the model and ignores the interaction between features.

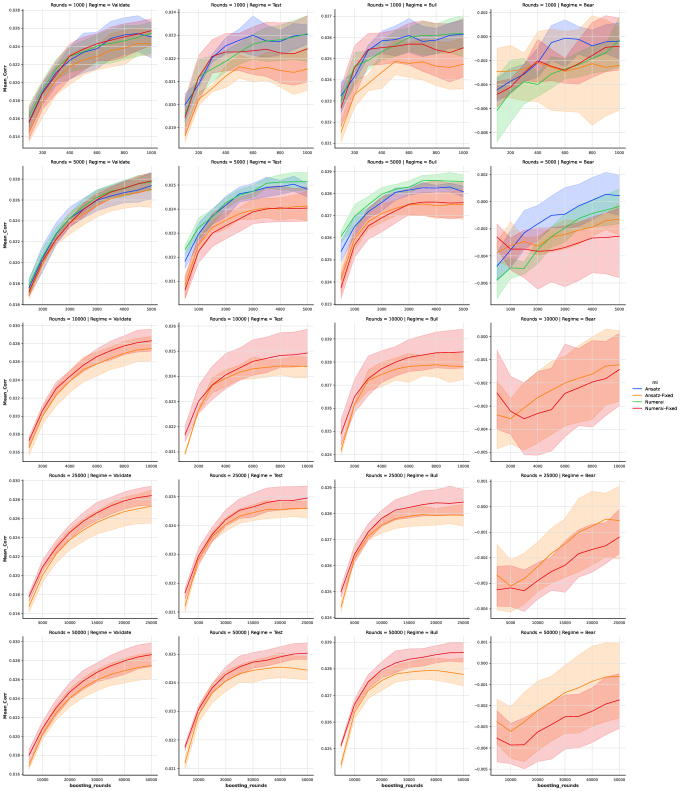

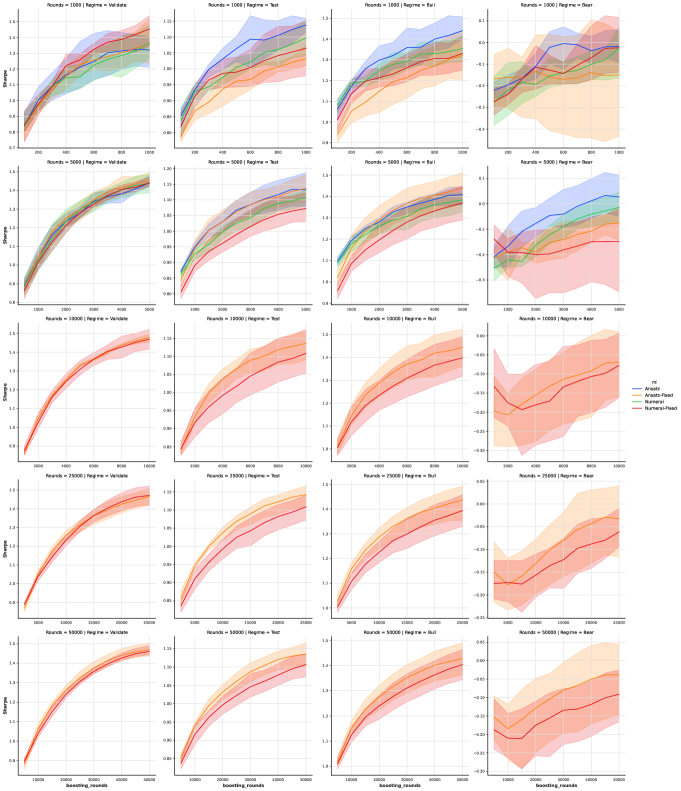

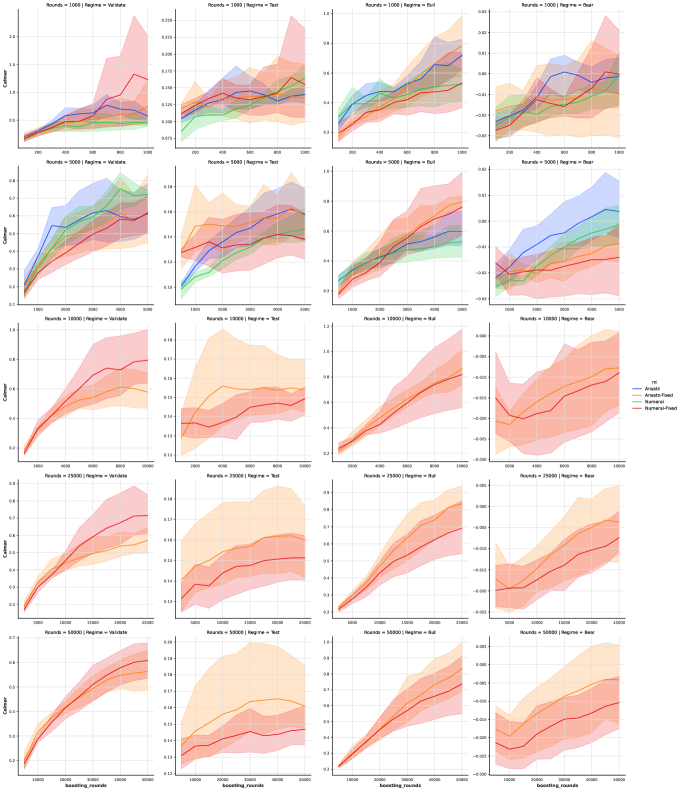

6.2.1 Differences between benchmark models

To understand the differences between models trained with different hyperparameters, we use the structural similarity measure (4) to understand the overall structural similarity between the Ansatz and Numerai benchmark models.

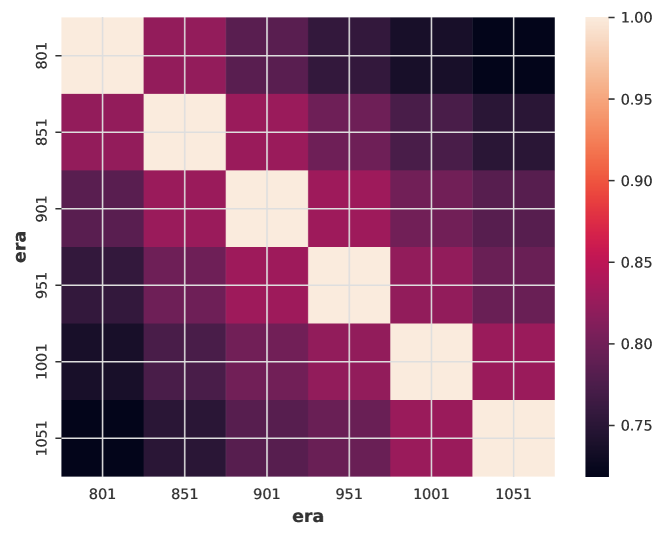

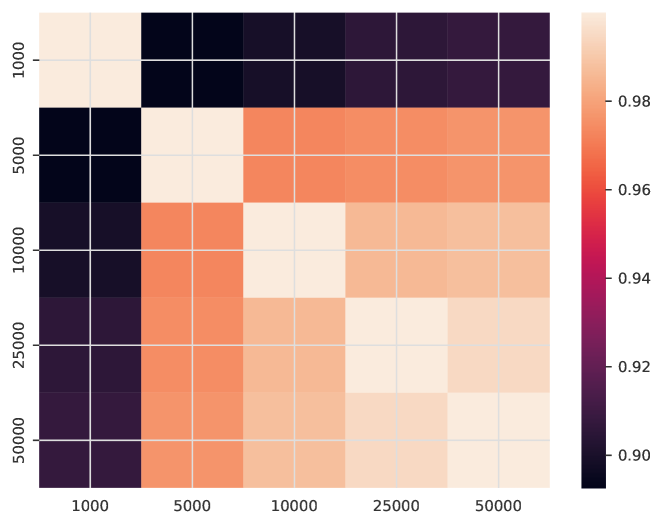

In Figure 7, we show the temporal correlation structure of the Ansatz and Numerai benchmark models with sizes . As expected, the correlation between the retrained models decreases as the time gap between model retrains increases. Smaller models () are less correlated with each other than larger models (), which can have even after 150 eras. This observation supports our choice not to retrain models with sizes , as the models are expected to be highly correlated with each other within the validation and test period.

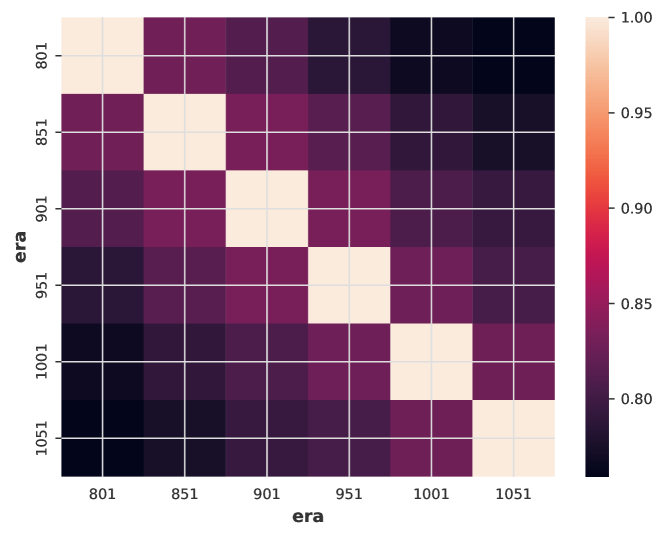

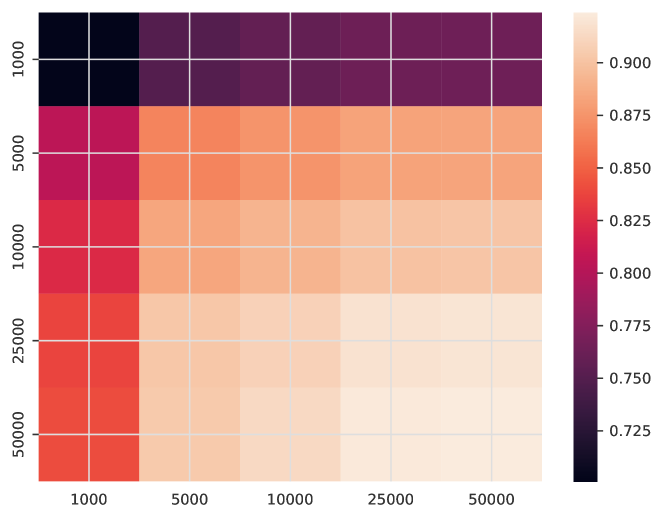

Figure 8 shows the correlation structure of benchmark models of different sizes at Era 801, the first model training time. For both Ansatz and Numerai hyperparameters, models with sizes are highly correlated. Cross-correlation between Ansatz and Numerai models of the same size is lower but the difference is negligible for models with sizes .

From the above observation, we hypothesise that models with different tree structure hyperparameters converge to the theoretical learning limit when the number of boosting rounds increases, on the condition that the learning rate of model is selected by the Ansatz formula. This means that hyperparameter optimisation is not necessary for large GBDT models so that we may pick any reasonable hyperparameter set (e.g., Ansatz) based on computational requirements.

Considering the fact model performances do not significantly improve beyond , we conclude it is not necessary to train single models with size as it consumes more computational resources while not providing meaningful gain in model performance. It is better instead to allocate the computational resources to train in parallel an ensemble of models with size .

7 Deep IL XGBoost Models

We now deploy the full deep IL model with dynamic ensembling, in which models trained with different sampling schemes and hyperparameters are combined dynamically to create better models. This is inspired by our previous work on dynamic forecasting in financial data [24] and by models used in weather forecasting [56], where ensemble forecasting has been used to improve robustness of predictions. Instead of creating predictions based on a single set of data/parameters, multiple sets of data/parameters are used to capture a range of scenarios, which represent possible trajectories for the evolution of weather or financial systems.

A key assumption for model ensembling is to use a diversified set of base models that are not so correlated to achieve the variance reduction benefits during ensembling. As a result, we explore different sampling strategies to create diversified base models. In particular, we study model ensembles created with different (1) training sizes, (2) learning rates, (3) targets and (4) feature sets. Unless otherwise specified, we apply regular era sampling in training the XGBoost models in Layer 1, which in turn gives 4 different models for each deep IL ensemble strategy.

The deep IL models used a 2-layer model structure. The Layer 1 models are XGBoost models trained with different hyperparameters and settings described below. The Layer 2 models , are chosen as:

-

•

: Simple average over all predictions

-

•

: Ridge Regression with L2-regularisation and parameters are restricted to be non-negative.

The purpose of Layer 2 models is to refine predictions obtained in Layer 1. By combining predictions at individual observation (stock) level instead of model level, this approach is more flexible than the dynamic model selection.

7.1 Ensemble strategies based on data sampling

7.1.1 Training Size Ensemble

For incremental learning problems, it is not known in advance how much data is required for model learning. Trade-offs are made when deciding the training sizes. If more data is used, the training data can cover more historical regimes, but also have the risk of including data no longer relevant. If less data is used, the training data can adapt more quickly to concept drift, but can also increase the risk of overfitting the models towards the current data regime. Therefore, there is no universal rule to select the training set size. The standard training set size recommended by Numerai is 600. Here, we explore if adjusting the training set sizes can improve model performances.

In Algorithm 4, the maximum training set size of Layer 1 models is increased to 800 eras and we train 5 models using the most recent of data. The number of boosting rounds is scaled with respect to training size. The learning rates of models is determined by the Ansatz formula , using the scaled number of boosting rounds.

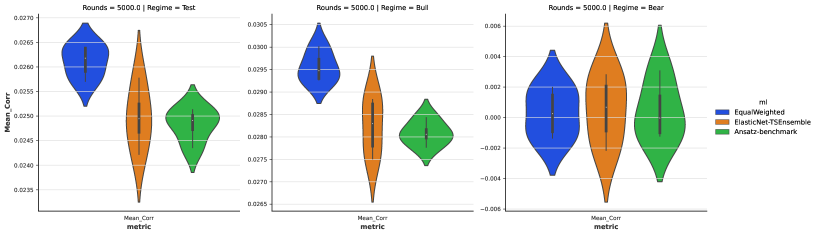

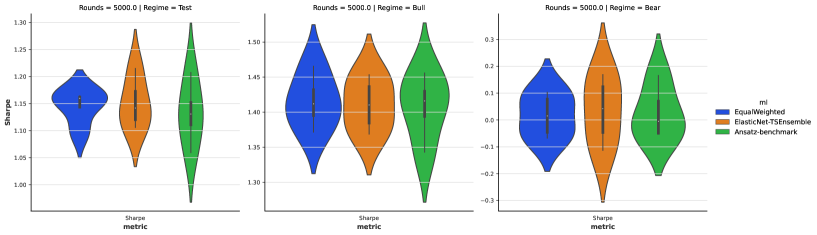

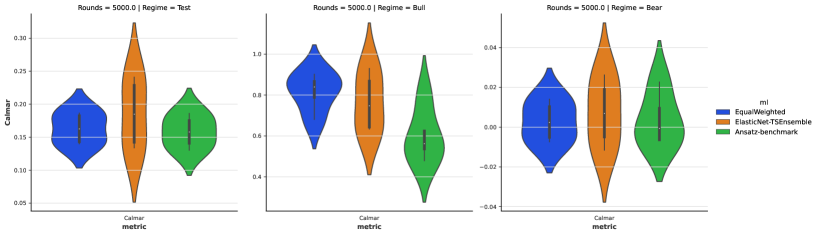

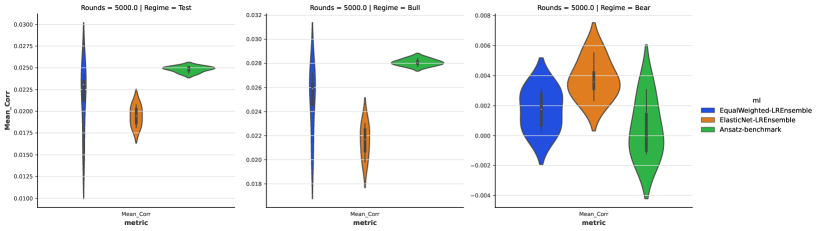

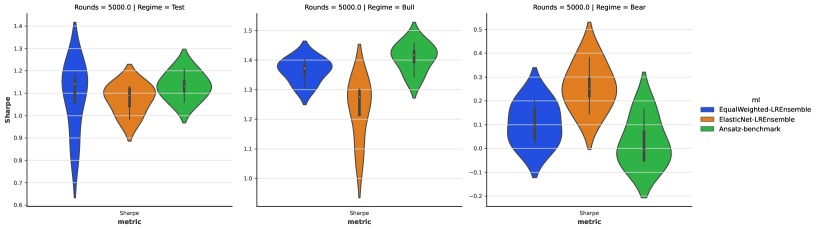

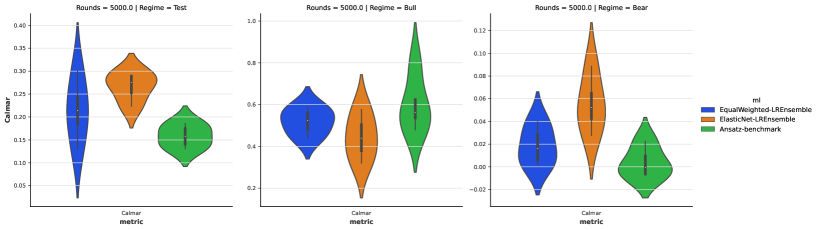

In Figure 9, we compare the performances of the two Layer 2 models (Elastic Net, Equal Weighted) with the benchmark Ansatz model of . The Equal Weighted model over all possible training set sizes achieves a higher Mean Corr than the benchmark model in the test period, yet there is improvement in the Bull market but not in the Bear market. The Elastic Net model does not significantly improve the risk metrics compared to benchmark. Calmar ratio of Equal Weighted model is improved in the Bull market but not in the Bear market.

7.2 Ensemble strategies based on different learning strategies

7.2.1 Learning Rate model ensemble (Complexity ensemble)

Recent research suggests that features are learnt with different speeds within a neural network [57, 58]. Inspired by this idea, we combine GBDT models with different learning rates to learn models capturing both fast and slowing features.

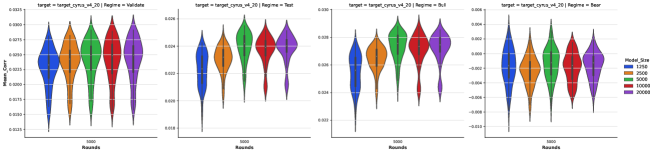

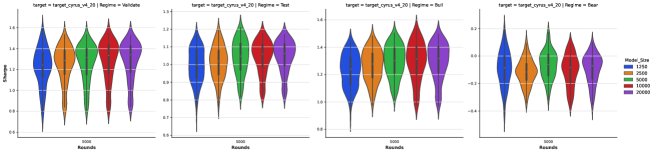

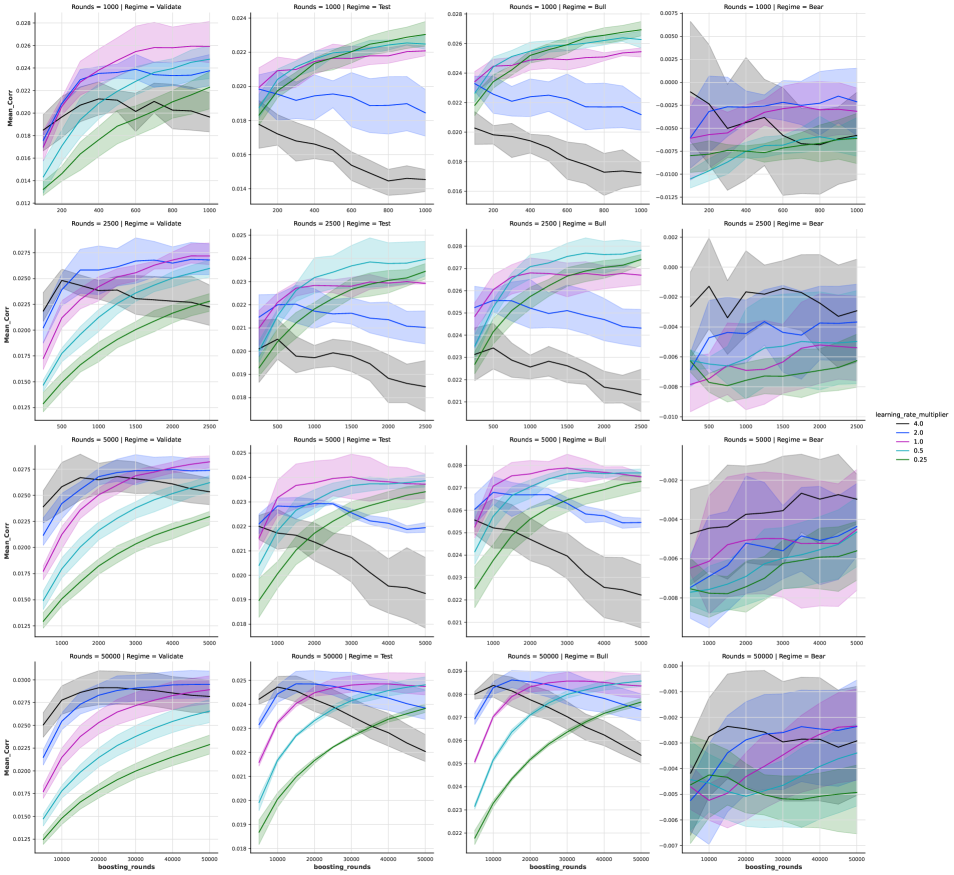

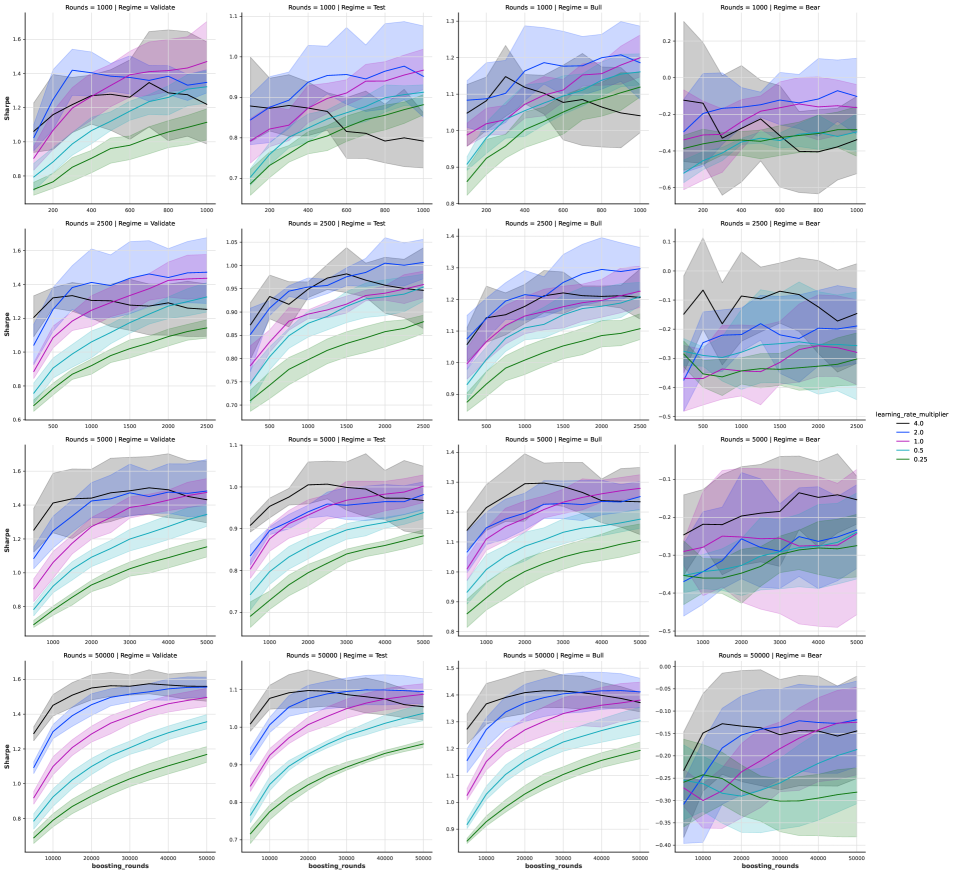

In Algorithm5, we combine XGBoost models with 5 different learning rates. For a given number of boosting rounds , in addition to training the model of size as above, we train two larger models of size and and two smaller models of size and where the learning rate are adjusted by the Ansatz formula. To reduce computational costs, the two larger models are not regularly retrained. Only models with number of boosting rounds less than or equal to are regularly retrained. The Layer 2 models used in Algorithm5 are the same as those used in Algorithm 4. Since the Ansatz formula is used to determine the learning rate and the number of boosting rounds pair for the Layer 1 models, the above procedure is equivalent to combining models with different complexities, where the number of boosting rounds is used to measure the complexity of GBDT models.

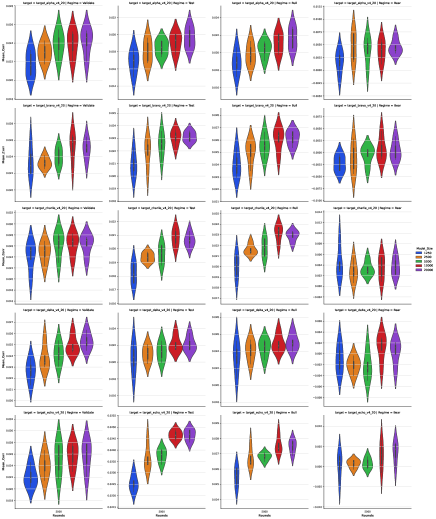

We run Algorithm 5 for and performances for the two Layer 2 models are shown in Figure 10, compared with the Ansatz benchmark model with . Both the Equal Weighted and Elastic Net models improve Mean Corr and Sharpe ratio in the test period compared to the benchmark. Calmar ratio is also improved in the Bull market, but not in the Bear market.

In Figure 19 in SI, we show the learning curves of the 5 Layer 1 XGBoost models with different learning rates and the corresponding number of boosting rounds (1250,2500,5000,10000,20000). Although larger models perform slightly better than smaller models in the validation and test period, there are no significant differences in model performances in the Bear market. Therefore, there is no single optimal complexity across all regimes. This observation supports our proposed use of deep IL to combine the strength of models with different complexity (learning rates) so that the ensemble model is more robust.

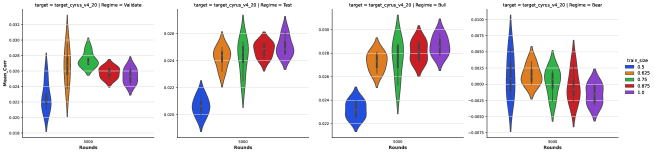

7.3 Ensemble strategies based on different targets

Feature projection was used to reduce drawdown of trading strategies in [24]. In the V4.2 dataset [49], Numerai provides 5 different targets (Alpha-20D, Bravo-20D, Charlie-20D, Delta-20D, Echo-20D) in addition to the main scoring target (Cyrus-20D) which incorporates various risk management and hedging strategies. By design, these targets will offer a lower return (Mean Corr) but with lower risks (Max Drawdown and Volatility). The overall risk profile is improved even the portfolio return is reduced.

7.3.1 Model ensemble with different targets and learning rates

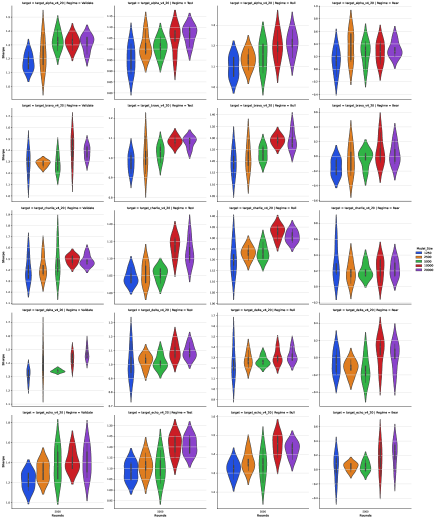

In Algorithm6, we combine XGBoost models trained with the five different targets using different learning rates as in Algorithm 5. In total, we train 25 Layer 1 XGBoost models to be combined in Layer 2. The Layer 2 models used in Algorithm6 are the same as those used in Algorithm 4.

In Figure 11, we compare the performances of the two Layer 2 models (Elastic Net, Equal Weighted) against the benchmark Ansatz model of . The Equal Weighted model over all 25 Layer 1 XGBoost models with different targets over different learning rates achieves a higher Sharpe and Calmar ratio than the benchmark model in the test period at a lower Mean Corr ( of the Benchmark model). Elastic Net can further improve the Calmar ratio but with a further lower Mean Corr ( of the Benchmark model). The improvement of Sharpe and Calmar of models using different targets can be attributed to a lower downside in the Bear market. Employing various hedging strategies, such as using the risk-controlled targets in model training will result in a lower performance in Bull market. The diversification benefits can only been observed when there are regime changes in the data, such as during the Bear market where the benchmark unhedged strategy performs poorly. Therefore, to fairly access the merit of different hedging strategies, the test period needs to be long enough to cover different market regimes.

7.4 Ensemble strategies based on feature sampling

7.4.1 Feature Sets model ensemble

Feature selection and sampling methods are useful in training models. Random feature sampling, a common procedure used at the local level before the start of training each tree can be applied at the global level before model training. By design, the learnt models are more diverse, as some features will never be used in the overall model rather than simply missing in some trees. It also lowers computational requirements of models as we do not have to fit all the data to the model. Here, we study Jackknife sampling [59] among other sampling techniques to build diversified models suitable for ensembling.

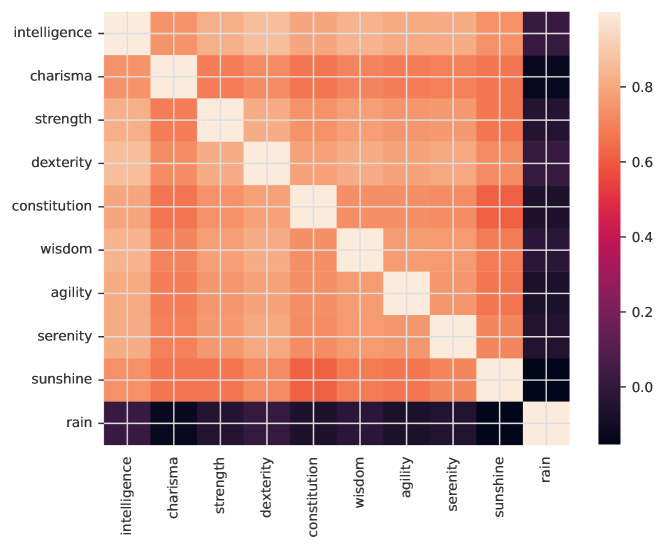

The feature group labels in Numerai V4.2 dataset can be considered as a way of feature clustering using domain knowledge. Instead of analysing the high-dimensional temporal correlation structure of the features by clustering or dimensionality reduction methods, we use the labels provided by Numerai, which are created with the knowledge of data sources and feature generation process to correctly group features into different categories. This approach saves computational time and avoids identifying spurious relationships between features.

Jackknife feature sets , for are created as follows. For each for the 10 feature groups (Intelligence, Charisma, Strength, Dexterity, Constitution, Wisdom, Agility, Serenity, Sunshine, Rain), we remove that set from the 2132 features one at a time, and then use the remaining 9 groups to form the Jackknife feature sets . The Jackknife feature sets are then used to train XGBoost models, using the procedure described in Algorithm7. The Layer 2 models used in Algorithm7 are the same as those used in Algorithm4.

To evaluate the usefulness of feature group labels in model building, we compare our approach with two different baseline methods: (i) Deep IL XGBoost models over random feature sampling, as described in Algorithm8; and (ii) benchmark XGBoost models trained with all the features using Ansatz hyperparameters. The Layer 2 models used in Algorithm8 are the same as those used in Algorithm7. The reason to use (i) as a benchmark is to calibrate if feature group labels offer information that is better than random in separating the features into groups representing different signal sources, thus creating information barriers between models so that they are forced to learn rules that are different from each other. This would reduce correlation between predictions. The reason to use (ii) as a benchmark is to check if any form of feature selection is beneficial to model performance at all.

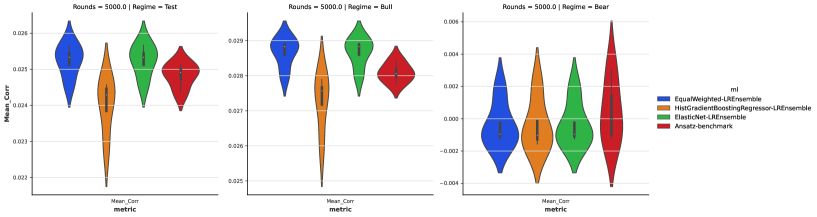

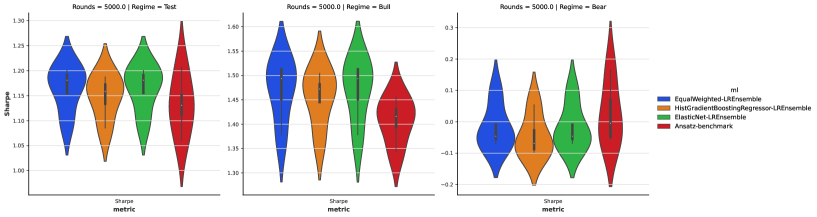

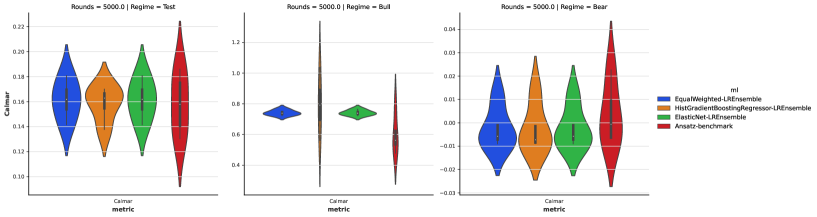

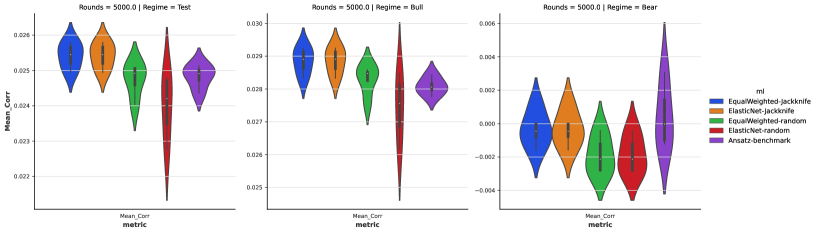

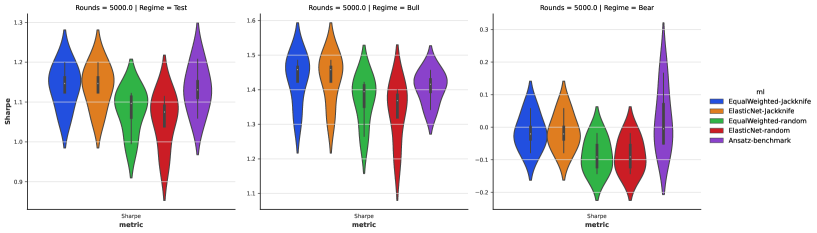

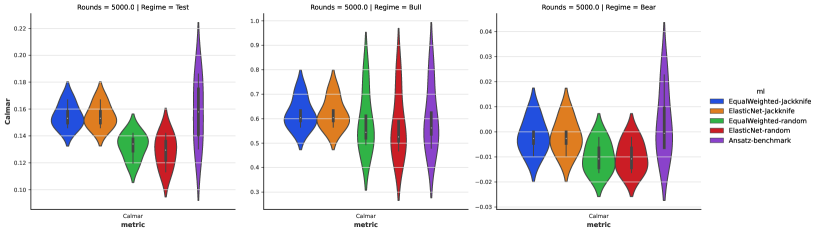

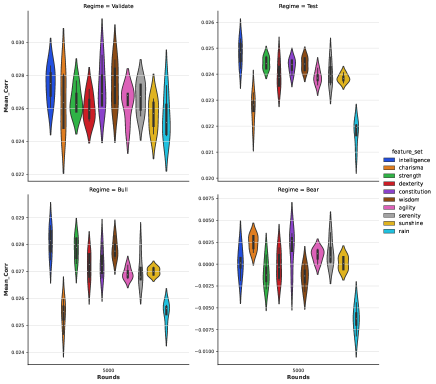

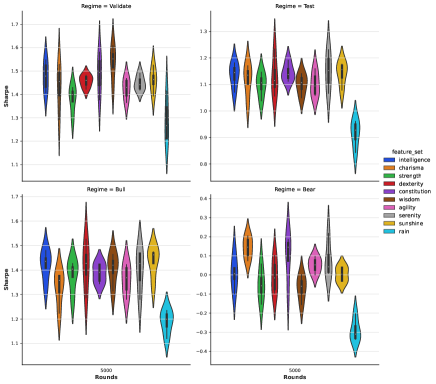

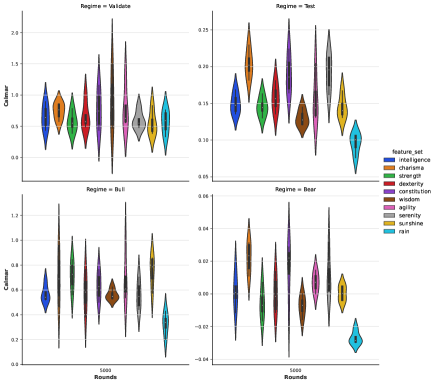

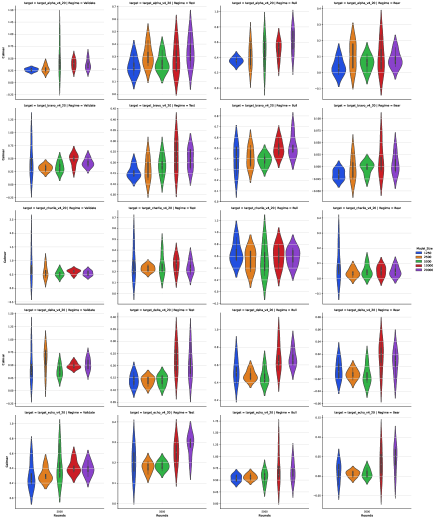

We run these two algorithms for . In Figure 13 we show the performances of the four Layer 2 models from Jackknife and random feature sampling against the benchmark Ansatz model with , which is also regularly retrained. The Layer 2 models from Jackknife sampling have a higher Mean Corr and Sharpe ratio than the models from random sampling and the benchmark model in both the validation and test period. The Layer 2 models using random sampling have comparable Mean Corr and Sharpe ratio with the benchmark model in both the validation and test period. Within models using Jackknife sampling, there are no significant differences between the Equal Weighted and Elastic Net model. However, for models using random sampling, Elastic Net model underperformed relative to the Equal weighted model. The historical performances of models from random sampling are simply noise, and we are not supposed to be able to learn any useful patterns from them.

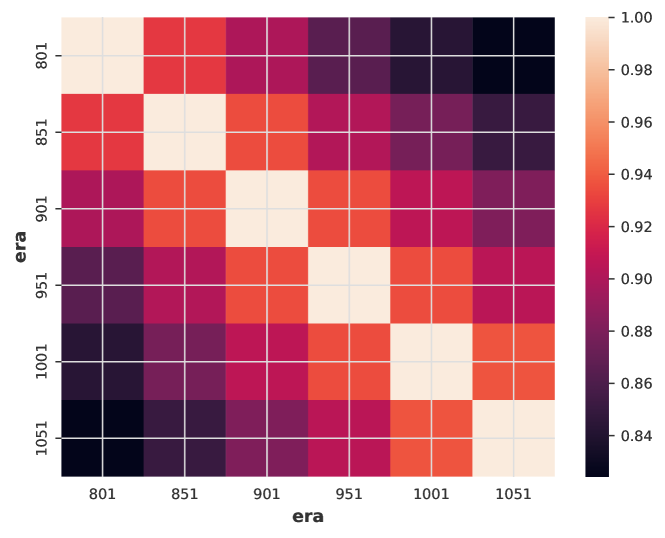

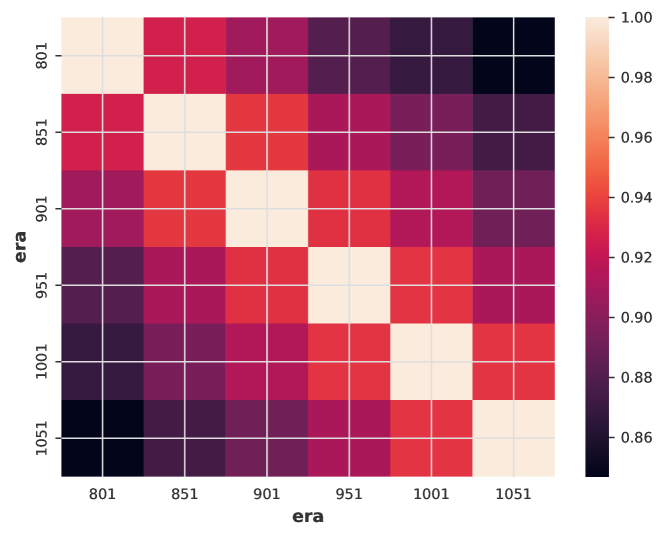

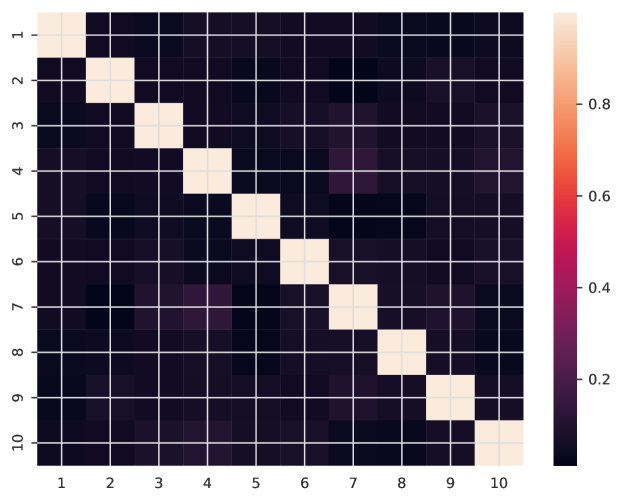

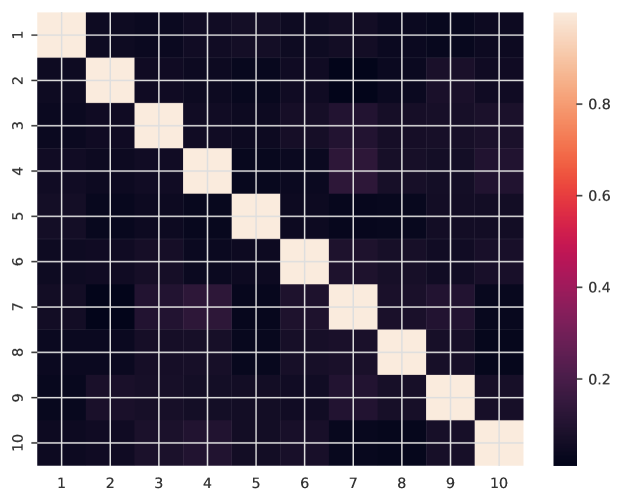

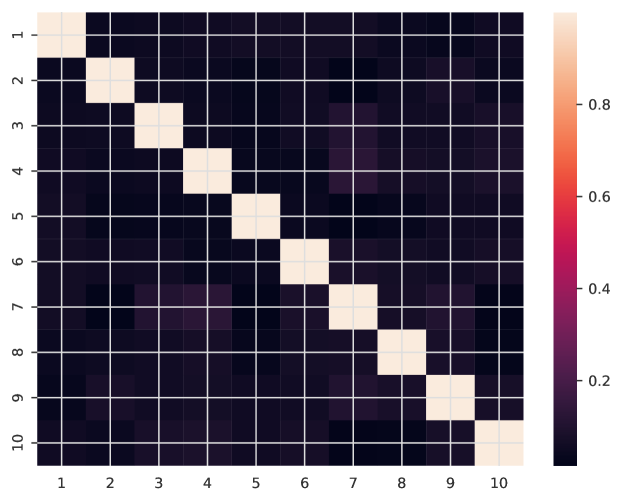

In Figure 12, we compare the correlation between the 10 Layer 1 XGBoost models obtained by Jackknife and random feature sampling. Models trained without rain feature set are uncorrelated to the rest of the models. Models trained by removing the other nine feature sets one at a time have correlation lower than 0.86 with average structural similarity of 0.66. Structural similarity of models obtained by Jackknife sampling is also stable across time, demonstrated by the similar heatmap representation of the models’ structural similarity at Era 801,901,1001. Models obtained by random feature sampling do not have any stable structural similarity by design.

While highly similar models offer limited diversification benefits in model ensembling, uncorrelated models created by random failed to generate better predictions. In conclusion, using domain knowledge about the data generation process, we can create models that are not over-similar to each other which can significantly improve model performances after ensembling.

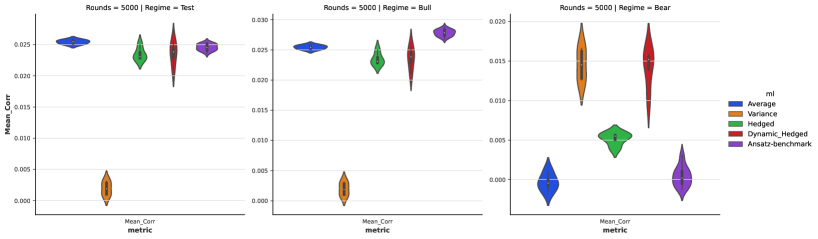

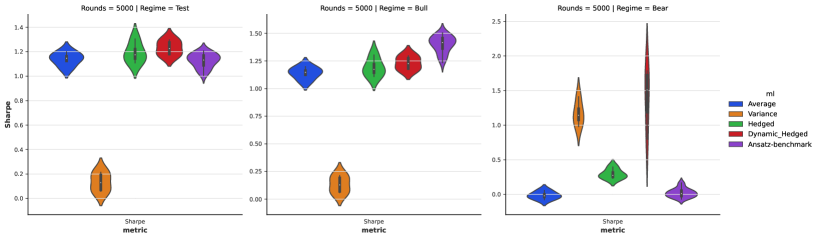

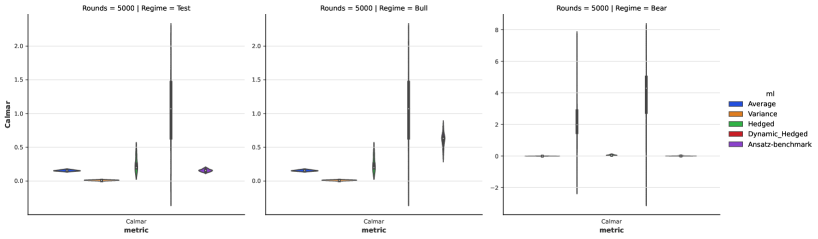

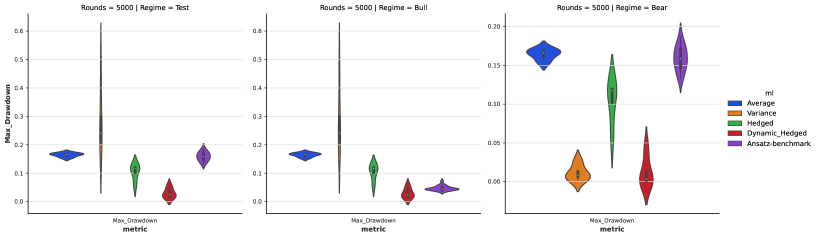

7.5 Dynamic Hedging based on model variances

Recent research suggests that disagreement between investors is an indicative signal of stock returns [bali2023machine]. In particular, under the Bull market, stocks that have the highest degree of disagreement between investors will under-perform relative to stocks that have the lowest degree of disagreement between investors. The opposite holds under the Bear market.

Here, the variance between model predictions from different Layer 1 models are used as proxy of disagreement between investors. In Algorithm9, two strategies are built based on predictions from the Layer 1 models, namely the Baseline model predictions based on the simple average and the Tail model predictions based on the standard deviation. The Tail risk model will buy stocks that the investors (Layer 1 models) disagree with each other the most and sell stocks that the investors agree with each other the most. Two approaches are then used to combine the Baseline and Tail Risk model predictions. With Static hedging, a linear combination of Baseline and Tail Risk is used for the whole test period. With Dynamic hedging, the hedging ratio, which determines how much Tail Risk strategy is used, is adjusted according to the prevailing performances of the Tail Risk strategy. The hedging ratio is switched between two modes: (i) No hedging and (ii) Baseline and Tail Risk according to the most recent 50-week performance of the Tail Risk strategy.

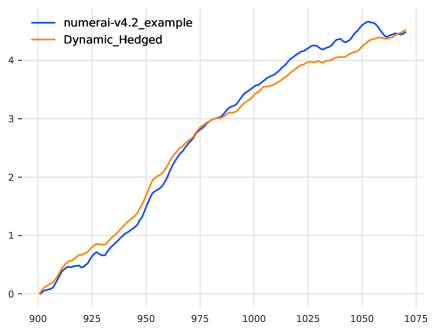

In Table 2, we compare the dynamic hedged model from deep IL XGBoost ensemble using feature set Jackknife and the dynamic hedging strategy described above, with the example model provided by Numerai. To note, the example model is trained using of data which is not replicated directly here due to memory limits. We used regular era sampling to train 4 models each with of data and then take the simple average over those. The Tail Risk model works well when the Baseline model has poor performances, demonstrating its complementary nature. The Dynamic hedged model achieves comparable Mean Corr with the example model provided by Numerai. The Sharpe ratio is improved from 0.9626 to 1.3169 while the Max Drawdown reduces from 0.2608 to 0.0237, a more than reduction. The portfolio return curve is much smoother for the Dynamic hedged model, as shown in Figure 15. We have checked the dynamic hedging procedure on deep IL XGBoost models with random feature sampling, over different targets, learning rates and training sizes. Detailed results are shown in Tables 6,9,8,7 in SI. The results show that dynamic hedged models from these ensembles are inferior to the above, as they have a lower Mean Corr and Sharpe ratio.

| Regime | Strategy | Mean Corr | Sharpe | Max Drawdown |

|---|---|---|---|---|

| Test | Example Model | 0.0264 | 0.9626 | 0.2608 |

| Baseline Model | 0.0266 | 1.1725 | 0.1602 | |

| Tail Risk Model | 0.0023 | 0.1601 | 0.2385 | |

| Static Hedged Model | 0.0203 | 1.2159 | 0.0435 | |

| Dynamic Hedged Model | 0.0266 | 1.3169 | 0.0237 | |

| Bull | Example Model | 0.0307 | 1.2512 | 0.0693 |

| Baseline Model | 0.0302 | 1.4780 | 0.0396 | |

| Tail Risk Model | 0.0006 | 0.0435 | 0.2385 | |

| Static Hedged Model | 0.0215 | 1.3014 | 0.0309 | |

| Dynamic Hedged Model | 0.0283 | 1.3844 | 0.0237 | |

| Bear | Example Model | -0.0060 | -0.2306 | 0.2608 |

| Baseline Model | -0.0002 | -0.0080 | 0.1602 | |

| Tail Risk Model | 0.0153 | 1.2929 | 0.0000 | |

| Static Hedged Model | 0.0109 | 0.7489 | 0.0435 | |

| Dynamic Hedged Model | 0.0137 | 1.1500 | 0.0220 |

Model ensembles created based on Jackknife feature set sampling use knowledge about the dataset and thus offer a better approximation of disagreement between investors. Therefore, the Tail Risk model created based on the variance between models trained with Jackknife feature set sampling is the most effective hedging strategy in the Bear market.

8 Conclusion

In this study, both traditional tabular and factor-timing models have been studied for the IL problem on the temporal tabular dataset from Numerai. Traditional tabular models, if retrained regularly can adapt to distribution shifts in data. On the other hand, factor-timing models failed to adapt to distribution shifts.

GBDT are robust ML models

We found that GBDT models performed best for the Numerai datasets, agreeing with the findings of [37], which demonstrate the robust and superior performances of GBDT models on large datasets. This is also partly due to the nature of features being binned values from continuous underlying measures, which favours models based on decision rules rather than regression. With suitable designs of the training process, such as a slow learning rate with a large number of boosting rounds, we can train XGBoost models with good performance, slowly converging to the theoretical optimal.

GBDT models are also highly scalable and have robust performance over slightly perturbed hyperparameters. The larger the GBDT model, the smaller the effect of model hyperparameters on the learning process and model performances. GBDT models are numerically stable, without the convergence issues that commonly plague the training of neural networks.

Feature and Data Sampling

Data management and forgetting mechanism is an integrated part of an IL pipeline [3] to build robust prediction models on a data stream. The impact of data sampling methods is usually over-looked in most quantitative finance research and even in hedge funds [25]. Data and feature sampling methods can have significant effects on model performances.

Removing data with targets equal to the Median value can reduce computational time by half without significant loss to model performances. This demonstrates the point that well designed sampling procedures can be used to filter data for effective model training.

Feature sampling can also be used to increase diversity of models by enforcing constraints on features that are allowed to be used or interact in a model. Using feature set group labels can create feature sets that are more efficient in creating diverse model ensembles than random sampling.

In all incremental problems we encounter the stability-plasticity dilemma [60], which is the trade-off between the ability of ML models to adapt to new patterns and preserve existing knowledge. It is not known in advance which data sampling method will have the optimal performance and therefore ensembling models with different training sizes with equal weights is often a robust strategy when there are no additional information to decide how much data to use for model training.

Retraining benchmark models regularly can improve performances significantly compared to using the same model without updating. In general, model performances improves with the frequency of retrain but the requirements on computational resources also increase. Therefore, trade-offs between computational costs and the marginal gain in model performances are made for practical IL systems.

Learning rates and model complexity

We derive an Ansatz formula to determine the learning rate for a GBDT model given a fixed number of boosting rounds . We show the formula is optimal for our benchmark GBDT models over a wide range of sizes, from to .

Combining models with different degree of complexity, created with different number of boosting rounds with learning rates derived using the Ansatz formula, can improve model performances compared to models using a fixed number of boosting rounds. The optimal model complexity is regime dependent and therefore using deep IL techniques to dynamically combine model predictions can reduce downside risks in models.

Connection with Model Stacking/Selection

Stacking is a simple but highly effective technique to combine different ML model predictions. The concept of stacking is not limited to machine learning. In finance, portfolio optimisation is studied in detail to improve investment returns, where a convex optimisation is solved at each time step to find the linear combination of assets or strategies that maximise risk-adjusted return. Under the IL framework, model stacking can be performed dynamically. Here, we combine the predicted rankings from different ML models at each era with different weights. Instead of considering model stacking as a separate step to model training, model stacking can be incorporated as an integrated part in the IL framework, as an extra layer in the IL model.

Hedging against regime changes

Using the variance between models within the ensemble as a signal, tail risk strategy can be created to hedge the baseline prediction strategy based on simple average of different component models. Regime changes in data can be captured by uncertainty of model predictions, as a higher variance between models within the ensemble suggests a lower confidence of the predictions. Therefore, prediction based on variance would perform well under regime changes, such as the Bear market period identified in this study. The best performance is achieved when the component models are trained using different combinations of feature subsets based on economic knowledge about the dataset. In this case, the variance between models are the most informative approximation of disagreement between investors in the stock market.

Further Work

In most practical applications, multiple machine learning methods are used together to create an ensemble prediction. The IL model presented in this paper provides a comprehensive way to integrate different ML models in a consistent and systematic way to create point-in-time predictions. With a multi-layer structure and modularised design within each layer, the deep IL model can flexibly model datasets with different complexities and structures. Further work can be done by integrating different deep tabular models into the model and bench-marking different machine learning methods under the IL framework.

Within our incremental learning framework, we retrain each XGBoost model from scratch without using any information from previous ones. Currently, new methods [61, 62] have been developed which adapt towards concept drift in data by adding a suitable amount of trees to existing GBDT models. Different approaches, such as reusing a certain amount of base learners (trees) from previous trained GBDT models or updating the weights of trees dynamically depending on the severity of concept drift can be explored in future work.

We only consider the simplest form of deep learning models, MLP in this paper. Recent research suggests regularisation techniques [40] can improve performances of neural networks models over a wide range of network architecture. Further work can be done to investigate if careful design of the model training process with suitable regularisation can improve the scalability and model performances.

9 Acknowledgements

This work was supported in part by the Wellcome Trust under Grant 108908/B/15/Z and by the EPSRC under grant EP/N014529/1 funding the EPSRC Centre for Mathematics of Precision Healthcare at Imperial. MB also acknowledges support by the Nuffield Foundation under the project “The Future of Work and Well-being: The Pissarides Review”. We thank Numerai GP, LLC for providing the datasets used in the study.

10 Data and Code Availability

The data and code used in this paper are available at https://github.com/barahona-research-group/THOR-2.

References

- [1] Mingcong Song et al. “In-situ ai: Towards autonomous and incremental deep learning for iot systems” In 2018 IEEE International Symposium on High Performance Computer Architecture (HPCA), 2018, pp. 92–103 IEEE

- [2] Anna L Buczak and Erhan Guven “A survey of data mining and machine learning methods for cyber security intrusion detection” In IEEE Communications surveys & tutorials 18.2 IEEE, 2015, pp. 1153–1176

- [3] João Gama et al. “A Survey on Concept Drift Adaptation” In ACM Comput. Surv. 46.4 New York, NY, USA: Association for Computing Machinery, 2014 DOI: 10.1145/2523813

- [4] Eden Belouadah, Adrian Popescu and Ioannis Kanellos “A comprehensive study of class incremental learning algorithms for visual tasks” In Neural Networks 135 Elsevier, 2021, pp. 38–54

- [5] Yue Wu et al. “Large scale incremental learning” In Proceedings of the IEEE/CVF conference on computer vision and pattern recognition, 2019, pp. 374–382

- [6] Gido M Ven, Tinne Tuytelaars and Andreas S Tolias “Three types of incremental learning” In Nature Machine Intelligence 4.12 Nature Publishing Group UK London, 2022, pp. 1185–1197

- [7] Fei Zhu, Zhen Cheng, Xu-Yao Zhang and Cheng-lin Liu “Class-incremental learning via dual augmentation” In Advances in Neural Information Processing Systems 34, 2021, pp. 14306–14318

- [8] Yixuan Pei et al. “Learning a Condensed Frame for Memory-Efficient Video Class-Incremental Learning” In Advances in Neural Information Processing Systems 35 Curran Associates, Inc., 2022, pp. 31002–31016 URL: https://proceedings.neurips.cc/paper_files/paper/2022/file/c8ac22c0d4b263618f2a4f4657948912-Paper-Conference.pdf

- [9] Yixiong Zou, Shanghang Zhang, Yuhua Li and Ruixuan Li “Margin-Based Few-Shot Class-Incremental Learning with Class-Level Overfitting Mitigation” In Advances in Neural Information Processing Systems 35 Curran Associates, Inc., 2022, pp. 27267–27279 URL: https://proceedings.neurips.cc/paper_files/paper/2022/file/ae817e85f71ef86d5c9566598e185b89-Paper-Conference.pdf

- [10] Jie Lu et al. “Learning under Concept Drift: A Review” In IEEE Transactions on Knowledge and Data Engineering 31.12, 2019, pp. 2346–2363 DOI: 10.1109/TKDE.2018.2876857

- [11] Firas Bayram, Bestoun S Ahmed and Andreas Kassler “From concept drift to model degradation: An overview on performance-aware drift detectors” In Knowledge-Based Systems 245 Elsevier, 2022, pp. 108632

- [12] Kai Arulkumaran, Marc Peter Deisenroth, Miles Brundage and Anil Anthony Bharath “Deep reinforcement learning: A brief survey” In IEEE Signal Processing Magazine 34.6 IEEE, 2017, pp. 26–38

- [13] Yitian Hong, Yaochu Jin and Yang Tang “Rethinking Individual Global Max in Cooperative Multi-Agent Reinforcement Learning” In Advances in Neural Information Processing Systems 35 Curran Associates, Inc., 2022, pp. 32438–32449 URL: https://proceedings.neurips.cc/paper_files/paper/2022/file/d112fdd31c830900d1f2e4ccebffb54f-Paper-Conference.pdf

- [14] Osbert Bastani, Jason Yecheng Ma, Estelle Shen and Wanqiao Xu “Regret Bounds for Risk-Sensitive Reinforcement Learning” In Advances in Neural Information Processing Systems 35 Curran Associates, Inc., 2022, pp. 36259–36269 URL: https://proceedings.neurips.cc/paper_files/paper/2022/file/eb4898d622e9a48b5f9713ea1fcff2bf-Paper-Conference.pdf

- [15] Kaiqing Zhang et al. “Robust Multi-Agent Reinforcement Learning with Model Uncertainty” In Advances in Neural Information Processing Systems 33 Curran Associates, Inc., 2020, pp. 10571–10583 URL: https://proceedings.neurips.cc/paper_files/paper/2020/file/774412967f19ea61d448977ad9749078-Paper.pdf

- [16] Yue Deng et al. “Deep direct reinforcement learning for financial signal representation and trading” In IEEE transactions on neural networks and learning systems 28.3 IEEE, 2016, pp. 653–664

- [17] David Acuna, Jonah Philion and Sanja Fidler “Towards Optimal Strategies for Training Self-Driving Perception Models in Simulation” In Advances in Neural Information Processing Systems 34 Curran Associates, Inc., 2021, pp. 1686–1699 URL: https://proceedings.neurips.cc/paper_files/paper/2021/file/0d5bd023a3ee11c7abca5b42a93c4866-Paper.pdf

- [18] Jens Kober, J Andrew Bagnell and Jan Peters “Reinforcement learning in robotics: A survey” In The International Journal of Robotics Research 32.11 SAGE Publications Sage UK: London, England, 2013, pp. 1238–1274

- [19] Karol Arndt, Murtaza Hazara, Ali Ghadirzadeh and Ville Kyrki “Meta reinforcement learning for sim-to-real domain adaptation” In 2020 IEEE international conference on robotics and automation (ICRA), 2020, pp. 2725–2731 IEEE

- [20] Irina Higgins et al. “Darla: Improving zero-shot transfer in reinforcement learning” In International Conference on Machine Learning, 2017, pp. 1480–1490 PMLR

- [21] Xiaobai Ma, Katherine Driggs-Campbell and Mykel J Kochenderfer “Improved robustness and safety for autonomous vehicle control with adversarial reinforcement learning” In 2018 IEEE Intelligent Vehicles Symposium (IV), 2018, pp. 1665–1671 IEEE

- [22] Alexander Mott et al. “Towards interpretable reinforcement learning using attention augmented agents” In Advances in neural information processing systems 32, 2019

- [23] Ashley I Naimi and Laura B Balzer “Stacked generalization: an introduction to super learning” In European journal of epidemiology 33 Springer, 2018, pp. 459–464

- [24] Thomas Wong and Mauricio Barahona “Online learning techniques for prediction of temporal tabular datasets with regime changes”, 2023 arXiv:2301.00790 [q-fin.CP]

- [25] Corey Hoffstein, Nathan Faber and Steven Braun “Rebalance timing luck: the (dumb) luck of smart beta” In SSRN 3673910, 2020

- [26] Geoffrey Hinton “The Forward-Forward Algorithm: Some Preliminary Investigations” arXiv, 2022 DOI: 10.48550/ARXIV.2212.13345

- [27] Antoine Didisheim, Bryan Kelly and Semyon Malamud “Deep Regression Ensembles”, 2022 arXiv:2203.05417 [stat.ML]

- [28] Sepp Hochreiter and Jürgen Schmidhuber “Long Short-Term Memory” In Neural Computation 9.8, 1997, pp. 1735–1780

- [29] Bryan Lim, Sercan Ö Arık, Nicolas Loeff and Tomas Pfister “Temporal fusion transformers for interpretable multi-horizon time series forecasting” In International Journal of Forecasting 37.4 Elsevier, 2021, pp. 1748–1764

- [30] Shereen Elsayed et al. “Do We Really Need Deep Learning Models for Time Series Forecasting?”, 2021 arXiv:2101.02118 [cs.LG]

- [31] Terry J. Lyons “Differential Equations Driven by Rough Paths : Ecole d’Eté de Probabilités de Saint-Flour XXXIV-2004”, École d’Été de Probabilités de Saint-Flour, 1908 Berlin, Heidelberg: Springer Berlin Heidelberg, 2007

- [32] Ilya Chevyrev and Andrey Kormilitzin “A Primer on the Signature Method in Machine Learning”, 2016 arXiv:1603.03788 [stat.ML]

- [33] Terry Lyons and Andrew D. McLeod “Signature Methods in Machine Learning”, 2023 arXiv:2206.14674 [stat.ML]

- [34] Bryan T Kelly, Semyon Malamud and Kangying Zhou “The Virtue of Complexity Everywhere” In Available at SSRN, 2022

- [35] Danica J. Sutherland and Jeff Schneider “On the Error of Random Fourier Features” In Proceedings of the Thirty-First Conference on Uncertainty in Artificial Intelligence, UAI’15 Amsterdam, Netherlands: AUAI Press, 2015, pp. 862–871

- [36] Valentin Haddad, Serhiy Kozak and Shrihari Santosh “Factor timing” In The Review of Financial Studies 33.5 Oxford University Press, 2020, pp. 1980–2018

- [37] Duncan McElfresh et al. “When Do Neural Nets Outperform Boosted Trees on Tabular Data?”, 2023 arXiv:2305.02997 [cs.LG]

- [38] Ravid Shwartz-Ziv and Amitai Armon “Tabular data: Deep learning is not all you need” In Information Fusion 81 Elsevier, 2022, pp. 84–90

- [39] Léo Grinsztajn, Edouard Oyallon and Gaël Varoquaux “Why do tree-based models still outperform deep learning on typical tabular data?” In Advances in Neural Information Processing Systems 35, 2022, pp. 507–520

- [40] Arlind Kadra, Marius Lindauer, Frank Hutter and Josif Grabocka “Well-tuned simple nets excel on tabular datasets” In Advances in neural information processing systems 34, 2021, pp. 23928–23941

- [41] Sercan Ö. Arik and Tomas Pfister “TabNet: Attentive Interpretable Tabular Learning” In Proceedings of the AAAI Conference on Artificial Intelligence 35.8, 2021, pp. 6679–6687 URL: https://ojs.aaai.org/index.php/AAAI/article/view/16826

- [42] George Cybenko “Approximation by superpositions of a sigmoidal function” In Mathematics of control, signals and systems 2.4 Springer, 1989, pp. 303–314

- [43] Anton Maximilian Schäfer and Hans Georg Zimmermann “Recurrent neural networks are universal approximators” In Artificial Neural Networks–ICANN 2006: 16th International Conference, Athens, Greece, September 10-14, 2006. Proceedings, Part I 16, 2006, pp. 632–640 Springer

- [44] Balaji Lakshminarayanan, Alexander Pritzel and Charles Blundell “Simple and scalable predictive uncertainty estimation using deep ensembles” In Advances in neural information processing systems 30, 2017

- [45] Florian Wenzel, Jasper Snoek, Dustin Tran and Rodolphe Jenatton “Hyperparameter Ensembles for Robustness and Uncertainty Quantification” In Neural Information Processing Systems (NeurIPS), 2020 URL: https://papers.nips.cc/paper/2020/hash/481fbfa59da2581098e841b7afc122f1-Abstract.html

- [46] Sheheryar Zaidi et al. “Neural ensemble search for uncertainty estimation and dataset shift” In Advances in Neural Information Processing Systems 34, 2021, pp. 7898–7911

- [47] Donald B. Percival and Andrew T. Walden “Spectral Analysis for Univariate Time Series”, Cambridge Series in Statistical and Probabilistic Mathematics Cambridge University Press, 2020 DOI: 10.1017/9781139235723

- [48] Numerai “Numerai Hedge Fund” (2023, Feb 15) URL: https://numer.ai/data/v4.1

- [49] Numerai “Numerai Hedge Fund” (2023, Sep 6) URL: https://numer.ai/data/v4.2

- [50] Numerai “Numerai Hedge Fund” (2023, Apr 19) URL: https://docs.numer.ai/tournament/correlation-corr

- [51] Numerai “Numerai Hedge Fund” (2023, Aug 29) URL: https://numerai.fund/

- [52] David H. Bailey and Marcos Lopez Prado “Stop-outs under serial correlation and the triple penance rule” In JOURNAL OF RISK 18.2, 2015, pp. 61–93 DOI: 10.21314/JOR.2015.317

- [53] Bryan T. Kelly and Semyon Malamud “The virtue of complexity in machine learning portfolios” In SSRN Electronic Journal, 2021 DOI: 10.2139/ssrn.3984925

- [54] Lifan Zhao, Shuming Kong and Yanyan Shen “DoubleAdapt: A Meta-learning Approach to Incremental Learning for Stock Trend Forecasting” In Proceedings of the 29th ACM SIGKDD Conference on Knowledge Discovery and Data Mining, 2023, pp. 3492–3503

- [55] Trevor Hastie, Andrea Montanari, Saharon Rosset and Ryan J Tibshirani “Surprises in high-dimensional ridgeless least squares interpolation” In Annals of statistics 50.2 NIH Public Access, 2022, pp. 949

- [56] Prasad G. Thoppil et al. “Ensemble forecasting greatly expands the prediction horizon for ocean mesoscale variability” In Communications Earth & Environment 2.1, 2021, pp. 89 DOI: 10.1038/s43247-021-00151-5

- [57] Mohammad Pezeshki, Amartya Mitra, Yoshua Bengio and Guillaume Lajoie “Multi-scale feature learning dynamics: Insights for double descent” In International Conference on Machine Learning, 2022, pp. 17669–17690 PMLR

- [58] Mario Geiger et al. “Jamming transition as a paradigm to understand the loss landscape of deep neural networks” In Physical Review E 100.1 APS, 2019, pp. 012115

- [59] B. Efron and C. Stein “The Jackknife Estimate of Variance” In The Annals of Statistics 9.3 Institute of Mathematical Statistics, 1981, pp. 586–596 DOI: 10.1214/aos/1176345462

- [60] Gail A Carpenter and Stephen Grossberg “Normal and amnesic learning, recognition and memory by a neural model of cortico-hippocampal interactions” In Trends in neurosciences 16.4 Elsevier, 1993, pp. 131–137

- [61] Kun Wang et al. “Elastic gradient boosting decision tree with adaptive iterations for concept drift adaptation” In Neurocomputing 491, 2022, pp. 288–304 DOI: https://doi.org/10.1016/j.neucom.2022.03.038