Kullback-Leibler Divergence and Akaike Information Criterion in General Hidden Markov Models

Abstract

To characterize the Kullback-Leibler divergence and Fisher information in general parametrized hidden Markov models, in this paper, we first show that the log likelihood and its derivatives can be represented as an additive functional of a Markovian iterated function system, and then provide explicit characterizations of these two quantities through this representation. Moreover, we show that Kullback-Leibler divergence can be locally approximated by a quadratic function determined by the Fisher information. Results relating to the Cramér-Rao lower bound and the Hájek-Le Cam local asymptotic minimax theorem are also given. As an application of our results, we provide a theoretical justification of using Akaike information criterion (AIC) model selection in general hidden Markov models. Last, we study three concrete models: a Gaussian vector autoregressive-moving average model of order , recurrent neural networks, and temporal restricted Boltzmann machine, to illustrate our theory.

Keywords AIC, Boltzmann machine, Cramér-Rao lower bound, Fisher information, Hájek-Le Cam theorem, hidden Markov model, Kullback-Leibler divergence, Markovian iterated function system, recurrent neural network.

1 Introduction

Kullback-Leibler (KL) divergence, also called relative entropy, has been widely used in information theory, machine learning, statistics, econometrics, and others. Its applications include information theory ([1]), speech recognition via deep neural networks ([2]), chemical kinetics ([3]), physics ([4]), statistics and econometrics ([5, 6, 7, 8]). Theoretical properties of the KL-divergence and its relationship with the Fisher information matrix have been well established, particularly for models with independent and identically distributed (i.i.d.) observations.

Nonetheless, many real applications now build on more complex hidden Markov models (HMMs) with finite states, or even general hidden Markov models (GHMMs) with general states. The former includes machine learning applications in speech recognition ([9]) and computational biology ([10]), econometric applications with Markov switching models ([11, 12]), Markov switching GARCH models ([13, 14]) and many other applications. The latter includes factorial HMMs ([15]), switching state-space models ([16, 17, 18]) and adversarial models ([19]) in machine learning, (G)ARCH models ([20, 21, 22, 23, 24]) and stochastic volatility models (SVs) ([25, 26, 27]) in statistics and econometrics, and others from various disciplines. It is also known that KL-divergence plays an important role in HMMs and GHMMs. For example, [28] applies KL-divergence for model selection in Markov switching models. [29] and [30] use KL-divergence to detect change points for HMMs, while [31] studies the detection for GHMMs. [32] further provides a numerical computational method via Fredholm integral equations in a two-state HMM. See also [33] and [34], as well as [35] for the more general Rényi entropy in Markov models. This motivates us to have a theoretical investigation of the KL-divergence in GHMMs.

Note that there are many results and mathematical mechanisms for i.i.d. models, but many of them cannot be directly applied to GHMM, or even to HMM. The main reason is that the log likelihood of a HMM or GHMM is not the sum of i.i.d. random variables or even a functional of Markov chains; thus the classical law of large numbers (LLN) approach cannot be directly applied. Instead, [36] applies Kingman’s subadditive ergodic theorem to provide a generalized KL-divergence, while [37] uses an ergodic process to approximate the log likelihood function in a finite-state HMM. [38] applies the Shannon-Breiman-McMillan theorem to have the limit as the KL-divergence in a general-state HMM. However, their results require stationarity for the HMM, and do not characterize the KL-divergence in HMM or GHMM, nor does the Fisher information; hence many asymptotic properties for HMM and GHMM remain uninvestigated, including KL-divergence and its relationship with Fisher information.

To formally explain this phenomenon in details, we first follow the definition in [39] to define the GHMM. Let be a Markov chain on a general state space , with transition probability kernel and stationary probability with respect to a -finite measure on , where denotes the unknown parameter. Let be the observations from to such that with a distribution depending on and , but independent to others. Let be the probability density function (pdf) of given and , with respect to a -finite measure on . Further let be the pdf of given . Note that this setting includes interesting examples such as Markov-switching autoregression models, (G)ARCH models, stochastic volatility models, recurrent neural networks (RNNs) and temporal restricted Boltzmann machine. When is a finite state space and are independent for given , this is the classical hidden Markov model.

For given random observations , the full likelihood is

| (1) | ||||

In addition, denote as the likelihood. Note that in (1) the initial distribution of is taken as the stationary distribution for convenience, indeed any suitable initial distribution works well.

Then, for any two parameters and , the KL-divergence is defined as

| (2) |

where denotes the probability measure when are distributed according to . In addition, the Fisher information under can be defined as

| (3) |

where the superscript denotes the transpose; see the last equation on page 2047 of [39].

When are i.i.d. random variables with pdf , then

| (4) |

is a sum of i.i.d. random variables . Hence, under some regularity conditions, by (2) and the strong law of large numbers (SLLN), we have

| (5) |

where denotes the expectation under . Similarly, for ,

| (6) |

is a sum of i.i.d. random variables , therefore by (3) and SLLN, we have

| (7) |

Finally, with the help of (5) and (7), it is known that as , we have

| (8) |

where denotes the Euclidean norm.

Nevertheless, for HMM and GHMM cases, we do not have (4), which precludes us from directly obtaining (5) through SLLN. Similarly, since we do not have (6), (7) cannot be derived using the same argument. As a consequence, although (8) has been long conjectured in the literature (see, for example, Remark 2 in [40]), a rigorous proof is still lacking.

Note that these difficulties are all highly related to the complex structure of (1). Therefore, in this paper, we use an innovative representation of the log likelihood and its derivatives in GHMM, which gets around this complexity. By such, we provide characterizations of the KL-divergence and Fisher information, and prove the relationship between these two via the corresponding convergence in (8).

Given these newly developed characterizations, we further provide the Cramér-Rao lower bound and Hájek-Le Cam local asymptotic minimax theorem ([41]) for GHMM, which shows that the classical bounds in i.i.d. scenarios remain valid for GHMM. We also show that as in the i.i.d. case, the KL-divergence satisfies the non-negativity and additivity properties. However, it is not convex in general, which is in contrast to the traditional i.i.d. or Markov chain cases for which the KL-divergence is convex. As another application of our results, we further provide a theoretical justification of using Akaike information criterion (AIC) model selection in GHMMs.

The rest of the paper is organized as follows. In Section 2 we present conditions and state main results. Section 3 studies the application to AIC model selection. To illustrate our theoretical results, three concrete models: a Gaussian vector autoregressive-moving average model of order , recurrent neural networks, and temporal restricted Boltzmann machine, are discussed in Section 4. Section 5 concludes. All proofs of theoretical results are given in Appendix.

2 Main Results

We split this section into three parts. Section 2.1 defines notations and states conditions. Section 2.2 presents preliminary results, which show that the log likelihood and the derivatives of the log likelihood can be represented as an additive functional of a Markovian iterated function system (MIFS). Section 2.3 states our main results, which include characterizations of the KL-divergence, Fisher information matrix, and the relationship between these two for a GHMM. Moreover, we show the results relating to the Cramér-Rao lower bound and Hájek-Le Cam local asymptotic minimax theorem.

2.1 Notations and Conditions

Denote as the expectation defined under with initial state and as the expectation defined under with initial state . For any and positive integer , let be the partial derivative with respect to the -th dimension of in some neighborhood of the true value , and let be the corresponding -th partial derivative. In addition, for a given non-negative integer vector , write , , and let denote the -th derivative with respect to in .

The following conditions will be used throughout the rest of this paper.

C1. For a given , the Markov chain is aperiodic, irreducible, and satisfies

with some weight function and . Assume that

| (9) |

and

| (10) |

Since is -finite, there exist pairwise disjoint ’s such that , and . Assume that

| (11) |

Furthermore, let

and assume that there exists such that

| (12) | |||

| (13) |

C2. The true parameter is an interior point of . For all , , and with , the partial derivatives and exist. In addition, for all , and have th-order continuous derivatives in some neighborhood of .

C3. For all with and

and

C4. For all , and ,

for , and

for .

C5.

C6. For any and with ,

Furthermore, let

and assume that there exists such that

Remark 1.

Conditions C1 and C2–C5 are essentially the same as conditions C1 and C2’–C5’ in [39], respectively. The purpose of the additional condition C6, on the other hand, is to extend (9)–(13) in C1 to higher-order derivatives in some neighborhood of . Many commonly used models satisfy these conditions, including Markov switching models, ARMA models, (G)ARCH models as well as stochastic volatility models; see [39] for details. Furthermore, we will check conditions C1–C6 also hold under RNN and temporal restricted Boltzmann machine with specific distributions.

2.2 Preliminary Results

[39] has represented the log likelihood as an additive functional of a MIFS as follows. To be more specific, we consider the function space

Moreover, for , define the random functions and on as

and define the composition of two random functions as

Now, consider

| (14) |

Further denote . Then, we have

| (15) |

where

| (16) |

In other words, is an additive functional of . In addition, [39] shows that forms an ergodic Markov chain, induced by the MIFS based on (14), on the state space . [39] further uses this result to prove the SLLN for the log likelihood. The rate of convergence of to its invariant measure is studied in [42].

The following lemmas extend this idea to the derivatives of . To do so, for any -dimensional non-negative integer vector , define

Now let us consider all derivatives with order or less. Note that for a fixed integer , there are exactly different satisfying . Label all such by , and let .

The first lemma shows that we can construct a MIFS through .

Lemma 1.

Assume conditions C1–C6 hold with some . Then, for any ,

is an aperiodic, -irreducible and Harris-recurrent Markov chain.

See the supplementary for the proof.

The second lemma shows that the derivatives of can be represented as an additive functional of this particular MIFS.

Lemma 2.

Assume conditions C1–C6 hold with some . Then, for any and any -dimensional non-negative integer vector with , there exists function and such that

| (17) |

See the supplementary for the proof.

2.3 Main Results

We will use Lemmas 1 and 2 to evaluate Fisher information, KL-divergence and other properties. However, as these quantities might involve different probability measures as well as evaluated at different , some additional notations are needed to clarify the statement. For , let be the constructed with the evaluated at . In addition, for any , let be the -th component in the Fisher information matrix . Further denote and with being at the -th entry.

Our first theorem shows that the Fisher information matrix of a GHMM can be written as an expectation similar to (7).

Theorem 1.

Assume conditions C1–C6 hold with . Then, we have

| (18) |

where is the stationary distribution of , is the expectation taken when the above induced Markov chain is governed by and has an initial distribution equal to , and

| (19) |

with defined in Lemma 2, and for all ,

Remark 2.

Note that one can link the function to the second derivatives of . See Remark 9 below for details.

Our second theorem shows that the KL-divergence for GHMM can also be written in a form similar to (5), and can be locally approximated by a quadratic function determined by the Fisher information matrix as in (8).

Theorem 2.

Remark 3.

Note that one can link the function to . See Remark 10 below for details.

With the help of (18) and (20), we will prove the following results related to the Cramér-Rao lower bound and the Hájek-Le Cam local asymptotic minimax theorem. The Hájek-Le Cam convolution theorem for a finite state HMM can be found in [44]. For any , let be the space of all estimators of based on , and be the space of all unbiased estimators of based on . Denote as an estimator based on

Theorem 3.

Assume conditions C1–C6 hold with . Then, for any and ,

| (22) |

In addition, assume C1–C6 hold with . Then, for , we have

| (23) |

Remark 4.

Remark 5.

Equations (22) and (23) are similar to the classical case where are i.i.d. random variables. In particular, (23) states that as long as the estimator can shrink to a -neighborhood of , regardless of the constant term, then the square loss is uniformly bounded from below. An interesting phenomenon here is that we still have the same constant in (23) as that in the i.i.d. case. For this GHMM version, however, since we have no characterization of the Fisher information matrix for fixed , the argument requires that goes to infinity to link the mean square error to the Fisher information .

Finally, with the help of (20), we can prove the following properties for KL-divergence in GHMM.

Corollary 1.

Assume conditions C1–C2 hold with . Then, for any ,

-

1.

(Non-Negativity) .

-

2.

(Additivity) Suppose , and for any and , we have for . Then,

where for , is the KL-divergence defined by replacing in (2) by , respectively.

Remark 6.

Note that when is a sequence of i.i.d. finite mixture random variables or a Markov chain, one can additionally prove that is a convex function. However, this is not the case here in general. To see why, let us consider the case in which is a Markov chain. By using an argument similar to Theorem 1 of [46], one can show that

| (25) |

where is the invariant measure of under , and is the expectation when the Markov chain is governed by and is -distributed. By such, the classical argument applying log-sum inequality leads to the convexity of .

This argument, however, does not work for the case where is a HMM. This is because unlike (6), the two expectations in (20) are under different invariant measures, so they cannot be combined as in (6), and the log-sum inequality cannot be applied. This non-convexity becomes a unique feature for HMM that is different from an i.i.d. or Markov chain scenario. Similar non-convexity for the KL-divergence is observed in [47].

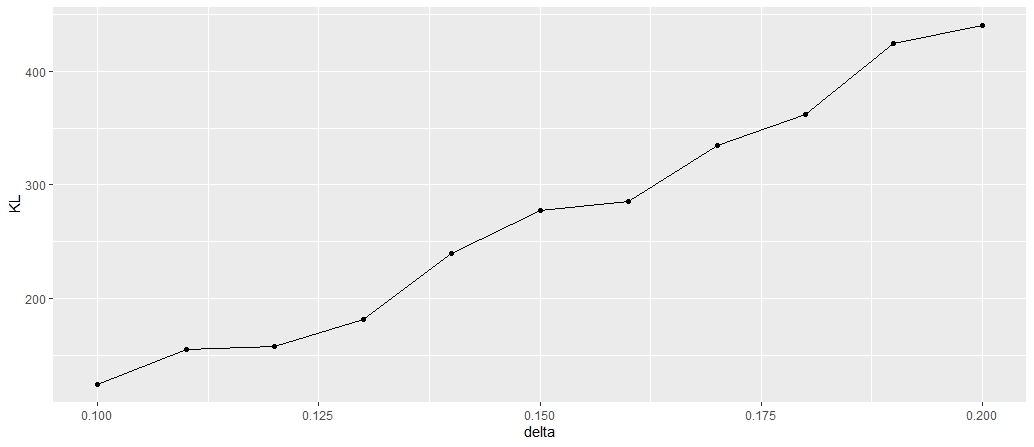

We end this remark by a numerical illustration. Consider a three-state HMM with , for which for all . As for the observations, we assume with , where

Let be the corresponding probability measure with , and be the corresponding probability measure with ranging from to . The computed is presented in Figure 1. As expected, is decreasing when decreases. However, the figure shows that is not convex, as mentioned above.

Remark 7.

The conditions can be slightly relaxed. For example, as Theorems 1–3 and Corollary 1 only involve the neighborhood of , the differentiability assumption in C2 can be relaxed to only instead of all . Also, as one can see in the proof, the second part of C4 is used only to bound the third-order derivatives of in order to obtain the small- term in (21). By such, C4 can be relaxed for the results unrelated to the small- term in (21).

3 AIC Model Selection

In this section, we will use Akaike’s information criterion (AIC) in determining the order of a GHMM. Note that the HMM is defined in a general sense as that in Section 1. To this end, we present an objective procedure for the determination of the order of an ergodic general hidden Markov model with a finite state space. The procedure exploits the asymptotic properties of the likelihood ratios statistics in [43], and the KL-divergence, defined in Theorem 2, for the discrimination between two GHMM distributions.

is called a -order Markov chain if is the smallest non-negative integer such that

In what follows we assume that is an -order Markov chain on a finite state space . It is known that for an -order Markov chain , then forms a Markov chain. Following the definition in Section 1 and (1), is called an -order GHMM. In what follows in this section, we further assume conditions C1-C6 hold for this -order GHMM.

Let be the observations from an -order GHMM such that with a distribution depending on and , but independent to others. Let be the pdf of given and , with respect to a -finite measure on , where with . Furthermore, let be the pdf of given . Denote for , then the full likelihood of this -order GHMM is

| (26) |

where is the stationary distribution of the Markov chain and is the corresponding transition probability kernel. Denote

That is, is the maximum likelihood estimator (MLE) of based on the observations from this -order GHMM. In what follows, we suppose the true value of is . Denote as the Fisher information matrix which corresponds to this -order GHMM. Then, for any we denote

Let be the difference operator on the superscript, for As in [48], we consider the case where . Suppose that is restricted to the parameter space with components of being equal to zero due to the change of order from to for the Markov chain . Without loss of generality, we suppose that the last components of are restricted to be zero when the order of the Markov chain changes from to . Denote the above restricted parameter space as , and let be the MLE of in this restricted parameter space. Moreover, let such that

That is, is the projection of in the space with respect to the metrics defined by . Denote , which is the active dimension of the restricted parameter space . Then, it is easy to see that

where stands for the -th element of . This further implies that

| (27) |

In what follows, we take as the loss function, because it is approximately equal to , which is close to with denoting the KL-divergence between the -order GHMM and the -order GHMM.

Denote

as the ratio of the maximum likelihood given that is from an -order GHMM to that given that is from a -order GHMM. Then

| (28) |

Taking into account the relations

it follows from the Taylor expansions that

| (29) |

with , and

with . Applying the decomposition in (2.2), we write

where the definitions of and can be found in (16). Then, we have

provided is bounded since actually is the MLE of which is asymptotically efficient (cf. Theoreom 2 in [43]). This together with (3) imply that

Similarly, it can be proved that if is bounded,

Thus, it follows from (3) that

| (30) |

where denotes the inner product of and defined by the Fisher information matrix .

By Theorem 2 in [43], we have

Note that geometrically is approximately the projection of into the space of , therefore as long as is bounded, it is true that

and and are asymptotically independent. Note that Theorem 2 of [43] also implies that the standard deviation of the asymptotic distribution of is equal to . Thus, is negligible in comparison with the term if the latter is large enough.

Then, it follows from the above arguments and the equations (27) and (3) that serves as a useful estimator of . That is, the determining the order of a GHMM can be conducted via minimizing the following AIC criterion

| (31) |

by recalling that . Getting rid of the terms which are independent of from the RHS of (31), we arrive at the following AIC criterion for GHMM:

| (32) |

By making use of the same method, it can be shown that for a given -order GHMM, the AIC criterion for selecting the number of hidden states is

| (33) |

where denotes the number of hidden states in the -order GHMM, and denotes the MLE of the parameter in such model. [49] considers AIC model selection for HMM when depends on only.

4 Examples

Example 1.

Gaussian Vector Autoregressive-Moving Average Model.

Consider a Gaussian vector autoregressive-moving average (VARMA) model of order in dimension (see [50]) such that, for all ,

| (34) |

in which and are -by- real-valued matrices with (the -by- identity matrix), and are i.i.d. -dimensional normal random variables with zero mean and covariance matrix . Here, we assume that , and are known, so the unknown parameter can be denoted as

where for any matrix , denotes the vector created by stacking all the columns of on top of each other.

It is known that the VARMA model in (34) can be represented as a linear state space model (LSSM) in various ways, cf. [51]. For example, let , and suppose and satisfying the LSSM

| (35) |

where

and , with being the -by- zero matrix, for all and for all . Then, [51] has shown that the in (1) satisfies the VARMA model in (34); see also [50], [52] and [53].

Since (1) is in the form of LSSM, consider the sample innovation obtained by the following Kalman filter equations:

| (36) |

with given by . Further denote . Then, the log likelihood of the VARMA can be written as

which further implies that

| (37) |

where denotes the Kronecker product. See [50] for details.

To apply Theorems 1 and 2, we need to check conditions C1-C6 hold. Section 6.2 of [39] checks that conditions C1-C6 hold for ARMA. As for LSSM, Section 16.5.1. of [54] shows that C1 (the -uniformity) hold for any dimensional LSSM, therefore by using the same argument, C1 holds for VARMA (34) and (1). By using the normality of , it is straightforward to check conditions C2-C6 hold.

Now, [50] has shown that, when , the limiting distribution of is the same as the distribution of . In addition, since both and are Gaussian, the covariance matrix of converges to that of ; in other words, , which is independent to . By such, the first term in (1) goes to zero as , and therefore,

| (38) |

In addition, it is known that as for some finite constant matrix (depending on ). Therefore the asymptotic version of (36) becomes

| (39) |

Then by (38), we have

| (40) |

Now, by (39), we have

| (41) |

which indicates that forms a Markov chain. Moreover, note that , which implies

| (42) |

In other words, is a function of . Therefore, Theorem 1 essentially shows that is stationary under , and therefore

| (43) |

The result (43) is the same as that in [50], in which they use to denote a random variable with distribution as the limiting distribution of as . Here we derive the Fisher information (43) from the invariant probability measure of the enlarged Markov chain point of view. The Fisher information for a general LSSM can be found in [55].

Note that the result above is made possible due to the fact that, if follows the LSSM with parameter , then under , the limiting distribution of is the same as . If we want to find a representation of the KL-divergence, then we need to evaluate the limiting distribution of under for . This is due to that the second expectation in (20) involves and under with . Instead, (21) in Theorem 2 provides a local approximation of the KL-divergence in terms of Fisher information. Moreover, we provide a theoretical justification of using AIC model selection criterion in (33) to choose in (34) and (1). A computational method of the KL-divergence and AIC model selection for LSSM can be found in [56].

Example 2.

Recurrent Neural Networks.

To start with, we consider the following linear recurrent neural network (RNN) as

| (44) |

where , with can be any highly flexible function such as neural networks. P-a.s., is a sequence of i.i.d. random variables, and is independent of for all .

To illustrate the GHMM approach for the linear RNN. By using (44) as the output model for , the linear RNN updates its hidden state using the recurrence equation:

| (45) |

where and are constants.

As noted in [42] that the linear RNN model (44) and (45) can be regarded as the celebrated GARCH model when and in (44), and is replaced by in (45). However, and , defined in (44), can be nonlinear functions of in general.

To have an explicit computation of the Fisher information and KL-divergence, we consider a specific form of (44), a simple GARCH model (see [21]), as follows:

where , and are constants with , and are i.i.d. standard normal random variables with independent of .

Section 6.3 of [39] has checked that conditions C1-C6 hold for the GARCH model. As for the linear RNN, condition C1 (the -uniformity) can be found in Section 16.5.1 of [54] using the state space representation. Conditions C2-C6 hold due to the normality assumption of . Therefore Theorems 1 and 2 can be applied.

Denote . Note that the log likelihood function of GARCH model can be expressed as

| (46) |

which further implies

| (47) |

See [57] for details. Indeed, Theorem 1 essentially indicates that

| (48) |

where is the stationary distribution of .

We can further link (48) to the formula in [57]. For illustration, let us only consider the partial derivative with respect to . A direct computation shows that

(See also equation (7) in [58].) In addition, under , using the classical procedure of extending the Markov chain to a doubly infinite stationary sequence (see, for example, Section 4 of [37]), we have

| (49) |

which has the same distribution as as . Combining with (47) and (48), we have

| (50) |

which is consistent to the closed-form expression provided in (17) of [57].

Similar approach works for the KL-divergence. Let for , and denote be the evaluated under . Since (46) already writes the log likelihood as an additive functional, Theorem 2 essentially means that

| (51) |

To further link (51) with the doubly infinite stationary sequence, note that for , a direct computation leads to

and so, by stationarity,

Remark 8.

As demonstrated in (50), the invariant measure in Theorem 1 actually incorporates the data of the entire past history. This can be viewed as follows: the invariant probability measure represents the limiting behaviour of the derivatives of , which is equivalent to the limiting behaviour of the derivatives of when the process is stationary. Similar situation holds for in Theorem 2.

To analyze the linear RNN (44) and (45), we apply the same method in [42] as follows: let be the Markov chain on . Denote and let . Let be a -by- matrix, written as

| (52) |

Note that are random matrices driven by the Markov chain .

Let . Then we have the following state space representation of the linear RNN (44) and (45): is a Markov chain govern by

| (53) |

and , the observed random quantity, is a non-invertible function of .

By Theorem 1 in [42], a sufficient condition for stability is , where , with as the stationary distribution of the Markov chain . Condition C1 (the -uniformity) can be found in Section 16.5.1 of [54] using the state space representation. Conditions C2–C6 in Theorems 1 and 2 hold under the normality assumption in (44). By using a similar method as that in (43), we have a representation of the Fisher information matrix.

In general, a RNN can take as input a variable-length sequence by recursively processing each symbol while maintaining its internal hidden state . At each time step , the RNN reads the symbol and updates its hidden state by

| (54) |

where is a deterministic non-linear transition function, and is the parameter of .

For a given RNN model’s sequence, by parameterizing a factorization of the joint sequence probability distribution as a product of conditional probabilities, we have

| (55) | |||||

where is a function that maps the RNN hidden state to a probability distribution over possible outputs, and is the parameter of .

As noted in [59], given a set of training sequences , the parameters in RNN can be estimated by minimizing the following cost function,

| (56) |

where is a predefined divergence measure between and , such as Euclidean distance or KL-divergence (or cross entropy). Theorem 2 indicates that the KL-divergence is well-defined in terms of the stationary distribution of the enlarged Markov chain. This provides a theoretical foundation of using KL-divergence as a cost function in RNN. For the regularization issue, one possible method is the celebrated AIC model selection method in (32) and (33), in which we present a theoretical justification of using this method in RNN.

Example 3.

Temporal Restricted Boltzmann Machine.

A Boltzmann machine is a network with stochastic binary units, which contains a set of visible units and a set of hidden units . The energy of is defined as

| (57) |

where are the parameters: represent visible-to-hidden, visible-to-visible, and hidden-to-hidden symmetric interaction terms. The diagonal elements of and are set to . The probability that the model assigns to a visible vector is:

| (58) | ||||

| (59) |

where denotes unnormalized probability, and is the partition function (normalizing constant).

Setting both and recovers the well-known restricted Boltzmann machine (RBM) model, cf. [60]. An RBM defines a probability distribution over pairs of vectors, and by the equation

| (60) | ||||

| (61) |

where is a vector of bias for the visible vector, is a vector of bias for the hidden vector, is the matrix of connection weights, and is the partition function (normalizing constant).

Next, we consider the temporal restricted Boltzmann machine (TRBM), cf. [61]. In its simplest form, the TRBM can be viewed as a hidden Markov model (HMM) with an exponentially large state space that has an extremely compact parameterization of the transition and the emission probabilities. Denote . The TRBM defines a probability distribution by the equation

| (62) |

which has the form as the probability defined in (1). Here can be any suitable initial distribution of . The conditional distribution is that of an RBM, whose biases for are a function of . That is

| (63) |

where and are as in Equation (60), and is the weight matrix of the connection from to , making be the bias of RBM at time .

Now we need to check conditions C1–C6 in Theorems 1 and 2 hold under model assumptions in (62) and (63). First, we note that the state space of is , which is finite (although exponentially large); this implies the uniform ergodicity of the underlying Markov chain, and therefore leads that C1 holds. As for the other conditions, note that since the state space is finite, all the supremum or integration over in C2-C6 are finite. Furthermore, the state space of is , which is finite; this implies that the moment generating function of exists. In addition, since the log of logistic function is infinite differentiable in any local neighbourhood of , the supremum over in C2-C6 is finite. This leads that C2-C6 hold.

As noted in [62], variational learning has the nice property that in addition to trying to maximize the log likelihood of the training data, it tries to find parameters that minimize the KL-divergences between the approximating and true posteriors. Theorem 2 indicates that the KL-divergence is well-defined in terms of the stationary distribution of the enlarged Markov chain. This provides a theoretical justification of using the KL-divergence as a cost function in stochastic gradient descent of TRBM. For the regularization issue, one possible method is the celebrated AIC model selection method in (32) and (33), in which we present a theoretical justification of using this method in TRBM.

However, calculation of the KL-divergence as well as Fisher information in TRBM and RNN are not straightforward. This is due to that, unlike the i.i.d. case, the limits in (2) and (3) for TRBM have no explicit form. Traditionally, it is numerically computed by simulating long string of TRBM to approach the limits. Here, thanks to Theorems 1 and 2, we can use Monte Carlo method and other computational technique to evaluate the expectations in (18) and (20) instead. It is worth mentioning that evaluating these expectations are still not straightforward, Theorems 1 and 2 provide a possible tool for numerical computation via various statistical computation technique.

5 Conclusion

In this paper, we present explicit characterizations of the KL-divergence and Fisher information for GHMMs, and derive the relationship between these two important quantities. The results are based on a representation of the log likelihood and its derivatives as an additive functional of a MIFS, which allows one to study the behavior of the log likelihood using SLLN and other related results. By using these results, we also present the Cramér-Rao lower bound and Hájek-Le Cam local asymptotic minimax theorem under GHMMs. The characterization further shows that the KL-divergence in HMM is not convex in general, which is different from the traditional i.i.d. or Markov chain scenario. Moreover, we provide a theoretical justification of using AIC model selection in GHMM with finite state space.

It is expected that this representation device will be beneficial for further studies in GHMMs such as model selection and the generalized method of moments in stochastic volatility models, exponential tilting estimators and quasi-maximum likelihood estimators in GHMMs, regularization in RNN with KL-divergence (relative entropy) as the penalized term and other related topics.

References

- [1] C. Aghamohammadi, S. P. Loomis, J. R. Mahoney, and J. P. Crutchfield, “Extreme quantum memory advantage for rare-event sampling,” Physical Review X, vol. 8, no. 1, p. 011025, 2018.

- [2] D. Yu, K. Yao, H. Su, G. Li, and F. Seide, “KL-divergence regularized deep neural network adaptation for improved large vocabulary speech recognition,” in 2013 IEEE International Conference on Acoustics, Speech and Signal Processing. IEEE, 2013, pp. 7893–7897.

- [3] K. M. Hangos, “Engineering model reduction and entropy-based Lyapunov functions in chemical reaction kinetics,” Entropy, vol. 12, no. 4, pp. 772–797, 2010.

- [4] C. Beck, “Generalised information and entropy measures in physics,” Contemporary Physics, vol. 50, no. 4, pp. 495–510, 2009.

- [5] H. White, “Maximum likelihood estimation of misspecified models,” Econometrica, vol. 50, pp. 1–26, 1982.

- [6] C. Gourieroux, A. Monfort, and A. Trognon, “Pseudo maximum likelihood methods: Theory,” Econometrica, vol. 52, pp. 681–700, 1984.

- [7] Y. Kitamura and M. Stutzer, “An information-theoretic alternative to generalized method of moments estimation,” Econometrica, vol. 65, no. 4, pp. 861–874, 1997.

- [8] G. W. Imbens, R. H. Spady, and P. Johnson, “Information theoretic approaches to inference in moment condition models,” Econometrica, vol. 66, pp. 333–357, 1998.

- [9] B. H. Juang and L. R. Rabiner, “Hidden Markov models for speech recognition,” Technometrics, vol. 33, no. 3, pp. 251–272, 1991.

- [10] J. C. Marioni, N. P. Thorne, and S. Tavaré, “BioHMM: a heterogeneous hidden Markov model for segmenting array CGH data,” Bioinformatics, vol. 22, no. 9, pp. 1144–1146, 2006.

- [11] J. D. Hamilton, “A new approach to the economic analysis of nonstationary time series and the business cycle,” Econometrica, vol. 57, no. 2, pp. 357–384, 1989.

- [12] L. E. Calvet and A. J. Fisher, “Forecasting multifractal volatility,” Journal of Econometrics, vol. 105, pp. 27–58, 2001.

- [13] J. Cai, “A Markov model of switching-regime ARCH,” J. Business Econom. Statist., vol. 12, pp. 309–316, 1994.

- [14] J. D. Hamilton and R. Susmel, “Autoregressive conditional heteroskedasticity and changes in regime,” Journal of Econometrics, vol. 64, pp. 307–333, 1994.

- [15] Z. Ghahramani and M. I. Jordan, “Factorial hidden Markov models,” Machine Learning, vol. 29, no. 2, pp. 245–273, 1997.

- [16] C. J. Kim, “Dynamic linear models with Markov-switching,” Journal of Econometrics, vol. 60, pp. 1–22, 1994.

- [17] C. J. Kim and C. R. Nelson, “Business cycle turning points, a new coincident index, and tests of duration dependence based on a dynamic factor model with regime switching,” Review of Economics and Statistics, vol. 80, pp. 188–201, 1998.

- [18] Z. Ghahramani and G. E. Hinton, “Variational learning for switching state-space models,” Neural Computation, vol. 12, no. 4, pp. 831–864, 2000.

- [19] I. Goodfellow, J. Pouget-Abadie, M. Mirza, B. Xu, D. Warde-Farley, S. Ozair, A. Courville, and Y. Bengio, “Generative adversarial nets,” in Advances in Neural Information Processing Systems, 2014, pp. 2672–2680.

- [20] R. F. Engle, “Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation,” Econometrica, vol. 50, no. 4, pp. 987–1007, 1982.

- [21] T. Bollerslev, “Generalized autoregressive conditional heteroskedasticity,” Journal of Econometrics, vol. 31, no. 3, pp. 307–327, 1986.

- [22] J. Fan and Q. Yao, Nonlinear time series. Springer series in statistics. Springer New York, 2003.

- [23] P. Hall and Q. Yao, “Inference in ARCH and GARCH models with heavy–tailed errors,” Econometrica, vol. 71, no. 1, pp. 285–317, 2003.

- [24] C. Francq and J.-M. Zakoïan, “Strict stationarity testing and estimation of explosive and stationary generalized autoregressive conditional heteroscedasticity models,” Econometrica, vol. 80, no. 2, pp. 821–861, 2012.

- [25] P. K. Clark, “A subordinated stochastic process model with finite variance for speculative prices,” Econometrica, vol. 41, no. 1, pp. 135–155, 1973.

- [26] S. Taylor, Modeling Financial Time Series. John Wiley & Sons, Great Britain, 1986.

- [27] O. E. Barndorff-Nielsen and N. Shephard, “Power and bipower variation with stochastic volatility and jumps,” Journal of Financial Econometrics, vol. 2, no. 1, pp. 1–37, 2004.

- [28] A. Smith, P. A. Naik, and C.-L. Tsai, “Markov-switching model selection using Kullback–Leibler divergence,” Journal of Econometrics, vol. 134, no. 2, pp. 553–577, 2006.

- [29] C. D. Fuh, “SPRT and CUSUM in hidden Markov models,” The Annals of Statistics, vol. 31, pp. 942–977, 2003.

- [30] E. Andreoua and E. Ghysels, “Quality control for structural credit risk models,” Journal of Econometrics, vol. 146, pp. 364–375, 2008.

- [31] C. D. Fuh, “Asymptotically optimal change point detection for composite hypothesis in state space models,” IEEE Transactions on Information Theory, vol. 67, pp. 485–505, 2021.

- [32] C. D. Fuh and Y. J. Mei, “Quickest change detection and Kullback-Leibler divergence for two-state hidden Markov models,” IEEE Transactions on Signal Processing, vol. 63, no. 18, pp. 4866–4878, 2015.

- [33] A. N. Gorban, P. A. Gorban, and G. Judge, “Entropy: the Markov ordering approach,” Entropy, vol. 12, no. 5, pp. 1145–1193, 2010.

- [34] N. F. Travers, “Exponential bounds for convergence of entropy rate approximations in hidden Markov models satisfying a path-mergeability condition,” Stochastic Processes and their Applications, vol. 124, no. 12, pp. 4149–4170, 2014.

- [35] M. Obremski and M. Skorski, “Complexity of estimating Rényi entropy of Markov chains,” in 2020 IEEE International Symposium on Information Theory (ISIT). IEEE, 2020, pp. 2264–2269.

- [36] B. G. Leroux, “Consistent estimation of a mixing distribution,” Annals of Statistics, vol. 20, no. 3, pp. 1350–1360, 1992.

- [37] P. J. Bickel, Y. Ritov, and T. Ryden, “Asymptotic normality of the maximum-likelihood estimator for general hidden Markov models,” Annals of Statistics, vol. 26, no. 4, pp. 1614–1635, 1998.

- [38] R. Douc, E. Moulines, J. Olsson, and R. V. Handel, “Consistency of the maximum likelihood estimator for general hidden Markov models,” Annals of Statistics, vol. 39, no. 1, pp. 474–513, 2011.

- [39] C. D. Fuh, “Efficient likelihood estimation in state space models,” Annals of Statistics, vol. 34, pp. 2026–2068. Corrigendum in 38, 1279–1285, (2010), 2006.

- [40] ——, “On Bahadur efficiency of the maximum likelihood estimator in hidden Markov models,” Statistica Sinica, vol. 14, pp. 127–154, 2004.

- [41] A. Van der Vaart, “The statistical work of Lucien Le Cam,” Annals of Statistics, vol. 30, no. 3, pp. 631–682, 2002.

- [42] C. D. Fuh, “Asymptotic behavior for Markovian iterated function systems,” Stochastic Processes and their Applications, vol. 138, pp. 186–211, 2021.

- [43] C. D. Fuh and T. Pang, “Asymptotic behavior of the maximum likelihood estimator for general Markov switching models,” Statistica Sinica, 2022 (To appear, doi:10.5705/ss.202021.0336).

- [44] P. J. Bickel and Y. Ritov, “Inference in hidden Markov models i: Local asymptotic normality in the stationary case,” Bernoulli, vol. 2, no. 3, pp. 199–228, 1996.

- [45] A. Van der Vaart, Asymptotic Statistics. Cambridge University Press, 2000, vol. 3.

- [46] Z. Rached, F. Alajaji, and L. L. Campbell, “The Kullback-Leibler divergence rate between Markov sources,” IEEE Transactions on Information Theory, vol. 50, no. 5, pp. 917–921, 2004.

- [47] M. Vidyasagar, “Kullback-Leibler divergence rate between probability distributions on sets of different cardinalities,” in 49th IEEE Conference on Decision and Control (CDC). IEEE, 2010, pp. 948–953.

- [48] H. Akaike, “Information theory and an extension of the maximum likelihood principle,” in Proceeding of the Second International Symposium on Information Theory, 1973, pp. 267–281.

- [49] S. Yonekuraa, A. Beskosa, and S. S. Singhb, “Asymptotic analysis of model selection criteria for general hidden Markov models,” Stochastic Processes and their Applications, vol. 132, pp. 164–191, 2021.

- [50] A. Klein, G. Mélard, and A. Saidi, “The asymptotic and exact Fisher information matrices of a vector ARMA process,” Statistics & probability letters, vol. 78, no. 12, pp. 1430–1433, 2008.

- [51] A. C. Harvey and G. D. Phillips, “Maximum likelihood estimation of regression models with autoregressive-moving average disturbances,” Biometrika, vol. 66, no. 1, pp. 49–58, 1979.

- [52] J. Pearlman, “An algorithm for the exact likelihood of a high-order autoregressive-moving average process,” Biometrika, vol. 67, no. 1, pp. 232–233, 1980.

- [53] E. J. Hannan and M. Deistler, The statistical theory of linear systems. SIAM, 2012.

- [54] S. P. Meyn and R. L. Tweedie, Markov chains and stochastic stability. Springer Science & Business Media, 2012.

- [55] A. Klein and H. Neudecker, “A direct derivation of the exact Fisher information matrix of Gaussian vector state space models,” Linear Algebra and its Applications, vol. 321, no. 1-3, pp. 233–238, 2000.

- [56] T. Bengtsson and J. E. Cavanaugh, “An improved Akaike information criterion for state-space model selection,” Computational Statistics & Data Analysis, vol. 50, no. 10, pp. 2635–2654, 2006.

- [57] J. Ma, “A closed-form asymptotic variance-covariance matrix for the quasi-maximum likelihood estimator of the GARCH (1, 1) model,” Available at SSRN 889461, 2008.

- [58] G. Fiorentini, G. Calzolari, and L. Panattoni, “Analytic derivatives and the computation of GARCH estimates,” Journal of applied econometrics, vol. 11, no. 4, pp. 399–417, 1996.

- [59] R. Pascanu1, C. Gulcehre1, K. Cho, and Y. Bengio, “How to construct deep recurrent neural networks,” ICLR, 2014.

- [60] G. Hinton and R. Salakhutdinov, “Reducing the dimensionality of data with neural networks,” Science, vol. 313, no. 5786, p. 504–507, 2006.

- [61] H. Sutskever, G. E. Hinton, and T. W. Graham, “The recurrent temporal restricted Boltzmann machine,” In NIPS, 2008.

- [62] R. Salakhutdinov and G. E. Hinton, “Deep Boltzmann machines,” Proceedings of the 12th International Conference on Artificial Intelligence and Statistics (AISTATS), 2009.

- [63] T. S. Ferguson, A Course in Large Sample Statistics. Routledge, Boca Raton, 2017.

- [64] A. B. Tsybakov, Introduction to Nonparametric Estimation. Springer Science & Business Media, 2008.

- [65] J. L. Jensen, “On some problems in the article efficient likelihood estimation in state space models,” Annals of Statistics, vol. 38, no. 2, pp. 1279–1281, 2010.

Appendix A Appendix: Proofs of the Main Results

As Lemmas 1 and 2 are almost the same as Lemmas 3 and 5, respectively, of [43] for a two-layer HMM, here we give proofs of these two lemmas in the supplementary for completeness. By using these two lemmas, we first prove Theorems 1 and 2 in Sections A.1 and A.2, respectively. Then we prove Theorem 3 and Corollary 1 in Section A.3 based on Theorems 1 and 2.

A.1 Proof of Theorem 1

To prove Theorem 1, we only need to prove the following lemma:

Lemma 3.

Proof.

Remark 9.

One can further link the function with the second order derivatives of . Define

| (66) |

Then, by (17), we have

and so we have

A.2 Proof of Theorem 2

To prove Theorem 2, we extend the definition of to with . Note that Lemma 1 also holds for ; see [39]. Thus, we can define as the stationary distribution of the induced Markov chain .

Proof of Theorem 2.

For simplicity, we prove the case with and ; the general case can be proved similarly.

First, it is easy to check that (17) also holds for , then we have

| (67) |

Taking on both sides of (A.2), then by Lemma 1, (17), and the SLLN for Markov random walks in [54], we have

which completes the proof for (20).

For the first term on the RHS of (A.2), by an argument similar to the proof of Theorem 1, we have

| (70) |

At the meantime, we also have due to the fact that is the likelihood under . Moreover,

| (71) |

Combining (70) and (71), we prove that the first term goes to zero -a.s.

Remark 10.

A.3 Proofs of Theorem 3 and Corollary 1

Proof of Theorem 3.

Let us begin with (22). For any fixed , the classical multivariate Cramér-Rao lower bound gives

| (74) |

where is the Fisher information based on . By using the same argument as in the proof of Theorem 1, we have

| (75) |

Let us now turn to (23). Denote as the probability distribution of under . Then, by Le Cam’s method with squared error loss ([64], Chapter 2), we have

| (76) |

where denotes the total variation distance. In addition, for any probability distribution and , Pinsker’s inequality ([64], Lemma 2.5(i)) states that , where is the KL-divergence between and . By such, we have

| (77) |

Proof of Corollary 1.

For the non-negativeness, note that (20) is obtained through SLLN for Markov random walks applied to (2), by which we also have

However, by Gibb’s inequality, we have , so the non-negativeness follows.

The additivity, on the other hand, is a direct consequence of (2) and the fact that for and all . ∎

Remark 11.

Supplementary

Kullback-Leibler Divergence and AIC

in General Hidden Markov Models

Cheng-Der Fuh, Chu-Lan Michael Kao and Tianxiao Pang

Before proving Lemma 1, we need the following definitions. Since we will differentiate , we need to investigate how the differential operator interacts with the operator . Recall and defined in the first paragraph of Section 2.2. Note that for any two given random functions and , and any , by conditions C1–C6 and the dominated convergence theorem, we have

| (80) |

and

By such, we have . Moreover, for given and , let denote the componentwise addition of the vectors. Then, similar to (A.3), we have

Therefore, we have

| (81) |

Hence, if for all , then through an argument similar to that in the proof of Lemma 3 in [39] (with the condition C1 within replaced by our condition C6), we have for all . In addition, by C2 and C3, we have for all .

We are now ready to prove Lemma 1.

Proof of Lemma 1.

First, based on the argument above, we have . This means that is a stochastic process on .

To see that is a MIFS, let us investigate the dynamics of . Note that for any ,

| (82) |

Hence, we can define a -by- matrix form , with each defined as

| (83) |

In addition, for each -by- -valued matrix form , and each -dimensional -valued vector , we define

| (84) |

Then by (A.3), we have , and thus

| (85) |

where with

More importantly, since , and by (83), the value of is determined solely by , we know that the value of is determined solely by . In addition, since the distribution of is based on and , and is a Markov chain, is Markovian, as desired.

Remark 12.

To illustrate (85), let , i.e., is one-dimensional. In this case, and we can simply label all by natural order such that , the vector of the first -th derivatives. Then for any , we have

where . Therefore with

| (86) |

where denotes the zero function in .

Remark 13.

Note that in (83) and in (85) are -valued, other than the traditional -valued matrix and vector, respectively. To illustrate this phenomenon, we consider a -state HMM with one-dimensional parameter case; then in (86) is a -by- matrix form with each element being a -by- matrix (with being a -by- zero matrix). In the same manner, although the operator defined in (84) appears to be traditional matrix multiplication, it is different in that the multiplication within each component is replaced by . Nevertheless, the essential idea is to introduce a matrix form for , which can be used to show that it forms an ergodic Markov chain via (85).

Remark 14.

The critical innovation in this construction is that one needs to consider all derivatives with order equals or less than in order to have a Markovian structure. The reason is that, as shown in (A.3), the iterated representation of involves all and with . This is why one will need to consider instead of .

Note that this makes the approach considerably different from previous studies on HMM such as [37], who study only the second derivatives of when investigating the Fisher information matrix. We, on the other hand, study all derivatives with order being equal to or less than two when doing such investigation.

It is worth mentioning that the feature of getting a neat form in (85) is based on a matrix representation (83) for all partial derivatives up to the -th order. This largely helps us to obtain the result in Lemma 1.

Before proving Lemma 2 for general , we present a specific form of the first and second order partial derivatives of the log likelihood function as follows. For , note that we have

for any . Therefore

| (87) |

That is, the first order derivative of the log likelihood function can be rewritten as an additive functional of the Markov chain .

To represent the second order partial derivative of the log likelihood, for , let us write such that . Then, we have

| (88) |

where

| (89) |

and

That is, the second order derivative of the log likelihood function can also be rewritten as an additive functional of the Markov chain .

Proof of Lemma 2.

We proved the lemma by mathematical induction as follows. As stated in (A.3), such and exist for all . Now suppose and exist for all . Then, when , take and such that and . By induction assumption, and exist, therefore we have

Moreover, as shown in (A.3), and involve the derivatives only up to the order of , so and involve the derivatives only up to the order of . In other words, they are functions of as they consist of all derivatives up to the order of . Thus, such and exist for all , which completes the proof. ∎