Adjusting for time-varying treatment switches

in randomized clinical trials:

the danger of extrapolation and how to avoid it

Correspondence: hege.michiels@ugent.be

Abstract

When choosing estimands and estimators in randomized clinical trials, caution is warranted- as intercurrent events, such as - due to patients who switch treatment after disease progression, are often extreme. Statistical analyses may then easily lure one into making large implicit extrapolations, which often go unnoticed. We will illustrate this problem of implicit extrapolations using a real oncology case study, with a right-censored time-to-event endpoint, in which patients can cross over from the control to the experimental treatment after disease progression, for ethical reasons. We resolve this by developing an estimator for the survival risk ratio contrasting the survival probabilities at each time if all patients would take experimental treatment with the survival probabilities at those times if all patients would take control treatment up to time , using randomization as an instrumental variable to avoid reliance on no unmeasured confounders assumptions. This doubly robust estimator can handle time-varying treatment switches and right-censored survival times. Insight into the rationale behind the estimator is provided and the approach is demonstrated by re-analyzing the oncology trial.

Keywords: Causal inference, Estimand, Hypothetical estimand, Instrumental variable, Treatment switching

1 Introduction

Since the publication of the addendum of the ICH E9 guideline [19], the choice of estimands for treatment efficacy in the presence of intercurrent events has received more attention. The addendum is definitely a step in the right direction, as it emphasizes the importance of estimating an effect that answers the clinical question of interest. However, so far, relatively little attention has been paid to criteria on the basis of which to choose an estimand, which estimators can be used for it, and the assumptions on which they rely. Caution is nonetheless warranted when choosing estimands and estimators, as intercurrent events, such as - patients who switch treatment after disease progression, are often extreme. Therefore, statistical analyses may easily lure one into making large implicit extrapolations. In this paper, we will illustrate this problem using an oncology case study performed by Janssen Pharmaceuticals and propose solutions.

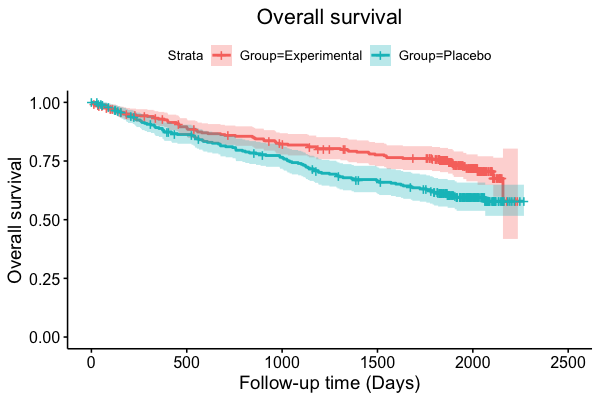

In oncology trials, it is common that patients randomized to the control group can cross over to the experimental group during the trial [14, 20, 21, 24], typically after disease progression, defining a second line treatment [13]. It can also occur due to changes in the treatment guidelines during the trial [49]. For example, in the HELIOS trial [11] (NCT01611090), performed by Janssen Pharmaceuticals, 578 patients with relapsed/ refractory chronic lymphocytic leukemia/small lymphocytic lymphoma without deletion 17p were randomized 1:1 to 420mg daily ibrutinib or placebo plus 6 cycles of bendamustine plus rituximab (BR), followed by ibrutinib or placebo alone. Randomization was stratified by purine analog refractory status (failure to respond or relapse in 12 months) and prior lines of therapy (1 line versus 1 line). Upon disease progression, patients from the placebo plus BR arm were allowed to cross over to ibrutinib, as an ethical requirement to offer experimental treatment to all. The median follow-up time was 63.7 months. At the final 5-year analysis, the intention-to-treat effect on the overall survival endpoint showed a significant effect from ibrutinib plus BR versus placebo plus BR (HR 0.611 95% CI [0.455; 0.822]), despite crossover in 63.3% of the control patients. These kinds of scenarios with large proportions of treatment switching are not uncommon (e.g. [31, 9, 11, 7, 42]).

While patients may benefit from changing treatment, it complicates the interpretation of the intention-to-treat (ITT) or treatment policy analysis [14], which contrasts the treatment groups as randomized. In particular, the magnitude of the ITT effect might have limited relevance as it compares immediate experimental treatment with delayed experimental treatment [14]. However, adjusting for crossover is challenging as oncology trials often have complex designs, with different treatment changes at different points that may occur over time [14]. Moreover, a diversity of patient journeys is expected in oncological trials as patients can discontinue treatment as a result of an adverse reaction, start a new anticancer regimen before observing the endpoint of interest or die while on treatment [6]. In addition, whether it is useful to adjust for treatment switches depends on the clinical questions of interest, which are not always straightforward to define. For example, if interest lies in the comparison of the effect of the two treatment policies implemented in the trial, then an intention-to-treat (ITT) or treatment policy estimand is ideal. However, a decision problem might also require an evaluation of what would have happened in the study if there were no treatment changes, corresponding to a hypothetical estimand. In general, it is important to define treatment switches clearly and specify which treatment changes one wishes to adjust for [14].

Different estimands and estimators have been used to correct for crossover as the treatment policy estimand is typically diluted in these settings [23, 24, 30, 46]. Traditional methods include removing switchers from the analysis, i.e. estimating a per-protocol effect, censoring patients at the time of crossover, or modeling the treatment as a time-varying covariate [13, 49]. These methods are often used but are prone to selection bias as patients who cross over and those who do not are generally not comparable in terms of the survival times one would observe if patients stayed on the assigned treatment [49]. These methods should not be considered as providing conclusive evidence as they give up on the balance offered by randomization [22].

In the HELIOS trial, crossover does not reflect clinical practice as the experimental treatment was not yet approved at the time of conducting the trial. Therefore, according to Manitz et al. [26], the analysis should ideally target a hypothetical estimand [19], quantifying the treatment effect if none of the patients had switched treatment. In this paper, we will focus on the estimation of this hypothetical estimand.

Several estimators have been developed to estimate hypothetical estimands. For example, g-estimation methods under rank preserving structural failure time models (RPSFTMs) can be used to estimate the treatment effect under perfect compliance with the assigned treatment. These methods rely on randomization as an instrumental variable [14, 45], thus assuming that (i) it is associated with the treatments actually taken, (ii) it does not share a common cause with the survival times, and (iii) it only affects the survival times through treatments actually taken. These conditions are expected to hold in a double-blinded randomized trial and will be formally introduced later on in the paper. Instrumental variable methods succeed to estimate the average effect of the treatments actually taken on the outcome, regardless of whether we measured the (time-varying) confounders between treatment and outcome by explicitly exploiting the randomization of study arms [17]. G-estimation methods for RPSFTMs rely on those instrumental variable assumptions and additionally on a common treatment effect assumption that the treatment effect received in the experimental group does not differ from the treatment effect received by control patients who cross over to the experimental treatment. A major limitation of these methods is that the handling of administrative censoring requires artificially censoring the observed event times for some patients. A further key concern is that it is vulnerable to extrapolation due to the parametric nature of the model. In particular, it is assumed that the experimental treatment extends the underlying survival by a constant amount, regardless of when the treatment is given [46].

The inverse probability of censoring weights (IPCW) method [37] instead censors patients at the time of crossover and reweights the remaining records to remove selection bias. It does not suffer from the aforementioned disadvantages. However, it relies on the assumption that, at each time, there are no systematic differences between those who switch and those who do not, conditional on measured variables, i.e. there should be no unmeasured confounding between crossover and the outcome [14]. Often only baseline covariates are included in the IPCW analysis, violating this assumption if switching is based on time-varying confounders like disease progression, as is nearly always the case. In IPCW analyses, it is therefore essential to include disease progression as a time-varying predictor in the inverse probability weights. Even when this is done the IPCW estimator shows erratic behavior in case of perfect prediction for crossover. In that case it can suffer from so called positivity violations [14] as there are no similar patients, in terms of the measured confounders, who cross over and who do not. In that case certain subgroups, defined by the measured confounders, would always cross over to experimental treatment if assigned to the control arm. Such positivity violations are common with treatment crossover because study protocols may indicate when, based on measured confounders, patients should cross over, and are problematic as they can lead to significant bias, large variance and invalid inference [33, 39]. Violations of this assumption in inverse weighting analyses will typically be reflected in large weights and are therefore generally easy to diagnose. However, this can go unnoticed when weights are truncated. In addition, imputation strategies hide this problem by making implicit extrapolations [44].

In the final analysis of the HELIOS trial, only an intention-to-treat estimand was considered but corrections for crossover have been made in interim [3] and 3-year analyses [10]. In particular, inverse probability of censoring weights and rank preserving structural failure time models were used in an attempt to target the treatment effect one would have observed if patients would have stayed on the assigned treatment. As in many such analyses, it is unclear what covariates have been used to correct for crossover in the IPCW analysis and which model estimation method was used in the RPSFTM analysis. This makes it impossible to judge whether the assumptions made are plausible. In addition, extrapolations are a major complication of these analyses as patients switch after disease progression, implying that there are no comparable patients, in terms of measured confounders, who cross over and who do not.

To alleviate concerns about extrapolation, it is often wise to target less ambitious estimands. For instance, Rudolph et al. [39] discussed positivity violations in health policy evaluation settings and proposed to redefine the estimand to correspond to a shift intervention or a modified treatment policy [8, 15, 32]. Michiels et al. [29] also proposed an alternative estimand to lessen the extrapolations that are typically needed to infer the treatment effect that would have been observed had all patients stayed on the assigned treatment. Alternatively, a solution may be obtained in terms of estimators rather than estimands. In particular, in this paper, we develop an instrumental variable estimator for the hypothetical risk ratio, comparing always taking experimental treatment to always taking control treatment, that does not rely on no unmeasured confounders assumptions. Our method does not suffer from the same concerns with censoring as an RPSFTM analysis, as a result of modeling survival probabilities instead of event times. It builds on the work by Ying and Tchetgen Tchetgen [49] but has the advantage that it preserves the -value from the treatment policy analysis. We consider this as an advantage, as under the null hypothesis of no treatment effect, crossover has no impact on the survival times and therefore the -value obtained by a treatment policy analysis is valid. This may sound disadvantageous but is reflective of the fact that ‘honest’ IV analyses extract information from the data and not from structural assumptions. In contrast, IPCW analyses can achieve more power by relying on a no unmeasured confounders assumption and a model assumption to predict crossover.

In this paper, we consider the setting where patients can cross over from the control to the experimental arm. We aim to provide insight into the rationale behind the model proposed by Ying and Tchetgen Tchetgen using simple examples and figures, so that it can be applied in case studies. Moreover, we improve the estimator proposed by Ying and Tchetgen Tchetgen by developing a doubly robust estimator, relying on a model for the randomized arm and a model for the hazards of death, that is unbiased even if one of these models is misspecified. By additionally using a model for the hazard, efficiency gains in the treatment effect estimator are expected. In addition, software in R to apply our method is provided. The approach is illustrated by re-analyzing the HELIOS trial.

2 Estimands

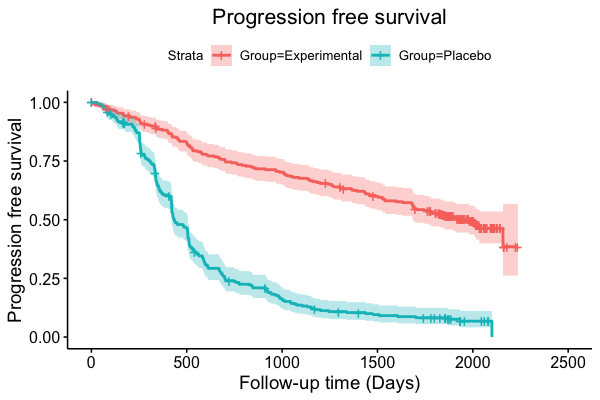

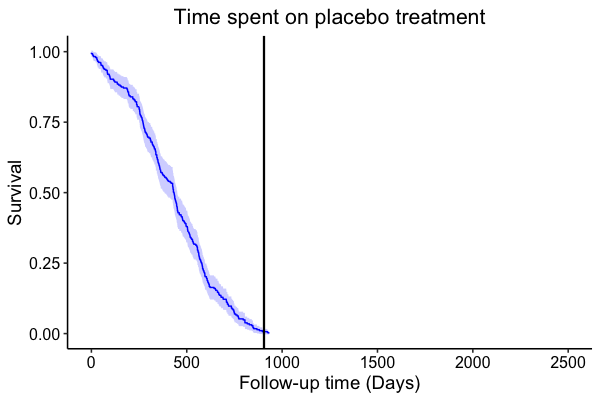

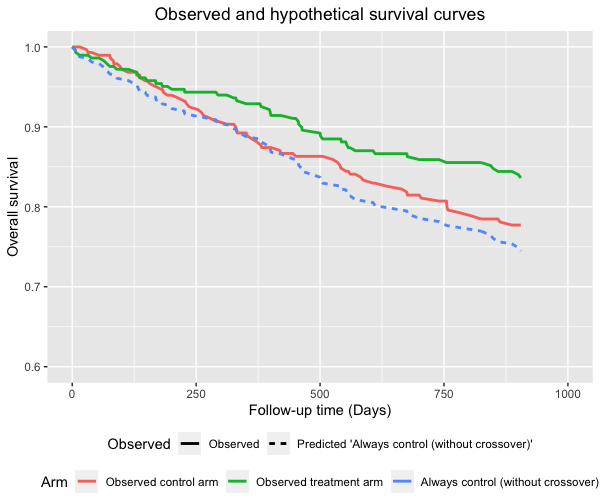

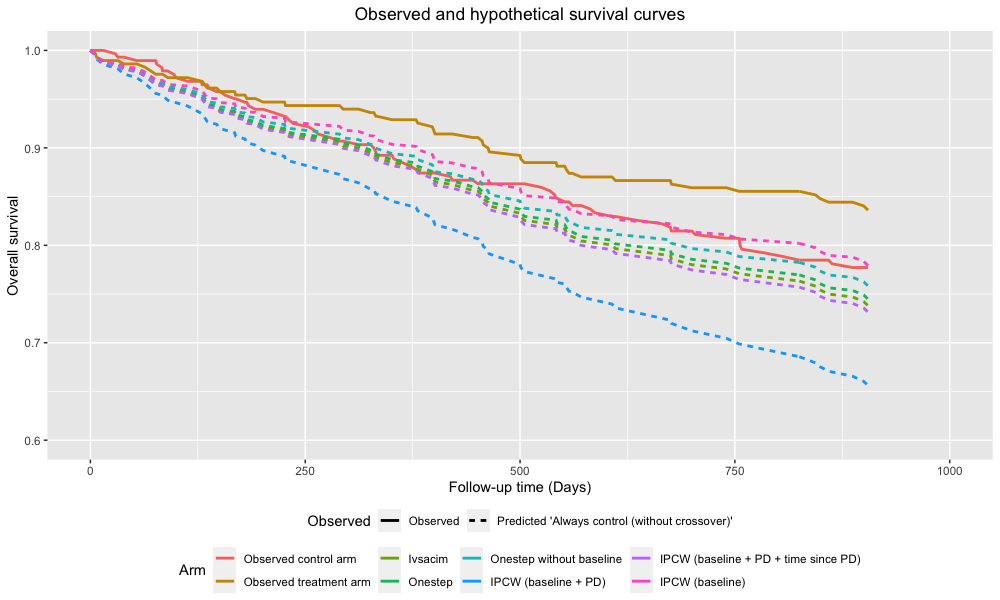

In the HELIOS trial, the overall survival hazard ratio is diluted compared to the progression free survival hazard ratio (figure 1), as many control patients start experimental treatment after disease progression, impacting the overall survival times. According to Manitz et al. [26], in the HELIOS trial, it is recommended to consider the hypothetical scenario in which crossover would not have existed, because crossover does not represent clinical practice given that the experimental treatment was not yet approved at the time of conducting the trial. However, estimating the 5-year mortality risk if all control patients would stay on their assigned treatment requires strong extrapolations. This is because, after approximately 1000 days of follow-up, all control patients who were still in the trial stopped taking control treatment, crossed over to the experimental treatment, or started subsequent therapy (figure 2). Therefore, inferring the effect if all patients would stay on the assigned treatment for 5 years is too ambitious, though not unusual to consider. In the remainder of the paper, we will therefore focus on estimating the hypothetical effect of experimental treatment up to the day of unblinding the trial had none of the patients crossed over from control to experimental, since we do have information about taking control treatment until that day. This day is indicated with a black vertical line in figure 2. In the remainder of the paper, for ease of explanation, we refer to this day as the end of the trial.

2.1 Hypothetical risk ratio

In this paper, we develop an estimator that targets a hypothetical estimand considering the setting that all patients would stay on the assigned treatment. In particular, we consider the risk ratio contrasting the survival probabilities if all patients would take experimental treatment with the survival probabilities if all patients would take control treatment. This estimand can be evaluated at different time points in the trial, as it is of interest to observe how the effect evolves over time. In the next section, this estimand, together with an instrumental variable estimator, is formally introduced.

3 Instrumental variable estimator

Ying and Tchetgen Tchetgen [49] proposed an estimator for a causal treatment effect to account for selective treatment switching using a structural nested cumulative survival time model (SNCSTM) for censored time-to-event outcomes [41]. As in the Aalen additive hazards model [1], it is assumed that the treatment has an additive effect on the hazard, unlike Cox proportional hazard models [5] that assume a multiplicative effect of the treatment on the hazard. However, while the Aalen additive hazards model can be used to estimate the treatment policy effect of being assigned to the experimental arm compared to being assigned to the control arm, the SNCSTM can be used to target the hypothetical effect if all patients would stay on the assigned treatment for the entire duration of the trial. This SNCSTM is fitted using randomization as an instrumental variable, avoiding unconfoundedness or positivity assumptions. However, the estimator for this SNCSTM proposed by Ying and Tchetgen Tchetgen has the disadvantage of not preserving the -value obtained in a treatment policy analysis. Therefore, in this paper, we improve the estimator proposed by Ying and Tchetgen Tchetgen [49] by using a doubly robust estimator, relying on a model for the randomized arm and a model for the hazards of death, that is unbiased even if one of these models is misspecified. Moreover, by adjusting for baseline covariates we require a weaker assumption for administrative censoring or censoring due to drop-out. Readers who are not interested in the technical details of the estimand and estimator can skip this section and continue reading from section 4 onwards.

3.1 Notation

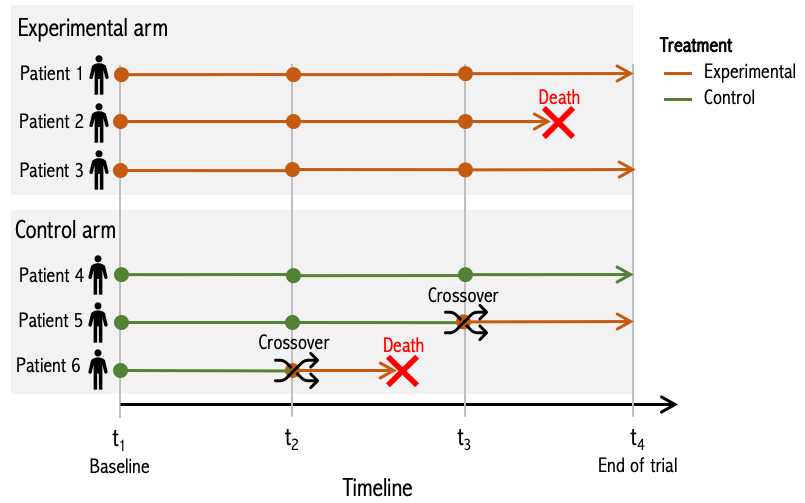

Let denote the survival time, the potential censoring time and the censored survival time. Let be the event indicator, the counting process and the at-risk process. In addition, we denote the randomized arm by , with 1 indicating the control arm and 0 the experimental arm, and the vector of baseline covariates by . Let indicate the treatment taken at time , with if the patient takes experimental treatment at time and 1 otherwise. We assume that the treatments are taken at discrete times . The history of treatments is denoted by a bar, i.e. for . The treatment is not observed if . It is assumed that the first treatment is taken at baseline, i.e. corresponds to the baseline visit. Consequently, for all patients in the trial, we have . The causal ordering of the variables is , where indicates the minimum of and . The observed data consist of independent and identically distributed observations . Different patient pathways and notation are illustrated in figure 3.

In the SNCSTM [49], counterfactual survival times for time-varying treatments [34, 35] are modeled. Let denote the potential time to event had the patient, possibly contrary to fact, taken control treatment up to time and experimental treatment thereafter. It holds that for patients who take control treatment up to time and experimental treatment thereafter. In addition, intervening on treatment can only impact the survival after the time of that treatment, i.e. the event only occurs if the event occurs for all [49]. Consequently, and are the same events for .

| Patient | Arm | Treatments | ||||

| 1 | Experimental | 0 | 0 | 0 | 0 | 0 |

| 2 | Experimental | 0 | 0 | 0 | 0 | / |

| 3 | Experimental | 0 | 0 | 0 | 0 | 0 |

| 4 | Control | 1 | 1 | 1 | 1 | 1 |

| 5 | Control | 1 | 1 | 1 | 0 | 0 |

| 6 | Control | 1 | 1 | 0 | / | / |

3.2 Model

In this section, we discuss the SNCSTM [27], contrasting the ratio of survival probabilities at time upon starting experimental treatment at time versus at time , for patients still alive at time , in the control arm, taking control treatment till time and with baseline covariates :

| (1) |

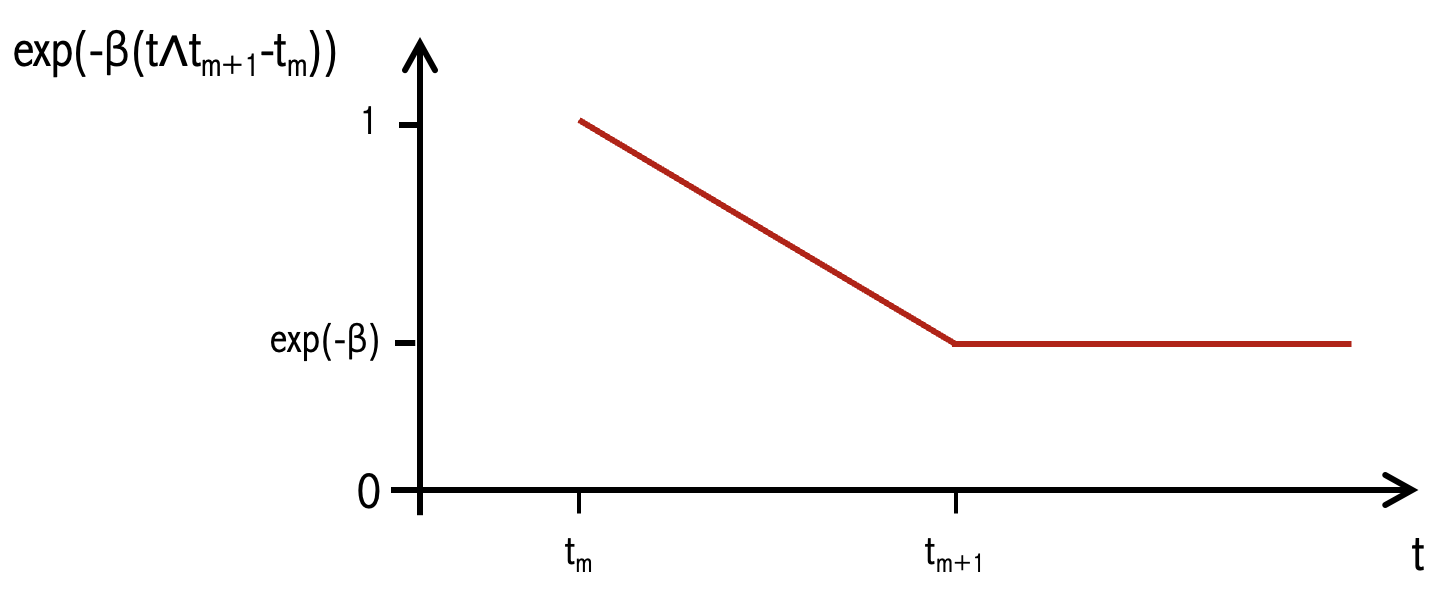

with unknown scalar parameter . In figure 4, this model is illustrated, showing that it is assumed that the effect of taking experimental treatment decreases till the next visit and stays constant afterwards. This is realistic as a new dose of treatment is taken at the next visit.

By taking logs of each side of equation (1) and differentiating with respect to , it can be shown that this model can be written equivalently as

where and are the conditional hazards of and at time for control patients who were still taking control treatment at visit and with baseline covariates . Note that, after time , the hazard difference becomes 0, as it is assumed that the effect of taking experimental treatment at time stops at the next visit. Thus, the effect of crossover at every time boils down to a decrease in the hazard of death with units. Therefore, the experimental treatment is assumed to have an additive effect on the hazard and describes a hazard difference. A positive value implies that the experimental treatment increases patients’ survival probability. This model is referred to as the ‘constant hazards difference model’ [49]. In Appendix A, a more general model is described, allowing the effect of experimental treatment on the hazard to change over time.

Parameter can be used to target the hypothetical risk ratio comparing always treated versus never treated regimen up to time [49] (see section 3.5):

| (2) |

Note that the model assumes this ratio not to depend on the baseline covariates . As patients can only cross over from the control to the experimental arm and not vice versa, the counterfactual survival probability equals the observed survival probability in the treatment arm , which can be estimated using a Kaplan-Meier estimator. In that case, equation (2) can be used to predict the survival probabilities if patients would take control treatment and not cross over, for a given value of (see section 3.5). This is illustrated in figure 5. An advantage of this risk ratio is that it can be interpreted as a causal contrast, unlike hazard ratios that have a built-in selection bias [16]. The role of the baseline covariates will be discussed in section 3.5.

3.3 Assumptions

The randomization indicator is used as an instrumental variable, meaning that it is assumed to satisfy the following conditions [49]:

-

1.

IV relevance

The instrument is associated with the treatment actually taken at time for patients still at risk at time , given history: , for all .

This assumption is stronger than strictly needed. It suffices to satisfy an assumption expressed in terms of the expectation of the derivative of the score function (see section 3.4.3). However, this assumption is less insightful.

-

2.

IV independence

The instrument is independent of the potential outcome under treatment, conditional on the baseline covariates: .

-

3.

Exclusion restriction

The instrument has no direct causal effect on the outcome other than through the exposure: , for all values of , , and , where indicates the potential survival time had one set the treatments to and the treatment arm to .

In a double-blinded randomized trial, these assumptions are expected to hold. In particular, assumption 1 is satisfied if patients still at risk are more likely to receive treatment at time if they were assigned to treatment, even after conditioning on treatment and covariate history. This is especially expected to hold in the HELIOS trial as patients can only cross over from the control to the experimental arm. The second assumption is expected to hold because of randomization and the third because of double-blinding. However, this could be violated if patients become aware of the treatment they are taking, e.g. because of adverse events. This might be the case in the HELIOS trial as 69% of the patients in the experimental arm experienced a serious treatment-emergent adverse event [11].

We also make the following assumption about administrative censoring or censoring due to drop-out:

-

4.

Conditional independent censoring

Censoring is independent of survival times, randomization and treatments actually taken, given baseline covariates: .

This assumption can be relaxed by using inverse probability of censoring weighting [37] but we will not discuss this further here.

3.4 Identification

3.4.1 Estimator by Ying and Tchetgen Tchetgen

Ying and Tchetgen Tchetgen [49] proposed a two-step estimator for the parameter of interest . In the first step, a model for the expected assigned treatment given baseline covariates, i.e. , is fitted. Note that this probability is known by design in a randomized trial. In the second step, an estimator of is obtained using an explicit recursive form. Ying [2] developed an R package called ‘ivsacim’ that implements this two-step estimator. Moreover, an estimator for a more general model, allowing the effect of experimental treatment on the hazard to change over time, together with a goodness-of-fit test for the constant hazards model, is provided. However, at the moment of writing, the package does not allow to include baseline covariates in the propensity score model for . By doing so, it is assumed that censoring due to drop-out or administrative censoring is marginally independent of survival times, randomization and treatments actually taken, which is possibly a much stronger assumption than our "conditional independent censoring" assumption.

Ying and Tchetgen Tchetgen [49] proved that their proposed estimator is uniformly consistent and asymptotically normal. However, the -value of in the Aalen additive hazards model [1], targeting a treatment policy estimand, is not preserved. This can be problematic as different conclusions may then be drawn based on a treatment policy estimand than based on the hypothetical estimand. Therefore, in section 3.4.3, we introduce a new estimator that does preserve the -value and has the advantage of being doubly robust. By adding a model for the hazard, we expect to obtain a more efficient treatment effect estimator. Moreover, model selection can be performed for this model [4]. First, we briefly describe the Aalen least squares estimator [1] for the treatment policy estimand.

3.4.2 Aalen least squares estimator for the treatment policy estimand

Consider a semiparametric additive hazards model [28] with time-varying intercept and constant treatment effect :

| (3) |

In this model, represents a treatment policy effect. In particular, it is the additive effect on the hazard of being assigned to the experimental arm compared to being assigned to the control arm. An estimator for can be obtained by solving estimating equations

| (4) |

with

with the time point indicating the end of the study. A -value for the test can be obtained by performing a one-sample t-test on the score functions evaluated in and the variance of using the sandwich estimator. In addition, a 95% confidence interval for can be found by searching for the values that lead to a -value of 5% in the t-test on the score functions. Aalen additive hazards models, e.g. model (3), can be fitted in R using the aalen function from the timereg package. However, -values and variance estimates provided by this function correspond to Wald tests rather than score tests. We will use score tests as the estimator for the hypothetical effect, discussed in the next section, which preserves the -value provided by the treatment policy analysis, by imitating its score equations.

3.4.3 One-step estimator

We developed a one-step estimator [25] for the hypothetical effect , where the initial estimator is obtained using the method by Ying and Tchetgen Tchetgen [49]. This estimator is updated using a single Newton step on the score equation. In particular, in Appendix C.2 we show that, for ,

| (5) |

with

In equation (5), the treatment effect at every time is subtracted from the counting and the at-risk process, thereby mimicking the counterfactual survival time when always taking experimental treatment, i.e. . The parameter is then chosen such that the IV assumption is satisfied. However, in equation (5), we calculate the expected value of conditional on and , to imitate the estimating function of the Aalen additive hazards model for the treatment policy estimand (4).

From (5) it follows that, if is the time point indicating the end of the study, can be estimated by solving estimating equations

| (6) |

with

where is an estimate of obtained by fitting a logistic regression model, with as outcome, baseline covariates as predictors and weights . Parameter can be estimated by solving estimating equations (6) directly, but we propose a one-step estimator [25], which is usually computationally more efficient. By starting from a consistent estimator for , we obtain an asymptotically equivalent estimator (see theorem 5.45 in [43], which also holds for M-estimators). This motivates the following approach:

-

1.

Compute an initial estimate for using the method by Ying and Tchetgen Tchetgen [49].

-

2.

Fit an Aalen additive hazards model or Cox proportional hazards model in the experimental arm for the observed event times, conditional on baseline covariates .

-

3.

Let denote the observed event times in the dataset. For every ():

-

(a)

Use the model from step 2 to estimate hazards for every patient.

-

(b)

Fit a weighted logistic regression model with as outcome, baseline covariates as predictors and weights . As patients can only cross over from the control to the experimental arm, these weights simplify to for patients in the experimental arm, for control patients who did not cross over before time and for control patients who did cross over at time .

-

(c)

Use the model from step 3 (b) to make predictions for every patient. Denote these predictions as ().

-

(d)

Calculate

with = 0, for every patient.

-

(a)

-

4.

Calculate the score function for every patient.

-

5.

Calculate the derivative of the score function w.r.t. , i.e. , for every patient, evaluated in , as described in Appendix C.2.1.

-

6.

Update the initial estimate of :

We implicitly assume that the expectation of the derivative of the score function differs from 0 when evaluated at the truth , i.e. , which typically holds because of the IV relevance assumption. The variance of can be estimated using the sandwich estimator [18]:

A -value for the test can be obtained by performing a one-sample t-test on the score functions evaluated in . In addition, the boundaries of a 95% confidence interval for can be found by searching for the values that lead to a -value of 5% in the t-test on the score functions. In the online supplementary material, it is illustrated how this can be implemented in R.

As proven in Appendix C.3, the obtained estimator for is doubly robust, meaning that it is unbiased even if the model for the randomized arm, i.e. , or the model for the hazards, i.e. , but not both, is misspecified. By adding a model for the hazard, we expect to obtain a more efficient treatment effect estimator. Moreover, as the estimator is doubly robust, model selection can be performed for the model for the hazard [4].

This estimating function for equals the estimating equation of the treatment policy estimand in the Aalen additive hazards model under the null hypothesis . Therefore, we will obtain the same -value when performing a score test in the treatment policy analysis.

3.5 Hypothetical risk ratio

Consider the additional assumption of no-current treatment value interaction, stating that the causal effect of taking control at time versus experimental treatment, among patients who were taking control at time is equal to that among patients who were treated at time (see Appendix B). Under this assumption, the effect can be interpreted as the hypothetical risk ratio comparing always treated versus never treated regimes up to time [49]:

| (7) |

The no-current treatment value interaction assumption could be violated if patients who cross over do not experience the same treatment effect as those who do not. As these are two, possibly very different, subgroups, this assumption can be violated. However, it can be relaxed by including time-varying covariates in the SNCSTM, but this complicates the estimation procedure. Implementation of this hypothetical estimand (7) is illustrated in the online supplementary material.

As patients can only cross over from the control arm to the experimental arm and not vice versa, the survival probability if all patients would take control treatment and not cross over can be estimated using risk ratio (7), as shown in Appendix D:

The survival probabilities can be obtained by fitting a Cox proportional hazards model or an Aalen additive hazards model to the observed experimental arm.

4 Data analysis

4.1 Methods

In the data analysis of the HELIOS trial, we consider the treatment policy and hypothetical estimand regarding the intercurrent event ‘treatment crossover’. In addition, we apply three traditional methods, i.e. excluding patients who cross over, censoring patients at the time of crossover and including treatment as a time-varying covariate. The hypothetical estimand is targeted using the IPCW method, the IV method by Ying and Tchetgen Tchetgen and the one-step estimator proposed in this paper. For all effects, the relative risk (RR) at the end of the trial is considered as summary measure. In particular, the treatment policy estimand contrasts the survival probabilities if all patients would be assigned to the experimental arm versus the control arm, while the hypothetical estimand contrasts the survival probabilities if all patients would take experimental treatment versus control treatment for the entire study duration. These estimands can be defined according to the guidelines of the ICH E9(R1) guideline (see Appendix E.1).

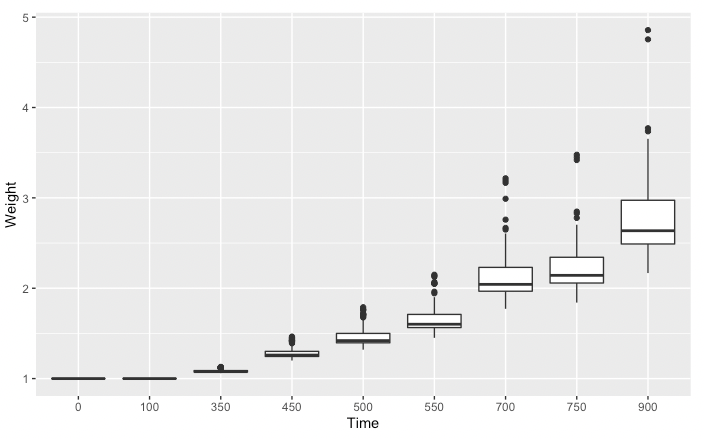

All analyses are performed using the software R (version 4.0.4). For the treatment policy estimand and the traditional methods, these risk ratios are assessed using the aalen function from the timereg package [40], fitting an Aalen additive hazards model [1]. To target the hypothetical estimand, we apply the IPCW method to the Aalen additive hazards model. In particular, the ipcw function from the ipcwswitch package [12] is used to compute stabilized IPCweights with baseline and time-varying predictors, as described by Graffeo et al. [13]. As baseline covariates, we include the two stratification factors, i.e. purine analog refractory status (failure to respond or relapse in 12 months) and prior lines of therapy (1 line versus 1 line), sex and age, and as time-varying confounders, a binary variable indicating whether or not, at every day, the patient had already disease progression. This method is compared to the method where we additionally include the time since progression as time-varying predictor. Finally, we also compute weights without time-varying predictors, e.g. only baseline covariates, as described by Willems et al. [47]. The weights are then incorporated into an Aalen additive hazards model with as predictor.

To target the hypothetical risk ratio, we also consider different IV methods. In particular, the method developed by Ying and Tchetgen Tchetgen [49] is applied by using the ivsacim function from the ivsacim package [48]. This method is compared to the one-step estimator discussed in section 3.4.3, including the two stratification factors, sex and age as baseline covariates. R code for these estimators can be found in the online supplementary material. To make a fair comparison of the considered methods, all -values for the tests are obtained by performing a one-sample t-test on the score functions evaluated in (see Appendix E.2). In addition, the variance of is obtained using the Sandwich estimator and 95% confidence intervals are obtained by searching for the values that lead to a -value of 5% in the t-test on the score functions. Finally, the relative risks are estimated using expression (7) and a 95% confidence interval is obtained using the same transformation of the bounds of the confidence interval for .

4.2 Results

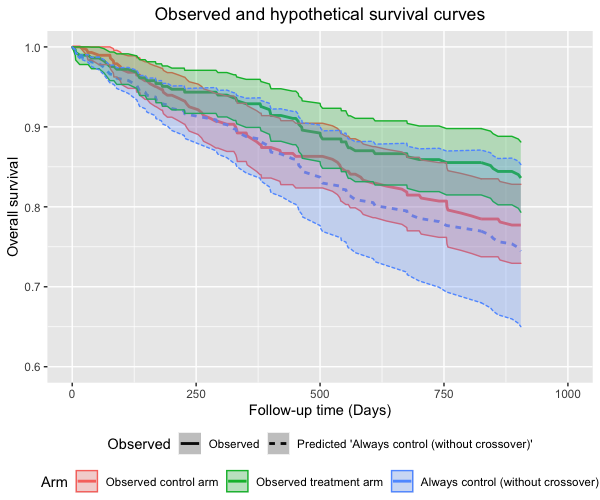

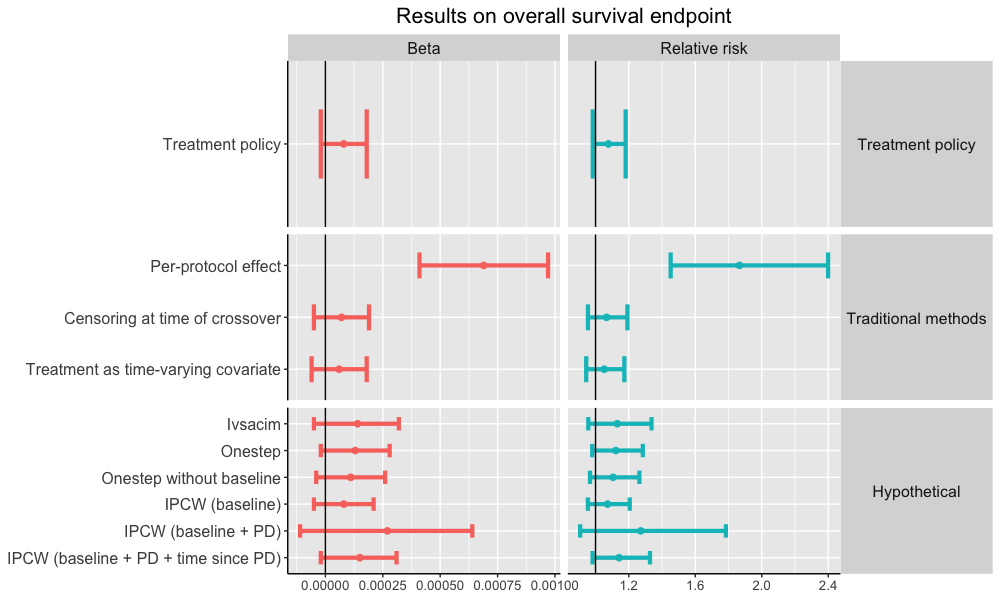

In total, 41 patients (7%) were censored during the trial, for unknown reasons. This censoring was not found to depend on the randomized arm, or on one of the baseline covariates. Table 1 and figure 6 summarize the results of the data analysis, while the obtained models and weights and predicted survival curves "if all patients would take control treatment and not cross over" are shown in Appendix E.4. The treatment policy relative risk (1.08, 95% CI [0.98; 1.18]) shows an effect that is not significant. As expected, the hypothetical estimands, both using the ivsacim estimator (1.13, 95% CI [0.96; 1.34]) and the one-step estimator (1.12, 95% CI [0.98; 1.28]), indicate a somewhat larger treatment effect, as the setting is considered where control patients do not experience the possibly beneficial effect of crossover. However, the confidence intervals are a little wider too. In addition, the variance of the proposed one-step estimator () is smaller than the one of the ivsacim estimator (). The -value obtained using the one-step estimator is 8%, lower than the -value obtained by the ivsacim estimator (18%). If no baseline covariates are included in the one-step estimator, the same -value (12%) as in the treatment policy analysis is obtained. In addition, we found the estimated function not to depend on , as expected if holds (see Appendix E.4.1). Moreover, all IV methods result in realistic counterfactual survival curves (see Appendix E.4), indicating that the control patients would have a somewhat worse survival curve if they were not allowed to cross over.

The IPCW estimator using only baseline covariates as predictors (1.07, 95% CI [0.95; 1.21]) does not perform better than simply censoring patients at the time of crossover, without correction for selection bias. This indicates that some important confounders of the crossover-outcome relationship may not have been included. When disease progression is included as a time-varying predictor in the inverse probability weights, we obtained a larger, treatment effect (1.27, 95% CI [0.91; 1.78]) than the treatment policy estimand. However, the model for the probability of crossover does not fit the data well and the standard error of the time-varying predictor for disease progression is very large (see Appendix E.4.2). This results in a very wide confidence interval for the relative risk. In addition, the counterfactual survival curve is not realistic as the effect of crossover seems to be overrated (see Appendix E.4). However, no indications of positivity violations were observed. When instead the time since disease progression is included as predictor, the model for the probability of crossover fits the data better and an effect (1.14, 95% CI [0.98; 1.33]) in line with the one-step estimator is obtained. However, the -value of the IPCW estimator is smaller (6%), which may be due to the fact that additional model assumptions are being made. Moreover, as shown by Latimer et al. [24], these IPCW estimates might be biased as a lot of patients crossed over in the HELIOS trial.

From the results, it is also clear that the traditional methods, which are prone to selection bias when selective crossover occurs, should ideally be avoided. In particular, the per-protocol effect, which excludes patients who cross over, gives an effect (1.87, 95% CI [1.47; 2.40]) that is not at all in line with the other results (see figure 6). In addition, a lot of data is removed as 63% of the control patients cross over. When treating treatment as a time-varying treatment the effect (1.05, 95% CI [0.94; 1.17]) moves somewhat towards one, compared to the treatment policy estimand. This effect is very close to the effect where patients are censored at the time of crossover (1.07, 95% CI [0.95; 1.19]).

The fact that the results of this data analysis on the overall survival endpoint are not significant is consistent with the published interim results of the HELIOS trial [3]. However, the results presented in this paper are intended for illustrative purposes only.

| Estimand | Estimator | Relative risk | |||

| Estimate (SE) | Estimate | 95% CI | -value | ||

| Treatment policy | Aalen least squares | () | 1.08 | [0.98; 1.18] | 0.12 |

| Per-protocol effect | Aalen least squares | () | 1.87 | [1.45; 2.40] | 0.00 |

| (excluding patients | |||||

| who cross over) | |||||

| Censoring patients | Aalen least squares | () | 1.07 | [0.95; 1.19] | 0.25 |

| at time of crossover | |||||

| As treated | Aalen least squares | () | 1.05 | [0.94; 1.17] | 0.35 |

| (Treatment as time- | |||||

| varying covariate) | |||||

| Hypothetical | IV estimators | ||||

| Ivsacim [2] | () | 1.13 | [0.96; 1.34] | 0.18 | |

| One-step estimator | () | 1.12 | [0.98; 1.28] | 0.08 | |

| One-step estimator | () | 1.11 | [0.97; 1.26] | 0.12 | |

| without baseline covariates | |||||

| IPCW estimators | |||||

| Baseline covariates as predictors | () | 1.07 | [0.95; 1.21] | 0.22 | |

| Baseline covariates and | () | 1.27 | [0.91; 1.78] | 0.15 | |

| indicator for PD as predictors | |||||

| Baseline covariates, indicator for | () | 1.14 | [0.98; 1.33] | 0.06 | |

| and time since PD as predictors | |||||

PD: progressive disease

5 Discussion

In this article, we considered the setting in randomized clinical trials with time-to-event endpoints, where patients can cross over from the control to the experimental arm, typically after disease progression. We explained how traditional methods to correct for crossover easily lure one into making large extrapolations. In view of this, we discussed a structural nested cumulative survival time model that can be used to target the hypothetical estimand "if all patients would stay on the assigned treatment arm", summarized as a survival risk ratio. An estimator for this effect, developed by Ying and Tchetgen Tchetgen [2], was compared to the one-step estimator we developed. These estimators do not suffer from positivity or unconfoundedness assumptions, as may often be the case with IPCW methods. In particular, these methods use randomization as an instrumental variable. The developed one-step estimator, in contrast to the estimator by Ying and Tchetgen Tchetgen [2], is a doubly robust estimator, meaning that it is unbiased even if one of the working models is misspecified. In addition, data-adaptive methods (e.g. variable selection) can be used for the model for the hazard of death.

This paper also aimed to give more insight into the model proposed by Ying and Tchetgen Tchetgen [2], and apply it to a real case study. Moreover, we aimed to obtain insight into the performance of the instrumental variable estimator in settings with a lot of crossover, as in the data analysis performed by Ying and Tchetgen Tchetgen [2] the number of switchers was rather limited, i.e. 5% of the treated patients and 10% of the control patients crossed over. All instrumental variable estimators showed good performance in the conducted data analysis, even though 63% of the control patients switched treatment.

In this paper, we only considered the setting where patients can cross over from one arm to the other. However, SNCSTM (1) can be extended to the setting where patients can cross over from both arms:

| (8) |

with the potential time to event had the patient, possibly contrary to fact, taken treatments up to time and control treatment thereafter. However, in model (8) it is assumed that the ratio of survival probabilities does not depend on , which might be a strong assumption.

References

- Aalen, [1989] Aalen, O. O. (1989). A linear regression model for the analysis of life times. Statistics in medicine, 8(8):907–925.

- Andrew, [2022] Andrew, Y. (2022). Package ‘ivsacim’.

- Chanan-Khan et al., [2016] Chanan-Khan, A., Cramer, P., Demirkan, F., Fraser, G., Silva, R. S., Grosicki, S., Pristupa, A., Janssens, A., Mayer, J., Bartlett, N. L., et al. (2016). Ibrutinib combined with bendamustine and rituximab compared with placebo, bendamustine, and rituximab for previously treated chronic lymphocytic leukaemia or small lymphocytic lymphoma (helios): a randomised, double-blind, phase 3 study. The Lancet Oncology, 17(2):200–211.

- Chernozhukov et al., [2018] Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters.

- Cox, [1972] Cox, D. R. (1972). Regression models and life-tables. Journal of the Royal Statistical Society: Series B (Methodological), 34(2):187–202.

- Degtyarev et al., [2019] Degtyarev, E., Zhang, Y., Sen, K., Lebwohl, D., Akacha, M., Hampson, L. V., Bornkamp, B., Maniero, A., Bretz, F., and Zuber, E. (2019). Estimands and the patient journey: Addressing the right question in oncology clinical trials. JCO Precision Oncology, 3:1–10.

- Demetri et al., [2012] Demetri, G. D., Garrett, C. R., Schöffski, P., Shah, M. H., Verweij, J., Leyvraz, S., Hurwitz, H. I., Pousa, A. L., Le Cesne, A., Goldstein, D., et al. (2012). Complete longitudinal analyses of the randomized, placebo-controlled, phase iii trial of sunitinib in patients with gastrointestinal stromal tumor following imatinib failure. Clinical Cancer Research, 18(11):3170–3179.

- Díaz et al., [2021] Díaz, I., Williams, N., Hoffman, K. L., and Schenck, E. J. (2021). Nonparametric causal effects based on longitudinal modified treatment policies. Journal of the American Statistical Association, pages 1–16.

- Feyerabend et al., [2019] Feyerabend, S., Saad, F., Perualila, N. J., Van Sanden, S., Diels, J., Ito, T., De Porre, P., and Fizazi, K. (2019). Adjusting overall survival estimates for treatment switching in metastatic, castration-sensitive prostate cancer: results from the latitude study. Targeted Oncology, 14:681–688.

- Fraser et al., [2019] Fraser, G., Cramer, P., Demirkan, F., Silva, R. S., Grosicki, S., Pristupa, A., Janssens, A., Mayer, J., Bartlett, N., Dilhuydy, M.-S., et al. (2019). Updated results from the phase 3 helios study of ibrutinib, bendamustine, and rituximab in relapsed chronic lymphocytic leukemia/small lymphocytic lymphoma. Leukemia, 33(4):969–980.

- Fraser et al., [2020] Fraser, G. A., Chanan-Khan, A., Demirkan, F., Santucci Silva, R., Grosicki, S., Janssens, A., Mayer, J., Bartlett, N. L., Dilhuydy, M.-S., Loscertales, J., et al. (2020). Final 5-year findings from the phase 3 helios study of ibrutinib plus bendamustine and rituximab in patients with relapsed/refractory chronic lymphocytic leukemia/small lymphocytic lymphoma. Leukemia & lymphoma, 61(13):3188–3197.

- Graffeo, [2021] Graffeo, N. (2021). Package ‘ipcwswitch’.

- Graffeo et al., [2019] Graffeo, N., Latouche, A., Le Tourneau, C., and Chevret, S. (2019). ipcwswitch: An r package for inverse probability of censoring weighting with an application to switches in clinical trials. Computers in biology and medicine, 111:103339.

- Halabi and Michiels, [2019] Halabi, S. and Michiels, S. (2019). Textbook of clinical trials in oncology: a statistical perspective. CRC Press.

- Haneuse and Rotnitzky, [2013] Haneuse, S. and Rotnitzky, A. (2013). Estimation of the effect of interventions that modify the received treatment. Statistics in medicine, 32(30):5260–5277.

- Hernán, [2010] Hernán, M. A. (2010). The hazards of hazard ratios. Epidemiology, 21(1):13.

- Hernán and Robins, [2006] Hernán, M. A. and Robins, J. M. (2006). Instruments for causal inference: an epidemiologist’s dream? Epidemiology, pages 360–372.

- Huber, [1967] Huber, P. (1967). The behavior of maximum likelihood estimates under nonstandard conditions in: Fifth symposium on mathematical statistics and probability. University of California, Berkeley, California.[Google Scholar].

- International Council for Harmonisation, [2019] International Council for Harmonisation (2019). Addendum on estimands and sensitivity analysis in clinical trials. https://database.ich.org/sites/default/files/E9-R1_Step4_Guideline_2019_1203.pdf.

- Ishak et al., [2014] Ishak, K. J., Proskorovsky, I., Korytowsky, B., Sandin, R., Faivre, S., and Valle, J. (2014). Methods for adjusting for bias due to crossover in oncology trials. Pharmacoeconomics, 32(6):533–546.

- Jönsson et al., [2014] Jönsson, L., Sandin, R., Ekman, M., Ramsberg, J., Charbonneau, C., Huang, X., Jönsson, B., Weinstein, M. C., and Drummond, M. (2014). Analyzing overall survival in randomized controlled trials with crossover and implications for economic evaluation. Value in Health, 17(6):707–713.

- Latimer et al., [2017] Latimer, N. R., Abrams, K., Lambert, P., Crowther, M., Wailoo, A., Morden, J., Akehurst, R., and Campbell, M. (2017). Adjusting for treatment switching in randomised controlled trials–a simulation study and a simplified two-stage method. Statistical methods in medical research, 26(2):724–751.

- Latimer et al., [2015] Latimer, N. R., Abrams, K. R., Amonkar, M. M., Stapelkamp, C., and Swann, R. S. (2015). Adjusting for the confounding effects of treatment switching—the break-3 trial: dabrafenib versus dacarbazine. The oncologist, 20(7):798–805.

- Latimer et al., [2014] Latimer, N. R., Abrams, K. R., Lambert, P. C., Crowther, M. J., Wailoo, A. J., Morden, J. P., Akehurst, R. L., and Campbell, M. J. (2014). Adjusting survival time estimates to account for treatment switching in randomized controlled trials—an economic evaluation context: methods, limitations, and recommendations. Medical Decision Making, 34(3):387–402.

- Le Cam, [1956] Le Cam, L. (1956). On the asymptotic theory of estimation and testing hypotheses. In Proceedings of the Third Berkeley Symposium on Mathematical Statistics and Probability, Volume 1: Contributions to the Theory of Statistics, volume 3, pages 129–157. University of California Press.

- Manitz et al., [2022] Manitz, J., Kan-Dobrosky, N., Buchner, H., Casadebaig, M.-L., Degtyarev, E., Dey, J., Haddad, V., Jie, F., Martin, E., Mo, M., et al. (2022). Estimands for overall survival in clinical trials with treatment switching in oncology. Pharmaceutical Statistics, 21(1):150–162.

- Martinussen et al., [2011] Martinussen, T., Vansteelandt, S., Gerster, M., and Hjelmborg, J. v. B. (2011). Estimation of direct effects for survival data by using the aalen additive hazards model. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73(5):773–788.

- McKeague and Sasieni, [1994] McKeague, I. W. and Sasieni, P. D. (1994). A partly parametric additive risk model. Biometrika, 81(3):501–514.

- Michiels et al., [2021] Michiels, H., Sotto, C., Vandebosch, A., and Vansteelandt, S. (2021). A novel estimand to adjust for rescue treatment in randomized clinical trials. Statistics in Medicine, 40(9):2257–2271.

- Morden et al., [2011] Morden, J. P., Lambert, P. C., Latimer, N., Abrams, K. R., and Wailoo, A. J. (2011). Assessing methods for dealing with treatment switching in randomised controlled trials: a simulation study. BMC medical research methodology, 11(1):1–20.

- Munir et al., [2019] Munir, T., Brown, J. R., O’Brien, S., Barrientos, J. C., Barr, P. M., Reddy, N. M., Coutre, S., Tam, C. S., Mulligan, S. P., Jaeger, U., et al. (2019). Final analysis from resonate: Up to six years of follow-up on ibrutinib in patients with previously treated chronic lymphocytic leukemia or small lymphocytic lymphoma. American journal of hematology, 94(12):1353–1363.

- Muñoz and Van Der Laan, [2012] Muñoz, I. D. and Van Der Laan, M. (2012). Population intervention causal effects based on stochastic interventions. Biometrics, 68(2):541–549.

- Petersen et al., [2012] Petersen, M. L., Porter, K. E., Gruber, S., Wang, Y., and Van Der Laan, M. J. (2012). Diagnosing and responding to violations in the positivity assumption. Statistical methods in medical research, 21(1):31–54.

- Robins, [1986] Robins, J. (1986). A new approach to causal inference in mortality studies with a sustained exposure period—application to control of the healthy worker survivor effect. Mathematical modelling, 7(9-12):1393–1512.

- Robins, [1987] Robins, J. (1987). A graphical approach to the identification and estimation of causal parameters in mortality studies with sustained exposure periods. Journal of chronic diseases, 40:139S–161S.

- Robins, [1994] Robins, J. M. (1994). Correcting for non-compliance in randomized trials using structural nested mean models. Communications in Statistics-Theory and methods, 23(8):2379–2412.

- Robins and Finkelstein, [2000] Robins, J. M. and Finkelstein, D. M. (2000). Correcting for noncompliance and dependent censoring in an aids clinical trial with inverse probability of censoring weighted (ipcw) log-rank tests. Biometrics, 56(3):779–788.

- Robins et al., [2000] Robins, J. M., Hernan, M. A., and Brumback, B. (2000). Marginal structural models and causal inference in epidemiology. Epidemiology, 11(5):550–560.

- Rudolph et al., [2022] Rudolph, K. E., Gimbrone, C., Matthay, E. C., Díaz, I., Davis, C. S., Keyes, K., and Cerdá, M. (2022). When effects cannot be estimated: redefining estimands to understand the effects of naloxone access laws. Epidemiology, 33(5):689–698.

- Scheike, [2022] Scheike, T. (2022). Package ‘timereg’.

- Seaman et al., [2020] Seaman, S., Dukes, O., Keogh, R., and Vansteelandt, S. (2020). Adjusting for time-varying confounders in survival analysis using structural nested cumulative survival time models. Biometrics, 76(2):472–483.

- Sternberg et al., [2013] Sternberg, C. N., Hawkins, R. E., Wagstaff, J., Salman, P., Mardiak, J., Barrios, C. H., Zarba, J. J., Gladkov, O. A., Lee, E., Szczylik, C., et al. (2013). A randomised, double-blind phase iii study of pazopanib in patients with advanced and/or metastatic renal cell carcinoma: final overall survival results and safety update. European journal of cancer, 49(6):1287–1296.

- Van der Vaart, [2000] Van der Vaart, A. W. (2000). Asymptotic statistics, volume 3. Cambridge university press.

- Vansteelandt and Keiding, [2011] Vansteelandt, S. and Keiding, N. (2011). Invited commentary: G-computation–lost in translation? American journal of epidemiology, 173(7):739–742.

- Walker et al., [2004] Walker, A. S., White, I. R., and Babiker, A. G. (2004). Parametric randomization-based methods for correcting for treatment changes in the assessment of the causal effect of treatment. Statistics in Medicine, 23(4):571–590.

- Watkins et al., [2013] Watkins, C., Huang, X., Latimer, N., Tang, Y., and Wright, E. J. (2013). Adjusting overall survival for treatment switches: commonly used methods and practical application. Pharmaceutical statistics, 12(6):348–357.

- Willems et al., [2018] Willems, S., Schat, A., van Noorden, M., and Fiocco, M. (2018). Correcting for dependent censoring in routine outcome monitoring data by applying the inverse probability censoring weighted estimator. Statistical Methods in Medical Research, 27(2):323–335.

- Ying, [2022] Ying, A. (2022). Package ‘ivsacim’.

- Ying and Tchetgen, [2022] Ying, A. and Tchetgen, E. J. T. (2022). Structural cumulative survival models for estimation of treatment effects accounting for treatment switching in randomized experiments. Biometrics.

Appendix A SNCSTM

In this appendix, we discuss the SNCSTM proposed by Ying and Tchetgen Tchetgen [49]. Let denote the potential time to event had the patient, possibly contrary to fact, taken treatments up to time and control treatment thereafter.

In the SNCSTM, one contrasts the ratio of survival probabilities at time upon starting experimental treatment at time versus at time , for patients still alive at time , in arm , with treatment history and with baseline covariates :

| (9) |

for an unknown function . In this model, can be interpreted as a measure of the treatment effect for patients who share the same history and take control at time and are treated thereafter, compared to those who are treated after time . A positive value implies that the treatment increases patients’ survival probability. If , function (9) becomes 1, because then the two treatment regimes being compared are identical.

Appendix B Hypothetical estimand

In this appendix, we show that under model (9), and the no-current treatment value interaction assumption (see below), it holds that

| (10) |

The no-current treatment value interaction assumption [36, 49] states that the causal effect of control at time versus experimental treatment among patients who were taking control at time is equal to that among patients who were treated at time conditional on past history [49]:

| (11) |

In the setting where patients can only cross over from the control to the experimental arm and not vice versa, this assumption boils down to

| (12) |

stating that the causal effect of switching at time versus at time is the same for control patients who in fact did switch at time and for those who did not, with the same baseline covariates. This assumption could be violated if patients who cross over do not experience the same treatment effect as those who do not. This assumption can be relaxed by including time-varying covariates in the SNCSTM, but this will complicate the estimation procedure.

Proof of (10)

For , model (9) implies

| (13) | ||||

| (14) |

and assumption (11) implies

| (15) | ||||

| (16) |

From model (13) and assumption (15) it follows that

| (17) |

where the third equality follows from the consistency assumption. Model (14) and assumption (16) imply

From (17) it then follows that

Assuming and , it follows that

For general , it can likewise be shown by induction that

Appendix C One-step estimator

C.1 Proof of unbiasedness of estimating equation

Theorem 1

with the hazard rate function of conditional on and

assuming and .

To prove this, we first need some lemmas.

Lemma 1

If SNCSTM (9) holds, and assuming and ,

it follows that

| (18) | |||||

| (19) | |||||

| (20) | |||||

| (21) |

Proof

For , we have that:

where the third equation follows from SNCSTM (9) and the fourth from the consistency assumption.

For , we have that:

where the second equation follows from SNCSTM (9). This can be further rewritten as

where the third equality follows from the consistency assumption and the fourth equality from SNCSTM (9). Again using the consistency assumption, this can be further rewritten as

For general , it can likewise be shown by induction that

From it follows that:

In addition, from it follows that

Consequently,

Therefore, the counterfactual survival probabilities ‘when always taking control treatment’ can be obtained by removing the effect of non-zero treatment at each period from the beginning of the study period to the end.

Lemma 2

If SNCSTM (1) holds, and assuming and ,

it follows that

Proof

Proof of Theorem 1

From equation (18) and the assumption , it follows that

with . By taking logs of each side of this equation and differentiating with respect to , it follows that

with the hazard rate function of conditional on .

Let denote the survival probability at time conditional on exposures , treatment assignment and baseline covariates and the density function of at time conditional on exposures , treatment assignment and baseline covariates . It then follows that

It follows that

Consequently,

with .Therefore, it holds that

Consequently,

| (22) |

In the probability , we condition on the counterfactual survival time under treatment, i.e. , to mimic the estimating equations of the Aalen least squares estimator (see Appendix E.2) that also uses at-risk sets.

In the setting with right-censored data, it then follows from (22) and the assumption that

which completes the proof of Theorem 1.

C.2 One-step estimator for in model (1)

Under the SNCSTM assuming a constant treatment effect where patients can only cross over from the control to the experimental arm, i.e.

it holds that

| (23) |

with

assuming and . This follows from Theorem 1, with and acknowledging that the counterfactual hazard equals the observed hazard in the experimental arm as patients can not cross over from the experimental to the control arm.

Consequently, if is the time point indicating the end of the study, can be estimated by solving estimating equations

| (24) |

with

| (25) |

where is an estimate of obtained by fitting a logistic regression model, with as outcome, baseline covariates as predictors and weights .

C.2.1 Derivative of score equation

In this subsection, we calculate the derivative of score equation (25) w.r.t. .

Let denote a vector with constant 1, baseline covariates and possible interactions between them. If is estimated by fitting a logistic regression model, with as outcome, as predictors and weights , it holds that

| (26) |

with a parametric function of dimension . This function is a function of as the weights used in the estimating procedure depend on this parameter. From (26) it follows that the derivative of the score equation (25) w.r.t. equals

| (27) |

The derivative can be obtained as follows. From the estimating equations used to estimate a logistic regression model with as outcome, as predictors and weights , it follows that

for all . Because this is a constant function, then by differentiating with respect to , it follows that

Consequently,

C.2.2 One-step estimator

A one-step estimator [25] for can be obtained as follows. Suppose is an initial estimate for . This estimator can be updated using a single Newton step:

with the score function, evaluated in , and the derivative of the score function w.r.t. , evaluated in .

C.3 Proof of double robustness

Theorem 2

The estimator for discussed in the main paper and Appendix C.2, is doubly robust, meaning that it is unbiased even if the model for the randomized treatment, i.e. , or the model for the hazards, i.e. , but not both, is misspecified.

Lemma 3

Proof

Let be a function conditional on the baseline covariates . From equation (18) it follows that

assuming . Consequently, from (22) it follows that

In the setting with right-censored data, it then follows from the assumption that

Proof of Theorem 2

First, let be an estimator for , which is possibly misspecified. We will prove that equation (23) is still on average 0. Equation (23) can be rewritten as

where the second equality follows from Lemma 3. Using equality (19) and assuming , this can be further rewritten as

Next, let be an estimator for , which is possibly misspecified. From equation (18) and the assumption , it follows that

By taking logs of each side of this equation and differentiating with respect to , it follows that

It then follows that

It follows that

Consequently,

Therefore, it holds that

with as patients in the experimental arm stay on experimental treatment. In the setting with right-censored data, it then follows from the assumption that

Consequently,

Appendix D Counterfactual survival curve under control

If patients can only cross over from the control arm to the experimental arm and not vice versa, the survival probability if all patients would take control treatment and not cross over can be estimated as follows. From the hypothetical risk ratio (10) and assumption it follows that

| (28) | |||||

where the third equality follows since all treated patients take experimental treatment for the entire duration of the trial. Marginal survival probabilities can be obtained by averaging out the baseline covariates in equation (28):

Therefore, the marginal probabilities can be obtained by averaging over all patients in the dataset:

The survival probabilities can be obtained by fitting a Cox proportional hazards model or an Aalen additive hazards model to the observed data.

Appendix E Data analysis

E.1 Estimands framework

The treatment-policy and hypothetical estimand in the HELIOS trial, described in section 4, can be defined according to the estimands framework described in the addendum of the ICH E9(R1) guideline [19]:

-

•

Treatment: 420mg daily ibrutinib or placebo, plus 6 cycles of bendamustine plus rituximab, as defined by the study protocol.

-

•

Population: the entire study population, as defined by the inclusion-exclusion criteria of the study.

-

•

Variable: time to death.

-

•

Intercurrent events: crossover from the control to the experimental treatment:

-

–

Treatment-policy estimand: the value of the outcome is of interest regardless of crossover.

-

–

Hypothetical estimand: the hypothetical scenario is envisaged where patients on the control arm would not start experimental treatment.

-

–

-

•

Population-level summary: the risk ratio comparing survival times in the experimental arm versus the control arm.

-

–

Treatment-policy estimand: the risk ratio at the end of the trial, contrasting the survival probabilities if all patients would be assigned to the experimental treatment arm with the survival probabilities if all patients would be assigned to the control arm.

-

–

Hypothetical estimand: the risk ratio at the end of the trial, contrasting the survival probabilities if all patients would take experimental treatment for the entire duration of the trial with the survival probabilities if all patients would take control treatment for the entire duration of the trial.

Here, we only considered the intercurrent event ‘crossover from the control to the experimental treatment’ and handled it using the treatment-policy or hypothetical estimand. However, in clinical trials different intercurrent events might occur, such as starting prohibited medication. According to the addendum of the ICH E9(R1) guideline, it is not necessary to use the same estimand to address all intercurrent events. In particular, different estimands can be used to reflect the clinical question of interest in respect to different intercurrent events.

-

–

E.2 Aalen additive hazards model

We consider a semiparametric additive hazards model [28] with time-varying intercept and constant treatment effect :

To estimate , we solve estimating equations

| (29) |

with

To obtain a -value for the test , a one-sample t-test is performed on the score functions evaluated in . The variance of is estimated using the sandwich estimator. In addition, a 95% confidence interval for is found by searching for the values that lead to a -value of 5% in the t-test on the score functions.

E.3 Score equations IPCW

Let denote the time to crossover for control treatments, defined as if the patient does not cross over. In addition, let be a vector of longitudinal confounders for crossover. The stabilized inverse probability weights [38] to correct for censoring for patient are then defined as:

If only baseline covariates are included to predict crossover, the weights are defined as:

When IPCWeights are used to correct for crossover, is estimated by solving estimating equations

with

where equals or .

E.4 Results

E.4.1 Hypothetical estimand: One-step estimator

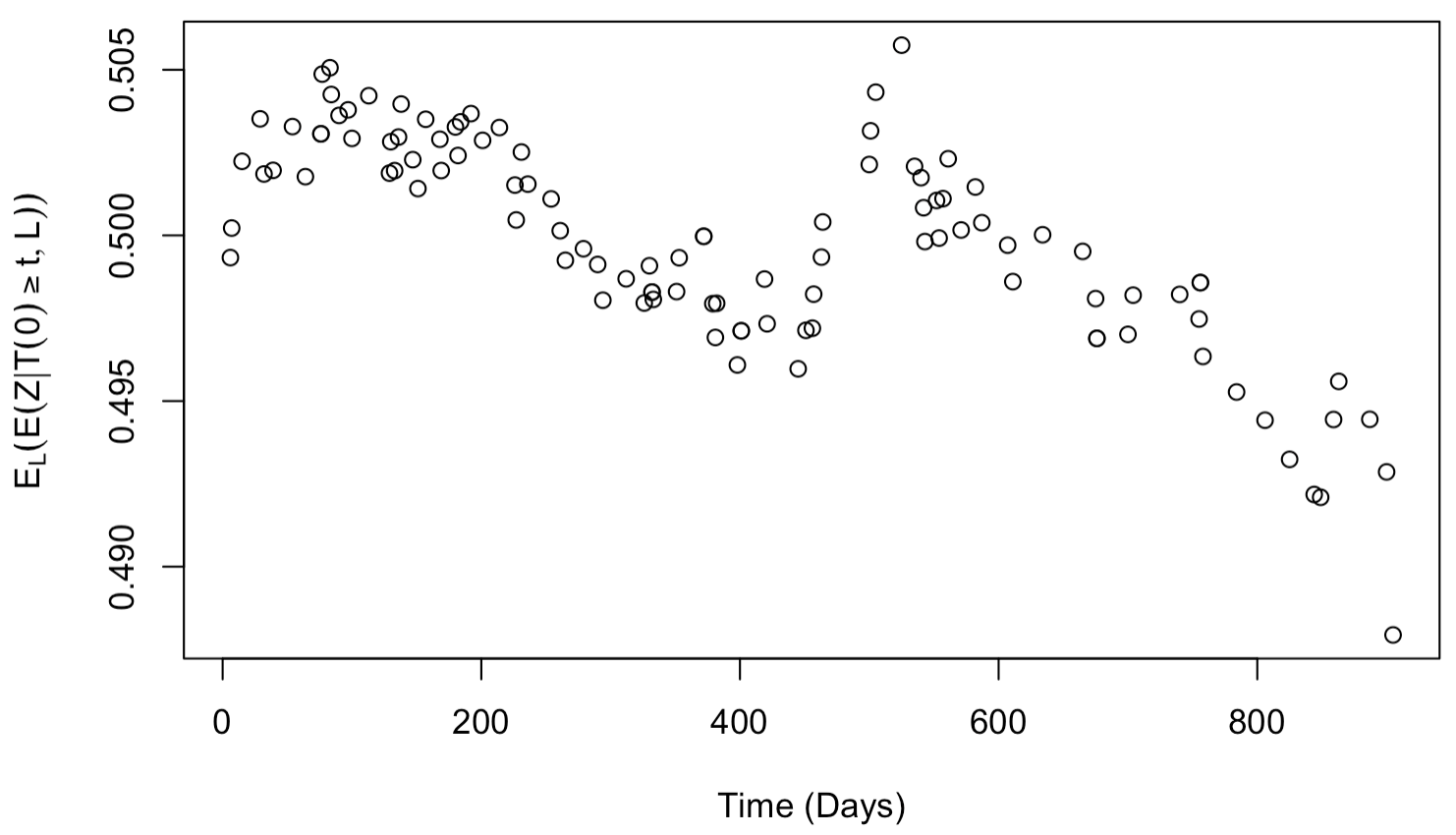

Under the assumption , does not depend on . To verify this, was estimated for the obtained using the one-step estimator. Here, indicates that the average was taken over the baseline covariates . In figure 2, it can be observed that indeed practically does not depend on in the HELIOS trial.

E.4.2 Hypothetical estimand: IPCW estimators

Only baseline covariates as predictors

| Variable | Coefficient | SE | -value |

| STRATA1 (1) | -0.1544 | 0.1663 | 0.353 |

| STRATA2 (yes) | 0.3037 | 0.1968 | 0.123 |

| SEX (man) | 0.1609 | 0.1750 | 0.358 |

| AGE | -0.0034 | 0.0086 | 0.694 |

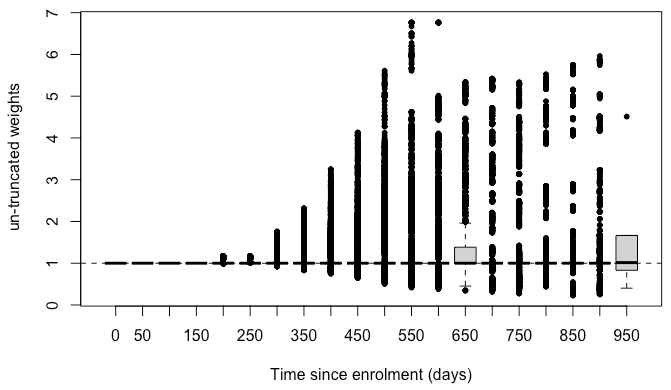

(To make the plot more clear, only weights per 50 days are shown)

Min: 1.00, 1st quantile: 1.00, median: 1.073, mean: 1.33, 3rd quantile: 1.48, max: 4.97.

Baseline covariates and indicator for PD as predictors

| Variable | Coefficient | SE | -value |

| STRATA1 (1) | -0.1539 | 0.1663 | 0.355 |

| STRATA2 (yes) | 0.3024 | 0.1968 | 0.124 |

| SEX (man) | 0.1600 | 0.1750 | 0.361 |

| AGE | -0.0034 | 0.0086 | 0.693 |

| Variable | Coefficient | SE | -value |

| STRATA1 (1) | 0.3202 | 0.1776 | |

| STRATA2 (yes) | 0.0560 | 0.2093 | 0.7890 |

| SEX (man) | 0.0057 | 0.1865 | 0.9754 |

| AGE | 0.0129 | 0.0087 | 0.1357 |

| PD | 22.225 | 2.906 | 0.9939 |

(To make the plot more clear, only weights per 50 days are shown)

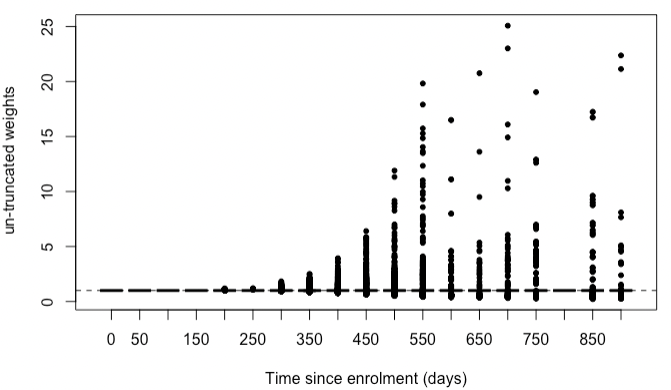

Min: 0.23, 1st quantile: 0.91, median: 1.00, mean: 1.02, 3rd quantile: 1.00, max: 25.07.

Baseline covariates, indicator for PD and time since PD as predictors

| Variable | Coefficient | SE | -value |

| STRATA1 (1) | -0.1539 | 0.1663 | 0.355 |

| STRATA2 (yes) | 0.3024 | 0.1968 | 0.124 |

| SEX (man) | 0.1600 | 0.1750 | 0.361 |

| AGE | -0.0034 | 0.0086 | 0.693 |

| Variable | Coefficient | SE | -value |

| STRATA1 (1) | 0.2025 | 0.1771 | 0.2528 |

| STRATA2 (yes) | 0.1918 | 0.2092 | 0.3594 |

| SEX (man) | 0.0265 | 0.1828 | 0.8848 |

| AGE | 0.0071 | 0.0089 | 0.4270 |

| PD | 22.31 | 2.517 | 0.9929 |

| Time since PD | -0.0036 | 0.0009 |

(To make the plot more clear, only weights per 50 days are shown)

Min: 0.23, 1st quantile: 0.98, median: 1.00, mean: 1.41, 3rd quantile: 1.47, max: 6.76.