Robust Social Welfare Maximization via Information Design in Linear-Quadratic-Gaussian Games

Abstract

Information design in an incomplete information game includes a designer with the goal of influencing players’ actions through signals generated from a designed probability distribution so that its objective function is optimized. We consider a setting in which the designer has partial knowledge on agents’ utilities. We address the uncertainty about players’ preferences by formulating a robust information design problem against worst case payoffs. If the players have quadratic payoffs that depend on the players’ actions and an unknown payoff-relevant state, and signals on the state that follow a Gaussian distribution conditional on the state realization, then the information design problem under quadratic design objectives is a semidefinite program (SDP). Specifically, we consider ellipsoid perturbations over payoff coefficients in linear-quadratic-Gaussian (LQG) games. We show that this leads to a tractable robust SDP formulation. Numerical studies are carried out to identify the relation between the perturbation levels and the optimal information structures.

I Introduction

An incomplete information game is comprised of multiple agents who takes actions which maximizes their utilities depending on actions of other agents and unknown states. Incomplete information games are used to model federated edge learning [1], electricity spot market [2], cyber defense in EV charging [3] and traffic flow in communication or transportation networks [4, 5].

Information design problem entails decision over informativeness of signals given to agents regarding the payoff state so that induced actions maximize a system level objective. Information designer as an entity commits to an optimal probability distribution of signals conditional on payoff states before state realization (for an example in pandemic control see Fig. 1). The selected distribution maximizes the designer objective and adheres to equilibrium constraints. Various entities such as social media companies [6], advertisements platforms [7] and public health agencies [8] could be considered as information designers. In control systems, information design is employed for routing games [9], Vehicle-to-Vehicle communication [10], and queue management under heterogeneous users [11].

In this paper, we propose a robust optimization approach to the information design problem considering the fact that the designer cannot know the players’ payoffs exactly. Indeed, while the designer may be knowledgeable about the payoff relevant random state, it may have uncertainty about the payoff coefficients of the players. For instance, in the pandemic control example (Fig. 1) above while the public health department may have near-certain information about the potential risks of a disease or intervention, it may not know how the society weights the risks and benefits in their decision-making. Here, we assume the designer has partial knowledge about players’ utilities, and wants to perform information design over the payoff relevant states.

When the payoffs of the players are unknown, the designer cannot be sure of the rational behavior under a chosen information structure. We formulate this problem as a robust optimization problem where the designer chooses the “best” optimal information structure for the worst possible realization of the payoffs. That is, we do not make any assumptions on the distribution of the players’ payoff coefficients.

Specifically, we assume the players have linear-quadratic payoffs with coefficients unknown by the designer. We further assume that the payoff relevant states and signals generated by the designer come from a Gaussian distribution. In this setting, we show that the robust information design with the goal to maximize social welfare can be formulated as a tractable SDP given ellipsoid perturbations on the payoff coefficients–see Theorem 1.

In Bayesian persuasion literature, robustness is explored in worst case, online and various other settings [12, 13, 14, 15, 16]. For instance, [17] considers information design where the designer learns unknown utilities via auctions. Instead, here we consider the multi-player setting, i.e., information design, and assume an incomplete information game among the players. In our setting, the designer maximizes the worst-case objective under the rational behavior.

I-A Notation

We use to denote the element in the th row and th column of matrix . For matrices and . We use to represent the Frobenius product, e.g., . We use and to represent the set of symmetric and symmetric positive semi-definite matrices, respectively. Trace of a matrix is denoted with . indicates an identity matrix. is a column vector of all ones.

II Generic Robust Information Design Problem for Welfare Maximization

An incomplete information game involves a set of players belonging to the set , each of which selects actions to maximize the expectation of its individual payoff function where , , and correspond to an action profile, a payoff state vector, and a payoff parameter, respectively. The payoff state of player directly influences agent ’s payoff, and is unknown by the player. Agent forms expectation about the payoff state based on its signal/type . The payoff coefficients are unknown to the designer, but known to the players. We represent the incomplete information game given by the tuple . We use to refer to the set of games parameterized by .

The information designer does not know that actual payoff parameter , but knows that the game played belongs to . An information designer aims to maximize a system level objective function , e.g., social welfare, that depends on the actions of the players (), and the state realization () by deciding on an information structure belonging to the feasible space of probability distributions on the signal space given a game with payoff coefficients . The information structure determines the fidelity of signals that will be revealed to the players given a realization of the payoff state .

We introduce social welfare as a design objective.

Definition 1 (Social Welfare)

Social welfare design objective is the sum of individual utility functions,

| (1) |

Social welfare is a common design objective used in congestion [5], global [18] or public goods games [8].

A strategy of player maps each possible value of the private signal to an action , i.e., . A strategy profile is a Bayesian Nash equilibrium (BNE) with information structure of the game , if it satisfies the following inequality

| (2) |

for all , and is the equilibrium strategy of all the players except player , and is the expectation operator with respect to the distribution and the prior on the payoff state . We denote the set of BNE strategies in a game with

In this paper, the designer does not make any distributional assumptions on the payoff parameter , and aims to select the best signal distribution for the worst case scenario, i.e.,

| (3) |

Inner optimization problem in (3) evaluates to the designer’s objective under the worst possible payoff parameter realization and BNE actions given a signal distribution . The designer wants to do the best it can to maximize the system objective assuming the realization of the worst-case scenario.

We denote the optimal solution to (3) by . Given the robust optimal information structure , the information design timeline is given in the following:

-

1.

Designer notifies players about

-

2.

Realization of payoff state , and payoff parameter with subsequent draw of signals from

-

3.

Players take action according to BNE strategies under information structure

The generic robust information design problem in (3) is not tractable in general. In the following we make assumptions on the payoff structure and the signal distribution to attain a tractable formulation.

II-A Linear-Quadratic-Gaussian (LQG) Games

An LQG game corresponds to an incomplete information game with quadratic payoff functions and Gaussian information structures. Specifically, each player decides on his action according to a payoff function

| (4) |

where and that is a quadratic function of player ’s action, and is bilinear with respect to and , and and . The term is an arbitrary function of the opponents’ actions and payoff state . We collect the coefficients of the quadratic payoff function in a matrix . The payoff parameter unknown to the designer in (4) is the coefficients matrix .

Payoff state follows a Gaussian distribution, i.e., where is a multivariate normal probability distribution with mean and covariance matrix . Each player receives a private signal for some . We define the information structure of the game as the conditional distribution of given . We assume the joint distribution over the random variables is Gaussian; thus, is a Gaussian distribution.

Next, we provide two examples of LQG games.

Example 1 (The Beauty contest Game)

Payoff function of player is given by

| (5) |

where and represents the average action of other players. The first term in (5) denote the players’ urge for taking actions close to the payoff state . The second term accounts for players’ tendency towards taking actions in compliance with the rest of the population. The constant gauges the importance between the two terms. The payoff captures settings where the valuation of a good depends on both the performance of the company and what other players think about its value [18].

Example 2 (Social Distancing Game)

Player ’s action is its social distancing effort to avoid the infectious disease contraction/transmission (see also Fig. 1). The risk of infection depends on unknown disease specific parameters, e.g., severity, infection rate, and the social distancing actions individuals in contact with agent . We define the payoff function of player as follows,

| (6) |

where the risk of infection is , is the risk reduction coefficient. In the definition of risk , denotes the risk rate of the disease such as infection rate or severity, and determines the contacts of agent and the intensity of the contacts. First term in (6) represents the cost of social distancing. Second term in (6) denotes the overall risk of infection that scales with the player’s social distancing efforts.

Next we state the main structural assumption on perturbed LQG games.

Assumption 1

We assume the following perturbation structure on the payoff matrix ,

| (7) |

where is an element of the unknown perturbation matrix which covers a given closed and convex perturbation set such that and is the constant shift.

Assumption 1 means that the parameter in game corresponds to .

III Robust Information Design under Finite Scenarios

We will reformulate the problem in (3) in order to obtain a tractable formulation. The reformulation will first entail changing the design variables from signals to actions. In order to do this, we define the distribution of actions induced by the information structure under a given strategy profile.

Definition 2 (Action distribution)

An action distribution is the probability of observing an action profile when agents follow a strategy profile under , which can be computed as

| (8) |

According to the definition, the probability of observing action profile is the sum of the conditional probabilities of all signal profiles under that induce action profile given the strategy profile .

We denote the set of equilibrium action distributions induced by BNE strategies under an information structure for game as

| (9) |

The designer can recommend actions instead of sending signals to each player, if the designer knew the payoff coefficient . In such a case, the players would follow the recommended actions because they would satisfy the obedience condition as per the revelation principle, see [19, Proposition 1]. However, this principle does not apply in the setting where is adversarially chosen. To overcome this issue, we assume the obedience condition is only satisfied in the worst case scenario. We detail our approach first in the finite-scenario case, where can take finite set of values.

We begin by stating the BNE condition in (2) by a set of linear constraints for LQG games given the payoff coefficients .

Lemma 1

Define the covariance matrix as follows:

| (10) |

For a given payoff matrix , the BNE condition in (2) can be written as the following set of equality constraints,

| (11) |

where for , and , and .

Proof:

See Appendix. ∎

The condition in (11) ensures that is a Bayesian correlated equilibrium (BCE), see [19] for a definition.

In the following, we express the robust information design problem under a finite set of scenarios as a mixed integer SDP.

Proposition 1 (Finite-case)

Let the design objective be quadratic in its arguments with the coefficients stored in matrix , i.e., . Suppose Assumption 1 holds, and assume the design objective coefficients do not depend on . Consider a finite perturbation vector with scenarios, and let refer to perturbation vectors corresponding to one of the scenarios . We can express the robust information design problem in (3) as the following mixed-integer SDP:

| (12) | ||||

| s.t. | ||||

| (13) | ||||

| (14) | ||||

| (15) |

where is defined in (10), is given as:

| (16) |

is given as:

| (17) |

and refer to the elements of the perturbation vector with

| (18) |

Proof:

We can express the expected objective using the Frobenius product as follows,

| (19) | ||||

| (20) |

where and note that denotes the th submatrix.

Let be the worst-case scenario from the perspective of the designer. The designer chooses that maximizes its objective subject to rational behavior of players in the worst case scenario. As per Lemma 1, we have

| (21) | |||

| (22) |

We rewrite (22) in terms of matrices as in (16) and as in (10) to obtain (13). Minimization over enforces the constraint among the set of constraints in (13) to be selected. Constraint (15) corresponds to the assignment of to Constraint (15) is not affected by perturbations to ∎

According to the formulation in (12)-(15), the solution can entail finding the covariance matrix that maximizes for each scenario , and then picking the smallest among them. We note that an alternative equivalent formulation can entail covariance matrices, i.e., , and leave out the integer variables .

We use the scenario-based formulation (12)-(15) to motivate the tractable robust design formulations under ellipsoid and interval formulations. For illustration purposes, consider scenarios. Assume scenario is the worst case scenario, i.e., and . In such a case, will satisfy the BNE condition (22) for exactly while the BCE condition will be approximately satisfied for . Specifically, we have

| (23) | |||

| (24) | |||

| (25) |

We can interpret this relation as the optimal solution to (12)-(15) being induced by an approximate BNE for the good scenario . That is, is not necessarily incentive compatible with players’ realized payoffs. In the following, we leverage this observation to develop robust convex program for social welfare objective when the perturbation set is an ellipsoid.

IV An SDP Formulation for Social Welfare Maximization via Information Design

Under convex uncertainty sets, the number of scenarios goes to infinity. Thus, we cannot enforce exact BCE explicitly for the worst-case scenario, and annul the other cases using integer variables as is done in (12)-(15). Instead, we relax the BCE constraint in (11) as follows

| (26) |

where is a finite large-enough constant. Consider the following ellipsoid uncertainty subsets :

| (27) |

We take the social welfare (Example 1) as the designer’s objective , which depends on the payoff matrices .

Theorem 1

Assume is given by (7) and perturbation vectors exhibit ellipsoid uncertainty (27) and the objective is social welfare maximization with

| (28) |

The robust convex program under the welfare maximization objective is as follows:

| (29) | ||||

| s.t. | (30) | |||

| (31) | ||||

| (32) |

where matrices and are as defined in (16) and (17), respectively.

Proof:

See [20] on how to express the social welfare objective in (1) using (28), and in form . We start by writing the social welfare objective constraint under ellipsoid uncertainty:

| (33) |

Here we consider all elements of perturbation matrix for ellipsoid perturbations:

| (34) |

Using (34), we will obtain a robust counterpart for semi-infinite constraint (33). We start with writing (33) as a perturbation maximization problem:

| (35) |

Next, we substitute with (7) into (26):

| (36) |

We can rewrite (36) in terms of matrices and as in (10):

| (37) |

Similarly, we write the perturbation maximization problem over uncertain constraint (37) under ellipsoid uncertainty as

| (38) |

where is given by (1). Solution to (38) give us the tractable constraint (31).

Constraint (32) enforces assignment of known covariance matrix of payoff states, to the respective place in . ∎

The equilibrium constraints given in (31) make sure the recommended action distribution is an approximate BCE for every realization of the payoff coefficients matrix.

V Numerical Experiments

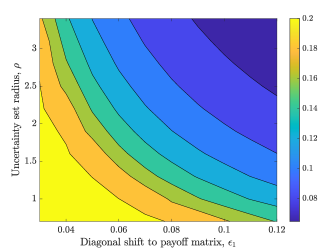

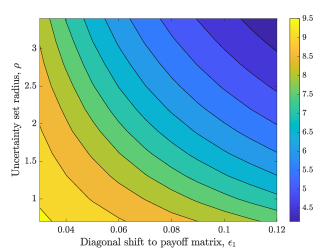

We consider a designer that wants to maximize the social welfare of players. The designer knows the perturbed payoff coefficients given as follows: for , and for , . The variance of the unknown payoff state is given as follows: for , and for . We consider ellipsoid perturbations with and let . Given the setup, we solve the robust convex program (29)-(32) in order to obtain the robust optimal information design .

We analyze the effects of shifts defined in (7) by assuming the diagonal elements and off-diagonal elements of shift matrix are homogeneous, i.e., and for all for constants and .

In order to systematically analyze the effects of the shifts, we fix the off-diagonal shifts to a small value , and vary the diagonal shift . Fig. 2(a) shows that as the uncertainty ball radius and diagonal shift increases, the optimal information structure remains a partial information disclosure but gets closer to the no information disclosure. Fig. 2(b) shows that social welfare decreases under increasing uncertainty.

|

| (a) |

|

| (b) Optimal objective value |

We can discuss Fig. 2 in terms of the beauty contest game, which is a supermodular game. If we consider the common goods in the beauty contest game as a stock, we see that a social welfare maximizing information designer, i.e. the company whose stock is traded releases less information about stock price , when the uncertainty about its shareholder’s payoff coefficients increases.

VI Conclusion

The paper considered the problem of designing information structures in incomplete information games when the designer does not know the game payoffs exactly. This is a common situation in many real-world settings, where the game payoffs are often uncertain due to various factors such as incomplete information, imperfect modeling, or unknown parameters. Specifically, we considered information design for the setting when the unknown payoff parameters are adversarially chosen. For the robust information design problem, we developed a tractable SDP formulation given quadratic payoffs, Gaussian signal distributions, ellipsoid perturbations to the unknown payoff parameters, and social welfare as the design objective. Numerical experiments show that the designer would choose to reveal less information about the payoff states to the players as its uncertainty about the players’ payoffs grow. This suggests that in situations where the game payoffs are highly uncertain, it may be more optimal to not disclose any information at all rather than risk providing misleading information.

References

- [1] M. Hu, W. Yang, Z. Luo, X. Liu, Y. Zhou, X. Chen, and D. Wu, “Autofl: A bayesian game approach for autonomous client participation in federated edge learning,” IEEE Transactions on Mobile Computing, pp. 1–15, 2022.

- [2] P. P. Verma, M. R. Hesamzadeh, R. Baldick, D. R. Biggar, K. S. Swarup, and D. Srinivasan, “Bayesian nash equilibrium in electricity spot markets: An affine-plane approximation approach,” IEEE Transactions on Control of Network Systems, vol. 9, no. 3, pp. 1421–1434, 2022.

- [3] Z. Yang, Y. Xiang, K. Liao, and J. Yang, “Research on security defense of coupled transportation and cyber-physical power system based on the static bayesian game,” IEEE Transactions on Intelligent Transportation Systems, vol. 24, no. 3, pp. 3571–3583, 2023.

- [4] P. N. Brown and J. R. Marden, “Studies on robust social influence mechanisms: Incentives for efficient network routing in uncertain settings,” IEEE Control Systems Magazine, vol. 37, no. 1, pp. 98–115, 2017.

- [5] M. Wu, S. Amin, and A. E. Ozdaglar, “Value of information in bayesian routing games,” Operations Research, vol. 69, no. 1, pp. 148–163, 2021.

- [6] O. Candogan, “Information design in operations,” in Pushing the Boundaries: Frontiers in Impactful OR/OM Research, pp. 176–201, INFORMS, 2020.

- [7] Y. Emek, M. Feldman, I. Gamzu, R. PaesLeme, and M. Tennenholtz, “Signaling schemes for revenue maximization,” ACM Trans. Econ. Comput., vol. 2, jun 2014.

- [8] S. Alizamir, F. de Véricourt, and S. Wang, “Warning against recurring risks: An information design approach,” Management Science, vol. 66, no. 10, pp. 4612–4629, 2020.

- [9] Y. Zhu and K. Savla, “Information design in nonatomic routing games with partial participation: Computation and properties,” IEEE Transactions on Control of Network Systems, vol. 9, no. 2, pp. 613–624, 2022.

- [10] B. T. Gould and P. N. Brown, “On partial adoption of vehicle-to-vehicle communication: When should cars warn each other of hazards?,” in 2022 American Control Conference (ACC), pp. 627–632, 2022.

- [11] N. Heydaribeni and A. Anastasopoulos, “Joint information and mechanism design for queues with heterogeneous users,” 2021 60th IEEE Conference on Decision and Control (CDC), 2021.

- [12] P. Dworczak and A. Pavan, “Preparing for the worst but hoping for the best: Robust (bayesian) persuasion,” Econometrica, vol. 90, no. 5, pp. 2017–2051, 2022.

- [13] J. Hu and X. Weng, “Robust persuasion of a privately informed receiver,” Economic Theory, vol. 72, no. 3, pp. 909–953, 2021.

- [14] Y. Zu, K. Iyer, and H. Xu, “Learning to persuade on the fly: Robustness against ignorance,” arXiv preprint arXiv:2102.10156, 2021.

- [15] Y. Babichenko, I. Talgam-Cohen, H. Xu, and K. Zabarnyi, “Regret-minimizing bayesian persuasion,” Games and Economic Behavior, vol. 136, pp. 226–248, 2022.

- [16] G. de Clippel and X. Zhang, “Non-bayesian persuasion,” Journal of Political Economy, vol. 130, no. 10, pp. 2594–2642, 2022.

- [17] A. Bonatti, M. Dahleh, T. Horel, and A. Nouripour, “Coordination via selling information,” arXiv preprint arXiv:2302.12223, 2023.

- [18] S. Morris and H. S. Shin, “Social value of public information,” American Economic Review, vol. 92, no. 5, pp. 1521–1534, 2002.

- [19] D. Bergemann and S. Morris, “Information design: A unified perspective,” Journal of Economic Literature, vol. 57, pp. 44–95, March 2019.

- [20] F. Sezer, H. Khazaei, and C. Eksin, “Maximizing social welfare and agreement via information design in linear-quadratic-gaussian games,” IEEE Transactions on Automatic Control, pp. 1–8, 2023.

Appendix A Proof of Lemma 1

We start with writing the first order condition equivalent to (2) for a given :

| (39) |

We solve (A) for the best response :

| (40) |

We look for an equilibrium strategy of the form given below:

| (41) |

where and are constants and constant vectors, respectively. We plug (41) into the first order condition (40):

| (42) |

. Via conditional expectation rule over multivariate normal distribution, we obtain following:

| (43) |

. Vectors and constants are determined by following set equations when we separate (43) into respective parts:

| (44) |

| (45) |