capbtabboxtable[][\FBwidth]

Identification of Ex ante Returns Using Elicited Choice Probabilities

Abstract.

This paper studies the identification of perceived ex ante returns in the context of binary human capital investment decisions. The environment is characterised by uncertainty about future outcomes, with some uncertainty being resolved over time. In this context, each individual holds a probability distribution over different levels of returns. The paper uses the hypothetical choice methodology to identify nonparametrically the population distribution of several individual-specific distribution parameters, which are crucial for counterfactual policy analyses. The empirical application estimates perceived returns on overstaying for Afghan asylum seekers in Germany and evaluates the effect of assisted voluntary return policies.

Keywords: Subjective expectations; ex ante returns; nonparametric; semiparametric; distribution regression; asylum seekers.

JEL codes: C20, D84, F22, J15, J18, J61, O15.

1. Introduction

A is an asylum seeker whose asylum claim has been rejected and is required to leave her host country within 30 days. When asked by a researcher: ‘what is the chance that you will overstay at the end of the 30-day grace period?’, she answers 60 percent. A’s answer conveys at least two information: (1) her perception about the returns on overstaying at the time she will take the decision, and (2) her uncertainty about possible changes in this perception between the time she is asked about her future decision, and the time she will take the actual decision 30 days later.111This point is made, for example, by Manski, (1999)

A’s perception of returns at the time of elicitation is known as her ex ante returns. These returns encompass both perceived pecuniary and non-pecuniary benefits attached to her choice as compared to her next best alternative. They can be measured by the pecuniary transfer that would make A indifferent between staying and leaving. Because of the uncertainty about possible shocks between the time of elicitation and the time of decision, A’s ex ante returns are best described by a probability distribution over different levels of returns. This probability distribution is individual-specific and is characterised by distribution parameters: mean, spread, or more generally, quantiles. Furthermore, each asylum seeker sharing A’s circumstances holds such private distribution of ex ante returns. Thus, aggregated at the population level, there exists a population distribution of individual-specific distribution parameters.

In recent years, probabilistic stated choice questions similar to or more complex than the one described above have become widely applied to understand individuals’ ex ante returns about several human capital decisions (e.g., education, major and career choices, migration and retirement decisions) and more general economic choices.222Examples of the use of the probabilistic stated choice methodology include Shoyama et al., (2013); Delavande and Manski, (2015); Wiswall and Zafar, (2015); Morita and Managi, (2015); Gong et al., (2019); Boyer et al., (2020); Gong et al., (2022); Arcidiacono et al., (2020). A larger literature on stated choice analysis is referenced in Koşar et al., (2021), footnotes 6 and 7. These applications pioneered by Blass et al., (2010) have largely focused on understanding mean ex ante returns and marginal effect of choice characteristics on mean returns.333In the motivating illustration, a marginal effect of interest would be, for example, the effect of an additional chance of becoming regularised in a later period on the mean returns. In an innovative contribution, Wiswall and Zafar, (2018) derived estimates of the population distribution of marginal mean returns of workplace attributes (or equivalently willingness-to-pay for these attributes).

Much less effort has been devoted to go beyond mean returns and understand the whole private distribution of ex ante returns. Yet, there exists two compelling arguments for going beyond the mean. First, for the purpose of describing individuals’ ex ante returns, distribution parameters such as quantiles give a more complete representation of both perceived returns and the associated uncertainty in the population. For example, whereas the population distribution of median ex ante returns reveals ‘typical’ expected returns, the distributions of upper and lower quantiles inform us on the whole range of returns that agents expect, and to which extent they perceive these returns as plausible. Moreover, the distribution of spreads describes the prevalence of uncertainty in the population. Finally, as the importance that agents put on some choice attributes can vary if they experience a ‘bad shock’ (low quantiles) or a ‘good’ shock (high quantiles), it is essential to investigate quantile effects as well as mean effects of choice characteristics.

Second, for the purpose of policy evaluation, one goal of stated preference analyses is to predict individuals’ outcomes and choice behaviour as a result of a (policy) change in their environment. Relying on an analysis of mean returns, although simple, can be short-sighted. High uncertainty signals that agents expect important variations in their ex ante perception and the mean might not be very informative about their outcome or future choice. Instead, understanding the whole private distribution of ex ante returns can be an important asset. More specifically, at the time of decision, the resolution of uncertainty will generate a mixture of shocks in the population. For some individuals, the realised uncertainty will correspond to the first quantile of their expectations, for others to the second quantile, to the third and so on. Thus, if preferences are stable, the realised distribution of returns, the main device for counterfactual analyses, will be a mixture of the distributions of quantile. The latter does not necessarily correspond to the distribution of mean (or median) returns. Yet, it can be estimated from the distributions of quantile, for any given prior of the policy maker about the accuracy of individuals’ perception. Thus, going beyond mean returns to identify distributions of quantile appears quintessential for careful policy evaluation.

The paper derives nonparametric identification results for the distribution of individual-specific quantiles, quantile effects, mean returns, mean effects, and spread of resolvable uncertainty. To the best of my knowledge, this is the first paper to propose a nonparametric characterisation and identification of these objects. They are defined formally in Section 3. For ease of language, they are referred to as to the population distributions of interest rather than as to the population distributions of individual-specific distribution parameters.

The identification result applies to a general model of human capital investment with uncertainty, for which the introductory example about the decision to overstay provides a prototypical illustration. Individuals make a binary investment choice (overstay or leave) in an environment characterised by uncertainty about their future outcomes (earning some income in the host country, being deported, becoming regularised). Some but not all uncertainty is resolved at the time of decision. In this context, individuals form subjective expectations about their outcomes and the nature of uncertainty. Further examples of related decisions include education investment, health investment, college major or occupation choices, job search, mobility and retirement decisions.

The paper considers the identification of the distributions of interest from the perspective of a (probabilistic) stated choice analysis (or stated preference analysis). Contrary to the revealed preference approach, which relies on observation of actual choices, the stated preference approach elicits individuals’ intended choice, often in hypothetical scenarios, alongside beliefs about choice characteristics (or attributes). The increasing interest in the stated preference approach stems from its advantages over the revealed preference approach. It avoids assumptions about agents’ belief formation and equilibrium allocation mechanisms, while being a more natural approach to questions pertaining to ex ante perceptions. Researchers can exploit hypothetical choice scenarios in stated choice analyses to tackle the pervasive problem of endogeneity arising because not all relevant beliefs and characteristics can be observed.444A main question is whether the elicited intentions predict actual decisions. This is not addressed in this research. However, there is growing evidence that carefully designed elicitations have predictive power in several contexts (see, e.g. Hurd,, 2009; Bah and Batista,, 2018; de Bresser and van Soest,, 2019; Arcidiacono et al.,, 2020).

A key contribution of the present paper is to demonstrate a further advantage of the stated preference analysis: it can recover rich information on individuals’ perception of returns and resolvable uncertainty. The literature on probabilistic stated choice has devoted little attention to the potential insights on individual-specific distribution parameters so far. Yet, these distribution parameters are useful for forming a better understanding of agent choices and essential for appropriate counterfactual analyses.

As a second contribution, the paper shows nonparametric identification of the population distributions of interest under mild assumptions and for a simple elicitation design. This is a significant contribution to the stated preference literature, which relies almost exclusively on parametric assumptions about individuals’ utility function and the resolvable uncertainty. The benefits and limitations of the parametric approach are discussed in Section 2.

In this paper, identification of the distributions of interest proceeds in two steps. In a first step, Section 4.1 shows that the population distributions of interest can be written as functional of two structural objects: (i) the structural function that maps observed and unobserved beliefs and characteristics into individuals’ probabilistic choices, and (ii) the joint distribution of observed and unobserved beliefs and characteristics. The main assumption is that there exists a set of traits and information, potentially unobserved, that determine the distribution of resolvable uncertainty. The characterisation result relates to a similar characterisation of the marginal distributions of equivalent variation and compensation variation in discrete choice models by Bhattacharya, (2015) (Theorem 1, p. 626).

In a second step, Section 4.2 shows that (i) and (ii) are recoverable from the joint distribution of intended choice and observed beliefs for a simple elicitation strategy and under mild assumptions. The elicitation strategy is as follows: the researcher elicits both actual beliefs and intentions and beliefs and intentions in a limited number of counterfactual/hypothetical scenarios. At least one of the hypothetical scenarios is common to all respondents. Hence, the data required for identification is similar to the data routinely collected for generic probabilistic stated choice analyses, except for the need of at least one common scenario. For example, as long as one common scenario is introduced, the identification and estimation procedures can accommodate the common elicitation strategy where scenarios are anchored in individuals’ actual experience and only the extent of departures from this scenario varies experimentally.

When the unobserved heterogeneity can be summarised by a unidimensional random variable, the identification problem translates into the identification of a nonadditive panel model with an individual fixed effect. One common hypothetical scenario is enough for identification. In this case, the identification result can be seen as an application of existing identification results in panel models with nonseparable fixed effects and classical measurement error on the outcome variable, in particular, the result of Evdokimov, (2010). The novelty is the application of the latter result to models of stated preference with data generated from a pseudo-panel.

When the unobserved heterogeneity is multidimensional, a random coefficient representation is introduced to model the quantile functions of (i) and (ii). Under this assumption, when the unobserved heterogeneity is two-dimensional, two common hypothetical scenarios are enough, when three-dimensional, three scenarios, and so forth. Thus, by introducing several hypothetical scenarios, one can consider a larger dimension of unobserved heterogeneity. In this case, the identification result extends the result of Evdokimov, (2010).

The third methodological contribution is a tractable estimation procedure introduced in Section 5. Starting from the constructive proof of identification, the paper provides a semiparametric procedure that builds on recent developments in distribution regression estimators such as Chernozhukov et al., (2013), Melly and Santangelo, (2015) and Chernozhukov et al., (2020).555Nonparametric estimation is feasible but comes with strong data requirements and the curse of dimensionality. In particular, estimation of the (i) and (ii) requires estimation of conditional CDFs. Appendix C provides a semiparametric approach for estimating these conditional CDFs. It is important to note that, unlike traditional approaches to models with subjective expectations, parametric assumptions are not introduced for the purpose of identification, but to alleviate strong data requirements for the purpose of estimation. In particular, in the case where the measurement error of the stated intention is negligible, it supplies a very simple two-stage estimator to recover the distributions of quantile in the population. To account for measurement error of these stated intention, the paper proposes an equally tractable bound approach that preserves the simplicity of the estimator. Inference uses a weighted bootstrap procedure, for which an asymptotic theory is developed in Appendix D.

The main advantages of the proposed approach are the following:

-

(1)

There is no need to impose a parametric and/or common distribution of the resolvable uncertainty.

-

(2)

There is no need to assume linearity and separability of individuals’ utility.

-

(3)

The number of hypothetical scenarios can remain limited and depends on the extent of unobserved heterogeneity one wishes to consider.

-

(4)

Estimation is feasible with usual econometric tools.

-

(5)

One can easily go beyond an analysis of mean and analyse quantiles of returns within the same econometric framework.

Thus, the proposed approach complements well the existing approaches in the stated preference literature presented in Section 2. It is especially appropriate when the researcher is unwilling to impose strong parametric assumptions, is interested in parameters derived from the resolvable uncertainty, needs to limit the number of counterfactual scenarios, or wishes to assess the sensitivity of their findings to parametric assumptions. Finally, it permits richer counterfactual analyses as illustrated in the empirical application.

The final contribution of the paper is empirical. The framework is used to estimate asylum seekers’ perceived returns on overstaying, with unique data on Afghan asylum seekers in Germany, the largest group of overstayers in the country. Section 6 gives unprecedented insights on the ex ante returns for this population. It also illustrates the meaningfulness of the estimates for the purpose of policy evaluation by evaluating the cost-effectiveness argument for a voluntary return policy. Within this application, semiparametric estimates of the distributions of quantile suggest that the common parametric assumption of a symmetric logistic distribution for the resolvable uncertainty may be incorrect. Moreover, the result shows that observing the distribution of quantiles allows a richer analysis than would be permitted by observing the distribution of mean (or median) returns only. As such, the paper contributes to a growing literature investigating migration decisions and migration policies using the elicited expectation framework (e.g. McKenzie et al.,, 2013; Hoxhaj,, 2015; Baláž et al.,, 2016; Lagakos et al.,, 2018; Koşar et al.,, 2021). Closely related to the present paper, Mbaye, (2014) and Bah and Batista, (2018) look at the effect of individual expectations on the decision to migrate illegally. In particular, Bah and Batista, (2018) emphasise the importance of the perceived chance of becoming regularised for the intention to migrate irregularly. Whereas previous contributions look at economic migrants, the focus of the current study is on a population of asylum seekers who have already arrived in the host country but face a significant risk of irregular stay. Asylum seekers with a rejected application form a large proportion of migrants with a legal obligation to leave Germany. The findings in this paper confirm the salience of subjective beliefs about the chance of becoming regularised in the future. They also speak against the cost-effectiveness argument for assisted voluntary return policies, as discussed in Section 6.

The rest of the paper is organised as follows. Section 2 summarises the main empirical approaches to the estimation of (marginal) ex ante returns using the probabilistic stated choice framework. Section 3 formally defines the population distributions of interest. Section 4 describes identification results for these distributions under a simple elicitation mechanism. Additional identification results and their main proofs are collected in the Appendix A and B, respectively. Section 5 discusses estimation briefly, with more details about estimation, inference and asymptotic theory provided in Appendix C and D. Section 6 presents the empirical analysis. Finally, Section 7 concludes the paper.

2. Existing Empirical Approaches to Stated Choice Models

The paper is part of an active literature on the identification and estimation of ex ante returns (and option values), which are understood as fundamental drivers of individuals’ decisions. Most contributions use a revealed preference approach (Heckman et al.,, 2006; Heckman and Navarro,, 2007; Stange,, 2012; Trachter,, 2015; Lee et al.,, 2015; Eisenhauer et al.,, 2015; Bhuller et al.,, 2022). The use of the stated preference approach makes this research closer to Wiswall and Zafar, (2018); Koşar et al., (2021) and Arcidiacono et al., (2020).Wiswall and Zafar, (2018) and Koşar et al., (2021) use an hypothetical choice analysis with parametric assumptions, discussed in further depth below, to recover the population distribution of marginal mean ex ante returns associated to different choice attributes. This research adds to this literature by studying for the first time individual-specific parameters associated to the private distribution of ex ante returns. In particular, it presents important results for the identification and understanding of the resolvable uncertainty, which is absent from the revealed preference framework and often neglected in the existing stated preference literature.

The paper also directly contributes to the relatively recent and growing literature using stated choice analysis with probabilistic elicited choice. Within this literature, it has become common to exploit the survey design to remedy an endogeneity problem that arises because observed and unobserved beliefs are correlated. An approach to use the survey design taken, for example, by Wiswall and Zafar, (2015); Ruder and Van Noy, (2017); Baker et al., (2018); Bleemer and Zafar, (2018) consists in eliminating the dependence between observed and unobserved beliefs through a linear fixed effect methodology. To achieve this goal, these studies elicit beliefs and intended choices twice, providing an information treatment between the two elicitation waves. For the linear fixed effect methodology to purge endogeneity, this approach rests critically on (i) the assumption that the treatment shifts both beliefs and expected behaviour/outcome, otherwise, one ends up regressing on noise, and (ii) the linear structure of the fixed effect.

Several studies choose instead to elicit choices in hypothetical (counterfactual) scenarios (e.g. Blass et al.,, 2010; Bah and Batista,, 2018; Wiswall and Zafar,, 2018; Maestas et al.,, 2018; Adams-Prassl and Andrew,, 2019; Koşar et al.,, 2021; Ameriks et al., 2020a, ; Ameriks et al., 2020b, ; Boyer et al.,, 2020; Fuster and Zafar,, 2021). In most cases, the hypothetical scenarios are created by inducing random variations from a baseline scenario that corresponds to the respondent’s actual beliefs and characteristics. To better appreciate the contribution of the present paper, it is useful to review the state-of-the-art approach to identification and estimation in the existing literature. This approach has been pioneered by Blass et al., (2010), and further developed, for example, by Wiswall and Zafar, (2018).

The starting point is an agent that faces a binary human capital investment decision (with choice options 0 and 1) in a series of scenarios . The actual decision does take place not at the time of elicitation but in a foreseeable future, so that it is important to distinguish between three consecutive periods: the time of elicitation, the time of decision and the time of outcome realisation. Scenarios refer to the time of decision and can be hypothetical, or refer to the actual beliefs of individuals. Throughout the paper, the scenario will denote the actual scenario, and the counterfactual scenarios. Each scenario is characterised by utility shifters observed by the analyst. More specifically, the analyst observes the expected income and a set of choice attributes (or beliefs about them), . When the scenarios are hypothetical, are experimentally varied by the analyst.

In addition to beliefs about choice characteristics , the analyst also observes ’s stated intention to choose option 1 over option 0 at the time of decision in scenario, . Uncertainty about the final choice stems from the fact that stated intentions are elicited before an actual decision is taken. Between the time of elicitation and the time of decision, anticipates a shock that may shift their utility. This shock is unobserved by both the analyst and the agent at the time of elicitation.

The most common approach to identification of preference parameters is for the researcher to posit an Additive Random Utility Model where , the utility of agent for choice in a given scenario , is given by:

| (2.1) |

Note that subsumes the utility of choice characteristics that do not change across scenarios and are not observed by the researcher. Hypothetical scenarios cannot account for all relevant characteristics (Blass et al.,, 2010). Therefore, they are incompletely defined, and different respondents impart different beliefs on these unobserved characteristics.

The ex ante returns on choosing option 1 in scenario , i.e. the pecuniary transfer that makes indifferent between option 1 and option 0, is given by the expression:

This quantity can also be interpreted as the willingness to pay to secure option 1. The resolvable uncertainty subsumed by is unobserved by both the agent and the analyst at the time of elicitation. Uncertainty about will be resolved at the time of decision. Meanwhile, the agent is assumed to hold a probability distribution of , say .

For identification, is often assumed to have a logistic distribution, i.e. has an Extreme Value Type 1 (EVT-1) distribution. Therefore, for , the log-odds of choosing of 1 over 0 in scenario is given by:

| (2.2) |

Note that the stated intention, , is allowed to differ from the true intention , because of a (classical) measurement error . Respondents are allowed to make mistake while reporting their intended choice. For example, it is common that respondents round the percentage chance to the next multiple of five of ten.

Provided and the researcher can observe a sufficient number of linearly independent scenarios for each agent , are identified from the data available to the researcher . Hence, the parametric, individual-specific distribution of ex ante returns is identified and given by:

| (2.3) |

Furthermore, the population distribution of quantiles from these distributions can be obtained by aggregation of the individual distributions.

In practice, the independence condition between observed beliefs and unobserved taste shifters is ensured by elicitation of intended choices in exogenous scenarios. However, it precludes using ’s actual beliefs for identification. For estimation, Equation (2.2) is estimated for each individual using a Least-Absolute Deviation estimator, which is robust to rounding and measurement error of the stated intention.666An alternative is to assume a further parametric distribution for and perform a maximum likelihood estimation.

The key assumptions for the validity of the above procedure are: (1) the additive separability of the utility, (2) the parametric specification of the resolvable uncertainty, and (3) the existence of a large enough number of scenarios for each individual. The additive separability (1) is restrictive. It implies, for example, that changes in the returns of each option depend on the expected variation of beliefs, and not on their levels. The choice of an EVT-1 distribution (2) is often made for convenience and has no compelling motivation, as acknowledged by Blass et al., (2010). Finally, the more attributes one considers, the larger the required number of scenarios (3) is, and the greater the complexity of the survey instrument. A high complexity makes it difficult for the respondent to parse out the relevant variations across scenarios and increases the cognitive cost of completing a questionnaire.777For example, Wiswall and Zafar, (2018) use up to 16 scenarios, Koşar et al., (2021), up to 22 scenarios.

The main innovation of the present paper is its analysis of a richer set of objects with a weaker set of assumptions: it provides identification results for the population distributions of quantiles and means of ex ante returns, quantile and mean effects of choice characteristics, and the dispersion of resolvable uncertainty, all these without imposing parametric restrictions on the resolvable uncertainty and the individuals’ utility.

3. Parameters of Interest

This section defines the population distributions of interest in a model where agents’ utility is not linearly separable. The discussion proceeds in two main steps: Section 3.1 introduces a more general model of individuals’ intended decision given their characteristics and beliefs about possible outcomes in the future. In this framework, individuals are uncertain about the returns to their choice and form subjective beliefs given their information set. Thus, each individual holds a private distribution of returns defined in Section 3.2. These private distributions are described through their quantiles and means. Aggregated at the population level, the private distributions give rise to probabilistic distributions of quantiles.

3.1. Conceptual Framework, Timing and Notations

The model describes the investment choice of an individual who seeks to maximise their perceived ex ante utility. The following exposition includes the empirical application as a motivating example. The paper adopts the convention that multivariate vectors are written in bold characters. Greek letter symbols pertain to variables unobserved by the analyst. Apart from Greek letter symbols, random variables and vectors are presented with capital letters.

The main ingredients consist of two sectors (e.g. migrate or stay, college degree or no college degree, STEM or non-STEM major, retire early or at the normal age) with their attached expected utility, . For each agent , the utility depends on an expected income stream attached to each sector, , and on a vector of choice characteristics, (e.g. chance of finding a job in the destination country, finding a job related to the degree, contracting a chronic disease). The pecuniary benefit of choosing over will be of singular importance, so we denote it . The expected incomes and choice characteristics are observable for the agent and the researcher. They can be manipulated by the researcher in different hypothetical scenarios as described later in this section. These observable choice characteristics will be summarised in a vector:

Not all relevant beliefs are observed by the researcher, and there exists a utility shifter that is known to agent only, .888The vector also encompasses beliefs about relevant moments of , which are not elicited by the analyst. At this stage, can be a multidimensional heterogeneity, with unrestricted finite dimension. Denote its supports.999It is straightforward to introduce a vector of individual observable characteristics (e.g., gender, education,age, etc.) as an argument in the utility function. In the remaining analysis, model, assumptions, and theoretical results are understood to be conditional on a such set of observed covariates .

To discuss the role of the resolvable uncertainty, the model distinguishes as before between three consecutive periods: the time of elicitation, the time of decision and the time of outcome realisation. This sequentiality introduces uncertainty about the final decision. The uncertainty stems from the fact that ’s beliefs are elicited before the actual decision and perceived utility might be affected by additional shocks and learning between the time of elicitation and the time of decision. These shocks are summarised by the random variable . This uncertainty will be resolved for the agent at the time of decision, but is never observed by the analyst. Given a realisation of at the time of decision, ’s choice is described by:

| (3.1) |

However, at the time of elicitation, is unobserved to the agent and he or she is assumed to entertain probabilistic beliefs about the magnitude of these shocks conditional on their information set, . Denote by this distribution. There is no other resolvable uncertainty; the uncertainty about is assumed to be unresolved at the time of decision.101010In this version of the model, agent does not update their belief about upon observing at the time of decision. This “myopic” behaviour is commonly assumed in the stated choice literature and simplifies the exposition. It is possible to show that all identification results in this paper follow if the updated beliefs about is separable in . For example, let , be the expected income for choice , once agent observes . All our results carry through for , where is a real function known to agent only.

Thus, the probability to choose over , say , is obtained as follows:

| (3.2) | |||||

Equation (3.2) is a structural form representation of the intended choice. It maps observed and unobserved beliefs into the probabilistic choice. The population is characterised by the joint distribution of observed and unobserved random variables , generating a random variable of probabilistic choice .

On a sample of the population , the analyst is able to elicit beliefs about choice characteristics and the associated probabilistic stated choice. As in the motivating description of Section 2, the stated choice, say , can differ from the actual intended choice, , because of a measurement error. The analyst is also able to vary experimentally choice characteristics in a series of counterfactual scenarios denoted , and observe an associate stated choice.

Let the subscript denote scenarios. Letting denote the elicitation of actual beliefs, the analyst observes , which constitutes the data available for making inference on the parameter of interest. The analyst can never observe , which represents the sets of private beliefs held by agent . Furthermore, at the time of elicitation, remains unobserved to both agent and the analyst.

Table 3.1 provides a description of the main variables of the model, while Section 3.1.1 maps the general framework into the specific empirical application of Section 6.

| Observed | Usable for | ||

| by the | experimental | ||

| Variables | Description | analyst | variation |

| Expected income stream in choice for | |||

| scenario | Y | Y | |

| Expected pecuniary benefits of choice | |||

| over for scenario : | Y | Y | |

| Other observed choice characteristics | Y | Y | |

| Vector of observed choice characteristics | |||

| Y | Y | ||

| Stated probabilistic choice in scenario | Y | N | |

| Probabilistic choice in scenario | N | N | |

| Utility shifter unobservable for the analyst | |||

| but observed by agent | N | N | |

| Utility shifter unobservable for both analyst | |||

| and agent at the time of elicitation | N | N |

3.1.1. Example: Overstay intention of asylum seekers

In the empirical application, is an Afghan asylum seeker currently living in Germany, their choice is between staying or leaving Germany conditional on not receiving the legal right to stay (RtS). The decision to overstay is seen as a utility maximisation decision as conceptualised by Sjaastad, (1962).

The framework considers three consecutive periods: the time of elicitation, the time of decision, and the time of outcomes realisation. Belief elicitation takes place at or very close to the time when the asylum seeker learns that he or she has not received the RtS. At the time of decision, must stay in Germany without the RtS () or exit to another country (), not necessarily Afghanistan. Exit is an absorbing state in that will not return to Germany in the next period. Between the time of elicitation and the time of decision, the agent receives some information about the returns to overstaying, which solves some, but not all uncertainty about the returns to overstaying. Uncertainty is solved only in the later period of outcome realisation.

and are, respectively, the expected utility functions in Germany and abroad. For each location, ’s utility is affected by the expected present value of income: in Germany, , or abroad, . It also depends on a set of probabilities on events that shift the utility of overstaying. For example, the returns on overstaying depend on the chance of becoming regularised and the chance of being deported. The individual forms subjective beliefs about these events represented by the probability . The researcher elicits .

is a utility shifter that is not observed by the researcher, but is known to the asylum seeker. For example, it varies with the perceived level of amenities enjoyed in Germany or abroad, and the private cost of deportation. also encompasses other unobserved beliefs, such as beliefs about higher moments of , which may be pertinent in the decision to overstay but are not elicited by the analyst (for example, because of budget and time constraints in fieldwork).

summarises all unforeseeable events that may shift the utility to stay between the time of elicitation and the time of decision. Examples include sickness, mating, or improvement or deterioration of conditions in Afghanistan. It also includes the information that the agent collects on the returns on overstaying up to the time of decision. At the time of elicitation, the realisation is observed neither by , nor by the researcher; however, this uncertainty will be resolved at the time of decision, when the asylum seeker will actually decide to stay or leave.111111See, for example, Blass et al., (2010) and Wiswall and Zafar, (2015) for a thorough discussion of resolvable uncertainty.

Finally, is the intention to overstay. It is elicited with some measurement error, so that the researcher observes instead . The researcher observes the stated (possibly mismeasured) intention to overstay in scenarios, . The scenario is the actual scenario, with actual beliefs and actual intention to overstay. The subsequent scenario vary experimentally to take values , for example, setting the probability of becoming regularised to 0 and/or the pecuniary benefits to 0.

3.2. Definition of Private Ex Ante Returns

This section defines the main parameters of interest. The subsequent development omits the subscript unless necessary.

3.2.1. Ex Ante Returns

To measure the ex ante returns perceived by an individual at the time of decision, one can define the pecuniary transfer that makes this agent indifferent between both options. Specifically, define , such that:

| (3.3) |

measures the minimum compensation to give to an agent with beliefs and characteristics and resolved uncertainty to induce him to choose option 0 over option 1 at the time of decision.121212In another context, this quantity would define the willingness to pay for securing the outcome . See, for example, Maestas et al., (2018); Koşar et al., (2021). However, at the time of elicitation, is unobserved by the agent (and so is ). Because each agent entertains probabilistic beliefs about , each agent perceives a different distribution of ex ante returns. Hence, the randomness of ’s perception originates from the uncertainty about , and the variation of distribution across individuals originates from the different beliefs and information. Therefore, one can define the individual-specific quantile function of ex ante returns:

where denotes the conditional quantile function of evaluated at some , the probability between the curly brackets is over , the conditional distribution of the resolvable uncertainty.

Our interest lies in the population distribution of , which takes the form , where the probability distribution is over , the joint distribution of beliefs . This quantity characterises the proportion of the population, which expects the -quantile of returns not to exceed an amount . For example, if , and , it characterises the proportion of the population who expects that their median returns are negative.

As discussed in the introduction, ex ante returns are the fundamental drivers of individuals’ decisions. As argued, for example, by Heckman, (2010), a distinction between ex ante and ex post returns is key because “[i]n environments of uncertainty, agent choices are made in terms of ex ante calculations.” Furthermore, ex ante returns provide a measure of agents’ perceived welfare when choosing option 1 over option 0. A reliable measure of welfare matters when evaluating the potential take-up and benefits of a policy against another.

Understanding the private distributions of quantile of ex ante returns, , can be an important asset for accurate policy prediction. Indeed, at the time of decision, the resolution of uncertainty will generate a mixture of shocks in the population. For some individuals, the realised uncertainty will correspond to the first quantile of their expectations, for others to the second quantile, to the third and so on. Thus, if preferences are stable, the realised distribution of returns, the main device for counterfactual analyses, will be a mixture of the distributions of quantile, .

For example, the empirical application assesses the cost-effectiveness of assisted voluntary return policies, a cash transfer to asylum seekers to leave their host country. To perform such an analysis, a predictor of the realised distribution of returns is necessary. First, it helps to understand the transfer required at each margin of the distribution, e.g. how much should be transferred to the median individual to induce them to leave or conversely how effective is a transfer of size ? Second, because these policies are non-discriminatory, the distribution is necessary to understand the excess transfer to inframarginal individuals. See Section 6.4 for more details.

For the reasons mentioned above, the identification of ex ante returns and their distribution in the population is of interest in and of itself. The ex ante returns are also fundamental to characterise further parameters that describe individual preferences. Complementing the definition of quantiles, it is straightforward to define parameters routinely encountered in the literature:

-

(1)

Mean returns: ;

-

(2)

Quantile effects: , where and is a vector of zeros except for the -th component, which equals one.

-

(3)

Mean effects: .

Quantile and mean effects measure the contribution of a specific choice characteristic to agents’ utility; in other words, the willingness to pay for these attributes. The quantile effect measures the shift in quantile that is attributable to a change in the -th component of the vector of choice characteristics. In our empirical application, it would measure, for example, how the -quantile of returns changes with an increase in the chance of becoming regularised. The mean effect has the same interpretation.

Several studies also attempt to measure the non-pecuniary (dis)utility of investment decisions (e.g. Eisenhauer et al.,, 2015; Wiswall and Zafar,, 2018; Arcidiacono et al.,, 2020; Koşar et al.,, 2021). This is defined as the (negative) transfer to a marginal individual who perceives no pecuniary benefit, i.e., . Specifically, define , such that:

| (3.4) |

summarises utility components other than expected income differences that influence the agent’s decision. In our empirical application, it includes perceived amenities such as access to the labour market, education, social assistance, and health services or the cost associated with the risk of deportation.

3.2.2. Uncertainty

The spread of the conditional distribution of provides a useful tool to quantify the importance of (resolvable) uncertainty. One measure of this spread is the interquantile range (IQR). For any , the interquantile range for an individual with beliefs and characteristics is defined by:

| (3.5) |

If and all would share the same beliefs about as usually assumed in empirical works, the distribution of the IQR would be degenerated. In the special case where is additively separable from , the IQR defined above simplifies to the IQR of the variable . Thus, it quantifies the amount of uncertainty that the agent expects to be resolved by the time of decision.

4. Characterisation and Identification

Section 4.1 characterises the population distributions of interest given knowledge of (i) the structural function that links beliefs and characteristics to probabilistic choice, and (ii) the joint distribution of observed and unobserved beliefs and characteristics. Then, Section 4.2 discusses the identification of (i) and (ii) from the perspective of a researcher who has some flexibility on the design of the belief elicitation.

4.1. Characterisation of the Population Distributions

The identification result requires that the utility is strictly increasing in income, a common restriction summarised in Assumption 1.

Assumption 1.

Lemma 1 below provides a characterisation of ’s perceived distribution of ex ante returns using the representation (3.2), under the following condition:

Assumption 2 is a restriction on the resolvable uncertainty. Intuitively, it imposes that is a sufficient statistic for the distribution of the resolvable uncertainty. To understand the intuition behind Assumption 2, it is useful to recall that pertains to shocks that occur prior to the decision, whereas are outcomes realised after the decision. Assumption 2 imposes that for predicting , the agent do not use their beliefs about events in the latter period, but the information they already hold. A structure satisfying Assumption 2 is the following:

| (4.3) |

with and and are, respectively, a non-degenerated random scalar and a non-degenerated random vector with support on the real space. Assumption 2 relaxes traditional assumptions about the resolvable uncertainty in two ways. First, it does not assume a particular distribution for the purpose of identification. Second, under this assumption, the distribution of resolvable uncertainty remains individual-specific (up to ).

In our application, Assumption 2 is satisfied if asylum seekers’ subjective beliefs are partially determined by a set of individual traits and individual information . Beliefs about expected income, pecuniary benefits, chance of becoming regularised, and resolvable uncertainty may all correlate with . Assumption 2 imposes that after conditioning on this set of traits and information, any additional information about the perceived chance of becoming regularised or the expected pecuniary benefit does not reveal more information on ’s prior about the resolvable uncertainty.

The next assumption is a support condition. It introduces an important tool in the analysis, the operator , which represents a pecuniary transfer of value from the expected income in option 1 to the income in 0: the expected income in option 0 is topped up by to reach and the benefit of choosing option 1 is reduced from to . It is important to note that, by Assumption 1, the map is monotone decreasing in .

Assumption 3 (Support Condition).

Assumption 3 describes two restrictions used for the characterisation. The first states that the observed beliefs can shift the intended choice so as to cover the whole unit interval. This ‘large support’ condition implies that the researcher must observe beliefs and choice characteristics relevant enough to move the intended choice between extreme choices. It also ensures that even after conditioning on , there is still variation in . The second condition requires that is connected in its first two dimensions, where the transfer operates. Besides, when the transfer takes potentially large values, so that , we can still infer that the intended choice is either 0 or 1.

The key result is the possibility to represent an agent’s perceived distribution of ex ante returns as a functional of the structural function (3.2).

Lemma 1 characterises a counterfactual object: the perceived distribution of ex ante returns for an agent with private information , whose observed beliefs are counterfactually set to equal . It states that the probability with which the ex ante return is perceived to be below is the probability that the agent chooses option 1 over 0 when she receives a transfer . Equation (4.4) bears a resemblance to the characterisation of the compensating variation in Bhattacharya, (2015), Theorem 1, p. 626. In fact, the method of proof is similar. The main difference is that in Bhattacharya, (2015) the equivalent object for pertains to a population distribution (the aggregate demand for a good), whereas in the present framework it pertains to an individual-specific distribution.

Theorem 1 below characterises the distribution of ex ante returns at the population level.

Theorem 1.

Theorem 1 characterises the distribution of individual-specific quantile . Its importance is to link the identification of the distribution of returns, , to the identification of the structural function and the (conditional) distribution of . Thus, identification hinges on the ability of the analyst to infer both quantities from the available data on elicited in a set of scenarios .

4.2. Identification Results

The main takeaway from this section is the possibility to identify (i) and (ii) the (conditional) distribution of from data combining stated choice and beliefs in the actual scenario and a set of hypothetical scenarios. The exposition is made much simpler by considering the case where is a uni-dimensional heterogeneity. In this case, the identification result can be seen as an application of existing identification results in panel models with nonseparable fixed effects, in particular, the result of Evdokimov, (2010), although the model here deviates from his (see footnote 14).

In the case of a unidimensional heterogeneity , the novelty is the application of the latter results to models of stated preference with data generated from a pseudo-panel. The proposed methodology takes full advantage of the flexibility offered by the stated choice procedure. Thanks to the possibility of observing all individuals in the same counterfactual scenario, identification of (i) and (ii) can be achieved on the full support of observable beliefs and characteristics, , even with just two scenarios. Furthermore, when the measurement error in stated choices is negligible, the resulting estimand for the distributions of quantile, , is very simple.

A further contribution of the paper is to go beyond the unidimensional case and extend Evdokimov, (2010)’s result to consider being multidimensional. It introduces a random coefficient representation to model the quantile functions of (i) and (ii). Under this assumption, when the unobserved heterogeneity is two-dimensional, two common hypothetical scenarios are enough, when three-dimensional, three scenarios, and so forth. Thus, by introducing several hypothetical scenarios, one can consider a larger dimension of unobserved heterogeneity.

The latter case of multidimensional heterogeneity requires additional notations that increase the length of exposition without adding much to the intuition of identification. Therefore, this discussion is differed to Section A.2 in Appendix A. Although this choice conceals somewhat the contribution of the paper, it has the advantage of preserving its simplicity.

4.2.1. Elicitation procedure

Before delving into the technical results, it is worth discussing the flexibility offered by the stated choice procedure. Given flexibility of the elicitation procedure, identification may seem obvious to achieve. However, the endeavour is more complex than it appears at first sight.

A straightforward strategy may consist in randomly drawing realisations of for multiple scenarios. It has been well documented that questions related to subjective expectations and stated preferences are more credible when scenarios are closer to individuals’ actual circumstances, especially for low educated groups (Delavande et al.,, 2011). Hence presenting randomly generated scenarios might induce substantial measurement error.

A common practice consists into generating exogenous departures from individuals’ actual beliefs. In this case, only the departures are random, not the base levels. This is the motivation for the ARUM representation of Section 2, with an appeal to a restrictive linear utility function. Note that the identification in this case does not make use of actual beliefs and intentions.

To address these limitations, the paper proposes to use the following elicitation design: the researcher elicits both actual beliefs and intentions and beliefs and intentions in a limited number of counterfactual/hypothetical scenarios. At least one of the hypothetical scenarios is common to all respondents. Thus, this strategy covers the common case where scenarios are anchored in individuals’ actual experience and only the extent of departures from this scenario varies experimentally, as long as it introduces scenarios that are common to all individuals. The requirement of common scenarios can be relaxed as discussed in Remark 1 below.

4.2.2. Data

Assumption 4 summarises the structure of the data available to the researcher in the case where is unidimensional.

Assumption 4 (Pseudo-panel).

Let denote the actual scenario, and be the index for hypothetical scenarios. The researcher observes an i.i.d. sample, such that:

| (4.5) |

where is a continuously distributed random variable.

In particular, among the counterfactual scenarios, one is common to all respondents:

-

(CF)

there exists , such that for all .

denotes the stated actual choice probability, the vector of observed beliefs held, the stated probabilistic choices in counterfactual scenarios, and the beliefs held in these counterfactual scenarios. The reported set of intentions of respondent , , deviates from the true intentions, , because of a measurement error summarised by the random variable . Condition states that the intended choices are observed for some counterfactual value that is common to all respondents. The latter restriction can be relaxed as discussed in Remark 1 below.

Since our model is not nested into Evdokimov, (2010)’s panel model with nonseparable fixed effects, and for the sake of completeness, Section 4.2.3 provides a detailed exposition of identification.141414With our notations, Evdokimov, (2010)’s model corresponds to replacing Equation (A.3) with: (4.6) Although this permits to consider more general assumptions on the measurement error variable, it does not fit well with a left-hand side variable that is bounded between 0 and 1. One possibility to use Equation (4.6) is to consider instead the log-odds of . The advantage of our formulation is that the left-hand side variable has a compact support. This simplifies the asymptotic theory and estimation. The second identification result described in Section A.2.3 shows how more counterfactual scenarios can be harnessed to relax restrictions on the dimension of .

4.2.3. Identification with a unidimensional heterogeneity

Identification requires a set of assumptions, which are mild restrictions on the variable , the function and the measurement error that allow identification.151515Compare to Evdokimov, (2010) (Assumption ID, p. 6).

Assumption 5 (Restrictions on , and ).

In the model (A.3), suppose:

-

(ME)

the distribution function of obeys:

-

(i)

, for all , and .

-

(ii)

for all and ,

-

(iii)

does not vanish for all and , where is the (conditional) characteristic function of , for all and .

-

(i)

-

(QF)

the function satisfies the following conditions:

-

(i)

For each , there exists and , , such that:

-

a.

is strictly monotonic in , on ,

-

b.

for all , ,

-

c.

for all , .

-

a.

-

(ii)

for all , .

-

(i)

-

(QR)

satisfies the following conditions:

, , and are everywhere continuous with respect to , , , for all , for .

Condition limits the scope of measurement error, imposing that it is independent of observed and unobserved beliefs. Condition guarantees invertibility of function in the second argument on a given interval. Outside this interval, the value taken by is known. Condition is a normalisation that is standard in nonseparable models. Finally, Condition is needed to handle conditioning on probability zero events.161616cf. Evdokimov, (2010), Appendix 6.3. The rest of the development omits the subscript unless necessary.

Theorem 2.

Suppose and Assumptions 1-5 all hold. Then, the distribution of interest as characterised in Theorem 1 and Theorem 3 are identified from the joint distribution of .

For example, in the case of negligible measurement error, , for all , we have:

| (4.7) |

Theorem 2 states that the distributions of interest are identified from the joint distribution of stated choice and observed beliefs and characteristics across scenarios.

The case of negligible measurement error serves two purposes: first, it illustrates the origin of the variation needed for identification. From Theorem 1, we learn that the -quantile of the ex ante return is less than a value , if and only if . With a unidimensional heterogeneity, can be interpreted as a nonseparable fixed effect, which measures the propensity to choose option 1 over option 0 (irrespective of ). Since one scenario is common to all the population (), the intended choice in this common scenario is a direct measure of this propensity. Hence, it is possible, without loss of generality, to normalise . Given this normalisation, one can show that, when the conditional distributions are strictly increasing,

Hence, if and only if . Therefore, the relevant variation for identification is the change of the propensity to choose option 1 over option 0 as one moves from the common scenario to the actual beliefs, .

To sum up, the common scenario helps to rank individuals according to their unobserved propensity and pins down . Given this ranking, the actual beliefs and intention provide the required variation to identify the effect of on . Finally, to obtain the distribution of the -quantile, it suffices to shift by the corresponding transfer operator . Thus, the primitive objects for estimation are the conditional distributions

A second reason for considering the case of negligible measurement error is that Equation (4.7) provides the rationale for a simple two-stage estimation. In the first stage, one recovers estimates of , evaluated at the appropriate values for each individual in the population, namely and . In the second stage, it suffices to take the empirical mean of the indicator within the expectation operator of Equation (4.7). This simple procedure is presented more formally in Section 5 and Appendix C.

Accounting for the possibility of measurement error involves one additional step: because provides only a noisy measure of the distribution of , one has to separate the distribution of from the distribution of . This step involves Kotlarski’s Theorem (Kotlarski,, 1967). It requires some overlap of beliefs across scenarios: some individuals in the population must have the same beliefs as in the counterfactual scenario.

Remark 1 (The role of condition (CF)).

In the proof detailed in Appendix B, note that the function is identified for all , such that belongs to the support of , say . Hence, identification of depends on the richness of the support , for individuals such that . Condition (CF) of Assumption 4 ensures that this support is not restricted, because one hypothetical scenario elicits intentions at for the entire sample. Instead of (CF), a sufficient condition would be that .

Theorem 2 shows that for a unidimensional heterogeneity, the parameters of interest are identified from the introduction of one counterfactual scenario. Additional counterfactual scenarios can increase the efficiency of estimation, as they bring additional observation points. These counterfactual scenarios do not need to define the whole vector , can alter a single dimension, and can be different for different respondents.

As discussed in Section A.2.2, the restriction on ’s dimensionality corresponds to assuming some Rank Invariance. In our application, it means that an asylum seeker relatively prone to overstay with a high value of will also be relatively prone to overstay with a low value of . This may not always be a desirable assumption. Counterfactual scenarios can be harnessed to relax this assumption. This insight is developed in Section A.2.3 in Appendix A, where can be multidimensional.

5. Estimation and Inference

This section briefly discusses some avenues for conducting estimation. The detailed development of estimation, inference and asymptotic theory is differed to Sections C and D in the Appendix.

In the leading case, where is unidimensional, the nonparametric procedure of Evdokimov, (2010) for the estimation of the functions and applies. It involves in a first step a deconvolution estimator that separates the distributions of measurement error and of , by taking advantage of the pseudo-panel structure of the data. In the second step, Kernel estimators provide empirical counterparts for and . These can then be used to estimate the distributions of interest. One hurdle is that this estimator performs poorly for extreme values of . In this case, one can construct bounds on the distributions of interest, as discussed in Appendix C.3.

When is multidimensional and under the assumptions of Theroem 4 in Appendix C.3, the same procedure could be applied for a linear combination of the vector defined in Theorem 4.

The nonparametric estimation comes with strong data requirements and the curse of dimensionality. In particular, estimation of the functions and requires estimation of conditional CDFs. For example, when , the conditional CDFs of and need to be estimated on the support of , for each subgroup of the population defined by a vector of observable . Appendix C provides a semiparametric approach for estimating these conditional CDFs. It is important to note that, unlike traditional approaches to models with subjective expectations, parametric assumptions are not introduced for the purpose of identification, but to alleviate strong data requirements for the purpose of estimation. The parametrisation presented in Assumption 9 in Appendix D provides an approximation for the aforementioned conditional CDFs.

In the case of negligible measurement error, the estimation procedure is a very simple two-stage estimator to recover the distribution of quantiles in the population. To account for measurement error, Appendix C.4 details an equally tractable bound approach that preserves the simplicity of the estimator. It provides an alternative to the deconvolution estimator and factors in the common rounding behaviour in probabilistic data on subjective expectations.

To account for the poor performance of the estimator at extreme quantiles, one can rely either on the extrapolation of the estimates at middle quantiles or modify the bound approach. Both procedures, detailed in Appendix C.3, are applied to the data.

6. The Intention to Overstay of Afghan Asylum Seekers in Germany

This section demonstrates the importance of the identification results by estimating the distributions of ex ante returns on overstaying in a population of Afghan asylum seekers in Germany.

In this application, the elicited intention corresponds to the choice between overstaying and leaving Germany. is univariate and represents the chance of becoming regularised. is also assumed to be unidimensional, so that the rank invariance assumption (Assumption 7) applies.

Section 6.1 starts with a brief description of the context and the data. The full description of the context of asylum migration and an in-depth description of the survey is available in Méango et al., (2020). Section 6.2 presents descriptively the elicited beliefs and stated probabilistic choices. Section 6.3 presents the main estimation results. Finally, Section 6.4 discusses some policy implications.

6.1. Context and Sample

In the aftermath of the so-called ‘refugee crisis’, many European States have seen a surge in the number of foreigners with a rejected asylum application and a legal obligation to leave the country. Germany, for example, has seen this number rise sharply from 4,500 in 2014 to 152,000 in 2019.171717Germany received nearly 1,100,000 registrations for asylum between 2014 and 2016. Afghan citizens accounted for a quarter of a million of registrations. Afghanistan placed second as the origin country as of 2019. Afghanistan, with close to 25,000 asylum seekers with an obligation to leave, represented the main origin country of overstayers in 2019. In a context where deportation occurs rarely but there is much uncertainty about the legal status, the decision to overstay depends mainly on the individual’s perception.181818At the time of the survey, the outcome of an asylum application was uncertain for Afghan citizens. Between 2014 and 2019, one out of two applications was rejected in the first instance. As of 2019, two out of three applicants were recognised as having protection status (92 percent of those as a temporary status with a maximum validity of three years), and 12 percent were denied and legally obliged to leave the country. Less than two percent of those with a legal obligation to leave have been actually deported. Departure of Afghan citizens from Germany is not rare. An estimated 5,580 Afghans left Germany in 2019, including 1,766 cases where the asylum seeker had been denied protection. These numbers should be seen as lower bounds, as the exit is not always registered (e.g. when travelling by land).191919The data collection for this application was conducted in 2019, prior to the takeover of Kabul by the Talibans. Voluntary returns and forced repatriations were still feasible options at the time of data collection. As of 17 August 2021, due to the deteriorating security situation in Afghanistan, assisted voluntary return to Afghanistan has been suspended until further notice.

This section takes advantage of a unique survey conducted during the second half of 2019 on Afghan asylum seekers in Berlin, Hamburg and Munich, the three German cities with the highest number of Afghan citizens. The questionnaire elicited subjective beliefs about the chance of obtaining the right to stay in Germany (RtS), the perceived risk of deportation, the expected income streams and further outcomes depending on legal status. Most importantly, the survey elicited the intention to overstay under different hypothetical scenarios about the chance of becoming regularised after three years.

The raw sample consists of 1,023 Afghan citizens, aged 18 or more, who arrived in Germany for the first time in 2014 or after, and live in one of the three urban areas. Computer assisted personal interviews were conducted by native speaker enumerators in Dari and Pashto, the two main languages spoken in Afghanistan. Recruitment was a mix of traditional sampling based on available register data, and peer-recruitment. Although not representative by design, the sample mimics key characteristics of the population. The sample is dominated by males (two thirds). The population is young (median age 28), less educated than comparable Germans with nearly two-thirds of respondents with lower secondary education or below.

6.2. Descriptive Evidence on Subjective Beliefs and Intention to Overstay

Table 6.1 presents averages and standard deviations of elicited subjective beliefs and intention to overstay for people in each city and the whole sample.202020The survey included questions that required the respondent to state subjective probabilities as a number between 0 and 100. The module on subjective expectations included a training phase where respondents were trained to state their subjective expectations with a number between 0 and 100. For example, respondents were asked to state how many out of 100 Afghans they thought could speak Dari, the most common language spoken in Afghanistan. Then the interviewer was asked to help respondents rephrase the answer. The same exercise was repeated for the proportion of Afghan migrants to Europe who came to Germany, and the proportion of Afghan migrants who obtain the right to stay in Germany. The questions were complemented with visual aids to facilitate understanding. For the subsequent analysis, the sample is restricted to respondents with non-missing answers in all key variables of interest, which is 858 observations. The expected income distributions are also trimmed at the top 95-percentile to minimise the effect of outliers.

| Berlin | Hamburg | Munich | Total sample | |

|---|---|---|---|---|

| Obtain RtS (Q3) | 73.20 | 70.07 | 56.22 | 68.05 |

| (26.39) | (23.83) | (27.36) | (27.03) | |

| Obt. RtS. after 3 yrs w/o RtS (Q4) | 66.13 | 67.81 | 51.35 | 62.62 |

| (27.97) | (25.95) | (26.90) | (28.04) | |

| Be deported if no RtS (Q5) | 32.53 | 37.12 | 48.58 | 37.74 |

| (32.73) | (26.75) | (24.88) | (30.27) | |

| Income with RtS | 1666.91 | 1731.19 | 1611.67 | 1666.12 |

| (745.5) | (567.0) | (517.8) | (653.4) | |

| Income w/o RtS | 1148.26 | 1385.99 | 1108.44 | 1193.44 |

| (647.5) | (487.5) | (535.5) | (590.6) | |

| Income abroad | 1132.58 | 1226.15 | 469.80 | 948.32 |

| (902.0) | (614.5) | (467.4) | (777.5) | |

| Stay w/o RtS (Q8) | 69.75 | 69.76 | 49.05 | 64.39 |

| (32.59) | (26.31) | (28.46) | (31.51) | |

| stay if percent (Q9) | 70.04 | 55.92 | 37.22 | 58.57 |

| (35.05) | (32.79) | (32.34) | (36.44) | |

| stay if percent (Q10) | 85.55 | 74.39 | 66.32 | 78.04 |

| (22.96) | (22.43) | (26.03) | (25.05) | |

| stay if percent (Q11) | 95.80 | 89.81 | 91.05 | 93.23 |

| (13.55) | (16.20) | (18.09) | (15.66) |

-

•

Note: Mean values calculated on non-missing observations. Standard deviation in parentheses. See the exact question wording in the online supplementary material, Appendix H.

Beliefs

Respondents report on average a 68 percent chance of obtaining the RtS. Beliefs in Munich are significantly lower than in the two other cities with a 14 to 17 pp difference. In Berlin, the average belief is slightly above the 2019 official proportion of asylum seekers with some protection (72 percent compared to 68 percent), while it is lower in Hamburg (70 percent compared to 80 percent). For Munich, the only publicly available comparison point is at state level, Bavaria. The average belief of 58 percent is 12 pp lower compared to the proportion in Bavaria in 2019 (68 percent). However, the average belief is slightly higher than the proportion of Afghans who received positive decisions in the first instance (51 percent). Thus, on average, beliefs about the chance of obtaining the RtS are not substantially biased. Nevertheless, standard deviations are large, which suggests a significant variation between individual beliefs. Beliefs about the chance to obtain the RtS conditional on overstaying three years are slightly lower than, but well aligned with, the elicited chance of obtaining the RtS.

Beliefs about the proportion of Afghans forcibly removed and sent back to Afghanistan and the chance of being deported when not obtaining the RtS are higher than suggested by available official statistics. On average, respondents believe that one out of five Afghans has been sent back to Afghanistan in the past years and there is a 37 percent chance of being deported conditional on not obtaining the RtS. However, deportation to Afghanistan is a rare event. In 2019, only 1.6 out of 100 Afghan asylum seekers with a rejected asylum application were deported, that is 1.8 out of 1,000 Afghan asylum seekers irrespective of the status.

With a RtS, respondents expect, on average, a monthly income of 1,676 EUR. This amount is lowest in Munich (1,610 EUR), which also displays the lowest variance, and highest in Hamburg (1,710 EUR). Without a RtS, respondents expect, on average, 1,261 EUR. As before, the average is lowest in Munich (1,122 EUR), and highest in Hamburg (1,424 EUR). These numbers imply an expected monthly return on legalisation of between 300 EUR and 500 EUR on average, depending on the city.212121According to Brücker et al., (2020), the average monthly gross income of refugees who entered Germany between 2013 and 2016 was 1,282 EUR in 2018, and 1,863 EUR for those in a full-time occupation. This represents between 54 percent and 89 percent of the average gross income of the comparable German workforce, depending on the category considered. Thus, on average, beliefs on income do not appear substantially biased.

Intention to overstay

The survey elicited the intention to overstay as choice probabilities and in two formats according to the methodology proposed in the theoretical exposition. The first format was a question about the respondent’s willingness to overstay given their actual beliefs and circumstances (see Q8 in Appendix H). The second format presented the respondents with three hypothetical scenarios about the chance of becoming regularised (see Q10 to Q12 in Appendix H). In the first one, the respondent has almost no chance of becoming regularised in the next three years if he or she overstays ( percent). In the second one, the respondent is almost sure of becoming regularised at the end of a three year overstay ( percent). Finally, we include an intermediate scenario where the chance of becoming regularised at the end of a three-year period stands at 50 percent ( percent). All respondents received all three questions. The order of questions was randomly assigned by the computer program.

Thus, the first format corresponds to the actual scenario refered to in Section 4, the second format to the countefactual scenarios. Note that the number of scenarios remains limited, making the key variation between them easy to understand. Note also that the hypothetical scenarios define only the chance of becoming regularised, but neither the income at origin , nor the pecuniary benefit associated with the overstay . As discussed in Section B.7, the generalised Roy model dispenses us from this requirement, if one assumes that . Thus, the counterfactual scenario is the same for everyone. can be interpreted as the pecuniary benefits stemming solely from the chance of becoming regularised. When the chance is close to zero, these benefits are almost null.

Intention to overstay as elicited through Q8 is high with an average of 64 percent. One of four respondents state a 100 percent chance to overstay, of whom close to 80 percent reside in Berlin. The intention to overstay in Munich is markedly lower than in the two other cities, with a 21 pp difference, on average.222222Compared to the hypothetical scenario of Q10-Q12, respondents seem to understate their willingness to overstay when asked directly in Q8. See Figure I.1 in the online Appendix I. In the empirical analysis, a dummy indicator is added to correct for this understatement.

Intention to overstay as elicited with questions Q10 to Q12 is also high. When , it displays an average of 93.23. The CDFs, in this case, are highly skewed as 68 percent of the respondents answer 100, and close to 90 percent give answers of 75 or above. This pattern is very consistent across all cities. The average intention to overstay drops by about 15 pp when . The magnitude of this change depends strongly on the city: Berlin, -10 pp; Hamburg, -16 pp; Munich, -25 pp. The distribution has a larger spread: 42 percent of the sample answer 100, and close to 90 percent give answers of 45 or above.

When , the drop in the average intention to overstay from the case where is, on average, 35 pp. Again, the magnitude of this change depends strongly on the city: Berlin, -26 pp; Hamburg, -44 pp; Munich, -54 pp. Thus, Munich residents appear the least willing to stay when there is almost no chance of becoming regularised. Overall, the chance of obtaining the RtS in the future appears to have a significant effect on the intention to overstay.

6.3. Estimated Distributions

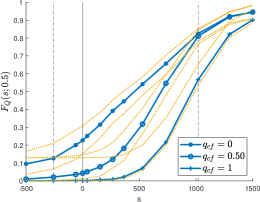

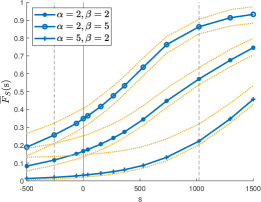

This section presents the estimated distribution of ex ante returns at different quantiles, for counterfactual values of the chance of becoming regularised, and the related distribution of IQR. It reports two types of estimates, which both correct for the measurement error and the poor performance of the DR estimator at extreme values of the quantile. The first estimate based on Equation (C.8) linearly extrapolates the estimates from the middle quantiles of the DR estimation and uses Equation (C.7) to account for measurement error. It is referred to as to the point-identified procedure. The second estimate uses instead the bounds in Equation (C.9). It is referred to as to the bound procedure.

Figure 2(f), panel (a), illustrates the CDF , the distribution of median ex ante returns at current beliefs , and compares it to the estimated distribution of mean returns . is measured in monthly equivalent and varies on the x-axis between -500 and 1,500 EUR. Values estimated for below -250 EUR and above 1,100, marked with a dashed vertical lined, are typically outside the observed support of , and therefore rely on extrapolating the conditional CDFs at larger values of . The solid middle line represents the estimated distribution based on the point-identified procedure, whereas the lower and upper dotted lines represent the bound procedure (with in Equation (C.9)). Accounting for measurement errors through bounds makes it more difficult to identify the tails of the distribution for the median returns. However, the central part of the distribution is relatively well estimated.

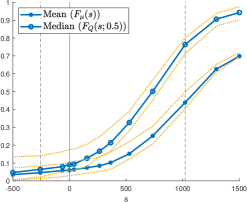

The insights derived from the distribution of median and mean are somewhat different. The perceived median returns are essentially positive, with between 82 and 94 percent of the population exhibiting positive returns on overstaying. About half of the population perceives median return larger than 730 EUR. At least 22 percent perceive returns larger than 1,000 EUR per month. Thus, the distribution of median ex ante returns is very heterogeneous, with non-negligible portions of the population perceiving either negative or very large median returns. In contrast, the distribution of mean returns is shifted to the right with a support that is essentially positive and a median above 1,000 EUR. The discrepancy between mean and median returns suggests the existence and influence of large perceived returns.

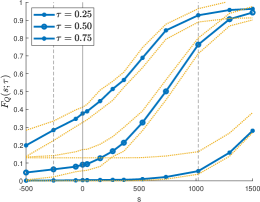

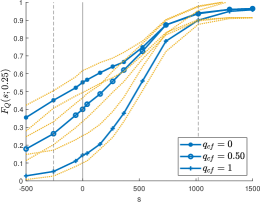

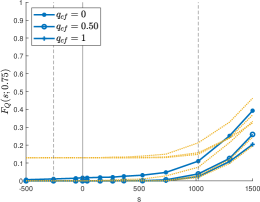

Figure 2(f), panel (b), compares the distribution of median returns to the distribution of returns for additional quantiles, that is for (left/top distribution) and (right/bottom). For the distribution of first quartiles, between 32 and 41 percent of the population perceives negative ex ante returns, and the median stands between 140 and 330 EUR. For the distribution of third quartiles, the returns are essentially positive and very large. The lower bound seems conservative. Compared to the distribution , is farther away from the distribution of median returns, , implying that the individual-specific distributions of ex ante returns have a long upper tail.

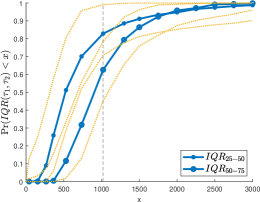

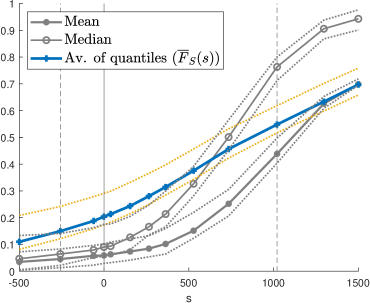

The last point is best illustrated by the distribution of and in Figure 2(f), panel (c). These CDFs represent the proportion of the population for which the spread of the distributions of ex ante returns is below a given value. The distribution of is shifted to the right compared to the distribution of . However, the latter results rely very much on the quality of our extrapolation. Notwithstanding this caveat, these findings suggest that usual assumptions on the resolvable uncertainty (independence with observed beliefs, separability, extreme-value type I representation and/or identical distribution) may not fit the data very well. Indeed, assuming that the resolvable uncertainty is separable, the long upper tail speaks against a symmetric distribution. Furthermore, the distribution of IQR does not seem to be degenerated, hinting to some variability of individuals’ perception of uncertainty.