Time-inconsistent contract theory111Camilo Hernández acknowledges the support of a Presidential Postdoctoral Fellowship at Princeton University, a Chapman Fellowship at Imperial College London and a CKGSB fellowship at Columbia University.

This paper investigates the moral hazard problem in finite horizon with both continuous and lump-sum payments, involving a time-inconsistent sophisticated agent and a standard utility maximiser principal. Building upon the so-called dynamic programming approach in Cvitanić, Possamaï, and

Touzi [18] and the recently available results in Hernández and Possamaï [43], we present a methodology that covers the previous contracting problem. Our main contribution consists in a characterisation of the moral hazard problem faced by the principal. In particular, it shows that under relatively mild technical conditions on the data of the problem, the supremum of the principal’s expected utility over a smaller restricted family of contracts is equal to the supremum over all feasible contracts. Nevertheless, this characterisation yields, as far as we know, a novel class of control problems that involve the control of a forward Volterra equation via Volterra-type controls, and infinite-dimensional stochastic target constraints. Despite the inherent challenges associated to such a problem, we study the solution under three different specifications of utility functions for both the agent and the principal, and draw qualitative implications from the form of the optimal contract. The general case remains the subject of future research.

Key words: Moral hazard, time-inconsistency, consistent planning, sophisticated agent, dynamic utilities, backward stochastic Volterra integral equations, stochastic target.

In this paper, we are interested in the moral hazard contracting problem between a principal and an agent with time-inconsistent preferences. A principal–agent problem pertains to the optimal contracting between two parties: the principal, who is interested in hiring the agent, offers a contract; provided the agent accepts, he can influence a random process, the outcome, via his actions. A key feature in these models is the amount of information available to the principal when designing the contract. There are three classical cases studied in the literature: risk-sharing with symmetric information, hidden action, and hidden type. We are only concerned with the first two in this work.

In the risk-sharing scenario, also referred to as the first-best, both parties have the same information and have to agree on how to share the underlying risk. The principal thus has all the bargaining power, i.e. she offers the contract and dictates the agent’s actions—the agent is compelled to follow or else he would be severely penalised. In the case of hidden actions, the principal is imperfectly informed about the agent’s actions. Either they are too costly to be monitored or simply unobservable. Consequently, the principal expects to receive a second-best utility compared to the risk-sharing case. As the agent is allowed to take actions that are not in the principal’s best interest, this situation is also referred to as moral hazard, and incentives play a crucial role. Indeed, the principal hopes to influence the agent’s actions by offering an appropriate contract.

In the case of a traditional (time-consistent) agent, a common feature of these models is that their resolution boils down to standard stochastic control theory. Indeed, in light of the principal’s bargaining power, the first-best case is always cast as a stochastic control problem for a single individual—the principal—who chooses both the contract and the actions under the participation constraint. On the other hand, in the second-best problem, it being a two-stage Stackelberg game, one has to solve the agent’s problem for any given fixed contract before moving to study the principal’s problem. In principle, this creates a much more complicated structure on the problem. Since the introduction of the continuous-time model, it took time for the literature to present a general approach that arrived at the same conclusion for the second-best problem.

The study of moral hazard problems in continuous time has its roots in the seminal paper of Holmström and Milgrom [45]. In this model, the principal and the agent have CARA utility functions, and the agent’s effort influences the drift of the output process, the solution to a controlled diffusion, but not the volatility. The resulting optimal contract is a linear function of the aggregate output. The model in [45] drew great attention as the resolution of the, seemingly more complicated, continuous-time formulation was actually much more tractable, could be rigorously justified, and provided useful explicit solutions for the economic analysis. These were typically harder to reach in most of the discrete-time models that dominated the existing literature, see Laffont and Martimort [49] for an overview. Following upon [45], Schättler and Sung [71, 72] studied the validity of the so-called first-order approach, while Sung [78, 79] provided extensions to the case of diffusion control and hierarchical structures. The linearity of the optimal contract, a feature also present in [78], is further studied in Müller [62, 63], Hellwig and Schmidt [40], Hellwig [39] and Sung [80, 81] for the first-best problem, the interplay between the discrete-time and continuous-time models, and for a robust setting, respectively. Notably, Williams [90] and Cvitanić, Wan, and

Zhang [16] characterise the optimal contract for general utilities by means of the so-called stochastic maximum principle and forward–backward stochastic differential equations (FBSDEs for short)444We refer to the monograph Cvitanić and Zhang [15] for a general framework that systematically surveys a great portion of the literature exploiting the maximum principle, in models driven by Brownian motion..

Nevertheless, it was not until the approach in Sannikov [68, 69] was available that the study of the moral hazard problem was, once again, reinvigorated and arrived finally at the methodical program presented in Cvitanić, Possamaï, and

Touzi [17, 18]. In a nutshell, this method leverages the dynamic programming principle and the theory of backward stochastic differential equations (BSDEs) to reformulate the principal’s problem as a standard optimal stochastic control problem with an additional state variable, namely, the agent’s continuation utility.

This methodology has been extended to several scenarii including random horizon contracting Lin, Ren, Touzi, and Yang [55], ambiguity features from the point of view of the principal, as in Mastrolia and Possamaï [60] and Hernández Santibáñez and

Mastrolia [44], a principal contracting a finite number of agents Élie and Possamaï [25], several principals contracting a common agent Mastrolia and Ren [61], a principal contracting a mean-field of agents [26], and applications in optimal electricity demand response contracting Aïd, Possamaï, and

Touzi [2], or Élie, Hubert, Mastrolia, and

Possamaï [27]. The road map suggested by this approach is quite clear: identify the generic dynamic programming representation of the agent’s value process, express the contract payment in terms of the value process, optimise the principal’s objective over such payments.

All in all, the previous literature is particular to the contracting problem between two (or more) standard utility maximisers, while there is a growing need for the development of models able to explain the behaviour of agents that fail to comply with classical rationality assumptions. Indeed, there is clear evidence of such attitudes in a number of applications, from consumption problems to finance, from crime to voting, and from charitable giving to labour supply, see Rabin [67] and Dellavigna [19] for detailed reviews. The distinctive feature in these situations is that human beings do not necessarily behave as perfectly rational decision-makers. In reality, their criteria for evaluating their well-being are, in many cases, a lot more involved than the ones considered in the classic literature. In light of the methodology introduced in [18], the recently available results in Hernández and Possamaï [43] unveil the possibility of extending this blueprint to cover the moral hazard problem between a principal and a sophisticated time-inconsistent agent. This is the task we seek to accomplish in this paper.

Time-inconsistency is, in general terms, the fact that marginal rates of substitution between goods consumed at different dates change over time, see Strotz [77], Laibson [50], O’Donoghue and Rabin [64, 65]. For example, the marginal rate of substitution between immediate consumption and some later consumption is different from when these two dates were seen from a remote prior date. In many applications, this introduces a conflict between ‘an impatient present self and a patient future self’, see Brutscher [11]. In mathematical terms, this translates into stochastic control problems in which the classic dynamic programming principle, or in other words, the Bellman optimality principle is not satisfied.

Time-inconsistency was first mentioned in [77] where three different types of agents are described: the pre-committed agent does not revise his initially decided strategy; the naive agent revises his strategy without taking future revisions into account; the sophisticated agent revises his strategy taking possible future revisions into account, and by avoiding such makes his strategy time-consistent. The comprehensive study of sophisticated agents started with Ekeland and Pirvu [23], see also Ekeland and Lazrak [21, 22], which later became the starting point of the general Markovian theory developed by Björk, Khapko, and Murgoci [7]. Nonetheless, none of these approaches could handle the typical non-Markovian problems that would necessarily arise in contracting problems involving a principal and a time-inconsistent agent. Hernández and Possamaï [43] provided a probabilistic formulation able to accommodate a general non-Markovian structure and provided an extended dynamic programming principle (DPP) for a refinement of the notion of equilibria first introduced in [22]. In turn, the extended DPP leads to the introduction of a system of BSDEs analogous to the classical HJB equation. This system is fundamental in the sense that its well-posedness is both necessary and sufficient to characterise the value function and equilibria, which are identified as maximisers of the Hamiltonian.

When it comes to incorporating time-inconsistent features into contract theory models, the economic literature is abundant in discrete-time models with two and up to three periods. A common feature in this literature is adopting quasi-hyperbolic discounting structures to draw conclusions in different mechanism design problems. Yet, the method of resolution in each problem remained limited to a case-by-case analysis. For instance, Amador, Werning, and

Angeletos [4] and Bond and Sigurdsson [8] study the feasibility of commitment in models of consumption and savings, whereas Galperti [31] considers the optimal provision of commitment devices to people who value both commitment and flexibility. Bisin, Lizzeri, and Yariv [6] examines policymakers’ responses to the political demands of agents with self-control problems, Halac and Yared [34] looks into a fiscal policy model in which the government has time-inconsistent preferences, while Lim and Yurukoglu [54] assesses the effects of time-inconsistency on monopoly regulation of electricity distribution. Heidhues [38] and Karaivanov and Martin [47] integrate time-inconsistent preferences into credit, mortgage, and insurance contract design problems, respectively. Englmaier, Fahn, and Schwarz [28], Gottlieb [32] and Gottlieb and Zhang [33] study contracting problems between firms and sophisticated, partially naive, and naive present-biased consumers. Yılmaz [91, 92] considers a repeated moral hazard problem involving a sophisticated and naive agent, respectively. Ma [58] studies a multi-period model in which contracts are subject to renegotiations, and the agent’s action has a long-term effect. Balbus, Reffett, and Wozny [5] shows the existence of time-consistent equilibria for dynamic models with generalised discounting. A survey of some of the state of behavioural economics research in contract theory was provided in Kószegi [48].

In continuous-time, where the dynamic models are sometimes more tractable and the solutions enjoy better interpretability, the literature becomes rather scarce. Models dealing with a pre-committed agent have been considered in Li and Qiu [52], in which a non-constant exponential discount factor is the source of time-inconsistency, and Djehiche and Helgesson [20], where the agent is allowed to have mean-variance utility functions. The case of a sophisticated agent was considered in Li, Mu, and Yang [53], Liu, Mu, and Yang [56], Liu, Huang, Liu, and Mu [57] and Wang, Huang, Liu, and Zhang [88] in the case of hyperbolic discounting. However, the time-inconsistency is restricted in the sense that it manifests only at discrete random times that are exponentially distributed. Lastly, Cetemen, Feng, and

Urgun [13] considers a Markovian continuous-time contracting problem and dynamic inconsistency arising from non-exponential discounting. The authors’ examples are limited to the case of a principal having time-inconsistent preferences, and the agent having standard time-consistent preferences. Altogether, a thorough analysis of the general non-Markovian continuous-time contracting problem between a standard utility maximiser principal and a sophisticated time-inconsistent agent is still missing in the literature. This is because, in our opinion, the crux of the problem lies in identifying a proper description of the problem of the principal. In the case of a classic time-consistent agent and a time-inconsistent principal, following [18], one expects the problem of the principal to boil down to a non-Markovian time-inconsistent control problem with an additional state variable. As studied in [43], these problems are characterised by an infinite family of BSDEs, equivalent to a so-called type-I extended BSVIE [42]. As such, we expect that the problem considered in this document will open the door to a complete analysis of the problem in which both the principal and the agent are time-inconsistent.

Our results

Our problem is cast in the context of a standard utility maximiser principal and an agent with time-inconsistent preferences. Indeed, the agent’s reward is given by the value of a so-called backward stochastic Volterra integral equation. This choice of preferences for the agent allows us to cover classic separable and non-separable utilities simultaneously.

As is standard in the literature, we consider the weak formulation of the problem. The state process is fixed, and the agent’s actions influence the drift of through its distribution over the interval . The principal chooses a contract, i.e.a process and a random variable adapted to the filtration generated by the path of the state process, which specifies the continuous payments, the terminal payment, and satisfies the agent’s participation constraint at time . As mentioned above, our approach is inspired by that of [18] and the recent results for non-Markovian time-inconsistent control problems from a game-theoretic point of view of [43]. Indeed, [43] established an extended dynamic programming principle for the agent’s value process associated with any equilibrium action. In turn, this result was used to establish a direct link between the agent’s problem and an infinite family of BSDEs. Following [42], such a system is actually equivalent to a so-called type-I extended BSVIE.

At this point, we notice the first stark difference between the classic time-consistent case and ours: the problem of the agent is, in general, linked to the solution of an infinite family of equations, namely the BSVIE, as opposed to one, a BSDE. Nevertheless, the agent’s preferences elucidate a connection at the terminal time between the terminal values of the BSVIE and the terminal payment offered by any admissible contract. This is the crucial insight in order to restrict our attention from the family of admissible contracts to a carefully tailored family of contracts for which the agent’s value process allows a dynamic programming representation capturing the Volterra nature of the agent’s reward. Extrapolating from the time-consistent case, the restricted family of contracts is defined in terms of a family of first-order sensitivities of the agent’s value process to the output. For this family of contracts, we show that the principal identifies the equilibrium action for the agent as the maximisers of the associated Hamiltonian. Nevertheless, echoing the agent’s time-inconsistent preferences, the resulting principal’s problem is, in general, far from being a standard stochastic control problem.

Our main contribution, namely Theorem3.9, consists in a characterisation of the moral hazard problem faced by the principal and a sophisticated time-inconsistent agent.

In particular, it shows that under relatively mild technical conditions on the data of the problem, the supremum of the principal’s expected utility over the restricted family of contracts is equal to the supremum over all feasible contracts.

Nevertheless, this characterisation yields, as far as we know, a novel class of control problems.

These problems involve the control of a forward Volterra equation via Volterra-type controls, and stochastic target constraints.

One of the novel features of our result is that the dynamics of this process involves the diagonal value of both the forward Volterra process and the Volterra control, see Definition3.5.

In addition, the stochastic target constraint arises due to the time-inconsistent preferences of the agent, see (3.6) and Remark3.7.

Despite the inherent challenges of this class of problems, we study the solution to moral hazard problem under three different specifications of utility functions for both the agent and the principal.

For instance, for non-separable reward functionals, we find that if both the agent and the principal have exponential utilities functions and the agent’s reward is given by the discounted value of his utility, the problem reduces to a standard control problem, see Section4.1 and Proposition4.3.

This is a feature that we also see in the risk-sharing (or first-best) contracting examples between the principal and a time-inconsistent agent that we present in Section2.

The second example considers a risk-neutral principal and a risk-neutral agent with separable reward functional. In this case, our analysis shows that it is possible to reduce the complexity of the problem.

Indeed, we can exploit the structure of the problem to formulate an ansatz to the principal’s problem, for which we present a result in the spirit of a verification theorem, see Section4.2 and Proposition4.10.

In the last example, we go back to the first setting, but in this case the agent’s (exponential) utility is taken on the discounted income. This simple modification highlights the intrinsic difficulties of the general case, and we are able to solve the problem of the principal for a class of contracts smaller than the one prescribed by the restricted family of contracts in Theorem3.9, see Section4.3 and Proposition4.17.

The general case remains the subject of future research.

Regarding the qualitative implications of our results we can mention the following:

from a methodological point of view, unlike in the time-consistent case, the solution to the moral hazard problem does not reduce, in general, to a standard stochastic control problem. Nevertheless, the solution to the risk-sharing problem between a utility maximiser principal and a time-inconsistent sophisticated agent does, see Section2. This suggest a dire difference between the first-best and second-best problems as soon as the agent is allowed to have time-inconsistent preferences;

a second takeaway from our analysis is associated with the so-called optimality of linear contracts. These are contracts consisting of a constant part and a term proportional to the terminal value of the state process as in the seminal work of [45]. This was also the conclusion of Carroll [12] in a two-stage time-consistent model in which the principal demands robustness, in the sense of evaluating admissible contracts by their worst-case performance, over unknown actions the agent might take. Similar results we obtained by [80, 81] and [60] in the continuous-time setting. Moreover, the results in Abi Jaber and Villeneuve [1] show that the optimal contract remains linear when the output is driven by a Gaussian Volterra process (instead of Brownian motion). We study two examples that can be regarded as (time-inconsistent) variations of [45], which we refer to as discounted utility, see Section4.1, and utility of discounted income, see Section4.3. In the former case, by virtue of the simplicity of the source of time-inconsistency, we find that the optimal contract is linear. In the latter case, we find that the optimal contract is no longer linear unless there is no discounting (as in [45]). Our point here is that slight deviations of the model in [45] seem to challenge the virtues attributed to linear contracts, and this suggests that they would typically cease to be optimal in general for time-inconsistent agents;

lastly, we comment on the non-Markovian nature of the optimal contract. It is known that, beyond the realm of the model in [45], the optimal contract in the time-consistent scenario is, in general, non-Markovian in the state process , see [18]. Indeed, we find the same result, see Proposition4.10, in the case of an agent with separable time-inconsistent preferences, see Section4.2. As such, we believe this is a manifestation of the agent’s time-inconsistent preferences.

Let us illustrate some of our results, see Section1 for precise definitions. Fix a time horizon and consider a sophisticated time-inconsistent agent with risk-neutral preferences. This is, if the agent enters into a terminal payment contract with the principal, the agent seeks an equilibrium strategy according to

The principal is a risk-neutral utility maximiser. This is, among all the admissible contracts of -measurable random variables satisfying the agent’s participation constraint , she maximises

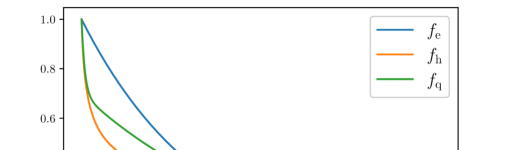

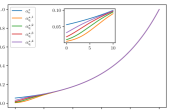

The agent is time-inconsistent in light of the general discounting function appearing in his reward. We summarise and illustrate some typical discounting models next. In all the illustrations in this section we take .

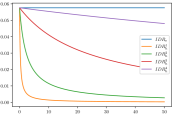

IDR

Figure 1: . On right graph, .

The most widely used discounting model in classic economics is the exponential discount function . This model captures the empirical evidence that future utils are worth less than current utils, yet the instantaneous discount rate (IDR), given by , is constant over time. To be able to accommodate the fact that consumers have both a short-run preference for instantaneous gratification and a long-run preference to act patiently, Ainslie [3] introduced the hyperbolic discounting model. Hyperbolic discounting generates the so-called self-control problem, e.g. it declines at a faster rate in the short run than in the long run, depending on the value of , whereas plays the role of baseline discounting rate. This qualitative property is even more evident in the so-called quasi-hyperbolic discounting model introduced by [50]. This model exhibits the short-run impatience of the hyperbolic model, but for long time horizons, its instantaneous discount rate resembles that of the exponential model. For this discounting, measures the value the agent gives to future periods, whereas measures the agent’s additional valuation for present/current periods. Once again, is the baseline discounting rate. We can see these observations in both the IDR column of the table to the left and the plot of the three models on the right.

Let us recall that the problem faced by an agent seeking to maximise his reward is time-consistent if and only if he discounts future utils/rewards with the exponential model. Thus, taking or in the above formulation leads to genuine time-inconsistent problems for which sophistication would have an inherent impact in the equilibrium actions followed by the agent under the optimal contract. In addition, it is easy to see that:

•

, as ,

•

, as either or .

For any sufficiently regular discounting model, including the ones just discussed, we find in Proposition4.10 that the associated optimal contract is given by

where is a constant depending on the agent’s reservation utility. The second term, however, reflects the non-Markovian nature of the terminal payment mentioned in above, and it is inherently related to the non-exponential discounting structure. Conversely, whenever the term becomes constant, leading to the well-known optimal contract that is linear in the terminal value of the output process.

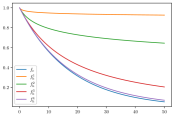

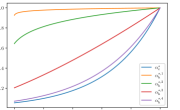

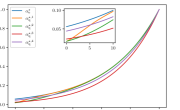

We now turn our attention to the agent’s equilibrium action under the optimal contract. We illustrate this in Figure 2 below. The three columns study the above model with , and for different values of , and , respectively. In light of the connection with the exponential discounting mentioned above, all columns include in blue, which serves as a true time-consistent baseline comparison model. The first row presents the value of the discounting functions and confirms the limits pictorially. The second row presents the associated instant discounting rates, IDR, and the last row does so for the equilibrium actions. Let us first note that the shape of the equilibrium action under exponential discounting is intuitively expected. It is convex and increasing with a shape that is inversely proportional to the exponential discounting term, this reflects that the discounted optimal effort should remain constant under the optimal strategy.

Let us first look at the case of hyperbolic discounting agents. We see that as increases, along the equilibrium effort, the sophisticated agent increases its level of effort during the initial stages. In addition, the rate at which the equilibrium effort changes over time (convexity/concavity) is positive for small values of and negative for large values, e.g. and , respectively. This means that as the time-inconsistency intensifies, sophistication causes the agent to exert larger levels of effort at the initial stages of the game. This reflects how sophistication can help overcome procrastination.

We now look at the quasi-hyperbolic agent in the centre and right column. As decreases, the agent gives less weight to the future periods and values more present over future gratification. In other words, the time-inconsistency intensifies, and the sophisticated agent decides to postpone some effort to the future period. In this scenario, despite sophistication, the agent cannot overcome procrastination. Lastly, as decreases, the agent weighs less the present period, where his time-inconsistency is more acute so that the inconsistency lessens. We nevertheless find that even though the initial effort decreases, and procrastination dominates for these decreasing values of , namely and , as the agent valuation of the present gets significantly small, and respectively, his effort increases overcoming procrastination and reaching the time-consistent level of effort. We believe that the different behaviours on the equilibrium effort for the quasi-hyperbolic discounting can be reconciled when looking at the associated IDR plots. For fixed, the IDR is monotonically decreasing in , whereas there are values of for which the IDR oscillates when decreases.

We leave the comprehensive study of these behaviours as the subject of future research. In particular, it would be interesting to study the extension of our results to the so-called instant gratification model in Harris and Laibson [37], which implements given by , as , and which are beyond the scope of this document.

(a)

(b)

(c)

(d)

(e)

(f)

(g)

(h)

(i)

Figure 2: First row: discounting models. Second row: IDR. Third row: agent’s equilibrium action under optimal contract. . Left: . Center: , . Right: , .

The rest of this article is organised as follows. Section1 takes care of the formulation of the problem, and Section2 presents the solution to the first-best problem under three different specifications of preferences. The common feature in these examples is that the problem boils down to solving a standard stochastic control problem. Section3 introduces our general approach to the second-best problem and presents the proof of Theorem3.9. Section4 is devoted to the analyses of three examples under different specifications of time-inconsistent preferences for the agent. Lastly, we include an Appendix section collecting some new results for time-inconsistent control problems with BSVIE rewards and other technical results.

Notations: denotes the set of non-negative real numbers. Let be an arbitrary finite dimensional normed space. Given a positive integer and a non-negative integer , will denote the space of functions from to which are at least times continuously differentiable. In the case , of continuous functions, we drop the dependence on and write .

By we denote the identity matrix of . denotes the set of symmetric positive semi-definite matrices. denotes the trace of a matrix .

Let be an arbitrary finite dimensional normed space. For a -algebra , denotes the space of -measurable -value functions. denotes the space of such that measurable. For a filtration on , (resp. , , ) denotes the set of -valued, -predictable processes (resp. –progressively measurable processes, -optional processes, -adapted and measurable).

1 Problem statement

We fix two positive integers and , which represent respectively the dimension of the process controlled by the agent, and the dimension of the Brownian motion driving this controlled process. We fix a time horizon , and consider the canonical space , with canonical process , and whose generic elements we denote . We reserve the notation and to denote -valued variables.

We let be the Borel -algebra on (for the topology of uniform convergence), and we denote by the natural filtration of . We let be a compact subspace of a finite-dimensional Euclidean space (typically is a subset of for some positive integer ), where the controls will take values.

1.1 Controlled state equation

We fix a bounded Borel measurable map , and an initial condition , and assume that there is a unique solution, denoted by , to the martingale problem for which is an –local martingale, such that with probability , and . Enlarging the original probability space if necessary (see Stroock and Varadhan [76, Theorem 4.5.2]), we can find an -valued Brownian motion such that

We now let be the –augmentation of which we assume is right-continuous. We recall that uniqueness of the solution to the martingale problem implies that the predictable martingale representation property holds for -martingales, which can be represented as stochastic integrals with respect to (see Jacod and Shiryaev [46, Theorem III.4.29]). We also mention that the right-continuity of guarantees that satisfies the Blumenthal zero–one law and consequently all –measurable random variables are deterministic. Let us note that these assumptions are standard in the existing literature on the continuous-time principal–agent problem.

We can then introduce our drift functional , which is assumed to be Borel-measurable with respect to all its arguments. Let us recall that for any -valued, -predictable process such that

(1.1)

we can define the probability measure on , whose density with respect to is given by

Moreover, by Girsanov’s theorem, the process is an -valued, –Brownian motion and we have

Let us emphasise that we are working under the so-called weak formulation of the problem.

This means that the state process is fixed and, in contrast to the typical strong formulation, the Brownian motion, and the probability measure are not fixed.

Indeed, the choice of corresponds to the choice of probability measure and thus impacts the distribution of process .

1.2 The agent’s problem

We aim to cover various specifications of time-inconsistent utility functions for the agent.

To motivate our formulation, let us start with an informal discussion on the typical nature of the reward functionals assigned to the agent in contract theory.

A contract consists of a tuple , where belongs the set of -predictable processes, and is a -measurable random variable.

At the intuitive level, a contract consists of a flow of continuous payments , and a terminal compensation .

The class of admissible contracts is introduced later in Section1.3 after imposing some integrability requirements.

Given a contract the value received by a time-inconsistent agent at the beginning of the problem from choosing an action typically takes the form

where denotes the agent’s utility function and denotes the cumulative net cost functional.

We highlight that the generic dependence of both and on accounts for the sources of time-inconsistency.

In the classic literature, utilities are usually classified under two categories, namely

separable utility functions, i.e. ,

non-separable utility functions, i.e. .

For instance, in the separable case the agent’s value takes the familiar form

which, by the Blumenthal zero–one law, satisfies , for the initial value of the first component of solution to the BSDE

Moreover, in the (time-consistent) case in which the agent discounts exponentially with constant factor , i.e. and , it holds that

The previous representation corresponds to a so-called recursive utility particularly known as standard additive utility, see Epstein and Zin [29].

Let us remark that an analogous argument holds in the case of the non-separable exponential utility and refer to El Karoui, Peng, and Quenez [24] for more examples of recursive utilities.

Intuitively, a recursive utility can be viewed as an extension of the classic separable or non-separable utilities in which the instantaneous utility depends on the instantaneous action and the future utility via .

Extrapolating these ideas, we may arrive at considering rewards functionals of the form where the pair satisfies the BSVIE

(1.2)

By letting both and depend on we allow for general discounting structures and incorporate time-inconsistency into the agent’s preferences.

Moreover, the previous discussion shows that this formulation encompasses time-inconsistent recursive utilities too.

Remark 1.1.

In a Markovian framework, time-inconsistent agents whose reward functional is given by (1.2) have been considered in Wei, Yong, and Yu[89], Wang and Yong[83] and Hamaguchi[35]. In these works, the dynamics of the controlled state process are given in strong formulation and, following the game-theoretic approach, they considered a refinement of the notion of equilibrium in [23] that was suitable to each of their settings. In this work, we use BSVIEs to model the agent’s reward and extend the non-Markovian framework proposed in [43].

Let us now present this formulation properly. We define the set of admissible actions, recall is compact, as

and assume we are given jointly measurable mappings for any , and satisfying the following set of assumptions.

Assumption 1.2.

For every , is invertible, i.e. there exists a mapping such that

resp. is continuously differentiable. for all , where is defined by

for , is uniformly Lipschitz-continuous

i.e. there exists some such that ,

Remark 1.3.

Let us comment on the previous assumptions. The first condition guarantees we can identify units of utility with terminal contract payments. Indeed, the utility is sufficient to identify, via , the payment . The second assumption guarantees sufficient regularity, with respect to the variable source of inconsistency, of the data prescribing the agent’s reward.

We assume the agent has a reservation utility below which he refuses to take the contract.

The agent is hired at time , and the contracts offered by the principal, for which she can only access the information about the state process , are assumed to provide the agent with a flow of continuous payments and a compensation at the terminal time .

Thus, we denote by , see Section3.1 for the definition of the integrability spaces, as the collection of contracts for the families

•

of -valued, -measurable such that ,

•

of -valued, -predictable such that .

If hired, the agent chooses an effort strategy , and at any time , his value, from time onwards, from performing is given by

where the pair satisfies the BSVIE (1.2). We recall is commonly referred to in the literature as the continuation utility. We always interpret as a map from to .

Given the choice of reward, the problem of the agent is time-inconsistent.

We therefore assume that the agent is a so-called sophisticated time-inconsistent agent who, aware of his inconsistency, can anticipate it, thus making his strategy time-consistent.

Consequently, the problem of the agent can be interpreted as an intra-personal game in which he is trying to balance all of his preferences and searches for sub-game perfect Nash equilibria.

We recall the definition of an equilibrium strategy introduced in [43], see further comments in Remark1.6.

Let , , and , we define .

Definition 1.4.

Let . We say is an equilibrium if for any , , where

Given a contract , we call the set of all equilibria associated with .

As such, the agent’s goal is, given a contract that is guaranteed by the principal, to choose an effort that aligns with his sophisticated preferences, i.e. to find .

In contrast to the case of a classic time-consistent utility maximiser, for a time-inconsistent sophisticated agent, there could be more than one equilibria with potentially different rewards, see for instance [51].

In this work, we will restrict our attention to the set of contracts inducing a unique equilibrium. See additional comments about this point in the following remark.

Definition 1.5.

denotes the family of contracts that lead to a unique equilibrium, i.e. .

All in all, for we can now define

Remark 1.6.

In the non-Markovian framework, the strategy devised in [43] builds upon the approach in [7] to study rewards given by conditional expectations of non-Markovian functionals.

This approach is based on decoupling the sources of inconsistency in the agent’s reward and requires introducing the terms and into the analysis, see AppendixB for details.

The integrability condition in the definition of guarantees that the BSVIE (1.2) is well-defined.

We also mention that TheoremB.3 generalises the extended dynamic programming principle obtained in [43] for the case of rewards given by (1.2) and equilibrium actions as in Definition1.4.

The previous definition of equilibrium can be regarded as a reformulation of the classic definition, in [23], via the . Indeed, it follows from Definition1.4 that given , , , such that

Lastly, we also expand on the necessity to focus our attention on contracts that lead to a unique equilibrium.

The need for said restriction is inherent to contract theory models involving a game-theoretic formulation at the level of the agent.

Indeed, in either the case of a finite number of competitive interacting agents seeking a Nash equilibrium, see Élie and Possamaï [25], or a continuum of players seeking a mean-field equilibrium, see Élie, Mastrolia, and Possamaï [26], it is generally possible for multiple equilibria to exist.

In such cases, the existence of a Pareto-dominating equilibrium, one for which all agents receive no worse reward if deviating from a current equilibrium, is by no means guaranteed.

In the context of contract theory, this means that there is no clear rule at the level of the problem of the agent to decide which equilibria should be taken for any two equilibria providing different values to different players.

As giving control of this decision to the principal makes little practical sense, one way to bypass this is to focus on contracts that lead to a unique equilibrium, as we did here.

Anticipating our analysis in Section3.1, we mention that this assumption is intimately related to the well-posedness of a fairly novel class of BSVIEs.

In the Lipschitz setting of this paper, we present conditions on the data of the problem under which this is the case for any , see 3.2 and Remark3.3.

As such, this is not such a stringent assumption in our context.

1.3 The principal’s problem

We now present the principal’s problem. We therefore let be the set of admissible contracts, defined by

In such manner, any contract is implementable, that is, there exists an equilibrium strategy, namely , for the agent’s problem.

The principal has utility functionals, , and and solves the problem

Remark 1.7.

We point out that we have assumed the principal is a standard utility maximiser.

This is because, in our opinion, the crux of the problem lies in identifying a proper description of the problem of the principal when contracting a time-inconsistent sophisticated agent.

In the case of a time-consistent agent, [18] identifies this description as a standard stochastic control problem with an additional state variable.

Therefore, in the case of a classic time-consistent agent and a time-inconsistent principal, following [18], one expects the problem of the principal to boil down to a non-Markovian time-inconsistent control problem with an additional state variable.

As studied in [43], these problems are characterised by an infinite family of BSDEs, analogue to the PDE system in [7] in the Markovian case.

2 The first-best problem

In the first-best, or risk-sharing, problem, the principal chooses both the effort and the contract for the agent, and she is simply required to satisfy the participation constraint. To provide appropriate characterisations of the solution to several examples, we will focus on a particular class of reward functionals for the agent. We recall that our goal is to study the second-best problem introduced in the previous section. As such, despite its inherent interest, the results in the current section serve mainly as a reference point for the general analysis we conduct in Section3. Moreover, the following specification is covered by the general formulation presented in Section1, see Remark2.1, and it is yet rich enough to cover examples of both separable and non-separable utilities. We highlight that in the next two examples, we consider contracts consisting of only a terminal payment, i.e. .

Let us assume the agent has a given increasing and concave utility function and Borel-measurable discount functions , and defined on , taking values in , with , which are assumed to be continuously differentiable with derivatives , and . Lastly, we have Borel-measurable functionals and , defined on and taking values in .

We then specify the agent’s continuation utility by

(2.1)

where

Regarding the principal, we assume she has her own utility function , which we assume to be concave and strictly increasing so that

where denotes a mechanism by which the principal collects the values of the different coordinates of the state process .

Remark 2.1.

As commented above, the previous type of rewards are covered by the formulation via BSVIEs (1.2) and satisfy 1.2. It corresponds to the choice and

Regarding the principal, our specification corresponds to . Let us mention that, to facilitate the resolution of the following examples, we assumed that depends only on the terminal value of . This allow us to use the dynamics of as given in Section1.1. We highlight this assumption is not necessary in general analysis for the second best problem we present in Section3.

We now move on to characterise the solution to the first-best problem in the case of a time-inconsistent agent with both separable and non-separable utility functions. Anticipating the result, we highlight that in the first-best problem, the problem of the principal reduces to solving a standard stochastic control problem.

2.1 Non-separable utility

We recall that the CARA utility function, commonly known as the exponential utility, constitutes the stereotypical example of non-separable utility. We then consider (2.1) under the choice ,

and assume is convex for any . We then have that

(2.2)

The value of principal is thus obtained through the following constrained optimisation problem

Note that, the concavity (resp. convexity) of both and (resp. ) and the fact is a convex set, imply that is a concave optimisation problem. The Lagrangian associated to this problem, where denotes the multiplier of the participation constraint, is

For convenience of the reader, we recall that the dual problem , which is an unconstrained control problem, is in general an upper bound of and is defined by

(2.3)

where we used the convention . As it is commonplace for convex problems, the next result exploits the absence of duality gap, i.e. , to compute the value of . It uses the following notations

Proposition 2.2.

Let

Suppose and for any , where

Then

Moreover, if is an optimal control for , then an optimal contract is given by .

2.2 Separable utility

We consider the case and in (2.1), and assume is convex for any . The agent’s reward from time onwards is given by

(2.4)

The value of principal is thus obtained through the following constrained optimisation problem

The Lagrangian associated to this problem is

Proposition 2.3.

Suppose and are such that mapping given as the solution to

is well-defined and for any . Let

Then

Moreover, suppose the pair is feasible for the primal problem, where resp. denote the maximiser in resp. the above problem, which we assume to exist. Then, there is no duality gap, i.e.

the optimal contract is given by .

If , for let

Then, the problem of the principal is given by the solution to the standard control problem

Moreover, for an optimal control of this problem, contains all the optimal contracts for the principal, e.g. the deterministic contract

Remark 2.4.

We remark that the assumption on the utility functions in Proposition2.3 is relatively reasonable. Indeed, it is immediately satisfied, for instance, in either of the following scenarii

and is strictly increasing;

for , is concave, strictly increasing and satisfies the following conditions

3 The second-best problem: general scenario

In this section, we bring back our attention to the second-best problem faced by the principal

We will exploit the theory of type-I BSVIEs. Consequently, we first introduce suitable integrability spaces.

3.1 Integrability spaces and Hamiltonian

Following [42, Section 2.2], to carry out the analysis we introduce the spaces

of , such that

of càdlàg such that

of , with ;

of such that

To make sense of the class of systems considered in this paper we introduce some extra spaces.

Given a Banach space of -valued processes, we define the space of such that is continuous and

For instance, denotes the space of such that is continuous and .

of such that is continuously differentiable with derivative , and , where is given by

Lastly, we introduce the space .

Remark 3.1.

The second set of these spaces are suitable extensions of the classical ones, whose norms are tailor-made to the analysis of the systems we will study.

Some of these spaces have been previously considered in the literature on BSVIEs, e.g.[42] and [83].

Of particular interest is the space which allows us to define a good candidate for as an element of , see [35].

3.2 Characterising equilibria and the BSDE system

Building upon the results in [43], where only the case of an agent with separable utility was considered, we wish to obtain a characterisation of the equilibria that are associated to any . For this we must introduce the Hamiltonian functional given by

Our standing assumptions on are the following.

Assumption 3.2.

The map is uniformly Lipschitz-continuous, i.e. there is such that for any

there exists a unique Borel-measurable map such that

The map is uniformly Lipschitz-continuous, i.e. there is such that for any .

To ease the notation we introduce , , and .

Remark 3.3.

Let us comment on the previous set of assumptions.

Even in the non-Markovian setting of this document, the problem faced by a sophisticated agent is related to a system of equations instead of just one, see [43].

This raises many issues, among which is the possibility of multiplicity of equilibria with different values.

3.2., 3.2. guarantee that for a given any equilibria corresponds to a maximisers of the Hamiltonian.

Ultimately, 3.2. guarantees that there is only one maximiser of the Hamiltonian.

Let us mention that the existence of is guaranteed under 1.2. by Schäl[70, Theorem 3].

This conciliates our focus on contracts leading to unique equilibria as we stated in Section1.2.

Under this set of assumptions, we are able to show, see AppendixB, that for any

where the processes come from the solution to the following infinite family of BSDEs which for any satisfies, –a.s.

(3.1)

Moreover, we have that

(3.2)

Given that 1.2 guarantees that invertible for every , we also have that

(3.3)

Remark 3.4.

We recall that the diagonal process is well-defined for elements in , see Section3.1.

Links between time-inconsistent control problems and a broader class of BSVIEs have been identified in the past.

The first mention of this link appears, as far as we know, in the concluding remarks of Wang and Yong [87].

The link was then made rigorous independently by [43] and Wang and Yong [83]. In our setting, in light of (3.2), such an equation appears as the one satisfied by the reward of the agent along the equilibrium.

As such, the pair solves a so-called extended type-I BSVIE, which for any satisfies

(3.4)

We highlight that this BSVIE involves the diagonal processes and that in light of [42, Theorem 4.4] the solutions of (3.2) are in correspondence to those of (3.4).

3.3 The family of restricted contracts

In light of our previous observation, namely (3.3), we will introduce next a family of restricted terminal payments, which we will denote , and

will denote the associated class of contracts.

For any contract in this family, we can solve the associated time-inconsistent control problem faced by the agent.

Moreover, we will show that any admissible contract available to the principal admits a representation as a contract in .

Consequently, the principal’s optimal expected utility is not reduced if she restricts herself to offer contracts in this family and optimises.

In order to define the family of restricted contracts, we introduce next the process , which for a suitable process will represent the value of the agent.

This is a preliminary step based on the observation, see (3.3), that the value of the agent at the terminal time coincides with the payment offered by the contract.

To alleviate the notation let us set .

Definition 3.5.

Let . We denote by the collection of processes satisfying , where for , satisfies for every ,

(3.5)

(3.6)

With this, it is natural to consider the class of contracts where denotes the set of terminal payments of the form

The main novelty of our argument, compared to that in the time-consistent case, is the fact that (3.6) imposes a constraint on the elements .

Remark 3.6.

We highlight is independent of the choice of and that establishing is inherently associated with the existence of solutions to (3.4).

For results on type-I BSVIEs we refer to [42] and [86].

The process denotes a solution to a so-called forward Volterra integral equation FSVIE, for short.

However, this is not a classic FSVIE in the sense that, in addition to , the diagonal processes appears in the generator.

For completeness, AppendixC includes a suitable well-posedness result.

As mentioned at the beginning of this section, we chose to work with a representation for the agent’s value as opposed to the value of the contract itself.

This determines the form of the terminal payments in the definition of and provides a quite general and comprehensive approach.

For instance, one could have chosen to represent the value of directly for an agent with a time-inconsistent exponential utility.

This would have produced a version of (3.2) whose generators have quadratic growth in and whose analysis is more delicate than in the Lipschitz case.

See for instance, Wang, Sun, and Yong [84], Fan, Wan, and Yong [30], Hernández [41] for the study of quadratic BSVIEs.

We recall that taking that approach in the time-consistent scenario requires, at the very least, assuming the contracts have exponential moments of sufficiently large order.

Our approach prevents this given our growth assumptions in 1.2.

However, one cannot expect to avoid such restrictions for problems that are inherently quadratic.

Remark 3.7.

We would like to highlight the nature of the constraint (3.6). Indeed, for any satisfying (3.6), it holds that , , . That is, if we let denote the family of continuously differentiable functions such that the map is constant, (3.6) is equivalent to the stochastic target constraint

(3.7)

Moreover, we emphasise that this constraint is there due to time-inconsistency. Indeed, going back to the time-consistent, i.e. exponential discounting, scenario presented in Section1.2, it is not hard to see that , , for any . Thus, (3.6) as well as the stochastic target constraint (3.7) are automatically fulfilled in the time-consistent, exponential discounting, scenario.

In light of our previous remarks, as a preliminary step, we must verify that (3.5) uniquely defines .

At the formal level, the following auxiliary lemma says that the integrability conditions on the pair guarantees this.

Lemma 3.8.

Let 1.2 and 3.2 hold. Given there exist unique processes such that satisfies (3.5) and satisfies

(3.8)

Proof.

Let us first argue the result for . Note that the integrability of , 1.2. and 3.2. yields

The result follows from PropositionC.5. The second part of the statement is a consequence of PropositionC.6 and the integrability of .

∎

We are now ready to state our main result, in words it guarantees that there is no loss of generality for the principal in offering contracts of the form given by .

Theorem 3.9.

We have . Moreover, for any contract , with associated to , we have

Let . The problem of the principal admits the following representation

(3.9)

where

Proof.

We first argue . Let .

In light of 1.2, the fact that , and Remark3.4., TheoremB.5 guarantees that for there exists solution to (3.4) and a process satisfying that the mapping is the derivative of .

We also note that 1.2. guarantees (3.6) holds.

Moreover, (3.2) implies , recall . From this, taking we have that .

Thus .

To show the reverse inclusion, let . This is, , where, in light of Lemma3.8, denotes the process, induced by , such that and (3.6) holds. In particular

Therefore, for any

(3.10)

We now show , see Section1.2. It is immediate to see that

Now, given solution to (3.5) and by definition of , Lemma3.8 guarantees there exists such that the pair satisfies (3.8). Moreover, by PropositionC.6 for any

Thus, . This shows .

Let us argue as in Definition1.5, i.e. that leads to a unique equilibrium.

In light of 3.2, TheoremB.5 and TheoremB.6, it suffices to establish leads to a solution of (3.2).

Let us recall that by [42, Theorem 4.4], the solutions of (3.2) are in correspondence to those of (3.4).

We now simply note that (3.10) defines a solution.

Thus

To conclude , note that by TheoremB.6, so that guarantees the participation constraint is satisfied.

∎

In view of Theorem3.9, the problem of the principal involves controlling, via , the processes . The dynamics of are given, in weak formulation, by

(3.11)

where is a –Brownian motion, and those of are given by

We highlight that on top of the Volterra nature of both the state process and the control , the constraint (3.6) must be satisfied.

However, building upon the discussion in Remark3.7, we see that the problem of the principal corresponds to a stochastic target control problem of FSVIEs with Volterra controls.

Indeed, the principal

controls the forward Volterra process ;

with Volterra-type controls , recall both and impacts the dynamics;

the state process is subject to the stochastic target constraint (3.7).

The literature on controlled FSVIEs began, to the best of our knowledge, with Chen and Yong [14] where the authors studied the control of FSVIE by means of a stochastic maximum principle.555Ever since, several works have extended this approach, a probably incomplete list includes Shi, Wang, and Yong[73], Wang[85] and Hamaguchi and Wang[36].

A recent milestone in the study of this problem is Viens and Zhang [82] where, via a dynamic programming approach, the authors arrive at a path-dependent HJB equation.

Nevertheless, in all of these works the control consists of an unconstrained stochastic process.

Thus the approach [82] is inoperable as it does not cover nor above.

Regarding the study of stochastic target control problems, the seminal works are due to Soner and Touzi [74, 75] where the state process is a controlled SDEs.

We also remark on the recent extension to targets in the Wasserstein space by Bouchard, Djehiche, and

Kharroubi [10], which shows the possibility of extending the original approach to infinite dimensional target problems like the one faced by the principal, namely above.

Particularly important to our analysis are the results in Bouchard, Élie, and

Imbert [9] on optimal control problems with stochastic target constraints.

Indeed, this work elucidates the blueprint that needs to be extended to the Volterra case to be able to obtain (infinite-dimensional) HJB-type PDEs that characterise the problem of the principal.

As the reader might be able to notice, in general, this seems to be quite a challenging task.

Therefore, we will, for now, concentrate our attention on simpler cases where we can actually transfer the stochastic target constraint on into a more manageable constraint on the controls directly.

The general case will be the subject of future research and will be studied in a separate paper.

As a motivation for our approach in the following examples, we recall that:

first, the flow of continuous payments enters the reduced problem of the principal as a standard control on the drift which raises no major challenges in the analysis, and thus we will omit it from the following examples and consider contracts consisting of only a terminal payment, i.e. .

Second, for classic separable utilities with exponential discounting it is known, see Remark3.7, that the Volterra nature of the state process becomes redundant.

Indeed, in this scenario is sufficient to describe to characterise the entire family.

This motivates the study of under particular specifications of utility functions for both the agent and the principal, hoping to be able to

reduce the complexity of the set ;

exploit its particular structure to formulate an ansatz to the problem of the principal.

This is exactly what we do in the following sections.

4 The second-best problem: examples

4.1 Agent with discounted utility reward

As an initial example, let us consider the scenario in Section2.1 under the additional choice , which implies does not depend on . Thus, we have

(4.1)

Under this specification, (3.2) reduces significantly. Indeed

Remark 4.1.

We highlight that the absence of accumulative cost in the agent’s reward functional, i.e., together with the choice makes the driver in the second family of BSDEs independent of the variable , i.e.. Moreover, it coincides with the functional maximised in the Hamiltonian .

We remark that in this scenario, the non-exponential discount factor, i.e. the time-inconsistent preferences, does not add much to the problem. Even though the agent’s continuation utility changes by a factor, the optimal/equilibrium control state pair coincides for both problems. Our aim in presenting it is to illustrate how the technique presented in Section3.3 is compatible with the results known in the case of a time-consistent agent.

The next result provides a drastic simplification of the infinite dimensional system introduced in Section3.2. This is due to the particular form of the reward of the agent (4.1).

Lemma 4.2.

Let and the agent’s reward be given by (4.1). Then, (3.2) is equivalent to the BSDE

Let . Then solves the BSDE

, where denotes the family of satisfying where, for any ,

All together, this shows that (3.2) reduces to the equation in the statement. The result then follows as we can trace back the argument and construct a solution to (3.2) starting from a solution to the BSDE in the statement.

We now argue . Let . Then, there is such that (3.6) holds and

Let us note that (3.6) implies . Since , we obtain

so that

Note that . Thanks to Theorem3.9, the result follows replacing in the first equation of (3.2).

We are left to argue as is argued as in Theorem3.9. follows by . Indeed, there is such that

Conversely, let and as in the statement. Then, letting

the martingale representation theorem, which holds in light of (B.1) and the integrability of , guarantees the existence of such that, as elements of ,

It then follows that .

∎

4.1.1 Principal’s second-best solution

In the following, we will exploit the so-called certainty equivalent, i.e. the relation between the contract and the terminal value of the value function. The benefits of this are twofold: it lays down an expression that can be replaced directly into the principal’s criterion, and it removes from the generator of the expression representing the contract in exchange for a term which is quadratic in . For this we need to introduce some extra notation.

Let be given by

with . The mapping is defined, as before, by the relation , and , are also defined.

Proposition 4.3.

The problem of the principal can be represented as the following standard control problem

where and is given by the terminal value of

Proof.

We first note that in light Lemma4.2, we may replace the optimisation over with . Let . The result then follows from Lemma4.2 by applying Itô’s formula to .

∎

Remark 4.4.

Let us highlight the main message behind Proposition4.3. When the agent’s reward is given by (4.1), the principal’s second-best problem reduces to a standard control problem. This is a drastic simplification of the result in Theorem3.9 and a consequence of the particular form of the agent’s reward.

In a Markovian setting in which the dependence of the data on the path is via the current value, we see from the controlled dynamics for and that the problem boils down to computing . Employing the standard dynamic programming approach we obtain that the relevant term for this problem is given for by

where

for , , , , and .

In the following proposition, whose proof is available in AppendixD, we study the case , so that

This result is equivalent to solving the HJB equation in Remark4.4.

Proposition 4.5.

Let principal and agent have exponential utility with parameters and , respectively. Let , , and assume that

the maps , and do not depend on the variable;

for any , the map has a unique maximiser , such that is square integrable.

Then

is an optimal solution to principal’s second-best problem and

Remark 4.6.

To close this section we present a few remarks:

comparing the results in Proposition4.5 and Proposition2.2 we see that, as expected, in general the solution to the second-best and first-best problem are not equal;

if we bring ourselves back to the setting of [45], i.e., , , we have

This recovers the result for the case of a risk-neutral principal, i.e., presented in [45]. The optimal contract and the respective rewards differ by a factor which depends on the discount factor and agent’s risk aversion parameter;

following upon the previous comment, we add that the optimal contract takes the form of a Markovian rule. Moreover, it is linear. This is consistent with the seminal work of [45] and the conclusion of [12] in which the robustness of these policies was studied. Nevertheless, as we will see in Section4.3, this appears to be a consequence of the simplicity of the source of time-inconsistency considered in this section.

The mappings , , , , and the probability are obtained accordingly.

In this section, we are trying to get a deeper understanding of the family under the previous specification of preferences for the agent. In particular, we want to understand how the elements of the family are related to each other. In light of 1.2 and 3.2, for any we denote the -square integrable martingale

where

We also recall that is the unique solution to the martingale problem for which has characteristic triplet . Thus, the representation property holds for -martingales (see [46, Theorem III.4.29]) and we can introduce the unique -predictable process such that ,666The integrability for fixed is clear. The follows as in [43, Theorem 3.5] as is uniformly continuous in . and, in light of (3.11),

The next lemma, proved in AppendixD, presents relationships satisfied by the family and how we can use them to obtain another characterisation of and .

Lemma 4.7.

Let , for any

Let , for any

, where denotes the class of such that , where for

and

(4.2)

. For any ,

Remark 4.8.

In the exponential discounting case, i.e. for some , we have

The problem of the principal can be represented as the following control problem

where and

We remark that contrary to the example in Section4.1, Proposition4.9 reduces the problem of the principal to a non-standard control problem. Indeed, we have to optimise over , a family of infinite-dimensional controls which has to satisfy a novel type of constraint, namely (4.2). Nonetheless, under additional assumptions on the model, we can proceed with the resolution.

Let , the principal and the agent be risk-neutral, i.e. , .

Suppose there is a unique measurable map satisfying

where for any

Moreover, assume the mapping is Lipschitz-continuous uniformly in with linear growth. Then, where the pair denotes a solution to the BSDE

In addition, let

and suppose . Then, there exists , such that define a solution to the second-best problem and the optimal contract is given by

Suppose the maps and do not depend on the variable and for any , the map has a unique maximiser , such that is Lebesgue integrable.

Then, a solution for the second-best problem is given by

Moreover, the associated optimal contract is given by

Proof.

Let us show . As both agent and principal are risk neutral, we have

An upper bound is obtained by ignoring (4.2). In such scenario, the mapping in the statement denotes the Hamiltonian and by classical arguments in control, see El Karoui, Peng, and Quenez [24], its value is given by where are as in the statement. We are left to show this bound is attained. For this we must verify .

On the one hand, note that the integrability of together with 1.2 guarantee

Therefore, by [86, Theorem 3.5], there exists a unique solution to the BSVIE with data given by

On the other side, under the integrability assumption on we have that for every

defines a -square integrable martingale. Thus, there exists a family of process such that

Moreover, in light of (1.2) we have that . Therefore, by uniqueness of the solution

From this, arguing as in Lemma4.7 we obtain that satisfies (4.2).

We now argue . Note that we can find an upper bound for . Indeed, we have

We now show that the pair given in the statement is a feasible solution that attains . To verify feasibility note that, by assumption, is deterministic, and so is . Thus, it is straightforward from the definition that . Lastly, it follows by definition that under the upper bound is attained.

∎

Remark 4.11.

Let us now present a formal argument regarding our choice in the previous result for solving (4.3). Suppose for simplicity the maps , and do not depend on the variable so that the dynamics of the state variables are given by

Moreover, suppose the value function is regular enough so that Itô’s formula yields,

Let us highlight the presence of both and in the last term. From this we can see, formally, that for general and the process alone is not sufficient to obtain the solution of (4.3). Moreover, recall we can not take and independently due to the constraint (4.2). Lastly, under the assumptions of Proposition4.10 one expects, intuitively, that so that the choice can be made after optimising over .

Remark 4.12.

We close this section with a few remarks.

It is worth mentioning that even in the setting of Proposition2.3. the optimal contract is neither linear nor Markovian. Moreover, from the expression describing the optimal contract we see that this is entirely related to the presence of the discounting structure which is the source of time-inconsistency.

It follows from Proposition2.3 that for risk-neutral preferences, the utility of the principal is the same for both the first-best and second-best problem and that the optimal second-best contract is also optimal there. This is a typical result for time-consistent risk-neutral agents, and it would certainly be worth studying whether this remains true for more general specifications of and . In light of Remark4.11, this question further motivates the study of the general class of non-standard control problems introduced by Theorem3.9.

4.3 Agent with utility of discounted income

We now consider the scenario in Section2.1 under the additional choice . We then have

The problem introduce by (4.4) is time-inconsistent even in the case of exponential discounting, i.e., , for some . This is due to the exponential utility . Indeed, the BSDE representation allows us to interpret the reward of the agent as a recursive utility in which the terminal value is discounted at a rate whereas the generator discounts at a rate . It is known, see Marín-Solano and Navas [59, Section 4.5], that even in the case of exponential discounting the problem becomes time-inconsistent as soon as the rates at which the terminal value and the running reward are discounted differ. We also recall that the case of no discounting, i.e., corresponds to the seminal work Holmström and Milgrom [45].

Let us note that exhibits both of the features of the examples in Sections 4.1 and 4.2, this is, the second term includes the discount factor and the variable.777In fact, (4.4) covers the situation in Section4.2 in the particular case of a risk-neutral agent, recall , whenever . We highlight that a key element in Proposition4.10 was the fact that the dynamics of were given by without on the right hand side. Consequently, the presence of in forces us to begin by changing variables to the certainty equivalent for the problem of the agent, i.e. from to as we denote below. In this way, we remove in the dynamics of at the expense of the mapping , which we use to identify an auxiliary martingale, becoming quadratic in the new variable . On the one hand, this creates a subtle issue when trying to establish a correspondence between the natural integrability of the variables and , and will ultimately prevent us from obtaining a complete characterisation of the family . On the other hand, the quadratic term does not correspond to the diagonal values of the control variable . This makes the approach in Section4.2, namely Proposition4.10, inoperable and forces us to restrict ourselves to a suitable subclass that is amenable to the analysis.

As we may probably expect after our analysis in Section4.1, the process in the definition of becomes more amenable to the analysis by working in terms of the certainty equivalent. For this, we introduce, for ,

The maps , , , , , and the probability are defined accordingly.

Moreover, inspired by Section4.2, we introduce the mapping given, for , by

The following result is analogue to Lemma4.7, we defer its proof to AppendixD.

Lemma 4.14.

Let .

There exists family of processes such that for every

If then for every

Moreover, if the process given by

is a square integrable -martingale, then

where denotes the term in the representation of .

Remark 4.15.

We highlight that in contrast to the analysis presented in Sections4.1 and 4.2, the previous result does not provide an equivalent representation of the set . This is intimately related to the square integrability condition on the process required in above, and the fact that is quadratic for fixed.

As a sanity check at this point, let us verify the coherence of the previous system in terms of the analysis of the previous section. In the following we omit the dependence on and assume . Let

By applying Itô’s formula to , we have that for any ,

As , we see the previous equation induces the corresponding one in Lemma4.7.

4.3.1 Principal’s second-best solution

Let us highlight that in contrast to Section4.2, the analysis in the previous section does not provide a full characterisation of for rewards given by (2.4). This is principally due to the integrability necessary on the variable , induced by the certainty equivalent, in order to apply the methodology devised in 4.2, see Lemma4.14. Nevertheless, given that the current example generalises the previous two, we build upon the structure of those optimal solutions to propose a family over which the optimisation in the problem of the principal can be carried out.

We will focus on the case and we will pay special attention to the class of processes for which given the pair , and given by (3.5), there exists a pair of predictable processes such that

We remark that the previous definition implicitly requires that for any the mapping is differentiable.

In addition, provided does not depend on it is easy to verify that that . In light of the previous lemma, we have that for

and

This implies that includes, in particular, all the processes that are induced by deterministic pairs . Indeed, for such class of processes we have that is deterministic, , and consequently, provides a non trivial element of . The previous argument also holds in the case of exponential discounting, in which we recall that the agent’s problem remains time-inconsistent.

The following result characterises the solution to . Its proof is available in AppendixD.

Proposition 4.17.

Let principal and agent have exponential utility with parameters and , respectively. Let , , and assume that:

the maps , and do not depend on the variable;

for any , the map given by

has a unique maximiser , such that is square-integrable.

Then

Moreover

let denote the restriction of to the subclass of with deterministic . Then the optimal deterministic contract is given by the family

and

in the case , i.e. the case of risk-neutral principal and agent, the solution to , and consequently of , agrees with the value given by Proposition4.10 and the optimal family is deterministic.

Remark 4.18.

We close this section with a few remarks.

The solution to the problem of the principal for the general class of restricted contracts induced by escaped the analysis presented above. As detailed in Remark4.13., this is due to subtle integrability issues when trying to identify an appropriate reduction of , and the quadratic nature of the generator when working in term of the certainty equivalent.We believe this echoes the intricacies of the non-standard class of control problem introduced in Theorem3.9.

If, as in Remark4.6, we bring ourselves back to the setting of [45], i.e., , , we have

We highlight that: in contrast to [45], for any type of discounting structure including exponential discounting the previous expression and consequently the optimal action is neither linear nor Markovian. This corroborates our comment in Remark4.13., in the sense that even in the case of exponential discounting the problem of the agent remains time-inconsistent; in the case of no discounting, i.e., when we bring ourselves back to the model of Remark4.6, the previous expression coincides with the linear contract result specified by [45]. This shows that, even if possibly not the best, the optimal contract in the class at least captures the optimal contract when the problem becomes time-consistent again.

Let be fixed and optimise the mapping . An upper bound of this problem is given by optimising -by-. This leads us to define, for any fixed, the candidate

To show the upper bound induced by is attained it suffices to note that by assumption. Replacing in we obtain

If , as the above function is a strictly convex function of , first order conditions gives as in the statement.

We are only left to show that , i.e. that there is no duality gap. For this, it suffices to verify that is primal feasible, i.e. that it satisfy the participation constraint. Indeed